century 21 accounting © 2009 south-western, cengage learning lesson 6-1 creating a worksheet four...

TRANSCRIPT

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 6-1LESSON 6-1

Creating a Worksheet

Four reasons Accountants use Worksheets;

1.To summarize general ledger account balances to prove that debits equal credits.

2.To plan needed changes to general ledger accounts to bring account balance up to date

3.To separate general ledger account balances according to the financial statements to be prepared.

4.To calculate the amount of net income or net loss for a fiscal period.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

2

Chapter Concepts:

Consistent Reporting: applied when the same accounting procedures are followed in the same way in each accounting period.

Accounting Period Cycle: Applied when changes in financial information are reported for a specific period of time in the form of financial statements.

Matching Expenses with Revenue: Applied when revenue from business activities and expenses associated with earning that revenue are recorded in the same accounting period.

Chapter ConceptsChapter Concepts

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

3

LESSON 6-1

PREPARING THE HEADING OF A PREPARING THE HEADING OF A WORK SHEETWORK SHEET page 153

Name of CompanyName of Company

11

Name of ReportName of Report

22

Date of ReportDate of Report

33

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

4

LESSON 6-1

1. Write the general ledger account titles.

2. Write the general ledger debit account balances. Write the general ledger credit account balances.

4. Add both the Trial Balance Debit and Credit columns.

3. Rule a single line across the two Trial Balance columns.

5. Write each column’s total below the single line.

6. Rule double lines across both Trial Balance columns.

PREPARING A TRIAL BALANCE ON A PREPARING A TRIAL BALANCE ON A WORK SHEETWORK SHEET page 154

11

22

44

33

55 66

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 6-2LESSON 6-2

Planning Adjusting Entries on a Work Sheet

In two accounts, supplies and prepaid insurance, we have used some of what we owned. During each month we used some of our supplies to run the business and we used a portion of our prepaid insurance. These are considered expenses for the business and we must account for the portion we used during the month we used it.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

6

LESSON 6-2

SUPPLIES ADJUSTMENT ON A SUPPLIES ADJUSTMENT ON A WORK SHEETWORK SHEET

11

22

page 158

33

1. Write the debit amount.

2. Write the credit amount.

3. Label the two parts of this adjustment.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

7

LESSON 6-2

PREPAID INSURANCE ADJUSTMENT PREPAID INSURANCE ADJUSTMENT ON A WORK SHEETON A WORK SHEET page 159

11

2233

1. Write the debit amount.

2. Write the credit amount.

3. Label the two parts of this adjustment.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

8

LESSON 6-2

PROVING THE ADJUSTMENTS PROVING THE ADJUSTMENTS COLUMNS OF A WORK SHEETCOLUMNS OF A WORK SHEET page 160

3. Rule double lines.

2. Add both the Adjustments Debit and Credit columns. Write each column’s total.

1. Rule a single line.

11

33

22

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

9

LESSON 6-2

PREPARING A WORK SHEETPREPARING A WORK SHEET page 160 C

1. Write the heading.

2. Record the trial balance.

3. Record the supplies adjustment.

4. Record the prepaid insurance adjustment.

5. Prove the Adjustments columns.

6. Extend all balance sheet account balances.

7. Extend all income statement account balances.

8. Calculate and record the net income (or net loss).

9. Total and rule the Income Statement and Balance Sheet columns.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

10

LESSON 6-2

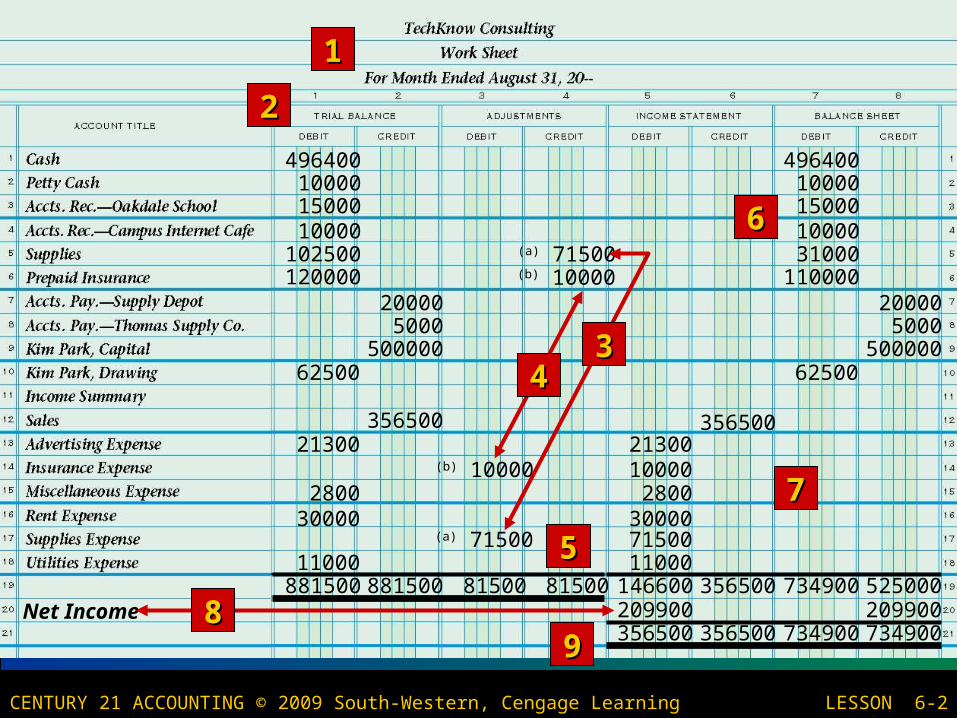

(b) 10000

44

(b) 10000

(a) 71500

(a) 71500

33

4964001000015000

11000

10000102500120000

200005000

50000062500

35650021300

280030000

881500 881500 81500 81500 146600 356500 734900 525000

356500 734900

49640010000150001000031000

11000020000

5000500000

62500

66

11000

21300

280030000

356500

10000

71500

77

209900 209900Net Income 8899

11

22

55

356500 734900

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 6-3LESSON 6-3

Extending Financial Statement Information on a Work Sheet

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

12

LESSON 6-3

EXTENDING BALANCE SHEET ACCOUNT EXTENDING BALANCE SHEET ACCOUNT BALANCES ON A WORK SHEETBALANCES ON A WORK SHEET page 162

1. Debit balances without adjustments

2. Debit balances with adjustments

3. Credit balances without adjustments

33

22

11

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

13

LESSON 6-3

EXTENDING INCOME STATEMENT ACCOUNT EXTENDING INCOME STATEMENT ACCOUNT BALANCES ON A WORK SHEETBALANCES ON A WORK SHEET page 163

1. Sales balance

2. Expense balances without adjustments

3. Expense balances with adjustments

11

33

22

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

14

LESSON 6-3

1. Single rule

2. Totals

3. Net income

RECORDING NET INCOME, AND TOTALING RECORDING NET INCOME, AND TOTALING AND RULING A WORK SHEETAND RULING A WORK SHEET

4. Extend net income 6. Totals

66 773355

221144

5. Single rule 7. Double rule

page 164

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

15

LESSON 6-3

CALCULATING AND RECORDING A NET CALCULATING AND RECORDING A NET LOSS ON A WORK SHEETLOSS ON A WORK SHEET page 165

2. Totals

3. Net loss

4. Extend net loss

1. Single rule 22

11

33

44

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 6-4LESSON 6-4

Finding and Correcting Errors on the Work Sheet

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

17

LESSON 6-4

CORRECTING AN ERROR IN POSTING CORRECTING AN ERROR IN POSTING TO THE WRONG ACCOUNTTO THE WRONG ACCOUNT page 168

1. Draw a line through the entire incorrect entry. Recalculate the account balance and correct the work sheet.

22 Correct entryCorrect entry

11 Incorrect entryIncorrect entry

2. Record the posting in the correct account. Recalculate the account balance, and correct the work sheet.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

18

LESSON 6-4

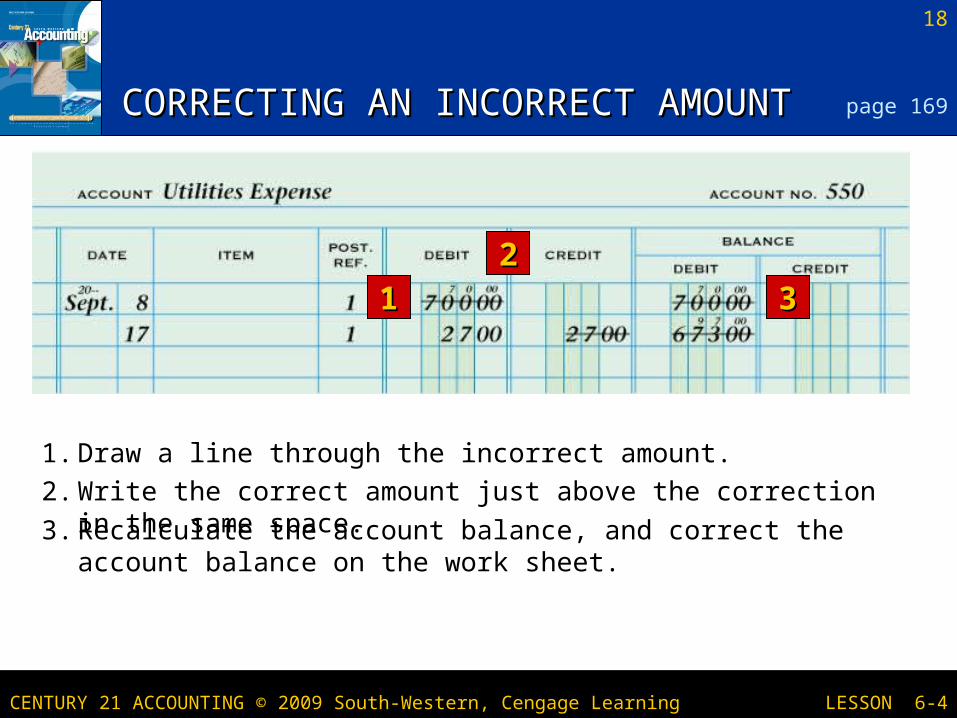

CORRECTING AN INCORRECT AMOUNTCORRECTING AN INCORRECT AMOUNT

1122

33

page 169

1. Draw a line through the incorrect amount.

2. Write the correct amount just above the correction in the same space.

3. Recalculate the account balance, and correct the account balance on the work sheet.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

19

LESSON 6-4

1122

33

CORRECTING AN AMOUNT POSTED TO CORRECTING AN AMOUNT POSTED TO THE WRONG COLUMNTHE WRONG COLUMN

55 44 66

page 169

6. Recalculate the account balance, and correct the work sheet.5. Record the posting in the correct amount column.4. Draw a line through the incorrect item in the account.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

20

LESSON 6-3

TERMS REVIEWTERMS REVIEW page 166

Adjustments Changes recorded on a work sheet to update general ledger accounts at the end of the fiscal period.

Balance sheet A financial statement that reports assets, liabilities and owner’s equity on a specific date.

Fiscal period The length of time for which a business summarizes and reports financial information.

Income statement A financial statement showing the revenue and expenses for a fiscal period.

Net income The difference between total revenue and total expenses when total revenue is greater.

Net loss The difference between total revenue and total expenses when total expenses are greater.

Trial balance A proof of the equality of debits and credits in a general ledger.

Worksheet A columnar accounting form used to summarize the general ledger information needed to prepare financial statements.