cdn market improving, but latest pricing data shows challenges still lie ahead

TRANSCRIPT

CDN Market Improving, But Latest Pricing Data Shows Challenges Still Lie

Ahead

Dan Rayburn, Principal Analyst

Digital Media

10/29/2009

Frost & Sullivan’s Growth Consulting can assist with your growth strategies

2

Today’s Agenda

• Current Market Size and Forecasts (2007-2012)

• Latest Trends In Video Consumption

• CDN Pricing: Survey Results

• What The Carriers Are Up To

• Problems The Carriers Face

• Impacts: HD Video, Video Advertising, Live Events, Devices

• Industry Consolidation and Outlook: 12-18 Months

• Questions

3

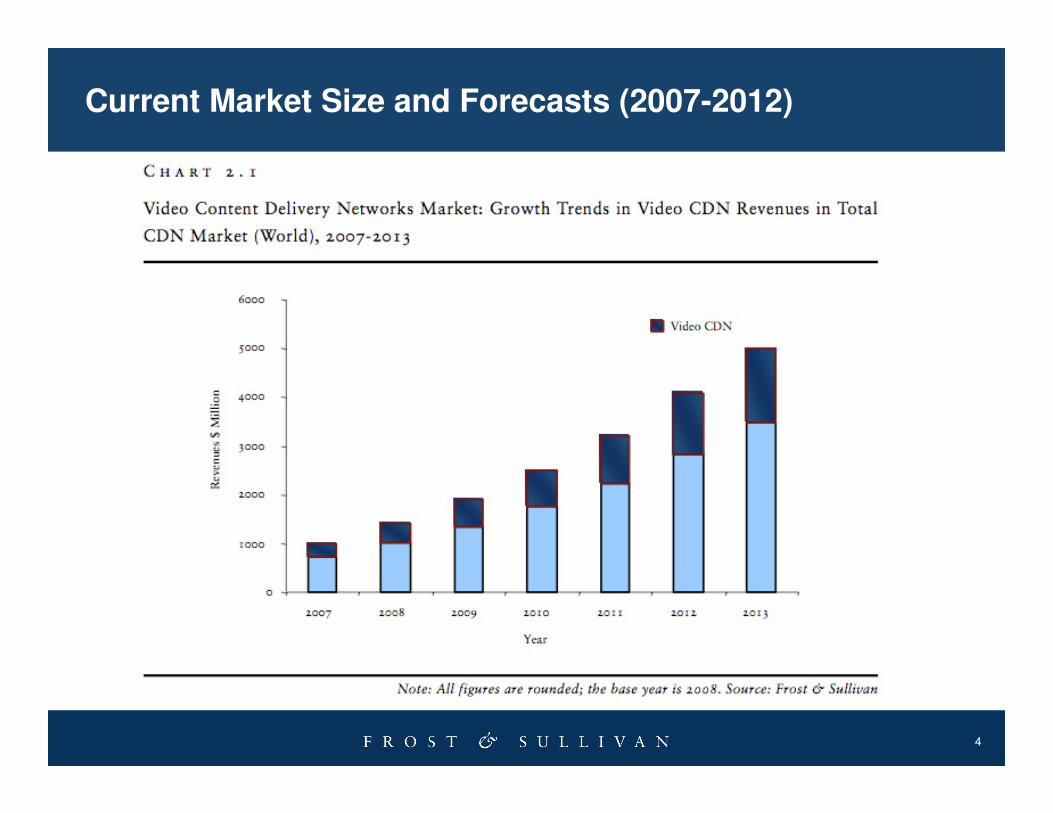

Current Market Size and Forecasts (2007-2012)

4

Current Market Size and Forecasts (2007-2012)

5

Latest Trends In Video Consumption

• More content being consumed, more often, at higher bitrates, for longer periods of time, on more devices

• Even with many devices in the market, Xbox 360, Roku, TiVo, VUDU, PS3 etc. the device market is small. Won’t have a major impact for a few years

• Content owners seeing more traffic, at higher bitrates, for longer periods of time, but growth CAGR in 08’ was not as high as 07’

• Average customer saw CDN pricing drop 35% for 08’ compared to 07’, but average traffic growth rate less than 25% in 09’

• Looks like average pricing decline in 2009 will be 20%, compared to 35% last year

6

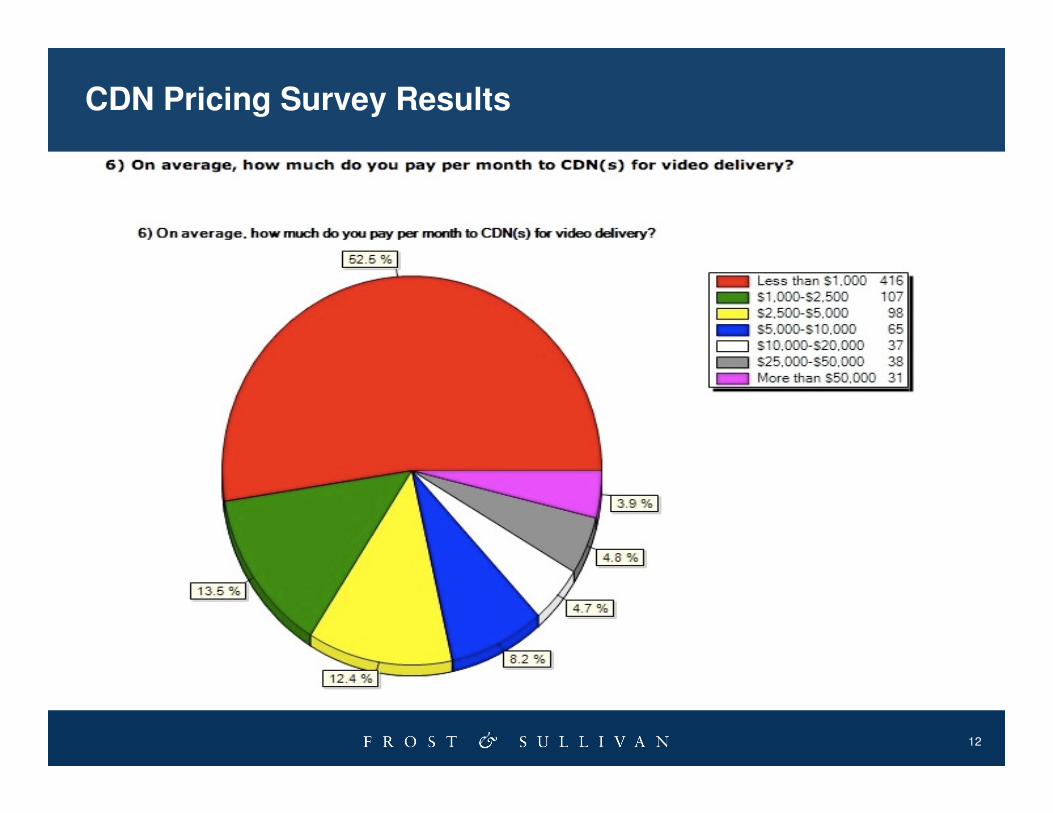

CDN Pricing Survey Results

• The results analysis includes answers from all respondents who took the StreamingMedia.com survey in the 51 day period from Wednesday, August 12, 2009 to Friday, October 02, 2009. 812 completed responses were received to the survey during this time.

• Survey asked the following questions:• Which industry vertical does your company best fall under?

• How are your videos being delivered across CDNs?

• How many CDNs do you currently use for video delivery?

• What is your current contract length with your CDN?

• How much has your total video traffic grown so far this year, compared to last year?

• On average, how much do you pay per month to CDNs for video delivery?

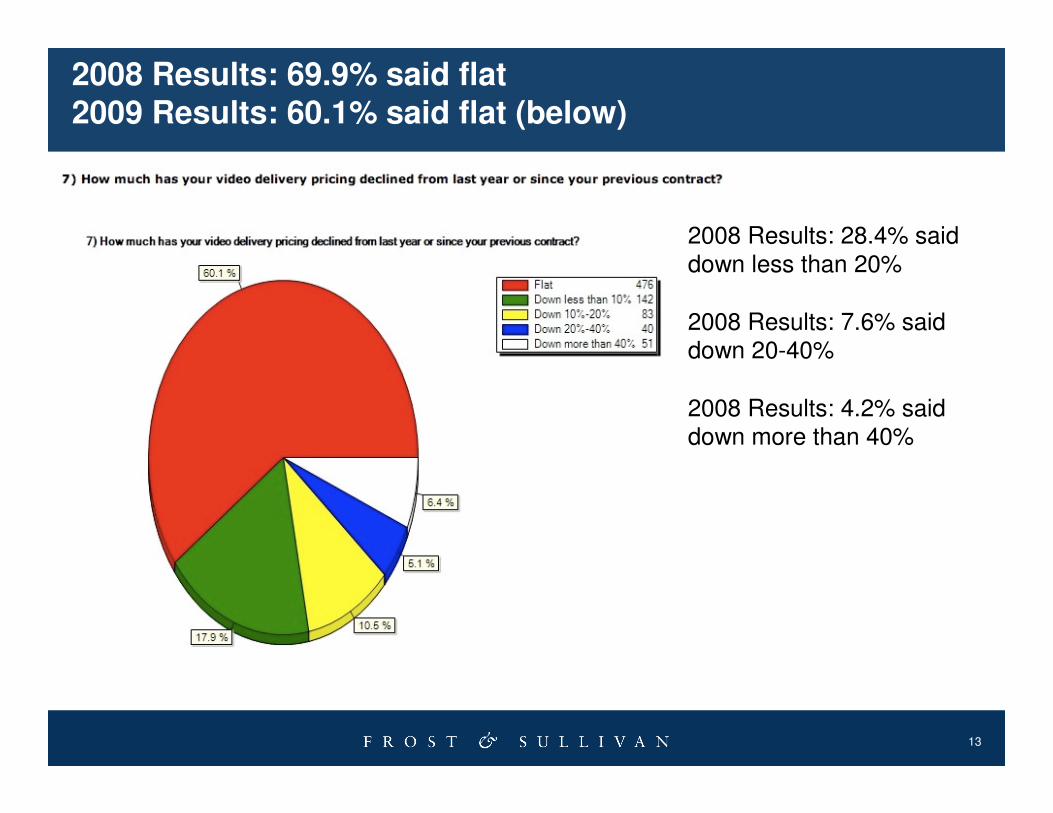

• How much has your video delivery pricing declined from last year or since your previous contract?

• Are you paying CDNs on a per GB delivered model or per Mbps sustained model?

• How much do you pay per Mbps sustained or per GB delivered?

• On average, what is your video delivery traffic per month?

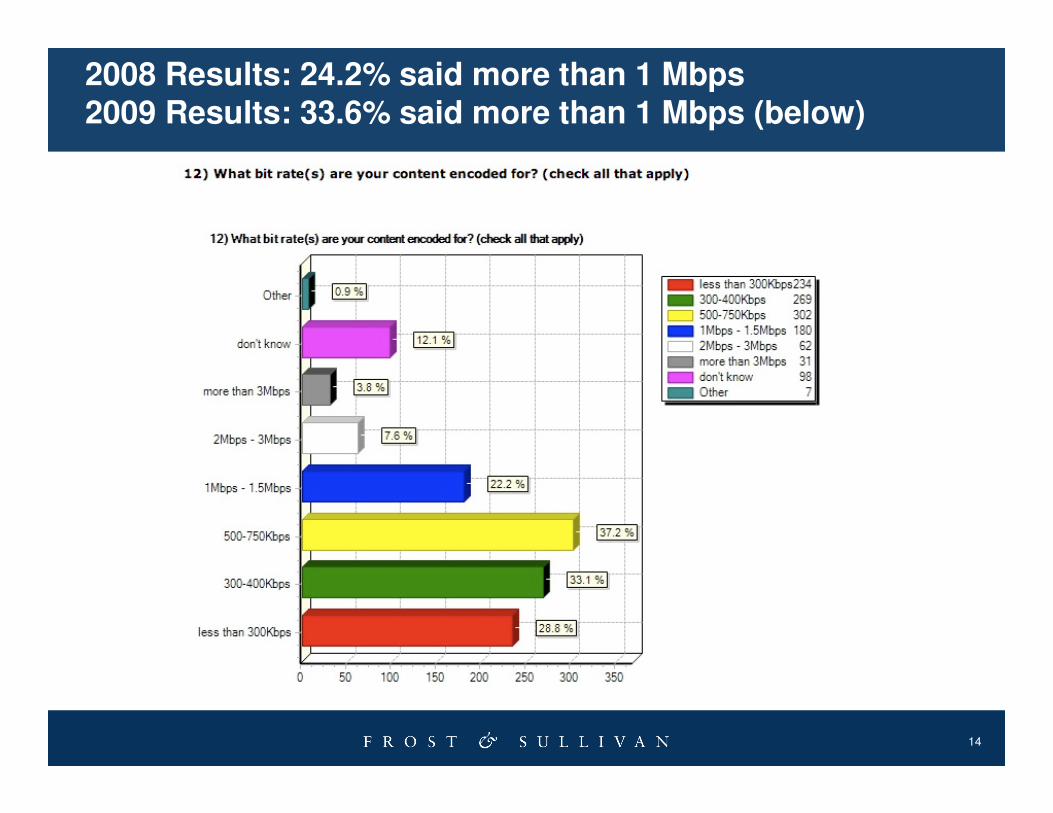

• What bit rates is your content encoded for?

• What is the one thing you think CDNs need to do a better job of?

7

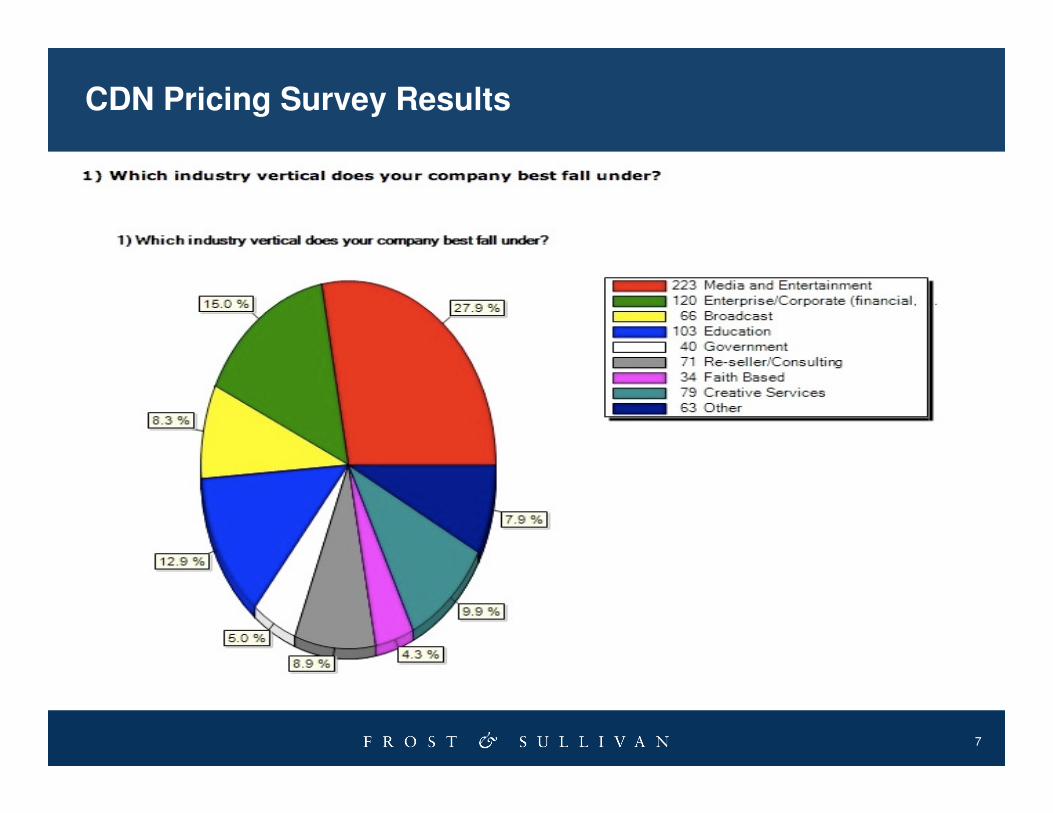

CDN Pricing Survey Results

8

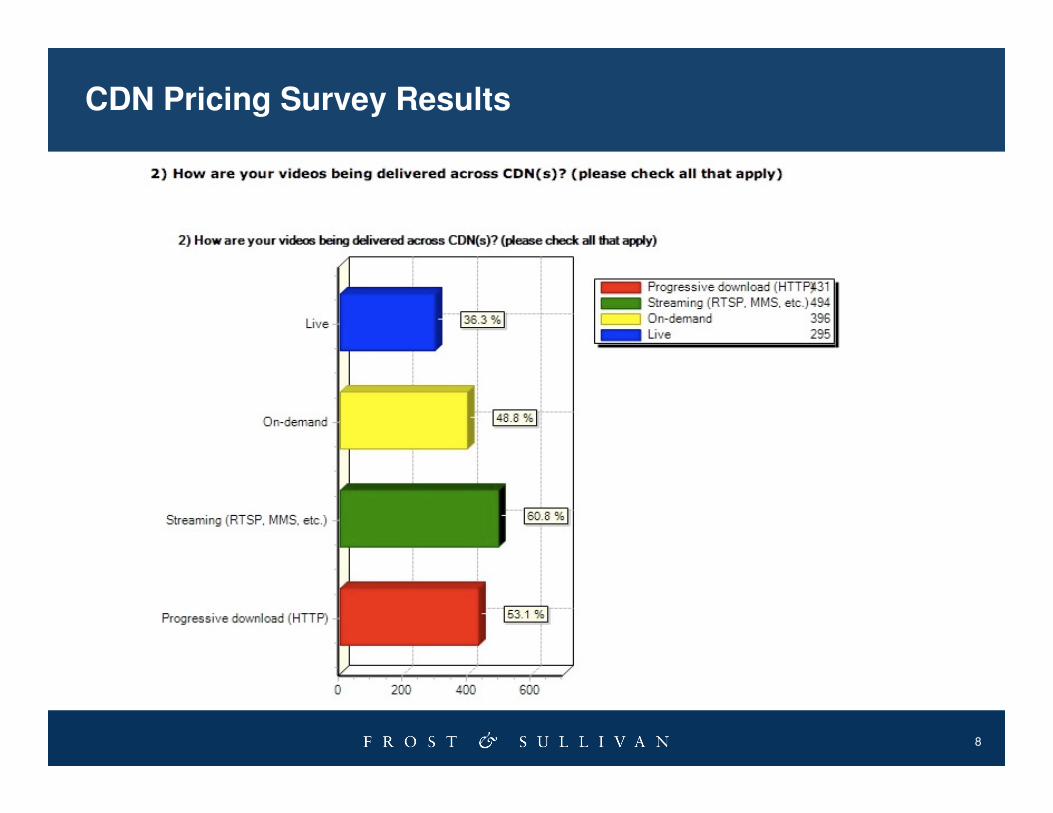

CDN Pricing Survey Results

9

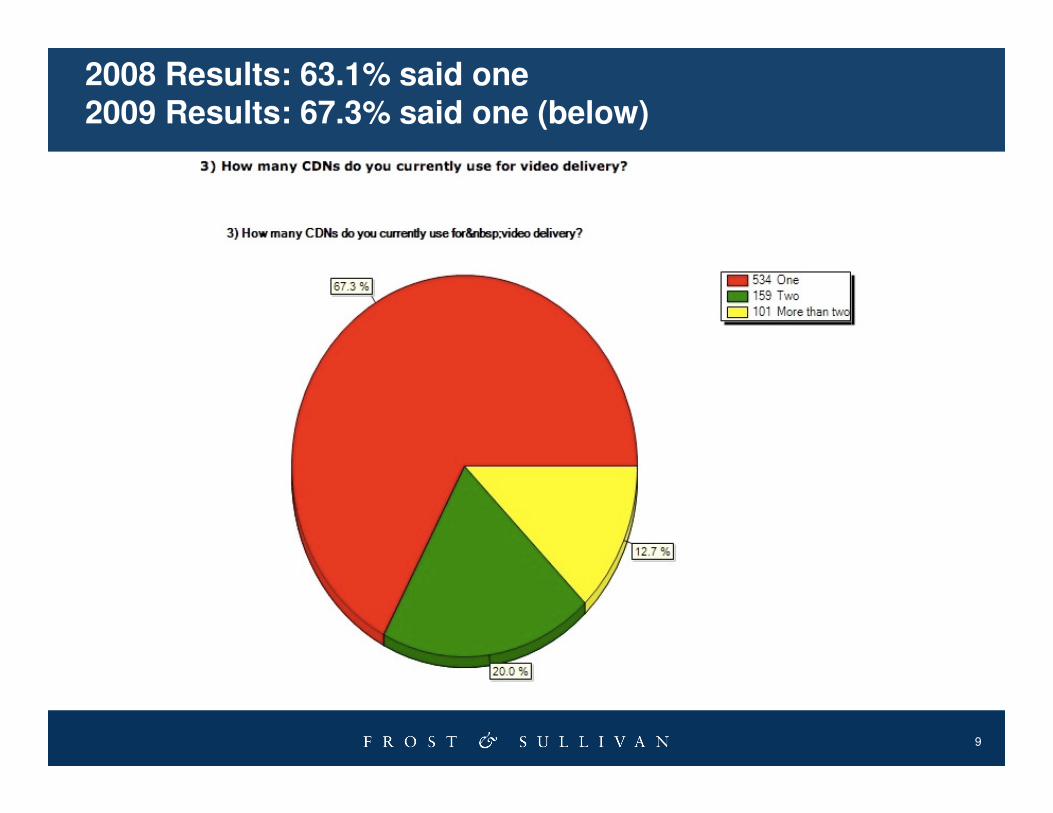

2008 Results: 63.1% said one2009 Results: 67.3% said one (below)

10

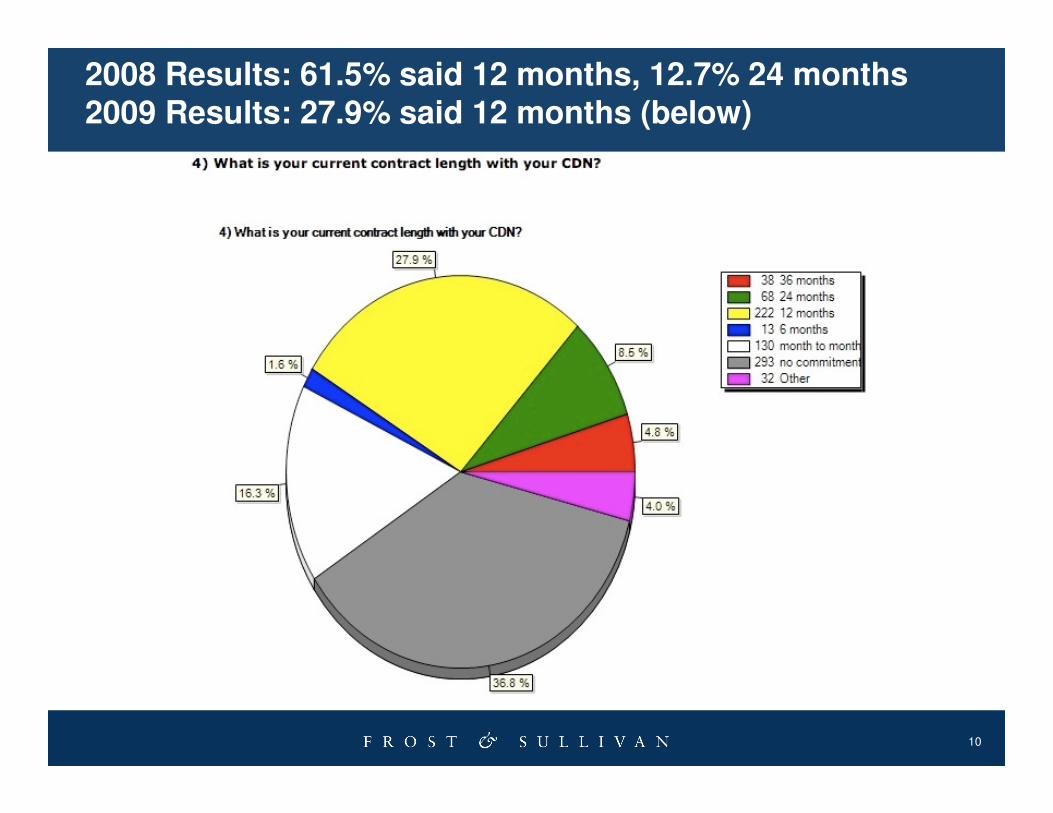

2008 Results: 61.5% said 12 months, 12.7% 24 months2009 Results: 27.9% said 12 months (below)

11

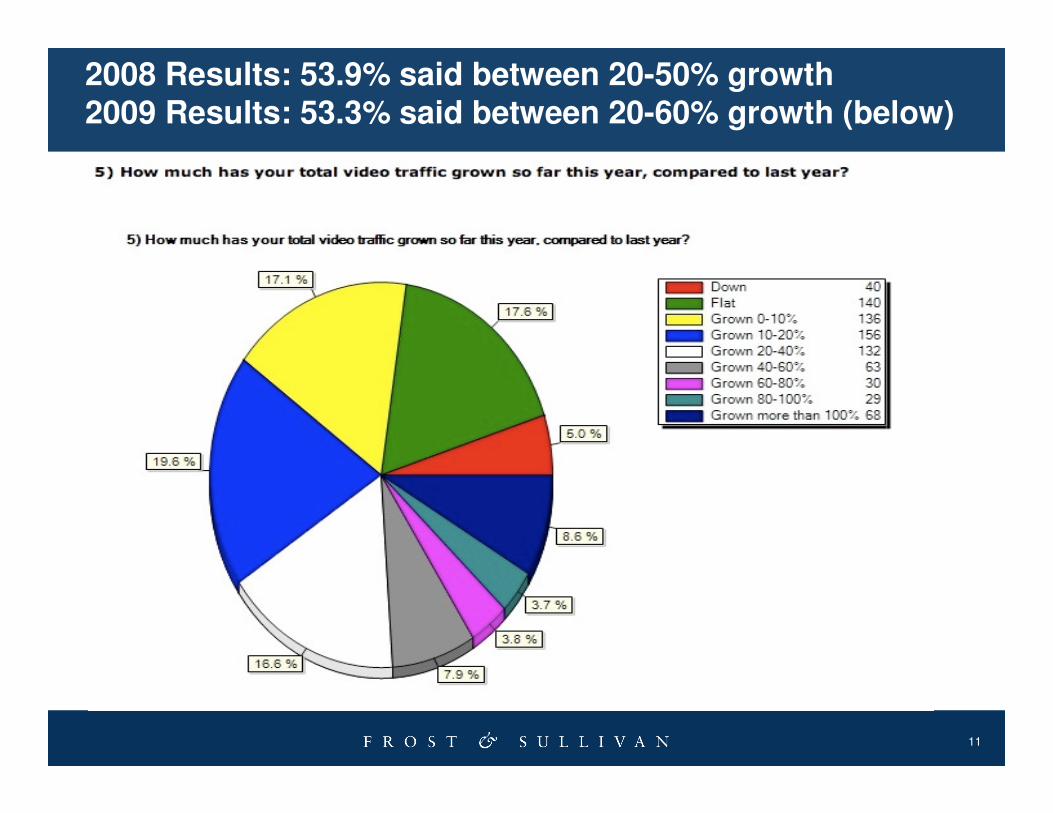

2008 Results: 53.9% said between 20-50% growth2009 Results: 53.3% said between 20-60% growth (below)

12

CDN Pricing Survey Results

13

2008 Results: 69.9% said flat2009 Results: 60.1% said flat (below)

2008 Results: 28.4% said down less than 20%

2008 Results: 7.6% said down 20-40%

2008 Results: 4.2% said down more than 40%

14

2008 Results: 24.2% said more than 1 Mbps2009 Results: 33.6% said more than 1 Mbps (below)

15

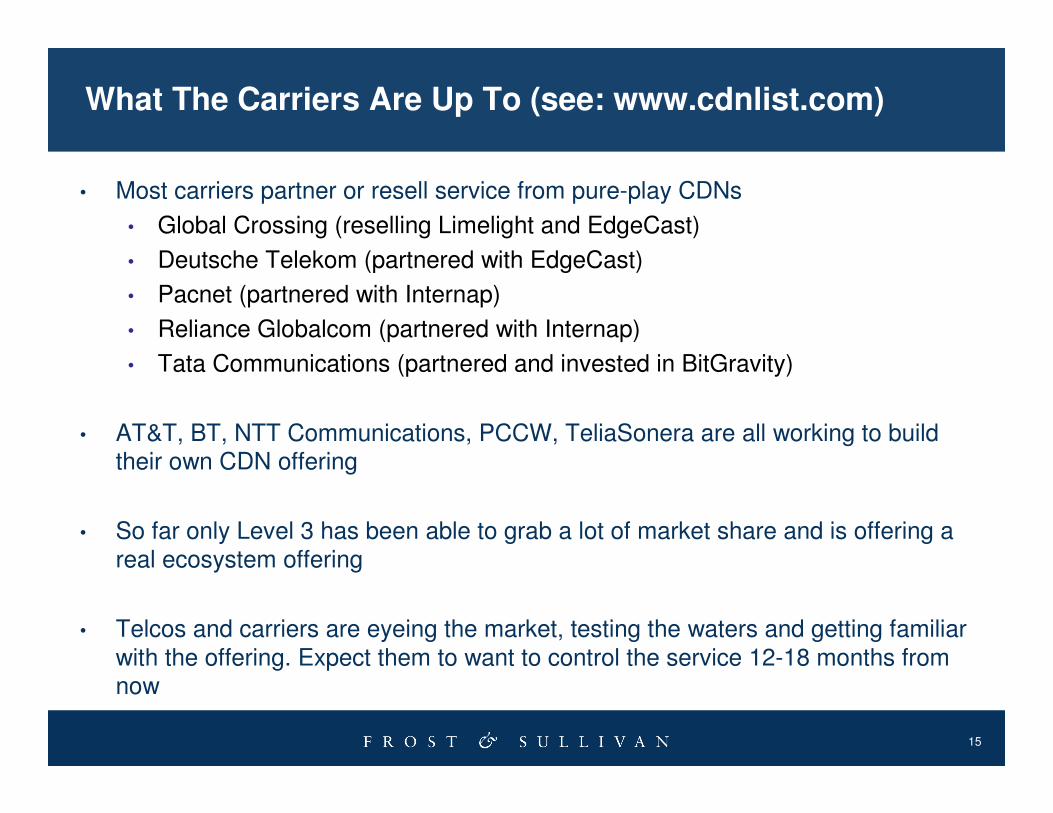

What The Carriers Are Up To (see: www.cdnlist.com)

• Most carriers partner or resell service from pure-play CDNs

• Global Crossing (reselling Limelight and EdgeCast)

• Deutsche Telekom (partnered with EdgeCast)

• Pacnet (partnered with Internap)

• Reliance Globalcom (partnered with Internap)

• Tata Communications (partnered and invested in BitGravity)

• AT&T, BT, NTT Communications, PCCW, TeliaSonera are all working to build their own CDN offering

• So far only Level 3 has been able to grab a lot of market share and is offering a real ecosystem offering

• Telcos and carriers are eyeing the market, testing the waters and getting familiar with the offering. Expect them to want to control the service 12-18 months from now

16

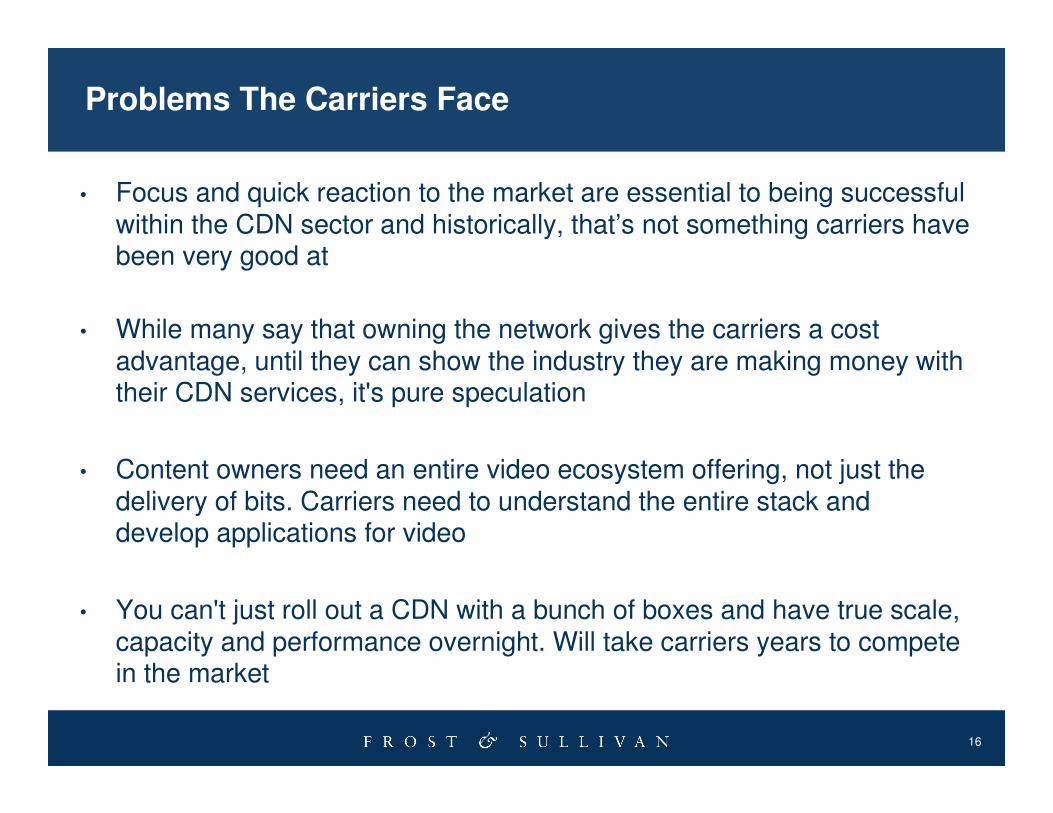

Problems The Carriers Face

• Focus and quick reaction to the market are essential to being successful within the CDN sector and historically, that’s not something carriers have been very good at

• While many say that owning the network gives the carriers a costadvantage, until they can show the industry they are making money with their CDN services, it's pure speculation

• Content owners need an entire video ecosystem offering, not just the delivery of bits. Carriers need to understand the entire stack and develop applications for video

• You can't just roll out a CDN with a bunch of boxes and have true scale, capacity and performance overnight. Will take carriers years to compete in the market

17

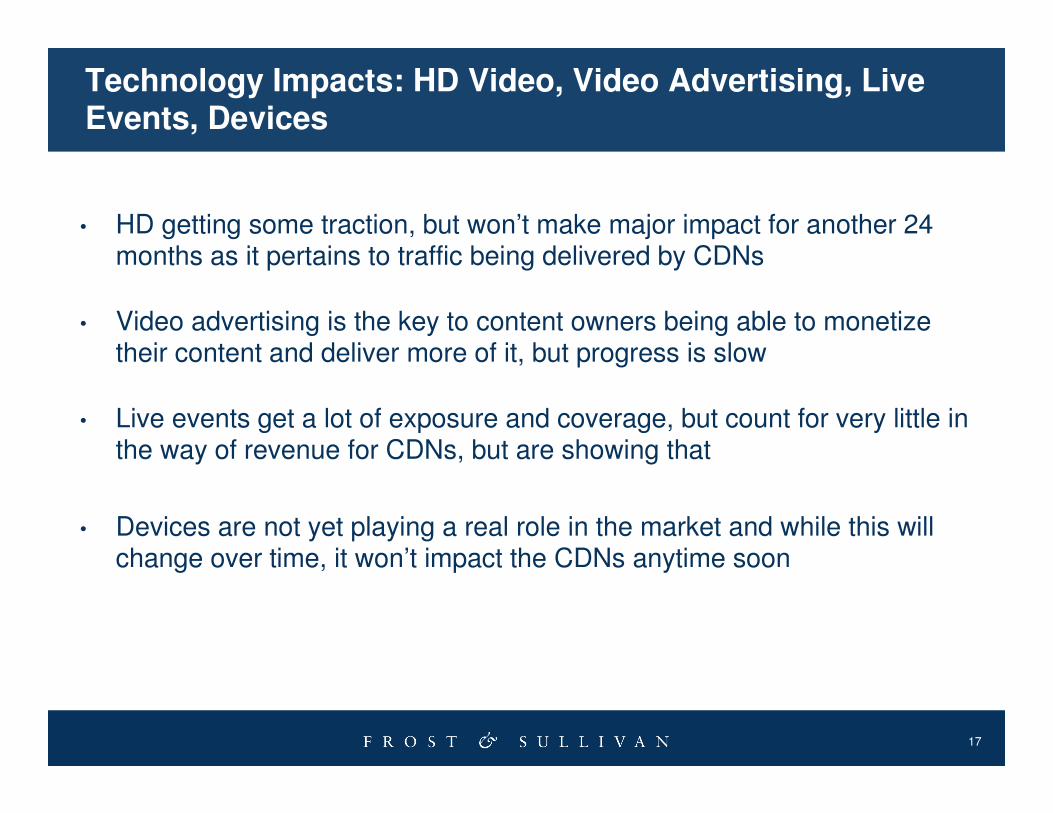

Technology Impacts: HD Video, Video Advertising, Live Events, Devices

• HD getting some traction, but won’t make major impact for another 24 months as it pertains to traffic being delivered by CDNs

• Video advertising is the key to content owners being able to monetize their content and deliver more of it, but progress is slow

• Live events get a lot of exposure and coverage, but count for very little in the way of revenue for CDNs, but are showing that

• Devices are not yet playing a real role in the market and while this will change over time, it won’t impact the CDNs anytime soon

18

Industry Consolidation and Outlook: 12-18 Months

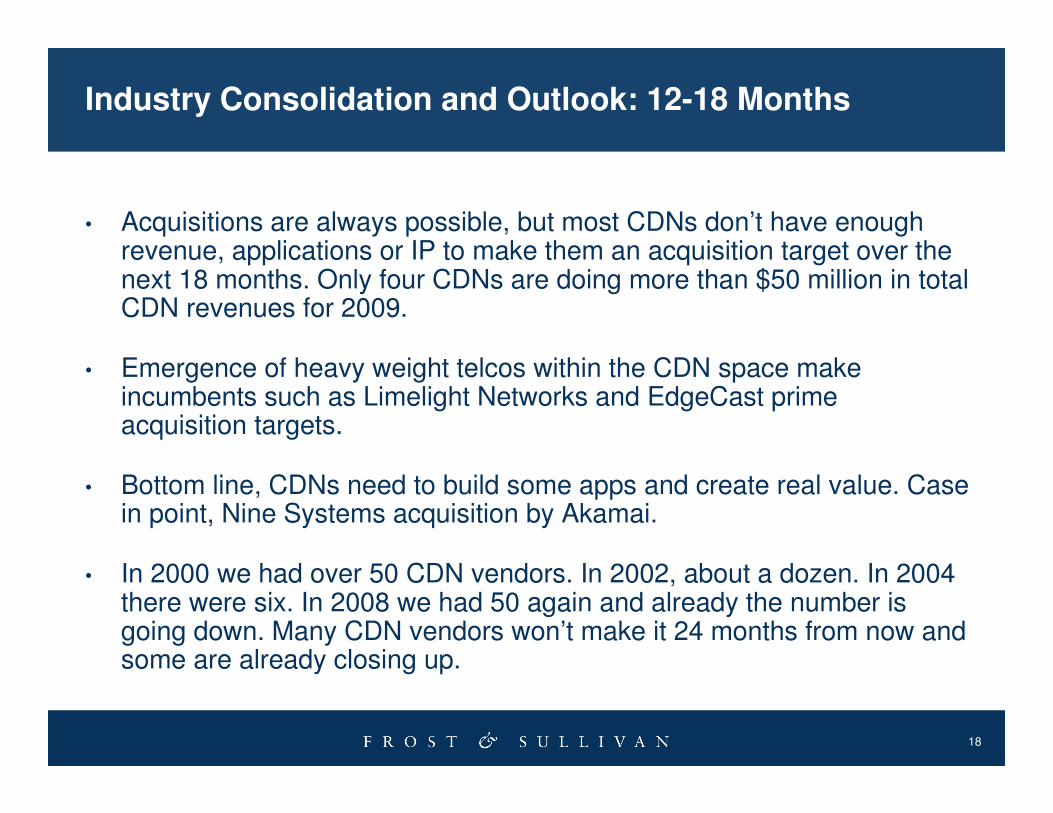

• Acquisitions are always possible, but most CDNs don’t have enough revenue, applications or IP to make them an acquisition target over the next 18 months. Only four CDNs are doing more than $50 million in total CDN revenues for 2009.

• Emergence of heavy weight telcos within the CDN space make incumbents such as Limelight Networks and EdgeCast prime acquisition targets.

• Bottom line, CDNs need to build some apps and create real value. Case in point, Nine Systems acquisition by Akamai.

• In 2000 we had over 50 CDN vendors. In 2002, about a dozen. In 2004 there were six. In 2008 we had 50 again and already the number is going down. Many CDN vendors won’t make it 24 months from now and some are already closing up.

19

Next Steps

� Request a proposal for a Growth Partnership Service or Growth Consulting Services to support you and your team to accelerate the growth of your company. ([email protected])1-877-GoFrost (1-877-463-7678)

� Join us at our annual Growth, Innovation, and Leadership 2010: A Frost & Sullivan Global Congress on Corporate Growth, September 12-15 2010, San Jose, CA (www.gil-global.com)

� Register for the next Chairman’s Series on Growth: The CEO's Perspective on

Competitive Intelligence (November 3rd) (http://www.frost.com/growth)

� Subscribe for Frost & Sullivan’s Growth Opportunity Newsletter and keepabreast of innovative growth opportunities(www.frost.com/news)

20

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

21

Additional Resources

www.contentdeliveryblog.comwww.cdnpricing.com

www.cdnlist.comwww.cdnmarket.comwww.cdnreport.com

www.contentdeliverysummit.com

22

For Additional Information

Jake Wengroff

Director of Corporate Communications

Information & Communication Technologies

(210) 247-3806

Dan RayburnPrincipal AnalystDigital Media Frost & Sullivan(917) [email protected]

Mukul Krishna

Global Program Manager

Digital Media

(210) 247-3850

Craig Hays

Sales Manager

Information & Communication Technologies

(210) 247-2460