caltrain sp qx4strategic+plan+2004/cal...28 the future scenarios ... paul ave bayshore south sf san...

TRANSCRIPT

2004 2023C A L T R A I N

S T R A T E G I C P L A N

J U L Y 1 , 2 0 0 4

P E N I N S U L A C O R R I D O R

J O I N T P O W E R S B O A R D

( C A L T R A I N )

1 2 5 0 S A N C A R L O S A V E .

S A N C A R L O S , C A L I F . 9 4 0 7 0

8 0 0 - 6 6 0 - 4 2 8 7

W W W . C A L T R A I N . C O M

1 From the Executive Director

2 Introduction

2 The Caltrain Strategic Plan 2004–20235 Along the Peninsula7 Caltrain Today

8 Vision & Guiding Principles

8 The Caltrain Vision9 Guiding Principles

20 From Principle to Policy

20 The Scenario Approach21 Policy Questions25 Snapshot of the Continuum

and Future Improvements

28 The Future Scenarios

28 Developing the Scenarios47 Evaluating the Scenarios

50 Conclusions

S T R A T E G I C P L A N

2 0 0 4 | 2 0 2 3

T A B L E O F C O N T E N T S

A C K N O W L E D G M E N T S

Peninsula Corridor Joint Powers Board1250 San Carlos Ave., San Carlos, California 94070

2004 BOARD OF DIRECTORS

John McLemore, ChairMike Nevin, Vice ChairMichael BurnsJosé CisnerosDon GageJim HartnettArthur L. LloydSophie MaxwellKen Yeager

Sue Lempert, Metropolitan Transportation Commission Liason

Michael J. Scanlon, Executive DirectorGeorge Cameron, Chief Administrative Officer and

Acting Chief Financial OfficerChuck Harvey, Chief Operating OfficerRita Haskin, Chief Communications OfficerIan McAvoy, Chief Development Officer

PROJECT STAFF

Larry Stueck, Manager, Planning and ResearchApril Chan, Manager, Capital Programming and GrantsCorinne Goodrich, Manager, Special ProjectsDouglas Kolozsvari, Associate Planner

HNTB CORPORATION1330 Broadway #1630, Oakland, CA 94612Camille Tsao, Senior Transportation Planner

NANCY WHELAN CONSULTING201 Mission Street #1450, San Francisco, CA 94105

NELSON\NYGAARD CONSULTING ASSOCIATES833 Market Street #900, San Francisco, CA 94103

WILBUR SMITH ASSOCIATES201 Mission Street #1450, San Francisco, CA 94105

Art direction, design and production by MIG, Inc., Berkeley, California

CALTRAIN STRATEGIC PLAN 2004 | 2023 1

From the Executive Director

Friends of Caltrain:

On behalf of the Peninsula Corridor Joint Powers Board, (JPB) we are pleased to present the

20-Year Strategic Plan for Caltrain service.

This document is a product of challenging economic times demanding hard choices and

difficult decisions. But it also reflects an optimistic vision and a conviction that continued

dramatic development and even more significant milestones lie ahead in the Caltrain corridor

as we respond to relentless demand by new generations of patrons for faster travel, frequent

schedules, improved facilities and more convenient access.

In 1992, the Joint Powers Board assumed stewardship of the Caltrain system, which was hard

pressed at the time to operate 52 weekday trains over a worn and tired infrastructure.

Throughout the industry, they called it a “fixer-upper railroad.” From any perspective, we have

done some significant fixing during the last 12 years. We have completed a $300 million infra-

structure upgrade including new trackage, rolling stock, signal systems, and—in conjunction with

many of the cities we serve—station improvements for comfort, convenience and accessibility.

That 52-train schedule has expanded to 86, including 10 Baby Bullet trips linking San Jose

Diridon and San Francisco stations in less than an hour.

Much of this upgrade effort has taken place during a chilling economic downturn that has

imposed unprecedented fiscal challenges on every transportation system. Nevertheless, we

have not stopped building; we have not stopped improving; and, as this document will attest,

we have not stopped planning for the future.

Where do we go from here?

This Strategic Plan positions us to proceed as fast, and as far, as market demand and resources

will permit. It outlines three distinct growth patterns: Moderate, Enhanced, and Build-Out. The

document provides for potential service extensions to the south, north and east; for system

electrification; additional trains and more express schedules; and, ultimately, incorporation of

High Speed Rail sometime in the next decade.

Any long-term planning document must contain the means to deal with contingencies. Caltrain

has met that challenge during its developmental years, and we believe the current Strategic

Plan includes adequate measures to assure continued success.

Michael J. ScanlonExecutive Director

CALTRAIN STRATEGIC PLAN 2004 | 2023

INTRODUCTION

3CALTRAIN STRATEGIC PLAN 2004 | 20232

Introduction

The Caltrain Strategic Plan 2004–2023The Strategic Plan is a blueprint for the future of Caltrain. It presents a vision

and guiding principles that shape broad-level policy decisions as well as specific

strategies for service and capital improvements. The Strategic Plan is intended to

be a reference for policymakers, Caltrain staff, and members of the public that

guides them toward a common vision for Caltrain. Above all, it is meant to be an

agent for change.

The Caltrain Strategic Plan includes the following elements:

(1) The Vision & Guiding Principles, which present a vision for Caltrain

and outline principles for guiding policy decisions;

(2) A summary of the Service Plan, which details the service characteristics,

policies, and budget requirements for Caltrain over the next 20 years;

(3) A summary of the Capital Improvement Program (CIP), which identifies

policy and prioritizes capital improvements over the next 20 years; and

(4) A summary of the Finance Plan, which discusses funding strategies

for Caltrain.

Information from the Service, Capital Improvement, and Finance plans is presented

through four future scenarios: the Status Quo, Moderate Growth, Enhanced, and

Build-Out Scenarios. The scenarios are described in detail in the Future Scenarios

chapter (page 28). The service characteristics, operations and capital costs, and

member agency contributions reflected in each of the scenarios are based upon

the Draft Short-Range Transit Plan, Capital Improvement Plan, and Finance Plan as

of June 1, 2004. The information in the Strategic Plan provides a general under-

standing of the costs and benefits of each scenario and provides a basis for com-

paring the scenarios. Adoption of the Strategic Plan does not commit the member

agencies to the funding requirements, service levels, or capital priorities presented

in this document but is an agreement on the principles and policies which will

guide the development of the Short-Range Transit Plan, Service Plan, Capital

Improvement Plan, and Finance Plan. These plans are being finalized and will be

adopted separately from the Strategic Plan in the Fall/Winter of 2004.

Any updated information related to JPB actions subsequent to the adoption of

the Strategic Plan will be included as these supporting plans are finalized. Any

revisions to the Strategic Plan after adoption will be included in an addendum or

in the next Strategic Plan update, anticipated by 2010.

StrategicPlan

Finance Plan

Vision & GuidingPrinciples

Service Plan

Capital Improvement

Plan

S T R AT E G I C P L A N C O M P O N E N T S

CALTRAIN STRATEGIC PLAN 2004 | 2023

INTRODUCTION

5

All of the scenarios are based on rea-

sonable assumptions of revenue avail-

ability—based on past experience and

estimates of future events—and opti-

mize federal and state funds. Where

estimated revenue meets or exceeds

capital program costs, the capital pro-

grams are considered to be fully fund-

ed. Underlying the financial analysis is

the assumption that the local funds

required to match the maximum avail-

able federal revenues will be provided

by Caltrain’s member agencies. These

local matching funds are subject to

annual approval by the three member

agencies. If local matching funds are

not allocated and alternative local

sources are not identified, Caltrain

would not be able to use all of the

federal funds included in the financial

plans and other sources will be required

to meet any shortfalls.

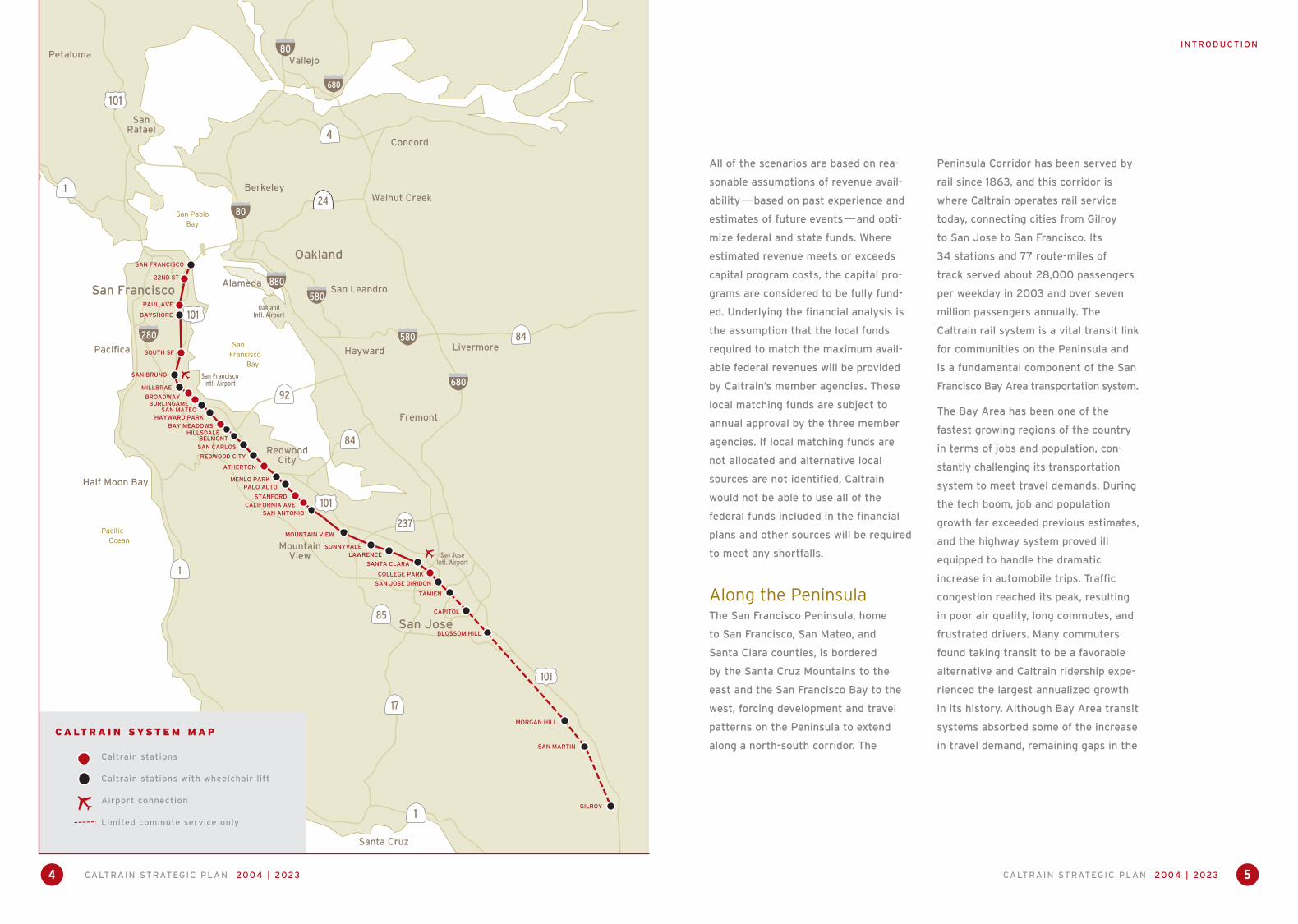

Along the PeninsulaThe San Francisco Peninsula, home

to San Francisco, San Mateo, and

Santa Clara counties, is bordered

by the Santa Cruz Mountains to the

east and the San Francisco Bay to the

west, forcing development and travel

patterns on the Peninsula to extend

along a north-south corridor. The

Peninsula Corridor has been served by

rail since 1863, and this corridor is

where Caltrain operates rail service

today, connecting cities from Gilroy

to San Jose to San Francisco. Its

34 stations and 77 route-miles of

track served about 28,000 passengers

per weekday in 2003 and over seven

million passengers annually. The

Caltrain rail system is a vital transit link

for communities on the Peninsula and

is a fundamental component of the San

Francisco Bay Area transportation system.

The Bay Area has been one of the

fastest growing regions of the country

in terms of jobs and population, con-

stantly challenging its transportation

system to meet travel demands. During

the tech boom, job and population

growth far exceeded previous estimates,

and the highway system proved ill

equipped to handle the dramatic

increase in automobile trips. Traffic

congestion reached its peak, resulting

in poor air quality, long commutes, and

frustrated drivers. Many commuters

found taking transit to be a favorable

alternative and Caltrain ridership expe-

rienced the largest annualized growth

in its history. Although Bay Area transit

systems absorbed some of the increase

in travel demand, remaining gaps in the

CALTRAIN STRATEGIC PLAN 2004 | 20234

1

880

80

580

80

680

4

280

1

1

680

580 84

85

237

101

101

101

101

92

84

17

San Francisco

Oakland

San Jose

RedwoodCity

Pacifica

Santa Cruz

Half Moon Bay

MountainView

Berkeley

San Leandro

Hayward

Alameda

Fremont

Livermore

Walnut Creek

SanRafael

Vallejo

Concord

Petaluma

24

OaklandIntl. Airport

San FranciscoIntl. Airport

San JoseIntl. Airport

Pacific Ocean

San Francisco Bay

San PabloBay

SAN FRANCISCO

22ND ST

PAUL AVE

BAYSHORE

SOUTH SF

SAN BRUNO

MILLBRAE

BROADWAYBURLINGAME

SAN MATEOHAYWARD PARK

BAY MEADOWSHILLSDALE

BELMONTSAN CARLOS

REDWOOD CITY

ATHERTON

MENLO PARKPALO ALTO

STANFORDCALIFORNIA AVE

SAN ANTONIO

MOUNTAIN VIEW

SUNNYVALELAWRENCE

SANTA CLARA

COLLEGE PARK

SAN JOSE DIRIDON

TAMIEN

CAPITOL

BLOSSOM HILL

MORGAN HILL

SAN MARTIN

GILROY

C A LT R A I N S YS T E M M A P

Caltrain stations

Caltrain stations with wheelchair lift

Airport connection

Limited commute service only

CALTRAIN STRATEGIC PLAN 2004 | 2023

INTRODUCTION

6

regional transit network became more

pronounced and many commuters

chose to drive and battle congested

roads and highways. It became appar-

ent that regional mobility and transit

connectivity in the Bay Area needed to

be improved to provide viable trans-

portation alternatives and choices.

Because the Bay Area is the foremost

international center for major tech-

nological development, travel demands

within, to, and from the region are

expected to grow dramatically in the

next 20 years and beyond. Plans for

a High Speed Rail (HSR) system in

California, and multiple Bay Area tran-

sit and highway projects, speak to the

urgency of these transportation needs.

In 2003, the Millbrae intermodal station

opened, making it possible for passen-

gers to transfer directly between

Caltrain and BART. In June 2004,

Caltrain introduced its express or

“Baby Bullet” service, which reduces

overall travel time between San Jose

and San Francisco. In the initial plan-

ning stages are the San Francisco

Downtown Extension, Dumbarton Rail

Project, and expansion of the Diridon

Station in San Jose, all of which will

greatly improve the connectivity

between Caltrain and other major tran-

sit systems in the region. Furthermore,

the prospect of HSR brings tremendous

opportunities for Caltrain to serve

interregional travelers and to imple-

ment system-wide improvements, given

that the two rail systems would share

the existing Caltrain corridor and key

stations between San Jose and San

Francisco. Through these and other

service and operational improvements,

Caltrain is positioned to assume an

ever increasing role in contributing to

regional mobility solutions to meet the

needs of Bay Area residents and visitors.

CALTRAIN STRATEGIC PLAN 2004 | 2023

INTRODUCTION

7

Whether serving travel needs at a

local or regional level, Caltrain is an

ideal transit alternative to support

the quality of life in local communities

along the Peninsula and contribute

to the achievement of the region’s

broader goals.

Caltrain Today Caltrain is owned and operated by

the Peninsula Corridor Joint Powers

Board (JPB), which consists of three

members from each of the JPB

partners: San Francisco, San Mateo,

and Santa Clara counties. The San Mateo

County Transit District (SamTrans) is

the managing agency which includes

oversight of the contract operator,

engineering, finance, capital project

development, project monitoring,

planning, marketing, customer service,

fare and schedule development,

performance monitoring, personnel

recruitment, budget and grant adminis-

tration, and public outreach. Amtrak

was awarded the operating contract

on a competitive basis and is responsi-

ble for providing train service, main-

taining Caltrain equipment, collecting

fares, and conducting ridership counts

and passenger surveys as necessary.

Four committees provide input to

Caltrain on a regular basis: the Staff

Coordinating Council, which includes

staff from the three partners; the

Citizens Advisory Committee, consist-

ing of three citizens from each of the

three counties; the Bicycle Advisory

Committee, comprised of Caltrain staff

and community members with an

interest in bicycle issues; and the

Accessibility Advisory Committee,

which includes Caltrain staff, Caltrain

riders with disabilities, and other repre-

sentatives of people with disabilities.

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

11,000,000

92–93 93–94 94–95 96–97 97–98 98–99 99–00 00–01 01–02 02–03 03–0490–91 91–92FY 95–96

A N N U A L R I D E R S H I P F Y 1 9 9 1 - F Y 2 0 0 4

CALTRAIN STRATEGIC PLAN 2004 | 2023

VIS ION & GUID ING PRINCIPLES

9CALTRAIN STRATEGIC PLAN 2004 | 20238

At the regional level, Caltrain must play a key role in mobility management. It must

offer people an attractive option to automobile travel while helping to achieve con-

gestion relief and air quality goals. It must encourage the use of other alternative

modes by facilitating seamless connections to local and regional transit systems,

providing state-of-the-art facilities for bicycles and wheelchairs, and improving

pedestrian access.

Guiding PrinciplesThe following Guiding Principles are designed to bring policy-makers and decision-

makers one step closer to turning the Caltrain vision into reality. The Guiding

Principles do not prescribe specific actions but provide a policy framework for lead-

ing the Caltrain management team in a direction that will enable it to achieve its

ultimate goals. They are:

• Satisfy passengers and build ridership

• Invest wisely in system improvements

• Promote regional connectivity and cooperation with other

transportation providers

• Partner with communities and broaden communications with the public

• Develop a solid financial foundation that ensures long-term sustainability

Each of the Guiding Principles is explained further on the following pages with asso-

ciated objectives, challenges, and opportunities.

Vision & Guiding Principles

The Caltrain VisionThe Caltrain Vision through 2023 is to become the preferred mode of travel along

the Peninsula Corridor by:

• Providing passengers with a world-class travel experience

• Acting as a major catalyst for redevelopment and economic activity in

communities along its route

• Playing a key role in mobility management along the Peninsula Corridor

and in the Bay Area region as a whole

Caltrain is a vital component of the Bay Area transportation system that will have

an ever increasing impact at the individual, local and regional levels. For it to be the

preferred mode of travel along the Peninsula Corridor, it must succeed and excel at

these three levels.

At the individual level, Caltrain must provide passengers with a world-class travel

experience. It should keep and attract passengers by offering convenient, efficient,

pleasant, and economical service that is safe and secure. Riding Caltrain should

allow people to enjoy a quality of life they cannot experience while driving in traffic.

At the local level, Caltrain must act as a major catalyst for redevelopment and eco-

nomic activity. It must support existing communities along its route by serving the

people that live, work, and play there. By keeping and attracting passengers, Caltrain

will bring potential customers to local businesses near its stations. Caltrain must be

a partner with the communities through which it travels to realize development

opportunities and meet other common goals. Caltrain stations must be inviting and

contribute to a community’s sense of place.

1

2

3

4

5

CALTRAIN STRATEGIC PLAN 2004 | 2023

GUID ING PRINCIPLES

11

To satisfy passengers and build ridership Caltrain must:

• Provide a flexible mix of local and express service that reflects the

travel needs of Caltrain passengers. Reduce overall travel time with

operational and platform improvements to facilitate faster boarding.

Increase frequency of service.

• Provide or facilitate passenger amenities on board trains and at stations,

such as Internet access, banking, dry cleaning, child care, and other

“non-transit” services.

• Address station access needs with a balanced approach that includes

coordinating service with connecting transit operators in San Francisco, San

Mateo, and Santa Clara counties; promoting walking, bicycling, carpooling,

and carsharing to and from stations; improving access for persons with

disabilities; and finding innovative and effective solutions for meeting

parking demand.

• Create inviting stations that serve as landmarks and activity centers for the

communities in which they are located.

• Provide complete, reliable, real-time information that is easily obtainable at

transit stations, over the phone, via the Internet, or through other media.

• Implement a fare structure that is easy to understand and a universal fare

medium that is easy to collect and transfer across transit providers.

• Understand current and potential markets along the Caltrain route to

establish ridership targets, set service levels, and market Caltrain service to

potential riders.

• Regularly conduct passenger market research to evaluate service

performance, measure customer satisfaction, and improve service.

• Continually strive to improve the passenger experience and the Caltrain

organization as a whole.

CHALLENGES

> A major challenge to satisfy-ing passengers and increasingridership will be to build a solidfinancial foundation thatensures long-term, dedicatedfunding for substantial systemand service improvements.

> Another challenge will be toreshape the public perceptionand brand image of Caltrain asa viable and preferred alterna-tive to the automobile.

OPPORTUNITIES

> Transit-Oriented Development(TOD) presents opportunities tobuild potential ridership bylocating residences, businesses,and services near Caltrain stations.

> The proposed California HighSpeed Rail would present anumber of opportunities forcomplementary capitalimprovements that will makeCaltrain a more attractive transit system by improvingservice, improving Caltrain’simage, and increasing opportu-nities for regional connections.

> Planned capital programs and enhanced service improve-ments can enable Caltrain toserve the travel demands ofcurrent and potential riders andshape the public perception ofCaltrain as a modern, fast, andreliable transportation mode.

> Amenities for Caltrain customers could be provided at low cost by providing anenvironment to attract privatevendors that could provideservices.

CALTRAIN STRATEGIC PLAN 2004 | 202310

1G U I D I N G P R I N C I P L E 1

Satisfy Passengers and Build Ridership

Without satisfied passengers, no part of the Caltrain vision can become a reality. To

keep and attract riders, Caltrain must be convenient to use, pleasant to ride, and take

people to places they want to go. Caltrain must be a competitive alternative to travel-

ling by automobile by providing its passengers with a world-class travel experience.

SERVICE & PASSENGERAMENITIES

STATION ACCESS & ENVIRONMENT

INFORMATION & FARE SYSTEM

MARKETING & SERVICEEVALUATION

Paramount to customer satisfaction is the quality of Caltrain service, which must be

fast, frequent, reliable, and safe. Caltrain should accommodate a variety of travel

needs, whether one is traveling a short distance to a neighboring town or traveling a

great distance between counties. Trains should use modern, comfortable, and clean

vehicles and technology to enhance operations, to provide passengers with information

and amenities, and to enhance the public image of Caltrain.

Convenient station access and inviting station facilities are also important to the passen-

ger experience. Stations play an important function, not only as the interface between

rail service and the communities they serve, but as gateways to the Caltrain system.

They should function as community meeting places and as landmarks that enhance the

neighborhoods in which they are located. Caltrain stations should contribute to each

community’s sense of place. Station access for all passengers, including seniors and per-

sons with disabilities, should be addressed by balancing the need for adequate parking

facilities with the need for improved access for pedestrians, transit, and bicycle.

Information on the Caltrain route, station access, schedules, and fares should be easily

obtained at stations, over the phone, via the Internet, or through other media. Real-

time information on arrival and departure times should be made available to passen-

gers and potential riders with the use of advanced technology. The fare payment

process should be simplified, and fare media should be universal to facilitate transfers

between different transit operators.

Passenger and public comments and suggestions are absolutely essential to improving

Caltrain in the future. Customer input should be collected on a regular basis to evalu-

ate service performance and measure customer satisfaction. Understanding the needs

of current and potential markets along the corridor through outreach and other com-

munication tools will enable Caltrain staff to identify and prioritize system improve-

ments, project future ridership, and attract more passengers.

CALTRAIN STRATEGIC PLAN 2004 | 2023

GUID ING PRINCIPLES

13

To invest wisely in system improvements Caltrain must:

• Balance service and capital improvements with market demand and

availability of financial resources. Develop financial and capital

improvement plans that consider various funding scenarios and subsequent

plans of action.

• Use valuable market research to inform decisions about service

improvements that will attract more riders, such as employing “universal

design elements” that appeal to many travelers.

• Develop standards and targets that are useful in monitoring the efficient

and effective use of resources.

• Balance system rehabilitation and modernization projects to increase

reliability; deliver fast and frequent service; and provide quieter, cleaner, and

more comfortable trains. Expand and manage system capacity effectively to

maximize use of the tracks without overbuilding.

• Find balanced and cost-effective solutions for improving station access for

all passengers. Ensure that Caltrain passengers can access rail stations via

transit, bicycle, or walking. Facilitate transfers by coordinating schedules

with other transit operators and promoting increased feeder service to

Caltrain stations. Encourage bicycling and walking to stations by providing

related facilities and amenities. Balance the need for adequate parking

facilities at stations where it is appropriate.

• Enhance stations to create transportation facilities that are “places” and

integral parts of the communities in which they are located. Factor in the

unique characteristics of stations when planning station facilities and

access.

• Capitalize on opportunities presented by partnerships and third party

investments to improve the system. (These may include route extensions,

station enhancements, or other system improvements that are funded by

other organizations.)

CALTRAIN STRATEGIC PLAN 2004 | 202312

2G U I D I N G P R I N C I P L E 2

Invest Wisely in System Improvements

Investing wisely means that capital programs and service improvements must be

balanced with market demand and financial feasibility. Capital projects must have

longevity, and improvements overall must benefit a majority of users and prove

effective in achieving Caltrain goals.

FINANCIAL FEASIBILITY

MARKETAWARENESS

SERVICE & CAPITALIMPROVEMENTS

THIRD PARTYINVOLVEMENT

Implementation of system improvements must be prioritized and measured against the

availability of financial resources. The development of multiple funding scenarios will

enable Caltrain to strategize the financing and implementation of improvements over

the next 20 years.

To provide the level of service that passengers seek from a world-class rail transit

system, ongoing efforts to plan and implement system improvements must be

complemented by market awareness. It is essential that regular market research

be conducted to evaluate whether Caltrain is meeting the needs of its passengers

and to plan for system improvements that will attract potential passengers.

The ability of Caltrain to provide enhanced service is inextricably linked to capital

improvements, therefore service and capital improvements must be carefully

coordinated. They must respond to market demand and be balanced with financial

feasibility. Management of system capacity will be required in conjunction with

capacity expansion in order to maximize use of the right-of-way and to avoid

costly overbuilding.

Involvement from partnering agencies or third parties, such as local government

funding of route extensions or private investment in station improvements, allows

Caltrain to stretch its dollars to fund more improvements. Working with other

organizations requires more coordination to maximize the opportunities that result

from pooling resources.

CHALLENGES

> Challenges to implementingsystem improvements willinclude acceptance by thegoverning boards of the JPB partners and securingadequate and long-term fundingto finance the improvements.Achieving consensus onpriorities and funding.

> Another challenge toimplementing systemimprovements will be to develop the public and privatepartnerships necessary to implement systemimprovements efficiently and effectively.

OPPORTUNITIES

> Many of the plannedimprovements to the Caltrainsystem will enable Caltrain to be more efficient and to be compatible with othersystems. Electrification, forexample, would be one of theways that would allow Caltrainto be extended into downtownSan Francisco and would berequired to accommodate futureHigh Speed Rail on the Caltrainroute. It would also improveenvironmental quality byreducing noise and emissions.

CALTRAIN STRATEGIC PLAN 2004 | 2023

GUID ING PRINCIPLES

15

To promote regional connectivity and cooperation with other

transportation providers Caltrain must:

• Understand the influence of the land use/transportation nexus so that

Caltrain can become an active participant in addressing regional mobility

needs.

• Maximize connectivity between Caltrain and regional transportation

providers including ACE, Amtrak, Capitol Corridor, BART, VTA light rail,

MUNI Metro, regional bus service, and airport connectors. Strategies include

increasing feeder service to stations, coordinating schedules, developing

fare agreements, and integrating public information. Minimize transfer time

and total travel time of regional trips with timed transfers, an integrated fare

system, and system improvements to facilitate quick boarding and alighting.

• Expand Caltrain service with network extensions to facilitate regional trips

and to better serve Caltrain passengers. (Service expansion could be

achieved through partnerships with other agencies or by third party

implementation.)

• Provide transit transfer information at stations that is easy to follow and

understand.

• Work with other transportation providers and local agencies to build

adequate facilities for joint use between multiple transit operators. (Factor

track capacity needs of other transit providers and freight operators that

use the Caltrain right-of-way.)

• Capture an increasing percentage of the mode split of north-south trips

made along the Peninsula corridor.

CHALLENGES

> The primary challenge to promoting regionalconnectivity is developing theinteragency partnerships thatare required to coordinatemultiple transit systems so thatthey function seamlessly.

> Another challenge topromoting regional connectivitywill be financing the capital andservice improvements thatmust be made in order tofacilitate seamless connectionsbetween transit systems.

OPPORTUNITIES

> Expansion projects at theDiridon Station in San Jose andthe Transbay Terminal in SanFrancisco would facilitate directconnections between multipletransit operators (rail and bus).

> Several of the planned system improvements presentopportunities for servingregional trips on Caltrain. These include extensions todowntown San Francisco, across the Dumbarton Bridge to the East Bay, and to Salinasand Monterey.

> By connecting with HighSpeed Rail, Caltrain will have an opportunity to serve ridersthat are traveling to and fromthe region.

CALTRAIN STRATEGIC PLAN 2004 | 202314

3G U I D I N G P R I N C I P L E 3

Promote Regional Connectivity and Cooperation with Other Transportation Providers

Promoting regional connectivity is essential to meet regional mobility needs, achieve

environmental goals, and provide Bay Area residents and visitors with viable

transportation options. It is also a critical component of developing a more

sustainable future for the Bay Area through a stronger integration of land use and

the transportation system. By cooperating with other agencies and transportation

providers, Caltrain can improve the movement of people and goods throughout

the region.

MOBILITY &CONGESTIONMANAGEMENT

INTERAGENCYCOORDINATION

FREIGHT & GOODS MOVEMENT

To serve regional objectives, Caltrain must be effective in alleviating traffic congestion,

particularly along the Peninsula Corridor. As population and job growth occur over

the next 20 years, continued low-density development patterns and the scarcity of

affordable housing in urban centers will result in more automobile travel, more traffic,

and environmental degradation. The problems that stem from traffic congestion

challenge all Bay Area transportation providers to be proactive in finding a solution.

To meet regional travel demands, the regional transportation system must function

as one seamless system rather than as multiple disjointed parts. An optimal regional

system facilitates timed transfers, employs an integrated fare system, and delivers

real-time information. The contribution that Caltrain makes to improve regional

connectivity will assist in meeting regional goals related to congestion management,

air quality, and land use. Coordinating with other transit providers to connect service

and build intermodal facilities will allow Caltrain to better serve its passengers and the

communities along its route.

The Caltrain right-of-way provides the only freight rail access to the Peninsula and

San Francisco. It plays a key role in goods movement and alleviating truck traffic

congestion on local roads and highways. Understanding freight needs is essential for

Caltrain to continue improving regional mobility and supporting local businesses.

CALTRAIN STRATEGIC PLAN 2004 | 2023

GUID ING PRINCIPLES

17

To partner with communities and broaden communications with

the public Caltrain must:

• Strive to improve relationships with cities and external agencies. Develop

strong relationships with the public, policy makers, and Caltrain staff by

conducting frequent outreach efforts and acting upon lessons learned

from outreach. Develop an effective external affairs program.

• Find win-win solutions for community issues, such as safety, and train and

construction noise.

• Manage corridor capacity to maximize and coordinate use of the tracks by

multiple transportation operators.

• Continue to improve system safety and security as necessary and work

with local jurisdictions and law enforcement to effectively implement

safety measures. Support programs in emergency preparedness and crime

prevention.

• Promote and create stations as public spaces. Present any station

improvements, grade separations, and other route enhancements as part of

a larger corridor plan.

• Maximize transit-oriented development opportunities along the Caltrain

route. Work with member agencies in pursuing TOD in the individual

counties. Work with local jurisdictions to support businesses by attracting

people to the communities where stations are located.

CHALLENGES

> A major challenge to partneringand broadening communicationswith the public and other transpor-tation providers is being able tobuild consensus and find win-winsolutions for competing interests.

OPPORTUNITIES

> Caltrain can foster solidrelationships with other agenciesand communities by collaboratingto achieve system improvements,whether gathering public input orsharing responsibility forimplementing projects. Systemimprovements that reduce trainnoise or increase system safety inthe Caltrain right-of-way benefitpassengers and non-passengersalike.

> Engaging in joint-developmentventures on TOD projects is one wayin which Caltrain can begin toestablish partnerships with publicand private entities. Future TODprojects in the planning stageinclude: (1) the new TransbayTerminal in downtown SanFrancisco, which will serve Caltrain,AC Transit, BART, Golden GateTransit, Muni’s Metro and buses,SamTrans, and HSR. It will besurrounded by over seven millionsquare feet of new developmentincluding 4,700 residential units; (2)the Peninsula Corridor Plan whichincludes plans for creating vibrantcommunities and building TODaround multiple San Mateo CountyCaltrain stations; and (3) theDiridon/Arena StrategicDevelopment Plan, which includesthe expansion of the Diridon Stationin San Jose and intensive housingand commercial development. Theexpanded Diridon Station will serveCaltrain, ACE, Amtrak, BART, CapitalCorridor, HSR, VTA light rail, andbuses.

CALTRAIN STRATEGIC PLAN 2004 | 202316

4G U I D I N G P R I N C I P L E 4

Partner with Communities and Broaden Communications with the Public

Caltrain's customer base includes a much larger group than the people who ride its

trains each day. Forming strong partnerships with these extended customers—

employers, local businesses, and communities—enables Caltrain to be more effective

in addressing system safety, improving station environments, and achieving

environmental quality.

COMMUNITYRELATIONSHIPS

SAFETY & SYSTEMIMPROVEMENTS

DEVELOPMENTPARTNERSHIPS

ENVIRONMENTALSTEWARDSHIP

The healthy relationships that Caltrain fosters with passengers, communities,

businesses, local governments, other transit operators, policy makers, and its staff

will ultimately affect the ability of Caltrain to achieve its goals. This requires regular

communication within and outside of the organization, followed by consensus building

and action.

Addressing system issues such as safety and management of track capacity benefit

the public and other transportation providers as well as Caltrain and its passengers.

Safety issues are critical as they affect passengers, operators, and people in the

communities along the Caltrain route. Several system improvements, such as fencing

and station/platform enhancements, can address immediate safety concerns. Some

improvements, such as grade separations, can achieve multiple objectives in addition

to increasing safety along the right-of-way, including reducing train noise. Programs

in emergency preparedness, crime prevention, and system safety and security play

important roles in making the Caltrain system safer.

Similarly, transit-oriented development (TOD) offers partnership opportunities, provides

a mix of housing and services near the stations, and enhances the communities

in which they are located. Development of strong working relationships with local

government will enable Caltrain to be more effective in this arena. Partnering with

local government and businesses to provide amenities and services for passengers

would be another opportunity for Caltrain to work with other organizations to provide

better service to its passengers.

By investing in system improvements that reduce noise and air pollution, promote

transit use and walkable communities, and facilitate regional mobility, Caltrain helps

improve the environmental quality of local cities and the region.

CALTRAIN STRATEGIC PLAN 2004 | 2023

GUID ING PRINCIPLES

19

To develop a solid financial foundation that ensures long-term

sustainability Caltrain must:

• Balance the implementation and timing of system improvements with

committed funding.

• Develop a capital improvement program that outlines potential development

scenarios based on prospective funding opportunities.

• Explore innovative ways to secure long-term funding to guide Caltrain into

the future. Programs such as high-speed rail bonds, bridge tolls, local sales

tax authorizations, future federal authorizations as well as non-traditional

programs such as tax increment financing, lease backs, public private part-

nerships, and joint TOD opportunities should be pursued to ensure funding is

available to meet future needs.

• Support each county’s effort toward developing a dedicated source of

funding. Secure local matching funds to leverage committed state and

federal capital grants.

• Develop financial plans and programs that reflect the financial capacity of

the member agencies.

CHALLENGES

> A major challenge to developing a strong financialfoundation will be garneringlegislative support for dedicat-ed funding sources, such as asales tax measure.

> Another challenge will be to establish partnerships with public or private entitiesto explore more innovativefinancing options.

OPPORTUNITIES

> Opportunities for solidifyinglong-term financial resourcesfor Caltrain include multipleinnovative funding strategiesthat have proven effective else-where, including joint TODopportunities near stations.

CALTRAIN STRATEGIC PLAN 2004 | 202318

5G U I D I N G P R I N C I P L E 5

Develop a Solid Financial Foundation that Ensures Long-term Sustainability

Because financial stability is an essential ingredient to the long-term success of

Caltrain, it is critical that Caltrain secure adequate funding for a multi-year period to

deliver a program consistent with its vision. The JPB must embrace a finance plan

that is acceptable to the three member agencies, while employing innovative

financial management to reach new levels of investments.

DEDICATEDFUNDING

INNOVATIVEAPPROACHES

Traditional funding sources alone will be insufficient to meet the long-term needs of the

future Caltrain system. Multi-year financial planning is essential to ensure that capital

and service visions become budgeted realities.

Partnering with local business, developers, cities, private interests and the utilization of

“cutting edge” and “yet-to-be-invented” financial techniques together with the funding

initiatives of tomorrow, such as high-speed rail bonds, federal reauthorization, local

sales tax reauthorization, etc., will provide the financial framework to increase

revenues. These strategies accompanied with traditional financial programs will guide

Caltrain to provide the financial means to meet the market demands of the future.

CALTRAIN STRATEGIC PLAN 2004 | 2023

FROM PRINCIPLE TO POLICY

21CALTRAIN STRATEGIC PLAN 2004 | 202320

The Build-Out Scenario is the “ultimate” scenario that integrates Caltrain and the

proposed statewide high-speed rail system. The objective of the Build-Out Scenario

is to capture a significant market share of trips by providing a travel experience sim-

ilar to the Enhanced Scenario that is complemented by the additional service and

amenities offered by the connection to high-speed rail. It assumes that additional

funding resources via high-speed rail bonds and other resources would be available.

An aggressive innovative financing program would be required.

More detailed information on each of the scenarios is presented in the chapter titled

“The Future Scenarios.”

Policy QuestionsSix policy questions were developed that address how Caltrain will make key decisions

regarding future service and capital improvements and financial strategies. Many

decisions regarding capital improvements need to be made within the next few years

so that the necessary funding can be secured and costly re-dos are avoided. The

findings and evaluation of the scenarios, along with input received from the member

agencies and the general public were used to answer the following policy questions:

• Scenario Approach: Should one scenario be selected or should the scenar-

ios be viewed as part of a continuum? In a continuum, key funding opportu-

nities and increased demand for service can trigger a shift to another

scenario.

• Financial Strategy: Should Caltrain continue with annual review utilizing the

“pay-as-you-go” approach or strive for long-term stability by utilizing innova-

tive finance techniques?

• Service Levels: Should service levels be determined by projected financial

resources or should it be market-driven?

• System Rehabilitation: Should Caltrain follow a normalized rehabilitation

and replacement schedule or follow an accelerated schedule that is com-

bined with other capital improvement projects?

From Principle to Policy

The Scenario ApproachFollowing the development of the Vision & Guiding Principles, four future scenarios

were developed to prepare Caltrain for different possible financial futures in light of

multiple unknowns, such as upcoming ballot measures and the economic climate.

These scenarios were used to answer key policy questions and will set a clear direc-

tion for making detailed service, capital, and financial decisions. The four scenarios

are: Status Quo, Moderate Growth, Enhanced, and Build-Out.

The Status Quo Scenario is the most financially constrained scenario. It follows a

“pay-as-you-go” approach and assumes that only current (2004) levels of commit-

ted and programmed funds are available. It is assumed that upcoming local sales tax

measures would not be reauthorized and no innovative funding sources would be

pursued. The objective of the Status Quo Scenario is to keep the railroad operating

at current levels of service, optimize existing infrastructure, and limit investment in

improvements other than normalized rehabilitation and replacement.

The Moderate Growth Scenario is a steady growth scenario and is financially con-

strained in the first five years. Similar to the Status Quo Scenario it follows a “pay-

as-you-go” approach, but requires some additional resources above current levels to

fund planned improvements. It is assumed that upcoming local sales tax measures

would not be reauthorized and no innovative funding sources would be pursued. The

objective of the Moderate Growth Scenario is to optimize the operating and capital

programs with limited increases in funding resources, service, and capital improve-

ments.

The Enhanced Scenario is the “market-driven” scenario. It is financially constrained

in the first five years (same as the Moderate Growth Scenario), and assumes that

additional resources become available in the outer years. The main objective of the

Enhanced Scenario is to capture latent market demand by providing optimal levels

of service, improving station access and regional connectivity, and incorporating uni-

versal design elements and customer amenities that are characteristic of a “world

class” railroad. Innovative financing techniques would have to be pursued.

CALTRAIN STRATEGIC PLAN 2004 | 202322 CALTRAIN STRATEGIC PLAN 2004 | 2023 23

FROM PRINCIPLE TO POLICY

approach given the unpredictable

nature of the economic climate and

future funding sources. The strategy

for Caltrain should be to begin with

the Status Quo Scenario and

advance to the Moderate Growth,

Enhanced, or Build-Out Scenario

when critical milestones are

reached. Critical milestones would

include securing additional capital

and operating funds. Because the

first five years of the capital pro-

gram are financially constrained

in all scenarios, there is some flexi-

bility with regard to securing funds

to meet the projected shortfalls.

• Financial Strategy: Should Caltrain

continue with annual review by

utilizing the “pay-as-you-go”

approach or strive for long-term

stability by utilizing innovative

finance techniques?

Given the uncertainty of the “pay-

as-you-go” approach and the com-

plexities it creates when planning

and coordinating future improve-

ments, Caltrain should strive for

long-term stability through dedicat-

ed funding sources and innovative

techniques. This strategy is in line

with the fifth guiding principle,

which is to “develop a solid financial

foundation that ensures long-term

sustainability.” Securing dedicated

funding sources will enable Caltrain

to meet projected funding shortfalls,

plan future service and capital

improvements, and implement the

improvements in a timely manner. It

will be critical for shifting from the

Status Quo or Moderate Growth to

the Enhanced or Build-Out Scenario.

• Service Levels: Should service

levels be determined by financial

resources or should it be market-

driven?

Service levels must be tied to

productivity and public demand, yet

balanced with funding availability.

Good information on market demand

is necessary to determine the

service characteristics that are

desired by the public and to

prioritize service improvements as

funding becomes available. Because

service improvements sometimes

require capital projects, the avail-

ability of capital funding can directly

affect service levels.

• System Rehabilitation: Should

Caltrain follow a normalized rehabili-

tation and replacement schedule or

an accelerated schedule?

FROM PRINCIPLE TO POLICY

• Electrification: Should electrifica-

tion be deferred until funding is

available or should design continue?

• Capacity Improvements:

What level of capacity improve-

ments should Caltrain invest in to

improve headways and reliability of

service in the peak periods?

Each scenario has a different combina-

tion of assumptions regarding funding

availability and finance strategies,

service levels, and capital improve-

ments. These shape the general policy

direction and objective of each

scenario. In general, the Status Quo

and Moderate Growth scenarios take a

more conservative approach in their

policy positions, while the Enhanced

and Build-Out Scenarios include

market-driven service and capital

improvements as well as innovative

financing techniques. The scenario policy

approaches are presented below in

Table 1.

The following conclusions to the six

policy questions were drawn based on

comprehensive outreach to the public

and to the member agencies:

• Scenario Approach: Should one

scenario be selected or should

the scenarios be viewed as part of

a continuum?

It is clear that the continuum is the

most prudent and practical scenario

TA B L E 1 : S C E N A R I O P O L I C I E S

MODERATESTATUS QUO GROWTH ENHANCED BUILD-OUT

Annual review, Long-term stability, Long-term stability,Financial Maintain 2004 Annual review, Innovative InnovativeStrategy level of Pay-as-you-go Finance Finance

investment Strategies Strategies

Service Maintain 2004 Moderate Market-driven Market-drivenLevels level of service growth

System Scheduled/ Scheduled/ Accelerated AcceleratedRehabilitation Normalized Normalized

Continue Deferred Deferred until with Design,

Electrification indefinitely funding Continue with must coordinate Design with HSR construction

Only CTX North quadrant Capacity improvements (San Mateo North, Central, Entire routeImprovements complete in County) and and South

2004 South (Partial)

available

CALTRAIN STRATEGIC PLAN 2004 | 2023

FROM PRINCIPLE TO POLICY

25

Snapshot of theContinuum and FutureImprovementsBased on the policy approach outlined

in the previous section, a conceptual

schedule was developed for the capital

improvements that can be expected in

the next 20 years. The following time-

line provides a snapshot of what the

capital program will include. The

projects or programs that depend on

service and financial triggers, such

as establishing dedicated funding

sources, are distinguished from ongoing

programs, such as rehabilitation, which

are almost completely funded.

Projections of revenue availability

are based on past experience and

reasonable estimates of future events.

These revenue projections assume

that all of the local matching funds

identified in the financial plans will

be approved annually by Caltrain’s

three member agencies.

As shown in the header row of the time-

lines below, Caltrain could begin with

the Status Quo Scenario and shift to

the Moderate Growth Scenario within

the first five years, once funding for

identified shortfalls is secured and a

funding plan for electrification is devel-

oped. By the end of the first five years,

CALTRAIN STRATEGIC PLAN 2004 | 2023

FROM PRINCIPLE TO POLICY

24

Capital replacement and rehabilita-

tion must not be deferred but should

be implemented in the most cost-

effective manner. When opportuni-

ties arise, rehabilitation should be

accelerated to prevent a situation of

deferred maintenance, which can

greatly increase maintenance costs.

It is critical to balance rehabilitation

with other improvements in the

capital program.

• Electrification: Should electrifica-

tion be deferred until funding is

available or should design continue?

Design for the electrification

project should continue and should

be factored into all improvement

projects along the right-of-way.

Phasing of implementation should

be part of the design development.

A funding plan must be created in

order to implement the project and

avoid further delays.

• Capacity Improvements: What level

of capacity improvements should

Caltrain invest in to improve head-

ways and reliability of service in the

peak periods?

Capital improvements that expand

system capacity, such as adding

additional tracks, must be tied to

service objectives, and must be bal-

anced with other projects in the

capital program. Caltrain should

explore the most cost-effective

means for improving service before

investing in capacity expansion.F U T U R E I M P R O V E M E N T S T I M E L I N E

REPLACEMENT AND REHABILITATION

ENHANCEMENT PROGRAM

Electrification

Other Enhancements

CAPACITY EXPANSION

SUPPORT PROGRAM

EXPANSION (THIRD-PARTY PROJECTS)

Downtown San Francisco Extension

Dumbarton Rail Corridor

Monterey/Salinas Extension

STATUS QUO TO

MOD. GROWTH

2004-2008

MOD. GROWTH TO

ENH./BUILD-OUT

2009-2013

ENHANCED/BUILD-OUT

2014-2018 2019-2023

Programmed for completion within timeframe

Requires funding or other trigger for completion within timeframe

(includes design/development and construction).

CALTRAIN STRATEGIC PLAN 2004 | 2023

FROM PRINCIPLE TO POLICY

27

ENHANCEMENT PROGRAM

• Electrification project completed

within the first ten years. Full

funding has been identified for

the project in the outer years of the

20-year time period. A funding plan

to bring all dedicated funds forward

must be developed in order to

implement the project within the

ten-year time frame.

• Other enhancements, such as

improved station access and

customer amenities, will require

additional funding.

CAPACITY EXPANSION

• Funding has been identified in

the first five years for capacity

expansion projects, which include

grade separations, track and signal

construction, and station improve-

ments. Additional capacity expansion

may be necessary to substantially

improve service levels and will

depend on demand for service

and the availability of funds.

SUPPORT PROGRAM

• The support program consists of

project development and capital pro-

gram development. Full funding has

been identified for the next 20 years.

REGIONAL EXTENSIONS

• Regional extensions include the

Downtown extension to a rebuilt

Transbay Terminal in San Francisco,

the Dumbarton Rail Corridor, and

the extension to Monterey and

Salinas. These are considered third-

party projects whose capital costs

are not included in the Capital Plan.

While they are all currently partially

funded and not included in the

Status Quo or Moderate Growth

Scenarios, it is assumed that plan-

ning and design will continue and

that they will be implemented within

the next 10 years.

CALTRAIN STRATEGIC PLAN 2004 | 2023

FROM PRINCIPLE TO POLICY

26

it will be determined whether or not

high-speed rail will be constructed

along the Caltrain corridor. In the

second five-year period, Caltrain could

shift from the Moderate Growth

Scenario to either the Enhanced or

Build-Out Scenario, depending on the

status of the high-speed rail project.

This scenario shift from the Moderate

Growth Scenario would require Caltrain

to secure operating and capital funds

for the Enhancement and Capacity

Expansion programs. By the second

half of the 20-year period, Caltrain

would be in the Enhanced or

Build-Out Scenario.

Existing sales tax measures (Measure

A) in San Mateo and (Measure A) Santa

Clara counties and a new sales tax

measure (Proposition K) in San

Francisco County provide funds for

Caltrain capital projects. Two upcoming

ballot measures that would provide

funding for enhancements and capacity

expansion are the reauthorization of

the San Mateo County sales tax

(November 2004) and the high-speed

rail bond measure (November 2006 or

2008). Revenue from the San Mateo

County sales tax would help to meet

most of the $220 million capital short-

fall in the Moderate Growth Scenario.

Any additional funding sources could be

used toward achieving improvements

included in the Enhanced Scenario.

If the high-speed rail bond measure

passes, Caltrain would be positioned

to shift into the Build-Out Scenario by

the second five-year period.

The following describes the capital

program according to the scenario

approach outlined above:

REPLACEMENT AND

REHABILITATION

• Ongoing throughout 20-year period

independent of scenario. May be

accelerated in the Enhanced and

Build-Out Scenarios. Full funding has

been identified for the Replacement

and Rehabilitation program in the

Status Quo and Moderate Growth

Scenarios. Over ninety-five percent

of Replacement and Rehabilitation

funding sources have been identified

for the Enhanced and Build-Out

Scenarios.

• Major programs include replacement

and overhaul of rolling stock and

rehabilitation of track, bridges,

tunnels, signals and grade crossings.

Replacement of rolling stock must

be coordinated with the timing of

the electrification project which will

require the purchase of new electric

locomotives. Platform improvements

at key stations to remove the hold-

out rule are included.

CALTRAIN STRATEGIC PLAN 2004 | 2023

THE FUTURE SCENARIOS

29CALTRAIN STRATEGIC PLAN 2004 | 202328

The Future Scenarios

Developing the ScenariosOnce the policy approach for each scenario was defined, the financial, service, and

capital assumptions were developed further and are detailed in three supporting

plans: the Finance, Service, and Capital Plans. The three plans are currently being

finalized and will be presented to the Joint Powers Board for adoption in Fall/Winter

of 2004. The following are descriptions and objectives of each supporting plan.

FINANCE PLAN OBJECTIVES

The Finance Plan details the funding assumptions and funding strategies for each

scenario. Specifically, the Finance Plan objectives are to:

• Identify available funding over the next 20 years

• Maximize the availability of federal and state revenues in cooperation

with the member agencies

• Identify discretionary sources that are not being utilized

• Develop an inventory of potential innovative finance programs

• Match available funding with eligible capital and service programs

• Project funding shortfalls and develop strategies to deliver future programs

SERVICE PLAN OBJECTIVES

The Service Plan outlines the service goals for each of the scenarios as well as a

20–year plan to deliver them. Its main objectives are to:

• Determine future level of service (Trains per day/per hour)

• Design a flexible mix of service (Express/Limited/Local)

• Identify the triggers (productivity or other performance measures)

for changes in service

• Identify the efforts needed to increase market share

As stated in the Guiding Principles, understanding market demand is the key to

retaining existing riders and attracting new riders. It will influence the mix and

scheduling of Caltrain service, the nature and timing of capital improvements that

support service and operations, and the overall passenger experience on Caltrain.

Meeting market demand requires:

• Creating a flexible mix of service—local, limited, express

• Optimizing service levels and reducing overall trip times

• Improving connections between Caltrain and other systems

• Providing better access to stations (pedestrian, ADA, transit, bicycle

and vehicular access)

• Providing amenities to enhance the passenger experience

Universal Design Elements. Market research in the Caltrain service area reveals

that many service improvements to transit will have broad appeal to existing and

potential riders and will substantially increase ridership. These universal design ele-

ments address key traveler attitudes and desires, forming the core of the Caltrain

brand identity:

• Privacy and Comfort is important to all of the service population in varying

degrees. Travelers desire comfortable, stress-free travel and privacy from

other travelers. Lower cost strategies include training and enforcement

policies to control noisy or unruly passengers. Higher cost efforts include

providing spacious seating on all trains and interiors with some separation

from other travelers.

• Personal Safety is perceived as very important to the vast majority of our

service population while accessing or riding the system. Strategies to address

the need for personal safety include zero tolerance policies for aggressive

behavior and well-lighted, graffiti-free shelters with 911 emergency phones.

• Addressing Flexibility, or the need to travel to many locations at times that

vary from day to day, is a challenge for transit. Successful strategies include

mid-day shuttle services at major business parks, station cars and other

personal transport rentals, and improved land use to increase access to

retail and commercial services.

CALTRAIN STRATEGIC PLAN 2004 | 2023

THE FUTURE SCENARIOS

31CALTRAIN STRATEGIC PLAN 2004 | 2023

THE FUTURE SCENARIOS

30

• Reliability of service is a key

attribute that addresses passengers’

desire to minimize unexpected delay.

Improving stations to eliminate

“hold-out” delays, providing for

faster boarding of passengers

needing assistance, and increasing

Caltrain track capacity will all

contribute to increased service reli-

ability. Also important are reliable

connections to other rail services,

buses, and shuttles.

• Increasing the Ease of Transit Use

is possible through service improve-

ments such as universal fare media

or including transfer costs in a sin-

gle fare, providing easy access to

transit information, and implement-

ing real-time information. In addition

to making transit more user-friendly,

the increasing hassle and cost of

auto use—external factors often

associated with parking and traffic

congestion—make transit a more

attractive option for travelers.

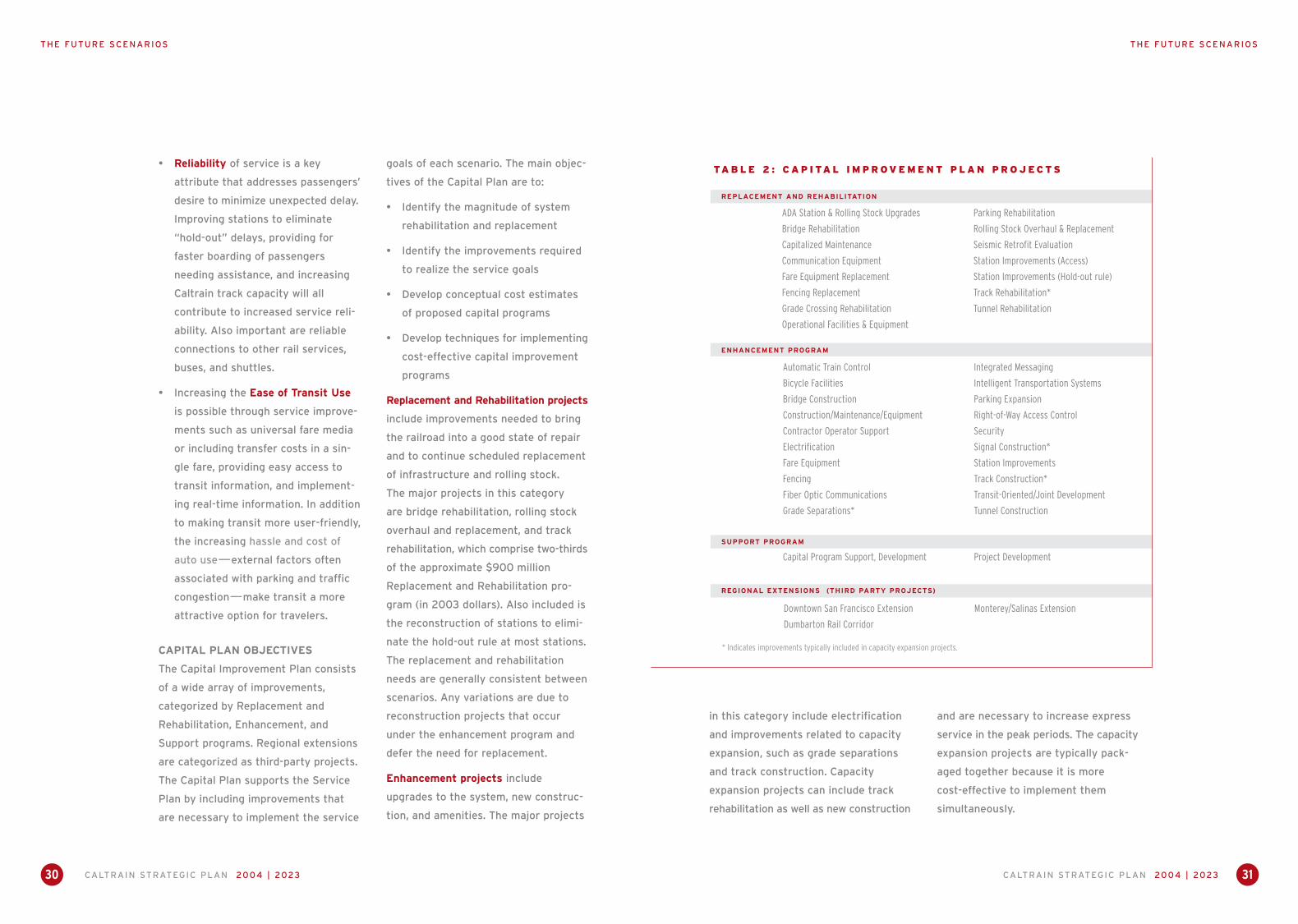

CAPITAL PLAN OBJECTIVES

The Capital Improvement Plan consists

of a wide array of improvements,

categorized by Replacement and

Rehabilitation, Enhancement, and

Support programs. Regional extensions

are categorized as third-party projects.

The Capital Plan supports the Service

Plan by including improvements that

are necessary to implement the service

goals of each scenario. The main objec-

tives of the Capital Plan are to:

• Identify the magnitude of system

rehabilitation and replacement

• Identify the improvements required

to realize the service goals

• Develop conceptual cost estimates

of proposed capital programs

• Develop techniques for implementing

cost-effective capital improvement

programs

Replacement and Rehabilitation projects

include improvements needed to bring

the railroad into a good state of repair

and to continue scheduled replacement

of infrastructure and rolling stock.

The major projects in this category

are bridge rehabilitation, rolling stock

overhaul and replacement, and track

rehabilitation, which comprise two-thirds

of the approximate $900 million

Replacement and Rehabilitation pro-

gram (in 2003 dollars). Also included is

the reconstruction of stations to elimi-

nate the hold-out rule at most stations.

The replacement and rehabilitation

needs are generally consistent between

scenarios. Any variations are due to

reconstruction projects that occur

under the enhancement program and

defer the need for replacement.

Enhancement projects include

upgrades to the system, new construc-

tion, and amenities. The major projects

TA B L E 2 : C A P I TA L I M P R O V E M E N T P L A N P R O J E C T S

REPLACEMENT AND REHABILITATION

ENHANCEMENT PROGRAM

SUPPORT PROGRAM

REGIONAL EXTENSIONS (THIRD PARTY PROJECTS)

ADA Station & Rolling Stock Upgrades

Bridge Rehabilitation

Capitalized Maintenance

Communication Equipment

Fare Equipment Replacement

Fencing Replacement

Grade Crossing Rehabilitation

Operational Facilities & Equipment

Parking Rehabilitation

Rolling Stock Overhaul & Replacement

Seismic Retrofit Evaluation

Station Improvements (Access)

Station Improvements (Hold-out rule)

Track Rehabilitation*

Tunnel Rehabilitation

Automatic Train Control

Bicycle Facilities

Bridge Construction

Construction/Maintenance/Equipment

Contractor Operator Support

Electrification

Fare Equipment

Fencing

Fiber Optic Communications

Grade Separations*

Integrated Messaging

Intelligent Transportation Systems

Parking Expansion

Right-of-Way Access Control

Security

Signal Construction*

Station Improvements

Track Construction*

Transit-0riented/Joint Development

Tunnel Construction

Capital Program Support, Development Project Development

Downtown San Francisco Extension

Dumbarton Rail Corridor

Monterey/Salinas Extension

* Indicates improvements typically included in capacity expansion projects.

in this category include electrification

and improvements related to capacity

expansion, such as grade separations

and track construction. Capacity

expansion projects can include track

rehabilitation as well as new construction

and are necessary to increase express

service in the peak periods. The capacity

expansion projects are typically pack-

aged together because it is more

cost-effective to implement them

simultaneously.

CALTRAIN STRATEGIC PLAN 2004 | 2023 33

THE FUTURE SCENARIOS

TA B L E 3 : S C E N A R I O C H A R A C T E R I S T I C S S U M M A R Y—S TAT U S Q U O A N D M O D E R AT E G R O W T H

FINANCE (IN 2003 $) STATUS QUO MODERATE GROWTH

OperationsFarebox Revenue Historical Some Growth

Member Contributions Stabilized* Stabilized* or Decrease

CapitalFederal/State/Local Historical Historical

San Francisco Sales Tax Through 2034 Through 2034

San Mateo Sales Tax Through 2008 Through 2008

Santa Clara Sales Tax Through 2036 Through 2036

High-Speed Rail Bonds None None

Innovative Techniques None None

SERVICE BY 2023 STATUS QUO MODERATE GROWTH

Express Service Goal 10 trains/weekday 20 trains/weekdayone-hour headways one-hour headways

Weekday Total Trains 86 100

Saturday/Sunday Trains 32/30 32/30

Shuttle Buses (station access) 45 59

Customer Amenities Low Low

Average Weekday Ridership 43,700 59,600

Annual Ridership 14,369,000 19,484,000

Annual Operating Cost Avg./Total $83M / $1.67B $90M / $1.81B

Annual Member Contrb. Avg./Total $44M / $873M $44M / $872M

CAPITAL (IN 2003 $) STATUS QUO MODERATE GROWTH

Replacement & Rehabilitation Same Rehabilitation needs in all scenarios

Capacity Expansion North quadrant North and (partial) (SM County grade South quadrants

separations) by 2011

Electrification (Revenue Service) None 2018

Regional Extensions (Third-Party Projects)Downtown San Francisco No No

Dumbarton No No

Salinas/Monterey No No

Calif. High-Speed Rail No No

Total Capital Program Cost $1.151 Billion $2.000 Billion

(Shortfall) without innovative sources $0M Assumes ($217M) Assumes and HSR bonds $159M local match $164M local match

Note: Some figures may be revised once the Service and Capital Plans are finalized.*Member contributions that are stabilized are constant year-to-year with the exception of increases due to inflation.

CALTRAIN STRATEGIC PLAN 2004 | 2023

THE FUTURE SCENARIOS

32

The cost of the Enhancement program

varies widely between the scenarios

and depends primarily on the inclusion

of electrification and the extent of

capacity expansion along the corridor.

Due to inflation, the timing of projects

will also affect costs; however, only

constant dollars (2003) are shown in

the Strategic Plan. In the case of elec-

trification, the timing and coordination

with other improvements is also criti-

cal. Estimates show that electrifying

the railroad prior to the construction of

a grade separation can increase capital

costs (of electrification and the grade

separation) in the vicinity of the grade

separation project by 65 percent.

The Support program includes capital

program development and project

development.

Regional Extensions include the exten-

sion to Downtown San Francisco to a

rebuilt Transbay Terminal, the

Dumbarton Rail Corridor, and the exten-

sion to Monterey/Salinas. These exten-

sions are considered to be third-party

projects, and their capital costs are not

included in the Caltrain Capital

Improvement Plan. Additional operating

costs associated with the extension to

Downtown San Francisco have been

included in the Enhanced Scenario

beginning in 2010 and Build-Out

Scenario beginning in 2014. Operating

costs that would be incurred by the

Joint Powers Board for the Dumbarton

and Monterey/Salinas projects have not

been determined.

The financial, service, and capital

characteristics of the scenarios are

summarized in Tables 3 and 4 (pages

33 and 34) and are described further

on the following pages, followed by a

comparison and evaluation of all three

scenarios. All costs and revenues are

shown in 2003 dollars and shortfalls do

not include potential revenue from

innovative funding sources.

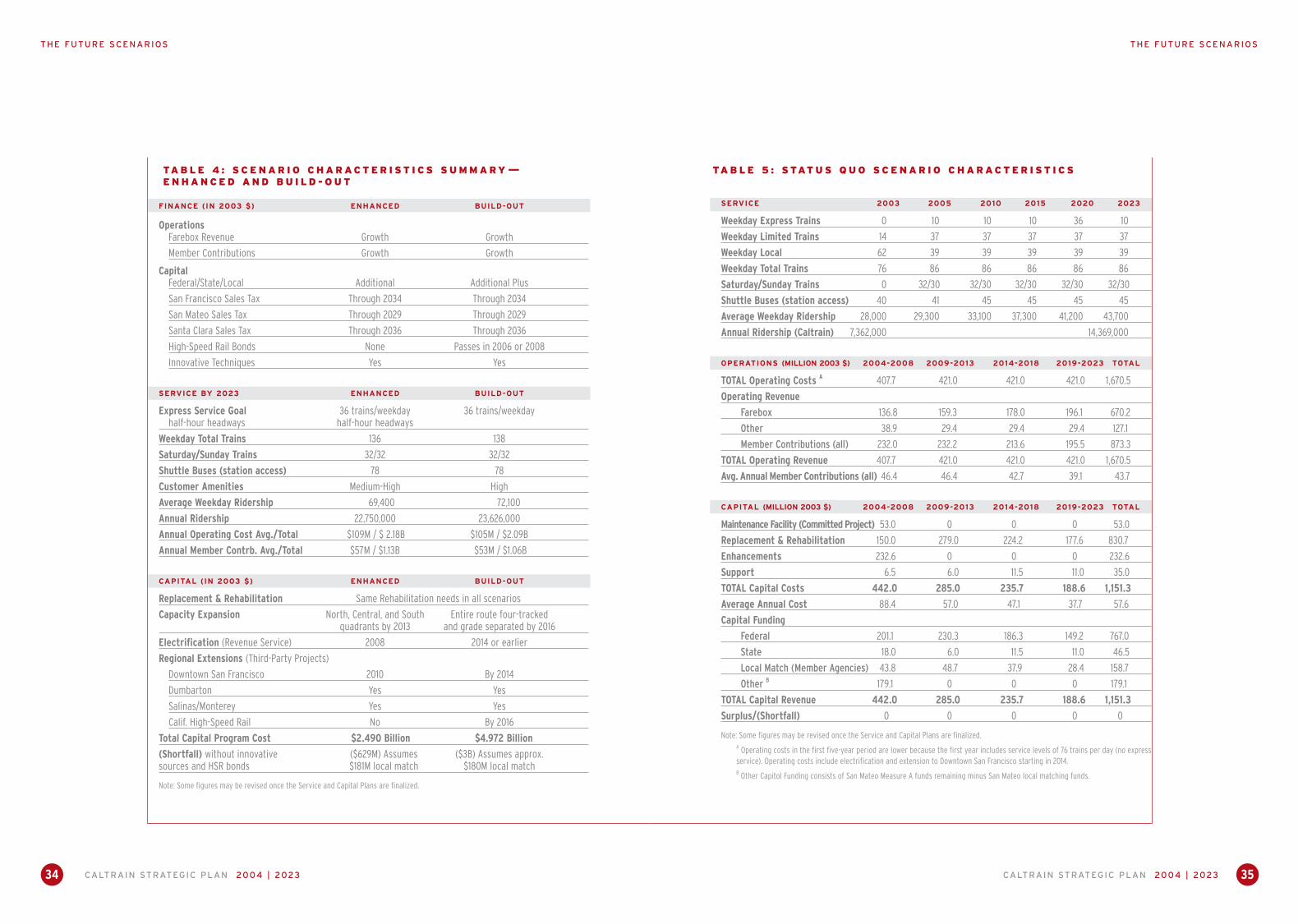

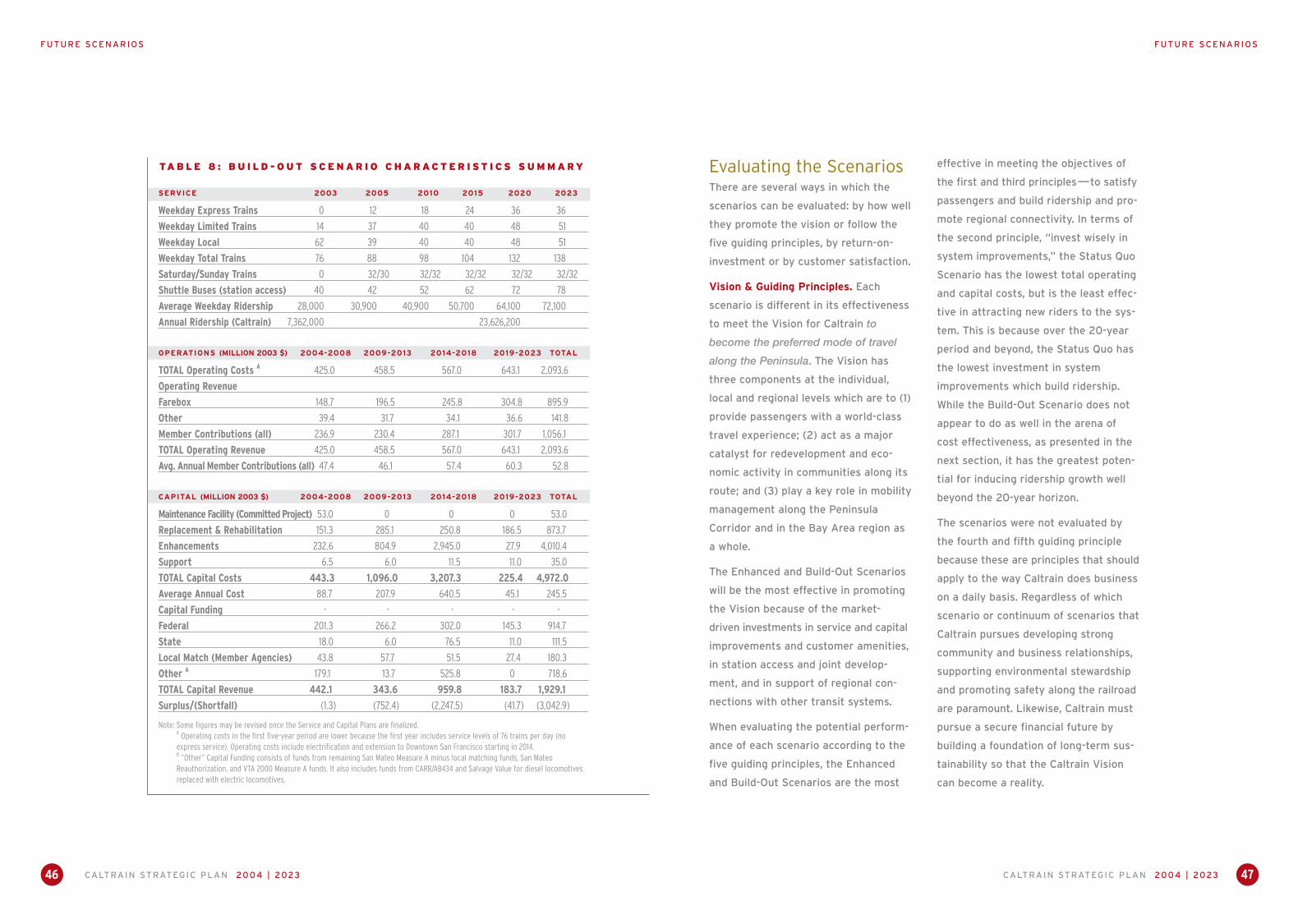

SERVICE 2003 2005 2010 2015 2020 2023

Weekday Express Trains 0 10 10 10 36 10

Weekday Limited Trains 14 37 37 37 37 37

Weekday Local 62 39 39 39 39 39

Weekday Total Trains 76 86 86 86 86 86

Saturday/Sunday Trains 0 32/30 32/30 32/30 32/30 32/30

Shuttle Buses (station access) 40 41 45 45 45 45

Average Weekday Ridership 28,000 29,300 33,100 37,300 41,200 43,700

Annual Ridership (Caltrain) 7,362,000 14,369,000

OPERATIONS (MILLION 2003 $) 2004-2008 2009-2013 2014-2018 2019-2023 TOTAL

TOTAL Operating Costs A 407.7 421.0 421.0 421.0 1,670.5

Operating Revenue

Farebox 136.8 159.3 178.0 196.1 670.2

Other 38.9 29.4 29.4 29.4 127.1

Member Contributions (all) 232.0 232.2 213.6 195.5 873.3

TOTAL Operating Revenue 407.7 421.0 421.0 421.0 1,670.5

Avg. Annual Member Contributions (all) 46.4 46.4 42.7 39.1 43.7

CAPITAL (MILLION 2003 $) 2004-2008 2009-2013 2014-2018 2019-2023 TOTAL

Maintenance Facility (Committed Project) 53.0 0 0 0 53.0

Replacement & Rehabilitation 150.0 279.0 224.2 177.6 830.7

Enhancements 232.6 0 0 0 232.6

Support 6.5 6.0 11.5 11.0 35.0

TOTAL Capital Costs 442.0 285.0 235.7 188.6 1,151.3

Average Annual Cost 88.4 57.0 47.1 37.7 57.6

Capital Funding

Federal 201.1 230.3 186.3 149.2 767.0

State 18.0 6.0 11.5 11.0 46.5

Local Match (Member Agencies) 43.8 48.7 37.9 28.4 158.7

Other B 179.1 0 0 0 179.1

TOTAL Capital Revenue 442.0 285.0 235.7 188.6 1,151.3

Surplus/(Shortfall) 0 0 0 0 0

Note: Some figures may be revised once the Service and Capital Plans are finalized. A Operating costs in the first five-year period are lower because the first year includes service levels of 76 trains per day (no expressservice). Operating costs include electrification and extension to Downtown San Francisco starting in 2014.B Other Capitol Funding consists of San Mateo Measure A funds remaining minus San Mateo local matching funds.

CALTRAIN STRATEGIC PLAN 2004 | 2023 35CALTRAIN STRATEGIC PLAN 2004 | 202334

THE FUTURE SCENARIOS

TA B L E 5 : S TAT U S Q U O S C E N A R I O C H A R A C T E R I S T I C S

THE FUTURE SCENARIOS

TA B L E 4 : S C E N A R I O C H A R A C T E R I S T I C S S U M M A R Y—E N H A N C E D A N D B U I L D - O U T

FINANCE (IN 2003 $) ENHANCED BUILD-OUT

OperationsFarebox Revenue Growth Growth

Member Contributions Growth Growth

CapitalFederal/State/Local Additional Additional Plus

San Francisco Sales Tax Through 2034 Through 2034

San Mateo Sales Tax Through 2029 Through 2029

Santa Clara Sales Tax Through 2036 Through 2036

High-Speed Rail Bonds None Passes in 2006 or 2008

Innovative Techniques Yes Yes

SERVICE BY 2023 ENHANCED BUILD-OUT

Express Service Goal 36 trains/weekday 36 trains/weekdayhalf-hour headways half-hour headways

Weekday Total Trains 136 138

Saturday/Sunday Trains 32/32 32/32

Shuttle Buses (station access) 78 78

Customer Amenities Medium-High High

Average Weekday Ridership 69,400 72,100

Annual Ridership 22,750,000 23,626,000

Annual Operating Cost Avg./Total $109M / $ 2.18B $105M / $2.09B

Annual Member Contrb. Avg./Total $57M / $1.13B $53M / $1.06B

CAPITAL (IN 2003 $) ENHANCED BUILD-OUT

Replacement & Rehabilitation Same Rehabilitation needs in all scenarios

Capacity Expansion North, Central, and South Entire route four-tracked quadrants by 2013 and grade separated by 2016

Electrification (Revenue Service) 2008 2014 or earlier

Regional Extensions (Third-Party Projects)

Downtown San Francisco 2010 By 2014

Dumbarton Yes Yes

Salinas/Monterey Yes Yes

Calif. High-Speed Rail No By 2016

Total Capital Program Cost $2.490 Billion $4.972 Billion

(Shortfall) without innovative ($629M) Assumes ($3B) Assumes approx.sources and HSR bonds $181M local match $180M local match

Note: Some figures may be revised once the Service and Capital Plans are finalized.

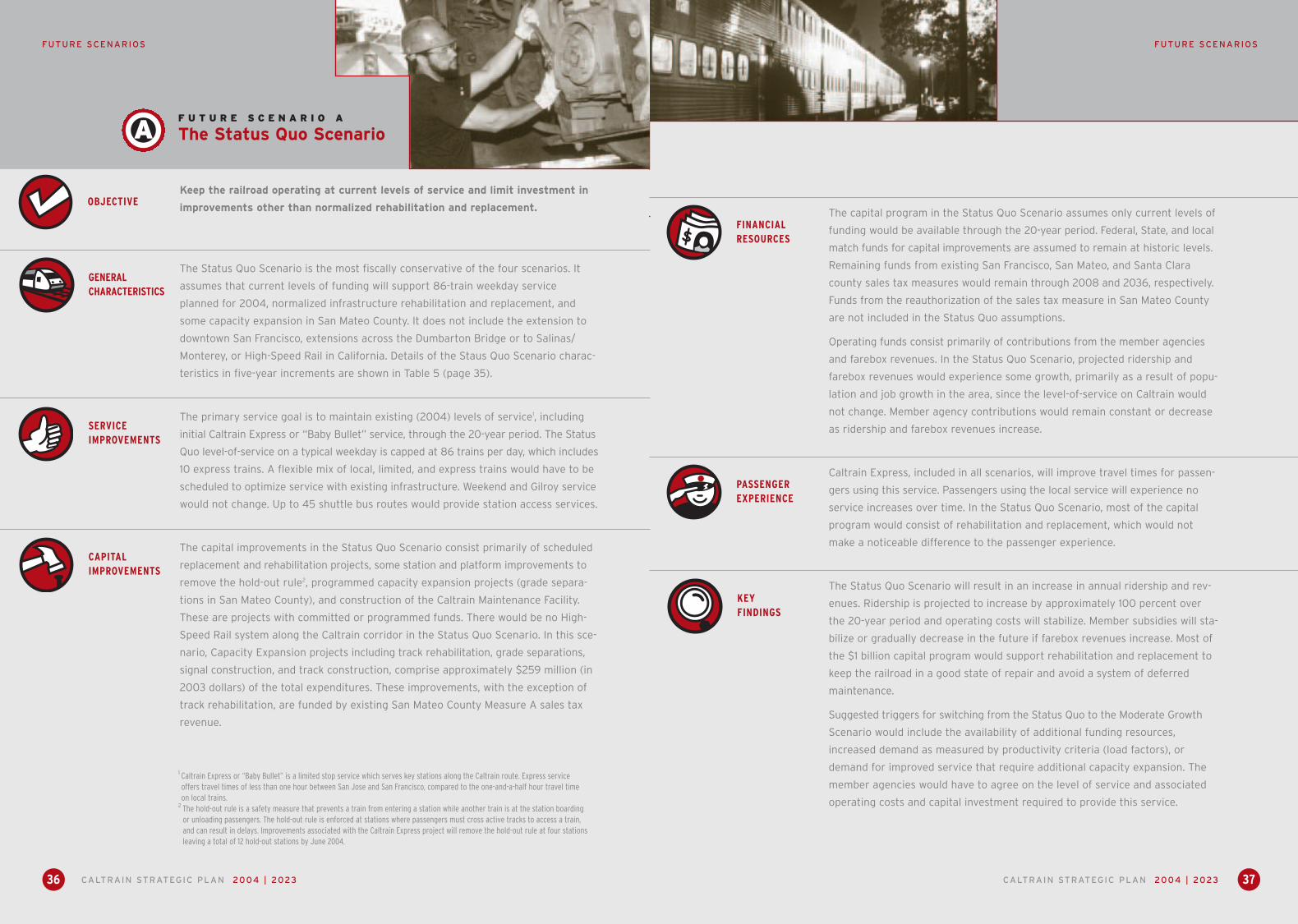

The capital program in the Status Quo Scenario assumes only current levels of

funding would be available through the 20-year period. Federal, State, and local

match funds for capital improvements are assumed to remain at historic levels.

Remaining funds from existing San Francisco, San Mateo, and Santa Clara