ca meet - jaipur december 13, 2014. 2 global economic environment key regulatory developments...

TRANSCRIPT

CA Meet - Jaipur

December 13, 2014

2

Global economic environment

Key regulatory developmentsPerformance review

3

Global economy: growth remains unevenGlobal economy: growth remains uneven

• GDP growth at 3.9% in Q3-CY2014 1 (CY2013: 2.2%)

• Update on QE• End to monthly bond purchases by the Fed• Fed will continue to reinvest proceeds• Low interest rates for “considerable period”

indicated• Growth remains muted with large economies facing challenges

• Deflation concerns persist; ECB reduced interest rates in Jun & Sep 2014

US

Eurozone

China

1. Based on seasonally adjusted annualized quarterly GDP growth

• Moderation in GDP growth to 7.3% y-o-y in Q3-CY2014 (>9.0% levels in 2011 & 2012)

4

Global monetary policyGlobal monetary policy

• Fed ends quantitative easing • However, interest rates likely to remain low

for considerable period

• Interest rates continue to remain at very low levels

• Long term refinancing operations to continue till June 2016

US

Eurozone

Japan• Persistent deflationary conditions; QE

increased from ¥60 trillion - ¥70 trillion to about ¥80 trillion each year

US

Accommodative global monetary policy likely to continue

Accommodative global monetary policy likely to continue

Key global developments to monitorKey global developments to monitor

5

Trends in global growth; developments in Euro area

Timing of rate increases by the US Federal Reserve

Growth trends in China

Geopolitical developments

6

India: long term growth potential

Key regulatory developmentsPerformance review

India: strong long term growth fundamentalsIndia: strong long term growth fundamentals

7

Favourable demographics

Healthy savings & investment rates

Rising per capita income

Rural India-high growth potential

Key drivers of growthKey drivers of growth

High potential for infrastructure development to support economic growth in the long term

Rising share of working age population

• Addition of around 12 million to the workforce every year for next five years

• Working age population to exceed 50% of total population in 2025

A young population with median age of 25 years

Dependency ratios to remain low till 2040

840

1,053

1,432 1,501

840

1,053

1,432 1,501

8

Favourable demographic profileFavourable demographic profile

Investments driven primarily by domestic savings

9

Healthy savings & investment rateHealthy savings & investment rate

FY2003 FY2013

~25%~35%

Investment rateInvestment rate

FY2008

~38%

FY2003 FY2013

~25%~30%

Savings rateSavings rate

FY2008

~37%

Per Capita GDP (USD)

Rising per capita GDP accelerating domestic

demand

Rising per capita GDP accelerating domestic

demand

8401,053

1,432 1,501~2x

2005 2013

7749

1,509

10 Source: IMF

Strong domestic demandStrong domestic demand

5.2%

8.7% 8.5%

9.4%

7.2%7.4%

8.7%9.3%

5.0% 4.8%

5.7%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

FY2005

FY2006

FY2007

FY2008

FY2009

FY2010

FY2011

FY2012

FY2013

FY2014

H1-2

015

% YoYPCE Long term average

11 Source: MOSPI

Revival in consumption growth…Revival in consumption growth…

Private consumption expenditure (PCE) growth was below long-term average of 7.2% YoY;

moderate pickup seen in H1-2015

Private consumption expenditure (PCE) growth was below long-term average of 7.2% YoY;

moderate pickup seen in H1-2015

12 Source: CEIC

• Historically, passenger vehicle (PV) sales are seen to track PCE growth, albeit with a lag

• Domestic car sales grew by 9.5% in November 2014 driven by lower fuel prices and continued relief in excise duty

• Historically, passenger vehicle (PV) sales are seen to track PCE growth, albeit with a lag

• Domestic car sales grew by 9.5% in November 2014 driven by lower fuel prices and continued relief in excise duty

...likely to drive passenger vehicle sales ...likely to drive passenger vehicle sales

13

30.7

38.851.4

23.927.5

20.0

37.3 41.728.6

0

20

40

60

80

100

FY2000 FY2005 FY2010*

Agriculture Industry ServicesShare in rural NDP

(%)

*ICICI Bank estimates

Trends for rural IndiaTrends for rural India

• Over 700 mn people spread across 600,000 villages

• Share of industry and services in rural economic growth now higher

• Over 700 mn people spread across 600,000 villages

• Share of industry and services in rural economic growth now higher

14 Source: MOSPI

Monthly per capita expenditure

INR CAGR growth (%)

Rural Urban Rural Urban

2011 - 12 1,430 2,630 16.5 15.1

2009 - 10 1,053 1,985 13.5 13.5

2004 - 05 559 1,052 2.8 4.2

1999 - 00 486 855 9.2 10.7

1993 - 94 286 464

Rural demand to be a growth leverRural demand to be a growth lever

Estimates of the consumer expenditure survey conducted by NSSO for 2011-12 show that growth in monthly per capita expenditure in rural India

has exceeded that in urban India for the first time since economic reforms began in early 1990s

Estimates of the consumer expenditure survey conducted by NSSO for 2011-12 show that growth in monthly per capita expenditure in rural India

has exceeded that in urban India for the first time since economic reforms began in early 1990s

15

India: recent developments

Key regulatory developmentsPerformance review

16

India: structural concerns being addressedIndia: structural concerns being addressed

• High level of fiscal deficit and domestic current account deficit

• Persistent high levels of inflation• Market volatility; sharp movement

in exchange rate• Reduction in fiscal deficit from 5.7% in FY2012 to 4.6% in FY2014

• Current account deficit has narrowed significantly from 4.8% in FY2013 to 2.1% in Q2-2015

• CPI inflation has moderated from an average of 9.5% in FY2014 to 5.5% in Oct 2014

• Improvement in capital flows

Recent developmen

ts

Earlier concerns

17

Continued optimism due to strong election mandate

Continued optimism due to strong election mandate

S&P raised outlook for India from ‘negative’ to ‘stable

Several agencies have revised India’s growth forecasts upwards in the range of

5.5%-6.0% for FY2015

18

Measures by the GovernmentMeasures by the Government

• Land acquisition reforms• Labour reforms• Introduction of goods and services

tax (GST)• Liberalisation of insurance sector

Other reforms being

considered

• Complete deregulation of diesel prices

• Ordinance relating to coal block de-allocation

• Approval of new domestic gas pricing policy

• Gas pricing to be reviewed every six months beginning April 1, 2015

• Launch of ‘Make in India’ campaign

Recent actions

19

India: economic outlookIndia: economic outlook

GDP growth in the range of 5.5%-6.0% for FY2015

March-2016 CPI inflation at 6.0%-6.5%

Anticipation of rate cut by RBI in early 2015

20

In summaryIn summary

Retail sector expected to benefit from improved macro economic outlook and

policy initiatives

Improvement in growth outlook for the Indian economy

21

India: Growth gathering momentum

Source: MOSPI, ICICI Bank Research

FY2015: 5.5-5.7% target; further acceleration expected over the next few years

0.0

2.0

4.0

6.0

8.0

Jun-1

1

Sep

-11

Dec

-11

Mar

-12

Jun-1

2

Sep

-12

Dec

-12

Mar

-13

Jun-1

3

Sep

-13

Dec

-13

Mar

-14

Jun-1

4

GDP growth(% YoY)

22

RBI has maintained a pause on rates

Source: RBI, ICICI Bank Research

RBI has maintained pause on policy rates since January-2014

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Aug-1

2

Nov-

12

Feb-1

3

May

-13

Aug-1

3

Nov-

13

Feb-1

4

May

-14

Aug-1

4

Repo (Policy) rate Cash Reserve Ratio(%)

23

Real estate sector

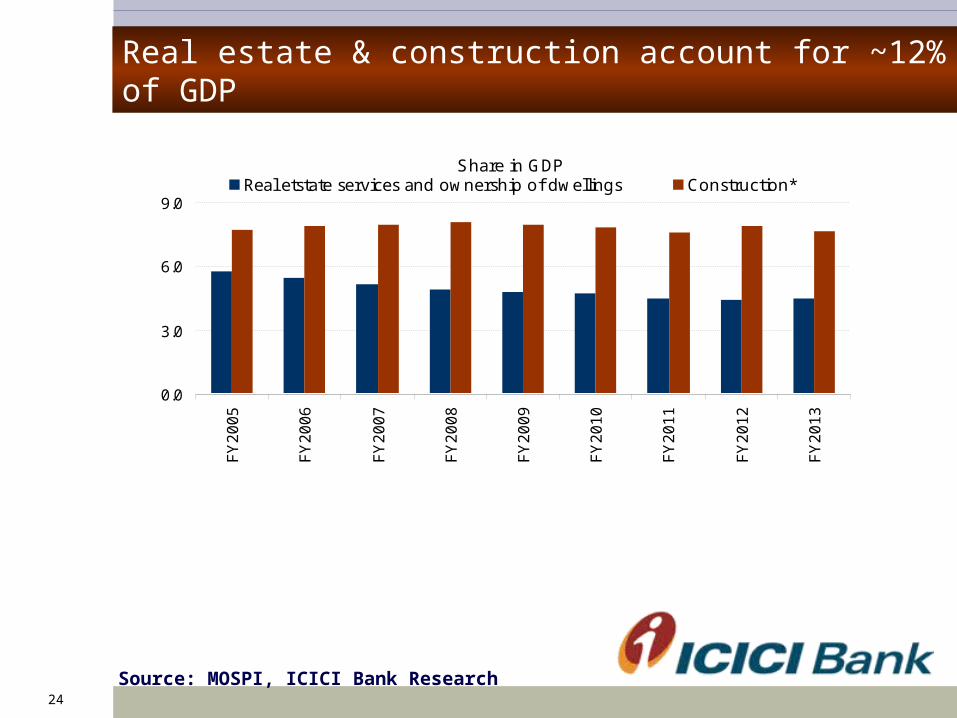

24Source: MOSPI, ICICI Bank Research

Real estate & construction account for ~12% of GDP

Share in GDP

0.0

3.0

6.0

9.0

FY20

05

FY20

06

FY20

07

FY20

08

FY20

09

FY20

10

FY20

11

FY20

12

FY20

13

Real etstate services and ownership of dwellings Construction*(%)

*includes residential and non-residential construction

25Source: NCAER, ICICI Bank Research

Residential and non-residential construction have high interlinkages with other sectors

•“output multiplier” refers to change in total output in economy in response to rise in 1 unit of exogenous demand for a sector’s output

0.0

0.6

1.2

1.8

2.4

3.0

Const

ruct

ion**

Tra

nsp

ort

***

Hote

l and

Res

taura

nts

Agricu

lture

Rea

l Est

ate

Ser

vice

s

Tra

de

Ban

king a

nd

Insu

rance

Output multiplier*

21-sector average (1.83)

** construction includes residential, non-residential and other construction *** excluding railways

Construction sector has strong inter-sectoral linkages leading to a high employment generation potential.

For instance, the employment multiplier for residential construction sector is ~3

26Source: RBI, ICICI Bank Research

Growth in house prices has come off

0

5

10

15

20

25

30

Q1

FY12

Q2

FY12

Q3

FY12

Q4

FY12

Q1

FY13

Q2

FY13

Q3

FY13

Q4

FY13

Q1

FY14

Q2

FY14

Q3

FY14

Q4

FY14

3.0

4.0

5.0

6.0

7.0

8.0

RBI House Price Index GDP growth (RHS)(% YoY) (% YoY)

The growth in house prices has slowed down to catch up with the erstwhile fall in GDP growth trajectory

27Source: HDFC, ICICI Bank Research

Overall affordability has remained static

Affordability of property by households has remained largely static over the last few years

Affordability calculated as the ratio of property value to annual income

0

10

20

30

40

50

60

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

0

2

4

6

8

10

12

Property Value Affordability Annual income* (RHS)(INR lac) (INR lac)

(*Income of an average property buyer)

28

Flow of funds into the real-estate sector

29Source: MOSPI, ICICI Bank Research

Share of physical savings in total savings has risen

20

30

40

50

60

70

80

1970-7

1

1973-7

4

1976-7

7

1979-8

0

1982-8

3

1985-8

6

1988-8

9

1991-9

2

1994-9

5

1997-9

8

2000-0

1

2003-0

4

2006-0

7

2009-1

0

2012-1

3

Financial saving Physical savingProportion of total household savings

(%)

While overall household savings have declined since FY2011, the share of physical savings (which includes real-estate) has increased

Financial savings (as % of GDP) remained static at ~7.0% even in FY2014

30Source: NCAER, ICICI Bank Research

Property a predominant investment avenue for households

According to an RBI-NCAER survey*, investment in property has taken priority over gold, deposits and equities for an average urban household

05

101520253035

Rea

l Est

ate

Gold

and a

rts

Ban

k dep

osi

t

Insu

rance

and p

ensi

on

Post

offi

ce

Mutu

al funds

Consu

mptio

n

Equiti

es

Oth

ers

Investment of urban households by asset (% of total investment)

* The study was conducted in 2011

31

Source: National Housing Bank (NHB), ICICI Bank Research

Credit-penetration in the sector remains very low

0

20

40

60

80

100

Indonesi

a

India

Thaila

nd

Chin

a

South

Kore

a

Mala

ysi

a

Sin

gapore

Hong

Kong

US

A

UK

Mortgage debt-GDP ratio(%)

India’s mortgage-debt to GDP ratio at 9% is one of the lowest in the world, suggesting scope for further penetration

Access to formal credit in India remains limited

32

^defined as townships, housing and built-up infrastructureSource: DIPP, MOSPI, ICICI Bank Research

FDI inflows into the sector have declined recently

(USD bn)

0

5

10

15

20

25

30

35

40

2010-11 2011-12 2012-13 2013-14 Q1 FY2015

012345678910

Total FDI

Share of construction development in FDI (RHS)(%)

6.2%

5.4%

5.0%

9.2%

Services (financial &non-financial)

Constructiondevelopment̂

Telecommunications

Automobile industry

Sectoral distribution of FDI equity inflows*

*FY2014

Share of construction development in FDI equity inflows has been declining

33

Policy initiatives to support the sector in this contextIn the FY2015 Union Budget, the Government announced a number of initiatives to support the sector

• INR 70.6 bn allotted for 100 smart cities • INR 80 bn allocated for rural housing schemes• Relaxations made in FDI in realty• Tax incentives given on home loans• Necessary incentives and a conducive tax regime for REITs• Banks permitted to issue bonds in order to finance long-term credit to infrastructure and affordable housing segments

34

Real Estate in Jaipur

35

Executive Summary

• Jaipur is expected to become a mega city by 2025 with a population of 10 million people covering an area of about 800 sq km.

• Jaipur residential real estate market is driven by a 60:40 mix of investors and end users respectively.

• Maximum supply and absorption in the Jaipur market falls in the price bracket of INR 3,000 – 3,500/sqft.

• Most preferred configuration in terms new launches and absorption for the residential units has been the 3-BHK segment.

Infrastructure Growthl Metro Rail Network

• One of the biggest growth stimulators for Jaipur reality market• Once operational, rates of residential property on and near the metro route

are expected to flare up

lBus Rapid Transit Service (BRTS) • Proposed to cater to city's growing traffic needs• "North-South Corridor" from Sikar Road to Tonk Road, and an "East-West

Corridor" from Ajmer Road to Delhi Road

l Ring Road• The proposed Ring Road project will be an arterial road connecting the

major areas of Jaipur together• The Expressway will have investment zones for commercial as well as

residential development on both the sides

Delhi Mumbai Industrial Corridor (DMIC)

• A band of 150 km on both sides of the DFC has been chosen to be developed DMIC

• Nearly 39% of DFC passing through Rajasthan; plenty of opportunities for industrial establishment

• About 60% of the State's area (locations like Jaipur, Alwar, Kota and Bhilwara) fall within the project influence area of DMIC.

Infrastructure Growth Contd..

l Dedicated Freight Corridor (DFC) running through Jaipur• Rail corridor connecting Jawaharlal Nehru Port near Mumbai to Dadri

near Delhi • Will allow high-speed connectivity for high axle load wagons (25 tonnes)

of double stacked container trains

l Other Infrastructural Developments to boost demand of housing • Knowledge cities: The Knowledge City North- near Chaup village.

Knowledge City South, will come up near the satellite town of Phagi • Science-Tech City: Near Achrol on the Jaipur-Delhi highway . The

location is opportune for investments in the higher education sector• Several healthcare projects : like Reliance Medicity and Bombay

Hospital will promote medical tourism and employment

39

Inventory Levels static at 12k – 14k

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Q4-2012 Q1-2013 Q2-2013 Q3-2013 Q4-2013 Q1-2014 Q2-2014 Q3-2014*

new launches new launch absorption total absorption unsold inventories

Source: PropEquity, ICICI Property Services Group.

Sales Trends QoQ

40

0

500

1000

1500

2000

2500

3000Ja

gatp

ura

Ton

kR

oad

Vai

shal

iN

agar

San

gane

r

Dur

gapu

ra

Ajm

erR

oad

Pat

raka

rC

olon

y

Kal

war

Roa

d

Sik

arR

oad

MW

CR

oad

Total Absorption (Unit) Total Availability (Unit)

*Source: PropEquity, ICICI Property Services GroupNote: Residential data for 2014 (from Jan-2014 to August-2014)

Top Micro Markets in Jaipur (based on sales)

Micro markets in JaipurlThe investors are willing to invest in the areas developing along the ‘spokes’ around the center of Jaipur. Following are the top 10 micro markets in Jaipur.

l Ajmer Road• Attracting investors from Delhi NCR and witnessing the development of

integrated townships• The occupancy rates are currently around 30%

l Patrakar Colony• Close to Mansarovar colony & Mansarovar Metro station• Situated around 8 kms from the airport • The ticket size lies in the range of 20-80 lacs

l Tonk Road• Builders are betting big on this area due to its proximity to Pratap Nagar• The second most active micro-market in terms of absorption with 312

units being absorbed in the first 7 months of 2014

l

l l

Micro markets in Jaipur

l Mahindra World City• Joint venture by Mahindra & Mahindra with RIICO, the Mahindra City,

spreads across 3,000-acres• Divided into two zones- one zone being the IT zone and the other zone

being dedicated to Export industries like Gem stones, handicrafts etc.• Located on NH-8 and well connected to the Kandla Port in Gujarat • Jaipur master plan has planned to develop the social and residential

infrastructure such as housing facilities, healthcare facilities, educational institutions, etc. for a holistic living environment

l The Jagatpura micro-market • 25 residential projects coming up in this area

• Located around 6 kms from Malviya Nagar

• The ticket size of in this area lies in the range of 30-40 Lacs

Micro markets in Jaipur Continuedl Vaishali Nagar

• Offers a healthy mix of residential, retail and commercial development• Low-rise floors as well as bigger projects by renowned local developers• Residential units in this region are priced in the range of INR 3,000 -

6,000/sq ft

lSikar Road • An industrial belt that witnesses some residential projects by local

developers. It is located along the Delhi Bypass connecting the heart of Jaipur to the Vishwakarma Industrial Area

• Close to Vidyadhar Nagar and its good connectivity through the Bus Rapid Transit Service (BRTS) system.

• This micro-market has the average ticket size (2 BHK) falling in the range of 30 – 35 Lacs.

Micro markets in Jaipur Continued

l Kalwar Road • The proposed Jaipur- Jodhpur mega highway project is expected to bring

more traction and focus to this area• The residential projects are priced in the range of INR 2500 - 3300 / sq ft

l Durgapura • Is densely populated residential area ,having one of the best proximity

and connectivity to the major commercial/retail hubs of Jaipur• Lies along the Tonk Road with the airport only a kilometer away and

Durgapur Railway Station lying within the area

l Sanganer• Jaipur is served by an International Airport, which is situated in its

satellite town of Sanganer, at a distance of 10 km from city center and offers sporadic service to major Domestic and International locations.

• The economic development is fuelled by proximity to airport

45

Key conclusions

India’s growth trajectory is on an upturn

Interest rates could be supportive if inflation eases

Real estate sector a critical driver of the growth story

Stability in Rupee to support India’s recovery

• Largest private sector bank in India • Largest private sector bank in India #1#1

• Largest branch network among private sector banks supplemented with large ATM network

• Largest branch network among private sector banks supplemented with large ATM network

N/WN/W

•Over 25 million customer accounts•Over 25 million customer accounts

•Strong capital base with CAR of 17.41% with Tier 1 ratio of 12.75% at September 30, 2014

•Strong capital base with CAR of 17.41% with Tier 1 ratio of 12.75% at September 30, 2014

ICICI Bank OverviewICICI Bank OverviewOverview

•Among Top 60 banks in the world by market cap

•Among Top 60 banks in the world by market cap

• Global presence in 18 countries• Global presence in 18 countries

• Retail deposit account for 70% of total domestic deposit

• CASA ratio at 43.7% at September 30, 2014

• 1.75 mn New customer accounts opened at September 30, 2014

• Larger Pre-qualified customer base, across all lending products.

• Retail deposit account for 70% of total domestic deposit

• CASA ratio at 43.7% at September 30, 2014

• 1.75 mn New customer accounts opened at September 30, 2014

• Larger Pre-qualified customer base, across all lending products.

A strong Retail base..

Total Customers > 25 mn

NRI customers > 1 mnHNI customers

> 0.40 mn

Salary Customers

> 11 mn

Branches 3,815

ATMs 11,739

Employees>

65,000

Serviced through…

Mobile Banking

2.5 mn

Internet Banking

5.2 mn

Retail DistributionRetail DistributionDistribution

Key initiatives during recent yearsKey initiatives during recent yearsTechnology

Tab bankingTab banking

Mobile banking: next generation

apps across domains

Mobile banking: next generation

apps across domains

24x7 touch banking:

facilitating day-to-day

transactions

24x7 touch banking:

facilitating day-to-day

transactionsComprehensive solutions: online

tendering, electronic toll

collection

Comprehensive solutions: online

tendering, electronic toll

collection

Leveraging social networking platforms

Leveraging social networking platforms

Redesigned & customized

website

Redesigned & customized

website

Supporting customer

service & cost efficiency

Supporting customer

service & cost efficiency

Leveraging mobility, digitisation and innovations in

payments technology

Leveraging mobility, digitisation and innovations in

payments technology

Tab Banking for hassle free account opening

Tab Banking for hassle free account opening

TAB BankingTAB BankingTab

Banking •25000 Tabs across India led to 25000 additional touch points

•Seamless integration with auto loans will ensur faster turnaround time and conversion.

•Field Investigation and Valuation in Auto Loans through TAB

•About 35-40% of the savings accounts opened every month are sourced using tab banking

•25000 Tabs across India led to 25000 additional touch points

•Seamless integration with auto loans will ensur faster turnaround time and conversion.

•Field Investigation and Valuation in Auto Loans through TAB

•About 35-40% of the savings accounts opened every month are sourced using tab banking

Thank you

50

Things that matter in investing…

Valuation

Sentiments

Triggers

Cycle