buy initiating coverage trent ltd target price 786

TRANSCRIPT

Initiating Coverage

28th

September 2020

Buy

Target Price

786

Trent Ltd Retail

1

Dressed up for growth We initiate coverage on Trent Ltd (Trent) with a BUY rating and a Target Price of Rs 786 based on SOTP valuation methodology. We believe Trent is well placed to bounce back post (impact of COVID-19) FY21E led by 1) Westside’s success in retail concept (only format to consistently deliver healthy SSSG and high store metrics amongst peers) driven by exclusive/trendy offerings at competitive prices 2) Significant growth opportunities in Zudio format driven by aggressive store additions beyond metros & rise in consumer preference towards value fashion owing to the pandemic led financial constraints 3) Sustainable margins led by Westside’s private label driven business model, higher focus on improving back end and fast fashion supply chain, superior store execution capability & diligent focus on cost efficiency 4) Significant improvement in return ratios (ROE to rise from 6% to 11% over FY20-23E) 5) Healthy balance sheet and additional capital raise (Rs 950 crs via its promoter group-Tata Sons) to support its ramp up in store addition plans in underpenetrated mirco markets across fashion formats (Westside/Zudio).

Our Investment Thesis Is Based On The Following Premises WESTSIDE – Strong brand with a proven business model

Over the past 5 years, Westside reported a strong ~8-9% SSSG and rising sales per sq.ft at Rs. 10k (5% CAGR) over FY14-20 driven by its unique business model vs peers in the apparel retail segment. Success of Westside’s model is driven by 1) highest (99%) share of private label/owned brands that allows complete control over entire value chain from sourcing to pricing leading to higher margins vs most of its listed peers, 2) 15%/7% CAGR over FY15-20 in walk-ins and bill size respectively owing to its ability of delivering latest fashion all year round at competitive prices, in-house brands driving effciency in execution, 3)~65% share of fast growing womens wear in the portfolio and 4) store modernization. Going forward we expect Westside to report 10% revenue CAGR over FY20-23E led by a combination of assortment freshness, latest fashion at lower prices, better customer experience, ability to sustain superior store metrics and sustained new store openings (we expect 8/20/30 new store openings over FY21/22/23E)

‘ZUDIO’ ramp up to unlock huge opportunity in value fashion market

We believe Zudio’s aggressive store addition plans beyond Metro and Tier 1 cities offers significant growth opportunities given strong underlying demand (value fashion constitutes more than 54% of the overall apparel market). Zudios’s infrastructure and backend processes are closely aligned to Westside and are thus effeciency accretive. Key drivers for significant traction observed in Zudio are its 1) small store size, 2) sharp (lower) pricing (ASP of Rs 500) and 3) fast ramp up of stores (3.5x sales growth over FY18-20). With value fashion gaining more importance in COVID period owing to reduction in consumer discretionary spends and aggressive new store additions of 20/40/50 over FY21/22/23E, we expect Zudio’s sales to grow 2.5x over FY20-23E.

Sustaining healthy growth over FY20-23E aided by private label business & operating efficiency

FY21E will be significantly affected due to COVID induced lockdown. However, as lockdown restriction ease and people movement progressively improves we believe Westside and Zudio revenues will bounce back sharply over FY20-23E driving Trent’s standalone business,expect Revenue/EBITDA/PAT CAGR of 16%/17%/27% over FY20-23E. Trent’s EBITDA Margin at 18% to see 30 bps improvement despite flat Gross Margins of 49% (rising share of value fashion) aided by Westside’s (>80% of standalone biz) superior store metrics, leveraging its supply chain model (automation, inventory discipline), diligent focus on cost efficiency because of Westside’s USP of 99% share of exclusive fashion brands/private lables business model.

Strong balance sheet and rising return ratios- A compelling proposition

Expect ROE to rise from 6% to 11% over FY20-23E driven by 27% PAT CAGR. Trent has strengthened its liquidity position (~Rs 680 crs cash & current investment as of FY20) by raising Rs 950 crs additional capital via preferential route to its promoters (Tata Sons) primarily to fund its aggressive store addition plans (Zudio and Westside) and expand/automate its back end operations going ahead. Also its strong parentage helps tide over uncertain business environment in the near term.

Trendy growth outlook – Initiate with BUY We initiate coverage on Trent Ltd with a BUY rating and TP of Rs. 786/share, 24% upside from CMP as we value the stock based on SOTP valuation methodology. We value ‘Westside biz at 23x (given a strong brand, unique and profitable business model) and ‘Zara’ at 20x (due to calibrated store openings) FY23E EV/EBITDA multiple. ‘Zudio’, its growth driver is valued at 2x, (aggressive store openings and huge underpenetrated market to tap growth) and ‘Star’ business at 1x (rising competition and loss making business) FY23E EV/Sales.

Key Financials (Standalone)

(Rs. Cr) FY20 FY21E FY22E FY23E

Net Sales 3,178 2,299 4,067 5,007

EBITDA 563 245 704 901

Net Profit 155 -62 221 321

EPS (Rs.) 4.3 -1.8 6.2 9.0

PER (x) 110.1 - 102.0 70.2

EV/EBITDA (x) 34.7 101.0 35.0 26.8

P/BV (x) 6.8 9.2 8.7 7.8

ROE (%) 6.2 -2.5 8.5 11.2

Source: Company, Axis Research

(CMP as of Sept 25, 2020)

CMP (Rs) 634

Upside /Downside (%) 24%

High/Low (Rs) 804/367

Market cap (Cr) 24,725

Avg. daily vol. (6m) Shrs. 3,63,691

No. of shares (Cr) 35.5

Shareholding (%)

Dec-19 Mar-20 Jun-20

Promoter 37.0 37.0 37.0

FIIs 20.9 21.2 20.9

MFs / UTI 12.2 11.8 11.8

Banks / FIs 0.0 0.0 0.0

Others 30.0 30.0 30.3

Financial & Valuations

Y/E Mar (Rs. Cr) FY21E FY22E FY23E

Net Sales 23.0 40.7 50.1

EBITDA 2.5 7.0 9.0

Net Profit -0.6 2.2 3.2

EPS (Rs.) -1.8 6.2 9.0

PER (x) - 102.0 70.2

EV/EBITDA (x) 101.0 35.0 27.0

P/BV (x) 9.2 8.7 7.8

ROE (%) -2.5 8.5 11.2

Key Drivers (%)

Y/E Dec FY21E FY22E FY23E

Net Sales growth -28 77 23

EBITDA growth -56.4 186.7 28.1

EBITDA margin 10.7 17.3 18.0

Relative performance

Source: Capitaline, Axis Securities

0

40

80

120

160

200

Sep-19 Mar-20 Sep-20

Trent Sensex

Tanvi Shetty Research Associate Email: [email protected]

Suvarna Joshi

Sr. Research Analyst Email: [email protected]

2

Story in charts

Exhibit 1: Westside’s consistent store additions and healthy sales per sq ft (at Rs. 10k) a key growth differentiator…

Exhibit 2: …to drive Westside sales at 10% CAGR over FY20-23E

Source: Company, Axis Securities Source: Company, Axis Securities

Exhibit 3: Ramp up of Zudio stores and high sales per sq ft (at ~Rs 12k) driven by sharp pricing and smaller store size (~7k sq ft)…

Exhibit 4: …to drive robust 2.5x revenue growth in Zudio (value fashion format) over FY20-23E

Source: Company, Axis Securities Source: Company, Axis Securities

Exhibit 5: Strong growth in Westside and Zudio to lead an overall 16% CAGR in standalone revenues over FY20-23E

Exhibit 6: Focus on operating efficiency (despite rising share of Zudio) to help stabilize EBITDA Margins at 18% over FY20-23E

Source: Company, Axis Securities Source: Company, Axis Securities, Post IND AS 116 financials FY20 onwards

0

50

100

150

200

250

0

2,000

4,000

6,000

8,000

10,000

12,000

FY18 FY19 FY20 FY21E FY22E FY23E

Westside Rev/Sq Ft. (Rs) No. of Westside stores

-40

-20

0

20

40

60

80

0

1,000

2,000

3,000

4,000

FY18 FY19 FY20 FY21E FY22E FY23E

Westside Sales (Rs Cr) Growth (%)

0

40

80

120

160

200

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY18 FY19 FY20 FY21E FY22E FY23E

Zudio Rev/Sq Ft. (Rs) No. of Zudio Stores

-40

0

40

80

120

160

0

400

800

1,200

1,600

FY18 FY19 FY20 FY21E FY22E FY23E

Zudios Revenue (Rs Cr) Growth (%)

-40

-20

0

20

40

60

80

100

0

1,000

2,000

3,000

4,000

5,000

6,000

FY18 FY19 FY20 FY21E FY22E FY23E

Total Revenue (Rs Cr) Growth (%)

0.0

4.0

8.0

12.0

16.0

20.0

0

200

400

600

800

1,000

FY18 FY19 FY20 FY21E FY22E FY23E

EBITDA (Rs Crs) EBITDA Margin (%)

3

Exhibit 7: Healthy operating profits over FY20-23E to drive 27% PAT CAGR

Exhibit 8: Sharp improvement in ROE expected over FY20-23E

Source: Company, Axis Securities Source: Company, Axis Securities, Post IND AS 116 financials FY20 onwards

Exhibit 9: Stable working capital cycle over FY20-23E owing to sourcing & supply chain control, focus on improving backend efficiency

Exhibit 10: Strong balance sheet and improving cash from operations to support aggressive store expansion plans over FY20-23E

Source: Company, Axis Securities Source: Company, Axis Securities

Exhibit 11: 12M Fwd EV/EBITDA Chart Exhibit 12: 12M Fwd EV/EBITDA Band Chart

Source: Company, Axis Securities Source: Company, Axis Securities

5.6 5.1 4.9

-2.7

5.4 6.4

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

-100

0

100

200

300

400

FY18 FY19 FY20 FY21E FY22E FY23E

PAT (Rs Crs) PAT Margin (%)

7.4 7.7 6.2

-2.5

8.5

11.2 10.3 10.8

13.3

3.0

10.9

13.5

-4.0

0.0

4.0

8.0

12.0

16.0

FY18 FY19 FY20 FY21E FY22E FY23E

ROE (%) ROCE (%)

0

20

40

60

80

FY18 FY19 FY20 FY21E FY22E FY23E

Debtor days Inventory days

Creditor days Working capital cycle

-400

-200

0

200

400

600

800

1,000

FY18 FY19 FY20 FY21E FY22E FY23E

CFO (Rs in Cr) FCFF (Rs in Cr)

0

10000

20000

30000

40000

Mar-

15

Jul-15

No

v-1

5

Mar-

16

Jul-16

No

v-1

6

Mar-

17

Jul-17

No

v-1

7

Mar-

18

Jul-18

No

v-1

8

Mar-

19

Jul-19

No

v-1

9

Mar-

20

Jul-20

EV 30x 40x 50x 60x

15

25

35

45

55

65

75

85

95

105

Mar-

15

Jul-15

Oct-

15

Jan-1

6

Ap

r-16

Jul-16

Oct-

16

Jan-1

7

Ap

r-17

Jul-17

Oct-

17

Jan-1

8

Ap

r-18

Jul-18

Oct-

18

Jan-1

9

Ap

r-19

Jul-19

Oct-

19

Jan-2

0

Ap

r-20

Jul-20

Mean Mean+1Stdev Mean-1Stdev EV/EBITA

4

Key Investment Arguments

WESTSIDE – Strong brand with a proven business model

Westside a successful apparel retail concept given healthy SSSG and highest store metrics amongst peers

Westside accounts for over 80% of the Company’s revenues and focuses on offering aspirational and exclusive own brands to consumers thus

differentiating its business vs peers. Westside has been consistent in reporting 8-9% SSSG, a key performance metric for any retail company

(FY20 saw a marginal decline owing to COVID-19 impact).

We believe, this has been possible due to 1) increasing footfalls that grew at 15% CAGR over FY15-20 aided by continued store expansion,

maintaining assortment freshness as Westside adopts a 12 season model (offer fresh merchandise, designs every month), competitive prices

and ~65% share of fast growing womens wear opening up opportunity for entire family to shop thus leading to 7% CAGR in bill size witnessed

over FY15-20.

Exhibit 13: Westside unfailingly consistent SSSG of ~8-9% over FY15-19 with COVID-19 impacting FY20 SSSG

Exhibit 14: Walk-ins and bill size grew at 15%/7% CAGR over FY15-20 led by trendy/ fresh designs and lower pricing

Source: RBI, Company, Axis Securities

The unique feature of Westside’s profitable and successful business model is the complete control over value chain that enables faster “design

to market” time thus ensuring latest fashion trends are offered at competitive prices compared to some of its peers. Further, >50% of SKUs are

priced below Rs. 1000 versus fast fashion brands like Forever 21, M&S and H&M thereby catering to a larger target audience. We believe, in

current times when consumers have become thrifty with discretionary spending alongside support for local brands, Westside is best placed

compared to some of the western brands.

Exhibit 15: Westside has own brands across categories like apparel, footwear, lingerie, cosmetics, perfume and accessories

Exhibit 16: Westside priced competitively vs most fast fashion brands

Source: Company, Axis Securities Source: Company, Axis Securities

11

8 9 9 9

7.3

0

2

4

6

8

10

12

FY15 FY16 FY17 FY18 FY19 FY20

SSSG (%)

0

10

20

30

40

50

60

0

500

1,000

1,500

2,000

2,500

FY15 FY16 FY17 FY18 FY19 FY20

Bill Size (Rs) Walk-ins (mn)

1023 1212 1093 1165

1509 1433

1943

0

500

1000

1500

2000

2500

WestsideShoppersStop

Lifestyle Forever21

H&M M&S Zara

Average Selling Price (ASP) (Rs)

5

Faster execution led by private label business model allows Westside to follow a 12 season model (offering fresh merchandise every month)

leading to lower requirement of End of Season Sales (EOSS) and faster inventory rotation, control over entire supply chain leading to operating

efficiency and steadily declining shrinkages (a measure to assess wastages in the entire value chain). Beside, consistent SSSG performance

it’s sales per sq ft have also been best in class owing to its focus on superior consumer experience, efficient utilization of retail space,

measured expansions and continuous improvements in store level metrics.

Exhibit 17: Consistently declining shrinkage ratio owing to supply chain efficiency

Exhibit 18: Rising sales per square feet over the years

Source: Company, Axis Securities Source: Company, Axis Securities

Exhibit 19: Westside is among the best performers vs most listed peers across key growth and profitability metrics

FY20 Westside Pantaloons

(ABFRL) Madhura (ABFRL)

Future Lifestyle Fashion (FLF)

Shoppers Stop

SSSG (%) 7.3 2.7 4.7 * 6 -2.5

Sales (Rs Crs) 2,703 3,514 5,434 6,188 4,835

Sales Growth (%) 16 10 8 10 9

Sales/ sq ft (Rs) 10,393 7,986 NA 8,626 9.616

Total Sq Ft Area (mn) 3 4.4 NA 7.3 4.5

EBITDA Margins (%) 11.0 6.3 5.8 8.1 4.2

No. of stores 165 342 2637 339 294

Source: Company, Axis Securities, Pre IND AS EBITDA margins, *FLF SSSG represents an estimate of Central format’s SSSG, SSSG was negative for its Brand Factory, NA (Data not available)

We expect Westide to post healthy single digit SSSG/revenue per sq ft growth going ahead as well aided by its efforts on modernising stores,

higher focus on improving its back end and fast fashion supply chain (recently raised Rs950 Crs equity via preferential issue to its parent-Tata

Group to invest in back-end technology/supply chain and to acquire retail properties).

0.24% 0.22%

0.16%

0.12%

0.18% 0.17%

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

FY15 FY16 FY17 FY18 FY19 FY20

Shinkage (%)

7500

8000

8500

9000

9500

10000

10500

11000

FY15 FY16 FY17 FY18 FY19 FY20

Westside Sales/sq ft (Rs)

6

Westside’s revenue to grow at 10% CAGR over FY20-23E driven by new store additions and healthy revenue per sq ft.

We expect revenue to grow at 10% CAGR over FY20-23E driven by a) exclusive brands, latest fashion at lower prices and better customer

experience leading to sustained sales per square ft and b) new store openings (expect 8/20/30 new stores over FY21/22/23E) beyond metros

and Tier 1 cities thereby targeting wider geographies. Further, with online sales gaining traction (reluctance of consumer to visit places with

posibility of crowding), it has recently launched Westside.com in addition to sales through Tata Cliq, it is also ramping up its efforts for an omni

channel proposition by leveraging its centralized inventory management system which would further boost its online revenue share (1.6% share

in FY20).

Exhibit 20: Westside’s consistent store additions and rising sales per sq ft (at Rs. 10k) ..

Exhibit 21: ..to drive Westside sales at 10% CAGR over FY20-23E

Source: Company, Axis Securities Source: Company, Axis Securities

Over FY20-23E, Westside margins expected to sustain

Westside’s higher EBITDA margin vs most of its listed peers is a result of a) margin accretive private lable business model b) superior operating

leverage (high sales per sq ft) driven by aspirational & afforadbale offerings c) fresher assortment (lesser need of discounts over MRPs). We

expect Westside to sustain its EBITDA Margins at 11% over FY20-23E aided by healthy store metrics (its ability to sustain sales per sq ft at

~Rs10k despite new stores additions) & higher focus on operating efficiency (focus on automating its supply chain, inventory control).

Westside’s expertise in execution was witnessed in FY20 as it managed to sustain EBITDA margin at 11% despite 180 bps GM dilution due to

sharper pricing.

Exhibit 22: Expect Westside to post consistent margins at 11% (Pre ind AS 116), despite flat GMs at 56% over FY20-23E

Source: Company, Axis Securities

0

50

100

150

200

250

0

5,000

10,000

15,000

FY18 FY19 FY20 FY21E FY22E FY23E

Westside Rev/Sq Ft. (Rs) No. of Westside stores

-40

-20

0

20

40

60

80

0

1,000

2,000

3,000

4,000

FY18 FY19 FY20 FY21E FY22E FY23E

Westside Sales (Rs Cr) Growth (%)

60 57.9 56.1 53.1

56.1 56.1

11 11 11 7

11 11

0

10

20

30

40

50

60

70

FY18 FY19 FY20 FY21E FY22E FY23E

Westside GM (%) EBITDA Margin (%)

7

Ramp up of ‘ZUDIO’ format to unlock huge opportunity in value fashion market

‘Zudio’ (value fashion format) offers 100% private label brands, curated in-house and based on ongoing fashion trends at sharp prices with

~70% of its SKUs priced at less than Rs. 500. Zudio operations (infrastructure and backend processes) are aligned with that of Westside and

thus is able to leverage the latters strong execution capabilites allowing it to operate at lower costs and offer merchandise at sharper (low) price

points (ASP at ~Rs 500). Company has rapidly expanded the Zudio concept owing to encouraging response from consumers. Its stores

expanded from just 7 standalone stores in FY18 to 80 in FY20, with its revenue contribution doubling from 7% to 16% (3.5x topline growth) over

3 years in the overall standalone business. It aims to further ramp up Zudio format beyond Metro and Tier 1 cities that offer significant growth

opportunities as it will then be able to address a larger target audience and widen its geographic reach where focus is on value fashion. We

note, value fashion (less than Rs. 1000) constitutes more than 54% of the Rs. 4.5 trillion Indian apparel market.

Going forward we believe, Trent’s aggressive store expansion in the Zudio format will be a key driver for growth as Zudio is a more

scalable format than Westside given a) lower capex requirement per store (~Rs 4cr vs 7cr in Westside) owing to smaller store size (~7,000 sq ft

vs Westside’s ~18,000 sq ft store size), b) faster ramp up/breakeven of stores driven by sharper pricing & optimal store size (high Like for Like

(LFL) sales sq ft), c) cost efficient business due to lower employee and rental expenses given its location in outskirts of cities. We expect Zudio

to continue its strong pace of store additions post FY21 (have factored in 20/40/50 new store additions in FY21/22/23E) supported by its fund

raise of Rs. 950crs form the parent group (Tata Sons). We expect it to deliver robust sales CAGR at 39% over FY20-23E (contributing >25% to

the standalone business) driven by healthy sales per sq ft (~Rs 12,000) and rapid store additions. We believe Zudio to further benefit from

sharper (lower than peers) priced offerings given the rise in consumer preference towards value fashion owing to COVID led financial

constraints on discretionary spends.

Exhibit 23: Rapid store additions and healthy sales per sq ft (at ~Rs 12k) over FY20-23E

Exhibit 24…to drive robust 2.5x revenue growth over FY20-23E

Source: Company, Axis Securities Source: Company, Axis Securities

0

50

100

150

200

0

4,000

8,000

12,000

16,000

FY18 FY19 FY20 FY21E FY22E FY23E

Zudio Rev/Sq Ft. (Rs) No. of Zudio Stores

-40

0

40

80

120

160

0

400

800

1,200

1,600

FY18 FY19 FY20 FY21E FY22E FY23E

Zudios Revenue (Rs Cr) Growth (%)

8

Strong underlying growth story for Indian apparel market

India’s total apparel market stands at around USD 66 bn (~Rs 4.5 trillion) and is expected to grow at 9% CAGR during 2020-25E led by young

demographics, rising disposable incomes, growing per capita spends, rapid urbanization in Tier 2 and Tier 3 cities and increasing aspiration for

branded products. Within the apparel market, branded apparel market (constituting ~42% share ), with a market size of ~USD 28bn is expected

to report robust growth of ~14% p.a. over 2020-25E, mainly driven by rise in e-commerce, entry of international players and influence of social

media.

Overall women’s apparel market at ~USD 20 bn is expected to grow at 10% CAGR over 2020-25E, whereas the organized apparel market for

women and kids fashion is expected to grow fast at a CAGR of 32% and 30% p.a. respectively mainly led by the growing number of urban

working women in India (growing at 7% YoY), changing social/cultural mind set, growing MT channels, increased mobile penetration and

convenience of online shopping. Also, the women’s ethnic wear segment, (~70% of the overall women’s apparel market) is expected to grow in

double digits with an increased need for comfortable work wear and weaker competition from global fashion brands in the short to medium

term.

Immense growth potential in the Value fashion market: Value fashion in India offers significant growth potential with around 66% of the

Indian apparel sector still unorganised and more than ~54% of the market constituting mass-economy segment (below Rs 1000). With

consumers forced to defer their discretionary spends due to financial uncertainty and curtailment of discretionary spends given COVID led

uncertainty, consumers preference towards value fashion would further gain traction in our view.

Competition in the branded apparel market: With recent announcement of the merger of Reliance Industries-Future Group’s retail business

(Reliance Retail & FBB/Future Lifestyle Fashion Ltd), RIL’s market share in the ~USD 28bn (Rs ~1.8 trillion) branded apparel market is

estimated to double from ~7% to ~14%, further strenghtening its position as the leader in the industry. The merger would provide operating

synergies and economies of scale opportunities leading to increased geographic presence, improving sourcing efficiencies and cost

rationalization benefits for RIL. However we believe, the consolidation in the industry would benefit organised players, with added advantage for

those players who have a strong parentage, well established customer loyalty, store execution capabilites and a robust backend infrastructure

like Trent. Trent with a 2% market share in branded apparel market has immense growth opportunities despite competition led by its

differentiated /exclusive brands across price points, healthy balance sheet, fast scale up of its value fashion ‘Zudio’ format beyond metros and

further strenthening of its liquidity position by way of a preference issue to its promoters Tata Sons.

Exhibit 25: Branded apparel market to grow at 14% CAGR over 2020-25E outpacing overall Indian apparel market

Exhibit 26: India’s low per capita spend on apparel vs other countries indicates huge potential

USD FY17 FY25

India 38 66

USA 1004 1081

China 207 389

UK 1040 1357

EU 707 906

Brazil 293 404

Russia 244 637

Source: Company, Axis Securities Source: Company, Axis Securities

0

20

40

60

80

100

120

2017 2020E 2025E

US

D b

n

Total Apparel market Branded apparel market

9

Competition to intensify in STAR business (50:50 JV between Trent & TESCO Plc.)

Although Star format (Food & Grocery retail business) delivered stable revenue CAGR at 12% over FY16-20, it is yet to become profitable. Star

(Trent Hypermarket Pvt Ltd) witnessed encouraging traction during FY20, with revenue growing by 23% at Rs 1,229 crs YoY, aided by new

store additions (added 13 stores) and strong Like for Like (LFL) growth of 10%, but its losses widened from Rs 85 crs in FY19 to Rs 166 crs on

the back of emphasis on sharp pricing, lower other income and the accounting change following adoption of the Ind AS 116 accounting

standard.

In order to make the business viable and scalable the management has been working on the following initiatives:

a) It has created a clustered presence with total 57 stores across 7 cities in the states of Maharashtra, Karnataka, Telangana and

Gujarat and aims to pursue this approach further as it allows better understanding of local needs and preferences, enables

economies of scale, and increases brand visibility.

b) It has differentiated itself from competition by offering fresher food by sourcing directly from over 800 farmers which ensures better

quality and faster availability at stores.

c) Forayed into private label offerings which comprised 9% share among participating categories (500 SKUs in home & personal care,

packaged food & beverages) in FY20 and further aims to expand this share. However the benefits of these initiaves would result over

long term.

Although, we expect its revenue to grow at CAGR of 10% over FY20-23E on back of store additions (expected to add over 20 stores under Star

Market), and brand salience, we do not expect the business to turn profitable in the near term given a) sharper pricing in the industry b) higher

costs related to new store additions c) lack of economies of scale benefits as it is operating at a small scale with <1% market share in the

organised grocery retail market in India (est USD 23 bn market) vs its large competitors, such as DMart (17% share), Reliance Retail (grocery

business) (23% share), and Big Bazaar (9%) c) heightened competition in the food and grocery retailing led by Reliance - Future deal which

would result into the merged entity becoming the largest player with more than 13,000 stores across India leading to pricing power and

significant economies of scale.

Exhibit 27: Star’s Revenue to grow at CAGR of 10% over FY20-23E Exhibit 28: Star’s EBITDA loss to reduce gradually over FY20-23E

Source: Company, Axis Securities Source: Company, Axis Securities

-15

-10

-5

0

5

10

15

20

25

30

35

0

400

800

1,200

1,600

2,000

FY18 FY19 FY20 FY21E FY22E FY23E

Star Revenue (THPL)(Rs in Crs) Growth (%)

-120

-100

-80

-60

-40

-20

0

FY18 FY19 FY20 FY21E FY22E FY23E

Star (THPL) EBITDA (Rs Cr)

10

Zara’s calibrated store openings to limit revenue growth

Zara stores in India are operated by Inditex Trent Retail India Private Ltd (ITRIPL), which is a 49%:51% Joint Venture between Trent and

Inditex group, a Spain based global fashion retailer. For this business, Inditex group takes business decisions and thus for Trent it is a financial

investment. Although Zara’s sales witnessed a higher growth trajectory of 17% CAGR over FY17-19, it slowed down to 13% CAGR over FY18-

20 owing to limited store openings (22 stores as of FY20) and rising competition from other global fashion retailers like H&M which added 49

stores vs just 6 store additions of Zara over FY15-20. With most of its fast fashion peers offering products at competitive prices, Zara (catering

to premium customer segment) had cut prices to sustain competition impacting its FY19 EBITDA margins (11-12% vs 14% levels earlier (Pre

IND AS)). Trent management indicated that the incremental store openings for Zara continues to be calibrated with focus on its presence in

very high-quality retail spaces. We expect Zara’s Revenue CAGR to moderate at 7% over FY20-23E due to limited store additions, however,

EBITDA Margins to remain stable over FY20-23E driven by consumer’s brand loyalty for Zara and its premium positioning.

Exhibit 29: Revenue to grow at 7% CAGR over FY20-23E aided by improvement in revenue/store

Exhibit 30: EBITDA to grow at 8% CAGR with stable margins at ~15% over FY20-23E aided by operating efficiency

Source: Company, Axis Securities Source: Company, Axis Securities, Post IND AS116 fin post FY20

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

0

500

1000

1500

2000

2500

FY18 FY19 FY20 FY21E FY22E FY23E

Zara Sales (Rs in Crs) Growth (%)

0

2

4

6

8

10

12

14

16

18

20

0

50

100

150

200

250

300

350

FY18 FY19 FY20 FY21E FY22E FY23E

Zara EBITDA (Rs Cr) Margin (%)

11

Financial commentary

Expect revenue growth to bounce back post FY21E

We expect Trent’s standalone revenue to grow at 16% CAGR driven by healthy sales growth in Westside (10% CAGR) and robust growth in

Zudio format (2.5x topline growth) over FY20-23E. Our expectations of 77%/23% YoY topline growth in FY22/23E is driven by pick up in store

additions across formats and healthy recovery in store metrics (revenue per sq ft) in Westside as well as Zudio post FY21E, which is aided by

exclusive offerings at lower price points, customer experience, efficient store management, warehousing and inventory management. We

believe Zudio to further benefit from the rise in consumer preference towards value fashion owing to pressure on consumer’s spending ability

impacted by COVID. However, Trent’s near-term revenue growth may see deceleration (expect 28% de-growth) given deferment in

discretionary spends owing to pandemic, nevertheless H2FY21E is likley to be relatively better than H1FY21 owing to an expectation of a

strong festive season and progressive normalization of lockdown guideline.

Exhibit 31: Trent’s standalone revenues to grow at 16% CAGR over FY20-23E

Source: Company, Axis Securities

Sustainable EBITDA margins supported by Westside’s operating efficiency

We expect Gross Margin (GM) to be flat at 49% over FY20-23E owing to aggressive store openings in Zudio business which is GM dilutive.

However expect EBITDA Margins to improve by ~30bps at 18% over FY20-23E aided by a) sustained healthy margins of Westside given its

margin accretive private lable business model & superior operating leverage b) higher focus on operating efficiency (focus on automating

supply chain). However FY21E EBITDA Margins to be impacted by negative operating leverage.

Exhibit 32: GMs to be flat with higher ‘Zudio’ contribution (limited value growth)

Exhibit 33: EBITDA to grow 17% CAGR thus aiding sustenance of, EBITDA margins over FY-20-23E

Source: Company, Axis Securities Source: Company, Axis Securities, Post IND AS 116 financials FY20 onwards

-40

-20

0

20

40

60

80

100

0

1,000

2,000

3,000

4,000

5,000

6,000

FY18 FY19 FY20 FY21E FY22E FY23E

Total Revenue (Rs in Cr) Westside Sales (Rs in Cr) Zudio Sales (Rs in Cr) Growth (%)

53.6

51.3

49.5

47.0 49.0

49.3

42.0

44.0

46.0

48.0

50.0

52.0

54.0

56.0

0

500

1,000

1,500

2,000

2,500

3,000

FY18 FY19 FY20 FY21E FY22E FY23E

Gross Profit (Rs Crs) Gross Margin (%)

0.0

4.0

8.0

12.0

16.0

20.0

0

200

400

600

800

1,000

FY18 FY19 FY20 FY21E FY22E FY23E

EBITDA (Rs Crs) EBITDA Margin (%)

12

PAT to grow at 27% CAGR over FY20-23E

Exhibit 34: Expect 27% PAT CAGR over FY20-23E driven by sustainably improving operating profit and sharp bounce back post FY21E decline

Source: Company, Axis Securities, Post IND AS 116 financials FY20 onwards

Despite, other income being higher in FY21E over the previous years owing to Rs. 950cr capital raise we expect Trent to report a Net Loss of

Rs. 60crs on standalone basis owing to COVID-19 impact.

Strong balance sheet to support expansion plans

Exhibit 35: Stable working capital cycle over FY20-23E supported by investments on improving back end operations offset by store additions

Exhibit 36: Expect ROE to improve from 6% to 11% aided by 27% PAT CAGR over FY20-23E

Source: Company, Axis Securities Source: Company, Axis Securities, Post IND AS 116 financials FY20 onwards

Trent enjoys low inventory and debtor days (~65 / 2 days) given brand ownership, sourcing and supply chain control and its focus on offering

fresh assortment every month (12 season model). Expect its working capital cycle to stabalize at 39 days over FY20-23E given its efforts on

automation/ expansion of its supply chain /warehouse capacity augmentation (one of the objects of its Rs 950 crs preference issue). Expect

ROE to improve from 6% to 11% over FY20-23E driven by 27% earnings CAGR.

Exhibit 37: Strong balance sheet and improving cash flow from operations …

Exhibit 38: to support capex/store expansion plans over FY20-23E

Source: Company, Axis Securities Source: Company, Axis Securities

Trent has maintained a healthy balance sheet with a positive CFO over last 5 years. It has further strengthened its liquidity position (~Rs 680

crs cash & current investment as of FY20) by raising Rs 950 crs additional capital via preferential route to promoters (Tata Sons) primarily to

fund Trent’s aggressive store expansion plans and expand/automate its back end operations going ahead.

5.6 5.1 4.9

-2.7

5.4 6.4

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

-100

0

100

200

300

400

FY18 FY19 FY20 FY21E FY22E FY23E

PAT (Rs Crs) PAT Margin (%)

0

20

40

60

80

FY18 FY19 FY20 FY21E FY22E FY23E

Debtor days Inventory days

Creditor days Working capital cycle

7.4 7.7 6.2

-2.5

8.5

11.2 10.3 10.8

13.3

3.0

10.9 13.5

-5.0

0.0

5.0

10.0

15.0

FY18 FY19 FY20 FY21E FY22E FY23E

ROE (%) ROCE (%)

0

200

400

600

800

1,000

FY18 FY19 FY20 FY21E FY22E FY23E

CFO (Rs in Cr)

-400

0

400

800

FY18 FY19 FY20 FY21E FY22E FY23E

FCFF (Rs in Cr) Capex (Rs in Crs)

13

Valuations and Outlook

We initiate coverage on Trent Ltd with a BUY rating as we value the stock on an SOTP basis thus arriving at a target price of

Rs. 786/share, which implies 24% upside from current market price. We believe Trent is well placed to bounce back post FY21E

given 1) Westside’s superior execution capabilites– expect healthy SSSG, better revenue per sq. feet vs peers driven by 99% share of in-

house (private labels) offerings that are margin lucrative, 2) aggressive store additions in Zudio to unlock huge underlying demand in value

fashion segment 3) Sustainable margins aided by strong margin profile of Westside and higher focus on operating efficiency 4) Significant

improvement in return ratios (expected to improve from 6% to 11% over FY20-23E) 5) Healthy balance sheet which is further strengthened by

additional capital raise (Rs 950 Crs via its promoter group-Tata Sons) to support its store addition/capex plans across Westside/Zudio formats

in underpenetrated markets beyond Metros and Tier 1 cities.

Based on our SOTP valuation, we value;

a) Westside at 23x FY23E EV/EBITDA supported by its strong brand and superior execution

b) Zara at 20x FY23E EV/EBITDA due to calibrated store openings & limited margin expansion to due pricing cuts.

c) Zudio at 2x FY23E EV/Sales being a key growth driver owing to its aggressive store openings and strong growth prospects in Value

Fashion market .

d) Star business at 1x FY23E EV/Sales as we expect it to countinue reporting loss at EBITDA level (declining YoY going forward)

Exhibit 39: SOTP Valuation

Segment Valuation Multiple

(x) Enterprise Value

(Rs Cr)

Westside EV/EBITDAR multiple (x) 23 23,400

Zudio EV / Sales Multiple (x) 2 2,730

Zara EV / EBITDA Multiple (x) 20 2,912

Star (THPL/FHL) EV/ Sales Multiple (x) 1 959

Total EV

30,001

Net Debt

2,048

Equity Value

27,954

Shares (Cr)

35.5

Target Price (INR)

786

CMP

634

% Upside

24.0%

Source: Company, Axis Securities

Risks:

Rapid rise in COVID-19 cases across the country post FY21 as well could could impact our estimates and is a key risk to our call.

Heightened competitive intensity in apparel retail post merger of RIL-Future retail business could impact Trent’s pricing power.

Slower than expected expansion of Westside and Zudio stores could impact topline growth.

Delay in breakeven for ‘Zudio’ format over medium term could impact its operating profits.

Increasing losses in the ‘Star’ business would impact consolidated PAT and earnings.

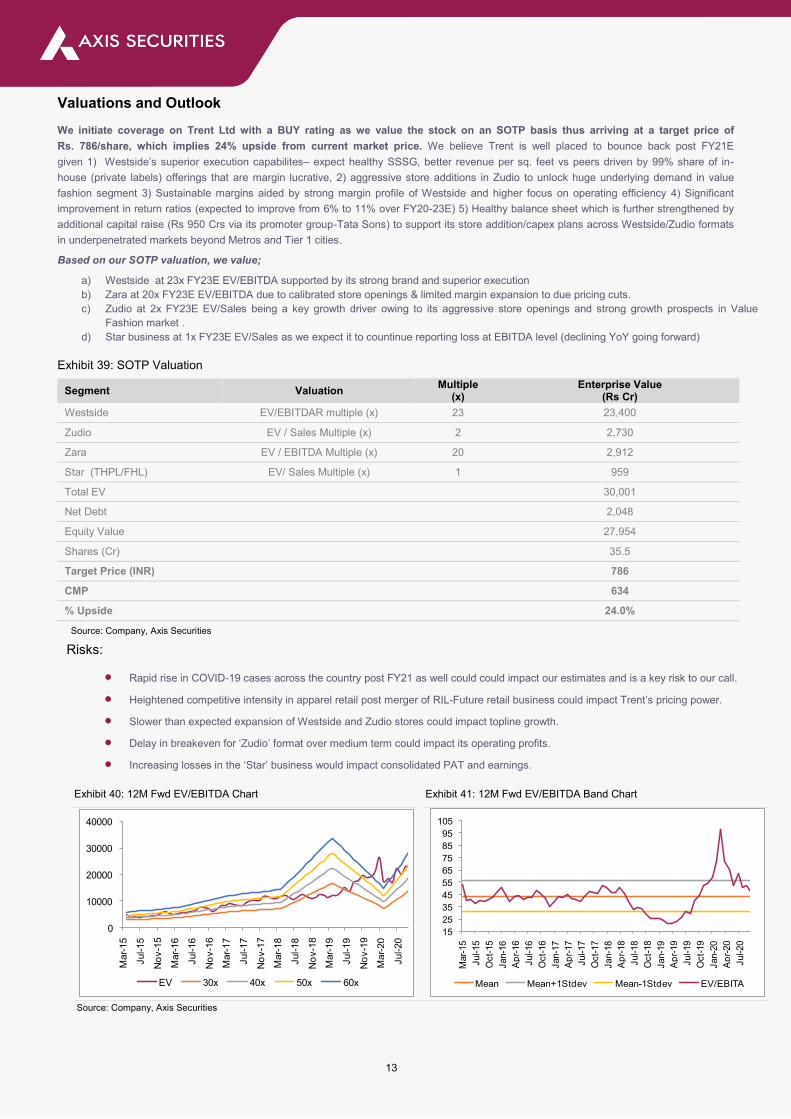

Exhibit 40: 12M Fwd EV/EBITDA Chart Exhibit 41: 12M Fwd EV/EBITDA Band Chart

Source: Company, Axis Securities

0

10000

20000

30000

40000

Mar-

15

Jul-15

No

v-1

5

Mar-

16

Jul-16

No

v-1

6

Mar-

17

Jul-17

No

v-1

7

Mar-

18

Jul-18

No

v-1

8

Mar-

19

Jul-19

No

v-1

9

Mar-

20

Jul-20

EV 30x 40x 50x 60x

15

25

35

45

55

65

75

85

95

105

Mar-

15

Jul-15

Oct-

15

Jan-1

6

Ap

r-16

Jul-16

Oct-

16

Jan-1

7

Ap

r-17

Jul-17

Oct-

17

Jan-1

8

Ap

r-18

Jul-18

Oct-

18

Jan-1

9

Ap

r-19

Jul-19

Oct-

19

Jan-2

0

Ap

r-20

Jul-20

Mean Mean+1Stdev Mean-1Stdev EV/EBITA

14

About company

Trent Ltd, incorporated in 1998, is the retail arm of the Tata group, with flagship retail chain ‘Westside’. The Westside fashion stores provide

women’s wear, men’s wear, kids’ wear, footwear, lingerie, cosmetics, perfumes, handbags and accessories. There are more than 160 Westside

stores across 87 cities. Zudio, operates in the value fashion format, has 80 stores, its offerings include apparel across men, women and kids,

footwear and home. Landmark is a family entertainment format store which focusses on toys, stationery, books, technology and sports. Trent has

also launched 2 stores under its new format ‘Utsa’ which is its women’s ethnic wear brand. Trent’s Food & Grocery offering under ‘Star’ brand

operates 49 stores in a 50:50 JV with TESCO Plc. under Trent Hypermarket Pvt Ltd (THPL) in addition to 8 stores being operated under Fiora

Hypermarket Ltd. (FHL), a subsidiary of the Company. During FY20, Trent acquired 51% share capital of Booker India Limited (BIL) operating in the

cash and carry business under the Booker Wholesale banner, which has 6 stores serving ~22,000 trade customers with products in categories

across staples, processed foods, confectionery, personal care, home care, dairy, chilled & frozen foods, bakery, fresh fruits etc. Post this acquisition,

Fiora Hypermarket Ltd. (FHL) has become a wholely owned subsidiary of BIL. Also,Trent has 2 joint ventures with Inditex group of Spain with a

shareholding of 49% under the name Inditex Trent Retail India Pvt Ltd to operate Zara (22 stores) and Massimo Dutti (3 stores) stores in India.

Exhibit 42: Company Chart

Source: Company, Axis Securities

Trent

Consolidated

Booker India Ltd

(51% owned subsidiary) (Operates FioraHypermarket-

Star stores in Gujarat)

Standalone

Westside Zudio

Landmark Utsa

Joint Ventures

Trent Hypermarket Pvt Ltd

(50-50 JV with Tesco Plc to operate Star Stores in India)

Inditex Trent Retail India Pvt Ltd

(49-50 JV with with Inditex group to operate Zara and Massimo Dutti stores)

15

Key Management Personnel

Name Experience

Noel Tata

Chairman

Mr. Noel Tata was appointed as Trent’s chairman in 2014, prior to that, he also served Trent for 4 years as

its Vice Chairman (Non Executive). He has an extensive experience in various fields including marketing,

administration and investments. He also serves as the Group CEO at Tata International Limited .He holds a

Bachelor of Arts degree in Economics from the University of Sussex, U.K. and I.E.P. from INSEAD, France.

Stephen Rayfield

Chief Executive Officer (CEO)

Mr. Stephen Rayfield has been appointed as the new CEO of Trent Ltd. Prior to this, Mr. Stephen worked in

AIFuttaim for ~5 years as Vice President of its Retail division, wherein he was responsible for Marks and

Spencer’s operations across MENA and Asia. He has a rich experience of 21 years in the Fashion Retail

industry.

Philip N. Auld

Executive Director

Mr. Philip Auld who retired from the position of Trent’s Managing Director (MD) has now been appointed as

its Executive Director, from 1st May’20 untill 2nd Sep’21. He was MD & CEO of Trent for 9 years and has

been a key architect behind it's success. Before joining Trent, he worked at Maxeda BV. (Netherlands) for 5

years. With Marks and Spencer Mr. Auld worked for 17 years and also started his career here.

P. Venkatesalu

Executive Director (Finance)

and Chief Financial Officer

Mr. P. Venkatesalu serves as the Chief Financial Officer and Executive Director of Trent Ltd. since June 1,

2015. He also serves on the board of several subsidiaries of Trent including Trent Hypermarket Private Ltd.

Prior to joining Trent he was associated with Tata Sons Ltd looking after group finance for a period of ~5

years.

Venu Nair

CEO-Westside

Mr. Venu Nair is currently CEO of Westside. Previously he was Chief Commercial Officer of the company

from Apr’17 to Dec’19. He has more than 11 years of experience working at Marks and Spencer.

16

Financials (Standalone)

Profit & Loss (Rs Cr)

Y/E March FY20 FY21E FY22E FY23E

Net sales 3,178 2,299 4,067 5,007

Growth, % 26 (28) 77 23

Raw material expenses 1,604 1,218 2,074 2,538

Gross Profits 1,574 1,081 1,993 2,468

Gross Margins % 50 47 49 49

Employee expenses 313 306 403 496

Rent 203 162 260 320

Ads & promotions - - - -

Other Expenses 495 367 626 751

EBITDA 563 245 704 901

Growth, % 138 (56) 187 28

Margin, % 17.7 10.7 17.3 18.0

Depreciation 231 239 253 274

Other Income 152 147 102 90

EBIT 484 153 553 717

Growth, % 114 (68) 261 30

Margin, % 15 7 14 14

Interest paid 238 232 257 288

Pre-tax profit 246 (79) 295 429

Tax provided (91) 17 (74) (108)

Profit after tax (Adjusted) 155 (62) 221 321

Growth, % 21 (140) (454) 45

Source: Company, Axis Securities

Balance Sheet (Rs Cr)

Y/E March FY20 FY21E FY22E FY23E

Equity 2,499 2,437 2,604 2,872

Debt 2,573 2,573 2,573 2,573

Other Non-Current Liabilities 23 23 23 23

Total Liabilities 5,095 5,032 5,200 5,468

Net Fixed Assets 2,577 2,412 2,345 2,339

Net Intangible Assets 65 65 65 65

Other Non-Curr Assets 1,329 1,329 1,329 1,329

Inventories 587 441 747 919

Trade Receivables 13 19 22 27

Other Current Assets 759 659 559 459

Trade Payables 256 176 323 412

Other Current Liabilities 43 43 43 43

Net Current Assets 1,059 899 961 951

Cash & Equivalents 44 306 478 763

Net Tax Assets 21 21 21 21

Total Assets 5,095 5,032 5,200 5,468

Source: Company, Axis Securities

17

Cash Flow (Rs Cr)

Y/E March FY20 FY21E FY22E FY23E

Pre-tax profit 246 153 553 717

Depreciation 231 239 253 274

Others 84 - - -

Opt Profits before working capital 560 392 805 991

Chg in working capital (111) 160 (62) 11

Total tax paid (81) 17 (74) (108)

Cash flow from operating activities 369 569 669 894

Capex (146) (74) (186) (268)

Proceeds from sale of FA 42 - - -

Current & Non-Current Investments (2,802) - - -

Interest income 31 - - -

Income from Investments 2,280 - - -

Investment in Subsidiaries, JV, Associates (108) - - -

Repayment of Advances (54) - - -

Cash flow from investing activities (757) (74) (186) (268)

Free cash flow 222 495 483 626

Equity raised/(repaid) 850 - - -

Debt raised/(repaid) (173) - - -

Interest Paid (244) (232) (257) (288)

Dividend Paid (52) - (53) (53)

Cash flow from financing activities 382 (232) (311) (341)

Net chg in cash (7) 262 172 285

Opening cash balance 51 44 306 478

Closing cash balance 44 306 478 763

Source: Company, Axis Securities

18

Ratio Analysis (%)

Y/E March FY20 FY21E FY22E FY23E

Per Share data

EPS (INR) 4.3 (1.8) 6.2 9.0

Growth, % 13.0 (140.4) (453.7) 45.4

Book NAV/share (INR) 70 69 73 81

DPS (INR) 1.5 - 1.5 1.5

Return ratios

Avg Return on assets (%) 4.2 (1.2) 4.3 6.0

Avg Return on equity (%) 6.2 (2.5) 8.5 11.2

Avg Return on capital employed (%) 13.3 3.0 10.9 13.5

Working Capital Days

Inventory Days 67 70 67 67

Receivable Days 2 3 2 2

Payable Days 29 28 29 30

Working capital days 39 45 40 39

Valuation

PER (x) 110.1 - 102.0 70.2

Price/Book (x) 6.8 9.2 8.7 7.8

Div Yield (%) 0.3 - 0.2 0.2

EV/Net sales (x) 6.2 10.8 6.1 4.9

EV/EBITDA (x) 34.7 101.1 35.0 27.0

EV/EBIT (x) 40.4 162.0 44.6 33.9

Source: Company, Axis Securities

19

About the analyst

Analyst: Tanvi Shetty

Contact Details: [email protected]

Sector: Consumer Sector

Analyst Bio: Tanvi Shetty is MBA (Finance) from Chetana’s Institute of Management & Research with over 3

years of equity research experience.

About the analyst

Analyst: Suvarna Joshi

Contact Details: [email protected]

Sector: FMCG, Consumption sector, Sp. Chemicals, Mid-Caps

Analyst Bio: Suvarna Joshi is MBA (Finance) from Mumbai University with about 10 years of experience in

Equity market and research.

Disclosures:

The following Disclosures are being made in compliance with the SEBI Research Analyst Regulations 2014 (herein after referred to as the Regulations).

1. Axis Securities Ltd. (ASL) is a SEBI Registered Research Analyst having registration no. INH000000297. ASL, the Research Entity (RE) as defined in the

Regulations, is engaged in the business of providing Stock broking services, Depository participant services & distribution of various financial products. ASL is a

subsidiary company of Axis Bank Ltd. Axis Bank Ltd. is a listed public company and one of India’s largest private sector bank and has its various subsidiaries

engaged in businesses of Asset management, NBFC, Merchant Banking, Trusteeship, Venture Capital, Stock Broking, the details in respect of which are available

on www.axisbank.com.

2. ASL is registered with the Securities & Exchange Board of India (SEBI) for its stock broking & Depository participant business activities and with the Association of

Mutual Funds of India (AMFI) for distribution of financial products and also registered with IRDA as a corporate agent for insurance business activity.

3. ASL has no material adverse disciplinary history as on the date of publication of this report.

4. I/We, Tanvi Shetty, PGDM (Finance) and Suvarna Joshi, PGDBM (Finance), author/s and the name/s subscribed to this report, hereby certify that all of the views

expressed in this research report accurately reflect my/our views about the subject issuer(s) or securities. I/We (Research Analyst) also certify that no part of

my/our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. I/we or my/our relative or ASL does

not have any financial interest in the subject company. Also I/we or my/our relative or ASL or its Associates may have beneficial ownership of 1% or more in the

subject company at the end of the month immediately preceding the date of publication of the Research Report. Since associates of ASL are engaged in various

financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies

mentioned in this report. I/we or my/our relative or ASL or its associate does not have any material conflict of interest. I/we have not served as director / officer,

etc. in the subject company in the last 12-month period.Any holding in stock – No

5. 5. ASL has not received any compensation from the subject company in the past twelve months. ASL has not been engaged in market making activity for the

subject company.

6. In the last 12-month period ending on the last day of the month immediately preceding the date of publication of this research report, ASL or any of its associates

may have:

Received compensation for investment banking, merchant banking or stock broking services or for any other services from the subject company of this research report

and / or;

Managed or co-managed public offering of the securities from the subject company of this research report and / or;

Received compensation for products or services other than investment banking, merchant banking or stock broking services from the subject company of this research

report;

ASL or any of its associates have not received compensation or other benefits from the subject company of this research report or any other third-party in connection

with this report.

Term& Conditions:

This report has been prepared by ASL and is meant for sole use by the recipient and not for circulation. The report and information contained herein is strictly

confidential and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form,

without prior written consent of ASL. The report is based on the facts, figures and information that are considered true, correct, reliable and accurate. The intent of this

report is not recommendatory in nature. The information is obtained from publicly available media or other sources believed to be reliable. Such information has not

been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such

information and opinions are subject to change without notice. The report is prepared solely for informational purpose and does not constitute an offer document or

solicitation of offer to buy or sell or subscribe for securities or other financial instruments for the clients. Though disseminated to all the customers simultaneously, not all

customers may receive this report at the same time. ASL will not treat recipients as customers by virtue of their receiving this report.

20

Disclaimer:

Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to the

recipient’s specific circumstances. The securities and strategies discussed and opinions expressed, if any, in this report may not be suitable for all investors, who must

make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient.

This report may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this report should make such investigations as

it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this report (including the merits and risks

involved), and should consult its own advisors to determine the merits and risks of such an investment. Certain transactions, including those involving futures, options

and other derivatives as well as non-investment grade securities involve substantial risk and are not suitable for all investors. ASL, its directors, analysts or employees

do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report,

including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income,

etc. Past performance is not necessarily a guide to future performance. Investors are advice necessarily a guide to future performance. Investors are advised to see

Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in

projections. Forward-looking statements are not predictions and may be subject to change without notice.

ASL and its affiliated companies, their directors and employees may; (a) from time to time, have long or short position(s) in, and buy or sell the securities of the

company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities or earn brokerage or other compensation or act as a market maker

in the financial instruments of the company(ies) discussed herein or act as an advisor or investment banker, lender/borrower to such company(ies) or may have any

other potential conflict of interests with respect to any recommendation and other related information and opinions. Each of these entities functions as a separate,

distinct and independent of each other. The recipient should take this into account before interpreting this document.

ASL and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, the recipients of this

report should be aware that ASL may have a potential conflict of interest that may affect the objectivity of this report. Compensation of Research Analysts is not based

on any specific merchant banking, investment banking or brokerage service transactions. ASL may have issued other reports that are inconsistent with and reach

different conclusion from the information presented in this report. The Research reports are also available & published on AxisDirect website.

Neither this report nor any copy of it may be taken or transmitted into the United State (to U.S. Persons), Canada, or Japan or distributed, directly or indirectly, in the

United States or Canada or distributed or redistributed in Japan or to any resident thereof. If this report is inadvertently sent or has reached any individual in such

country, especially, USA, the same may be ignored and brought to the attention of the sender. This report is not directed or intended for distribution to, or use by, any

person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would

be contrary to law, regulation or which would subject ASL to any registration or licensing requirement within such jurisdiction. The securities described herein may or

may not be eligible for sale in all jurisdictions or to certain category of investors.

The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the

views expressed in the report. The Company reserves the right to make modifications and alternations to this document as may be required from time to time without

any prior notice. The views expressed are those of the analyst(s) and the Company may or may not subscribe to all the views expressed therein.

Copyright in this document vests with Axis Securities Limited.

Axis Securities Limited, Corporate office: Unit No. 2, Phoenix Market City, 15, LBS Road, Near Kamani Junction, Kurla (west), Mumbai-400070, Tel No. – 022-40508080/ 022-61480808, Regd. off.- Axis House, 8th Floor, Wadia International Centre, PandurangBudhkar Marg, Worli, Mumbai – 400 025. Compliance Officer: AnandShaha, Email: [email protected], Tel No: 022-42671582.SEBI-Portfolio Manager Reg. No. INP000000654

DEFINITION OF RATINGS

Ratings Expected absolute returns over 12-18 months

BUY More than 10%

HOLD Between 10% and -10%

SELL Less than -10%

NOT RATED We have forward looking estimates for the stock but we refrain from assigning valuation and recommendation

UNDER REVIEW We will revisit our recommendation, valuation and estimates on the stock following recent events

NO STANCE We do not have any forward looking estimates, valuation or recommendation for the stock