business school for cle: how would a corporate strategist ...c.ymcdn.com/sites/ · how would a...

TRANSCRIPT

Business School for CLE: How Would a Corporate Strategist Look at

the CLE Industry?

Presented By:

Peter Berge Minnesota CLE

St Paul, Minnesota

Presented at: ACLEA 52nd Mid-Year Meeting January 30 - February 2, 2016

Savannah, Georgia

Peter Berge MinnesotaCLE

StPaul,Minnesota

Peter H. Berge is the Director of Web Education for Minnesota CLE where he has been a recognized

leader in the field of distance learning for over a decade. At Minnesota CLE, he has been a pioneer in

online education for lawyers, serving as the primary developer for all of Minnesota CLE’s online

programming in legal technology and substantive areas of law. Prior to his work with Minnesota CLE,

Peter has been an attorney in private practice and specialized in the practice areas of personal injury

and appeals, and served as Director of Risk Management at Minnesota Lawyers Mutual Ins. Co. He has

taught on the faculties of William Mitchell College of Law, Temple University School of Law, and

Georgetown Law Center. He is a 1983 graduate of William Mitchell College of Law and a member of the

William Mitchell Alumni Board. He is admitted to practice in Minnesota and the Eighth Circuit. When

not attending to online CLE, Peter amuses himself with music and photography. He plays guitar in the

R&B band The Midnight Mo Experience (www.midnightmo.com) and a new acoustic project, Old Soul

(https://www.facebook.com/oldsoulmn). You can see some of his photography at

www.peterberge.com and www.facesofmn.com.

Business School for CLE: How Would a Corporate Strategist Look at the CLE Industry?

Peter H. Berge

Web Education Director

Minnesota CLE

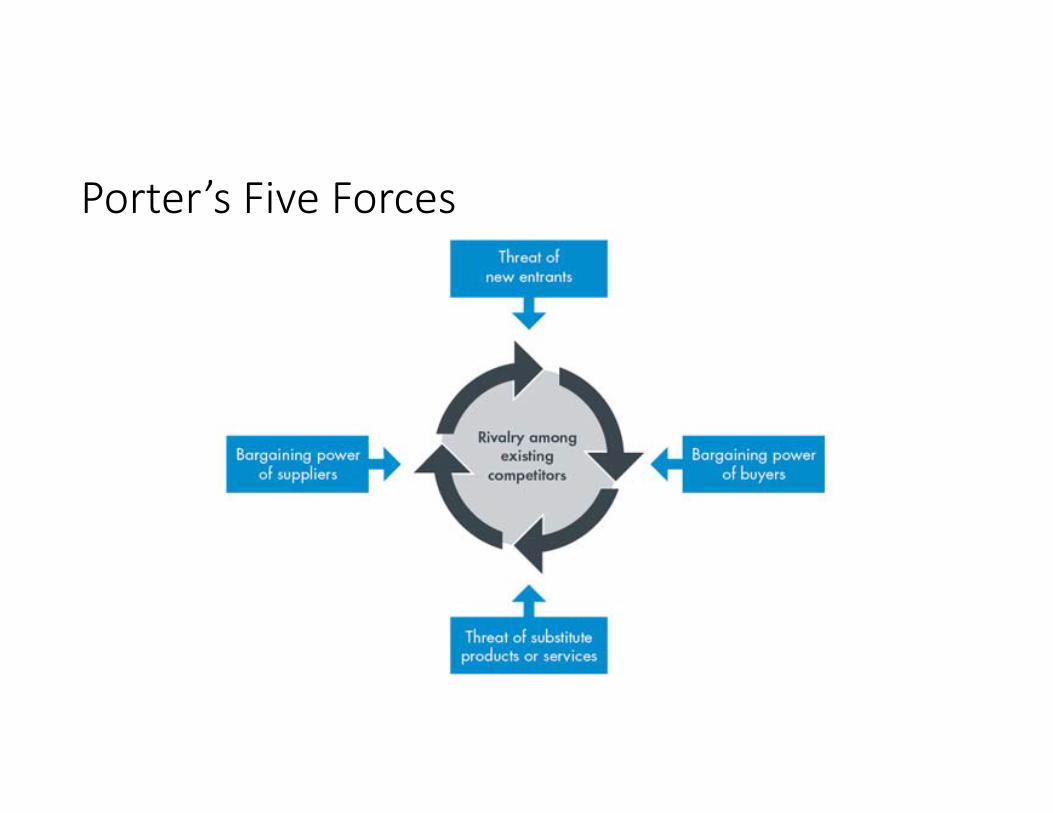

Porter’s Five Forces

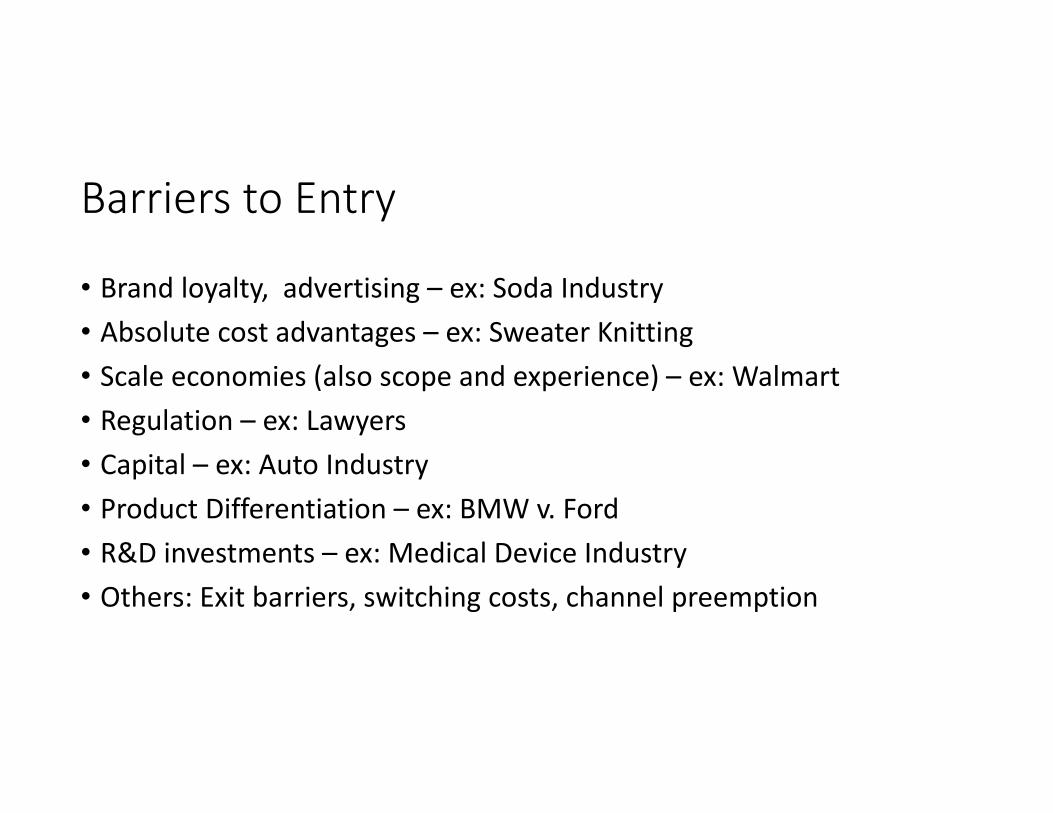

Barriers to Entry

• Brand loyalty, advertising – ex: Soda Industry• Absolute cost advantages – ex: Sweater Knitting• Scale economies (also scope and experience) – ex: Walmart

• Regulation – ex: Lawyers• Capital – ex: Auto Industry• Product Differentiation – ex: BMW v. Ford

• R&D investments – ex: Medical Device Industry

• Others: Exit barriers, switching costs, channel preemption

Competitive Rivalry

• Fragmented or consolidated industry

• Growth rate• Extent of differentiation• Lumpiness of additions to capacity

• Fixed costs

Bargaining Power of Buyers

• Relative concentration• Few vs many customers facing few vs many sellers

• Purchase volume as % of focal industry output• Large vs small purchase decisions

• Availability of substitute products • Buyer industry substitutes

• Switching costs• Threat of switching suppliers

• Threat of forward/backward integration• Ability of focal industry or buyer industry to become a competitor

Bargaining Power of Suppliers

• Relative concentration• Few vs many sellers facing few vs many buyers

• Purchase volume as % of supplier industry output• Large vs small purchase decisions

• Availability of substitute products • Supplier industry substitutes

• Switching costs• Threat of switching suppliers

• Threat of backward integration• Ability of focal industry to become a competitor

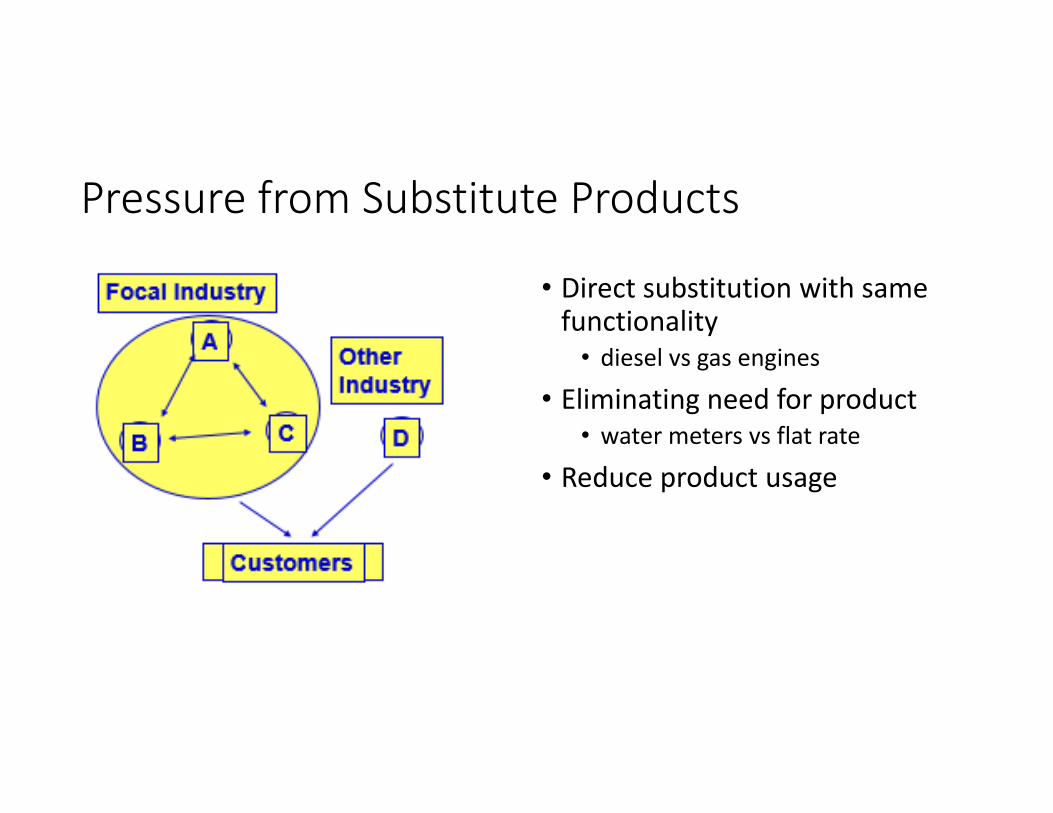

Pressure from Substitute Products

• Direct substitution with same functionality• diesel vs gas engines

• Eliminating need for product• water meters vs flat rate

• Reduce product usage

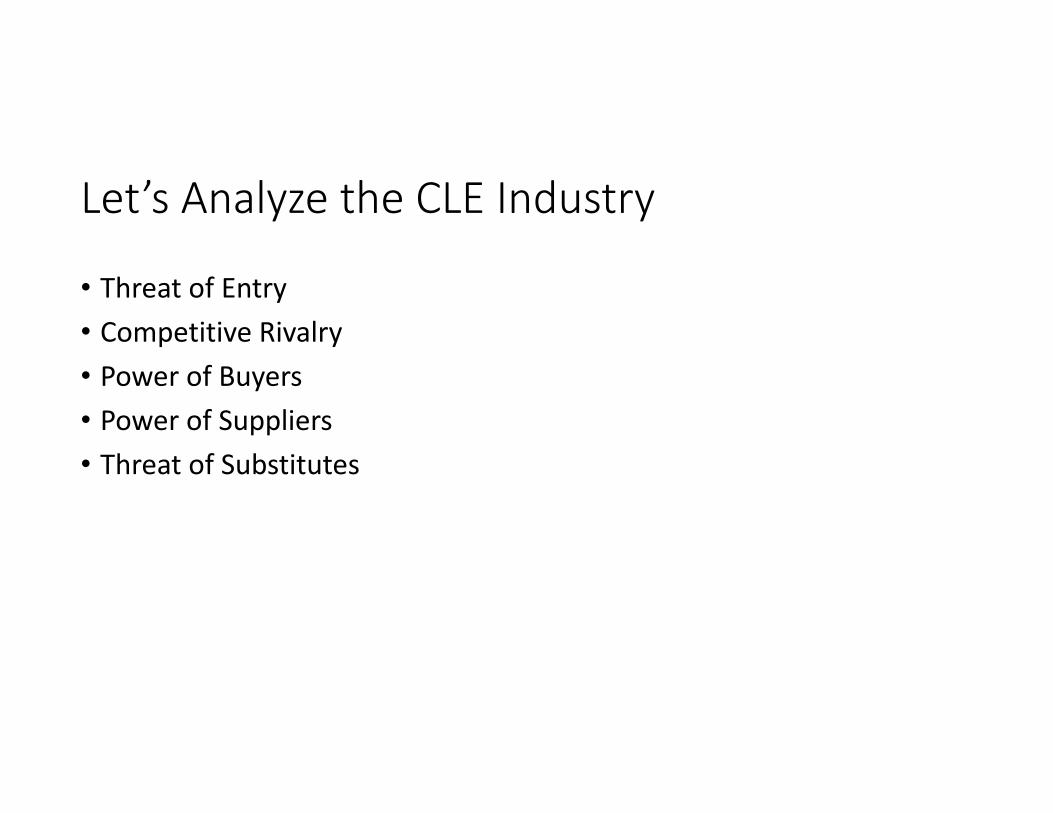

Let’s Analyze the CLE Industry

• Threat of Entry• Competitive Rivalry

• Power of Buyers• Power of Suppliers• Threat of Substitutes

Integrating Industry and Firm

CompetitiveAnalysis

Capability Assessment

• Analyze industry structure• Create product/market

positioning

• Analyze firm resources• Develop unique firm-specific positions

Create sustainablecompetitive advantage

IndustryOpportunities

STRATEGY

Firm Resources& Capabilities

Business School for CLE: How Would a Corporate Strategist Look at the CLE

Industry?

ACLEA 52nd Mid‐Year Meeting – Savannah, GA

Peter H. Berge

Web Education Director

Minnesota CLE

Business School for CLE: Porter’s Five Forces Page | 2

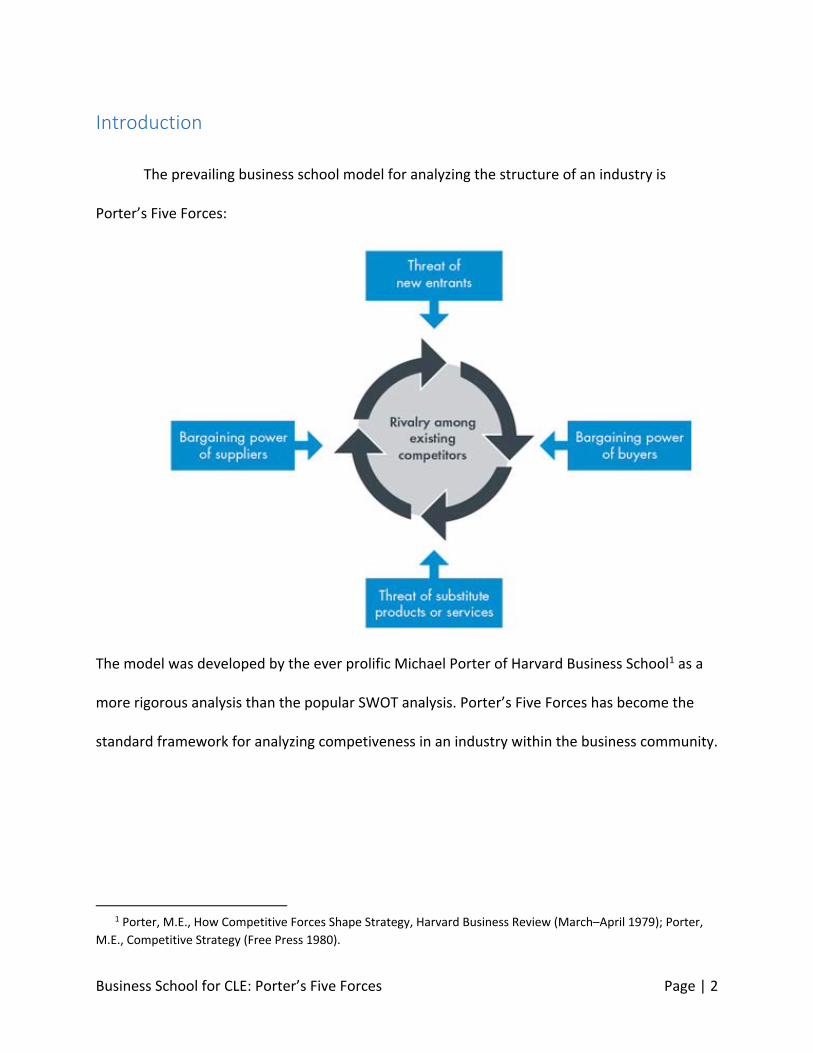

Introduction

The prevailing business school model for analyzing the structure of an industry is

Porter’s Five Forces:

The model was developed by the ever prolific Michael Porter of Harvard Business School1 as a

more rigorous analysis than the popular SWOT analysis. Porter’s Five Forces has become the

standard framework for analyzing competiveness in an industry within the business community.

1 Porter, M.E., How Competitive Forces Shape Strategy, Harvard Business Review (March–April 1979); Porter,

M.E., Competitive Strategy (Free Press 1980).

Business School for CLE: Porter’s Five Forces Page | 3

Threat of New Entrants

Any market in which high returns are made will attract entrants. Those new entrants

create more competition which will decrease profitability. The question is, how easy is it for

new entrants to enter the market – that is, are there barriers to entry? Barriers to entry can

include:

Brand loyalty, advertising

Absolute cost advantages

Scale economies (also scope and experience)

Regulation

Capital

Product Differentiation

R&D investments

Others: Exit barriers, channel preemption

The soft drink industry is a good example where extensive marketing has created band

loyalty that has made it difficult for competitors to enter the market. An industry that sits close

to natural resources or has a monopoly on skilled labor can produce at a lower costs than

others thus giving it an absolute cost advantage. Walmart can drive prices down and resist

competitors because its scope gives it economies of scale. Lawyers are protected from many

forms of competition by government regulation and licensure requirements. It takes a great

deal of capital to enter the auto industry, thus keeping competitors out and within the industry.

Luxury manufacturers, like BMW, create a sub‐group within the market through product

differentiation. The medical device industry is hard to enter because of the significant R&D

Business School for CLE: Porter’s Five Forces Page | 4

exposures required. The harder it is for competitors to enter the market, the more profitable it

is for the incumbents in the market.

Competitive Rivalry

Competitive rivalry within an industry is driven by the structure of the market including:

Fragmented or consolidated industry

Growth rate

Cost structures of industries: fixed costs

Extent of differentiation

Lumpiness of additions to capacity

A fragmented industry is one in which there are a large number of small to medium sized

businesses, none of which capable of setting price; a consolidated industry is one in which a few

larger companies dominated. There will be more competition in an industry that is fragmented

than consolidated. A fast growing market has room for more competitors as the number of

customers is growing while a mature market has increased competition because increasing

revenue likely means having to steal market share from someone else. Where there are high

fixed costs there is pressure to sell in volume which tends to drive competition. Differentiation

is when products are more specifically created for customers’ needs. With more differentiation,

there is less competitive pressure; with less differentiation there is more competitive pressure.

To the extent that additional capacity for production cannot be added smoothly, competitive

pressures are added in a similar fashion to an industry with high fixed costs.

Business School for CLE: Porter’s Five Forces Page | 5

Bargaining Power of Buyers

Buyers are those who purchase the industry’s products. Depending on where the

industry sits, they may be to end‐user customers or they may be to other businesses. Powerful

buyers are a threat. Buyers can have more or less power depending upon:

• Relative concentration

• Purchase volume as percentage of focal industry output

• Availability of substitute products

• Switching costs

• Threat of forward/backward integration

Relative concentration has to do with whether an industry has few or many customers facing

few or many sellers. For example, if the industry supplying a product or service has many small

companies and the buyers are large and few in number, the buyers can dominate the supplying

companies. Purchasing in large quantities gives the buyer leverage to bargain for a cheaper

price. If a product has few substitutes, it is vital to the industry and thus the supplier has power.

When switching costs are low, buyers can pit the supplying companies against each other to

force prices down. Buyers can sometimes move into the suppliers’ industry and vice versa,

putting pressure on the threatened industry to keep prices low to prevent the forward or

backward integration.

Business School for CLE: Porter’s Five Forces Page | 6

Bargaining Power of Suppliers

Suppliers can include those who provide materials, services, or labor. Their power is

similar in structure to the power of buyers. These suppliers can have more or less power to

raise costs in an industry depending on:

Relative concentration

Purchase volume as percentage of focal industry output

Availability of substitute products

Switching costs

Threat of forward/backward integration

Relative concentration has to do with whether an industry has few or many customers facing

few or many sellers. For example, the computer industry is highly dependent on a very few chip

makers, Intel chief amongst them. Intel holds a great deal of power over the computer industry.

The larger the purchases buyers in an industry make, the more power they have. For example,

Walmart and Costco buy in such bulk that they have considerable power over suppliers. If a

product has few substitutes, it is vital to the industry and thus the supplier has power. Even if

there is an ability to switch suppliers, there are often costs to switching that can inhibit

changing suppliers and thus gives the supplier power. Suppliers can sometimes move into the

buyers’ industry and vice versa putting pressure on the threatened industry to keep prices low

to prevent the forward or backward integration.

Business School for CLE: Porter’s Five Forces Page | 7

The analysis of the power of buyers and suppliers is similar. This makes sense because

this analysis just focuses on one part of a chain of buying and selling. A raw mineral industry

depends on suppliers of labor to extract minerals and prepare them to sell them to a buyer

industry that might make electronic components. The electric components industry supplier

has buyers in the computer industry for whom the component manufacturing industry is a

supplier and ultimately to the ultimate consumer. Whether one is a buyer or seller is just a

matter of where one is focusing on the chain.

Substitute Products

Substitute products are products of a different business or industry can satisfy customer

needs. For example, companies in the coffee industry compete indirectly with those in the tea

and soft drink industries because all three serve customer needs for nonalcoholic drinks. There

are three basic ways that substitution can be an issue for an industry:

• Direct substitution with same functionality – ex: diesel vs gas engines

• Eliminating need for product – ex: water meters vs flat rate

• Reduce product usage

If an industry’s products have few close substitutes, companies in the industry have the power

to raise prices.

Business School for CLE: Porter’s Five Forces Page | 8

Sixth Force: Complementors

A sixth force has been suggested by Andy Grove of Intel: the Power of Complementors.

Complementors create products which combine with an existing product and make it more

valuable. For example, the network of complementary apps makes smartphones more valuable.

A Brief Overview of the CLE Industry

Applying Porter’s Five Forces will give us a guide to how our industry is structured so

that we can better plot our own strategies for dealing with the structure and differentiating

ourselves.

Threat of New Entry

While there is regulation in our industry, particularly in mandatory jurisdictions, it is a

relatively low entry barrier. Some of us have built up a certain brand loyalty, but as a general

matter there is no particular band loyalty amongst our lawyers. Economies of scale are more of

an issue now that the internet has allowed companies with a national reach to compete in state

markets. None of us have absolute cost advantages unless you can prevent your volunteer

speakers from volunteering elsewhere. Customers have almost no switching costs, unless the

customer has purchased a package plan. It is easy to enter the CLE industry and this puts

competitive pressure on the industry.

Competitive Rivalry

Ours is, for the most part, a fragmented industry. It has never been a fast growing

market and, of late, little if any growth. There is some differentiation with higher end products,

Business School for CLE: Porter’s Five Forces Page | 9

but the very fact of mandatory rules tends to undifferentiate products toward a common

denominator of compliance. Our industry has a relatively high amount of fixed costs versus

variable costs, particularly in an organization with a substantial publishing program. On the

whole, our industry’s structure is such so that there is a great opportunity for competitive

rivalry. This is likely to only increase in the future as online competition and archived

programing fosters even more competitive rivalry.

Bargaining Power of Buyers

There are many CLE providers and a limited pool of attorney customers. Buyers do not

have any particular power with the size of their purchases, though a larger law firm can create

such power by aggregation. In the programs area, there are no real substitute products in a

mandatory state since regulation requires accreditation. On the publications side, online

resources and search tools are increasingly powerful potential substitutes. To the extent there

are substitutions, there are no switching costs. There is little threat of backward or forward

integration. On the whole, the balance is tipped to buyers with competitive rivalry likely making

more or a difference.

Bargaining Power of Suppliers

Our big suppliers are our speakers and facilities providers. We are blessed with many

lawyers willing to speak on a volunteer basis but they also have many outlets for their speaking

and limited time. Facilities providers go through cycles with the economy and right now costs

are on the upswing. There is no threat of backwards integration. The balance here is toward the

suppliers.

Business School for CLE: Porter’s Five Forces Page | 10

Pressure from Substitute Products

Lawyers have many choices for CLE and with the increased use of the Internet as a

delivery medium, those choices are expanding. There is some elimination, or at least changing

of product types. Internet delivery and on‐demand viewing are substitutes for the live

programs; online resources and search are substitutes for publications. While these are not

eliminating the need for traditional programs and publications, they are reducing the usage of

those products. There is considerable threat in our industry from substitute products.

Conclusion

Porter’s frame work is a powerful tool to help us think strategically. All forces need to be

considered when performing an industry analysis. One competitive force often affects others.

This gives us a framework there for examining our own competitive strategy within a company

Business School for CLE: Porter’s Five Forces Page | 11

What it tells us specifically about the CLE industry is that ours is a tough and competitive

environment. Entry barriers are low, there is considerable and growing competitive rivalry, our

customers have lots of choices, our suppliers are good to us but have other options, and there

are, to a certain extent, substitutes. For anyone who thinks CLE is easy, they should reconsider.

Knowing what we know now about the copetitive nature of the market, what is your strategy to

give yourself a competitive advantage in this tough market?