budget for the year 2009 presented in the house 6 th july,2009

TRANSCRIPT

BUDGET FOR THE YEAR 2009 PRESENTED IN THE HOUSE 6TH JULY,2009

PROVISION RELATED TO INDIVIDUALS1. BASIC EXEMPTION INCREASED AS FOLLOWING

FOR MALE BELOW 65 YEARS Rs. 160,000

FOR WOMAN BELOW 65 YEARS Rs. 190,000

FOR SENIOR CITIZEN ABOVE Rs. 240,000ABOVE 65 YEARS

Net Impact on above change Rs. 1030 for Man & Woman Assessee and Rs. 1545 for Senior Citizen

2. SURCHARGE IS ABOLISHED FROM INDIVIDUAL/ HUF/AOP/BOI

Surcharged is abolished from above assesses, earlier it was applicable on Individual / HUF where taxable income exceeds 10 lakh, Education and Higher Edu cess remained continue.

Surcharge is Still Applicable for Corporate Assessees.

Changes applicable from April,09

BUDGET 2009 6th July,2009

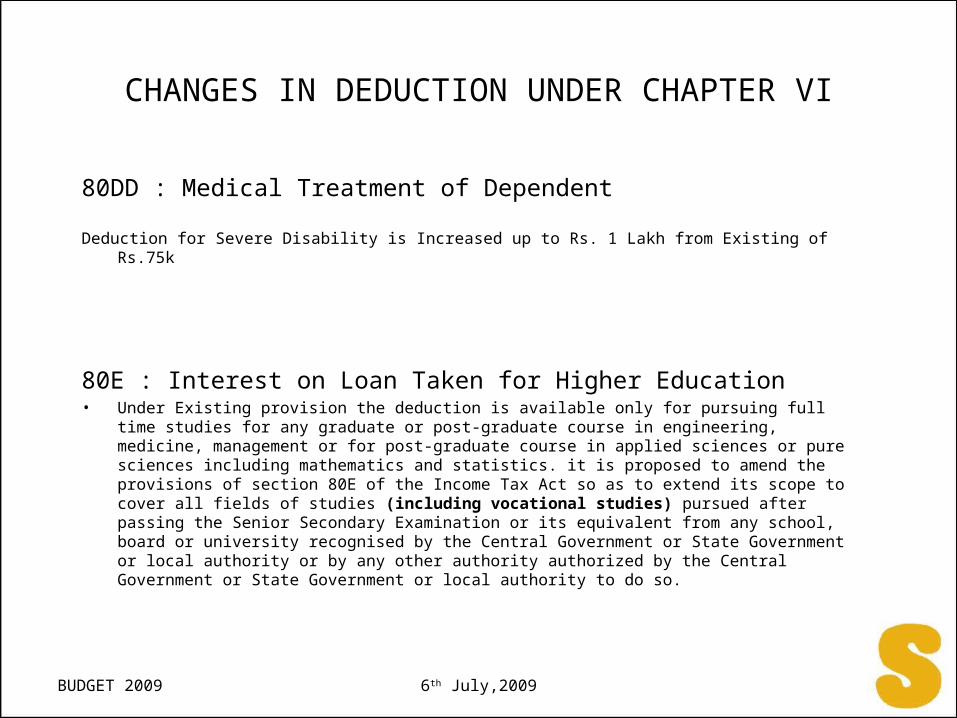

CHANGES IN DEDUCTION UNDER CHAPTER VI

80DD : Medical Treatment of Dependent

Deduction for Severe Disability is Increased up to Rs. 1 Lakh from Existing of Rs.75k

80E : Interest on Loan Taken for Higher Education• Under Existing provision the deduction is available only for pursuing full time studies for any

graduate or post-graduate course in engineering, medicine, management or for post-graduate course in applied sciences or pure sciences including mathematics and statistics. it is proposed to amend the provisions of section 80E of the Income Tax Act so as to extend its scope to cover all fields of studies (including vocational studies) pursued after passing the Senior Secondary Examination or its equivalent from any school, board or university recognised by the Central Government or State Government or local authority or by any other authority authorized by the Central Government or State Government or local authority to do so.

BUDGET 2009 6th July,2009

ADVANCE TAX & WEALTH TAX

1. ENHANCEMENT OF THE LIMIT FOR PAYMENT OF ADVANCE TAX

The proposed amendment will take effect from the 1st April, 2009. Accordingly, advance-tax forthe financial year 2009-2010 would be payable only if the advance tax liability is Rs. 10,000/- or more, earlier it was Rs. 5000/- or More.

2. ENHANCEMENT OF THE LIMIT FOR PAYMENT OF WEALTH TAX

Under existing Provision Wealth Tax is paid @ 1% on wealth above Rs. 15 Lakh , now limit of 15lakh is increased upto Rs. 30 lakh. The proposed amendment will apply for the valuation of netwealth as on 31st March, 2010 and will, accordingly, apply in relation to assessment year 2010-11 and subsequent years.

BUDGET 2009 6th July,2009

BUDGET 2009 6th July,2009

BUDGET HIGHLIGHTS FOR CORPORATE SECTOR

PROVISION RELATED TO CORPORATE SECTOR

1. FBT ABOLISHED It is proposed to insert a new section 115WM to abolish the fringe benefit tax. This amendment will take effect from the 1st April, 2010 and will accordingly apply to assessment year 2010-11And subsequent assessment years.

2. MINIMUM ALTERNATE TAX (MAT)

Rate of Minimum Alternate Tax Increased from 10 % to 15 %.Carry forward of MAT Credit also Increase from 7 Years to 10 Years

This amendment will take effect from the 1st April, 2010 and will accordingly apply to assessment year 2010-11 And subsequent assessment years.

3. LIABILITY TO PAY ADVANCE TAX INCREASE FROM 5K TO 10K

4. WEALTH TAX BASIC EXEMPTION INCREASE FROM 15 L TO 30 L

BUDGET 2009 6th July, 2009

5. PAYMENT MORE THAN 20000 BY CASH ( SEC 40A (3A))Given the special circumstances of transport operators for incurring expenditure on long haul journeys, it is proposed to raise the limit of payment to such transport operators otherwise thanby an account payee cheque or account payee bank draft to Rs 35,000/- from the existing limit of Rs 20,000/-. For this purpose a new proviso is proposed to be inserted after the proviso insub-section (3A) of section 40A of the Income-tax Act.

6. EXTENSION OF SUNSET CLAUSE FOR TAX HOLIDAY 80-IAIn Case of Power Generating Plant clause (v) of sub-sec 4 of 80 IA , Terminal date for commencing the activity extend from Mar,08 to Mar,11 ( With Retrospectively from Apr,08 )

In Case of Power Generating Plant clause (iv) of sub-sec 4 of 80 IA , Terminal date for commencing the activity extend from Mar,10 to Mar,11

7. EXTENSION OF SUNSET CLAUSE FOR SEZ AND EOU (10A, 10B )It is proposed to amend sections 10A and 10B to extend the tax benefit under both these sections by one year i.e., the deduction will be available upto assessment year 2011-12.

BUDGET 2009 6th July,2009

8. COMPUTATION OF BOOK PROFIT (SEC 115JB )It is proposed to insert a new clause (i) in Explanation 1 after sub-section (2) of the said section so as to provide that if any provision for diminution in the value of any asset has been debited tothe profit and loss account, it shall be added to the net profit as shown in the profit and loss account for the purpose of computation of book profit.

The amendment to section 115JB is proposed to be made effective retrospectively from 1st day of April, 2001 and will, accordingly, apply in relation to assessment year 2001-02 and subsequent assessment years.

9. COMPUTING PROFIT AND GAINS ON PRESUMPTIVE BASIS• The scheme shall be applicable to individuals, HUFs and partnership firms excluding Limited liability

partnership firms. It shall also not be applicable to an assessee who is availing deductions under sections 10A, 10AA, 10B, 10BA or deduction under any provisions of Chapter VIA under the heading “C.—Deductions in respect of certain incomes” in the relevant assessment year.

• The scheme is applicable for any business (excluding a business already covered under Sec. 44AE) which has a maximum gross turnover /gross receipts of 40 lakhs.

• The presumptive rate of income is prescribed at 8% of gross turnover /gross receipts.• An assessee opting for the above scheme shall be exempted from payment of advance tax related to

such business under the current provisions of the Income-tax Act.• An assessee opting for the above scheme shall be exempted from maintenance of books of accounts

related to such business as required under section 44AA of the Income-tax Act.• The proposed amendment will take effect from 1st April, 2011 and will, accordingly, apply in relation to

the assessment year 2011-12 and subsequent years.

BUDGET 2009 6th July,2009

RATIONALISATION OF TDS RATES• Nature of Payment (194-I) Existing

Proposed rate*

• rate (w.e.f. 1-10-2009)• a. rent of plant, machinery or equipment 10% 2%• b. rent of land, building or furniture to an individual and 15% 10%• Hindu undivided family• c. rent of land, building or furniture to a per son other than an 20% 10%• individual or Hindu undivided family• * The rate of TDS will be 20 per cent in all cases, if PAN is not quoted by the deductee w.e.f. 1.04.2010.• Nature of Payment (194C) Existing

Proposed rate**

• rate (w.e.f. 1-10-2009)• Payment to —• a. Individual/HUF contractor 2% 1%• b. Other than individual/HUF contractor 2% 2%• c. Individual/HUF sub-contractor 1% 1%• d. Other than individual/HUF sub-contractor 1% 2%• e. Individual/HUF contractor/sub-contractor for advertising 1% 1%• f. Other than individual/HUF contractor/ sub-contractor for advertising 1% 2%• g. Sub-contractor in transport business 1% nil*• h. Contractor in transport business 2% nil*The nil rate will be applicable if the transporter quotes his PAN. If PAN is not quoted the rate will be 1% for an individual/ HUF transporter and 2% for other transporters upto 31.3.2010.** The rate of TDS will be 20 per cent in all cases, if PAN is not quoted by the deductee w.e.f. 1.04.2010.

BUDGET 2009 6th July, 2009

BUDGET HIGHLIGHTS IN SERVICE TAX

BUDGET 2009 6th July,2009

PROVISION RELATED TO SERVICE TAX

• SERVICE TAX IS BEING IMPOSED ON THE FOLLOWING SPECIFIED SERVICES:

1) Service provided in relation to transport of goods by rail2) Service provided in relation to transport of (i) coastal goods; and (ii) goods through Inland Water including National Waterways3) Legal consultancy service4) Cosmetic and plastic surgery service

The above changes will come into effect from a date to be notified, after the enactment of Finance (No. 2) Bill, 2009. ?(i.e 1st april,09 )

BUDGET 2009 6th July,2009

AMENDMENTS IN THE RULES AND EXISTING NOTIFICATIONS

1) The scope of notification No. 1/2002–ST dated 01.03.2002 is being enlarged by extending the applicability of service tax provisions to installations, structures and vessels in the entire Continental Shelf of India and Exclusive Economic Zones of India.

2) Rule 6 (3) of the Cenvat Credit Rules, 2004 is being amended to prescribe that a provider of both taxable and exempted services, who does not maintain separate accounts of inputs, shall pay an amount equal to 6% of the value of exempted services instead of 8%.

3) Rule 3 (5B) of the Cenvat Credit Rules, 2004 is being amended so as to provide that a service provider shall pay back the amount of credit taken on inputs/capital goods fully written off.

4) Explanation provided in the Works Contract Rules, 2007 is being modified so as to allow the benefit of optional composition scheme only to such works contracts where the taxpayer declares the entire value of goods (whether supplied under anyother contract for a consideration or otherwise) and services used in the execution of the works contract as the ‘gross value'charged for the works contract. This restriction would not apply to current works contracts where either the execution has commenced or any payment has been made on or before 07.07.2009.

The changes mentioned in S. Nos. (1) to (4) above will come into effect

BUDGET 2009 6th July,2009

EXEMPTIONS

1) Exemption from service tax is being provided to inter-state or intra-state transportation of passengers in a vehicle bearing ‘Contract Carriage Permit’ with specified conditions.

2) Exemption from service tax (leviable under Club or Association Service) is being provided tothe Federation of Indian Export Organizations (FIEO) and specified Export Promotions Councils.The exemption is valid till 31.03.2010.

3) Exemption from service tax (leviable under banking and other financial services or under foreign exchange broking service) is being provided to inter-bank purchase and sale of foreign currency between scheduled banks.

The above changes will come into effect immediately.

BUDGET 2009 6th July,2009

FOLLOWING LINK IS THE SOURCE OF PRESENTATION

http://indiabudget.nic.in/ub2009-10/memo.htm

BUDGET 2009 6th July,2009

Thanks & Regards

CA. Sumit Gupta

Manger ( Finance & Accounts )

SPICE WORLD