budget 2010-11. 2 key announcements : taxes ● excise duty raised by 2% to 10% for all non...

TRANSCRIPT

Budget 2010-11

Budget 2010-11 2

Key Announcements : Taxes● Excise duty raised by 2% to 10% for all non petroleum goods● Service tax rates maintained at 10% , in parity with the new excise rate● Income Tax exemption limits tweaked ; Would result in 50K savings per year per individual

– Additional exemption of 20,000 for investments in long term infrastructure bonds.● MAT raised from 15% to 18%.● Surcharge for companies reduced from 10% to 7.5%● Import duty on crude products restored ● Excise duty of 1% per litre on petrol and diesel introduced● Service tax net widened● Direct Tax Code and GST to be implemented by April 2011

● Partial roll back in excise duty in line with expectations but may add to inflationary pressures

● Uniform goods and service tax ahead of the GST roll out positive

● Income tax changes would improve compliance and increase disposable income, - Will help maintain the momentum in consumption

● Tax concessions for infra bonds may ease dearth of domestic long term funding

● Clarity on GST and DTC roll out and implementation of the TFC recommendations positive

Income Slab

Tax rate

< 1.6 Lac Nil

1.6-5 Lac 10%

5-8 Lac 20%

> 8 Lac 30%

Budget 2010-11 3

Fiscal Numbers - Deficits

● Fiscal deficit estimated at 5.5% of GDP for FY11- 140 bps reduction from a year back, when the off budget liabilities of last year are included

● Absolute fiscal deficit number also estimated to fall by ~34K Cr

● Assuming states’ deficit stays flat at 3.2% of GDP in FY11, combined fiscal deficit slips below 9%

● Government’s decision to pay out subsidies as cash reduces ambiguity on the ‘actual” fiscal deficit

● For the same reason, the upside risk to expenditure estimates and therefore to the budgeted fiscal deficit may be substantial

All numbers are in Rs Cr

Budget 2010-11 5

Fiscal Numbers - Receipts

● Overall tax growth assumption of 17.9% - 1.4x to the GDP growth assumption of 12.5%

● Direct taxes assumed to grow by 11% - Income taxes expected to be in the negative

● Rate hikes assumed to help indirect tax collections – 32% growth in indirect tax collections estimated

● Disinvestment assumption of 40K Cr in FY 2010-11 aggressive -3G license fee of 36 K Cr assumed

● Grants to states raised from 26% to 28% of Gross Tax, in a bid to move to the TFC recommendation of 32%

● Greater reliance on non tax revenue - Net Tax/ GDP to rise by 22 bps while Non Tax revenue/GDP to rise by 32 bps.

All numbers are in Rs Cr

Budget 2010-11 8

Fiscal Numbers - Expenditure

● Increased in Plan Expenditure estimated to be higher than in FY10

● Subsidies estimated to fall by 11% - Has never happened in the past 15 years

● Drop in food subsidies may be ambitious in the wake of the drought last year and uncertainty in monsoons' next year

● Massive drop in fuel subsidies assumed – May be revised up given the under recoveries , unless price hikes are effected

All numbers are in Rs Cr

All numbers are in Rs Cr

Budget 2010-11 9

Expenditure

● Muted increase in allocation for rural development

● NREGA saw marginal increase in funds after the substantial jump last year

● Agriculture has received marginally higher proportion of funds

● As proportion of funds other social sectors such as education and health have risen as proportion of total spending

● Spending on rural sector has clearly taken a back seat

● Overall expenditure assumptions may be termed optimistic – the Budget builds in 58 bps fall in expenditure/GDP ratio

All numbers are in Rs Cr

Budget 2010-11 10

Expenditure in Pictures

IP Consumer Durables Car Sales

CV Sales Railway Freight

Budget 2010-11 11

Fiscal Numbers - Borrowings

● Net market borrowings lower by 50K Cr, surprising markets on the upside

● Financing assumes greater reliance on external funding

● Proceeds from small savings is assumed to be flat

● At mandatory SLR of 25%, demand from banks, insurance and provident funds should see the central government borrowing programme sail through.

● Fixed income market reacted as the fear of excessive borrowings turned out to be false

● Risks are in terms of higher than expected credit pick up and additional borrowing announcements

All numbers are in Rs Cr

Budget 2010-11 12

Takeaways from Numbers

● Clear intent to tax consumption and reduce subsidies

● Use of balance sheet (disinvestment) and income (taxes) to reduce fiscal deficit to 5.5%

● Increasing disposable income by lower taxes to raise consumption which has remained the bulwark of Indian economy.

• This is a continuing theme and we could see a regime of lower income taxes, but more goods and services being taxed. The intent is clear- consumption is being encouraged

● Additional surprise possible should oil and commodity prices fall sharply

● Divided house on ability of government to deliver fiscal consolidation

Budget 2010-11 13

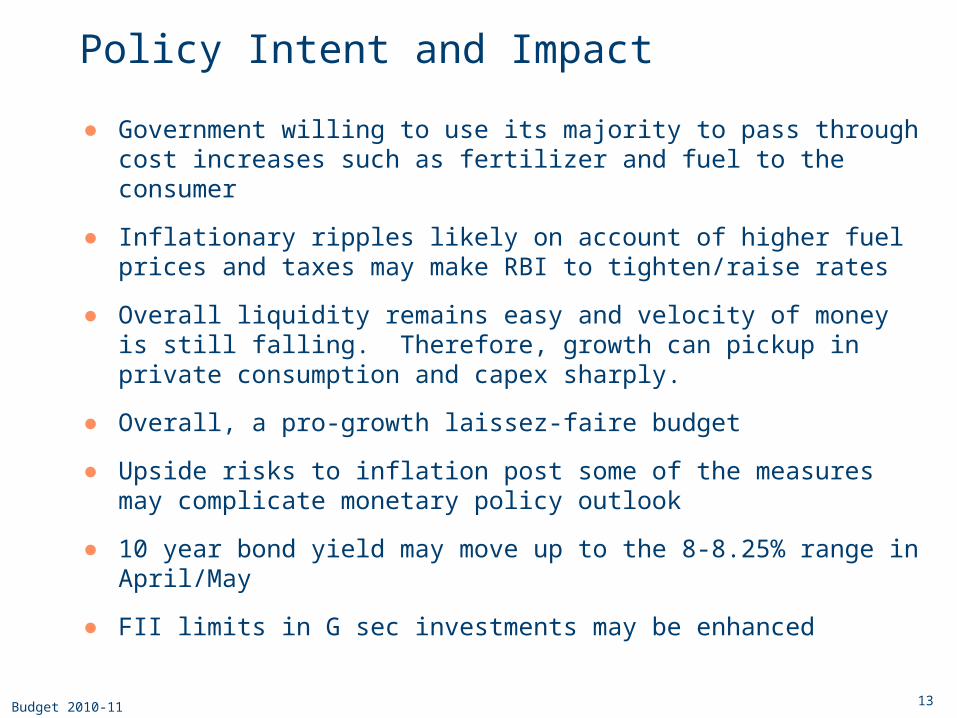

Policy Intent and Impact

● Government willing to use its majority to pass through cost increases such as fertilizer and fuel to the consumer

● Inflationary ripples likely on account of higher fuel prices and taxes may make RBI to tighten/raise rates

● Overall liquidity remains easy and velocity of money is still falling. Therefore, growth can pickup in private consumption and capex sharply.

● Overall, a pro-growth laissez-faire budget

● Upside risks to inflation post some of the measures may complicate monetary policy outlook

● 10 year bond yield may move up to the 8-8.25% range in April/May

● FII limits in G sec investments may be enhanced

Budget 2010-11 14

Risks

● Risks remain on ability to manage growth and have higher taxes

● Disinvestment and 3G targets need to be achieved for fiscal consolidation

● Assumption is that monsoons would be normal and inflation remains under check

● Consensus based politics may delay some of the proposals

Budget 2010-11 15

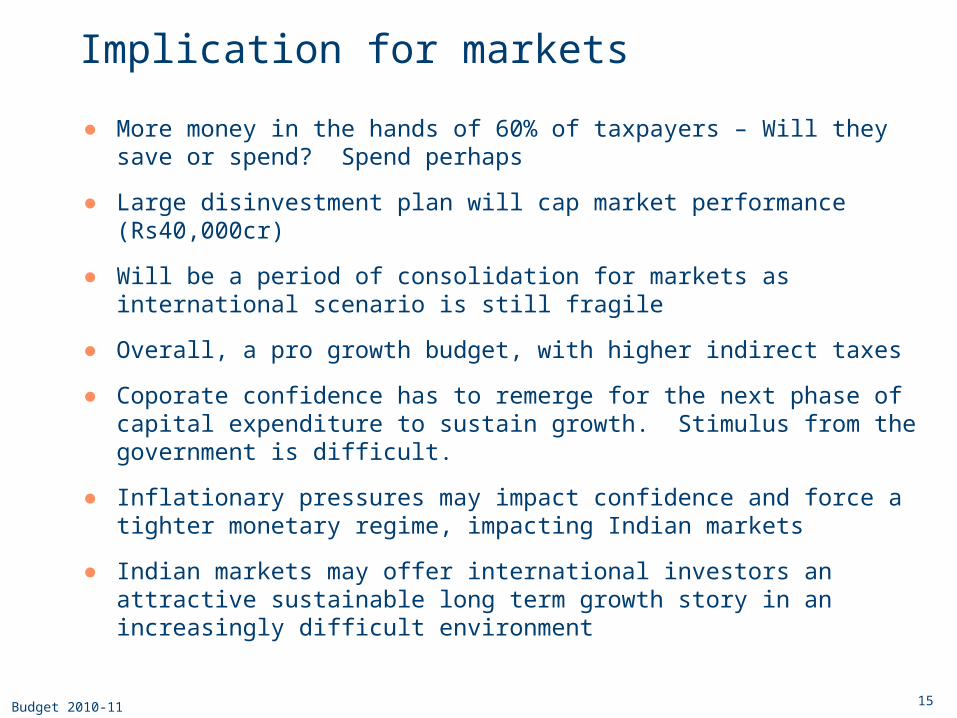

Implication for markets

● More money in the hands of 60% of taxpayers – Will they save or spend? Spend perhaps

● Large disinvestment plan will cap market performance (Rs40,000cr)

● Will be a period of consolidation for markets as international scenario is still fragile

● Overall, a pro growth budget, with higher indirect taxes

● Coporate confidence has to remerge for the next phase of capital expenditure to sustain growth. Stimulus from the government is difficult.

● Inflationary pressures may impact confidence and force a tighter monetary regime, impacting Indian markets

● Indian markets may offer international investors an attractive sustainable long term growth story in an increasingly difficult environment

Impact on Sectors

Budget 2010-11 17

Sector-wise AnnouncementsSECTOR ANNOUCEMENTS IMPACT

Agriculture 1. Agriculture Credit target increased to 375,000 crs. Target in 2009-10 was 325,000 crs.

2. Interest Subvention increased from 1% to 2% for timely payment of short-term crop loan.

3. Extension of time for farmers of debt under debt waiver scheme from 31st Dec09 to 30th June10

4. Allocation under NREGS increased marginally from 39100 crs to 40100 crs.

Focus on Agriculture continues. Will benefit farmers by improving their cash flows. Overall, positive for Rural economy which should enable the farmers to spend more on inputs such as pesticides, seeds, etc.

Airlines The scope of air passenger transport service is being expanded to domestic and International traffic on all classes (earlier only Business class travel on International routes)

Service tax of 10% will be levied on Airline passengers. Although airlines are most likely to pass on the hike, Leisure travel can see some softening of demand. No relief on reduction of excise duty on ATF (some relief was expected) is also a negative for the sector

Budget 2010-11 18

Sector-wise Announcements

SECTOR ANNOUNCEMENTS IMPACT

Auto – Entire Sector Hike in Excise duty came at 2% (from 8% to 10%) . Direct Tax slab increase partially offset this negative

A 2% increase across the board for 2W & cars reduces the elbow room for OEM’s to pass on impending raw material increases. However direct tax cuts for individuals positive for small cars (On a Rs8 lakh annual income, taxes have been reduced by ~Rs50,000 per year) by increasing affordability

Auto – Electric Vehicles

Concession on excise duty for parts for manufacture of these vehicles

Small positive for Tata Motors (Electric Indica is under development) and 2 wheeler manufacturers working on electric 2W

Cement 1.MRP>190/bag: Excise increased from 8 to 10%; MRP < 190/bag, from 230 to 290/ton and clinker: from 300 to 375/ton

2.Cess of Rs100/ton of coal (for the green fund) on both the domestic coal & imported coal. Railway freight under service tax of 10%

3.Potential diesel price hike

Impact of Rs3-5 per bag. Neutral to negative as challenging to pass on the increase

Coal cost to increase by Rs200-250/ton (incl. freight). Impact of Rs1.7-2.1 per bag. Negative

Outward freight cost to increase by ~ Rs1.2.

Total impact of Rs5-7 per bag. Neutral in the medium term as companies believe that they will pass-on on the back of strong demand

Budget 2010-11 19

Sector-wise AnnouncementsSECTOR ANNOUNCEMENTS IMPACT

Construction& Infrastructure

1. Higher allocation to infra schemes – NHAI (+13%), Bharat Nirman (+5%). Railways (+6%)

2. IIFCL to re-finance Rs60bn loans (+100%). Direct tax exemption of Rs20,000 on investment in LT infra bonds

3. MAT increased from 15% to 18%. Eff. Increase from 16.9 to 19.9%

1. Muted increase esp. in roads considering such aggressive plan

2. Infrastructure projects to get the long term funding support – positive

3. Negative for companies having BOT assets (under 80IA) – IRB Infra, IVRCL, HCC. NAV impact of 1-3%

FMCG 1. Increase in excise duty by 2%

2. Increase in excise duties for cigarettes by 11-18%

3. MAT increased to 18% of book profits from 15%.

4. Increase in Income tax slab rates.

1. Impact of increase in excise duty will be passed on to the end consumers.

2. Negative for the cigarette companies. But introduction of new category (filter less than 60mm) can capture some of the fall in volumes.

3. Marginally negative for the sector as it impacts the cash flows of the companies.

4. Tax payers will have more disposable income at their end and it can help to revive the volume growth of FMCG companies.

Budget 2010-11 20

Sector-wise AnnouncementsSECTOR ANNOUCNEMENTS IMPACT

Hotels Investment linked deduction allowed for all hotels constructed in 2 star category and above.

The investment-linked tax incentive allows 100 per cent deduction in respect of the whole of any expenditure of capital nature (other than on land, goodwill and financial instrument). Indian Hotels and Hotel leela could be beneficiaries.

IT 1.MAT increased to 18% of book profits from 15%.

2.The SEZ rule clarified last year for FY10 will be applicable retrospectively from FY07

1.Marginally negative for the sector as it impacts the cash flows of the companies.

2.Marginally positive since most of the IT companies assumed tat this clarification would emerge. It could result in a write back of tax provision for the period FY07-09.

Media 1. Tax rate reduction due to reduction in surcharge.

Will benefit Print companies, Sun TV, Zee TV which pay high taxes.

Budget 2010-11 21

Sector-wise AnnouncementsSECTOR ANNOUCNEMENTS IMPACT

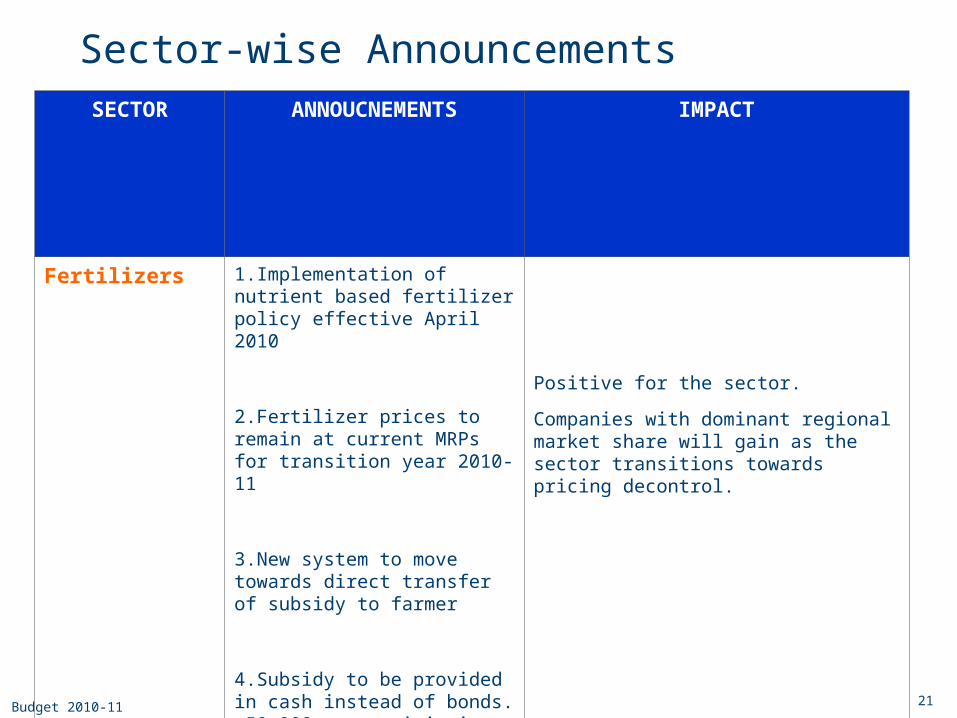

Fertilizers 1.Implementation of nutrient based fertilizer policy effective April 2010

2.Fertilizer prices to remain at current MRPs for transition year 2010-11

3.New system to move towards direct transfer of subsidy to farmer

4.Subsidy to be provided in cash instead of bonds. ~50,000crs provisioning for 2010-2011

Positive for the sector.

Companies with dominant regional market share will gain as the sector transitions towards pricing decontrol.

Budget 2010-11 22

Sector-wise AnnouncementsSECTOR ANNOUNCEMENTS IMPACT

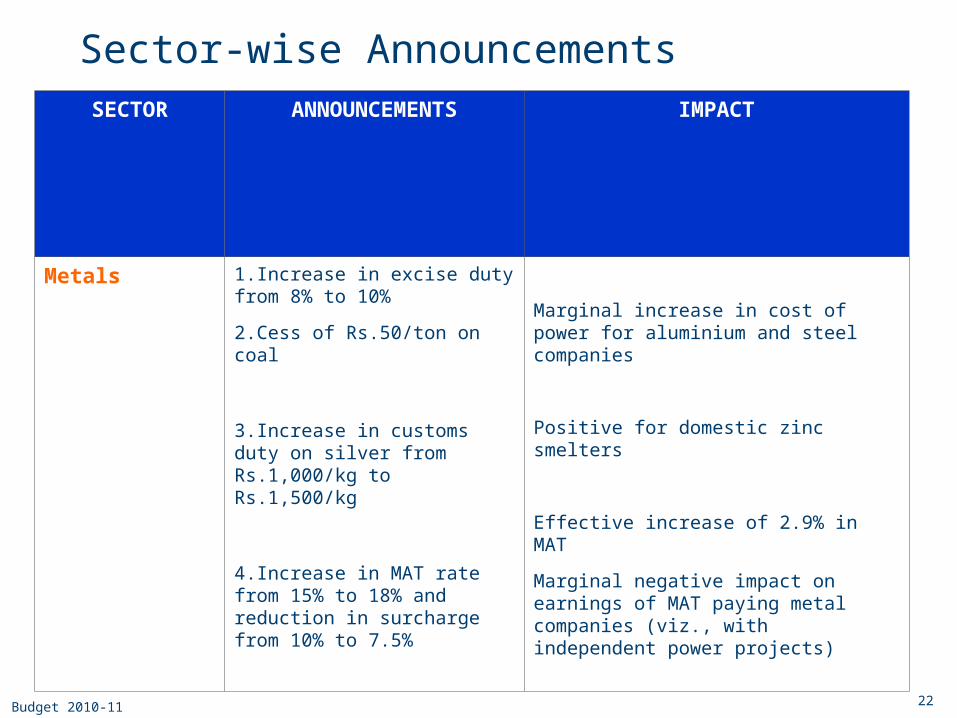

Metals 1.Increase in excise duty from 8% to 10%

2.Cess of Rs.50/ton on coal

3.Increase in customs duty on silver from Rs.1,000/kg to Rs.1,500/kg

4.Increase in MAT rate from 15% to 18% and reduction in surcharge from 10% to 7.5%

Marginal increase in cost of power for aluminium and steel companies

Positive for domestic zinc smelters

Effective increase of 2.9% in MAT

Marginal negative impact on earnings of MAT paying metal companies (viz., with independent power projects)

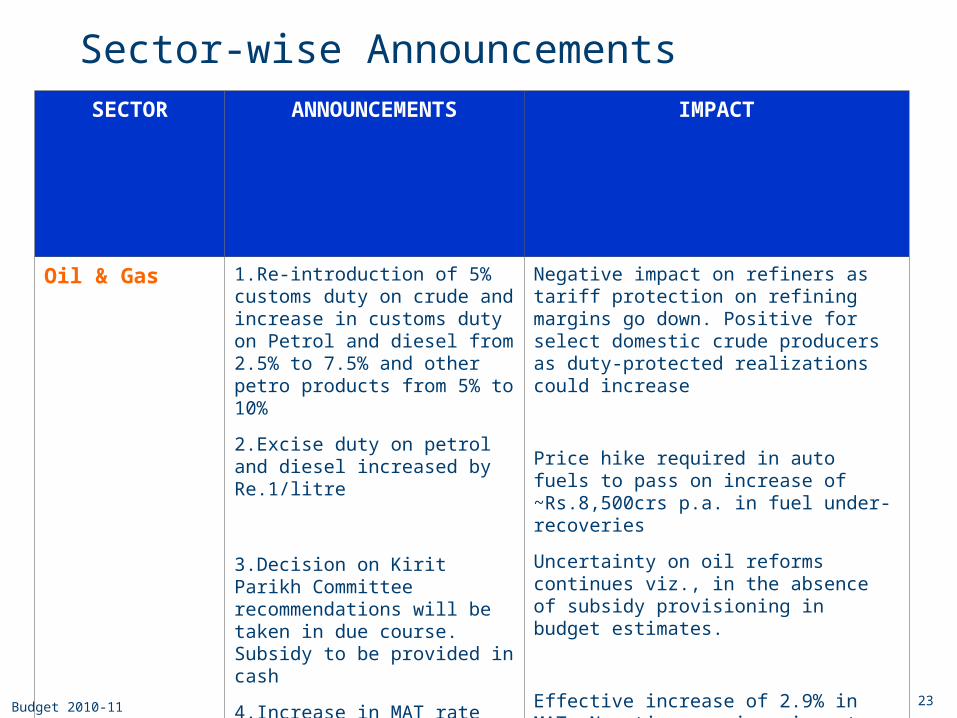

Budget 2010-11 23

Sector-wise AnnouncementsSECTOR ANNOUNCEMENTS IMPACT

Oil & Gas 1.Re-introduction of 5% customs duty on crude and increase in customs duty on Petrol and diesel from 2.5% to 7.5% and other petro products from 5% to 10%

2.Excise duty on petrol and diesel increased by Re.1/litre

3.Decision on Kirit Parikh Committee recommendations will be taken in due course. Subsidy to be provided in cash

4.Increase in MAT rate from 15% to 18% and reduction in surcharge from 10% to 7.5%

Negative impact on refiners as tariff protection on refining margins go down. Positive for select domestic crude producers as duty-protected realizations could increase

Price hike required in auto fuels to pass on increase of ~Rs.8,500crs p.a. in fuel under-recoveries

Uncertainty on oil reforms continues viz., in the absence of subsidy provisioning in budget estimates.

Effective increase of 2.9% in MAT. Negative earnings impact for MAT paying upstream and midstream companies in this sector.

Budget 2010-11 24

Sector-wise AnnouncementsSECTOR ANNOUCEMENTS IMPACT

Power 1. APDRP allocation at Rs. 3382 crs (151%) – an increase of 151% over BE 2009-10

2. RGGVY allocation – 9852 crs – growth of 30%

3. 16% Customs Duty on power exported from SEZ to Domestic Tariff area and non – processing zone of SEZ.

4. MAT rate increased from 15% to 18%.

5. Cess of Rs.50/T for imported and Domestic Coal. Will increase cost by ~ 3paise/unit.

Consultancy division of Power Grid Corporation will benefit. The company also executes projects under the RGGVY scheme. However, impact to be marginal for the company.

Customs duty imposition will affect Adani Power, JSW Energy.

Increase in MAT rate will increase tax outgo for power projects in the initial years. Companies can claim tax credit in future years. However, it will have a negative impact in the value for Power companies such as NTPC, Adani Power, JSW Energy, Tata Power, Reliance Power, GMR, GVK, etc.

Budget 2010-11 25

Sector-wise AnnouncementsSECTOR ANNOUNCEMENTS IMPACT

Pharmaceuticals 1. Weighted average deduction for in house R&D increased from 150% to 200%

Positive for research based firms. Encourages more investments in R&D

Power Equipment 1.Increased allocation to schemes like APDRP (+150%), RGGVY (+10%), PGCIL capex (+23%)

Positive for equipment companies like Areva, Crompton, ABB, ICSA India, etc

Shipyard 1.Subsidy of Rs 588 cr was alotted in the budget for govt and private sector shipyards

ABG Shipyard and Bharathi Shipyard could be beneficiaries

Budget 2010-11 26

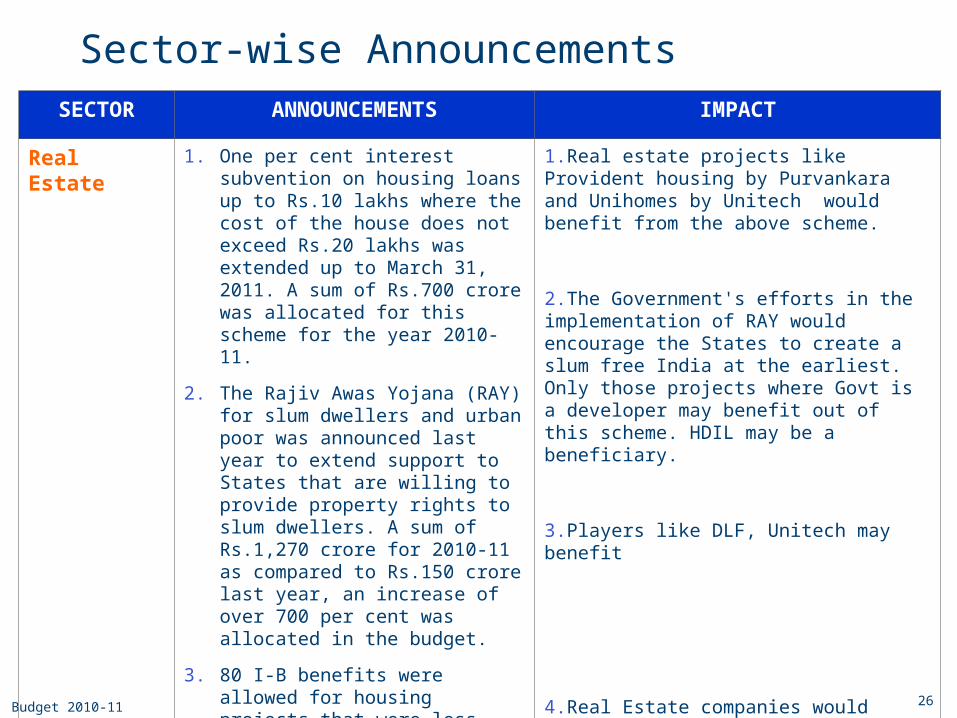

Sector-wise AnnouncementsSECTOR ANNOUNCEMENTS IMPACT

Real Estate 1. One per cent interest subvention on housing loans up to Rs.10 lakhs where the cost of the house does not exceed Rs.20 lakhs was extended up to March 31, 2011. A sum of Rs.700 crore was allocated for this scheme for the year 2010-11.

2. The Rajiv Awas Yojana (RAY) for slum dwellers and urban poor was announced last year to extend support to States that are willing to provide property rights to slum dwellers. A sum of Rs.1,270 crore for 2010-11 as compared to Rs.150 crore last year, an increase of over 700 per cent was allocated in the budget.

3. 80 I-B benefits were allowed for housing projects that were less than 1000 sq ft in metros and those that were 1500 sq ft which were launched before October 2008. The window was to expire in FY 12. Now, it has been extended to FY 13.

4. Real Estate Projects to be included in the service tax net

1.Real estate projects like Provident housing by Purvankara and Unihomes by Unitech would benefit from the above scheme.

2.The Government's efforts in the implementation of RAY would encourage the States to create a slum free India at the earliest. Only those projects where Govt is a developer may benefit out of this scheme. HDIL may be a beneficiary.

3.Players like DLF, Unitech may benefit

4.Real Estate companies would raise the rates to the extent the service tax is increased, thus impacting the near term volumes in the segment.

Budget 2010-11 27

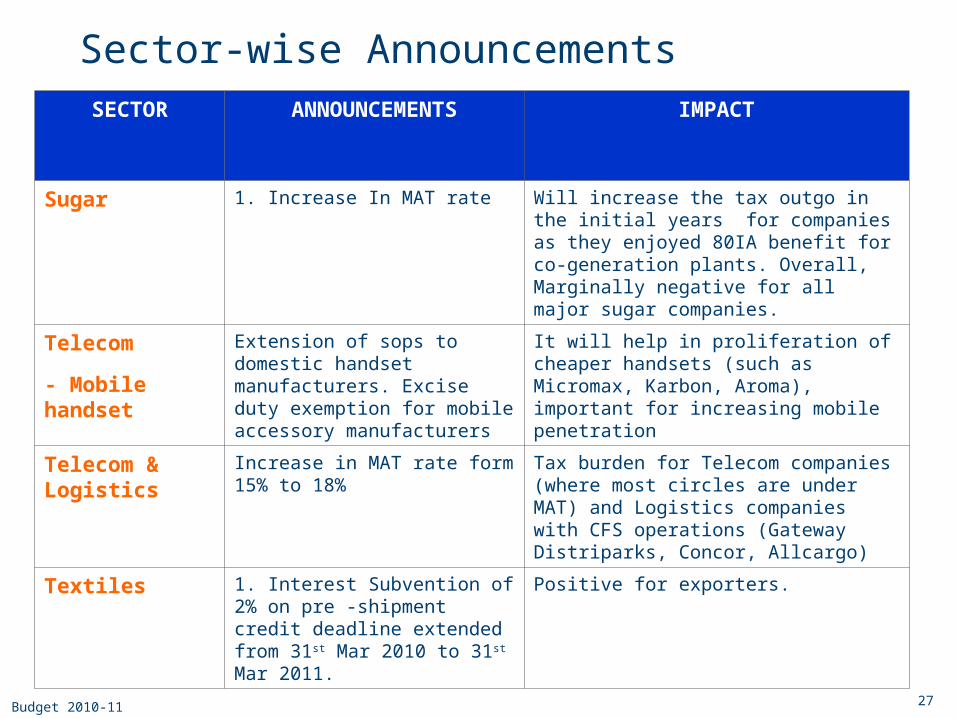

Sector-wise AnnouncementsSECTOR ANNOUNCEMENTS IMPACT

Sugar 1. Increase In MAT rate Will increase the tax outgo in the initial years for companies as they enjoyed 80IA benefit for co-generation plants. Overall, Marginally negative for all major sugar companies.

Telecom

- Mobile handset

Extension of sops to domestic handset manufacturers. Excise duty exemption for mobile accessory manufacturers

It will help in proliferation of cheaper handsets (such as Micromax, Karbon, Aroma), important for increasing mobile penetration

Telecom & Logistics Increase in MAT rate form 15% to 18% Tax burden for Telecom companies (where most circles are under MAT) and Logistics companies with CFS operations (Gateway Distriparks, Concor, Allcargo)

Textiles 1. Interest Subvention of 2% on pre -shipment credit deadline extended from 31st Mar 2010 to 31st Mar 2011.

Positive for exporters.

Thank you