bounty oil and gas nl - · pdf filebounty oil and gas nl . ... • the petroleum reserve...

TRANSCRIPT

Bounty Oil and Gas NL Presentation to QUPEX

Tattersalls Club Brisbane 2 August 2016

ASX Code: BUY

Philip F Kelso - CEO Gas Plant Songo Songo Island

2

Disclaimer/Competent Person

This presentation contains forward looking statements that are subject to risk factors associated with the oil and gas industry. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a range of variables which could cause actual results or trends to differ materially, including but not limited to: product price fluctuations, actual demand, currency fluctuations, geotechnical factors, drilling and production results, oil and gas commercialisation, development progress, operating results, engineering estimates, reserve estimates, loss of market, industry competition, environmental risks, physical risks, legislative, fiscal and regulatory developments, economic and financial markets conditions in various countries, approvals and cost estimates.

All references to dollars, cents or $ in this document are Australian currency, unless otherwise stated

QUALIFIED PERSON’S STATEMENT

• The petroleum Reserve and Resources estimates used in this report and ;the information in this report that relates to or

refers to petroleum or hydrocarbon production, development and exploration; Is based on information and reports prepared by, reviewed and/or compiled by the CEO of Bounty, Mr Philip F Kelso. Mr Kelso is a Bachelor of Science (Geology) and has practised geology and petroleum geology for in excess of 25 years. He is a member of the Petroleum Exploration Society of Australia and a Member of the Australasian Institute of Mining and Metallurgy.

• Mr Kelso is a qualified person as defined in the ASX Listing Rules: Chapter 19 and consents to the reporting of that information in the form and context in which it appears.

3

ASX Listing Rules – Chapter 5 Reserves and Resources

ASX LISTING RULES 5.25 – 5.45 • All Bounty Oil & Gas NL (Bounty) petroleum Reserves and Resources assessments follow guidelines set forth by the Society of

Petroleum Engineers – Petroleum Resource Management System (SPE-PRMS). Bounty is compliant with recent listing rule changes for reporting of estimates as defined in Chapter 5 of the ASX Listing Rules.

INFORMATION REQUIRED UNDER CHAPTER 5 OF ASX LISTING RULES - THIS ASX RELEASE For the purposes of Chapter 5 estimates of petroleum oil volumes presented in this release are: • Reported at the date of this release • Determined as an estimate of recoverable resources in place unadjusted for risk • Best Estimate Prospective Resources • Unless otherwise stated estimated using probabilistic methods • Reported at 100% net to Bounty • If specified as" boe" then they are converted from gas to oil equivalent at the rate of 182 bbls ≡ 1 million standard cubic feet of gas • The estimated quantities of petroleum that may potentially be recovered by the application of a future development project relate to

undiscovered accumulations. These estimates have both an associated risk of discovery and a risk of development. Further exploration, appraisal and evaluation is required to determine the existence of a significant quantity of potentially moveable hydrocarbons.

4

Bounty Oil & Gas NL – Gas Production Base - Low Risk Oil Upside

Major gas pipeline and plant construction at Kiliwani North (KN) completed and plant on stream at 20 -25mmcfd.

Bounty revenue expected to re-bound strongly in 2017 with Tanzanian gas sales after group oil revenue for the year down to $1.35 million (2015: $1.91 million) impacted by lower oil prices.

Take or pay Gas Sales Agreement in place. KN field anticipated to contribute revenue additions of $2.5 million in 2016/2017.

Production should increase to 500 BOED with revenue lifting to over $4 million pa.

5

Bounty Oil & Gas NL – Additional Oil Production Base

Bounty has increased its exposure to operated low risk oil Australian appraisal and development projects for 2017 and beyond. Has acquired controlling interest in development/appraisal targets:-

Bounty has now gained 100% control of PL 2 Alton – Surat Basin, and 82% of outer PL2 Kooroon JV Block – will place Alton wells on stream with EOR and drill Eluanbrook 2 an updip appraisal of the Eluanbrook 1 oil and gas well.

Bounty reviewing possible increase to interests in Rough Range (proven oil and new prospects with ~500,000+ bbl potential).

6

Bounty Oil & Gas NL – Growth Projects

Major Growth Projects:-

Australia – Oil: AC/ P 32 Azalea: 500 MMBBL target Permit in good standing until 2017 with farmout efforts continuing as E&P projects under pressure.

Tanzania Gas: As production revenue accrues in Tanzania Bounty will participate in Significant 3D Seismic Surveys to image 1 – 2.3 TCF gas plays in the east Nyuni PSA.

7

What we are Going to Discuss

Corporate • Financials • Projects

Production, Development and Appraisal • Production • Development/Appraisal

Rough Range • Existing Pools • Near Field Exploration

Growth • AC/P 32 • Nyuni (Tanzania) Deepwater Exploration

8

Corporate and Financials

• Current cash at 30/06/2016: $1.76 million • Current assets: $1.99 million • Balance sheet underpinned by conservatively valued reserves/resources • Many projects in the pipeline

ASX Code BUY

As at 1 August -16

52 Week Price Range $0.007 to $0.014

Shares Quoted 953,400,982

Options all series Nil

ASX Closing Price $0.010

Market Capitalisation $9 million

Net Assets as at 30 June 2015

$22.72 million

9

Projects

• Production: Oil and Gas sales now $1.35 million pa and will lift to +$4 million pa in 2017.

• Core Development/Appraisal and Exploration: PL2 Alton (Surat Basin QLD), Rough Range (WA) newly identified upside to known pools, Cooper (QLD) near field and oil behind pipe opportunities

• High Impact Exploration: targeting company-maker projects in Australia and Africa

Bounty’s Threefold Strategy

10

Production – Naccowlah (BUY 2%)

0.005.00

10.0015.0020.0025.0030.0035.0040.0045.0050.00

Jul-1

4

Aug-

14

Sep-

14

Oct

-14

Nov

-14

Dec-

14

Jan-

15

Feb-

15

Mar

-15

Apr-

15

May

-15

Jun-

15

Jul-1

5

Naccowlah Production BUY Share bopdc

• In recent years additional production has been from new fields - Irtalie East, Cooroo North West and Watson West

• Additional near field exploration targets available in Watson/Wandilo Area

Production – in well optimisation and cost effective maintenance have maintained production at ~30-40 bopd so far in 2016

Optimisation on hold , declining oil prices have forced capital investment only in rapid pay back operations

BUY sees production remaining relatively steady in 2017/16

11

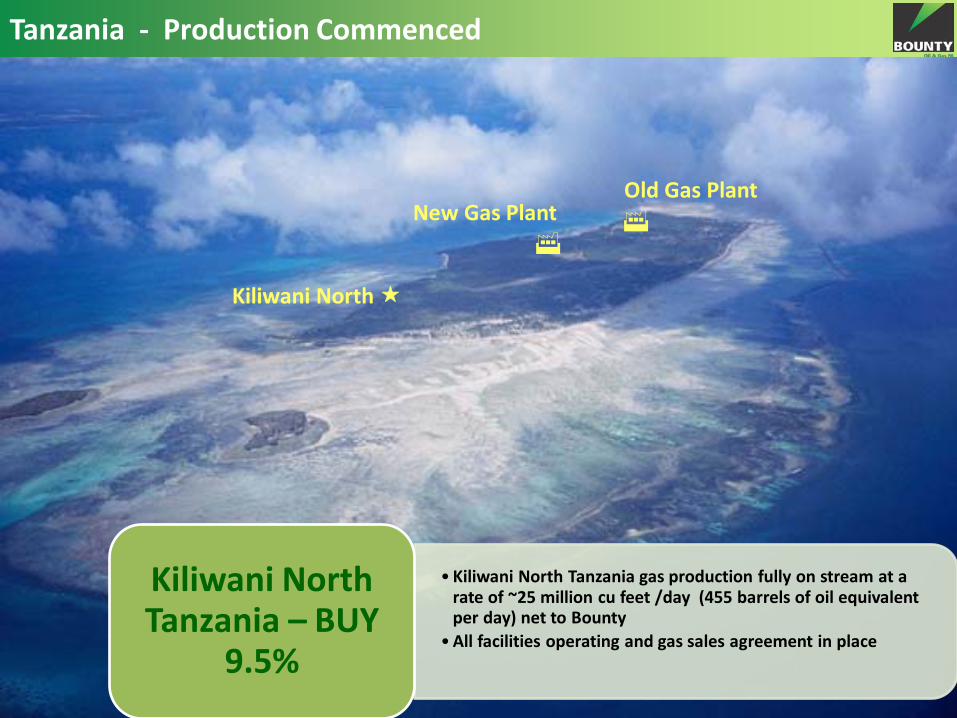

Tanzania - Production Commenced

Kiliwani North

• Kiliwani North Tanzania gas production fully on stream at a rate of ~25 million cu feet /day (455 barrels of oil equivalent per day) net to Bounty

• All facilities operating and gas sales agreement in place

Kiliwani North Tanzania – BUY

9.5%

New Gas Plant

Old Gas Plant

12

Tanzania Production - Kiliwani North Gas Field

Field pipeline connected and on stream. Metering equipment in place. The field contains ~44 BCF in place of which it is estimated 28 BCF (2.8 BCF net to BUY) is recoverable Initial production slated at 25 MMcf/day. Full commissioning due to occur on 30 July 2016.

Connecting Gas Pipeline to Project

13

Oil appraisal - PL2 Alton

Bounty has sold PL214 Utopia and acquired full control of PL2 Alton Oilfield. It also holds

50% of the surrounding ATP754P.

14

Oil appraisal - PL2 Alton Oilfield History

Discovered in August 1964 by Union Oil

15

Oil appraisal - PL2 Alton Regional Location

Cabawin

Denison

Alton Moonie

Cooper Basin Roma

16

Oil appraisal - PL2 Alton Oilfield General

Alton PL2: 100% Bounty Oil & Gas

Asset acquired in 2016 from Bridgeport Energy ex Santos

Mature field developed by 10 wells

Produced 2 mill bbls light oil

All wells were on Beam Pump

Located 370km west of Brisbane

Approx. 90km from Moonie

Surat/Bowen Basin: Early Jurassic Evergreen Formation

As operator Bounty will move to very low cost production using PL46 Facilities

17

PL2 Alton 2008 Reserves Review *

1P 2P 3P

OOIP (MMbbls) 10.106 12.173 14.408

EUR (MMbbls) 3.032 3.165 3.314

RF (%) 30% 26% 23%

Cumulative Production (MMbbls)

2.029 2.029 2.029

Reserves (MMbbls) 1.003 1.136 1.285

1P 2P 3P

OOIP (MMbbls) 10.106 12.173 14.408

EUR (MMbbls) 3.032 3.165 3.314

RF (%) 30% 26% 23%

Cumulative Production (MMbbls)

2.029 2.029 2.029

Reserves (MMbbls) 1.003 1.136 1.285

*Santos Limited Parameters based on “Production Enhancement Evaluation Study of the Alton Field,” Halliburton 1998. Additional volumes added after drilling of Alton 7 in western part of the field.

18

PL2 Alton Field Infill Opportunites

Well cost ~ $2,000,000 - Drill, complete, connect

Well Cost ~ 40 mbbls P10 Volume – 1908 mbbls

- P90 Volume – 523 mbbls - Pmean – 1183 mbbls

5 Opportunities Multiple sand

targets

ALTON FIELD

149 21 00E 149 22 00E 149 23 00E

27 5

7 00

S27

56

00S

730000M E 732000M E 734000M E

6906

000M

N69

0800

0M N

149 20 00E 149 23 42E

27 5

7 59

S27

55

09S

0 1 2

KILOMETRES

1875

1900

1900

1900

0091

0091

1900

5291

1925

1925

52915291

1950

1950

0591

5791

5791

80-11

80-7

80-8

S86-F

04

MS8

7-01

MS8

7-03

MS8

7-11

MS87-22MS87-24

MS87-42

MS87-44

MS87-46

MS87-48

MS87-50

MS87-52

SUSN

07-02

SUSN

07-0

3

SUSN

07-0

4

SN07-07

SN07-09

SN07-10

SN07-11

AW07-07

MS8

7-13

SUSN

07-02

SUSN

07-0

3

SUSN

07-0

4

SN07-07

SN07-09

SN07-10

SN07-11

AW07-07

Depth

met

res

SRD

1870

1997

188018901900191019201930194019501960197019801990

Lower Evergreen FmnDepth Structure Map

Alton AAlton B

Alton C

Alton D

Alton E

Sharon Langston 12/2/08

ALTON 1

2

3

4

5

6

7

8

910

Boxvale SandstoneOOIP (mbbls) 11,395RF 0.25Ultimate Recovery 3,127Cumulative Production 1,765Reserves (mbbls) 1,362

Basal Evergreen/PrecipiceOOIP (mbbls) 3,013RF 0.25Ultimate Recovery 807Cumulative Production 261Reserves (mbbls) 546

TotalOOIP (mbbls) 14,408RF 0.25Ultimate Recovery 3,934Cumulative Production 2,026Reserves (mbbls) 1,908

2008 Review - P10

“Alton Field PL2 Opportunities” April 2008

Opportunities scoped for potential farmout

19

Appraisal - PL 2A and 2B Kooroon Block other targets

In Eluanbrook 1 (drilled 1985) the perforations straddled OWC.

BUY targeting the better reservoir up dip above OWC.

P50 (probabilistic) estimate of recoverable oil is 22,000 bbls with an upside of ~600,000 bbls. Well depth to target 2000 m.

In addition to Alton Field Bounty has acquired 82% control of Block 2A and 2B Kooroon JV within PL2 and is operator

Other significant targets at Alton South East

20

Appraisal - PL2 Eluanbrook Opportunity

Louise Oil Field

Alton Oil Field

Updip Eluanbrook

Prospect

Fairymount Field

• Up-dip Eluanbrook is an appraisal opportunity targeting the proven oil accumulation of the Showgrounds Sst and testing the Evergreen Fmn.

• The prospect is located between Alton and Louise fields and is on trend with these and Fairymount fields.

• Eluanbrook 1 DST flowed gas to surface in 9 minutes and recovered 19 bbls oil from the Showgrounds Fmn.

• Mapping post 2007 seismic indicates Eluanbrook 1 is down dip on structure and was possibly outside of closure as an Evergreen sand reservoir target.

• POTENTIAL RESERVES – 2270 mbbls - P10

untruncated (Showgrounds Sst)

– Pg = 67% – 1460 mbbls – P10

untruncated (Evergreen Fmn)

– Pg = 53% – Key Risk: Reservoir

21

Rough Range WA

• Recent work by BUY has indicated the possibility of significant upside to a proven oil pool in PL L16 in which BUY already has a 10% Interest

• The same study has also identified an untested prospect in which BUY has a 10% interest with potential for a substantial oil pool

• Pools near Rough Range Field have remaining recoverable oil and production facilities.

BUY currently 10% - Considering additional equity

Rough Range from the East

22

Rough Range 1 and 1A Australia's first Oil Discovery

Oil in RR #1 1953

Rough Range 1A Christmas Tree - 1955

23

Rough Range 1B – mid 2000’s

• On site is the bulk of the production facilities to produce some of the other pools in the project area.

• The Rough Range Field suspended production at the end of 2007 , having produced 78,753 bbls of 38o API waxy crude

Established Infrastructure

24

Rough Range Opportunities

• Roberts Hill 1 well is cased to the bottom, and the pool has recoverable oil in the region of 16-24,000 bbls

• Parrot Hill pool appears on re-examination to be much larger than previously thought, the uncertainty is due to poor seismic imaging over the crest of the structure

• The Rough Range Oilfield requires additional study

• Further south is the Rough Range South B structure which has very similar size and structural characteristics to the Parrot Hill oil pool and is undrilled

• Bounty is looking at alternative ways to resolve the seismic mapping challenges at Rough Range aimed at gathering low cost production

• Bounty considering acquisition of additional interests and operatorship in this area.

25

AC/P 32 (BUY 100%) Azalea Prospect Overview - Timor Sea Regional Setting

AC/P 32 is located in the Vulcan Graben, Ashmore and Cartier Territory

Surrounded by oil fields and numerous wells with good shows and Azalea volumes match province field size distribution

Puffin, Skua, Swallow and Swift all have oil in the Puffin Sand

Azalea lies up dip from proven oil in Birch 1

26

AC/P 32 Timor Sea - Azalea Prospect Overview

Bounty has successfully delineated and de-risked the Azalea Prospect , ready for farmout

Azalea contains potential 500 million barrels of oil (MMbo) in place in the Puffin Sand reservoir up dip from proven oil in the well Birch 1

Bounty conservatively estimates that 100 MMbo are recoverable, making this one of the largest undrilled potential oil pools in the Timor Sea

Azalea Prospect is anticipated to be in excellent, high porosity and permeability sands of Puffin Formation and is located at 1800 metres depth in shallow water suitable for a jack up type rig

27

AC/P 32 Azalea Prospect Overview - Path to Development

Successful 100 plus million bbl oil discovery and appraisal via a two well farmout strategy of say 49% will provide a major multiplier to Bounty’s current

share price

Excellent development infrastructure in Timor Sea region

Standard FPSO development scenario and access to Singapore refineries

28

Tanzania - Regional Setting

Deep water offshore Tanzania and Mozambique has seen over 170 TCF of gas discoveries in deep water channel/fan systems related to the Rufiji and Ruvuma Deltas

Major players such as Exxon Mobil, Statoil, BG, Anadarko and ENI all have major discoveries

Drilling strike rate very high, only one or two dry holes, due to relative ease of identifying gas with modern 3D seismic

3D seismic in the Ophir/RAKGas permit which adjoins Bounty’s Nyuni PSA has identified several leads (green on the adjacent picture) some of which continue into the Nyuni PSA.

Targeting of over 2 TCF gas

29

Early Cretaceous channels are clearly visible on legacy seismic with anomalous amplitudes and possible flat spots directly up dip from the Chewa and Preza gas fields.

Anomalous amplitudes are also observed in the overlying Eocene age rocks

The 3D seismic will investigate this anomaly and others identified from the current sparse seismic coverage

Targets in the 1-2.3 TCF range are indicated. Only 20km from the new gas Infrastructure on Songo Songo Island

Nyuni Deep WaterExploration (BUY 5%)

30

Bounty 2017 Summary

Adding material revenues through new gas production in Tanzania and Rebuilding oil

revenue by appraisal/development work in Surat Basin and potentially Rough Range

Pursuing 100 – 200 MMbo recoverable oil play at Azalea Prospect (AC/P 32)

Commencing deepwater gas exploration for 1-2 TCF targets adjacent to new gas infrastructure

in Nyuni (Tanzania) with possible direct hydrocarbon indications (seismic gas

anomalies) in legacy seismic