book fao, farm_management

TRANSCRIPT

About the Farm Management Field Guide

About the Farm Management Field Guide The National Project Coordinator, Lamipeti Havea, and the FAO Consultant Euan Flemming developed a field manual for the use by Future Farmer Groups in the period September to November 2003. The manual is for use in the decentralized workshops for training farmers in farm management, conducting demonstrations and developing. The material presented at the Training of Trainers Workshop is being supplemented by additional material developed during the field trips we conducted in the final two weeks of my visit. The manual contains 11 modules that are closely based on material in the FAO Analytical Toolbox that is currently being prepared for publication. It also makes use of the material in the Farm Management Manual published by the Ministry of Agriculture, Forestry and Food (2000). The modules are:

1. Farming systems in Tonga; 2. Farm records; 3. Preparing background information on farm enterprises; 4. Calculating enterprise gross margin analysis; 5. Partial budgeting; 6. Scheduling labour activities; 7. Cash-flow budgeting; 8. Demonstrations; 9. Contract farming; 10. Whole-farm planning; 11. Participatory rural appraisal methods.

Each module commences with an introductory page that sets the scene and goals, prescribes expected outcomes and suggested duration of the session, and details the methods to be taught and outputs to be achieved by trainees. This page is followed by a mini lecture covering the concepts and material to be learnt and an example applying the method. The mini lecture section is kept brief and simple. The main part of the module is a set of exercises for small groups. Most exercises are based on four case studies that reflect different degrees of commercialization and intercropping arrangements in Tongan agriculture. These case studies are taken from examples of farming systems that are described in the second module of the manual:

1. Predominantly subsistence paper mulberry-based farming system, typical of smallholder agriculture in Ha’apai.

2. Semi-subsistence root crops-based farming system with some vegetables sold in the local market.

3. Predominantly commercial vanilla-based farming system intercropped with subsistence and commercial root crops and vegetables.

4. Predominantly commercial squash-based farming system, intercropped with kava and root crops.

The Farm Management Training Manual 1

Module 1: Farming Systems in Tonga

Module 1

Farming Systems in

Tonga

The Farm Management Training Manual 2

Module 1: Farming Systems in Tonga

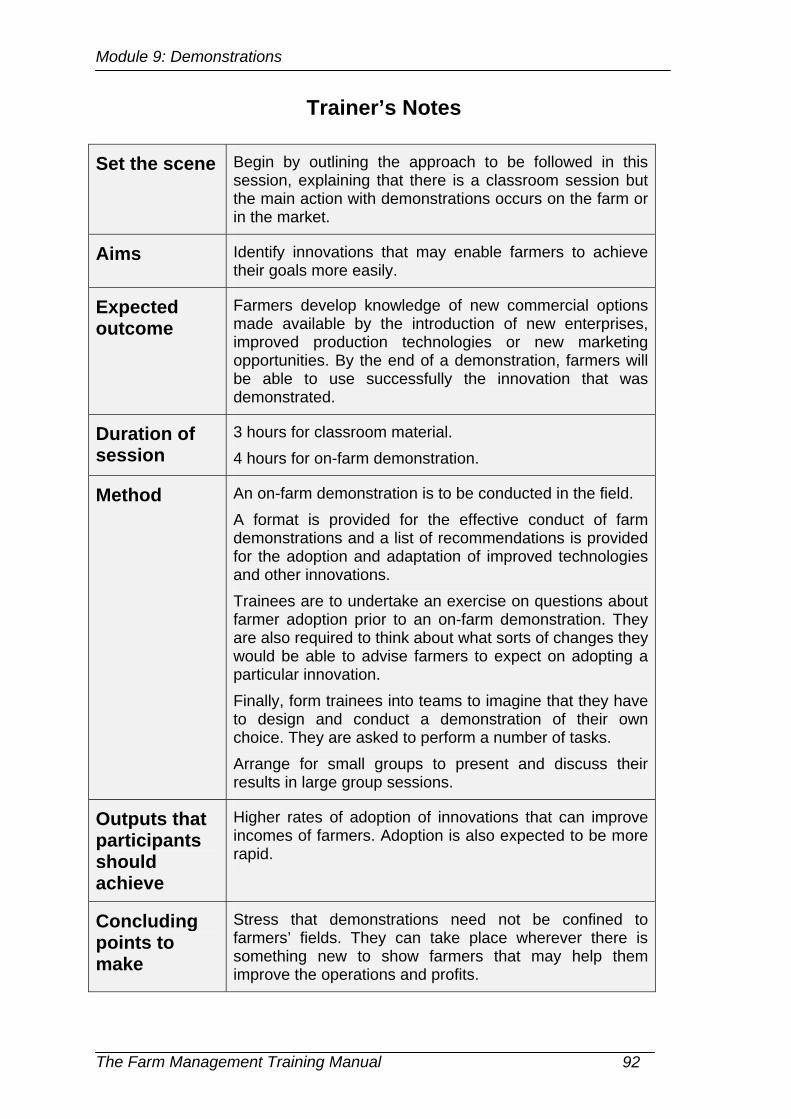

Trainer’s Notes

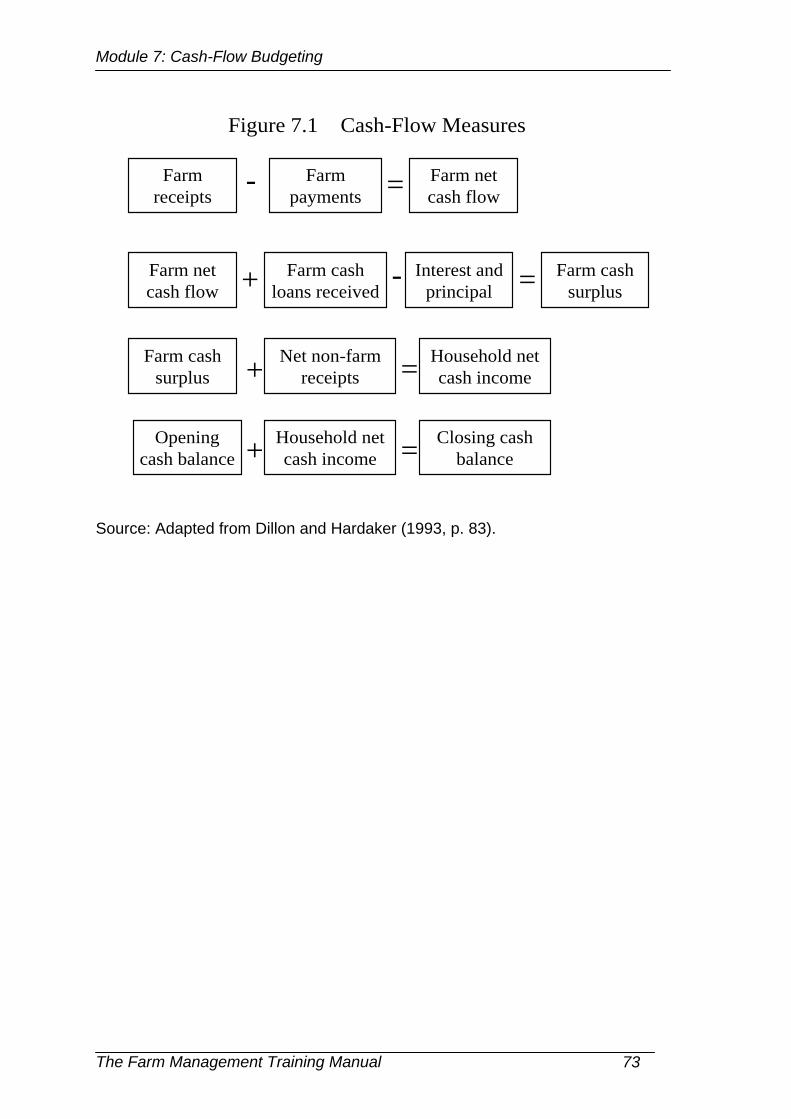

Set the scene Identifying a farming system that suits a farmer's circumstances is the crucial first step in farm management.

Aims To have knowledge of some common farming systems in Tonga, and to be aware of their attributes and relations between enterprises within each system.

Expected outcome

Farmers are expected to be able to identify and adopt farming systems that suit their particular circumstances, and to exploit complementarities and minimise competition and harmful interactions between enterprises in their adopted system.

Duration of session

3 hours.

Method Farming systems research and development. Some examples are provided of common farming systems in Tonga. In a small group exercise, trainees are to construct and describe a farming system that is different from the examples provided. Arrange for these small groups to present and discuss their results in a large group session.

Outputs that participants should achieve

Description of selected farming systems. Farm map. Seasonal calendars to show enterprise relationships.

Concluding points to make

The description of farming systems needs continual updating as new possibilities emerge for combining enterprises and using inputs.

Additional reading

MAFF (2000, pp. 69-72). Dillon and Hardaker (1993, pp. 2-4).

The Farm Management Training Manual 3

Module 1: Farming Systems in Tonga

Mini Lecture

Intercropping in Farming Systems

According to MAFF (2000, p. 69):

The traditional agricultural systems of Tonga involve intercropping with various crop sequences, and also incorporate fallow periods. These systems developed to ensure a stable and productive environment on farms.

Advantages of intercropping cited by MAFF (2000, p. 69) include:

a) less insect and pest damage

b) more efficient utilization of sunlight

c) higher biomass production per area

d) better protection from rain and wind damage

e) more mulch and less weeds

f) high diversity of outputs

g) higher security of yields and returns.

MAFF (2000, p. 69) warned of the dangers of losing these advantages by

recent trends towards machinery use, monocropping and reduced fallow

periods. These trends are closely associated with the growing

commercialization of farming operations.

Types of Farming Systems

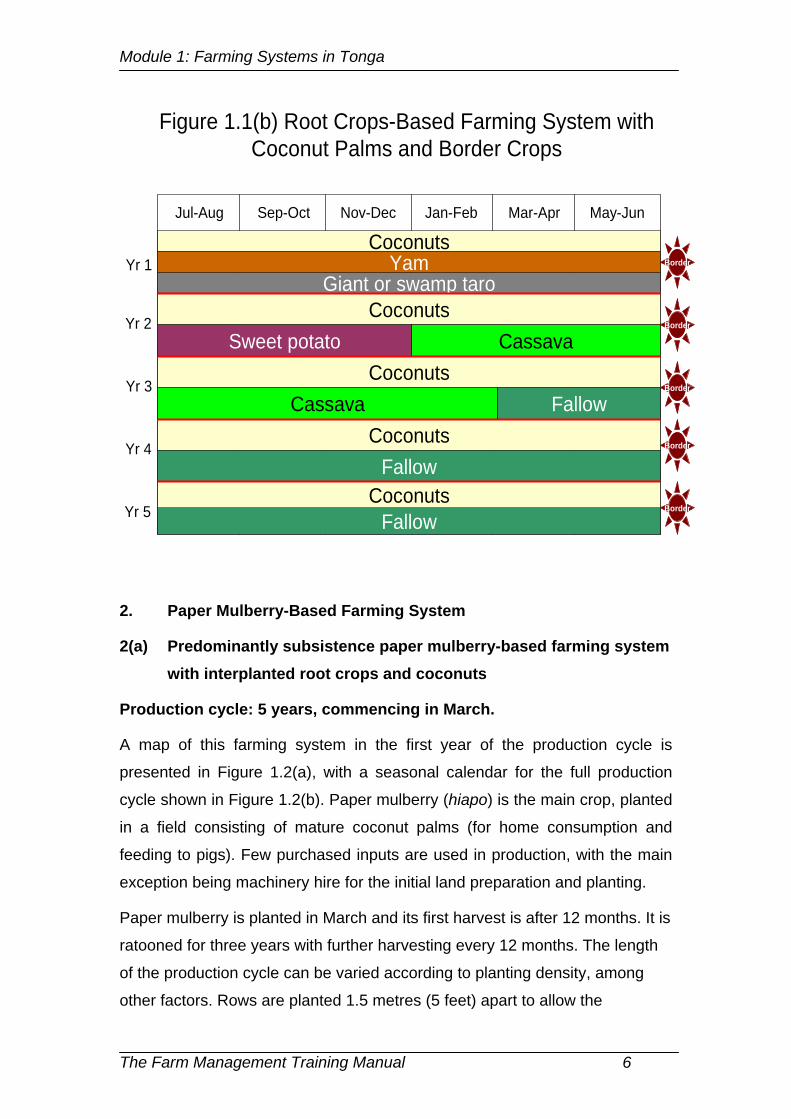

1. Predominantly subsistence root crops-based farming system

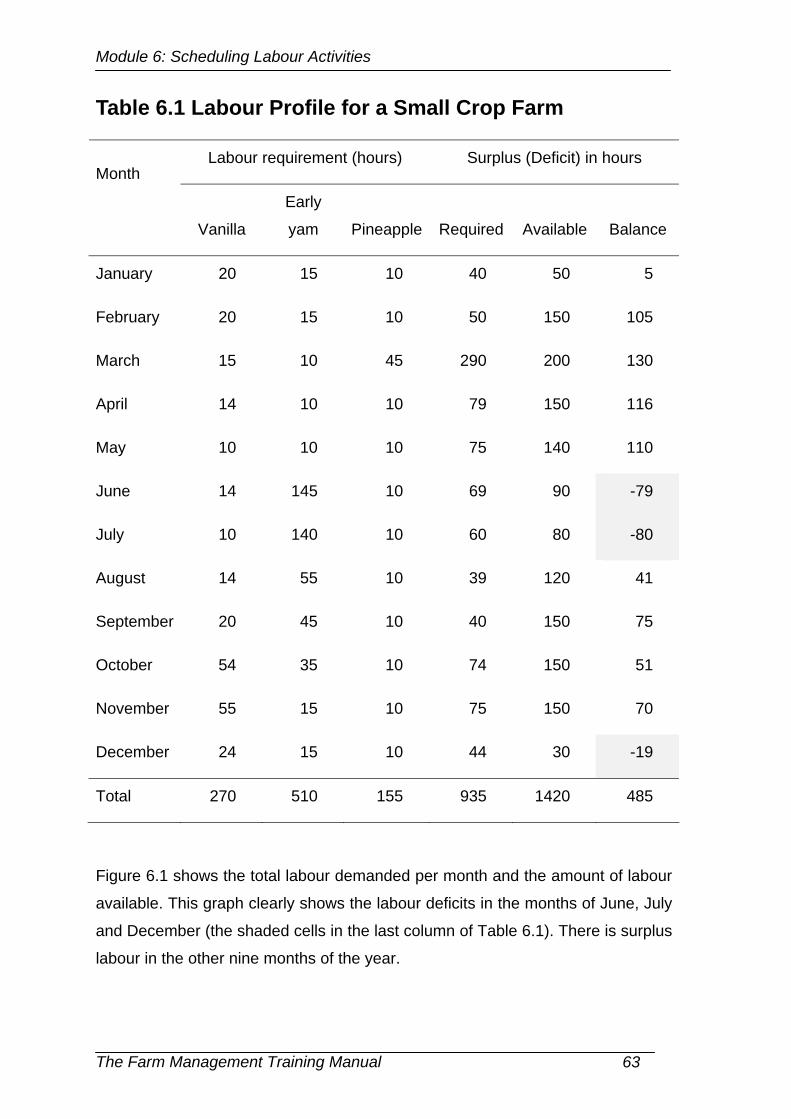

Length of the production cycle: 5 years, commencing in July.

A farm map for this farming system for the first year of the production cycle is

shown in Figure 1.1(a) and the seasonal calendar for the full production cycle

is presented in Figure 1.1(b). Few purchased inputs other than machinery hire

are used to produce these crops and there is a heavy reliance on family

labour. Consumption of produce is mainly within the household, with some

coconuts fed to scavenging animals.

The Farm Management Training Manual 4

Module 1: Farming Systems in Tonga

Yam ('ufi) is initially inter-planted with either giant taro (kape) or swamp taro

(talo tonga) and some coconut palms, and with a border of plantain (hopa or

pata). The ensuing short-term crops are typically sweet potato (kumala) and

cassava (manioke), and there is quite a lengthy fallow. This farming system is

likely also to have occasional breadfruit (mei) and mango trees.

Planting of main-season yam and taro commences in July. The yam is

harvested from April to June in the next calendar year, to be followed by a

crop of sweet potato in July that is harvested in November and December.

Cassava is planted in November and December for harvesting the following

December until February. A final ratoon of the plantain border crop is made in

the fifth year of the production cycle. The ground is then left fallow for the next

two years and four months.

Figure 1.1(a) Map of a Root Crops-Based Predominantly Subsistence Farming System: First Year

Coconut palmYamTaro Plantain Mango/Breadfruit

The Farm Management Training Manual 5

Module 1: Farming Systems in Tonga

Figure 1.1(b) Root Crops-Based Farming System with Coconut Palms and Border Crops

Mar-Apr May-JunJul-Aug Sep-Oct Nov-Dec Jan-Feb

Coconuts

Giant or swamp taro

Yr 5

Yr 3

Yr 2

Yr 1

Coconuts

Fallow

Yr 4

Yam

Sweet potatoCoconuts

Coconuts

CassavaCoconuts

Fallow

Fallow

Cassava

Border

Border

Border

Border

Border

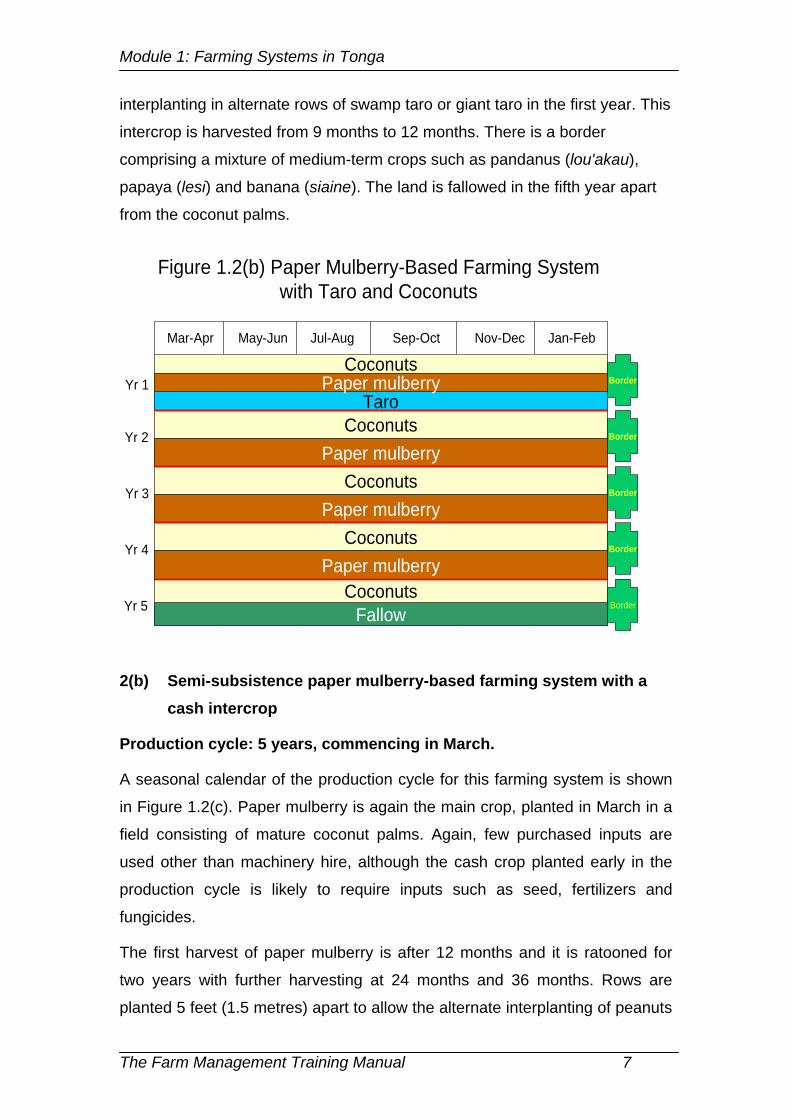

2. Paper Mulberry-Based Farming System

2(a) Predominantly subsistence paper mulberry-based farming system with interplanted root crops and coconuts

Production cycle: 5 years, commencing in March.

A map of this farming system in the first year of the production cycle is

presented in Figure 1.2(a), with a seasonal calendar for the full production

cycle shown in Figure 1.2(b). Paper mulberry (hiapo) is the main crop, planted

in a field consisting of mature coconut palms (for home consumption and

feeding to pigs). Few purchased inputs are used in production, with the main

exception being machinery hire for the initial land preparation and planting.

Paper mulberry is planted in March and its first harvest is after 12 months. It is

ratooned for three years with further harvesting every 12 months. The length

of the production cycle can be varied according to planting density, among

other factors. Rows are planted 1.5 metres (5 feet) apart to allow the

The Farm Management Training Manual 6

Module 1: Farming Systems in Tonga

interplanting in alternate rows of swamp taro or giant taro in the first year. This

intercrop is harvested from 9 months to 12 months. There is a border

comprising a mixture of medium-term crops such as pandanus (lou'akau),

papaya (lesi) and banana (siaine). The land is fallowed in the fifth year apart

from the coconut palms.

Figure 1.2(b) Paper Mulberry-Based Farming System with Taro and Coconuts

Mar-Apr May-Jun Jul-Aug Sep-Oct Nov-Dec Jan-Feb

Coconuts

Taro

Yr 5

Yr 3

Yr 2

Yr 1

Coconuts

Fallow

Yr 4

Paper mulberry

Paper mulberryCoconuts

Coconuts

Paper mulberryCoconuts

Paper mulberry

Border

Border

Border

Border

Border

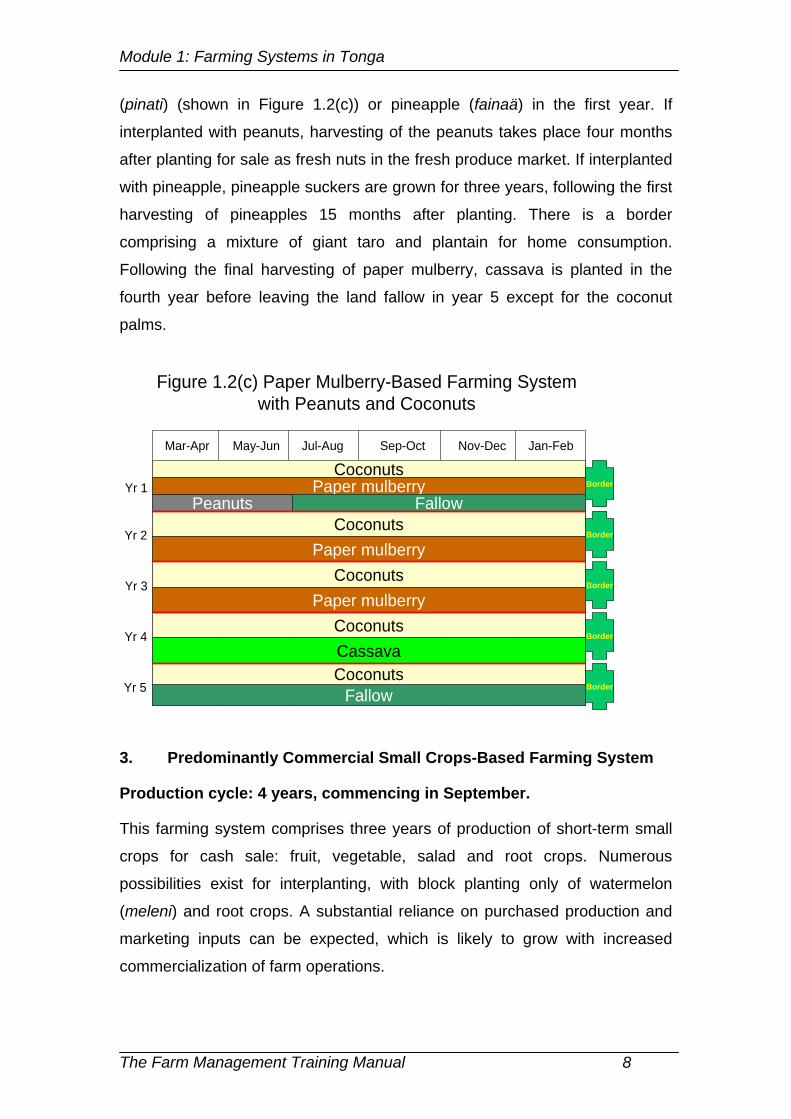

2(b) Semi-subsistence paper mulberry-based farming system with a cash intercrop

Production cycle: 5 years, commencing in March.

A seasonal calendar of the production cycle for this farming system is shown

in Figure 1.2(c). Paper mulberry is again the main crop, planted in March in a

field consisting of mature coconut palms. Again, few purchased inputs are

used other than machinery hire, although the cash crop planted early in the

production cycle is likely to require inputs such as seed, fertilizers and

fungicides.

The first harvest of paper mulberry is after 12 months and it is ratooned for

two years with further harvesting at 24 months and 36 months. Rows are

planted 5 feet (1.5 metres) apart to allow the alternate interplanting of peanuts

The Farm Management Training Manual 7

Module 1: Farming Systems in Tonga

(pinati) (shown in Figure 1.2(c)) or pineapple (fainaä) in the first year. If

interplanted with peanuts, harvesting of the peanuts takes place four months

after planting for sale as fresh nuts in the fresh produce market. If interplanted

with pineapple, pineapple suckers are grown for three years, following the first

harvesting of pineapples 15 months after planting. There is a border

comprising a mixture of giant taro and plantain for home consumption.

Following the final harvesting of paper mulberry, cassava is planted in the

fourth year before leaving the land fallow in year 5 except for the coconut

palms.

Figure 1.2(c) Paper Mulberry-Based Farming System with Peanuts and Coconuts

Mar-Apr May-Jun Jul-Aug Sep-Oct Nov-Dec Jan-Feb

Coconuts

Peanuts

Yr 5

Yr 3

Yr 2

Yr 1

Coconuts

Fallow

Yr 4

Paper mulberry

Paper mulberryCoconuts

Coconuts

Paper mulberryCoconutsCassava

FallowBorder

Border

Border

Border

Border

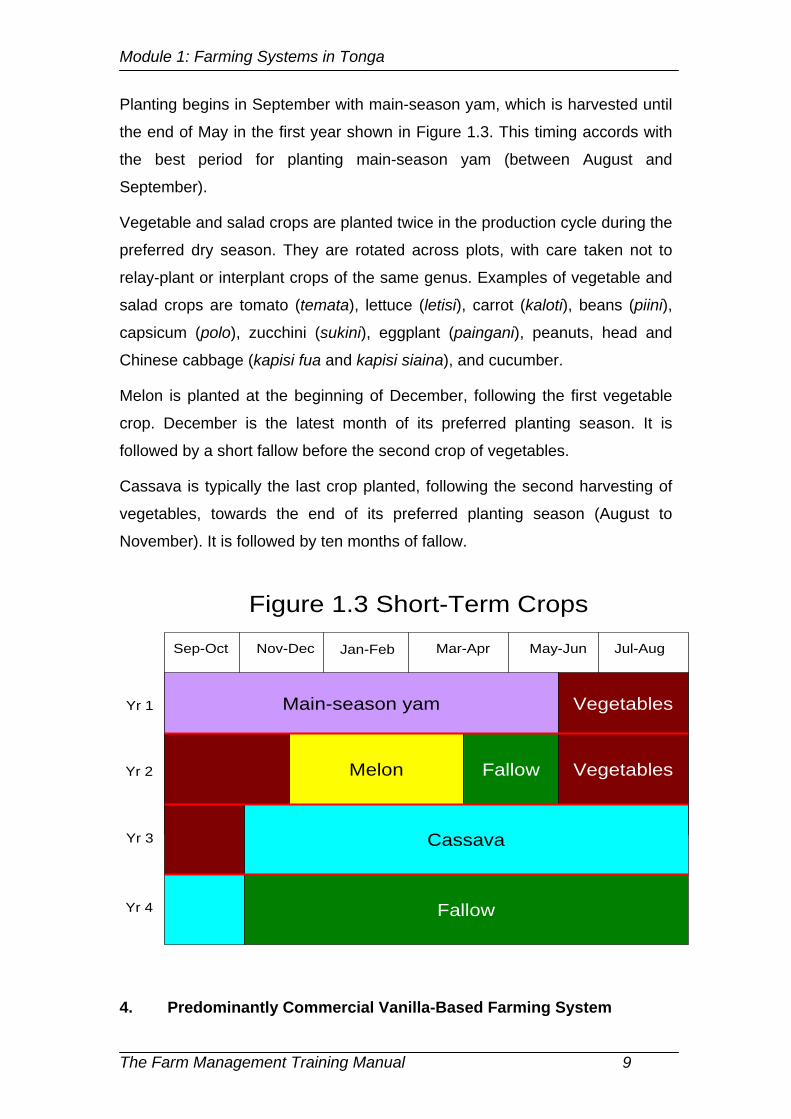

3. Predominantly Commercial Small Crops-Based Farming System

Production cycle: 4 years, commencing in September.

This farming system comprises three years of production of short-term small

crops for cash sale: fruit, vegetable, salad and root crops. Numerous

possibilities exist for interplanting, with block planting only of watermelon

(meleni) and root crops. A substantial reliance on purchased production and

marketing inputs can be expected, which is likely to grow with increased

commercialization of farm operations.

The Farm Management Training Manual 8

Module 1: Farming Systems in Tonga

Planting begins in September with main-season yam, which is harvested until

the end of May in the first year shown in Figure 1.3. This timing accords with

the best period for planting main-season yam (between August and

September).

Vegetable and salad crops are planted twice in the production cycle during the

preferred dry season. They are rotated across plots, with care taken not to

relay-plant or interplant crops of the same genus. Examples of vegetable and

salad crops are tomato (temata), lettuce (letisi), carrot (kaloti), beans (piini),

capsicum (polo), zucchini (sukini), eggplant (paingani), peanuts, head and

Chinese cabbage (kapisi fua and kapisi siaina), and cucumber.

Melon is planted at the beginning of December, following the first vegetable

crop. December is the latest month of its preferred planting season. It is

followed by a short fallow before the second crop of vegetables.

Cassava is typically the last crop planted, following the second harvesting of

vegetables, towards the end of its preferred planting season (August to

November). It is followed by ten months of fallow.

Figure 1.3 Short-Term Crops

Sep-Oct Nov-Dec Jan-Feb Mar-Apr May-Jun Jul-Aug

Melon

Yr 3

Yr 2

Yr 1 Main-season yam Vegetables

Cassava

Fallow Vegetables

FallowYr 4

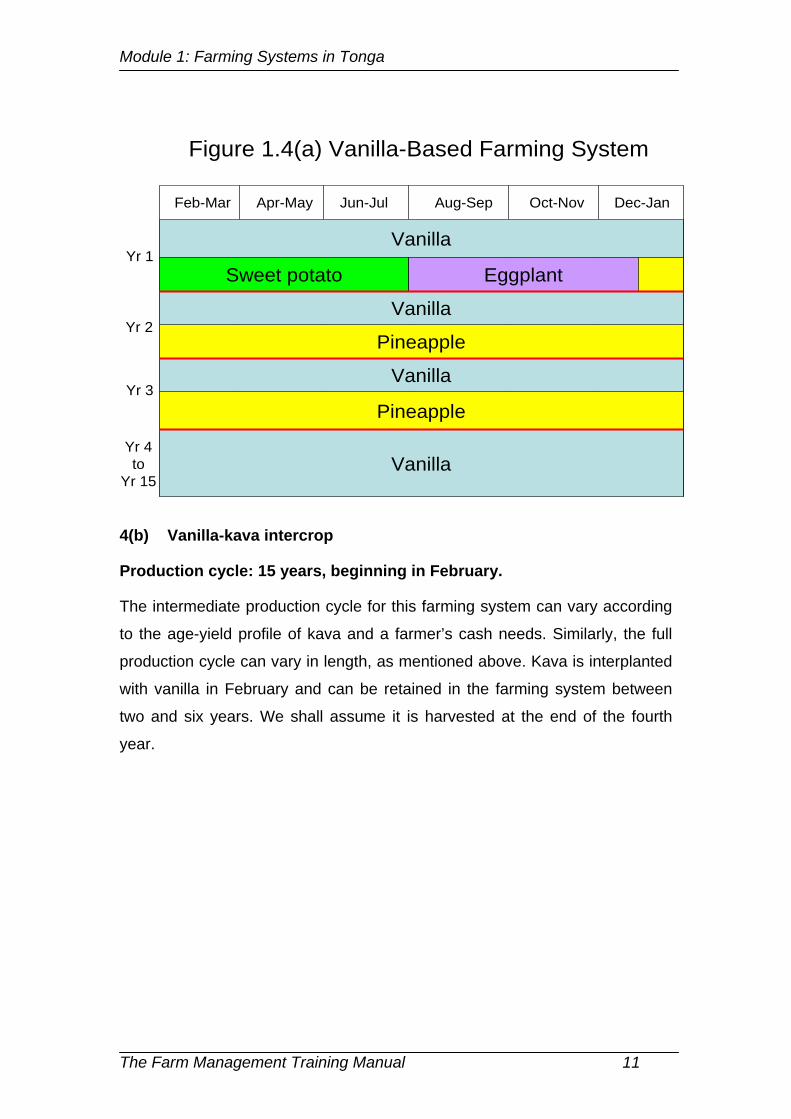

4. Predominantly Commercial Vanilla-Based Farming System

The Farm Management Training Manual 9

Module 1: Farming Systems in Tonga

Vanilla is intercropped in rows of 3 metres (10 feet) in a production cycle

lasting a period that is dictated by the length of productive life of the vanilla.

This period is assumed to be 15 years but could vary significantly from this

length according to economic circumstances and the age-yield profile of the

vanilla. Various intercropping options are available but we will consider two:

small crops and kava (kava tonga).

Interplanting is considered an important risk-management strategy because

fluctuating export prices can result in periods of low prices during which

growers are tempted to pull out the vanilla plants, as has happened in recent

years. Intercropping allows the grower to continue to maintain the plants

during these periods, while concentrating cash-earning efforts on the

intercrops, and take advantage of the upturn in export prices when it occurs.

Little is needed in the way of purchased inputs in vanilla production other than

the planting material. However, management and labour inputs are very

important to ensure a good-quality product with good yields.

4(a) Vanilla interplanted with small crops

Production cycle: 15 years, beginning in February.

Combinations of vegetable, salad and root crops are interplanted with vanilla

for the first three years of the production cycle, until the vanilla begins to yield

beans. The system consists of a vanilla monocrop for the remaining 12 years

of the cycle. Candidates among the small crops include those mentioned for

the third farming system above. Root crops that could be included are yam,

American and swamp taro, giant taro, cassava and sweet potato. Fiki trees

are planted to provide support and shade three to four months before planting

the vanilla in February, as shown in Figure 1.4(a). Sweet potato is planted

with the vanilla and is followed by a crop of eggplant from August to

December. Pineapples are planted at the end of the second year and

suckered in the third year. With wide plantings, intercrops can be reintroduced

in later years if vanilla prices fall.

The Farm Management Training Manual 10

Module 1: Farming Systems in Tonga

Figure 1.4(a) Vanilla-Based Farming System

Feb-Mar Apr-May Jun-Jul Aug-Sep Oct-Nov Dec-Jan

Vanilla

Sweet potato

Pineapple

Eggplant

Yr 4to

Yr 15

Yr 3

Yr 2

Yr 1

Vanilla

Pineapple

Vanilla

Vanilla

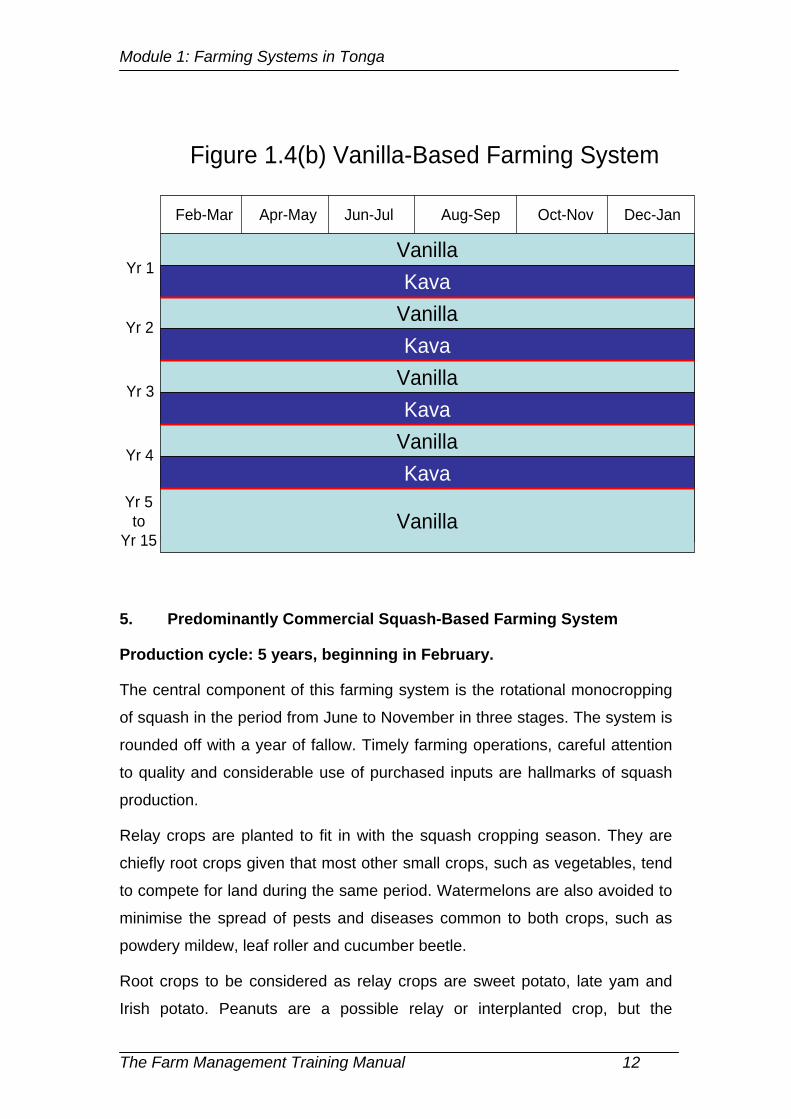

4(b) Vanilla-kava intercrop

Production cycle: 15 years, beginning in February.

The intermediate production cycle for this farming system can vary according

to the age-yield profile of kava and a farmer’s cash needs. Similarly, the full

production cycle can vary in length, as mentioned above. Kava is interplanted

with vanilla in February and can be retained in the farming system between

two and six years. We shall assume it is harvested at the end of the fourth

year.

The Farm Management Training Manual 11

Module 1: Farming Systems in Tonga

Figure 1.4(b) Vanilla-Based Farming System

Feb-Mar Apr-May Jun-Jul Aug-Sep Oct-Nov Dec-Jan

VanillaKava

Yr 5to

Yr 15

Yr 3

Yr 2

Yr 1

Vanilla

Vanilla

Vanilla

Kava

Kava

VanillaKava

Yr 4

5. Predominantly Commercial Squash-Based Farming System

Production cycle: 5 years, beginning in February.

The central component of this farming system is the rotational monocropping

of squash in the period from June to November in three stages. The system is

rounded off with a year of fallow. Timely farming operations, careful attention

to quality and considerable use of purchased inputs are hallmarks of squash

production.

Relay crops are planted to fit in with the squash cropping season. They are

chiefly root crops given that most other small crops, such as vegetables, tend

to compete for land during the same period. Watermelons are also avoided to

minimise the spread of pests and diseases common to both crops, such as

powdery mildew, leaf roller and cucumber beetle.

Root crops to be considered as relay crops are sweet potato, late yam and

Irish potato. Peanuts are a possible relay or interplanted crop, but the

The Farm Management Training Manual 12

Module 1: Farming Systems in Tonga

interplanting of small crops with squash is now uncommon. Only coconut

palms, mainly for domestic use and pig feed, tend to be used as a broad

intercrop with squash.

Figure 1.5 Squash-Based Farming System

Feb-Mar Apr-May Jun-Jul Aug-Sep Oct-Nov Dec-Jan

CassavaYr 3

Yr 2

Yr 1Yam Squash

Fallow

Cassava

Fallow

FallowYr 4

Yam SquashSquashYam

Yam

Yam Squash Sweet potato

Squash

SquashSquash

SquashSquash

CassavaFallow

CassavaTaro

Taro

Sweet potatoYam

Fallow

Yam

Fallow

YamYam

Sweet potato

FallowYr 5

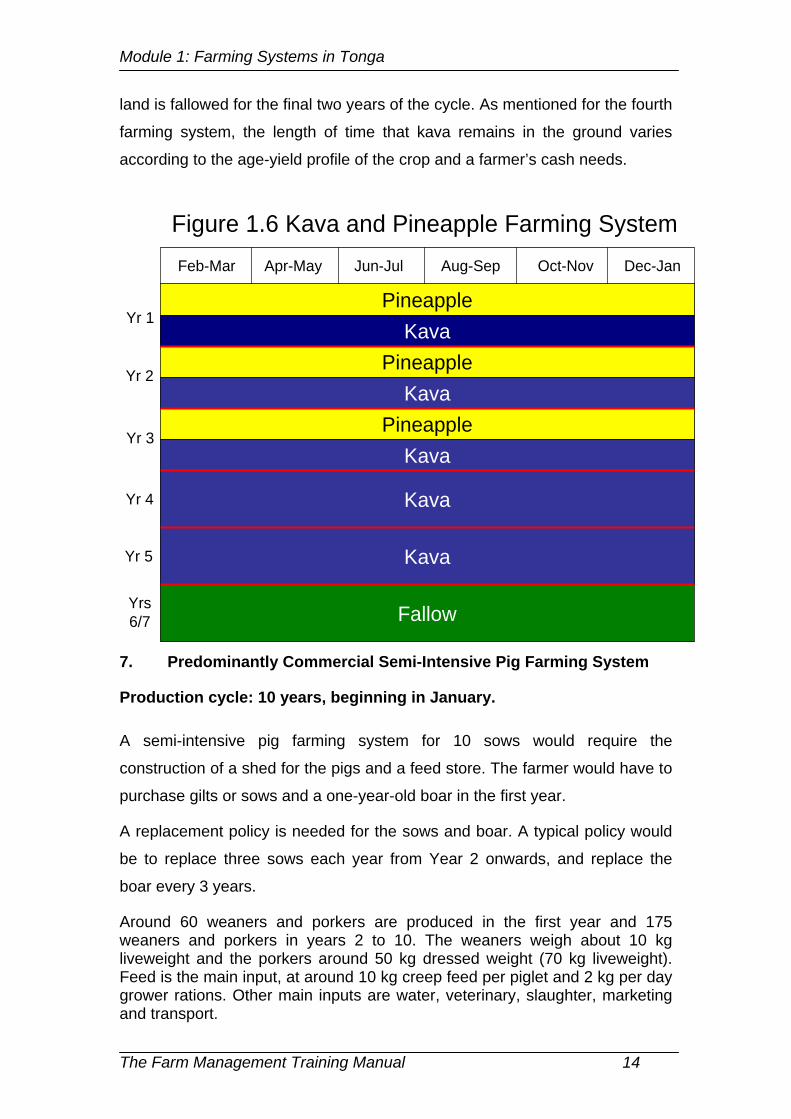

6. Predominantly Commercial Kava and Pineapple Farming System

Production cycle: 7 years, beginning in February.

The seasonal calendar for this farming system is shown in Figure 1.6.

Pineapples are interplanted with kava in alternate rows during the rainy

season. Kava requires few purchased inputs in production, with machinery

hire and seedlings the major items. The major cost is crushing the kava to

produce kava powder at a conversion rate from green kava to kava powder of

around 4:1. The chief purchased inputs for pineapples are suckers for planting

in the first year and fertilizer, and possibly herbicides but interplanting should

reduce the need for weeding.

The two crops are grown together for the first three years, which means there

are two pineapple suckerings. Kava is harvested at five years after which the

The Farm Management Training Manual 13

Module 1: Farming Systems in Tonga

land is fallowed for the final two years of the cycle. As mentioned for the fourth

farming system, the length of time that kava remains in the ground varies

according to the age-yield profile of the crop and a farmer’s cash needs.

Figure 1.6 Kava and Pineapple Farming SystemFeb-Mar Apr-May Jun-Jul Aug-Sep Oct-Nov Dec-Jan

PineappleKava

Yr 5

Yr 3

Yr 2

Yr 1

Pineapple

PineappleKava

Kava

Kava

Yr 4 Kava

Yrs 6/7 Fallow

7. Predominantly Commercial Semi-Intensive Pig Farming System

Production cycle: 10 years, beginning in January.

A semi-intensive pig farming system for 10 sows would require the

construction of a shed for the pigs and a feed store. The farmer would have to

purchase gilts or sows and a one-year-old boar in the first year.

A replacement policy is needed for the sows and boar. A typical policy would

be to replace three sows each year from Year 2 onwards, and replace the

boar every 3 years.

Around 60 weaners and porkers are produced in the first year and 175 weaners and porkers in years 2 to 10. The weaners weigh about 10 kg liveweight and the porkers around 50 kg dressed weight (70 kg liveweight). Feed is the main input, at around 10 kg creep feed per piglet and 2 kg per day grower rations. Other main inputs are water, veterinary, slaughter, marketing and transport.

The Farm Management Training Manual 14

Module 1: Farming Systems in Tonga

Small Group Exercise: Farming System

This exercise requires trainees to develop their own farming system for an 8-

acre farm, or part thereof, which is representative of Tongan agriculture. They

need to think about the complimentarily, competition and unsuitability between

enterprises.

Once the system has been defined for a production cycle, trainees are to

complete the following tasks:

1. Construct a farm map for the first year

Construct a seasonal calendar for the length of the production cycle.

The Farm Management Training Manual 15

Module 2: Keeping Farm Records

Module 2

Keeping Farm Records

The Farm Management Training Manual 16

Module 2: Keeping Farm Records

Trainer’s Notes

Set the scene A major obstacle to the use of farm management methods by smallholders in Tonga has been an absence of records on inputs used and their cost, and outputs obtained and the prices received for them. Encouragement of record-keeping can help to remove this obstacle.

Aim Identify farm records required for modern farm management.

Expected outcome

Farmers are expected to be able to enter basic farm records, and understand the importance of these records and how they are to be used to make farm management decisions.

Duration of session

3 hours.

Method Demonstrate the main forms needed and show how they are structured. Get trainees to form small groups and enter sample data that can be used in later sessions on budgeting. Arrange for these small groups to present and discuss their results in a large group session.

Outputs that participants should achieve

Plot history form. Form containing background information on an enterprise. Labour activity form. Input use form. Non-traded output and input price information form. Crops harvested and sold form. Cash book.

Concluding points to make

Farm records enable farmers to make better decisions, particularly when they are developing commercial activities. The number and complexity of the records depends on how commercialized the farmer is.

Additional reading

MAFF (2000). FAO (2004).

The Farm Management Training Manual 17

Module 2: Keeping Farm Records

Mini Lecture

Types of Information Requiring Records

A farmer needs to gather more information on becoming more involved in

commercial farming. The need to keep farm records increases as a result.

There are seven types of forms that a farmer may use to help make farm

management decisions.

Plot history form

Plot history forms are kept for each identifiable area of land owned by the

farmer. They should contain information on area, soil quality, drainage, slope,

erosion and other forms of degradation, fallow periods, crops grown and

livestock grazed on the plot, and past incidence of pests and diseases.

2. Form containing background information on an enterprise

Each of this type of form contains background information on an enterprise of

interest and use to the farmer. This information is updated for each production

cycle.

New background information is needed for new crops. Three examples follow

of background information on two new enterprises: capsicum and eggplant.

They are being considered by a farmer who, until now, has grown traditional

crops mainly for household consumption.

a) What is the export status of the two new crops?

Capsicums used to be a significant export to New Zealand prior to problems

faced by exporters some 15 years ago caused by fruit fly found in a

consignment of watermelons. The export of capsicums to New Zealand was

banned because capsicums are a potential fruit fly host. Vegetable exports

have since been reintroduced with the recent signing of a quarantine protocol

with New Zealand and the introduction of high-temperature forced-air (HTFA)

treatment of exported vegetables. However, capsicum exports have not yet

resumed because suitable HTFA treatment has not been available. Eggplant

has potential as an export crop. The farmer would need to know the export

status of products, how they should be presented for export and associated

costs, and marketing procedures needed to secure an export contract.

The Farm Management Training Manual 18

Module 2: Keeping Farm Records

b) Greater use of purchased inputs

Capsicums and eggplants both require more purchased inputs than the

traditional crops that the farmer is growing. The farmer would first need to

know what these inputs are. Examples are fertilizers, insecticides and

fungicides. He would also need to know how much to use, when and what the

cost would be.

c) Prices of new outputs produced

What price is the farmer going to receive for capsicums and eggplants sold in

the local market? Information is needed on local market prices for the crops

and any marketing costs incurred in getting produce to the market.

Alternatively, if the farmer expects to sell to a buyer who comes to the farm,

the farm-gate price must be known. Both are seasonal crops and so the

farmer would need to know how their prices are going to vary over the year.

Details on types of background information and for which enterprises are

provided in Module 3.

3. Labour activity form

A labour activity form contains information on the amount of labour used and

when, type of labour (hired or family, adult or child, male or female) and in

which enterprise it is used. Labour inputs would need to be split between the

enterprises involved where they are used on a plot with intercropping or mixed

cropping,. The information needs to be completed each time labour is used in

an enterprise. The use made of this information is shown in Module 6.

4. Input use form

This form contains information on the use of inputs other than labour. It should

contain information on how much of the input is used and when. This

information needs to be recorded on the form each time an input is used. It is

used when calculating gross margins in Module 4.

The Farm Management Training Manual 19

Module 2: Keeping Farm Records

5. Non-traded output and input price information form

Information on prices of non-traded outputs and inputs should be completed at

the end of each production cycle. The purpose of this form is to collect

information to value inputs and outputs for which no price information is

available. This information is also used to calculate gross margins in Module

4.

6. Crops harvested and sold form

This form contains two sets of information. The first set of information is on the

type of crop harvested, the number of units and the average weight of each

unit. The second set of information is on the number of units of the crop that

are sold, their average weight and the price received per unit for the produce

sold. Once again, this information is used to calculate gross margins in

Module 4.

7. Cash book

A seventh farm record that is important for keeping track of cash balances is a

cash book. This would contain some of the information collected on the forms

listed above. However, it also enables the farmer to estimate all non-farm

cash flows that need to be included in a cash flow budget. The preparation of

this budget is the subject of Module 7.

Examples of entries for the various forms described above are shown in the

exercise.

Source of information to be recorded

The farmer should be able to update the plot history information at the end of

each year. A map of the farm is helpful in dividing the farm into plots. MAFF

personnel should be able to help the farmer assess soil quality and identify

land problems such as erosion and pest and disease attacks that occur on

each plot.

The farmer is also the most likely source of background information on

enterprises, to be updated at the end of each year. The Farm Management

Manual (MAFF 2000) provides the farmer with general information on

The Farm Management Training Manual 20

Module 2: Keeping Farm Records

enterprises that can be adapted to suit circumstances on the farm. MAFF

should be able to provide updated market prices for products sold and costs

of the main inputs used, supplemented by cash book entries. It is desirable

that one family member takes responsibility for recording cash transactions on

a regular basis. Typical sources for entries are bank accounts, receipts and

invoices.

Individual family members can record on a regular basis the hours they work

on different enterprise and the quantities of inputs they used. The farmer

would normally be the person who keeps records on hired labour.

At the end of each production period, MAFF personnel should be able to

provide information on the range of prices of inputs and outputs that are not

traded by the farmer.

The Farm Management Training Manual 21

Module 2: Keeping Farm Records

Small Group Exercise: Keeping Records

This exercise requires trainees to enter a sample of different types of

information on appropriate farm record forms. First, some background

information is provided on crop production. The farm family consists of a

farmer, his wife and a son aged 16. The family has produced taro, bananas

and coconuts for a long time, and all family members know the production

practices well for these enterprises. Few purchased inputs are used on these

crops. The farmer has now decided to grow capsicum and eggplant that family

members sell in the local market and, hopefully at some stage, in the export

market.

During the year, the farmer produced 750 kg of capsicum from 0.3 acres,

1700 kg of eggplant from 0.2 acres, 2400 kg of first-ratoon bananas from 0.3

acres and 3200 kg of American taro from 0.8 acres. All of the capsicum and

eggplant, and 400 kg of bananas, were sold in the market. Coconut palms

produce 500 nuts per year. All taro and coconuts were consumed in the

household.

Labour activity form/Input use form

Examples follow of labour tasks and inputs used, to be entered on the

appropriate farm record forms. The entry for the first example needs special

consideration. There is usually a driver included with the hire of machinery but

the cost of providing the driver is included in the overall hiring cost. Therefore,

it is best to make a single entry as an input use rather than making separate

entries for input use and labour use.

• On 5 June 2003, the farmer hired machinery for two hours for

ploughing and disk harrowing to prepare half an acre for planting

capsicum and eggplant. The hire rate was T$40 per hour. (Assume that

1.2 hours are to be allocated to the capsicum enterprise and 0.8 hours

to the eggplant enterprise.)

• On 10 June, the farmer and his son took six hours between them to

broadcast 75 kg of NPK 8:33:18 and 200 kg of chicken manure over

the area to be planted to capsicum and eggplant. They lightly worked

The Farm Management Training Manual 22

Module 2: Keeping Farm Records

the fertilizer into the soil before planting. The chicken manure was not

purchased but obtained from relatives in the village.

• On 17 June, the farmer and his son spent six hours each planting a 20-

gram packet of capsicum seed.

• On 18 June, the farmer and his son spent three hours each planting

half a 20-gram packet of capsicum seed.

• On 19 June, the farmer and his son spent planted 50 grams of eggplant

seed, taking five hours each.

• On 7 July, the farmer’s wife spent 2 hours collecting mature coconuts.

• On 9 July, the farmer hired 1 hour of casual labour to harvest six

bunches of bananas. The labourer was paid T$5. The farmer’s wife

sold five of the bunches at the market on the next day, taking her six

hours and costing T$7 in marketing inputs.

• On 19 July, the farmer and his son applied 25 kg of urea along the

rows of eggplant and capsicum, taking two hours each.

• On 5 September, the farmer’s son spent two hours harvesting 50 kg of

capsicum.

• On 18 September, the farmer’s son spent an hour harvesting 60 kg of

eggplant.

• On 26 September, the farmer spent an hour harvesting a basket of

American taro.

Crops harvested and sold form

Examples follow of individual crops harvested and sold, to be entered on the

appropriate farm record form:

• Five bunches of bananas were sold on 10 July for T$0.60 per kg. One

remaining bunch was kept for consumption in the household and by

relatives. (Assume each bunch weighs 13 kg on average.)

The Farm Management Training Manual 23

Module 2: Keeping Farm Records

• On 7 July, four baskets of mature nuts were harvested for household

use. (Assume that one basket is equal to 15 kg and one nut is equal to

1.13 kg.)

• On 5 September, 50 kg of capsicum were harvested and sold for

T$2.30 per kg.

• An amount of 60 kg of eggplant was sold for T$1.80 per kg on 18

September.

• One basket of American taro was harvested on 26 September for home

use. (Assume that one basket weighs 15 kg.)

Non-traded input and output prices form

At year end, the following information on prices is to be recorded on the

appropriate farm record form for examples of non-traded inputs used and

outputs harvested:

• American taro prices per basket averaged T$8.55 during the year.

They varied from T$7.20 to T$10.20.

• Mature nuts had an average price of T$0.30 each during the year,

varying from a low of T$0.21 to a high of T$0.47.

• Family labour was valued at T$3.00 per hour throughout the year.

• Chicken manure was valued between T$3.50 per 50 kg bag and

T$5.00 per 50 kg bag during the year. The average price was T$4.00

per 50 kg bag.

Other cash transactions for entry in the cash book

Some cash book entries can already be made using the above information.

They are the hiring of labour for harvesting bananas, and the sales of

capsicum, eggplant and bananas. In addition, other entries are needed for the

following cash transactions:

• The following purchases of household goods were made: 6 May

T$41.50; 3 June T$54.20; 5 July T$38.60; 9 August T$31.30.

• 200 kg of NPK 8:33:18 were bought on 30 May for T$200.

The Farm Management Training Manual 24

Module 2: Keeping Farm Records

• On 8 June, purchases were made of two 20-gram packets of capsicum

seed, costing T$65 each, and two 25-gram packets of eggplant seed,

costing T$65 each.

• 100 kg of urea were bought on 10 July for T$90.

• Remittances of T$70 were received on 8 August.

Tasks

Enter the examples of cash transactions, labour activities, inputs, outputs, and

input and output prices on the farm record forms.

The Farm Management Training Manual 25

Module 4: Preparing Background Information on Enterprise

Module 3

Preparing Background

Information on

Enterprise

The Farm Management Training Manual 26

Module 4: Preparing Background Information on Enterprise

Trainer’s Notes

Set the scene Emphasize that all farm management decisions depend on an accurate knowledge of the physical and technical conditions on the farm. They also depend on a good knowledge of the markets in which products are sold.

Aims To enable farmer to have a thorough understanding of what they are capable of achieving with the resources they have.

Expected outcome

Farmers are expected to develop a good knowledge of what enterprise options they have available, and the different ways in which they can use their resources in these enterprises.

Duration of session

1.5 hours.

Method Material on the preparation of enterprise background information begins with an example of the yam enterprise. Trainees are then to form small groups and prepare background information on their own choice of enterprise, based on a checklist that is provided to them. Arrange for small groups to present and discuss their results in a large group session.

Outputs that participants should achieve

A set of enterprise background notes.

Concluding points to make

Stress the fact that these background notes are necessarily general, and need to be adjusted for specific circumstances.The notes also need to be updated regularly.

Additional reading

MAFF (2000). FAO (2004).

The Farm Management Training Manual 27

Module 4: Preparing Background Information on Enterprise

Mini Lecture

Accurate technical information about how farmers operate their enterprises is

the basis for any form of financial analysis in farm management.

The technical and financial information needed to make commercial farm

decisions takes many different forms. The best way to demonstrate this is to

use an example, and to have some practice at completing forms for different

enterprises in Tonga.

Consider the yam enterprise as an example. The following background

information is taken from the Farm Management Manual 2000 (MAFF 2000,

pp. 8-9).

2.1 YAMS

2.1.1 Introduction

Yams are one of the most important crops in Tonga; they are an essential

feast food and are traditionally given as gifts. They are also a valuable cash

crop for the domestic and export markets. In the 1993 Land Use and Crops

Survey, it was found that yams was grown by 83 percent of households

surveyed with 1489.5 acres of yam were grown yielding about 7346 tonnes of

tubers.

There are three types of yams grown in Tonga:

(a) Early yam: Scientific name - Dioscorea alata; Tongan name - 'ufi

tokamu'a;

(b) Late yam: Scientific name - Dioscorea alata; Tongan name - 'ufi

tokamui;

(c) Sweet yam: Scientific name - Dioscorea esculenta; Tongan

name - 'ufilei.

The Farm Management Training Manual 28

Module 4: Preparing Background Information on Enterprise

The early yams have long, thick tubers; late yams have smaller, spherical

tubers; and sweet yams are smallest and taste sweet. Yams are normally the

first crop to be planted after a fallow period.

2.1.2 Production notes

Climate: Requirements are at least 1500 mm of well-distributed rain per year,

and for high yields temperatures of 27-30°C are best. Yam requires day

length of less than 12 hours for tuberization.

Soil: Yam requires deep, loose, well-drained, deep, fertile loamy soils. Sweet

yams grow well in sandy soils.

Fertilizers: No fertilizers are required for fallowed land. In overcropped land,

use 15g each of urea and potash per hill. Do not band fertilizer, apply evenly

around the mound.

Propagation: Cuttings of large tubers, small whole tubers and aerial tubers

for some varieties are used for propagation. For early yams the average set

size is 0.67 kg and for late yams the average is 0.25 kg.

Planting: Three major planting times: early yams are planted from May to

July; main planting (ta’u lahi) – August to September; and late yams are

planted from October to December. Fill dug holes with topsoil. Place set on

the ground level, skin downward and the top end facing the side of the hole.

Cover set with soil to form a mound. Use one tuber piece per planting holes

for early yam. For late yam, use two sets if the using smaller size sets.

Planting density: Average planting densities for each type of yam are: Early

yam (1000-2300 plants/ac); Late yam (1300-2700 plants/ac); and sweet yam

(1700-2666 plants/ac). Orient row parallel to wind direction for quick drying to

reduce disease.

Intercropping: Yams are commonly grown as an intercrop with giant taro,

plantain or American taro.

Growth period: Early yams usually grow for 9 to 12 months and late yams

normally grow for 8 to 12 months. Sweet yams may remain in the ground for

more than one year.

The Farm Management Training Manual 29

Module 4: Preparing Background Information on Enterprise

Disease and pest control: Yams can be affected by insects such as the

rose beetle and caterpillars, and by land diseases such as seed piece rot,

yam tuber rot, anthracnose, and stem rot and leaf spot diseases. Nematodes:

Use fallowed land. Rose beetles and caterpillars: spray weekly with Sevin, 1

tablespoon per gallon. Anthracnose: use resistant varieties or spray fortnightly

yam either with Benlate, ½ tablespoon, or weekly with Mancozeb, 2

tablespoons, per 5 litres or spray them alternately to prevent anthracnose

developing resistance to Benlate. Tuber scales: dip for 10 minutes in

Perfekthion, 1 teaspoon per 5 litres. Tuber rots: dip sets for 10 minutes in

Benlate (½ tablespoon) or Mancozeb (1 tablespoon) plus Sevin (½

tablespoon) and Agral (1 teaspoon) per 5 litres. Sand and ash are used also.

Weeding: Hoe every two weeks. Hoeing during dry times provides a dry soil

mulch which reduces evaporation losses.

Storage: Yams store better than other root crops and can be kept for 3 to 6

months if kept in a well-ventilated cool store. Careful harvest and post-harvest

handling will also ensure longer storage life.

2.1.3 Marketing notes

Yams are the most expensive of the root crops. The average prices at Talamahu Market from 1994-1999 were early yam (T$1.97/kg); late yam (T$1.20/kg); and sweet yam (T$0.87/kg). About 361 tonnes of yams were exported annually during this period. 2.1.4 Economics of yam production

See budgets for the production of early, late and sweet yam on the following

pages.

The Farm Management Training Manual 30

Module 4: Preparing Background Information on Enterprise

Small Group Exercise: Preparation of Background Information for an Enterprise

The aim of the exercise on preparing background information for enterprises

is to enable trainees to understand what information they should collect in

order to make good decisions when managing the operations of that

enterprise. Arrange trainees into small groups and ask them to select a farm

enterprise. They are to provide background information on their selected

enterprise.

Separate checklists are provided below for background information on crop

and livestock enterprises. Depending on the nature of the enterprise,

additional headings might need to be added to the checklist and some of

those included might be ignored. No model answer is provided for this

exercise. Trainers can refer to MAFF (2000) for background information on

the enterprises that trainees choose.

Checklist for Background Information on a Crop Enterprise

1. Types/varieties

2. Production notes

Climatic suitability

Soil suitability

Fertilizer requirements

Propagation

Planting times

Planting methods

Planting density

Intercropping

Growth period

Disease and pest control

The Farm Management Training Manual 31

Module 4: Preparing Background Information on Enterprise

Weeding

Harvesting methods

Storage

Yields

3. Marketing notes

Marketing outlets

Transport needs

Packaging needs

Prices and price variability

Checklist for Livestock Enterprise Background Information

1. Reproduction

Breeds

Selection of breeding stock

Breeding/mating:

Weight of breeding stock at puberty

Age of breeding stock at puberty

Oestrus cycle

Heat period

Gestation period

Breeding interval

Offspring per breeding cycle

Birth weight of offspring

Mortality rate

Offspring weaned per breeding cycle

Offspring weaned per breeding stock per year

The Farm Management Training Manual 32

Module 4: Preparing Background Information on Enterprise

Average breeding life

Replacement rate of breeding stock

2. Growth

Age at weaning

Weight at weaning

Proportion sold as weaners

Non-livestock products sold

Sale weight

Age at sale

Post-weaning mortality rate

Weight of cull breeding stock

3. Feeding

Feeding requirements

Feed quality

Feed mix

Rations

Feed costs

Feed supply

4. Management

Management skills needed

Pasture management

Housing

Water supply

The Farm Management Training Manual 33

Module 4: Preparing Background Information on Enterprise

Hygiene

Special requirements during pregnancy

Disease and parasite control

5. Processing and Marketing

Slaughtering needs

Market outlets

Transport needs

Packaging needs

The Farm Management Training Manual 34

Module 4: Calculating Enterprise Gross Margins

Module 4

Calculating Enterprise

Gross Margins

The Farm Management Training Manual 35

Module 4: Calculating Enterprise Gross Margins

Trainer’s Notes

Set the scene

Farm profit usually features strongly in the goals of most small farmers. The first step in deciding how to get the best profit from farm resources is to determine which enterprises provide the highest gross margin per unit of a resource.

Aim To find out how profitable each farm enterprise is.

Expected outcome

The farmer is able to determine whether a particular farm enterprise is profitable, and how well it ranks compared with other enterprises.

Duration of session

3 hours.

Method Gross margin planning and sensitivity analysis. Begin with the mini lecture and the example using the banana enterprise, to be followed by small group exercises. Seven exercises are included, covering a range of enterprises that are common in Tonga. Arrange for small groups to present and discuss their results in a large group session.

Outputs that participants should achieve

Estimates of gross margins for potential enterprises that the farmer can use when deciding on which enterprises are the most profitable. These gross margins may be expressed per acre, per day or hour of labour, per dollar of capital, per dollar of working capital or per dollar of fixed capital.

Concluding points to make

Gross margins are an essential ‘building block’ in preparing a farm plan. Recognize the uncertainty associated with the gross margin estimate. Yields and output prices are particularly volatile.

Additional reading

MAFF (2000). Dillon and Hardaker (1993, pp. 159-162). FAO (2004).

The Farm Management Training Manual 36

Module 4: Calculating Enterprise Gross Margins

Mini Lecture

Definitions

The gross margin of a farm enterprise is the gross income from output

produced minus the cost of variable inputs used to produce that output.

The gross income of an enterprise is the value of all outputs produced in that

enterprise. For each output, it is calculated as the farm-gate price of the

output multiplied by the quantity produced. Valuing output can cause

problems in situations where the price paid to the farmer is not available.

However, a local market price or export price may be available. In these

cases, marketing costs must be calculated and deducted to obtain a farm-gate

price. The form of the output for which there is an available price might be

different from that which the farmer sells. In the broiler enterprise, price is

quoted in dressed weight while the output is measured before dressing takes

place. In addition, not all quantities are recorded in the same units. They may

be in kilograms, bags or baskets, for example. It is important to have a means

of converting all quantities to a common unit, usually kilograms or tonnes. The

Talamahu Market Reports provide average weights in kilograms for common

trade units.

Variable costs are the sum of costs of inputs that vary with the level of

production in the enterprise. Each variable cost is calculated by multiplying the

price the farmer pays for the input by the quantity of the input used in the

enterprise. Some common examples are seed and other planting materials,

feed, veterinary supplies, fertilizers, chemicals and biological agents to control

pests, diseases and weeds, packing material, transport and hired casual

labour.

A fixed cost is estimated by multiplying the quantity of the fixed input by the

price paid for it. Examples of fixed inputs are rents, licences and costs

associated with the upkeep of fixed assets such as buildings, plant and

machinery. A fixed input is distinguished from a variable input in that it does

not vary with the level of production of the enterprise. Repairs to machinery

are a fixed cost but machinery hire is a variable cost because the amount of

time a machine is hired varies with the level of production.

The Farm Management Training Manual 37

Module 4: Calculating Enterprise Gross Margins

The treatment of family labour is difficult when deciding on variable and fixed

costs. It depends on how easy it is for family members to switch from farming

to other activities from one day to the next. In most cases, family labour inputs

are best treated as fixed inputs and their costs excluded from the calculation

of a gross margin even though they can be varied to some extent, according

to access to alternative income-earning possibilities. Ask trainees to calculate

gross margin per hour of family labour used, considering family labour as a

fixed cost. The solutions to the exercises also contain estimates of the value

of family labour inputs, with gross margins calculated after subtracting this

value from gross income in addition to other variable costs. A gross margin

calculated in this way would be used when it is assumed family labour is a

variable input.

Stress to the trainees that there is always some uncertainty about the

accuracy of the information used in estimating a gross margin because we are

dealing with future events. Therefore, it is always wise to do some sensitivity

analysis. This means we calculate how much a gross margin changes when

there is a change in the values used to calculate it.

Which enterprises to choose for calculating gross margins?

Most farmers in Tonga have many enterprises to choose from to include in

their farm plan. It would take a lot of work to calculate gross margins for all of

them. Fortunately, the Farm Management Manual produced by MAFF (2000)

covers the important crop and livestock enterprises in Tonga and the gross

margin budgets presented in the manual can provide a good guide. Farmers

should concentrate on calculating gross margins for those enterprises that

best suit their resources and circumstances, and use the estimates in the

manual as a starting point.

Steps in gross margin planning Explain to trainees that the main purpose of gross margins is to compare the

profitability of different enterprises to get the best profit from the resources

available. This assumes all enterprises use fixed inputs to about the same

The Farm Management Training Manual 38

Module 4: Calculating Enterprise Gross Margins

degree. Gross margins have to be expressed in a consistent way for all

enterprises. It is usual to express them for one acre per year, as done below.

However, there is no hard-and-fast rule on which resource should be used as

the basis for getting the highest gross margin. It depends on what the farmer

thinks is the most limiting resource. In some cases, a comparison of gross

margins per acre might not be appropriate. An intensive broiler enterprise, for

example, might use little land but be a heavy user of capital. In this situation, it

would be wise to compare gross margins per dollar invested in the enterprise.

Then again, gross margins per unit of various resources can all be used,

leaving the farmer to make a choice between the different measures. In all

cases, it is good practice to calculate gross margin per labour unit (hour or

day, for example) because labour is an important input in all enterprises in

Tonga.

There is also a problem of different lengths of the production cycle of

enterprises. In the exercises that follow in which gross margins are calculated

for one acre of land, different crops are in the ground for different lengths of

time and so the gross margins for the crops cannot be directly compared. In

Module 8, trainees get experience in compiling a farm plan consisting of a

number of enterprises with different production periods. At this stage, they will

simply calculate gross margins per acre for the length of the production cycle

of each enterprise.

Assuming one acre of land, which is the most limiting resource, the method of

gross margin planning follows six steps:

1. Prepare the background information on enterprises that potentially

could be grown on the farm (discussed in Module 3).

2. Prepare an inventory of available resources on the farm that can be

used in production of the enterprises identified in Step 1.

3. Obtain data on input and output quantities and prices for each

enterprise.

4. Calculate gross income from the enterprise for one acre.

The Farm Management Training Manual 39

Module 4: Calculating Enterprise Gross Margins

5. Identify and calculate the costs of variable inputs used to produce the

output from one acre.

6. Subtract variable costs from gross income to obtain gross margin per

acre.

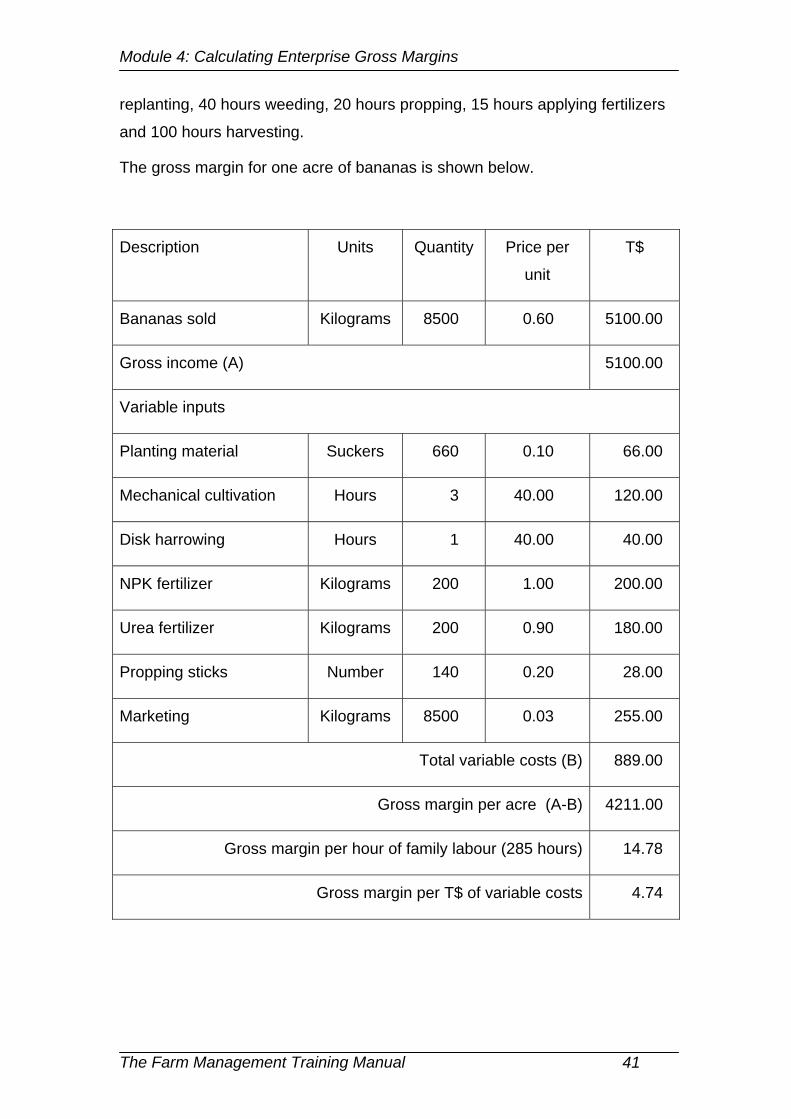

Gross Margin Example: Banana Enterprise

While a banana plant remains in the ground for a few ratoons, we will ignore

the ratoons and calculate the gross margin for the first year only. Calculation

is based on one acre.

Output is estimated to be 8.5 tonnes per acre and the price received by the

farmer is forecast to be T$0.60 per kilogram. Because the price is in

kilograms, we must put output in the same units (8,500 kg). Therefore, gross

income is calculated as 8,500 kg multiplied by T$0.60, which equals T$5,100.

As there is only one output in this enterprise, the value of T$5,100 is also

gross income.

There are seven variable inputs used in the production of the bananas in their

first year:

• 3 hours of machinery hire for ploughing and slashing, costing T$40 per

hour

• 1 hour of machinery hire for disk harrowing, costing T$40 per hour

• 660 suckers used as planting material, costing T$0.10 each

• 200 kg of NPK 8:33:18, costing T$1.00 per kg

• 200 kg of urea, costing T$0.90 per kg

• 140 propping sticks, costing T$0.20 each

• Marketing cost of T$30 per tonne.

The price is multiplied by the quantity in each case to calculate the variable

costs.

The following details are provided on family labour inputs per acre. Forty

hours are spent preparing the planting material, 70 hours planting and

The Farm Management Training Manual 40

Module 4: Calculating Enterprise Gross Margins

replanting, 40 hours weeding, 20 hours propping, 15 hours applying fertilizers

and 100 hours harvesting.

The gross margin for one acre of bananas is shown below.

Description Units Quantity Price per

unit

T$

Bananas sold Kilograms 8500 0.60 5100.00

Gross income (A) 5100.00

Variable inputs

Planting material Suckers 660 0.10 66.00

Mechanical cultivation Hours 3 40.00 120.00

Disk harrowing Hours 1 40.00 40.00

NPK fertilizer Kilograms 200 1.00 200.00

Urea fertilizer Kilograms 200 0.90 180.00

Propping sticks Number 140 0.20 28.00

Marketing Kilograms 8500 0.03 255.00

Total variable costs (B) 889.00

Gross margin per acre (A-B) 4211.00

Gross margin per hour of family labour (285 hours) 14.78

Gross margin per T$ of variable costs 4.74

The Farm Management Training Manual 41

Module 4: Calculating Enterprise Gross Margins

Small Group Exercise: Calculating Gross Margins Seven enterprises have been chosen for calculating gross margins. Allocate

one enterprise to each group. The groups are to calculate the gross margin for

the enterprise assigned to them, using the information provided.

Task 1 Identifying variable inputs

Before they begin to calculate gross margins, each group is to suggest which

variable inputs they would include for the enterprise that they have been

assigned. There is no single correct answer for this task because farmers may

apply different inputs according to their different situations. For example, a

farmer on very fertile soils might apply no fertilizer whereas a farmer on poor

soils may need to apply several fertilizers for the same crop enterprise.

Task 2 Calculating gross margins

Trainees are to begin by calculating gross income. Gross income is the sum

of revenues obtained from all outputs in the enterprise. There will usually be

only one but, in some cases, there might be more than one. In the final

exercise, semi-intensive broiler, for example, poultry manure is sold as well as

the broilers themselves.

Explain that gross revenue is calculated by multiplying the price per unit of

output by the quantity produced. As mentioned in Module 2, all outputs should

be valued regardless of their final destination. Trainees should value unsold

output at the same price that is used for output that is sold.

Ask trainees how they would decide which values to vary when undertaking a

sensitivity analysis. Two things should influence their choice. First, ask them

to think about which factors are most critical to their profit. The most common

examples are output prices and yields, and these are the variables that tend

to get used in the exercises. Other possibilities are prices of key inputs.

Second, choose those factors whose values vary a lot and are uncertain.

Again, yields and prices of the main output are often difficult to forecast. On

the other hand, you usually have a better idea of the prices and quantities of

farm inputs used.

The Farm Management Training Manual 42

Module 4: Calculating Enterprise Gross Margins

Calculations

Each group is to perform the following calculations, except for the semi-

intensive broiler enterprise:

• Total gross margin per acre for the production period.

• Gross margin per dollar of variable cost.

• Gross margin per hour of family labour.

An additional calculation for groups that select the kava or paper mulberry

enterprise is the gross margin in each year.

Groups choosing the semi-intensive broiler enterprise are to calculate the total

gross margin for the production period, gross margin per bird sold and gross

margin per dollar of fixed capital.

Check that all groups have managed to estimate gross income successfully

before continuing to calculate variable costs.

The Farm Management Training Manual 43

Module 4: Calculating Enterprise Gross Margins

Enterprise 1 Sweet potato

Outputs

Five tonnes of sweet potato tubers are produced on an acre of land. Four

tonnes of tubers are sold in Talamahu market at T$0.60 per kilogram and the

farm household consumes the other tonne.

Variable inputs

Production inputs

A total of 10,000 vine tip cuttings are planted in mounds. Each cutting is

estimated to have a value of T$0.02.

The farmer hires machinery for ploughing, slashing and ridging that costs

T$40 per hour. The first ploughing/slashing takes 1.5 hours and the second

ploughing also takes 1.5 hours. Ridging takes 1 hour.

The farmer controls for sweet potato scab by applying 1.8 kg of the fungicide,

Manzate 200 80% WP. Also, 9 litres of the insecticide, Diazinon 20% EC, are

used to prevent infestation of the sweet potato weevil. Manzate costs the

farmer T$20 per kg and Diazinon costs T$35 per litre. Mistblower operations

take place on three occasions costing T$4 each time.

The following details are provided on family labour inputs per acre. Twenty

hours are spent preparing planting material, 60 hours planting, 100 hours

weeding, 40 hours mounding, 24 hours spraying and 50 hours harvesting.

Marketing inputs

It costs T$42.50 to sell each tonne of tubers sold in Talamahu market.

The Farm Management Training Manual 44

Module 4: Calculating Enterprise Gross Margins

Enterprise 2 Watermelon

Outputs

The output of watermelons on an acre of land is estimated to be 12 tonnes.

None is to be retained for consumption by the household. Ten tonnes are to

be sold for export to New Zealand and the remaining 2 tonnes are to be sold

in Talamahu market. The export price is T$1.00 per kg. The farmer expects to

sell watermelons destined for Talamahu market at T$0.80 per kg.

Variable inputs

Production inputs

The farmer uses 1 kg of watermelon seeds per acre, costing T$120 per

kilogram.

The farmer hires machinery for ploughing, slashing and disk harrowing that

costs T$40 per hour. The first ploughing/slashing takes 1.5 hours and the

second ploughing also takes 1.5 hours. The disk harrowing takes 1 hour.

Two fertilizer applications are recommended. The farmer applies 200 kg of

NPK 8:33:18, at a cost of T$1.00 per kg, and 80 kg of urea are applied at a

cost of T$0.90 per kg.

The farmer applies 2 kg of the fungicide, Manzate 200 80% WP, one litre each

of Afugan and Agral, and 0.4 litre of Punch. One litre each is used of the

insecticides, Malathion and Perfekthion, in addition to 1 kg of Snail Away. The

costs of the chemicals to the farmer are T$20 per kg for Manzate, T$45 per

litre for Malathion, T$42 per litre for Perfekthion, T$120 per litre for Afugan,

T$8 per litre for Agral and T$280 per litre for Punch. Snail Away costs T$13

per kg. Mistblower operations cost T$4 and take place on 10 occasions.

The following details are provided on family labour requirements. Planting

takes 40 hours; fertilizer application takes 20 hours; spraying takes 30 hours;

weeding takes 60 hours; watering and mulching take 55 hours; and harvesting

takes 60 hours.

Marketing inputs. The marketing costs charged by the exporter are T$0.35 per

kg. It costs T$0.25 to sell each tonne of watermelons in Talamahu market.

The Farm Management Training Manual 45

Module 4: Calculating Enterprise Gross Margins

Enterprise 3 Tomato

Outputs

The output of tomatoes on an acre of land is estimated to be 7.5 tonnes. None

is to be retained for consumption by the household and all is to be sold in

Talamahu market. The farmer expects to receive T$2.00 per kg.

Variable inputs

Production inputs

The farmer uses three 20-gram packets of tomato seeds per acre. Each

packet of seed is estimated to cost T$20.

The farmer hires machinery for ploughing, slashing and disk harrowing that

costs T$40 per hour. The first ploughing/slashing takes 1.5 hours and the

second ploughing also takes 1.5 hours. The disk harrowing takes 1 hour.

Three fertilizers are applied: chicken manure (600 kg); NPK 8:33:18 (150 kg);

and urea (100 kg). Their costs are T$0.10/kg, T$1.00/kg and T$0.90/kg,

respectively.

Staking of the tomatoes requires a total of 8900 stakes per acre. Each stake is

valued at T$0.05.

The farmer applies 0.5 kg of the fungicide, Benlate 50% WP, which costs

T$85 per kg. Three kilograms of the fungicide, Manzate 200 80% WP, are

used at a cost of T$20 per kg. Two litres of the insecticide, Malathion, are

applied to control for leaf rollers, leaf miners and cucumber beetles, at a cost

of T$45 per litre. Mistblower operations cost T$4 and take place on 10

occasions.

The following family labour requirements are provided. Planting takes 106

hours; pruning takes 40 hours; fertilizing takes 12 hours; spraying takes 40

hours; weeding takes 150 hours; watering and mulching take 100 hours; and

harvesting takes 240 hours.

Marketing inputs

It costs an average of T$0.04 to sell each kilogram of tomatoes in Talamahu market.

The Farm Management Training Manual 46

Module 4: Calculating Enterprise Gross Margins

Enterprise 4 Squash

Outputs

The output of squash on an acre of land is estimated to be 3.5 tonnes. All of

the output is to be sold for export to Japan. The price received by the farmer is

T$0.60 per kg.

Variable inputs

Production inputs

The farmer uses 0.5 kg of squash seeds per acre. Each kilogram of seed is

estimated to cost T$240.

The farmer hires machinery for ploughing, slashing, disk harrowing and

ripping that costs T$40 per hour. The first ploughing/slashing takes 3.5 hours.

The disk harrowing takes 1 hour, as does the ripping.

Nitrophoska is applied at the rate of 6 litres, costing T$5.50 per litre. A total of

200 kg of NPK 8:33:18 are applied, at a cost of T$1.00 per kg, and 80 kg of

urea are applied at a cost of T$0.90 per kg.

The farmer applies 1 kg of the fungicide, Manzate 200 80% WP, 1 litre each of

Afugan and Agral, and 0.4 litre of Punch. One litre each of the insecticides,

Malathion 50% EC, Perfekthion, is applied to control for leaf miners, leaf

rollers and cucumber beetles. The costs of the chemicals to the farmer are

T$20 per kg for Manzate, T$45 per litre for Malathion, T$42 per litre for

Perfekthion, T$120 per litre for Afugan, T$8 per litre for Agral and T$280 per

litre for Punch. Mistblower operations take place on 15 occasions and cost

T$4 per operation.

The family labour requirements are 40 hours for planting, 20 hours for

fertilizing, 50 hours for spraying, 30 hours for weeding, 50 hours for harvesting

and 15 hours for processing and packing.

Marketing inputs

The farmer spends T$40 per tonne to get the squash prepared for the

exporter.

The Farm Management Training Manual 47

Module 4: Calculating Enterprise Gross Margins

Enterprise 5 Kava

Output

The output of green kava is 8.6 tonnes per acre. All is to be harvested in year

5 and sold in the domestic market in powder form. The conversion rate from

green kava to kava powder is 4:1.The price received for 1 kilogram of kava

powder is T$20.

Variable inputs

Production inputs

The farmer uses 1800 seedlings per acre in year 1. Each seedling is

estimated to cost T$1.50.

The farmer applies 0.5 litres of Diazinon 20% EC in each of the first three

years at a cost of T$35 per litre.

The following family labour requirements are provided. Land preparation and

planting take 130 hours in the first year. Maintenance takes 250 hours in the

first year and 400 hours in each year from the second to the fourth year. In the

fifth year, harvesting takes 230 hours, processing and packing into kava

powder takes 430 hours, and selling the kava powder takes 70 hours.

Processing inputs

Crushing costs in year 5 are T$375 per tonne of green kava.

Marketing inputs

The marketing costs are T$300 in year 5.

The Farm Management Training Manual 48

Module 4: Calculating Enterprise Gross Margins

Enterprise 6 Paper Mulberry

Output

A farmer grows paper mulberry in Ha'apai in a four-year production cycle, with

380 bundles of sticks harvested in year 2, 500 bundles in year 3 and 500

bundles also in year 4. One bundle is equal to 20 sticks. The skin is taken off

the stick and each skin is sold in Nuku'alofa for an average price of T$4.00.

Variable inputs

Production inputs

In the first year of the production cycle, the farmer plants 2600 suckers per

acre, worth T$0.30 each, and hires machinery to cultivate the land for three

hours, costing T$40 per hour.

Only family labour is used in production, processing and marketing. Land

preparation and planting take 60 hours in the first year. Maintenance takes

100 hours in the first year and 60 hours in each year from the second to the

fourth year. Weeding takes 30 hours in each of the first three years and 20

hours in the fourth year. Harvesting takes 60 hours in year 2 and 100 hours in

each of years 3 and 4. Four hours of labour are needed to take the skins of a

bundle of 20 sticks.

Marketing inputs

The non-labour cost of marketing 100 skins is T$8.20. Marketing also requires

70 hours of family labour in each year from the second to the fourth year.

The Farm Management Training Manual 49

Module 4: Calculating Enterprise Gross Margins

Enterprise 7 Semi-intensive broiler

Outputs

Broilers are sold for T$10.00 dressed weight. The dressing out percentage is

65 per cent. The byproduct of manure is sold for T$6 per 50 kg bag. The

amount of manure produced is an average of 2 kg per bird for the birds sold at

the end of the production period.

Variable inputs

Production inputs

The farmer purchases 110 chicks at a cost of T$1.10 each. Five chicks die in

the first few days and five more birds die before they are finished off for sale.

The production period is 8 weeks. An amount of 0.05 kg of starter feed per

day is fed to the surviving chicks for the first 4 weeks and 0.1 kg of finishing

feed per day is fed for the final four weeks to the 100 birds that survive

beyond the first four weeks. The starter mix costs T$0.80 per kg and the

finishing feed costs T$0.70 per kg.

Other production costs per bird over the production period (assume an

average of 105 birds) are estimated to be T$0.03 for electricity, T$0.02 for

water and T$0.05 for veterinary expenses. Labour inputs consist of 2 persons

working full-time throughout the production period.

Marketing inputs

There are two marketing inputs. First, plastic bags cost T$0.04 for each bird

sold. Second, two trips are made to the market at T$6 per trip.

Fixed capital

The broiler and feed sheds are the only items of fixed capital. They cost

T$200 to build.

The Farm Management Training Manual 50

Module 5: Partial Budgeting

Module 5

Partial Budgeting

The Farm Management Training Manual 51

Module 5: Partial Budgeting

Trainer’s Notes

Set the scene

Once a gross margin of an enterprise has been estimated, it is possible to use partial budgets see the effect on profit of small to moderate changes in the enterprise.

Aim To develop the farmer’s skill to make adjustments to the farming system to achieve a higher profit.

Expected outcome

Farmers are expected to be able to calculate the effects on net profit of minor to moderate changes to their farm plan. These effects can also be calculated as part of a demonstration or on-farm trial (see Module 9).

Duration of session

2 hours.

Method Tools used are:

• Partial budgeting.

• Break-even budgeting. Begin with the mini lecture and the example of the change in fungicide use in squash production. Trainees are to calculate changes to the same seven enterprises used to calculate gross margins in small groups. Arrange for these small groups to present and discuss their results in a large group session.

Outputs that participants should achieve

A new farm plan that can be compared for relative profitability with the existing farm plan.

Concluding points to make

Partial budgeting can be used in a variety of ways. It is useful to look at the effects on cash flow as well as profitability when examining a change in the farm plan. Also, its use is not confined to changes in gross margin. It can be used to analyse the effects of a change in fixed inputs or capital expenditure on net farm profit.

Additional reading

Dillon and Hardaker (1993, pp. 155-159). FAO (2004).

The Farm Management Training Manual 52

Module 5: Partial Budgeting

Mini Lecture The main purpose of a partial budget is to calculate the effect on profit of a

small change in the enterprise. This should help the farmer evaluate whether

a change is worthwhile making to get a higher profit from the resources

available. Partial budgeting is used mostly when compiling a farm plan.

The four possible changes that make up a partial budget are:

1. Additional costs 2. Loss of revenue 3. Costs saved 4. Additional revenue.

The first two changes reduce net farm profit while the last two changes

increase net farm profit.

Partial budgeting can also be used to assess the effect on profit of changing

the value of a key variable whose value is uncertain. Break-even budgeting is

used to find out the worst value that can occur for such a variable without

making a loss. In other words, it is the value of an output or an input that still

allows the farmer to break even in the enterprise concerned.

Example: Change in a squash enterprise

The farmer is considering the use of Systhane instead of Afugan as an

alternate spray to control powdery mildew. Application of 180 grams of

Systhane is expected to cost $91.50 and yield an extra 100 kg of export-

quality squash. The saving in application of Afugan would be $60.

Calculate the change in total gross margin for the production period as a

result of this change in chemical application. Should the farmer make the

change?

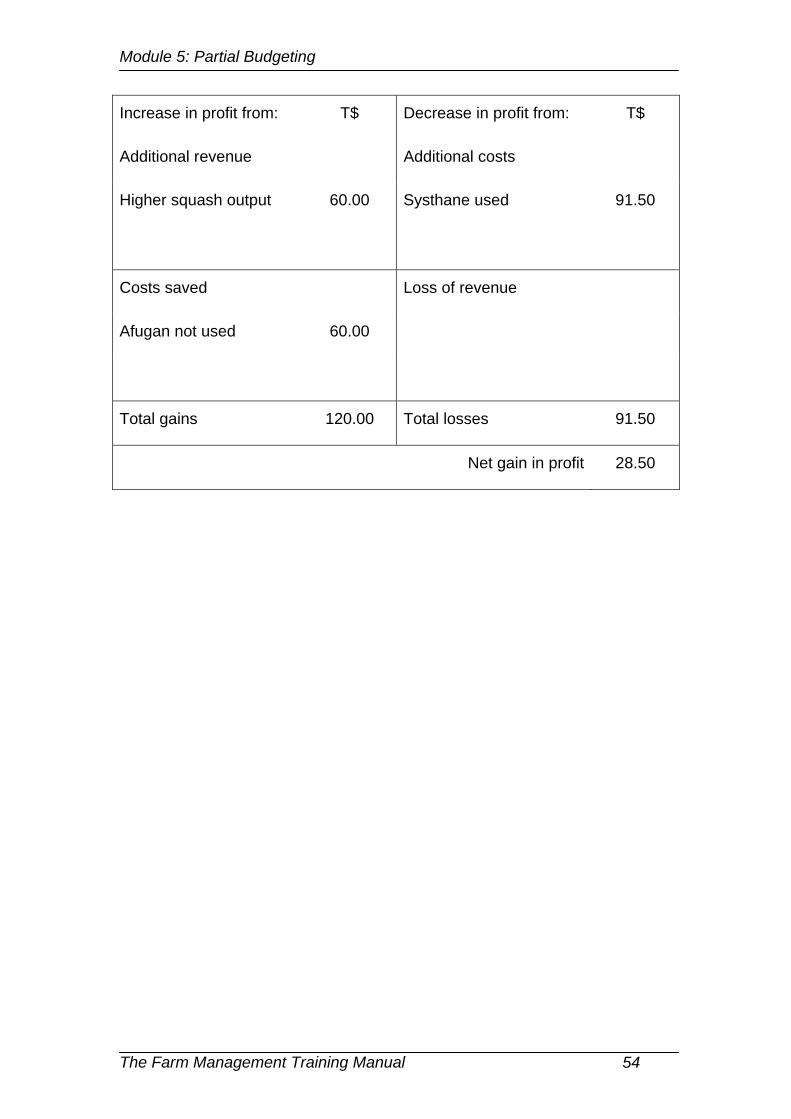

The answer is shown below in tabular form, which is a handy way to tackle the

exercises. There is a net gain in profit of T$28.50, which suggests that the

squash producer should make the change to Systhane.

The Farm Management Training Manual 53

Module 5: Partial Budgeting

Increase in profit from: T$ Decrease in profit from: T$

Additional revenue Additional costs

Higher squash output 60.00 Systhane used 91.50

Costs saved Loss of revenue

Afugan not used 60.00

Total gains 120.00 Total losses 91.50

Net gain in profit 28.50

The Farm Management Training Manual 54

Module 5: Partial Budgeting

Small Group Exercise: Calculating Partial Budgets

Form the trainees into the same small groups that calculated gross margins

and assign the same enterprise that the group chose in the gross margins

exercise. The following information on changes to the farm plan for each

enterprise is provided to calculate the partial budget.

Start by explaining to trainees the main purpose of a partial budget. Inform

them that they get experience in using them in Module 8 when compiling a

farm plan.

Normally, a farmer would evaluate the effect on the farm plan of a single

change at a time. This is the case in some exercises. In others, trainees are

asked to make two separate changes so that they have experience in

calculating all four types of effects on profit.

Ask all groups to start by identifying any additional costs and then to calculate

them. Check that all groups have managed to calculate them successfully

before continuing. Do the same for calculation of revenue lost, then costs

saved and, finally, additional revenue.

The Farm Management Training Manual 55

Module 5: Partial Budgeting

Enterprise 1 Sweet potato

Task 1

The farmer has decided no longer to apply any of the fungicide, Manzate 200

80% WP. The effect is to reduce the yield of tubers of sweet potato produced

from 5 tonnes per acre to 4.8 tonnes per acre.

Calculate the change in total gross margin for the production period as a

result of not applying Manzate. Should the farmer make the change?

Task 2

The farmer uses hired labour for land preparation instead of hiring machinery

for ploughing, slashing and ridging. Hired labour is to be employed for 10 days

and the wage paid is T$24 per day. There is no effect on any other farm

operation or on the output of tubers.

Calculate the change in total gross margin for the production period as a