bgh business profile 2016

TRANSCRIPT

2016

Big Grape Holdings

John Bere, Tapiwa Karoro

2

Executive summary

• Big Grape’s goal is to provide much needed credit to small scale farmers and market traders • Big Grape Holdings is structured as two separate business units

• Big Grape Financial Services (BGFS) provides $100 to $500 loans to traders and SMEs

• Big Grape Capital (BGC) operates a chicken out-grower project in Domboshawa – so far we have set up 18 chicken runs each producing 1600 chickens every 7 weeks

• Our mission is to help people move from being informal farmers and traders to become established members of the formal financial sector • BGMF’s has experimented with different borrowing segments, our focus now on lending to Traders/SME’s • BGMF has created a customer database of key informal markets in the capital city Harare

• The e-Mali banking system and our ‘Human ATM’ model will expand the reach of our MF products

• BGC is well exposed to the large, fast growing broiler chicken market • We have developed a streamlined model for financing and overseeing the growth of broilers • We are providing our small holder farmers with an average of $4,800/yr of cash income

• BGC’s existing poultry farmers provide an immediate consumer pool for additional financial services • BG can extend the CRISP program to rural farmers nationwide • Opportunities to further invest in the poultry supply and value chains – specifically cold-chain facilities

3

Agenda

• Background on Big Grape Holdings

• Business overview: Big Grape Micro-Finance

• Business overview: Big Grape Capital

• Big Grape’s Value Proposition

• Appendix

4

Big Grape’s goal is to provide much needed credit to small scale farmers and market traders

• One of the UN’s Millennium Development Goals (MDGs) is to halve poverty by 2015

• Financial services play a key role in enabling households to acquire assets, engage in productive economic activity and pay for goods and services that can improve and protect human well-being • When provided with accessible and flexible financial services those in

the informal sector can be key actors in contributing to the attainment of the MDGs

• Big Grape’s mission is to provide members of Zimbabwe’s informal economy with access to financial services to help bring them out of poverty

• Building a network of creditworthy small scale farmers will allow us to grow as a microfinance firm by bringing our customers into the formal economy

• Our Chicken Rearing and Investment Self-Help Project (CRISP) in Domboshava and Insiza district in Matebeleland is our first step to creating a sizable pool of creditworthy communal farmers.

5

Big Grape Holdings is structured as two separate (but integrated) business units

BG Financial Services

• BGFS (Pvt) Ltd provides financial inclusion models for the informal, mass market sector in Zimbabwe

• Experimented with different products and identified loans to Traders/ SMEs as the most viable segment

• Winding down our other loan products in order to focus on Farmers and Traders/SMEs

• Peak loan book size: $243k

Big Grape Capital

• BGC (Pvt) Ltd is an agro-focused structured finance firm that focuses on community based developmental projects

• BGC operates a chicken out-grower project in the Domboshawa area & Insiza

• Number of farmers: 28 • Annualised bird production: 283 ,

020 broilers • Annuali broiler sales: $1,546,928

Planned flow of customers as our

farmers’ enter the formal

financial sector

6

The BGC-BGMF integration: developing ‘unbankable’ farmers into empowered, loyal customers

Small-holder farmer 1

• Our farmers initially have no financial or credit track record

• BGC provides farmers with financing for construction of a chicken run, as well as input financing for feed and day old chicks

• These loans are secured against the physical assets provided

Microfinance customer

2 Banking services customer

3

• Farmers develop a credit track record through their chicken production activities

• BGMF is able to provide the farmer with financing for other essential items such as water pumps, heating and lighting equipment.

• Farmers can also access beneficial consumptive loans for dependents’ school fees, medical fees and bereavements.

• Farmers accumulate savings and develop a need for conventional banking products

• Big Grape’s long term goal is to obtain a micro-banking license, allowing us to provide an inclusive, low cost and convenient banking platform

• The long standing, trusted relationship with our farmers will encourage them to bank with us

Huge opportunity exists to expand this model into layers, cattle, pigs and numerous other livestock and crop

commodities

7

Big Grape Holdings Directors

• 4-years experience as a money market dealer with HSBC and Barnfords Securities • 6-years experiences

with Tetrad Group – rose to position of Exec Director of Operations • Bcom (Hons), National

University of Sciences & Technology • Studying for a Masters

in Business Leadership

John Bere Group Managing

Director • Founding partner and

non-exec director of Reach Africa Investments • Formerly ‘GM – Global

Markets and Trade Finance’ at Tetrad Bank • Bachelor of Business

Science and Master of Commerce (Hons) from Rhodes University • Studying for a PhD in

International Finance from Wits Business School

Tapiwa Karoro Managing Director

BGFS

8

Agenda

• Background on Big Grape Holdings

• Business overview: Big Grape Micro-Finance

• Business overview: Big Grape Capital

• Big Grape’s Value Proposition

• Appendix

9

BGMF’s goal is to overcome liquidity constraints for traders and SME’s

• Big Grape Microfinance (Pvt) Ltd is a microfinance company focused on developing financial inclusion models for the informal mass market sectors of the economy • We provide $100-$500 loans to market traders, with daily and weekly

repayment schedules

• BGMF’s medium to long term goal is to evolve into a microfinance bank that provides an inclusive, low cost, convenient and simple banking platform

• Our loan book has been an exploratory one, geared towards proofing the viability of various microfinance models and products – our aim is to officially launch and grow our loans offering to Traders/SMEs

10

BGMF’s has experimented with different borrowing segments, the focus is increasingly on SME’s

BG Micro-Finance

• Private sector loans were purely cash loans

• Hire purchase loans were also granted to salaried Pvt. Sector clients

• Big Grape Micro-finance started out as a micro-lending Joint Venture

• We experimented with numerous types of borrowers, with varied degrees of success • Private sector, salary based loans turned out to be very risky due to private

companies not consistently paying their employee’s wages

• Trader/SME loans have consistently shown very low default rates, and so we have set ourselves the target of 75% of loans to be underwritten to these borrows

11

Trader/SME loans are popular amongst informal store owners, particularly amongst females

BG Micro-Finance

High default rate results from formal

sector employers failing to pay their

employees

Majority of Trader/SME loans are to female

business owners

Monthly interest rates

Product Tenor Pricing Average loan Size Default RateTraders

Avondale 1 Month 10% 500.00$ 4%Mbare 24 days 10% 100.00$ 1%Gulf 1 Month 10% 300.00$ 2%Tamic 24 days 10% 100.00$ 2%Other 1 Month 10% 300.00$ 3%

Salary Based 3 Months 6.50% 390.00$ 27%Hire Purchase 3, 6, 9, 12 Months 4% 462.00$ 0%Civil Servants 3 Months 4.50% 300.00$ 0%

12

The e-Mali banking system and our ‘Human ATM’ model will expand the reach of our MF products

BG Micro-Finance

The e-Mali payment system allows us to reach a vast number of clients

Our “Big” idea is to empower our traders to act as human ATMs

• e-Mali is an S.A. based mobile technology company

• e-Mali has operated in Zimbabwe since 2010

• The e-Mali system works off an agency network much like Ecocash, and also has an existing distribution network across the country

• We have piloted the platform in the Mbare Agriculture Market, and it is proving to be the ideal solution to service the high transactional mass markets

• We will empower our informal trading clients to disburse and collect on approved loans • These traders are accustomed to

handling cash on a daily basis

• This will enable our existing and new traders to “sweat” their daily cash holdings and earn additional income

• This “human ATM” model will expand the reach of BGMF’s lending programs

13

Agenda

• Background on Big Grape Holdings

• Business overview: Big Grape Micro-Finance

• Business overview: Big Grape Capital

• Big Grape’s Value Proposition

• Appendix

14

BGC’s goal is to facilitate the inclusion of small-holder farmers into the formal financial sector

• BGC looks to invest in a number of community based projects and businesses that bring the ordinary Zimbabwean closer to financial services and solutions through financial inclusion, while building key competencies and capacity along investment value chains.

• Big Grape Capital believes in investing in projects that empower rural smallholder farmers through sustainable income generation, job creation and development, and thus creating a reliable credit pool for Big Grape Microfinance.

• We are currently focused on growing our Chicken Rearing and Investment Self Help Project (CRISP) in Domboshava District.

15

The market for broiler chickens is fast growing, leaving significant room for BGC to grow

BG Capital

10

0

20

70

30

60

50

40

55

2010 2012

18

2013 2011 2009

52

38

17

2008 2007

30

64

Domestic production Broiler DOC* production (2007-13) Million chicks

* Day-old chick Source: ZPA

Since 2009, Zimbabwe broiler production has increased 3.5x to 64M

birds per year

• Our 14 farmers currently produce 16MT of meat per month (0.46% of the Zimbabwe market). We have just added an additional 4 farmers who will begin production soon

• We plan to add an additional 50 farmers, which would bring production to 40MT/month (1.44% of the ZIM market) – still only a small fraction of the overall market

16

Big Grape is positioned to benefit from growth in domestic small holder broiler production

-

2,000

4,000

6,000

8,000

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Monthly domestic broiler production (metric tonnes of meat)

Small holder farmers

Large scale farmers

BG Capital Source: ZPA

• African Development Bank statistics indicate domestic production accounts for only 55% of demand

• There is a huge opportunity to replace imports with local production

17

CRISP engages small holder farmers to grow broiler chicken over a 5 week cycle

Provide training to

farmers (BGC extension

officers)

Monitor farming

throughout the cycle

(BGC extension officers)

Collect birds from farmer

(BGC)

Pay farmer within 14 days

of delivery (BGC)

Slaughter birds (Abattoir)

Market birds (BGC)

Identify small holder farmers

(BGC)

Select & contract farmers (BGC)

Finance inputs: chicken runs,

chicks and feed (BGC)

5 week chicken rearing cycle

BGC’s process oversight roles: • Providing a

guaranteed market for the birds

• Managing the end to end value chain and supply chain

• Providing program management and quality control of bird production

• Providing financial literacy training to farmers

BG Capital

18

Each stakeholder brings key resources to CRISP’s poultry farming operation

Big Grape Capital • Market linkages

and off-take relationships

• Access to capital • Experience

managing the chicken rearing cycle

Small-holder farmer • Labour • Land • Security

Abattoir • Slaughtering facility • Distribution of slaughtered

birds • Packaging and branding

BGC Extension Officer

• Technical expertise • Relationships with

farmers

BG Capital

19

BGC provides numerous benefits to farmers participating in the CRISP program

1. Access to finance

‒ Finance for infrastructure and production inputs

‒ Access to equipment, including feeders and drinkers

2. Access to training & support

‒ BGC extension officers resident in the area provide assistance

‒ Irvine’s and Profeeds also act as advisors to farmers

3. Guaranteed off-take for the chickens

‒ Full payment for delivered birds as contracted despite market uncertainties

4. Improved financial literacy and income generating potential

BG Capital

20

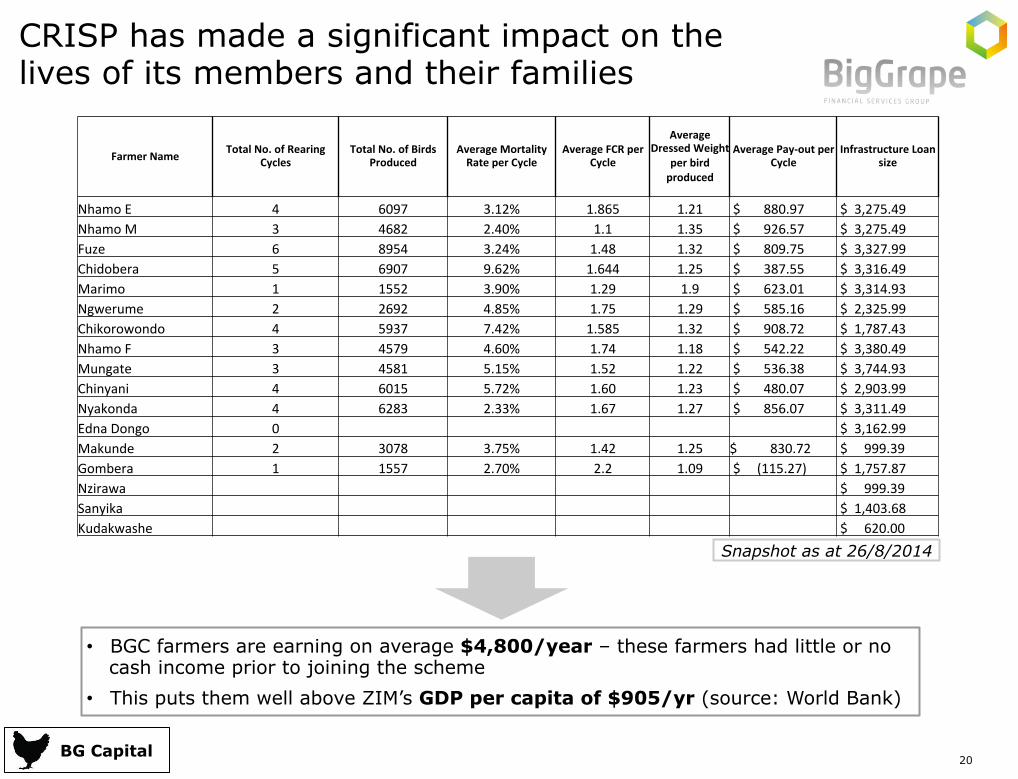

CRISP has made a significant impact on the lives of its members and their families

BG Capital

• BGC farmers are earning on average $4,800/year – these farmers had little or no cash income prior to joining the scheme

• This puts them well above ZIM’s GDP per capita of $905/yr (source: World Bank)

Snapshot as at 26/8/2014

Farmer Name Total No. of Rearing Cycles

Total No. of Birds Produced

Average Mortality Rate per Cycle

Average FCR per Cycle

Average Dressed Weight

per bird produced

Average Pay-‐out per Cycle

Infrastructure Loan size

Nhamo E 4 6097 3.12% 1.865 1.21 $ 880.97 $ 3,275.49 Nhamo M 3 4682 2.40% 1.1 1.35 $ 926.57 $ 3,275.49 Fuze 6 8954 3.24% 1.48 1.32 $ 809.75 $ 3,327.99 Chidobera 5 6907 9.62% 1.644 1.25 $ 387.55 $ 3,316.49 Marimo 1 1552 3.90% 1.29 1.9 $ 623.01 $ 3,314.93 Ngwerume 2 2692 4.85% 1.75 1.29 $ 585.16 $ 2,325.99 Chikorowondo 4 5937 7.42% 1.585 1.32 $ 908.72 $ 1,787.43 Nhamo F 3 4579 4.60% 1.74 1.18 $ 542.22 $ 3,380.49 Mungate 3 4581 5.15% 1.52 1.22 $ 536.38 $ 3,744.93 Chinyani 4 6015 5.72% 1.60 1.23 $ 480.07 $ 2,903.99 Nyakonda 4 6283 2.33% 1.67 1.27 $ 856.07 $ 3,311.49 Edna Dongo 0 $ 3,162.99 Makunde 2 3078 3.75% 1.42 1.25 $ 830.72 $ 999.39 Gombera 1 1557 2.70% 2.2 1.09 $ (115.27) $ 1,757.87 Nzirawa $ 999.39 Sanyika $ 1,403.68 Kudakwashe $ 620.00

21

An average Farmer can generate $4,100/yr of cash income for themselves. BGC receives a return of 230%/yr

BG Capital

Revenue (1600 birds @ 5% mortality): $6,047

Less Costs:

Cost of day old chicks $1,200

Starter $682 Grower crumps $552 Grower Pellets $1,104 Finisher $863

Total feed $3,201

Vaccines $13 Poultry medication $108

Transportation-feed $140 Transportation- livebirds $150

Total cost per 1,600 birds $4,811

Profit from chicken rearing $1,235

Less BGC charges:

BGC Management Fee (5% of input costs) $241 Chick commission $160 Feed commission $320

Total BGC charges per 1600 birds: $721

Farmer income: $515

Less infrastructure loan repayments: (paid by farmer for first 12 months only)

$184

Farmer Income after loan repayments: (first 12 months only) $331

Unit economics: representative example of small poultry farm profitability per cycle

• Feed makes up 66% of overall costs for chicken rearing

• Each chicken run consumes 3.7 tonnes of feed for every 5 week cycle

• BGC generates $721 of gross profit per cycle off a base of $4,811 of invested capital

• This equates to a monthly return of 7.2%, or an annual return of 230%

• Each project runs 8 cycles per year – chicken rearing takes 5 weeks and the run is rested for 2 weeks between each batch of chickens

• Bird mortality rate is the key driver of project profitability

• 5% mortality is a conservative estimate, current mortality rates are 4.3%

• Farmers generate $515 of cash income per cycle – equates to $4,100/yr

• Farmer receives a loan of $1,130 to build their chicken run

• The loan is paid off in 8 installments at an interest rate of 2.5%/month – this equates to an annualised return of 34% for BGC on these infrastructure loans

22

Agenda

• Background on Big Grape Holdings

• Business overview: Big Grape Micro-Finance

• Business overview: Big Grape Capital

• Big Grape’s Value Proposition

• Appendix

23

Our business model is aligned with our goal of financial inclusion for the informal sector

• The two sides of our business harness the potential of the informal market: • Chicken Rearing and Investment Self-Help Project (CRISP) • Traders and SME loans

• Strategic and operational infrastructure in place: • Management team • Operational systems and procedures for credit

assessment, processing, disbursement and collection • Flagship Microfinance Branch • Existing database of small scale farmers and informal

traders

• Raised funding through developmental initiatives • AIZ/Technoserve Award Winner • Create Fund Beneficiary

A proven, integrated business model

The capabilities needed to expand our footprint

Experience accessing low cost financing

24

Expansion opportunities for Big Grape

1. Big Grape’s existing poultry farmers provide an immediate consumer pool for other financial services, including: • Asset financing – farm equipment, home appliances etc. • Consumer loan – school fees and medical fees loans, emergency loans • Micro insurance • Transactional services – money transfer and payment services • Savings and investment services

2. Big Grape’s existing informal market trader base provides an immediate distribution channel (and market) for third party products • Database of 315 Mbare traders dealing in fresh and dried food products • Opportunities for micro-consignment models for commodities ranging from timber and

steel, to soya chunks and dried fish

3. Big Grape can extend the CRISP program across the country to other rural districts, targeting the youth, women and the populous at large.

4. Opportunities to invest in the poultry supply and value chains – specifically cold-chain facilities • Invest in abattoir facilities with guaranteed supply through CRISP farmers • Placing 5 farmers/week à 7,752 birds/week à process at least 1,550 birds/day

25

Agenda

• Background on Big Grape Holdings

• Business overview: Big Grape Micro-Finance

• Business overview: Big Grape Capital

• Big Grape’s Value Proposition

• Appendix

26

Agenda

• Background on Big Grape Holdings

• Business overview: Big Grape Micro-Finance

• Business overview: Big Grape Capital

• Appendix

27

Investment risks and mitigation strategies

Risks Mitigation strategy

• Default rates on loans rise above historical levels

• Daily collections through in-house and independent agents

• Prudent provision levels • Credit Insurance

• Inability to find a sufficient number of bankable loan recipients

• Create bankable loan recipients through initiatives such as the CRISP program

• Work with established informal trader organisations

• The Regulator introduces a cap on interest rates

• Raise cheaper sources through developmental funding sources based on the social impact of our projects

• Increase in mortality rates as existing chicken runs age and/or disease outbreak

• Expand the production capacity of existing farmers by funding the completion of new houses

• Bring on new farmers, from different areas on to the program

• Inability to find suitable abattoir facilities for the new birds

• Invest in own abattoir facilities – BGC has current applications for funds with SNV and RVO – Facility for Sustainable Entrepreneurship and Food Security

• Side marketing of birds becomes more prolific

• Conduct autopsies on birds reported as deceased • Provide immediate cash payment on delivery • Alleviate farmer cash shortages by giving them

access to credit facilities

Big

Grape Micro

Finance

Big

Grape Capital

28

Sensitivity analysis: loan default rates and bird mortality rates are the key profitability drivers

Bird mortality rate: 12.5% 10.0% 7.5% 5.0% 2.5% 0.0%

CRISP project NPV ($274,687) $157,679 $590,046 $1,022,412 $1,454,778 $1,887,145

CRISP project IRR (3%) 33% 70% 109% 151% 197%

Bird mortality rate: 12.5% 10.0% 7.5% 5.0% 2.5% 0.0% Farmer income

(excluding loan repayment) $37 $196 $355 $515 $674 $833

Farmer income per cycle (after loan repayment) ($146) $13 $172 $331 $490 $649

BGMF loan default rate 12.50% 10% 7.50% 5% 2.50% 0%

BGMF project NPV -$599,603 -$564,643 -$402,596 $61,445 $1,201,595 $3,797,014

BGMF project IRR negative negative negative 37% 232% 490%

29

Broiler production has recovered strongly following a dip in early 2014

BG Capital Source: ZPA