bfa715 accounting theory - university of tasmania theory represents the capstone of your studies in...

TRANSCRIPT

1

BFA715

Accounting Theory

Semester 1, 2014

THIS UNIT IS BEING OFFERED IN

HOBART

Teaching Team

Unit Co-Ordinator and Lecturer

Associate Professor Trevor Wilmshurst

Tutor

Ms Claire Horner

CRICOS Provider Code: 00586B

2

Contents

Contact Details 2

Unit Description 3

Prior Knowledge &/or Skills OR Pre-Requisite Unit(s) 3

Enrolment in the Unit 3

Intended Learning Outcomes and Generic Graduate Attributes 4

Learning Expectations and Teaching Strategies/Approach 5

Occupational Health and Safety (OH&S) 5

Learning Resources 5

Student Feedback via eVALUate 7

Details of Teaching Arrangements 8

Learning expectations and strategies 8

Specific attendance/performance requirements 9

Assessment 10

Submission of Assessment Items 12

Review of Assessment and Results 13

Further Support and Assistance 14

Academic Misconduct and Plagiarism 14

Study Schedule 16

Unit Schedule – Lecture Presentations, Pre Reading and Question Completion Requirements 16

Assessment 17

Tutorials 17

Task 1 - Academic Journal Articles – Team Presentations 19

Task 2 – Research Focused Project - 25% 27

Contact Details

Unit Coordinator Associate Professor Trevor Wilmshurst

Tutor Ms Claire Horner

Campus Launceston Campus Hobart

Room Number D101-102

Hobart L219

Room Number

TBA

Email [email protected] Email [email protected]

Phone 6324 3570 Phone TBA

3

Unit Description Accounting Theory represents the capstone of your studies in financial accounting and exposes you to the underlying theories and other influences that have played an important role in shaping accounting practice. Further, the unit considers emerging issues currently being addressed by researchers. In this way, the unit will give you an understanding of the historical and contemporary issues that have influenced the development of accounting practice, accounting regulation and accounting thought. Over time, accounting theory has focused on three main approaches or viewpoints. These are the descriptive (positive), normative and critical viewpoints. Using these theoretical points of view, this unit will help you examine current issues such as social and environmental accountability, the ethical and global dimensions of accounting, Conceptual Framework projects and the political context within which accounting policy decisions are made.

We present a theoretical framework for examining accounting issues and practices and a chance for you to develop high-level critical and analytical skills. This will help you present arguments and opinions on a broad range of accounting issues, with some authority. Knowing about historical and contemporary issues will also give you a foundation for understanding the rationale (main reasons) for current accounting policies and practices, and the directions in which accounting policies are likely to develop. In this way to better prepare you for the changes that the profession will inevitably need to be a part of.

Prior Knowledge &/or Skills OR Pre-Requisite Unit(s) The pre-requisite to complete this unit is a pass grade or better in BFA705 Financial and Corporate Accounting. This background knowledge is essential to enable effective participation in the achievement of the outcomes expected in this unit. This unit offers the theoretical perspective for evaluating accounting practices and policies.

Enrolment in the Unit Unless there are exceptional circumstances, students should not enrol in this unit after the end of week two of semester, as the Tasmanian School of Business and Economics (TSBE) cannot guarantee that: • any extra assistance will be provided by the teaching team in respect of work covered in the

period prior to enrolment; • penalties will not be applied for late submission of any piece or pieces of assessment that were

due during this period nor will special consideration be applied in respect of work requirements prior to late enrolment; and

• students enrolling late will be required to promptly complete any outstanding assessment tasks, pre reading for lectures and tutorials, and review lectures already presented.

4

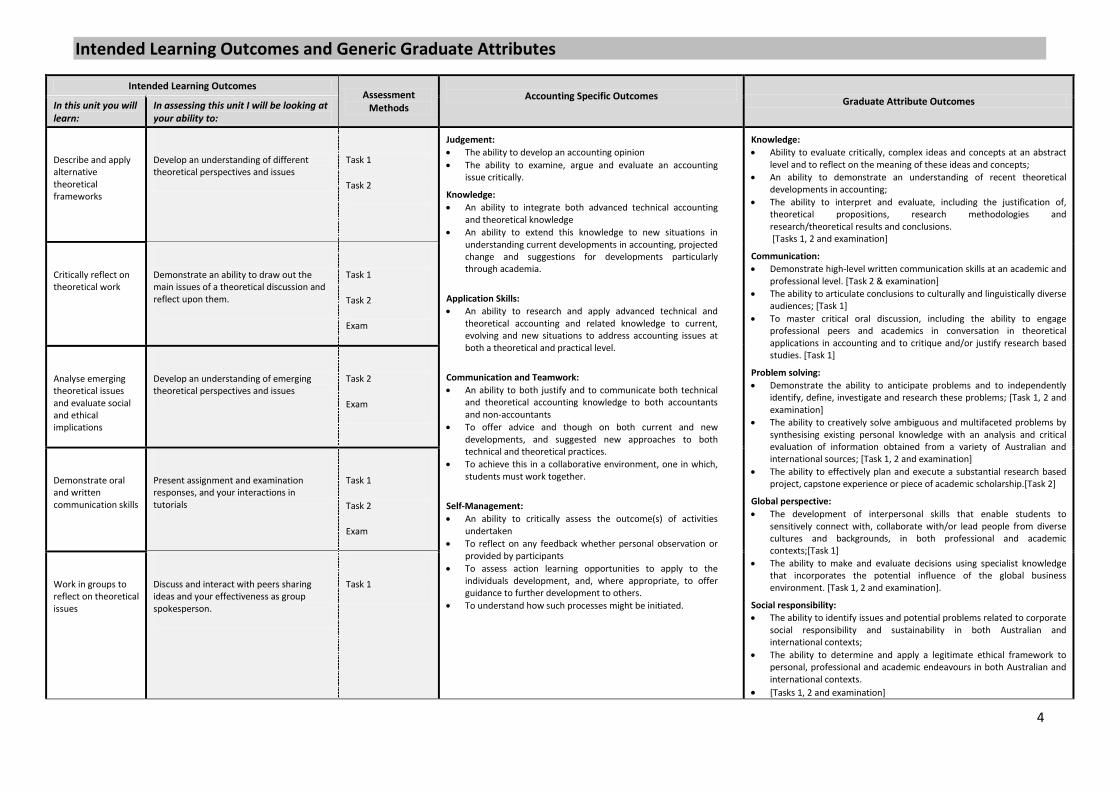

Intended Learning Outcomes and Generic Graduate Attributes

Intended Learning Outcomes Assessment

Methods

Accounting Specific Outcomes Graduate Attribute Outcomes In this unit you will

learn: In assessing this unit I will be looking at your ability to:

Describe and apply alternative theoretical frameworks

Develop an understanding of different theoretical perspectives and issues

Task 1

Task 2

Judgement: • The ability to develop an accounting opinion • The ability to examine, argue and evaluate an accounting

issue critically.

Knowledge: • An ability to integrate both advanced technical accounting

and theoretical knowledge • An ability to extend this knowledge to new situations in

understanding current developments in accounting, projected change and suggestions for developments particularly through academia.

Application Skills: • An ability to research and apply advanced technical and

theoretical accounting and related knowledge to current, evolving and new situations to address accounting issues at both a theoretical and practical level.

Communication and Teamwork: • An ability to both justify and to communicate both technical

and theoretical accounting knowledge to both accountants and non-accountants

• To offer advice and though on both current and new developments, and suggested new approaches to both technical and theoretical practices.

• To achieve this in a collaborative environment, one in which, students must work together.

Self-Management: • An ability to critically assess the outcome(s) of activities

undertaken • To reflect on any feedback whether personal observation or

provided by participants • To assess action learning opportunities to apply to the

individuals development, and, where appropriate, to offer guidance to further development to others.

• To understand how such processes might be initiated.

Knowledge: • Ability to evaluate critically, complex ideas and concepts at an abstract

level and to reflect on the meaning of these ideas and concepts; • An ability to demonstrate an understanding of recent theoretical

developments in accounting; • The ability to interpret and evaluate, including the justification of,

theoretical propositions, research methodologies and research/theoretical results and conclusions. [Tasks 1, 2 and examination]

Communication: • Demonstrate high-level written communication skills at an academic and

professional level. [Task 2 & examination] • The ability to articulate conclusions to culturally and linguistically diverse

audiences; [Task 1] • To master critical oral discussion, including the ability to engage

professional peers and academics in conversation in theoretical applications in accounting and to critique and/or justify research based studies. [Task 1]

Problem solving: • Demonstrate the ability to anticipate problems and to independently

identify, define, investigate and research these problems; [Task 1, 2 and examination]

• The ability to creatively solve ambiguous and multifaceted problems by synthesising existing personal knowledge with an analysis and critical evaluation of information obtained from a variety of Australian and international sources; [Task 1, 2 and examination]

• The ability to effectively plan and execute a substantial research based project, capstone experience or piece of academic scholarship.[Task 2]

Global perspective: • The development of interpersonal skills that enable students to

sensitively connect with, collaborate with/or lead people from diverse cultures and backgrounds, in both professional and academic contexts;[Task 1]

• The ability to make and evaluate decisions using specialist knowledge that incorporates the potential influence of the global business environment. [Task 1, 2 and examination].

Social responsibility: • The ability to identify issues and potential problems related to corporate

social responsibility and sustainability in both Australian and international contexts;

• The ability to determine and apply a legitimate ethical framework to personal, professional and academic endeavours in both Australian and international contexts.

• [Tasks 1, 2 and examination]

Critically reflect on theoretical work

Demonstrate an ability to draw out the main issues of a theoretical discussion and reflect upon them.

Task 1

Task 2

Exam

Analyse emerging theoretical issues and evaluate social and ethical implications

Develop an understanding of emerging theoretical perspectives and issues

Task 2

Exam

Demonstrate oral and written communication skills

Present assignment and examination responses, and your interactions in tutorials

Task 1

Task 2

Exam

Work in groups to reflect on theoretical issues

Discuss and interact with peers sharing ideas and your effectiveness as group spokesperson.

Task 1

5

Learning Expectations and Teaching Strategies/Approach The University is committed to a high standard of professional conduct in all activities, and holds its commitment and responsibilities to its students as being of paramount importance. Likewise, it holds expectations about the responsibilities students have as they pursue their studies within the special environment the University offers. The University’s Code of Conduct for Teaching and Learning states:

Students are expected to participate actively and positively in the teaching/learning environment. They must attend classes when and as required, strive to maintain steady progress within the subject or unit framework, comply with workload expectations, and submit required work on time.

Occupational Health and Safety (OH&S) The University is committed to providing a safe and secure teaching and learning environment. In addition to specific requirements of this unit you should refer to the University’s policy at: http://www.utas.edu.au/work-health-safety/ Learning Resources Prescribed Text Deegan, C. 2014. Financial Accounting Theory. 4th Edition. McGraw-Hill Education. Recommended Texts Chartered Accountants Financial Reporting Standards 2012 (or similar) – Statements of Accounting Concepts 1 and 2, and the Framework for the Preparation and Presentation of Financial Statements.

Fleet, W, Summers, J & Smith, B 2006, Communication Skills Handbook for Accounting, 2 edn, John Wiley & Sons, Brisbane.

Rankin, M., Stanton, P., McGowan, S, Tilling, M., Ferlauto, K. and Tilt, C. 2012. Contemporary Issues in Accounting. 9780730300267. John Wiley and Sons.

Neville, C 2007, The Complete Guide to Referencing and Avoiding Plagiarism, McGraw Hill Open University Press. ISBN. -13 9780335220892, -10 0335220894

The Framework is in CPA Australia’s Accounting Handbook and you can download it at http://www.aasb.com.au. You will need to bring all the required texts to each lecture and tutorial session. We may give you extra journal articles to read during the semester.

You will benefit from reading as broadly as possible, especially for your assignments. Accounting theory is about ideas, and the more literature you survey the more you will understand about alternative approaches to accounting. References that might be helpful include:

Belkaoui, A.R. 2004. Accounting Theory, 5th Edn, Thomson, London.

Brooks, L.J. 2004. Business & Professional Ethics for Directors, Executives & Accountants, 3rd Edn, Thomson Learning, Ohio, USA.

Evans, T.G. 2003. Accounting Theory, Contemporary Accounting Issues, McGraw-Hill, Roseville, NSW.

6

Gaffiken, M 2008. Accounting Theory: Research, regulation and accounting practice. Pearson Education Australia, Frenchs Forest, NSW

Godfrey, J, Hodgson, A., & Holmes, S. 2003. Accounting Theory, 5th Edn, John Wiley & Sons, Brisbane,

Henderson, S., Peirson, G. & Harris, K. 2004. Financial Accounting Theory, Pearson Education Australia, Frenchs Forest, NSW.

Schroeder, R.G., Clarke, M.W., and Cathey, J.M. 2013. Financial Accounting Theory and Analysis: Text and Cases. 11th ed. Wiley.

Whittred, G, Zimmer, I., & Taylor, S. 2004 Financial Accounting Incentive Effects and Economic Consequences, 6th Edn, Thomson, Southbank, Vic.

The library has available many texts in this area, and the University data base has access to many academic and professional journals in this area. Journals and Periodicals Within your time constraints, you should allow 9 hours for independent study (see later in this outline), we expect you to read beyond the textbooks, especially for tutorial sessions and other tasks. If you are aiming for a distinction grade you will need to keep up to date with new issues and developments.

You can do this by reading widely, including the financial press, journals of the professional accounting bodies and some scholarly literature. In reading the scholarly literature, you should focus on the theory given at the start and end of papers. Don’t be distracted by the research methodology as your main focus is on the theory developed through research and the conclusions drawn. The following are some journals that you may find readable and useful:

− Accounting, Auditing and Accountability Journal − Accounting Forum − Accounting Horizons − Accounting Organisations and Society − Australian Accounting Review − The British Accounting Review Critical Perspectives on Accounting Useful Websites IFRS www.ifrs.org/ AASB www.aasb.gov.au/ CA www.chartere.daccountants.com.au/ CPA www.cpaaustralia.com.au/ IPA www.publicaccountants.org.au/ My Learning Online (MyLO) This unit is [web supported/web dependent/fully online], and access to the online MyLO unit is required. Log into MyLO at: http://www.utas.edu.au/learning-teaching-online and then select BFA715 Accounting Theory from the list of units. For help using MyLO go to http://www.utas.edu.au/learning-teaching-online/new-mylo/home .

7

Technical requirements for MyLO For help and information about setting up your own computer and web browser for MyLO, see: http://uconnect.utas.edu.au/

You can access the University network and MyLO via a laptop computer or other mobile device. See: http://uconnect.utas.edu.au/uana.htm

MyLO can be accessed in the Library computers and in computer labs. See: http://www.utas.edu.au/it/computing-distributed-systems/computer-labs-facilities-and-locations

For further technical information and help, contact the UTAS Service Desk on 6226 1818 or at http://www.utas.edu.au/service-desk/ MyLO Expectations 1. Students are expected to maintain the highest standards of conduct across all modes of

communication, either with staff or with other students. Penalties may be imposed if the Unit Coordinator believes that, in any instance or mode of communication, your language or content is inappropriate or offensive. MyLO is a public forum. Due levels of respect, professionalism and high ethical standards are expected of students at all times.

2. Submission of assessment tasks via MyLO presumes that students have read, understood and

abide by the requirements relating to academic conduct, and in particular, those requirements relating to plagiarism. All work submitted electronically is presumed to be “signed-off” by the student submitting as their own work. Any breach of this requirement will lead to student misconduct processes.

3. MyLO is an Internet service for teaching and learning provided by the University. It is expected

that at least once a day students will check MyLO. Student Feedback via eVALUate At the conclusion of each unit students will be asked to provide online responses to a number of matters relating to the learning and teaching within that unit. All students are asked to respond honestly to these questions, as all information received is used to enhance the delivery of future offerings. Changes to this Unit Based on Previous Student Feedback The unit will continue to focus on tutorial attendance, engagement and student leadership opportunities. Students will continue to present in tutorials though this will now be limited to 50% the tutorial time.

8

Details of Teaching Arrangements We have planned this unit to occupy, on average, 12 hours of your time for each of the 13 weeks of the semester. The hours are allocated between:

Lectures Tutorial Independent study & assignments

2 hours 1 hour 9 hours (minimum)1

12 hours per week If you are not a fast reader you may have to spend longer on independent study as it is expected that you will undertake a significant part of your learning by reading, independent study, group work and writing assignments. If you are working full time or work for more than 20 hours a week part-time you may find it very difficult to achieve the aims set for the unit. Learning expectations and strategies Expectations

The University is committed to high standards of professional conduct in all activities, and holds its commitment and responsibilities to its students as being of the utmost importance. Similarly, it has expectations about the responsibilities you, as students, have as you pursue your studies within the special environment the University offers.

The University’s Code of Conduct for Teaching and Learning states, very formally:

Students are expected to participate actively and positively in the teaching/learning environment. They must attend classes when and as required, strive to maintain steady progress within the subject or unit framework, comply with workload expectations, and submit required work on time.

This means that a lot is expected of you and of us!

This is a demanding unit worthy of an MPA course. It is planned to introduce many new, and often complex, concepts, and to extend your knowledge of the philosophy of accounting. We expect all aspects of your work to be of a high standard, including the academic content and the quality of presentation.

Learning strategies

If you are studying this unit you will already have developed learning skills and strategies that have helped you succeed in previous accounting units. However, this unit is different. It involves more reading, more theorising (and abstract thinking), a wider vocabulary of accounting terms and good verbal and writing skills. The emphasis is on reading, understanding, discussing and writing, and not on technical procedures.

It is important that you prepare before you attend classes. This means reading the textbook before lectures and writing answers to tutorial problems before tutorials. Otherwise, you will get very little benefit from attending, and won’t be able to contribute to the development of group knowledge. Encouraging you to study and learn independently is an important goal of university education. It is a

1 Some students may need to spend additional time reading and rereading material in order to understand the material.

9

feature of a reflective approach to learning in which you reflect on (think about) what it is you are learning and how you plan your learning strategy.

The tutorial sessions in particular give an interactive forum for developing and sharing ideas. Participation is an important feature of this unit, and below are some questions that are useful to think about when you discuss issues:

Are your points relevant to the discussion? Do they increase the understanding of the class?

Is there continuity in your contributions or do your comments tend to be disjointed and isolated? (The best class contributions reflect thorough preparation and good listening, interpretive and integrative skills);

Do your comments show that you are willing to put forward new and challenging ideas or are you always agreeable and “safe”?

Are you able and willing to interact with others by asking questions, providing supportive comments or challenging constructively what has been said?

Don’t be reluctant to ask questions or contribute ideas, even if only partly formed, as these are often a basis for very constructive interaction. A wrong answer is often very useful!

Depending on your reading and writing skills, you should succeed in this unit if you:

• keep up-to-date with the reading; • consolidate your reading by making appropriate short notes and summaries; • give yourself plenty of time to write your assignments; • prepare for and actively participate in the tutorial sessions; • keep your reflective learning journal up to date, and take responsibility for your own learning. If you fall behind with your reading and rush your written work you may have too much to make up before the examination and will be under-prepared. It is a risk you must consider.

You must take responsibility for your learning

Specific attendance/performance requirements It is expected that you will attend all lectures and your allocated tutorial. As with other accounting units this unit involves incremental learning, and a failure to attend may impede your progress. Activities to be undertaken in tutorials will normally be given in the tutorial. A substantial part of these activities will involve team work followed by class discussion. It is expected that you will pass each component of the assessment required in this unit. Pay particular attention to the requirements in each part of the assessment, and especially pay attention to and gain an understanding of what is meant by plagiarism and the risks of not doing so. These are important responsibilities you must accept.

You are expected to attend all timetabled sessions

(2 hours of lectures, 1 hour of tutorial per week)

Materials, audio or visual provided on MyLO DO NOT, nor are they intended to, replace attendance at lectures and tutorials. If you choose not to attend classes scheduled this as at YOUR RISK.

10

Communication, Consultation and Appointments NOTE WELL - Email Correspondence: Students are also expected to check their UTAS email site on a regular basis (at least three times a week). Students submitting requests or queries to staff via email should provide very clearly there: Family name: Preferred name; Student ID; Unit code (i.e. BFA103) and allow teaching staff at least two (2) business days to reply. Staff are not required to respond to emails in which students do not directly identify themselves, which are threatening or offensive, and that come from external (non-UTAS) email accounts. Students are advised not to have their UTAS email forwarded to an external email service (such as Gmail or Hotmail). In the past there have been significant issues where this has occurred, resulting in UTAS being blacklisted by these email providers for a period of up to one month. Assessment Assessment Schedule In order to pass this unit you must achieve an overall mark of at least 50 per cent of the total available marks. It is also expected that you pass each component of the assessment. Details of each assessment item are outlined below. Assessment Items Due Date Percentage Link to Learning

Outcomes

Task 1 Tutorial Presentation and Participation

Allocated Tutorial 25% Refer to Schedule p. 4

Task 2 Research Interest May 12th 25% Refer to Schedule p. 4

Task 3 Examination

As listed by University

50% Refer to Schedule p. 4

Total 100% Assessment Item 1 – Tutorial Presentation and Participation

Task Description: Tutorial Presentation and Participation

Task Length See p. 19 for task and team allocation. Team allocation will be made once tutorial attendance is known. Each group will compose of THREE (3) members where practical. Allocation will be random.

Assessment Criteria: Refer to detailed assessment information below.

Link to Unit’s Learning Outcomes:

Refer to p. 4

Due Date: Teams are allocated individual dates.

Value: 25% - 15% presentation, 10% attendance and participation.

11

Assessment Item 2 – Research Interest

Task Description: Research Focused Project

Task Length 3500 words

Assessment Criteria: Refer to detailed project information below

Link to Unit’s Learning Outcomes:

Refer to p. 4

Due Date: Monday 12 May. Hardcopy and Electronic Submission required.

Value: 25%

Assessment Item 3 – Closed Book Examination

Task Description: Examination

Task Length Not specified

Assessment Criteria: Refer to learning outcomes identified above

Link to Unit’s Learning Outcomes:

Refer to p. 4.

Due Date: As scheduled by Student Administration in the examination period.

Value: 50%

Your final examination for this unit will be held during the scheduled examination period as indicated by Student Administration in correspondence to you. Examinations will normally be scheduled Monday to Saturday inclusive. Examinations may be held during the day or evening and students should consult the university information which will be made available towards the end of semester. You are advised to make any necessary arrangements with employers now for time off during the examination period to sit this examination. Your participation at the scheduled time is not negotiable unless there are exceptional circumstances. Note that you will be expected to sit the examination at your recorded study centre. To find out more go to the Exams Office website: http://www.utas.edu.au/exams/home . How Your Final Result Is Determined. Your final result is determined by the sum of grades that you receive on the three assessment tasks. To obtain a pass grade or better in the unit, the sum of the weighted marks must be 50% or more of the marks available. It is expected that you pass each component of the assessment. In borderline cases for pass or honours grade your performance in tutorials and in online activities are considered in consultation with your tutor.

12

Submission of Assessment Items Lodging Assessment Items Assignments must be submitted electronically through the relevant assignment drop box in MyLO. All assessment items must be handed in by 2.00pm on the due date. Where appropriate, unit coordinators may also request students submit a paper version of their assignments. All assignments must have a TSBE Assignment Cover Sheet, which is available as a blank template from the TSBE website: [http://www.utas.edu.au/business-and-economics/student-resources]. All assignments must include your name, student ID number, tutorial day/time, and your tutor’s name. If this information is missing the assignment will not be accepted and, therefore, will not be marked. Please remember that you are responsible for lodging your assessment items on or before the due date. We suggest you keep a copy. Even in ‘perfect’ systems, items sometimes go astray. Late Assessment and Extension Policy In this Policy

1. (a) ‘day’ or ‘days’ includes all calendar days, including weekends and public holidays;

(b) ‘late’ means after the due date and time; and

(c) ‘assessment items’ includes all internal non-examination based forms of assessment

2. This Policy applies to all students enrolled in Faculty of Business Units at whatever Campus or geographical location.

3. Students are expected to submit assessment items on or before the due date and time specified in the relevant Unit Outline. The onus is on the student to prove the date and time of submission.

4. Students who have a medical condition or special circumstances may apply for an extension. Requests for extensions should, where possible, be made in writing to the Unit Coordinator on or before the due date. Students will need to provide independent supporting documentation to substantiate their claims.

5. Late submission of assessment items will incur a penalty of 10% of the total marks possible for that piece of assessment for each day the assessment item is late unless an extension had been granted on or before the relevant due date.

6. Assessment items submitted more than five (5) days late will not be accepted.

7. Academic staff do NOT have the discretion to waive a late penalty, subject to clause 4 above.

Academic Referencing and Style Guide In your written work you will need to support your ideas by referring to scholarly literature, works of art and/or inventions. It is important that you understand how to correctly refer to the work of others and maintain academic integrity.

Failure to appropriately acknowledge the ideas of others constitutes academic dishonesty (plagiarism), a matter considered by the University of Tasmania as a serious offence.

The appropriate referencing style for this unit is: the Harvard style. For information on presentation of assignments, including referencing styles: http://utas.libguides.com/referencing

13

Review of Assessment and Results Review of Internal Assessment It is expected that students will adhere to the following policy for a review of any piece of continuous/internal assessment. The term continuous/internal assessment includes any assessment task undertaken across the teaching phase of any unit (such as an assignment, a tutorial presentation, and online discussion, and the like), as well as any capstone assignment or take-home exam. Within five (5) days of release of the assessment result a student may request a meeting with the assessor for the purpose of an informal review of the result (in accordance with Academic Assessment Rule No. 2 Clause 22 – www.utas.edu.au/university-council/university-governance/rules). During the meeting, the student should be prepared to discuss specifically the marks for the section(s) of the marking criteria they are disputing and why they consider their mark(s) is/are incorrect. The assessor will provide a response to the request for review within five (5) days of the meeting. If the student is dissatisfied with the response they may request a formal review of assessment by the Head of School, with the request being lodged within five (5) days of the informal review being completed. A Review of Internal Assessment Form must be submitted with the formal review (http://www.studentcentre.utas.edu.au/examinations_and_results/forms_files/review_of_assessment.pdf). Review of Final Exam/Result In units with an invigilated exam students may request a review of their final exam result. You may request to see your exam script after results have been released by completing the Access to Exam Script Form, which is available from the TSBE Office, or at the following link – http://www.utas.edu.au/business-and-economics/student-resources. Your unit coordinator will then contact you by email within five (5) working days of receipt of this form to go through your exam script. Should you require a review of your final result a formal request must be made only after completing the review of exam script process list above. To comply with UTAS policy, this request must be made within ten (10) days from the release of the final results (in accordance with Academic Assessment Rule No. 2 Clause 22 – www.utas.edu.au/university-council/university-governance/rules). You will need to complete an Application for Review of Assessment Form, which can be accessed from www.studentcentre.utas.edu/examinations_an_results/forms_files/review_of_assessment.pdf. Note that if you have passed the unit you will be required to pay $50 for this review. The TSBE reserves the right to refuse a student request to review final examination scripts should this process not be followed.

14

Further Support and Assistance If you are experiencing difficulties with your studies or assessment items, have personal or life-planning issues, disability or illness which may affect your study then you are advised to raise these with your lecturer or tutor in the first instance. If you do not feel comfortable contacting one of these people, or you have had discussions with them and are not satisfied, then you are encouraged to contact the Director of Postgraduate Programs:

Name: Rob Hecker Room: 307 Phone: 6226 1774 Email: [email protected]

There is also a range of University-wide support services available to students, including Student Centre Administration, Careers and Employment, Disability Services, International and Migrant Support, and Student Learning and Academic Support. Please refer to the Current Students website (available from www.utas.edu.au/students) for further information. If you wish to pursue any matters further then a Student Advocate may be able to assist. Information about the advocates can be accessed from www.utas.edu.au/governance-legal/students-complaints . The University also has formal policies, and you can find out details about these policies from the following link – www.utas.edu.au/governance-legal/student-complaints/how-to-resolve-a-student-complaint/self-help-checklist. Academic Misconduct and Plagiarism Academic misconduct includes cheating, plagiarism, allowing another student to copy work for an assignment or an examination, and any other conduct by which a student: (a) seeks to gain, for themselves or for any other person, any academic advantage or advancement to

which they or that other person are not entitled; or (b) improperly disadvantages any other student.

Students engaging in any form of academic misconduct may be dealt with under the Ordinance of Student Discipline. This can include imposition of penalties that range from a deduction/cancellation of marks to exclusion from a unit or the University. Details of penalties that can be imposed are available in the Ordinance of Student Discipline – Part 3 Academic Misconduct, see http://www.utas.edu.au/universitycouncil/legislation/. Plagiarism is a form of cheating. It is taking and using someone else’s thoughts, writings or inventions and representing them as your own, for example:

• using an author’s words without putting them in quotation marks and citing the source; • using an author’s ideas without proper acknowledgment and citation; or • copying another student’s work. • using ones’ own work from previously submitted assessment items if repeating a unit.

15

If you have any doubts about how to refer to the work of others in your assignments, please consult your lecturer or tutor for relevant referencing guidelines, and the academic integrity resources on the web at http://www.academicintegrity.utas.edu.au/ The intentional copying of someone else’s work as one’s own is a serious offence punishable by penalties that may range from a fine or deduction/cancellation of marks and, in the most serious of cases, to exclusion from a unit, a course, or the University. The University and any persons authorised by the University may submit your assessable works to a plagiarism checking service, to obtain a report on possible instances of plagiarism. Assessable works may also be included in a reference database. It is a condition of this arrangement that the original author’s permission is required before a work within the database can be viewed. For further information on this statement and general referencing guidelines, see http://www.utas.edu.au/plagiarism/ or follow the link under ‘Policy, Procedures and Feedback’ on the Current Students homepage.

16

Study Schedule Unit Schedule – Lecture Presentations, Pre Reading and Question Completion Requirements

Lecture Week Beginning Text Reading* Questions**

Feb 24 Introduction Ch1 1.1, 1.7, 1.11, 1.14, 1.15, 1.22

Mar 3 Reporting Environment and Regulation

Ch2 and 3 2.3, 2.5, 2.13, 2.19, 3.5, 3.6, 3.13, 3.29

17 International Accounting Ch4 4.3, 4.4, 4.9, 4.17, 4.25, 4.34

24 Measurement Issues Ch5 5.1, 5.8, 5.13, 5.19, 5.24, 5.29

31 Conceptual Frameworks Ch6 6.2, 6.7, 6.17, 6.19, 6.26, 6.31

Apr 7 Positive Accounting Theory Ch7 7.3, 7.11, 7.18, 7.22, 7.24, 7.31

14 Systems Theories Ch8 8.1, 8.7, 8.17, 8.26, 8.30, 8.34

Mid-Semester Break: Easter Friday 18 – Friday 25 April inclusive

Apr 28 Corporate Accountability Ch9 9.2, 9.10, 9.16, 9.18, 9.24, 9.28, 9.39

May 5 Capital Markets Theory Ch10 10.1, 10.10, 10.19, 10.21, 10.26

12 Behavioural Research Ch11 11.5, 11.10, 11.15, 11.19

19 Critical Perspectives Ch12 12.1, 12.6, 12.8, 12.16, 12.18, 12.19

26 Revision

June 2-3 Available for Consultation

Examination Period: 7 – 24 June 2014

* You must read the textbook and any supplementary readings recommended before classes each week.

** If time permits you should think about all questions. The ones noted will be those given preference in tutorials and need to be considered prior to the respective tutorial

17

Assessment Assessment schedule

Task Assessment Dates due Percent weighting

Task 1 Tutorial Presentation and Participation Team Dates and Attendance 25%

Task 2 Research Interest 12 May 25%

Exam End of semester exam – 3 hours 50 %

100%

Assessment task 1 –Tutorial Activity – 25%

Task description: See p.19 for task and team allocation. Team allocation will be made once tutorial attendance is known. Each group will compose of THREE (3) members.

Task length

One tutorial plus preparation time

Links to learning outcomes:

Refer to the table on page 4

Assessment criteria: Refer to the table on page 4

Date due: Team presentation date (as advised on MyLO and/or by your tutor)

Tutorials The tutorials form an important part of your assessment in this unit. Once you are allocated to tutorials you will be allocated ‘team partners’. Teams will consist of THREE (3) students. When enrolling be very careful to AVOID enrolling in units in which there are clashes with this unit that you will not be able to avoid. Such justification is NOT an acceptable reason for not attending tutorials. On enrolment it is your responsibility to ensure you are able to attend the class requirements of each unit.

Team Roles in Tutorials On the allocated date YOUR team will be responsible for the conduct of approximately 50% of the tutorial time. It will be your responsibility to lead a presentation and discussion in relation to the case studies or academic journal articles allocated to your team. Your tutor will be there to facilitate but the conduct of your team’s part of the tutorial will be your team’s responsibility. It is your presentation it is therefore up to you to choose the manner of presentation.

18

Tutorial Assessment A total of 25% has been allocated to tutorials this semester. It will be divided in the following way:

Task Marks

Presentation – information to tutor and to tutorial group

Presentation of the tutorial – at tutorial

15%

Attendance and participation at tutorials (2 parts as below) 10%

Total 25%

Attendance Percentage Number of Tutorials Attended

Assessment to maximum 5%

12-13 5%

8-11 3.5%

5-7 2.5%

3-4 1%

<3 0%

Participation Requirements

Performance Indicators

1 Attendance at tutorial

2 Evidence of pre reading for the tutorial

3 Questions asked

4 Response in discussion/argument

5 Evidence of wider reading

6 Evidence of innovative thinking (eg. problem resolution)

19

Task 1 - Academic Journal Articles – Team Presentations Task 1 - Tutorial Schedule

Lecture Week Beginning Presentation Articles Names (3 students per team)

Feb 24 1 No Student Presentation

Mar 3 2 No Student Presentation

Mar 17 3 Accountability Articles

Mar 24 4 Information Systems Articles

Mar 31 5 Research 1 Articles

Apr 7 6 Legitimacy Theory Articles

Apr 14 7 Culture 1 Articles

Apr 28 8 Positive Accounting Articles

May 5 9 Disclosure 1 Articles

May 12 10 Motivation 1 Articles

May 19 11 Sustainability Articles

May 26 12 No Student Presentation

20

Articles Accountability

Richards, Tamara and Debbie Dickinson. 2007. Guidelines by stakeholders, for stakeholders. JCC. 25. pp.19-21.

Canadian Democracy and Corporate Accountability Commission. 2002. The New Balance Sheet. Corporate Profits and Responsibility in the 21st Century. Jan.

Batten, Jonathan, Samanthala Hettihewa, and Robert Mellor. 1997. The ethical management practices of Australian firms. Journal of Business Ethics. 16/12-13. pp.51-61.

Everson, Miles, Charles Ilako and Carlo di Florio. 2003. Corporate governance, business ethics and global compliance management. ABA Bank Compliance. 24/3. pp.22-32.

Painter-Morland, Mollie. 2007. Defining accountability in a network society. Business Ethics Quarterly. 17/3. pp.515-534.

Information Systems

Brown, Darrell L., Jesse F. Dillard and R. Scott Marshall. 2005. Strategically informed, environmentally conscious information requirements for Accounting Information Systems. Journal of Information Systems. 19/2. pp.79-103.

Bradley, Randy V., Jeannie L. Pridmore and Terry Anthony Byrd. 2006. Information systems success in the context of different corporate cultural types: an empirical investigation. Journal of Management Information Systems. 23/2. pp.267-294.

Bennett, Mark and Jeffrey Unerman. Towards universally acceptable corporate social responsibilities through internet stakeholder discourse.

Wheeler, Patrick R., James E. Hunton and Stephanie M. Bryant. 2004. Accounting information systems research opportunities using personality type theory and the Myers-Briggs type indicator. Journal of Information Systems. 18/1. pp.1-19.

Wheeler, Patrick R., James E. Hunton and Stephanie M. Bryant. 2004. Authors’ reply to commentary on accounting information systems research opportunities using personality type theory and the Myers-Briggs type indicator. Journal of Information Systems. 18/1. pp.35-38.

Research 1

Miley, Frances and Andrew Read. 2012. Jokes in popular culture: the characteristics of the accountant. Accounting, Auditing and Accountability Journal. 25/4. pp.703-718.

Chalmers, Keryn, Jayne M. Godfrey and Barbara Lynch. 2012. Regulatory theory insights into the past, present and future of general purpose water accounting standard setting. Accounting, Auditing and Accountability Journal. 25/6. pp.1001-1024.

MacKenzie, Kim, Sherrena Buckby and Helen Irvine. 2013. Business research in virtual worlds: possibilities and practicalities. Accounting, Auditing and Accountability Journal. 26/3. pp.352-373.

Jeacle, Ingrid. 2012. Accounting and popular culture: framing a research agenda. Accounting, Auditing and Accountability Journal. 25/4. pp.580-601.

Lehman, Cheryl. 2012. We’ve come a long way! Maybe! Re-imagining gender and accounting. Accounting, Auditing and Accountability Journal. 25/2. pp.256-294.

21

Legitimacy Theory

Tilling, Matthew. Refinements to legitimacy theory in social and environmental accounting. Commerce Research Paper Series No. 04-6. ISSN: 1441-3906.

Emtairah, Tareq and Oksana Mont. 2008. Gaining legitimacy in contemporary world: environmental and social activities of organisations. International Journal of Sustainable Society. ½. pp.134-148.

Tregidga, Helen, Marcus Milne and Kate Kearins. Organisational legitimacy and social and environmental reporting research: the potential of discourse analysis.

Guthrie, James, Suresh Cugabesan and Leanne Ward. Legitimacy theory: a story of reporting social and environmental matters within the Australian food and beverage industry.

Suchman, Mark. 1995. Managing Legitimacy: strategic and institutional approaches. Academy of Management Review. 20/3. pp.571-610.

Culture 1

Tsakumis, George T. 2007. The influence of culture on accountants’ application of financial reporting rules. ABACUS. 43/1. pp.27-48.

Gordon, Elizabeth A., Adam Greiner, Mark J. Kohlbeck, Steven Lin, and Hollis Skaife. 2013. Challenges and opportunities in cross country accounting research. Accounting Horizons. 27/1. pp.141-154.

Wong-on-Wing, Bernard and Gladie Lui. 2013. Beyond cultural values: an implicit theory approach to cross-cultural research in accounting ethics. Behavioural Research in Accounting. 25/1. pp.15-36.

Askary, Saeed. 2006. Accounting professionalism – a cultural perspective of developing countries. Managerial Auditing Journal. 21/1-2. pp.102-111.

Ali, Muhammad Jahangir. 2005. A synthesis of empirical research on international accounting harmonisation and compliance with international financial reporting standards. Journal of Accounting Literature. 24. pp.1-52.

Positive Accounting

Christenson, Charles. 1983. The methodology of positive accounting. The Accounting Review. LVIII/1. Jan. pp.1-22.

Watts, Ross L. and Jerold L. Zimmerman. 1990. Positive Accounting Theory: A ten year perspective. The Accounting Review. 65/1. Jan. pp.131-156.

Bennett, Bruce, Michael Bradbury and Helen Prangnell. 2006. Rules, principles and judgements in Accounting Standards. ABACUS. 42/2. Pp.189-204.

Adams, Michael B. 1994. Agency theory and the internal audit. Managerial Auditing Journal. 9/8. pp.8-12.

Lambert, Richard A. 2001. Contracting theory and accounting. Journal of Accounting and Economics. 32. pp.3-87.

Disclosure 1

Hess, David and Thomas W. Dunfee. 2007. The Kasky-Nike threat to corporate social reporting. Business Ethics Quarterly. 17/1. pp.5-32.

22

Hasnas, John. 2007. Up from the flatland: Business ethics in the age of divergence. Business Ethics quarterly. 17/3. pp.399-426.

Adams, Mike. 1997. Ritualism, opportunism and corporate disclosure in the New Zealand life insurance industry: field experience. Accounting, Auditing and Accountability Journal. 10,5. pp.718-734.

Barako, Dulacha, G., Phil Hancock and H.Y.Izan. 2006. Factors influencing voluntary corporate disclosure by Kenyan companies. Corporate Governance. 14/2. March. pp.107-125.

Campbell, David. 2004. A longitudinal and cross sectional analysis of environmental disclosure in UK companies – a research note. The British Accounting Review. 36. pp.107-117. Motivation 1

Gonzalez-Benito, Javier and Oscar Gonzalez-Benito. 2005. A study of the motivations for the environmental transformation of companies. Industrial marketing management. 34. pp. 462-475.

Deegan, Craig, Michaela Rankin, and Peter Voght. 2000. Firms’ disclosure reactions to major social incidents: Australian evidence. Accounting Forum. 24/1. March. pp.101-130.

Tilt, Carol. 2001. The content and disclosure of Australian corporate environmental policies. Accounting, Auditing and Accountability Journal. 14,2. pp.190-212.

Kolk, Ans. 2005. Environmental reporting by multinationals from the Triad: convergence or divergence? Management International Review. 45/1. pp.145-166.

Adams, Carol. 2002. Internal organisational factors influencing corporate social and ethical reporting – beyond current theorising. 15/2. pp.223-250.

Sustainability

Bebbington, Jan and Rob Gray. 2001. An account of sustainability: failure, success and a reconceptualization. Critical Perspectives on Accounting. 12. pp.557-587.

Birkin, Frank, Pam Edwards, and David Woodward. 2003. Accounting’s contribution to a conscious cultural evolution: an end to sustainable development. Critical Perspectives on Accounting.

Luken, Ralph A. and Paul Hesp. 2007. The contribution of six developing countries’ industry to sustainable development. Sustainable Development. 15. pp.242-253.

Dyllick, Thomas and Kai Hockerts. 2002. Beyond the business case for corporate sustainability. Business Strategy and the Environment. 11. pp.130-141.

Chang, Dong-shang and Li-chin Regina Kuo. 2008. The effects of sustainable development on firms’ financial performance – an empirical approach. Sustainable Development.

Milne, Marcus J., Kate Kearins, and Sara Walton. 2006. Creating adventures in wonderland: the journey metaphor and environmental sustainability. Organization. 13/6. pp.801-839.

A Touch of Critical Plus 1

Choudbury, Masudul Alam. 1996. Markets as a system of social contracts. International Journal of Social Economics. 23/1. pp.17-36.

Rowley, Tim and Shawn Berman. 2000. A brand new brand of corporate social performance. Business and Society. 39/4. pp. 397-418.

23

Lehman, Glen. 1999. Disclosing new worlds: a role for social and environmental accounting and auditing. Accounting, Organisations and Society. 24. pp.217-241.

Lehman, Cheryl. 2005. Accounting and the public interest. All the world’s a stage. Accounting, Auditing and Accountability Journal. 18/5. pp.675-689.

Bebbington, Jan and Rob Gray. 1999. Seeing the wood for the trees. Taking the pulse of social and environmental accounting. 12/1. pp.47-51.

NOTE: The academic articles for each presentation will be loaded under ‘extra resources’. These are your primary source of information from which to prepare though you may seek additional resources should you choose. The academic articles for each presentation will be loaded under ‘extra resources’. I will load a document with the articles linked to each topic, and then load each of the articles.

24

BFA 715 Accounting Theory Criteria sheet for tutorial presentations

Criteria HD (High Distinction) DN (Distinction) CR (Credit) PP (Pass) NN (Fail)

Preparation Prepared seminar presentation including visual materials and appropriate questioning of group. Group displayed interest.

Prepared seminar presentation but visual materials or questioning did not embrace the case/academic journal adequately.

Prepared seminar presentation but visual materials or questioning - basic

Evidence of little effort. Issues not addressed. Questioning and audience interaction minimal.

No preparation/ad hoc presentation

Analysis Identified all the points in the case/article which should be addressed and comprehensively analysed and evaluated each point.

Identified most points in the case/article that should be addressed and analysed and evaluated each point.

Identified most points in the case/article that should be addressed and a reasonable analysis and evaluation of each point.

Identified some points in the case/article that should be addressed but a limited analysis and evaluation indicating only a partial understanding of the topic.

Identified few or no points in the case/article that should be addressed and analysed and evaluated each point inadequately.

Respond to questions raised by audience and or lecturer

Responded successfully to all questions and supported responses with authorities from the literature and/or logical reasoning

Responded successfully to some questions and supported responses with authorities from the literature and/or logical reasoning

Responded successfully to some questions but did not support them all with authorities from the literature and/or logical reasoning

Did not respond to any questions successfully and did not support them all with authorities from the literature and/or logical reasoning

Engage with audience

Engaged audience by: • maintaining eye contact,

using suitable gestures and body language

• responding to the audience in a confident manner

• a conversational tone • fluent speech without

reading notes • questioning to suit content,

audience and purpose • clarified content with real

world examples

Engaged audience by • maintaining eye contact, using suitable gestures and body

language • responding to the audience in a confident manner • a conversational tone • fluent speech without reading notes • questioning to suit content, audience and purpose • clarified content with real world examples

Partially engaged audience by: • occasionally making eye

contact and using limited gestures and body language

• responding to the audience in a hesitant manner

• halting speech with some reading of notes

• questioning that suits content, audience and purpose to some extent

• did not clarifiy content with real world examples

Sat in front of an audience and: occasionally made eye contact asked questions from a script/slides may have acknowledged their responses

25

Date: ______________________________________________________________________________________________________________

ID Name

Criteria - Skill/Qualities Assessed Level

Basic Criteria Indicators of Quality Excellent Very Good Good Poor Not at All

Preparation Hardcopy/electronic copy received before tutorial

Evidence of pre reading/analysis/critique

Power point or other visual aids

Evidence of wider reading/supportive materials

Summary materials made available tutorial members

Questions to be asked of tutorial members

Analysis Hardcopy evidences understanding/critique of area

Identified issues/points of interest/deficiencies

Introduced additional material

Response to audience Asked audience questions

Responded to questions from audience

Able to offer ‘quality’ responses

26

Engaged Audience Eye contact

Visual body cues

Confident manner

Fluent no reference to notes

Involved audience

As appropriate used examples

27

Task 2 – Research Focused Project - 25%

This project is intended to introduce you to the research process that underlies much of the work and theoretical discussions you have undertaken this semester. You will need to draw on skills learnt and on your thinking about the information provided in lectures and in the textbook, in the tutorials and through the academic journal articles you have read this semester.

This task will be completed in a number of parts identified below:

1. Identify an area of research that you believe is both important and of interest to you, and write a

short paragraph indicating why you believe this area of research is important, and why it is interest to you. (350 words)

2. Briefly describe the research problem you would like to explore. Identify a research question

that would lead your exploration of the problem. (250 words) 3. Find TEN (10) academic journal articles that relate to your area of research interest – write a

maximum of ten lines for each article indicating why that article is relevant to your research, and why the information will contribute to being able to support the research investigation proposed. (1400 words max)

4. Normally when undertaking research we would have expectations about what the findings might

be. In responding to your research question what result(s) would you expect to find? (200 words) 5. In 500 words indicate which of the accounting theories you have studied this year would help to

you explain the expectations you have for your research question. What role would this theory play in your research? Why this theory more appropriate than other choices?

28

6. How would you collect the data to respond to your research question? Why do you think this approach is appropriate? For example, searching a data base, content analysis of annual reports, a mail, internet or telephone survey, conduct of interviews. (200 words).

7. Do you think that ethical considerations are important to your research? In undertaking

research at UTAS ethical approval is required. What do you need to do at UTAS to obtain ethical approval? (200 words)

8. In seeking to respond to your Research Question(s) what questions would you need to ask

respondents, or what questions would you need to ask to interrogate data collected from a data base or an annual report? Identify TEN (10) questions that you believe would need to be asked, and indicate why these questions would need to be asked to gather the information you require to respond to your research question. (400 words)

Task length

A maximum of 3500 words

The word limit specified for your assignment is a maximum. If you submit over-length work there is an automatic 10% penalty of available marks. It is at the discretion of the Unit Coordinator whether the words beyond the limit will be assessed. Title pages, reference lists and appendices are not included in word counts.

Links to learning outcomes:

Refer to the table on page 4.

Assessment criteria:

Marks awarded will be based on the criteria stated on page 4 but students also need to demonstrate the following skills: evidence of research; relevance and understanding of the issues and concepts; strength of argument developed; use of language; quality of explanations and presentation style; readability of the essay and use of Harvard referencing.

Date due: Monday 12 May 2014.

29

Student Id: __________________ Name: ________________________________

BFA 715 Accounting Theory

Criteria sheet – Research Focused Projects

Criteria HD (High Distinction) DN (Distinction) CR (Credit) PP (Pass) NN (Fail)

Area of Interest

Clear, Coherent with Strong, Logical Justification

Clear and Coherent with Logical Justification

Clear and Coherent with Justification

Clear but Justification weak Confused

Research Question

Well written, testable and focused

Well written and testable Well written but general in nature Question identified but not well written and untestable

Not clear, poorly focused, untestable, general

Academic Articles

ALL articles justified in terms of the research question, relevance clear

MOST articles justified in terms of the research question, relevance clear

SOME articles justified in terms of the research question, relevance clear

Provide an article summary with little justification or links to the research question

Articles not relevant to the research question

Expectations Expectations clearly identified and briefly justified or the link is clear from what had been discussed in previous answers.

Expectations clear but not justified or no clear link. No clear expectations

Accounting Theories

A specific link to theory made and justified

A specific link to theory made but lacks justification

A tenuous link to theory is made but lacks justification

Attempts to link multiple theories without justification

No link to theory made

Data Collection

Appropriate method(s) identified briefly discussed and justified in terms of the research project

Appropriate methods identified but not clearly justified in terms of the research project

Methods not identified or general and vague in relation to proposed research project

Ethics

Able to clearly explicate ethical requirements and processes, and able to relate these to the proposed research project if applicable (or explain why not).

Able to explicate ethical requirements and processes, but does not draw links to the proposed research project (or explain why it is not applicable).

No understanding of ethical requirements demonstrated

Question Development

ALL Questions are clear, well written, appropriate and linked to the data requirements for the research project with justification.

MOST Questions are clear, well written, appropriate and linked to the data requirements for the research project with justification.

SOME Questions are clear, well written, and appropriate and linked to the data requirements for the research project with justification.

Questions are clear and well written but lack justification or would not meet the data requirements for the project.

No questions or poorly written and inappropriate to research question

Overall An excellent, executable and well justified research project .

A very good executable research project with minor changes required.

A good executable research project with major changes in one or two areas.

A satisfactory idea for a research project but would require major changes prior to execution.

The research project could not be implemented.

30

Sample of Assessment – checklist

Assessment of Learning outcomes

(Assessor to CROSS appropriate box)

Strongly Agree Agree Neutral Disagree Strongly

Disagree

Student demonstrates an understanding of different theoretical perspectives and issues is developed

1 2 3 4 5

Student demonstrates an understanding of emerging theoretical perspectives and issues is evidenced

1 2 3 4 5

Student displays quality written communication skills evidenced in the presentation of this assignment

1 2 3 4 5

Student demonstrates evidence of an ability to draw out the main theoretical issues of this discussion and critically reflect upon them.

1 2 3 4 5

Final Exam – 50%

Description/conditions Closed book examination – 3 hours duration + 15 minutes reading time

The exam will require you to demonstrate the breadth and depth of your understanding across all the course topics. All topics are examinable but you will be given some direction in the revision week.

Date The final exam is conducted by the University Registrar in the

formal examination period. See the Current Students homepage on the University’s website.