berry petroleum company ipaa ogis - new york – april 20, 2004 1 berry petroleum company safe...

TRANSCRIPT

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

1

Berry Petroleum Company

Safe Harbor Statement

Safe Harbor under the Private Securities Litigation Reform Act of 1995: With the exception of historical information, the matters presented in this presentation or associated documents are forward-looking statements that involve risks and uncertainties. Although the Company believes that its expectations are based on reasonable assumptions, it can give no assurance that its goals will be achieved. Important factors that could cause actual results to differ materially from those in the forward-looking statements herein include, but are not limited to, the timing and extent of changes in the commodity prices for oil, natural gas and electricity, a limited marketplace for electricity sales within California, counterparty risk, competition, environmental and weather risks, litigation uncertainties, drilling, development and operating risks, uncertainties about the estimates of reserves, the availability of drilling rigs and other support services, legislative and/or judicial decisions and other governmental regulations.

Presented byRalph J. Goehring - Senior Vice President and Chief Financial Officer

April 20, 2004 - IPAA OGIS

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

2

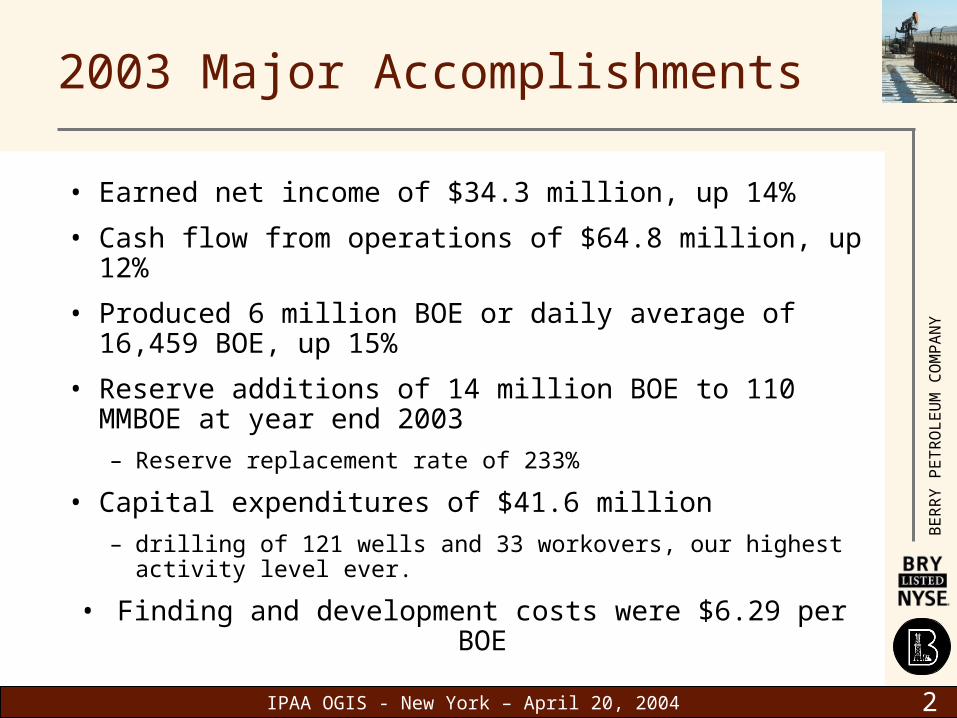

2003 Major Accomplishments

• Earned net income of $34.3 million, up 14%

• Cash flow from operations of $64.8 million, up 12%

• Produced 6 million BOE or daily average of 16,459 BOE, up 15%

• Reserve additions of 14 million BOE to 110 MMBOE at year end 2003

– Reserve replacement rate of 233%

• Capital expenditures of $41.6 million

– drilling of 121 wells and 33 workovers, our highest activity level ever.

• Finding and development costs were $6.29 per BOE

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

3

2004 Targets Include

• Growing production by 24% over 2003 to approximately 20,500 BOE per day

• Capital expenditures of $50 million plus

• Increasing earnings

• Increasing cashflow

• Adding significant new reserves

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

4

BRY Background Summary

• Independent oil and gas producer

– Founded 1909 in California, currently 131 employees

– Headquarters in Bakersfield, California with Denver, CO office to operate Rocky Mountain assets

• Financial overview

– Current borrowing base - $200 MM, outstanding - $50 MM

– Dividend $.44/share – approx. a 1.6% yield

– Total shares outstanding - Approx. 22 million

• Cogeneration (Steam & Electricity) Assets

– Three cogeneration facilities

– Provides economical steam

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

5

Primary Producing Asset Locations

Brundage Canyon Field - Uinta Basin ,UT

Midway-Sunset Field - San Joaquin Valley Basin, CA

Placerita Field - Los Angeles Basin, CA

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

6

Midway-Sunset Field - San Joaquin Basin

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

7

Midway-Sunset Field, CA

• Asset type – Heavy crude oil - EOR

• Berry operating since 1909

• Total average daily production (BOE)

– 2001 10,314 BOE per day

– 2002 10,722 BOE per day + 4%

– 2003 11,502 BOE per day + 7%

• Target production

– 2004 12,200 BOE per day + 6%

• Reserves - 73.4 MMBOE; 67% of total

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

8

Placerita Field - LA Basin

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

9

Placerita Field, CA

• Asset type – Heavy crude oil - EOR

• Berry operating since 1999

• Total average daily production (BOE)

– 2001 2,659 BOE per day

– 2002 2,627 BOE per day - 1%

– 2003 3,214 BOE per day + 22%

• Target production

– 2004 3,400 BOE per day + 5%

• Reserves - 18.4 MMBOE; 17% of total

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

10

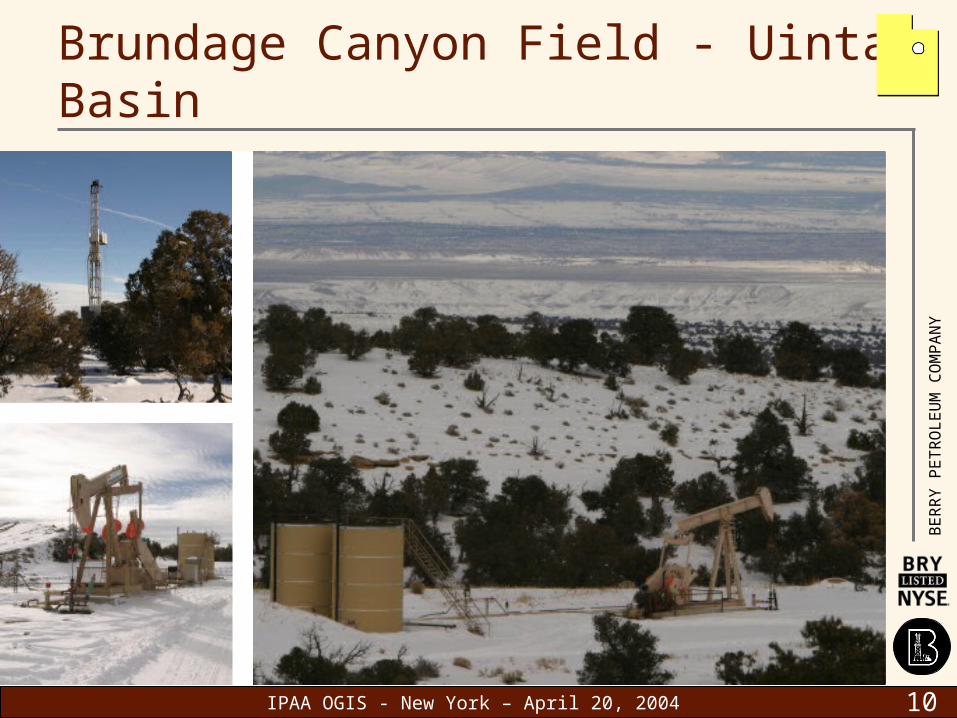

Brundage Canyon Field - Uinta Basin

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

11

Brundage Canyon Field, UT

• Asset Type – 75% Light Crude – 25% Gas

• Berry operating since August 2003

• Total average daily production (BOE)

– 2003 2,111 BOE per day (fourth quarter)

• Target production

– 2004 4,100 BOE per day + 49%

• Reserves - 9.2 MMBOE; 8% of total

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

12

HeatZone

HeatZone

Viscous(Thick)

Oil

Viscous(Thick)

Oil

Viscous(Thick)

Oil

Condensed Steam(Hot Water)

Heated ZoneCondensed Steam

and Thinned Oil

DepletedOil Sand

Injection Soak Production

Injected Steam

Condensed Steam(Hot Water)

Area Heated byConvection From

Hot Water

ProducedFluids

From SteamGenerator

~7000 bbl 3-7 days 6 monthsApprox. 7,000 Bbls of steam Soaks for 3-7 days Produces for 6 months

Cyclic Steam Injection (EOR)

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

13

Cogeneration Summary

• Facilities provide:

– 57% of steam generation

– natural hedge with natural gas prices

– competitive advantage over other heavy oil operators

• Units positioned in key producing areas

– Midway-Sunset Field

•38 MW, to PG&E under contract*

•18 MW, to PG&E under contract*

– Placerita Oilfield

•21 MW, 7.2 ¢/Kwh to 2006 - SRAC to 2009 - SoCal Edison (SCE)

•21 MW, to SCE under contract*

*Have contracts for 2004 electricity

*Negotiating and reviewing 5-year electricity contracts

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

14

Historical Crude Oil Prices

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

15

Crude Oil Sales

California• SJV heavy differential to WTI remains tight

– California refineries designed for heavy crude slate

– California production remains low from energy crisis

• Have crude oil sales contract with a major refiner through 2005, with fixed differential to WTI

Rocky Mountains• Have crude oil sales contract with a major

• Approximates WTI less $2.00 per Bbl

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

16

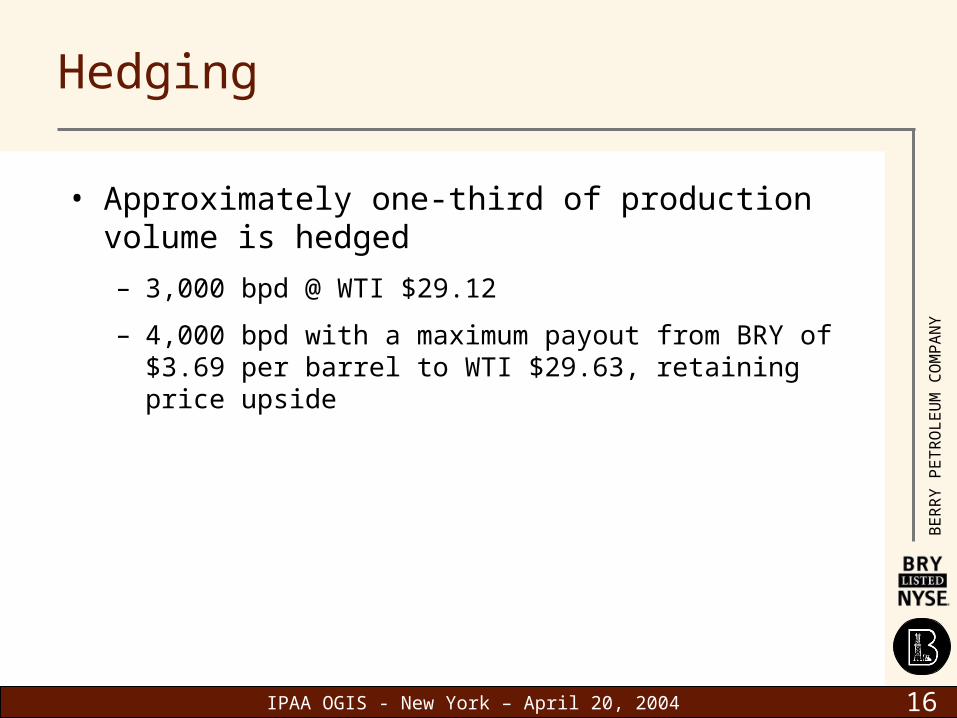

Hedging

• Approximately one-third of production volume is hedged

– 3,000 bpd @ WTI $29.12

– 4,000 bpd with a maximum payout from BRY of $3.69 per barrel to WTI $29.63, retaining price upside

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

17

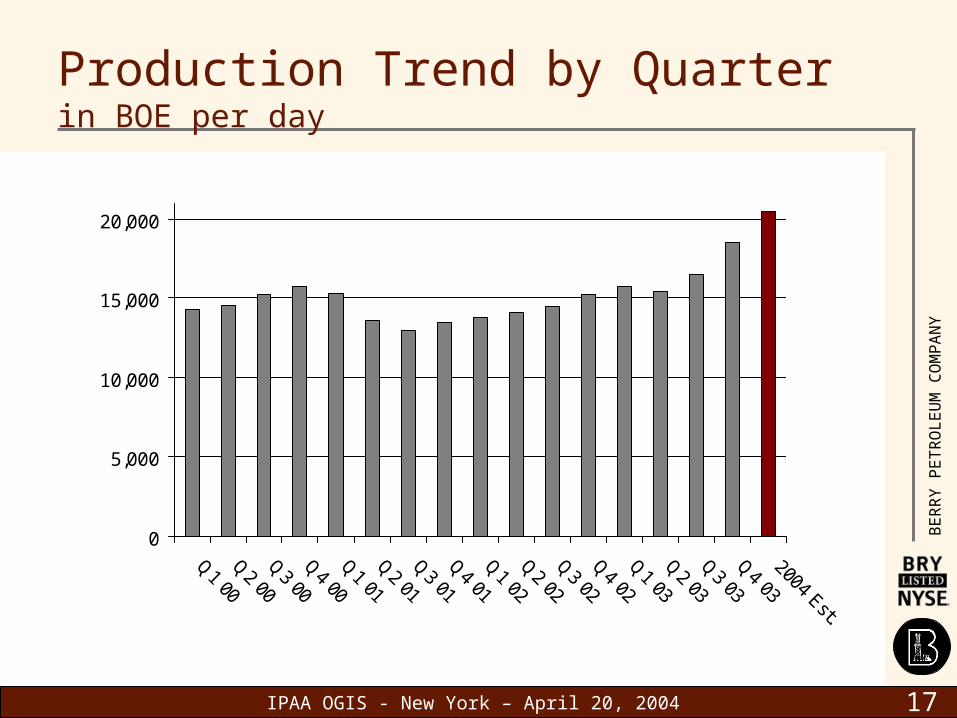

Production Trend by Quarterin BOE per day

0

5,000

10,000

15,000

20,000

Q1 00

Q2 00

Q3 00

Q4 00

Q1 01

Q2 01

Q3 01

Q4 01

Q1 02

Q2 02

Q3 02

Q4 02

Q1 03

Q2 03

Q3 03

Q4 03

2004 Est.

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

18

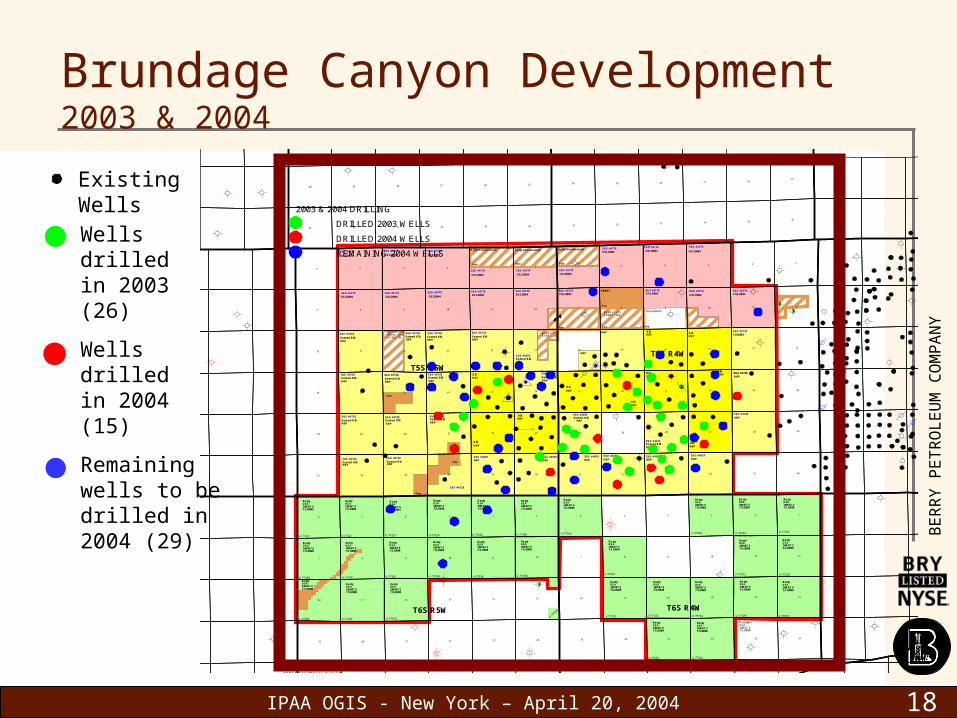

Brundage Canyon Development2003 & 2004

T5S R4W

T5S R5W

T6S R4WT6S R5W

282829

123456

7 9 10 11 12

131415161718

19 20 21 22 23 24

2527282930

32 33

3

10

1314

21 22 23 24

25262728

5

10

19 23 24

10

131518

21 22 24

252627

293025262730

363534333231363534333231

12456

81211987

15161718

2019

262930

3635343134 35 36333231

12341 623456

1211912 7 811987

13141518 17 16141617

2221202319 20

BERRY

Fee

FeeFee Fee

Fee

Fee

Fee

Fee

BERRY - 73%SHEN. - 22%OPEN - 5%

BERRY - 67%SHEN. - 33%

BERRY - 67%SHEN. - 33%

Shenandoah

Berry/Shenandoah Berry/Shenandoah Berry/Shenandoah

Fee Fee

3/11/2004

3/11/2004

3/11/2004 3/11/2004

3/11/2004 3/11/2004

3/11/2004

3/11/2004

3/11/2004

3/11/2004 3/11/2004

3/11/2004

3/11/2004 3/11/2004 3/11/2004

3/11/20043/11/2004 3/11/2004

E&D #4778 E&D #4778 E&D #4778

E&D #4778 E&D #4778 E&D #4778

E&D #4778 E&D #4778 E&D #4778

E&D #4778E&D #4778E&D #4778E&D #4778E&D #4778E&D #4778E&D #4778 E&D #4778E&D #4778

7/2/2003E&D #4728 E&D #4728

E&D #4728

E&D #4728E&D #4728

E&D #4728 E&D #4728

E&D #4728 E&D #4728

E&D #4728

E&D #4728

E&D #4728

E&D #4728

HBPHBP

HBP

HBP

HBP

HBPHBP

HBP

HBP

BIA BIA

BIABIA

BIA

BIA

BIA

BIA

BIA

Earned BIA

Earned BIA

HBP

HBP

HBP

HBPEarned BIA

Earned BIAHBP

HBP

Earned BIAHBP

HBPEarned BIA Earned BIA

HBP

E&D #4659

E&D #4659

E&D #4659

E&D #4659E&D #4728E&D #4728

E&D #4728

BIA

E&D #4659 E&D #4659 E&D #4659 E&D #4659 E&D #4659 E&D #4659

HBP HBP HBP HBP HBP

HBP

Earned BIAEarned BIAHBPHBP

HBP

HBP

Earned BIA

Earned BIA Earned BIA

Earned BIA Earned BIA

HBP HBP

HBP

Earned BIA Earned BIAHBP HBP

HBP

HBP

HBP

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

BerryUSA100/87.57/1/2008

U-77323

U-77323

U-77321U-77321U-77321

U-77323

MedallionUSA100/87.57/1/2008

U-77322

U-77322

U-77324U-77324

U-77324U-77325

U-77325U-77325

U-77326U-77326U-77326U-77327U-77327U-77327

U-77328 U-77328

U-77328 U-77329 U-77329

U-77329 U-77330 U-77330 U-77330

X

2003 & 2004 DRILLING

DRILLED 2003 WELLS

DRILLED 2004 WELLS

REMAINING 2004 WELLS

PETRA 3/18/2004 11:39:49 AM

Wells drilled in 2003 (26)

Wells drilled in 2004 (15)

Remaining wells to be drilled in 2004 (29)

Existing Wells

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

19

Total Proved ReservesIn million BOE

113107 103 102

110

0

20

40

60

80

100

120

1999 2000 2001 2002 2003

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

20

Proved Reserve MixBy geography in BOE

CaliforniaRockies

CaliforniaRockies

At 12/31/02 At 12/31/03

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

21

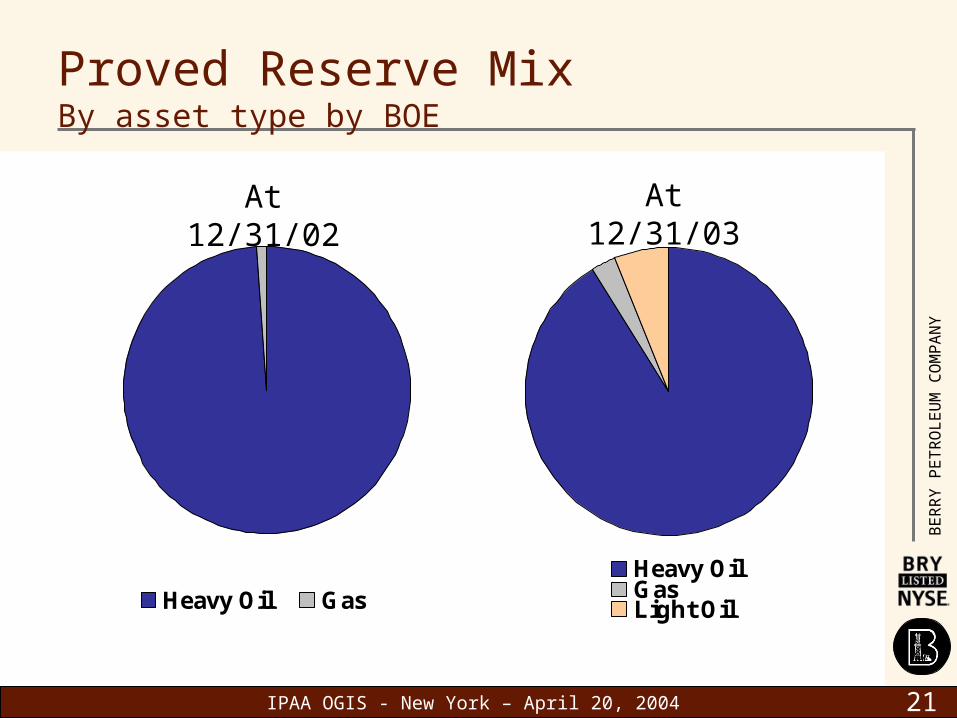

Proved Reserve MixBy asset type by BOE

Heavy Oil GasHeavy OilGasLight Oil

At 12/31/02 At 12/31/03

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

22

Berry’s Plan to Achieve Growth Targets

Two key elements to growth strategy:

1.Maximize production from existing assets

2. Add reserves through:

a. development

b. acquisitions

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

23

Maximizing Production for Growth

• Continue drilling at Brundage Canyon

• Focus on five new EOR projects in California

• Exploitation team to focus on unproven reserves

• Utilize technology, squeeze more barrels out of older reservoirs

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

24

Acquisition Focus

• Expand acreage position near Brundage Canyon; focus on light oil reserves and natural gas

• Add new field in the Rockies with growth opportunities

• Add properties in California which are strategic

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

25

Financial Review

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

26

Revenuesin millions

$67

$172

$139 $133

$181

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

1999 2000 2001 2002 2003

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

27

Net Income & Cash Flow In millions of dollars

$24.8

$65.9

$35.4

$57.9

$64.8

$37.2

$21.9

$30.0$34.3

$18.0

$0

$10

$20

$30

$40

$50

$60

$70

1999 2000 2001 2002 2003

Cash Flow Net Income

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

28

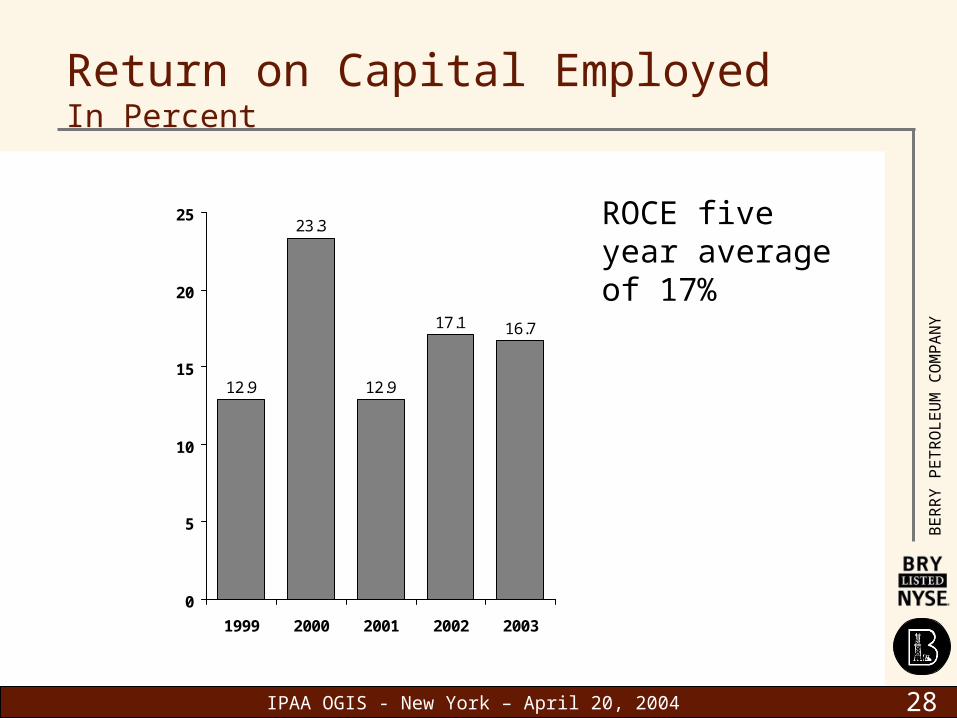

Return on Capital EmployedIn Percent

ROCE five year average of 17%

12.9

23.3

12.9

17.1 16.7

0

5

10

15

20

25

1999 2000 2001 2002 2003

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

29

Return on EquityIn Percent

16.5

28.5

14.7

18.5 18.7

0

5

10

15

20

25

30

1999 2000 2001 2002 2003

ROE five year average of 19%

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

30

Total Long-Term Debtin millions

$52

$25 $25

$15

$50

$0

$10

$20

$30

$40

$50

$60

1999 2000 2001 2002 2003

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

31

Total Debt/Capitalizationin Percent

30.9%

14.7% 14.0%

8.0%

20.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

1999 2000 2001 2002 2003

Long-term Debt/(Long Term Debt + Shareholders’ Equity)

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

32

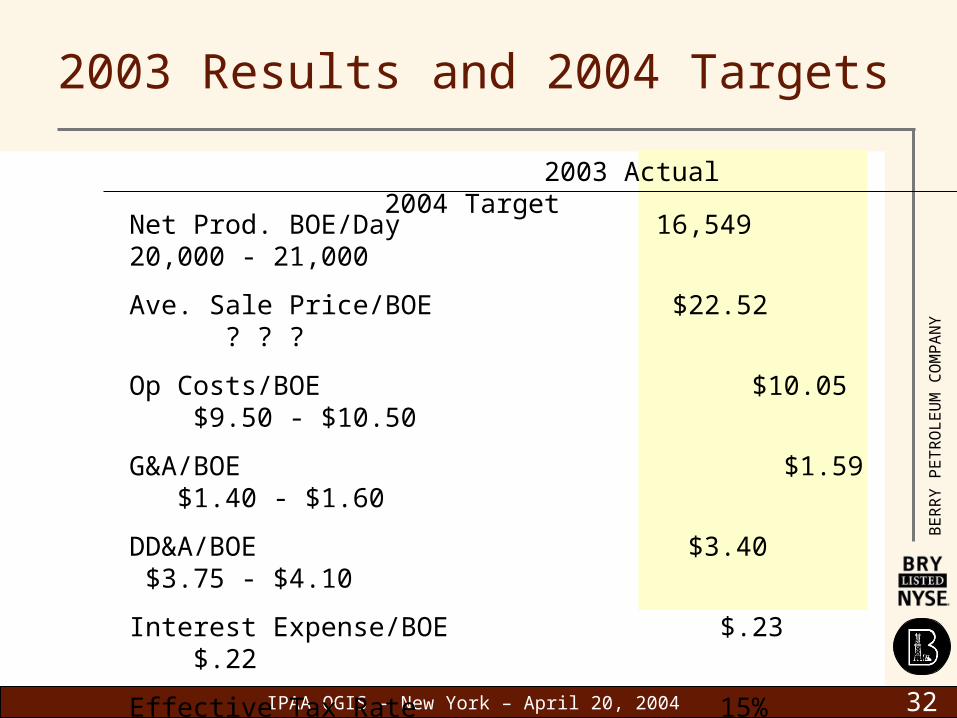

2003 Results and 2004 Targets

2003 Actual 2004 Target

Net Prod. BOE/Day 16,549 20,000 - 21,000

Ave. Sale Price/BOE $22.52 ? ? ?

Op Costs/BOE $10.05 $9.50 - $10.50

G&A/BOE $1.59 $1.40 - $1.60

DD&A/BOE $3.40 $3.75 - $4.10

Interest Expense/BOE $.23 $.22

Effective Tax Rate 15% 23% - 28%

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

33

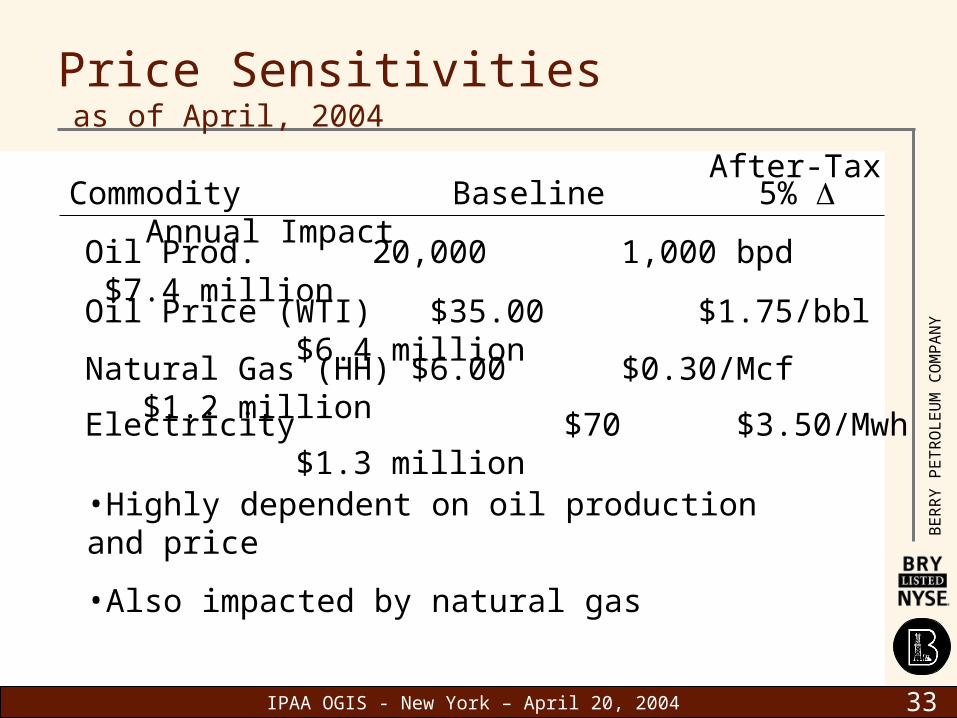

Price Sensitivities as of April, 2004

Commodity Baseline 5% Annual Impact

Natural Gas (HH) $6.00 $0.30/Mcf $1.2 million

Electricity $70 $3.50/Mwh $1.3 million

Oil Price (WTI) $35.00 $1.75/bbl $6.4 million

Oil Prod. 20,000 1,000 bpd $7.4 million

•Highly dependent on oil production and price

•Also impacted by natural gas

After-Tax

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

34

BRY Strengths

• Solid, long-lived existing asset base (16 years)

• Strong financially - $150 MM available for growth plus internally generated cash flow

• Long history of profitability and dividends

• Electricity generating assets assist in lowering costs

• Significant portion of production is royalty-free

• Well positioned to acquire properties

• Well respected in industry

• Delivering on growth strategy

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

35

Questions and Answers

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

36

Contact Information

Jerry V. HoffmanPresident & CEO

Ralph J. GoehringSr. Vice President & CFO

Michael DuginskiVice President of Corporate Development

Todd A. CrabtreeInvestor Relations Specialist

Phone: 661-616-3832 or 866-IR AT BRY

Fax: 661-616-3881

email: [email protected]

website: www.bry.com

Berry Petroleum Company5201 Truxtun Ave., Ste. 300Bakersfield, CA 93309-0640

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

37

Glossary of Terms and Abbreviations

• API – American Petroleum Institute – The American Petroleum Institute was established on March 20, 1919, and focuses on Statistics, Standards and Taxation

• BOE – Barrel of oil equivalent – a unit of measure which includes oil and gas (with 6,000 cubic feet of gas equal to one barrel of oil)

• BOPD – Barrels of oil per day

• Cogeneration – a process in which natural gas is burned to generate two energy outputs; steam and electricity

• DD&A – Depreciation, Depletion, and Amortization

• EOR – Enhanced Oil Recovery, usually accomplished by the injection of steam or water

• Fee property – A property which does not have a royalty payment to a land owner

• G&A – General and Administrative

• HH – Henry Hub - The Pipeline interchange and the delivery point for the NYMEX active natural gas futures market, located in Erath, LA.

• Mcf – Thousand cubic feet of gas

• MM – millions

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

38

Glossary of Terms and Abbreviations

• MMBbl – Millions of barrels of oil

• MMBOE – Millions of barrels of oil equivalent

• Mw – Megawatt – one million watts

• Mwh – Megawatt hour – one million watts generated per hour

• MWSS – Midway-Sunset, a large oilfield in California’s Central Valley

• NYMEX – New York Mercantile Exchange – It is the world's largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals

• OOIP – Original oil in place – The estimate of the quantity of oil in a reservoir prior to any production

• ROCE – Return on capital employed, calculated as net income + after-tax interest expense divided by average long-term debt + average shareholders’ equity

• ROE – Return on equity, calculated as net income divided by average shareholders’ equity

IPAA OGIS - New York – April 20, 2004

BER

RY P

ETR

OLE

UM

C

OM

PA

NY

39

Glossary of Terms and Abbreviations

• R/P – Reserves over Production, or the calculation used to determine reserve life

• SJV – San Joaquin Valley – The central California benchmark for heavy crude oil, approximating 13° API gravity

• Spark Spread – The difference between the sales price of electricity and its cost of production

• SRAC – Short run avoided cost – The estimated cost of the “next” megawatt of electricity generated

• Standard Offer – The sales contract offered by the utilities, not open market sales

• WTI - West Texas Intermediate – the US benchmark crude oil, approximating 40° API gravity