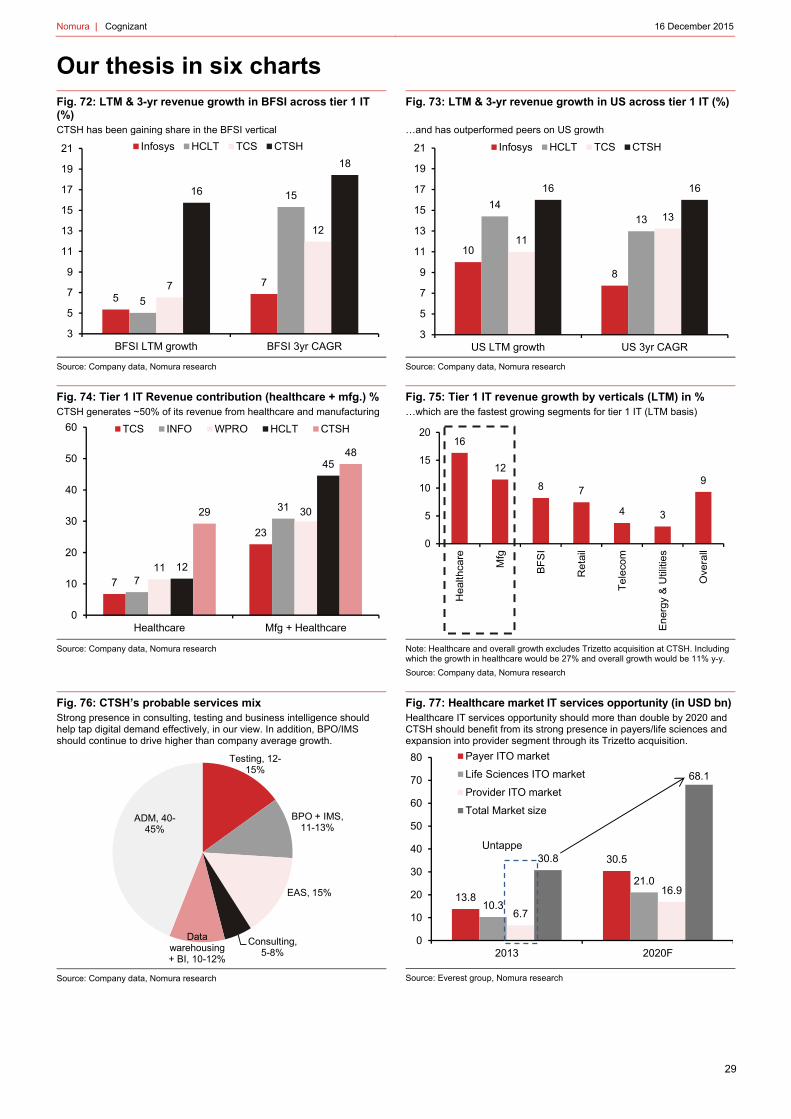

be selective, back better business mix - myirisbreport.myiris.com/nfasipl/tatconse_20151216.pdf ·...

TRANSCRIPT

See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts.

Global Markets Research

AN

CH

OR

RE

PO

RT

India IT services: Outlook 2016 – Navigating tech transitions

Be selective, back better business mix

Indian IT services is grappling with the challenges of reinventing the old and driving the new, as technology changes (Digital - social, mobile, analytics, cloud and IoT) and business gradually controls a higher share of IT budgets. So, while continuing themes such as segment penetration and market share gains are still relevant, newer technology transitions is a story of some gain and some pain. As demand diverges across segments and macro is less supportive, business mix assumes greater importance in stock selection.

HCLT (High IMS/BPO/Engg services exposure) and CTSH (Strong Digital, high healthcare/manufacturing exposure) are our top Buys.

Key themes and analysis in this Anchor Report include:

Penetration levels across segments, what drives growth and how are individual companies placed to gain market share?

Underlying trends driving tech transitions, how they affect the old and add to the new areas and which companies benefit the most?

How are macro demand indicators tracking and how they correlate with sector demand?

16 December 2015

Research analysts

India Technology/Services & Software

Ashwin Mehta - NFASL [email protected] +91 22 4037 4465

Rishit Parikh - NFSPL [email protected] +91 22 4037 4360

Anchor themesWe prefer companies that have a better skew towards growing segments and are available at reasonable valuations.

Nomura vs consensusHCLT, CTSH and INFO are our top Buys.

Research analysts

India Technology/Services & Software

Ashwin Mehta - NFASL [email protected] +91 22 4037 4465

Rishit Parikh - NSFSPL [email protected] +91 22 4037 4360

India IT services

EQUITY: SOFTWARE & SERVICES

Outlook 2016: Navigating tech transitions

Tech transitions driving push-pull of old vs new leading to caution on FY17F demand Demand outlook unexciting, back better business mix Indian IT services are in transition due to new technology trends (Digital – social, mobile, analytics, cloud and IoT) and shifts in spending authority at clients from IT to business. Thus, we expect diverging demand trends across segments and changes in the nature of demand within segments too. This coupled with weakening macro demand indicators (client financials and US PMI) limits the potential for demand to accelerate in FY17F. We recommend staying selective and prefer IT services names with: 1) a higher skew towards faster growing areas (eg, digital, infrastructure management services (IMS)/engineering services, Europe, healthcare/manufacturing); 2) potential for market-share gains in the more sluggish segments (e.g ADM/BFSI); and 3) less exposure to work subject to cannibalisation. While fundamentally demand looks less than exuberant, reasonable valuations at near five-year averages and USD strength lend defensiveness to the sector.

Key tech transitions that are likely to shape the demand for the industry As CIO budgets contract, segment penetration, market share gains and level of automation will remain big growth drivers. However, increases in non-CIO spend will shift demand in favour of Digital leading to significant transitions like 1) on-premise s/w to SaaS; 2) on-premise datacenters to cloud; 3) under-exploited corporate data silos to open data flows; 4) desktop-based systems to mobility and 5) from mandate of reliability of IT systems to dual mandate of reliability and agility. The negative impacts on legacy work and newer opportunities will co-exist; hence business mix will decide which companies do better. Accenture clearly has lead versus Indian IT, but we expect HCLT/TCS to gain from back-end digital and CTSH/INFO/TCS to gain from front-end digital demand.

Top Buys: HCLT, CTSH and INFO HCLT (~60% exposure to IMS/engineering services and business process outsourcing (BPO), coupled with reasonable valuations), CTSH (strong digital capabilities, market-share gains in BFSI and nearly half of revenues from faster growing healthcare/ manufacturing), followed by INFO (focus on non-CIO spending and improved performance in legacy segments). Fig. 1: Stocks for action

Source: Bloomberg, Nomura estimates. Note: Pricing as of 11 December 2015

Company Code Rating Mkt Cap(USD mn)

Avg. TO(USD mn)

Targetprice

Price (as of11-Dec)

Upside(%)

Cognizant CTSH US Buy 35,450 214 72↓ 58.30 23%

HCL Tech HCLT IN Buy 17,704 29 1,020 841 21%

Infosys INFO IN Buy 36,150 65 1,225 1,053 16%

TCS TCS IN Neutral 70,281 45 2,500 2,386 5%

Tech Mahindra TECHM IN Neutral 7,760 12 560 537 4%

Wipro WPRO IN Neutral 20,897 13 570 566 1%

Mphasis MPHL IN Reduce 1,486 3 410 473 -13%

Hexaware HEXW IN Reduce 1,065 4 200 236 -15%

Global Markets Research 16 December 2015

See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts.

Nomura | India IT services 16 December 2015

2

Contents

Coverage Summary ................................................................................. 3

Indian IT: Cautious on demand in FY17F ................................................ 4

What is contributing to or dragging down Indian IT growth? ........................... 5

Shift in IT spend from CIO to non CIO (business) is shaping the demand

trends in the sector .......................................................................................... 7

CIO spend squeeze: Segment penetration, market-share gains and level of

automation would be key growth drivers ......................................................... 8

Non-CIO spend increases: To spawn newer tech demand in

SMAC/IoT/security ......................................................................................... 11

Sector seeing significant transitions – business mix/execution to navigate

these transitions will determine success ....................................................... 13

Demand becoming more macro dependent: Client financials and US PMI

suggest worsening demand trends ................................................................ 20

Valuations and USD strength lend defensiveness ........................................ 22

Be selective, back better business mix – HCLT, CTSH followed by INFO are

our top Buys ................................................................................................... 24

Cognizant .............................................................................................. 27

HCL Technologies ................................................................................. 31

Infosys ................................................................................................... 35

Tata Consultancy Services .................................................................... 39

Tech Mahindra ....................................................................................... 42

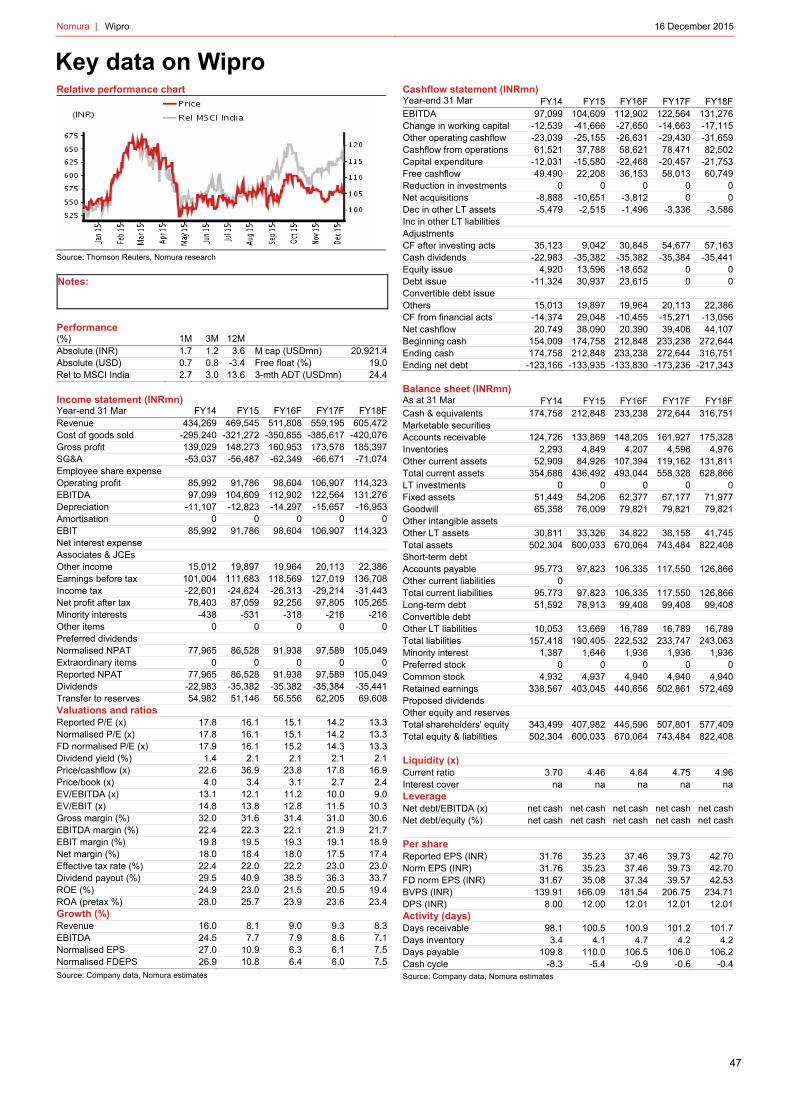

Wipro ..................................................................................................... 46

Appendix A-1 ......................................................................................... 50

Nomura | India IT services 16 December 2015

3

Coverage Summary Fig. 2: IT coverage universe – relative valuation

Note: Pricing as of 11December 2015. FY16F corresponds to fiscal year end Dec-15 for CTSH, HEXW, while it corresponds to Jun-16 for HCLT and Mar-16 for others

Source: Bloomberg, Nomura estimates

Fig. 3: Indian IT coverage universe – growth comparison

Note: EPS in local currency, FY16F corresponds to fiscal year end Dec-15 for CTSH, HEXW, while it corresponds to Jun-16 for HCLT and Mar-16 for others. For Wipro, revenue growth and EBIT margin is for IT service divisions

Source: Nomura estimates

Company Ticker Rating FY16F FY17F FY16F FY17FHCL Tech. HCLT IN BUY 17.7 841 1,020 16x 15.4 13.5 11.1 9.4Cognizant CTSH US BUY 35.5 58 72 20x 21.9 18.1 12.9 10.4Infosys INFO IN BUY 36.1 1,053 1,225 18x 18.3 16.3 12.2 10.5TCS TCS IN NEUTRAL 70.3 2,386 2,500 18x 19.4 17.6 14.1 12.4Wipro WPRO IN NEUTRAL 20.9 566 570 14x 15.2 14.3 11.2 10.0Tech Mahindra TECHM IN NEUTRAL 7.8 537 560 14x 16.1 14.1 11.1 9.2Hexaware HEXW IN REDUCE 1.1 236 200 12x 18.0 15.2 12.3 10.3Mphasis MPHL IN REDUCE 1.5 473 410 11x 13.9 13.0 8.2 7.4

EV/EBITDA (x)Mkt cap (USDbn)

Price (LC)

Target Price (LC)

Target P/E multiple

P/E (x)

FY15 FY16F FY17FCAGR

(FY15-17F) FY15 FY16F FY17F FY15 FY16F FY17FCAGR

(FY15-17F)HCL Tech. 11.1 8.6 14.4 11 22.3 21.2 21.1 51.4 54.8 62.3 10Cognizant 16.1 20.9 13.9 17 18.4 17.4 18.1 2.35 2.66 3.22 17Infosys 5.6 8.5 11.2 10 25.9 24.9 25.0 53.9 57.5 64.5 9TCS 15.0 7.8 10.7 9 26.9 27.0 26.5 110.9 123.1 135.3 10Wipro 7.0 4.4 8.8 7 22.0 21.0 20.4 35.1 37.3 39.6 6Tech Mahindra 18.3 11.4 9.0 10 15.6 13.7 14.7 29.6 33.4 38.1 14Hexaw are 8.9 15.4 11.5 13 16.8 16.1 16.9 10.6 13.1 15.5 21Mphasis (7.8) (1.2) 3.2 1 13.3 14.0 14.8 32.2 34.1 36.4 6

USD revenue growth (%) EBIT margin (%) EPS

Nomura | India IT services 16 December 2015

4

Indian IT: Cautious on demand in FY17F In India, we are cautious on the possibility of demand acceleration in FY17F, mainly owing to the diverging demand trends and weakening macro indicators:

• Sector remains in transition and demand trends are diverging across segments: The industry is grappling with fast changing demand dynamics across segments, driven by technology changes and a shift in spending authority from IT to business within client organisations. Even within segments, the nature of demand is shifting, with 1) deal size and duration getting smaller, 2) increasing complexity, and 3) annuity characteristics of business seeing a change with more transformational project based work coming from clients. Further, IT services vendors need to adjust to the dual mandate of reliability and agility of IT systems, which have repercussions from staffing/skills/sales and investment perspectives. These transitions are leading to diverging demand trends across segments:

– New vs legacy offerings: Smaller newer technology offerings (digital – social, mobile, analytics, cloud and IoT) and IMS/engineering services are growing well, but this is being countered by larger more sluggish legacy segments like application development and maintenance (ADM) and enterprise application services (EAS).

ADM is seeing deflationary impacts as automation, competitive pressures and rationalization in the app landscape counter legacy app modernisation efforts.

EAS is seeing cannibalisation of on-premise software implementation and support work, despite growth in SaaS (software as a service) and analytics, which are smaller.

IMS, a faster growing service, is also seeing a change in the nature of demand with: 1) a shift from more annuity monitoring/troubleshooting work to more project-based transformational work across cloud/mobility, 2) a shift from manpower-led to software/automation-led work, and 3) new opportunities to take complete ownership of work related to multiple cloud instances (public/private). Increasing complexity and changes in the nature of the work are causing volatility in this segment.

– US vs Europe: The US market has grown steadily in the 10% y-y range for the past six quarters, but has not accelerated despite stronger macro. Meanwhile, Europe is outperforming on growth (ex-currency impact), driven by cost-focused demand.

– Across verticals: BFSI/retail/telecom/energy, which contribute ~60% of tier-1 IT revenues, are underperforming, while healthcare/manufacturing are growing well.

We expect these divergent trends to continue in FY17F and believe that in such a scenario, stocks with better business mix will drive growth and share price performance.

• Macro demand indicators are not supportive and suggest decelerating trends: We see worsening key macro demand indicators, which typically affect demand with a 2-3 quarter lag: 1) decelerating or negative revenue growth trends across key client industries such as oil & gas, BFS, consumer, retail, and manufacturing at Fortune 500 US corporates; 2) the US PMI at 48.6 in Nov-15 is at the lowest level since Jun-09, vs its previous peak of 58.1 in Aug-14; and 3) ~20% lower monthly private job additions in the US in 2015 YTD vs 2014. This has already started to get reflected in the softer 2HFY16F outlook at tier-1 IT companies, with weak guidance at Infosys/Wipro, a pre-2Q warning at HCLT, and the cautious tone at TCS. Weaker exit rates for FY16F will likely limit the potential for demand acceleration in FY17F.

The above mentioned factors make us cautious on revenue acceleration in FY17F versus FY16F, and we look for constant currency growth of 12% over FY16-18F (vs 14%+ in FY16F) for tier-1 IT (including CTSH).

What prevents us from taking a more negative stance is that relatively: 1) valuations at 17.8x one-year forward P/E for tier-1 IT (incl. CTSH) (~3% premium to five-year historical averages), while not cheap, are not very expensive either; 2) a stronger USD plays to the sector’s advantage and lends certain defensiveness to the sector; and 3) Indian IT is still available at higher than historical valuation discounts versus other defensive sectors like FMCG and pharma.

Nomura | India IT services 16 December 2015

5

What is contributing to or dragging down Indian IT growth?

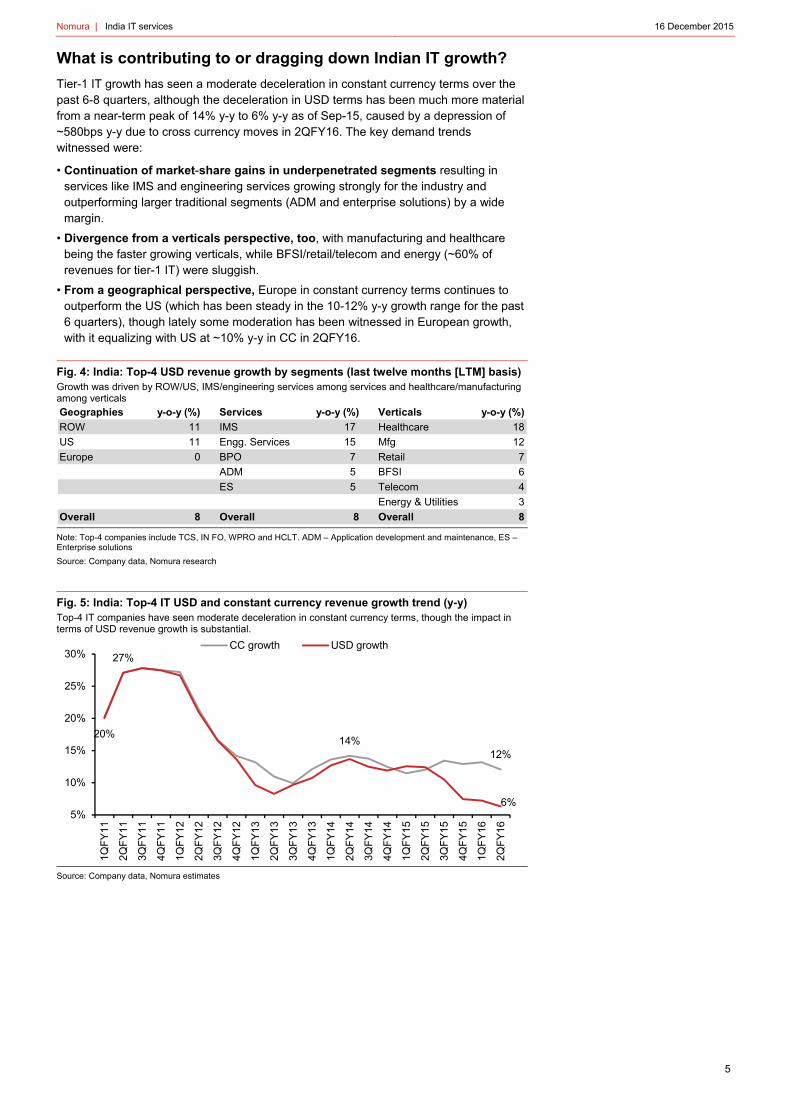

Tier-1 IT growth has seen a moderate deceleration in constant currency terms over the past 6-8 quarters, although the deceleration in USD terms has been much more material from a near-term peak of 14% y-y to 6% y-y as of Sep-15, caused by a depression of ~580bps y-y due to cross currency moves in 2QFY16. The key demand trends witnessed were:

• Continuation of market-share gains in underpenetrated segments resulting in services like IMS and engineering services growing strongly for the industry and outperforming larger traditional segments (ADM and enterprise solutions) by a wide margin.

• Divergence from a verticals perspective, too, with manufacturing and healthcare being the faster growing verticals, while BFSI/retail/telecom and energy (~60% of revenues for tier-1 IT) were sluggish.

• From a geographical perspective, Europe in constant currency terms continues to outperform the US (which has been steady in the 10-12% y-y growth range for the past 6 quarters), though lately some moderation has been witnessed in European growth, with it equalizing with US at ~10% y-y in CC in 2QFY16.

Fig. 4: India: Top-4 USD revenue growth by segments (last twelve months [LTM] basis) Growth was driven by ROW/US, IMS/engineering services among services and healthcare/manufacturing among verticals

Note: Top-4 companies include TCS, IN FO, WPRO and HCLT. ADM – Application development and maintenance, ES – Enterprise solutions

Source: Company data, Nomura research

Fig. 5: India: Top-4 IT USD and constant currency revenue growth trend (y-y) Top-4 IT companies have seen moderate deceleration in constant currency terms, though the impact in terms of USD revenue growth is substantial.

Source: Company data, Nomura estimates

Geographies y-o-y (%) Services y-o-y (%) Verticals y-o-y (%)

ROW 11 IMS 17 Healthcare 18

US 11 Engg. Services 15 Mfg 12

Europe 0 BPO 7 Retail 7

ADM 5 BFSI 6

ES 5 Telecom 4

Energy & Utilities 3

Overall 8 Overall 8 Overall 8

27%

14%12%

20%

6%5%

10%

15%

20%

25%

30%

1QF

Y11

2QF

Y11

3QF

Y11

4QF

Y11

1QF

Y12

2QF

Y12

3QF

Y12

4QF

Y12

1QF

Y13

2QF

Y13

3QF

Y13

4QF

Y13

1QF

Y14

2QF

Y14

3QF

Y14

4QF

Y14

1QF

Y15

2QF

Y15

3QF

Y15

4QF

Y15

1QF

Y16

2QF

Y16

CC growth USD growth

Nomura | India IT services 16 December 2015

6

Growth by geography: US is steady though not accelerating, Europe is seeing some moderation after outperformance in CC terms and strong ROW depressed by currency.

Fig. 6: US revenue growth (y-y) US growth steady at 10-12% for 6 quarters

Source: Company data, Nomura research

Fig. 7: Europe revenue growth (y-y) Europe lately seeing some weakening

Source: Company data, Nomura estimates

Fig. 8: ROW revenue growth (y-y) ROW impacted substantially by CC moves

Source: Company data, Nomura estimates

Growth by vertical: Healthcare leads growth, retail shows improvements after being sluggish, and manufacturing shows steady demand trends, BFSI/energy and telecom underperform, where rebounds are required for any positive surprises.

Fig. 9: BFSI growth (y-y) Seen deceleration, rebound illusive

Source: Company data, Nomura estimates

Fig. 10: Manufacturing growth (y-y) Some moderation lately after strong growth

Source: Company data, Nomura estimates

Fig. 11: Retail growth (y-y) Some improvement lately, sustainability key

Source: Company data, Nomura estimates

Fig. 12: Energy & Utilities growth (y-y) Pain from oil price fall continues to weigh

Source: Company data, Nomura estimates

Fig. 13: Telecom & media growth (y-y) Continues to underperform

Source: Company data, Nomura estimates

Fig. 14: Healthcare growth (y-y) Remains the strongest growing vertical

Source: Company data, Nomura estimates

12%10%

0%

5%

10%

15%

20%

1QF

Y12

1QF

Y13

1QF

Y14

1QF

Y15

1QF

Y16

10%

0%

-10%

0%

10%

20%

30%

40%

1QF

Y11

3QF

Y11

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

17%

3%0%

10%

20%

30%

40%

50%

1QF

Y11

3QF

Y11

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

11%

6%

0%

5%

10%

15%

20%

25%

30%

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

12%

8%

0%

5%

10%

15%

20%

25%

30%

35%

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

14%

8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

5%

-3%

-5%

5%

15%

25%

35%

45%

55%

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

8%

1%

-10%

-5%

0%

5%

10%

15%

20%

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

24%

20%

10%

12%

14%

16%

18%

20%

22%

24%

26%

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

Nomura | India IT services 16 December 2015

7

Growth by service line: Engineering services and IMS lead, though some moderation has been seen in IMS lately, BPO/Testing outperform aggregate growth, while ADM/ES are sluggish Fig. 15: ADM growth (y-y) Tech shifts/pricing pressure drive sluggishness

Source: Company data, Nomura estimates

Fig. 16: ES growth (y-y) Decelerating trends, though INFO outperforms

Source: Company data, Nomura estimates

Fig. 17: IMS growth (y-y) Still healthy, but decelerates materially

Source: Company data, Nomura estimates

Fig. 18: BPO growth (y-y) Growing in line with top-4 growth

Source: Company data, Nomura estimates

Fig. 19: Engg. Services growth (y-y) Is the strongest growing service line

Source: Company data, Nomura estimates

Fig. 20: Testing growth (y-y) Outperforming aggregate growth

Source: Company data, Nomura estimates

Note: We have assumed similar cross currency impacts for services as seen in overall revenues, given lack of such granularity. Constant currency growth might be overstated in ADM/Engg. Services due to possible US skew, while could be understated in IMS where European skew is higher.

Shift in IT spend from CIO to non CIO (business) is shaping the demand trends in the sector

While IT spending has grown historically at around 4% y-y, there is a reallocation of authority in terms of who controls the spend, as is visible in Fig. 21 and Fig. 22, wherein CIO spend is expected to come down to near half of overall IT spend, from near three-fourths as early as six years ago. In effect, the absolute CIO spend is also seeing a reduction because of this trend.

This shift has several repercussions for IT demand:

• CIO spend squeeze: To lead to segment penetration, market-share gains and level of automation becoming key determinants of growth.

• Non-CIO spend increases: To spawn newer tech demand in SMAC/IoT/security.

10%

4%0%

5%

10%

15%

20%

25%

30%

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

10%

4%0%

5%

10%

15%

20%

25%

30%

35%

40%

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

15%

9%

5%

10%

15%

20%

25%

30%

35%

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

12%

6%

0%

5%

10%

15%

20%

25%

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth19%

13%

0%

5%

10%

15%

20%

25%

30%

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

13%

7%

0%5%

10%15%20%25%30%35%40%45%

1QF

Y12

3QF

Y12

1QF

Y13

3QF

Y13

1QF

Y14

3QF

Y14

1QF

Y15

3QF

Y15

1QF

Y16

CC growth

USD growth

Nomura | India IT services 16 December 2015

8

Fig. 21: Distribution of IT spend by decision maker (% share)Business buyers are likely to control near half of IT services spends by 2016, which was as low as near one fourth of spends six years ago

Source: Forrester, Offshore Insights, NASSCOM, Note P= projected

Fig. 22: Absolute IT spend by decision maker (USD bn) while IT department controlled budgets shrink both in share and absolute spends

Source: Forrester, Offshore Insights, NASSCOM, Note P=projected

CIO spend squeeze: Segment penetration, market-share gains and level of automation would be key growth drivers

The squeeze in CIO spends will likely lead to:

• Increased offshore penetration in underpenetrated segments: An increased cost optimization pressure would likely lead to greater offshoring in low-penetration segments like IMS, BPO, engineering services and Europe (Fig. 23, Fig. 24, Fig. 25). From within verticals, healthcare and manufacturing and possibly energy (once the current curtailments in overall operations subside due to oil price fall and clients focus on cost optimization) would likely see continued demand (Fig. 26 & Fig. 27).

• Commoditization pressures in high-penetration segments: In segments like ADM where the penetration of Indian IT companies is of the order of 40%, the same cost optimization efforts will likely lead to pricing pressures (Fig 28) and hence sluggish demand. In addition, new technology transitions will also put pressure on ADM demand as 1) clients choose software over custom development; 2) some applications become redundant as legacy applications are rationalised as clients go digital, leading to reduced support requirements; and 3) the segment faces the deflationary effects of automation.

Fig. 23: Indian IT market share by service line (%) IMS, BPO and engineering services less penetrated, while ADM is substantially penetrated at ~40%

Note: Based on 2015E data

Source: Zinnov, NASSCOM, Nomura research

1%10%

25%36%

74%

53%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2010 2012 2014P 2016P

Workforce Lines of Business IT

5

114

337

15

136

335

37

169

321

60

209

304

Workforce Lines of Business IT

2010 2012 2014P 2016P

Service line break-upGlobal spending

(USDbn)Indian IT's share

(%)

Traditional service lines (ADM)

Overall ADM 105 40.0%

Under penetrated service lines

Package Implementation & Consulting 154 6.3%

IT Consulting 33 9.4%

Systems Integration 121 5.5%

IMS 270 4.6%

Netw ork Consulting & Integration 43 1.4%

IS Outsourcing (RIM) 227 5.2%

BPO 167 15.6%

Engineering Services 614 3.9%

Global IT spend (excl H/W) 1,254 9.5%

Nomura | India IT services 16 December 2015

9

Fig. 24: Distribution of global IT spend by geography (%) Of the overall Global IT Services spend of ~USD660bn, Europe is near 80% of the US spends at ~USD240bn

Note: Based on 2015 data Source: NASSCOM, Nomura research

Fig. 25: India IT services market share by geography (%) Europe and ROW remain the underpenetrated geographies, which should continue to grow better than the US in our view

Note: Based on 2015 data Source: NASSCOM, Nomura estimates

Fig. 26: Vertical-wise split (%) of global IT services spend BFSI is the largest spender on IT services and most penetrated as well.

Note: Based on 2012 data Source: NASSCOM, Nomura research

Fig. 27: India IT services market share by verticals (%) Under penetration in manufacturing and emerging areas (Health/Energy)

Note: Based on 2012 data Source: NASSCOM, Nomura estimates

Fig. 28: Infosys: Constant currency offshore pricing trend (base 100) Commoditisation pressures in highly penetrated ADM is a big driver of offshore pricing declines at INFO

Source: Company data, Nomura research

Hence, what drives growth in this scenario in the CIO spend areas is: 1) market-share gains driven by capabilities in certain segments; 2) automation levels, which will impact both ability to win deals and to protect margins under commoditisation pressures; 3) mix of segments with higher exposure to faster growing areas likely leading to better growth.

Americas, 44

EMEA, 36

Asia Pacific, 20

12%

7%

4%

Americas Europe ROW0%

2%

4%

6%

8%

10%

12%

14%

BFSI, 21

Manufacturing, 20

Hitech/ Telecom,

10

Government, 16

Emerging, 33

Manufacturing, 20

Government, 16

18%17%

7% 7%

1%

BFSI Hitech/Telco Mfg. Emerging Govt.

India IT market share (%)

97

95

97

96

94

96

98

97 97

95

93

91

94

90

92

94

96

98

100

102

4QF

Y12

1QF

Y13

2QF

Y13

3QF

Y13

4QF

Y14

1QF

Y14

2QF

Y14

3QF

Y14

4QF

Y14

1QF

Y15

2QF

Y15

3QF

Y15

4QF

Y15

1QF

Y16

2QF

Y16

Nomura | India IT services 16 December 2015

10

Despite increasing importance of newer technology spends, the trend of India IT gaining market share remains a continuing growth driver, in our view.

Fig. 29: India IT and top-3 MNC revenue trends and changes in the share of aggregate revenues India IT has gained 6.1% share in the past 8 quarters and is now half of the top-3 global players in terms of size vs one-third two years ago

Note: Top-five Indian players include Infosys, TCS, HCL Tech, Cognizant and Wipro, while Top-3 MNCs include Accenture, IBM and HP. Source: Company data, Nomura research

We believe growth in IMS/BPO/engineering services and testing within services, Europe among geographies, and healthcare/manufacturing among verticals will be continuing trends in FY17F and beyond. However, we remain cautious on ADM demand in FY17F. On account of this, we find HCLT benefiting from strong positioning in IMS/engineering services (Fig 30-33) and less exposure to ADM than peers, while CTSH should benefit from higher exposure to healthcare/manufacturing and market-share gains in BFSI/US.

Fig. 30: Deal renewal opportunity (USD bn) ~USD150bn worth of deals coming up for rebid over CY16-18, where churn towards newer players is expected to be of the order of 40% and ~80% of these deals are IMS led deals.

Note: Excludes government vertical and BPO opportunities

Source: ISG, HCLT, Nomura estimates

Fig. 31: Deal renewal opportunity by geography (%) CY16-18 Europe is the biggest area of deal rebid with near 60% of the deal rebids originating from Europe. This coupled with under penetration makes us positive on the prospects of growth in IMS and Europe

Note: Excludes government vertical and BPO opportunities

Source: ISG, H CLT, Nomura research

Fig. 32: E and R&D revenues (USD mn) across India IT HCLT is the largest in India and third largest globally in engineering services; and it is the 2nd largest Indian player in IMS. From a contribution perspective too, HCLT generated ~54% of its revenues from IMS + engineering services (vs 11-36% at peers)

Source: Company data, Nomura research

Fig. 33: E and R&D outsourcing addressable market (FY15) India currently captures only ~25% of the outsourced service provider (SP) market of USD36bn, which is 1/6th of the total addressable market (TAM)

Source: Zinnov, NASSCOM, Nomura research

Revenue (USDbn) 3QCY13 4QCY13 1QCY14 2QCY14 3QCY14 4QCY14 1QCY15 2QCY15 3QCY15 Change( 8 qtrs)Top-5 Indian IT 10.6 10.9 11.1 11.5 11.9 12.2 12.2 12.7 13.1 2.5Top-3 MNC 29.2 29.7 28.8 29.4 29.1 28.4 26.4 27.0 26.9 -2.3Overall 39.8 40.6 39.9 40.9 41.0 40.6 38.7 39.7 40.0 0.2Share Indian IT (%) 26.6% 26.8% 27.8% 28.1% 29.1% 30.0% 31.6% 32.0% 32.8% 6.1%Share MNC IT (%) 73.4% 73.2% 72.2% 71.9% 70.9% 70.0% 68.4% 68.0% 67.2% -6.1%

51

46

50

CY16F CY17F CY18F

EMEA, 58Americas, 24

APAC, 18

HCLT TCS WPRO INFO Overall

Engineering Services

LTM revenue (USD bn) 1.1 0.7 0.5 0.3 2.7

Revenue contribution (%) 19 5 8 3 7

LTM growth y-y (%) 25 7 11 8 15

3 year CAGR (%) 13 13 2 8 10

IMS

LTM revenue (USD bn) 2.1 2.3 2.0 0.7 7.2

Revenue contribution (%) 35 15 28 8 19

LTM growth y-y (%) 11 27 15 14 17

3 year CAGR (%) 26 26 13 17 21

India USD9bn

USD614bn,Global

500 E & RD spend

USD216bn,

Outsource TAM

USD 36bn,Current SP revenues

USD 9bn,India SP revenues

Nomura | India IT services 16 December 2015

11

Non-CIO spend increases: To spawn newer tech demand in SMAC/IoT/security

The focus of the non-CIO or business is likely to be more on front-end revenue generating areas and overall improvement in customer experience, which will likely drive demand for newer technology areas like digital – social, mobile, analytics, cloud, security and IoT (internet of things). Ability to win business in this area will be determined by skill sets, investments in capabilities, partnerships with start-ups, and a strong consulting front end.

We believe the demand in digital will have two elements – front end and back end. Front end comprises work related to customer experience, analytics, digital marketing, developing enterprise mobile apps with vertical domain capabilities, and SaaS implementations, while back end comprises work related to cloud transformation, mobility transformation, legacy app modernization, creation/management of big data, and security. We believe Indian IT is likely to have a bigger role in back end vs front end digital.

We believe global IT companies like Accenture have an edge versus tier-1 Indian IT companies in the digital space both in terms of scale as well as capabilities. This is especially true in the front-end digital areas where consulting capabilities and better C level connects play to their advantage. In addition, Accenture also scores on having strong downstream capabilities by virtue of it having ~257,000 people in offshore delivery locations (larger than the offshore headcount of all tier-1 IT players ex TCS). Another area where we believe Indian IT players are deficient is the security space, which is one of the top most priorities for clients going digital. (Fig 34 & Fig 35)

Fig. 34: Comparison of Accenture versus Indian IT players in terms of size, expectations and classifications in Digital Accenture generates ~23% (ex-cloud) of its revenues from digital, vs single-digit contributions from digital for top Indian IT companies (ex TCS)

Source: Company data, Nomura research

Company Scale Whats included in Digital?

Accenture

-Generated ~USD7bn in revenues in FY15, nearly 23% of the total.-Digital comprises of Accenture Interactive (USD2bn), Analytics (USD 4bn) and Mobility (USD 2bn)-Currently has 36,000 digital professionals

Social, Analytics, Mobile, Interactive platforms/solutions (Does not include cloud w hich is nearly USD3.5bn in revenues annually)

TCS-Generated annualized revenues of ~USD2.2bn in the 2QFY16, nearly 13.3% of its revenues from digital.-Expects to train 100,000 employees on digital technologies by FY2016

AI, Robotics, Mobility and Channels, Cloud, Big Data, Analytics and Social segments

Infosys

-Generated ~USD800mn in revenues in FY15, nearly 8% of it reveneus from digital.-Expects to train all employees on design thinking by year end

SMAC (Social, mobile, analytics and cloud)

CTSH-Generated ~USD500mn in revenues in 2013, nearly 5% of its revenues then from digital.

SMAC (Social, mobile, analytics and cloud)

TechM-Expects its digital revenue to cross USD500mn (~10% of total) by end of CY2015

NMACS (Netw orks, Mobile, Analytics, Cloud, Security, Social and Sensors)

Wipro-Expects to generate ~USD1bn in revenues in 3 years (from Mar-2015) from digital -Expects to train 10,000 employees on digital technologies in 2016

SMAC (Social, mobile, analytics and cloud)

Nomura | India IT services 16 December 2015

12

Fig. 35: Headcount comparison of Accenture (offshore) and Indian IT companies (overall) In addition, to larger scale and stronger front-end digital capabilities, Accenture has substantially augmented its offshore delivery capabilities to capture downstream digital demand

Source: Company data, Nomura research

So while we believe taking share against a player like Accenture might be difficult for Indian IT players, there is still scope to win share against other players and get downstream work once pure consulting companies (with limited downstream delivery capabilities) have advised clients. In addition, digital is a new area wherein none of the players have a substantial lead (as opposed to the traditional system integration area where global players did have a substantial lead) and hence capability gaps can be reduced or specialization can be built in specific areas (e.g. Cognizant in healthcare)

We believe digital will be additive for India IT over the medium term. However, over the near term, companies will have to bear with significant transitions in existing services and changes in the nature of demand within segments due to the shift towards newer technologies. So growth in the interim will be more dependent on 1) exposure to segments which are growing versus segments that are getting cannibalized due to the changes in the nature of demand; and 2) how players adjust to new realities in terms of sales, staffing, skill levels and partnerships for IP through own development, using open source and through acquisitions.

From among the tier-1 Indian IT players, we see CTSH, TCS and INFO being the stronger players in front-end digital capabilities, while HCLT/TCS would likely be the stronger players in the back-end digital elements, especially in the biggest transformation areas like mobility and cloud, given their strong IMS practices. Presence in security, which is likely to be among the top priorities for organizations as they undergo digital transformation, is an area where we believe Indian IT companies have weaker capabilities. IoT demand should benefit players with stronger engineering services and analytics capabilities. From an engineering services perspective, we believe HCLT is the strongest player, while from an analytics perspective we believe CTSH/INFO/TCS would be stronger. We highlight our view on the IT services work involved under SMAC and who benefits the most from those capabilities in Fig. 36. The segments which are blank are typically areas where we believe the Indian IT companies have a weaker presence and players like Accenture/IBM would the stronger players.

Headcount comparison Current headcount LTM growth 3-year CAGR

Accenture 256,846 25% 17%

Indian IT 1,016,863 9% 9%

HCLT 105,571 11% 7%

Cognizant 219,300 10% 13%

Infosys 187,976 14% 7%

TCS 335,620 7% 10%

Wipro 168,396 9% 6%

Nomura | India IT services 16 December 2015

13

Fig. 36: IT services work involved in SMAC and how are IT companies positioned? HCLT/TCS stronger on back-end SMAC related work, while CTSH/INFO/TCS stronger on the front end side. Blank areas are where we think global IT companies like Accenture/IBM or consulting companies are stronger and Indian IT has a more limited play.

Source: Nomura research

Sector seeing significant transitions – business mix/execution to navigate these transitions will determine success

The next question that typically investors have is whether the new technology spends will be incremental or this will come at the cost of the legacy spends. Clearly the sector is going through multiple transitions, which will lead to additional opportunities but also cannibalize existing business. Hence, the mix of business and execution would determine growth for individual players in such a scenario. Over the medium term, we think this will be additive for Indian IT but near term the cannibalization aspects could weigh.

SMAC segment IT services work involved Best placed companiesSocial media analytics

Consulting on social media strategy and implementation to enhance effectiveness on this medium Technology solutions or BPO offerings to integrate w ith CRM, offer analytics and BI offerings analyze customer feedback, brand perception etc. and provide decision support for closing gaps/increasing effectiveness.

Typically players strong in analytics - CTSH/TCS/INFO

Media engagement solutions for real time engagement on a global scale

Enterprise mobility related offerings

Provide data remotely to implement w orkflow , provide services and enable sales on the go through extension of enterprise solutions applications like supply chain management,customer relationship management and enterprise resource management on to mobiles

Companies strong in ES - INFO/HCLT/TCS

Develop industry specif ic applications eg mobile banking, trading, customer services, mobile commerce, transportation etc.Extension of end user computing (a big area of spend in the IMS area) to mobiles/tablets. This is the big area of transformation for enterprises. Largely IMS w ork - TCS and HCLT

Big Data offerings

Big Data production ‐ Gather raw data on an industrial scale from both structured and unstructured sources like Social media, databases, Internet of Things, transactions, documents etc. TCS/CTSH/INFOBig Data Management ‐ Data architecture, storage, security, data w arehousing and maintaining data quality related w ork TCS/CTSH/INFOBig Data Analytics ‐ Related to making commercial uses of data through draw ing insights.e.g. BFSI ‐ trade monitoring, analytics, risk & compliance related, Retail ‐ real time analyis of purchases, customer behaviour insights and driving targetted sales, Telecom ‐ fraud/failure detection, netw ork planning & optimization, Healthcare ‐ analysis of treatment & outcome, real time monitoring, Manufacturing ‐ demand forecasting, supply chain management, product feedbacks

Analytics players - TCS/CTSH/INFO

Cloud computing offerings

Related to provisioning servers, storage, database services across public, private or hybrid cloud options and rearchitecting the current datacenters. This is part of most IMS deal rebids currently. IMS players - HCLT/TCSLegacy application modernisation and testing to make applications cloud compliant

TCS/CTSH/INFO - CTSH is largest in testing

Softw are as a service implementation, support, integration w ith legacy systems, analytics and business process reingeering related w ork. INFO/TCS/CTSHPlatform BPO offerings as a service under a pay as you go model. TCSEnabling front end analytics through use of the cloud. TCS/CTSH

Nomura | India IT services 16 December 2015

14

Fig. 37: Top technology shifts under way that are causing IT services transitions

Source: ZDNet, Nomura research

The key transitions that the industry is going through are: 1) on-premise software to SaaS; 2) on-premise datacenters to cloud; 3) under-exploited corporate data silos to open data flows; 4) desktop-based systems to mobility and omni-channel apps; 5) from mandate of reliability of IT systems to dual mandate of reliability and agility.

Delving deeper into each of the transitions and the repercussions:

1. On-premise software to SaaS • Key technology trend: SaaS software spend is expected to grow at ~5x the growth of

on-premise software over 2013-18. CRM (customer relationship management, where players like Salesforce are prominent) and ERM (enterprise resource management, which includes areas like human capital management where players like Successfactors and Workday are prominent) are likely to contribute ~80% of SaaS spend in 2015. In CRM and ERM, ~45% and ~30% of the total software spend is already SaaS spend, respectively. These are areas where the cannibalisation of on-premise is most prominent as SaaS adoption expands.

Fig. 38: SaaS versus on-premise software growth across categories SaaS software is growing at ~5x the growth rate of on premise software, this trend has repercussions for Indian IT services, which are involved in the implementation and support of both these categories

SaaS vs On-premise growth (in %) 2015 SaaS to

total S/W spend2013-18 SaaS

Growth 2013-18 On-

premise growth

CRM 44.4% 19.6% -3.9%

Engineering 2.3% 21.3% 4.4%

ERM 28.9% 17.2% 1.6%

Ops Manufacturing 8.7% 13.7% 5.6%

SCM 5.0% 14.1% 5.1%

Enterprise Applications 20.7% 17.6% 3.1%

Source: IDC, Nomura estimates

Nomura | India IT services 16 December 2015

15

Fig. 39: CRM software spending (USD bn) CRM is the fastest adopter of SaaS, where cannibalisation is most pronounced

Source: IDC, Nomura estimates

Fig. 40: ERM software spending (USD bn) … followed by ERM

Source: IDC, Nomura estimates

• Why is this change happening? Client needs to shift capex to opex, lower expenses and make their costs variable based on usage.

Fig. 41: On-premise model: Cost analysis On premise has high upfront license, continuing maintenance and intermittent upgrade costs

Source: BCG, Nomura estimates

Fig. 42: SaaS model: Cost analysis SaaS costs are driven by usage and maintenance is non-existent, but over a period add-ons and cross selling leads to growth opportunities

Source: BCG, Nomura estimates

• Repercussions: In a SaaS scenario, there are shorter implementation cycles, limited upgrade related revenues, limited hosting and application management revenue versus on-premise. Although over a period higher add-on work related to integration/analytics are opportunities as data flows much more freely. This could lead to cannibalization of implementation and support revenues as on-premise shifts to SaaS. In addition, within on-premise software areas like core ERP there is work happening on consolidation and simplification wherein clients are focused on reducing multiple instances of the software running. This in turn has a negative impact on support revenues for IT services players. So mix of business between on-premise implementation and support versus SaaS/Analytics determines growth in enterprise solutions (ES) segment.

• Results: Slower growth in HCLT in ES, declines in TCS in ES, and better performance of CTSH and INFO in these areas are possibly the result of these trends in our view. Also, in Accenture as it grows its base of SaaS/analytics portions the cannibalization of legacy work is now having a lesser impact leading to better consulting growths, while for IBM shrinkage in revenues is being seen as legacy ERP portions are large.

10

20

15

12

2

4

6

8

10

12

14

16

18

20

22

2014 2015 2016F 2017F 2018F

SaaS, CAGR=19.6% On-premise, CAGR = -3.9%

13

24

3638

8

12

16

20

24

28

32

36

40

2014 2015 2016F 2017F 2018F

SaaS, CAGR = 17.2% On-premise, CAGR = 1.6%

20

20

8

0

20

40

60

80

100

120

140

One Two Three Four Five Average

Initial License Maintenance Upgrades

48

34 344

17

20

40

60

80

100

120

140

One Two Three Four Five Average

Subscriptions Usage Growth

Add-ons and cross-selling

55

Nomura | India IT services 16 December 2015

16

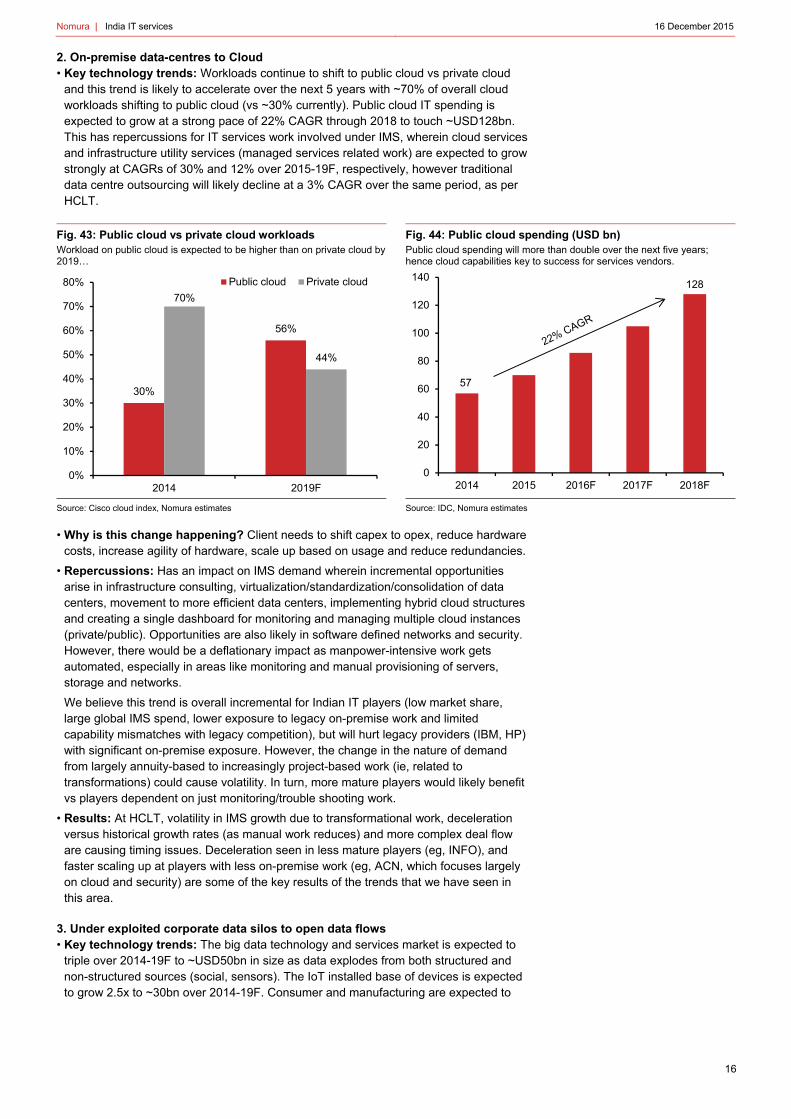

2. On-premise data-centres to Cloud • Key technology trends: Workloads continue to shift to public cloud vs private cloud

and this trend is likely to accelerate over the next 5 years with ~70% of overall cloud workloads shifting to public cloud (vs ~30% currently). Public cloud IT spending is expected to grow at a strong pace of 22% CAGR through 2018 to touch ~USD128bn. This has repercussions for IT services work involved under IMS, wherein cloud services and infrastructure utility services (managed services related work) are expected to grow strongly at CAGRs of 30% and 12% over 2015-19F, respectively, however traditional data centre outsourcing will likely decline at a 3% CAGR over the same period, as per HCLT.

Fig. 43: Public cloud vs private cloud workloads Workload on public cloud is expected to be higher than on private cloud by 2019…

Source: Cisco cloud index, Nomura estimates

Fig. 44: Public cloud spending (USD bn) Public cloud spending will more than double over the next five years; hence cloud capabilities key to success for services vendors.

Source: IDC, Nomura estimates

• Why is this change happening? Client needs to shift capex to opex, reduce hardware costs, increase agility of hardware, scale up based on usage and reduce redundancies.

• Repercussions: Has an impact on IMS demand wherein incremental opportunities arise in infrastructure consulting, virtualization/standardization/consolidation of data centers, movement to more efficient data centers, implementing hybrid cloud structures and creating a single dashboard for monitoring and managing multiple cloud instances (private/public). Opportunities are also likely in software defined networks and security. However, there would be a deflationary impact as manpower-intensive work gets automated, especially in areas like monitoring and manual provisioning of servers, storage and networks.

We believe this trend is overall incremental for Indian IT players (low market share, large global IMS spend, lower exposure to legacy on-premise work and limited capability mismatches with legacy competition), but will hurt legacy providers (IBM, HP) with significant on-premise exposure. However, the change in the nature of demand from largely annuity-based to increasingly project-based work (ie, related to transformations) could cause volatility. In turn, more mature players would likely benefit vs players dependent on just monitoring/trouble shooting work.

• Results: At HCLT, volatility in IMS growth due to transformational work, deceleration versus historical growth rates (as manual work reduces) and more complex deal flow are causing timing issues. Deceleration seen in less mature players (eg, INFO), and faster scaling up at players with less on-premise work (eg, ACN, which focuses largely on cloud and security) are some of the key results of the trends that we have seen in this area.

3. Under exploited corporate data silos to open data flows • Key technology trends: The big data technology and services market is expected to

triple over 2014-19F to ~USD50bn in size as data explodes from both structured and non-structured sources (social, sensors). The IoT installed base of devices is expected to grow 2.5x to ~30bn over 2014-19F. Consumer and manufacturing are expected to

30%

56%

70%

44%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2014 2019F

Public cloud Private cloud

57

128

0

20

40

60

80

100

120

140

2014 2015 2016F 2017F 2018F

Nomura | India IT services 16 December 2015

17

contribute ~50% of overall IoT spend, with retail, transportation and healthcare being the other big spenders. Services and platforms would be the biggest portions of IoT spending and hence a big opportunity area for IT services companies.

Fig. 45: Big data technology and services market Big data IT spend expected to nearly triple over 2014-2019F

Source: IDC, Nomura estimates

Fig. 46: IoT installed base IoT devices installed base to touch 30bn by 2020

Source: IDC, Nomura estimates

Fig. 47: Expected IoT spending by verticals by 2018F Consumer and manufacturing would drive ~50% of IoT spend in 2018

Source: IDC, Nomura estimates

Fig. 48: IoT revenues split across segments (in USD bn) Services and platforms account for the biggest proportions of IoT spend, hence a significant opportunity for IT services companies.

Source: IDC, Nomura estimates

16.5

48.6

0

5

10

15

20

25

30

35

40

45

50

2014 2015 2016F 2017F 2018F 2019F

12

30

0

5

10

15

20

25

30

2014 2015 2016F 2017F 2018F 2019F 2020F

Consumer, 29%

Manufacturing, 20%

Government , 12%

Retail, 7%

Transportation, 7%

Healthcare, 7%

Utilities, 4%

Communications and Media, 4%

Banking , 3% Others, 6%

0

50

100

150

200

250

300

350

2013 2014 2015 2016F 2017F 2018F 2019F 2020F

Devices Connectivity Platforms Analytics Services

Services to grow at 20% CAGR over 2015-20

Nomura | India IT services 16 December 2015

18

• Why is this change happening? This change is driven by client needs to generate greater insights into customer behaviour, improve customer experience and aid decision support. In addition, in areas like industrial/consumer IoT this opens up a newer revenue stream for customers, where they would require help from IT service providers to reach out to enterprise customers. For example, GE expects more than USD15 billion in software and solutions revenue by 2020 driven by Predix - the cloud-based platform for creating industrial internet applications.

• Repercussions: Players strong in business intelligence and analytics would benefit from big data demand, while players strong in engineering services + analytics would gain from IoT work. Further, vertical knowledge to generate better insights and help decision support would lend greater strengths to the Big Data and IoT practices of services providers, in our view. There would be opportunities in the ADM space to facilitate open data flows across applications and external/internal data sources.

• Results: Strong growth in engineering services is partly contributed by IoT demand (though it is still low in terms of contribution but holds significant promise), and companies that are growing better in the enterprise solutions (ES) area are likely to be players with smaller on-premise exposure, higher SaaS exposure and higher analytics strengths.

We expect CTSH/INFO/TCS to benefit more from big data demand, while HCLT should be a strong contender in IoT (especially industrial IoT) given its strength in engineering services. This would be one area where we believe companies would look towards acquiring assets or developing own IP to augment analytics capabilities and vertical expertise.

4. Desktop-based systems to mobility and omni-channel apps • Technology trends: Historically, enterprise app environments have been focused on

desktops with fragmented user experiences. However, as mobility catches up and customers access enterprise apps from across channels, there is a need for apps to be more open (providing access to other apps through APIs – application programming interfaces), to provide a uniform user experience across channels, and to be developed with a mobile first approach. This entails a change at the backend as well to support these changed user requirements.

• Why is this change happening? Due to proliferation of smartphones and tablets, customers/employees now have superior computing power at hand anytime, anywhere, and hence clients cannot neglect any of these modes of access.

• Repercussions: This will have an impact on enterprise solutions (ES) and IMS demand with work related to BYOD (Bring your own device) or enabling mobility for clients, exposing corporate apps on mobiles and advanced security aspects will come into play. Typically, IMS players stronger in the end-user computing segment will gain – HCLT/TCS are bigger in this area, in our view, which will benefit from mobility transformation. However, desktop outsourcing related work will likely see shrinkage. Players stronger in enterprise solutions and ADM areas, coupled with stronger vertical expertise, will benefit from app development and work related to extending enterprise apps to mobiles. CTSH/INFO should be bigger beneficiaries in this area, in our view.

5. From mandate of reliability of IT systems to dual mandate of reliability and agility • Technology trends: Given that IT systems now have a dual mandate of being reliable

(old school) and agile or more innovative (new school), this will lead to changes in the organizational structures from hierarchical to networked, and IT departments from uni-modal (focusing on reliability and predictability) to bi-modal (reliability and innovating at scale) and tri modal (focused on reliability, focused on process improvement in traditional areas and focused on innovating at scale).

• Why is this change happening? Hierarchical and waterfall approaches will not be able to help organizations tackle digital disruption and organisations need to gain efficiencies in traditional areas, which can then be redeployed to drive innovation.

• Repercussions: Different people within the organization would be given this responsibility to drive reliability, agility and process change, and hence service providers will have to adjust their sales processes to target these different needs, eg,

Nomura | India IT services 16 December 2015

19

for reliability-related work, farming was very important, and now for agility, hunting capabilities would be important. The work profile in the agility areas is changing from do as directed to more consultative selling, suggesting what is possible, how can business models be disrupted, and how can internal processes be reengineered.

Second, to drive innovation at scale, investments will have to happen on IP both own and acquired and leveraging of open source aggressively. To achieve this inorganic strategies and collaborations with startups at the cutting edge of technology/solutions will become important success drivers.

Third, organizations within service providers themselves will require a change which will require staff reskilling, a change from the historical pyramid structure to building more differentiated skills, adoption of different development methodologies (eg, Agile, Devops) with greater automation (artificial intelligence/machine learning).

• Results: First, this change in technology has seen an increase in M&A wherein more than 60% of the acquisitions for global majors have been in the SMAC space (close to 40% for India IT). Though for Indian IT, a still larger chunk of acquisitions has been towards, expanding specific vertical domain knowledge, geographical reach and consulting capabilities. Second, efforts to reskill have been announced across companies, with TCS looking at skilling ~100,000 people on digital, INFO indicating ~70,000 people would be trained on design thinking, and WPRO indicating ~10,000 people would be trained in digital in 2016. Third, efforts to build IP solutions/platforms incorporating artificial intelligence have been announced across companies, to automate traditional work.

Fig. 49: Acquisition by area for IBM, Accenture & Tier-1 IT from 2012 to date (nos.) Accenture and IBM have been substantially more acquisitive versus Indian IT in emerging spend areas

Source: Bloomberg, Nomura research

Fig. 50: Acquisition spend of Accenture versus Indian IT companies (USD bn) Accenture has acquired close to 40 companies since 2012 (of which ~60% are in digital space) leading to a total spend of ~USD2.5bn, significantly higher than most Indian IT companies (ex CTSH which acquired Trizetto for ~ USD2.7bn)

Source: Company data, Nomura research

Acquisition area IBM Accenture Tier 1 Indian IT

Emerging spend areas

Analytics 9 8 2

Digital Marketing 2 9 3

Cloud Computing 16 6 3

Mobility 3 1 2

Sub Total 30 24 10

Traditional spend areas

Products, platforms & solutions 0 3 0

Industry solutions 0 6 7

IT Services/Consulting 2 8 7

Technology 3 0 2

Sub Total 5 17 16

Overall 35 41 26

% emerging 86% 59% 38%

3.0

2.5

0.6 0.5

0.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Cognizant Accenture Infosys Wipro TCS

Nomura | India IT services 16 December 2015

20

Demand becoming more macro dependent: Client financials and US PMI suggest worsening demand trends

We believe near-term demand indicators like client financials and US PMI suggest worsening trends, despite expectations of an increase in nominal US GDP from 2.5% in 2015 to 4.1% in 2016, as per our house view, and an increase in business spending to 3.7% in 2016 vs 3% in 2015, which augur well from a medium-term demand perspective (possibly towards 2HFY17F). These indicators impact demand with a 2-3 quarter lag. Hence, we believe a softer 2HFY16F and a weak start to FY17F will likely limit chances of an acceleration in FY17F.

• Client financials: We are witnessing deterioration in Fortune 500 US companies with decelerated or negative revenue growth across a range of sectors over the past 3-4 quarters. The correlation of revenue growth in Fortune 500 companies across verticals with the corresponding revenue growth in that segment for tier-1 IT shows the improvement or deterioration in client financials impacts demand with a 2-3 quarter lag (refer to figures below).

• US PMI has hit the lowest level since June 2009 at 48.6, down from a near term peak of 58. This indicator correlates well with both the CNXIT (IT stock index performance) and the demand for tier-1 IT in the US. Demand in the US lags the PMI by 2-3 months, in our view.

• US private jobs data too suggest that the monthly average job additions YTD in 2015 are nearly 20% lower than 2014 levels. IT services being a linear sector dependent on job addition correlates with US private job additions.

Fig. 51: US Fortune 500 revenue and operating income progression over the past two years Deterioration in client financials with deceleration or negative revenue growth seen across most sectors in the US. Typically, demand lags client financial improvement/deterioration by 2-3 quarters

Note: L2P indicates a move from loss to profit, while P2L indicates vice-versa. Source: Bloomberg, Nomura research

2014 2015y-o-y growth (%) Q1 Q2 Q3 Q4 Q1 Q2 Q3BFSRevenue (3) (1) 4 (2) 2 0 (3)Operating income (4) (14) 22 (12) 20 19 8InsuranceRevenue 0 7 8 5 5 0 3Operating income 9 37 10 (20) 17 (22) 20RetailRevenue 2 4 4 2 1 0 (0)Operating income (5) 0 6 9 6 5 0Oil & GasRevenue (2) 4 (5) (19) (38) (33) (37)Operating income (17) (7) (8) (59) (76) (78) (83)TelecomRevenue 7 5 4 5 2 3 1Operating income 9 5 4 P2L 4 3 2ConsumerRevenue (3) (1) (3) (2) (4) (5) (7)Operating income 2 (0) (7) (27) (16) (22) 43PharmaRevenue 3 8 6 6 5 2 5Operating income 14 25 6 14 11 (0) 18Mfg - HiTechRevenue 9 11 9 6 2 (3) (2)Operating income 53 55 33 25 0 (17) (9)Mfg - ChemicalsRevenue 3 3 1 0 (8) (8) (11)Operating income 8 6 9 (17) 3 3 10Mfg - AutoRevenue 0 1 (2) (3) (5) (4) (3)Operating income (56) (7) (50) (13) 103 42 29Aero and DefenseRevenue 3 3 3 5 1 2 1Operating income 10 4 12 18 5 2 (4)

Nomura | India IT services 16 December 2015

21

Fig. 52: BFSI client revenue growth vs Tier 1 IT BFSI growth (2-quarter lag) Over the last 2 quarters, BFS client revenue growth has decelerated, which could depress growth in this vertical for tier 1 IT

Source: Bloomberg, Nomura research

Fig. 53: Energy client revenue growth vs Tier 1 IT Energy growth (2-quarter lag) Near-term pain, but stabilisation could push up cost focused outsourcing in the medium term

Source: Bloomberg, Nomura research

Fig. 54: Manufacturing (Hi-Tech + Auto) client revenue growth vs Tier 1 IT Mfg growth (2-quarter lag) Manufacturing revenue growth for Tier 1 IT has seen moderation in line with financials

Source: Bloomberg, Nomura research

Fig. 55: Retail client revenue growth vs Tier 1 IT retail growth (1-quarter lag) Stabilisation visible in retail, but sustainability key to watch especially in light of further deceleration in client revenue growth

Source: Bloomberg, Nomura research

Fig. 56: US manufacturing PMI vs CNX IT Index Weakening of US PMI is reflected in IT stock performance with a lag, which could imply some further weakening

Source: Bloomberg, Nomura research

Fig. 57: US PMI vs Tier-1 IT US growth with a two-quarter lagFall in US PMI will likely be reflected in weaker US y-y growth (ex TriZetto) over the next 2 quarters before an improvement from 1Q/2QFY17F

Source: Bloomberg, Nomura research

-30%

-20%

-10%

0%

10%

20%

0%

10%

20%

30%

40%

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Tier 1 IT Fortune 500 (RHS)

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

-10%

0%

10%

20%

30%

40%

50%

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Tier 1 IT Fortune 500 (RHS)

-5%

0%

5%

10%

15%

20%

-5%

0%

5%

10%

15%

20%

Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16

Tier 1 IT Fortune 500 (RHS)

-2%

0%

2%

4%

6%

8%

0%

10%

20%

30%

40%

50%

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Tier 1 IT Fortune 500 (RHS)

30

40

50

60

70

1,500

4,500

7,500

10,500

13,500

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

CNXIT Index (LHS)

US Mfg PMI (RHS)

0%

10%

20%

30%

40%

50%

30

35

40

45

50

55

60

65

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

Mar

-14

Mar

-15

US Mfg PMI (LHS)

Tier-1 IT US y-y growth (2qtr lag) (RHS)

Nomura | India IT services 16 December 2015

22

Fig. 58: US private job addition trends (in 000's) Average monthly private job additions in 2015 are near 20% lower than those in 2014. A sustained pick up in job additions could translate to strong IT services demand

Source: Bloomberg, Nomura research

Valuations and USD strength lend defensiveness

IT stocks have corrected after the 2QFY16 results on moderation in the 2HFY16F outlook. However, the stocks have still outperformed the Nifty from an LTM perspective. We believe two factors that will limit material downside risks for the stocks are: 1) valuations, which at ~17.8x 1-year forward P/E for tier-1 IT are close to the 5-year historical average and thus are not too expensive; 2) USD strengthening and associated INR depreciation lately should play to the advantage of IT stocks lending defensiveness to earnings, even in a scenario of slight deceleration and 3) Compared to other defensive sectors FMCG and Pharma, IT sector still trades at lower than historical discounts. These reasons prevent us from being overly negative on the names, even though we are cautious on demand going into FY17F.

Fig. 59: Tier-1 IT 1-yr fwd P/E trend vs 5-yr average Tier 1 IT is trading at ~3% premium to its 5-year average

Source: Bloomberg, Nomura estimates

Fig. 60: Tier-1 IT (ex CTSH) vs Sensex P/E Tier 1 IT trades at a ~10% premium to the Sensex

Source: Bloomberg, Nomura research

200 193 204

254

202

5

55

105

155

205

255

305

355

405

455Ja

n-1

1

Ap

r-11

Jul-1

1

Oct

-11

Jan

-12

Ap

r-12

Jul-1

2

Oct

-12

Jan

-13

Ap

r-13

Jul-1

3

Oct

-13

Jan

-14

Ap

r-14

Jul-1

4

Oct

-14

Jan

-15

Ap

r-15

Jul-1

5

Oct

-15

private job additions m-m avg for the year

17.8

17.3

5

10

15

20

25

30

Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Aggregate Tier-1 IT P/E avg P/E 24

-23

100

-25

-15

-5

5

15

25

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

IT P/E prem/(disc) to Sensex Avg

Nomura | India IT services 16 December 2015

23

Fig. 61: Tier-1 IT P/E (ex CTSH) vs pharma P/E multiples Tier-1 IT is currently trading at lower than historical discounts to pharma

Source: Bloomberg, Nomura research

Fig. 62: Tier-1 IT P/E (ex CTSH) vs FMCG P/E multiples … while being marginally ahead of historical discounts to FMCG

Source: Bloomberg, Nomura research

Fig. 63: IT stock performance over LTM ACN and CTSH have outperformed peers over LTM. WPRO/TCS/TECHM and IBM have materially lagged

Source: Bloomberg, Nomura research

Fig. 64: IT sector relative performance over LTM IT sector returns have been better than Nifty

Source: Bloomberg, Nomura research

Fig. 65: Inter-tech median performance over LTM IT services median stock return has underperformed only Software & Internet sectors over the last 12 months among tech subsectors

Source: Bloomberg, Nomura research

2

-41

-29-20

-50

-40

-30

-20

-10

0

10

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

IT P/E prem/(disc) to Pharma Avg -17

-64

-49

-45

-75

-65

-55

-45

-35

-25

-15

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

IT P/E prem/(disc) to FMCG Avg

29

1511

94

-3

-13-17-20

-10

0

10

20

30

40

ACN Cognizant HCL Tech Infosys Wipro TCS IBM TechM

2 1

-5-7 -7 -8 -9 -10 -11

-20

-35-40

-35

-30

-25

-20

-15

-10

-5

0

5

Ph

arm

a IT

Au

to

FM

CG

Nift

y

Oil

Cap

Goo

ds

Po

wer

Ba

nks

Rea

lty

Met

als 27

15

10

4

2

-24

-30 -25 -20 -15 -10 -5 0 5 10 15 20 25 30

Internet

Software

IT Services

Comm.Equipment

Semis

Computers &Peripherals

Nomura | India IT services 16 December 2015

24

Be selective, back better business mix – HCLT, CTSH followed by INFO are our top Buys

The continuing themes in the sector are: 1) strong traction in IMS, engineering services and BPO among services, 2) healthcare and manufacturing among verticals, 3) US macro not yet being reflected while Europe continues to show strength on cost-focused outsourcing, with likelihood of some worsening in US growth given the macro deterioration, and 4) Lower cannibalisation and greater benefits from digital. So, essentially the business mix is becoming a crucial factor in determining stock preferences alongside execution in order to determine the fortunes of tier-1 IT companies.

• Share of growing segments: IMS/BPO/engineering services and testing vs. ADM/consulting and SI – HCLT and TCS score higher than INFO on this parameter, but INFO/CTSH are gaining share in larger segments ADM/consulting & SI. Even though WPRO has a higher contribution from faster growing services (vs INFO/TCS), execution and much higher drag in other services is an issue for growth.

Fig. 66: Share of fast growing service lines (LTM) % HCLT and TCS have a higher share of fast growing service lines (IMS/BPO/Engg Services/Testing) vs. INFO

Source: Company data, Nomura research

Fig. 67: Growth comparison between service lines (LTM) % Faster growing services (IMS/BPO/Engg. services/testing) have grown materially faster than other services across companies.

Note: Fast growing segments for Infosys is calculated excluding a one-off revenue of $23mn, including which the growth would have been 11%

Source: Company data, Nomura research

• Share of Europe versus US: HCLT and TCS have higher European share which might be currently hurting in reported terms due to cross currency, but longer-term demand trends are more positive in Europe. However, divergence in European growth is significant with HCLT growing the fastest, TCS and INFO seeing similar growth inline with aggregate tier 1 IT and WPRO seeing minimal growth. Here too, while WPRO’s share from Europe is higher than INFO/TCS execution, higher share of the sluggish energy sector within Europe and weaker overall positioning is driving flattish growth trends at WPRO.

59

45

39

26

HCLT Wipro TCS Infosys

16

12

14

7

2

-2

7

5

HCLT Wipro TCS Infosys

LTM growth fast-growing service lines

LTM growth other service lines

Nomura | India IT services 16 December 2015

25

Fig. 68: Revenue share of US/Europe (LTM) % HCLT and TCS have a higher share of revenue from Europe. However, there is significant divergence in growth, with HCLT fastest, TCS/INFO growing inline with aggregate and WPRO flat

Source: Company data, Nomura research

Fig. 69: Growth comparison between geographies Europe in constant currency terms has consistently outperformed growth in US, though lately some moderation has been seen. We expect outperformance of Europe to be sustained going forward.

Source: Company data, Nomura research

• Share of BFSI/retail versus growing segments like manufacturing/healthcare: HCLT/INFO and CTSH score on this parameter, while TCS has a handicap of having a relatively larger BFSI/retail practice. BFSI growth to be largely dependent on market share gains as we remain cautious on incremental spending in light of weakening client financials.

Fig. 70: Share of manufacturing + healthcare vs. BFSI + retail (LTM) % HCLT and INFO have a higher share of the fast growing verticals vs WPRO/TCS

Source: Company data, Nomura research

Fig. 71: Growth comparison – manufacturing + healthcare vs.BFSI + retail (LTM) % Verticals like manufacturing +healthcare have grown faster than BFSI + retail at most companies

Source: Company data, Nomura research

• Lower cannibalisation and greater benefits from digital: The determinants of which company grows better are 1) share of on premise implementation and support vs SaaS – in ES practice and stronger consulting capabilities (CTSH, INFO), 2) greater ability to handle complexity in IMS practice, crucial for winning large deals in cloud/mobility transformation (HCLT/TCS) 3) Strong analytics and engineering services practice to benefit from IoT (HCLT) and 4) Stronger analytics capabilities to benefit from Big Data (CTSH/INFO/TCS). Overall, we believe HCLT will likely benefit the most from back-end digital and IoT, while CTSH should benefit from stronger front-end digital capabilities. We like INFO strategy of trying to target the newer technology spends through investment in IP (organic/inorganic/collaboration), bringing about organisational changes and increased aggression in traditional services (ADM/ES) by leveraging automation – reflected in better top clientele traction and ES turning the corner after underperforming for the last three years. While, TCS has strengths on both front-end

58

52 52

63

3126 27

23

HCL Tech Wipro TCS Infosys

US Europe

10%

10%

0%

5%

10%

15%

20%

25%

1QF

Y13

2QF

Y13

3QF

Y13

4QF

Y13

1QF

Y14

2QF

Y14

3QF

Y14

4QF

Y14

1QF

Y15

2QF

Y15

3QF

Y15

4QF

Y15

1QF

Y16

2QF

Y16

US Europe cc

35

50

58

4142 40

33 33

HCLT Infosys TCS Wipro

BFSI + Retail Mfg + Healthcare

8

45

7

21

10

7

14

0

5

10

15

20

25

TCS Infosys Wipro HCLT

BFSI + Retail Mfg + Healthcare

Nomura | India IT services 16 December 2015

26

and back-end digital, we believe currently the skew towards higher on-premise support in ES and larger presence in ADM will create a handicap for growth.

Pecking order: HCLT > CTSH > INFO > TCS > TECHM > WPRO • HCLT (HCLT IN, Buy, TP: INR1,020): We are positive on HCLT due to its: 1) superior

positioning in IMS (~35% of revenue) and likely market share gains in upcoming deal rebids (worth ~USD150bn over CY16-18); and 2) largest presence in engineering services (~19% of revenue), which we believe over the medium term could see similar trends as IMS on larger deals, increased interest in Europe and market share gains for Indian IT. We believe valuations are reasonable at ~13.5x FY17F P/E (EPS: 62.6) at a discount of ~18-24% to similar growing peers INFO/TCS. We expect HCLT to perform better than peers in 2HFY16F.

• CTSH (CTSH US, Buy, TP: USD72): We like CTSH as we believe it is well positioned relative to peers to benefit from: 1) nearly half of its revenues coming from healthcare and manufacturing (faster growing segments for Indian IT) 2) market share gains in BFSI and stronger positioning in the US; and 3) stronger front-end digital capabilities. This, we believe, is likely to enable the company to post best-in-class revenue and EPS CAGR of ~14% and ~18% respectively over FY15-17F.