suzlon energy suzl.ns suel in - myirisbreport.myiris.com/nfasipl/suzenerg_20150406.pdf · repower),...

TRANSCRIPT

Rating Starts at BuyTarget price Starts at INR 38

Closing price 1 April 2015 INR 26

Potential upside +43.7%

Anchor themesSuzlon Energy is a play on the emerging wind power sector in India. It has been India's market leader in this segment but has suffered multiple crises mostly related to an overstretched balance sheet. It is now a potential turnaround story.

Nomura vs consensusOur TP is in line with the Street, but we note that the stock is not well covered.

Research analysts

India Capital Goods

Amar Kedia - NFASL [email protected] +91 22 4037 4182

Key company data: See page 2 for company data and detailed price/index chart

Suzlon Energy SUZL.NS SUEL IN

EQUITY: POWER & UTILITIES

Wind with chance of sun; initiate w/Buy

Strategic corporate moves fuel turnaround story

Action: Initiate at Buy with TP of INR38; c.44% upside potential Suzlon Energy (SUEL) is a potential turnaround story in the emerging wind power sector in India, where it has traditionally been a market leader due to its strong end-to-end EPC and O&M capability. From a position of strength, SUEL has gone through multiple crises over the past five years including debt default. However, it has since taken corrective steps to substantially repair its balance sheet by selling off its German offshore wind arm, Senvion (formerly REpower), for €1bn and issuing fresh equity worth INR18bn to Dilip Shanghvi & Associates (DSA) – a promoter for Sun Pharma (SUNP IN).

After the financial restructuring and Senvion sell-off, SUEL is now an India pure play set to refocus on new order wins and execution, and well placed to win back 50% market share in the domestic wind equipment market.

Re-introduction of wind power incentives and supportive policy aimed at meeting the government’s ambitious wind energy target of 60GW by 2022 should help to drive demand for wind equipment, in our view.

Strong operating/financial leverage from under-utilised manufacturing facilities and debt reduction is likely to drive normalisation of margins and strong earnings growth for SUEL in the years ahead, as per our estimates.

Catalysts: Improving financials and PAT breakeven by early FY17F

Valuation: Trading at 11.5x FY17F EV/EBITDA SUEL is trading at 11.5x FY17F EV/EBITDA, which we believe does not reflect the company’s strong growth prospects over FY15-20F. On our estimates, not only is SUEL likely to recover 50% market share by FY17F thus aiding its PAT breakeven by then, but it also has the potential to grow its EBITDA by ~50% over FY17-20F thus justifying a premium valuation over its regional peers (Fig 33). Accordingly, we value SUEL at 15x FY17F EV/EBITDA to arrive at our TP of INR38/share, which implies c.44% upside.

Year-end 31 Mar FY14 FY15F FY16F FY17F

Currency (INR) Actual Old New Old New Old New

Revenue (mn) 204,029 N/A 201,538 N/A 95,036 N/A 124,670

Reported net profit (mn) -34,679 N/A -84,415 N/A -804 N/A 9,372

Normalised net profit (mn) -29,806 N/A -22,004 N/A -804 N/A 9,372

FD normalised EPS -8.02 N/A -4.86 N/A -0.14 N/A 1.57

FD norm. EPS growth (%) N/A N/A N/A N/A N/A N/A N/A

FD normalised P/E (x) N/A N/A N/A N/A N/A N/A 16.9

EV/EBITDA (x) N/A N/A 27.4 N/A 23.8 N/A 11.2

Price/book (x) N/A N/A N/A N/A N/A N/A N/A

Dividend yield (%) N/A N/A N/A N/A N/A N/A N/A

ROE (%) N/A N/A N/A N/A N/A N/A N/A

Net debt/equity (%) N/A N/A N/A N/A N/A N/A N/A

Source: Company data, Nomura estimates

Global Markets Research 6 April 2015

See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts.

Nomura | Suzlon Energy 6 April 2015

2

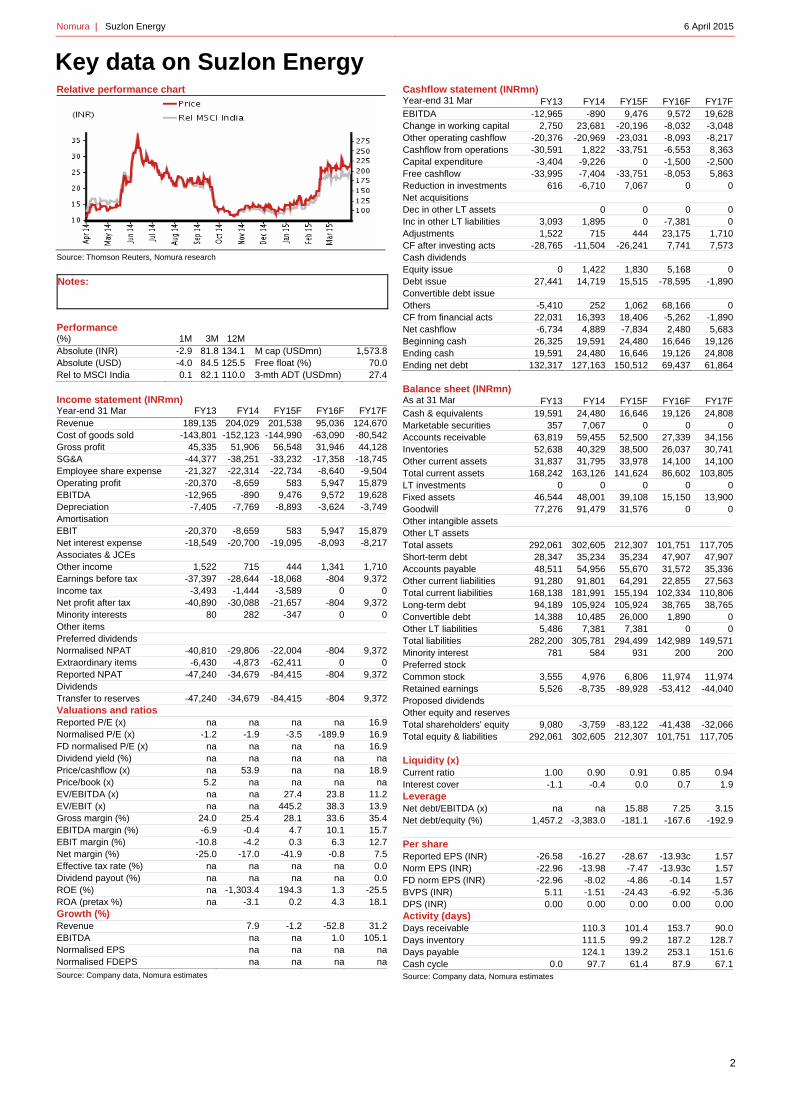

Key data on Suzlon Energy Relative performance chart

Source: Thomson Reuters, Nomura research

Notes:

Performance (%) 1M 3M 12MAbsolute (INR) -2.9 81.8 134.1 M cap (USDmn) 1,573.8Absolute (USD) -4.0 84.5 125.5 Free float (%) 70.0Rel to MSCI India 0.1 82.1 110.0 3-mth ADT (USDmn) 27.4 Income statement (INRmn) Year-end 31 Mar FY13 FY14 FY15F FY16F FY17FRevenue 189,135 204,029 201,538 95,036 124,670Cost of goods sold -143,801 -152,123 -144,990 -63,090 -80,542Gross profit 45,335 51,906 56,548 31,946 44,128SG&A -44,377 -38,251 -33,232 -17,358 -18,745Employee share expense -21,327 -22,314 -22,734 -8,640 -9,504Operating profit -20,370 -8,659 583 5,947 15,879EBITDA -12,965 -890 9,476 9,572 19,628Depreciation -7,405 -7,769 -8,893 -3,624 -3,749Amortisation

EBIT -20,370 -8,659 583 5,947 15,879Net interest expense -18,549 -20,700 -19,095 -8,093 -8,217Associates & JCEs

Other income 1,522 715 444 1,341 1,710Earnings before tax -37,397 -28,644 -18,068 -804 9,372Income tax -3,493 -1,444 -3,589 0 0Net profit after tax -40,890 -30,088 -21,657 -804 9,372Minority interests 80 282 -347 0 0Other items

Preferred dividends

Normalised NPAT -40,810 -29,806 -22,004 -804 9,372Extraordinary items -6,430 -4,873 -62,411 0 0Reported NPAT -47,240 -34,679 -84,415 -804 9,372Dividends

Transfer to reserves -47,240 -34,679 -84,415 -804 9,372Valuations and ratios

Reported P/E (x) na na na na 16.9Normalised P/E (x) -1.2 -1.9 -3.5 -189.9 16.9FD normalised P/E (x) na na na na 16.9Dividend yield (%) na na na na naPrice/cashflow (x) na 53.9 na na 18.9Price/book (x) 5.2 na na na naEV/EBITDA (x) na na 27.4 23.8 11.2EV/EBIT (x) na na 445.2 38.3 13.9Gross margin (%) 24.0 25.4 28.1 33.6 35.4EBITDA margin (%) -6.9 -0.4 4.7 10.1 15.7EBIT margin (%) -10.8 -4.2 0.3 6.3 12.7Net margin (%) -25.0 -17.0 -41.9 -0.8 7.5Effective tax rate (%) na na na na 0.0Dividend payout (%) na na na na 0.0ROE (%) na -1,303.4 194.3 1.3 -25.5ROA (pretax %) na -3.1 0.2 4.3 18.1Growth (%)

Revenue 7.9 -1.2 -52.8 31.2EBITDA na na 1.0 105.1Normalised EPS na na na naNormalised FDEPS na na na naSource: Company data, Nomura estimates

Cashflow statement (INRmn) Year-end 31 Mar FY13 FY14 FY15F FY16F FY17FEBITDA -12,965 -890 9,476 9,572 19,628Change in working capital 2,750 23,681 -20,196 -8,032 -3,048Other operating cashflow -20,376 -20,969 -23,031 -8,093 -8,217Cashflow from operations -30,591 1,822 -33,751 -6,553 8,363Capital expenditure -3,404 -9,226 0 -1,500 -2,500Free cashflow -33,995 -7,404 -33,751 -8,053 5,863Reduction in investments 616 -6,710 7,067 0 0Net acquisitions Dec in other LT assets 0 0 0 0Inc in other LT liabilities 3,093 1,895 0 -7,381 0Adjustments 1,522 715 444 23,175 1,710CF after investing acts -28,765 -11,504 -26,241 7,741 7,573Cash dividends Equity issue 0 1,422 1,830 5,168 0Debt issue 27,441 14,719 15,515 -78,595 -1,890Convertible debt issue Others -5,410 252 1,062 68,166 0CF from financial acts 22,031 16,393 18,406 -5,262 -1,890Net cashflow -6,734 4,889 -7,834 2,480 5,683Beginning cash 26,325 19,591 24,480 16,646 19,126Ending cash 19,591 24,480 16,646 19,126 24,808Ending net debt 132,317 127,163 150,512 69,437 61,864 Balance sheet (INRmn) As at 31 Mar FY13 FY14 FY15F FY16F FY17FCash & equivalents 19,591 24,480 16,646 19,126 24,808Marketable securities 357 7,067 0 0 0Accounts receivable 63,819 59,455 52,500 27,339 34,156Inventories 52,638 40,329 38,500 26,037 30,741Other current assets 31,837 31,795 33,978 14,100 14,100Total current assets 168,242 163,126 141,624 86,602 103,805LT investments 0 0 0 0 0Fixed assets 46,544 48,001 39,108 15,150 13,900Goodwill 77,276 91,479 31,576 0 0Other intangible assets Other LT assets Total assets 292,061 302,605 212,307 101,751 117,705Short-term debt 28,347 35,234 35,234 47,907 47,907Accounts payable 48,511 54,956 55,670 31,572 35,336Other current liabilities 91,280 91,801 64,291 22,855 27,563Total current liabilities 168,138 181,991 155,194 102,334 110,806Long-term debt 94,189 105,924 105,924 38,765 38,765Convertible debt 14,388 10,485 26,000 1,890 0Other LT liabilities 5,486 7,381 7,381 0 0Total liabilities 282,200 305,781 294,499 142,989 149,571Minority interest 781 584 931 200 200Preferred stock Common stock 3,555 4,976 6,806 11,974 11,974Retained earnings 5,526 -8,735 -89,928 -53,412 -44,040Proposed dividends Other equity and reserves Total shareholders' equity 9,080 -3,759 -83,122 -41,438 -32,066Total equity & liabilities 292,061 302,605 212,307 101,751 117,705

Liquidity (x)Current ratio 1.00 0.90 0.91 0.85 0.94Interest cover -1.1 -0.4 0.0 0.7 1.9LeverageNet debt/EBITDA (x) na na 15.88 7.25 3.15Net debt/equity (%) 1,457.2 -3,383.0 -181.1 -167.6 -192.9

Per shareReported EPS (INR) -26.58 -16.27 -28.67 -13.93c 1.57Norm EPS (INR) -22.96 -13.98 -7.47 -13.93c 1.57FD norm EPS (INR) -22.96 -8.02 -4.86 -0.14 1.57BVPS (INR) 5.11 -1.51 -24.43 -6.92 -5.36DPS (INR) 0.00 0.00 0.00 0.00 0.00Activity (days)Days receivable 110.3 101.4 153.7 90.0Days inventory 111.5 99.2 187.2 128.7Days payable 124.1 139.2 253.1 151.6Cash cycle 0.0 97.7 61.4 87.9 67.1Source: Company data, Nomura estimates

Nomura | Suzlon Energy 6 April 2015

3

Wind with chance of sun

Recapitalisation of the company to refuel growth story

Suzlon Energy is a well-known name in the wind equipment market in India and has been a market leader in its segment for over a decade in India. However, following product quality issues and subsequent financial crisis, the company suffered a liquidity squeeze and defaulted on repayments (as we discuss later in this report on pages 4 and 5). This had a negative impact on the company’s execution, given that the banks froze its working capital limit and customers turned cautious about placing orders with Suzlon.

During this period, Suzlon suffered from a massive debt overhang, which it had to clear.

After much deliberation, the company has finally addressed this by making two major strategic decisions:

1) It has agreed to a recapitalisation of the balance sheet by way of issuing new shares to Dilip Shanghvi & Assocoiates, which has brought in fresh equity of INR18bn apart from new working capital lines (over and above its existing banking facilities).

2) It has also sealed a deal in January 2015, to sell its 100% stake in German wind equipment maker Senvion that it had bought in 2008. This move will bring in €1bn for the company. As per the announcement, the deal is likely to have been closed by 31 March 2015.

Both moves are likely to yield ~INR90bn to the company, which will go towards repayment of its INR170bn debt and thus provide a much needed boost to repair its balance sheet.

As highlighted earlier, with these initiatives, the company is back on track to execute and source orders as it has in the past.

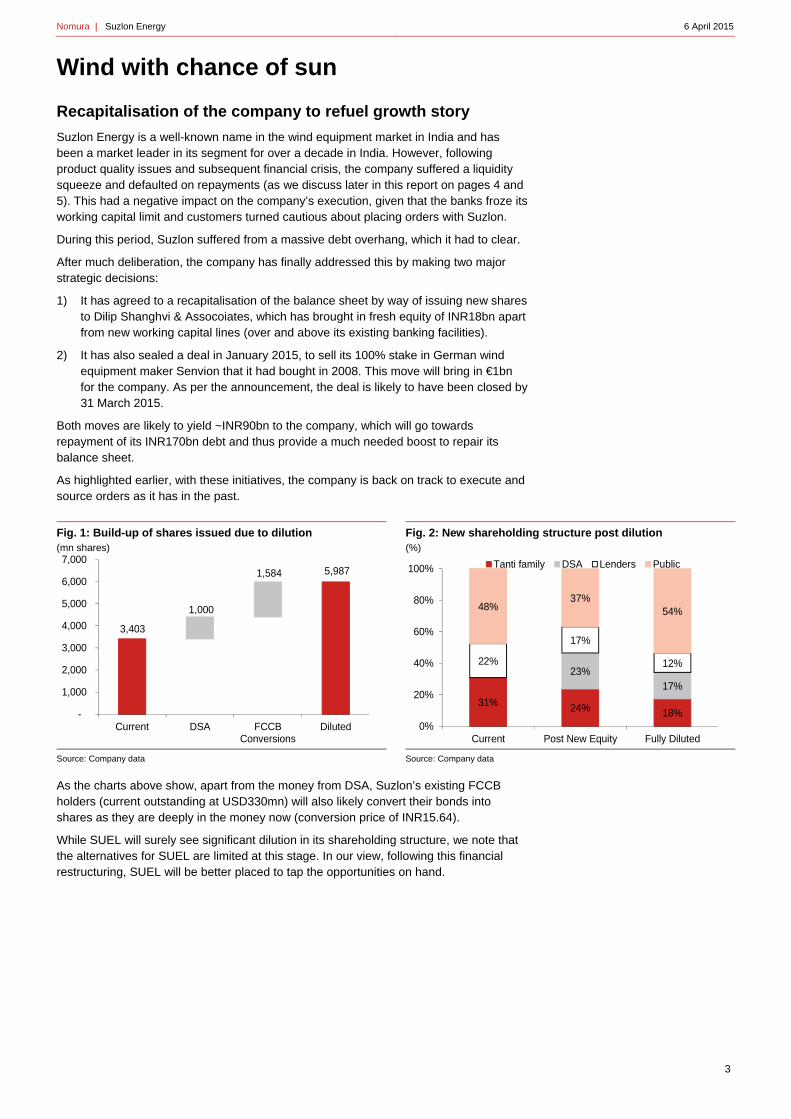

Fig. 1: Build-up of shares issued due to dilution (mn shares)

Source: Company data

Fig. 2: New shareholding structure post dilution (%)

Source: Company data

As the charts above show, apart from the money from DSA, Suzlon’s existing FCCB holders (current outstanding at USD330mn) will also likely convert their bonds into shares as they are deeply in the money now (conversion price of INR15.64).

While SUEL will surely see significant dilution in its shareholding structure, we note that the alternatives for SUEL are limited at this stage. In our view, following this financial restructuring, SUEL will be better placed to tap the opportunities on hand.

3,403

5,987

1,000

1,584

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Current DSA FCCBConversions

Diluted

31% 24% 18%

23%17%

22%

17%

12%

48%37%

54%

0%

20%

40%

60%

80%

100%

Current Post New Equity Fully Diluted

Tanti family DSA Lenders Public

Nomura | Suzlon Energy 6 April 2015

4

Senvion sale to reduce leverage

Suzlon’s acquisition of Senvion (formerly REpower) in 2008 helped it to optimise its product offerings as well as geographic presence. Senvion has been amongst the leaders in offshore wind technology and thus with the acquisition, Suzlon transformed itself into one of the world’s top-5 wind equipment makers. Soon after the acquisition, Senvion became the most profitable asset for Suzlon and even today accounts for the bulk of Suzlon’s consolidated orders and revenue.

In FY14, Senvion contributed ~73% of consolidated revenues for SUEL and more than 100% of its EBITDA as the domestic entity, Suzlon Wind, was making losses at the EBITDA level. In FY15F, we estimate a similar trend with Senvion contributing ~74% of consolidated revenues (INR149bn) and more than 100% of EBITDA (INR11.3bn from Senvion out of consolidated EBITDA of INR9.5bn).

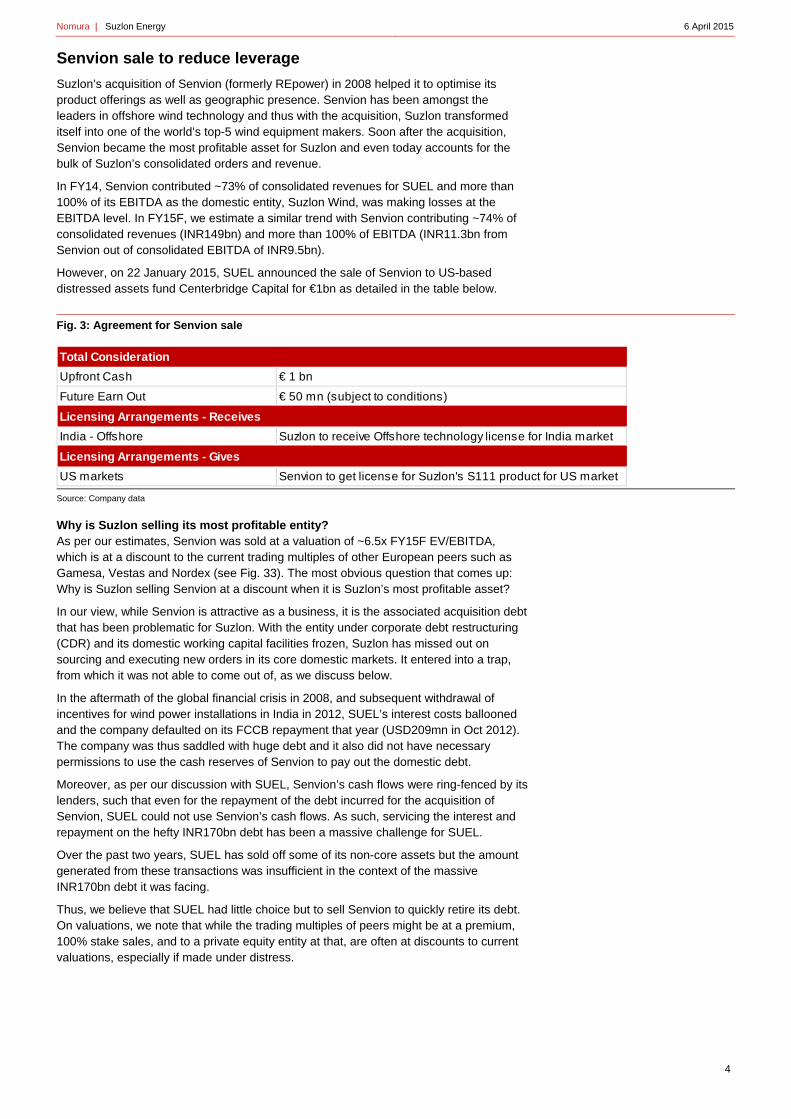

However, on 22 January 2015, SUEL announced the sale of Senvion to US-based distressed assets fund Centerbridge Capital for €1bn as detailed in the table below.

Fig. 3: Agreement for Senvion sale

Source: Company data

Why is Suzlon selling its most profitable entity? As per our estimates, Senvion was sold at a valuation of ~6.5x FY15F EV/EBITDA, which is at a discount to the current trading multiples of other European peers such as Gamesa, Vestas and Nordex (see Fig. 33). The most obvious question that comes up: Why is Suzlon selling Senvion at a discount when it is Suzlon’s most profitable asset?

In our view, while Senvion is attractive as a business, it is the associated acquisition debt that has been problematic for Suzlon. With the entity under corporate debt restructuring (CDR) and its domestic working capital facilities frozen, Suzlon has missed out on sourcing and executing new orders in its core domestic markets. It entered into a trap, from which it was not able to come out of, as we discuss below.

In the aftermath of the global financial crisis in 2008, and subsequent withdrawal of incentives for wind power installations in India in 2012, SUEL’s interest costs ballooned and the company defaulted on its FCCB repayment that year (USD209mn in Oct 2012). The company was thus saddled with huge debt and it also did not have necessary permissions to use the cash reserves of Senvion to pay out the domestic debt.

Moreover, as per our discussion with SUEL, Senvion’s cash flows were ring-fenced by its lenders, such that even for the repayment of the debt incurred for the acquisition of Senvion, SUEL could not use Senvion’s cash flows. As such, servicing the interest and repayment on the hefty INR170bn debt has been a massive challenge for SUEL.

Over the past two years, SUEL has sold off some of its non-core assets but the amount generated from these transactions was insufficient in the context of the massive INR170bn debt it was facing.

Thus, we believe that SUEL had little choice but to sell Senvion to quickly retire its debt. On valuations, we note that while the trading multiples of peers might be at a premium, 100% stake sales, and to a private equity entity at that, are often at discounts to current valuations, especially if made under distress.

Total Consideration

Upfront Cash € 1 bn

Future Earn Out € 50 mn (subject to conditions)

Licensing Arrangements - Receives

India - Offshore Suzlon to receive Offshore technology license for India market

Licensing Arrangements - Gives

US markets Senvion to get license for Suzlon's S111 product for US market

Nomura | Suzlon Energy 6 April 2015

5

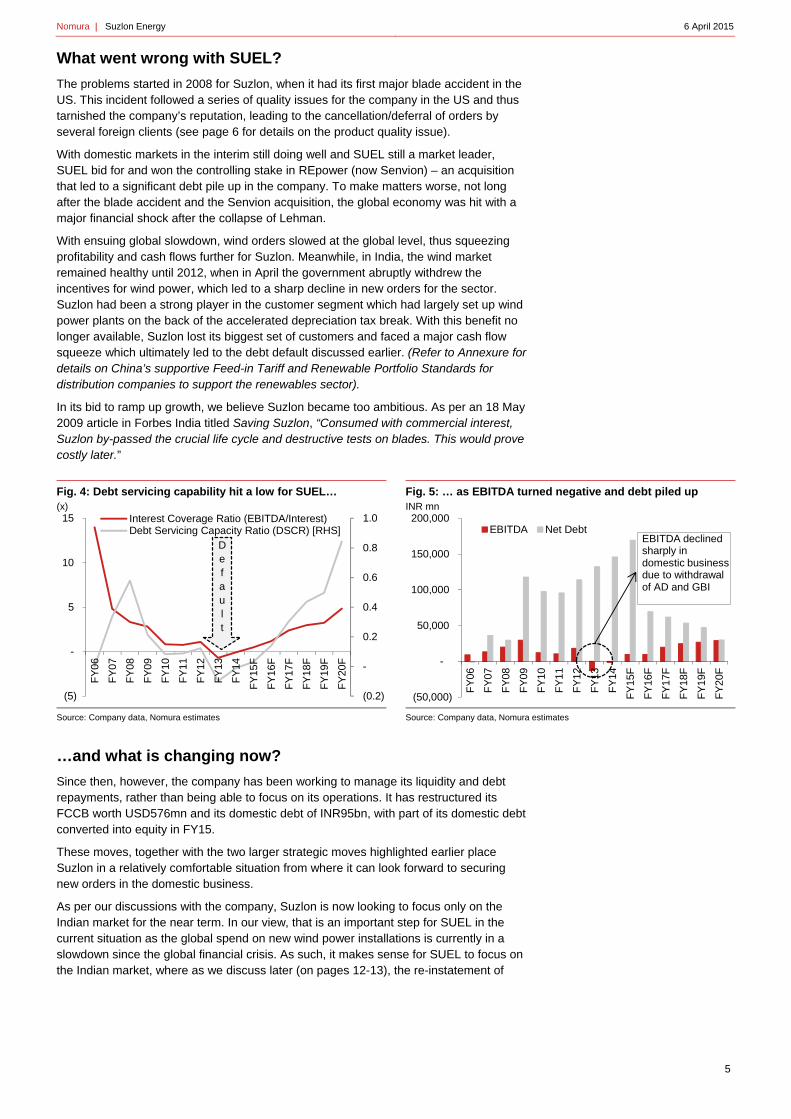

What went wrong with SUEL?

The problems started in 2008 for Suzlon, when it had its first major blade accident in the US. This incident followed a series of quality issues for the company in the US and thus tarnished the company’s reputation, leading to the cancellation/deferral of orders by several foreign clients (see page 6 for details on the product quality issue).

With domestic markets in the interim still doing well and SUEL still a market leader, SUEL bid for and won the controlling stake in REpower (now Senvion) – an acquisition that led to a significant debt pile up in the company. To make matters worse, not long after the blade accident and the Senvion acquisition, the global economy was hit with a major financial shock after the collapse of Lehman.

With ensuing global slowdown, wind orders slowed at the global level, thus squeezing profitability and cash flows further for Suzlon. Meanwhile, in India, the wind market remained healthy until 2012, when in April the government abruptly withdrew the incentives for wind power, which led to a sharp decline in new orders for the sector. Suzlon had been a strong player in the customer segment which had largely set up wind power plants on the back of the accelerated depreciation tax break. With this benefit no longer available, Suzlon lost its biggest set of customers and faced a major cash flow squeeze which ultimately led to the debt default discussed earlier. (Refer to Annexure for details on China’s supportive Feed-in Tariff and Renewable Portfolio Standards for distribution companies to support the renewables sector).

In its bid to ramp up growth, we believe Suzlon became too ambitious. As per an 18 May 2009 article in Forbes India titled Saving Suzlon, “Consumed with commercial interest, Suzlon by-passed the crucial life cycle and destructive tests on blades. This would prove costly later.”

Fig. 4: Debt servicing capability hit a low for SUEL… (x)

Source: Company data, Nomura estimates

Fig. 5: … as EBITDA turned negative and debt piled up INR mn

Source: Company data, Nomura estimates

…and what is changing now?

Since then, however, the company has been working to manage its liquidity and debt repayments, rather than being able to focus on its operations. It has restructured its FCCB worth USD576mn and its domestic debt of INR95bn, with part of its domestic debt converted into equity in FY15.

These moves, together with the two larger strategic moves highlighted earlier place Suzlon in a relatively comfortable situation from where it can look forward to securing new orders in the domestic business.

As per our discussions with the company, Suzlon is now looking to focus only on the Indian market for the near term. In our view, that is an important step for SUEL in the current situation as the global spend on new wind power installations is currently in a slowdown since the global financial crisis. As such, it makes sense for SUEL to focus on the Indian market, where as we discuss later (on pages 12-13), the re-instatement of

(0.2)

-

0.2

0.4

0.6

0.8

1.0

(5)

-

5

10

15

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15F

FY

16F

FY

17F

FY

18F

FY

19F

FY

20F

Interest Coverage Ratio (EBITDA/Interest)Debt Servicing Capacity Ratio (DSCR) [RHS]

Default

(50,000)

-

50,000

100,000

150,000

200,000

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15F

FY

16F

FY

17F

FY

18F

FY

19F

FY

20F

EBITDA Net DebtEBITDA declined sharply in domestic business due to withdrawal of AD and GBI

Nomura | Suzlon Energy 6 April 2015

6

incentives for the sector and supportive government policies are likely to drive a resurgence of demand for wind equipment.

Moreover, Suzlon has historically been a very strong player in the Indian market with over 50% market share. It still operates and manages (on behalf of its customers) ~38% of the total installed wind capacity in India. Thus, it has a rich experience of working with the local authorities, securing land, working with the often difficult state electricity boards or distribution companies (discoms), and managing difficult logistics/transportation requirements in India. As per our feedback from the industry not only for the wind power equipment market but even for other capital goods components, foreign companies have often found the conditions in India difficult when related to managing local authorities, land issues, transmission or logistical issues, etc. As such, we think SUEL is best placed to win back its 50% market share within a short span of time.

Its order backlog of ~1.15GW (bulk of this in India) already implies ~40% market share of potential installations in India in FY16F.

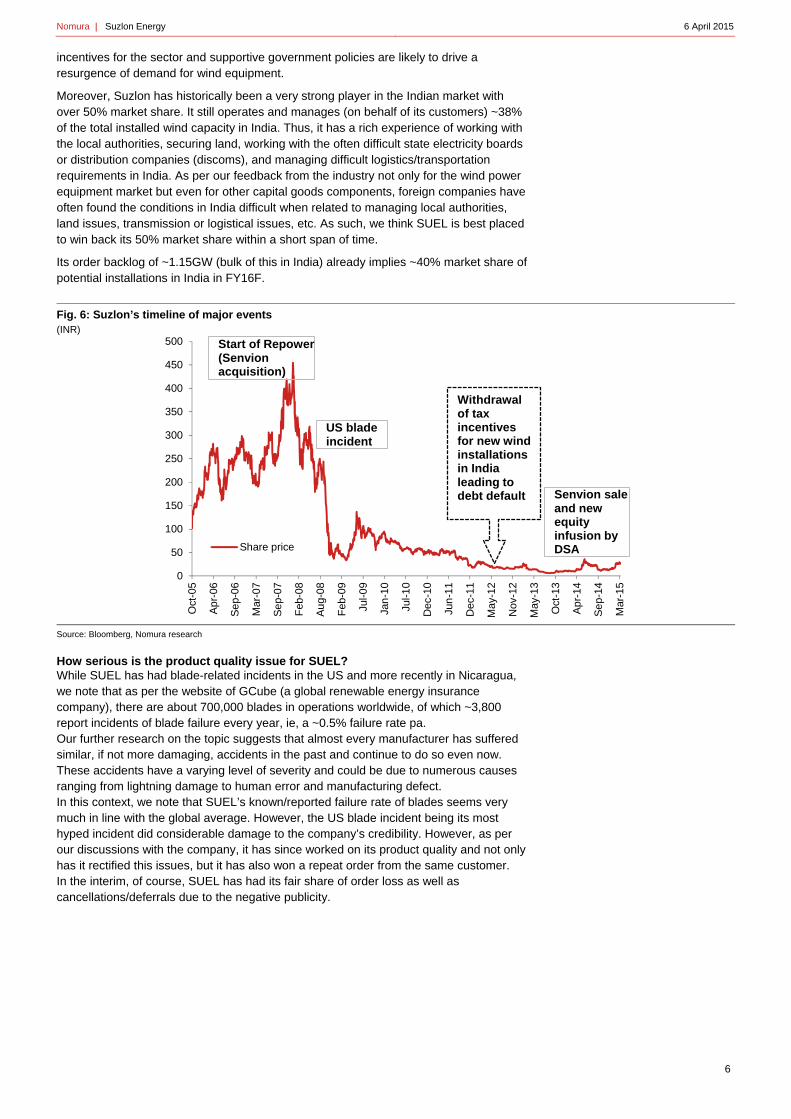

Fig. 6: Suzlon’s timeline of major events (INR)

Source: Bloomberg, Nomura research

How serious is the product quality issue for SUEL? While SUEL has had blade-related incidents in the US and more recently in Nicaragua, we note that as per the website of GCube (a global renewable energy insurance company), there are about 700,000 blades in operations worldwide, of which ~3,800 report incidents of blade failure every year, ie, a ~0.5% failure rate pa. Our further research on the topic suggests that almost every manufacturer has suffered similar, if not more damaging, accidents in the past and continue to do so even now. These accidents have a varying level of severity and could be due to numerous causes ranging from lightning damage to human error and manufacturing defect. In this context, we note that SUEL’s known/reported failure rate of blades seems very much in line with the global average. However, the US blade incident being its most hyped incident did considerable damage to the company’s credibility. However, as per our discussions with the company, it has since worked on its product quality and not only has it rectified this issues, but it has also won a repeat order from the same customer. In the interim, of course, SUEL has had its fair share of order loss as well as cancellations/deferrals due to the negative publicity.

0

50

100

150

200

250

300

350

400

450

500

Oct

-05

Ap

r-06

Se

p-06

Mar

-07

Se

p-07

Feb

-08

Au

g-08

Feb

-09

Jul-0

9

Jan

-10

Jul-1

0

Dec

-10

Jun

-11

Dec

-11

May

-12

Nov

-12

May

-13

Oct

-13

Ap

r-14

Se

p-14

Mar

-15

Share price

Start of Repower (Senvion acquisition)

US blade incident

Senvion sale and new equity infusion by DSA

Withdrawal of tax incentives for new wind installations in India leading to debt default

Nomura | Suzlon Energy 6 April 2015

7

Key investment thesis

Bright medium-term prospects for India’s wind industry

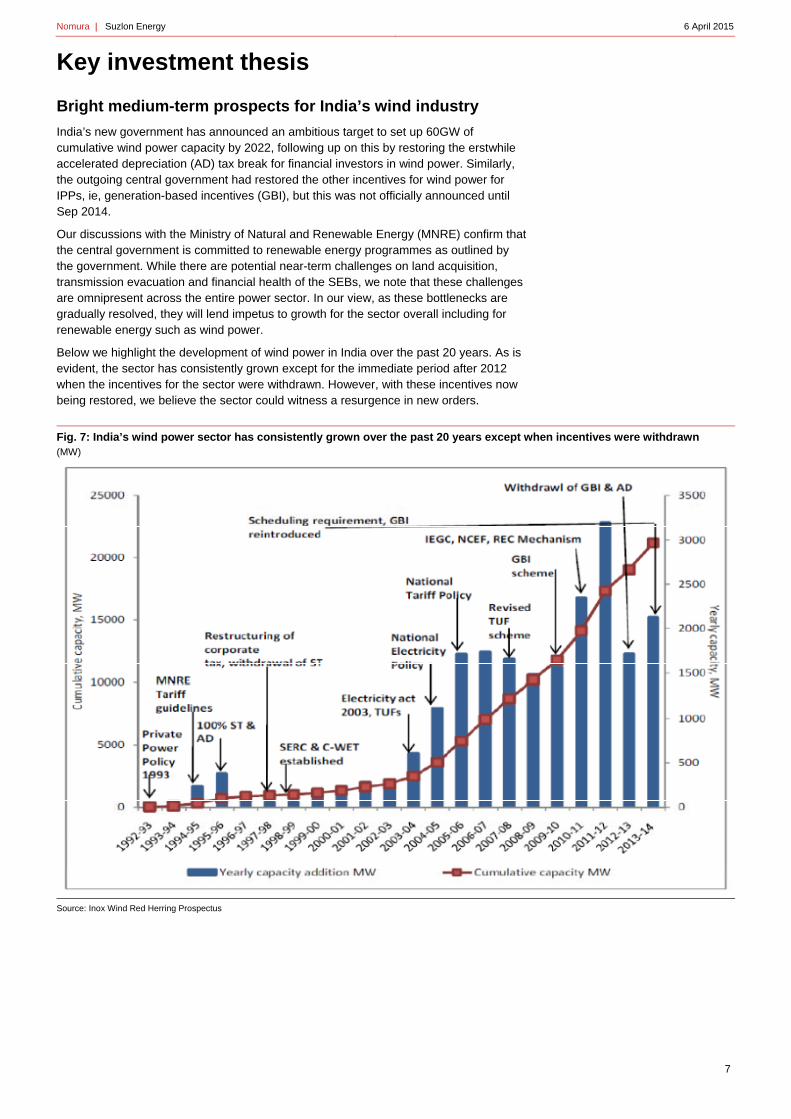

India’s new government has announced an ambitious target to set up 60GW of cumulative wind power capacity by 2022, following up on this by restoring the erstwhile accelerated depreciation (AD) tax break for financial investors in wind power. Similarly, the outgoing central government had restored the other incentives for wind power for IPPs, ie, generation-based incentives (GBI), but this was not officially announced until Sep 2014.

Our discussions with the Ministry of Natural and Renewable Energy (MNRE) confirm that the central government is committed to renewable energy programmes as outlined by the government. While there are potential near-term challenges on land acquisition, transmission evacuation and financial health of the SEBs, we note that these challenges are omnipresent across the entire power sector. In our view, as these bottlenecks are gradually resolved, they will lend impetus to growth for the sector overall including for renewable energy such as wind power.

Below we highlight the development of wind power in India over the past 20 years. As is evident, the sector has consistently grown except for the immediate period after 2012 when the incentives for the sector were withdrawn. However, with these incentives now being restored, we believe the sector could witness a resurgence in new orders.

Fig. 7: India’s wind power sector has consistently grown over the past 20 years except when incentives were withdrawn (MW)

Source: Inox Wind Red Herring Prospectus

Nomura | Suzlon Energy 6 April 2015

8

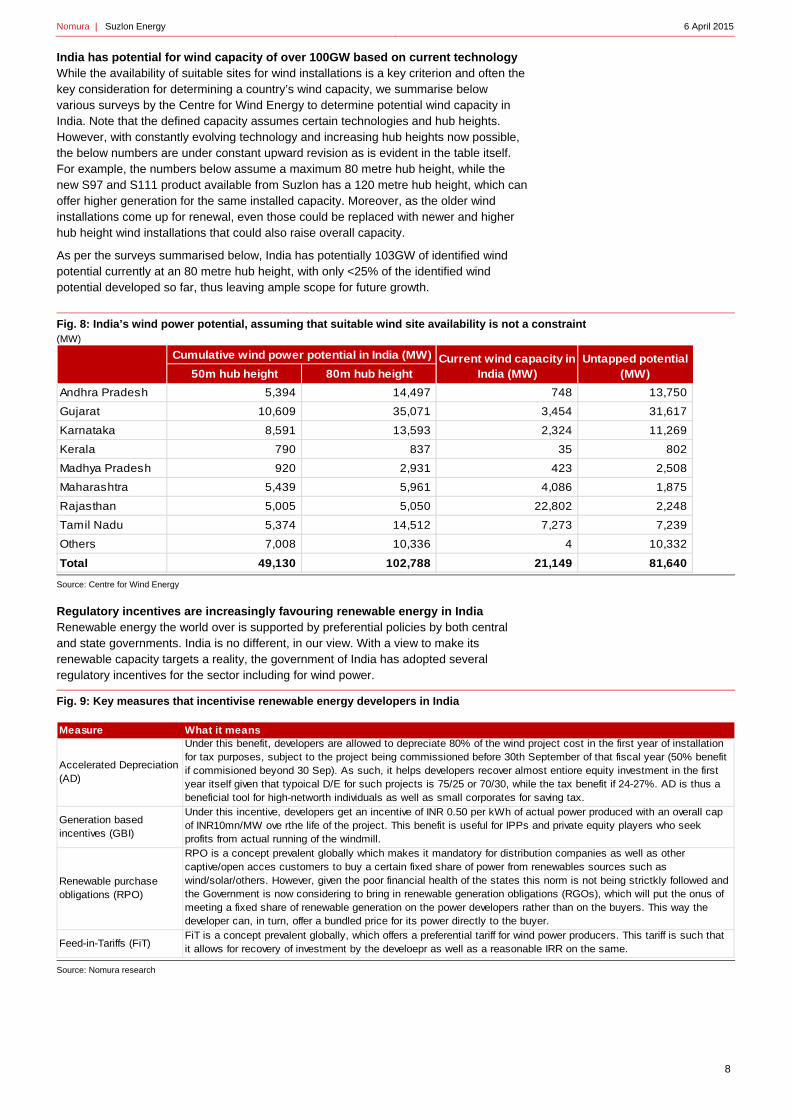

India has potential for wind capacity of over 100GW based on current technology While the availability of suitable sites for wind installations is a key criterion and often the key consideration for determining a country’s wind capacity, we summarise below various surveys by the Centre for Wind Energy to determine potential wind capacity in India. Note that the defined capacity assumes certain technologies and hub heights. However, with constantly evolving technology and increasing hub heights now possible, the below numbers are under constant upward revision as is evident in the table itself. For example, the numbers below assume a maximum 80 metre hub height, while the new S97 and S111 product available from Suzlon has a 120 metre hub height, which can offer higher generation for the same installed capacity. Moreover, as the older wind installations come up for renewal, even those could be replaced with newer and higher hub height wind installations that could also raise overall capacity.

As per the surveys summarised below, India has potentially 103GW of identified wind potential currently at an 80 metre hub height, with only <25% of the identified wind potential developed so far, thus leaving ample scope for future growth.

Fig. 8: India’s wind power potential, assuming that suitable wind site availability is not a constraint (MW)

Source: Centre for Wind Energy

Regulatory incentives are increasingly favouring renewable energy in India Renewable energy the world over is supported by preferential policies by both central and state governments. India is no different, in our view. With a view to make its renewable capacity targets a reality, the government of India has adopted several regulatory incentives for the sector including for wind power. Fig. 9: Key measures that incentivise renewable energy developers in India

Source: Nomura research

50m hub height 80m hub height

Andhra Pradesh 5,394 14,497 748 13,750

Gujarat 10,609 35,071 3,454 31,617

Karnataka 8,591 13,593 2,324 11,269

Kerala 790 837 35 802

Madhya Pradesh 920 2,931 423 2,508

Maharashtra 5,439 5,961 4,086 1,875

Rajasthan 5,005 5,050 22,802 2,248

Tamil Nadu 5,374 14,512 7,273 7,239

Others 7,008 10,336 4 10,332

Total 49,130 102,788 21,149 81,640

Cumulative wind power potential in India (MW) Current wind capacity in India (MW)

Untapped potential (MW)

Measure What it means

Accelerated Depreciation (AD)

Under this benefit, developers are allowed to depreciate 80% of the wind project cost in the first year of installation for tax purposes, subject to the project being commissioned before 30th September of that fiscal year (50% benefit if commisioned beyond 30 Sep). As such, it helps developers recover almost entiore equity investment in the first year itself given that typoical D/E for such projects is 75/25 or 70/30, while the tax benefit if 24-27%. AD is thus a beneficial tool for high-networth individuals as well as small corporates for saving tax.

Generation based incentives (GBI)

Under this incentive, developers get an incentive of INR 0.50 per kWh of actual power produced with an overall cap of INR10mn/MW ove rthe life of the project. This benefit is useful for IPPs and private equity players who seek profits from actual running of the windmill.

Renewable purchase obligations (RPO)

RPO is a concept prevalent globally which makes it mandatory for distribution companies as well as other captive/open acces customers to buy a certain fixed share of power from renewables sources such as wind/solar/others. However, given the poor financial health of the states this norm is not being strictkly followed and the Government is now considering to bring in renewable generation obligations (RGOs), which will put the onus of meeting a fixed share of renewable generation on the power developers rather than on the buyers. This way the developer can, in turn, offer a bundled price for its power directly to the buyer.

Feed-in-Tariffs (FiT)FiT is a concept prevalent globally, which offers a preferential tariff for wind power producers. This tariff is such that it allows for recovery of investment by the develoepr as well as a reasonable IRR on the same.

Nomura | Suzlon Energy 6 April 2015

9

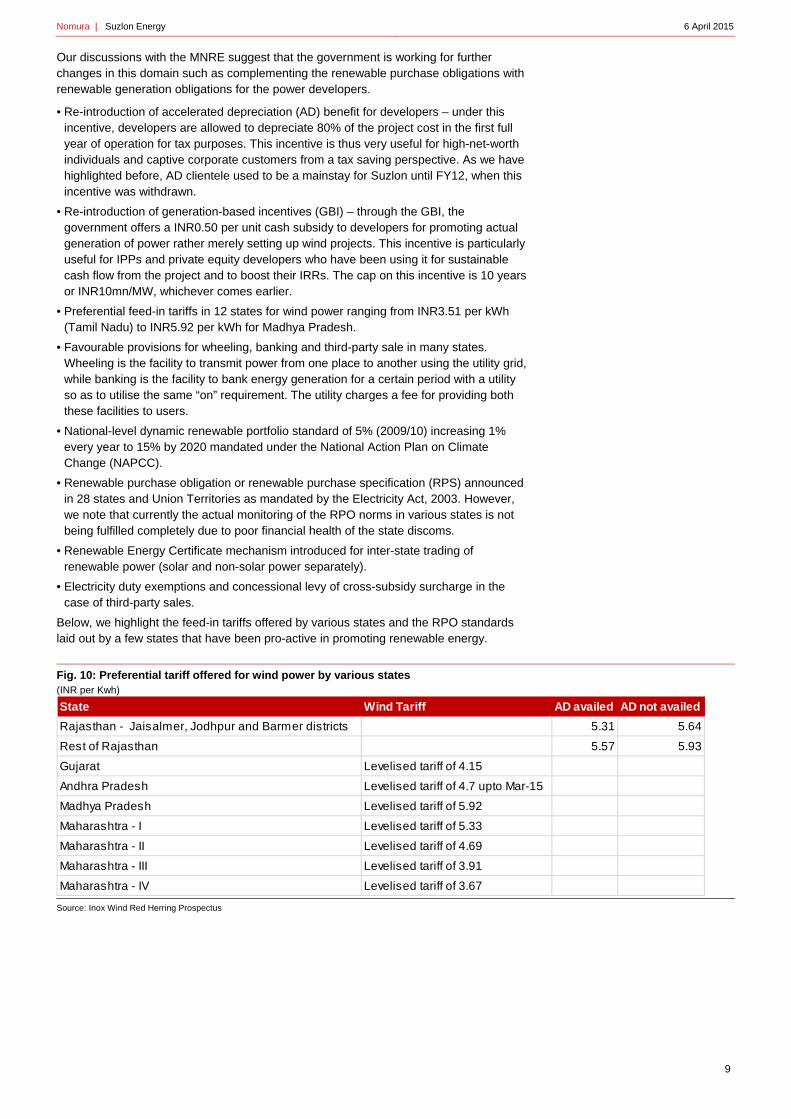

Our discussions with the MNRE suggest that the government is working for further changes in this domain such as complementing the renewable purchase obligations with renewable generation obligations for the power developers.

• Re-introduction of accelerated depreciation (AD) benefit for developers – under this incentive, developers are allowed to depreciate 80% of the project cost in the first full year of operation for tax purposes. This incentive is thus very useful for high-net-worth individuals and captive corporate customers from a tax saving perspective. As we have highlighted before, AD clientele used to be a mainstay for Suzlon until FY12, when this incentive was withdrawn.

• Re-introduction of generation-based incentives (GBI) – through the GBI, the government offers a INR0.50 per unit cash subsidy to developers for promoting actual generation of power rather merely setting up wind projects. This incentive is particularly useful for IPPs and private equity developers who have been using it for sustainable cash flow from the project and to boost their IRRs. The cap on this incentive is 10 years or INR10mn/MW, whichever comes earlier.

• Preferential feed-in tariffs in 12 states for wind power ranging from INR3.51 per kWh (Tamil Nadu) to INR5.92 per kWh for Madhya Pradesh.

• Favourable provisions for wheeling, banking and third-party sale in many states. Wheeling is the facility to transmit power from one place to another using the utility grid, while banking is the facility to bank energy generation for a certain period with a utility so as to utilise the same “on” requirement. The utility charges a fee for providing both these facilities to users.

• National-level dynamic renewable portfolio standard of 5% (2009/10) increasing 1% every year to 15% by 2020 mandated under the National Action Plan on Climate Change (NAPCC).

• Renewable purchase obligation or renewable purchase specification (RPS) announced in 28 states and Union Territories as mandated by the Electricity Act, 2003. However, we note that currently the actual monitoring of the RPO norms in various states is not being fulfilled completely due to poor financial health of the state discoms.

• Renewable Energy Certificate mechanism introduced for inter-state trading of renewable power (solar and non-solar power separately).

• Electricity duty exemptions and concessional levy of cross-subsidy surcharge in the case of third-party sales.

Below, we highlight the feed-in tariffs offered by various states and the RPO standards laid out by a few states that have been pro-active in promoting renewable energy.

Fig. 10: Preferential tariff offered for wind power by various states (INR per Kwh)

Source: Inox Wind Red Herring Prospectus

State Wind Tariff AD availed AD not availed

Rajasthan - Jaisalmer, Jodhpur and Barmer districts 5.31 5.64

Rest of Rajasthan 5.57 5.93

Gujarat Levelised tariff of 4.15

Andhra Pradesh Levelised tariff of 4.7 upto Mar-15

Madhya Pradesh Levelised tariff of 5.92

Maharashtra - I Levelised tariff of 5.33

Maharashtra - II Levelised tariff of 4.69

Maharashtra - III Levelised tariff of 3.91

Maharashtra - IV Levelised tariff of 3.67

Nomura | Suzlon Energy 6 April 2015

10

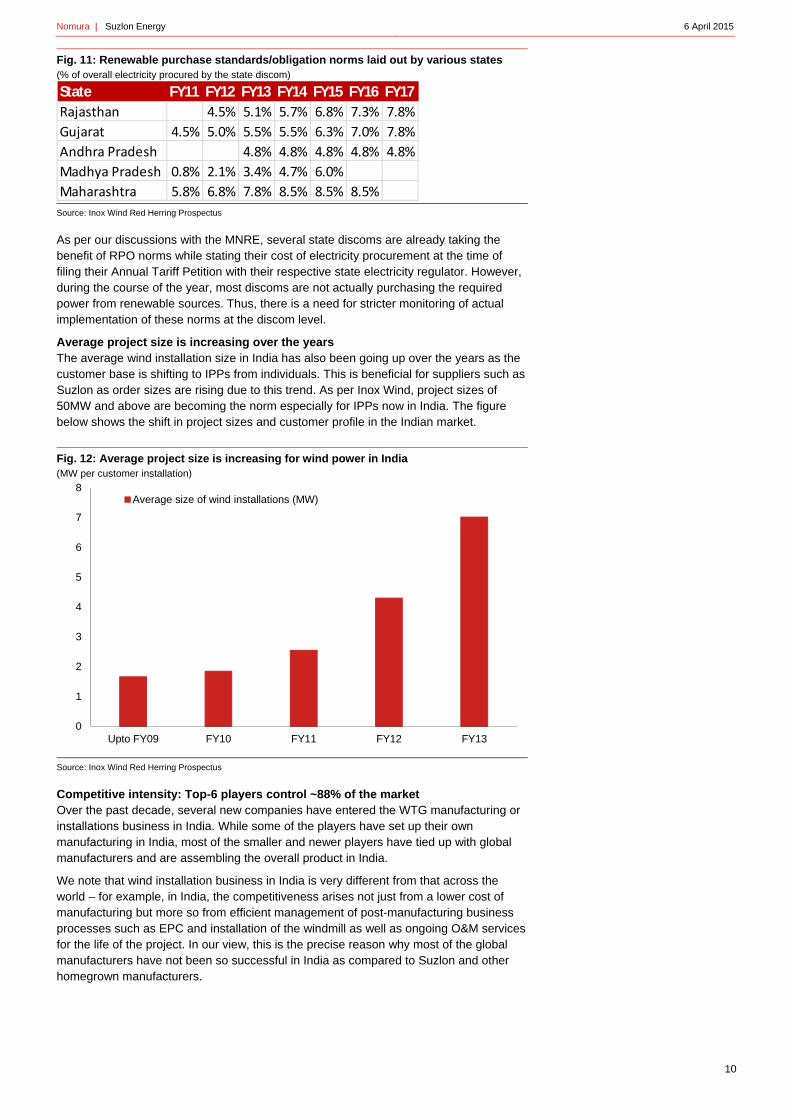

Fig. 11: Renewable purchase standards/obligation norms laid out by various states (% of overall electricity procured by the state discom)

Source: Inox Wind Red Herring Prospectus

As per our discussions with the MNRE, several state discoms are already taking the benefit of RPO norms while stating their cost of electricity procurement at the time of filing their Annual Tariff Petition with their respective state electricity regulator. However, during the course of the year, most discoms are not actually purchasing the required power from renewable sources. Thus, there is a need for stricter monitoring of actual implementation of these norms at the discom level.

Average project size is increasing over the years The average wind installation size in India has also been going up over the years as the customer base is shifting to IPPs from individuals. This is beneficial for suppliers such as Suzlon as order sizes are rising due to this trend. As per Inox Wind, project sizes of 50MW and above are becoming the norm especially for IPPs now in India. The figure below shows the shift in project sizes and customer profile in the Indian market.

Fig. 12: Average project size is increasing for wind power in India (MW per customer installation)

Source: Inox Wind Red Herring Prospectus

Competitive intensity: Top-6 players control ~88% of the market Over the past decade, several new companies have entered the WTG manufacturing or installations business in India. While some of the players have set up their own manufacturing in India, most of the smaller and newer players have tied up with global manufacturers and are assembling the overall product in India.

We note that wind installation business in India is very different from that across the world – for example, in India, the competitiveness arises not just from a lower cost of manufacturing but more so from efficient management of post-manufacturing business processes such as EPC and installation of the windmill as well as ongoing O&M services for the life of the project. In our view, this is the precise reason why most of the global manufacturers have not been so successful in India as compared to Suzlon and other homegrown manufacturers.

State FY11 FY12 FY13 FY14 FY15 FY16 FY17

Rajasthan 4.5% 5.1% 5.7% 6.8% 7.3% 7.8%

Gujarat 4.5% 5.0% 5.5% 5.5% 6.3% 7.0% 7.8%

Andhra Pradesh 4.8% 4.8% 4.8% 4.8% 4.8%

Madhya Pradesh 0.8% 2.1% 3.4% 4.7% 6.0%

Maharashtra 5.8% 6.8% 7.8% 8.5% 8.5% 8.5%

0

1

2

3

4

5

6

7

8

Upto FY09 FY10 FY11 FY12 FY13

Average size of wind installations (MW)

Nomura | Suzlon Energy 6 April 2015

11

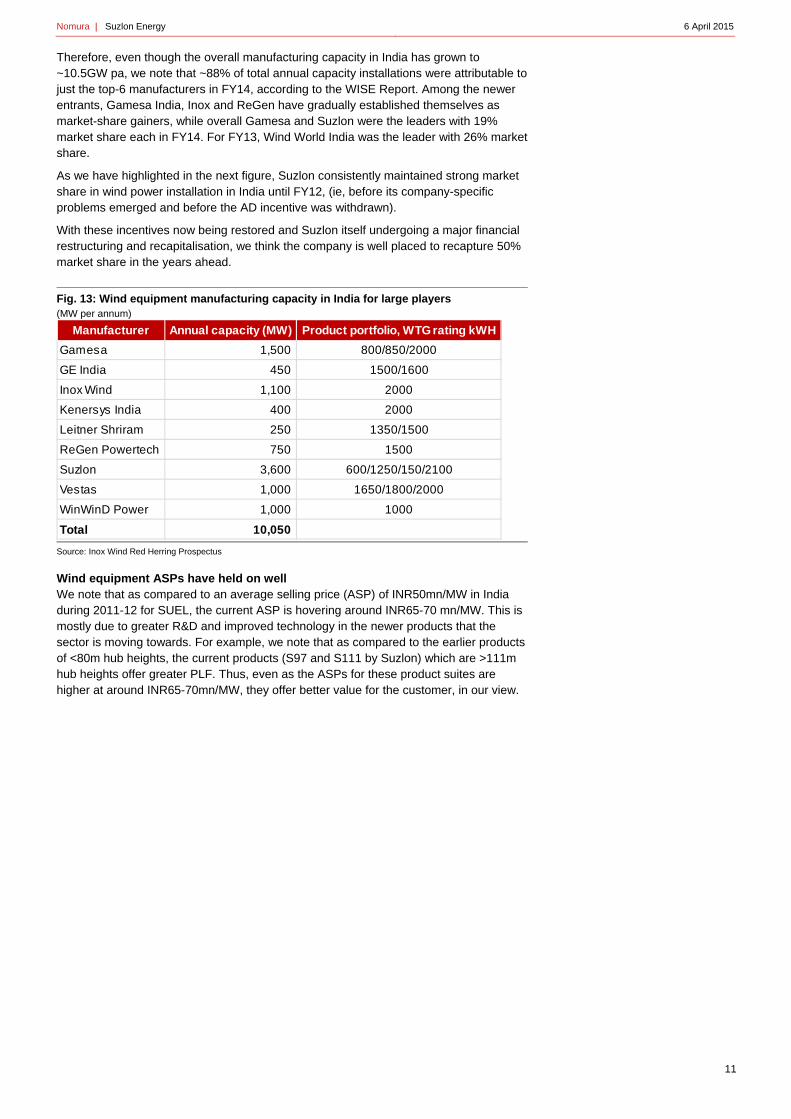

Therefore, even though the overall manufacturing capacity in India has grown to ~10.5GW pa, we note that ~88% of total annual capacity installations were attributable to just the top-6 manufacturers in FY14, according to the WISE Report. Among the newer entrants, Gamesa India, Inox and ReGen have gradually established themselves as market-share gainers, while overall Gamesa and Suzlon were the leaders with 19% market share each in FY14. For FY13, Wind World India was the leader with 26% market share.

As we have highlighted in the next figure, Suzlon consistently maintained strong market share in wind power installation in India until FY12, (ie, before its company-specific problems emerged and before the AD incentive was withdrawn).

With these incentives now being restored and Suzlon itself undergoing a major financial restructuring and recapitalisation, we think the company is well placed to recapture 50% market share in the years ahead.

Fig. 13: Wind equipment manufacturing capacity in India for large players (MW per annum)

Source: Inox Wind Red Herring Prospectus

Wind equipment ASPs have held on well We note that as compared to an average selling price (ASP) of INR50mn/MW in India during 2011-12 for SUEL, the current ASP is hovering around INR65-70 mn/MW. This is mostly due to greater R&D and improved technology in the newer products that the sector is moving towards. For example, we note that as compared to the earlier products of <80m hub heights, the current products (S97 and S111 by Suzlon) which are >111m hub heights offer greater PLF. Thus, even as the ASPs for these product suites are higher at around INR65-70mn/MW, they offer better value for the customer, in our view.

Manufacturer Annual capacity (MW) Product portfolio, WTG rating kWH

Gamesa 1,500 800/850/2000

GE India 450 1500/1600

Inox Wind 1,100 2000

Kenersys India 400 2000

Leitner Shriram 250 1350/1500

ReGen Powertech 750 1500

Suzlon 3,600 600/1250/150/2100

Vestas 1,000 1650/1800/2000

WinWinD Power 1,000 1000

Total 10,050

Nomura | Suzlon Energy 6 April 2015

12

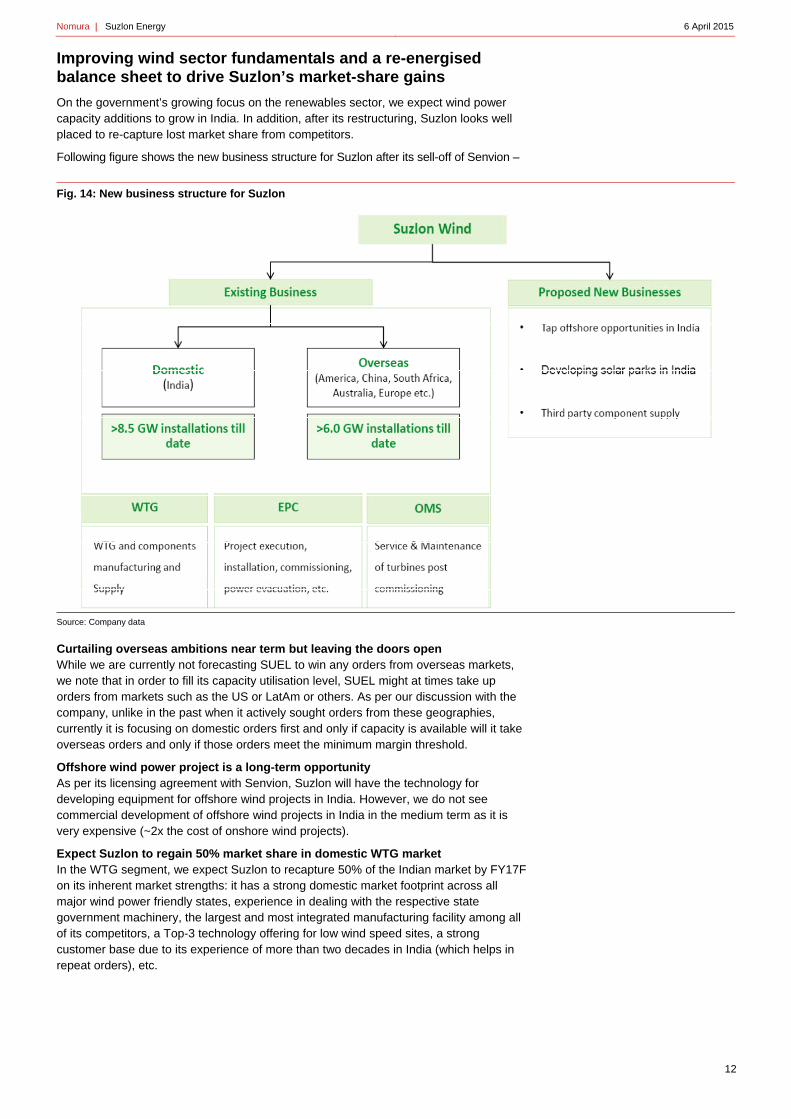

Improving wind sector fundamentals and a re-energised balance sheet to drive Suzlon’s market-share gains

On the government’s growing focus on the renewables sector, we expect wind power capacity additions to grow in India. In addition, after its restructuring, Suzlon looks well placed to re-capture lost market share from competitors.

Following figure shows the new business structure for Suzlon after its sell-off of Senvion –

Fig. 14: New business structure for Suzlon

Source: Company data

Curtailing overseas ambitions near term but leaving the doors open While we are currently not forecasting SUEL to win any orders from overseas markets, we note that in order to fill its capacity utilisation level, SUEL might at times take up orders from markets such as the US or LatAm or others. As per our discussion with the company, unlike in the past when it actively sought orders from these geographies, currently it is focusing on domestic orders first and only if capacity is available will it take overseas orders and only if those orders meet the minimum margin threshold.

Offshore wind power project is a long-term opportunity As per its licensing agreement with Senvion, Suzlon will have the technology for developing equipment for offshore wind projects in India. However, we do not see commercial development of offshore wind projects in India in the medium term as it is very expensive (~2x the cost of onshore wind projects).

Expect Suzlon to regain 50% market share in domestic WTG market In the WTG segment, we expect Suzlon to recapture 50% of the Indian market by FY17F on its inherent market strengths: it has a strong domestic market footprint across all major wind power friendly states, experience in dealing with the respective state government machinery, the largest and most integrated manufacturing facility among all of its competitors, a Top-3 technology offering for low wind speed sites, a strong customer base due to its experience of more than two decades in India (which helps in repeat orders), etc.

Nomura | Suzlon Energy 6 April 2015

13

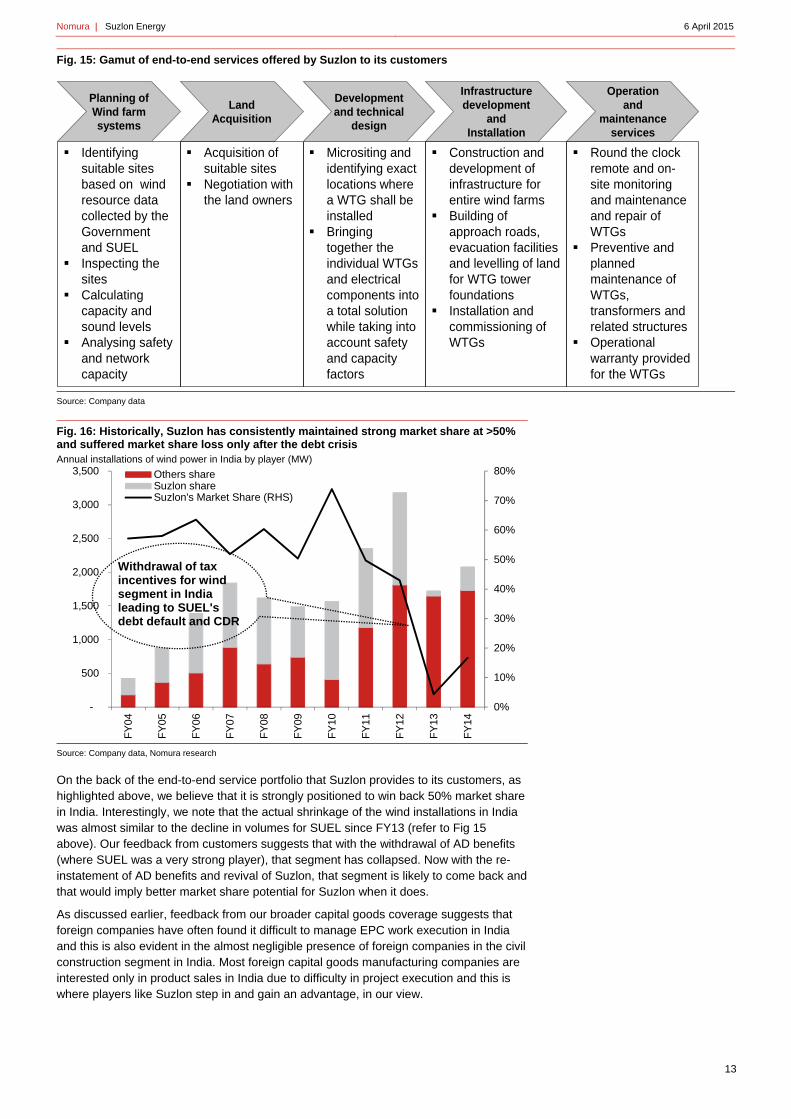

Fig. 15: Gamut of end-to-end services offered by Suzlon to its customers

Source: Company data

Fig. 16: Historically, Suzlon has consistently maintained strong market share at >50% and suffered market share loss only after the debt crisis Annual installations of wind power in India by player (MW)

Source: Company data, Nomura research

On the back of the end-to-end service portfolio that Suzlon provides to its customers, as highlighted above, we believe that it is strongly positioned to win back 50% market share in India. Interestingly, we note that the actual shrinkage of the wind installations in India was almost similar to the decline in volumes for SUEL since FY13 (refer to Fig 15 above). Our feedback from customers suggests that with the withdrawal of AD benefits (where SUEL was a very strong player), that segment has collapsed. Now with the re-instatement of AD benefits and revival of Suzlon, that segment is likely to come back and that would imply better market share potential for Suzlon when it does.

As discussed earlier, feedback from our broader capital goods coverage suggests that foreign companies have often found it difficult to manage EPC work execution in India and this is also evident in the almost negligible presence of foreign companies in the civil construction segment in India. Most foreign capital goods manufacturing companies are interested only in product sales in India due to difficulty in project execution and this is where players like Suzlon step in and gain an advantage, in our view.

Identifying suitable sites based on wind resource data collected by the Government and SUEL

Inspecting the sites

Calculating capacity and sound levels

Analysing safety and network capacity

Land Acquisition

Acquisition of suitable sites

Negotiation with the land owners

Planning of Wind farm systems

Micrositing and identifying exact locations where a WTG shall be installed

Bringing together the individual WTGs and electrical components into a total solution while taking into account safety and capacity factors

Infrastructure development

and Installation

Construction and development of infrastructure for entire wind farms

Building of approach roads, evacuation facilities and levelling of land for WTG tower foundations

Installation and commissioning of WTGs

Development and technical

design

Operation and

maintenance services

Round the clock remote and on-site monitoring and maintenance and repair of WTGs

Preventive and planned maintenance of WTGs, transformers and related structures

Operational warranty provided for the WTGs

0%

10%

20%

30%

40%

50%

60%

70%

80%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14Others shareSuzlon shareSuzlon's Market Share (RHS)

Withdrawal of tax incentives for wind segment in India leading to SUEL's debt default and CDR

Nomura | Suzlon Energy 6 April 2015

14

We think SUEL is best placed to win back its 50% market share within a short span of time. The successful execution of its current order backlog of ~1.15GW (bulk of this in India) would already imply ~40% market share of potential installations in India in FY16F.

Exploring hybrid solar and wind power projects as a commercial option Suzlon has an effective customer base of ~8.5GW of wind installations in India. With land availability and grid connectivity being key bottlenecks for incremental renewable energy installations, Suzlon is currently considering hybrid development of wind and solar at the same site. For this, Suzlon is likely to approach its existing customers for renting out the existing wind sites for installing solar panels at the same sites, which can thus have synergies in terms of O&M cost, grid infrastructure and land. Hybrid parks will also qualify for feed-in tariffs by discoms, unlike solar power which is not allowed feed-in tariffs. However, the proposal is still at the initial stages and will likely commercialise towards the end of FY17F. Meanwhile, Suzlon itself does not plan to take up manufacturing of solar equipment but will play the role of an EPC and O&M player only.

Our discussion with the MNRE confirmed that this model is viable and even the MNRE is thinking in similar directions. However, there are certain challenges with respect to water availability for solar panels at wind sites. We currently do not forecast any contribution from Suzlon’s proposed venture into hybrid development of solar and wind parks.

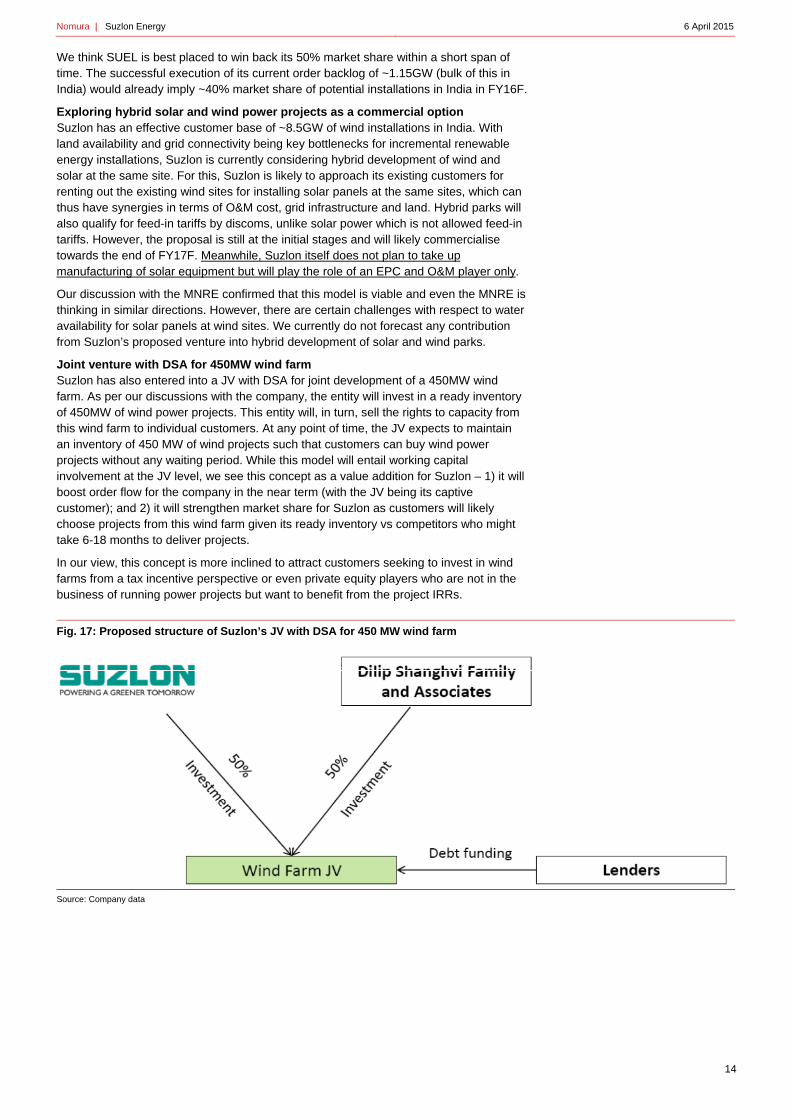

Joint venture with DSA for 450MW wind farm Suzlon has also entered into a JV with DSA for joint development of a 450MW wind farm. As per our discussions with the company, the entity will invest in a ready inventory of 450MW of wind power projects. This entity will, in turn, sell the rights to capacity from this wind farm to individual customers. At any point of time, the JV expects to maintain an inventory of 450 MW of wind projects such that customers can buy wind power projects without any waiting period. While this model will entail working capital involvement at the JV level, we see this concept as a value addition for Suzlon – 1) it will boost order flow for the company in the near term (with the JV being its captive customer); and 2) it will strengthen market share for Suzlon as customers will likely choose projects from this wind farm given its ready inventory vs competitors who might take 6-18 months to deliver projects.

In our view, this concept is more inclined to attract customers seeking to invest in wind farms from a tax incentive perspective or even private equity players who are not in the business of running power projects but want to benefit from the project IRRs.

Fig. 17: Proposed structure of Suzlon’s JV with DSA for 450 MW wind farm

Source: Company data

Nomura | Suzlon Energy 6 April 2015

15

Financials

Return to business-as-usual scenario to drive 27% revenue CAGR over FY15-20F

Suzlon has suffered from liquidity constraints over the past few years that have affected its execution and have dried up its order pipeline after 2012 when the government withdrew AD and GBI benefits from the wind sector. However, with both these concerns now behind the company, Suzlon looks well placed to return to business as usual.

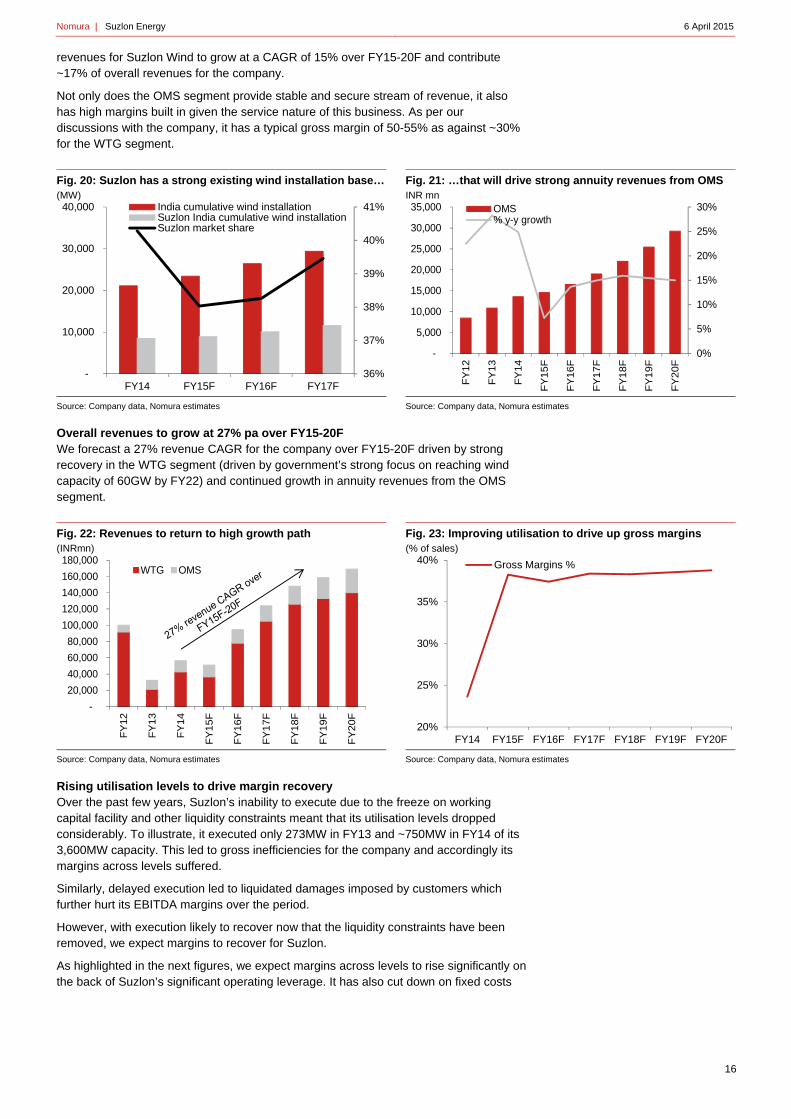

Market-share gain in WTG segment As we highlighted earlier, Suzlon has historically enjoyed a very strong market share in India (over 50%) due to its strong execution track record and complete EPC and OMS offering. We believe these advantages remain in Suzlon’s favour even now and this should help it regain market share in India. We estimate a 40% market share over FY16-20F. Also, the re-introduction of the AD and GBI benefits for wind installations along with the government’s focus on reaching 60GW cumulative capacity in India by 2022 are likely to drive sector growth.

This spells strong growth in WTG revenues for Suzlon over FY15-20F, on our estimates. We forecast a 30% CAGR in WTG revenues over this period. We note that realisations in the WTG segment have consistently been rising over the past few years mostly owing to improvement in technology. Even as capex cost/MW has increased, we note that efficiency of the wind mills has increased even more over the years leading to lower unit cost of electricity produced.

Fig. 18: Suzlon could regain 50% market share by FY17F… (MW)

Source: Nomura estimates

Fig. 19: … which will likely drive strong WTG revenue growth(INRmn)

Source: Company data, Nomura estimates

OMS segment: Strong base of high-margin annuity revenues With a cumulative base of 8.5GW of wind installation in India and almost 100% of this outsourcing the operation and maintenance services (OMS) to Suzlon, this segment has strong annuity revenue potential for Suzlon.

As per our estimates as well as discussions with the company, Suzlon charges roughly INR1mn/MW pa to customers for OMS. The typical contract duration is for five years, although it is most often renewed. Since most of the customers for SUEL are individuals or small IPPs with hardly any technical expertise, they are like to retain SUEL as their OMS partner for the life of the project.

Windmills normally have a life of 20-25 years after which repowering of the windmills is a typical option, which uses the same available infrastructure and land for installing a new windmill as per latest technology. Again Suzlon’s captive base of 8.5GW of installations in India makes this a lucrative long-term revenue option.

As of now, almost 38% of India’s current installed wind capacity is done by Suzlon and we forecast that to grow modestly over the next few years. Overall, we forecast OMS

0%

10%

20%

30%

40%

50%

60%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

FY15F FY16F FY17F

India overall installationSuzlon shareMarket share of Suzlon

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

-

20,000

40,000

60,000

80,000

100,000

120,000

FY

12

FY

13

FY

14

FY

15F

FY

16F

FY

17F

WTG% y-y growth

Nomura | Suzlon Energy 6 April 2015

16

revenues for Suzlon Wind to grow at a CAGR of 15% over FY15-20F and contribute ~17% of overall revenues for the company.

Not only does the OMS segment provide stable and secure stream of revenue, it also has high margins built in given the service nature of this business. As per our discussions with the company, it has a typical gross margin of 50-55% as against ~30% for the WTG segment.

Fig. 20: Suzlon has a strong existing wind installation base…(MW)

Source: Company data, Nomura estimates

Fig. 21: …that will drive strong annuity revenues from OMS INR mn

Source: Company data, Nomura estimates

Overall revenues to grow at 27% pa over FY15-20F We forecast a 27% revenue CAGR for the company over FY15-20F driven by strong recovery in the WTG segment (driven by government’s strong focus on reaching wind capacity of 60GW by FY22) and continued growth in annuity revenues from the OMS segment.

Fig. 22: Revenues to return to high growth path (INRmn)

Source: Company data, Nomura estimates

Fig. 23: Improving utilisation to drive up gross margins (% of sales)

Source: Company data, Nomura estimates

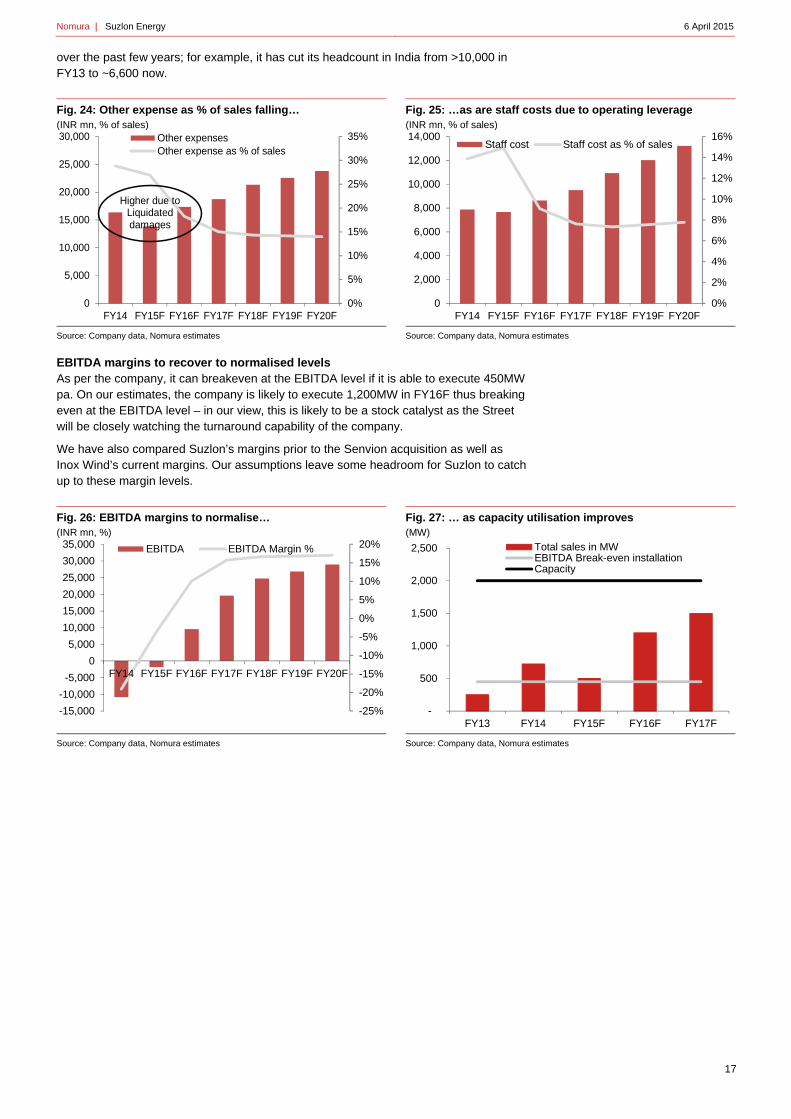

Rising utilisation levels to drive margin recovery Over the past few years, Suzlon’s inability to execute due to the freeze on working capital facility and other liquidity constraints meant that its utilisation levels dropped considerably. To illustrate, it executed only 273MW in FY13 and ~750MW in FY14 of its 3,600MW capacity. This led to gross inefficiencies for the company and accordingly its margins across levels suffered.

Similarly, delayed execution led to liquidated damages imposed by customers which further hurt its EBITDA margins over the period.

However, with execution likely to recover now that the liquidity constraints have been removed, we expect margins to recover for Suzlon.

As highlighted in the next figures, we expect margins across levels to rise significantly on the back of Suzlon’s significant operating leverage. It has also cut down on fixed costs

36%

37%

38%

39%

40%

41%

-

10,000

20,000

30,000

40,000

FY14 FY15F FY16F FY17F

India cumulative wind installationSuzlon India cumulative wind installationSuzlon market share

0%

5%

10%

15%

20%

25%

30%

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

FY

12

FY

13

FY

14

FY

15F

FY

16F

FY

17F

FY

18F

FY

19F

FY

20F

OMS% y-y growth

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

FY

12

FY

13

FY

14

FY

15F

FY

16F

FY

17F

FY

18F

FY

19F

FY

20F

WTG OMS

20%

25%

30%

35%

40%

FY14 FY15F FY16F FY17F FY18F FY19F FY20F

Gross Margins %

Nomura | Suzlon Energy 6 April 2015

17

over the past few years; for example, it has cut its headcount in India from >10,000 in FY13 to ~6,600 now.

Fig. 24: Other expense as % of sales falling… (INR mn, % of sales)

Source: Company data, Nomura estimates

Fig. 25: …as are staff costs due to operating leverage (INR mn, % of sales)

Source: Company data, Nomura estimates

EBITDA margins to recover to normalised levels As per the company, it can breakeven at the EBITDA level if it is able to execute 450MW pa. On our estimates, the company is likely to execute 1,200MW in FY16F thus breaking even at the EBITDA level – in our view, this is likely to be a stock catalyst as the Street will be closely watching the turnaround capability of the company.

We have also compared Suzlon’s margins prior to the Senvion acquisition as well as Inox Wind’s current margins. Our assumptions leave some headroom for Suzlon to catch up to these margin levels.

Fig. 26: EBITDA margins to normalise… (INR mn, %)

Source: Company data, Nomura estimates

Fig. 27: … as capacity utilisation improves (MW)

Source: Company data, Nomura estimates

0%

5%

10%

15%

20%

25%

30%

35%

0

5,000

10,000

15,000

20,000

25,000

30,000

FY14 FY15F FY16F FY17F FY18F FY19F FY20F

Other expensesOther expense as % of sales

Higher due to Liquidated damages

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY14 FY15F FY16F FY17F FY18F FY19F FY20F

Staff cost Staff cost as % of sales

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

FY14 FY15F FY16F FY17F FY18F FY19F FY20F

EBITDA EBITDA Margin %

-

500

1,000

1,500

2,000

2,500

FY13 FY14 FY15F FY16F FY17F

Total sales in MWEBITDA Break-even installationCapacity

Nomura | Suzlon Energy 6 April 2015

18

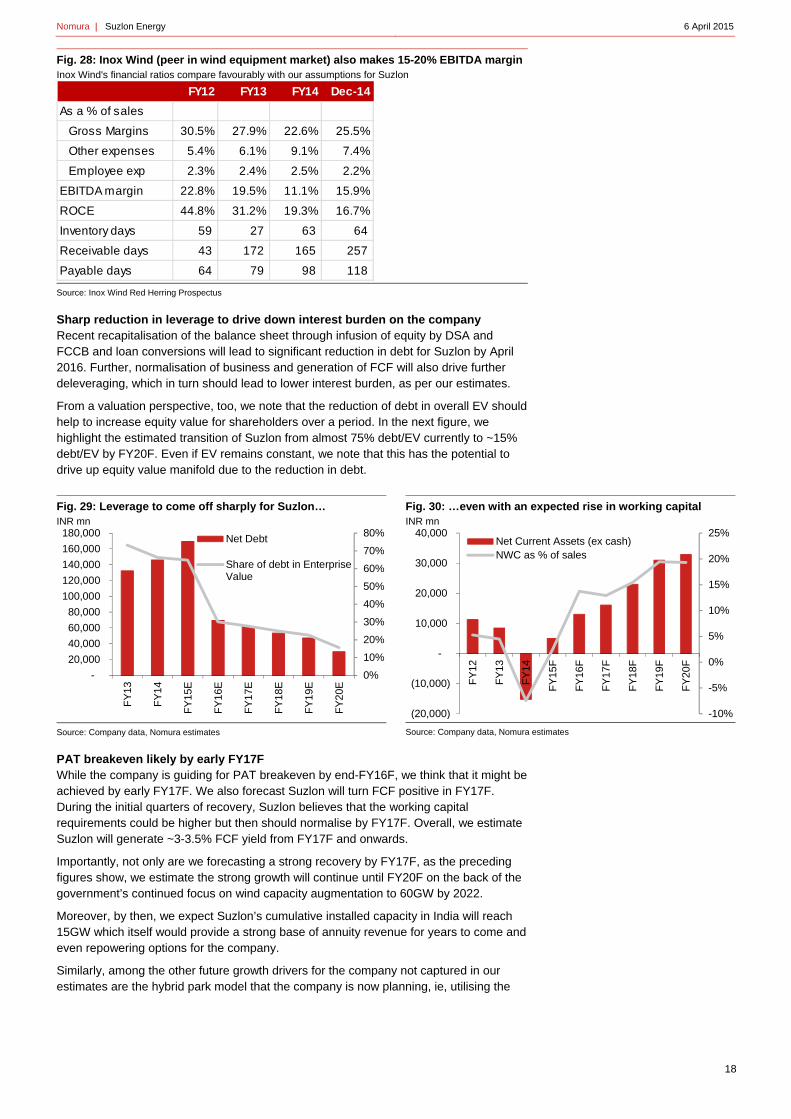

Fig. 28: Inox Wind (peer in wind equipment market) also makes 15-20% EBITDA margin Inox Wind's financial ratios compare favourably with our assumptions for Suzlon

Source: Inox Wind Red Herring Prospectus

Sharp reduction in leverage to drive down interest burden on the company Recent recapitalisation of the balance sheet through infusion of equity by DSA and FCCB and loan conversions will lead to significant reduction in debt for Suzlon by April 2016. Further, normalisation of business and generation of FCF will also drive further deleveraging, which in turn should lead to lower interest burden, as per our estimates.

From a valuation perspective, too, we note that the reduction of debt in overall EV should help to increase equity value for shareholders over a period. In the next figure, we highlight the estimated transition of Suzlon from almost 75% debt/EV currently to ~15% debt/EV by FY20F. Even if EV remains constant, we note that this has the potential to drive up equity value manifold due to the reduction in debt.

Fig. 29: Leverage to come off sharply for Suzlon… INR mn

Source: Company data, Nomura estimates

Fig. 30: …even with an expected rise in working capital INR mn

Source: Company data, Nomura estimates

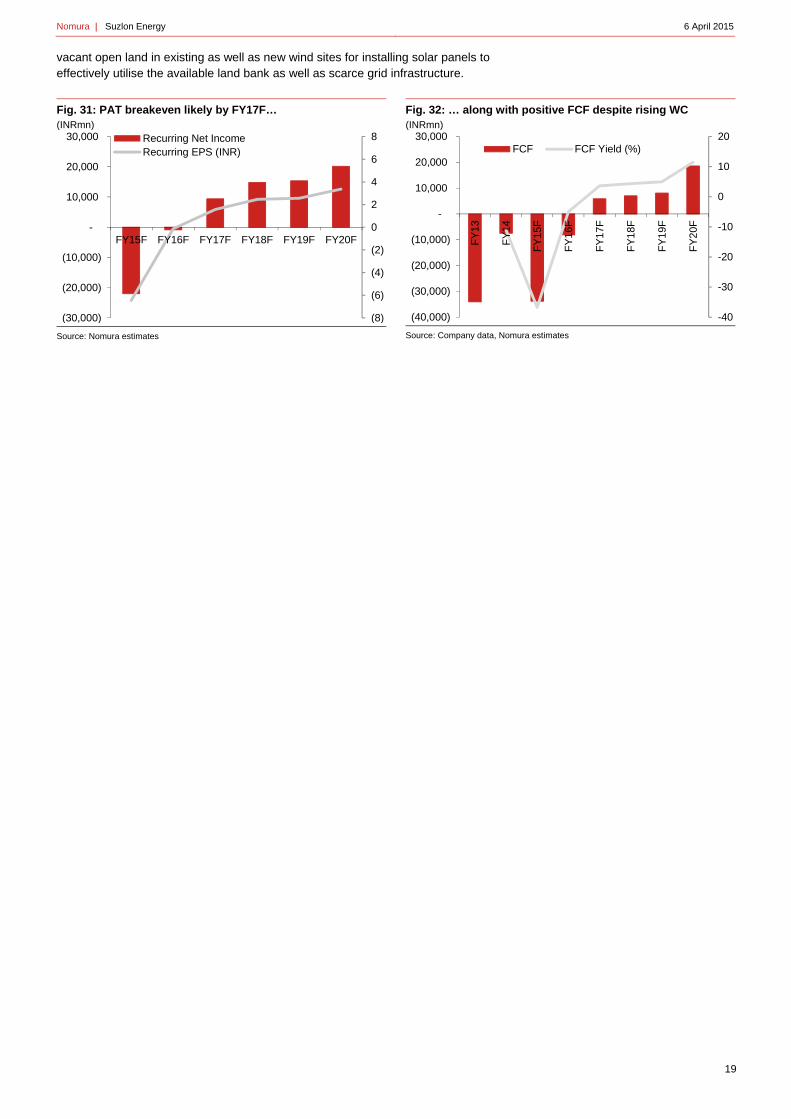

PAT breakeven likely by early FY17F While the company is guiding for PAT breakeven by end-FY16F, we think that it might be achieved by early FY17F. We also forecast Suzlon will turn FCF positive in FY17F. During the initial quarters of recovery, Suzlon believes that the working capital requirements could be higher but then should normalise by FY17F. Overall, we estimate Suzlon will generate ~3-3.5% FCF yield from FY17F and onwards.

Importantly, not only are we forecasting a strong recovery by FY17F, as the preceding figures show, we estimate the strong growth will continue until FY20F on the back of the government’s continued focus on wind capacity augmentation to 60GW by 2022.

Moreover, by then, we expect Suzlon’s cumulative installed capacity in India will reach 15GW which itself would provide a strong base of annuity revenue for years to come and even repowering options for the company.

Similarly, among the other future growth drivers for the company not captured in our estimates are the hybrid park model that the company is now planning, ie, utilising the

FY12 FY13 FY14 Dec-14

As a % of sales

Gross Margins 30.5% 27.9% 22.6% 25.5%

Other expenses 5.4% 6.1% 9.1% 7.4%

Employee exp 2.3% 2.4% 2.5% 2.2%

EBITDA margin 22.8% 19.5% 11.1% 15.9%

ROCE 44.8% 31.2% 19.3% 16.7%

Inventory days 59 27 63 64

Receivable days 43 172 165 257

Payable days 64 79 98 118

0%

10%

20%

30%

40%

50%

60%

70%

80%

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

FY

13

FY

14

FY

15E

FY

16E

FY

17E

FY

18E

FY

19E

FY

20E

Net Debt

Share of debt in EnterpriseValue

-10%

-5%

0%

5%

10%

15%

20%

25%

(20,000)

(10,000)

-

10,000

20,000

30,000

40,000

FY

12

FY

13

FY

14

FY

15F

FY

16F

FY

17F

FY

18F

FY

19F

FY

20F

Net Current Assets (ex cash)NWC as % of sales

Nomura | Suzlon Energy 6 April 2015

19

vacant open land in existing as well as new wind sites for installing solar panels to effectively utilise the available land bank as well as scarce grid infrastructure.

Fig. 31: PAT breakeven likely by FY17F… (INRmn)

Source: Nomura estimates

Fig. 32: … along with positive FCF despite rising WC (INRmn)

Source: Company data, Nomura estimates

(8)

(6)

(4)

(2)

0

2

4

6

8

(30,000)

(20,000)

(10,000)

-

10,000

20,000

30,000

FY15F FY16F FY17F FY18F FY19F FY20F

Recurring Net IncomeRecurring EPS (INR)

-40

-30

-20

-10

0

10

20

(40,000)

(30,000)

(20,000)

(10,000)

-

10,000

20,000

30,000

FY

13

FY

14

FY

15F

FY

16F

FY

17F

FY

18F

FY

19F

FY

20F

FCF FCF Yield (%)

Nomura | Suzlon Energy 6 April 2015

20

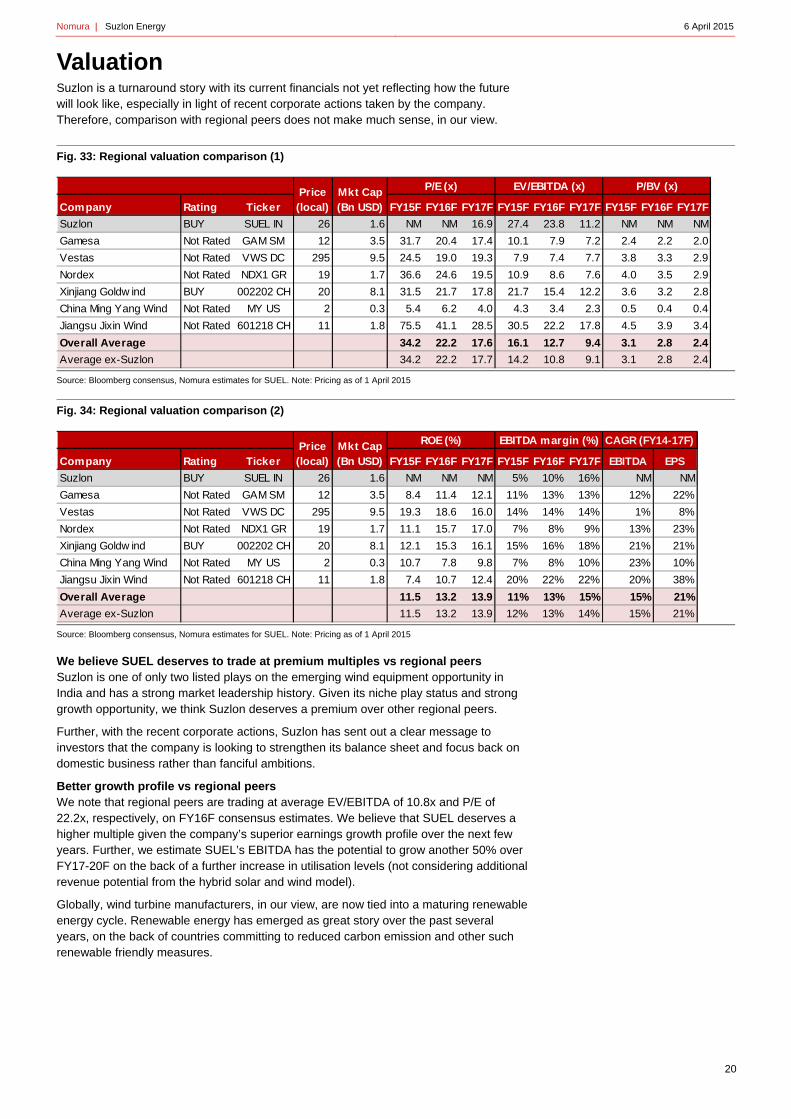

Valuation Suzlon is a turnaround story with its current financials not yet reflecting how the future will look like, especially in light of recent corporate actions taken by the company. Therefore, comparison with regional peers does not make much sense, in our view.

Fig. 33: Regional valuation comparison (1)

Source: Bloomberg consensus, Nomura estimates for SUEL. Note: Pricing as of 1 April 2015

Fig. 34: Regional valuation comparison (2)

Source: Bloomberg consensus, Nomura estimates for SUEL. Note: Pricing as of 1 April 2015

We believe SUEL deserves to trade at premium multiples vs regional peers Suzlon is one of only two listed plays on the emerging wind equipment opportunity in India and has a strong market leadership history. Given its niche play status and strong growth opportunity, we think Suzlon deserves a premium over other regional peers.

Further, with the recent corporate actions, Suzlon has sent out a clear message to investors that the company is looking to strengthen its balance sheet and focus back on domestic business rather than fanciful ambitions.

Better growth profile vs regional peers We note that regional peers are trading at average EV/EBITDA of 10.8x and P/E of 22.2x, respectively, on FY16F consensus estimates. We believe that SUEL deserves a higher multiple given the company’s superior earnings growth profile over the next few years. Further, we estimate SUEL’s EBITDA has the potential to grow another 50% over FY17-20F on the back of a further increase in utilisation levels (not considering additional revenue potential from the hybrid solar and wind model).

Globally, wind turbine manufacturers, in our view, are now tied into a maturing renewable energy cycle. Renewable energy has emerged as great story over the past several years, on the back of countries committing to reduced carbon emission and other such renewable friendly measures.

Company Rating Ticker FY15F FY16F FY17F FY15F FY16F FY17F FY15F FY16F FY17F

Suzlon BUY SUEL IN 26 1.6 NM NM 16.9 27.4 23.8 11.2 NM NM NM

Gamesa Not Rated GAM SM 12 3.5 31.7 20.4 17.4 10.1 7.9 7.2 2.4 2.2 2.0

Vestas Not Rated VWS DC 295 9.5 24.5 19.0 19.3 7.9 7.4 7.7 3.8 3.3 2.9

Nordex Not Rated NDX1 GR 19 1.7 36.6 24.6 19.5 10.9 8.6 7.6 4.0 3.5 2.9

Xinjiang Goldw ind BUY 002202 CH 20 8.1 31.5 21.7 17.8 21.7 15.4 12.2 3.6 3.2 2.8

China Ming Yang Wind Not Rated MY US 2 0.3 5.4 6.2 4.0 4.3 3.4 2.3 0.5 0.4 0.4

Jiangsu Jixin Wind Not Rated 601218 CH 11 1.8 75.5 41.1 28.5 30.5 22.2 17.8 4.5 3.9 3.4

Overall Average 34.2 22.2 17.6 16.1 12.7 9.4 3.1 2.8 2.4

Average ex-Suzlon 34.2 22.2 17.7 14.2 10.8 9.1 3.1 2.8 2.4

Mkt Cap (Bn USD)

P/E (x) EV/EBITDA (x) P/BV (x)Price(local)

Company Rating Ticker FY15F FY16F FY17F FY15F FY16F FY17F EBITDA EPS

Suzlon BUY SUEL IN 26 1.6 NM NM NM 5% 10% 16% NM NM

Gamesa Not Rated GAM SM 12 3.5 8.4 11.4 12.1 11% 13% 13% 12% 22%

Vestas Not Rated VWS DC 295 9.5 19.3 18.6 16.0 14% 14% 14% 1% 8%

Nordex Not Rated NDX1 GR 19 1.7 11.1 15.7 17.0 7% 8% 9% 13% 23%

Xinjiang Goldw ind BUY 002202 CH 20 8.1 12.1 15.3 16.1 15% 16% 18% 21% 21%

China Ming Yang Wind Not Rated MY US 2 0.3 10.7 7.8 9.8 7% 8% 10% 23% 10%

Jiangsu Jixin Wind Not Rated 601218 CH 11 1.8 7.4 10.7 12.4 20% 22% 22% 20% 38%

Overall Average 11.5 13.2 13.9 11% 13% 15% 15% 21%

Average ex-Suzlon 11.5 13.2 13.9 12% 13% 14% 15% 21%

Mkt Cap (Bn USD)

ROE (%) EBITDA margin (%)Price(local)

CAGR (FY14-17F)

Nomura | Suzlon Energy 6 April 2015

21

However, all of this came to an abrupt halt with the global financial crisis, when the governments started ignoring the high-cost renewable commitments. In fact, capex, overall, went downhill and remains soft.

In the meantime, emerging markets have continued to grow on the back of their rising demand for energy and shortage of fossil fuels. We believe India therefore fits in perfectly well in this story as the next driver of renewable energy, though supported by government incentives. As such, we think India offers a much better growth profile for companies as compared to global economies particularly Europe, which in our view, has already matured in terms of renewable sources of energy.

Therefore, we think SUEL deserves to trade at a higher premium compared to global players where the growth outlook is weaker as compared to a pure play India story in SUEL.

O&M revenues provide solid financial support As we highlighted earlier in this report, Suzlon’s O&M revenues are set to grow and provide strong financial support to the company. Notably, even during the past few years, Suzlon continued to benefit from its strong installed base of ~8.5GW across India and the associated O&M revenues from the same. Not only is this segment a good annuity revenue source for the company, but it will also keep growing as the installed wind base for SUEL ramps up further. O&M is also a higher-profit business and one that provides greater visibility and stability in revenue/profits.

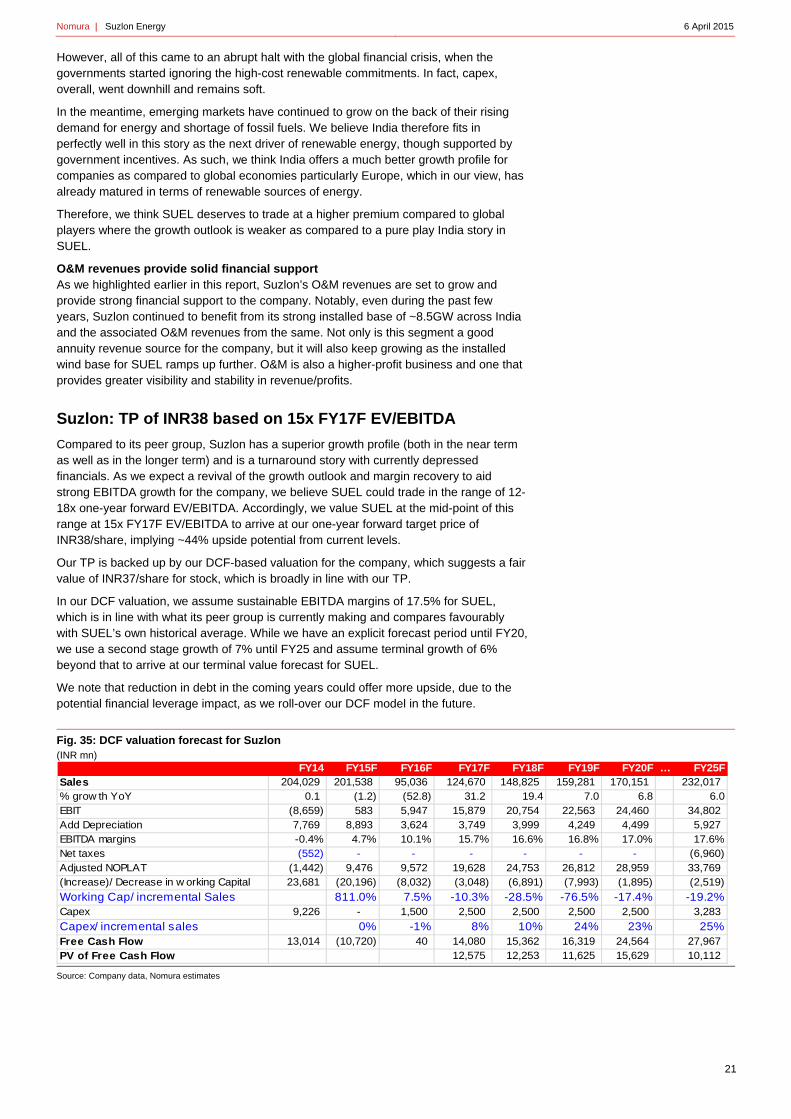

Suzlon: TP of INR38 based on 15x FY17F EV/EBITDA

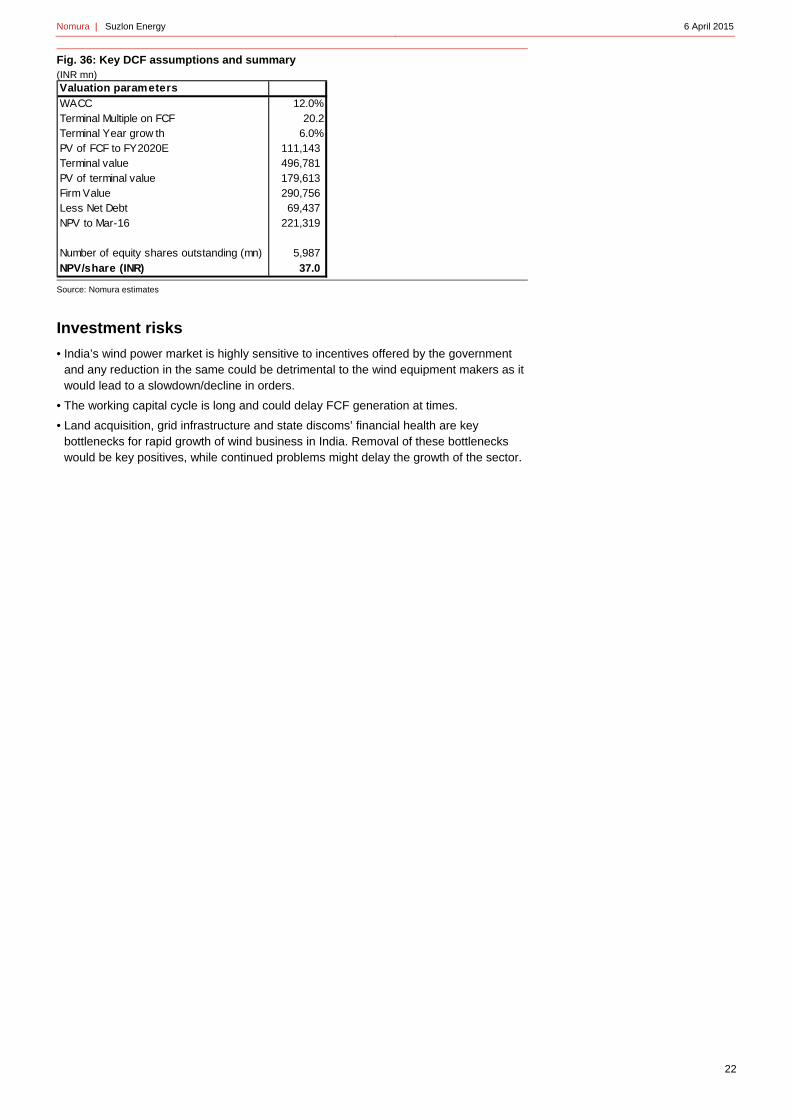

Compared to its peer group, Suzlon has a superior growth profile (both in the near term as well as in the longer term) and is a turnaround story with currently depressed financials. As we expect a revival of the growth outlook and margin recovery to aid strong EBITDA growth for the company, we believe SUEL could trade in the range of 12-18x one-year forward EV/EBITDA. Accordingly, we value SUEL at the mid-point of this range at 15x FY17F EV/EBITDA to arrive at our one-year forward target price of INR38/share, implying ~44% upside potential from current levels.

Our TP is backed up by our DCF-based valuation for the company, which suggests a fair value of INR37/share for stock, which is broadly in line with our TP.

In our DCF valuation, we assume sustainable EBITDA margins of 17.5% for SUEL, which is in line with what its peer group is currently making and compares favourably with SUEL’s own historical average. While we have an explicit forecast period until FY20, we use a second stage growth of 7% until FY25 and assume terminal growth of 6% beyond that to arrive at our terminal value forecast for SUEL.

We note that reduction in debt in the coming years could offer more upside, due to the potential financial leverage impact, as we roll-over our DCF model in the future.

Fig. 35: DCF valuation forecast for Suzlon (INR mn)

Source: Company data, Nomura estimates

FY14 FY15F FY16F FY17F FY18F FY19F FY20F … FY25FSales 204,029 201,538 95,036 124,670 148,825 159,281 170,151 232,017 % grow th YoY 0.1 (1.2) (52.8) 31.2 19.4 7.0 6.8 6.0EBIT (8,659) 583 5,947 15,879 20,754 22,563 24,460 34,802 Add Depreciation 7,769 8,893 3,624 3,749 3,999 4,249 4,499 5,927 EBITDA margins -0.4% 4.7% 10.1% 15.7% 16.6% 16.8% 17.0% 17.6%Net taxes (552) - - - - - - (6,960) Adjusted NOPLAT (1,442) 9,476 9,572 19,628 24,753 26,812 28,959 33,769 (Increase)/ Decrease in w orking Capital 23,681 (20,196) (8,032) (3,048) (6,891) (7,993) (1,895) (2,519)

Working Cap/ incremental Sales 811.0% 7.5% -10.3% -28.5% -76.5% -17.4% -19.2%Capex 9,226 - 1,500 2,500 2,500 2,500 2,500 3,283

Capex/ incremental sales 0% -1% 8% 10% 24% 23% 25%Free Cash Flow 13,014 (10,720) 40 14,080 15,362 16,319 24,564 27,967 PV of Free Cash Flow 12,575 12,253 11,625 15,629 10,112

Nomura | Suzlon Energy 6 April 2015

22

Fig. 36: Key DCF assumptions and summary (INR mn)

Source: Nomura estimates

Investment risks

• India’s wind power market is highly sensitive to incentives offered by the government and any reduction in the same could be detrimental to the wind equipment makers as it would lead to a slowdown/decline in orders.

• The working capital cycle is long and could delay FCF generation at times.

• Land acquisition, grid infrastructure and state discoms’ financial health are key bottlenecks for rapid growth of wind business in India. Removal of these bottlenecks would be key positives, while continued problems might delay the growth of the sector.

Valuation parameters

WACC 12.0%Terminal Multiple on FCF 20.2Terminal Year grow th 6.0%PV of FCF to FY2020E 111,143 Terminal value 496,781 PV of terminal value 179,613 Firm Value 290,756 Less Net Debt 69,437 NPV to Mar-16 221,319

Number of equity shares outstanding (mn) 5,987 NPV/share (INR) 37.0

Nomura | Suzlon Energy 6 April 2015

23

Annexure

Comparison with China wind equipment sector

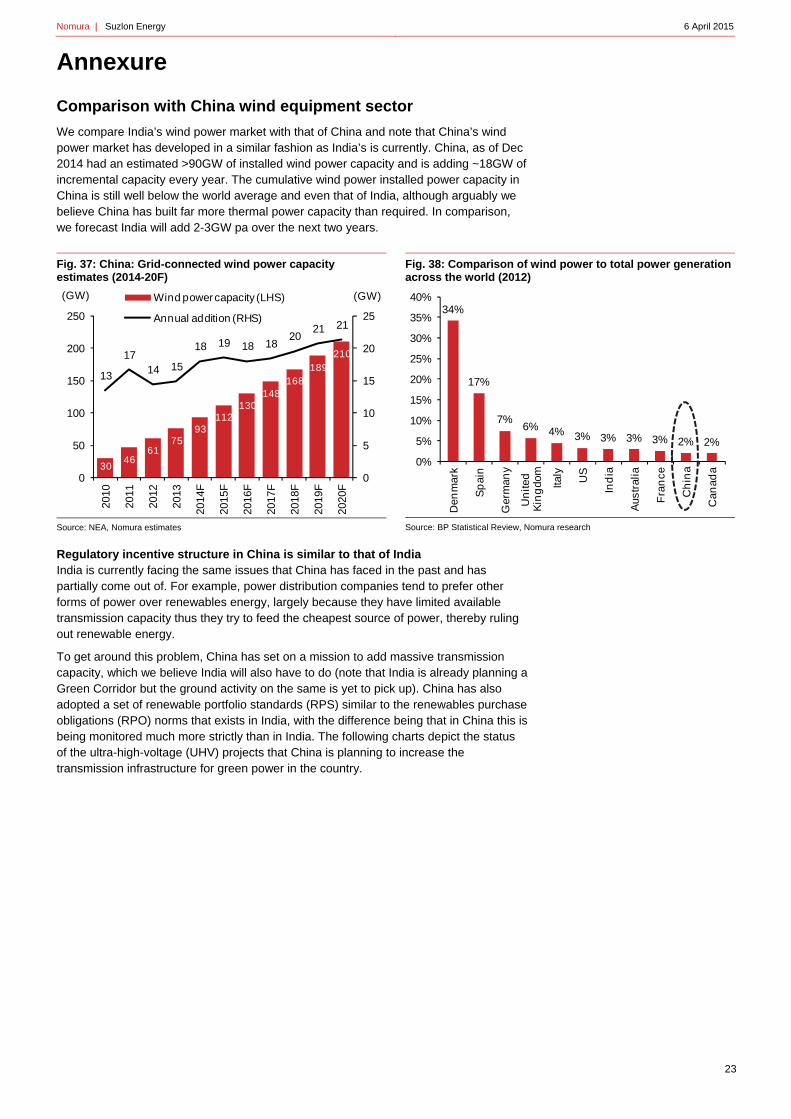

We compare India’s wind power market with that of China and note that China’s wind power market has developed in a similar fashion as India’s is currently. China, as of Dec 2014 had an estimated >90GW of installed wind power capacity and is adding ~18GW of incremental capacity every year. The cumulative wind power installed power capacity in China is still well below the world average and even that of India, although arguably we believe China has built far more thermal power capacity than required. In comparison, we forecast India will add 2-3GW pa over the next two years.

Fig. 37: China: Grid-connected wind power capacity estimates (2014-20F)

Source: NEA, Nomura estimates

Fig. 38: Comparison of wind power to total power generation across the world (2012)

Source: BP Statistical Review, Nomura research

Regulatory incentive structure in China is similar to that of India India is currently facing the same issues that China has faced in the past and has partially come out of. For example, power distribution companies tend to prefer other forms of power over renewables energy, largely because they have limited available transmission capacity thus they try to feed the cheapest source of power, thereby ruling out renewable energy.

To get around this problem, China has set on a mission to add massive transmission capacity, which we believe India will also have to do (note that India is already planning a Green Corridor but the ground activity on the same is yet to pick up). China has also adopted a set of renewable portfolio standards (RPS) similar to the renewables purchase obligations (RPO) norms that exists in India, with the difference being that in China this is being monitored much more strictly than in India. The following charts depict the status of the ultra-high-voltage (UHV) projects that China is planning to increase the transmission infrastructure for green power in the country.

30 46

61 75

93 112

130 148

168 189

210

13

17 14 15

18 19 18 18 20

21 21

0

5

10

15

20

25

0

50

100

150

200

250

2010

2011

2012

2013

2014

F

2015

F

2016

F

2017

F

2018

F

2019

F

2020

F

(GW)(GW) Wind power capacity (LHS)

Annual addition (RHS)34%

17%

7%6% 4% 3% 3% 3% 3% 2% 2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Den

mar

k

Sp

ain

Ger

man

y

Un

ited

K

ing

dom

Italy

US

Ind

ia

Aus

tral

ia

Fra

nce

Ch

ina

Can

ada

Nomura | Suzlon Energy 6 April 2015

24

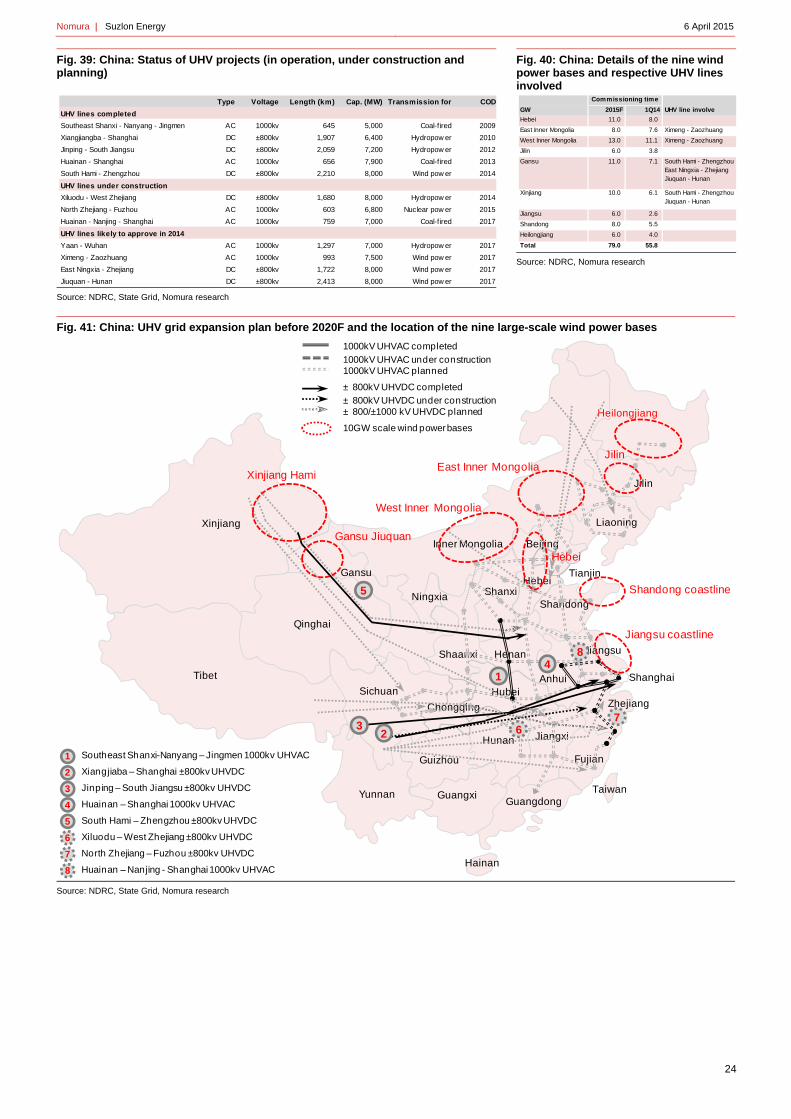

Fig. 39: China: Status of UHV projects (in operation, under construction and planning)

Source: NDRC, State Grid, Nomura research

Fig. 40: China: Details of the nine wind power bases and respective UHV lines involved

Source: NDRC, Nomura research

Fig. 41: China: UHV grid expansion plan before 2020F and the location of the nine large-scale wind power bases

Source: NDRC, State Grid, Nomura research

Type Voltage Length (km) Cap. (MW) Transmission for COD

UHV lines completed

Southeast Shanxi - Nanyang - Jingmen AC 1000kv 645 5,000 Coal-f ired 2009

Xiangjiangba - Shanghai DC ±800kv 1,907 6,400 Hydropow er 2010

Jinping - South Jiangsu DC ±800kv 2,059 7,200 Hydropow er 2012

Huainan - Shanghai AC 1000kv 656 7,900 Coal-f ired 2013

South Hami - Zhengzhou DC ±800kv 2,210 8,000 Wind pow er 2014

UHV lines under construction

Xiluodu - West Zhejiang DC ±800kv 1,680 8,000 Hydropow er 2014

North Zhejiang - Fuzhou AC 1000kv 603 6,800 Nuclear pow er 2015

Huainan - Nanjing - Shanghai AC 1000kv 759 7,000 Coal-f ired 2017

UHV lines likely to approve in 2014

Yaan - Wuhan AC 1000kv 1,297 7,000 Hydropow er 2017

Ximeng - Zaozhuang AC 1000kv 993 7,500 Wind pow er 2017

East Ningxia - Zhejiang DC ±800kv 1,722 8,000 Wind pow er 2017

Jiuquan - Hunan DC ±800kv 2,413 8,000 Wind pow er 2017

GW 2015F 1Q14 UHV line involve

Hebei 11.0 8.0

East Inner Mongolia 8.0 7.6 Ximeng - Zaozhuang

West Inner Mongolia 13.0 11.1 Ximeng - Zaozhuang

Jilin 6.0 3.8

Gansu 11.0 7.1 South Hami - ZhengzhouEast Ningxia - ZhejiangJiuquan - Hunan

Xinjiang 10.0 6.1 South Hami - ZhengzhouJiuquan - Hunan

Jiangsu 6.0 2.6

Shandong 8.0 5.5

Heilongjiang 6.0 4.0

Total 79.0 55.8

Commissioning time

Hainan

Inner Mongolia

Jilin

Beijing

HebeiTianjin

Jiangsu

Anhui Shanghai

Zhejiang

Henan

Hubei

Shaanxi

Ningxia

Qinghai

Xinjiang

Tibet

Sichuan

Yunnan Guangxi

Guizhou Fujian

Hunan Jiangxi

ShanxiShandong

Taiwan

Heilongjiang

Liaoning

Guangdong

Chongqing

Gansu

1000kV UHVAC planned

± 800/±1000 kV UHVDC planned

± 800kV UHVDC completed

1000kV UHVAC completed

± 800kV UHVDC under construction

1000kV UHVAC under construction

10GW scale wind power bases

23

1

5

4

7

6

1

2

3

4

5

7

Southeast Shanxi-Nanyang – Jingmen 1000kv UHVAC

Xiangjiaba – Shanghai ±800kv UHVDC

Jinping – South Jiangsu ±800kv UHVDC

South Hami – Zhengzhou ±800kv UHVDC

Huainan – Shanghai 1000kv UHVAC

6

Xiluodu – West Zhejiang ±800kv UHVDC

North Zhejiang – Fuzhou ±800kv UHVDC

Xinjiang Hami

Gansu Jiuquan

West Inner Mongolia

East Inner MongoliaJilin

Hebei

Shandong coastline

Jiangsu coastline

Huainan – Nanjing - Shanghai 1000kv UHVAC8

8

Nomura | Suzlon Energy 6 April 2015

25

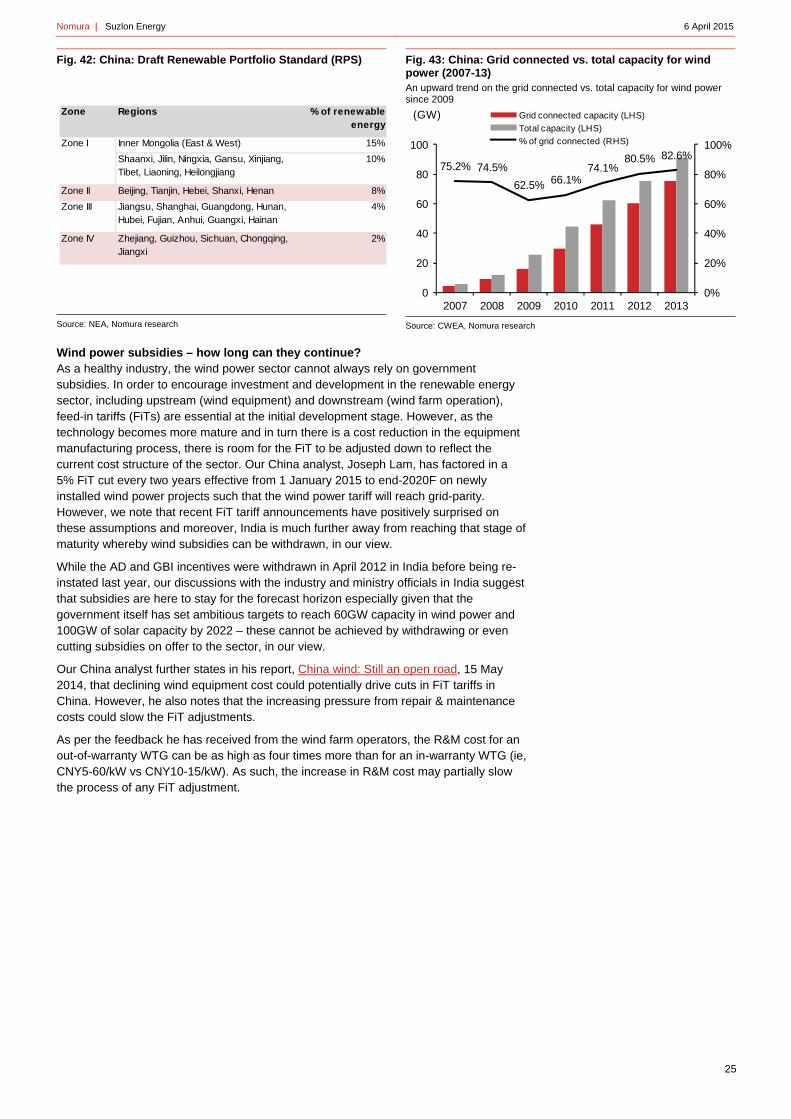

Fig. 42: China: Draft Renewable Portfolio Standard (RPS)

Source: NEA, Nomura research

Fig. 43: China: Grid connected vs. total capacity for wind power (2007-13) An upward trend on the grid connected vs. total capacity for wind power since 2009

Source: CWEA, Nomura research

Wind power subsidies – how long can they continue? As a healthy industry, the wind power sector cannot always rely on government subsidies. In order to encourage investment and development in the renewable energy sector, including upstream (wind equipment) and downstream (wind farm operation), feed-in tariffs (FiTs) are essential at the initial development stage. However, as the technology becomes more mature and in turn there is a cost reduction in the equipment manufacturing process, there is room for the FiT to be adjusted down to reflect the current cost structure of the sector. Our China analyst, Joseph Lam, has factored in a 5% FiT cut every two years effective from 1 January 2015 to end-2020F on newly installed wind power projects such that the wind power tariff will reach grid-parity. However, we note that recent FiT tariff announcements have positively surprised on these assumptions and moreover, India is much further away from reaching that stage of maturity whereby wind subsidies can be withdrawn, in our view.

While the AD and GBI incentives were withdrawn in April 2012 in India before being re-instated last year, our discussions with the industry and ministry officials in India suggest that subsidies are here to stay for the forecast horizon especially given that the government itself has set ambitious targets to reach 60GW capacity in wind power and 100GW of solar capacity by 2022 – these cannot be achieved by withdrawing or even cutting subsidies on offer to the sector, in our view.

Our China analyst further states in his report, China wind: Still an open road, 15 May 2014, that declining wind equipment cost could potentially drive cuts in FiT tariffs in China. However, he also notes that the increasing pressure from repair & maintenance costs could slow the FiT adjustments.

As per the feedback he has received from the wind farm operators, the R&M cost for an out-of-warranty WTG can be as high as four times more than for an in-warranty WTG (ie, CNY5-60/kW vs CNY10-15/kW). As such, the increase in R&M cost may partially slow the process of any FiT adjustment.

Zone Regions % of renewable energy

Zone I Inner Mongolia (East & West) 15%

Shaanxi, Jilin, Ningxia, Gansu, Xinjiang, Tibet, Liaoning, Heilongjiang

10%

Zone II Beijing, Tianjin, Hebei, Shanxi, Henan 8%

Zone III Jiangsu, Shanghai, Guangdong, Hunan, Hubei, Fujian, Anhui, Guangxi, Hainan

4%

Zone IV Zhejiang, Guizhou, Sichuan, Chongqing, Jiangxi

2%

75.2% 74.5%

62.5% 66.1%74.1%

80.5% 82.6%

0%

20%

40%

60%

80%

100%

0

20

40

60

80

100

2007 2008 2009 2010 2011 2012 2013

(GW) Grid connected capacity (LHS)

Total capacity (LHS)

% of grid connected (RHS)

Nomura | Suzlon Energy 6 April 2015

26

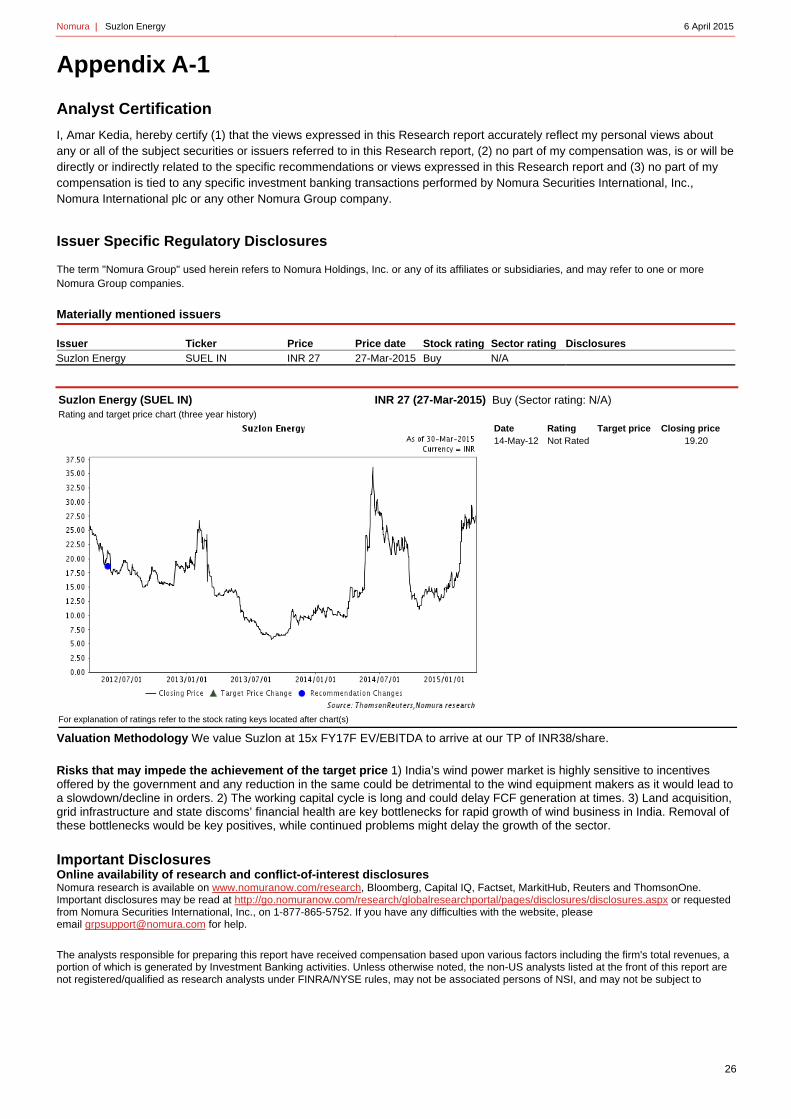

Appendix A-1

Analyst Certification

I, Amar Kedia, hereby certify (1) that the views expressed in this Research report accurately reflect my personal views about any or all of the subject securities or issuers referred to in this Research report, (2) no part of my compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this Research report and (3) no part of my compensation is tied to any specific investment banking transactions performed by Nomura Securities International, Inc., Nomura International plc or any other Nomura Group company.

Issuer Specific Regulatory Disclosures The term "Nomura Group" used herein refers to Nomura Holdings, Inc. or any of its affiliates or subsidiaries, and may refer to one or more Nomura Group companies.

Materially mentioned issuers Issuer Ticker Price Price date Stock rating Sector rating Disclosures Suzlon Energy SUEL IN INR 27 27-Mar-2015 Buy N/A

Suzlon Energy (SUEL IN) INR 27 (27-Mar-2015) Rating and target price chart (three year history)

Buy (Sector rating: N/A)

Date Rating Target price Closing price 14-May-12 Not Rated 19.20

For explanation of ratings refer to the stock rating keys located after chart(s)

Valuation Methodology We value Suzlon at 15x FY17F EV/EBITDA to arrive at our TP of INR38/share. Risks that may impede the achievement of the target price 1) India’s wind power market is highly sensitive to incentives offered by the government and any reduction in the same could be detrimental to the wind equipment makers as it would lead to a slowdown/decline in orders. 2) The working capital cycle is long and could delay FCF generation at times. 3) Land acquisition, grid infrastructure and state discoms’ financial health are key bottlenecks for rapid growth of wind business in India. Removal of these bottlenecks would be key positives, while continued problems might delay the growth of the sector.