bausparen an international success story

DESCRIPTION

Bauspar productsTRANSCRIPT

BAUSPARENAn International Success Story

Beneficial for Both People and the Economy

The safe way to finance a home

Contents

03 Foreword

04 Bausparen (Contractual Savings for Housing) – Appealingly Simple and SecureA guaranteed interest rate provides reliability

06 Positive Effects on the EconomyBausparen benefits the state and the society

08 Partnering with the Market Leader to Achieve SuccessCompetitive advantages for banks

10 A Schwäbisch Hall Export That’s a WinnerBausparkasse Schwäbisch Hall is a pioneer abroad

12 Success on an International ScaleBausparkasse Schwäbisch Hall’s affiliated companies

19 GlossaryThe most important terms relating to Bausparen

20 ContactReach out to us

2 Contents

3Foreword

In Germany, Bausparen is a tried and true model forsuccess with a long history. After World War II, thismethod of saving contributed considerably to the reconstruction of our country. Bausparkasse Schwä-bisch Hall alone has contributed to financing the construction, purchase, or modernization work onroughly 8.4 million apartments and houses since1948. Saving money through a Bausparen savingsplan helps people to create – and keep – a home where the heart is.

This is why we believe that this product is an attrac -tive and secure financing instrument for many coun-tries. On the following pages we present how Bauspa-ren works and what advantages it has to offer for thestate and the economy.

We look forward to talking to you about the great opportunity this represents.

Reinhard KleinChairman of the Management BoardBausparkasse Schwäbisch Hall AG

Dear Reader,All over the world, people dream of owning their ownhome. Many go to great lengths to make this deeplyheld dream come true. They save, they borrow, theytake construction and modernization work into theirown hands. For most of them, buying real estate is thebiggest investment of their lives. To successfully tack-le this challenge they need inexpensive and low-riskfinancing instruments.

This is exactly what Bausparen offers. Little by little,customers build up capital by making regular depositsinto their savings account – which means they don’tneed to borrow as much later. When financing theirnew homes, these savers are able to take advantage oflow, fixed interest rates over the entire term of theirloans. This not only makes the individual home financ-ing reliable, it also provides stability for the entireeconomy.

The institutions that offer these savings plans – Bau-sparkassen (Contractual Savings for Housing compa-nies) in Germany – are subject to clear requirementsspecified by the law and are monitored by banking regulators. The financial crisis showed just how impor-tant it is to have savings that are protected: The Bau-sparkassen came through the crisis unscathed, andnone of the savers lost any money – not one cent.

Saving money through Bausparen helps people all overthe world to create – and keep –a home where the heart is.

4 Bausparen – Appealingly Simple and Secure

Bausparen – AppealinglySimple and Secure

phases, the savings phase and the loan phase. Thesystem is based on a mathematical formula that ensu-res that all customers are treated equally, factoring inthe period of time over which the individual customerwill be saving money as well as the amount.

A guaranteed interestrate provides reliability

With Bausparen, the interest rate on both the savingsand on the loan is determined by the time the con-tract is signed, which means that customers can be

Bausparen (Contractual Savings for Housing) is asimple, secure, and sustainable financial product thatis suitable for anyone who wants to build, buy, or mo-dernize a property. The basic concept is seductivelyappealing: During the first phase, the customer makesregular deposits of a fixed amount into the savings account, up to a maximum of half of the agreed totalfunds to be disbursed, building up the balance over time. The remaining amount is later disbursed to thecustomer by the savings institution as a loan, and thecustomer repays this loan in monthly installments.Simply put, the Bausparen process is divided into two

5Bausparen – Appealingly Simple and Secure

How it works

The closed system makes this savings method a sustainable financing instrument that is able to withstand crises.

instructions concerning the ways the funds are per-mitted to be used. Customers are allowed to use theirfunds for almost anything related to building, buying,or modernizing residential real estate. Many savers invest in renovations that improve energy usage or inremodeling that helps make their property more suit-able for modern life.

All of the requirements imposed by law protect thesavers as a community, known as the “home saverscollective”, since the primary goal of this special sa-vings system is to create maximum security for custo-mers’ deposits. All of the countries that offer Bauspa-ren as a financing instrument profit from its excellentperformance and security during times of crisis. InGermany, Bausparen has proven successful for over90 years.

absolutely certain of the interest throughout the enti-re term of the contract. The loans that are issued arefunded from customers’ deposits, meaning that all ofthe money saved remains in a closed system. Ultima-tely, this renders institutions offering contractual sa-vings for housing plans (Bausparkassen) essentiallyindependent from the capital market.

The law provides maximum security

The backbone of this system is legislation. In Germa-ny, customers are protected by the Bausparkassenge-setz – the Building and Loan Associations Act – whichis the law that regulates contractual saving institu -tions. This law stipulates exactly how such institutionscan invest money, as well as how risks are required tobe limited and monitored. The law also provides clear

Saver

Savings balance on theBauspar account+ Bauspar Loan+ Interest+ Government subsidy

Government subsidy

Saver repays the loan

Savings deposits onthe Bauspar account

6 Positive Effects on the Economy

Positive Effectson the Economy

greater variety of financing products means morecompetition in the construction financing sector andleads to greater stability in the financial sector.Highly effective products increase the ability to with-stand financial crises, which in turn boosts people’strust in their domestic financial system. Bausparenhas other effects as well:

Positive influence on saving habits:The systematic nature of Bausparen encouragespeople to save.

The distinctive features of Bausparen have a benefi-cial effect on a country’s entire economy. The bene-fits are far-reaching, and although they primarily affect private households, they also have a positiveimpact on the real estate sector and the financial system.

Contractual saving benefits the state and the society

The Bausparen savings system is another importanttool in a country’s arsenal of financing products. A

7Positive Effects on the Economy

Planning certainty: Thanks to fixed interest rates,savers can plan the financing of their home withpeace of mind over the entire term of the loan.

Higher-quality housing: Bausparen enablespeople to take housing into their own hands to improve their standard of living.

Bausparen reinforce people’s efforts to takeres ponsibility for themselves: People who becomehome owners simultaneously assume responsibilityfor accumulating wealth, contributing to their ownsocial safety net, and last but certainly not least,for planning how to save for retirement.

The government’s decision to make a contribution to Bausparen is one that promotes the long-termsuccess of contractual savings with all its positive effects. By taking this action, the government funnelsfunds specifically into private home construction andreinforces borrowers’ capital. Additionally, the con-tribution enhances the appeal of Bausparen while simultaneously providing some compensation for in-flation and steering the populace toward investingtheir assets in safe financial products.

A plus for social andeconomic policy

The positive economic effects outweigh the expenseof subsidizing Bausparen, which is why in many coun-tries, Bausparen is a suitable tool for successful soci-al and economic policy (for more information in thisregard, see pages 12-17).

Own funds reinforces the financing process:During the savings phase, customers build up theirown capital, proving their dependability and abilityto make regular payments. This in turn reduces therisk of a loan default to a minimum (see illustration).

Lower loan interest rates: Thanks to lower costsassociated with risk factors and the fact that loansare refinanced with funds from customers’ deposits,savings institutions that offer contractual savingsplans are able to offer interest rates on borrowedfunds that are lower in comparison to the market.

Loans issued in the local currency: Bausparen isimplemented in the local currency. This not onlymakes the individual financing process safer, it alsomakes the economy more independent from inter-nal capital markets.

Subsequent benefits for the construction industry

Bausparen funnels funds that have been saveddirect ly to the real estate sector, which also createspositive effects for this area of the economy bystrengthening demand in the real estate market. Thisin turn provides a better cushion for fluctuations inthe economy. Investments in the construction indus-try create major secondary benefits. They create newjobs and financial incentives for construction compa-nies and regional contractors. Private householdsalso benefit from Bausparen:

Low costs: As a rule, the total costs for financing im-plemented through Bausparen are low. For many me-dian-income households, this is what makes housingaffordable or even a viable option to begin with.

Bausparen reduces risks

People who save through Bausparen are especially reliable customers. Thanks to their

savings discipline, they are already providing proof of their ability to make regular payments

during the savings phase, thereby reducing the risks of a loan default. From the perspective

of “principal-agent theory”, this in turn reduces the risk of “moral hazard” as well as that of

“adverse selection”.

8

Partnering with the MarketLeader to Achieve Success

Partnering with the Market Leader to Achieve Success

tive effects of cooperating with a Bausparkasse. Theadvantages for financial services providers are manyand varied:

By offering Bausparen in combination with their usualproducts, banks can offer their customers appealingfinancing models. The institutions acquire new cus-tomer groups and increase their financing volume.

Contractual savers have own funds, a situationwhich decreases the risk of a loan default. Costs associated with lending decrease not only for the

In Germany, cooperation between banks with privatecustomers and institutions offering contractual sa-vings for housing plans (Bausparkasse) has alreadyproven successful over the long term. Nearly every retail bank in Germany cooperates with one of the 22 Bausparkassen.

Competitive advantages for banks

Numerous banks and financial services providers inother countries offering Bausparen modeled after theGerman system have also come to recognize the posi-

9

Having capital provides for stability when financing

The “golden rule” for privately financing housing in Germany recommends that around one fifth of funds be comprised of the borrower’s personal capital.

60 % Bank loan

20 % Bauspar Loan

20 % Savings balance on the Bauspar account (= borrower’s personal capital)

= 100 % of the purchase price/building costs

Savings balance on the Bauspar account+ Bauspar Loan

= Total contractually stipulatedBauspar sum

Partnering with the Market Leader to Achieve Success

Bausparkasse Schwäbisch Hall is especially efficientin processing the saving plans and housing loans.

State-of-the-art IT solutions ensure the company’ssuccess.

Customers’ inclination to seek security creates ongoing demand.

These strengths serve to solidify BausparkasseSchwäbisch Hall’s market leadership. We have alsobeen successful in the international arena for morethan 20 years.

When it comes to the introduction of Bausparen innew markets as well as the establishment and deve-lopment of contractual savings for housing institu -tions, Bausparkasse Schwäbisch Hall has extensive expertise.

Because Bausparkasse Schwäbisch Hall strives for cooperative relationships that are not only strategi-cally beneficial but also promote trust, both partnersbenefit from the strengths and experience of the other, allowing them to achieve ambitious objectivestogether.

customer but also for the lender. The long contractterms associated with Bausparen facilitate long-term relationships with customers. Attractive pro-ducts and higher market share lead to an improvedimage and competitive advantages. When banksand institutions offering contractual savings forhousing plans cooperate, this opens up a range ofcross-selling opportunities.

To benefit mutually from strengths

With more than seven million customers, Bausparkas-se Schwäbisch Hall is the largest institution offeringcontractual savings for housing plans and has beenthe market leader in Germany for decades. We oweour success to the following factors, among others:

Bausparen is an attractive, flexible product.

Bausparkasse Schwäbisch Hall has exceptional mar-keting and sales expertise with Bausparen as a pro-duct.

As a contractual savings for housing institution,Bausparkasse Schwäbisch Hall has invested in long-term product management.

Liquidity and risk management are organized withthe long term in mind.

10 A Schwäbisch Hall Export That’s a Winner

A Schwäbisch Hall Export That's a Winner

sparkasse (SGB) in 2004. The company began in Tian-jin, a region along the east coast with fifteen million inhabitants. At the end of 2011, Sino-German Bauspar-kasse opened a second branch in the province of Chong-qing, one of the largest metropolises worldwide.

Stability for new market economies

As the political landscape changed in the 1990s, thestate-directed economies of Eastern Europe collapsedand transitioned to market economies. While this was taking place, government-sponsored housing was alsobecoming privatized, which rapidly increased demandamong the populace for a means to finance the purchase,construction, and modernization of housing. However,the state banks in these countries were not prepared tohandle private financing for residential construction. Loan interest rates of more than 20 percent made borrow-ing unaffordable for citizens, while at the same time highinflation also kept people from developing good savingshabits. For these new market economies, Bausparen pro-vided an attractive and suitable method for financing therequired investments in residential construction. Thisnew financial product gave many people their first op-portunity to save up the funds needed to have their ownhome. Since this stimulated housing construction, gov-erments provided the appropriate legislative environ-ment and an attractive subsidy.

Bausparen as a stabilizing factor

Real estate loans that were issued too carelessly triggeredthe international financial crisis. This situation showedthat the purportedly “conservative” German system forfinancing housing construction also has considerablestrengths from an economic perspective, for example thehigh proportion of funds coming from the borrower, andfixed interest rates on loans. In this context, the Bausparcontract functions as an additional stabilizing element.Countries with a Bauspar savings system in place weath-ered the crisis considerably better than nations withoutthis financing system. Today, Bausparen makes a signifi-cant contribution in many countries to sustainable socialand economic policy.

Bausparkasse Schwäbisch Hall is the largest institutionin Germany to offer contractual savings for housingplans and has the largest customer base. With more thaneight million Bausparen savings contracts for more than264 billion euros in total funding, the company has beenthe market leader for many years. Business in othercountries is an integral part of our corporate strategy.

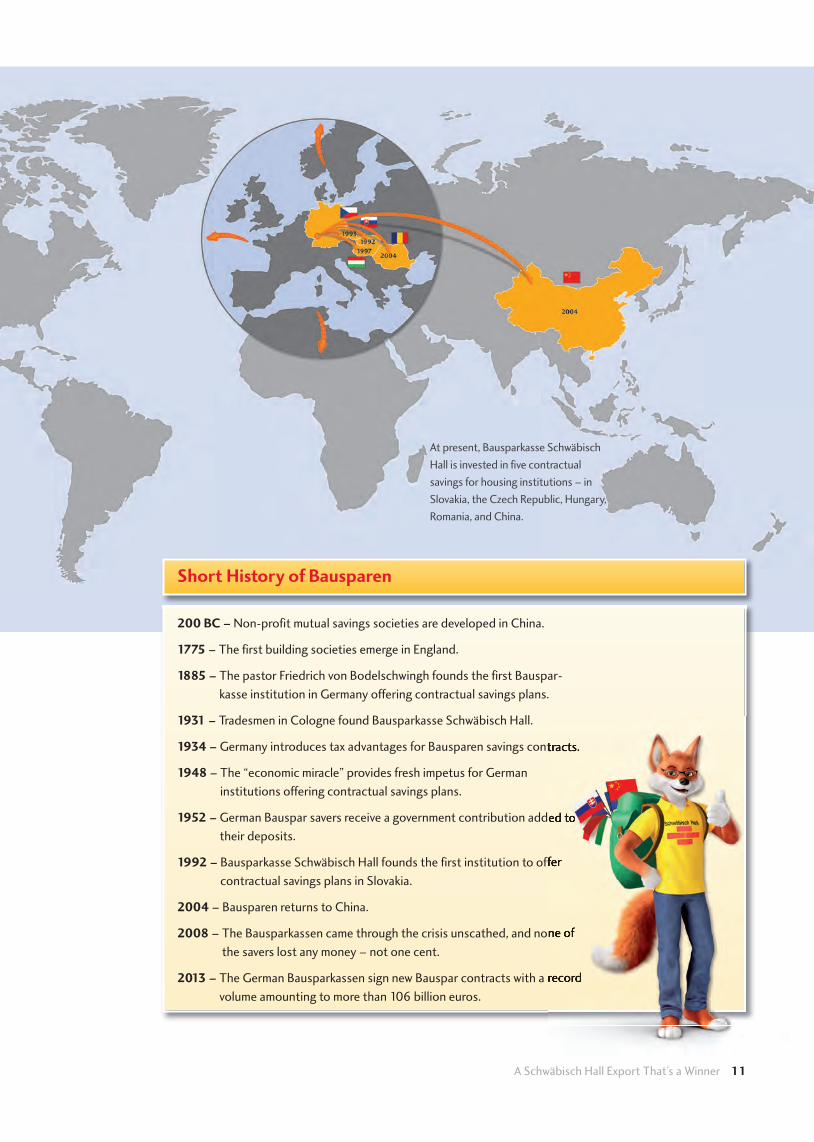

Bausparkasse Schwäbisch Hall is a pioneer abroad

Bausparkasse Schwäbisch Hall has been active in the in-ternational arena since 1992. Its affiliated companies inSlovakia, the Czech Republic, Hungary, Romania, andChina have a total of 3.1 million customers with around3.5 million Bauspar contracts and 6,500 employees.Nearly all of these affiliated companies are market lead-ers in their countries. Bausparkasse Schwäbisch Hall wasa pioneer in the field of exporting Bausparen modeledafter the German system. The amendment of the Ger-man Bausparkassengesetz – the Building and Loan Asso-ciations Act – in 1991 made it possible for the first timeto establish affiliated companies in foreign countries. Asearly as 1992, Bausparkasse Schwäbisch Hall and itspartners founded Prvá stavebná sporitel’na (PSS, whichtranslates as “First Bausparkasse”), the first institution ofits kind in Eastern Europe. In 1993, Ceskomoravská sta-vební sporitelna (CMSS, which translates as “Bohemian-Moravian Bausparkasse”) was launched in the Czech Re-public. In Hungary, Bausparkasse Schwäbisch Hall intro-duced the concept of Bausparen through what is todaythe institution Fundamenta- Lakáskassza (FLK) in 1997.The first institution offering Bausparen in the Romanianmarket, Raiffeisen Banca pentru Locuint,e (RBL, whichtranslates as “Raiffeisen Housing Bank”), opened itsdoors in June 2004.

Bausparen has proven itself internationally

The success of Bausparen in Eastern Europe also kindledinterest in China. Bausparkasse Schwäbisch Hall and Chi-na Construction Bank Corporation, one of the largestbanks in the world, jointly established Sino-German Bau-

11A Schwäbisch Hall Export That’s a Winner

Short History of Bausparen

200 BC – Non-profit mutual savings societies are developed in China.

1775 – The first building societies emerge in England.

1885 – The pastor Friedrich von Bodelschwingh founds the first Bauspar -kasse institution in Germany offering contractual savings plans.

1931 – Tradesmen in Cologne found Bausparkasse Schwäbisch Hall.

1934 – Germany introduces tax advantages for Bausparen savings contracts.

1948 – The “economic miracle” provides fresh impetus for German institutions offering contractual savings plans.

1952 – German Bauspar savers receive a government contribution added totheir deposits.

1992 – Bausparkasse Schwäbisch Hall founds the first institution to offercontractual savings plans in Slovakia.

2004 – Bausparen returns to China.

2008 – The Bausparkassen came through the crisis unscathed, and none ofthe savers lost any money – not one cent.

2013 – The German Bausparkassen sign new Bauspar contracts with a recordvolume amounting to more than 106 billion euros.

At present, Bausparkasse SchwäbischHall is invested in five contractual savings for housing institutions – inSlovakia, the Czech Republic, Hungary,Romania, and China.

12 Success on an International Scale

Germany

Bausparkasse Schwäbisch Hall AG

Corporate headquaters Schwäbisch Hall, Germany

Year established 1931

Core business Bausparen,construction financing,additional provision products

Employees 7,300

Customers 7.3 million

Active contracts 8.14 million

Berlin, Brandenburger Tor

Germany is the land of Bausparen– and has beenfor nearly 100 years. Bausparkasse SchwäbischHall is the market leader and has the largest custo-mer base.

Bausparen is what makes it possible for many peopleto have their own home. The political and demogra-phic changes occurring after the fall of the Berlin wallcaused a further surge in demand. Today, roughly 80million people live in Germany, and there are roughly25 million Bauspar savers.With 7.3 million customers, Bausparkasse SchwäbischHall is Germany’s largest institution offering con-tractual savings for housing plans and the market lea-

der. Bausparkasse Schwäbisch Hall sells its financialproducts for contractual savings, construction finan-cing, and additional provision products for owner-oc-cupied residential real estate in partnership with the“genossenschaftlichen Banken” – banks that functionas credit unions. With more than 1,000 institutionsand roughly 13,000 branch offices, they offer one ofthe densest banking services networks in Germany.Bausparkasse Schwäbisch Hall has about 4,000 salesrepresentatives working as field agents and 3,300employees located in its headquarters in SchwäbischHall. With more than 10 billion euros worth of privatehousing loans per year, Schwäbisch Hall is one of thelargest construction financiers in Germany.

13Success on an International Scale

Slovakia

Prvá stavebná sporitel’na, a.s. (PSS)

Corporate headquaters Bratislava, Slowakia

Year established 1992

Core business Bausparen,construction financing

Employees 1,395

Customers 761,000

Active contracts 833,000

In 1992, Slovakia was the first country in EasternEurope to introduce Bausparen – with incrediblesuccess. PSS is the leading company in this impressive success story.

During the political changes that took place at thebeginning of the 1990s, many apartments were priva-tized. At the same time, the Slovakian governmentwas looking for tools to improve its housing inventoryand methods for financing residential construction. Itrightfully trusted the German Bauspar System. Thesuccess of Bausparen in the market from the very be-ginning also encouraged and enthused neighbouring

countries for the concept of Bausparen.

In the meantime, more than one in four Slovaks hasimproved his or her housing situation with the help ofBausparen. The institutions offering Bausparen inSlovakia concentrate in particular on financing mo-dernization, renovation and repair work. Around 60percent of the funds loaned through these measuresare used for the improvement of existing apartmentsand houses. With nearly 80 percent of market share,the undisputed market leader is Prvá stavebná sporitea (PSS), a company in which BausparkasseSchwäbisch Hall is invested.

ˇ

Bratislava, Bratislavsky hrad (Burg Bratislava)`

14

The Czech Republic

Ceskomoravská stavební sporitelna, a.s.(CMSS)ˇ ˇˇ

Corporate headquaters Prague, Czech Republic

Year established 1993

Core business Bausparen,construction financing,retirement planning

Employees 2,678

Customers 1.5 million

Active contracts 1.8 million

Success on an International Scale

Prag, Karluv most (Karlsbrücke)

Whether for financial planning or financing – inthe Czech Republic, Bausparen savings plans aresynonymous with trust and reliability: Nearly oneout of every two Czech citizens saves throughBausparen.

In the Czech Republic, Bausparen is a true successstory. Nearly one out of every two of the 10.5 milli-on Czech citizens has opted for Bausparen. This ma-kes Bausparen an integral component in financialplanning, enjoying immense popularity since its introduction in 1993. The following figures speakfor themselves: The Czech populace has invested aquarter of its savings in Bausparen. Over the last

20 years, institutions offering contractual savingsfor housing plans have provided three quarters of allfunding for housing construction.

Of a total of five market participants, BausparkasseSchwäbisch Hall together with a major local bankhas been the driving force behind this success – the market leader Ceskomoravská stavební sporitelna(CMSS). The opportunity to invest money safelyand receive a government subsidy is the corner-stone of its success. CMSS takes advantage of itsoutstanding market position to place supplementalfinancial planning products and is thus an attractivesales partner for the local bank.

1515Success on an International Scale

Hungary

Fundamenta-LakáskasszaLakás-takarékpénztár Zrt. (FLK)

Corporate headquaters Budapest, Hungary

Year established 1997

Core business Bausparen,construction financing,retirement planning

Employees 1,242

Customers 578,000

Active contracts 658,000

Budapest, Országház (Parlament)

Bausparkassen provided stability during the ban-king crisis. The financing business segment is FLK’sgreatest strength.

During the last few years, the 10 million people livingin Hungary experienced a profound economic crisis,in particular in the banking sector. Loans in foreigncurrencies used to be very popular for financing hou-sing. But facing a deteriorating exchange rate, manyHungarians were no longer able to repay their loans,and default rates rose at many financial institutions.By contrast, the institutions offering contractual savings for housing plans – which had been operatingin Hungary since 1997 – weathered the crisis well.

They even had good enough credit quality to expandtheir financing business, since they provided funds forhousing exclusively in the domestic currency. Moreo-ver, Bausparkassen are in a better position than banksto judge their customers’ ability to make regular pay-ments.

There are four Bausparkassen in Hungary. The largestof these is Fundamenta-Lakáskassza (FLK), a companyin which Bausparkasse Schwäbisch Hall is invested.Bausparen is not the only segment in which FLK hasan outstanding market position. With a market shareof over 30 percent, in 2013 FLK was also the coun-try’s largest construction financier.

16 Success on an International Scale

The Middle Kingdom is experiencing dynamicgrowth and needs solid funding methods for housing construction. The government supportsBausparen.

The economies in Asia and in particular China with its1,3 billion inhabitants are developing at a breakneckpace. Many people are moving from the country tothe major cities, creating high demand for housing. Incontrast to the situation in European countries, it isprimarily large apartment complexes that are beingbuilt in China, and the individual apartments are thensold as condominium units.Searching for solid financing solutions for middle-in-

come groups, China introduced the German Bausparsystem. This is the reason why this system has alsobeen used in Asia since the beginning of the millenni-um. In 2004, Bausparkasse Schwäbisch Hall and Chi-na Construction Bank Corporation, one of the largestbanks in the world, jointly established Sino-GermanBausparkasse (SGB). The joint venture was launchedin the metropolis of Tianjin (near Beijing), where fifteenmillion people live. In 2011, SGB expanded its busi-ness territory to include Chongqing in western China,and further expansion measures are planned for thenear future. In addition to its core business of Bau-sparen, SGB also offers mortgages and developmentloans.

China

Sino-German Bausparkasse (SGB)

Corporate headquaters Tianjin, China

Year established 2004

Core business Bausparen, mortgage loans,property financing

Employees 1,131

Customers 144,000

Active contracts 140,000

Peking, Tiantán (Himmelstempel)

17Success on an International Scale

The newest market for Bausparen in Europe showssigns of very promising development.

Bausparen has been in place in Romania since 2004.This country, with a population of about 21 millionpeople, is currently the newest market in Europe forBausparen. Over half a million Romanians currentlyhave a Bauspar contract. Now that the crisis years have passed, the general populace’s ability and wil-lingness to save is once again trending upward. This isalso reflected in the growing number of Bauspar con-tracts managed by market participants. The motto ofthe Romanian association of contractual savings forhousing institutions is: “Everyone should have a Bau-

spar contract”. This association is convinced thatroughly 6.6 million people could be benefiting rightnow from Bausparen. After all, many apartments stillneed to be renovated and remodeled from the groundup.

Bausparkasse Schwäbisch Hall is active in Romania incooperation with the Romanian Raiffeisenbank andRaiffeisen Bausparkasse from Austria. Raiffeisen Banca pentru Locuințe is the oldest bank to offercontractual savings for housing plans in the Romanianmarket and has around 200,000 customers. The pro-ducts are sold via Raiffeisenbank and through its ownsales representatives working as field agents.

Romania

Raiffeisen Banca pentru Locuinte (RBL)

Corporate headquaters Bukarest, Romania

Year established 2004

Core business Bausparen,construction financing

Employees 139

Customers 191,000

Active contracts 196,000

Bukarest, Ateneul Român (Athenäum)

´

´

Bausparen encourages people to develop good savings habits and strengthens their reliance ontheir own resources.

When it comes to financing their construction projects, the guaranteed interest rate allows saversto plan with peace of mind.

The capital saved reduces the risk of default during the financing phase and decreases lendingcosts for banks and customers.

Legislation ensures that investors are protected and provides for stability in times of financial crisis.

Bauspar funds promote construction activity and provide for continual demand while creating revenues and jobs throughout the entire industry.

The government subsidy mobilizes private capital for residential construction and funnels the population’s investments into safe financial products.

The positive effects on the economy outweigh the costs of subsidizing the Bausparen savings system.

18

Bausparen (Contractual Savings for Housing) – A Tool for Successful Social and Economic Policy

Bausparen – A Tool for Successful Social and Economic Policy

Allocation Point in time at which all of the requirements for the savings contract (e.g., minimum savings balance on the Bauspar acount, minimum savings period) have been satisfied so that the total funds (savings balance on the Bauspar account plus Bauspar loan) can be disbursed.

Bausparen (Contractual An especially safe method of saving money to make housing dreams come true, Savings for Housing) it allows the saver to access a loan through the contractual savings plan at a

favourable, fixed rate of interest.

Bauspar Contract Contract between the institution offering contractual savings for housing plansand the customer (saver) in which key parameters are set down for the savings and loan phases.

Bauspar Loan A loan that is used for housing; the interest rate is set by means of the Bauspar contract.

Bauspar Sum Contractually stipulated amount comprised of the savings balance on the Bauspar account and the Bauspar loan through the contractual savings plan.

Bausparkasse Special financial institution offering Bausparen from a closed collective.(Contractual Savings for Housing Company)

Collective Community of savers who save money on the basis of Bauspar contracts and repay Bauspar loans.

Government Subsidy State support for Bauspar clients, that is paid to the customer´s Bauspar saving account.

Loan Phase Period between allocation and full repayment of the Bauspar loan.

Savings Balance on the Deposits made by customers; interest is paid on the balance and in Bauspar account certain cases the government also makes a contribution.

Savings Phase Period between the time the savings contract is signed and the allocation; it is during this phase that the customer builds up his or her savings balance on the Bauspar account.

Schedule of Framework for Bausparen with essential key figures, e.g., interest rates for the Rates and Fees savings and loan phases, savings and principal repayment amounts, fees as

applicable

19Glossary

Glossary – All of Arguments at a Glace

2001

9671

MAV

08/

14

Bausparkasse Schwäbisch HallInternational MarketsCrailsheimer Straße 5274523 Schwäbisch HallGermany

Telephone: +49 791 46-3706International.Markets@schwaebisch-hall.dewww.schwaebisch-hall.de

Reach out to us – we look forward to speaking with you personally.

Christian OestreichHead of International Markets

Tel. +49 791 [email protected]

Dr. Jirka GehrtHead of Foreign Investments

Tel. +49 791 [email protected]

Michael DornerHead of International Projects

Tel. +49 791 [email protected]