bank of ceylon annual report 2010

TRANSCRIPT

The Plurality of the Singular as implied when we consider One Nation… One People is clear. The Bank of Ceylon is Sri Lanka’s No. 1 Bank… we are 1 with the Nation…1 with the People…in fact 1 figures largely in our enterprise as we work to support the Government’s vision of uniting and prospering Sri Lanka as 1 Nation…1 People.

THE POWER OF1…

BANK OF CEYLON ANNUAL REPORT 2010 1

VisionBankers to the nation

MissionCustomers - Foster mutually rewarding customer relationships with all our customers exceeding their expectations.

Staff - Give all our staff the recognition and rewards to be the best team of achievers in service excellence.

Owners - Be a profitable catalyst for equitable development covering urban and rural areas.

Society - Provide world-class banking services across the nation as a beacon for progress and growth.

1 customer base…millions of people of every persuasion,every occupation, every race…1 Product Portfolio…

1 Customer Service regime…1 Bank…BoC

1 Customer base…9 million

customers…1 Bank…Bank of Ceylon

Contents5 Business Highlights

6 Historical Review

7 Financial Highlights

8 Chairman’s Message

11 General Manager’s Review

14 Board of Directors

17 Corporate Management Team

26 Executive Management Team

30 Management Discussion and Analysis

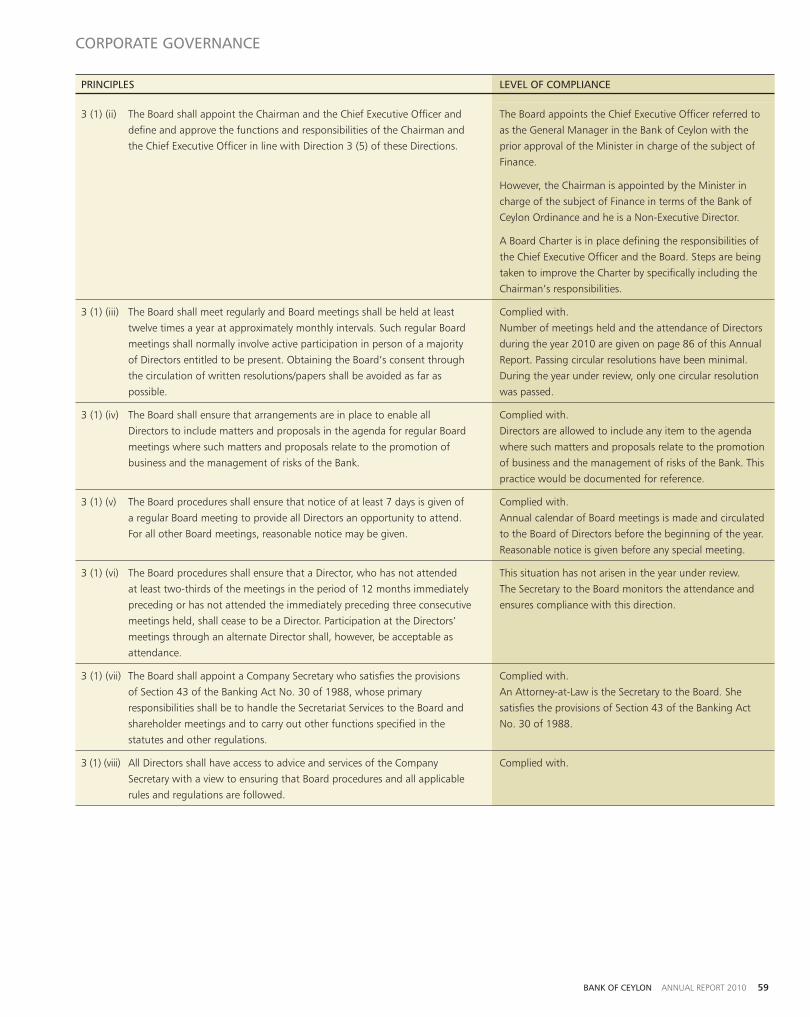

56 Corporate Governance

80 Board & Board Subcommittees

81 Report of Board Subcommittees

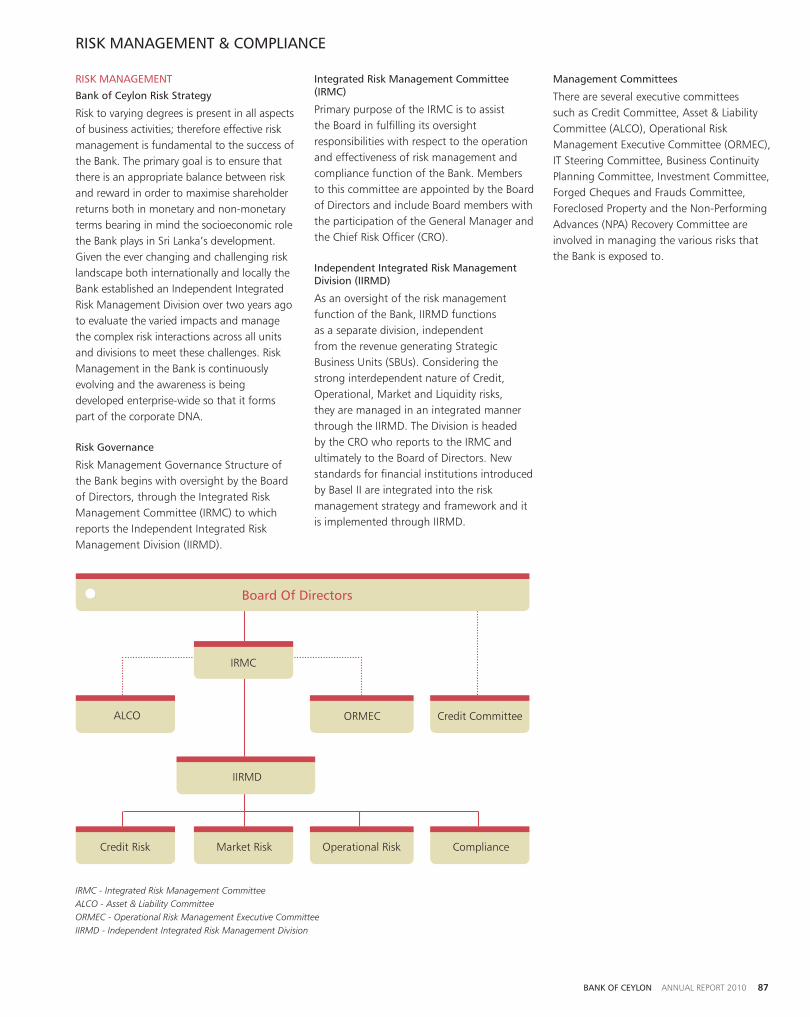

87 Risk Management & Compliance

95 Sustainability Report

126 G3 Standard Disclosures Index

132 Products & Services

135 Financial Reports

137 Annual Report of the Board of Directors on the State of Affairs of the Bank of Ceylon

141 Directors’ Interests in Contracts

145 Directors’ Responsibility for Financial Reporting

146 Independent Assurance Report

147 Directors’ Statement on Internal Control

149 Report of the Auditor General

150 Income Statement

151 Balance Sheet

152 Statement of Changes in Equity

153 Cash Flow Statement

156 Significant Accounting Policies

167 Notes to the Financial Statements

237 Capital Adequacy

241 Investor Information

255 Group Structure

256 Subsidiaries & Associates

260 Corporate Offices & Overseas Branches

262 BoC Service Points

276 Correspondent Banks by Country

282 Exchange Companies by Country

283 Glossary of Financial/Banking Terms

Inner Back Cover Corporate Information

BUSINESS HIGHLIGHTS

Highest ranked Sri Lankan bank in the Bankers Almanac.

Wider customer base over 9 million accounts.

Leader in treasury operations with over 50% of local foreign exchange market.

Worldwide network reaching over 800 foreign correspondents.

Leader in inward foreign remittances with over 43% market share.

Nation’s first locally-owned bank, expanded its operations with an island-wide network of 875 service points; 854 connected on-line.

Representing largest off-shore banking operations with the highest market share of assets.

Bank of Ceylon‘s outlook has been revised by Fitch Ratings Lanka Limited to positive from stable, and affirmed its National Long-Term Rating at ‘AA (lka)’.

Bank achieved a remarkable breakthrough in trade finance by centralising its activities for customer convenience and recognised as the best Sri Lankan Trade Bank for 2010 for the second consecutive year with over 50% market share.

The first State Bank to commence 24 hour service point.

The London branch of the Bank was converted as an independent fully-owned Subsidiary, operating in United Kingdom.

Single borrower exposure capacity in excess of Rs. 10 billion.

BoC‘s new corporate plan branded ‘one 10 TWELVE’ (ie, Rs. 1 trillion assets, Rs. 10 billion profit before tax by year 2012) reached to Rs. 715 billion assets, Rs. 10 billion profit before tax in the year 2010.

Bank’s deposit mobilisation campaigns throughout the country achieved a remarkable deposit base of Rs. 524 billion.

Lending to private sector increased by Rs. 62 billion, 34% up.

Increased penetration in branchless banking by introduction of internet banking and mobile banking.

Bank successfully raised Rs. 5 billion for the second time by issuing subordinated 5 year debentures listed on the Colombo Stock Exchange.

Bank of Ceylon introduced new business lines by adding an investment arm and Islamic banking into its banking stream.

BANK OF CEYLON ANNUAL REPORT 20106

HISTORICAL REVIEW

Bank of Ceylon has evolved continuously over the years, undergoing changes in its business operations, branch network, ownership, people, products and services to emerge as the largest financial service provider in Sri Lanka. Such progress is summarised below:

1939Bank of Ceylon established as the nation’s first modern, locally-owned bank. Ceremonially opened on 1 August by Governor, Sir Andrew Caldecott, at the present-day premises of the City Office.

1941Operations commence in Kandy with opening of a branch office. Other branches opened subsequently in other large outstation towns: Galle, Jaffna and Trincomalee.

1946Foreign Department established. Operates from offices at the Grand Oriental Hotel (GOH) Building, Colombo Fort.

1949First overseas branch opens in London shortly after Independence; it is the thirteenth bank branch to be opened.

1953C Loganathan becomes first Sri Lankan General Manager.

1954Central Office moves from City Office to premises at GOH Building.

1959Authorised capital enhanced to Rs. 50 million by Act of Parliament.

1961Nationalisation. The Government of Ceylon becomes sole owner of Bank of Ceylon.

Kachcheri branch network set up in alignment with the Government’s District Administration System.

1973Agriculture Service Centre concept implemented. Operations commence at over 350 Agricultural Service Centre Branches. Comprehensive Rural Credit Scheme implemented.

1978Non-Residents Foreign Currency (NRFC) deposit scheme introduced.

1979Off-shore banking operations commenced with the establishment of the Foreign Currency Banking Unit.

1980Computer Division established; automation of business operations commences.

1981Branch opened in Malé, Republic of Maldives.

1985Head Office moves to 32-storey BOC Tower in Colombo.

1988Installation of the first BOC ATMs ushers in the electronic banking era.

1989Ceybank Visa credit card introduced in collaboration with Visa International.

1995Overseas branch network augmented with offices in Madras and Karachi.

1996Joint venture with Nepal Bank establishes Nepal Bank of Ceylon Limited.

1998MoU with Government results in greater management autonomy and target-based performance.

2000Authorised capital further enhanced to Rs. 50 billion by Act of Parliament.

2004Real estate subsidiary Mireka Capital Land (Private) Limited formed to invest in Havelock City, the largest single condominium development in Sri Lanka.

2005Balance Sheet footings top Rs. 300 billion, the largest asset base of any Sri Lankan bank.

Wide range of relief, rehabilitation and reconstruction activities undertaken and financed in the aftermath of the December 2004 tsunami.

2006Wins IBM/FISERV prize for the fastest deployment of an online core banking system in Asia Pacific region.

2007Raises US$ 210 million, the largest internationally syndicated debt by any Sri Lankan issuer; appointed Co-Manager of historic US$ 500 million debut bond issued by the Government of Sri Lanka; commences Village Development Programme focused on engaging rural communities.

2008Raises Rs. 4.2 billion via a listed subordinated rupee debenture of 5 years; raises US$ 21.6 million via a private placement of a 5-year subordinated dollar debenture.

2009BoC completed online branch network by bringing in Kilinochchi, Mankulam and Mullaitivu branches into the network, the operations of which were disrupted at the time of ending the war. BoC celebrated its70th Anniversary.

Bank launched an Islamic Banking Unit, which operates through Island-wide network.

2010BoC diversified its operations in the United Kingdom by upgrading its London branch to a Subsidiary of BoC that will be used as a platform for global banking and to attract more foreign investment to the country.

Bank has set up a specialised investment banking unit aiming to diversify its portfolio in non-core banking.

Bank successfully raised Rs. 5 billion in the second public issue of unsecured, subordinated redeemable five-year debentures.

BoC acted as the Bankers to the issue, Managers, sponsors and registrars for the Urban Development Authority‘s Rs. 10 billion debenture issue.

BANK OF CEYLON ANNUAL REPORT 2010 7

Bank Group

Key Financial Data2010

Rs. million2009

Rs. million Change

%2010

Rs. million2009

Rs. million Change

%

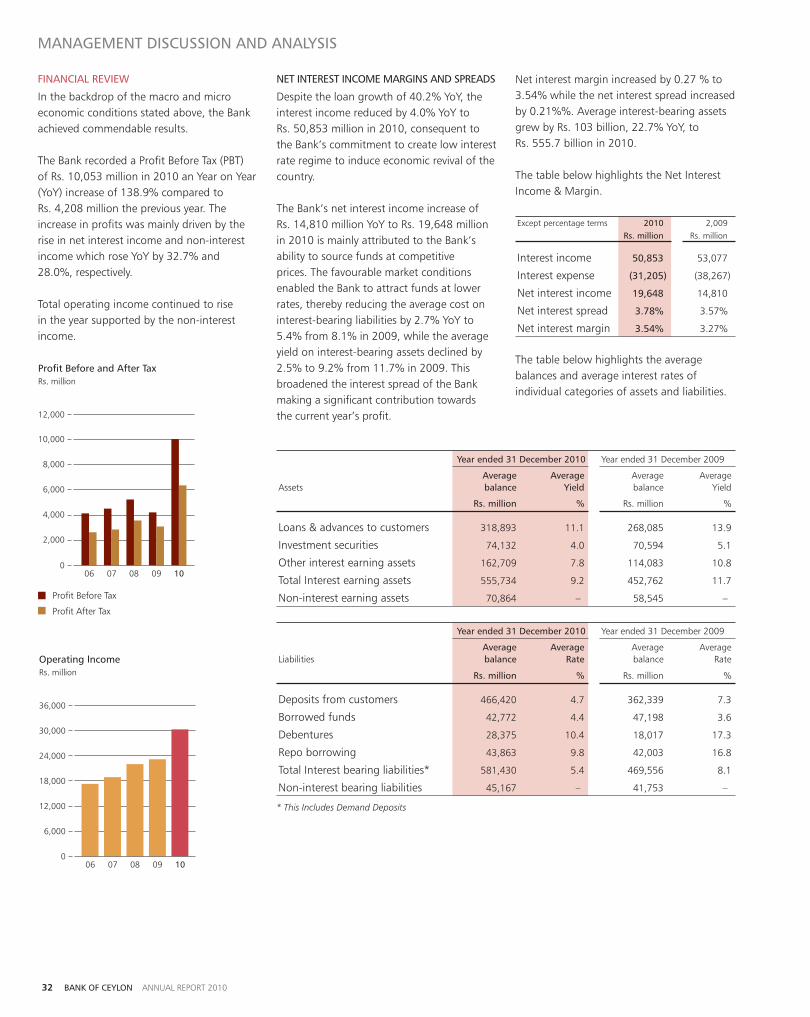

Results for the YearTotal revenue 63,363 63,461 (0.2) 66,867 66,128 1.1

Net interest income 19,648 14,810 32.7 21,043 15,789 33.3

Profit before financial VAT and taxation 14,054 7,202 95.1 14,990 7,666 95.5

Profit before taxation 10,053 4,208 138.9 11,075 4,720 134.6

Provision for taxation 3,687 1,124 228.0 4,162 1,403 196.7

Profit after taxation 6,365 3,084 106.4 6,913 3,317 108.4

Value to the Government 10,784 5,465 97.3 11,385 5,826 95.4

Position at the Year EndTotal assets 714,954 538,241 32.8 730,065 547,421 33.4

Shareholders’ funds (Capital & Reserves) 28,132 24,899 13.0 31,261 27,534 13.5

Deposits from customers 524,233 408,607 28.3 529,319 411,460 28.6

Gross loans and advances 382,310 275,022 39.0 392,708 283,298 38.6

Non-performing assets 12,639 15,542 (18.7) 13,701 16,281 (15.8)

Net non-performing assets 5,247 7,317 (28.3) 5,751 7,466 (23.0)

Per Share Data (Rs.)Earnings per share 1,273 617 106.3 1,352 660 104.8

Net assets per share 5,626 4,980 13.0 6,039 5,317 13.6

Profitability Ratios (%)Return on average equity 24.0 12.9 11.1 23.8 12.8 11.0

Return on average assets 1.6 0.8 0.8 1.7 0.9 0.8

Interest margin 3.1 2.9 0.2 3.3 3.0 0.3

Cost to income 53.7 68.3 (14.6) 53.9 68.0 (14.1)

Loans to deposits ratio 72.9 67.3 5.6 74.2 68.9 5.3

Year on Year Growth in Earnings (%) 106.4 (13.4) 119.8 108.4 (16.0) 124.4

Assets Quality Ratios (%)NPA ratio 3.3 5.7 (2.4) 3.5 5.8 (2.3)

Net NPAs/Shareholders’ equity 18.7 29.4 (10.5) 19.0 28.1 (9.0)

Statutory Ratios (%)Capital adequacy ratio: Tier I Capital (minimum required 5%) 10.3 11.2 (0.9) 11.4 12.0 (0.6)

Tier I & II Capital (minimum required 10%) 13.7 14.2 (0.5) 15.2 15.1 0.1

Liquid assets ratio (Domestic) (minimum required 20%) 28.7 21.1 7.6 N/A N/A N/A

FINANCIAL HIGHLIGHTS

BANK OF CEYLON ANNUAL REPORT 20108

CHAIRMAN’S MESSAGE

It is my pleasure to present to you the Annual Report and Financial Statements of the Bank of Ceylon (BoC) for the year 2010. The Bank celebrated 71 years as the Bankers to the Nation and was engaged in many initiatives to become an integrated financial services provider. The Bank has positioned itself to benefit from considerable earnings growth over the next few years, in tandem with the positive economic outlook of Sri Lanka.

ECONOMIC ENVIRONMENT

Having weathered a severe recession, the global economy is now showing signs of recovery. Although financial markets have recovered from their lows in 2009, they are still characterised by tight economic conditions. International capital flows to developing nations are projected to gather momentum. Modest demand growth has been tempered by factors including continued weakness in European Economy and slow adjustment of fiscal policies in developing economies. Medium-term prospects and development are heavily dependent on recovery and fiscal consolidation of developing economies.

Sri Lanka’s economy was relatively unharmed by the global crisis and it is satisfying to note that the optimism placed on economic growth due to the cessation of war was not merely an expectation but a reality.

We are encouraged by signs of economic recovery and solid performance in key sectors consequent to stoppage of war. I believe it is

the consensus opinion that our economy will grow at the above trend levels over the next few years with the expectation of doubling of GDP in the medium-term. Certain challenges are posed in this framework where local economy is likely to maintain a growth rate unparalleled to global counterparts. Policy makers are tested in this environment to support the growth momentum in the country whilst maintaining attractive interest rates, addressing supply side anomalies and maintaining inflation at a subdued level. In this context, BoC continues to be the leader in several core banking sectors. At a time when Sri Lanka is on the threshold of rapid economic growth with foreign investor confidence at unprecedented levels, BoC is engaged in prudent and strategic banking operations as encompassed in its corporate plan. Its position of strength, stability and potential is affirmed by the national long-term rating of AA (lka) and an upgrade to positive outlook by Fitch Ratings.

FINANCIAL PERFORMANCE

The Bank consolidated its position as the premier public sector bank by posting a staggering Group profit before tax of Rs. 11.1 billion in 2010, the highest ever in the Bank’s history. This is mainly attributed to the Bank’s fee-based income and investment banking activities which rose by 58% Year on Year (YoY). The Group Balance Sheet reached Rs. 730 billion with loans and advances reaching Rs. 393 billion. Deposits increased to Rs. 529 billion while the quality of the assets improved as reflected in the reduced NPA of 3.5%.

In 2009, we set ourselves a challenging target as set out in our Corporate Plan, “one 10 TWELVE” to reach Rs. 1 trillion in assets and attain Rs. 10 billion in profits by the end of year 2012. It is with pleasure that I mention that we have achieved the profit target through dedication and by adopting a well-focused approach, thus paving the way to set new milestones.

LOCAL FRANCHISE

Through our network of over 300 branches, 218 extension offices and 352 ATMs island-wide, we strive to expand banking facilities across the country in an equitable manner.

The Bank commenced night and day banking and extending allied services to assist the Government in its efforts of transforming the City of Colombo. A multi-purpose branch was established in the Head Office to play a greater role in stimulating economic activities. It was the first time a State commercial bank embarked on such a venture in Sri Lanka.

The Bank initiated target savings schemes to foster the savings habit among citizens in the rural areas. The primary objective of the Gam Udana programme is to promote all Sri Lankans to open and maintain bank accounts.

The Bank consolidated its position as the premier public sector bank by posting a staggering Group profit before tax of Rs. 11.1 billion in 2010, the highest ever in the Bank’s history.

BANK OF CEYLON ANNUAL REPORT 2010 9

CHAIRMAN’S MESSAGE

GLOBAL BANKING

Whilst being in the forefront of national development, the Bank also made its presence felt in the global arena during the year. The London Branch of the Bank, re-named as Bank of Ceylon (UK) Limited, operates as an independent wholly- owned subsidiary, regulated by the Financial Services Authority of the United Kingdom. This Bank is the springboard to other destinations of the world, especially to the European Union, United States, Canada, Australia and Japan. The subsidiary is currently engaged in lending services and strategies to expand its reach and product-base over the coming years.

The Bank secured Rs. 200 billion worth of inward remittances during the year while 50,997 new Non-Resident Foreign Currency accounts were opened increasing the total accounts to 353,863. The Bank also expanded correspondent relationships with 60 new global banks and 6 exchange houses.

Through several bilateral agreements and loan syndications amounting to approximately US$ 300 million, BoC was able to establish long-term relationships to achieve growth targets, trade finance and infrastructure development of Sri Lanka.

THE ROLE OF THE BANK AS A CATALYST FOR DEVELOPMENT

At a time when Sri Lanka is entering a new era in its history with rapid changes in the socio economic and business sectors, the Bank of Ceylon is in the forefront of the nation’s active development programmes as the premier in the Business and Finance industry.

As the resurgence of the North and the East has been prioritised in the nation’s development agenda, BoC entered the development process by aligning its strategies with national development goals. The Bank successfully brought the community in the North and the East to the formal commercial banking stream, through providing access to funding, safekeeping of valuables and facilitating entry for entrepreneurship activities in the SME sector. Further, the Bank dedicated itself to improve and empower the Internally Displaced Persons (IDP) of the North and the

East through the expansion of the Bank’s branch network in the two Provinces by more than 100 service points and committing to extend advances in excess of Rs. 17 billion to the Northern and the Eastern Provinces. Our involvement encompassed distribution of donor funding. The Bank’s timely activities in this regard were commended by bilateral donor agencies.

The 24-hour call centre that was set up to provide a multi-lingual service to displaced customers in the North and the East. It was the first time a State Bank extended such a service.

The Bank of Ceylon was instrumental in bringing together the entrepreneurs of the North and the South through a joint programme with the private sector, creating markets for the produce of farmers in Jaffna through programmes such as ‘Yal Uthpaththi’ to assist the Poverty Alleviation Scheme of the Central Bank of Sri Lanka.

The Bank further aims to involve the Sri Lankan diaspora to actively contribute to the North and the East socioeconomic revival and thereby facilitate benefits to permeate to the whole economy.

The Bank, in partnership with the private sector, extended financial services to the corporate sector and institutions. The strategic transactions being the assistance given to the Urban Development Authority to issue a debenture worth Rs. 10 billion to address the housing demand in Colombo. The newly set up Investment Banking Unit of the Bank, managed the debenture of Rs. 5 billion to raise funds for the Bank in 2010.

During the year, the Bank of Ceylon became fully geared in implementing the Shariah-compliant Islamic Banking operations, exemplifying the Bank’s corporate adage, ‘Bankers to the Nation’.

The Bank will continue to play a crucial role by aligning its corporate strategy to partner the national development goals aimed at transforming Sri Lanka into a dynamic global hub for Naval, Aviation, Commercial, Energy and Knowledge.

BANK OF CEYLON ANNUAL REPORT 201010

The Bank of Ceylon in keeping with its traditional role as a socially responsible bank, introduced several innovative products and services to uplift the quality of life of diverse customers across the entire social strata, targeting economic, rural and social development which would benefit the country and its people. Products and services were introduced to complement consumer needs and aspirations and also address economic and infrastructure development. The Bank recognised the need for a retirement benefit scheme in the light of demographic changes and an ageing population. The Bank assisted the agrarian sector in order to propel the nation to be self-sufficient and ensure food security. The Bank continued to be a leader in providing assistance to small and medium enterprises through financing of debt and equity.

ACKNOWLEDGEMENTS

I wish to extend my sincere gratitude and appreciation to my Board Colleagues namely, Dr. R H S Samaratunga, Mr. G K A C K Kularatne, Mr. G Gallage and Dr. B Kaluarachchi who resigned from the Board in 2010. I really appreciate the significant contribution made by them to the Bank‘s affairs, during the period they served on the Board.

I also welcome Mr. S R Attygalle, Ms. Nalini Abeywardene, Mr. Chandrasiri de Silva and Mr. K L Hewage to the Board, who will bring a wealth of experience in diverse business sectors to our midst.

I wish to thank my fellow Board members for their invaluable contribution in steering the Bank’s strategic direction and providing concentrated focus in achieving our challenging goals. Their contribution in driving the current corporate plan and their unwavering support and commitment during the year is invaluable.

I also extend my appreciation to the General Manager for his contribution as helmsman of this institution in achieving commendable results in the operations of the Bank. The unstinting support and dedication to work ethic by the Corporate, Executive Management and the staff of the Bank of Ceylon is much appreciated.

We are grateful for the sustained support and patronage of our customers and we recognise and continue to commit ourselves to deliver exemplary banking services.

The contribution made by the auditors, legal advisors, consultants, correspondents and external advisors is thankfully acknowledged. The positive role played by the trade unions in the Bank’s operations is also appreciated.

I thank His Excellency Mahinda Rajapaksa, the President who is also the Minister of Finance and Planning, Honourable Deputy Minister of Finance and Planning, the Secretary to the Ministry of Finance and Planning, the Governor of the Central Bank of Sri Lanka, the Auditor General and the Attorney General and respective officials for their guidance and support.

CHAIRMAN’S MESSAGE

CONCLUSION

I strongly believe the economic sentiment of Sri Lanka remains optimistic. In order to grasp the opportunities, we will continue to formulate strategies on innovations, skills development, customer centricity and diversification whilst paying due attention to managing risks and good governance. Having taken the initial steps to re-invent ourselves as a financial powerhouse, the Bank of Ceylon will continue to reach greater heights in the banking industry with the support and patronage of the Government of Sri Lanka, its stakeholders and well wishers.

Targeting to become a truly integrated financial services provider, the Bank of Ceylon will inspire and continue to deliver value to the Government of Sri Lanka, its customers and other stakeholders. In this regard, we have declared 2011 to be the “Year of IT enabled Customer Service Excellence”, with the intention of taking advantage of the rapidly evolving technology to provide the highest quality service to our customer base in a competitive manner.

Dr. Gamini WickramasingheChairman

Colombo24 March 2011

BANK OF CEYLON ANNUAL REPORT 2010 11

GENERAL MANAGER’S REVIEW

By any measure, 2010 was a year of spectacular results. After three years of consistently high profits in 2007, 2008 and 2009 the Bank was able to achieve a record profit, the highest in its history. The profit before tax of Rs. 10.0 billion it achieved is more than double (139%), that of last year’s and 92% above the previous highest of Rs. 5.2 billion in 2008.

Not only did the Bank achieve this record profit but it also performed well across a range of performance measures. This also follows three years of consistently good performance.

At the end of 2010, its asset base stands at Rs. 715 billion - a 33 % growth over the previous year. For three years in succession, from 2007 to 2009, it had achieved a growth of over 48%. Our asset base is by far the largest for any bank operating locally.

In 2010, our deposits rose by 28% to reach Rs. 524 billion. This is a very creditable achievement by the teams involved as this is a fiercely competitive area in local banking.

At the end of 2010, our capital adequacy stood strong at 13.7%. Our Non-performing advances stood at 3.3%.

In 2010, as in 2009, the Bank played a clearly visible role in national economic development. What makes the current performance levels spectacular is that this performance was achieved without sacrificing our commitment to being a catalyst to national economic growth and our obligations to society at large as a good corporate citizen. The range of activities and operations aimed at this was quite broad. More product and service lines supported micro level start-ups and businesses and also small and medium-sized enterprises (SMEs). Increased facilities were made available to support fisheries, animal husbandry and agriculture-related activities. Bank of Ceylon acted as a facilitator to the United Nations High Commissioner for Refugees (UNHCR) to help distribute approximately Rs. 1.5 billion as assistance to nearly 75,000 families rated as Internally Displaced Persons (IDPs). The Bank also supported many activities at a cost of Rs. 29 million under its Corporate Social Responsibility initiatives.

The Bank continued to offer a complete range of services over the largest geographical area covered by any bank operating locally. We continued to provide services in areas under served by other banks including areas undergoing post-conflict rehabilitation. In 2010 we continued to build and broaden our range of professional expertise and to maintain and raise, skills and capability levels, amongst staff.

Comprehensive coverage of all geographical areas in our services and maintaining high levels of expertise and high professional standards in all areas of activity are long-term commitments that are an integral part of our mission. The spread of the branch network and our human resources development activities reflect this commitment.

In 1948, nine years after our Bank commenced business, we opened our branch in London. In 2010 it was converted into a fully-owned subsidiary Bank of Ceylon (UK)Limited - a milestone in our presence overseas and a first-step in our plans to expand operations in Europe.

In 2010, the Bank added a fully-fledged investment arm to its operations - another milestone. The plans were laid in 2009 and in 2010, it became fully operational.

RETAIL BANKING

2010 was quite an innovative year for our retail operations. Our retail sector portfolio recorded over 47% growth.

Our online branch network - the largest on the island - is being used to increasingly better effect in our retail operations and to maintain full geographic coverage as per our strategic objectives. It is mostly through our retail operations that we addressed the needs of national economic development, providing services to support micro, small and medium enterprises and also the distribution of assistance in partnership with UNHCR. Our service excellence initiatives continued with the number of branches implementing quality circles, 5S and other such initiatives rising from 178 to 278.

Products to the retail market are frequently reviewed to take into account changes in market behaviour. A great many products were introduced to cater to changing customer needs backed by focused marketing for maximum impact. Among them were Smart Saver, BoC Infinity and Islamic Banking products. Many steps were taken to improve customer service quality, accessibility and convenience like relocating service points and packaging these new products with new features.

CORPORATE BANKING AND OFF-SHORE BANKING

In 2010, as in 2009 and before, our Bank continued to dominate the corporate banking segment. The second part of this year produced an increase in demand for credit and this division was able to make a significant contribution to the Bank’s profits. We recorded a growth exceeding 36% in our portfolio. Our close relationships and deep understanding of the customers’ requirements give us the edge over our competitors. The IT facilities that we provide are now well-utilised by our customers. Our vigilance on facilities to businesses vulnerable to the downturn in overseas markets was continued.

INTERNATIONAL

2010 was a successful year for the International Division. The most notable achievement was the completion of converting the London branch into a fully-owned subsidiary of the Bank called Bank of Ceylon (UK) Limited. This subsidiary is intended to be the gateway to enter Europe. Chennai and Male Branches reported improved performances in 2010.

The Bank continued to lead in the inward remittances market. This year remittances grew by around 20% on average.

To support its international activities the Bank continued to expand its network of foreign correspondents in many countries. At the end of 2010, this network stands at more than 800 correspondents. We continued to work at maintaining and developing relationships with other banks and financial institutions worldwide.

BANK OF CEYLON ANNUAL REPORT 201012

GENERAL MANAGER’S REVIEW

TREASURY

2010 was an exceptionally successful year for the treasury. Its contribution to the Bank’s profits was quite significant. In 2009 it operated successfully managing liquidity though that year began amidst volatility in financial markets. In 2010 it used the market conditions to its advantage.

Our treasury plays a vital role in helping key institutions with their funding and this year too our treasury succeeded in mobilising the required funding. The Bank acted as a co-arranger with HSBC to the issue of Sovereign Bonds of the Government of Sri Lanka and also played the role of Paying Agent for Sri Lanka Development Bond issues. In 2010 the Bank was able to raise US$ 285 million from foreign sources demonstrating the trust placed by foreign sources in Bank of Ceylon.

INVESTMENT BANKING

In 2010 as mentioned earlier the Bank added a fully-fledged investment arm to its operations. This newly-formed arm successfully handled the debenture issue of a state institution - the largest issue made so far by such an entity.

With this arm the Bank now has the capacity to offer, under one roof, a complete range of investment banking services such assisting in raising capital, underwriting issues, mergers and acquisitions and other investment related services.

HUMAN RESOURCES

As mentioned earlier a part of the Bank’s mission is to maintain high levels of

professional skills in Banking and to expand its range of expertise through human resource development.

To expand its range of expertise the Bank continued to deploy experts recruited from outside in the areas of finance, auditing, risk management, research, marketing, investment banking, information technology and human resources management.

To maintain, improve and expand professional skills many training opportunities were made available to staff to train both locally and overseas. More than 500 training programmes, both internal and external, were made available to the staff. More than 400 staff trained overseas. In 2010, the Bank recruited 1,274 personnel to its workforce.

The Human Resources Division implemented many improvements. Many processes underwent automation in various degrees.

INFORMATION TECHNOLOGY

In 2010 too, the Bank continued to enhance its IT capabilities. It has now become routine to report the position of our expanding online network. At the end of 2010 it stands at 309 Branches and 218 extension offices. This makes a total of 527 fully- automated service points backed by 352 ATMs in 329 locations. Services were extended to cover relatively underserved parts of the country in the North and the East.

During 2010, with the main systems now completely operational and running, we focused on the supporting systems that would add value and provide backup.

Among those focused on were the further strengthening of our disaster recovery capabilities, enhancing security features and other features that increase accessibility and convenience. The IT unit itself was strengthened by recruiting extra personnel.

In 2010 too, as in 2009, we continued to upgrade facilities and continued our training of personnel in more efficient and effective use of the IT resources now available.

THE WAY FORWARD

Primarily our target is to consolidate the present performance level so as to set this as the springboard to reach more ambitious performance levels in the future.

In our planning we have always stayed close to our core values and our plans have been built around them. Results we have obtained have further strengthened our belief that we are correct in adopting this approach. As in the past few years we shall continue to strengthen our ability to compete and expand our scope of operations. Continuing in the manner we did in 2009, we shall continue to develop human resources, develop expertise in several areas, continue investments in IT and take necessary steps to enter into new areas.

Human resources development is set to continue. This development covers the strengthening of the Human Resources Division through development of Human Resources Development (HRD) related skills and expertise, recruitment of personnel and the improvements to policies and practices. Our reviews of our policies and practices have

In 2010 we continued to build and broaden our range of professional expertise and to maintain and raise, skills and capability levels, amongst staff.

BANK OF CEYLON ANNUAL REPORT 2010 13

GENERAL MANAGER’S REVIEW

revealed areas that could be improved. One such decision is that we intend to establish a performance-based rewards culture in stages. Training and skill development activities will be continued with areas such as treasury, risk management, investments and customer service improvement receiving extra attention.

As in 2009 and 2010, the development of new areas of expertise and obtaining expertise will continue. Specialists deployed in the areas of research, internal audit, marketing, finance, information technology, investment banking, human resources development and risk management are expected to continue their work.

IT will continue as a main area of investment. We will continue to enhance our disaster recovery capability, continue to strengthen the Risk Management Division and also we intend to enhance the Asset and Liability Management Systems. The Human Resource Division will also be strengthened with IT based processes. Other investments in IT will be focused on adding value to existing products and services. IT Division is to be expanded with extra personnel.

With regard to our international operations, the Chennai and Male Branches, and Bank of Ceylon (UK) Limited are expected to expand operations.

The Bank intends to widen its scope of operations with substantial activity in the area of investment banking. With the development activity planned by the Government along with the special focus on the North and the East this investment division is expected to play a very significant role. As mentioned last year this is expected to be a new chapter in the Bank’s history.

ACKNOWLEDGEMENT

2010 was a hugely successful year for the Bank of Ceylon. The Bank kept up its work through the challenges of 2008 and 2009 staying close to the strategies and plans worked out in the last few years to achieve a strong competitive edge. This year we were able to give an indication of how this underlying strength would affect results.

This was a year where we were able to demonstrate the practical effectiveness of the strategies we are pursuing and the soundness of the core principles and values around which we built our strategies.

These results are even more satisfying when we consider that all this was achieved whilst fulfilling our obligations to national economic development.

I gratefully acknowledge the support provided by the Secretary to the Treasury, the Governor of the Central Bank of Sri Lanka, the Auditor General, the Attorney General, the Chairman of the Strategic Enterprises Management Agency and the other officials of these institutions.

Our staff, as in the years past, demonstrated their loyalty to the Bank, their dedication to maintaining high professional standards and their commitment to duty. I wish to thank them for their continuing dedication, loyalty and commitment and to thank their representatives - our trade unions - for their co-operation.

I, very gratefully acknowledge the guidance and support of the Chairman and other members of the Board of Directors. In this regard, I also gratefully acknowledge the contribution of the four subcommittees of the Board covering the areas of audit, risk management, human resources and corporate governance.

The years of investment to develop increased capability is now beginning to show its effectiveness. Through the challenges of 2008 and 2009, we maintained steady results consistently. Now with a wide range of opportunities opening up, I close this review of a spectacular 2010 looking forward, with great enthusiasm, to a very exciting and rewarding 2011.

B A C FernandoGeneral Manager

Colombo24 March 2011

BANK OF CEYLON ANNUAL REPORT 201014

BOARD OF DIRECTORS

Dr. Gamini WickramasingheChairman

Appointed as the Chairman of the Board of

Bank of Ceylon in May 2007 and reappointed in

May 2010. Serves as an Independent

Non-Executive Director.

Dr. Wickramasinghe brings to the Board

business experience in both domestic and

international markets with his extensive senior

level experience obtained in the United Kingdom

and Belgium. He was the Chairman of the

Securities and Exchange Commission of

Sri Lanka from 2006 to 2009 and the Insurance

Board of Sri Lanka from 2006 to 2008.

He is the Managing Director of Informatics

Group of Companies, one of the largest

software development houses in the country.

He is also the Chairman of Bank of Ceylon (UK)

Limited, Property Development PLC, Ceybank

Holiday Homes (Private) Limited and Koladeniya

Hydropower (Private) Limited and a Director of

Mireka Capital Land (Private) Limited and The

Lanka Hospitals Corporation PLC.

Dr. Wickramasinghe holds a Master’s Degree

in Systems Analysis from the University of

Aston, Birmingham, United Kingdom (UK)

and a Doctorate in Business Administration

(DBA) from the Manchester Metropolitan

University, UK. He is a Fellow of the Chartered

Management Institute (FCMI), UK and also of

the British Computer Society (FBCS).

S R AttygalleEx officio Director

Appointed as a Director to the Board of Bank of

Ceylon in June 2010 and serves as the

Non-Executive Ex officio Director.

Mr. Attygalle brings to the Board the

knowledge that bridges the Bank’s goals with

Government’s objectives and the experience in

financial services sector.

He was a Senior Economist of the Central Bank

of Sri Lanka for a number of years and has also

served as a Director and Acting Chairman of

National Savings Bank and a Director of Shell

Gas Lanka Limited.

He presently serves as the Director General of

the Department of Public Enterprises of the

Ministry of Finance & Planning. He is also a

Director of the Sri Lanka Ports Authority and the

Board of Investment of Sri Lanka.

Mr. Attygalle holds a Bachelor of Science (B.Sc)

Degree in Mathematics from the University of

Colombo, Sri Lanka and a Master’s Degree in

Economics from Warwick University,

United Kingdom.

Raju SivaramanDirector

Appointed as a Director to the Board of

Bank of Ceylon in January 2006 and

reappointed in June 2007 and May 2010.

Serves as an Independent Non-Executive

Director.

Counting over 30 years of experience in

architecture and management, Mr. Sivaraman

brings to the Board business experience in both

public and private sectors. He is the Associate

Consultant of Plan 3 Architects in India and the

Managing Director of Arch-Triad Consultants

(Private) Limited, an architectural consultancy

firm since 1980.

Mr. Sivaraman is the Chairman of Ceylease

Financial Services Limited and also serves as a

Director of Merchant Credit of Sri Lanka Limited

and Milco (Private) Limited. He is the Managing

Director of Ram Developers (Private) Limited.

He served as a Director of Merchant Bank of Sri

Lanka PLC, Mireka Capital Land (Private) Limited

and Property Development PLC. He served as

a Member of the National Police Commission

from 2006 to 2009 and as a Council Member

and Treasurer of the Sri Lanka Institute of

Architects over a period of six years.

Mr. Sivaraman is a Chartered Architect holding

a Master’s Degree in Architecture [M.Sc.(Arch)]

and a Fellow Member of the Sri Lanka Institute

of Architects (F.I.A.).

BANK OF CEYLON ANNUAL REPORT 2010 15

BOARD OF DIRECTORS

Ms. Nalini Abeywardene Director

Appointed as a Director to the Board of Bank of

Ceylon in May 2010. Serves as a Non-Executive

Director.

Ms. Abeywardene brings to the Board her

experience in the field of commercial law and

25 years of management experience in the

private sector tea industry. She was formerly

attached to a leading legal firm in the country.

She was a Commissioner of the Human Rights

Commission of Sri Lanka from 2006 to 2009.

She is a Member of the Board of Management

of the Galle Heritage Foundation of the Ministry

of National Heritage and Cultural Affairs and a

Director of Hotels Colombo (1963) Limited and

Mussendapotta Estates (Private) Limited.

Ms. Abeywardene is an Attorney-at-Law.

Chandrasiri de Silva Director

Appointed as a Director to the Board of Bank of

Ceylon in May 2010. Serves as a Non-Executive

Director.

Being a practicing lawyer Mr. de Silva brings

to the Board his specialised experience in law,

as well as business, insurance, etc. He was

a former Director of People’s Bank, People’s

Merchant Bank PLC and People’s Insurance

Company Limited and also a former Chairman

of People’s Travels Limited.

He is the Chairman of BOC Travels (Private)

Limited and a Director of Hotels Colombo

(1963) Limited.

Mr. de Silva is an Attorney-at-Law and holds a

Master’s Degree in International Trade Law from

the University of Wales, United Kingdom.

BANK OF CEYLON ANNUAL REPORT 201016

V. Kanagasabapathy Alternate Director

Appointed as Alternate Director to

Mr. S R Attygalle, the Ex officio Director from

July 2010. Serves as a Non-Executive Alternate

Director to the Ex officio Director on the Board.

He was serving as the Alternate Director to

former Ex officio Directors too since March 2006.

Mr. Kanagasabapathy brings to the Board his

wide experience in the public sector of over

30 years in several senior capacities such as

Director/Additional Director General of Public

Finance, Director General of Public Enterprises

and Financial Management Reform,

Co-ordinator of the Ministry of Finance &

Planning. He also served as a Director of

People’s Bank, State Mortgage & Investment

Bank and Merchant Credit of Sri Lanka Limited.

He is presently the Financial Consultant of

the Academy for Financial Studies, which is

the training arm of the Ministry of Finance &

Planning. He is a Director on the Boards of

Merchant Bank of Sri Lanka PLC, Lanka Hydraulic

Institute Limited, Hotel Developers Lanka PLC

and De La Rue Lanka Currency and Security Print

(Private) Limited. He is also the Chairman of the

Distance Learning Centre, Council Member of

The Institute of Chartered Accountants of

Sri Lanka, Member on the Board of

Management of the Postgraduate Institute of

Management and Member of the National

Salaries and Cadres Commission.

Mr. Kanagasabapathy is a Chartered Accountant

and holds a Master’s Degree in Public

Administration from Harvard University, U.S.A.

He is a Fellow Member of The Institute of

Chartered Accountants of Sri Lanka, The Institute

of Public Finance and Development Accountancy,

The Institute of Certified Management

Accountants of Sri Lanka and The Association of

Accounting Technicians of Sri Lanka.

Ms. Janaki Senanayake SiriwardaneSecretary Bank of Ceylon/Secretary to the Board

Attorney-at-Law, LLB, MBA.

K L HewageDirector

Appointed as a Director to the Board of Bank of

Ceylon in June 2010. Serves as an Independent

Non-Executive Director.

Mr. Hewage brings to the Board his experience

of over 40 years in the spheres of consultancy,

management, training, project finance,

marketing, agriculture development and

extension, planting, etc.

Mr. Hewage served as the Chairman of People’s

Merchant Bank PLC, the Chairman/Chief

Executive Officer of Janatha Fertilizer Enterprises

Limited, State Plantations Corporation, State

Printing Corporation and Provincial Road

Development Authority (Western Province).

He also served as a Member of the Board of

Directors of People’s Bank, Janatha Estates

Development Board and as the General

Manager of Sri Lanka Institute of Co-operative

Management.

He is the Chairman of Ceybank Asset

Management (Private) Limited. He also serves

as a Member of the Governing Council of the

University of Visual and Performing Arts.

He holds a Bachelor of Science (B.Sc) Degree in

Bio Science from the University of Kelaniya,

Sri Lanka and a Master's Degree in Science

(M.Sc) in Agricultural Extension from the

University of Reading, United Kingdom.

BOARD OF DIRECTORS

BANK OF CEYLON ANNUAL REPORT 2010 17

CORPORATE MANAGEMENT TEAM

B A C Fernando General Manager

Appointed General Manager in February 2007,

Mr. Fernando is a career banker with over

40 years of diversified banking experience.

He joined the Bank in early 1970. Prior to

his appointment as General Manager, from

December 2002 to February 2007, he was

Deputy General Manager in charge of the

Bank’s retail operations. He has also served

as the Assistant General Manager in charge

of Corporate Banking Operations and as the

Assistant General Manager in charge of the

Southern Province.

Mr. Fernando specialises in retail banking and

credit-including both corporate and rural,

and credit administration. His experience

ranges from operational level to managerial

level. He has contributed immensely to the

improvement of credit knowledge and credit

skills among staff through training and has

provided leadership in restructuring initiatives.

He is a Director of the Institute of Bankers

of Sri Lanka and a Trustee of Bank of Ceylon

Pension Trust Fund. He is also a Director of the

Credit Information Bureau and many of the

subsidiary companies of Bank of Ceylon.

Mr. Fernando holds a Bachelor’s Degree in Arts

from the University of Sri Lanka, Vidyodaya

Campus and a Master’s Degree in Business

Administration from the University of Colombo,

Sri Lanka. He is also a Fellow of the Institute of

Bankers of Sri Lanka.

Ms. W A Nalani Senior Deputy General Manager (Corporate & Offshore Banking)

Ms. Nalani has been a Deputy General Manager

for over 6 years and appointed as Senior

Deputy General Manager (Corporate & Offshore

Banking) in December 2008. She joined the

Bank in April 1975.

Ms. Nalani is a career banker with over 35 years’

diversified banking experience. She has been

the Head of Corporate and Offshore Banking

operations for nearly 5 years, contributing

significantly for expansion of corporate banking

activities including trade finance in the Bank.

Presently, she is steering the Project formed

for ‘5 S System’ implementation, which is

integrated with the branch reorganisation under

model branch concept.

Prior to the present position, Ms. Nalani headed

the dedicated Recovery Unit for over 3½ years

until 2006 and played a dynamic role in

reducing the bank’s non-performing assets.

As an Assistant General Manager, she headed

important provincial business units including

the Metropolitan Branch for 5 years, the largest

middle market business unit and Sabaragamuwa

Province for 3 years covering economically

important Districts of Kegalle and Ratnapura.

Specialised in credit and recovery management

she has contributed significantly for human

resources development in those areas. She was

also actively involved in the implementation of

IT solutions for trade finance activities in the

Bank. She was a co-winner of the ‘Zonta Award

for Excellence’ in banking category for the

year 2009.

She is a Non-Executive nominee Director on

the Boards of Regional Development Bank

and Merchant Bank of Sri Lanka PLC. She also

serves as an Alternate Director on the Boards of

Credit Information Bureau, Institute of Bankers

of Sri Lanka and BoC Travels (Private) Limited.

She represents Bank of Ceylon on the Board

of SriLankan Airlines. She is the Senior Vice-

President of the Association of Professional

Bankers of Sri Lanka and Committee Member

of the Alumni Organisation, University of

Colombo. She also serves as a Director on the

Committee of Rotary Club of Colombo Central.

Ms. Nalani holds a Bachelor of Arts Degree

in Economics and Bachelor of Philosophy in

Economics from the University of Colombo,

Sri Lanka. She is also a Fellow Member of the

Institute of Bankers of Sri Lanka.

BANK OF CEYLON ANNUAL REPORT 201018

K Dharmasiri Deputy General Manager (Recovery)

Mr. Dharmasiri brings a rich and diversified

banking experience both locally and abroad,

since joining the bank in 1975. He bears a First

Class Honours Degree in Commerce in 1974 and

holds a Bachelor of Philosophy in Economics in

1976 from the University of Colombo, Sri Lanka.

Since his appointment to the grade of Deputy

General Manager in 2002, he brings to bear

his extensive knowledge and expertise in

monitoring and restructuring non-performing

assets, strategic planning, corporate financial

reporting and reorganisation of branches.

Mr. Dharmasiri has made an immense

contribution in maintaining the Bank’s NPA level

below the industry average. He has also held key

positions in audit and Corporate and Offshore

Banking. He held overseas assignments as the

Country Manager at BoC branch in Male from

1997 to 2000 and Managing Director of Nepal

Bank of Ceylon Limited in Nepal, in 2002.

A Non-Executive nominee Director on the Board

of Lanka Securities (Private) Limited and BOC

Management and Support Services (Private)

Limited. He also served as a Non-Executive

nominee Director on the Boards of Janashakthi

Insurance Company Limited, Ceybank Holiday

Homes (Private) Limited, Hotels Colombo (1963)

Limited, BOC Property Development (Private)

Limited, BOC Travels (Private) Limited, Mireka

Capital Land (Private) Limited, BOC Property

Development & Management (Private) Limited

and Sabaragamuwa Development Bank.

He is also an Associate Member of the Institute

of Bankers of Sri Lanka.

Ms. Kumudiniy Kulathunga Deputy General Manager (Retail Banking)

Joining the Bank in 1975, Ms. Kulathunga took

on the new role of Deputy General Manager

(Retail Banking) in April 2010.

Counting over 36 years’ experience in

banking and since her appointment to the

grade of Deputy General Manager in 2004,

Ms. Kulathunga has played a dynamic role

in various positions in the Bank including

branch operations, retail lending, supplies &

procurement and construction of new branches

in addition to training and Human Resources.

She has wide knowledge and expertise in

leading the teams in the Eastern, North Western

and Western Provinces as Assistant General

Manager in charge prior to her appointment as

Head of Human Resources. She played a major

role in implementing the present Performance

Potential Appraisal System, formulating the

transfer policy and promotion policies in the

Bank, and initiating procedures for productivity

improvements and cost reduction.

She is a Non-Executive nominee Director on

the Boards of Institute of Bankers of Sri Lanka

since 2002 and BOC Travels (Private) Limited

since 2010. She was a Non-Executive nominee

Director on the Boards of Hotels Colombo

(1963) Limited from 2006 to 2009, BOC

Property Development & Management Limited

from 2004 to 2006 and also Alternate Director

on the Boards of Property Development Limited

from 2006 to 2008 and Mireka Capital Land

(Private) Limited in 2007.

Having graduated from the University of

Colombo, Sri Lanka Ms. Kulathunga holds

a Special Bachelor’s Degree in Arts in 1972

and Bachelor of Philosophy Honours Degree

in 1973. A Fellow Member of the Institute of

Bankers of Sri Lanka, she obtained a Diploma in

Bank Management from the Institute of Bankers

of Sri Lanka in 1989, in addition to being a

Diploma Holder in Personnel Management from

the Institute of Personnel Management in 1997.

CORPORATE MANAGEMENT TEAM

BANK OF CEYLON ANNUAL REPORT 2010 19

C Samarasinghe Deputy General Manager (Product & Development Banking)

Joining the Bank in 1975, Mr. Samarasinghe

was appointed to the post of Deputy General

Manager (Product & Development Banking) in

May 2006. He holds a Bachelor's Degree in Arts

(Special) with a 2nd Class from the University

of Colombo, Sri Lanka in 1975 and also holds a

Bachelor of Philosophy in Economics from the

University of Colombo, Sri Lanka in 1976.

In his current position he leads the Development

Banking activity, spearheading the card

business, electronic delivery channels,

Microfinance, Project Finance, SME lending, BoC

Assurance and Islamic Banking arm. Prior to

the assignment to the grade of Deputy General

Manager, Mr. Samarasinghe was instrumental in

establishing a large financial house based in the

Middle East and played a key role in introducing

organisational and structural changes in the

face of the changing business environment. He

has also served in Support Services, Recovery,

Sales & Channel Management and Credit Cards.

He is the Non-Executive Chairman on the

Board of Transnational Lanka Record Solutions

(Private) Limited since 2006 and serves as a

Non-Executive Director on the Board of Ceybank

Holiday Homes (Private) Limited since 2010.

A member of the Bankers Technical Assistance

Committee since 2007, he also served as a

Director on the Board of Merchant Credit of

Sri Lanka from 2006 to 2008.

H M A B Weerasekara Deputy General Manager (International & Treasury)

Appointed Deputy General Manager

(International & Treasury) in July 2006,

Mr. Weerasekara joined the Bank in May

1975, having graduated from the University

of Colombo, Sri Lanka in Economics in 1972.

Additionally, he holds a Bachelor of Philosophy

in Industrial Management in 1974 from the

same University.

His exposure to both the domestic and

international arena has contributed significantly

to sustain BoCs leadership position in treasury

and international operations. He has extensive

experience in trade finance, treasury operations,

offshore banking, international, retail banking

and investment banking. Mr. Weerasekara led

the Recovery Division of the Bank in 2006.

Prior to the assignment to the grade of Deputy

General Manager in 2006, he served in the

London Branch and was successful in enhancing

inward remittances and treasury activities of the

Bank. He played a pivotal role in subsidiarisation

of the BoC Branch in London and expansion of

the correspondent banking network.

He is a Non-Executive nominee Director on the

Board of Merchant Credit of Sri Lanka (Private)

Limited (MCSL) since 2006 and serves as the

Chairman of both the Audit & Risk Management

Committees of MCSL.

CORPORATE MANAGEMENT TEAM

Ms. Deepa WanniaratchiDeputy General Manager (Finance & Planning)

Ms. Deepa Wanniaratchi joined the Bank in

May 1975. She holds a Bachelor’s Degree in

Commerce from the University of Peradeniya,

Sri Lanka obtained in 1974. In 2004, she

obtained a Postgraduate Diploma in Business

& Financial Administration from The Institute

of Chartered Accountants of Sri Lanka in

association with the Cranfield University School

of Management, UK. Appointed Deputy General

Manager (Finance & Planning) in April 2008.

She has wide experience in diverse fields such

as managing large technology projects, bank

restructuring under financial sector reforms and

Corporate & Retail Banking activities. Prior to

the present assignment, she provided leadership

in the restructuring project, designed to

implement the core banking system island-wide.

She has imparted her knowledge by conducting

extensive training courses in corporate and sales

related areas.

She is a Non-Executive nominee Director on

the Board of BOC Travels (Private) Limited since

December 2008 and served as a Non-Executive

nominee Director on the Board of Property

Development & Management Limited from

2006 to 2008. She is also a Trustee of the

Pension Trust Fund and the Humanitarian Trust

Fund of the Bank.

She is an Associate Member of the Institute of

Bankers of Sri Lanka.

BANK OF CEYLON ANNUAL REPORT 201020

M K Nandasiri Deputy General Manager (Support Services)

Having obtained a First Class Honours in

Economics from the University of Colombo,

Sri Lanka in 1974 together with a Bachelor of

Philosophy in Economics in 1975, Mr. Nandasiri

entered the Bank in 1975. He holds the position

of Deputy General Manager (Support Services)

since May 2009.

His experience in both domestic and

international banking operations has taken

through management and leadership roles in

the branch network. He has served in Corporate

Branch in various positions of which the period

he served in Corporate Imports was more

important. He played a leading role to improve

the department and was the team leader in

implementation of new Computer Package.

Specialised in Trade Finance and Credit fields,

he has contributed a lot in training staff in that

area. He served as Country Manager of the BoC

branch in Chennai from 2005 to 2008. He was

the Assistant General Manager (Pettah) prior to

taking up the appointment of Deputy General

Manager (Support Services).

A Non-Executive nominee Director on the Board

of Grand Oriental Hotel since September 2009,

Mr. Nandasiri is also the President of the Trade

Finance Association of Bankers of Sri Lanka since

April 2010.

He is an Associate Member of the Institute of

Bankers of Sri Lanka.

H M MudiyanseDeputy General Manager (Human Resource)

Mr. Mudiyanse joined the Bank in August 1973

and was appointed as Deputy General Manager

(Human Resource) in October 2010.

His extensive experience in retail banking is held in

good stead for managing and developing human

resources in his present position. Demonstrating

a remarkable leadership role due to his expertise

in microfinance, retail banking and agriculture

sectors, he was able to propel BoC to a higher

plane in the North Western Province.

He has been a Non-Executive Director on the

Board of Ceybank Holiday Homes (Private)

Limited and an Alternate Director of The Institute

of Bankers of Sri Lanka since October 2010.

Mr. Mudiyanse also served as a Non-Executive

Director on the Boards of Wayamba Chamber

of Commerce, Industrial Service Bureau and the

Wayamba Development Bank from 2007 to 2010.

Mr. Mudiyanse, an Associate Member of the

Institute of Bankers of Sri Lanka and obtained

a Postgraduate Diploma in Executive Bank

Management from the same institute in 2001.

P A Lionel Deputy General Manager (Investment Banking)

Appointed as Deputy General Manager

(Investment Banking) in October 2010. Mr. Lionel

joined the Bank in December 1983.

Counting over 27 years’ experience in banking

and financial services, Mr. Lionel has specialised

in the areas of treasury, international operations

and investments. He has been involved in

managing liquidity, assets and liabilities, fund-

raising activities, risk management in relation to

treasury and cross border funding. Additionally,

he has a flair for developing and marketing

treasury products. He held the position of CEO of

the Primary Dealer Unit of the Bank and headed

the Treasury and Investment Unit. He received

broad exposure and extensive training in Treasury

Management and Dealing Activities in London

from 1988 to 1989. He served as Head of

Treasury at the BoC Branch in Karachi.

He is a Non-Executive Director on the Board of

Lanka Hospitals (Private) Limited since 2010,

Property Development (Private) Limited since

2009 and Primary Dealer Association since 2007.

He is also an Alternate Director of Ceybank

Unit Trust since 2006 and the Vice-President of

Sri Lanka Forex Association since 2008.

Mr. Lionel obtained his Bachelor of Arts Degree

from the University of Colombo, Sri Lanka in 1980.

CORPORATE MANAGEMENT TEAM

BANK OF CEYLON ANNUAL REPORT 2010 21

D M Gunasekara Deputy General Manager (Sales & Channel Management)

Appointed as Deputy General Manager

(Sales & Channel Management) in October

2010. Mr. Gunasekara joined the Bank having

graduated from the University of Colombo,

Sri Lanka with a Special Degree in Public Finance

& Taxation in 1981.

Commencing his career with retail banking,

Mr. Gunasekara has amassed a wealth of

knowledge and experience in all aspects of credit

management and administration. His recent

stint in Corporate and Offshore Banking has

seen the growth and expansion of this segment

significantly. Serving at the BoC London Branch

from 1997 to 2000, he obtained comprehensive

experience in international banking operations.

As an Associate Faculty Member of the Banks'

Training Institute, Mr. Gunasekara has readily

responded to uplifting the knowledge of our staff.

He is a Non-Executive nominee Director on the

Board of Ceybank Asset Management (Private)

Limited since August 2010 and Ceybank Holiday

Homes (Private) Limited since June 2009. He

served as a Non-Executive nominee Director on

the Board of Merchant Credit of Sri Lanka from

2008 to 2009.

He is an Associate Member of the Institute of

Bankers of Sri Lanka.

CORPORATE MANAGEMENT TEAM

M K Muthukumar Chief Legal Officer

Attorney-at-Law, Mr. Muthukumar, a lawyer since

July 1975, was appointed as Chief Legal Officer

in September 2010. He joined Bank of Ceylon in

1992.

Counting over 19 years of experience in legal

affairs at the Bank, Mr. Muthukumar, served as

a Senior Legal Officer (Recovery) from January

1998 to October 2003 and as a Deputy Chief

Legal Officer (Recovery) from November 2003

to August 2010. He is a visiting lecturer on

Commercial and Banking Law at the Central

Bank Training Institute, Chartered Institute of

Management Accountants and Institute of

Bankers of Sri Lanka since 1996. He is also the

Chief Examiner for Laws relating to Financial

Services at the Institute of Bankers of Sri Lanka

since 2000.

He is also a Non-Executive nominee Director on

the Board of BOC Travels (Private) Limited since

2005 and serves as a Trustee of the Bank of

Ceylon Provident Fund since September 2010.

Ms. Janaki Senanayake Siriwardane Secretary to the Board/Secretary, Bank of Ceylon

Ms. Siriwardane, joined the Bank in January

1996 as its Assistant Secretary to the Board

and was appointed as Secretary to the Board/

Secretary, Bank of Ceylon in December

2005. She also serves as Secretary to all the

subcommittees of the Board.

She is an Attorney-at-Law by profession and was

a practicing lawyer. She also holds a Bachelor’s

Degree in Law and a MBA from the University of

Colombo, Sri Lanka.

Prior to joining the Bank, Ms. Siriwardane

was employed in the private sector handling

company secretarial work. She was also a visiting

lecturer, examiner and moderator on Commercial

and Industrial Law at the Industrial Management

Department of the University of Kelaniya,

Sri Lanka. She was a Non-Executive nominee

Director on the Board of Ceybank Holiday Homes

(Private) Limited up to September 2010.

She is also the Company Secretary for some of

the Subsidiaries of the Bank.

BANK OF CEYLON ANNUAL REPORT 201022

W A Asoka Rupasinghe Chief Financial Officer

Appointed as Chief Financial Officer in October

2009. Graduating from the University of

Sri Jayawardenapura, Sri Lanka, Mr. Rupasinghe

holds a Special Degree in Business

Administration in 1991 and a MBA in Finance

from the University of Southern Queensland,

Australia in 2007.

With over 24 years of experience in finance,

14 of which is in the financial services industry,

Mr. Rupasinghe has exposure in mergers and

acquisitions, cross border listing, cross border

fund raising through Euro Medium Term Notes

(EMTN) & Global Depository Receipts (GDRs)

programmes, in addition to specialisation in

group performance management. He had

been a resource person in several educational

institutions including The Institute of Chartered

Accountants of Sri Lanka and the University of

Sri Jayawardenapura.

Prior to joining Bank of Ceylon, he worked

as Head of Corporate Financial Affairs at

Commercial Bank of Qatar and Head of Finance

and Administration at Securities & Exchange

Commission of Sri Lanka.

A Non-Executive nominee Director of Ceylease

Financial Services Limited since March 2010,

Mr. Rupasinghe is also a Fellow Member of The

Institute of Chartered Accountants of Sri Lanka.

Trevine Fernandopulle Chief Risk Officer

Graduated from Imperial College, London with

a Bachelor of Science in 1977 in addition to a

Master’s degree in Statistics from the London

School of Economics in 1978, Mr. Fernandopulle

joined the Bank as the Chief Risk Officer in May

2009 after retirement from the services of HSBC

as Deputy CEO Sri Lanka.

In a Banking career spanning 30 years, he

has specialised in Corporate Banking and Risk

Management whilst acquiring wide experience

in all aspects of commercial banking including

treasury, corporate, retail and international

trade. He was seconded to the Saudi British

Bank an associate of HSBC Holdings PLC,

UK, as Manager Corporate Banking Eastern

Province Saudi Arabia and was responsible for

restructuring the Credit Control and Credit Risk

Departments.

He played a pivotal role in the successful issue of

the debut sovereign bond for US$ 500 million

for the Government of Sri Lanka in 2007.

Mr. Fernandopulle is a Trustee of Joseph Fraser

Memorial Hospital since 2010, President of

Sri Lanka Branch of the Chartered Institute of

Bankers, London since 2009 and a Fellow of the

Chartered Institute of Bankers, London.

CORPORATE MANAGEMENT TEAM

BANK OF CEYLON ANNUAL REPORT 2010 23

Dr. W G KarunadasaChief Internal Auditor

Appointed as the Chief Internal Auditor of the

Bank of Ceylon in March 2009.

With over 30 years of experience in the

fields of accounting, auditing and financial

management, Dr. Karunadasa oversees the

internal audit function of the Bank.

Prior to enlisting at BoC, he headed the Internal

Audit Department of HDFC Bank and Veytex

(Private) Limited. He served on the Board

of Directors/Corporate Management of The

Finance Company PLC from 1988 to 2001.

Dr. Karunadasa holds a Master’s Degree in

Business Administration from the University of

Sri Jayawardenapura, Sri Lanka in 1996 and

obtained a Doctorate in Business Administration

from the Irish International University (EU)

in 2005.

He is also a Fellow Member of The Institute of

Chartered Accountants of Sri Lanka and also a

Fellow Member of the Certified Management

Accountants of Sri Lanka.

Rohan PeirisHead of Information Technology

Joined the Bank of Ceylon in February 2009, as

the Head of Information Technology, from his

previous position at DFCC Vardhana Bank.

Mr. Peiris holds a Master’s Degree in

Information Technology from Keele University,

UK in 2002.

Counting over 28 years’ experience in the

fields of Data Processing and Information and

Communication Technology, he is specialised in

software development and project management

and pioneering in facilities management.

He also served at Pan Asia Bank and Merchant

Bank of Sri Lanka. He was appointed as the

National Consultant on IT Projects funded

by United Nations Industrial Development

Organisation (UNIDO) in 1990 and served in

many committees of national interest. He is also

Information Technology Infrastructure Library

(ITIL) certified.

Additionally, he holds a Diploma in Systems

Analysis/Design. Mr. Peiris has membership

in the Computer Society of Sri Lanka, British

Computer Society, Institute of Electrical &

Electronic Engineers and Project Management

Institute and is also a Chartered Information

Technology Professional.

CORPORATE MANAGEMENT TEAM

BANK OF CEYLON ANNUAL REPORT 201024

Dr. Lionel SiriwardenaHead of Research & Development

Appointed as Head of Research and Development

of the Bank of Ceylon in August 2009.

Dr. Siriwardena has over 21 years’ experience

in the banking sector handling macroeconomic

research, financial performance analysis

and forecasting. He has special exposure on

business process re-engineering, productivity

management, organisational restructuring and

customer care.

Prior to his appointment as Head of Research

and Development in Bank of Ceylon, he

served at the United Nations Development

Programme (UNDP) Regional Centre for Asia

Pacific Region as a Senior Researcher from

2005 to 2009 and Research Director at the

People’s Bank from 1991 to 2004. He was

also a Research Consultant for UNDP Maldives,

Lao PDR and Sri Lanka from 2008 to 2009,

Regional Researcher for microfinance and rural

development at the Asia Pacific Rural Agricultural

Credit Association (APRACA) from 2001 to

2004, the editor of Economic Review from

1991 to 2004, visiting lecturer at the University

of Colombo from 1995 to 1997 and Visiting

Research Fellow at the University of Burgen,

Norway and the University of Wageningen, the

Netherlands from 1979 to 1980.

Dr. Siriwardena holds a Master of Arts Degree

in Economics from the University of Kelaniya,

Sri Lanka in 1980 and obtained a Doctorate

in Social Sciences from the University of

Wageningen, the Netherlands in 1989.

M F GhaffoorHead of Marketing

Appointed as the Head of Marketing of the

Bank of Ceylon in January 2010.

In his current role he has responsibility for the

Banks’ CSR programmes.

Mr. Ghaffoor joined the Bank of Ceylon having

previously been with British American Tobacco

in East Africa, Pakistan and Iran from 2001

to 2008, as Marketing Director in each of

the Group’s subsidiaries. Prior to his overseas

secondments, he served in many roles at

Ceylon Tobacco Company before heading up its

Marketing Division in 1997.

During his tenure at British American Tobacco,

he acquired a thorough knowledge of Strategic

Planning, Product Development, Brand Planning

& Development, Supply Chain & Logistics and

Consumer Touch Point Management. His flair

for brand rejuvenation helped to secure market

leadership for British American Tobacco in

Pakistan.

Additionally, Mr. Ghaffoor served as General

Manager of Whittals Insurance and Country

Manager of DHL Sri Lanka from 1993 to 1996

during his tenure with John Keells Holdings.

CORPORATE MANAGEMENT TEAM

1 Country…9 Provinces…

307 Branches… 1 Bank…Bank of Ceylon

1 Bank…on the ground in hundreds of towns, villages andhamlets across the country…1 Bank…BOC

BANK OF CEYLON ANNUAL REPORT 201026

EXECUTIVE MANAGEMENT TEAM

01 Ms. B D C WijekulasuriyaAGM - Product & Development Banking

02 Ms. Y A M M P KarunadharmaAGM - Metropolitan Branch

03 Ms. S W S FernandoAGM - Province Sales Management

04 Ms. K M AmarasuriyaAGM - Recovery (Provinces)

09 Ms. Sriyani AnandagodaAGM - Trade Finance

10 D L C AtapattuAGM - Central Province

11 H K W GunasingheAGM - Sabaragamuwa Province

12 Ms. K A D A PemadasaAGM - Administrative Services

17 W P R P H FonsekaAGM - Budget & Strategic Planning

18 I G C MadadeniyaAGM - Country Manager - London

19 T MutugalaAGM - Information System Audit

20 M WickramasingheAGM - Human Resource Operations

01 02 03 04

09 10 11 12

17 18 19 20

BANK OF CEYLON ANNUAL REPORT 2010 27

EXECUTIVE MANAGEMENT TEAM

05 Ms. R G V S GunatilakeAGM - Credit Audit

06 Ms. W K I KularatneAGM - Western Province North

07 Ms. K A D FernandoAGM - Offshore Banking

08 P J JayasingheAGM - Corporate Credit

13 Ms. P R UnawatunaAGM - Branch Credit

14 Ms. L W WijesundaraRecovery Corporate

15 K B S BandaraAGM - Corporate Relations

16 D N J CostaAGM - North Central Province

21 Ms. L S L de S WijeyeratneAGM - Pettah Branch

22 D N L FernandoAGM - Western Province South

23 K T KarunaratneAGM - Support Services

24 D M L C KumaraAGM - Country Manager - Male

05 06 07 08

13 14 15 16

21 22 23 24

BANK OF CEYLON ANNUAL REPORT 201028

EXECUTIVE MANAGEMENT TEAM

25 T M SafaAGM - Country Manager – Chennai

26 S S S SenanayakeAGM - Province & Branch Audit/Investigations

27 W G AriyaratneAGM - International

28 G H ChandrasiriAGM - Business Process Re-Engineering Project

33 C W WelagederaAGM - Eastern Province

34 D P K GunasekeraAGM - Overseas Branches

35 K E D SumanasiriAGM - Northern Province

36 W M S WanasingheAGM - BoC Card Centre

41 Ms. H M RatnayakeAGM - Accounting & MIS

42 Ms. C K JayarathneAGM - Customer Relations

43 T P G RanaweeraAGM - Consumer Product Management

44 K G JinadasaDeputy Chief Legal Officer (Operations)

25 26 27 28

33 34 35 36

41 42 43 44

BANK OF CEYLON ANNUAL REPORT 2010 29

EXECUTIVE MANAGEMENT TEAM

29 M L J FernandoAGM - Risk Management & Compliance

30 G L P JinasomaAGM - Uva Province

31 S M S C JayasuriyaAGM - Treasury

32 G D SilvaAGM - Training & Development

37 D K N PiyasomaAGM - Southern Province

38 E M U BandaraAGM - North Western Province

39 H G NihalAGM - Superannuation Schemes

40 Ms. S S EkanayakeAGM - Marketing

45 Ms. S H RanawakaDeputy Chief Legal Officer (Recovery)

46 H R F FonsekaAssistant Director IT (Operations/Tech. Support)

47 Jagath KurundukumburaAssistant Director IT (Operations/Tech. Support)

29 30 31 32

37 38 39 40

45 46 47

BANK OF CEYLON ANNUAL REPORT 201030

MANAGEMENT DISCUSSION AND ANALYSIS

ABOUT THE BANK

The Bank of Ceylon (BoC) is the premier State owned commercial bank in Sri Lanka.

It provides diversified fully-fledged banking services including Retail, Corporate, International, Treasury, Development/Investment Banking Services, Credit Cards, Islamic Banking, Safe Deposit, Custodian and Pawn Broking Services through a network of 307 local and 2 overseas branches (Male and Chennai).

The Bank is subject to examination and regulation of the Central Bank of Sri Lanka and subject to listing rules of the Colombo Stock Exchange by virtue of its listed debenture. The overseas branches are subject to Banking Regulations prevalent in the respective countries.

The stability and strength of the Bank is affirmed by the AA (lka) rating with a positive outlook bestowed by Fitch Ratings Lanka Limited.