bahrain food & drink report 2011

DESCRIPTION

Bahrain Food & Drink Report Q1 2011TRANSCRIPT

Q1 2011www.businessmonitor.com

food & drink report

iSSn 1749-2599published by Business Monitor international Ltd.

BAHrAin INCLUDES 5-YEAR FORECASTS TO 2014

Business Monitor International Mermaid House, 2 Puddle Dock, London, EC4V 3DS, UK Tel: +44 (0) 20 7248 0468 Fax: +44 (0) 20 7248 0467 Email: [email protected] Web: http://www.businessmonitor.com

© 2011 Business Monitor International. All rights reserved. All information contained in this publication is copyrighted in the name of Business Monitor International, and as such no part of this publication may be reproduced, repackaged, redistributed, resold in whole or in any part, or used in any form or by any means graphic, electronic or mechanical, including photocopying, recording, taping, or by information storage or retrieval, or by any other means, without the express written consent of the publisher.

DISCLAIMER All information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time of publishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business Monitor International accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of the publication. All information is provided without warranty, and Business Monitor International makes no representation of warranty of any kind as to the accuracy or completeness of any information hereto contained.

BAHRAIN FOOD & DRINK REPORT Q1 2011 INCLUDING 5-YEAR INDUSTRY FORECASTS BY BMI

Part of BMI’s Industry Report & Forecasts Series

Published by: Business Monitor International

Copy deadline: October 2010

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 2

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 3

CONTENTS

BMI Industry View ............................................................................................................................................ 5

SWOT Analysis ........................................................................................................................................................................................................... 7 Bahrain Food Industry SWOT ............................................................................................................................................................................... 7 Bahrain Drinks Industry SWOT ............................................................................................................................................................................. 8 Bahrain Mass Grocery Retail SWOT ..................................................................................................................................................................... 9

Business Environment .................................................................................................................................. 10

BMI’s Core Global Industry Views ........................................................................................................................................................................... 10 BMI Food & Drink Core Views ........................................................................................................................................................................... 11

Middle East Food & Drink Business Environment Ratings ...................................................................................................................................... 12 Regional Food & Drink Business Environment Ratings ...................................................................................................................................... 14

Bahrain’s Food & Drink Business Environment Rating ........................................................................................................................................... 15 Macroeconomic Outlook ........................................................................................................................................................................................... 16

Table: Bahrain – Economic Activity .................................................................................................................................................................... 19

Industry Forecast Scenario ........................................................................................................................... 20

Consumer Outlook .................................................................................................................................................................................................... 20 Food.......................................................................................................................................................................................................................... 22

Food Consumption ............................................................................................................................................................................................... 22 Table: Food Consumption Indicators - Historical Data & Forecasts .................................................................................................................. 23 Trade ................................................................................................................................................................................................................... 23 Table: Bahrain Sectoral Trade Balance - Historical Data & Forecasts .............................................................................................................. 24

Drink ......................................................................................................................................................................................................................... 24 Soft Drinks ........................................................................................................................................................................................................... 24 Table: Drinks indicators ...................................................................................................................................................................................... 25

Mass Grocery Retail ................................................................................................................................................................................................. 25 Table: Bahrain Mass Grocery Retail Sales - Value by Format - Historical Data & Forecasts ........................................................................... 26 Table: Bahrain Grocery Retail Sales By Format, 2009 & 2019........................................................................................................................... 27

Food ................................................................................................................................................................. 28

Key Industry Trends and Developments .................................................................................................................................................................... 28 Increasing Interest In Processed Foods ............................................................................................................................................................... 28 Continued Government Investment ...................................................................................................................................................................... 28 Growing Investment Interest From Non-Regional MNCs .................................................................................................................................... 29

Market Overview ...................................................................................................................................................................................................... 30 Agriculture ........................................................................................................................................................................................................... 30 Key Food Processors ........................................................................................................................................................................................... 30 Halal Food ........................................................................................................................................................................................................... 31 Table: Muslim Populations In Selected Middle East & Africa Countries, 2009 .................................................................................................. 32

Drink ................................................................................................................................................................ 33

Key Industry Trends and Developments .................................................................................................................................................................... 33 Carbonates Still Strong ........................................................................................................................................................................................ 33 Diversifying Towards New Product Categories ................................................................................................................................................... 33

Market Overview ...................................................................................................................................................................................................... 34 Soft Drinks ........................................................................................................................................................................................................... 34 Alcoholic Drinks .................................................................................................................................................................................................. 35 Hot Drinks ........................................................................................................................................................................................................... 35

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 4

Mass Grocery Retail ....................................................................................................................................... 36

Key Industry Trends and Developments .................................................................................................................................................................... 36 Growing Investment In Convenience Retailing .................................................................................................................................................... 36 Catching the Eye of Foreign Investors ................................................................................................................................................................. 36

Market Overview ...................................................................................................................................................................................................... 37 Table: Structure Of Bahrain’s MGR Market – Number Of Outlets, 2004-2009 ................................................................................................... 38 Table: Structure Of Bahrain’s MGR Market – Sales By Retail Format, 2004-2009 (US$mn) ............................................................................. 38 Table: Structure Of Bahrain’s MGR Market – Sales By Retail Format, 2004-2009 (BHDbn) ............................................................................. 38 Table: Value Of Sales Per Outlet, 2008e ............................................................................................................................................................. 38

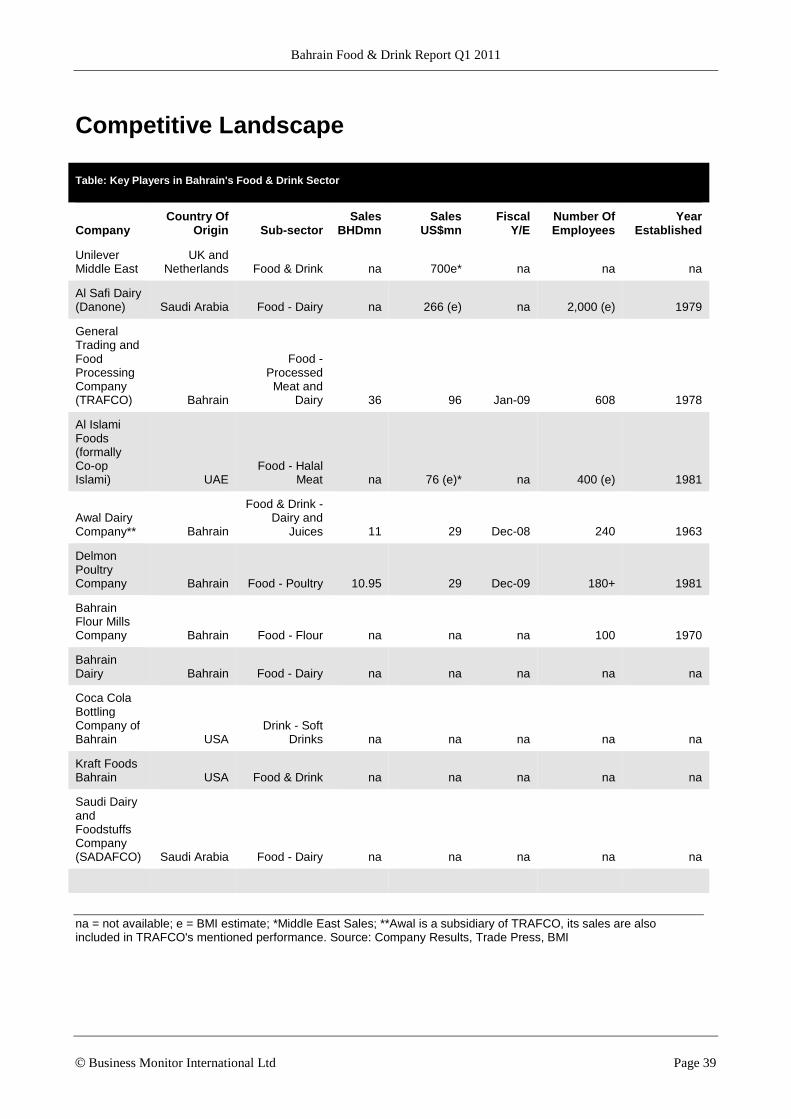

Competitive Landscape ................................................................................................................................. 39

Table: Key Players in Bahrain's Food & Drink Sector ........................................................................................................................................ 39 Table: Bahrain’s MGR Key Players .................................................................................................................................................................... 40

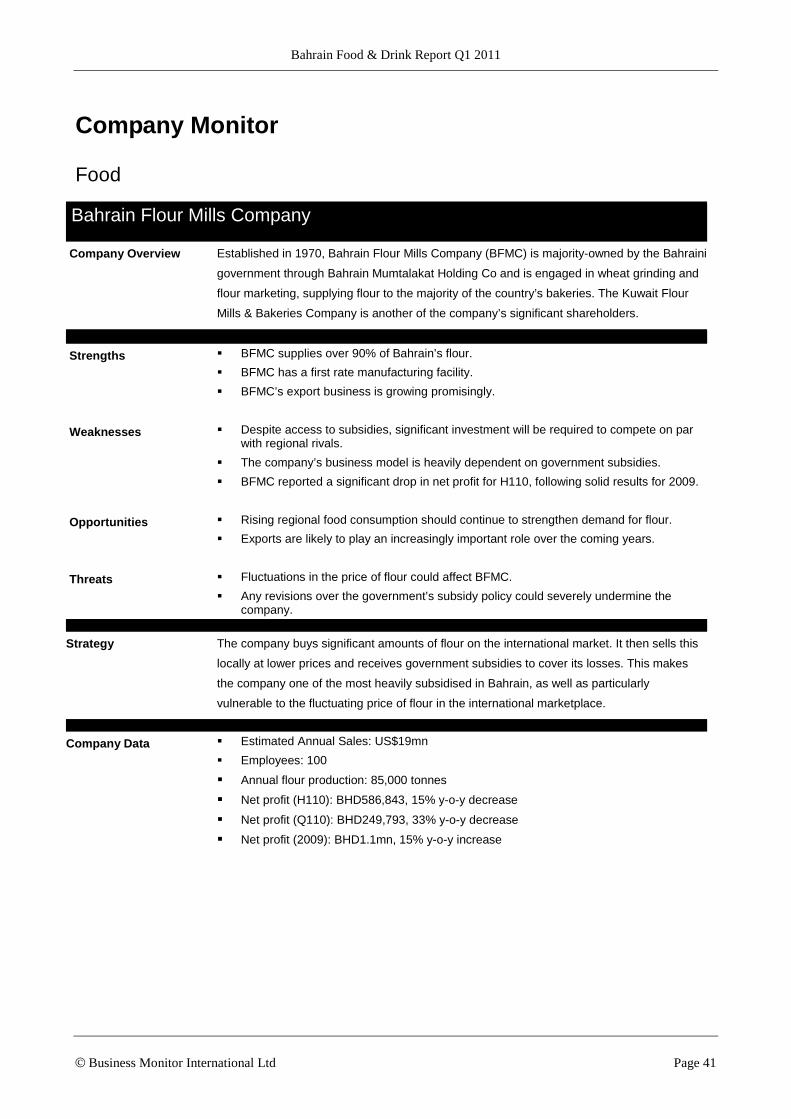

Company Monitor ........................................................................................................................................... 41

Food.......................................................................................................................................................................................................................... 41 Bahrain Flour Mills Company ............................................................................................................................................................................. 41 General Trading And Food Processing Company (TRAFCO) ............................................................................................................................. 42 Kraft Foods MEA ................................................................................................................................................................................................. 43 Delmon Poultry Company .................................................................................................................................................................................... 44

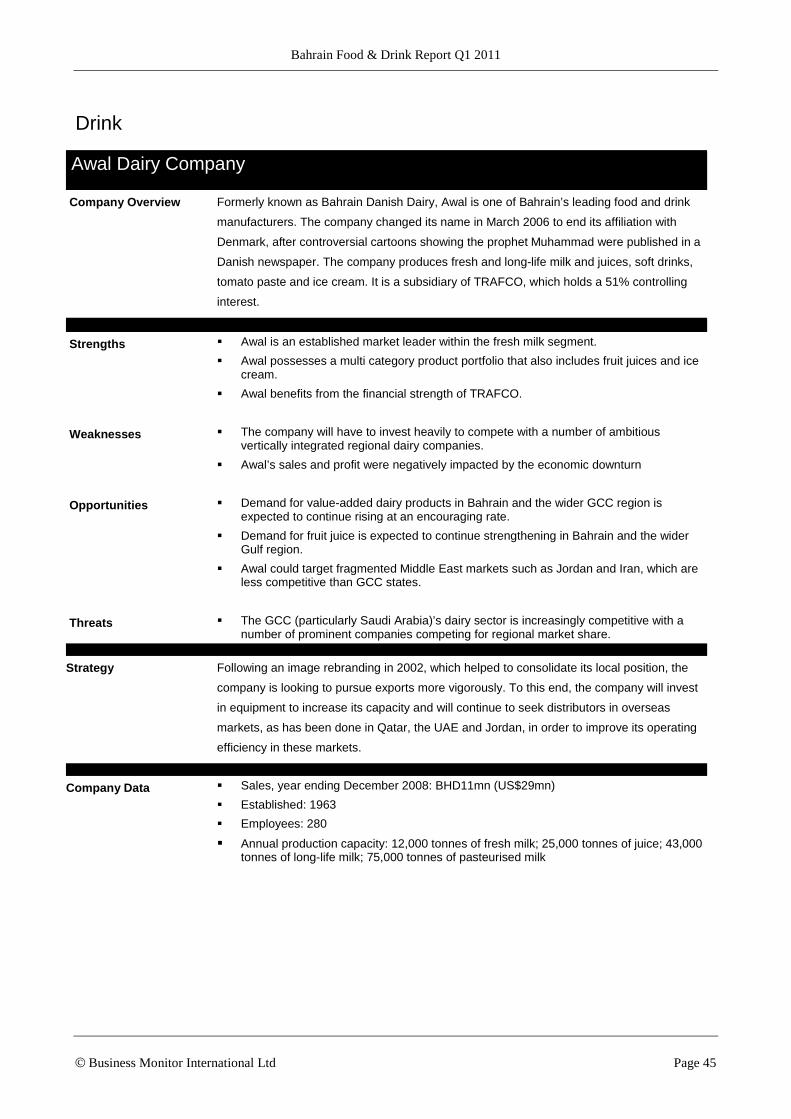

Drink ......................................................................................................................................................................................................................... 45 Awal Dairy Company ........................................................................................................................................................................................... 45

Mass Grocery Retail ................................................................................................................................................................................................. 46 EMKE Group ....................................................................................................................................................................................................... 46 Fu-Com International/Géant ............................................................................................................................................................................... 47 Carrefour MAF .................................................................................................................................................................................................... 48

BMI Methodology ........................................................................................................................................... 49

Food & Drink Business Environment Ratings .......................................................................................................................................................... 49 Table: Returns ..................................................................................................................................................................................................... 50 Table: Risks ......................................................................................................................................................................................................... 51

Weighting .................................................................................................................................................................................................................. 51 Table: Weightings ................................................................................................................................................................................................ 52

BMI Food & Drink Industry Glossary ...................................................................................................................................................................... 53 Mass Grocery Retail ............................................................................................................................................................................................ 53

BMI Food & Drink Forecasting And Sourcing ......................................................................................................................................................... 55 How We Generate Our Industry Forecasts .......................................................................................................................................................... 55 Sourcing ............................................................................................................................................................................................................... 56

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 5

BMI Industry View

The Bahraini economy does appear to be showing signs of improvement, although we do not see what

will drive the recovery beyond government spending. As such, our forecasts are somewhat conservative.

However, despite the subdued outlook for the economy, the food and drink industry continues to illustrate

considerable potential, as it is far from maturity. For most residents, personal wealth growth is likely to

remain subdued throughout the forecast period, with a concomitant effect on retail sales. Falling

property and stock prices will have damaged savings, not to mention consumer confidence, and will add

to the effect of job losses and pay cuts. However, while BMI estimates that consumer spending in 2009

was flat, we expect a rebound to 5.0% growth in 2010 and 6.0% in 2011.

Key Company Trends

Online Grocery Shopping Debut – In August 2010, Bahrain’s first virtual supermarket was launched.

Called Cart, the company has started a new grocery shopping website (cart.com.bh) in Bahrain. The

website helps the company to deliver food orders directly to shoppers' doorsteps, with the site having

received about 250,000 visitors since its launch in July 2010, making it the seventh most visited website

in the country, according to visitor tracking website Alexa Rank. Project Development Co-Ordinator

Ebrahim Haroon said the retailer aims to deliver 100 orders per day in three months. Haroon added that

the company is also looking to expand its service outside of Bahrain. The initial success of Cart reflects

the growing importance of convenience in consumers’ shopping decisions, particularly with increasingly

modern lifestyles and longer working hours.

Investments By Local Player – In October 2010, local retail operator BMMI announced its plans to

launch a major retail expansion in Bahrain. The retailer said that it plans to have opened five large

supermarkets as well as five neighbourhood stores in the country within five years. The first large

supermarket will be opened shortly in Amwaj under the Alosra banner. The Alosra supermarket chain

specialises in sourcing Western brands and specialty products, and the company plans on also carrying

prepared salads, sandwiches and sushi which will be offered as both take-away and at the in-store cafes,

as BMMI looks to target high-spending and health-conscious consumers who value quality and

convenience.

Key Risks To Outlook

National Debt Growing – Bahrain has already doubled its national debt (to 25% of GDP) and earned itself

a ratings downgrade by Moody's. Any problems in the financial industry could further delay a private-

sector recovery and derail investor and consumer confidence, leaving the government in charge of

growth, which is all well and good as long as oil prices stay high. However, as Moody's pointed out

recently, the breakeven price has been getting higher and higher. We estimate Bahrain needs an average

oil price of US$72/bbl just to balance its books, with anything lower than that likely to entail deficits and

further borrowing.

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 6

A drop in oil prices – While a drop in oil prices does not look likely at the moment, it is certainly not

beyond the realm of possibility if BMI’s double-dip global downturn scenario plays out. Bahrain will

muddle through if the oil price stays high, as is our core scenario, but if it drops again, making the

implementation of income tax necessary, then there are serious risks to growth, the size of the expatriate

population and the financial sector.

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 7

SWOT Analysis

Bahrain Food Industry SWOT

Strengths Consumers are brand-loyal and susceptible to new products and innovations.

Rising incomes and the development of the mass grocery retail sector has benefited the packaged and processed food industries.

The country has a large high spending expatriate population.

Food consumption growth in Bahrain is forecast to outperform the wider Gulf Cooperation Council region to 2015.

Bahrain’s regulatory environment is business-friendly and has succeeded in attracting a number of multinational food companies.

The dinar’s peg against the US dollar shields multinational companies from adverse exchange rate movements.

Weaknesses Companies looking for long-term volume gains will be limited by Bahrain’s small population of under 1mn.

A relatively low GDP per capita means that consumers are price conscious by regional standards.

Similar to the wider region, Bahrain runs a large food and drink trade deficit.

The outlook for the agricultural sector is limited by the small size of the country and the hot, arid climate. Many key food ingredients need to be imported.

Opportunities A number of segments remain fairly fragmented, creating opportunities for new product launches.

Opportunities for premiumisation will return as the downturn passes.

Demand for packaged and convenience foods will continue to pick up as lifestyles get busier and eating habits become more Westernized.

Bahrain has a Free Trade Area (FTA) with the US.

Threats Consumer confidence remains lower than pre-downturn levels, which is affecting demand for higher value products.

As the dinar is pegged to the US dollar, weakness from the latter is leading to imported inflation.

Despite the country’s wealth, there is high unemployment, particularly among the Shi’a community, which is a persistent source of unrest.

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 8

Bahrain Drinks Industry SWOT

Strengths Consumers are brand-loyal and susceptible to Western consumer trends.

Per capita consumption of soft and hot drinks is high.

Alcohol consumption is fairly high by regional standards, driven largely by the tourism sector.

Bahrain’s regulatory environment is business friendly.

The dinar’s peg against the US dollar shields multinational companies from adverse exchange rate movements.

Weaknesses At under 1mn, Bahrain’s small population deters investors seeking long-term volume gains.

Consumers are relatively price-conscious by regional standards.

Although fairly dynamic by regional standards, the alcoholic drinks industry is highly unlikely to attract major investment due to the small market and strict sale regulations.

Opportunities All soft drinks categories have yet to saturate.

The bottled water category will continue to provide opportunities.

Demand for healthier fruit juices, energy drinks and other value-added products will continue to increase.

Further premiumisation potential exists across all soft drink segments.

Non-alcoholic malt drinks could replace beer and provide a niche market.

Threats The downturn’s negative effect on Bahrain’s expatriate population, and therefore the size of the market, is likely to affect the wider drinks industry.

There is ongoing talk of banning or severely restricting alcoholic drinks sales, as many Bahrainis are growing increasingly unhappy with the level of tolerance of Western cultural imports such as alcohol consumption.

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 9

Bahrain Mass Grocery Retail SWOT

Strengths Consumers are brand-loyal and susceptible to Western consumer trends.

The MGR sector continues to grow, with consumers increasingly favouring modern retailing.

The market entry of regional majors Carrefour, EMKE and Waitrose will fuel MGR growth and convert more shoppers to modern retail formats.

Bahrain’s regulatory environment is business friendly.

Weaknesses The entry of discounters is unlikely as most consumers’ perception that discounted goods lack quality remains intact.

Bahrain’s small population, even by regional standards, means it will probably remain a supplementary rather than growth market for regional retailers.

Downward price trends as a result of the global economic slowdown have put pressure on the margins of retail operators and their suppliers.

Opportunities All MGR categories have yet to saturate.

Private label products are more popular in Bahrain than in most Gulf countries, with the economic downturn having increased their popularity and allowed private labels to establish themselves.

The end of the real estate bubble has made it easier to locate appropriate retail space and could speed up the transition from attached-mall to standalone retail outlets.

Mirroring the latest developments in the UAE, the underdeveloped convenience store segment could be boosted by the development of community stores.

Threats The downturn’s negative effect on Bahrain’s expatriate population, and therefore the size of the market, is likely to affect the wider retail industry.

The relatively limited long-term volume potential of the sector means likely entrants will be pressed to enter sooner rather than later.

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 10

Business Environment

BMI’s Core Global Industry Views

Developments within the global food and drink industry in the past three months have continued to reflect

and support BMI's core industry views. In major developed markets, fiscal austerity measures and slow

recovery in employment continue to weigh on our expectations for growth in the medium term. However,

over the last quarter, emerging markets have again demonstrated their ability to outperform the wider

market and have continued to attract investment. One major trend during the quarter has been the

increased role of private equity groups in the food and drink sector, which we think is indicative of its

‘safe haven’ status and the uncertainty surrounding the strength of the wider economic recovery.

In many markets the strength of the recovery has disappointed, with little sign of resurgence in consumer

demand across the US, Western Europe or emerging markets that were particularly hard hit by the

downturn, such as Venezuela and Romania. In line with our wider economic outlook and our core short-

term view, we believe the recovery in demand will continue to be muted. Our caution can be traced to the

fact that unemployment in many markets remains high and shows little sign of retracing, with companies

still wary about the strength of the recovery and holding back on hiring. Meanwhile, many consumers

who are still in employment have yet to be hit in the pocket by the downturn, but this is set to change as

fiscal austerity measures are implemented.

Over the last few months, emerging markets have again shown their importance, delivering significant

outperformance over their developed market peers, in line with our core long-term view. However, even

in those markets that bounced back strongly from the global downturn, such as Brazil and China, we

remain cautious, due to signs of slowing growth in H210 as the knock-on effects from a weaker US and

eurozone weigh on global demand. Despite this relatively subdued short-term outlook, the long-term

picture is undoubtedly favourable and investment continues to flow into the most attractive regions.

Our core view that government legislation will continue to play a role in marginalising unhealthy foods

and drinks has come to the fore in the alcoholic drinks sector over the latest quarter, with a rise in excise

duties in several key markets. This trend is likely to have been accelerated by a drop in tax revenues as a

result of the downturn, with excise duties an easy way for governments to help prop up their tax income.

Perhaps the most significant movement has been in Russia, where restrictions on the sale of alcohol and

hefty tax hikes have led to higher average prices and a significant drop in consumption, while other

markets hit by tax hikes include Turkey, Greece and Spain.

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 11

BMI Food & Drink Core Views

Short-term Outlook

Consumer demand in developed markets remains too weak to support a strong rebound in sector growth

A stuttering recovery in the US and Eurozone will increasingly way on the performance of emerging markets

Commodity price volatility will continue to affect producer earnings

Premiumisation will remain on hold

Private labels and off-trade alcoholic drinks will outperform their respective sectors

Discount grocery retailers will continue to gain market share

Government fiscal policy – austerity – will be unsupportive of industry growth

Government monetary policy – the reduced likelihood of further rate hikes – will help limit demand destruction

Major takeovers will remain scarce, leaving room for the private equity sector to step in

We continue to favour private consumption-led economies, over export-oriented states for consumer goods investment

Long-term Outlook

Companies with strong emerging market exposure will continue to outperform

Emerging market multinationals will increasingly pursue frontier market investments

Tension between producers and retailers will remain

Investment in innovation will increase as producers seek differentiation; emphasis will be placed on protecting innovations

Brand builders will continue to leave sectors under threat from private labels

Government legislation will play an increasing role in marginalising unhealthy food and beverage products; notably alcohol

Demand for convenience in retail and food will continue to grow

Functional foods will be the highest growth sector in developed markets

Consolidation will continue as producers seek greater efficiencies

Beverage companies will continue to invest in diversification away from carbonated beverages and into healthier sub-sectors

Source: BMI

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 12

Middle East Food & Drink Business Environment Ratings

UAE Tops Ratings But Egypt The Real Story

With the exception of the UAE, the Middle East and North Africa (MENA) has by in large not been

dramatically affected by the global economic weakness that has pervaded over the past two years.

Although outlandish premiumised spending has been reined in within the Gulf, the evolvement of

consumer spending in absolute spending and taste terms in some of the frontier MENA markets (Egypt in

particular stands out) has largely continued apace.

While the sheer weight of growth (most of it led by energy) racked up by most of the Gulf region over the

past decade has pushed up per capita GDPs in the UAE, Kuwait and Qatar to the upper echelons of the

global economy, the atypical pace at which this has taken place has meant that the development of the

food and drink industry was bound to lag behind. With key industry indicators such as organised retail’s

proportional contribution to absolute retail sales still comfortably lagging most developed economies,

even in the UAE, investment from both Gulf and foreign-based companies is likely

As a result, even though with the exception of Saudi Arabia, which makes up about two thirds of the Gulf

consumer market, the region lacks long-term scale, perpetually evolving tastes and preferences dictates

that the Gulf should retain its attractiveness to non-regional food, drink and retail companies. Moreover,

markets like the UAE and Bahrain in particular continue to serve as exciting export bases into the wider

MENA region.

Egypt Closes On UAE

Notwithstanding the fact that disposable incomes in the Gulf region remain considerably higher than in

the rest of the MENA region, the Gulf’s dominance of the top positions in BMI’s regional food and drink

business environment ratings no longer appears as secure. Egypt has pushed into second place behind the

UAE and looks very well placed to assume top position in the near future. Even though its food and drink

industry is clearly not nearly as sophisticated as the UAE’s, this does in fact count in Egypt’s favour from

a ratings point of view.

Egypt’s push into second place reflects our industry and macroeconomic expectations. We like the long-

term promise of the Egyptian domestic demand story, which backed by a population approaching 82mn,

provides dynamic long-term growth potential. Comparing historical and forecast annual per capita food

consumption growth in both Egypt and the UAE highlights Egypt’s outperformance in this regard (see

chart). Its economy is growing strongly and is expected to continue doing so, as reflected in our outlook

to 2015.

Egypt’s position as the standout frontier market in the MENA region is largely uncontested. Iran and Iraq,

two of the other potential rivals for this tag, for a variety of reasons cannot match Egypt, certainly when it

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 13

comes to pulling in investment from Gulf and Western companies alike. From an investment point of

view, Egypt’s trade links are also important. In addition to smooth access to the Gulf Cooperation

Council (GCC) region, Egypt is a major net exporter to the emerging Common Market for Eastern and

Southern Africa (COMESA).

Therefore from both a ratings and competiveness standpoint, Egypt uniquely combines a strong long-term

economic and subsequently consumer spending outlook, with an unusually large market by regional

standards and an ability to attract foreign investment. It will therefore be increasingly difficult for the

UAE to maintain its hold on first position.

Assessing The Rest Of The Gulf

Saudi Arabia is the big underperformer in this quarter. Placing sixth does not do it justice as the Gulf

region’s most promising long-term growth. It is the only Gulf market that combines scale with a strong

scope for long-term growth. Its lowly ranking comes despite an above average Risk score and clearly

emphasises the fact that a much stronger Industry Reward score is necessary for Saudi Arabia to push up

the ratings table. Saudi Arabia’s size and the fact that on a per capita GDP basis disposables incomes are

reasonably high suggests that it has the potential to move the ratings, possibly eventually settling into the

top three alongside the UAE and Egypt, although for now this remains only a distant possibility.

Fundamentally speaking and momentarily looking over nuances, Kuwait and Qatar are in essence less

dynamic versions of the UAE from a ratings point of view, if only – particularly in the latter’s case –

because they have smaller populations. It will be difficult for them to distinguish themselves and move

much higher up the ratings than where they currently find themselves. Third placed Bahrain largely

benefits from the fact that in addition to having the region’s strongest Risk score, some of the key

indicators within its food and drink industry are poised for fairly strong growth to 2014 from a lower base

than the UAE, Kuwait and Qatar.

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 14

Regional Food & Drink Business Environment Ratings

Reward Risk

Industry Reward

Country Reward Reward

Industry Risk

Country Risk Risk

Food & Drink Risk/Reward

Rating Regional Ranking

UAE 67 60 64 70 39 51 60.0 1

Egypt 63 55 59 50 62 57 58.4 2

Bahrain 53 53 53 70 66 68 57.3 3

Kuwait 34 58 46 65 71 69 52.6 4

Qatar 41 52 46 65 66 65 52.1 5

Saudi Arabia 31 60 45 60 66 63 50.8 6

Oman 29 46 38 60 72 67 46.4 7

Lebanon 32 46 39 45 51 49 41.9 8

*Israel 49 45 47 70 76 74 55.2 *4

*Israel has been included for comparative purposes only. Had it been ranked, it would have scored fourth respectively. Source: BMI. Scores out of 100, with 100 highest. The Food & Drink BE Rating is the principal rating. It is comprised of two sub-ratings Reward' and 'Risk'', which have a 70% and 30% weighting respectively. In turn, the 'Reward' Rating is comprised of Industry Reward and Country Reward, which have equal weighting and are based upon growth/size of food/alcohol and soft drinks industry (Market) and the broader economic/socio-demographic environment (Country). The 'Risk' rating is comprised of Industry Risk and Country Risk which have a 40% and 60% weighting respectively and are based on a subjective evaluation of industry regulatory and competitive issues (Market) and the industry's broader Country Risk exposure (Country), which is based on BMI's proprietary Country Risk Ratings. The ratings structure is aligned across the 14 Industries for which BMI provides Business Environment Ratings methodology, and is designed to enable clients to consider each rating individually or as a composite, which the choice depending on their exposure to the industry in each particular state. For a list of the data/indicators used, please consult the appendix at the back of the report.

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 15

Bahrain’s Food & Drink Business Environment Rating

Bahrain has dropped to third position from its previously held first in BMI’s quarterly Food & Drink

Business Environment Ratings for the MENA region. Displaced by the UEA and Egypt, which took first

and second place respectively, we can see that the Gulf countries’ dominance of the top positions in

BMI’s ratings no longer appears as secure.

Despite losing its top place ranking, Bahrain nevertheless manages to do well, thanks to a winning

combination of the region’s highest F&D market score and one of the region’s highest Risk scores. While

spending on food and drink is relatively low compared to its Gulf peers, this low base gives Bahrain one

of the region’s strongest food and drink consumption growth forecasts, giving it a major competitive

edge.

Bahrain’s strong business environment continues to be one of its key strengths, particularly compared to

its regional peers. Despite significant economic progress over the past decade, business environments

across much of the region remain fairly bureaucratic compared to Bahrain – a fact that continues to draw

investors to this stable country. Unsurprisingly, Bahrain’s Risks score is second only in the region to

Kuwait.

However, there are some obvious drawbacks, such as the very small population of under 1mn, which

significantly limits the long-term growth opportunities. GDP per capita is relatively modest by Gulf

standards, which also weighs down the Country Reward score. These two factors are the main reasons

why Bahrain lost its pole position this quarter. Nevertheless, the country remains an attractive proposition

for Gulf and non-regional food and drinks companies, particularly given the lack of premiumisation in the

local market, with the food and drink industry posed for fairly strong growth.

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 16

Macroeconomic Outlook

Strong Q1 Figures Masking Weak

Domestic Demand Picture

BMI View: We do not see what will

drive the recovery for Bahrain,

beyond government spending; and,

as such, our forecasts are low. That

said, we acknowledge that official

figures may paint a rosier picture.

We remain concerned about the

stability and health of the Bahraini

services economy and private sector

in general. Latest figures suggest

that there was a substantial rebound

in overall growth in Q110, but we

see risks for the remainder of the

year. Although fiscal stimulus plans

remain in place, they remain under threat from lower oil prices, while further turmoil in the financial

sector is not out of the question. We could well see defaults from some of the over-leveraged investment

companies, hitting banks' asset sheets and investor confidence more generally. Although the official

numbers may come in higher than our projections, we believe that our low forecasts are a more accurate

reflection of the state of the economy.

Our forecasts see a slowdown in growth in 2010 (to 1.5%) and only a mild uptick in 2011 (to 1.9%), with

sub-optimal rates of expansion persisting throughout the forecast period. However, with 2009 growth

figures having surprised to the upside (going against our own and anecdotal perceptions of growth in the

Kingdom), the 2010 and 2011 figures could do the same. Overall GDP figures tell a different story to

individual indicators. Our forecast figures are primarily being held back more by sluggish oil exports: we

do see a moderate uptick in gross fixed capital formation and private consumption from 2009's low base.

Uninspiring

Real GDP Growth (%) and OPEC Basket Price (US$/bbl)

Source: Central Informatics Organisation, BMI

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 17

Contradictory Indicators

Looking at Q1 results, the economy

does appear to be on the rebound.

Overall real GDP growth came in at

an annualised 5.2%, compared with

2009's full-year outturn of 3.1%,

with strong performances registered

by hotels and restaurants (up 14.4%),

onshore financial institutions

(12.8%) and social and personal

services (14.9%). The latter

encompasses private health and

education, which are mainly used by

expatriates, as the government

subsidises these services for

Bahrainis. Even construction growth

came in at 2.2% in Q1, after

averaging -2.5% over Q109-Q409,

with real estate managing the same rate.

The government also estimates that employment stood at 489,657 in Q110, up 1.2% on Q109, and

accounting for 44.2% of the population. Although this could imply some decline in population – in line

with the view we have been promoting for some time – we do not expect to see the government

confirming this in official data. In any case, the percentage is the highest since the government's data

series began in 2006. Against this backdrop, the outperformance of these three sectors suggests a strong

global and expatriate consumer demand situation, which is, in theory, very good news for the Bahraini

economy.

Indeed, this is in line with our forecasts. We do see private consumption growth of 3.0% for 2010, rising

to 4.0% in 2011. Unfortunately, the government has not yet provided a breakdown of either Q110 or 2009

growth by expenditure, so we cannot compare it at this stage, but a 3.0% growth rate in real terms is not

to be sniffed at in this climate. However, we also think that private consumption – and the sectors

highlighted above – are also growing from the lowest bases. Indeed, while private consumption accounted

for 45.2% of real GDP in 2006, we estimate that it made up just 42.0% in 2009 and 2010. Moreover, we

think that enthusiasm over the double-digit GDP growth figures will be mitigated by (a) anecdotal

evidence and (b) other indicators.

Among other reasons for concern, we see the bank lending growth rate as a sign that consumers have not

gone back to their old ways: Bahrain's banks have seen the lowest loan growth in the Gulf region, with a

Call This A Recovery?

Bahrain - Aluminium Output (metric tonnes)

Source: Bahrain Central Informatics Organisation

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 18

y-o-y increase of 3.9% (against inflation of 2.4%) in May, compared with 27.0% y-o-y in Qatar. This

compared with around 45% at its peak. True, personal wealth may have increased due to the apparent rise

in employment, but given the extent to which credit fuelled spending during the boom years – even now,

retail banks' client loans per capita amount to US$67,764 (although this includes business loans) – it is

hard to imagine the stagnation not having an effect. In addition, there are risks going forward: tax rises

are more than possible after the elections, given the fiscal position.

Did Recovery Peak In Q309?

That said, it is not just services that have driven Q1's impressive growth number. Goods exports are also

doing well. Manufacturing apparently rose by 6.8%, quarrying by 8.9% and even oil and gas managed an

upturn of 0.5%.

Again, though, individual data sets cast some doubt on these impressive outturns. In volume terms, oil

output growth remains subdued, threatening to undermine our forecast for a 1.0% rise in volume terms in

2010. Bahrain ramped up oil output from its Abu Saafa oil field in Q309, in line with the price increase;

but, unlike most of the OPEC countries, it has since reduced output again. Total output from the Abu

Saafa and Bahrain oil fields came in at around 164,360 b/d in Q110, down from a nine-month high of

169,720 b/d in Q309. Refined oil output is coming from a lower base than crude, so y-o-y growth remains

high (at 17.9%), but this also peaked in Q309 – and was down 2.2% q-o-q in the first three months of the

year. Aluminium followed the same pattern: output bounced to 213,224 metric tonnes in Q309, but

remained lower in y-o-y terms, and then fell again in Q409 and Q110 (at a rate of 1.6% y-o-y, to 210,009

metric tonnes).

Meanwhile, global demand does not inspire much confidence either. As we move towards the end of the

year, the global economic scenario we had envisaged for 2010 – namely, a shaky and largely jobless

recovery slowing in the second half, alongside continued deflationary pressures – is playing out. This

suggests sluggish demand going forward, and we forecast a slowdown in growth for all the major

economies except the eurozone (which, in any case, is coming from a much lower base). Against this

backdrop, we see downside risks to our oil price forecast (US$85/bbl for the OPEC Basket in 2011, rising

to US$90/bbl in 2012), as well as lower demand for Bahraini industrial exports: we are pencilling in 0.8%

average annual growth for the period 2010-13, outpaced by greater import growth (around 3.0%) as

infrastructure spending pushes up the capital goods bill.

Fiscal Expansion To Continue

On the government spending front, we expect growth to remain strong in 2010 and 2011, in spite of the

fiscal difficulties, pencilling in real growth of 8.0% and 6.0% respectively. Indeed, from the tone of the

Central Informatics Organisation's latest bulletin, there does not appear to be much impetus to pare down

spending, unless it becomes urgent: the bulletin states that the better economic performance and higher oil

prices in Q110 will afford 'greater discretion to the government over its spending plans and financial

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 19

policies' – implying that any austerity measures had more to do with financing ability than a desire to

change tack.

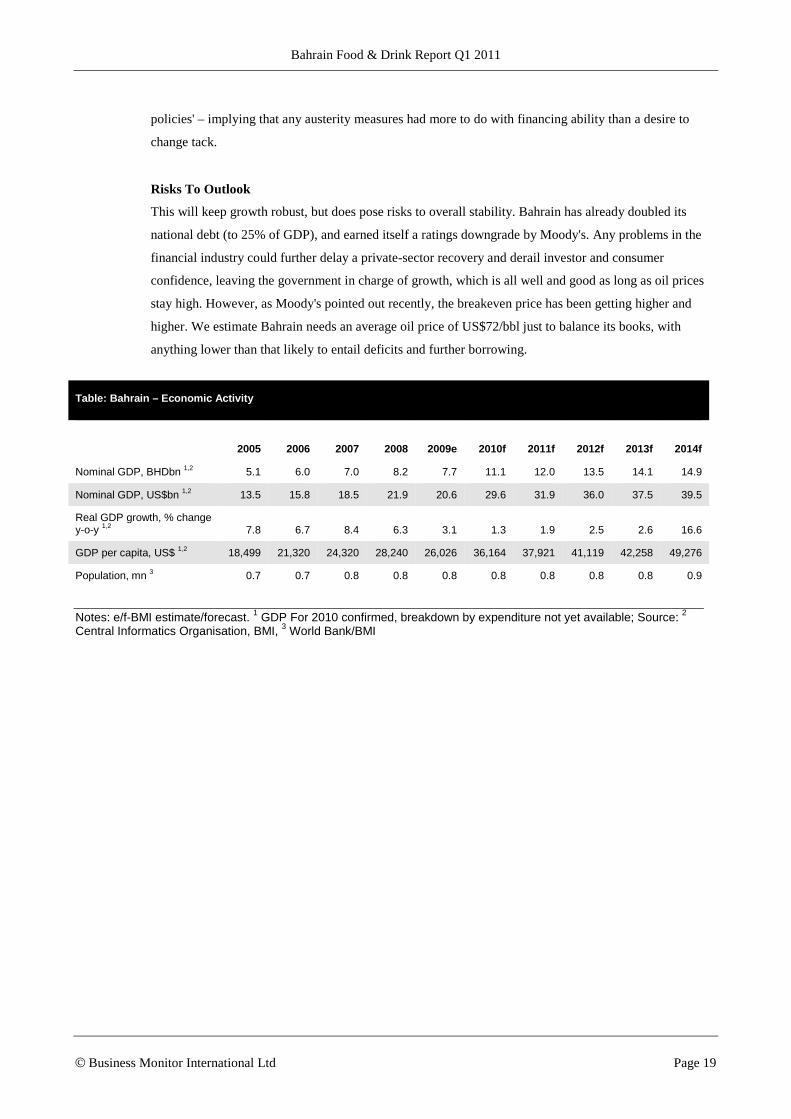

Risks To Outlook

This will keep growth robust, but does pose risks to overall stability. Bahrain has already doubled its

national debt (to 25% of GDP), and earned itself a ratings downgrade by Moody's. Any problems in the

financial industry could further delay a private-sector recovery and derail investor and consumer

confidence, leaving the government in charge of growth, which is all well and good as long as oil prices

stay high. However, as Moody's pointed out recently, the breakeven price has been getting higher and

higher. We estimate Bahrain needs an average oil price of US$72/bbl just to balance its books, with

anything lower than that likely to entail deficits and further borrowing.

Table: Bahrain – Economic Activity

2005 2006 2007 2008 2009e 2010f 2011f 2012f 2013f 2014f

Nominal GDP, BHDbn 1,2 5.1 6.0 7.0 8.2 7.7 11.1 12.0 13.5 14.1 14.9

Nominal GDP, US$bn 1,2 13.5 15.8 18.5 21.9 20.6 29.6 31.9 36.0 37.5 39.5

Real GDP growth, % change y-o-y 1,2 7.8 6.7 8.4 6.3 3.1 1.3 1.9 2.5 2.6 16.6

GDP per capita, US$ 1,2 18,499 21,320 24,320 28,240 26,026 36,164 37,921 41,119 42,258 49,276

Population, mn 3 0.7 0.7 0.8 0.8 0.8 0.8 0.8 0.8 0.8 0.9

Notes: e/f-BMI estimate/forecast. 1 GDP For 2010 confirmed, breakdown by expenditure not yet available; Source: 2 Central Informatics Organisation, BMI, 3 World Bank/BMI

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 20

Industry Forecast Scenario

Consumer Outlook

Bahrain’s consumer outlook appears fairly weak over our five-year forecast period as the economic

slowdown has affected consumer confidence. While the official numbers suggest an economic recovery is

in place, with real GDP growing by 3.1% in 2009 according to the CIO, other indicators such as bank

lending, the stock market, house prices and consumer confidence suggest otherwise, indicating that the

real picture is somewhat bleaker. There is also a degree of public discomfort with their government’s

relentless pursuit of foreign investment. In a bid to attract foreign business, Manama has allowed an

increasingly liberal leisure environment and many Bahrainis are unhappy with the level of tolerance of

Western cultural imports such as alcohol consumption, which could mean a long-term risk for the

alcoholic drinks industry.

Bahrain has one of the most open economies in the Middle East and is home to a large financial services

sector. Developing the service economy has been a top priority for the government given Bahrain’s

relatively small, and dwindling, oil reserves, and the financial services sector has emerged as a major

driver of economic growth. The small size of the local population is a significant limitation for the growth

of mass retail but tourism plays an important part in boosting retail sales in the region. In Bahrain, tourist

arrivals have risen by an average of 10-15% annually over the past three years and are projected to rise by

an average of 2.5% a year over the next decade, according to the Ministry of Culture and Information’s

tourism affairs division. Bahrain also remains a popular weekend shopping destination for many Saudi

consumers, who cross the King Fahd Causeway, boosting local retail sales.

BMI estimates that consumer spending in

Bahrain was flat in 2009 due to low

consumer confidence and high levels of

unemployment, but we expect a rebound

to 5.0% growth in 2010 and 6.0% in

2011. While private consumption is now

growing again, we believe that this

growth is starting from a low base.

Indeed, while private consumption

accounted for 45.2% of real GDP in

2006, we estimate that it made up just

42.0% in 2009 and 2010. Currently, we

see private consumption growth of 3.0%

Bahrain GDP & CPI

2008-2019

Source: CIO, CBB, BMI forecasts (2010-2019)

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 21

for 2010, rising to 4.0% in 2011. Unfortunately, the government has not yet provided a breakdown of

either Q110 or 2009 growth by expenditure, so we cannot compare it at this stage, but a 3.0% growth rate

in real terms is not to be sniffed at in this climate.

The local retail sector is characterised by an increased tendency on the part of consumers to trade up to

higher value products, a trend that slowed significantly during the downturn as consumers turned to more

economically priced food and drink products. Despite the country’s wealth, unemployment remains a

problem, particularly among the Shi’a population, where unemployment can exceed 30% and is a

continual source of unrest. However, looking at Q1 results, the economy does appear to be on the

rebound. Overall real GDP growth came in at an annualised 5.2%, compared with 2009's full-year outturn

of 3.1%, with strong performances registered by hotels and restaurants, up 14.4%.The government also

estimates that employment stood at 489,657 in Q110, up 1.2% on Q109, and accounting for 44.2% of the

population. Although this could imply some decline in population – in line with the view we have been

promoting for some time – we do not expect to see the government confirming this in official data. In any

case, the percentage is the highest since the government's data series began in 2006. Against this

backdrop, the outperformance of these three sectors suggests a strong global and expatriate consumer

demand situation, which is, in theory, very good news for the Bahraini economy.

Looking further ahead we are projecting very modest GDP recovery as the financial and real estate

sectors remain very subdued. This is in line with the view that we expressed at the beginning of 2009: for

all the talk of the importance of economic diversification over recent years, and despite the drop in oil

prices, it will be the economies that are least diversified that will emerge from this particular crisis

strongest in the short-to-medium term. Bahrain’s oil resources and revenues are relatively low compared

with its neighbours and there is little scope for major increases in production. With a very hefty financial

sector, Bahrain is very vulnerable to volatile global financial sentiment and overseas demand. While

economic growth is expected to return to positive territory from 2010, averaging around 2.8% over 2015-

2019, we expect a spurt of 16.4% in 2014 on the back of an increase in oil output from the Abu Saafa

fields, which will then boost the export sector in real terms.

The 10-year outlook for Bahrain is similar to its fellow GCC members. As long as political stability is

maintained, robust government spending and oil-based liquidity will keep it a relatively attractive

destination for investment. However, the last few years have been a boom time and we do not see growth

returning to the levels posted over 2001-2008 (7.8% on average). Attracted by the country’s stability and

positive business environment, a number of major international retailers, including Carrefour and

Waitrose, have been drawn to the Bahraini market, investing in new store openings. Such investments

will bring a wider range of food and drink products to market, thereby driving demand and boosting sales.

The Bahraini retail market will also continue to benefit from events such as the annual Formula One

grand prix in Sakhir, which has generated hundreds of millions of dollars in revenues since it became a

fixture on the racing calendar in 2004.

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 22

Risks To Outlook

The clear downside risk to this scenario is a drop in oil prices, which is not beyond the realm of

possibility if BMI’s double-dip global downturn scenario plays out. Bahrain will muddle through if the

oil price stays high, as is our core scenario, but if it drops again, making the implementation of income

tax necessary, then there are serious risks to growth, the size of the expatriate population and the financial

sector.

The government is going all out to promote its business environment with its worldwide Business

Friendly marketing campaign. However, we note substantial risks to the investment climate emanating

from the worsening fiscal situation. In October 2009, it was reported that the government was considering

increasing corporate tax for Bahraini and foreign businesses, although there have been no further details

since then. Meanwhile, the business community is already up in arms about the expatriate workers’ tax.

Furthermore, Bahrain has already doubled its national debt (to 25% of GDP), and earned itself a ratings

downgrade by Moody's. Any problems in the financial industry could further delay a private-sector

recovery and derail investor and consumer confidence,

Food

Food Consumption

BMI’s current outlook for the Bahraini

economy is rather subdued, although we

are continuing to forecast steady growth

in headline food and drink consumption.

We remain concerned about the stability

and health of the Bahraini services

economy and private sector in general.

Latest figures suggest that there was a

substantial rebound in overall growth in

Q110, but we see risks for the remainder

of the year. Although fiscal stimulus

plans remain in place, they are under

threat from lower oil prices, while further

turmoil in the financial sector is not out

of the question.

Currently we are forecasting that total food consumption will grow by 10.9% between 2010 and 2015 to

reach a total value of BHD0.214bn. We do believe that good growth opportunities remain, despite the

small size of the market at just under 1mn. While this size does significantly limit long-term growth

opportunities, there nevertheless remains considerable room for growth in most segments of the wider

Food Consumption

2005 - 2015

e/f = BMI estimate/forecast. Source: Bahrain Monetary Agency, Bahrain Centre for Research & Studies, Gulf Cooperation Council Secretarial General, BMI

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 23

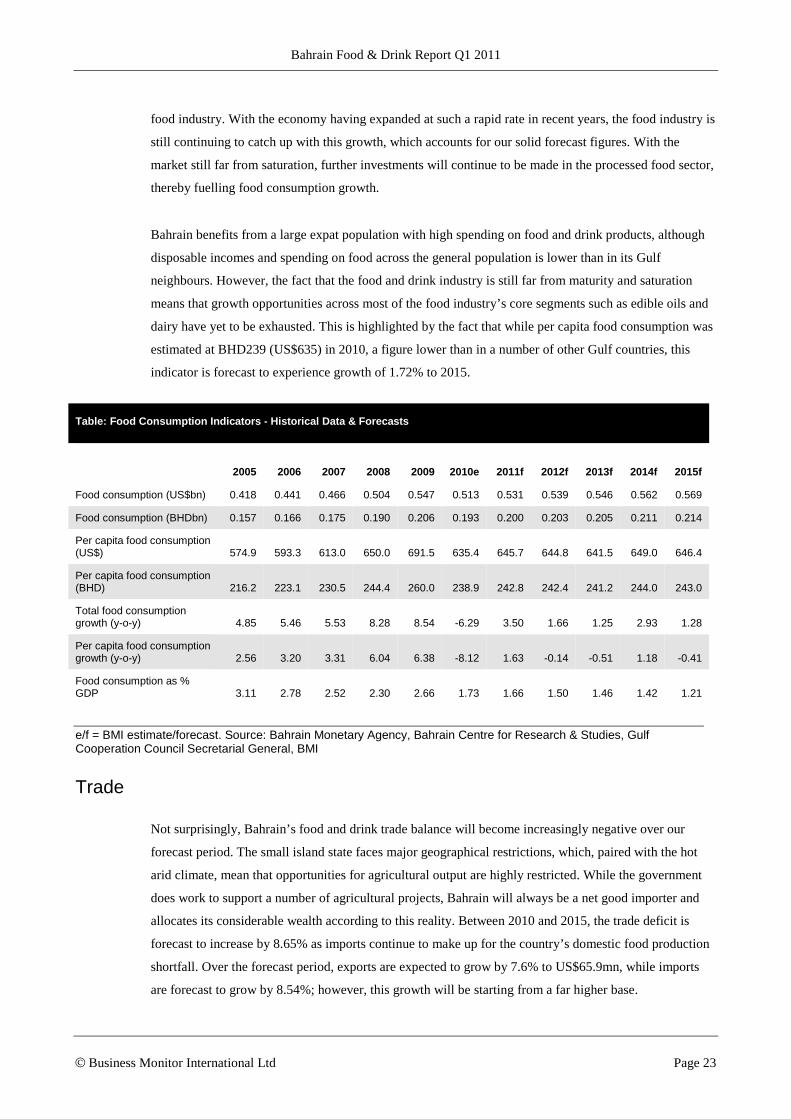

food industry. With the economy having expanded at such a rapid rate in recent years, the food industry is

still continuing to catch up with this growth, which accounts for our solid forecast figures. With the

market still far from saturation, further investments will continue to be made in the processed food sector,

thereby fuelling food consumption growth.

Bahrain benefits from a large expat population with high spending on food and drink products, although

disposable incomes and spending on food across the general population is lower than in its Gulf

neighbours. However, the fact that the food and drink industry is still far from maturity and saturation

means that growth opportunities across most of the food industry’s core segments such as edible oils and

dairy have yet to be exhausted. This is highlighted by the fact that while per capita food consumption was

estimated at BHD239 (US$635) in 2010, a figure lower than in a number of other Gulf countries, this

indicator is forecast to experience growth of 1.72% to 2015.

Table: Food Consumption Indicators - Historical Data & Forecasts

2005 2006 2007 2008 2009 2010e 2011f 2012f 2013f 2014f 2015f

Food consumption (US$bn) 0.418 0.441 0.466 0.504 0.547 0.513 0.531 0.539 0.546 0.562 0.569

Food consumption (BHDbn) 0.157 0.166 0.175 0.190 0.206 0.193 0.200 0.203 0.205 0.211 0.214

Per capita food consumption (US$) 574.9 593.3 613.0 650.0 691.5 635.4 645.7 644.8 641.5 649.0 646.4

Per capita food consumption (BHD) 216.2 223.1 230.5 244.4 260.0 238.9 242.8 242.4 241.2 244.0 243.0

Total food consumption growth (y-o-y) 4.85 5.46 5.53 8.28 8.54 -6.29 3.50 1.66 1.25 2.93 1.28

Per capita food consumption growth (y-o-y) 2.56 3.20 3.31 6.04 6.38 -8.12 1.63 -0.14 -0.51 1.18 -0.41

Food consumption as % GDP 3.11 2.78 2.52 2.30 2.66 1.73 1.66 1.50 1.46 1.42 1.21

e/f = BMI estimate/forecast. Source: Bahrain Monetary Agency, Bahrain Centre for Research & Studies, Gulf Cooperation Council Secretarial General, BMI

Trade

Not surprisingly, Bahrain’s food and drink trade balance will become increasingly negative over our

forecast period. The small island state faces major geographical restrictions, which, paired with the hot

arid climate, mean that opportunities for agricultural output are highly restricted. While the government

does work to support a number of agricultural projects, Bahrain will always be a net good importer and

allocates its considerable wealth according to this reality. Between 2010 and 2015, the trade deficit is

forecast to increase by 8.65% as imports continue to make up for the country’s domestic food production

shortfall. Over the forecast period, exports are expected to grow by 7.6% to US$65.9mn, while imports

are forecast to grow by 8.54%; however, this growth will be starting from a far higher base.

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 24

Table: Bahrain Sectoral Trade Balance - Historical Data & Forecasts

2005 2006 2007 2008 2009 2010e 2011f 2012f 2013f 2014f 2015f

Exports (food, drink & tobacco) (US$mn) 58.62 57.36 59.12 63.27 57.28 61.20 61.80 62.72 62.83 65.73 65.85

Imports (food, drink & tobacco) (US$mn) 634.7 512.7 539.4 626.9 551.4 532.7 541.1 549.8 558.9 568.4 578.2

Balance (US$mn) -576.1 -455.4 -480.3 -563.6 -494.1 -471.5 -479.3 -487.1 -496.1 -502.6 -512.3

e/f = BMI estimate/forecast. Source: Bahrain Monetary Agency, Bahrain Centre for Research & Studies, Gulf Cooperation Council Secretarial General, BMI

Drink

Soft Drinks

As the country’s leading drinks sector,

strong and steady growth is forecast for

Bahrain’s soft drinks industry. Due to the

severe restrictions on the sale of alcoholic

drinks and the hot climate, soft drinks are

very popular and play an important role

in social occasions. Sales of soft drinks

are forecast to experience growth of

40.4% between 2010 and 2015 to reach

BHD47.99mn. While segmented soft

drinks data is not available, BMI believes

that higher-value segments such as fruit

juices and functional drinks will begin to

outperform the more established and lower-cost carbonates segment, as premiumisation begins to play a

stronger role in driving values sales over the forecast period.

Looking ahead, we see that the two key trends expected to be the main drivers of industry growth are

rising health consciousness and premiumisation. Rising health consciousness will provide opportunities

for carbonate producers as low-calorie substitutes will become increasingly popular. Higher value

segments such as fruit juices and functional drinks are expected to continue to gain traction as the

evolution of the wider industry and rising health consciousness trend plays out. The flourishing bottled

water category and energy drinks are also expected to continue performing well. Non-alcoholic beers and

other malt beverages are also benefiting from stronger demand, particularly among younger consumers

that are keen to experiment with new products.

Soft Drink Sales

2005 - 2015

NB Historical data are estimates, based on country sales as a % of total Gulf sales. Source: Company information, Trade press, BMI

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 25

Table: Drinks indicators

2005 2006 2007 2008 2009 2010e 2011f 2012f 2013f 2014f 2015f

Soft drinks sales (BHDmn) 26.65 27.99 29.43 30.98 32.64 34.19 36.40 40.21 42.04 47.40 47.99

Soft drink sales growth, BHD, (y-o-y) 9.77 5.04 5.15 5.25 5.38 4.74 6.47 10.45 4.56 12.74 1.25

Soft drinks sales (US$mn) 70.9 74.4 78.3 82.4 86.8 90.9 96.8 106.9 111.8 126.1 127.6

Per capita soft drink spend (US$) 97.4 100.1 103.0 106.2 109.7 112.7 117.8 127.8 131.3 145.5 144.9

NB Historical data are estimates, based on country sales as a % of total Gulf sales. Source: Company information, Trade press, BMI

Mass Grocery Retail

While the small size of the local market

places significant limitations on the

potential growth of the Bahraini MGR

industry, we are nevertheless forecasting

strong growth ahead, as the informal

sector currently still accounts for a large

proportion of sales. Between 2010 and

2015, total MGR sales are forecast to

increase by 47.0% to reach a value of

BHD243.5mn. The main drivers will be

the continued robustness of the local

economy and the conversion of many

shoppers from traditional to organized

retail. While the small size of the

population suggests that the opportunities for long-term growth will be fairly negligible, the fact that the

informal sector still accounts for more than 50% of food and drink sales suggests there are still significant

opportunities available through organic store growth.

MGR sales experienced explosive growth between 2002 and 2008 on the back of the country’s

hydrocarbon-fuelled economic boom, increasing by over 95%. This rapid economic expansion attracted

investment into the country’s underdeveloped retail sector, with operators targeting the spending power of

the expatriate-heavy consumer base, the increasing preference for Western-style consumption trends and

the subsequent desire for modern retailing.

Mass Grocery Retail

2005 - 2015

e/f = BMI estimate/forecast. Source: Bahrain Monetary Agency, Bahrain Centre for Research & Studies, Gulf Cooperation Council Secretarial General, BMI

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 26

The hypermarket and supermarket segments will continue to be the main drivers of growth in the MGR

sectors, with sales forecast to grow by 38.8% and 30.7% respectively between 2010 and 2015. Due to the

vast selling power of hypermarkets, the addition of just one store (there are currently only five in the

whole country) can significantly add to MGR sector sales. Meanwhile, supermarkets will continue to

cater to those consumers seeking a more niche retail experience, as can be seen with the opening of the

high-end supermarket Waitrose. It is the convenience sector that is forecast strong growth, with sales

expected to rise by an impressive 97.8% to 2015. This is partly a reflection of convenience stores’ ability

to penetrate urban residential areas far more easily than larger store formats, but also reflects the far lower

base of the sales figures.

Looking further ahead, by 2019, we expect that the food retail sales split will shift to 65:35 in favour of

organized retail, which should enable the annual headline MGR growth rate to remain strong past the

2015 forecast period.

Table: Bahrain Mass Grocery Retail Sales - Value by Format - Historical Data & Forecasts

2005 2006 2007 2008 2009 2010e 2011f 2012f 2013f 2014f 2015f

Supermarkets (BHDbn) 0.0417 0.0469 0.0515 0.0566 0.0613 0.0641 0.0682 0.0725 0.0769 0.0825 0.0838

Hypermarkets (BHDbn) 0.0466 0.0542 0.0609 0.0664 0.0729 0.0699 0.0739 0.0796 0.0864 0.0954 0.0970

Convenience stores (BHDbn) 0.0132 0.0155 0.0199 0.0230 0.0268 0.0317 0.0371 0.0438 0.0513 0.0616 0.0627

Total mass grocery retail sector (BHDbn) 0.1015 0.1165 0.1324 0.1460 0.1609 0.1656 0.1793 0.1960 0.2146 0.2395 0.2435

Total mass grocery retail sector growth, BHD, (y-o-y) 17.3913 14.7594 13.6032 10.3409 10.1992 2.9197 8.2333 9.3118 9.4950 11.5974 1.6708

Supermarkets (US$bn) 0.1110 0.1246 0.1370 0.1506 0.1630 0.1705 0.1813 0.1928 0.2044 0.2194 0.2228

Hypermarkets (US$bn) 0.1240 0.1441 0.1620 0.1766 0.1938 0.1858 0.1967 0.2118 0.2298 0.2537 0.2579

Convenience stores (US$bn) 0.0350 0.0411 0.0530 0.0612 0.0713 0.0842 0.0988 0.1166 0.1364 0.1637 0.1668

Total mass grocery retail sector (US$bn) 0.2700 0.3099 0.3520 0.3884 0.4280 0.4405 0.4768 0.5212 0.5707 0.6368 0.6475

e/f = BMI estimate/forecast. Source: Bahrain Monetary Agency, Bahrain Centre for Research & Studies, Gulf Cooperation Council Secretarial General, BMI

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 27

Table: Bahrain Grocery Retail Sales By Format, 2009 & 2019

2009 2019f

Organised/MGR 48% 65%

Non-organised/Independent 52% 35%

f = forecast. Source: BMI

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 28

Food Key Industry Trends and Developments

Increasing Interest In Processed Foods

While traditional foods and diets are still very popular in Bahrain, a major shift has been occurring with

processed foods and fast food restaurants becoming increasingly popular. These changing eating habits

have seen consumers demonstrating a growing preference for processed Western foods and snacks. In line

with this trend, snack food producers and chain restaurants have been ramping up their investments in the

Bahraini market.

The end of 2009 witnessed a spree of investments from a number of food producers. In December India-

based Britannia and Oman-based al-Sallan Food Industries relaunched the popular biscuit brand

Baker’s Pride in the Bahraini market, working with local distribution partner A. Latif al-Aujan Food

International. The relaunch strategy for the Baker’s Pride range, which is manufactured at the

company’s plant in Sohar, Oman, included an improved recipe and new packaging, designed to give the

brand a new look and feel, while the sales price remained the same. The Bahraini biscuit market is

estimated to be worth US$21.42mn annually, with per capita consumption of biscuits estimated at 5.65kg

per annum. Meanwhile, the Auntie Anne’s pretzel chain opened its first location at the Seef Mall and

stated that it will continue to expand in the country, with plans to open at least five stores over five years,

and may eventually develop customized products to fit local taste profiles. The local operations in

Bahrain are managed through a sub-franchise license by Da’Rosa Food Company.

Also, in late December 2009, Bahrain’s Global Banking Corporation announced that it established a

new limited liability company called Diyafa Holdings Company to capitalise on opportunities in the

food and beverage, hospitality and retail and business service sectors. The new company plans to target

some of the leading international food and hospitality brands, while also creating and developing its own

brands in specific market segments. Diyafa is expected launch two major restaurants in Bahrain and is

also looking into the boutique hotel market.

Continued Government Investment

Bahrain’s food production industry is characterised by very high levels of government involvement. The

government has made investing into the local food industry a priority, with this sector providing

employment for its citizens, as well as a means of wealth redistribution. Furthermore, the country is

highly dependent on food and drink imports due to its geographical restrictions and the very harsh local

climate. More recently, these projects have gained growing importance as the country looks to decrease

dependence on imports where possible and to keep inflation in check. To this end, in July 2010 it was

announced that plans are underway for the establishment of a private poultry firm in the country as a part

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 29

of a BHD10mn (US$26.6mn) investment project. The government is supporting an initiative spearheaded

by the private sector with the aim of promoting the country’s food security. When completed, the facility

is expected to produce up to 10mn chickens annually, which will go a long way in meeting consumer

demand at affordable prices.

Growing Investment Interest From Non-Regional MNCs

While regionally based companies have a strong presence in the local food and drink sector, multinational

companies operating in the Gulf region have also been seeking expansion into the wider Middle East and

North Africa region.

In May 2010, Mars GCC launched a US$40mn manufacturing facility in Dubai as the Gulf Cooperation

Council (GCC) region assumed greater strategic significance. As emphasised by the fact that the region

has consistently posted double-digit sales growth since 2000, demand for Western chocolate brands

(Mars produces its namesake and the Snickers brand) is widespread, with the demand for snack foods

growing strongly, as discussed above. Companies such as Mars can also leverage off duty-free export

opportunities to efficiently supply all six GCC markets (including Bahrain), as well the wider Middle East

region.

Also in May, Nestlé announced it was investing in four new manufacturing facilities across the Gulf,

while bullishly forecasting 2010 sales growth of 10% year-on-year (y-o-y). Consolidated Nestlé Middle

East region sales reached US$1.4bn in 2009 from 17 factories, with the UAE accounting for between

10% and 11% of the total. Nestlé is expanding organically from a position of significant strength, having

established itself as comfortably one of the region’s most well-invested firms.

In mid 2009, global dairy firm Fonterra announced that it expects the Middle East region (specifically

the affluent GCC area) to be one of its key long-term growth engines, following this comment with full

takeover of the outstanding 51% stake in its Saudi joint venture partner Saudi New Zealand Dairy

Products Company from Saudi Dairy and Foodstuff Company (Sadafco) in a deal believed to be

worth about SAR120mn (US$32mn). Based out of New Zealand, Fonterra has reported double-digit

turnover growth in the region over the last three years.

American food and drink major Kraft Foods has long been a major presence in the country’s food and

drink sector, having invested US$40mn in a manufacturing plant in the Bahrain International Investment

Park. Having already established its presence in the country, Kraft is looking to develop further its

operations and has been pursuing a drive to become more environmentally friendly. Paying particular

attention to the water scarcity issue in Bahrain, in mid-2009 the company announced that it had reduced

the amount of water used in manufacturing by 21% since 2005, having reached its targeted goal two years

early.

Bahrain Food & Drink Report Q1 2011

© Business Monitor International Ltd Page 30

Market Overview

Agriculture

Given its geographical restrictions and desert climate, Bahrain is highly dependent on food and drink

imports to meet the needs of its population. Most of these imports are sourced from the US and Saudi

Arabia. The government has made some efforts to address this dependence, such as its investments in

poultry farms, as it has generally sought to diversify the economy away from the oil industry. However,

the country’s agricultural sector still only employs just over 1% of the population while contributing less

than 0.7% to GDP.

The reality is that despite heavy government subsidies, which have prevented the country from falling

even further behind in terms of self-sufficiency, the sector is held back considerably by a climate

unsuitable for most forms of agriculture. Bahrain receives minimal rainfall, with annual harvests and

outputs highly dependent on whether the sector has been fortunate enough to receive favourable weather

conditions during the year. This lack of consistency prevents continual reinvestment in the sector.

Similarly, the technological and harvesting techniques that need to be adopted to improve output in such

conditions require considerable investment. Despite the government’s commitment to diversification, it is

unlikely to be persuaded into making such a risky and low-return investment, when returns elsewhere, not