bae financial strategy fmfada board november 19, 2009

TRANSCRIPT

bae

Financial Strategy

FMFADA Board

November 19, 2009

bae

Today’s AgendaToday’s Agenda

BAE/RCLCO Analysis

Capital market conditions

Developers in down markets

Current RFI/Q/P solicitation strategy

Master versus multiple developer partners

FMFADA as “master developer”

Recommended revision to developer RFI/Q/P process

bae

BAE and RCLCO AnalysisBAE and RCLCO Analysis

In the course of performing their respective work, BAE and RCLCO have independently come to the same conclusion regarding FMFADA’s master developer RFI/P/Q strategy

BAE and RCLCO have conferred over the past several weeks and prepared a joint analysis for FMFADA

This presentation shares our analysis and recommendations

bae

Big Picture Economic ConditionsBig Picture Economic Conditions

National economy emerging from steep recession

• 8M jobs lost

• Unemployment at 26-year high

Blue Chip Economic Indicators - November Forecast for 2010

• Consensus forecast GDP growth @ 2.7%

• Growth slower than normal recovery

• 1.4% disposable personal income growth

• 2% inflation

Wall Street Journal Survey - November Survey for 2010

• Average forecast of solid 2.9% GDP growth

• Employment growth slow - 600,000 non-farm jobs

• Low inflation @1.8%

• Shape of recovery:

• Half of respondents: “U-shaped” -slowness followed by solid growth

• 31% “V-shaped” -strong rebound

• 11% “L-shaped” - economy stabilizes at lower level

• 7% “W-shaped” or “Double-dip” recession

bae

Constraints on Capital AvailabiliityConstraints on Capital Availabiliity

Real estate credit markets have been “frozen” for the past 18 months and despite some recent “thawing” remain extremely challenging.

The “great de-leveraging” of commercial real estate is expected to absorb much of real estate capital over the next several years, constraining capital available for new projects.

$950B+/- commercial real estate debt maturing over next three years

bae

Lack of capital will constrain developer response to opportunities at Fort Monroe, particularly for new development

Developers are reluctant to expend precious equity dollars for pre-development activities as would be required for planning new development at Fort Monroe

Soliciting a master developer for the entirety of Fort Monroe will attract interested parties seeking to “tie-up” the property and “wait-out” the market

Developers in Down MarketDevelopers in Down Market

bae

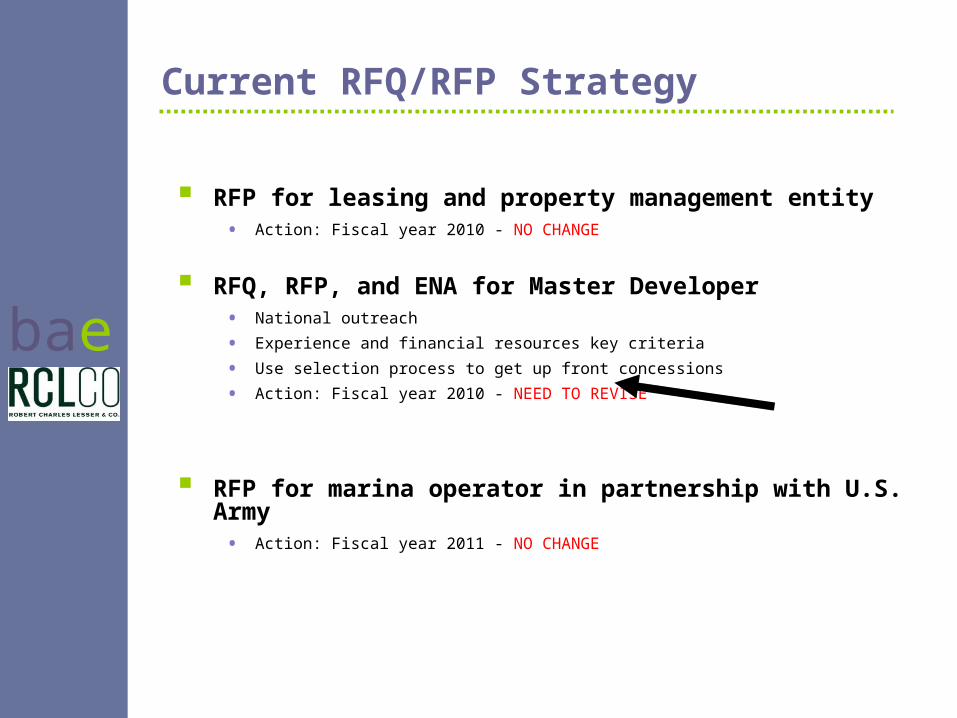

Current RFQ/RFP Strategy

RFP for leasing and property management entity• Action: Fiscal year 2010 - NO CHANGE

RFQ, RFP, and ENA for Master Developer• National outreach

• Experience and financial resources key criteria

• Use selection process to get up front concessions

• Action: Fiscal year 2010 - NEED TO REVISE

RFP for marina operator in partnership with U.S. Army• Action: Fiscal year 2011 - NO CHANGE

bae

Master Developer Pros and Cons Master Developer Pros and Cons

Pros:

• Single entity handles real estate on behalf of FMFADA

• Integrated planning and development

• Access to private/public debt and equity markets

• “Lean and mean” staffing of FMFADA

Cons:

• Risky: “All of one’s eggs in one basket”

• Encumbers Fort Monroe if partner’s financial conditions deteriorate

• Rare for one developer to excel in all development types

• Financial returns: reduced due to lease “sandwiches” with sub-developer

• Too many financial pockets to feed

• Lack of control: economic and programmatic interests not always aligned

bae

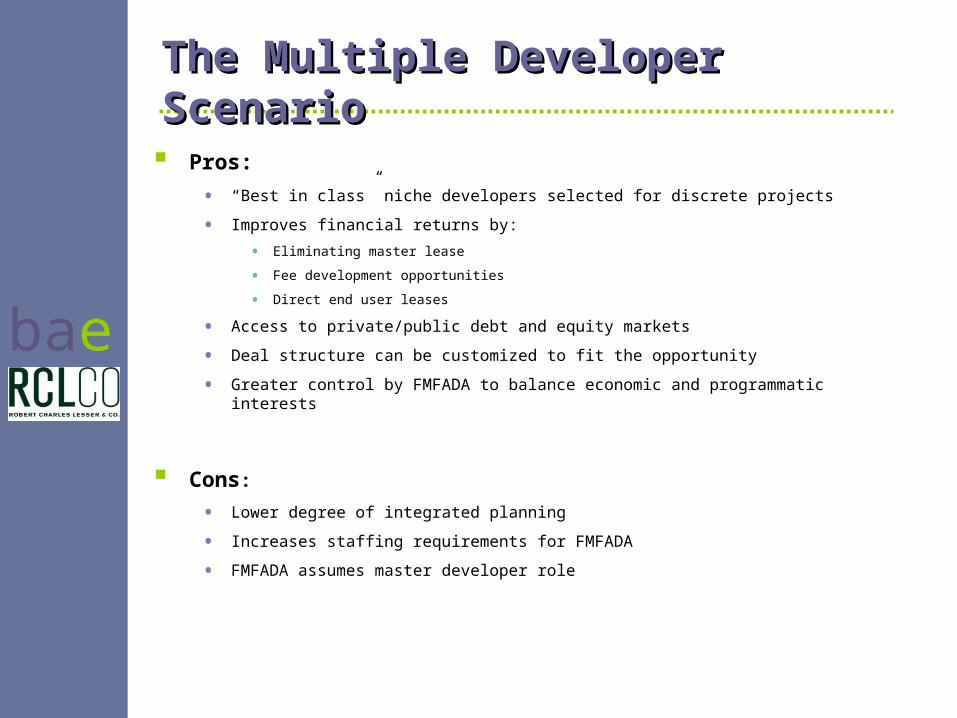

The Multiple Developer Scenario The Multiple Developer Scenario

Pros:

• “Best in class” niche developers selected for discrete projects

• Improves financial returns by:

• Eliminating master lease

• Fee development opportunities

• Direct end user leases

• Access to private/public debt and equity markets

• Deal structure can be customized to fit the opportunity

• Greater control by FMFADA to balance economic and programmatic interests

Cons:

• Lower degree of integrated planning

• Increases staffing requirements for FMFADA

• FMFADA assumes master developer role

bae

FMFADA as Master Developer FMFADA as Master Developer

Integrated planning

Overall real estate marketing and branding

Infrastructure financing and construction

Lease negotiation and execution

Project coordinating and monitoring

Lease administration

Under a multiple development partner scenario the FMFADA acts as master developer providing:

Under a multiple development partner scenario the FMFADA acts as master developer providing:

As a master developer, FMFADA will require a larger staff than previously planned.

As a master developer, FMFADA will require a larger staff than previously planned.

bae

174 historic residences

Good to excellent condition

Have value today that can be leveraged

Low-to-moderate capital investment required

Can be offered on a cluster-by-cluster or neighborhood basis

Developer can be engaged on “fee” basis

• Developer invests little of own capital and is compensated by a fee (percent of project value and performance bonus)

Leaseholds used as collateral to secure financing

Near Term Development Opportunity

Prepaid Residential LeaseholdsPrepaid Residential Leaseholds

bae

Recommendations

Adopt a multiple developer approach

Reduce scope of first RFI/P/Q to Residential Lease Program

Postpone Industry forum to mid-2010• Allows participation of new Interim Director of Real Estate

• Permits FMFADA to resolve planning, historic tax credit, and infrastructure issues

• Time to formulate Residential Leasehold program details

“Soft” Marketing Campaign• Identify and brief potential “best in class” developers

• Ensure developer market understands and buys into program

• Line up local lender and real estate community support

• Need to ensure qualified developer response

bae

Background Slides

bae

Concept approved by Board:

Offer long-term (50+ year) leases of historic residences with pre-payment of rent

Establish endowment/pay for capital costs with proceeds

Issues:

• Pioneering product in Hampton Roads

• Need to develop support infrastructure (e.g, local lenders, brokers, title companies)

• Avoiding fixed rental rates/avoiding “surprises” to leaseholders

• Capturing future property appreciation

Examples:

• Sea Colony, Delaware

• Pensacola, Florida

• Jekyll Island, Georgia

• Palm Desert/Palm Springs, California

Residential Leasehold Program

• Hawaii

• Santa Inez, California

• Universities/Colleges

• Land Trusts

bae

Capital Requirements: “Three Buckets”

Reuse and redevelopment of Fort Monroe will require significant capital at three levels:

This suggests different contractual arrangements and deal structures with private management and development entities.

Interim Leasing

•Own land and improvements “free & clear”•Minor upgrades•Little capital at risk• Exposure to “market” risk • Leasing and property management functions

LowLow MediumMedium HighHighNew Construction

• Own land only• New construction of improvements & infrastructure• Highest capital requirement• Highest level of risk• 3rd-party capital required

Residential Leasehold

• Own land and improvements “free & clear”• Moderate unit rehab • Site & parking improvements • 3rd-party capital required