b&a%20consumer%20confidence%20tracker%20may%202014

DESCRIPTION

http://www.banda.ie/assets/files/pdf/B&A%20Consumer%20Confidence%20Tracker%20May%202014.pdfTRANSCRIPT

Consumer Confidence Tracker

May 2014

PREPARED BY:Luke Reaper and Ciara McCarthy

Behaviour & AttitudesJ.5270

2 2

Introduction

3

Introduction

This report presents the findings of the latest phase of the Behaviour &

Attitudes’ Consumer Confidence Tracker.

Survey results for this phase are based on a sample of 1,006 adults aged

16+, quota controlled in terms of age, gender, socio-economic class and

region to reflect the profile of the adult population of the Republic of

Ireland.

All interviewing on the survey is conducted on our fortnightly face-to-face

Barometer by trained members of the B&A field force working under

ESOMAR guidelines.

Fieldwork on the latest wave was carried out between 10th – 20th of April

2014.

4

About Behaviour & Attitudes

Behaviour and Attitudes is Ireland’s largest and most experienced

independently owned research company.

We pride ourselves on having the most experienced director team

in Ireland. All projects have a director involved.

Established over 25 years ago, Behaviour and Attitudes provides a full

range of market research services, ranging from CAPI, CATI, online and of

course qualitative.

Specialist sectors include: Retail & Shopper, Technology & Telecoms, Media,

Financial, Political & Social, Polling, Automotive, Healthcare and Public

Sector & Utilities.

For more information please visit our website at: www.banda.ie or contact

us on +353 1 2057500.

5

Summary

Looking forward, consumers are the most confident they’ve ever been since the start of this study. Almost 1 in 3 adults now believe that improvements to the economy will be made in one years time. We have finally entered positive territory.

While consumers agree that things have improved, they remain sceptical about how they spend/save their own personal finances. Disposable income is still low, this the macro optimism has yet to filter down to the consumer level. Those outside Dublin display most scepticism (albeit improvements are being registered) – those outside Dublin lag Dubliner optimism.

Encouragingly, unemployment levels are the lowest they’ve been since the start of the global recession, and employment is expected to increase by 2% this year alone.

7 7

The Macro Context

8

At a Macro Level, Improvements to Irelands Domestic Economy are evident…

Source: CSO Estimates as of 14th May 2014/EY Economic Eye Summer Report (2013)/ESRI Quarterly Commentary (2013)

-1.5 -1.5

-0.6

-3.6

-1.1

-1.5 -1.3

-1.0

0.9

-0.4

0.7

-1.2

1.7 1.5

-0.4

0.6

-0.3

0.7

-1.7

0.2

-1.1

1.0

1.5

-2.3

2.2

0.9

-1.3

-2.7 -2.8

-2.4

-2.8

-1.9

-0.9

0.3

1.8

2.2

0.8

-3.3

-0.0

0.1

-1.3

0.6

-2.3

0.4

2.0

-0.1

1.6

0.2

2.7

-4.0

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0GDP GNP

0

2008 2009 2010 2011 2012 2013 2014(FORECASTED

TOTAL)

Ireland’s GDP experienced positive growth during Q2 and Q3 2013, GNP also improved in Q3 2013. In 2014, GDP is forecasted to increase by a further 2.2%.

9

Exports – Improvements are evident, driven by Higher Food and Chemical Exports

-1.1

-3.8

6.2

5.0

2.9

2.2

4.24.5

2008 2009 2010 2011 2012 2013 2014 (f) 2015 (f)

% Annual Growth

Source: EY Economic Eye Summer Report (2013)/Bord Bia Export Performance & Prospects Report (2014)/CSO Goods Exports and Imports (March 2014).

Irelands exports rose by 4% to

€7.031 billion in January 2014 vs. January 2013.

Food +9.8% €2,136million

Chemicals +22.2% €203million

Main Contributors(Jan-March 2014 vs. 2013)

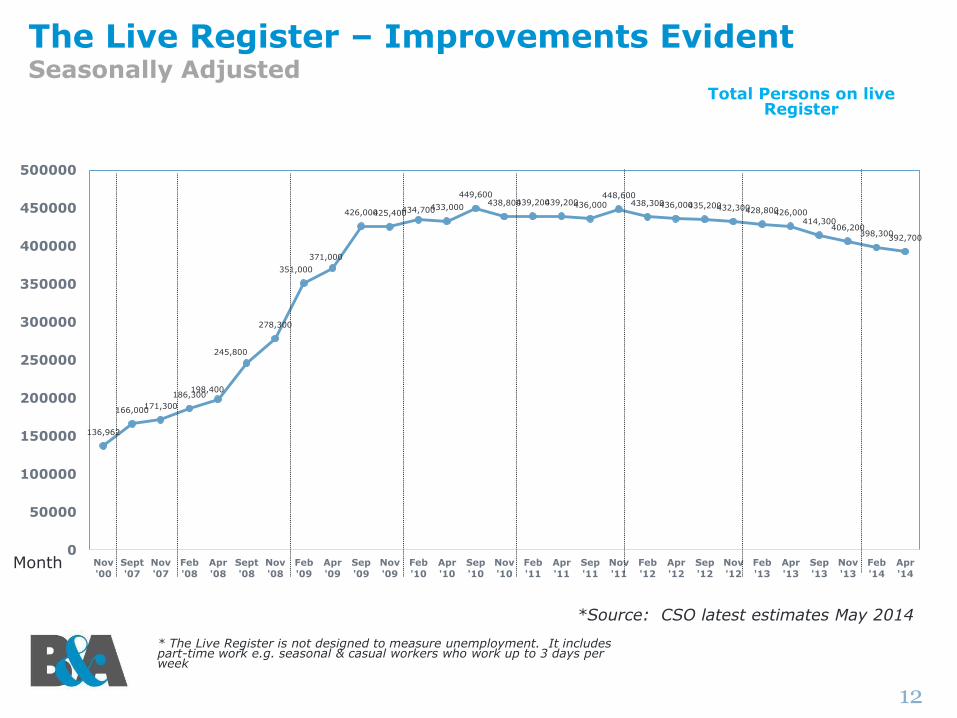

The number of people on the Live Register is the

lowest levelrecorded since April 2009.

Source: CSO latest Estimates (April 2014)

11Source: CSO Estimates as of 15th May 2014

-7.8%Overall Change vs. April 2013.

-2.3%vs. April 2013

-9.6%vs. April 2013

11.7%Current Rate of unemployment.

149,018 239,541

The Live Register

1213.8 14.6 14.7

13.611.7

0

5

10

15

20

2009 2010 2011 2012 2013 Apr '14

% Rate of Unemployment

The Live Register and Unemployment Figures

Unemployment in Ireland

-22.5% vs. peak in 2012 of 15.1%

12

The Live Register – Improvements EvidentSeasonally Adjusted

* The Live Register is not designed to measure unemployment. It includes part-time work e.g. seasonal & casual workers who work up to 3 days per week

*Source: CSO latest estimates May 2014

136,962

166,000171,300

186,300198,400

245,800

278,300

351,000

371,000

426,000425,400434,700433,000

449,600438,800439,200439,200436,000

448,600438,300436,000435,200432,300428,800426,000

414,300406,200

398,300392,700

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

Nov

'00

Sept

'07

Nov

'07

Feb

'08

Apr

'08

Sept

'08

Nov

'08

Feb

'09

Apr

'09

Sep

'09

Nov

'09

Feb

'10

Apr

'10

Sep

'10

Nov

'10

Feb

'11

Apr

'11

Sep

'11

Nov

'11

Feb

'12

Apr

'12

Sep

'12

Nov

'12

Feb

'13

Apr

'13

Sep

'13

Nov

'13

Feb

'14

Apr

'14

Total Persons on live Register

Month

13

A Somewhat Brighter Picture…

Source: Central Bank Quarterly Bulletin (April 2014)/ ESRI Quarterly Report (April 2014)/2013/EY Economic Eye Summer Report (2013)/B&A Consumer Confidence Index (April 2014).

Inflation edged up 0.3% in April 2014.

Employment is expected to increase by 2% in 2014.

GDP expected to grow by 2.2% and 2.6% in 2014 and 2015

respectively.

Disposable income is slowly increasing (+2% this Qtr. vs. last).

Unemployment rate set to decrease to 10.9% this year, and 10.4% in

2015.

Almost 1 in 3 adults agree that the country is better of now than it was

a year ago.

1414

Consumer ConfidenceFindings

15

-88-93 -91

-86-81

-50

-82

-86

-72 -59

-69-64

-56 -57-62

-51 -53

-46

-27-31

-7

0

-74 -76

-65

-58-54

-20

-74-70

-58

-45

-64

-52

-44-50

-60

-39-44

-36

-18

-25

-4

6

-100

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

10

Mar May Sept Nov Mar July Nov Jan Apr July Nov Mar May Sept Nov Feb Apr July Sept Dec Feb Apr

Looking Back

Looking Forward

The Future Looks Bright: Ireland Returns to Positive Territory for the First Time Since 2009

Balance +/-

2009 2010 2011 2012

Source: B&A Consumer Confidence Report

2013

Q.1 Thinking about the economy as a whole, do you think that the country is better off, worse off, or about the same as last year?

Q.2 And what about the coming year, do you think that the country will be better off, worse off or about the same as this year?

Dublin +16Outside +3

2014

19

The Economy:Looking Forward

20

The Economy: Looking Forward – We have finally entered positive territory, at least at a Macro LevelBase: All Adults 18+

Q.2 And what about the coming year, do you think that the country will be better off, worse off or about the same as this year?

26%

42%

32%

Dublin: +16

OutsideDublin: +3

2006 2007 2008 2009 2010 2011 2012 2013 Feb ‘14 Apr ’14

Gap = -15 -59 -68 -49 -58 -52 -32 -5 +6

Better of

The same

Worse of

April 2014

For the first time ever, consumers

feel that the economy will be better of next year vs. this year. This

opinion applies to those living in both Dublin and outside Dublin (albeit outside lags Dublin).

21

The Economy: Looking Forward – We have finally entered positive territory, at least at a Macro LevelBase: All Adults 18+

Q.2 And what about the coming year, do you think that the country will be better off, worse off or about the same as this year?

0

-15

-59

-68

-49

-58

-52

-32

-5

6

2006 2007 2008 2009 2010 2011 2012 2013 Feb '14 Apr '14

Consumers are more positive about the future of the Irish Economy now than they have been in the history of this study.

24

Economy – Looking Forward Trended x Region Base: All adults 18+

-44

-61

-42

-32-30

-4

-20

7

16

-52

-60

-38

-48

-39

-23

-36

-9

3

-70

-65

-60

-55

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

20

Sep 12 Nov 12 Feb-13 Apr-13 Jul-13 Sep-13 Nov-13 Feb-14 Apr-14

Dublin

Outside Dublin

Q.1 Thinking about the economy as a whole, do you think that the country is better off, worse off, or about the same as last year?

Balance +/-

2012 2013

The gap between Dublin and outside still

exists, however both registered a dramatic increase in confidence this

wave. Outside Dublin has finally

left negative territory.

2014

25

Balance Of Opinion - Economy

Balance +/-

YEARLY AVERAGES 2012

Long Term Short Term

2013

When viewed longitudinally a pattern of consistent improvement has been noted over the past three years.

2014

-40

-59

-13

38

-6

-64

-89

-71 -71

-59

-42

-64

-56 -57-62

-51-55

-46

-27-31

-70

-36

-50

-17

-2 0

-15

-59

-68

-49

-58-52

-32

-52

-44-50

-60

-39-44

-36

-18-25

-4

6

-100

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

10

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Mar May Sept Nov Feb Apr July Sept Dec Feb Apr

Looking Back

Looking Forward

26

Personal Finances

31

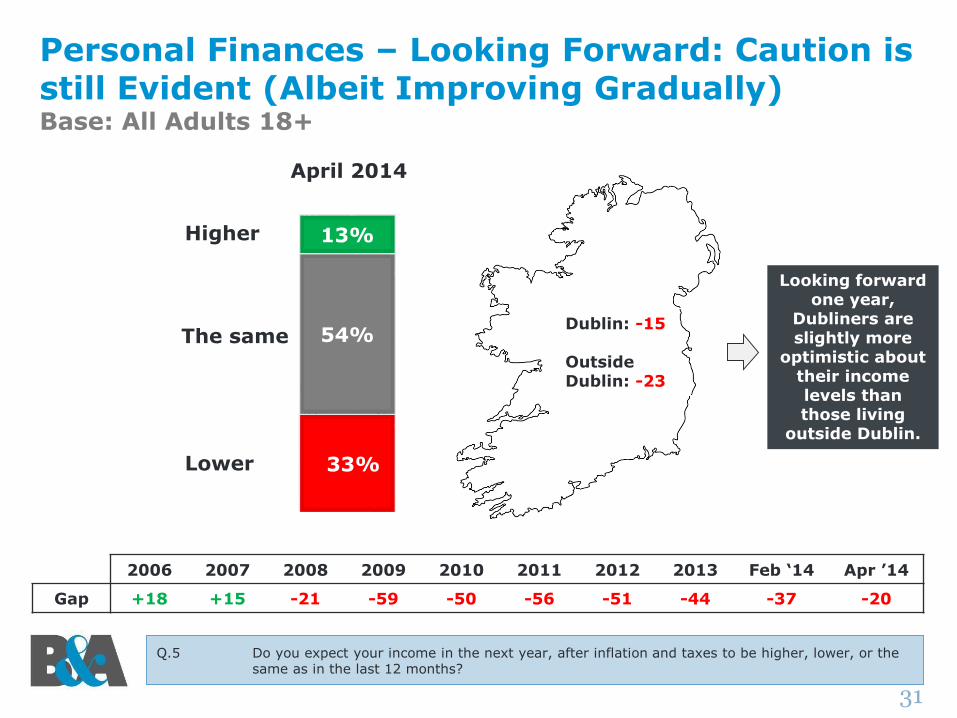

Personal Finances – Looking Forward: Caution is still Evident (Albeit Improving Gradually)Base: All Adults 18+

Q.5 Do you expect your income in the next year, after inflation and taxes to be higher, lower, or the same as in the last 12 months?

33%

54%

13%

Dublin: -15

OutsideDublin: -23

2006 2007 2008 2009 2010 2011 2012 2013 Feb ‘14 Apr ’14

Gap +18 +15 -21 -59 -50 -56 -51 -44 -37 -20

Higher

The same

Lower

April 2014

Looking forward one year,

Dubliners are slightly more

optimistic about their income levels than those living

outside Dublin.

32

Price Increases Across Some Sectors Perhaps Contributing to Increased Caution

Source: Consumer Price Index (April 2014)

+4.5%

+3.7%+3.2%

+2.0%

-3.7%

-2.1%

Education Alcohol and

Tobacco

Misc. goods and

services

Restaurants and

hotels

Clothing and

footwear

Food and non-

alcoholic

beverages

Grew primarily due to higher health and motor insurance premiums and the increased costs associated with the local property tax

Increased due to higher prices for alcohol sold in off licences and supermarkets and higher tobacco prices.

Fell due to clothing and footwear sales.

Decreased due to lower prices across a range of products such as vegetables, bread and cereals, and meat.

Increased largely due to higher prices for alcoholic drinks and food consumed in licensed premises, restaurants, cafes, and canteens.

April 2014 vs. April 2013

33

24% 27%

17%13% 12% 13%

34%

64%57%

63%59%

51%58% 56% 59% 59%

55%60%

53%

44% 44% 45%

33%

54% 54%

58%58%

58% 59%

52%

30%

35%31%

34%

41%35% 37% 34% 34%

38%34%

41%

46% 47% 46%

54%

22% 22%25% 25%

30% 28%

13%5% 7% 7% 7% 8% 8% 7% 7% 7% 7% 6% 6%

10% 9% 9%13%

Q.5 Do you expect your income in the next year, after inflation and taxes,

to be higher, lower or the same as in the last twelve months?

Personal Finances – Looking Forward

Higher

The same

Lower

Expect it to be …

Gap -2 -8 +8 +16 +18 +15 -21 -59 -50 -56 -51 -44 -50 -49 -52 -52 -48 -54 -47 -34 -35 -37 -20

The gap is decreasing each year and has returned to match that of 2008 (hence, improvements are being made).

LONG TERM 2012 2013

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Mar May Sept Nov Feb April July Sept Dec Feb Apr

2014

35

Personal Finances - Looking Forward x Region Base: All adults 18+

-43

-54 -54

-48

-53

-39

-27

-40

-15

-55-55

-45

-56

-44

-33

-39

-35

-23

-70

-65

-60

-55

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

Sep 12 Nov 12 Feb-13 Apr-13 Jul-13 Sep-13 Dec-13 Feb-14 Apr-14

Dublin

Outside Dublin

Q.5 Do you expect your income in the next year, after inflation and taxes,

to be higher, lower or the same as in the last twelve months?

Balance +/-

Those living outside Dublin feel marginally more positive

about their personal

finances for the year ahead.

2012 2013 2014

36

Balance Of Opinion - Personal Finances

Balance +/-

-23

-34

-11

14 4

-35

-63-58

-61-57

-47

-61-56

-52

-59

-52-55

-47

-38-44

-36

-21

-2-8

8

16 1815

-21

-59

-50-56

-51

-44-50 -49

-52 -52-48

-54

-47

-34-35

-37

-21

-75

-65

-55

-45

-35

-25

-15

-5

5

15

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Mar May Sept Nov Feb Apr July Sept Dec Feb Apr

Looking Back

Looking Forward

Long Term Short Term

Gains being made over time. However we are still in negative territory.

YEARLY AVERAGES 2012 2013 2014

37

Savings

38

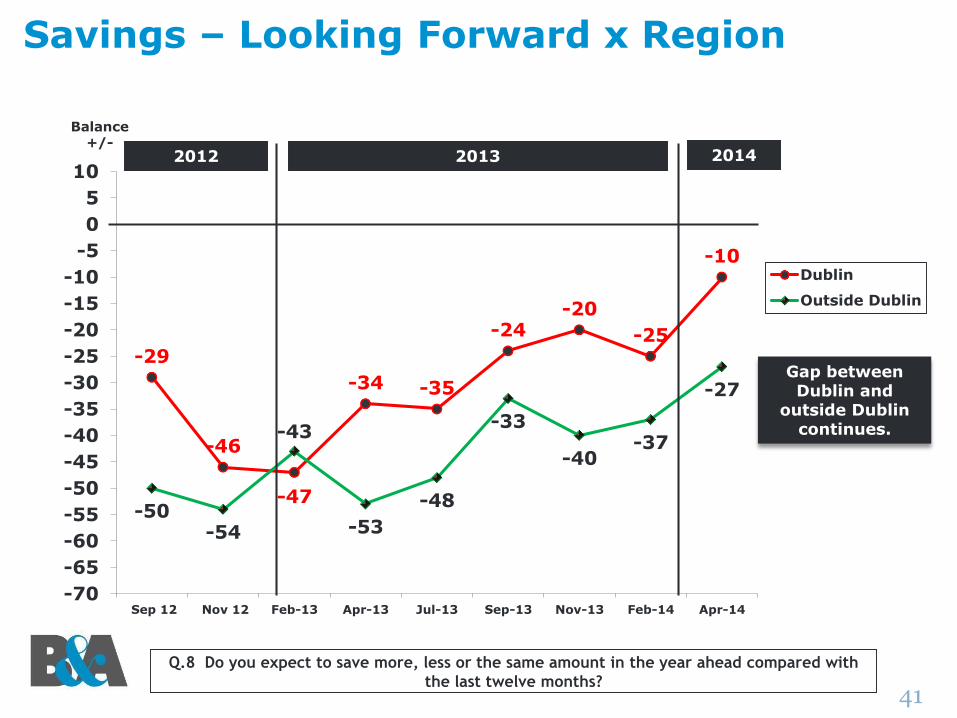

Saving Levels– Looking ForwardBase: All Adults 18+

Q.8 Do you expect to save more, less or the same amount in the year ahead compared with the last twelve months?

33%

57%

10%

Dublin: -10

OutsideDublin: -27

2006 2007 2008 2009 2010 2011 2012 2013 Feb ‘14 Apr ’14

Gap -1 -5 -34 -56 -48 -50 -48 -40 -33 -23

Higher

The same

Lower

April 2014

Dubliners are slightly more

likely to save in the year ahead vs.

those living outside Dublin. Both, however,

remain in negative territory.

41

Q.8 Do you expect to save more, less or the same amount in the year ahead compared with

the last twelve months?

Savings – Looking Forward x Region

-29

-46

-47

-34 -35

-24-20

-25

-10

-50-54

-43

-53

-48

-33

-40-37

-27

-70

-65

-60

-55

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

Sep 12 Nov 12 Feb-13 Apr-13 Jul-13 Sep-13 Nov-13 Feb-14 Apr-14

Dublin

Outside Dublin

Balance +/-

Gap between Dublin and

outside Dublin continues.

2012 2013 2014

42

Personal Assets

43

Personal Assets: Looking ForwardBase: All Adults 18+

Q.6 Do you expect your assets (your house, shares, pension entitlements, savings) in the next year to be higher, lower or the same as in the past year?

16%

69%

15%

Dublin: +6

OutsideDublin: -3

2006 2007 2008 2009 2010 2011 2012 2013 Feb ‘14 Apr ’14

Gap +33 +20 -25 -53 -43 -41 -31 -18 -8 -1

Higher

The same

Lower

April 2014

Those living in Dublin feel

slightly more optimistic about their

personal assets looking

ahead vs. those outside

Dublin.

46

Q.6 Do you expect your assets (your house, shares, pension entitlements, savings)

In the next year to be higher, lower or the same as in the past year?

Personal Assets– Looking Forward x RegionExpect them to be …

-25 -29

-18-21

-12-9

+20 +6

-34 -33

-22

-32

-23

-11 -13-11

-4

-70

-65

-60

-55

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

Sep 12 Nov 12 Feb-13 Apr-13 Jul-13 Sep-13 Dec-13 Feb-14 Apr-14

Dublin

Outside Dublin

Balance +/-

Dublin has returned to

positive territory this wave, whilst

outside Dublin remains in

negative territory (albeit improving).

2012 2013 2014

47

Purchasing Goods and Services

48

Purchasing Goods and Services – Looking Forward: Improvements are EvidentBase: All Adults 18+

Q.7 In the year ahead, do you expect to purchase more, less or the same amount of goods and services as in the past year?

26%

64%

10%

Dublin: -9

OutsideDublin: -19

2006 2007 2008 2009 2010 2011 2012 2013 Feb ‘14 Apr ’14

Gap +7 +5 -29 -63 -47 -52 -45 -37 -30 -16

More

The same

Less

April 2014

Dubliners feel slightly more

confident about spending in the coming year vs.

those living outside Dublin

(albeit they remain in negative

territory).

51

Q.7 In the year ahead, do you expect to purchase more, less or the same amount of goods and services as in the past year?

Purchasing Goods And Services – Looking Forward x RegionExpect to purchase …

-41

-46

-48

-31-34

-21 -24

-33

-9

-45

-50

-42

-47

-42

-32 -31

-28

-19

-70

-65

-60

-55

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

Sep 12 Nov 12 Feb-13 Apr-13 Jul-13 Sep-13 Dec-13 Feb-14 Apr-14

Dublin

Outside Dublin

Balance +/-

2012 2013 2014

52

69

21

31 33

20

-25

-53

-43-41

-31

-18

-39

-28-31 -33

-21

-29

-20

-10 -9 -8

-1

-10 -12 -12

47 5

-29

-63

-47-52

-45

-37

-46

-40-44

-48-43 -43

-40

-29 -29 -30

-16

-23-28

-8-5

-1-5

-34

-56

-48 -50 -48

-40

-51

-42-45

-52

-44-48

-44

-31-34 -33

-23

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

40

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Mar May Sept Nov Feb Apr July Sept Dec Feb Apr

Assets Value

Purchase

Savings

Balance Of Opinion in Summary – The Year AheadExpectations in regard to assets value, purchases, and savings

Balance +/-

Long Term Short Term

Improvements are noted and momentum is slowly improving. However, any further imposition that directly affects real incomes of consumers will impact this area negatively.

Growth in personal financial situations continues to be finely balanced.

YEARLY AVERAGES 2012 2013 2014

Disposable Income

54

€50.94

€61.29

€83.97

€62.32

€46.86€43.57

€47.08 €47.23€51.06

€43.66 €42.97 €43.85

2001 2004 2008 2010 2012 Feb

'13

Apr

'13

Jul '13 Sept

'13

Dec

'13

Feb

'14

Apr

'14

Discretionary Income Has Halved in 5 Years but decline appears to have abatedBase: All adults 18+

Q. About how much would you say you spend each week on things you buy for yourself including money spent on clothes, eating out, going for a drink, going to the cinema, gambling, sporting activities and so on?

LONG TERM SHORT TERM

Dublin €50.23Outside Dublin €41.33 ABC1 €51.78C2DE €38.47