b s r & co. llp specified domestic transactions pankil ... · specified domestic transactions...

TRANSCRIPT

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Specified Domestic Transactions

Pankil Sanghvi Director

10 October 2015

1

B S R & Co. LLP

Background

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Genesis of Domestic Transfer Pricing Regulations

Supreme Court (SC) in the case of CIT v Glaxo SmithKline Asia (P) Ltd [195 Taxman 35(SC)]

• Recognized ― Revenue neutrality of domestic transactions except in case of taxarbitrage on account of tax holiday or loss making situations

• Certain sections of the Act provide for determination of expenses / profits having regardto fair market value (FMV). However the manner of determination of FMV is notprescribed. Accordingly to reduce litigation, SC suggested that Finance Ministry shouldconsider making TP applicable to such sections

Intent of Law – Explanatory Memorandum to Finance Bill 2012

• Objectivity in ascertaining reasonableness of expenditure incurred between relatedparties and the appropriateness of profits earned by the business undertakings claimingtax holidays or deductions

• Create and obligation on assessees’ to maintain proper documentation

3

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Domestic Transfer Pricing regime in India

Scope of TP regulations expanded to include ‘specified domestic transactions’ (SDT)

• Expenses or payments made to domestic related persons as specified in Section40A(2)(b) of the Income-tax Act, 1961 (the Act)

• Transactions between undertakings of same taxpayer or transactions by taxpayer withclosely connected persons for the purpose of Chapter VI-A (which includes tax holidayprovisions like 80IA of the Act) and Section 10AA of the Act

SDT regime applicable from FY 2012-13 where value of SDTs in aggregate exceeds INR 5crores annually – threshold increased to INR 20 crores annually from FY 2015 – 16

Preparation of Form No 3CEB and transfer pricing (TP) study report mandatory even forSDTs – hence onus of identifying and reporting all covered transactions on the tax payers

Non-compliance with reporting requirements would now result in onerous additionalpenalties

4

SDTs -Payments to related parties [Sec 40A(2)(b)]

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Section 40A(2)(b) – only expenditure covered

The proposed section

Refers only to ‘expenditure’ incurred in payments made or to be made to persons specified under Section 40A(2)(b) of the Act

Does not refer to any ‘income’

Expenditure by one group entity is income for another group entity - arms length analysis may consider both transacting parties

Only the entity incurring the expense will need to complete the prescribed compliances

6

Capital expenditure and Availing of free services – debatable

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

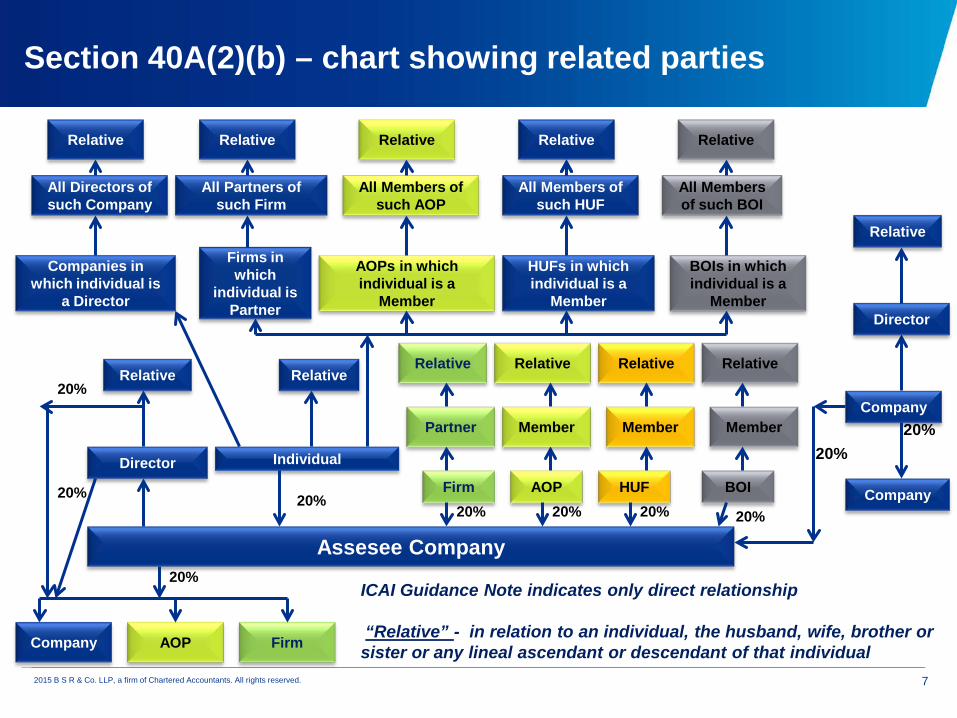

Section 40A(2)(b) – chart showing related parties

Assesee Company

Company

Company

20%Director

Relative

Individual

Relative

Companies in which individual is

a Director

All Directors of such Company

20%

AOPs in which individual is a

Member

All Members of such AOP

Firms in which

individual is Partner

All Partners of such Firm

HUFs in which individual is a

Member

All Members of such HUF

Firm AOP HUF20%

Relative

Company

20%

20%

20%Relative Relative

Partner

20% 20%

Member Member

Director

Relative

BOI

Relative

Member

20%

All Members of such BOI

BOIs in which individual is a

Member

AOP Firm

20%

Relative Relative Relative Relative Relative

ICAI Guidance Note indicates only direct relationship

“Relative” - in relation to an individual, the husband, wife, brother or sister or any lineal ascendant or descendant of that individual

7

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Related parties as mentioned u/s 40A(2)(b)

Coverage -Substantial direct

and indirect interest?

Transactions between sister concerns now

covered

Direct Interest

Indirect Interest

X

X1 X2

X

X1 X2

X3 X4

X5 X6 X7 X8

X3 X4

X5 X6 X7 X8

Indirect interest illustrated

8

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

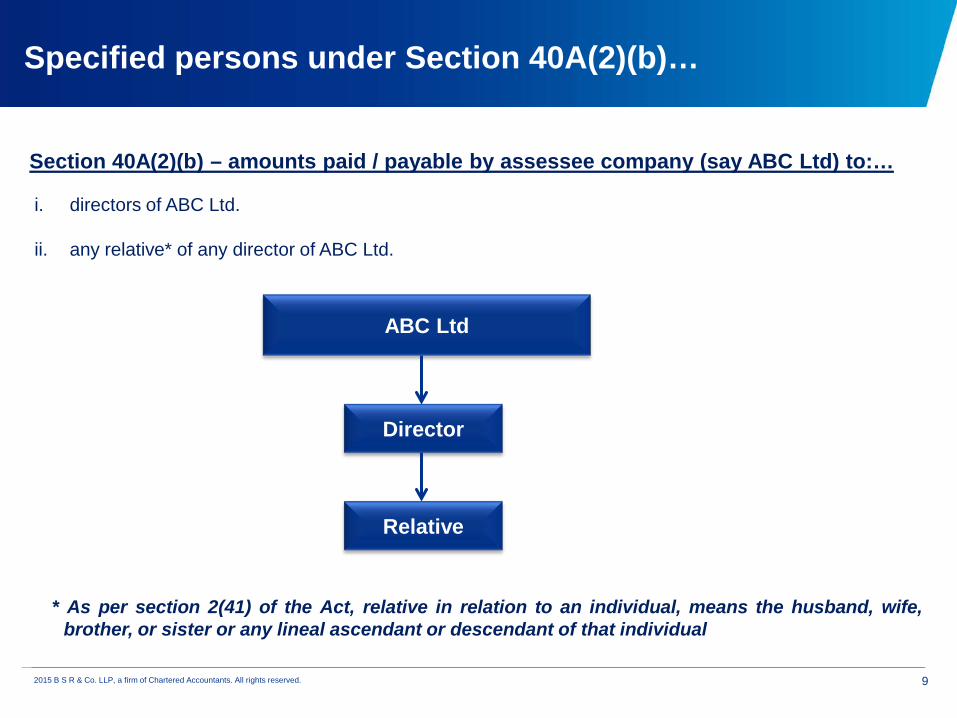

Specified persons under Section 40A(2)(b)…

Section 40A(2)(b) – amounts paid / payable by assessee company (say ABC Ltd) to:…

i. directors of ABC Ltd.

ii. any relative* of any director of ABC Ltd.

* As per section 2(41) of the Act, relative in relation to an individual, means the husband, wife,brother, or sister or any lineal ascendant or descendant of that individual

ABC Ltd

Director

Relative

9

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

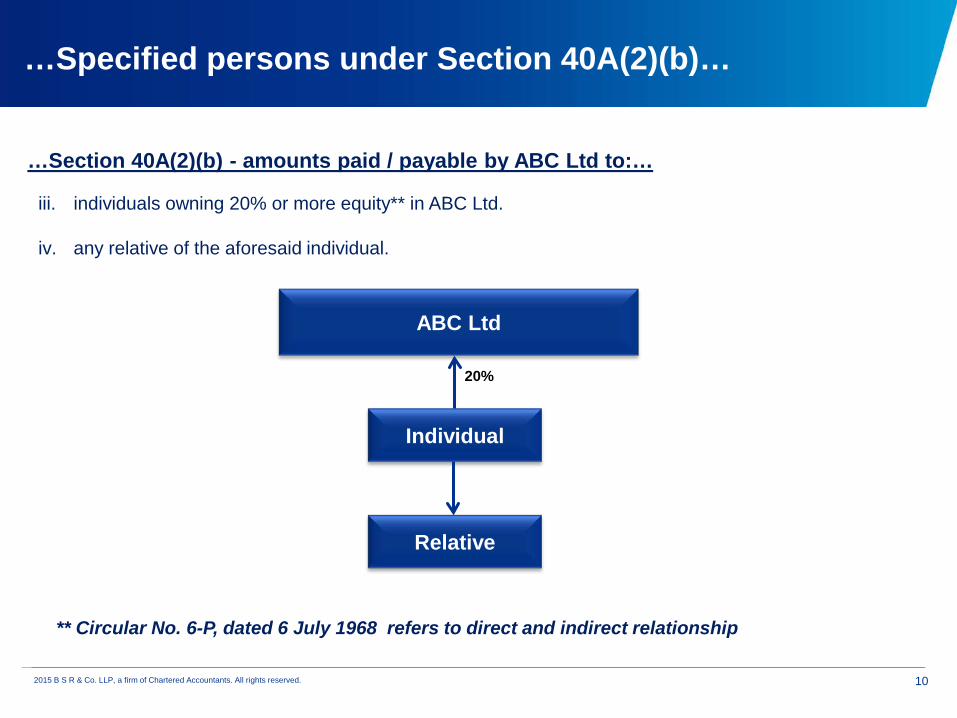

…Section 40A(2)(b) - amounts paid / payable by ABC Ltd to:…

iii. individuals owning 20% or more equity** in ABC Ltd.

iv. any relative of the aforesaid individual.

** Circular No. 6-P, dated 6 July 1968 refers to direct and indirect relationship

ABC Ltd

Individual

Relative

20%

…Specified persons under Section 40A(2)(b)…

10

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

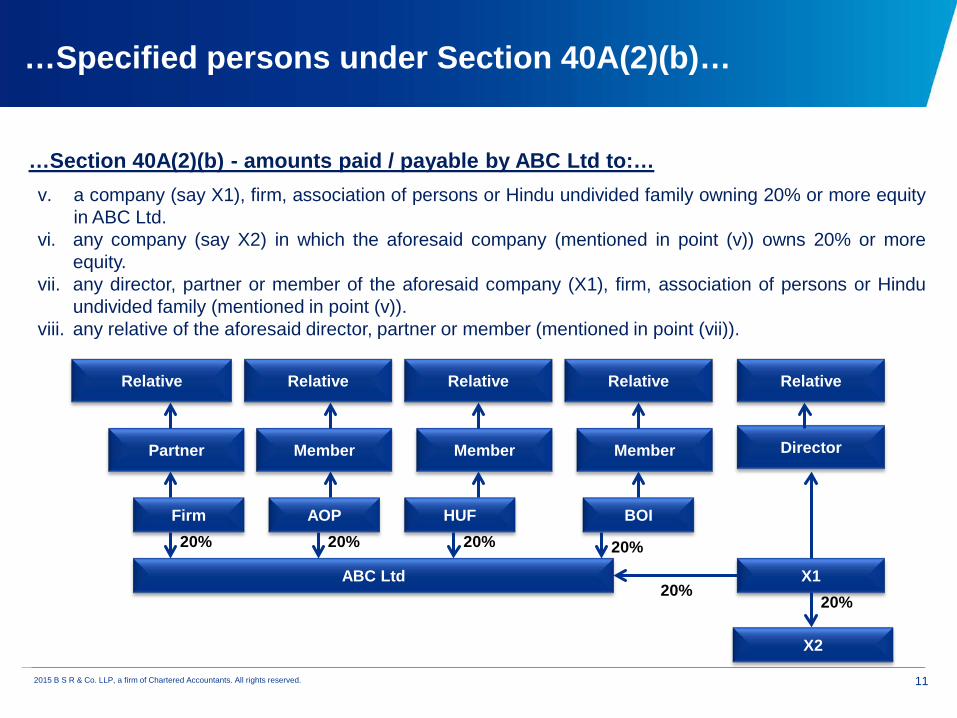

…Section 40A(2)(b) - amounts paid / payable by ABC Ltd to:…v. a company (say X1), firm, association of persons or Hindu undivided family owning 20% or more equity

in ABC Ltd.vi. any company (say X2) in which the aforesaid company (mentioned in point (v)) owns 20% or more

equity.vii. any director, partner or member of the aforesaid company (X1), firm, association of persons or Hindu

undivided family (mentioned in point (v)).viii. any relative of the aforesaid director, partner or member (mentioned in point (vii)).

ABC Ltd X1

X2

20%

Firm AOP HUF20%

Relative

20%

Relative Relative

Partner

20% 20%

Member Member Director

Relative

BOI

Relative

Member

20%

…Specified persons under Section 40A(2)(b)…

11

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

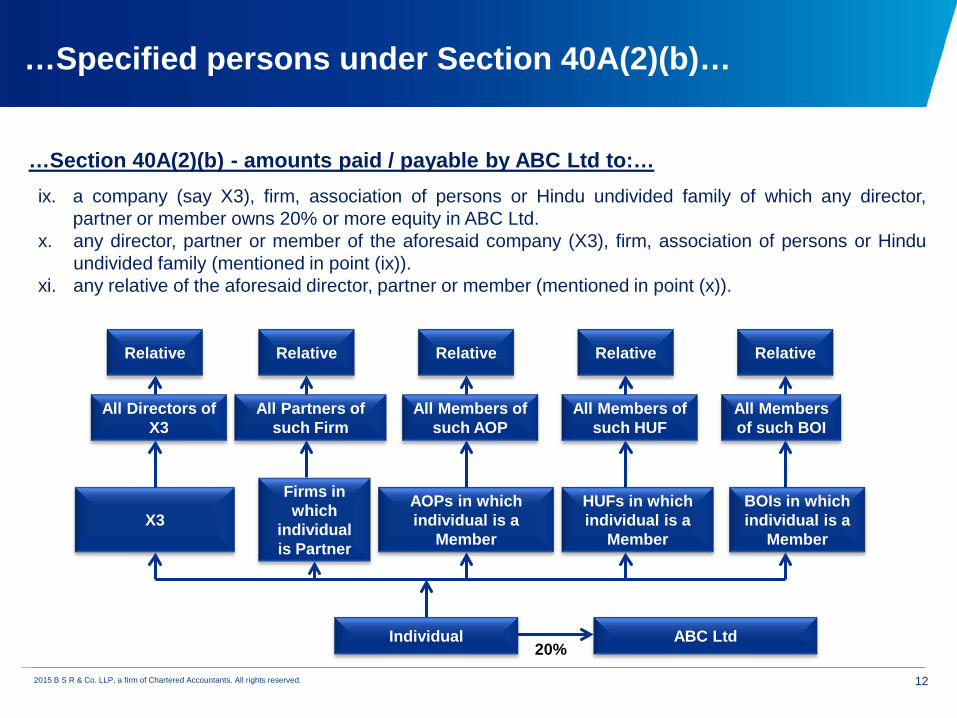

…Section 40A(2)(b) - amounts paid / payable by ABC Ltd to:…ix. a company (say X3), firm, association of persons or Hindu undivided family of which any director,

partner or member owns 20% or more equity in ABC Ltd.x. any director, partner or member of the aforesaid company (X3), firm, association of persons or Hindu

undivided family (mentioned in point (ix)).xi. any relative of the aforesaid director, partner or member (mentioned in point (x)).

Individual

X3

All Directors of X3

AOPs in which individual is a

Member

All Members of such AOP

Firms in which

individual is Partner

All Partners of such Firm

HUFs in which individual is a

Member

All Members of such HUF

All Members of such BOI

BOIs in which individual is a

Member

Relative Relative Relative Relative Relative

ABC Ltd20%

…Specified persons under Section 40A(2)(b)…

12

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

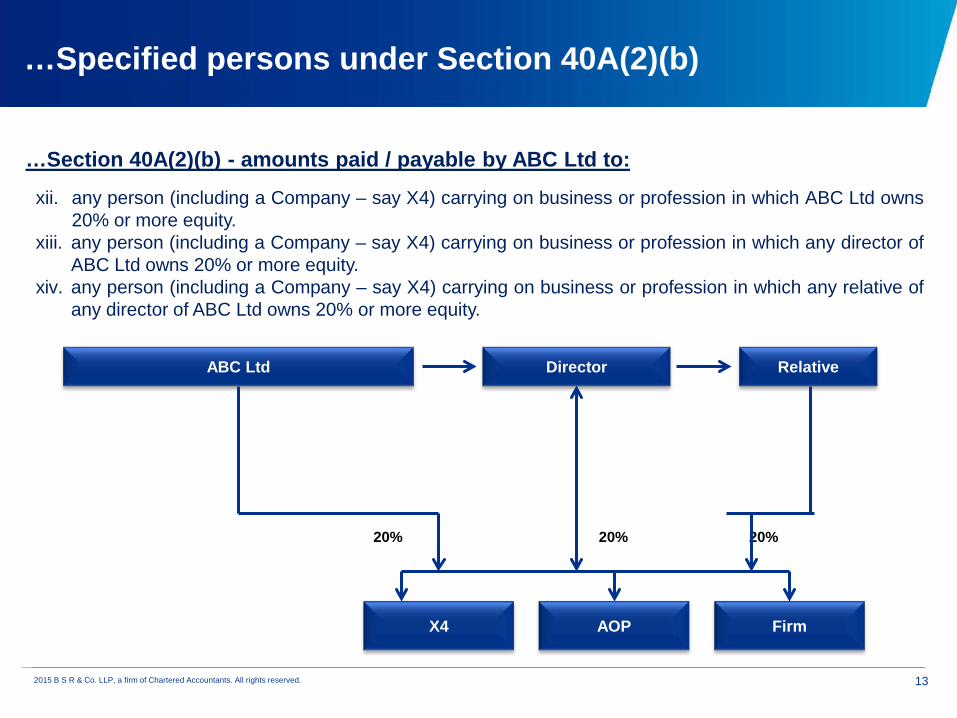

…Section 40A(2)(b) - amounts paid / payable by ABC Ltd to:

xii. any person (including a Company – say X4) carrying on business or profession in which ABC Ltd owns20% or more equity.

xiii. any person (including a Company – say X4) carrying on business or profession in which any director ofABC Ltd owns 20% or more equity.

xiv. any person (including a Company – say X4) carrying on business or profession in which any relative ofany director of ABC Ltd owns 20% or more equity.

Director Relative

X4

20%

AOP Firm

20%

ABC Ltd

20%

…Specified persons under Section 40A(2)(b)

13

SDTs – units availing a tax holiday

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Tax holiday unit Other unit

Sub-section (8) of section 80-IA (and similar such provisions in Chapter VI –A)

Inter unit transfers (goods and services etc.)

Other person having close connection

Tax holiday company

Business transacted (wider than transfer of goods orservices)

Sub-section (10) of section 80-IA (and similar such provisions in Chapter VI –A)

Not corresponding to market value [adherence to arm’s length price (ALP) proposed]Appropriate allocation keys to be used to allocate costs and overheads for computation of tax holiday

Revenue will challenge use of ad-hoc allocation keys

More than ordinary profits earned by business unit claiming deduction (adherence to ALP proposed)

Corresponding provisions to the above would be covered in Chapter VI-A and Section 10AA

Transactions to be reported in Accountant’s Report and their arms’ length nature to be substantiated in the TP Report

Anti abuse conditions under tax holiday provisions

15

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

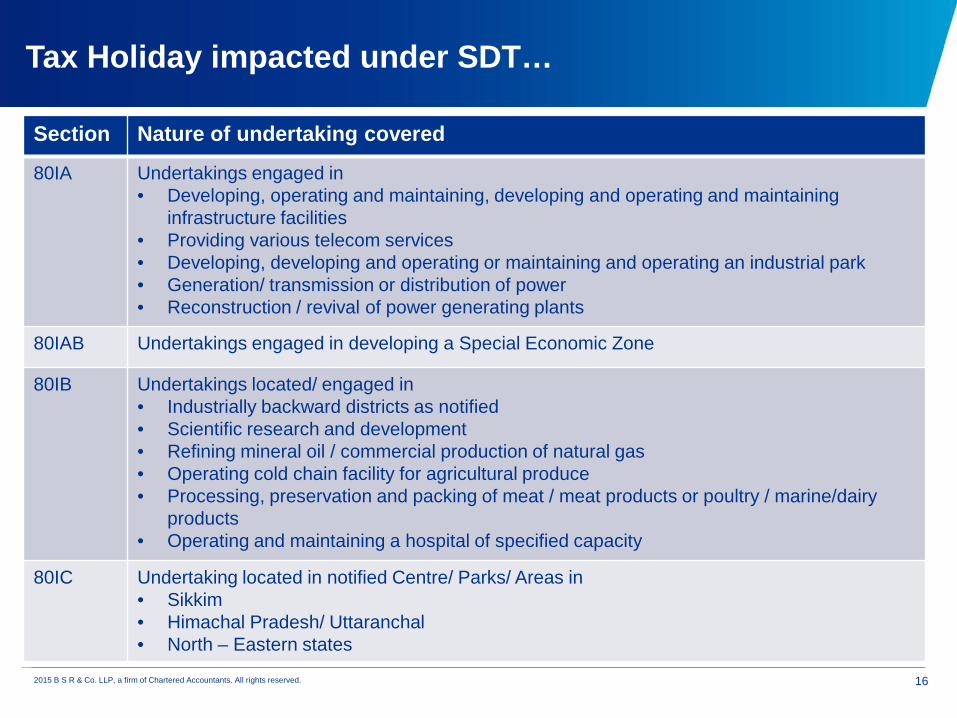

Tax Holiday impacted under SDT…

Section Nature of undertaking covered

80IA Undertakings engaged in• Developing, operating and maintaining, developing and operating and maintaining

infrastructure facilities• Providing various telecom services• Developing, developing and operating or maintaining and operating an industrial park• Generation/ transmission or distribution of power• Reconstruction / revival of power generating plants

80IAB Undertakings engaged in developing a Special Economic Zone

80IB Undertakings located/ engaged in • Industrially backward districts as notified• Scientific research and development• Refining mineral oil / commercial production of natural gas• Operating cold chain facility for agricultural produce• Processing, preservation and packing of meat / meat products or poultry / marine/dairy

products• Operating and maintaining a hospital of specified capacity

80IC Undertaking located in notified Centre/ Parks/ Areas in• Sikkim• Himachal Pradesh/ Uttaranchal• North – Eastern states

16

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

SDT – Non-compliance may lead to significant exposure

2% of Transaction Value for:

a) Non-maintenance of documents

b) Non-submission of documents

In case of adjustment

a) 100% to 300% of additional tax

Existing penalty provisions now also applicable to SDT

New penalty provisions introduced for SDT & International Transactions

2% of Transaction Value for:

a) Non-reporting of transaction

b) For incorrect maintenance/submission of documents

Transfer Pricing addition – Tax payable thereon

17

Practical Issues - SDT

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

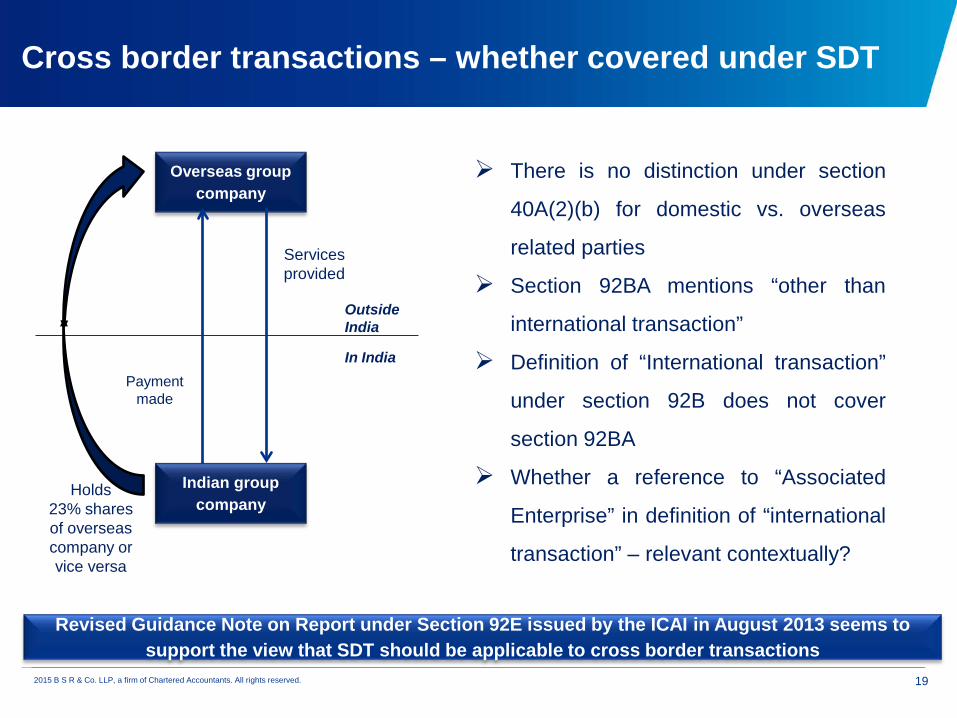

Cross border transactions – whether covered under SDT

Overseas group company

Services provided

Outside India

In India

Indian group company

Payment made

Holds 23% shares of overseas company or vice versa

There is no distinction under section

40A(2)(b) for domestic vs. overseas

related parties

Section 92BA mentions “other than

international transaction”

Definition of “International transaction”

under section 92B does not cover

section 92BA

Whether a reference to “Associated

Enterprise” in definition of “international

transaction” – relevant contextually?

Revised Guidance Note on Report under Section 92E issued by the ICAI in August 2013 seems to support the view that SDT should be applicable to cross border transactions

19

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

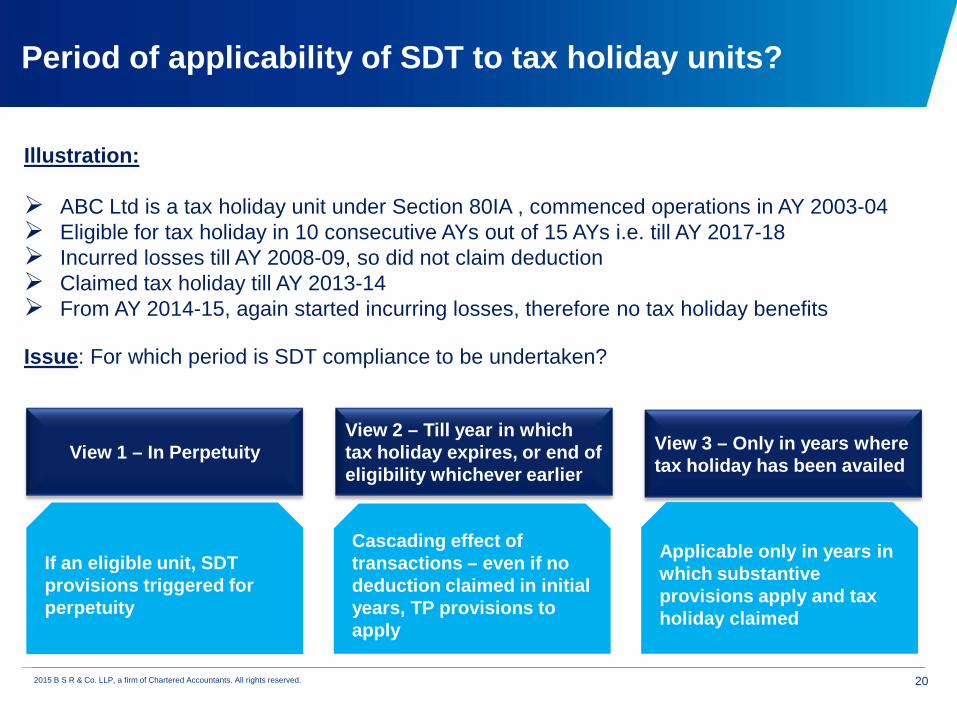

Period of applicability of SDT to tax holiday units?

Illustration:

ABC Ltd is a tax holiday unit under Section 80IA , commenced operations in AY 2003-04 Eligible for tax holiday in 10 consecutive AYs out of 15 AYs i.e. till AY 2017-18 Incurred losses till AY 2008-09, so did not claim deduction Claimed tax holiday till AY 2013-14 From AY 2014-15, again started incurring losses, therefore no tax holiday benefits

Issue: For which period is SDT compliance to be undertaken?

View 2 – Till year in which tax holiday expires, or end of eligibility whichever earlier

View 1 – In Perpetuity View 3 – Only in years where tax holiday has been availed

If an eligible unit, SDT provisions triggered for perpetuity

Cascading effect of transactions – even if no deduction claimed in initial years, TP provisions to apply

Applicable only in years in which substantive provisions apply and tax holiday claimed

20

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Direct v/s indirect ownership

Section 40A(2)(b) silent on indirect ownership

Circular 6P of 1968 (explaining 40A(2) as introduced) – mentions direct / indirect for

downstream

Circular (especially those in conflict with Act) not binding - Act is supreme

Definition of ‘associated enterprise’ u/s 92A uses the expression ‘directly or indirectly’ and

‘through one or more intermediaries’ - Such language not used in Section 40A(2)(b)

Revised Guidance Note on Report under Section 92E issued by the ICAI in August 2013

seems to support the view that only direct holdings should be considered

Reporting penalty may be a concern – 2% of transaction value

Retrospective amendment cannot be ruled out

21

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

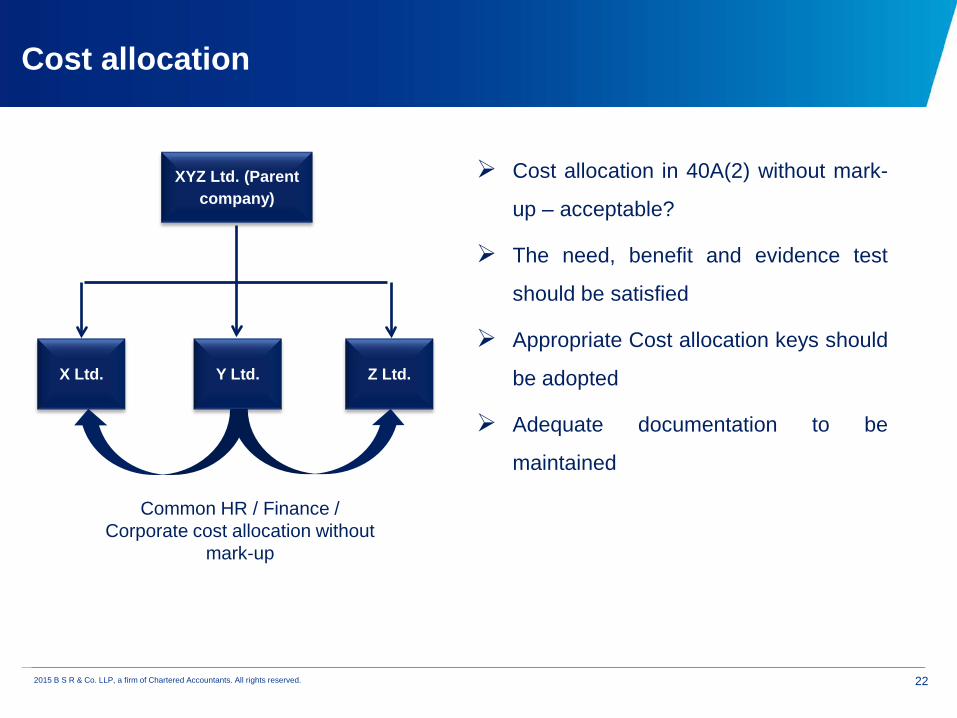

Cost allocation

Cost allocation in 40A(2) without mark-

up – acceptable?

The need, benefit and evidence test

should be satisfied

Appropriate Cost allocation keys should

be adopted

Adequate documentation to be

maintained

XYZ Ltd. (Parent company)

X Ltd. Z Ltd.Y Ltd.

Common HR / Finance / Corporate cost allocation without

mark-up

22

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Determination of the 5 crores limit

Section 92BA just mentions “transactions entered into by the assessee”

Whether ‘transactions entered’ alludes to book value or ALP

No clarity in sec 92BA or 40A(2)

If ALP is more than book value in one of the transactions can SDT be triggered – even

though book value in aggregate is less than 5 crores

Can the TPO determine ALP even where no reporting / benchmarking is carried out – i.e.,

where as per book value SDT not triggered?

23

Threshold increased to INR 20 crores annually from FY 2015 – 16

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Capital expenditure

Section 92BA says “any expenditure”

Whether capital expenditure covered?

Section 92(2A) says “allowance for expenditure”

Depreciation does not constitute an allowance for expenditure. View upheld by SC in the

case of Nectar Beverages P. Ltd. (182 Taxman 319)

Whether acquisition of shares a capital expenditure or investment – whether such share

acquisition needs to be reported?

Whether reporting or benchmarking is required?

Recently issued Guidance Note of the ICAI specifically includes “expenditure on purchase of

tangible and intangible property” in ambit of Section 40A(2)(a) transactions

Reporting penalty may be a concern – 2% of transaction value

24

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Only business or other sources also covered?

Section 92BA only talks about “any expenditure” to related persons

Does not specify “business income”

Expenditure under CG / IFOS covered?

Cost of acquisition and / or transfer expenses covered?

Whether reporting to be done?

25

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Loans / guarantees without consideration

Not relevant under SDT in a non tax holiday scenario

37(1) exposure for entity giving such loan / guarantee without consideration

Whether SC judgment of S. A. Builders Ltd. applies – shareholders activity argument

SLP by 3 member bench admitted in the case of Tulip Star Hotels Ltd.

Whether shareholder activity argument still valid?

26

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Director’s remuneration benchmarking

Every director is a related party – No uncontrolled transactions possible

Various approaches in benchmarking of director’s remuneration possible to consider

Transaction Net Margin Method (TNMM) – Transaction subsumed as part of overall TNMM

Use of average ratio – Director’s remuneration as a percentage of total cost or sales

Comparison with survey carried out by external agencies

Remuneration specified in appointment letter issued at the time of recruitment – may be

treated as uncontrolled transaction

Use of ceiling provided by the Companies Act, 1956 for managerial remuneration

Section 40(b) for Partner’s salary?

Technical argument – No tax leakage since entire salary offered to tax (no expense deduction)

27

Generic Case Studies

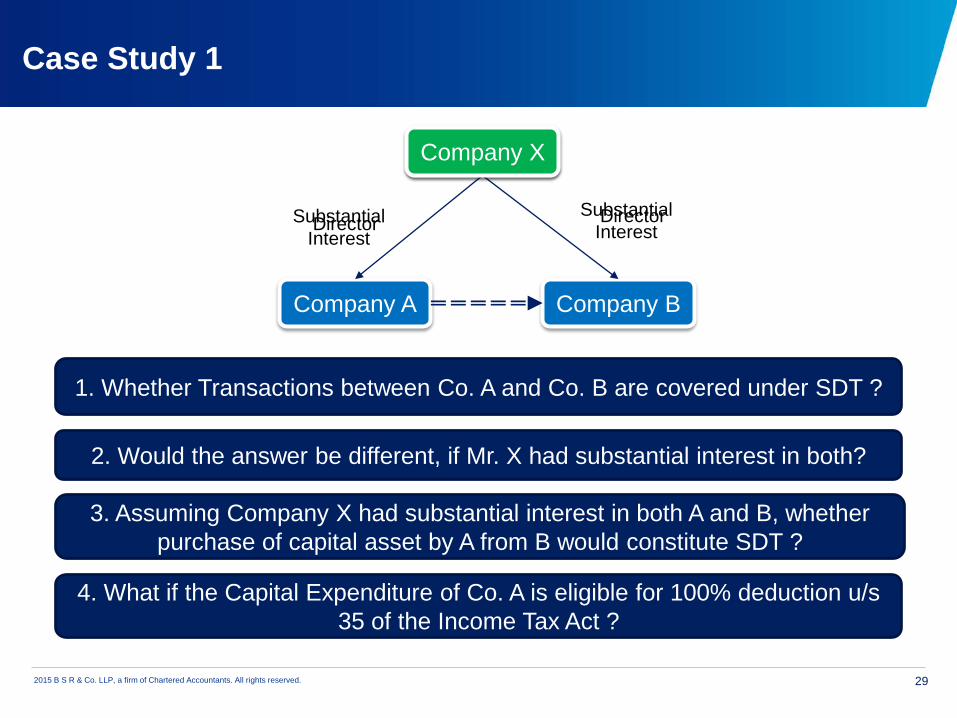

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved. 29

Mr. X

Company B

Director

Company A

Director

1. Whether Transactions between Co. A and Co. B are covered under SDT ?

2. Would the answer be different, if Mr. X had substantial interest in both?

4. What if the Capital Expenditure of Co. A is eligible for 100% deduction u/s 35 of the Income Tax Act ?

Substantial Interest

Substantial Interest

3. Assuming Company X had substantial interest in both A and B, whether purchase of capital asset by A from B would constitute SDT ?

Company X

Case Study 1

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved. 30

A

Company B

Directors

Company A

Whether Transactions

between Co. A and Co. B are covered

under SDT ?

B C D Others

60%10%10%10%10%

Case Study 2

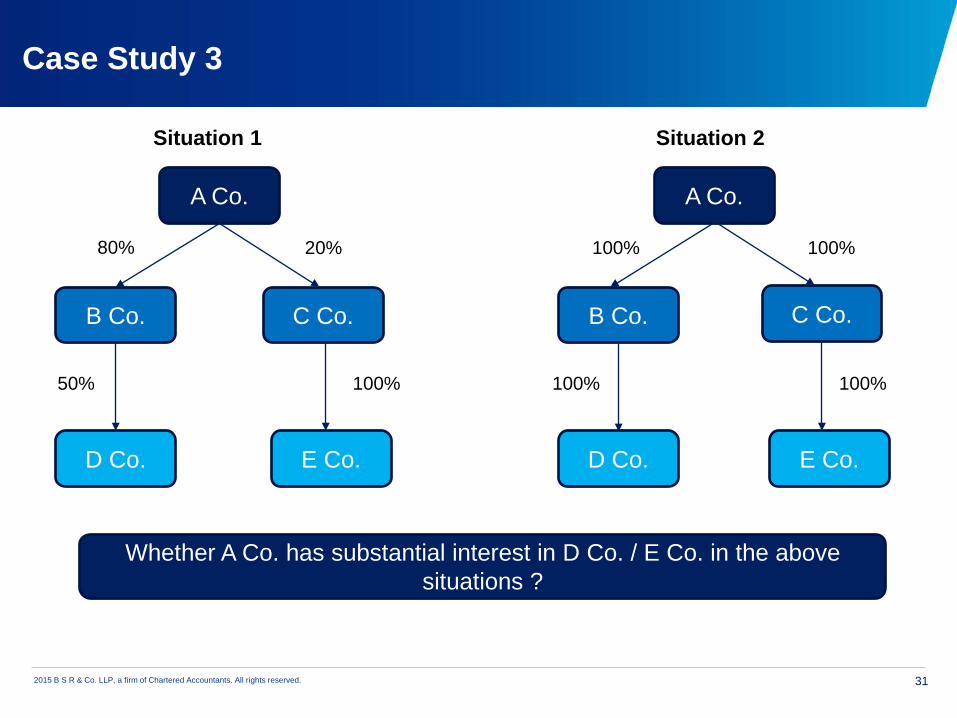

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved. 31

A Co.

C Co.B Co.

D Co. E Co.

A Co.

C Co.B Co.

D Co. E Co.

80% 20%

50% 100% 100% 100%

100% 100%

Whether A Co. has substantial interest in D Co. / E Co. in the above situations ?

Situation 1 Situation 2

Case Study 3

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved. 32

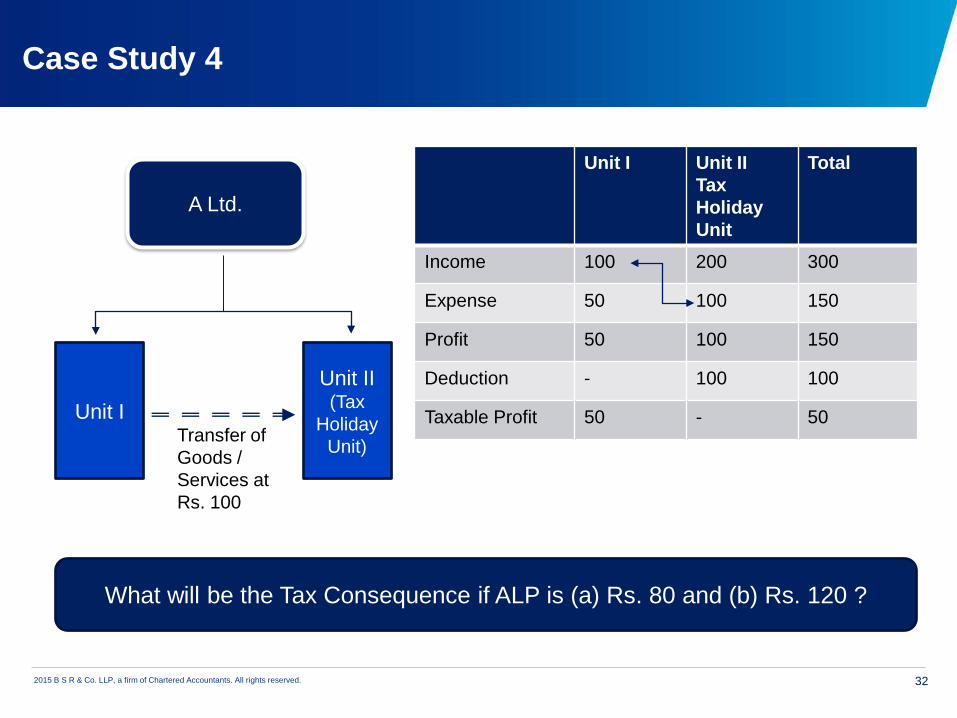

A Ltd.

Unit IUnit II(Tax

Holiday Unit)Transfer of

Goods / Services at Rs. 100

Unit I Unit IITax Holiday Unit

Total

Income 100 200 300

Expense 50 100 150

Profit 50 100 150

Deduction - 100 100

Taxable Profit 50 - 50

What will be the Tax Consequence if ALP is (a) Rs. 80 and (b) Rs. 120 ?

Case Study 4

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved. 33

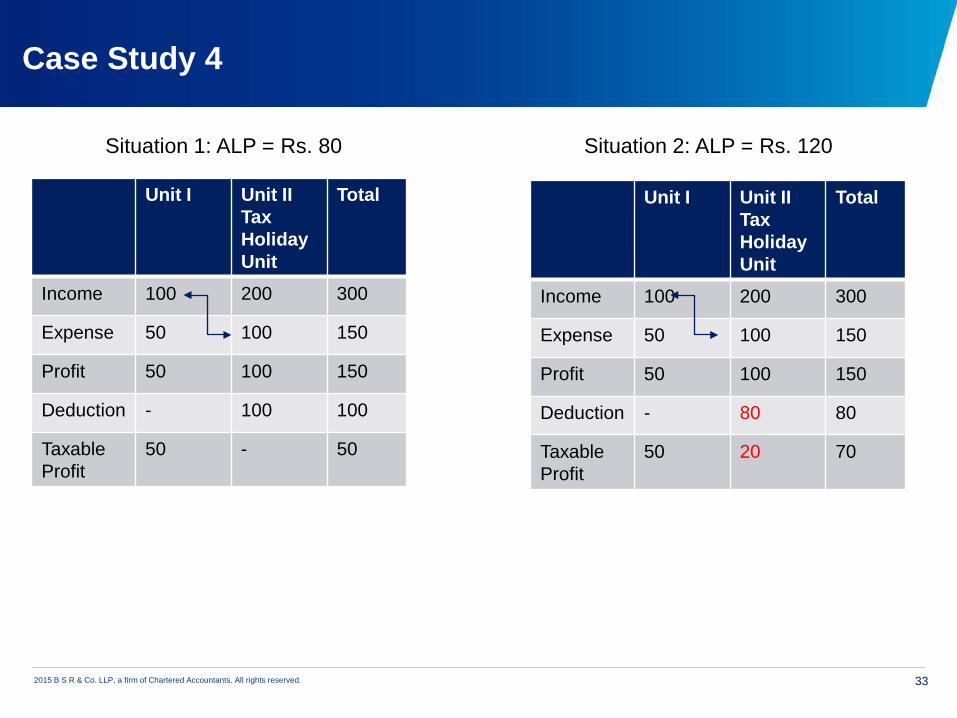

Unit I Unit IITax Holiday Unit

Total

Income 100 200 300

Expense 50 100 150

Profit 50 100 150

Deduction - 100 100

Taxable Profit

50 - 50

Situation 1: ALP = Rs. 80

Unit I Unit IITax Holiday Unit

Total

Income 100 200 300

Expense 50 100 150

Profit 50 100 150

Deduction - 80 80

Taxable Profit

50 20 70

Situation 2: ALP = Rs. 120

Case Study 4

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

Questions & Answers

Questions

&

Answers

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved.

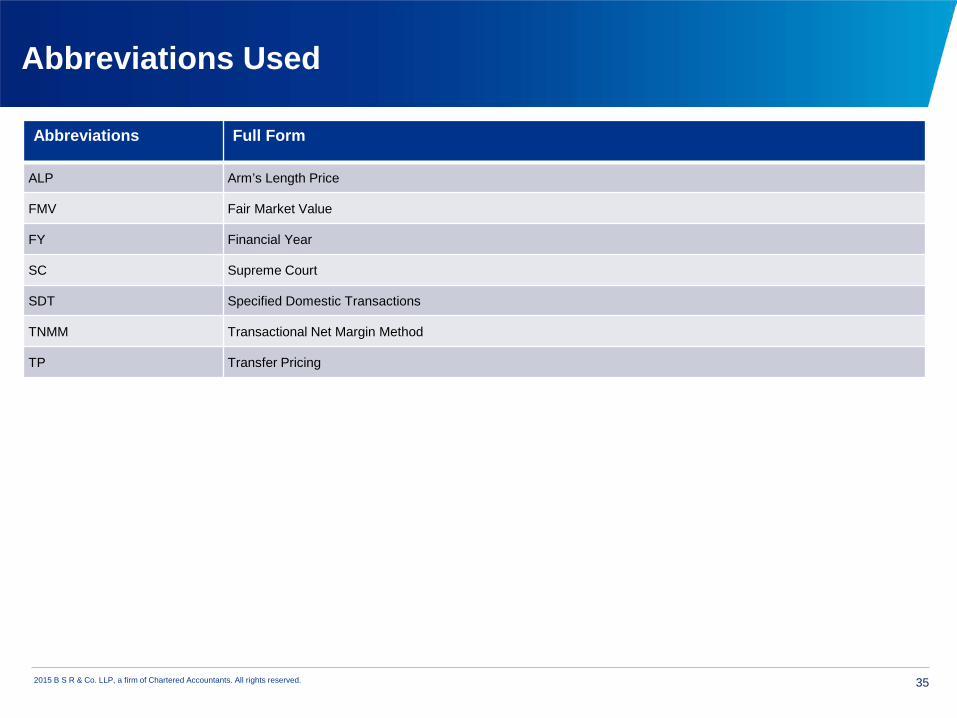

Abbreviations Used

35

Abbreviations Full Form

ALP Arm’s Length Price

FMV Fair Market Value

FY Financial Year

SC Supreme Court

SDT Specified Domestic Transactions

TNMM Transactional Net Margin Method

TP Transfer Pricing

Thank you

The information contained herein is of a general nature. The content provided here treats the subjects covered here in

condensed form. It is intended to provide a general guide to the subject matter and should not be relied on as a basis for

business decisions. A detailed analysis of the tax and regulatory implications should be done prior to implementation in order to

determine the feasibility of the transaction at the time of implementation.

Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate

as of the date it is received or that it will continue to be accurate in the future. No one should act upon such information without

appropriate professional advice after a thorough examination of the particular situation. Specialist advice should be sought with

respect to any individual circumstances.

2015 B S R & Co. LLP, a firm of Chartered Accountants. All rights reserved