aveva group plc/media/aveva/english/... aveva group plc results for the year ended 31 march 2014

TRANSCRIPT

www.aveva.com

AVEVA Group plc

Results for the year ended 31 March 2014

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

This presentation may include predictions, estimates, intentions, beliefs and other statements that are or may be construed as being forward-looking. While these forward-looking statements represent our current judgment on what the future holds, they are subject to risks and uncertainties that could result in actual outcomes differing materially from those projected in these statements. No statement contained herein constitutes a commitment by AVEVA to perform any particular action or to deliver any particular product or product features. Readers are cautioned not to place undue reliance on these forward-looking statements, which reflect our opinions only as of the date of this presentation. The Company shall not be obliged to disclose any revision to these forward-looking statements to reflect events or circumstances occurring after the date on which they are made or to reflect the occurrence of future events.

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Strategic highlights

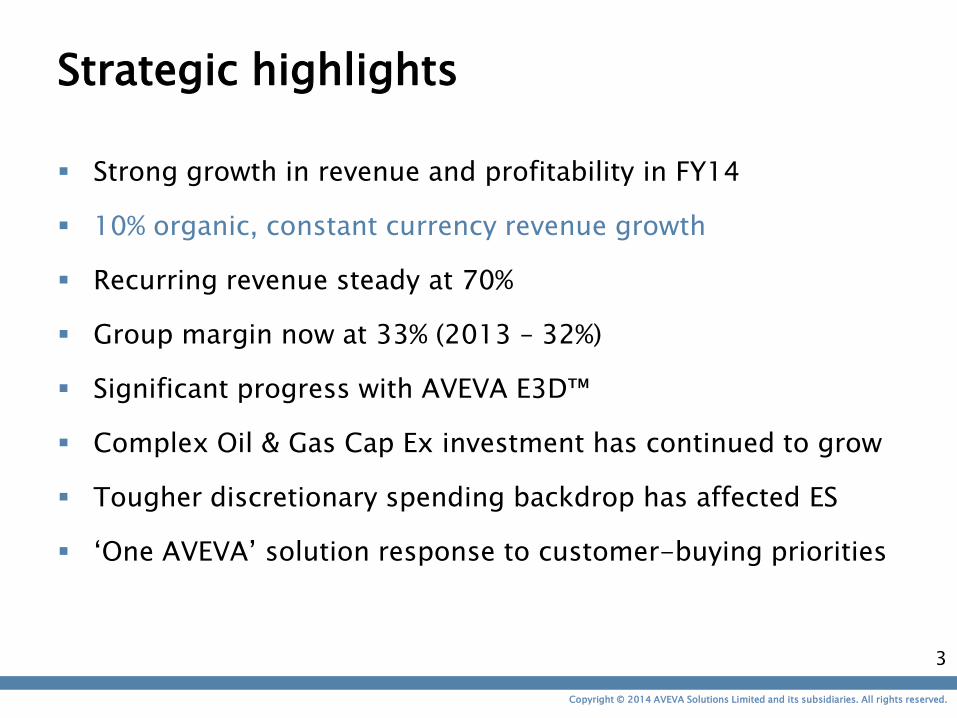

Strong growth in revenue and profitability in FY14

10% organic, constant currency revenue growth

Recurring revenue steady at 70%

Group margin now at 33% (2013 – 32%)

Significant progress with AVEVA E3D™

Complex Oil & Gas Cap Ex investment has continued to grow

Tougher discretionary spending backdrop has affected ES

„One AVEVA‟ solution response to customer-buying priorities

3

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Financial highlights

FY 2014

FY 2013

Total revenue £237.3m £220.2m 8%

Constant currency revenue £242.1m £220.2m 10%

Adjusted* profit before tax £78.3m £70.6m 11%

Adjusted* basic EPS 89.1p 74.7p 19%**

Adjusted* profit before tax margin 33.0% 32.1%

Final dividend per share 22.0p 19.5p 13%

Special dividend paid of 147 pence £100.0m -

Net cash £117.5m £190.4m

Operating cash flow before tax £70.2m £60.3m 16%

* Adjusted profit before tax, adjusted profit margin and adjusted basic earnings per share are calculated before amortisation of intangible assets (excluding other software), share-based payments, gain/loss on the fair value of forward foreign exchange contracts and exceptional items. In addition, adjusted basic earnings per share also includes the tax effects of these adjustments. ** After adjusting for the effect of the share consolidation and the related reduction in interest income following the associated special dividend of £100 million, the underlying adjusted basic earnings per share rose by 16% to 86.59 pence.

4

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Summary income statement (statutory)

FY 2014 £m

FY 2013 £m

Growth

Total revenue 237.3 220.2 8%

Cost of sales (17.4) (16.1)

Research and Development costs (38.3) (35.5) 8%

Selling and distribution expenses (93.0) (87.6) 6%

Administrative expenses (20.1) (18.6) 8%

Net interest receivable 0.5 1.1

Normalised items 9.3 7.1

Adjusted* profit before tax 78.3 70.6 11%

Reported profit before tax 69.0 63.5 9%

Income tax (18.0) (18.1)

Profit after tax 51.0 45.4 12%

Adjusted* profit margin 33.0% 32.1%

Adjusted* basic EPS (pence) 89.1 74.7 19% 5

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

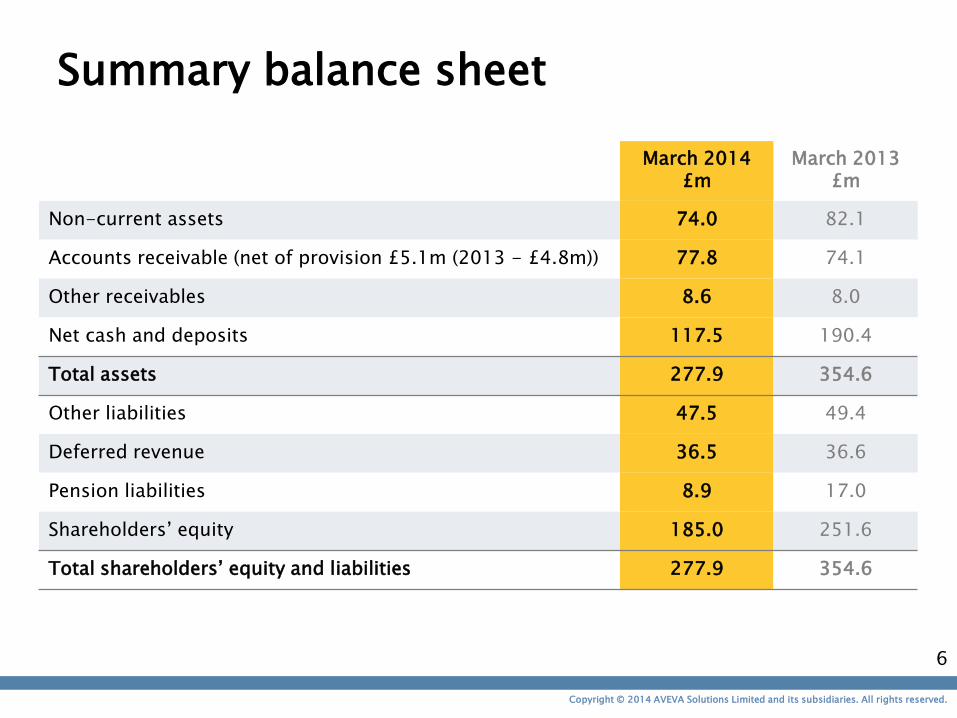

Summary balance sheet

March 2014 £m

March 2013 £m

Non-current assets 74.0 82.1

Accounts receivable (net of provision £5.1m (2013 - £4.8m)) 77.8 74.1

Other receivables 8.6 8.0

Net cash and deposits 117.5 190.4

Total assets 277.9 354.6

Other liabilities 47.5 49.4

Deferred revenue 36.5 36.6

Pension liabilities 8.9 17.0

Shareholders‟ equity 185.0 251.6

Total shareholders‟ equity and liabilities 277.9 354.6

6

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Global performance

Robust growth in Central and Western

EMEA, soft demand in Russia and Middle

East

EMEA

£112.0m

(2013 - £107.6m)

Growth +4%

Asia Pacific

£86.9m

(2013 - £73.3m)

Growth +19%

Rental fees

Initial fees

Annual fees

Training & services

North America mid-teens growth,

Latin America broadly flat +

effect of currency

Strong performance in South Korea

Americas

£38.4m (2013 - £39.3m)

Growth -2%

7

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Revenue by category

Recurring revenue at 70%

Rental fees +11%

ILF +14%

0

50

100

150

200

250

Annual fees Rental fees Initial licence fees

Services Total revenue

57.1

109.9

48.4

21.9 237.3

+5%

+11%

+14%

-11% +10%

FY 2

014

54.4

98.8

42.4

24.6 220.2

FY 2

013

8

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Currency effect on revenue

Translation effect of overseas subsidiaries

FY14*

Material movement in average rates vs FY13

£4.8 million (2%) negative impact on revenue

H1 benefit £2.3 million; H2 headwind £7.1 million

*See appendix for further detail on exchange rates

FY15*

If spot rates remain at March „14 levels – 4-5% headwind to revenue in FY15

Impact principally in H1

9

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

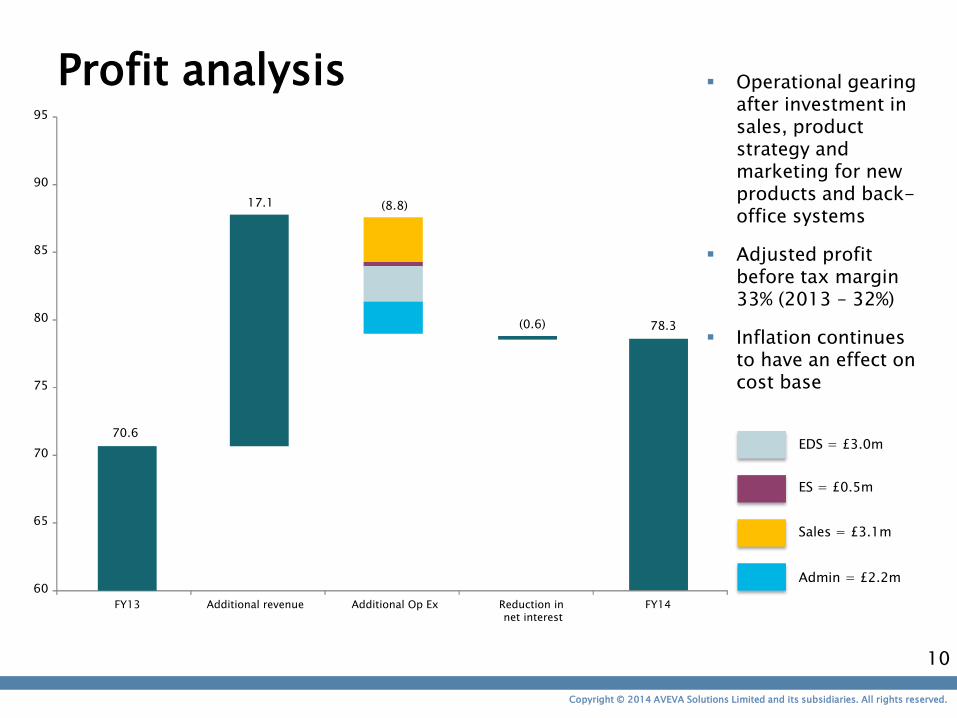

Profit analysis Operational gearing after investment in sales, product strategy and marketing for new products and back-office systems

Adjusted profit before tax margin 33% (2013 – 32%)

Inflation continues to have an effect on cost base

EDS = £3.0m

ES = £0.5m

Sales = £3.1m

Admin = £2.2m 60

65

70

75

80

85

90

95

FY13 Additional revenue Additional Op Ex Reduction in net interest

FY14

70.6

17.1 (8.8)

(0.6) 78.3

10

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

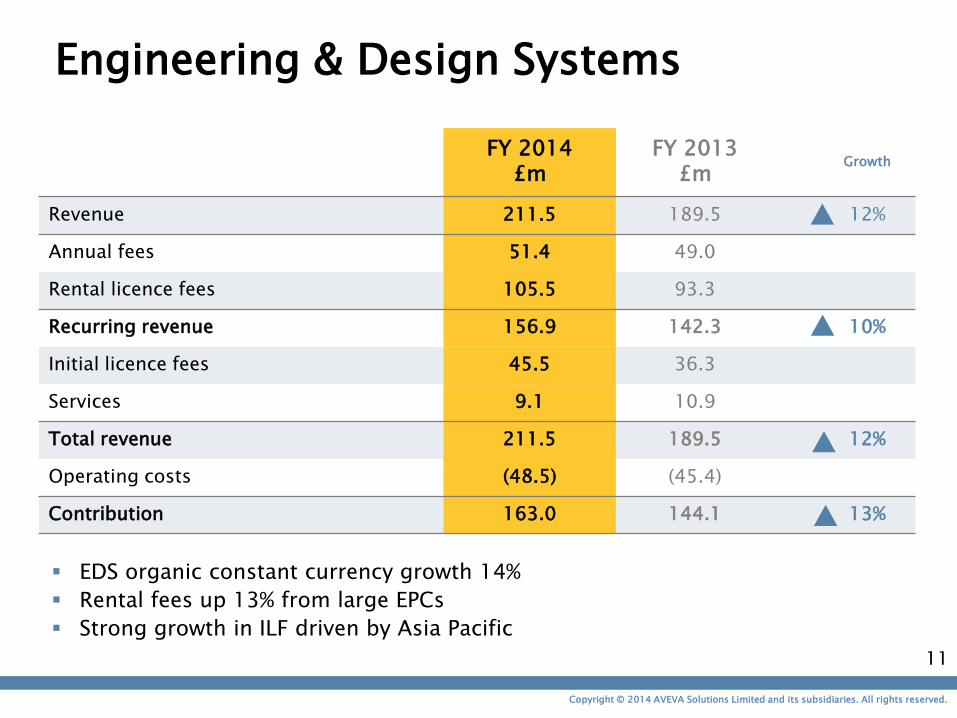

Engineering & Design Systems

FY 2014 £m

FY 2013 £m

Growth

Revenue 211.5 189.5 12%

Annual fees 51.4 49.0

Rental licence fees 105.5 93.3

Recurring revenue 156.9 142.3 10%

Initial licence fees 45.5 36.3

Services 9.1 10.9

Total revenue 211.5 189.5 12%

Operating costs (48.5) (45.4)

Contribution 163.0 144.1 13%

EDS organic constant currency growth 14%

Rental fees up 13% from large EPCs

Strong growth in ILF driven by Asia Pacific

11

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Enterprise Solutions

FY 2014 £m

FY 2013 £m

Growth

Revenue 25.9 30.7 16%

Annual fees 5.7 5.3

Rental licence fees 4.5 5.5

Recurring revenue 10.2 10.8 6%

Initial licence fees 2.9 6.2

Services 12.8 13.7

Total revenue 25.9 30.7 16%

Operating costs (29.3) (28.7)

Contribution (3.4) 2.0 -

Backlog £10.7m (30/09/13 - £11.4m; 31/03/13 - £14.4m)

„One AVEVA‟ pull-through effect as customers focus on integrated offerings

Pressure on discretionary spend amongst customers

12

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Movement in net cash position

Operating cash conversion at 102%

Cash flow from operations +16%, after £2.5 million pension payment

£100 million special dividend paid in August 2013

0

50

100

150

200

250

300

350

400

FY13 Cash from

operations

Tax Cap Ex Special dividend Dividend FX/Other FY14

190.4

70.2 (18.2)

(4.9) (100)

(16.5)

(3.5) 117.5

13

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

„One AVEVA‟

The „One AVEVA‟ approach – common products sold differently to each type of customer by one sales force

EPCs and OOs have different buying priorities

– EPCs need technology advantage, capital project-led

– OOs want solutions to improve operational profitability and reduce risk

AVEVA‟s increasingly broad product portfolio meets both of these customer requirements

Token licensing and product integration reinforces this trend

14

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

What this means for customers

Cost Time Risk

Quality Collaboration Decision-making

Project efficiency Asset optimisation

15

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

AVEVA E3D™ update

• Clearly differentiated product

• Pace of adoption and pricing are fully on track

• Good momentum of Global Accounts licensing AVEVA

E3D™

– These include KBR, Worley Parsons, Foster Wheeler, Jacobs

Engineering, Shell, Siemens Power

• Token licensing helping to drive adoption amongst

larger customers

• Underpinning long-term sustainable growth ambitions

16

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

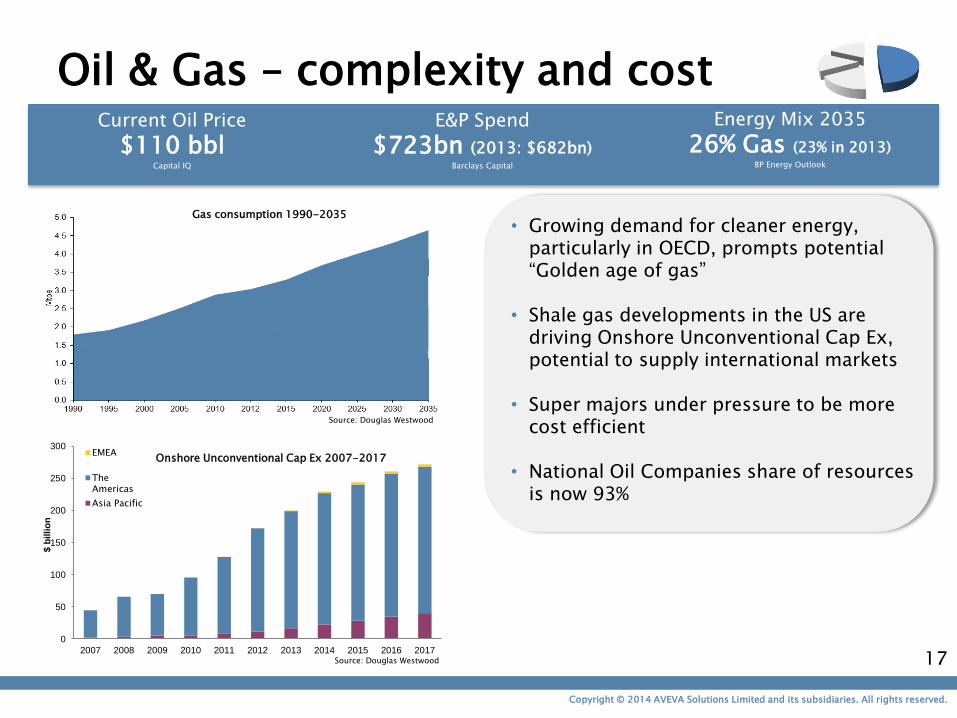

Oil & Gas – complexity and cost Current Oil Price

$110 bbl Capital IQ

E&P Spend

$723bn (2013: $682bn) Barclays Capital

Energy Mix 2035

26% Gas (23% in 2013) BP Energy Outlook

Gas consumption 1990-2035

Source: Douglas Westwood

0

50

100

150

200

250

300

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

$ b

illio

n

EMEA

The

Americas

Asia Pacific

Onshore Unconventional Cap Ex 2007-2017

Source: Douglas Westwood

• Growing demand for cleaner energy, particularly in OECD, prompts potential “Golden age of gas”

• Shale gas developments in the US are

driving Onshore Unconventional Cap Ex, potential to supply international markets

• Super majors under pressure to be more

cost efficient

• National Oil Companies share of resources is now 93%

17

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Managing complexity, risk and cost

Sou

rce:

AV

EVA

20

14

©

18

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Energy Consumption

+56% 2010-40 EIA

Power – long term growth World Population

7.2bn Geohive

China & India Population

42% of Global Geohive

0

5

10

15

20

25

30

35

40

45

2005 2010 2015 2020 2025 2030 2035 2040

Tri

llio

n K

illo

watt

ho

urs

EMEA

The

Amercas

Global Electricity Generation Forecast 2005-2040

-100

0

100

200

300

400

500

China India Other AsiaPacific

Russia The Americas EMEA

Cap

acit

y A

dd

itio

ns (

GW

)

Coal

Gas

Nuclear

Increase in Total Capacity 2013-2040

Rising populations are driving the demand for more power

Developing Non-OECD countries are the source of future energy consumption growth

The largest capacity additions will be gas in developed countries and coal in developing nations

Nuclear is also seen as a key element to add capacity to the grid for China and India

19

Source: EIA

Source: Douglas Westwood

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

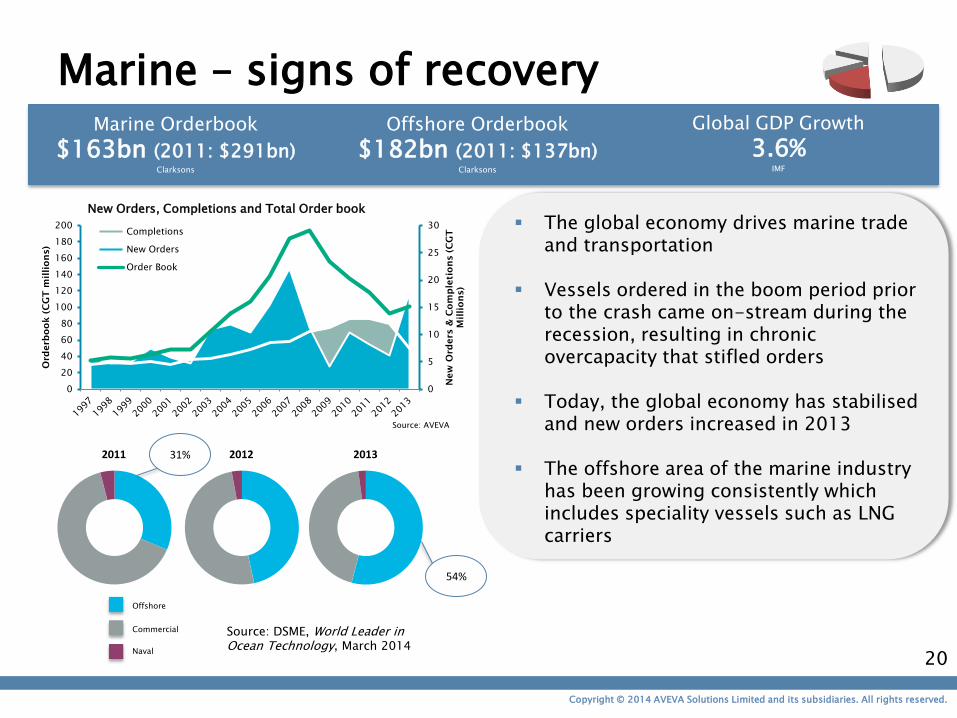

Marine – signs of recovery Marine Orderbook

$163bn (2011: $291bn) Clarksons

Offshore Orderbook

$182bn (2011: $137bn) Clarksons

Global GDP Growth

3.6% IMF

0

5

10

15

20

25

30

0

20

40

60

80

100

120

140

160

180

200

New

O

rd

ers &

C

om

pletio

ns (C

GT

Millio

ns)

Ord

erb

oo

k (C

GT

m

illio

ns)

Completions

New Orders

Order Book

The global economy drives marine trade and transportation

Vessels ordered in the boom period prior to the crash came on-stream during the recession, resulting in chronic overcapacity that stifled orders

Today, the global economy has stabilised and new orders increased in 2013

The offshore area of the marine industry has been growing consistently which includes speciality vessels such as LNG carriers

Source: AVEVA

New Orders, Completions and Total Order book

20

Source: DSME, World Leader in Ocean Technology, March 2014

2011 2012 2013

Offshore

Commercial

Naval

31%

54%

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Outlook

Extending our technology leadership, particularly in Cloud and Mobile

„One AVEVA‟ – common product set sold to each type of customer by one sales force

Broad exposure to multiple growth markets

High recurring revenues

Good sustainable growth, whilst continuing to invest in the business

21

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Appendix

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

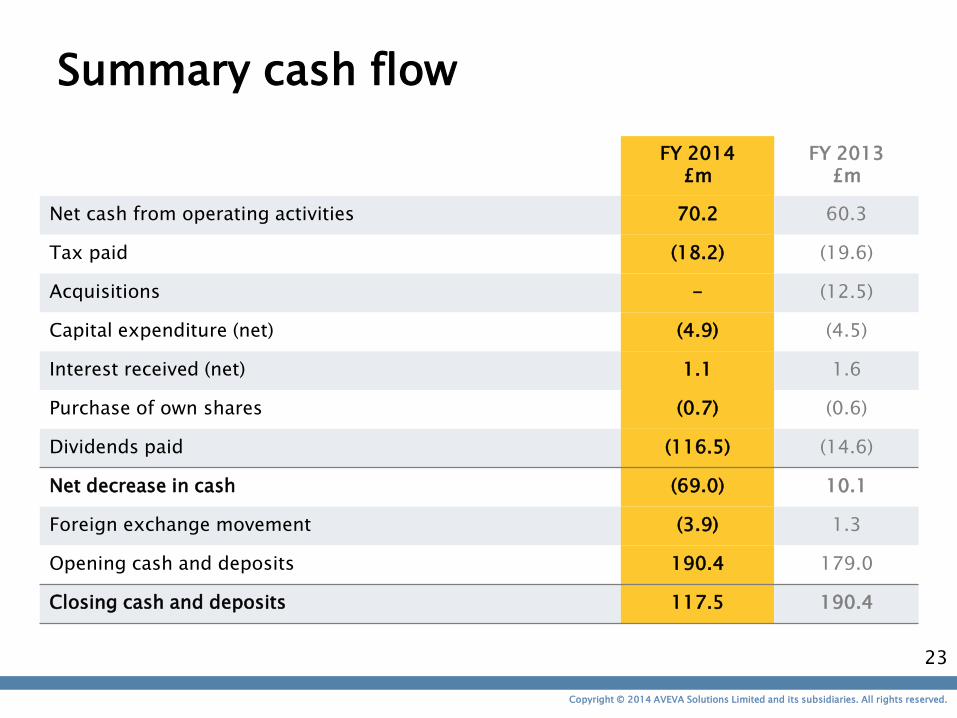

Summary cash flow

FY 2014 £m

FY 2013 £m

Net cash from operating activities 70.2 60.3

Tax paid (18.2) (19.6)

Acquisitions - (12.5)

Capital expenditure (net) (4.9) (4.5)

Interest received (net) 1.1 1.6

Purchase of own shares (0.7) (0.6)

Dividends paid (116.5) (14.6)

Net decrease in cash (69.0) 10.1

Foreign exchange movement (3.9) 1.3

Opening cash and deposits 190.4 179.0

Closing cash and deposits 117.5 190.4

23

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Currency – FY14 effect Currency % of FY’14

revenue A: Average rate FY’14

B: Average rate FY’13

Delta (A / B)

FY’14 rev impact

EMEA 16% -

EUR 1.19 1.23 -3%

NOK 9.54 9.14 +4%

RUB 52.55 49.30 +7%

Asia Pacific 35% -4%

INR 96.16 86.23 +12%

JPY 159.42 131.12 +22%

KRW 1,738.60 1,769.63 -2%

AUD 1.71 1.46 +17%

Americas 49% -5%

USD 1.59 1.58 -

BRL 3.59 3.18 +13%

MXP 20.54 20.68 -

Total 100% -2% 24

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Currency –annualised for FY15 Currency A: Average

rate FY’14 B: Spot rate (31/03/14)

Delta (B / A)

FY’15 rev impact**

EMEA -2-3%*

EUR 1.19 1.21 +2%

NOK 9.54 10.0 +5%

RUB 52.55 59.83 +14%

Asia Pacific -4-5%

INR 96.16 99.62 +4%

JPY 159.42 171.11 +7%

KRW 1,738.60 1,782.37 +3%

AUD 1.71 1.80 +5%

Americas -4-5%

USD 1.59 1.66 +4%

BRL 3.59 3.77 +5%

MXP 20.54 21.77 +6%

Total -4-5%

* Excluding UK sterling revenues ** If we assume same regional revenue split as FY‟14 25

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

SIEMENS

AVEVA products and competitive landscape

Aspen

Hexagon

Bentley

Dassault

Aspen

SIEMENS

Bentley

Hexagon

AVEVA ES AVEVA EDS

Dassault

SAP

In-house solutions In-house solutions

Point solutions

Project phase 2-6 years (c.$1.6 billion) Operations phase up to 50 years (>$2 billion)

Autodesk

26

Conceptual Design

FEED

Detailed Design

Construction & Commissioning

Operations

Decommissioning

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Customer examples 2013/14

AMEC

– 5 year baseline agreement, standardising on IE&D

Fluor and Jacobs Engineering

– Multi year agreements provide strategic platform for growth

Petroleum Development Oman

– Mandate AVEVA 4D construction management system (ERM plus AVEVA NET)

Bruce Steel

– First Bocad project in Canadian oil-sands, competitive replacement

APLNG (Conoco Phillips, Origin Energy, Sinopec)

– AVEVA NET for project information control and handover

Compania Minera Milpo S.S.A.

– Mining company with headquarters in Lima; first AVEVA NET contract in Peru

27

Copyright © 2014 AVEVA Solutions Limited and its subsidiaries. All rights reserved.

Definition of terms Item Definition

Initial Licence Fee Initial Licence Fee (ILF) - users are charged an initial licence fee per seat together with an obligatory annual fee.

Annual Fee Charged in association with an ILF providing customer support and maintenance, which includes core updates. Users must pay the annual fee in order to maintain the right to use the software.

Rental licence model An alternative to the ILF plus annual fee model, there are three different types of rental licence: Monthly invoicing, contractual period (typically one year, invoiced up front) or token licensing.

Token-based licensing The user pays for a 'basket of tokens' representing licences to use different software products over a defined period of time. The customer can draw down on these licences as required.

Revenue recognition

ILFs – recognised upfront after usual delivery and acceptance conditions are met. Annual fees – recognised ratably over the period (typically 12 months). Rental licences - an estimated licence element is recognised up front, and the remaining maintenance element is recognised ratably over the contracted period. Services are recognised on a percentage complete basis.

Revenue by geography The sales force is organised into three geographic regions. Revenue is allocated based on where the contracting entity of the customer is based. AVEVA's global accounts often choose to purchase software in one geography for use in another.

Recurring revenue Annual fees plus rental fees.

Adjusted PBT Profit Before Tax adjusted to exclude the effects of amortisation of intangibles (excluding software), share-based payments, gain/loss on fair value of forward foreign exchange contracts and exceptional items.

Constant currency The period‟s reported result restated to reflect the previous year‟s average exchange rates, for the purpose of a constant currency comparison.

Adjusted EPS Adjusted PBT is used to calculate the adjusted earnings per share, after an adjustment for the tax effect of the items adjusted.

Cash conversion Cash flow from operations divided by the operating profit for the period, measured as a percentage.

Enterprise Solutions backlog Contracted Enterprise Solutions revenue that has not yet been recognised but which is expected to be recognised in the next 12 months. Revenue backlog also includes 12 months of annual fees.

33

28