australian retail banker - february 2016

TRANSCRIPT

FEBRUARY 2016

RFi Group Opinion

All Mortgage Brokers Care About is….. Credit Policy and Process Efficiency!

03

RFi Group Insight

Gen Y and the Future of Banking 05

RFi Group Women in Leadership

Susie Babani - ANZ 07

RFi Group Interview

John Arnott – ING Direct 13

RFi Group Interview

Sue Coulter - CUA 18

Transactions CBA launches innovation lab in downtown Hong Kong

21

Savings Two out of three Aussies short on retirement savings

22

Mortgages

Yellow Brick Road brand gets a facelift 23

Cards Push for transparency on credit card rates and fees

24

Personal Loans

A rise in interest rates could threaten P2P lending 25

Payments and Digital Samsung Pay coming to Australia in 2016

26

www.rfintelligence.com

Did a colleague forward you the Australian Retail Banker? Subscribe to receive YOUR FREE monthly copy by clicking here

2 www.rfintelligence.com.au

Letter from the Editor Welcome to the February 2016 edition of the Australian Retail Banker, a newsletter designed to give you an update on news and trends within the Australian retail banking market specifically in the areas of transactions, savings, deposits, mortgages, cards, personal lending, payments and digital banking. Only a few short weeks away from RFi Group’s Australian Mortgage Innovation Summit, this month’s Opinion Piece (page 3), authored by RFi Group’s Managing Director – Advisory, Alan Shields, suitably shares thoughts on the mortgage market’s drivers over the last 12 months, with a close up on the broker channel. Meanwhile, this month’s Insight Piece (page 4) - ‘Gen Y and the Future of Banking’ - looks at the customers of tomorrow. In our Women in Leadership piece, I talk to none other than the Chief Human Resources Officer at ANZ, Susie Babani. Susie shared some frank and very honest feedback from her position as not only a woman in a C-level leadership role, but one who looks after the career trajectories of so many. Susie has a sharp eye on young people and their success in her own organisation and provides some fantastic advice, with lots of laughs along the way. I hope you enjoy the interview. This issue’s RFi Group Thought Leader Interviews feature ING Direct’s Executive Director for Customers, John Arnott, as well as CUA’s General Manager for Business Transformation & Technology (and CIO), Sue Coulter. John and Sue are also both appearing as key speakers at RFi Group’s upcoming Australian Mortgage Innovation Summit, and we welcome you to read the pieces for a sneak preview into their presentations. As you know, we really enjoy our privileged position of meeting with these industry experts and welcome you to let us know if there is anyone you think would be great to highlight this year. This month’s product news covers CBA’s new Hong Kong based innovation hub, concerns about Australian’s retirements savings, a new look for major industry broker Yellow Brick Road, a continued need for transparency in the credit card space, some new threats to P2P and the arrival of Samsung Pay in Australia. We hope you enjoy this edition and as always, welcome any feedback you may have. Have a great month,

Chloé James Media & PR Director RFi Group +61 (0) 451 790 929 [email protected] https://twitter.com/RFiMediaGRB

3 www.rfintelligence.com.au

Source: RFi Group

If you have any questions, please don’t

hesitate to contact me directly:

Alan Shields,

Managing Director - Advisory, RFi Group

Main. 02 9146 5950

Mobile. 0405 000 766

RFi Group Opinion All Mortgage Brokers Care About is….. Credit Policy and Process Efficiency! RFi Group’s Australian Mortgage Innovation Summit is this month so I thought it might be a good time to reflect on the mortgage market and its drivers over the last 12 months. In my article in December, I spoke a little about the different pricing dynamics that had occurred during the course of 2015 – something which has more or less defined the mortgage market conversation in recent times. Another factor that I think is worth a mention is the rise of the broker segment in Australia. According to APRA, the proportion of bank loans that are distributed via the third party channel is creeping inexorably towards the 50% mark, which would make the reliance on the broker channel in Australia one of the highest in the Western world. In addition, in most markets, the broker channel has seen a decline in recent years, rather than the growth we have seen here in Australia. In the face of this broker success, it is critical that banks understand how best to appeal to the broker segment. In a recent survey of the broker market conducted by RFi Group, the attributes of a ‘good lender’ are a constant and obvious theme running through the results. These are: The 3 attributes that make a lender the ‘most preferred’ for brokers

Fastest turnaround times

Best (consistent) credit policy

Best BDMs

The top 3 attributes that correlate to satisfaction with a lender

Ease of application assessment

Loan approval process

BDM Support

Essentially, this makes a lot of sense. It’s all about making the broker’s life easier. If brokers know that when they submit a loan to a particular lender that they will get a consistent outcome in a known timeframe, then they are happy. The end customer won’t be surprised, nor will they need to badger their broker for updates on the application process. So what about price? And commission? Interestingly, these factors do rate highly for certain segments of the broker market when it comes to lender preference. If we cut the data by value of loans written in a year, then there is a clear trend. The less business the broker writes in total, the more concerned they are likely to be with pricing and commission (as shown in the chart on the left). So for lenders, this should read a bit like the story of the hare and the tortoise. The hare goes out hard with price and commission and wins over an initial group of brokers writing business for them. Meanwhile, the tortoise takes its time to ensure that credit policy is consistent and as few manual interpretations of it are made as possible, while ironing out the application process. Only then does the tortoise start to sell loans. At the end of the reporting period, the tortoise wins. Without wanting to sound any more like Aesop, the moral of the story is that if you have a great rate and hefty incentives but no back-end rigour, then it’s all for nought.

0%

10%

20%

30%

40%

50%

60%

Why do you most prefer working with this lender?By residential mortgage

lending written in the last 12 months

Less than $5 million*

$5 million to $10 million

$10 million to $18 million

$18 million to $30 million

More than $30 million

5 www.rfintelligence.com.au

RFi Group Insight

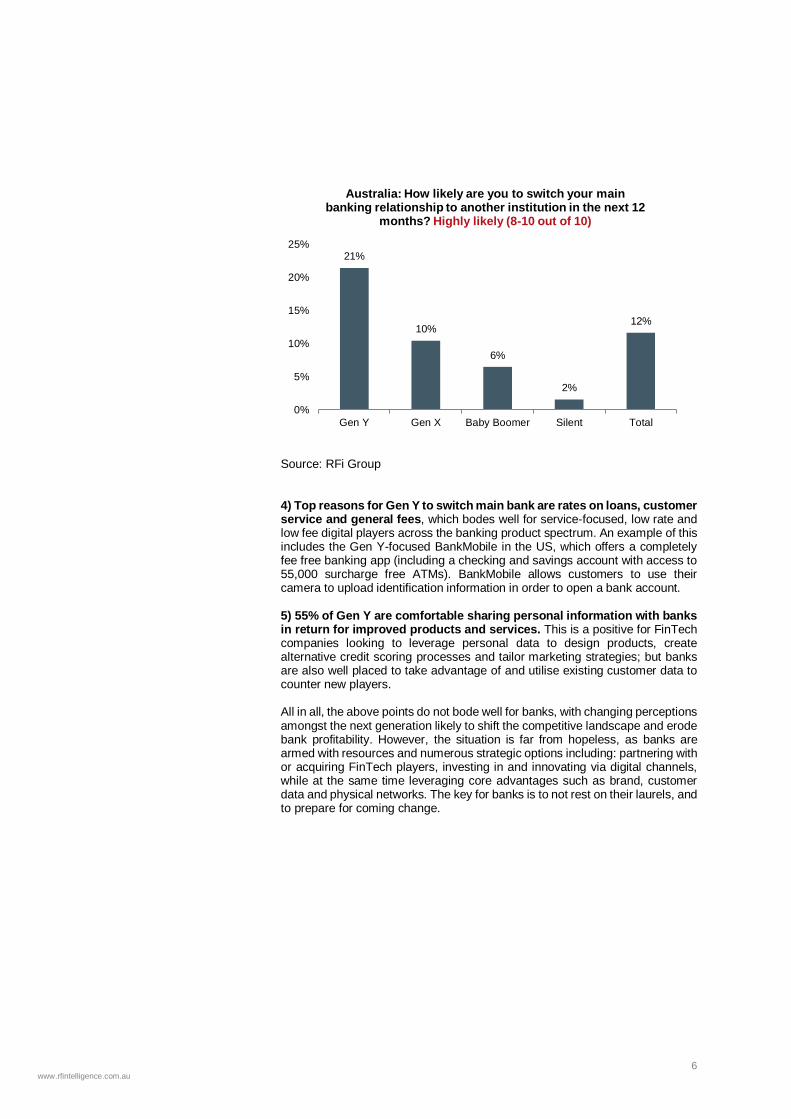

Gen Y and the Future of Banking In previous editions of the Australian Retail Banker, we have looked at changing consumer perceptions towards banking, and, in particular, the potential for FinTech players to capitalise on these changes. Leading on from this, in this edition, we look at Gen Y’s perspective towards banking – how they differ in terms of channel usage, product applications and attitudes towards switching – and what this means for the future of banking. The overarching theme in banking over the last decade has been digitisation, with the rise of online and mobile banking. Nevertheless, traditional physical networks, including branches and ATMs, have been surprisingly resilient, driven by sticky consumer preferences. However, as Gen Y grow older and increase their economic prominence, we could see a rapid erosion for the traditional means of banking, paving the way for new digital focused players to make significant inroads. RFi Group’s global data reveals that Gen Ys are characterised by the following: 1) More digitally engaged, with 52% of Gen Y classified as highly digitally engaged, (use mobile banking at least once a week, alongside other banking channels). This compares to 38% of Gen X and 14% of Baby Boomers. This implies mobile banking will gain prominence over time, a positive for digital-only new entrants (like Simple and Moven in the US). Source: RFi Group 2) More likely to apply via digital channels with 38% of Gen Y customers currently applying for products* via digital channels and 44% preferring to apply via digital channels in 2020 (when asked about future preference). Product applications, especially for more complex products, remain one of the primary reasons as to why branch networks retain a degree of prominence. Furthermore, branch proximity is consistently cited as a top reason for customers choosing their main bank. Thus, a rapid shift in preference for digital, particularly if facilitated by FinTech players, could erode one of the core competitive advantages of established banks. *includes credit cards, personal loans, transaction accounts and term deposits 3) More likely to switch their main bank, with 21% of Gen Y indicating they are more likely to switch their main bank in the next 12 months compared to an average of 12%.

52%

38%

14%10%

32%

0%

10%

20%

30%

40%

50%

60%

Gen Y Gen X Baby Boomer Silent Total

Australia: % Highly digitally engaged

6 www.rfintelligence.com.au

Source: RFi Group 4) Top reasons for Gen Y to switch main bank are rates on loans, customer service and general fees, which bodes well for service-focused, low rate and low fee digital players across the banking product spectrum. An example of this includes the Gen Y-focused BankMobile in the US, which offers a completely fee free banking app (including a checking and savings account with access to 55,000 surcharge free ATMs). BankMobile allows customers to use their camera to upload identification information in order to open a bank account. 5) 55% of Gen Y are comfortable sharing personal information with banks in return for improved products and services. This is a positive for FinTech companies looking to leverage personal data to design products, create alternative credit scoring processes and tailor marketing strategies; but banks are also well placed to take advantage of and utilise existing customer data to counter new players. All in all, the above points do not bode well for banks, with changing perceptions amongst the next generation likely to shift the competitive landscape and erode bank profitability. However, the situation is far from hopeless, as banks are armed with resources and numerous strategic options including: partnering with or acquiring FinTech players, investing in and innovating via digital channels, while at the same time leveraging core advantages such as brand, customer data and physical networks. The key for banks is to not rest on their laurels, and to prepare for coming change.

21%

10%

6%

2%

12%

0%

5%

10%

15%

20%

25%

Gen Y Gen X Baby Boomer Silent Total

Australia: How likely are you to switch your main banking relationship to another institution in the next 12

months? Highly likely (8-10 out of 10)

7 www.rfintelligence.com.au

“I’m optimistic. I tend to have a very ‘can-do’ attitude to life so I hope that makes me an easy person to work with. It doesn’t mean I’m not demanding, as people who work with me know, I am, but I tend to look at the bright side of most of things during that.” Susie Babani Chief Human Resources Officer ANZ

RFi Group

Women in Leadership Chloé James in interview with Susie Babani, Chief Human Resources Officer, ANZ Susie Babani is curious, bright and sharp as a tack. A passionate lover of travel, food, novels, the essential mani-pedi, and any new experience she can find in work and in life. She has lived and worked all over the world, with absolutely no sign of slowing down. As this month’s Women In Leadership interviewee, we jumped right into what makes her tick, what makes her who she is, and what she has done to bring the unbridled success to ANZ’s HR machine. She is fast, fun and full of energy, ensuring I am recording our conversation so she can speak quickly, truly and freely about where she finds herself today. And so we begin, with what I see as some truly wonderful advice as we embark on 2016…

How did you get where you are today and what, or who, has been your greatest influence in business?

Susie explains it’s absolutely been a combination of hard work and determination. “I come from a Baby Boomer generation so we didn't have offers of formal ‘mentors’ or ‘sponsors’ as we tend to give our talent and younger people nowadays. You just got on, and you ‘did’. As far as my success today, I think I’ve always been that ‘deliverer’.” “I’ve also worked with some great bosses who really pushed me.” Interestingly, especially for RFi Group’s Women in Leadership series – these first two bosses were, in fact, women. “It was back in the late 70s and early 80s when it was even more unusual to have women in these leadership-type roles - although I never really realised that at the time! On reflection, and for the purposes of this interview, that was certainly very influential to me. I was 18, 19 and they were probably around 35, which to an 18 year old felt much older and wiser! I guess their influence was that I never had that concept of ‘there are senior jobs that women simply can’t do’. It was my norm.” Susie cites a trait in herself that I often hear from my Women In Leadership interviewees. “I’m also highly curious as an individual.” She is interested in learning new things, meeting new people, going to new places, and experiencing all life has to offer. “I’ve lived all over the world and I’ve loved it.” She tells me she is on her 7th country! “I feel I’ve got two more in me!” “I’m also optimistic. I tend to have a very ‘can-do’ attitude to life so I hope that makes me an easy person to work with. It doesn’t mean I’m not demanding, as people who work with me know, I am, but I tend to look at the bright side of most of things during that.”

8 www.rfintelligence.com.au

“I have been in really very tough environments when I’ve spoken up about things that I simply didn’t think were right. I knew at these times this would most probably (and she discloses, it did) damage me personally, but nevertheless I felt I had to raise those issues.” Susie Babani Chief Human Resources Officer ANZ

What is the driving force behind your career goals/aspirations?

Susie is startlingly honest, a refreshing theme that continues throughout our conversation. “When I started work, I never thought about a ‘career’ to be frank, I thought about a ‘job’.” Starting professional employment at the ripe age of 18, during a time when the UK was experiencing a major recession, Susie explains to me that jobs were hard to come by and careers were “a bit of a luxury honestly!” “If I look back, what ‘drove’ me was a desire for financial independence. I am and always have been a fiercely independent person. I know my own mind and I always wanted, from a very young age, not to have to rely on anybody else. Roof, clothes and food on the table, that was what I wanted.” she quite honestly proclaims. “It’s what propelled me, probably more than ‘the career’ actually.” The other thing Susie “knew for sure”, was that she wanted to live and work all over the world. “I didn’t mind where, I didn’t even really mind what I was going to be doing to be honest! Well, to have someone pay me to live in another country? Yes I thought, that would be pretty cool.” she laughs. “So, that was then and this is now – and, what gets me out of bed today and every day? I love my job. I really enjoy working. It is such a core part of who I am and what makes my life, my life. I don't have any trouble getting up in the morning. As long as I’m not bored and as long as I’m being stretched, I’m happy.” Have you ever made a business decision you've regretted and can you share it? And, what would you say is your greatest professional achievement to date?

Susie explains she’s made a lot of tough ones, but hasn’t regretted them. “I have been in really very tough environments when I’ve spoken up about things that I simply didn’t think were right. I knew at these times this would most probably (and, she discloses, it did) damage me personally, but nevertheless I felt I had to raise those issues.” “That’s really hard. People don’t want you around when you’re the person talking about the elephant in the room, but, for me, I have to sleep at night and have to keep to some degree true to what I believe is the right thing to do, even if it’s sometimes easier to shut up and not say anything. So I’ve always done that. I wouldn’t say I’ve regretted it and I feel sometimes I’ve been vindicated years later, so it’s not a regret - in fact I think I would have regretted more, not saying something.” Susie explains some of the initiatives she’s been heavily involved in at ANZ, of which she is understandably proud. “Our work on diversity, particularly gender diversity with our Notable Women program has really focused on ensuring women in our organisations have a voice.” “We want them to be confident to speak up as experts, to use them with the media as spokespeople for the bank. The program has really created a degree of confidence from our women that we really didn’t have before.” She tells me proudly of the success of ANZ’s Laos-based CEO Tammy Medard who participated in the program. “Tammy had loads of ability but no one knew who she was. She went on the program, got focused on LinkedIn and Twitter and has since become one of the

9 www.rfintelligence.com.au

“The nice thing about being senior is that you can say and do a lot more and not worry so much about what people think. You can do the right thing, be outspoken and have a point of view, which I always have and I’m quite happy to share it with people. I think overall, people appreciate honesty from others.” Susie Babani Chief Human Resources Officer ANZ

‘Under 40 - People To Watch’. She was invited to present at the United Nations conference in New York, speaking to heads of state about, perhaps most importantly, women's issues in this sector. She rang the bell of the New York Stock Exchange! Something she’s never imagined doing. It’s helped put Laos on the map and it is fantastic for the bank to have these kinds of confident women.” “I’m proud to be a part of this, especially when you see the progress that is being made, like with Tammy.” What do you do to keep evolving your career, to ensure its fulfilling and successful longevity?

For Susie – it’s about a genuine, raw enjoyment. “It’s about what can I do that is new.” Susie tells me, as is no doubt true of most highly functioning successful individuals, she is very easily bored and when she gets bored she admits to being bad tempered and difficult to deal with. “So, thankfully enough, I recognise this and throughout my life and career, I’ve tried to ensure that I don’t get bored. It's not nice for me or anybody else around me!” Although Susie has moved around in her career, ANZ has had her in their midst for 8 years and therefore she consistently ‘reinvents’ aspects of her role. With this in mind, Susie tells me about how over the last 18 months it’s been all about social media. “It’s something that honestly, I wasn't at all interested in, but when I discovered reasons as to why it would be good for the bank, Twitter, LinkedIn, writing articles for BlueNotes (ANZ’s new digital publication for news, insight and opinion), it made perfect sense to jump on-board. And jump on board she did. “I love writing articles. I think I’m probably a frustrated journalist! I like writing for the masses about topics that I’m interested in that hopefully they’re also interested in. It’s probably provided me a bit of a different release. And, when you get to this level, you can write about almost whatever you feel like writing about and people will read it!” she laughs out loud “and that’s really nice!” She continues to say that using new technology has been a fun way for her to share and spread the word typically further than you could have in previous times. Susie shares a moving tale of a post she made some months ago. In the process, she thanks ANZ for their support in what was the sharing of a very confronting music video about a topic Susie felt needed sharing in her own networks. “The nice thing about being senior is that you can say and do a lot more and not worry so much about what people think. You can do the right thing, be outspoken and have a point of view, which I always have and I’m quite happy to share it with people. I think overall, people appreciate honesty from others.” “A few months ago I posted a music video to LinkedIn - Lady Gaga’s “Til It Happens To You”. It is a very, very confronting song and film about violence towards women in colleges in the United States, where 1 in 5 women are assaulted during their time spent studying. It is a beautiful song with a very graphic video which gets you right between the eyes. I felt it was a very powerful message against violence towards women. Now, 10 years ago I probably wouldn’t have had the confidence to post something like that, but today and at

10 www.rfintelligence.com.au

“I'm banning ‘work/ life balance’ as a phrase! I like ‘life balance’... I think work is a really big part of life and I feel ‘work/ life balance’ makes ‘work’ sound like this big, bad, dreadful thing and ‘life’ the fun, lovely thing, when actually, for a lot of people, work is a really cool part of life.” Susie Babani Chief Human Resources Officer ANZ

this level of my career I think ‘No, this is really, really important and powerful and I’m going to tell people that I think this is really important and powerful’.” “I think I have a responsibility to use the position I’ve got to make statements I feel are very important, particularly when it comes to women’s issues.” How do you achieve a work/life balance and what activities do you participate in outside of your working life, that you see contributing to your business success?

“Well Chloé,” she abruptly stops me, but of course, with a smile, “I'm banning ‘work/ life balance’ as a phrase! I like ‘life balance’.” She goes on to make a very good point. “I think work is a really big part of life and I feel ‘work/ life balance’ makes ‘work’ sound like this big, bad, dreadful thing and ‘life’ the fun, lovely thing, when actually, for a lot of people, work is a really cool part of life.” But for the ‘life balance’ she offers some sound advice. Having lived all over the world, Susie is a traveller who is on the quest to visit 100 countries in her lifetime (she has currently visited around 83!) and explains that whenever she can travel for business, she is always the person who will spend the Sunday to extend any business trip and explore. “I have done, and always will, absolutely love it.” “Other than that, I’m a reader, but mostly of novels, not of business books! I go to the theatre and my special time is in spas. Going to the spa for me, massages, facials, scrubs, manicures and pedicures are what I do to unwind. I really do think they help me be successful. Not because my nails always look lovely, but because I take the time to be pampered. I work very hard, I work long hours, I’m on the road a lot so I think it is very important to make sure I take the time to look after myself.” I couldn’t agree more. Do you mentor others? And, what have you learnt in the process?

As the Head of HR, Susie can only informally do so but has “picked up a few” along the way. “They are mostly women, and what I most often learn is, a lot of people who are younger than me, know a lot about things I know very little about! There are so many very smart and very capable people here at ANZ. We also have a reverse mentoring program, whereby I have a young chap (Peter) who mentors me on technology and social. He’s great. Quite a few of us at senior levels have them because we are not the digital natives, we're the digital immigrants!”

What do you think is the most significant barrier when it comes to women in leadership roles?

“In this day and age, even in 2016, so many young women still lack self-belief. There is a lack of confidence, self-belief and willingness to self-promote. That is in stark contrast to what guys are willing to do. I also think many women underplay their competencies. There’s still a bit of that ‘waiting to be tapped on the shoulder/ waiting to be noticed’ and not talking about themselves, out of fear of how that might be perceived.” “It’s such a shame!” I ask her advice on how to overcome these types of issues. “Individuals need to find a way to do it, in a way they are comfortable with. You also need to let management know what you want to do. What’s that next dream job on your horizon? Where do you want to move? What would you like to try? Management are not mind readers, and if you don’t speak up, someone else will.”

11 www.rfintelligence.com.au

“Don’t underestimate how much harder it might be to succeed in the corporate world than you think it will be. It is outlined in clear black and white statistics, that young women are graduating from school and university out-performing their male peers. Over the last few years especially, for the first time they outperform in almost everything. The issue there lies that if this is happening in our schools and universities, why is it not carrying through to our senior, leadership roles in professional services?” Susie Babani Chief Human Resources Officer ANZ

What advice would you give to young women who want to succeed in the workplace and what do you see as the biggest challenge for future generations of business women?

She offers some gentle words of warning, which echo back to the reasons for her own success – hard work and determination. “Don’t underestimate how much harder it might be to succeed in the corporate world than you think it will be. It is outlined in clear black and white statistics, that young women are graduating from school and university out-performing their male peers. Over the last few years especially, for the first time they outperform in almost everything. The issue there lies that if this is happening in our schools and universities, why is it not carrying through to our senior, leadership roles in professional services?” Susie admits that something absolutely ‘happens’ in the work place. “We are doing the research, looking at our data and coming to a clearer understanding around this. We find that even at the point where women are being considered to move into a management role, they are holding back. They are high performers, the role is right, but they’re not following through with an application. We feel there’s a perception of 'if I become a manager, I will be responsible for all sorts of different things. I may not have the flexibility I need at this stage of my life. I may have to go out with clients in the evenings. I may not like it. So I won’t apply’. Rather than ‘actually, let me find out about the facts of the role and even if some of these things are the case, they could, at hiring stage, be up for discussion.’“ Susie also believes that quite often the system also holds them back.

“I call it a ‘benevolent bias’ - the macho phrase of 'oh you probably wouldn’t

want to be out a few nights a week anyway.'. We are looking at the systemic stuff that goes on, as well as the women piece.” “This whole ‘be more assertive, speak up, be direct, be decisive’, which is really just an attempt to make us more like men! It happened in the 80s, 90s and so on but we really need to focus on what the system is doing.” Susie has a leadership level of control in this area and doesn’t take it lightly. “We are looking at how we are recruiting, how we are promoting, what messages we are getting early on in people’s careers that cause the drop off. Like most banks we have lots of women in our non-management grade, but as soon as it gets to that first level of management it drops right off and it continues to drop off as you go further and further up. My view is the glass ceiling starts a lot lower and at a senior management level, it gets exacerbated.” Like many things in life, Susie thinks there is true importance in being aware and thinking about these kinds of issues. Adjusting behaviour, thought process, language is only half the battle. “All I will say is, for the next generation, just because things were great at school and university, that’s not necessarily what the workforce will be like. Don’t be complacent. It’s not bad, it's just tougher than you think.” What’s the best piece of advice you have received as a woman in a leadership role that you would pass on to others hoping to get there?

Susie has two clear pieces of advice. The first being career management. “A boss once told me ‘no one will care about your career as much as you do.’ It was such a good piece of advice. It's moving away from that victim or waiting to

12 www.rfintelligence.com.au

“A boss once told me ‘no one will care about your career as much as you do.’ It was such a good piece of advice. It's moving away from that victim or waiting to be picked mentality. It’s being the picker, the person who goes out there and says ‘well it’s my career, I have to manage and own it.’” Susie Babani Chief Human Resources Officer ANZ

be picked mentality. It’s being the picker, the person who goes out there and says ‘well it’s my career, I have to manage and own it.’” The same boss gave Susie the second piece of advice she chose to share: “Don't dwell on your mistakes for days on end, because no one else will. Pick yourself up and move on. Again for women this is particularly relevant, we tend to dwell for ages. ‘I made a mistake so my boss must hate me.’ Well no, he might hate the piece of work you did, but he doesn't hate you. The mistake is not about you, it's about what you did. We beat ourselves up privately and it really has to stop. Don’t keep making the mistake obviously, but get over it, move on and keep growing.” It was my true pleasure to interview Susie; an insightful, moving and inspirational interviewee and I hope you enjoyed this Women in Leadership piece. To read the full Women in Leadership series and all past Australian Retail Banker editions, feel free to visit to archive centre on our website.

13 www.rfintelligence.com.au

“When I first moved to Australia my view of the broker was that they got you the best deal, now, I have completely changed my view. They facilitate the whole thing. The good deal and taking care of you during the process, giving you the peace of mind that you are prepared and have ticked all the boxes.” John Arnott Executive Director – Customers ING Direct

RFi Group Interview Chloé James’ interview with John Arnott, Executive Director – Customers, ING Direct On the eve of RFi Group’s biggest ever Australian Mortgage Innovation Summit, Chloé James sat down with John Arnott, Executive Director – Customers (a most fitting job title, which we will come to later) at ING Direct, to discuss all things mortgages. John is one of the key speakers at the 2016 event and we felt it pertinent to pick his brains about the mortgage market, the industry’s response, as well as his perceptions and advice for those working in the space. Amidst a most timely week, John arrived for our interview straight from one of his own, having just purchased a new home and ‘going through the same motions’ as many of his customers. The first words from his lips: “This process is not easy!” John echoes many customer’s sentiments that a mortgage is going to be hard work, with a sense that one must “brace themselves for the challenge.” And herein for John, lies the challenge for banks to see how they can make the process easier. In the past, the Australian mortgage market had been one where credit growth was so strong, he feels that for some time, there hadn’t been a need to focus greatly on the mortgage product, and even more so, the experience that came with it. “In years gone by, business just kept coming through the door. But in today’s climate, if you look at putting the customer back into the home buying experience, it’s not just around the design of products anymore, but the experience you go though in selling or buying a home – it’s a really complicated process.” We know that home lending takes time, is emotionally heavy and undoubtedly one of the most significant financial decisions a person will make and John can, through his own experience, understand why the broker value proposition is incredibly compelling. “When I first moved to Australia my view of the broker was that they got you the best deal, now, I have completely changed my view. They facilitate the whole thing. The good deal and taking care of you during the process, giving you the peace of mind that you are prepared and have ticked all the boxes.” John explains that if he didn’t sit where he does (surrounded by numerous home lending experts), the broker would absolutely be his first port of call. But – he challenges – what can the industry do to make the other channels as attractive? “The product may be technical, but the process isn’t. My feelings are that the industry has not made it easy. A broker makes it simple, they take the complexity away. Now, to me, although I obviously advocate the broker channel, there’s no reason why we as an industry shouldn’t be able to simplify this process.” He continues on to say that the entire industry has a lot of room for improvement. “From a very simplistic view, banks have relied heavily on medium to high levels of credit growth and with that, has come a continual flow of new business through the door.”

14 www.rfintelligence.com.au

“In my view, when you buy a home you want it to be an exciting process. Yes, it’s a huge financial commitment but it’s also the place where your kids are going to grow up, where you can decide what kind of BBQ you’re going to buy. This industry should be focused on making the experience of going through that process, at least on some level, enjoyable. That’s where I truly feel the industry is lacking and if someone can get that part right – it is just a massive opportunity.” John Arnott Executive Director – Customers ING Direct

An area he feels needs more attention at an industry level is catering to existing customers. “I will say that there has been a significant lack of focus in this area.” He believes that the level of engagement is low, with far too much focus on winning new customers. The question then is, how do banks maintain growth and also deliver for their existing customer? “Thus far, the churn has been more than offset by new business. Where I feel there now needs to be a true focus, is on standing up and looking at what we can do for our existing customer base. How do we deepen and lengthen those relationships? There’s a danger for many organisations that once you have provided a home loan, there can be a supremely low level of customer engagement – it becomes the ‘sell and forget’ product, which I feel absolutely has to change.” At ING Direct, John explains, it’s about providing customers with financial empowerment and giving them the facts about their loan or their investment, balanced with correct levels of engagement. When a customer chooses their lender, they choose based on peace of mind, so John and his team are fine-tuning where on the spectrum the level of communication should sit. “It’s a fine line between giving customers’ choice and making it easy for them.” With this in mind John points out that in the service sector, pretty much everything else in life is easy and if banks don’t make what they do ‘easy’, “someone else will”. He believes that it’s about creating simplicity and forcing the industry to look at the way they do things. “Regulation and legislation also play a large part in making sure customers are protected, and where other sectors of the industry have done a good job of creating simplicity, I do think in the home buying business, it’s just not there yet.” Speaking of his own experience: “In my view, when you buy a home you want it to be an exciting process. Yes, it’s a huge financial commitment but it’s also the place where your kids are going to grow up, where you can decide what kind of BBQ you’re going to buy. This industry should be focused on making the experience of going through that process, at least on some level, enjoyable. That’s where I truly feel the industry is lacking and if someone can get that part right – it is just a massive opportunity. In plain English and to be honest with you, there is a lot of jargon in this industry which indicates to me the industry designed the process around themselves, not the customer. That needs to change.” For ING Direct, digital of course continues to be an area of focus for the lender. “Such a large proportion of our customers are savers, and they save in a digital way. We are looking closely at how to engage via the right channel, at the right time.” John explains how the use of mobile has increased the opportunity for engagement exponentially, as these customers are - by nature of the channel - far more engaged with their personal finances and their lender. “For us it is about leveraging these multiple touch points in the right way, to engage these customers with compelling offerings that are relevant to them and their needs. My focus is offering the right deal, at the right time, at the right price.” In terms of the customer, I wonder where John sees the pockets of opportunity. “While it’s true that credit growth is slowing, our country’s population is certainly not. Sydney’s population alone has predictions of up to 6 million people over the next few years. Pockets of cultural immigration centres are absolutely of

15 www.rfintelligence.com.au

“While it’s true that credit growth is slowing, our country’s population is certainly not. Sydney’s population alone has predictions of up to 6 million people over the next few years. Pockets of cultural immigration centres are absolutely of interest, but for me, the inter-generational transfer of wealth is really, really interesting. Especially for ING Direct.” John Arnott Executive Director – Customers ING Direct

interest, but for me, the inter-generational transfer of wealth is really, really interesting. Especially for ING Direct.” As Baby Boomers mature, John speculates about how their wealth will transfer through generations, creating a new cohort of customers who, with inflation, will potentially have higher levels of deposits than their predecessors. “I’m interested to see how this will affect the mortgage industry in particular. If so much advocacy is now via word of mouth and based on customer experience, at ING Direct for example, we are seeing more and more of our saver customers growing up, buying houses with us, and can only hope their children are our future customers. People who joined 17 years ago for example, with our hugely successful savings product, chances are they have bought a home, maybe got married, had kids – in 20 or so years these children will start to think ‘where’s my first home loan coming from?’.” John knows full well that the socially connected world we live in today means advocacy is one of the most important, if not the most important, factors in retention and acquisition. “Word of mouth goes a long, long way. Far beyond that what we probably even think. A few years ago, talking about your financial product was unheard of. But as attention has moved from product to experience, across varied industries, people are more than happy to talk about their experiences, and this includes their banking experiences. I’m absolutely sharing my views around my own home buying experience with people. Not rates etc., but the experience I’m having - 100%!” John has been with ING DIRECT for 9 years. He was in fact, the very first client I met when I began working at RFi Group and his energy has always caught my attention. We therefore close with what gets him out of bed every day, and what it’s like to work for a steadily growing challenger. “I really feel I am at an organisation where I can make a difference. Accountability and empowerment is heavily promoted and readily available to those who seek it. I love the freedom of driving innovation. ING Direct is not afraid to try things. It’s ‘Give it a crack. Fail fast. Learn.’. I’ve always really enjoyed that. Also, variety. In nine years I’ve had six different roles, allowing me the opportunity to try new things and stretch my capabilities. It’s knowing you can throw yourself into the unknown, with the knowledge that you’ve got a strong support network to back you.” “It’s not a typical “bank-like” environment. We feel more like a disruptor and we revel in that space. I also like our global element. We have the privilege of global advice and the ability to export ideas. Being a global organisation with local autonomy is an exciting place to be.” “Finally, customer centricity. It’s a well-used and well-talked phrase, but I’m not convinced how true that is of the industry. I believe we have and have always had, a true customer focus and I’m really, really proud of that. Our products and service are designed around the customer as opposed to around a P&L or balance sheet. Of course we acknowledge that our business needs to be profitable, but the balance between the business and the customer winning is truly equitable. We strive to achieve sustainable profit growth without compromising the customer experience.” Lastly, John comments on his obsession with continuously trying new things. Doing the right thing by the customer and trying and failing, is a business attribute and is in line with the core value around simplicity, true to ING Direct.

16 www.rfintelligence.com.au

“It’s not a typical “bank-like” environment. We feel more like a disruptor and we revel in that space. I also like our global element. We have the privilege of global advice and the ability to export ideas. Being a global organisation with local autonomy is an exciting place to be.” John Arnott Executive Director – Customers ING Direct

“To sum it up, I think ING Direct has got the right mix of understanding where technology and customer needs collide; the sweet spot. I believe we have the understanding of embracing technology without losing site of these core hygiene customer moments of truth.” We look forward to hearing more from John in a few weeks. Secure one of the last remaining tickets to the Australian Mortgage Innovation Summit today.

Follow @RFiMediaGRB on Twitter to keep up to date with the latest information and news at RFi Group.

18 www.rfintelligence.com.au

“During periods of changing housing market conditions it’s important for us to constantly challenge ourselves that we are continuing to offer customers the right products to meet their needs through the channels where they want to interact with us.” Sue Coulter General Manager Business Transformation & Technology (CIO) CUA

RFi Group Interview Chloé James’ interview with Sue Coulter, General Manager, Business Transformation & Technology (CIO), CUA On the eve of the Australian Mortgage Innovation Summit, RFi Group thought it pertinent to sit down with CUA’s Sue Coulter, one of the key speakers at the Summit, who joined the customer-owned financial institution in 2010 to take ownership of their technology and business transformation. With a new core banking platform in place and performing well, one of Sue’s focus areas is on leveraging this investment through the delivery of a continuous program of customer service and product enhancements. She is also responsible for replacing the remaining legacy systems and enhancing CUA’s digital and data technology solutions. With over 30 years’ financial services experience across a broad range of senior management and executive positions within Australia and the UK, ahead of the 2016 Summit, we requested Sue’s view on the ‘state of play’, if you like, of the Australian housing and mortgage market. With the current unstable state of the housing market in Australia, particularly in Sydney and Melbourne, we wondered how Sue suggests banks can survive and thrive. “Much like our fellow financial institutions, we are not expecting the same results as last year in Sydney and Melbourne. However, from a CUA perspective, we continue to experience steady growth in other areas. We were delighted in the first three months of FY2016 to deliver a 9.8% annualised year to date balance growth in home loans, compared to 7% system growth. During periods of changing housing market conditions it’s important for us to constantly challenge ourselves that we are continuing to offer customers the right products to meet their needs through the channels where they want to interact with us. Selling our loans through brokers is also an advantage given the popularity of the channel however, we are also focused this financial year on enhancing the loan origination experience in our 59 branches.” Sue continued that if your products are competitive then there is only one area left to compete in, and that’s service. So CUA have tended to focus on what they are in control of and what they can do better. Sue revealed some clearly focused initiatives: “We are focusing a lot of attention on internal processes such as streamlining various steps which are unnecessary in the end-to-end home loan process, in areas such as verification. There are often so many steps that have built up over a period of time that need to be challenged!” she exclaims. Focusing on efficiencies in the back office to help speed up what can be such a lengthy process is CUA’s focus this year. They clearly know it is no secret that the faster you can make an offer and facilitate an approval, the higher the likelihood of retaining that yield. And they’ve had some pretty impressive results. In FY2015, CUA achieved significant growth in new home loans – the $3.35 billion in new loans issued during the year was up by 55% from the previous year. Sue continued to say “that was a very good year for us – a record in fact, and I believe it had a lot to do with our focus on improving our back office processes, an area we could control. Anything to shave some time off can be a lengthy and often arduous process.” If the processes are speeding up, what is CUA’s view on the consumer? Their customers, behaviour, habits, and trends.

19 www.rfintelligence.com.au

“P2P isn’t particularly threatening the home loan space yet, but in terms of personal loans and the potential knock on impacts to credit cards, the threat from P2P is already very real.” Sue Coulter General Manager Business Transformation & Technology (CIO) CUA

“Over the past 10 years the biggest shift has been the greater and greater use of the broker channel. Going forward I think Positive Credit Reporting will drive another shift in lending and consumer behavioural change. This will not only provide institutions with the ability to price more reliably for risk and tailor our products and services at an individual level. Perhaps most importantly, it will give customers much greater insight into their own credit score and how they can positively and negatively influence it as well as giving them the power to potentially negotiate their own deals based on their credit score. I absolutely see this changing consumer borrowing behaviour.” In terms of lower value lending, Sue’s eye is sharply set on P2P lending. Not only in changing consumer behaviours, but in changing their expectations. “It’s the speed at which the P2P lenders are rattling through an online application and getting funds in customers’ accounts that are making the larger more traditional players sit up and realise we’ve got to try to compete in that market too. P2P isn’t particularly threatening the home loan space yet, but in terms of personal loans and the potential knock on impacts to credit cards, the threat from P2P is already very real.” As Sue rightly points out, P2P lenders and other new entrants don't have to deal with the same legacy constraints that larger, more established organisations do. They have the opportunity to work in a truly Greenfield way, which will put more and more pressure on established banks. “We need to be constantly cognisant of that,” Sue added. “I think from a customer experience perspective, customers are wanting and expecting a more frictionless, omni-channel experience, where they can move seamlessly between applying online, to picking up the phone, or going in to a branch. They also then want to be able to transact and service that product in a way that works best for them.” To tackle the task, CUA are about to embark on Phase Two of their new Loan Origination Platform, which will incorporate a process that will allow customers the ability to do precisely this. “The home loan process can be complex enough, particularly if you’ve never done it before, so we are doing everything in our power to streamline and make the process easier. This involves a seamless experience from browsing on the web to completing an application - whilst technically we might move from one system to another, the experience is seamless for our customers”. Sue explains this involves going back to basics - not asking for the same information twice, giving customers a decision as quickly as possible and really, just making the process simple for them end-to-end. If a customer wants to do everything online, then make that possible. “From the uploading and submitting of documents, to electronic verification and so on, Phase Two is about trying to build one, single origination interface which will work for any product. It is about streamlining as much as possible, making systems available in any form a customer wants and it’s absolutely about stripping out anything you don't need, particularly around documentation. It goes right down to the contract, trying to make contracts simpler to understand - it is truly simplifying the full end-to-end process.” Simplifying processes, Sue explains, is enhanced exponentially with the right technology and digital applications. Although it has never been more important for the financial services industry to ensure they are operating in a digitally savvy way, they also need to continue to offer choice. “What’s really interesting is when you survey 20 to 30 year olds who might be looking for their first loan, you will see that although some want to conduct this all online, others absolutely want to talk to someone. It’s a complex product for some. I think it all comes back to tailoring products and services based on the needs of individual people in a digital world, as well as face-to-face. I don't think there's a ‘one size fits all’ approach and when you look at the research, it is

20 www.rfintelligence.com.au

“A few years ago we took on the most complex project you can do in banking, replacing our core system in two and a half years and we are now reaping the rewards. We are now able to tailor products and roll them out quickly so we are really seeing the benefits of that investment.” Sue Coulter General Manager Business Transformation & Technology (CIO) CUA

certainly showing a varied desire for a totally online experience, especially with products such as a home loan.” Sue is clearly driving significant change at CUA and we closed with her joy and obvious passion in doing so. “What I love most is the diversity of my role. I look after technology as well as business transformation, so my team and I are involved in every project in the organisation. When you blend technology and transformation, it’s incumbent on me to look at opportunities in non-traditional areas that might provide improved experiences for our customers or staff via external innovators or partners. She described a current “passion project” with ‘River City Labs’, an initiative where CUA sponsors desks in the thriving Brisbane start-up community. “Sponsoring desks so that new starts-ups have somewhere to go and work within an environment to foster their ideas is amazing.” And it’s a two-way street. In the process, CUA has been approached by a number of bright young start-ups (and vice versa) to discuss joint opportunities. Because CUA is smaller than the regional and major institutions, Sue enjoys agility and being able to do things more quickly, with less red tape. “A few years ago we took on the most complex project you can do in banking, replacing our core system in two and a half years and we are now reaping the rewards. We are now able to tailor products and roll them out quickly so we are really seeing the benefits of that investment.” CUA has a true customer focus, of which Sue is extremely proud. “For me, it really is about the customer, it is what we can do for them, what we can do to make their life easier and simpler so they have more time to focus on what makes them happy, whilst having confidence their finances are with an organisation they can trust. That truly is CUA's ethos. We are a customer-owned banking institution, not driven by shareholders, and our conversations, thinking and strategic planning will always remain focused on that.” We look forward to hearing more form Sue at the AMIS 2016. Be sure to secure your ticket today. Follow @RFiMediaGRB on Twitter to keep up to date with the latest information and news at RFi Group.

21 www.rfintelligence.com.au

Source: RFi Group

Transactions news

CBA opens ‘innovation lab’ in HK

CBA has launched an ‘innovation lab’ in downtown central Hong Kong, which is based on the bank’s innovation lab in Sydney. According to KC Chan, Secretary for Financial Services and the Treasury of Hong Kong, "Financial institutions in Hong Kong are adopting the innovations and I see a lot of collaborative opportunities between financial institutions and start-ups." CBA utilises a “partnership model”, unlike other Big Four banks who have taken equity stakes in FinTech start-ups, whereby CBA collaborates on particular bank projects and particular consumer problems. According to Kelly Bayer Rosman, CBA Group Executive of Institutional Banking and Markets, CBA does not apply a one-size-fits-all rule when dealing with FinTech start-ups. “As the partnerships evolve, we will negotiate the right terms and basis [to] suit that specific partnership.” CBA also plans to open a similar facility in London in July. Ms Bayer Rosmarin indicated that the opening of the new labs is a valuable means of both engaging with the FinTech community and keeping CBA staff engaged with creative ideas FinTechs could bring to the table, and not merely a marketing ploy. The importance of keeping up with FinTech innovations is supported by RFi Group data, which shows around 1 in 7 Australians under 35 years old define their main bank as the bank that has the best mobile banking offering.

Growth in New Zealand transactions

Earlier this year, New Zealand payments firm Paymark said December activity showed strong growth, with the number of card transactions up by 8.2% from a year earlier. There were 106.05 million transactions conducted on the Paymark network in December, which accounts for more than three quarters of New Zealand’s EFTPOS terminals. Figures, subsequently released, from Statistics New Zealand also indicate that the number of electronic card transactions rose 6.2% year-on-year in December to 143 million. Additionally, the average value per card transaction rose to $54 in December, up from $51 in November. Statistics New Zealand figures also indicate that an increasing number of card transactions are being made on credit cards at the expense of debit cards. In December, 54.3% of transactions were made on debit cards compared to 55.6% a year earlier, and 45.7% on credit compared to 44.4% over the same period.

Basel committee eases global bank capital build

While global banks will still need to lift the amount of capital they hold against their trading books, the increase required by the Basel Committee on Banking Supervision will be lower than originally proposed. Rather than an increase of 75%, as suggested by the original consultation paper, the Basel Committee has released revised minimum capital requirements for market risk, that will see the average global bank needing to increase the amount of high-quality capital held against trading books by an average of 40% come January 2019. According to industry analysts, the softening stance is an indication regulators are moving away from punishing banks for the impact of the global financial crisis, and allowing them to focus more on lending and generating economic growth. An easing in the global capital build may see Australian banks more easily achieve ‘unquestionably strong’ status – the capital adequacy measure put forward by the Financial Systems Inquiry in 2015. For banks to be regarded as ‘unquestionably strong’, they would need to have capital ratios that position them in the top quartile of internationally-active banks.

17%

14%15%15%

5%

8%

0%

5%

10%

15%

20%

25%

Under35 yo

Above35 yo

Total

What makes you define your main bank ?

It has the best internet bankingoffering

It has the best mobile bankingoffering

22 www.rfintelligence.com.au

Source: RFi Group

Savings news

Retirees spending less to leave nest egg

According to RFi Group data, only 5% of over 65 year olds are saving for a comfortable lifestyle, compared to 40% who have no savings goal. This may be explained by a new study by the Commonwealth Scientific and Industrial Research Organisation (CSIRO), which found that Australian retirees are spending modestly to leave behind a nest egg for their children and family instead. According to behaviour economist, Andrew Reeson, “It does seem far from ideal… that so much of the savings people have built up may end up being enjoyed by others.” “It seems no matter how large a person’s superannuation balance, they stick to the minimum drawdown rates mandated by the government [for tax and pension purposes],” said Reeson. Politicians have long encouraged retirees to spend their superannuation savings instead of counting on pension payments. “It is not unreasonable for people who have benefited from tax concessions to build up sizeable superannuation balances to then be expected to draw down on those balances in retirement, rather than draw on a taxpayer-funded pension," said then Minister for Social Services, Scott Morrison at a press conference last year. Since becoming Treasurer of the Federal Government, Scott Morrison could be looking into cutting tax concessions for those who retire wealthy. In November last year, he spoke at the Association of Superannuation Funds Australia and hinted at potential superannuation changes for the future generations of retirees.

Share market threatens superannuation savings

The volatile share market is becoming an increasingly dangerous risk to retirees’ superannuation savings. Economist Mike Rafferty from the University of Sydney Business School told the ABC's AM program that, while there is always risk in the share market, some retirees are more exposed than they think. "Over the last 20 years we've forced more and more people into the stock market through compulsory superannuation," Dr Rafferty said. "So suddenly people have woken up after the global financial crisis and found out that their retirement expectations are very highly exposed to movements in the stock market." According to Dr Rafferty, up to 90% of the returns on superannuation funds are linked in some way or another with stock market returns. "Australia's probably the most highly-exposed in terms of putting its retirement savings in the stock market and events like the last week or two really bring that risk home again," he warned.

Two out of three Aussies short on retirement savings

According to the latest MLC Wealth Sentiment Survey, two out of three Australians do not think they will have enough savings to fund their retirement. The study also found that almost half of Australian women consider taking a career break to raise children. This represents a barrier to saving sufficient retirement funds, with around two thirds of women taking more than two years out of the workforce to have kids. Australians, on average, expect to retire with about $471,000, but women believe they will have only $390,000 while men project they will have $538,000. In addition, households with kids rated all barriers to retirement higher than those with no kids. Only 30% of Aussies with children believed they have enough funds to invest in retirement. “The survey results highlight that more needs to be done across the board to ensure a comfortable retirement – particularly for families with kids. It’s important for families to not only consider their immediate budget, but also their future cash-flow,” said NAB’s general manager, corporate super, Lara Bourguignon.

40%

16%

13%

10%

5%

0% 20% 40% 60%

I have nosavings goal

Retirementsavings

Unexpectedexpenses

Travel/ holiday

To have a morecomfortable

lifestyle

Top 5 savings goals65+ year olds

23 www.rfintelligence.com.au

Source: RFi Group

Source: RFi Group

Source: RFi Group NZ Program Research Data

Mortgage news

Tighter lending policies have created a reduction in “borrower power”

New data shows that the major banks have become stricter in their home lending controls and reduced the amount they are willing to lend home buyers. Mortgage broker, Homeloanexperts.com.au, reported that a couple with a combined income of $120,000 can now borrow up to $80,000 less on an investment property than they could a year ago, and up to $65,000 less on an owner-occupied loan. The fall in "borrowing power" is attributed to the tighter bank credit policies, which were introduced during 2015 amid the Australian Securities and Investments Commission’s (ASIC) concerns that mortgage lending had become too risky. Christina Parnham, a mortgage broker at Homeloanexperts.com.au, believes that as a result of the new regulations banks are testing prospective borrowers on how they would cope with higher interest rates, despite the current cash rate being at an all-time low. Additionally, Parnham believes banks have adopted more conservative assumptions about customers’ living expenses, after ASIC claimed that many lenders were incorrectly assessing these costs.

Yellow Brick Road brand gets a facelift

Yellow Brick Road (YBR), an ASX-listed mortgage and wealth management franchise, has rejuvenated its brand, with Chief Commercial Official Scott Graham saying, “The old branding had served us well for some time but over the years our business has grown and developed. While the old look was fashion forward at the time it has grown tired. It was time for an update.” YBR will move away from the traditional six year old yellow and brown logo to a new brighter yellow and charcoal look that better demonstrates YBR’s desired image. The franchise has also opted for a more engaging interior design, with trendy furnishings and wall graphics. The new brand look will be rolled out in a staged approach to over 250 branch licensees across Australia.

First NZ home loan rate cuts in 2016 by SBS Bank and BNZ

Non-major lender SBS Bank has cut its ‘special’ three year fixed home loan rate by 14 basis points to 4.65%, making it the lowest offer currently on the market. The new rate will be available in January for existing SBS Bank customers; new customers may qualify if they take out new lending of at least $100,000 and also take up at least one SBS insurance product. The SBS Bank ‘special’ requires borrowers to have a minimum of 20% equity in the property, with salary or wage payments to also be made into an SBS transaction account. The SBS offer was quickly followed by Bank of New Zealand (BNZ), which unveiled its own 4.49% special offer for 3 year fixed loans. BNZ also lowered its two year fixed rate to 4.39%. Bruce McLachlan, Chief Executive of The Co-operative Bank, which currently leads the market across one year to five year fixed term categories – without ‘specials’ – personally believes the current rates are certainly at the bottom of the cycle. “I would expect that over time we will see them edge up," he said. According to RFi Group New Zealand data, in September 2015 81% of mortgage holders had a fixed or partially fixed rate loan on their most recent loan, up from 78% 12 months ago.

78%

81% 81%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Sep-14 Apr-15 Sep-15

What type of interest do you pay on your most

recent loan?Fixed rate or part fixed

rate

24 www.rfintelligence.com.au

Source: RFi Group

Cards news

Push for transparency on credit card rates and fees

A Senate committee has recommended that Australian financial institutions include the interest rate and the continuing annual fee on monthly credit card bills. In its recommendation to the Government, the committee said it believes “there is strong and compelling evidence to suggest that part of the reason credit card interest rates are so high is that card providers know consumers often pay little attention to their significance.” The committee argued that by drawing attention to the interest rate and ongoing fees, Australians would become more aware of the unnecessary costs they are footing and seek to switch their to lower-cost alternatives.

New year, new credit card deals

RFi Group data shows that 12% of credit cardholders chose their most used card because of the rewards program attached to the card, with air points being considered the most appealing type of reward. In order to attract new customers in the New Year, many credit card providers are offering bonus Qantas Frequent Flyer points to new cardholders. American Express (AMEX) has released two promotional deals to accompany its Platinum Charge Card and Qantas Premium Credit Card. New customers who apply for the Platinum Charge Card will receive 100,000 Membership points which can be converted to 100,000 Frequent Flyer points, with an ongoing offer of 2 Frequent Flyer points per dollar spent on airlines, hotels tours and travel agents in Australia. AMEX is also offering 82,500 Frequent Flyer Points when a new customer takes out a Qantas Premium Card and these customers will continue to earn 2 Qantas Frequent Flyer Points for every dollar spent at major supermarkets and at petrol stations in Australia. In addition to AMEX, ANZ, Citibank and NAB are also offering promotional deals, with new cardholders receiving at least 60,000 Frequent Flyer points when signing up to the Qantas Frequent Flyer Black, Prestige Visa Infinite and Qantas Rewards Premium cards, respectively.

Card spending rises while ATM withdrawals fall

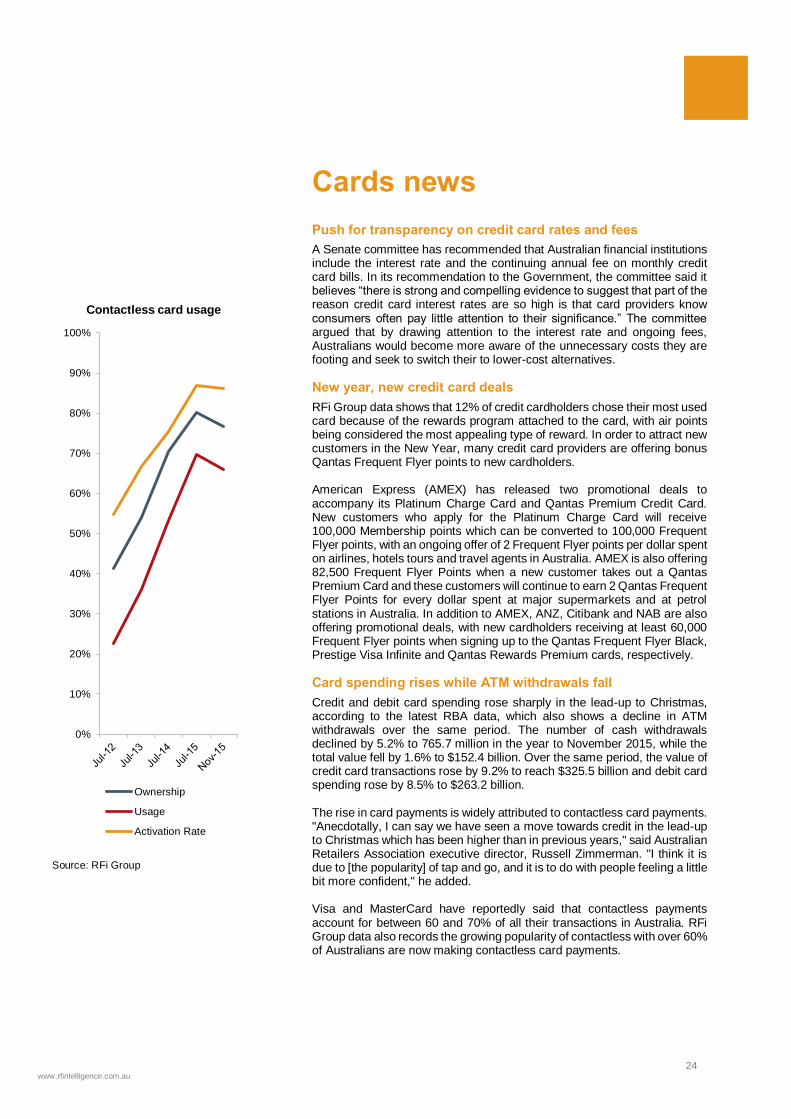

Credit and debit card spending rose sharply in the lead-up to Christmas, according to the latest RBA data, which also shows a decline in ATM withdrawals over the same period. The number of cash withdrawals declined by 5.2% to 765.7 million in the year to November 2015, while the total value fell by 1.6% to $152.4 billion. Over the same period, the value of credit card transactions rose by 9.2% to reach $325.5 billion and debit card spending rose by 8.5% to $263.2 billion. The rise in card payments is widely attributed to contactless card payments. "Anecdotally, I can say we have seen a move towards credit in the lead-up to Christmas which has been higher than in previous years," said Australian Retailers Association executive director, Russell Zimmerman. "I think it is due to [the popularity] of tap and go, and it is to do with people feeling a little bit more confident," he added. Visa and MasterCard have reportedly said that contactless payments account for between 60 and 70% of all their transactions in Australia. RFi Group data also records the growing popularity of contactless with over 60% of Australians are now making contactless card payments.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Contactless card usage

Ownership

Usage

Activation Rate

25 www.rfintelligence.com.au

Source: RFi Group

Personal loan news

A rise in interest rates could threaten P2P lending

The booming peer-to-peer (P2P) lending market has been helped by a period in which interest rates have dropped to a historic low, as well as struggling equity markets that have made fixed returns of more than 10% attractive to prospective investors. However, in 2016 the sector may face its biggest test yet. When US Federal Reserve chair, Janet Yellen, raised rates for the first time in nine years in December 2015, American analysts started speculating that customers of P2P lending start-ups such as SocietyOne, RateSetter and MoneyPlace, would return to more traditional banking institutions which now offer healthier margins to investors. If the RBA lifts the official cash rate in 2016, analysts believe the pressure on the P2P is likely to be worse than it is overseas, given that the big banks are still trusted in Australia. While the financial crisis severely undermined trust in banks in the US and Europe, that hasn't been the case in Australia.

CBA does referral deal with OnDeck

CBA has forged a deal with lending start-up OnDeck to refer customers to each other after a year assessing suitors from an explosion of lending start-ups. CBA said it will refer selected small businesses from its 500,000 customer base that it can't lend to because they do not meet strict requirements – including the need for security, such as a family home – to OnDeck, which set up in Australia in April 2015 and began lending in late November. Clive van Horen, CBA's head of small business and retail banking services said the bank has spoken to a large number of potential partners among the numerous start-up business lenders, but decided OnDeck – which has loaned US$3 billion ($4 billion) since starting in 2006 at interest rates of between 5.99 and 9.9% – has the proven track record it required. Westpac is considering forming a similar partnership with lending start-up Prospa, after initiating a trial in December 2015.

Females more likely to take out a loan for travel

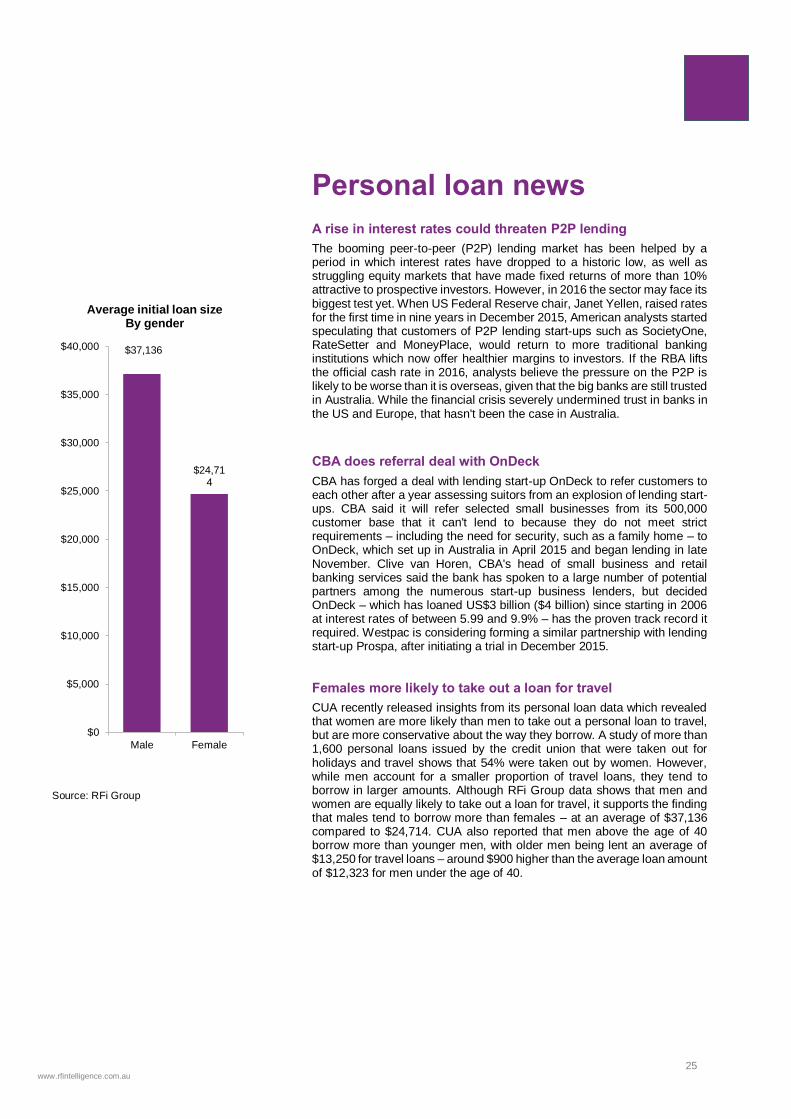

CUA recently released insights from its personal loan data which revealed that women are more likely than men to take out a personal loan to travel, but are more conservative about the way they borrow. A study of more than 1,600 personal loans issued by the credit union that were taken out for holidays and travel shows that 54% were taken out by women. However, while men account for a smaller proportion of travel loans, they tend to borrow in larger amounts. Although RFi Group data shows that men and women are equally likely to take out a loan for travel, it supports the finding that males tend to borrow more than females – at an average of $37,136 compared to $24,714. CUA also reported that men above the age of 40 borrow more than younger men, with older men being lent an average of $13,250 for travel loans – around $900 higher than the average loan amount of $12,323 for men under the age of 40.

$37,136

$24,714

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

Male Female

Average initial loan sizeBy gender

26 www.rfintelligence.com.au

Source: RFi Group

Payments & digital news

Samsung Pay coming to Australia in 2016

Samsung recently announced it will be bringing its Samsung Pay system to Australia in 2016. Australia's banks are likely to be drawn to Samsung Pay over Apple Pay, given that it will not be charging a commission. The goal of Samsung Pay is to help Samsung sell more phones. Thomas Ko, the global co-general manager and vice president of Samsung Pay, said "We don't charge a fee to the banks, and so far that has been one of the reasons why the banks are very receptive to our propositions." Samsung says it has already signed up at least two Australian banks to support Samsung Pay. None of the major banks have yet announced a deal with Apple Pay, which is currently only available in Australia via American Express (AMEX). RFi Group data suggests Apple Pay adoption is likely to remain low in Australia – just 9% of smartphone and/ or tablet owners surveyed in December 2015 are likely to use Apple Pay, while an even lower proportion are likely to apply for an AMEX card to use Apple Pay.

Big jump in mobile banking in 2015

Bank customers are increasingly using mobile apps as a way of checking their finances on the run, with NAB reporting that the number of account logins using smart phones grew by 26% in the 12 months to December 2015. This figure is up by 92% compared to three years ago and is in line with RFi Group data, which shows that the proportion of smartphone owners that use mobile banking apps has increased from 38% to 49% over the 2 years to December 2015. NAB's general manager of digital, Todd Copeland, said there is also a growing shift towards customers logging in for sessions of less than 30 seconds. As a response to this trend, NAB has this month become the latest Australian bank to target customers seeking quick access to information on their money by launching an app for Apple watch. It will allow customers to check their balance more quickly without entering a password, a feature also available on its mobile app.

UBank relaunches with ‘Just the Bank You Need’ rebrand

In the last week of January 2016, Australia’s online-only bank UBank unveiled its new brand identity ‘Just the Bank You Need’. UBank believes the rebrand and ethos behind the phrase will allow them to better service customers by offering them only what they ‘need’ from a bank, and nothing they don’t. The bank’s new philosophy will challenge customers to take a look at the life they’re leading and question what they really need, versus what they want, in effect encouraging them to borrow less, have less debt and subsequently live more. UBank CEO Lee Hatton said of the new rebrand “It’s about asking the question – could you borrow less and live a happy, or even happier, life? We want our customers to have a healthy relationship with their finances, and that can come down to taking out a smaller mortgage, reducing credit card limits, or simply switching to a higher interest rate bank account.” Lee will present more on this at RFi Group’s upcoming Australian Mortgage Innovation Summit where she joins us a speaker.

9%

4%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Likely to useApple Pay

Likely toapply for

AMEX card touse Apple

Pay

Proportion of consumers likely to use

Apple Pay