what is happening in retail and the australian consumer group- retail presentation by trent... ·...

TRANSCRIPT

What is happening in retail and the Australian consumer goods market?

Disclaimer

These slides are not for commercial use or redistribution. The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. KPMG have indicated within this presentation the sources of the information provided. KPMG has not sought to independently verify those sources unless otherwise noted within the presentation. No reliance should be placed on additional oral remarks provided during the presentation, unless these are confirmed in writing by KPMG. KPMG is under no obligation in any circumstance to update this presentation, in either oral or written form, for events occurring after the presentation has been issued in final form. The findings in this presentation have been formed on the above basis.

Forecasts are based on a number of assumptions and estimates and are subject to contingencies and uncertainties. Forecasts should not be regarded as a representation or warranty by or on behalf of KPMG or any other person that such forecasts will be met. Forecasts constitute judgement and are subject to change without notice, as are statements about market trends, which are based on current market conditions.

Neither KPMG nor any member or employee of KPMG undertakes responsibility arising in any way from reliance placed by a third party on this presentation. Any reliance placed is that party’s sole responsibility. The presentation (and the accompanying slide pack) is provided solely for the benefit of the conference attendees and is not to be copied, quoted or referred to in whole or in part without KPMG’s prior written consent. KPMG accepts no responsibility to anyone other than the conference attendees for the information contained in this presentation.

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

How is the Australian market performing?

…trends have continued based on public Q3 sales information3

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Growth has been strong and consistent across most categories – Electricals and Hardware have outperformed

Australian Retail Sales Statistics – Year-on-Year Movement, By Category

Source: ABS 8501; Table 11 Unashamedly.com.au

Prior year Current year

Dec-13 Jan-14 Feb-14 Mar-14 Dec-14 Jan-15 Feb-15 Mar-15Supermarkets 7% 8% 5% 4% 4% 3% 4% 4%Liquor 0% 5% 3% -2% 7% 3% 5% 7%Specialty food 4% 4% 1% 0% 0% -6% 0% -2%Cafes, restaurants 16% 17% 15% 18% 2% 5% 3% 2%Takeaway food 4% 7% 4% 1% 8% 7% 8% 7%Furniture, homewares 8% 8% 7% 12% 9% 6% 6% 7%Electricals 0% -1% -1% 2% 9% 12% 14% 11%Hardware and garden 7% 7% 12% 8% 6% 9% 8% 11%Clothing 11% 12% 10% 16% 1% 0% -2% 3%Footwear and accessories -3% -3% -3% 1% 13% 14% 12% 12%Department stores -1% 4% -4% -7% 1% 1% -1% 6%News and books -9% -7% -10% -4% -6% -13% -10% -8%Recreational goods 15% 21% 13% 11% 1% -3% -4% -5%Pharmaceuticals, health and beauty 3% 4% 4% 2% -1% 1% 1% 2%

All retail 5% 7% 5% 4% 4% 4% 4% 5%

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

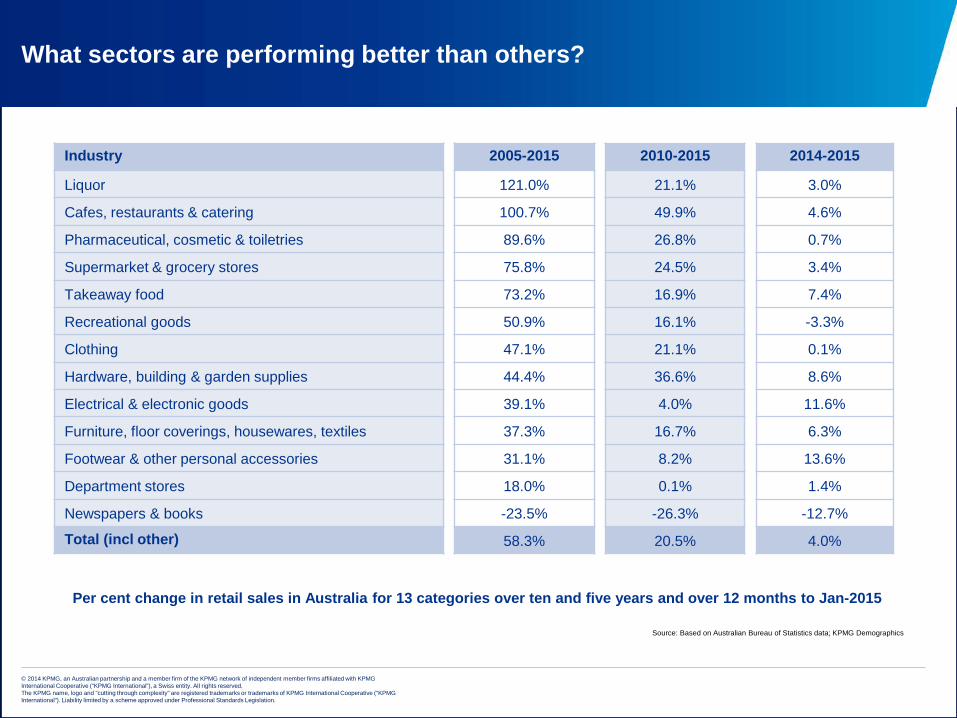

2014-2015

3.0%

4.6%

0.7%

3.4%

7.4%

-3.3%

0.1%

8.6%

11.6%

6.3%

13.6%

1.4%

-12.7%

4.0%

What sectors are performing better than others?

Per cent change in retail sales in Australia for 13 categories over ten and five years and over 12 months to Jan-2015

Source: Based on Australian Bureau of Statistics data; KPMG Demographics

2010-2015

21.1%

49.9%

26.8%

24.5%

16.9%

16.1%

21.1%

36.6%

4.0%

16.7%

8.2%

0.1%

-26.3%

20.5%

2005-2015

121.0%

100.7%

89.6%

75.8%

73.2%

50.9%

47.1%

44.4%

39.1%

37.3%

31.1%

18.0%

-23.5%

58.3%

Industry

Liquor

Cafes, restaurants & catering

Pharmaceutical, cosmetic & toiletries

Supermarket & grocery stores

Takeaway food

Recreational goods

Clothing

Hardware, building & garden supplies

Electrical & electronic goods

Furniture, floor coverings, housewares, textiles

Footwear & other personal accessories

Department stores

Newspapers & books

Total (incl other)

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

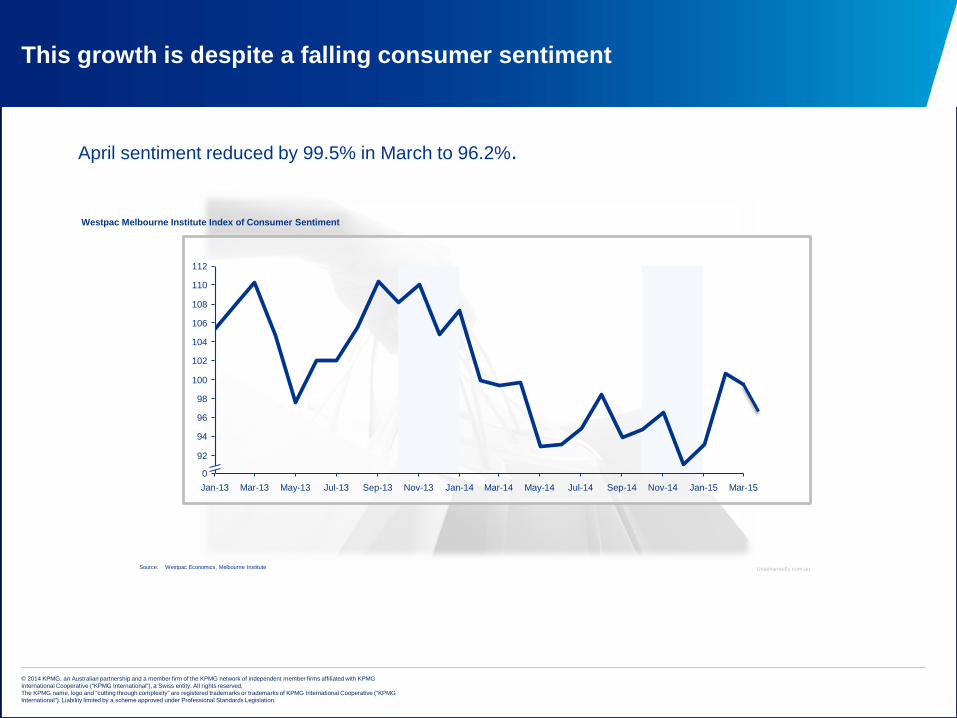

This growth is despite a falling consumer sentiment

Westpac Melbourne Institute Index of Consumer Sentiment

Source: Westpac Economics, Melbourne Institute

98

104

108

100

110

112

94

92

102

106

96

Jan-15Sep-13 Mar-14 May-14 Sep-14Mar-13 Nov-14Jan-13 Jul-13 Jul-14May-13 Jan-14Nov-13 Mar-150

Unashamedly.com.au

April sentiment reduced by 99.5% in March to 96.2%.

Why is the Australian market faring relatively well through these tough economic times?

Growth in the number of high income earners

Increased life expectancy

translating to a growing “lifestyle”

and an older, wealthier customer

segment

Growing levels of wealth and strong

GDP growth

Strong population growth has supported

increased demand for goods and

services

Growing professional

workforce and continued job

growth

Increased participation in the

workforce by women

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Australia is a good place to do business …

BIGGEST1. United States 17.419

2. China 10.380

3. Japan 4.616 4. Germany 3.860 5. United Kingdom 2.945

6. France 2.847

7. Brazil 2.353

8. Italy 2.148

9. ...

12. Australia 1.444

RICHEST1. Norway 97,000

2. Switzerland 87,000

3. Australia 61,000

4. Sweden 58,000

5. United States 55,000

6. Netherlands 51,000

7. Canada 50,000

8. Belgium 48,000

9. Germany 48,000

10. United Kingdom 46,000

FASTEST-RISING1. China 98%2. Nigeria 85%3. Korea 53%4. Saudi Arabia 52%5. Russia 51%6. Indonesia 43%7. India 40%8. Argentina 36%9. Mexico 35%10. …11. Australia 34%

GDP > $US500bn$US GDP pc 2014$UStn GDP 2014 GDP > $US500bn

2009 - 2014Source: Based on International Monetary Fund, World Economic Outlook Database, April 2015; KPMG Demographics

…I expect continuation of the growing number of new foreign businesses starting operations in Australia…specialty fashion, health and beauty, discount grocery

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

23 years of continuous economic prosperity shapes a nation and its people … creates a culture of “consumerism”

Source: ABS Catalogue 5206.0 Australian National Accounts: National Income, Expenditure and Product; KPMG Demographics

Per cent change in Australian GDP by quarter from September 1959

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3

Sep-

1959

Mar

-196

0Se

p-19

60M

ar-1

961

Sep-

1961

Mar

-196

2Se

p-19

62M

ar-1

963

Sep-

1963

Mar

-196

4Se

p-19

64M

ar-1

965

Sep-

1965

Mar

-196

6Se

p-19

66M

ar-1

967

Sep-

1967

Mar

-196

8Se

p-19

68M

ar-1

969

Sep-

1969

Mar

-197

0Se

p-19

70M

ar-1

971

Sep-

1971

Mar

-197

2Se

p-19

72M

ar-1

973

Sep-

1973

Mar

-197

4Se

p-19

74M

ar-1

975

Sep-

1975

Mar

-197

6Se

p-19

76M

ar-1

977

Sep-

1977

Mar

-197

8Se

p-19

78M

ar-1

979

Sep-

1979

Mar

-198

0Se

p-19

80M

ar-1

981

Sep-

1981

Mar

-198

2Se

p-19

82M

ar-1

983

Sep-

1983

Mar

-198

4Se

p-19

84M

ar-1

985

Sep-

1985

Mar

-198

6Se

p-19

86M

ar-1

987

Sep-

1987

Mar

-198

8Se

p-19

88M

ar-1

989

Sep-

1989

Mar

-199

0Se

p-19

90M

ar-1

991

Sep-

1991

Mar

-199

2Se

p-19

92M

ar-1

993

Sep-

1993

Mar

-199

4Se

p-19

94M

ar-1

995

Sep-

1995

Mar

-199

6Se

p-19

96M

ar-1

997

Sep-

1997

Mar

-199

8Se

p-19

98M

ar-1

999

Sep-

1999

Mar

-200

0Se

p-20

00M

ar-2

001

Sep-

2001

Mar

-200

2Se

p-20

02M

ar-2

003

Sep-

2003

Mar

-200

4Se

p-20

04M

ar-2

005

Sep-

2005

Mar

-200

6Se

p-20

06M

ar-2

007

Sep-

2007

Mar

-200

8Se

p-20

08M

ar-2

009

Sep-

2009

Mar

-201

0Se

p-20

10M

ar-2

011

Sep-

2011

Mar

-201

2Se

p-20

12M

ar-2

013

Sep-

2013

Mar

-201

4Se

p-20

14

1960s 1970s 1980s 1990s 2000s 2010s

MenziesWhitlam

Fraser

Hawke

GST GFC

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

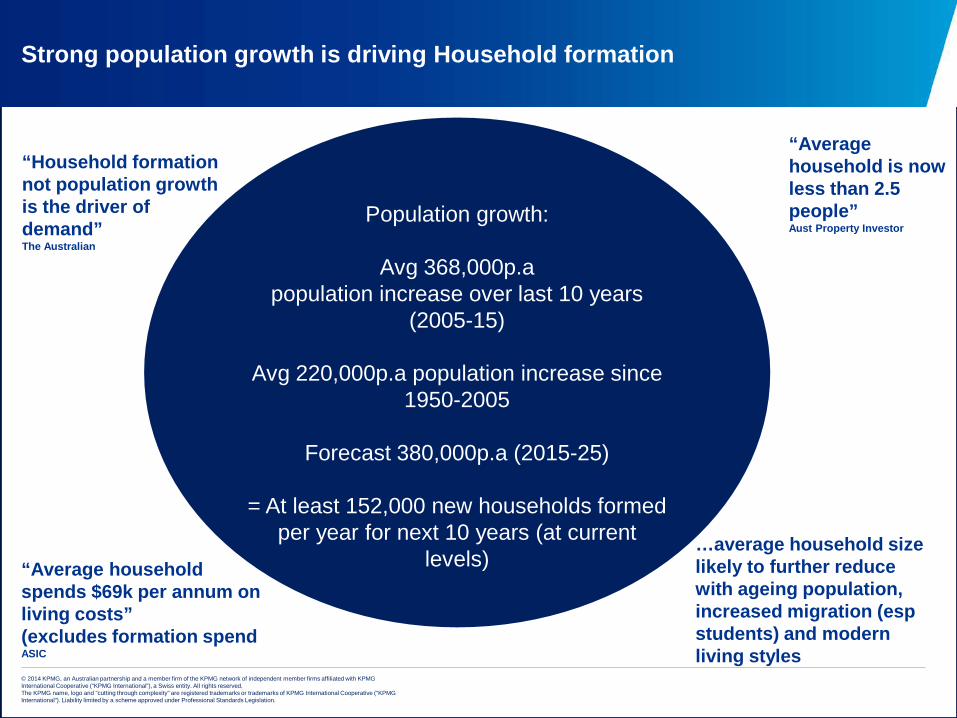

Strong population growth is driving Household formation

“Household formation not population growth is the driver of demand” The Australian

Population growth:

Avg 368,000p.a population increase over last 10 years

(2005-15)

Avg 220,000p.a population increase since 1950-2005

Forecast 380,000p.a (2015-25)

= At least 152,000 new households formed per year for next 10 years (at current

levels)

“Average household is now less than 2.5 people” Aust Property Investor

“Average household spends $69k per annum on living costs” (excludes formation spendASIC

…average household size likely to further reduce with ageing population, increased migration (espstudents) and modern living styles

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Source: Based on Australian Bureau of Statistics data; KPMG Demographics

Consumer demand is shaped by changes in the demographic profile

2003-2013: 3.4 million (19.7m to 23.1m)

Net change in Australian population by 5-year age group over 10 years to 2013 and 10 years to 2023

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

0-4 5-9 10-14 15-19 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+

2013-2023: 4.2 million (23.1m to 27.3m)

Mature adults

Premium products

Young adults

Household formation

Kids & teenagers

Social & leisure

Active retirees

+Convenience & value

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

What will be the effect of the Federal Government budget…

12

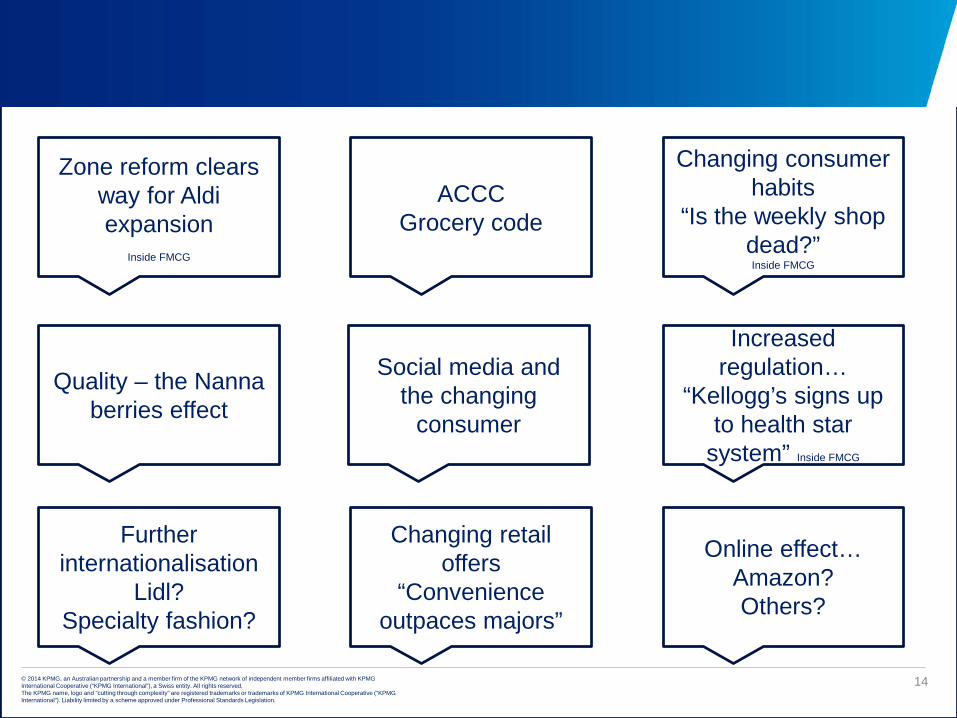

What disruptors are impacting the retail market

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Zone reform clears way for Aldi expansion

Inside FMCG

Quality – the Nanna berries effect

Online effect…Amazon?Others?

Changing retail offers

“Convenience outpaces majors”

Increased regulation…

“Kellogg’s signs up to health star

system” Inside FMCG

Changing consumer habits

“Is the weekly shop dead?”Inside FMCG

ACCCGrocery code

Further internationalisation

Lidl? Specialty fashion?

Social media and the changing

consumer

14

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Defining the new consumer

Consumers are… Which means they… So companies must…

Connected Can shop anytime and anywhereGet products to consumers when and where they want them

InformedHave unlimited information at their fingertips and are constantly looking for more

Embrace the shift in buying behavior andhelp them learn more (don’t always go for the conversion)

Conscious Are socially, ethically and environmentally aware

Meet the demand for transparency

Empowered Have many outlets to express their opinion

Use consumer generated content to innovate and improve

Individual Expect a personalized experienceAnalyze consumer data to provide a targeted and meaningful journey

Vulnerable Are more exposed to riskPut measures in place to protect theconsumer

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

The consumer has fundamentally changed through technology

TODAY ... A “CONNECTED” CONSUMER IS ...

A Consumer A Creator A Critic A Producer A Spectator A Community Manager A Collaborator

L I K E

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

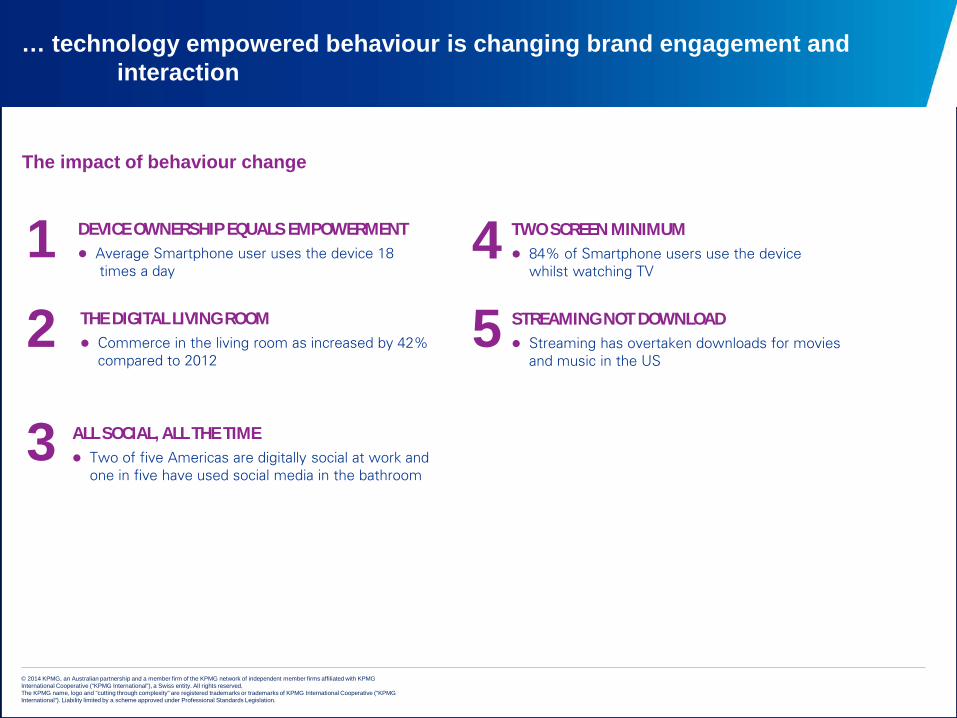

… technology empowered behaviour is changing brand engagement and interaction

The impact of behaviour change

1 DEVICE OWNERSHIP EQUALS EMPOWERMENT Average Smartphone user uses the device 18

times a day

2 THE DIGITAL LIVING ROOM Commerce in the living room as increased by 42%

compared to 2012

3 ALL SOCIAL, ALL THE TIME Two of five Americas are digitally social at work and

one in five have used social media in the bathroom

4 TWO SCREEN MINIMUM 84% of Smartphone users use the device

whilst watching TV

5 STREAMING NOT DOWNLOAD Streaming has overtaken downloads for movies

and music in the US

© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority toobligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

What can we learn from these trends and how can we respond?

18© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority toobligate or bind KPMG International or any other member firm third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

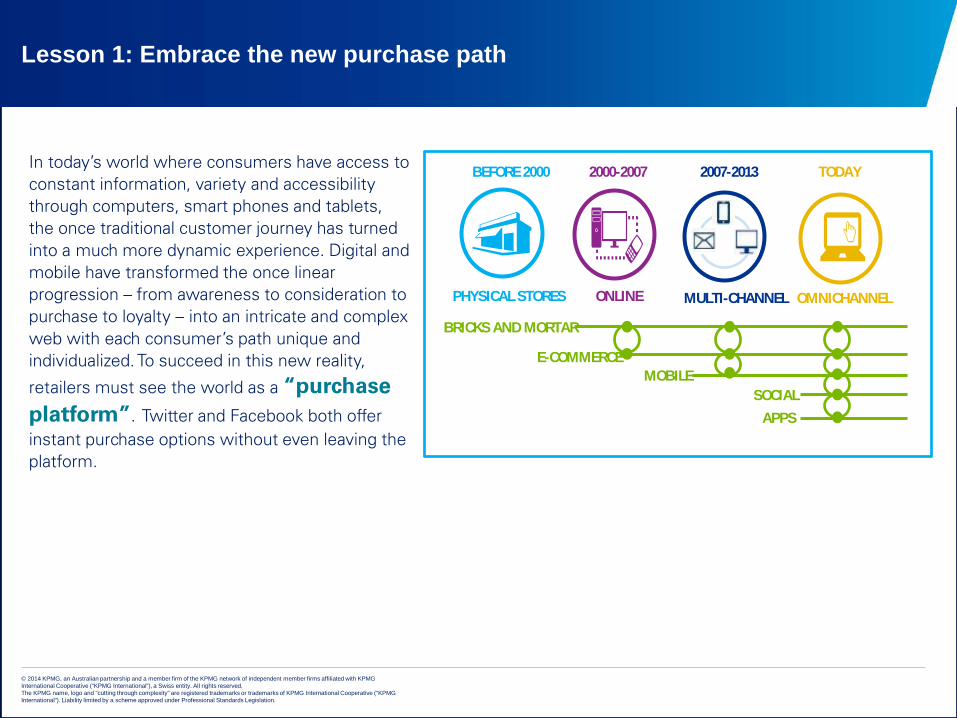

Lesson 1: Embrace the new purchase path

In today’s world where consumers have access to constant information, variety and accessibility through computers, smart phones and tablets, the once traditional customer journey has turned into a much more dynamic experience. Digital and mobile have transformed the once linear progression – from awareness to consideration to purchase to loyalty – into an intricate and complex web with each consumer’s path unique and individualized. To succeed in this new reality,

retailers must see the world as a “purchase platform”. Twitter and Facebook both offer instant purchase options without even leaving the platform.

BEFORE 2000 2000-2007 2007-2013 TODAY

PHYSICAL STORES ONLINE MULTI-CHANNEL OMNICHANNEL

BRICKS AND MORTAR

E-COMMERCEMOBILE

SOCIAL

APPS

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Lesson 2: Merge online/offline to create a “frictionless” experience

Consumers are looking for a frictionless shopping experience across channels and for retailers to be successful we recommend they remain focused on removing friction from every point in the purchasing journey. Mobile and social platforms should be embraced and leveraged to close the gap between product discovery and purchase. Retailers should be present and accessible on a wider variety of channels in a consistent way that allows for customers to make purchases instantly and seamlessly.

An opportunity: consumer engagement across platforms

Retailers can increase the information provided to consumers with variety in media – such as using videos and increasing social engagement with product reviews.

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Lesson 3: Empower consumers to own their shopping experience

Consumers want to own their shopping experience. They want the relevant information to be readily available whenever they need it. We recommend retailers don’t always look for the conversion – if their consumers are looking for more product information, help them with that. Providing customers with a near real-time view of what’s in stock in every store or available for delivery helps them feel informed and empowered to make choices. In exchange, consumers are more willing to share their data with retailers.

Mike Rogers, Vice President of eCommerce & Digital Operations at JCPenney on Customer Experience

Help me find it, Help me get it, Make it worth it. Customers know more than they used to, have access to more data than they used to and have come to expect more than they used to.

An opportunity: Cloud in the supply chainCloud based software can increase the speed of data transfer across the supply chain. These solutions have allowed retailers to link POS transactions to inventory reports, updating the systems in minutes.

The implementation process may include the preparation of internal processes, organizational re-structuring (as required) and education on how to get the most out of this new level of information sharing.

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Lesson 4: Offer on-demand delivery options

Click & Collect (also known as ‘Buy online and pick-up in store’) is quickly becoming one of the most desired delivery options. A 2014 survey of 1,992 US consumers showed in 2013, 4 percent of customers had ordered online and picked up in store and in 2014, 64 percent of consumers had ordered online and picked up in store*. Retailers are finding that if they do offer click & collect many customers don’t even want to come into the store – or even get out of their car. This has led to pick-up desks at the front of stores, or drive-up kiosks in the parking lot. In cities, we will see a rise in collection locations at major commuter hubs.

UK retailer John Lewis, for example, recently opened a 'click and commute' store in a major London train station. Retailers offering delivery services are also under pressure to deliver products increasingly faster. Amazon’s next day delivery service is becoming insufficient for many of its customers looking for immediate satisfaction. Cole Haan in the US is now working with NYC courier UberRush to provide their online shoppers the option of ”rush 2-hour delivery” for an additional US$10.

*Report source: BOPIS & BISBO will propel retail into orbit by Blackhawk Engagement Solutions

No Inventory Model: Drop ShippingDrop shipping enables retailers to forward orders to a third party which holds their stock and fulfills orders on their behalf. This services allows retailers to offer a wider range of products without the cost associated to storing inventory.

John Lewis has adopted a hybrid fulfillment strategy – storing most of their products in warehouses and then delivering them via their own fleet of vans. However, for slower moving items, it’s not always practical to keep high stock levels so in those cases they use drop shippers.

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Lesson 5: Fulfill each order profitably

With the increasing complexity of converged channels, retailers are focusing heavily on inventory and fulfillment management. Retailers may know that the cost of fulfillment is high but do they…

- Know how to make the most profitable decision for each order?

- Fulfill from their stores and leave their shelves short of product?

- Fulfill from their own distribution centers and interrupt a third party logistics provider?

- Fulfill orders directly from suppliers via drop ship?

To enable smarter decision making, retailers need to dynamically connect their warehouse, distribution system and their stores. They need a clear fulfillment strategy that makes use of predictive analytics to enable better demand planning. Smarter stores have better inventory visibility, better fulfillment and efficient labor productivity.

To succeed in omnichannel you must have a really good front end, but unless you have re-engineered the back-end and are ready to cope with peaks in traffic you’ll have real issues. There’s no point doing one without the other.

An opportunity: Cost-to-serve and supply chain analyticsRetailers can determine the product and channel cost-to-serve –analyzing operational and financial data to provide insights into the true cost of fulfillment. This cost and performance data can be used to recommend fulfillment process improvements, for example adjusting the pricing processes at distribution centers such as packing and scanning.

Mike Rogers, Vice President of eCommerce & Digital Operations at JCPenney on Customer Experience

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Lesson 6: Create an unforgettable experience

The physical store still remains a critical part of the shopping journey. Consumers crave social interaction and they want to experience the brand and have an emotional connection. They also want instant gratification —to be able to find what they need and leave the store with bag-in-hand. Experiences help to forge meaningful connections and relationships with retailers that transcend the transaction.

This is the Achilles' heel for pure-play e-commerce as consumers may obtain the product but there is no sensory element, no immediacy and no social interaction. Pure play e-tailers are recognizing the power of a physical consumer-facing presence with Amazon, Birchbox and Rent the Runway all moving into bricks.

Focus on experiences not products

Stores need to be both fulfillment centers and social playgrounds, allowing consumers to interact with products, sales associates and the brand. The degree of which is dependent on the type of retailer. Creating aspirational settings presents customers with novel ways to use products and helps upsell a total ”look” or lifestyle.

Cultivate a community

Retailers need to offer customers reasons to visit their store beyond the product. By bringing like-minded individuals together, involving them in product decisions and offering complementary services, retailers can build on emotional touch points and create relationships that go beyond the transaction.

Future of Retail 2015, PSFK Labs

Offer complementary services and experiences that go well beyond products, reimagining stores are market places for relationships.

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Lesson 7: Make it personal

A core part of making an experience unforgettable is about meeting the needs of the modern consumer and making it relevant for each individual.

Retailers are increasingly offering consumers the opportunity to customize or personalize their products. Micro-manufacturing, segmenting to deliver-to-scale and 3-D printing provide profitable ways to make customers feel like products were made just for them. Selfridges’ in-store ”Lab” offers assessment-based fragrance recommendations or the option to create a custom scent. Levis Lot 1 is a premium service offering made-to-order bespoke jeans.

In an effort to offer increased personalization, retailers are focusing on the collection of customer data. To accomplish this they are building sophisticated analytics into their back-end strategies to ensure the most seamless, simplistic, customized experience for their customers on the front-end. The amount of personal information that customers are willing to share is directly correlated to the value of what they receive in return.

Personalize the experience Customize products

IBM Insights on Business: The Power of Insight: Delivering on Brand Promise, 2014

In the online world, consumer experience is as important as product and price. A recent IBM Institute for Business Value study shows 81 percent of consumers expect the same brand experience across channels and 54 percent of consumers would end their relationship with a retailer if not given personalized content.

Retail trends

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Retail trends

1. OMNI channel will be the norm

27

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Retail trends

1. OMNI channel will be the norm

2. Increasing use of in-store experience

28

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Retail trends

1. OMNI channel will be the norm

2. Increasing use of in-store experience

3. Technology integrated into bricks and mortar stores

29

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Retail trends

1. OMNI channel will be the norm

2. Increasing use of in-store experience

3. Technology integrated into bricks and mortar stores

4. Re-invention of loyalty programs

30

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Retail trends

1. OMNI channel will be the norm

2. Increasing use of in-store experience

3. Technology integrated into bricks and mortar stores

4. Re-invention of loyalty programs

5. Social media influence on purchasing decisions

31

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Retail trends

1. OMNI channel will be the norm

2. Increasing use of in-store experience

3. Technology integrated into bricks and mortar stores

4. Re-invention of loyalty programs

5. Social media influence on purchasing decisions

6. Investment in Big data by retailers – improved personalised offers

32

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Retail trends

1. OMNI channel will be the norm

2. Increasing use of in-store experience

3. Technology integrated into bricks and mortar stores

4. Re-invention of loyalty programs

5. Social media influence on purchasing decisions

6. Investment in Big data by retailers – improved personalised offers

7. Likeable “experts” in store and “online”

33

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Retail trends

1. OMNI channel will be the norm

2. Increasing use of in-store experience

3. Technology integrated into bricks and mortar stores

4. Re-invention of loyalty programs

5. Social media influence on purchasing decisions

6. Investment in Big data by retailers – improved personalised offers

7. Likeable “experts” in store and “online”

8. Mobile wallet

34

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Retail trends

1. OMNI channel will be the norm

2. Increasing use of in-store experience

3. Technology integrated into bricks and mortar stores

4. Re-invention of loyalty programs

5. Social media influence on purchasing decisions

6. Investment in Big data by retailers – improved personalised offers

7. Likeable “experts” in store and “online”

8. Mobile wallet

9. Ongoing internationalisation of Australian retail landscape

35

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Retail trends

1. OMNI channel will be the norm

2. Increasing use of in-store experience

3. Technology integrated into bricks and mortar stores

4. Re-invention of loyalty programs

5. Social media influence on purchasing decisions

6. Investment in Big data by retailers – improved personalised offers

7. Likeable “experts” in store and “online”

8. Mobile wallet

9. Ongoing internationalisation of Australian retail landscape

10. Consumer demanding increased speed – service, offer and delivery flexibility

36

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Retail execution with the consumer...the past...

37

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

38

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

The present...

39

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Coming to Australia?....

40

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Back to the future...

41

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Emergence of in-home enablers...Amazon Dash

42

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Online delivery wars…

eBay’s CEO dismisses drone concept as “fantasy”

eBay Now - $5 for local delivery within an hour in participating cities including San Francisco, Chicago, Dallas and New York

Likely launch of Amazon PrimeAir delivery drone in 2015/6

Regulatory and technological hurdles still to be overcome

Opportunity to provide 30 minute delivery option for small items

Competitor response:

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Retail trends

1. OMNI channel will be the norm

2. Increasing use of in-store experience

3. Technology integrated into bricks and mortar stores

4. Re-invention of loyalty programs

5. Social media influence on purchasing decisions

6. Investment in Big data by retailers – improved personalised offers

7. Likeable “experts” in store and “online”

8. Mobile wallet

9. Ongoing internationalisation of Australian retail landscape

10. Consumer demand increased speed – service, offer and delivery flexibility

Bricks and mortar wont

die!…but it will

evolve

44

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

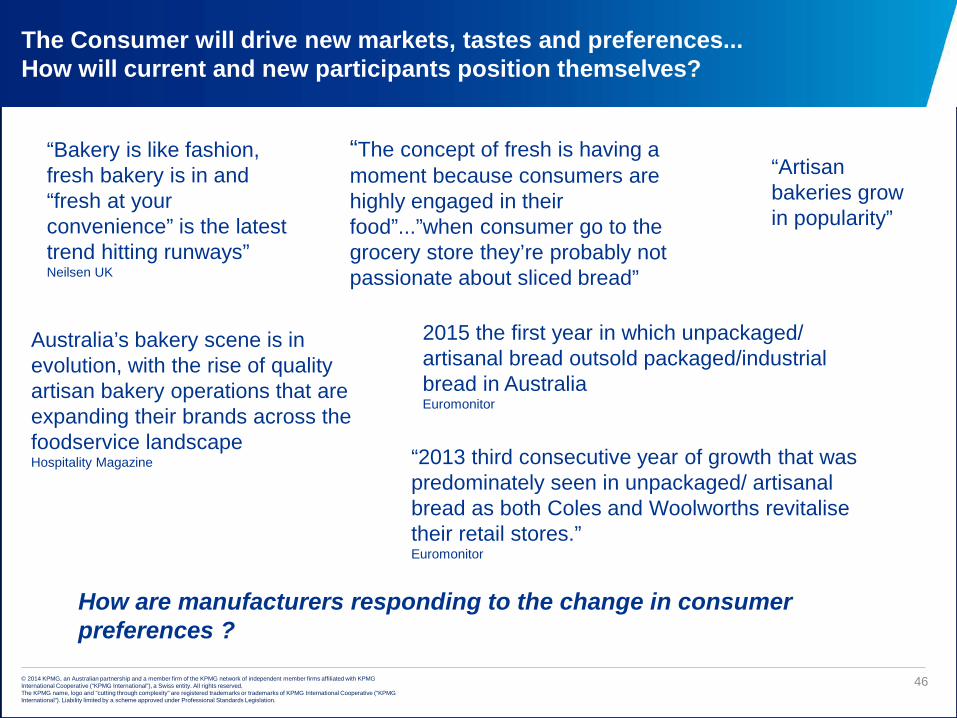

The Consumer will drive new markets, tastes and preferences...How will current and new participants position themselves?

The Bakery example:

Bakery industry going through major period of change

Per capita consumption of bread is fallingBUTAustralians are spending more on higher quality, fresher breads and baked goods.

Typical family used to purchase a few loaves of factory-produced white bread once a week

Consumers are now more likely to buy a much wider range of freshly baked bread daily, including sourdough, ciabatta, brioche and baguettes.

Rising health awareness has caused demand for new products (eg wholemeal, seeded, gluten-free and other health breads) to soar.

Introduction of functional breads that have been fortified or enriched with nutrients has also contributed to the growing demand for premium breads and bakery products

Source IBIS

45

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

The Consumer will drive new markets, tastes and preferences...How will current and new participants position themselves?

“Bakery is like fashion, fresh bakery is in and “fresh at your convenience” is the latest trend hitting runways”Neilsen UK

“The concept of fresh is having a moment because consumers are highly engaged in their food”...”when consumer go to the grocery store they’re probably not passionate about sliced bread”

How are manufacturers responding to the change in consumer preferences ?

“Artisan bakeries grow in popularity”

Australia’s bakery scene is in evolution, with the rise of quality artisan bakery operations that are expanding their brands across the foodservice landscapeHospitality Magazine “2013 third consecutive year of growth that was

predominately seen in unpackaged/ artisanal bread as both Coles and Woolworths revitalise their retail stores.”Euromonitor

2015 the first year in which unpackaged/ artisanal bread outsold packaged/industrial bread in AustraliaEuromonitor

46

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

Packaged lunch offers...

47

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

...to present

48

© 2010 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International"). Liability limited by a scheme approved under Professional Standards Legislation.

49

Data…the next frontier

Digital engagement

rank digital as very important

54%say digital is critical

29%

61%rank digital as a

top concern

today’s consumers are online, all the time

digital strategy

© 2014 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

56%rank digital as a

top concern

© 2014 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

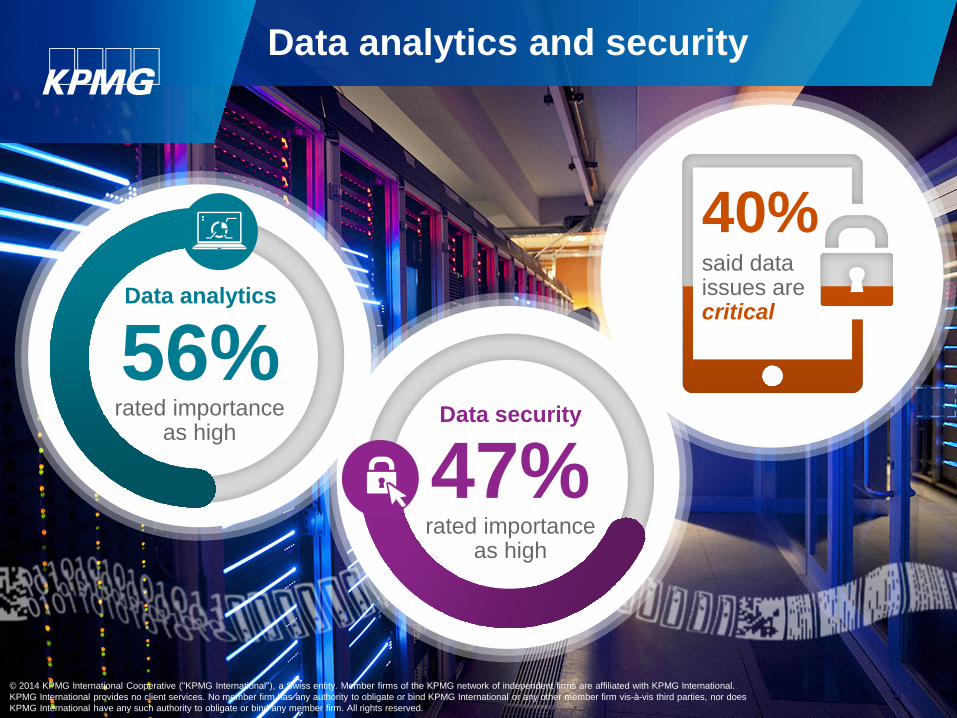

56%Data analytics

rated importance as high

47%Data security

rated importance as high

40%said data issues are critical

Data analytics and security

© 2014 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

think companies collect too much

customer info

82%

(Adobe, June 2013)

have tried to remove or mask

online activity

86%(Pew Research Center,

September 2013)

Source: http://mashable.com/2014/04/15/data-breach-infographic/

78%Of companies have had at least 1 data

breach in last 2 years

60%of small to medium businesses have

no routine backup

36%of data lost is

customer and financial info

72%of businesses

with a major data loss shut down within 2 years

© 2014 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

© 2014 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (KPMG International), a Swiss entity. All rights reserved.

The KPMG name, logo and ‘cutting through complexity’ are registered trademarks or trademarks of KPMG International Cooperative (KPMG International).