audit planning need an effective and efficient audit planneed an effective and efficient audit plan...

TRANSCRIPT

Audit PlanningAudit Planning

• Need an Need an effectiveeffective and and efficientefficient audit plan audit plan

• UnderauditUnderaudit - see you in court - see you in court

• OverauditOveraudit - lose - lose clients to competitorsclients to competitors

PlanningPlanning

1.1. Accept client and perform initial Accept client and perform initial planningplanning

2.2. Understand client’s business and Understand client’s business and industryindustry

3.3. Assess client business risk Assess client business risk

4.4. Perform preliminary analytical Perform preliminary analytical proceduresprocedures

Note:Note: Planning also includes fraud risk Planning also includes fraud risk brainstorming required by SAS #99brainstorming required by SAS #99

Client AcceptanceClient Acceptance

• Do we want this client?Do we want this client?

-- Are we independent?Are we independent?

- Are we technically competent?- Are we technically competent?

- Is client reputable?- Is client reputable?

• Who will use financial statements?Who will use financial statements?

(Key part of acceptable audit risk - (Key part of acceptable audit risk - discussed in Ch. 9)discussed in Ch. 9)

Communication With PredecessorCommunication With Predecessor

• Required by SAS #84Required by SAS #84• Purpose is to assess whether to accept Purpose is to assess whether to accept

clientclient

• Successor initiatesSuccessor initiates- - predecessor needs client predecessor needs client

permission to release informationpermission to release information

Successor - Predecessor Successor - Predecessor CommunicationCommunication

• Usually review prior auditor Usually review prior auditor workpapers workpapers

– Determine whether problems exist Determine whether problems exist that impact client acceptancethat impact client acceptance

– Support beginning asset balances Support beginning asset balances (why?)(why?)

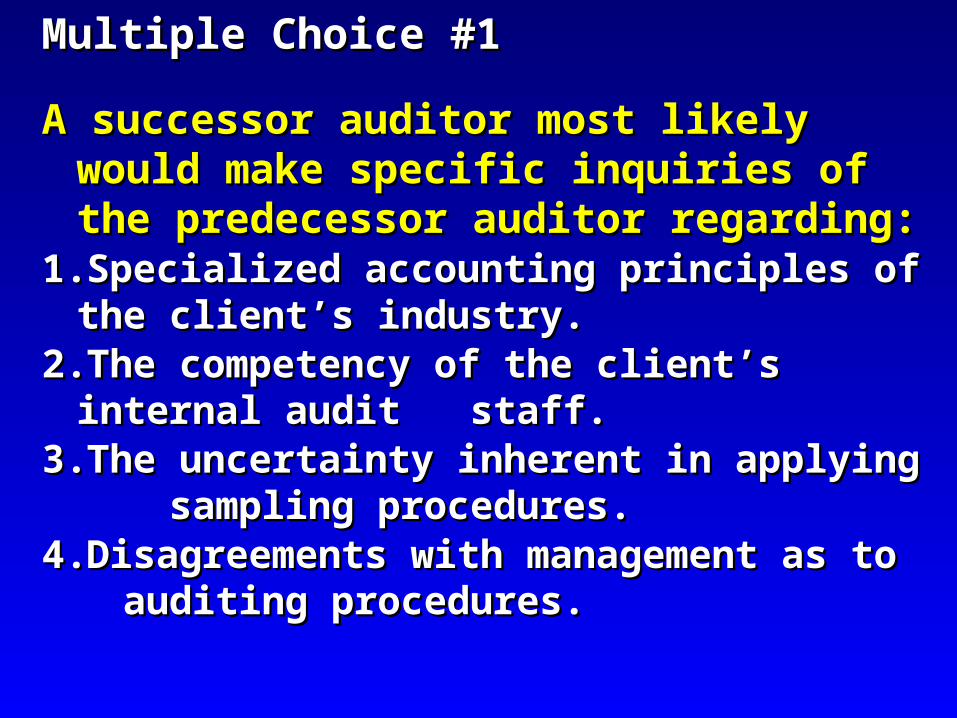

Multiple Choice #1Multiple Choice #1

A successor auditor most likely would make A successor auditor most likely would make specific inquiries of the predecessor auditor specific inquiries of the predecessor auditor regarding:regarding:

1.1. Specialized accounting principles of the client’s Specialized accounting principles of the client’s industry.industry.

2.2. The competency of the client’s internal audit The competency of the client’s internal audit staff.staff.

3.3. The uncertainty inherent in applying sampling The uncertainty inherent in applying sampling procedures.procedures.

4.4. Disagreements with management as to auditing Disagreements with management as to auditing procedures.procedures.

Understanding with ClientUnderstanding with Client• Must obtain and document Must obtain and document

understanding (SAS #108)understanding (SAS #108)

• Written engagement letter Written engagement letter now requirednow required

-- Engagement objectivesEngagement objectives

- Management responsibilities- Management responsibilities- Responsibilities of auditor- Responsibilities of auditor- Limits of engagement- Limits of engagement

SpecialistsSpecialists

• Used to address complex issues where Used to address complex issues where auditor is not qualifiedauditor is not qualified

• May be hired by May be hired by client client or or auditorauditor• Auditor should evaluate qualifications, and Auditor should evaluate qualifications, and

relationship with clientrelationship with client• May refer to specialist in audit report only May refer to specialist in audit report only

when opinion is when opinion is qualifiedqualified or or explanatory explanatory paragraphparagraph added based on specialist’s report added based on specialist’s report

MC #2 MC #2

An auditor may refer to the specialist in the An auditor may refer to the specialist in the auditor’s report if the:auditor’s report if the:

1. Specialist’s findings provide the auditor 1. Specialist’s findings provide the auditor greater assurance of reliability about greater assurance of reliability about management's representations.management's representations.2. The auditor qualifies the opinion as a 2. The auditor qualifies the opinion as a result of the specialist’s findings.result of the specialist’s findings.3. Auditor’s use of the specialist’s findings is 3. Auditor’s use of the specialist’s findings is different from that of prior years.different from that of prior years.4. Specialist is a related party whose findings4. Specialist is a related party whose findings fully corroborate management’s financial fully corroborate management’s financial statement assertions.statement assertions.

Understanding of the Client’s Understanding of the Client’s Business and IndustryBusiness and Industry

Understand Client’s Business and Industry

Industry and External Environment

Business Operations and Processes

Management and Governance

Objectives and Strategies

Measurement and Performance

Related PartiesRelated Parties

• Concern is that they are Concern is that they are adequately disclosedadequately disclosed

• By nature, are By nature, are not arm’s not arm’s lengthlength

MC #3MC #3

When auditing related party transactions, When auditing related party transactions, an auditor places primary emphasis on:an auditor places primary emphasis on:

1. Confirming the existence of the related 1. Confirming the existence of the related parties.parties.

2. Verifying the valuation of the related2. Verifying the valuation of the related parties.parties.

3. Evaluating the disclosure of the related3. Evaluating the disclosure of the related party transactions.party transactions.

4. Ascertaining the rights and obligations of 4. Ascertaining the rights and obligations of the related parties.the related parties.

MC #3MC #3

When auditing related party transactions, When auditing related party transactions, an auditor places primary emphasis on:an auditor places primary emphasis on:

1. Confirming the existence of the related 1. Confirming the existence of the related parties.parties.

2. Verifying the valuation of the related2. Verifying the valuation of the related parties.parties.

3. Evaluating the disclosure of the related3. Evaluating the disclosure of the related party transactions.party transactions.4. Ascertaining the rights and obligations of 4. Ascertaining the rights and obligations of the related parties.the related parties.

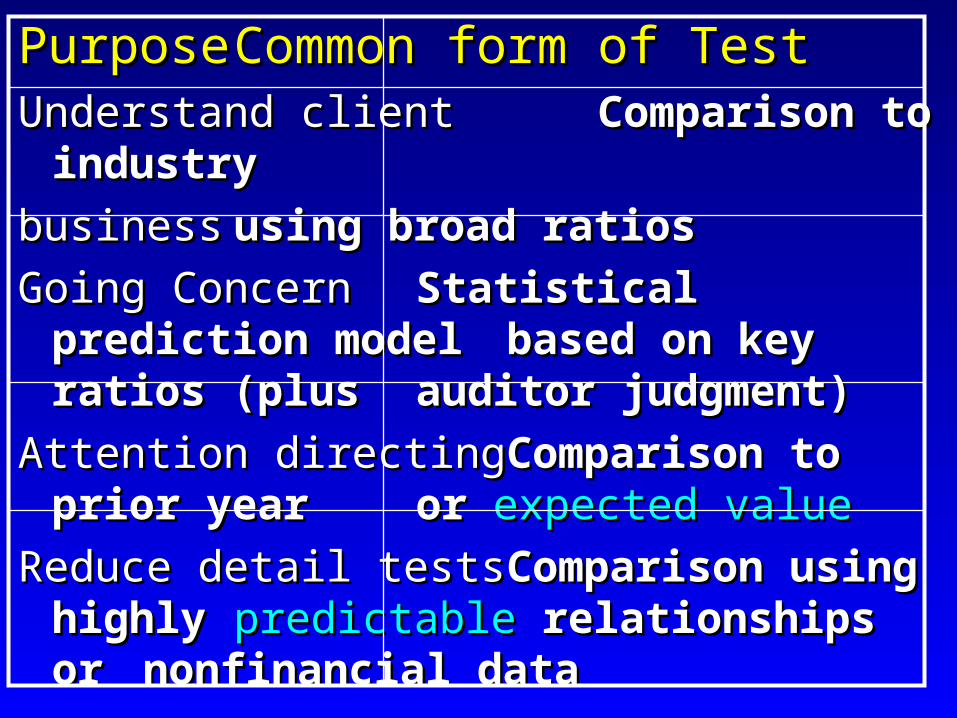

PurposePurpose Common form of TestCommon form of TestUnderstand clientUnderstand client Comparison to industry Comparison to industry

businessbusiness using broad ratiosusing broad ratios

Going ConcernGoing Concern Statistical prediction Statistical prediction model model based on key ratios based on key ratios (plus (plus auditor judgment)auditor judgment)

Attention directingAttention directing Comparison to prior year Comparison to prior year or or expected valueexpected value

Reduce detail testsReduce detail tests Comparison using highly Comparison using highly predictablepredictable relationships relationships

or or nonfinancial datanonfinancial data

Auditors try to identify predictable Auditors try to identify predictable relationships when using analytical relationships when using analytical procedures. Relationships involving procedures. Relationships involving transactions from which of the transactions from which of the following accounts most likely would following accounts most likely would yield the highest level of evidence?yield the highest level of evidence?

1. Accounts payable1. Accounts payable

2. Advertising expense2. Advertising expense 3. Accounts receivable3. Accounts receivable 4. Interest expense4. Interest expense

8-27(d)8-27(d)

Which of the following situations has the best chance Which of the following situations has the best chance of being detected when a CPA compares 2009 of being detected when a CPA compares 2009 revenues and expenses with the p/y, and revenues and expenses with the p/y, and investigates all changes exceeding a fixed %?investigates all changes exceeding a fixed %?

1. Increase in property tax rates has not 1. Increase in property tax rates has not been recognized in the 2009 accrual.been recognized in the 2009 accrual.

2. Cashier began lapping A/R in 2009.2. Cashier began lapping A/R in 2009.

3. Because economy worsened, 2009 3. Because economy worsened, 2009 provision for bad debts is insufficient.provision for bad debts is insufficient.

4. Company changed capitalization for small 4. Company changed capitalization for small tools in 2009.tools in 2009.

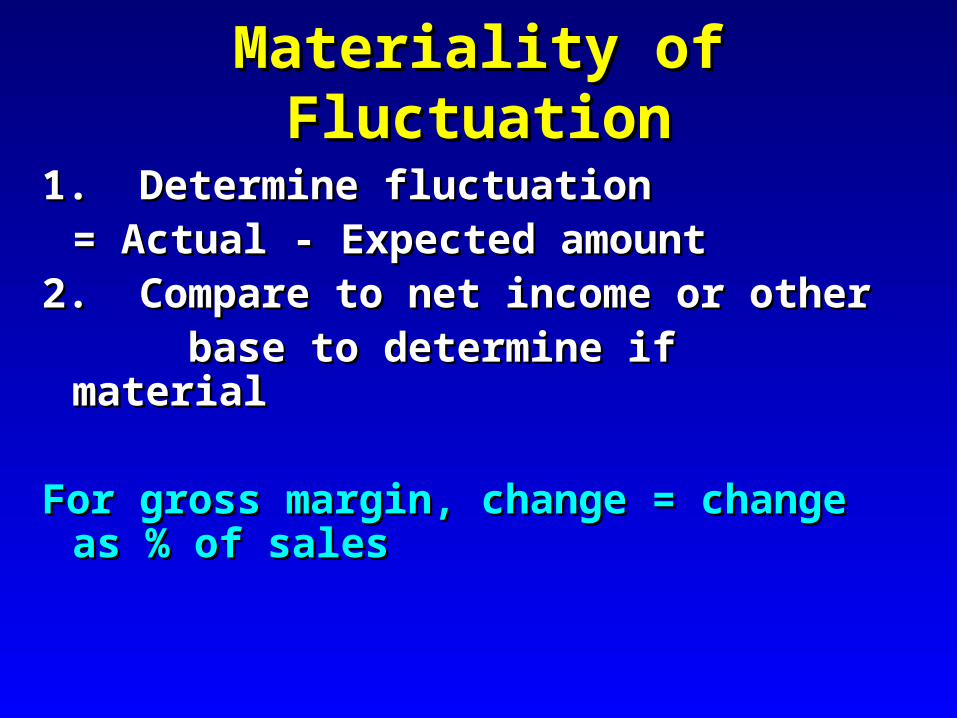

Materiality of FluctuationMateriality of Fluctuation

2009 Gross Margin2009 Gross Margin 42% 42%2008 Gross Margin2008 Gross Margin 40% 40%2009 Sales2009 Sales $20,000,000 $20,000,0002009 Net Income2009 Net Income $ 1,000,000 $ 1,000,000MaterialityMateriality $ 50,000 $ 50,000

Is the change material?Is the change material?

Change in gross marginChange in gross margin(2009=49%, 2005=40%)(2009=49%, 2005=40%) 2% 2%SalesSales $ 20,000,000$ 20,000,000Dollar changeDollar change $ 400,000 $ 400,000

Change is material (> materiality of $50,000)Change is material (> materiality of $50,000)

Materiality of FluctuationMateriality of Fluctuation

1. Determine fluctuation 1. Determine fluctuation = Actual - Expected amount= Actual - Expected amount

2. Compare to net income or other 2. Compare to net income or other base to determine if materialbase to determine if material

For gross margin, change = change as % For gross margin, change = change as % of salesof sales

For balance sheet accounts, need to For balance sheet accounts, need to compute expected amount compute expected amount (alternate (alternate method % method % change in ratiochange in ratio))

Predicted inventory if turnover constant:Predicted inventory if turnover constant:

20092009 20082008Inv. Turn Inv. Turn (Cos/EI)(Cos/EI) 3.25 5.20 3.25 5.20

2009 COS/2008 Turn = 194,371/5.2 = 2009 COS/2008 Turn = 194,371/5.2 =

Predicted inventory = 37,379Predicted inventory = 37,379

Recorded inventory = Recorded inventory = 59,864 59,864

Increase in inventory 22,485Increase in inventory 22,485

Alternate method - % change in ratioAlternate method - % change in ratioFor turnover ratios, can’t subtract ratio since For turnover ratios, can’t subtract ratio since

involves B/S and I/S amountsinvolves B/S and I/S amounts– can computer dollar change as percentage change can computer dollar change as percentage change

in ratioin ratio 20092009 20082008

Inv. Turn Inv. Turn (Cos/EI)(Cos/EI) 3.25 5.20 3.25 5.20

% Change in turn =% Change in turn =

(2008 – 2009) /2008 = (2008 – 2009) /2008 =

5.20 - 3.25 = 1.95/5.20 = 37.5 %5.20 - 3.25 = 1.95/5.20 = 37.5 %

x EI x EI 59,864 59,864

Increase in inventory 22,449Increase in inventory 22,449

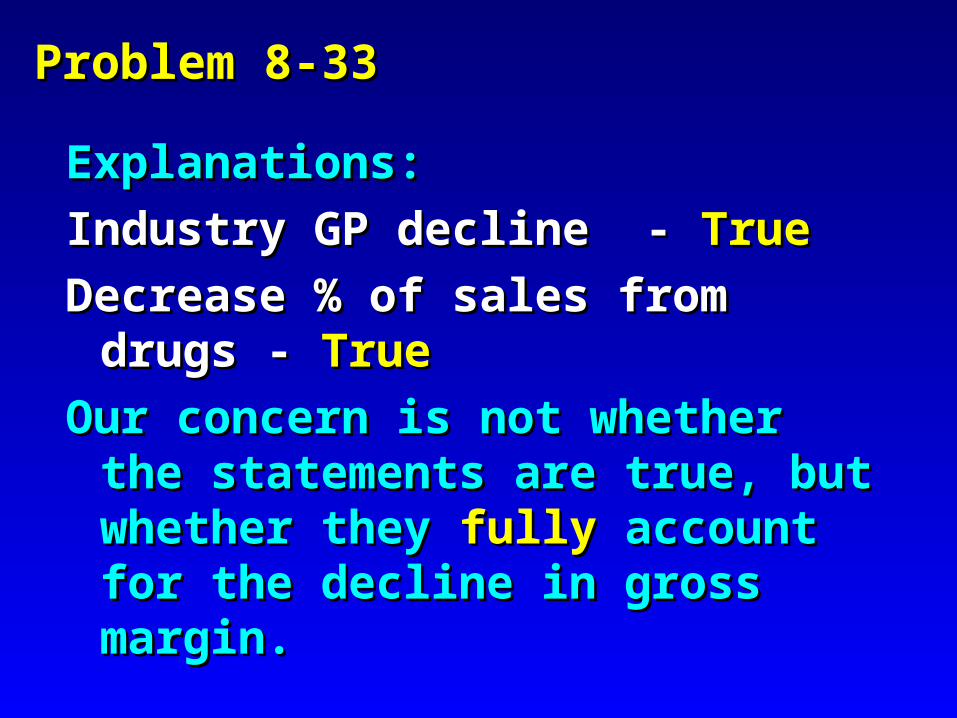

Problem 8-33Problem 8-33

Change in Gross Margin:Change in Gross Margin:

(36.0 - 35.1) x 14,211 = 128 (36.0 - 35.1) x 14,211 = 128

Explanations:Explanations:Industry GP declineIndustry GP decline

Decrease % of sales from drugsDecrease % of sales from drugs

Problem 8-33Problem 8-33

Explanations:Explanations:

Industry GP decline - Industry GP decline - True True

Decrease % of sales from drugs - Decrease % of sales from drugs - TrueTrue

Our concern is not whether the Our concern is not whether the statements are true, but whether they statements are true, but whether they fullyfully account for the decline in gross account for the decline in gross margin.margin.

Total GP declineTotal GP decline 128 128

Industry (.2% x 14,211) (28)Industry (.2% x 14,211) (28)

Change in mix:Change in mix:

09 Drugs = 39% sales09 Drugs = 39% sales

08 Drugs = 36%08 Drugs = 36%

(3% x 14,211) = 426 (3% x 14,211) = 426 (decline in(decline in drug sales)drug sales)

Drug - Nondrug GP =Drug - Nondrug GP =

(40.6 - 32.0) = (40.6 - 32.0) = 8.6 %8.6 % (37)(37)

Unaccounted forUnaccounted for 63 63

Problem 8-33Problem 8-33::

DrugsDrugs NondrugsNondrugs

20092009 40.6%40.6% 32.0% 32.0%

20082008 42.2%42.2% 32.0% 32.0%

20072007 42.1%42.1% 31.9% 31.9%

20062006 42.3%42.3% 31.8% 31.8%

The change in drug gross margin is much larger than The change in drug gross margin is much larger than for the industry, and appears to be material ([42.2 for the industry, and appears to be material ([42.2 - 40.6] x 5,126,000 = $82,000). - 40.6] x 5,126,000 = $82,000). (drug sales)(drug sales)

Assessment of Going ConcernAssessment of Going Concern

Auditor must assess whether client will Auditor must assess whether client will continue in existence for a continue in existence for a reasonable reasonable periodperiod of time. of time.

• RequiredRequired on all audit engagements on all audit engagements

• Reasonable period is usually Reasonable period is usually one yearone year from from f/s datef/s date

• Auditor should consider Auditor should consider management management plansplans affect going concern status affect going concern status