as 23 and 27 consolidation of associates / joint...

TRANSCRIPT

AS 23 and 27 –

Consolidation of Associates

/ Joint Ventures

Presentation by:

CA Geetha Jayakumar

November 15, 2014

2

General Introduction

Companies Act, 2013

Consolidated Financial Statements

Where a company has one or more subsidiaries, it shall, in addition

to standalone financial statements prepare a consolidated financial

statement (CFS) of the company and of all the subsidiaries in the

same form and manner as that of its own which shall also be laid

before the AGM of the company along with the laying of its financial

statement.

Company shall also attach along with its financial statement, a

separate statement containing the salient features of the financial

statement of its subsidiary or subsidiaries in Form AOC I

‘Subsidiary’ includes ‘associate company’ and ‘joint venture’

(Associate means a Company other than a subsidiary company and

joint venture company in which the other Company has a significant

influence)

Consolidated Financial Statements…

Manner of consolidation of accounts.-

The consolidation of financial statements of the company

shall be made in accordance with the provisions of Schedule

III of the Act and the applicable accounting standards.

Provided that in case of a company covered under Sec.

129(3) which is not required to prepare consolidated financial

statements under the Accounting Standards, it shall be

sufficient if the company complies with provisions on

consolidated financial statements provided in Schedule III of

the Act.

Rule 6 of Companies (Accounts) Rules, 2014

Preparation of CFS will not be applicable to an Intermediate

Wholly Owned Subsidiary, except if its immediate parent is a

company incorporated outside India.

For Financial Year ending 31 March 2015, if a company does

not have any subsidiaries, but only has associates and/or joint

ventures, then the company would not have to prepare CFS in

respect of such associates and/or joint ventures

As per MCA Circular, Schedule lll to the Act read with

Accounting Standards does not envisage a company to merely

repeat the disclosures made by it under stand-alone accounts

when it prepares CFS.

In the CFS, a company would need to give all disclosures

relevant for the CFS only.

Consolidated Financial Statements…

MCA Circular dated October 14, 2014

Consolidated Financial Statements

Section 2(6) defines associate company.

Associate company, in relation to another company, means a company in

which that other company has a significant influence, but which is not a

subsidiary company of the company having such influence and includes a

joint venture company.

Explanation - For the purpose of this clause, significant influence means

control of at least twenty per cent of total share capital, or of business

decisions under an agreement.

Section 2 (87) defines subsidiary company.

“subsidiary company” or “subsidiary”, in relation to any other company (that

is to say the holding company), means a company in which the holding

company—

(i) controls the composition of the Board of Directors; or

(ii) exercises or controls more than one-half of the total share capital either

at its own or together with one or more of its subsidiary companies:

7

Accounting Standard 27

Financial Reporting of

Interests in Joint Ventures

8

Topics Covered

I. Definitions

II. Forms of Joint Ventures

III. Jointly Controlled Operations

IV. Jointly Controlled Assets

V. Jointly Controlled Entities

VI. Disclosure

Scope

To be applied in accounting for investment in joint ventures,

and the reporting of joint venture assets, liabilities, income and

expenses in the financial statements of venturers and

investors, regardless of the structure and forms under which

the joint venture activities take place

Applicable only where CFS is prepared and presented by the

venturer

Control

1. Voting Power 50 % or more

OR AS 21

2. Power to Compose General Body AS 18

OR

3. Substantial Interest and

Power to Direct Financial /

Operating Matters

4. Power to govern Fin. and Op. Matters AS 27

5. Power to Participate AS 23

(significant Influence)

11

Interests in Joint Ventures - Definitions

A Joint Venture is a contractual arrangement whereby

two or more parties undertake an economic activity

which is subject to joint control

Control is the power to govern the financial and

operating policies of an economic activity so as to

obtain benefits from it

Joint control is the contractually agreed sharing of

control over an economic activity

12

Interests in Joint Ventures - Definitions

Venturer is a party to the Joint Venture and has joint

control over that

An investor in a joint venture is a party to a joint venture

and does not have joint control over that joint venture

Proportionate consolidation is a method of accounting

whereby a venturer’s share of each of the assets, liabilities,

income and expenses of a jointly controlled entity is

combined line by line with similar items in the venturer’s

financial statements or reported as separate line items in

the venturer’s financial statements.

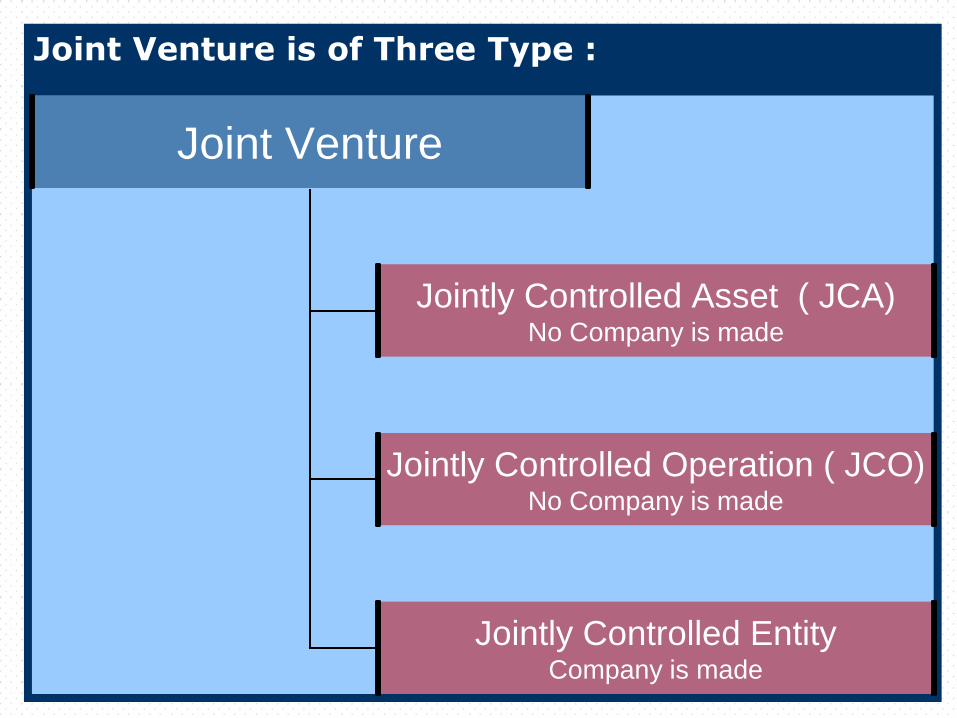

Joint Venture is of Three Type :

Joint Venture

Jointly Controlled Asset ( JCA) No Company is made

Jointly Controlled Operation ( JCO) No Company is made

Jointly Controlled Entity Company is made

14

Jointly Controlled Operations

No separate entity

Each of the venturers use their own assets and

incurs its own expenses and liabilities

The joint venture agreement provides basis for

share of joint revenue and expense

No adjustments or consolidation procedures

required when CFS is presented

Eg: Aircraft manufacture and sale.

15

Jointly Controlled Operations

Presentation and Accounting

A venturer should recognise in its separate financial statements:

The assets that it controls and the liabilities that it incurs; and

The expenses that it incurs and its share of the income that it earns from the sales of goods or services by the joint venture.

16

Jointly Controlled Assets

No separate entity

Joint control or ownership of one or more assets contributed to

or acquired for the purpose and dedicated to a joint venture

Each of the venturers has control over its share of the future

economic benefits through its share of the jointly controlled

asset.

The joint venture agreement provides basis for share of joint

revenue and expense. Each venturer to recognise its share

of asset / liability / income / expense in its accounts. No adjustments on CFS

Eg: Oil, gas and mineral extraction industry.

17

Jointly Controlled Assets

Presentation and Accounting

Each venturer should include the following items in its accounting records:

Its share of the jointly controlled assets

Any liabilities which it has incurred on behalf of the joint venture

Its share of income, together with its share of any expenses incurred by the joint venture

18

Jointly Controlled Entities

Establishment of a corporation, partnership or any

other entity

Contractual agreement between venturers establish

joint control over the economic activity of the entity

Jointly controlled entity maintains its own set of

accounts and prepares financial statements.

Each venturer contributes cash or other resources to

the jointly controlled entity.

19

Jointly Controlled Entities

Description

A jointly controlled entity controls the assets of the

joint venture, incurs liabilities and expenses and

earns income. It may enter into contracts in its own

name and raise finance for the purposes of the

joint venture activity.

A jointly controlled entity maintains its own

accounting records and prepares and presents

financial statements in the same way as other

entities.

20

Jointly Controlled Entities

Presentation and Accounting

A venturer shall recognise its interest in a jointly

controlled entity using either proportionate consolidation

When investment ceases to be a JCE – From the date of

cessation, the net assets of the JV after adjusting the

goodwill/ capital reserve are treated as investment in the

venture

21

Jointly Controlled Entities

Transactions between venturer and joint venture

When venturer contributes or sells assets to JV, and

the asset is retained, then the venturer shall recognise

only the portion of gain or loss that is attributable to the

interests of the other venturer.

When venturer purchases assets from a JV, the

venturer shall not recognise its share of profits until it

resells the assets to an independent party.

Transactions between the venturer and the

venture

Upon sale of any individual asset to the JV, only proportional gain

(that is, interest of other venturers) should be recognised by the

venturer

– Example: in a venture, A has 30% interest, others have the

remaining 30%. A sells an asset, having carrying value of Rs 1000 for

a price of Rs 1500.

• In separate financial statements, A would book a gain of Rs 500

• In consolidated financial statements, A would book a gain of only 70% of

500 – correspondingly, the value of the asset bought will stand reduced in

consolidated statements

If an asset is sold for a loss – If the loss represents impairment, it is

booked fully

– As a loss in separate accounting statements

– As impairment in consolidated fin statements

22

23

Disclosures

Contingencies

A venturer should disclose the aggregate amount of the contingent liabilities, unless the probability of loss is remote, separately from the amount of other contingent liabilities.

A venturer discloses the aggregate amount of any capital commitments in respect of its interests in joint ventures separately from other commitments

24

Disclosures

A venturer should list and describe interests in

significant joint ventures and the proportion of ownership interest held in jointly controlled entities.

A venturer which reports its interests in jointly controlled entities using the line by line reporting format for proportionate consolidation or the equity method should disclose the aggregate amounts of each of:

Current assets

Long term assets

Current liabilities

Long term liabilities

Income and expenses related to its interests in joint ventures.

A venturer should disclose a list of all joint ventures and description of interests in significant joint ventures. In respect of jointly controlled entities, the venturer should also disclose the proportion of ownership interest, name and country of incorporation or residence.

Disclosure for Joint Venture

19 INVENTORIES March 201X March 201X

(at Lower of Cost or Realisable value)

Raw materials and components

4,313

4,313

Raw material overseas goods-in transit

203

203

Work-in-progress

2,422

2,200

Stores and Spares

1,693

1,634

Loose Tools

43

714

Finished Goods

4,148

2,600

Finished goods-in transit

614

277

Stock in Trade

81

24

Share in Joint Ventures

6,062

4,019

Total Inventories

19,579

15,984

Disclosure for discontinuance of accounting for JV

Interests in joint ventures-

a) During the year, the Company’s venture in Tunisia [the Tunisian Indian

Fertiliser S.A. (TIFERT)], has commissioned the phosphoric acid plant and

commenced production. Pursuant to the shareholders’ agreement in relation to

TIFERT, the day to day operations have been assumed by the Tunisian

Partners and the Company has accordingly discontinued proportionate

consolidation under Accounting Standard 27 - “Financial Reporting of Interests

in Joint Ventures” and is treating its investment in TIFERT under AS 13 -

“Accounting for Investments

Disclosure for Joint Venture

32 Information on Joint Venture Entities

The particulars of the Company's Joint Venture Entities as at March 31, 2014 including percentage holding and its proportionate share of assets, liabilities, income and expenditure of the Joint Ventures are given below:-

S No. Name of the Joint

Venture

As at March 31, 2014 2013-2014

% of Holding

Assets Liabilities Contingent Liabilities

Capital Commitme

nts Income Expenses

1 Rane TRW Steering Systems Limited

50%

18,578

18,578

1,920

789

30,070

28,844

50%

(18,001)

(18,001)

(2,194)

(1,040)

(32,304)

(30,091)

2 Rane NSK Steering Systems Limited

49%

12,848

12,848

41

150

25,871

24,745

49%

(10,179)

(10,179)

(41)

(686)

(28,213)

(26,436)

3 JMA Rane Marketing Limited

49%

1,248

1,248

-

-

2,708

2,576

49%

(1,181)

(1,181)

-

-

(2,507)

(2,351)

Note:

1. Figures in bracket relates to the previous year.

2. All the above Joint Venture Entities located in India.

29

Accounting Standard 23

Accounting for Investments

in Associates in Consolidated

Financial Statements

30

Topics Covered

I. Scope and Definitions

II. Significant Influence

III. Potential voting rights

IV. Methods of Consolidation

V. Disclosures

Scope

To be applied in accounting for investment in

associates in the preparation and presentation of

consolidated financial statements by an investor.

Definition

An associate is an enterprise over which the investor

has significant influence and that is neither a subsidiary

nor an interest in a joint venture.

Significant influence is the power to participate in

the financial and/or operating policy decisions of the

investee but is not control or joint control over those

policies.

Definition

If an investor holds, directly or indirectly (eg through subsidiaries),

20 per cent or more of the voting power of the investee, it is

presumed that the investor has significant influence, unless it can be

clearly demonstrated that this is not the case.

Conversely, if the investor holds, directly or indirectly (eg through

subsidiaries), less than 20 per cent of the voting power of the

investee, it is presumed that the investor does not have significant

influence, unless such influence can be clearly demonstrated.

A substantial or majority ownership by another investor does not

necessarily preclude an investor from having significant influence.

Potential equity shares of the investee held by the investor should

not be taken into account for determining the voting power of the

investor

Significant influence….

Representation on the board of directors or equivalent

governing body of the investee;

Participation in policy-making processes, including

participation in decisions about dividends or other

distributions;

Material transactions between the investor and the

investee;

Interchange of managerial personnel; or

Provision of essential technical information.

Significant influence….

The chairman of the investee owns a large, but not necessarily controlling,

block of the investee's outstanding stock; the combination of the chairman's

substantial shareholding and his position with the investee may preclude the

investor from having an ability to influence the investee.

Adverse political and economic conditions in the country of existence

Opposition by the investee

Agreement between investor and investee

Majority ownership of the investee is concentrated among a small group of

shareholders who operate the investee without regard to the views of the

investor.

Litigation against an investee

Severe long-term restrictions impair the investor's ability to repatriate funds

Equity Method

Under the equity method, the investment in an associate is

initially recognised at cost and the carrying amount is increased or

decreased to recognise the investor's share of the profit or loss of

the investee after the date of acquisition.

Adjustments to the carrying amount may also be necessary for

changes in the investor's proportionate interest in the investee

arising from changes in the investee's other comprehensive income.

Such changes include those arising from the revaluation of property,

plant and equipment and from foreign exchange translation

differences.

Application of Equity Method

Interests other than equity interest may form part of net

investment.

Net investment initially recognized at cost.

Carrying amount increased/decreased based on

investor’s share of profit/loss of investee.

Investor’s share of profit/loss recognized in investor’s

profit/loss.

Distributions reduce carrying amount.

Investor’s share of profit/loss reflects present ownership

interests and/or other contractual arrangements.

Exceptions to Equity Method

If the investment is acquired and held exclusively with a

view to its subsequent disposal in the near future; or

The associate operates under severe long term

restrictions that significantly impair its ability to transfer

funds to the investor

Application of Equity Method - Losses

If losses exceed interest in associate

Interest in associate is carrying amount of investment together with

any long-term interests that, in substance, form part of the investor’s

net investment in the associate.

If losses exceed interest in associate, investor should discontinue

recognizing its share of further losses unless a legal obligation

exists.

Future profits recognized only when profits exceed share of losses

not recognized.

If distribution by associate is in excess of investor’s carrying amount,

record distribution as income, provided:

Distributions are not refundable by agreement or law and

Investor is not liable for obligations of associate or committed to

provide financial support to the associate

On Acquisition

An investment in an associate is accounted for using the

equity method from the date on which it becomes an

associate. On acquisition of the investment any

difference between the cost of the investment and the

investor's share of the equity of the associate is

described as goodwill or capital reserve as the case may

be.

Example -equity method

On 1/3/20X1 A buys 30% of B for Rs.300,000 (assume

no implicit goodwill).

B’s profit = Rs.80,000 for the year ended 31/12/20X1

(including 66,667 from March to Dec).

On 31/12/20X1 B declared a dividend of Rs.100,000.

At 31/12/20X1 the recoverable amount of A’s

investment in B = Rs.290,000 (ie Rs.300000 minus

Rs.30000 plus Rs. 20000).

41

Example -equity method

A Limited holds 22% share of B Limited on 1st April of

the year and the relevant information available on the

date of investments are: Cost of investment Rs.33000

and total equity on date of acquisition Rs.200000

Ans:

A Ltd’s equity will be 22% of Rs.200000 = Rs.44000

Less: Cost of Investment- Rs.33000

Capital Reserve Rs.11000

42

On Acquisition

Therefore:

a. goodwill relating to an associate is included in the

carrying amount of the investment. However,

amortisation of that goodwill is not permitted and is

therefore not included in the determination of the

investor's share of the associate's profits or losses.

b. any excess of the investor's share of the net fair value of

the associate's identifiable assets, liabilities and

contingent liabilities over the cost of the investment is

excluded from the carrying amount of the investment and

is instead included as income in the determination of the

investor's share of the associate's profit or loss in the

period in which the investment is acquired.

Distributions

How should distributions, by an equity method investee

to an investor in excess of the investor's carrying

amount, be recorded?

If distributions by an equity method investee to an

investor are in excess of the investor's carrying amount,

and (1) the distributions are not refundable by agreement

or law, and (2) the investor is not liable for the obligations

of the investee or otherwise committed to provide

financial support to the investee, then cash distributions

received in excess of the investment in the investee

should be recorded as income.

Disclosures

• Investment in associates to be listed by proportion of ownership

interest / voting power held in each associate

• Investments to be classified as long-term investments

• Investor's share of the profits / losses to be disclosed separately

• Associates where reporting date is different with difference in

dates

• In case of difference in accounting policies between parent and

associate, make appropriate adjustments in CFS to account for

the difference. Where this is not practicable, the fact should be

disclosed along with a brief description of differences in

accounting policies.

• Investor’s share of the contingencies and capital commitments of

an associate for which it is also contingently liable

Disclosure for Associates

An appropriate listing and description of associates including the proportion of ownership interest and, if different, the proportion of voting power held should be disclosed in the consolidated financial statements.

Companies Equity shares held % of voting power

held

As at March

31,2014

As at March

31,2013

As at

March

31,2014

As at

March

31,2013

Associates

Kar Mobiles Limited 886,369 884,369 40% 39%

SasMos HET Technologies Private Limited

351,400 351,400 26% 26%

Investments in associates accounted for using the equity method should be

classified as long-term investments and disclosed separately in the

consolidated balance sheet. The investor’s share of the profits or losses of

such investments should be disclosed separately in the consolidated statement

of profit and loss. The investor’s share of any extraordinary or prior period

items should also be separately disclosed.

Year ended March

31, 2014

Year ended March 31,

2013

IX. Profit after tax before share of Profit/(Loss) of associates and minority interest (VII - VIII)

4,501 4,887

X. Share of Profit /(Loss) of associates 174 -27

XI. Less: Minority Interest 327 1,023

XII. Profit for the year (IX + X - XI) 4,347 3,837

Equity accounted associates March 2014 March 2013

(i) Cost of investment

[including Rs. 129.96 crores (31.03.2013: Rs117.90 crores) of

goodwill (net of capital reserve) arising on consolidation]

698.59 654.99

(ii) Share of post acquisition profit (net of losses) 117.68 259.24

Total 816.27 913.23

48

Thank you for listening

Any Questions