argus minor metalsview.argusmedia.com/rs/584-buw-606/images/argus-minor-metals-s… · for early...

TRANSCRIPT

Copyright © 2015 Argus Media Ltd

Argus Minor Metals

Issue 15-34 | Tuesday 13 October 2015

prICESMarkEt HIgHlIgHtS

Global market prices, news and analysis

analysis: lithium mines line up battery supplyThe prospects for increased lithium demand in the coming years run counter to general weakness in the minor met-als markets, as projects are bought up in the US and supply lines put in place for the next generation of lithium prod-ucts. p7

analysis: European magnesium prices weakenThe European magnesium market has fallen to a fresh eight-year low after six weeks of stability, but renewed demand is expected in November as consumers look to secure supplies for early 2016. p7

Markets: prices resume fall post China holidayPrices for several metals fell following the Golden Week national holiday (1-7 October), as producers lowered their offers in response to weak demand. p2-6

lME calls for tailored EU metals regulationThe risks in metals trading are different from those in the financial markets and require tailored EU regulation, the London Metal Exchange (LME) said. p9

Vanadium: Market to cut back amid oversupplyThe vanadium market is turning around and expected to go through a period of production cutbacks and restocking, af-ter several years of oversupply, US-based vanadium, molyb-denum and titanium distributor Motiv Metals said. p9

ContEntS

Market commentary 2-6 Electronic metals prices 2Battery metals prices 3Light metals prices 4High-temperature metals prices 5Market news and analysis 7-16Price indexes (monthly averages) 17-18Price summary 19-23

Market snapshot13 oct

Unit low High ±

Antimony

Regulus grade II min 99.65% Sb du Rotterdam $/t 5,850 5,950 -112

Cobalt

Min 99.8% alloy grade du Rotterdam $/lb 12.80 13.50 -

Indium

Min 99.99% du Rotterdam $/kg 230.00 290.00 -

Manganese

Flake min 99.7% du Rotterdam $/t 1,480 1,520 -100

Tungsten

APT du Rotterdam $/mtu WO3 175.00 185.00 -5.000

Tantalum

Min 99.8% du Rotterdam $/kg 315.00 325.00 -7.500

± value represents week-on-week change

The service also incorporates price assessments from MetalPrices.com, which Argus Media acquired

in January 2015.

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

14 Apr 15 28 May 15 14 Jul 15 27 Aug 15 13 Oct 15

Manganese flake 99.7pc du Rotterdam, $/t

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 2 of 24

EuropE markEt CommENtarY priCEs

High-temperature metals lead lossesMarkets for high-temperature and light metals in particular moved down to fresh lows following recent stability as per-sistent weak demand eroded offer prices.

antimonyThe range for 99.65pc grade II metal narrowed to $5,850-5,950/t from $5,925-6,100/t previously as the market re-mained under downward pressure. Stocks are building up in Hunan province warehouses despite the recent closure of a number of producers and export prices fell by $100/t.

CadmiumConsistent demand saw price ranges for the metal rise at the top end, assessed up to 37-44¢/lb and 39-45¢/lb for 99.95pc and 99.99pc material respectively. Indian consum-ers continued to buy up available material from European producers and were willing to pay higher prices for prompt delivery as the festival season approaches.

CobaltPrices were assessed flat for a third week with trading activ-ity curtailed by London Metal Exchange week. Russian-grade 99.3pc metal held at $12.40-13/lb, with 99.6pc chemical grade used widely in the battery sector at $12.60-13.20/lb. Alloy-grade 99.8pc metal remained in a $12.80-13.50/lb range. But a spread appears to be opening between partici-pants' views of the market ahead of annual negotiations.

magnesium Lower Chinese export prices weighed on the market, which moved down after holding steady since the start of Septem-ber (see separate story). The range for 99.9pc ingot fell to $2,050-2,100/t, from $2,080-2,120/t previously and a fresh eight-year low. Sellers reported deals at $2,080/t for single 25t containers being shipped in early November.

manganeseThe flake market fell by $100/t in the past week to $1,480-1,520/t, its lowest level since November 2006, on weak demand from ferro-alloy producers that supply to the steel sector. Chinese exporters offered material at $1,500-1,550/t fob, down by $50/t. Consumer demand in the construction and energy sectors, where manganese-contained steel is used in tubes and pipes, has been weakening in 2015, with flat steels lagging but also getting weaker. There have been production cuts at southern and eastern European steelmak-ers and news this week that SSI in the UK has failed to find

Electronic metals price assessments13 oct

unit Low High ±

Arsenic

Min 99% du Rotterdam $/lb 0.90 1.05 -

Min 99% fob US (09 Oct) $/lb 0.98 1.20 0.010

Bismuth

Min 99.99% du Rotterdam $/lb 4.90 5.30 -

Bismuth min 99.99% ex-works China Yn/t 70,000 72,000 -3,500

Bismuth min 99.99% fob China $/lb 5.00 5.30 -0.200

Bismuth Ingot min 99.99% fob US (09 Oct) $/lb 4.60 5.05 -0.100

Gallium

Min 99.9999% ex-works China Yn/kg 1,150 1,250 -

Min 99.99% ex-works China Yn/kg 850 950 -

Min 99.99% fob China $/kg 135.00 160.00 -

Min 99.99% cif Main Airport $/kg 180.00 200.00 -

Germanium

Dioxide min 99.999% ex-works China Yn/kg 7,300 8,000 -

Dioxide min 99.999% fob China $/kg 1,250 1,350 -

Dioxide min 99.99% du Rotterdam $/kg 1,145 1,195 -

Metal (zone refined ingot) min 99.999% ex-works China Yn/kg 10,800 11,800 -

Metal min 99.99% cif Main Airport $/kg 1,725 1,800 -

Min 99.999% fob China $/kg 1,750 1,850 -

Indium

Min 99.99% du Rotterdam $/kg 230.00 290.00 -

Min 99.99% ex-works China Yn/kg 1,500 1,700 -

Min 99.99% fob China $/kg 240.00 280.00 -

Ingot min 99.99% fob US (09 Oct) $/kg 240.00 300.00 -2.500

Min 99% ex-works China Yn/kg 1,300 1,500 -

Selenium

Dioxide min 99% ex-works China Yn/kg 85.00 95.00 -

Min 99.5% du Rotterdam $/lb 8.00 10.00 -

Min 99.5% fob US (09 Oct) $/lb 7.50 10.00 -0.375

Powder min 99.9% ex-works China Yn/kg 140.00 160.00 -

Tantalum

Tantalite basis 30% Ta2O5 du Rot-terdam $/lb Ta2O5 60.00 65.00 -2.500

Min 99.8% du Rotterdam $/kg 315.00 325.00 -7.500

Tellurium

99.99% ex-works China Yn/kg 290.00 330.00 -

Min 99.99% du Rotterdam $/kg 40.00 60.00 -2.500

Min 99.95% fob US (09 Oct) $/kg 45.00 65.00 -12.500

Zirconium

Fused zirconia 98.5% ZrO ex-works China Yn/t 18,800 19,000 -

Oxychloride 36% Zr(Hf)O2 ex-works China Yn/t 8,200 8,800 -

Oxychloride 36% Zr(Hf)O2 fob China $/t 1,420 1,470 -

Silicate 65% Zr(Hf)O2 ex-works China Yn/t 9,400 9,700 -

Sponge 99.4% Zr+Hf ex-works China Yn/kg 152.00 157.00 -

± value represents week-on-week change

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 3 of 24

a buyer and will shut permanently its 2.5mn t/yr blast steel-making furnace after going into liquidation.

MolybdenumThere was little sign of an end to the recent slide in roasted concentrate prices, with material assessed lower for a third week at $4.40-4.60/lb from $5.00-5.20/lb previously.

SiliconReluctance among suppliers to cut their offer prices despite low demand from consumers kept prices unchanged for a third week. But the market could make further gains in the coming weeks, having bottomed out last month. The end of the rainy season in China will increase hydropower costs in the south of the country and in turn the cost of silicon pro-duction in the region. There have also been production cuts in China, and supplies are expected to tighten.

TantalumOre prices have come under pressure from overcapacity in the downstream sector, falling to $60-65/lb Ta2O5 for 30pc grade material from $62-68/lb Ta2O5 a week earlier, while 99.8pc metal moved down to $315-325/kg from $320-335/kg. The Tantalum-Niobium International Study Center has warned its members to be vigilant after a container load Rwandan columbite-tantalite ore tagged by the International Tin Research Industry's Tin Supply Chain Initiative (iTSCi) was reported stolen recently in the Tanzanian port of Dar es Salaam, the main export shipping route for minerals out of central Africa.

TelluriumThe price range narrowed amid limited business, moving to $40-60/kg from $40-65/kg. Consistently low prices have pushed some producers to consider halting production to wait for any future rises. Persistent low offers could result in larger and more robust producers edging out smaller busi-nesses while absorbing losses.

TungstenAmmonium paratungstate (APT) resumed its decline after holding steady for the past two weeks, with prices down to $175-185/mtu from $180-190/mtu. Prices had been at their lowest levels since July 2009, but with the latest decline have fallen to a level not seen since March 2005.

VanadiumThinly-traded pentoxide fell further after stabilising in the previous week, with prices for 98pc fused flake assessed at $2.50-3.00/kg from $2.90-3.20/kg previously.

PriceS

Battery metals price assessments13 Oct

Unit Low High ±

Antimony

Ingot min 99.65% ex-works China Yn/t 37,000 39,000 -500

Ingot min 99.65% fob China $/t 6,100 6,300 -100

Min 99.65% cif US ports (09 Oct) $/lb 2.88 3.03 -0.020

Regulus grade II min 99.65% Sb du Rot-terdam $/t 5,850 5,950 -112

Regulus Trioxide grade min 99.65% Sb du Rotterdam $/t 5,950 6,050 -150

Trioxide min 99.5% ex-works China Yn/t 34,000 35,000 -500

Trioxide min 99.5% fob China $/t 5,400 5,700 -100

Cadmium

Min 99.99% du Rotterdam $/lb 0.39 0.45 0.005

Min 99.99% ex-works China Yn/t 7,800 8,800 -

Min 99.99% cif India Rs/kg 114.00 118.00 -

Min 99.99% fob US (09 Oct) $/lb 0.37 0.43 -

Min 99.95% du Rotterdam $/lb 0.37 0.44 0.005

Min 99.95% fob US (09 Oct) $/lb 0.35 0.40 -

Min 99.95% cif India Rs/kg 103.00 110.00 -

Oxide min 99.5% ex-works China Yn/t 10,000 11,500 -

Cobalt

(Electrolytic metal) min 99.8% ex-works China Yn/kg 210.00 220.00 2.000

Chloride min 24% ex-works China Yn/t 45,500 48,000 -

Min 99.8% alloy grade du Rotterdam $/lb 12.80 13.50 -

Min 99.8% fob US (09 Oct) $/lb 13.20 13.50 -

Min 99.6% chemical grade du Rotterdam $/lb 12.60 13.20 -

Min 99.3% Russian grade du Rotterdam $/lb 12.40 13.00 -

Min 99.3% fob US (09 Oct) $/lb 12.75 13.05 -

Oxide 72% ex-works China Yn/kg 150.00 154.00 -

Powder min 99.8% ex-works China Yn/kg 230.00 250.00 -

Sulphate min 20% ex-works China Yn/t 39,500 42,500 -

Tetroxide min 73% ex-works China Yn/kg 153.00 157.00 -

Lithium cobalt oxide

Min 60% Co ex-works China Yn/kg 169.00 171.00 -

Mercury

Min 99.99% du Rotterdam $/Flask 1,800 2,100 -

± value represents week-on-week change

London Metal Exchange official closing cobalt prices $/t12 Oct 5 Oct ±

Cash buyer 27,490 27,740 -250

Cash seller 27,500 27,750 -250

3-month buyer 27,250 27,500 -250

3-month seller 27,750 28,000 -250

15-month buyer 27,730 27,710 20

15-month seller 28,730 28,710 20

London Metal exchange cobalt stocks t12 Oct 5 Oct ±

Stocks 558 558 -

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 4 of 24

Markets extend losses on destockingThe US dollar weakened in recent days on indications that the Federal Reserve could hold off on raising interest rates before the end of the year. The strong dollar has weighed on exports of minor metals in recent months, and prices contin-ued to fall in the past week.

CobaltThe market held onto late September's gains for a second week, with 99.3pc grade metal assessed flat at $12.75-13.05/lb and 99.8pc grade at $13.20-13.50/lb. Global prices have found some support from news of Glencore subsidiary Katanga Mining's 18-month production suspension and the Chinese government's stockpiling of 400t of metal.

IndiumThe extended run of losses continued on an absence of demand, with 99.99pc metal assessed down to $240-300/lb from $245-300/lb. But the market remained higher than in Europe at the top end of the range, commanding a premium for prompt delivery.

MagnesiumLower offer prices appeared on the market as suppliers tried to entice potential buyers off the sidelines. The range for 99.9pc metal edged down by 2¢/lb to $1.73-1.83/lb. Demand was not expected to rise in the near term with consumers well supplied and the focus turning to annual contracts.

SiliconThe 5-5-3 market held at a five-year low of $1.19-1.24/lb. The market has found some support as a recent wave of lower offers hitting the market has slowed, and a recent move by consumers to switch over to aluminium scrap has started to ease with scrap availability tightening.

TelluriumFalling demand has seen sellers increasingly look to offload inventory rather than wait for prices to rebound. The range for 99.95pc metal dropped by $12.50/kg to $45-65/kg from $55-80/kg a week earlier, its lowest level since March 2007.

uS MarkeT CoMMenTary prICeS

London Metal Exchange official closing aluminium price $/t12 oct 5 oct ±

Cash buyer 1,607.00 1,546.50 60.50

Cash seller 1,607.50 1,547.00 60.50

3 months buyer 1,626.50 1,555.50 71.00

3 months seller 1,627.00 1,556.00 71.00

Light metals price assessments13 oct

unit Low High ±

Magnesium

Alloy min 90% Mg AZ91 ex-works China Yn/t 14,000 14,300 -

Alloy min 90% Mg AZ91 fob China $/t 2,320 2,370 -

Min 99.9% ddp US $/kg 1.73 1.83 -0.020

Min 99.9% du Rotterdam $/t 2,050 2,100 -25

Min 99.9% ex-works China Yn/t 12,400 12,800 -

Min 99.9% fob China $/t 2,040 2,100 -20

Powder 99.9% Mg 20-80 mesh ex-works China Yn/t 13,500 13,700 -

Powder 99.9% Mg 20-80 mesh fob China $/t 2,150 2,200 -

Manganese

Briquette 97% Mn fob China $/t 1,550 1,600 -30

Electrolytic metal min 99.7% fob US (08 Oct) $/lb 1.09 1.12 -

Flake 99.7% Mn ex-works China Yn/t 9,500 9,700 -200

Flake min 99.7% fob China $/t 1,500 1,550 -30

Flake min 99.7% du Rotterdam $/t 1,480 1,520 -100

Lump 95% Mn fob China $/t 1,590 1,670 -30

Silicon

5-5-3 min 98.5% Si dat Chinese ports Yn/t 10,300 10,500 -

5-5-3 min 98.5% Si fob China $/t 1,610 1,640 -

5-5-3 min 98.5% Si ddp Europe works €/t 2,000 2,050 -

5-5-3 min 98.5% Si ddp US $/lb 1.19 1.24 -

4-4-1 min 99% Si dat Chinese ports Yn/t 11,050 11,250 -

4-4-1 min 99% Si fob China $/t 1,750 1,780 -

4-4-1 min 99% Si ddp Europe works €/t 2,120 2,170 -

Titanium

Concentrate 50% TiO2 ex-works China (VAT unpaid) Yn/t 770 800 -

Concentrate 46% TiO2 ex-works China (VAT unpaid) Yn/t 510 530 -

Ingot min 99% Ti pure TA1 ex-works China Yn/t 58,000 60,000 -

Ingot min 99% Ti pure TA2 ex-works China Yn/t 56,000 58,000 -

Ingot min 99% Ti pure TA3 ex-works China Yn/t 60,000 62,000 -

Slag min 92% TiO2 ex-works China Yn/t 4,200 4,300 -

Sponge 99.7% Ti ex-works China Yn/t 48,000 49,000 -

Sponge 99.6% Ti ex-works China Yn/t 47,000 48,000 -

Sponge TG-Tv 10x30mm du Rotterdam $/kg 5.00 5.20 -

Tetrachloride min 99.9% TiCl4 ex-works China Yn/t 5,600 5,700 -

Scrap 6Al 4V bulk weldable fob US (08 Oct) $/lb 3.25 3.35 -

Scrap 6Al 4V clips fob US (08 Oct) $/lb 2.95 3.05 -

Scrap grade 1 CP solids fob US (08 Oct) $/lb 2.15 2.20 -0.050

Scrap grade 2 CP solids fob US (08 Oct) $/lb 1.85 1.95 -0.050

Scrap grade 3-4 CP solids fob US (08 Oct) $/lb 1.65 1.70 -0.025

Scrap 6Al 4V turnings aero quality fob US (08 Oct) $/lb 2.10 2.20 -

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 5 of 24

Markets resume downward trend post holidayPrices for several metals fell following the Golden Week national holiday (1-7 October), as producers lowered their offers in response to weak demand.

AntimonyMetal and trioxide producers continued to reduce their of-fer prices. But business was thin as buyers waited for the market to bottom out. The range for 99.65pc metal was as-sessed at Yn37,000-39,000/t, a Yn500/t decrease from before the holiday, while trioxide prices also declined by Yn500/t to Yn34,000-35,000/t. BismuthPrices continued to retreat from September's two-month high. Producers were looking to liquidate stocks before prices fall further but buying interest has ebbed as consum-ers have finished restocking and are avoiding capital tight-ness. Prices for 99.99pc metal fell to Yn70,000-72,000/t from Yn72,000-75,000/t previously. CobaltThe market lost its pre-holiday upward momentum in recent days as consumer demand remained unchanged. The market was pushed up by national stockpiling late last month, and was assessed up by Yn2,000/t at Yn210,000-220,000/t. Prices could turn lower as buyers have not accepted higher prices. GalliumPrices remained rangebound at Yn850-950/kg, although pro-ducers expect more orders from overseas consumers as they are likely to replenish stocks this month. Export prices have been steady at $135-160/kg fob for more than two weeks. IndiumProducers were reluctant to accept lower prices in view of firm production costs and prices were assessed unchanged for a second week at Yn1,500-1,700/kg for 99.99pc metal, with 99pc grade at a Yn200/kg discount. The Wuxi Stain-less Steel Exchange listed 99.99pc grade at Yn1,403/kg on 13 October. Export prices for 99.99pc grade held at $240-250/kg fob, with no deals reported. MagnesiumPrices were rangebound between firm production costs and low consumer buying. Stocks accumulated after the holiday and producers are looking to sell off stocks, pointing to downside potential. Producers remain cautious about the

ChInA MArket COMMentArY prICes

high-temperature metals price assessments13 Oct

Unit Low high ±

Chromium

(alumino-thermic) min 99% du Rot-terdam $/t 7,900 8,350 -225

(aluminothermic) min 99% Cr ex-works China Yn/t 60,000 65,000 -

Molybdenum

Oxide min 57% Mo du Rotterdam $/lb Mo 4.40 4.60 -0.600

Oxide min 57% fob US (08 Oct) $/lb 5.70 5.85 -0.075

Rhenium

APR min 69.2% Re (basic grade) du Rotterdam $/kg Re 1,350 1,450 -

APR min 69.4% Re (catalyst grade) dp Rotterdam $/kg Re 2,600 2,750 -

APR min 69.4% Re ex-works China Yn/kg 8,400 9,300 -

Pellets min 99.9% Re dp Rotterdam $/lb 870 1,130 -

Tungsten

APT du Rotterdam $/mtu WO3 175.00 185.00 -5.000

APT fob China $/mtu WO3 168.00 178.00 -2.000

APT min 88.5% ex-works China Yn/t 89,000 91,000 -3,000

Carbide min 99.7% ex-works China Yn/kg 150.00 153.00 -4.000

Carbide powder (3-4micron) fob China $/kg 24.00 25.00 -0.500

Oxide (Yellow/Blue oxide) fob China $/t 17,800 18,800 -200

Oxide min 99.95% ex-works China Yn/t 105,000 109,000 -3,500

Concentrates min 65% ex-works China Yn/t 59,000 61,000 -1,000

Vanadium

Pentoxide fused flake min 98% du Rotterdam $/lb V2O5 2.50 3.00 -0.300

Pentoxide 98% V2O5 ex-works China Yn/t 38,000 40,000 -1,500

± value represents week-on-week change

London Metal Exchange official closing molybdenum prices $/t12 Oct 5 Oct ±

Cash buyer 10,200.00 11,050.00 -850.00

Cash seller 10,700.00 11,550.00 -850.00

3-month buyer 10,200.00 11,050.00 -850.00

3-month seller 10,700.00 11,550.00 -850.00

15-month buyer 10,440.00 11,300.00 -860.00

15-month seller 11,440.00 12,300.00 -860.00

London Metal exchange molybdenum stocks t12 Oct 5 Oct ±

Stocks 132 132 -

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 6 of 24

outlook for the remainder of the year amid tight cash flow and year-end stock liquidation.

Manganese The market resumed its decline on weak demand from stain-less steelmakers. Flake prices were assessed Yn200/t lower at Yn9,500-9,700/t for 99.7pc grade, its lowest level since November 2006. A large stainless steelmaker that purchased 320t/month of 97pc lump in 2014 has not purchased lumps for nearly six months as they have cut manganese applica-tion in stainless production. In line with the lower domestic prices, export prices dipped by $30/t to $1,500-1,550/t fob. Posco, one of the world's largest manganese consumers, has not begun its monthly purchase for October requirements. SeleniumConsumers were well supplied after restocking before the holiday and prices were unchanged. The range for 99pc diox-ide held at Yn85-95/kg, with 99.9pc powder at Yn140-160/kg. Both markets ticked up by Yn5/kg in September, although dioxide prices subsequently fell back. Prices were expected to remain flat amid low import costs and weak consumption from the manganese and glass industries. SiliconA number of smelters in Inner Mongolia resumed produc-tion over the holiday period on tight spot supply, although prices remained flat. Prices for 5-5-3 grade have been at Yn10,300-10,500/t for two weeks, with 4-4-1 grade also flat at Yn11,050-11,250/t. Export prices have been stable for more than a month, although there has been active interest from overseas buyers looking to build up inventory. TelluriumSpot trading has dried up and consumers are sufficiently sup-plied by deliveries from long-term contracts and seldom buy

additional material. The market is expected to remain under downward pressure from sustained oversupply. Titanium Sponge prices have been rangebound for more than a month on sparse business from downstream mill product manufac-turers. There has been a small number of enquiries, none of which translated into concluded deals. Producers have con-trolled output, with profit margins squeezed by low prices paid by mill products manufacturers and higher production costs. Prices for 99.7pc grade remained in a Yn48,000-49,000/t range, with 99.6pc at a Yn1,000/t discount. TungstenProducers lowered their offer prices in view of reduced demand from the cemented alloy sector. Prices for 65pc wolframite declined by Yn1,000/t to Yn59,000-61,000/t. Prices for ammonium paratungstate (APT) and carbide also declined in response to the downturn for raw material. Busi-ness has been thin as downstream buyers are seeing reduced orders from customers. VanadiumThe pentoxide market resumed its decline as buying from ferro-vanadium and vanadium nitrogen alloy smelters has eased on account of falling tender prices and reduced demand from steelmakers. The range for 98pc flake fell to Yn38,000-40,000/t, down from Yn40,000-41,000/t previously. ZirconiumProduction capacity utilisation of Chinese zirconium sponge has been falling on account of slow purchases from consum-ers inside and outside of China. Guangdong Orient Zirconic Ind Sci & Tech and Aohan Huatai Metal Industry have not re-sumed operations. Prices for 99.4pc grade zirconium sponge have been in a Yn152-157/kg range since late August.

Fanya Metal Exchange bismuth stocks t

18,000

18,400

18,800

19,200

19,600

20,000

02 Jan 15 14 Mar 15 24 May 15 03 Aug 15 13 Oct 15

Fanya Metal Exchange indium stocks t

3,400

3,450

3,500

3,550

3,600

3,650

02 Jan 15 14 Mar 15 24 May 15 03 Aug 15 13 Oct 15

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 7 of 24

market news and analysis

spite increased enquiries from consumers that are not fully covered under full-year contract delivery requirements and are looking for new supplies.

The onset of China's dry season does not affect magne-sium production costs — minor metals producers are in the the north of the country where power supply is mainly coal fired.

Freight rates have fallen to around $600/container, from as much as $1,500/container in the previous quarter. Rates are usually available on ships in the coming week or two, al-though the trend this year has been for prices to rise around the start of a calendar month before falling in the following weeks.

European magnesium prices fell in the days after China devalued its currency in mid-August, although some of that drop was absorbed by a subsequent increase in sea freight rates.

But consumers are less keen to commit to longer-term deliveries, opting instead for spot settlements to avoid build-ing inventories. Demand for finished products has weakened and falling prices mean that they can probably restock at lower prices.

Magnesium is primarily used as an alloy with aluminium, accounting for some 45pc of total world consumption. Another 35pc is consumed in magnesium alloys in structural metals, about 13pc in steel making, with the rest used in electro-chemical and other sectors.

analysis: lithium mines line up battery supplyThe prospects for increased lithium demand run counter to general weakness in the minor metals markets. But projects are being bought in the US and supply lines established for the next generation of lithium products.

The acquisition of two US lithium exploration projects in Nevada by explorer Nevada Sunrise Gold reflects expecta-tions of increased demand, despite falling prices for other minor metals.

And share prices are reflecting optimism about the lithium market's prospects. Australia-listed explorer Pilbara Minerals' shares rose by 21.5pc on 12 October to a 52-week after it revealed a supply agreement for lithium-containing spudomene from its Pilgangoora project in Western Austra-lia. Pilgangoora holds 52.2t grading at 1.28pc lithium oxide (LiO), which should yield 668,000t of LiO.

Prices for other battery and electronic minor metals, such as bismuth and indium, have fallen consistently for months — bismuth is assessed at $4.90-5.30/lb in Europe, down from $10.60-11.20/lb at the start of this year, while

analysis: magnesium resumes decline in europeThe European magnesium market has fallen to a fresh eight-year low after six weeks of stability. But renewed demand is expected next month as consumers look to secure supplies for early 2016.

The market in Europe has dropped in line with lower magnesium export prices from key supplier China. The range for 99.9pc ingot in-warehouse Rotterdam has moved down to $2,050-2,100/t, having held steady at $2,080-2,120/t since the start of September. The price in Europe was last this low in February 2007.

The European market has been in decline since May 2014 — falling demand and oversupply have weighed heavily on prices across minor metals markets. And there has been increased availability of aluminium alloy scrap with a high magnesium content, which some consumers have favoured over higher-priced magnesium metal.

A slowdown in Chinese demand has resulted in increased aluminium scrap availability in the Atlantic basin. US mag-nesium prices have fallen on this increased availability and rising imports because of the stronger dollar. US prices had been supported up to December by a shortage exports from countries such as Russia and Kazakhstan.

Magnesium prices in China have been steady for five weeks — prices are close to output costs and producers are reluctant to cut. But domestic demand from the down-stream aluminium, magnesium alloy and magnesium powder industries shows no signs of picking up after the low-demand summer period.

Chinese exporters have tried to hold prices stable since returning from the week-long national holiday at the start of this month, but international market fundamentals remain weak. Prices have dropped by $20/t to $2,040-2,100/t de-

2,000

2,100

2,200

2,300

2,400

2,500

02 Jan 15 14 Mar 15 24 May 15 03 Aug 15 13 Oct 15

Magnesium min 99.9% du Rotterdam, $/t

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 8 of 24

indium has dropped to $230-290/kg from $670-730/kg. And markets will remain under pressure in the near term and could remain lower into the second quarter of 2016, accord-ing to some market participants.

The prospects for new and sustained commercial ap-plications for lithium is largely attributable to battery and electric-vehicle manufacturers such as US firm Tesla. Its am-bitious production targets — 500,000 electric-powered cars a year by 2020 — would demand a significant jump in global production of lithium-ion batteries.

Tesla's under construction Gigafactory in Nevada will pro-duce 50 GWh/yr of battery capacity, absorbing high quanti-ties of lithium.

Nevada state holds significant lithium and lithium-brine deposits, many of which are producing or in the process of development. And US consumers are keen to source more supply from closer to home. Supply arrangements for the Gigafactory are in place with Canadian miner Pure Energy Minerals, which operates Nevada's Clayton Valley lithium brine project, and Bacanora Minerals, which is constructing the Sonora project in northern Mexico. Much of the supply now is mined in Australia and South America.

And Tesla vehicles are not the only potential driver of market growth. The use of wall-mounted lithium-ion battery systems could rise significantly as consumers seek to offset rising electricity prices and fluctuations in grid supply. US property developer Irvine plans to install battery-powered energy systems, supplied by Tesla, in each of its 15 office buildings to use at peak demand times.

And demand for lithium-ion batteries used in personal electronics, such as tablets, mobile phones and laptops, en-sures continuing demand as these devices become cheaper and more accessible.

But whether lithium consumption fulfils this promise remains to be seen. The $80,000 base price of Tesla's Model

X car could prove an obstacle to widespread adoption. And there are questions surrounding the company's ability to ful-fil orders ahead of the planned launch of the Mark 3 in 2017.

The price trajectory of other battery and electronic met-als in recent years could offer warning signs — oversupply and lower-than-expected demand have driven down prices. The gallium market, for example, ramped-up production capacity in anticipation of widespread adoption of LED light-ing. But the higher consumption failed to materialise, leaving a supply surplus that will take the market a long time to absorb.

Lithium: Nevada Sunrise to acquire two projectsCanada-based mineral exploration firm Nevada Sunrise Gold is to acquire two additional lithium exploration properties in Esmeralda County in the US state of Nevada.

According to an interim agreement, the Vancouver-based company will purchase the Clayton Northeast property, which consists of 16 unpatented association placer claims totalling 526 acres (2km²), and the Jackson Wash property made up of 58 unpatented association placer claims totalling about 2,215 acres.

Both properties are near the Silver Peak lithium mine property operated by US specialty chemicals group Albe-marle.

Nevada Sunrise Gold announced last month that it had entered into an agreement to [purchase the Neptune lithium project in Clayton Valley, Nevada](http://direct.argusmedia.com/newsandanalysis/article/1097200).

A number of US lithium projects are under development, as explorers look to exploit resources outside traditional lithium-producing locations such as Australia and South America.

Market sentiment is positive as lithium-ion battery manufacturer Tesla has signed a number of agreements with producers, aimed at supplying its Gigafactory sites.

Lithium: Avalon to complete pilot projectCanada's Avalon Rare Metals is due to complete a pilot plant programme at its Separation Rapids lithium project in Ke-nora, Ontario, by the first quarter of next year.

Lithium concentrate from the project will be available for distribution in the first quarter, the company said.

Avalon shipped a 30t bulk sample of crushed ore this summer from the project and work is now under way in a German laboratory to process it.

The sample will be processed using the company's flow sheet to produce a high-purity lithium mineral (petalite)

mArket NewS ANd ANALySiS

illuminating the markets

Market ReportingConsulting

Events

China Metals Week 201516-19 NovemberMarriot Guangzhou Tianhe, ChinaDiscover global market outlook from three independent conferences for selected minor metals throughout the week:▸ Antimony Conference▸ Tungsten Conference▸ Electronic & Battery Metals Conference

For enquiry, please contact Yuan Chang at [email protected]

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 9 of 24

concentrate in order to deliver further product samples to potential customers in the glass ceramics industry.

Critical materials consulting firm Stormcrow Capital esti-mates that demand could reach 410,000t of lithium carbon-ate equivalent in 2025 compared with 200,000t in 2015.

Lithium: Electric car sales no threat to leadLithium-ion batteries pose major competition to lead-acid batteries in electric cars but the proliferation of conven-tional cars will keep overall lead demand stable over the coming years according to an analyst at consultancy AME, Ian Warden.

Over 60pc of global lead is used in lead-acid batteries in conventional cars, Warden told delegates at the annual London Metal Exchange Week seminar. But modern electric vehicles use lithium-ion batteries. Electric car production is the fastest-growing segment of the car industry, but these types of vechiles still make up only a small proportion of total sales — about 0.8pc of the 1.2bn units sold worldwide. Electric vehicle sales make up more than 1pc of total car sales in only four countries.

Demand for new conventional cars, particularly in emerging countries, is so high compared with electric ve-hicles that alternative metals in car batteries will not pose a significant threat to lead demand for more than seven years, Warden said.

Unlike in other metals, the supply response from produc-ers is fairly inelastic. Lead is mainly mined as a by-product of other metals such as copper, silver or zinc and production levels are dominated by the prices of the other metals.

Warden expects supply levels and demand growth to be flat this year, but supply growth is likely to increase slightly over the next few years because of new projects.

Several big closures of zinc-lead mines have not led to an aggressive reduction in lead supply because production has risen elsewhere. The closures of the Century mine in Aus-tralia and the Lisheen mine in Ireland this year will remove about 120,000 t/yr from the supply chain.

China remains by far the biggest producer of the metal, making up 42pc of global refined lead output and 52pc of global lead mine output. This production may decline by about 3pc in the medium term because the country has introduced new environmental legislation that stipulates a minimum mine size, requires better water treatment and caps smelters's emission levels.

The cost of production is on a declining trend, like in other base metals, and will not provide any price support if lead prices start to decline. Warden expects prices to

average $1,816/t this year and to rise to $2,000/t next year and to $2,100/t in 2017, with growth increasing by 2.9pc next year and 4pc in 2017.

LME calls for tailored EU metals regulationThe risks in metals trading are different from those in the financial markets and require tailored EU regulation, the London Metal Exchange (LME) said.

“The LME supports EU regulators’ aims to increase trans-parency and reduce risk in the markets," LME chief executive Garry Jones said.

"But requiring the metals industry to comply with regula-tion that is designed for other, completely different, asset classes may stifle participants’ ability to create world refer-ence prices and manage their price risk," he said.

The wide scope of the EU's Markets in Financial Instru-ments Directive (MiFID 2), Market Abuse Regulation, Bench-mark Regulation and European Market Infrastructure Regula-tion mean that many in the LME markets, such as commodity traders, may face stringent new EU rules.

But little attention has been focused by regulators, and to some extent the industry, on how the new rules will af-fect the metals markets in particular, the LME said.

“The LME is working with regulators to ensure that the cumulative effect of these rules on the metal trading community is not underestimated," LME head of regulation Kirstina Combe said.

The implementation dates of many of these rules are rapidly approaching, and participants throughout the metals value chain should be thinking about what the changes mean for their business, she said.

Vanadium: Market to cut back amid oversupplyThe vanadium market is turning around and expected to go through a period of production cutbacks and restocking, after several years of oversupply, the president of US-based vanadium, molybdenum and titanium distributor Motiv Met-als, Terry Perles, said.

Annual vanadium production has outstripped consump-tion since 2010, except in 2013, Perles said. Vanadium stocks grew during this period, but are expected to decline to the equivalent of less than a month of consumption, he said.

Global vanadium production increased at a compound annual growth rate (CAGR) of 5.5pc between 2003 and 2015, with 95pc of this increase coming from China. The country accounts for 54pc of global vanadium supply compared with South Africa's 15pc share and Russia's 10pc. Europe had a 6pc share, with most of its output coming from South African

MarkEt nEws and anaLysis

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 10 of 24

market news and analysis

raw materials.Motiv expects vanadium production to fall to 82,000t in

2015 from 92,000t last year, because of price declines and the bankruptcy of South Africa's Evraz Highveld Steel and Vanadium and as blast furnaces that produce vanadium slag are idled in China. Most of this reduction will happen in the second half of this year as blast furnaces close, with 65-70pc of global vanadium production coming from slag gener-ated as a by-product of the steel industry, while some 20pc comes from primary titanium-iron-magnetite ore and 13pc from secondary materials including oil industry waste.

Just eight steel mills in the world generate raw materials for 80pc of vanadium production and the vanadium industry is losing this supply as the mills cut output, Perles said.

Vanadium consumption growth has been consistently higher than steel production, which is increasing at a CAGR of 5pc. Two-thirds of the growth in vanadium consumption comes from increasing steel production and about one-third from the rising vanadium content in steel. Motiv expects this split to change to 50:50.

titanium: russian demand to remain steadyRussian titanium consumption is expected to remain stable at 12,000-13,000 t/yr of mill products over the next 5-6 years, according to the president of VSMPO-Tirus US, Mike Metz, who was speaking at the ITA Titanium 2015 conference in Orlando, Florida.

New commercial aircraft programmes are expected to grow, although they will add to stable business in industrial market. The titanium market in Russia differs from that in western countries in that it is dominated by industrial ap-plications led by shipbuilding, which alone accounts for 25pc of consumption.

Demand in shipbuilding peaked at 4,200t in 2014 but

declined significantly this year and will level out at 2,400 t/yr by the end of this decade. Commercial shipbuilding is dominated by region-specific vessels such as icebreakers for arctic shipping and vessels designed for arctic explora-tion and inland waterways. But a larger share of demand for titanium comes from military shipbuilding, including subma-rines, mini submarines and navy surface vessels.

Another major area of industrial titanium demand in Russia is power engineering, mainly in nuclear power plants — with demand closely aligned with the timing of nuclear projects. Titanium is used in condensers built in Russia both for the Russian market and for export.

Titanium is also consumed by the non-ferrous metal manufacturing and chemical processing industries in Russia. It enjoys steady demand from the oil and gas sector for use in production equipment, although this may change given the fall in oil prices, Metz noted. Russian demand for tita-nium in welded tubes dropped sharply this year, as a result of the downturn in this sector, to 450t from 850t in 2014, but is set to recover to average 700 t/yr in the coming years. Over the next 5-6 years, overall Russian industrial demand for titanium is set to average 5,000-6,000 t/yr, compared with 6,500t in 2014.

Russian aerospace accounts for 28pc of titanium con-sumption in airframes and 29pc in engines. Titanium demand in this sector is projected to rise to 8,000 t/yr from 7,000 t/yr by the start of the next decade, Metz said.

Russian aircraft production is growing and is led in the commercial sector by the Sukhoi SuperJet, which is expect-ed to see a 60pc increase in build rates. Production capacity is set to reach 48 aircraft in 2019 from 21 in 2015. Output of the new MS21 single aisle aircraft is expected to triple to 18 by 2021 from 6 built in 2015.

Build rates are also rising in the defence sector, including for the military Sukhoi jet and Ilyushin aircraft. The produc-tion of Be-20 amphibious aircraft is set to rise to six each year by the end of the decade from two next year.

titanium: Japanese shipments rising in 2015Japanese titanium sponge shipments are set to rise to 45,000t this year from around 35,000 t/yr in 2013-2014, Toho Titanium president and Japan Titanium Society chairman Kazuo Kagami told the ITA Titanium 2015 conference.

Supplies to domestic and export markets have fallen in recent years from over 55,000t in 2012, as a result of the in-creased use of scrap and lower demand for titanium sponge, particularly in the industrial markets as nuclear projects were delayed in the wake of the Fukushima disaster. But

2.5

3

3.5

4

4.5

14 Apr 15 28 May 15 14 Jul 15 27 Aug 15 13 Oct 15

Vanadium pentoxide fused flake min 98pc du Rotterdam, $/lb V2O5

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 11 of 24

market news and analysis

Japanese titanium manufacturers are now seeing an increase in demand for both sponge and mill products and are gradu-ally increasing production. But while volumes are increas-ing, this is not being matched by an improvement in prices according to market participants.

Kagami told the conference that given the slowdown in the Chinese economy, there is some uncertainty about the market, but infrastructure projects in the Middle East are expected to boost titanium demand.

The Japan Titanium Society forecast that Japanese titanium mill product shipments will rise to 14,000t this year from 13,000t last year, based on shipments of 7,000t in the first half of 2015. The metal is being incorporated into new alloys and applications in Japan, which is helping to bolster domestic demand. Titanium sheet is being used in heat exchangers for ocean thermal energy conversion in Okinawa and Hawaii.

New alloys include the TNCZ strength, lightweight alloy (Ti-20Nb-5Cr-4Zr) developed by Daido Steel. A titanium-alu-minium-iron alloy (Super-TIX51–Ti-5Al-1Fe) which offers good balance between machinability and workability is used in the connecting rod for the new Yamaha sports motorcycle. Meanwhile Toyota Mirai, the first commercial hydrogen fuel call car, uses titanium in separators for its fuel cell stack which forms part of the powertrain. Titanium is also used in roof tiles, including in temple renovation projects, and the roof on the Kyushu National Museum is made from blue an-odized titanium and worked from a 120m single roof sheet.

titanium: sponge capacity overhang persistsGlobal titanium sponge capacity continues to outstrip de-mand despite growth in its main consuming market, aero-space.

Stocks of titanium sponge worldwide were 25,000t at the

end of the first quarter, industry consultancy TZMI managing director David McCoy told the ITA Titanium 2015 conference in Orlando.

Output from the largest aerospace-grade titanium pro-ducer, Russian firm VSMPO-Avisma, has dropped to around 30,000t from 42,000t in 2012, McCoy said. The company is not fully integrated and relies on imports of raw material ilmenite, from Ukraine and Australia. But VSMPO-Avisma plans to invest $300mn-400mn to develop the Centralnoye titanium-zircon sands deposit in Russia to provide a local source of ore.

Japan's Osaka Titanium is running slightly below 2012 production of 40,000t, while fellow Japanese producer Toho Titanium has output of around 32,000t, McCoy said. Toho Titanium commissioned its Wakamatsu plant in 2011 but cut output at Chigasaki last year. Japan's exports dropped to 16,000t last year, from 19,000t in 2013 and 31,000t in 2012, in line with lower production.

But Toho Titanium has entered a joint venture to build a titanium sponge plant in Saudi Arabia with titanium dioxide manufacturer Cristal Global and Saudi state-owned Tasnee. The 15,600 t/yr facility is under construction and target-ing first production in late 2017. It will benefit from lower energy costs, compared with Japan, and from associated infrastructure at the existing Yanbu industrial complex.

TZMI estimates US sponge production increased to 12,000-15,000 t/yr last year from 9,000-10,000 t/yr three years earlier — official industry figures are not released, particularly following industry consolidation. “US capacity is around 24,000 t/ty and operations are running at 50pc of capacity,” McCoy said.

TZMI puts China’s titanium sponge production at 68,000t, an estimated 45pc utilisation rate of its 150,000 t/yr capac-ity. Capacity has raced ahead of output, growing by 50pc in the past 10 years to account for 40pc of the global produc-tion capacity.

China exported 6,000t of titanium sponge in last year, compared with 4,000t in 2013 and 5,000t in 2012, McCoy said.

Under Beijing's 12th five-year plan, China is phasing out titanium sponge plants with less than 5,000 t/yr of capac-ity and is targeting reduced electricity costs of 26 MW/t of sponge. Any new Chinese plant must have a capacity of at least 10,000 t/yr.

titanium: VsmPO to increase machined outputRussian titanium producer VSMPO-Avisma is increasing the proportion of finished machined forgings and stampings in its

5

5.2

5.4

5.6

5.8

6

6.2

14 Apr 15 28 May 15 14 Jul 15 27 Aug 15 13 Oct 15

Titanium sponge TG-Tv 10x30mm du Rotterdam, $/kg

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 12 of 24

titanium mill product mix.The company is on course to produce between 28,500-

29,000t of titanium mill products this year, executives told Argus.

The company reported output of 29,264t of titanium mill products in 2014, up from 28,855t the previous year. While the company’s melting volumes are rising from year to year, the mill product volumes this year reflect an increased pro-portion of finished machined forgings and stampings in the product mix.

VSMPO is the leading supplier of titanium to both Boeing and Airbus aircraft programmes and operates a joint venture with Boeing — Ural Boeing Manufacturing — in Verkhnaya Salda, which machines titanium parts for Boeing aircraft. The company is also close to completing construction on its own new machining plant in the Titanium Valley special economic zone developed around its works in Russia’s Sverd-lovsk region, which will serve a number of customers.

VSMPO's titanium sponge plant Avisma in Berezniki produces its own magnesium for use as reductant and has previously exported a significant surplus to overseas mar-kets. But, with the magnesium market dominated by Chinese production, Avisma's magnesium output has been reduced to only about 6,000t/yr, most of which is consumed internally, the company said.

Meanwhile, after suspending them earlier in the year, Avisma has resumed imports of the titanium raw material ilmenite from Ukraine, where the control of Volnogorsk min-ing complex passed from private operator Group DF to state owned United Mining Chemical Company.

The titanium trade between Russia and Ukraine and between Russia and the US has continued despite politi-cal frictions and US and EU sanctions particularly affecting due-purpose technology supply to Russia. Last month the US

government extended sanctions related to arms non-prolif-eration in Syria to Russian state arms company Rosoboronex-port, a subsidiary of state corporation Rostec which also holds a minority stake in the titanium producer. But neither the US nor the EU have extended sanctions to Rostec-affiliat-ed non-defence companies.

Boeing and VSMPO-Avisma told Argus that their long-term contracts and new business have not been impacted by sanc-tions. “We are taking steps to mitigate any risk to our supply chain, but VSMPO remains an important supplier to Boeing commercial aircraft programs,” William Shaffer, Boeing’s director material and standards, said.

Titanium: Alcoa signs $1.1bn Lockheed contractUS aluminum producer Alcoa was awarded a contract to pro-vide titanium for Lockheed Martin's F-35 Lightning II aircraft program at an estimated value of $1.1bn.

The company will supply titanium for the airframe struc-tures of all three F-35 variants from 2016 to 2024.

Under a different contract, the company will forge the largest titanium bulkheads for the F-35A conventional takeoff and landing (CTOL) aircraft at facilities in Cleve-land, Ohio. Approximately 75pc of F-35s produced today are CTOLs. Bulkheads are structural components that divide the aircraft into compartments.

Lockheed Martin aims to produce 13 aircraft per month by the mid-2020s, up from an average of three aircraft per month in 2014.

Alcoa produces aluminum bulkheads, aluminum die forg-ings, and fasteners for COTL craft, in addition to aluminum and titanium vane box assemblies that direct airflow in vertically landing F-35s.

Yesterday, Alcoa appointed Roy Harvey as president of global primary products, which follows last week's an-nouncement that the company plans to divide itself into two publicly traded firms. One half will focus on primary alumi-num and the other will focus on value-added products.

Tiantium: Sierra Rutile warns of rutile shortfallGlobal demand for high-grade titanium mineral rutile is expected to outpace supply, the chief marketing officer of London-based mining company Sierra Rutile, Derek Folmer, told the ITA Titanium 2015 conference in Orlando.

Declining reserves and grades will constrain future avail-ability of rutile, the titanium oxide mineral favoured as a high-grade raw material by pigment and titanium metal industries, he said.

The warning comes as the company, which mines tita-

48,000

48,500

49,000

49,500

50,000

50,500

15 Apr 15 29 May 15 14 Jul 15 28 Aug 15 13 Oct 15

Titanium sponge 99.7% Ti ex-works China, Yn/t

mARkeT newS And AnALySiS

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 13 of 24

nium minerals in Sierra Leone, targets the metals industry for some of its 2016 sales, having contracted all its planned sales in 2015, and is working to boost production. Sierra Ru-tile recently started construction on the Gangama dry mine, and first production is expected in June 2016, Folmer said.

It will ultimately boost production capacity at Sierra Rutile from 125,000 t/yr of rutile to in excess of 160,000 t/yr. This is the latest step in the company's transition from dredging to more economic dry mining in Sierra Leone, but lower-quality grades are a challenge.

“Whereas we used to mine 3-4pc rutile, now we work with half of that rutile content, which means we have to mine twice as much raw material to process as much rutile,” Folmer said. “These lower-quality deposits require more selective mining methods, more investment in processing capability.”

Demand for titanium dioxide (TiO2) supply will outpace demand, Sierra Rutile said, and vertical integration by pig-ment companies is driven by a desire to lock in raw material supply. Almost a third of today's rutile supply is locked into long-term contracts by TiO2 pigment companies, Folmer said. New demand is expected to emerge over the next 3-5 years as China's chloride TiO2 industry develops.

Around 745,000t of rutile was produced worldwide last year, with Australia accounting for half of this. Only three companies — UK-Australian group Rio Tinto, Australia-based Iluka and Sierra Rutile — have the capacity to produce more than 100,000 t/yr of rutile, and most of this supply is sourced from mines that have less than 15 years of life left.

Supply is expected to barely maintain existing levels and is likely to plateau at around 800,000 t/yr in 2016-18, Folmer said. Supply from Africa, including Sierra Leone, will increase while Australian supply will depend on investment decisions.

Sierra Rutile is targeting output of 150,000t next year and 160,000t in 2017, and hopes to raise production to 200,000t in 2018. But without investment its production is likely to decrease from 2016-17, Folmer said.

Rutile, in preference to the bulk iron-titanium oxide ore ilmenite, is especially important for companies concerned about the supply of strategic high-purity material. Rutile is high in TiO2 and low in tin, which is vital for aerospace ap-plications, and low in alkali and trace metals, both impor-tant for chlorination and the subsequent quality of titanium tetrachloride (TiCl4), the intermediate metal feedstock. It also has low radioactivity, which is important for safe opera-tion of titanium sponge plants.

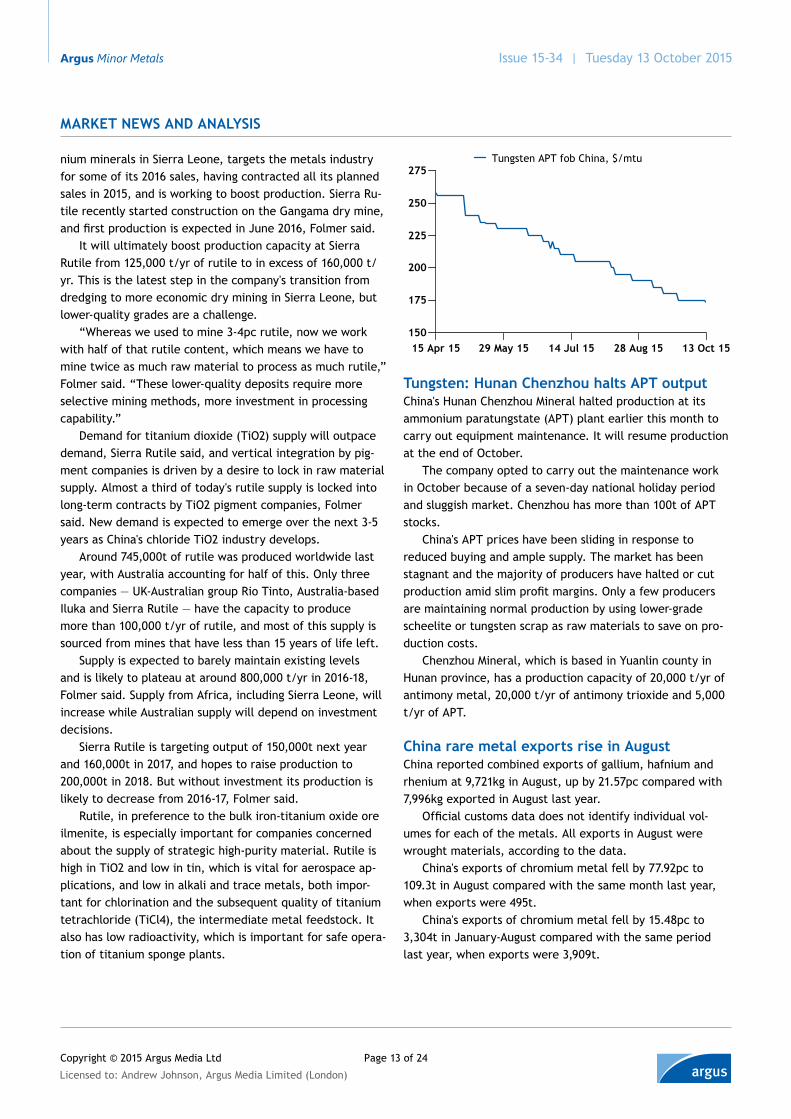

Tungsten: Hunan Chenzhou halts APT outputChina's Hunan Chenzhou Mineral halted production at its ammonium paratungstate (APT) plant earlier this month to carry out equipment maintenance. It will resume production at the end of October.

The company opted to carry out the maintenance work in October because of a seven-day national holiday period and sluggish market. Chenzhou has more than 100t of APT stocks.

China's APT prices have been sliding in response to reduced buying and ample supply. The market has been stagnant and the majority of producers have halted or cut production amid slim profit margins. Only a few producers are maintaining normal production by using lower-grade scheelite or tungsten scrap as raw materials to save on pro-duction costs.

Chenzhou Mineral, which is based in Yuanlin county in Hunan province, has a production capacity of 20,000 t/yr of antimony metal, 20,000 t/yr of antimony trioxide and 5,000 t/yr of APT.

China rare metal exports rise in AugustChina reported combined exports of gallium, hafnium and rhenium at 9,721kg in August, up by 21.57pc compared with 7,996kg exported in August last year.

Official customs data does not identify individual vol-umes for each of the metals. All exports in August were wrought materials, according to the data.

China's exports of chromium metal fell by 77.92pc to 109.3t in August compared with the same month last year, when exports were 495t.

China's exports of chromium metal fell by 15.48pc to 3,304t in January-August compared with the same period last year, when exports were 3,909t.

150

175

200

225

250

275

15 Apr 15 29 May 15 14 Jul 15 28 Aug 15 13 Oct 15

Tungsten APT fob China, $/mtu

mArkeT news And AnAlysis

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 14 of 24

Cobalt imports fallChina's cobalt concentrate imports declined in August,

with the devaluation of the yuan in the middle of the month increasing the cost of imports at the same time as consumer demand for the metal was weak.

China imported 17,939t of cobalt concentrate in August, down by 1.59pc compared with 18,228t a year earlier. Prices averaged $1,722/t, down by 16.16pc on the year. China imported 160,276t of cobalt concentrate in the first eight months of 2015, up by 32.86pc compared with 120,633t in the same period last year.

Molybdenum: American CuMo to drill in IdahoCanadian molybdenum producer American CuMo Mining has received clearance to undertake exploratory molybdenum, copper and silver drilling at its CuMo project in the US state of Idaho.

The Vancouver-based company has put forward plans to start drilling in an area of 3,000 acres in the Boise National Forest, hailing the site as the world's largest un-mined mo-lybdenum project.

Environmental groups have opposed plans for an open pit mine at the site, fearing it will lead to contamination of a local river.

Authorities said permits issued for use at the Boise County site only cover exploration drilling and do not include mining, for which the company would have to seek separate authorisation.

Molybdenum: Sierra output growth slowerPolish mining company KGHM's Sierra Gorda mine in Chile produced 618t (1.36mn lbs) of molybdenum concentrate in August, data from Chilean copper commission Cochilco show.

The mine, in Chile's northern Atacama desert region, started producing in April. It produced 3,164t in its first five months of operation, an average rate of 633 t/month. The highest monthly output was in July, when Sierra Gorda produced 986t.

Production in the nine months since April could hit 5,695t if the mine continues output at its current rate, or an an-nualised 7,594t.

Production was forecast at 50mn lbs/yr (23,000 t/yr) in the first five years, equivalent to about 8.6pc of global output based on the 583.7mn lbs total production in 2014. Output is forecast to fall to around 20mn lbs/yr for the remainder of its mine life of 20 or more years.

Sierra Gorda would need to produce around 1,900 t/month to meet its 50mn lbs/yr target. But given production

levels in April-August, it would need to raise output to 2,792 t/month from September 2015 to March next year to reach the target in its first year.

But this would be difficult after prices hit a 12-year low of $4.80-4.90/lb on 8 October, almost half levels of $9.05-9.15/lb at the start of 2015. The decline has prompted a number of secondary and by-product molybdenum producers to cut or suspend output, and could have a similar effect on primary production.

Molybdenum: Thompson Creek sells 3mn lb Colorado-based mining firm Thompson Creek Metals, which has idled its North American molybdenum mines because of low prices, sold 3mn lb of molybdenum concentrate in the third quarter of this year.

Of that total, 600,000lb came from inventory at Thomp-son Creek's mines, with 2.4mn lb from material sourced from third parties. It was the third successive quarter in which Thompson Creek posted sales-only figures for molybdenum processed at its Langloth plant in Pennsylvania, US.

The company shipped 4.3mn lb in the first quarter of this year and 2.2mn lb in the second quarter, compared with 6.7mn lb in the third quarter of 2014.

The firm's Thompson Creek mine in Idaho, US, was put on care and maintenance at the end of last year and the sus-pended Endako mine in British Columbia, Canada, followed suit in June. The mines produced a combined 26.3mn lb in 2014, accounting for 4.5pc of total global output of 583.7mn lb.

Roasted molybdenum concentrate prices have slumped to 12-year lows of $4.80-4.90/lb from $9.05-9.15/lb at the start of this year.

With its molybdenum mines off line, Thompson Creek is concentrating on ramping up production at its Mt Mil-

4.00

5.00

6.00

7.00

8.00

9.00

14 Apr 15 28 May 15 14 Jul 15 27 Aug 15 13 Oct 15

Molybdenum oxide min 57% Mo du Rotterdam , $/lb of Mo

MArkeT newS And AnAlySIS

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 15 of 24

ligan copper-gold mine in British Columbia. Copper produc-tion reached 16.3mn lb in the third quarter, in addition to 53,800oz of gold. Sales of copper totalled 24.4mn lb with gold sales at 75,400oz.

Ford to invest $1.8bn in China smart carsUS car maker Ford Motor will invest 11.4bn yuan ($1.8bn) to research and develop smart cars in China, the company said.

Under the five-year investment, Ford plans to research how to add greater smartphone connectivity, autonomous driving and other smart car features to its Chinese vehicles.

The investment will allow Ford to build up its research and development capabilities in the country — especially at its Nanjing Research and Engineering Center — and will help Ford create more vehicles in China, the company said.

Many minor metals and alloys, such as magnesium, ferro-manganese, ferro-silicon, antimony, cadmium, vanadium and molybdenum, are used in car production, along with rare earths. And smart car features require increased use of electronic metals.

With the introduction of these vehicles and technologies, Ford said that by 2020 its customers are expected to reduce fuel consumption by more than 200 litres/yr compared with 2015.

Molybdenum: Glencore to sell two copper minesSwitzerland-based mining and commodities trading firm Glencore is starting the process to sell its wholly-owned Co-bar copper mine in Australia and Lomas Bayas copper mine in Chile.

Glencore has started the sale process in response to receiving a number of unsolicited expressions of interest for these mines from various potential buyers, the company said. Glencore is seeking to reduce its debt and indicated last month that it may divest some of its non-core assets following a cut back on its copper and zinc production amid low prices.

The Lomas Bayas open pit copper mine is located in the Atacama desert in Chile, 120km northeast of the port of Antofagasta. The low-grade copper ore mined at this facil-ity is processed by heap leaching and converted to copper cathode after processing through a solvent extraction and electrowinning (SX-EW) plant. The Lomas Bayas operation produces approximately 75,000 t/yr of copper cathode.

Cobar, which is located in central western New South Wales, Australia, comprises a high-grade underground cop-per mine and a concentrate plant. The plant throughput is approximately 1.1mn t/yr of ore and it produces approxi-

mately 50,000 t/yr of copper in concentrate.The start of the sale process “will allow potential buyers

to bid to purchase either one or both of the mines and may or may not result in a sale”, Glencore said.

The Hong Kong and London-listed company requested a trading halt in Hong Kong with today’s announcement and plans to issue an update only when a sale of its copper as-sets is agreed or disclosure is otherwise required.

The news comes on the back of Glencore’s decision last month to idle copper production at its [Katanga and Mo-pani](https://direct.argusmedia.com/newsandanalysis/arti-cle/1102940) operations in the Democratic Republic of Congo and Zambia, respectively, over an 18-month period with a loss of 400,000t of copper cathode equivalent produc-tion and 3,000t of cobalt. Glencore last week announced a 500,000 t/yr [cut to zinc production](https://direct.argusme-dia.com/newsandanalysis/article/1116510) across its opera-tions in Australia, South America and Kazakhstan.

Tellurium: Singulus cuts 2015 business forecastGerman optical disc and solar product manufacturer Singulus Technologies has revised its business forecast for 2015 as demand for Blu-Ray discs — one of its key sectors — falls.

Conversations with key customers in the sector are continuing but the company expects that new orders of its Bluline II technology are unlikely in the near future. Develop-ment of new production technology for the Ultra-HD Blu-ray disc is not expected. Tellurium is a key component of the media layer of optical discs. Falling demand from this sector may weigh on prices for the metal, which are already falling on the back of low demand from consumers.

But Singulus expects a significant rise in revenues in its solar division, with sales in this sector exceeding €57mn ($64.4mn) in the first half of this year.

Singulus is working on larger copper-indium-gallium-sele-nide (CIGS) projects, chief executive Stefan Rinck said.

Kariba levels impact Zambia, Zimbabwe minesLow water levels at the Kariba dam are causing major problems for the mining industries in Zambia and Zimba-bwe, which rely on the hydropower facility for much of their power supply.

With the dam’s level at less than 30pc, compared with 70pc at the same time last year, its ability to produce around 1,600MW of electricity for two power plants — one each in Zambia and Zimbabwe — has been seriously af-fected. Power utilities in both countries are urging mining companies to cut their power usage by 25-30pc.

MarKeT newS and analySiS

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 16 of 24

market news and analysis

The drawdown of water for power generation at the dam has exceeded agreed threshold levels, causing water levels to drop to historically low levels, the Zambia Engineers Institute said.

Copper producers in Zambia have had their power supply cut by up to 30pc over the past few months, while the Zim-babwean government this week said platinum and chrome producers in the country need to reduce their consumption by 25pc.

The rainy season, which runs from October to April, is likely to improve dam levels, but long-range weather forecasts suggest a hot, dry summer for much of southern Africa, with below average rainfall.

South Africa is experiencing its worst drought for two decades but its mining industry is reliant on coal-fired power plant rather than hydropower.

Zimbabwe’s power shortage is exacerbated by the fact that two power plants are off line for maintenance, reducing grid capacity.

Also of concern for Zimbabwe and Zambia, respectively Africa’s second-largest chrome and copper producers, is the physical state of the Kariba dam, which was opened in 1959.

The Zambezi River Authority has over the past couple of years warned that the dam’s bedrock is eroding. The dam is adjacent to Lake Kariba, the world’s largest man-made lake, stretching 280km in length. There are concerns that if the dam wall bursts, it would send massive amounts of water down the Zambezi river to Mozambique where it would destroy the Cahora Bassa dam, wiping out most of southern Africa’s remaining hydropower capacity.

Us rig count below 800 in current downturnThe US drilling rig count dipped below 800 for the first time in the current market downturn, in its seventh straight week of declines.

The total fell by 14 to 795 this week, oil field services provider Baker Hughes said. That is the weakest since the 776 seen in May 2002.

A prolonged weakness in the crude market that’s lasted a year is forcing producers to make even deeper cuts to their capital expenditure (capex) by pulling back drilling plans. In the latest example of producers hunkering down, Canadian independent Encana announced selling its Denver Julesburg (DJ) basin assets in Colorado for $900mn to lower debt and shore up its balance sheet.

The sale is part of a plan to focus operations "on our four most strategic assets" in the Permian and the Eagle Ford in Texas, Duvernay in western Canada and Montney in Alberta,

Canada, said chief executive Doug Suttles.The US rig count had recovered in end-August and early

September, from a previous trough of 857, in part driven by a recovery in prices in the second quarter. But those gains have all been wiped out as the market witnessed a double dip. It had risen to 885 on 21 August, at par with the highest since 22 May. The latest count shows the number dropping by 90 since then.

The count is now down by 59pc from last year's peak of 1,931 and 57pc lower than end-2014 levels. The number of rigs drilling for oil fell by nine to 605. Those drilling for gas fell by six to 189.

Metalsilluminating the markets

Market ReportingConsulting

Events

Exclusive discounts available for aluminium producers and China-based metal producers.

Book before 2 September to save €700argusmedia.com/Light-Metals

Argus European Light Metals 2015 The premier metals event for Aluminium, Magnesium, Silicon and Manganese professionals.

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 17 of 24

price indexes

Argus minor metals indexes (monthly averages)Month index Month index Month index Month index

Unit Oct 2015 low Oct 2015 high Sep 2015 final low Sep 2015 final high

electronic metals

Arsenic

Min 99% du Rotterdam $/lb 0.90 1.05 0.90 1.05

Min 99% fob US $/lb - - 0.95 1.15

Bismuth

Min 99.99% du Rotterdam $/lb 4.90 5.30 4.91 5.32

Min 99.99% fob China $/lb 5.15 5.45 5.06 5.42

Ingot min 99.99% fob US $/lb - - 4.73 5.22

Gallium

Min 99.99% fob China $/kg 135.00 160.00 140.56 163.89

Min 99.99% cif Main Airport $/kg 180.00 200.00 180.00 200.00

Germanium

Dioxide min 99.999% fob China $/kg 1,250.00 1,350.00 1,250.00 1,366.67

Dioxide min 99.99% du Rotterdam $/kg 1,145.00 1,195.00 1,145.00 1,195.00

Metal min 99.99% cif Main Airport $/kg 1,725.00 1,800.00 1,725.00 1,800.00

Dioxide min 99.999% fob China $/kg 1,250.00 1,350.00 1,250.00 1,366.67

Min 99.999% fob China $/kg 1,750.00 1,850.00 1,750.00 1,867.00

Indium

Min 99.99% du Rotterdam $/kg 232.50 292.50 267.78 315.56

Min 99.99% fob China $/kg 240.00 280.00 248.89 298.33

Ingot min 99.99% fob US $/kg - - 260.00 315.00

Selenium

Min 99.5% du Rotterdam $/lb 8.00 10.00 8.67 10.67

Min 99.5% fob US $/lb - - 8.42 10.67

Tantalum

Tantalite basis 30% Ta2O5 du Rotterdam $/lb Ta2O5 62.25 68.25 70.11 73.00

Min 99.8% du Rotterdam $/kg 318.75 332.50 322.22 340.56

Tellurium

Min 99.99% du Rotterdam $/kg 42.50 65.00 63.33 75.00

Min 99.95% fob US $/kg - - 60.00 85.00

Zirconium

Oxychloride 36% Zr(Hf)O2 fob China $/t 1,420.00 1,470.00 1,420.00 1,470.00

Battery metals

Antimony

Ingot min 99.65% fob China $/t 6,175.00 6,375.00 6,400.00 6,600.00

Min 99.65% cif US ports $/lb - - 3.00 3.17

Regulus grade II min 99.65% Sb du Rotterdam $/t 5,912.50 6,075.00 6,155.56 6,383.33

Regulus Trioxide grade min 99.65% Sb du Rotterdam $/t 6,062.50 6,162.50 6,261.11 6,455.56

Trioxide min 99.5% fob China $/t 5,475.00 5,775.00 5,655.56 5,922.22

Cadmium

Min 99.95% du Rotterdam $/lb 0.37 0.43 0.37 0.42

Min 99.95% cif India Rs/kg 103.00 110.00 103.00 110.67

Min 99.99% fob US $/lb - - 0.37 0.42

Min 99.99% du Rotterdam $/lb 0.39 0.44 0.39 0.45

Min 99.95% fob US $/lb - - 0.35 0.40

Min 99.99% cif India Rs/kg 114.00 118.00 114.67 118.67

Cobalt

Min 99.8% alloy grade du Rotterdam $/lb 12.80 13.50 12.80 13.49

Min 99.8% fob US $/lb - - 13.10 13.47

Min 99.6% chemical grade du Rotterdam $/lb 12.60 13.20 12.60 13.24

Min 99.3% Russian grade du Rotterdam $/lb 12.40 13.00 12.39 13.09

Min 99.3% fob US $/lb - - 12.77 13.02

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 18 of 24

price indexes

Light metals

Magnesium

Alloy min 90% Mg AZ91 fob China $/t 2,320.00 2,370.00 2,320.00 2,370.00

Min 99.9% ddp US $/kg 1.75 1.85 1.79 1.88

Min 99.9% du Rotterdam $/t 2,072.50 2,115.00 2,080.00 2,120.00

Min 99.9% fob China $/t 2,055.00 2,115.00 2,060.00 2,120.00

Powder 99.9% Mg 20-80 mesh fob China $/t 2,150.00 2,200.00 2,150.00 2,200.00

Manganese

Briquette 97% Mn fob China $/t 1,572.50 1,622.50 1,602.22 1,652.22

Electrolytic metal min 99.7% fob US $/lb 1.09 1.12 1.09 1.12

Flake min 99.7% fob China $/t 1,522.50 1,572.50 1,552.22 1,602.22

Flake min 99.7% du Rotterdam $/t 1,555.00 1,595.00 1,608.89 1,653.33

Lump 95% Mn fob China $/t 1,612.50 1,692.50 1,642.22 1,722.22

Silicon

5-5-3 min 98.5% Si fob China $/t 1,610.00 1,640.00 1,610.00 1,640.00

5-5-3 min 98.5% Si ddp Europe works €/t 2,000.00 2,050.00 1,984.44 2,050.00

5-5-3 min 98.5% Si ddp US $/lb 1.19 1.24 1.22 1.27

4-4-1 min 99% Si fob China $/t 1,750.00 1,780.00 1,750.00 1,780.00

4-4-1 min 99% Si ddp Europe works €/t 2,120.00 2,170.00 2,117.78 2,190.00

Titanium

Sponge TG-Tv 10x30mm du Rotterdam $/kg 5.13 5.30 5.59 5.67

Scrap 6Al 4V bulk weldable fob US $/lb 3.25 3.35 3.25 3.35

Scrap 6Al 4V clips fob US $/lb 2.95 3.05 2.95 3.05

Scrap grade 1 CP solids fob US $/lb 2.18 2.23 2.23 2.31

Scrap grade 2 CP solids fob US $/lb 1.88 1.98 2.11 2.18

Scrap grade 3-4 CP solids fob US $/lb 1.65 1.73 1.79 1.89

Scrap 6Al 4V turnings aero quality fob US $/lb 2.10 2.20 2.13 2.23

High-temperature metals

Chromium

(alumino-thermic) min 99% du Rotterdam $/t 7,950.00 8,525.00 8,144.44 8,677.78

Molybdenum

Oxide min 57% Mo du Rotterdam $/lb Mo 4.91 5.06 5.63 5.83

Oxide min 57% fob US $/lb 5.73 5.90 5.76 5.96

Rhenium

APR min 69.2% Re (basic grade) du Rotterdam $/kg Re 1,350.00 1,450.00 1,361.11 1,450.00

APR min 69.4% Re (catalyst grade) dp Rotterdam $/kg Re 2,600.00 2,750.00 2,600.00 2,750.00

Pellets min 99.9% Re dp Rotterdam $/lb 870.00 1,130.00 867.78 1,126.67

Tungsten

APT du Rotterdam $/mtu WO3 177.50 187.50 183.89 193.89

APT fob China $/mtu WO3 169.50 179.50 177.22 187.22

Carbide powder (3-4micron) fob China $/kg 24.38 25.38 25.46 26.44

Oxide (Yellow/Blue oxide) fob China $/t 17,950.00 18,950.00 18,722.22 19,722.22

Vanadium

Pentoxide fused flake min 98% du Rotterdam $/lb V2O5 2.80 3.15 3.30 3.60

Argus minor metals indexes (monthly averages)Month index Month index Month index Month index

Unit Oct 2015 low Oct 2015 high Sep 2015 final low Sep 2015 final high

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 19 of 24

price Summary

electronic metals price assessments13 Oct 8 Oct

unit Low High ± 8 Oct Low High ± 6 Oct

Arsenic

Min 99% du Rotterdam $/lb 0.90 1.05 - 0.90 1.05 -

Bismuth

Min 99.99% du Rotterdam $/lb 4.90 5.30 - 4.90 5.30 -

Bismuth min 99.99% ex-works China Yn/t 70,000 72,000 -2,500 72,000 75,000 -1,000

Bismuth min 99.99% fob China $/lb 5.00 5.30 -0.200 5.20 5.50 -

Gallium

Min 99.9999% ex-works China Yn/kg 1,150 1,250 - 1,150 1,250 -

Min 99.99% ex-works China Yn/kg 850 950 - 850 950 -

Min 99.99% fob China $/kg 135.00 160.00 - 135.00 160.00 -

Min 99.99% cif Main Airport $/kg 180.00 200.00 - 180.00 200.00 -

Germanium

Dioxide min 99.999% ex-works China Yn/kg 7,300 8,000 - 7,300 8,000 -

Dioxide min 99.999% fob China $/kg 1,250 1,350 - 1,250 1,350 -

Dioxide min 99.99% du Rotterdam $/kg 1,145 1,195 - 1,145 1,195 -

Metal (zone refined ingot) min 99.999% ex-works China Yn/kg 10,800 11,800 - 10,800 11,800 -

Metal min 99.99% cif Main Airport $/kg 1,725 1,800 - 1,725 1,800 -

Min 99.999% fob China $/kg 1,750 1,850 - 1,750 1,850 -

Indium

Min 99.99% du Rotterdam $/kg 230.00 290.00 - 230.00 290.00 -

Min 99.99% ex-works China Yn/kg 1,500 1,700 - 1,500 1,700 -

Min 99.99% fob China $/kg 240.00 280.00 - 240.00 280.00 -

Min 99% ex-works China Yn/kg 1,300 1,500 - 1,300 1,500 -

Selenium

Dioxide min 99% ex-works China Yn/kg 85.00 95.00 - 85.00 95.00 -

Min 99.5% du Rotterdam $/lb 8.00 10.00 - 8.00 10.00 -

Powder min 99.9% ex-works China Yn/kg 140.00 160.00 - 140.00 160.00 -

Tantalum

Tantalite basis 30% Ta2O5 du Rotterdam $/lb Ta2O5 60.00 65.00 -2.500 62.00 68.00 -

Min 99.8% du Rotterdam $/kg 315.00 325.00 -7.500 320.00 335.00 -

Tellurium

99.99% ex-works China Yn/kg 290.00 330.00 - 290.00 330.00 -

Min 99.99% du Rotterdam $/kg 40.00 60.00 -2.500 40.00 65.00 -

Zirconium

Fused zirconia 98.5% ZrO ex-works China Yn/t 18,800 19,000 - 18,800 19,000 -

Oxychloride 36% Zr(Hf)O2 ex-works China Yn/t 8,200 8,800 - 8,200 8,800 -

Oxychloride 36% Zr(Hf)O2 fob China $/t 1,420 1,470 - 1,420 1,470 -

Silicate 65% Zr(Hf)O2 ex-works China Yn/t 9,400 9,700 - 9,400 9,700 -

Sponge 99.4% Zr+Hf ex-works China Yn/kg 152.00 157.00 - 152.00 157.00 -

Licensed to: Andrew Johnson, Argus Media Limited (London)

Copyright © 2015 Argus Media Ltd

Issue 15-34 | Tuesday 13 October 2015 Argus Minor Metals

Page 20 of 24

price Summary

Battery metals price assessments13 Oct 8 Oct

unit Low High ± 8 Oct Low High ± 6 Oct

Antimony