are you counting the cost - advent...

TRANSCRIPT

Are you counting the cost of your legacy system?

Is your current system holding you back? Are you ready for regulatory changes?

Read our seven sure signs that you have outgrown your portfolio management system.

To find out more visit www.capitaltrends.com

EDITORIAL

FUNDS EUROPEGROUP EDITOR Nick Fitzpatrick Tel: +44 (0)203 178 5875 [email protected] DEPUTY EDITOR Stefanie Eschenbacher Tel: +44 (0)203 178 5876 [email protected] SENIOR staff writer George Mitton Tel: +971 (0) 4295 4618 [email protected] STAFF WRITER Alix Robertson Tel: +44 (0)203 427 5224 [email protected] EDITORIAL DIRECTOR Fiona Rintoul [email protected] TECHNOLOGY & OPERATIONS EDITOR Nicholas Pratt [email protected] SUB-EDITOR David Ryan ART DIRECTOR Lucy Erikson PUBLISHER Alan Chalmers Tel: +44 (0)203 178 5877 [email protected] GROUP SALES MANAGER David Wright Tel: +44 (0)203 178 5878 [email protected] EDITORIAL AND EVENTS COORDINATOR Paula Towner Tel: +44 (0)203 178 5874 [email protected] WEB MANAGER Steve Dimitrov Tel: +44 (0)20 3178 5873 [email protected] READERSHIP ADMINISTRATOR Michael Fennessy Tel: +44 (0)20 5347 5226 [email protected]

EDITORIAL ADVISORY BOARD Penelope Biggs Northern Trust, London Nadine Chakar BNY Mellon, New York Jean-Baptiste de Franssu Incipit, Brussels Peter Elam Håkansson East Capital, Stockholm Robert Parker Credit Suisse, London Todd Ruppert RTR International, London & Baltimore

SUBSCRIPTIONSubscription enquiries: [email protected] Delivery in Europe: €385 Delivery outside Europe: €495

3 funds-europe.com

JUST BECAUSE THERE IS SO LITTLE IN-HOUSE DEVELOPMENT THESE

DAYS, IT WOULD BE WRONG TO THINK

LEGACY SYSTEMS ARE A THING OF THE PAST.

SPOTTING THE SIGNSLegacy technology conjures up nostalgic images to me. An Atari games

console, playing Pac-Man and Pong to a soundtrack of 80s synth pop on

cassette – all washed down with lashings of ginger beer, made in a Soda

Stream, of course.

Heads of IT and chief operating officers do not look at legacy systems

quite so fondly, though. For many they are the stuff of nightmares, from

the realisation that the 20-year-old system at the heart of the firm’s

infrastructure can no longer go on, to the painful and prolonged process

of replacing that unique piece of technology, specifically designed for

the firm, with something from a third-party vendor.

So perhaps I should not have been surprised when – during the panel

debate reported on page 16 – I asked if we should mourn the apparent

demise of these one-off systems, and the response was an overwhelming

‘no’. There is nothing romantic in designing your own software, I was told.

But just because there is so little in-house development, it would be

wrong to think that legacy systems are a thing of the past. Technology

moves at such a quicker rate than it used to, rendering software as

‘legacy’all the sooner.

Many vendors are releasing two updates a year and have to ensure

that their clients keep up to speed with new versions, which can be

hard to do when the old system appears to be fine. We are now seeing

this in personal computing with Microsoft’s decision to stop supporting

Windows XP.

Legacy issues will always be there, even in an outsourcing relationship.

What is important for asset managers and their operations teams is that

they are able to spot the signs of impending legacy and are prepared

for the necessary changes. The following report is designed to help you

identify these signs and give you some ideas about how to replace any

outdated technology.

Nicholas Pratt

Editor, technology and operations

funds europePublished by Funds Europe Limited288 BishopsgateLondon EC2M 4QPTel: +44 (0)203 178 5872Fax: +44 (0)203 178 4002© Funds Europe Limited, 2014Total average net circulation 10,257Audit period 1st July 2012 - 30th June 2013

ISSN 1477-4453

Printed by Buxton Press

The views expressed in Funds Europe do not necessarily coincide with the views of the publishers. Although the publishers have made every effort to ensure the accuracy of the information contained in this publication, neither Funds Eu-rope Limited nor any contributing author can accept any legal responsibility whatsoever for any consequences that may arise from errors or omissions contained in the publication or from acting on any advice given. In particular, this publication is not a substitute for professional advice on a specific transaction.

4

CONTENTS

Spring 2015

5 funds-europe.com

THE BIGGEST PROBLEM WITH LEGACY TECHNOLOGY IS ACTUALLY REPLACING IT.

Steve Young, Citisoft

06 SURVEYFunds Europe’s inaugural survey of legacy

systems offers an in-depth study of how legacy

technology is used and the industry’s attitudes

towards outsourcing and cloud computing

14 SPONSORED PROFILEFunds Europe talks to Hakan Valberg about the

vendor experience of moving clients from their

legacy systems.

18 ROUNDTABLEAfter discussing how to identify a legacy system

and deal with its operational challenges, our

experts contemplate what the IT department of

the future might look like

26 INTERVIEWAn asset manager’s operations head talks about

the legacy challenges of days gone by and the

present-day strategies – such as outsourcing –

designed to avoid such issues in the future

18PAG

E

2618

18

funds-europe.com

6 Spring 2015

SURVEY

7funds-europe.com

Funds Europe sought the views of European asset managers in December with the first comprehensive survey on legacy systems. The results reveal just how much of a problem outdated technology poses.

OUT OF TIME

operational problems asset

management firms face: the state

of their legacy systems and how

best to replace them.

In all, 67 executives responded.

As well as heads of IT and chief

operational officers, these

included managing directors and

chiefs of staff, lending weight to

the argument that, far from being

limited to technology teams,

legacy issues are now boardroom

concerns too.

The questions are grouped

into three distinct categories.

The first of these involves firms’

operational strategies and

the nature of their planned IT

investment; the second examines

the prevalence of legacy systems,

the operational problems they

create and the economics of

replacing them; and the final

section looks at the alternatives

to legacy systems.

The results show that legacy

systems are still present in more

than half of asset management

firms and are widely

acknowledged to be a problem

– not so much in terms of their

performance, but rather their

lack of compatibility with other

systems and the increasing cost

of maintenance.

Conscious of software’s

diminishing shelf life, it seems

that more and more firms

are considering alternative

approaches to in-house

installation such as outsourcing

and cloud computing.

Fears over data security and

the immaturity of suppliers is

holding back wider adoption –

but as legacy issues come to a

head, many firms may be forced

to overcome such concerns.

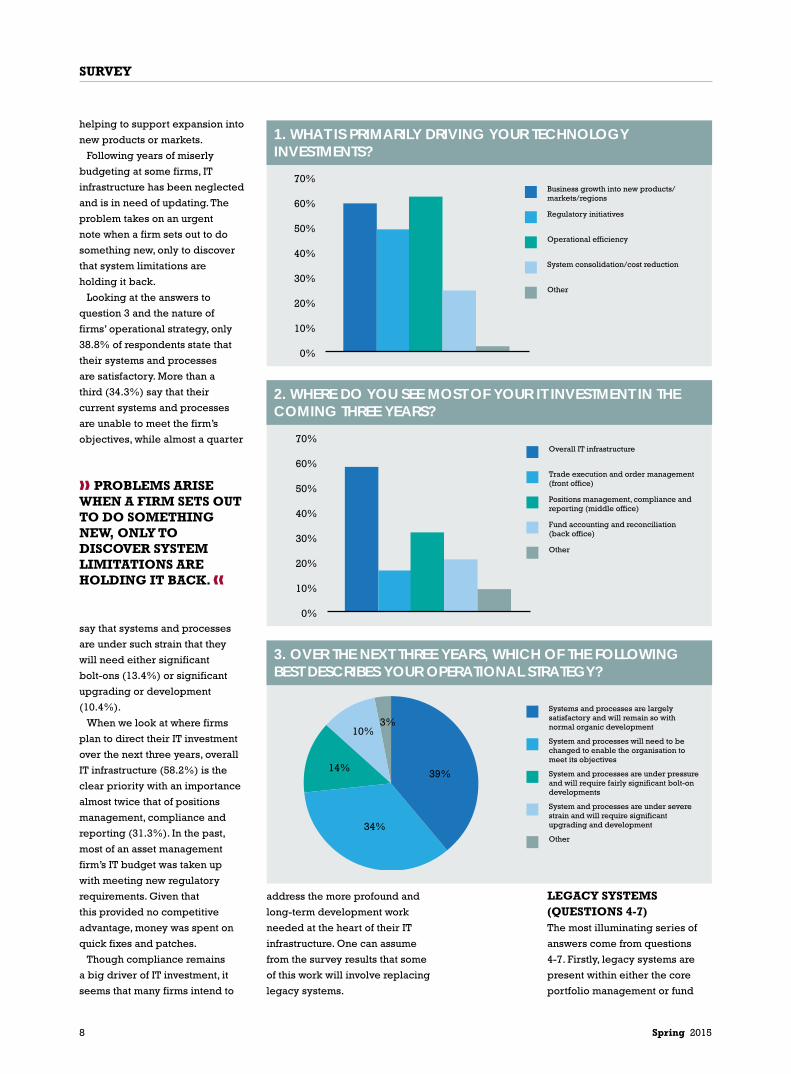

OPERATIONAL STRATEGY (QUESTIONS 1-3)According to respondents,

the primary drivers for firms’

technology investments are more

or less evenly spread between

operational efficiency (63%) and

business growth (59.7%), with

regulatory initiatives (49.3%)

slightly behind and system

consolidation/cost reduction

(23.9%) trailing further back.

These figures support what we

have heard anecdotally over the

past 12 months – that the focus

on cost-cutting and compliance,

which has dominated budgets

since the start of the financial

crisis, is finally fading.

Instead, firms are now devoting

the majority of their IT investment

into more positive channels –

either technology improvement

or new product development and

LEGACY SYSTEMS ARE STILL PRESENT IN MORE THAN HALF OF ASSET MANAGEMENT FIRMS AND ARE WIDELY ACKNOWLEDGED TO BE A PROBLEM.

LEGACY SYSTEMS HAVE long

been the stuff of nightmares for

asset managers’ IT departments.

When the term was originally

coined, ‘legacy’ referred to

a 20-year-old system that

was impenetrable to all but

the individual who designed

it. That person had left the

company some time ago, but in

the meantime, the system had

become embedded in the heart

of the IT infrastructure, lodged

like a bullet in the cranium. You

knew it should be removed, but

worried that the process could

trigger a fatal haemorrhage.

Things may be somewhat

different in 2015 with the rise

in outsourcing and with cloud

computing starting to gain

traction among asset managers.

But legacy issues have not

disappeared. There are still

four or five-year-old systems

that are no longer supported

by the vendor – and like a

household appliance for which

you can no longer obtain parts,

these need to be replaced before

they break down irreparably.

And as if that weren’t worrying

enough, the pace of technological

advances means that software

has an ever-decreasing shelf life,

granting systems the unenviable

‘legacy’ tag all the sooner.

Issues such as these have

prompted an inaugural survey

designed to shed light on one of

the biggest and most persistent

8 Spring 2015

SURVEY

LEGACY SYSTEMS (QUESTIONS 4-7)The most illuminating series of

answers come from questions

4-7. Firstly, legacy systems are

present within either the core

portfolio management or fund

address the more profound and

long-term development work

needed at the heart of their IT

infrastructure. One can assume

from the survey results that some

of this work will involve replacing

legacy systems.

helping to support expansion into

new products or markets.

Following years of miserly

budgeting at some firms, IT

infrastructure has been neglected

and is in need of updating. The

problem takes on an urgent

note when a firm sets out to do

something new, only to discover

that system limitations are

holding it back.

Looking at the answers to

question 3 and the nature of

firms’ operational strategy, only

38.8% of respondents state that

their systems and processes

are satisfactory. More than a

third (34.3%) say that their

current systems and processes

are unable to meet the firm’s

objectives, while almost a quarter

say that systems and processes

are under such strain that they

will need either significant

bolt-ons (13.4%) or significant

upgrading or development

(10.4%).

When we look at where firms

plan to direct their IT investment

over the next three years, overall

IT infrastructure (58.2%) is the

clear priority with an importance

almost twice that of positions

management, compliance and

reporting (31.3%). In the past,

most of an asset management

firm’s IT budget was taken up

with meeting new regulatory

requirements. Given that

this provided no competitive

advantage, money was spent on

quick fixes and patches.

Though compliance remains

a big driver of IT investment, it

seems that many firms intend to

1. WHAT IS PRIMARILY DRIVING YOUR TECHNOLOGY INVESTMENTS?

2. WHERE DO YOU SEE MOST OF YOUR IT INVESTMENT IN THE COMING THREE YEARS?

3. OVER THE NEXT THREE YEARS, WHICH OF THE FOLLOWING BEST DESCRIBES YOUR OPERATIONAL STRATEGY?

PROBLEMS ARISE WHEN A FIRM SETS OUT TO DO SOMETHING NEW, ONLY TO DISCOVER SYSTEM LIMITATIONS ARE HOLDING IT BACK.

70%

60%

50%

40%

30%

20%

10%

0%

Business growth into new products/markets/regions

Regulatory initiatives

Operational efficiency

System consolidation/cost reduction

Other

70%

60%

50%

40%

30%

20%

10%

0%

Overall IT infrastructure

Trade execution and order management (front office)

Positions management, compliance and reporting (middle office)

Fund accounting and reconciliation (back office)

Other

Systems and processes are largely satisfactory and will remain so with normal organic development

System and processes will need to be changed to enable the organisation to meet its objectives

System and processes are under pressure and will require fairly significant bolt-on developments

System and processes are under severe strain and will require significant upgrading and development

Other

3%

39%

34%

14%

10%

9 funds-europe.com

accounting platforms in almost

three-quarters (73%) of firms.

There may, though, be some

scepticism about the 16% of

respondents who say they have

no legacy systems at all.

While some companies may

be in denial about the state of

their IT, there are also a number

of start-ups that have had the

benefit of starting with a blank

slate, either bringing in new

technology or outsourcing the lot.

Of course, it could be that a

number of firms are sufficiently

well-organised to have ensured

that their core platforms are free

of legacy, limiting the blight of

outdated systems to periphery

platforms and technology.

Then there is the other

possibility, indicated by the 7.5%

of people who answered ‘don’t

know’ to question 4, that people

simply don’t recognise a legacy

system when they see one.

Looking at the operational

challenges created by legacy

systems, it is clear that the

most pressing issue is not a

lack of performance (cited by

only 16.4%). Instead, many of

the challenges reflect firms’

relationships with vendors –

either difficulty in updating

systems (28.4%) or the high cost

of maintenance.

The most commonly cited

challenge was the incompatibility

of legacy systems with other

technology (40.3%). This

provoked an additional comment

from one respondent, who laid

the blame for legacy issues at the

door of vendors rather than users.

4. TO WHAT EXTENT DO YOU EMPLOY LEGACY SYSTEMS WITHIN YOUR CORE PORTFOLIO MANAGEMENT OR FUND ACCOUNTING PLATFORM?

THE MOST COMMONLY CITED CHALLENGE WITH LEGACY SYSTEMS IS INCOMPATIBLITY WITH OTHER TECHNOLOGY.

Not at all

Slightly

A lot

Don’t know

Other

3%16%

48%

25%

8%

10 Spring 2015

SURVEY

“If a client has a legacy system, it

is the provider’s role to adapt to

the system and not to change it.

The more you, the supplier, push

against the legacy system, the

more your clients will become

frustrated by the inability of

the new system to provide

information with the clarity of

the old system.”

One is tempted to say:

“Good luck with that,” but

such a comment underlines

the challenge facing vendors

and clients when replacing

legacy systems with a third-

party alternative. As well as

the operational risk that the

replacement process will be

highly disruptive and won’t

perform as well or consistently

as the old one, there is also an

economic challenge.

Nonetheless, the survey results

suggest most firms are confident

that the replacement will prove

to be economically positive.

When asked, almost half of those

surveyed (49%) accept that there

is an initial cost involved but that

it will provide a return in the long

term. In addition, 19.4% believe

that the decreasing cost of third-

party software is making the

process ever more cost-effective.

OUTSOURCING OPTIONS (QUESTIONS 8-9)The alternative to installing

replacement systems is to

outsource. As question 6 tells us,

more than half are taking this

option with either a completely

outsourced or hosted model

(22.4%) or a part-outsourced

model (34.3%). The response

to question 8 suggests that the

outsourcing trend is about to

grow stronger, with the majority

(58.2%) set to increase their

spending on outsourcing or

hosted solutions over the next

three years and only a small

minority (7.5%) likely to reduce

this spend.

Looking more specifically at

5. WHAT IS THE BIGGEST OPERATIONAL CHALLENGE CREATED FROM LEGACY SYSTEMS?

6.IF YOU ARE EXPERIENCING CHALLENGES WITH IN-HOUSE LEGACY SYSTEMS, WHAT SOLUTIONS ARE YOU CONSIDERING?

7. HOW DO YOU VIEW THE ECONOMICS OF REPLACING LEGACY SYSTEMS WITH THIRD-PARTY SYSTEMS?

MOST FIRMS ARE CONFIDENT THAT REPLACING LEGACY SYSTEMS WILL PROVE TO BE ECONOMICALLY POSITIVE.

50%

40%

30%

20%

10%

0%

Difficulty in updating

Lack of performance

Incompatibility with other systems

High cost of maintenance

Other

Investment in on-premise third party systems, you have a controllable cost structure and you simply have to manage the vendor relationships.

A completely outsourced or hosted approach to IT services where you don’t have any infrastructure or hardware to worry about.

A part-outsourcing model to third party service provider(s)

We don’t employ legacy systems

Other

6%22%

34%

28%

9%

An initial cost that will be provided in the long-term

More expensive but necessary to maintain competitiveness

Becoming more cost –effective all the time due to the decreasing cost of third party software

Other

6%

49%

25%

19%

11 funds-europe.com

where exactly this outsourcing

investment will be directed, the

back office (43.3%) remains

the main destination, but it is

clear that other functions are

increasingly considered to be

suitable for outsourcing. These

include risk management,

investment research, portfolio

management/daily NAV

processing and even front-office

functions such as trading (6.0%)

that were previously considered

too proprietary to be left in the

hands of a third party.

CLOUD COMPUTING (QUESTIONS 10-13)It’s apparent that firms are

reconsidering which processes

are a genuine core competency

(to be kept in-house and as

proprietary as possible) and

which are commoditised

and non-competitive. These

considerations might be further

influenced by the maturity of

cloud-based services. Indeed,

the final section of the survey

suggests that asset managers are

warming to the idea of storing

data in the cloud.

According to question 10,

although more than half of the

respondents do not currently use

cloud solutions for any part of

the transaction life-cycle process

(52.2%), question 11 shows us

that a similar percentage (44.8%)

do intend to invest in cloud-

based technology over the next

three years. More than a third

(35.8%) are unsure, leaving less

than a fifth (19.4%) who have no

plans to do so at all.

When it comes to data types,

there are similar if not greater

levels of uncertainty about how

and where cloud technology

would be deployed. For

example, while almost half of

the respondents (44.8%) are

comfortable putting external or

market data into the cloud, an

equal number are unsure what

sort of data they would trust to it.

8. TO WHAT EXTENT DO YOU SEE YOUR SPEND ON OUTSOURCED TECHNOLOGY SOLUTIONS/HOSTING BY THIRD PARTIES CHANGING OVER THE NEXT THREE YEARS

9. IF YOU ARE WILLING TO OUTSOURCE, WITHIN WHAT AREAS WOULD YOU BE MOST LIKELY TO OUTSOURCE TO THIRD PARTIES?

10: DO YOU TODAY USE CLOUD TECHNOLOGY SOLUTIONS TO SUPPORT THE TRANSACTION LIFE-CYCLE PROCESS?

THE BACK OFFICE REMAINS THE MAIN DESTINATION FOR OUTSOURCING INVESTMENT, BUT OTHER FUNCTIONS ARE INCREASINGLY CONSIDERED TO BE SUITABLE.

70%

60%

50%

40%

30%

20%

10%

0%

Increasing

No change

Decreasing

Don’t know

50%

0%

Investment research

Accounting and reconciliation

Regulatory compliance and reporting

Trading

Risk management

Portfolio/Fund Management – daily NAV processing

Other

No

Yes

Partly

29%

19%

52%

12

SURVEY

Spring 2015

Given that concern about data

security is by far the biggest

obstacle (67.2%) to the more

widespread adoption of cloud

technology, the uncertainty about

what data to send to the cloud is

only to be expected. However, as

the other two hurdles mentioned

are unfamiliar providers and a

lack of solutions, the immaturity

of the vendors is as much an

issue as the concept of cloud

computing itself.

As vendors in the cloud space

become more familiar to asset

managers and introduce a

broader range of services, there

is every reason to expect that

the adoption of cloud services

will grow considerably in the

years to come. In some respects,

the timing could not be better.

The issue of legacy technology

has been around for as long as

systems, and the time it takes for

technology to become obsolete

is shortening all the time.

The days of an age-old

portfolio management system

remaining at the core of a firm’s

IT infrastructure are definitely

over, as are the days of the in-

house designed system. But as

more asset managers hand over

IT responsibilities to third-party

software vendors, the problems

associated with legacy systems

show no signs of disappearing.

These problems simply

transfer to the vendors, whose

responsibilities then include

making sure their clients use the

latest version of their software.

What easier way to do this than

to assume responsibility for IT

maintenance on their behalf?

Though there may be some

trepidation about the safety

of their data (particularly

confidential client data) and

trusting their IT to a third party,

the ongoing cost of avoiding

legacy issues will hasten the

move to outsourcing and the

cloud. For many firms, the clock

is ticking. fe

13. WHAT IS PREVENTING YOU FROM USING CLOUD-BASED SOLUTIONS?

11. DO YOU INTEND TO INVEST IN CLOUD-BASED TECHNOLOGY SOLUTIONS IN THE COMING THREE YEARS?

12. WHAT DATA ARE YOU COMFORTABLE PUTTING IN THE CLOUD?

THE DAYS OF AN AGE-OLD PORTFOLIO MANAGEMENT SYSTEM AT THE CORE OF A FIRM’S INFRASTRUCTURE ARE OVER.

Yes

No

Not sure

19%

36%45%

50%45%40%35%30%25%20%15%10%

5%0%

External data (market data)

Positions data Client data Not sure Other

80%

70&

60%

50%

40%

30%

20%

10%

0%Lack of suitable solutions

Concern about data security

unfamiliar providers

Other

13 funds-europe.com

1414 Spring 2015

SPONSORED ARTICLE

ONE OF THE biggest challenges

for vendors is helping clients

to recognise when they have

outgrown a platform and when it

has assumed ‘legacy’ status.

There are typically three

catalysts that lead firms to arrive

at this situation, says Hakan

Valberg, president of Advent

Software EMEA. The first is cost

– it becomes uneconomic to try

and maintain a system over a

long period when they become

outdated and rely on lots of

manual intervention; then there

is compliance – a new regulation

may have particular reporting

requirements that cannot be

met by existing systems; finally

there is a change – the firm may

want to enter a new market but is

prevented from doing so because

of legacy technology.

“Most firms will initially look

to make a series of small fixes

as required because changing

platforms is seen as such a large

commitment of both time and

money. But in many ways, that

approach is just creating another

challenge for the future,” says

Valberg. Often things will come

to a head when a firm falls foul

of compliance rules – either a

client’s mandate or a regulator’s

reporting requirement. However,

ideally a vendor can get involved

before that point is reached. The

better conversations take place

when a client is looking to grow

but is inhibited by their systems.

“Replacing a legacy system

Funds Europe talks to Hakan Valberg about the vendor experience of moving clients from their legacy systems onto new platforms and the importance of fostering a community of users

COMMUNITY SPIRIT

political and personal resistance

to overcome, says Valberg.

“Very often when systems have

been in place for many years,

people are naturally protective

towards any change. Our role is to

convince the firm of the benefits

a change can bring to their

business and their clients.”

Advent has also developed

a client portal called Advent

Direct Community., says Valberg.

“Clients can talk to other clients,

Advent staff, register support

cases, get latest updates and

information and share knowledge

on how they use Advent’s

solutions. Clients also use the

Community to recommend

enhancements and our latest

upgrades of our main solutions in

2014 were based on the feedback

received from clients via the

Community.

“A lot of IT and ops people have

great ideas that they are happy

to share with other users. It is

amazing to see how much they

help each other. We launched

it a year ago and have 12,000

users around the globe. Client

feedback has been positive with

a lot of traffic between them

discussing topics like how to

better use the products and how

to prepare for upgrades. It’s a win

for clients and a win for Advent

as it helps us get closer to clients

and continue understanding their

requirements.”

Advent has also looked

to develop its user group

is a major investment, it can be

disruptive and it is perceived as

a risk so it is easier to make that

decision when you are operating

in a steady market and looking

to be positive in terms of your

business model or product

development.”

There is also often some

MOST FIRMS WILL LOOK TO MAKE A SERIES OF SMALL FIXES AS REQUIRED. BUT IN MANY WAYS, THAT APPROACH IS JUST CREATING ANOTHER CHALLENGE FOR THE FUTURE.

1515funds-europe.com

16 Spring 2015

SPONSORED ARTICLE

The other challenge is

migrating the data from the

old systems to the new. This is

much more of a problem when

the former is a first generation

legacy system that is 20 years or

more old and deeply embedded

in the firm’s infrastructure.

However, while this presents

more of a technical challenge

for vendors, there are some

advantages, says Valberg. “When

the system is that old, the users

are much more motivated to

change to a new system.”

LEAP OF FAITHBy contrast, when they are

replacing a second or third

generation legacy system

supplied by a competing

vendor, there is generally more

reticence from the client about

the replacement. “Maybe that

legacy system is no longer

supported. Or maybe the client

is no longer happy with it but

that can lead to a nervousness

that is difficult to overcome as

the new vendor. They have failed

once and they do not want to

fail again, even if it was the fault

of the previous vendor. So the

negotiations tend to be longer

and the requirements more

detailed. But once they take a

leap of faith, our goal is to repay

that commitment by showing the

client how important they are

to us and develop a long term

relationship with them. We aim to

be a business partner rather just

a technology supplier.”

In the recent survey carried

out by Funds Europe into the

presence of legacy systems

within the funds management

industry, one additional comment

from a respondent stood out.

“If a client has a legacy system

it is the job of the provider to

adapt to that system and not to

change it.” The implication is

that too often asset managers are

forced into moving away from

their legacy systems because of

the incompatibility issues of the

vendor and not any processing or

performance issues for the client.

Valberg says he is empathetic.

“There is often a reluctance

among some managers to think

about best practice and the use

of only the latest versions of

technology. But there is another

side to new technology that

reminds me of the Henry Ford

quote – ‘you can have any colour

as long as it is black’. Our job as

a vendor is to make them in as

many as colours as feasible.

“Best practice can sometimes

be a dangerous phrase. Every

asset manager has different

business models and objectives

and works in different asset

classes and in different markets.

So there has to be some

flexibility in the technology

and we have to learn from our

clients.”

Once again, Advent’s user

groups and annual client

conference are integral to this

aim, says Valberg. Not only does

it provide mutual benefits in

terms of addressing industry

issues like regulatory reporting,

cyber security, cloud computing,

it also prevents clients slipping

into the situations where legacy

issues arise. “The users get to

learn more about the technology

and the roadmaps for future

development, while we get the

benefit of shared research and

development and peer advice.

It is a good way to keep up with

innovation and to prevent the

legacy issues of the past arising

in the future.”

community by holding a series

of events based on industry

segments – for example, a fund

administration forum in Dublin

that includes asset managers,

fund administrators and

distributors. The events continue

to grow and have a wide range of

people from the clients attending

beyond IT and operations, more

and more business director level

and C level are visitors.

More than 50% of Advent’s

projects are replacing first

or second generation legacy

systems, says Valberg. “Through

that experience we have

developed some best practice

guidelines and refined our

methodology. But there are some

challenges. Firms might try and

replicate the way they built their

old system when implementing

the new system but that doesn’t

always work.”

This tactic is born of the

familiarity and comfort that

users have derived from their

technology, says Valberg. “They

have used it for so long because

they know how it works.We have

two new releases every year that

we want our clients to use so

making the technology easy to

use is vital.”

As an example, Valberg points

to the fact that no one takes

lessons on how to use an iPhone.

And if an app doesn’t make sense

to a user within the first few

minutes of use, it will be killed

and they will move onto the next

one. So if fund management

platforms can aspire to that same

level of intuitive, ease of use,

then maybe legacy will not be a

problem to the same extent as it

has been in the past, says Valberg.

“We realise that in many cases

legacy systems will still exist, but

we are striving to deliver new

solutions that are so intuitive it

will make migrations much easier

than in the past decade, this is the

main reason firms are afraid to

make the jump.”

WE REALISE THAT LEGACY SYSTEMS WILL STILL EXIST, BUT WE ARE STRIVING TO DELIVER NEW SOLUTIONS THAT ARE SO INTUITIVE IT WILL MAKE MIGRATIONS MUCH EASIER THAN IN THE PAST DECADE.

Alibaba

AUTUMN 2014

South KoreaDistribution battle

WINTER 2014

Shanghai-Hong Kong Stock Connect

First-time issuersSukuk

4040

BATTLETOUGH

Listed asset managers in Europe

Aviva Investors, COOBNP Paribas IP

RATE Reducing duration

Saudi Arabia’s stock market

CORPORATE BONDS • CLEARING & SETTLEMENT • AWARDS SHORTLIST

NOVEMBER 2013 • ISSUE 121 • €40

Why Russian equities are dominating portfolios

Returning to global markets?

WINTER 2014

Private equity panel

Fund manager roundtable

AUTUMN 2014

Finding a debt solution

Brazilian retail investment The Cuba investor Custody banking

Colombia on the rise

40

CONTROLChina’s economy and systemic risk as seen by its local chief executives

Branding: special discussionEnding Europe’s inducements

STATEBeijing fund industry roundtable

The world at your fingertips

funds globalfunds global is dedicated to cross-border fund professionals operating in the global marketplace

funds europefunds europe is the only dedicated journal for cross-border fund professionals

funds europe and funds global are a key resource for everyone involved in the global investment fund business, and in tracking and interpreting developments in institutional and retail fund markets.

Whether you’re concerned with distribution, asset allocation, human resources, technology or outsourcing, we have the essential business strategy magazines for the asset management industry.

Request sample copies today! funds europe and funds global288 BishopsgateLondon EC2M 4QP, UK

T: +44 (0)20 3178 5872 F: +44 (0)20 3178 4002 E: [email protected]

www.funds-europe.com www.fundsglobalmena.comwww.fundsglobalasia.com

JULY/AUGUST2013

•ISSUE

118

EXCHAN

GE-TRA

DEDFUN

DS• RI

SK MANA

GEMENT

• AFRIC

A

Standard

Life

Investments

CEO

TheMEP

taking aim a

t fees

Keith

Skeoch

JULY/AUGUST 2013 • ISSUE 118 • €40

Switzer

land

Asset ma

nageme

nt roundtab

le

Changin

g times

ernf

:00cov

er12/

7/13

12:44

Page 1

MARCH

2013•

ISSUE114

US v EUROPEAN E

CONOMIC POLICY

• DISTRESSED DEB

T • VENTURE CAPIT

AL

Collateral manage

ment

Still opaque

Pimco’s trade-off

Don’t turnyour back

on the elephant

Risk systems and A

IFMD

MARCH 2013 • ISSUE 114 • €40cover - jssgmnf

:00 cover 27/

2/13 16:11 P

age 1

WINTER 2013

OUT OF THE SHADOWS

Securities lendingInfrastructure build

HOTmoneyBrazil after the taper

MEXICAN PENSION FUNDS LOOK INTERNATIONALLY

Spring 201518

ROUNDTABLE

19 funds-europe.com

Ian Barringer

Head of IT, F&C Investments

Catherine Doherty

Chief executive, Investit

Martin Engdal

Market strategist, Advent

Rakesh Vengayil

COO APAC and Emerging

Markets, BNP Patibas

Investment Partners

Steve Young

Chief executive, Citisoft

19funds-europe.com

Ian BarringerIan Barringer

Head of IT, F&C Investments

Catherine DohertyCatherine Doherty

Chief executive, Investit

Martin EngdalMartin Engdal

Market strategist, Advent

Rakesh VengayilRakesh Vengayil

COO APAC and Emerging

Markets, BNP Patibas

Investment Partners

Steve YoungSteve Young

Chief executive, Citisoft

PHOTOGRAPHER: Paul Cochrane

THE PANEL

Funds Europe: What is your

definition of a legacy system?

Is it purely based on age, or

that in-house, one-off aspect?

Or is it simply an older version

of the current system?

Steve Young, Citisoft: The age of

the system is clearly an indication

of its level of legacy. An important

factor is how bespoke it is.

But there are other indications

that people should look for –

something that’s not been sold

in the market or doesn’t have a

clear release pattern or any kind

of user group or community.

Funds Europe: Might some

firms not be aware that they

have a legacy system?

Young: Absolutely. Vendors

are sometimes quite strong at

clouding the level of legacy and

independence and any influence

that it may have, so they will often

position and talk about it as if

it’s a single product that’s shared

across a number of clients, but

the reality is that it’s heavily

bespoke to an individual client.

The user community need to test

that and talk to other users of the

system and really find out the

commonality of the application

across the user base.

Martin Engdal, Advent: There’s

no one definition, but I guess

there’s a checklist. Even standard

applications can be legacy. If you

don’t really have a roadmap to a

product, then I say it should be

characterised as a legacy system.

If you’re only doing maintenance

and you’re not really spending

R&D money on that platform, it’s

legacy. Is this platform future-

proof? Can this support where we

want to take our business? If you

answer “no” to that, often it is a

sign that this is a legacy system.

Unfortunately, we’re moving into

a world where becoming legacy

doesn’t take ages. It can be within

a year or two.

Rakesh Vengayil, BNP Paribas

Investment Partners: I would

Our panel discusses how to identify legacy systems, the challenge that businesses face when it’s time to replace them and the changing nature of asset managers’ IT departments. Chaired by Nicholas Pratt

GET WITH THE PROGRAM

UNFORTUNATELY WE ARE MOVING INTO A WORLD WHERE BECOMING ‘LEGACY’ DOES NOT TAKE AGES. IT CAN BE WITHIN A YEAR OR TWO.

Martin Engdal, Advent

20

its point in the legacy curve.

Vengayil: In the fund

management industry, operations

are divided into three key

segments – front, middle and

back office – and they are

increasingly outsourced or

offshored, but at the same

time getting highly integrated.

Therefore it’s really important

that everything works in tandem,

even if you are not necessarily

responsible for maintaining all

these three components. If one

of them is moving faster than the

others in terms of upgrades, then

it raises a compatibility issue and

forces you to examine the level

of potential legacy in the other

components.

Young: My strong suspicion is

the age of some systems being

legacy is shortening, because

we’re moving to the digital age

and people want to become more

data-centric. So, having legacy

systems as core components of

the architecture is increasingly

problematic and that is putting

more pressure on older systems.

Barringer: The rate of change of

front-office systems is definitely

increasing; in turn, this is

of time by which a system

becomes legacy changed?

Doherty: That definition can be

triggered by all sorts of things

like a major integration, but

other systems can hang around

for ages because there is not a

business case for replacing it,

even though it is becoming more

and more expensive to run. From

a departmental view, things may

look OK. They may say that they

are using ‘X’ system but when

you look more closely, there are

Excel programmes on the outside

propping things up.

Barringer: It is about

extensibility. If a system cannot

be extended, you end up with a

patchwork of additional solutions

to cater for new functionality –

another asset class, for example.

Young: If you look at the number

of stretches required around a

system, that’s a good indication of

ROUNDTABLE

Spring 2015

not define it by the age of a

system. As long as the system

is current, relevant, scalable,

sustainable and compatible with

the new technologies, it cannot

be classified as a legacy system.

Moreover, it also depends on

the context of the operating

model, as we operate on both

a global and local operating

model. From a global context,

we may have a piece of software

which is currently in frequent

use because of its flexibility and

agility but, within the front-to-

back connectivity of a global

system, it is not compatible

with the upgrades that are

happening. And from a local

context, there are systems that

are relevant for the local usage

but not compatible with our

global platforms for interfaces or

information exchanges.

In some other cases, a legacy

system could be a complex,

Excel macro which plays a

critical role in the overall flow.

This would have evolved over a

period of time, which is person-

dependant software and not

maintainable in an industrial way.

Ian Barringer, F&C

Investments: The big issue is

a lack of support, whether it’s

a vendor system or internally

built. Can it be developed or

extended? Is it based on a dying

language or a platform that is out

of support? Plenty of software

out there still relies on Windows

2003.

Catherine Doherty, Investit:

A legacy system is like a second-

hand car. It’s the point at which

repairs become uneconomic.

It becomes too difficult to change

bits of the system and that

pushes you into a huge

replacement project.

Funds Europe: Has the

definition of a legacy system

changed or has the length

A SYSTEM CAN HANG AROUND FOR AGES BECAUSE THERE IS NO BUSINESS CASE FOR REPLACING IT, EVEN THOUGH IT IS BECOMING MORE AND MORE EXPENSIVE TO RUN.

Catherine Doherty, Investit

funds-europe.com 21

Funds Europe: According to the

survey results, 50% of firms

said they used legacy systems

slightly, 30% said they used

them a lot, and 20% not at all.

Is that a fair reflection of the

industry?

Barringer: It depends on how

you define ‘use’. If one of your

primary systems is legacy, then

saying you only use it lightly

because all your other systems

are current is a bit disingenuous.

Young: A lot of people don’t

want to admit they’re on ageing

platforms, so I suspect the results

are understated.

Doherty: If you said to people:

“How many of your systems are

constraining your flexibility

because you’re finding it too

expensive to extend them?” or

“How many of those operations

people are there because

they’re making up for systems

shortfalls?” you’d get a different

answer.

Young: It’s also where you find

out who truly understands

the costs of running a legacy

system. They’ll generally say

they’re cheaper, which is in my

experience complete nonsense.

dragging other systems with

them. However, they are unable

to cope, which makes them

inherently legacy. If they were

standalone they would be fine,

but the tight coupling of the many

systems in a financial architecture

means they have to keep track of

the changes.

Vengayil: The ideal scenario

would be having a master/

slave architecture, but that’s not

often the case because there are

different external organisations

involved in your front-to-back

chain. They are changing the

components, or responding

to other external needs, so

it would not fit into that kind

of architecture. That’s where

sometimes we see the mismatch

arising.

Doherty: If you have an open

architecture, you can easily pull

bits of data out and you can plug

in a new risk system in the front

office. Whereas if the system

insists on keeping its data to

itself, it becomes a burden much

earlier.

Engdal: A lot of the innovations

have been in the front office

but not so much in the middle

and back office. We see some

organisations investing heavily

in front-end, client-facing tools

but neglecting the back end.

This might help them in the short

term but in the longer term it

tends to be an issue, especially

for some of these larger, tier-one

organisations. If the core engine

isn’t working and future-proofed,

you will eventually end up with

business constraints and a costly

platform.

Vengayil: I absolutely agree.

We do see this in local markets

as well, because in some of

the local markets the middle

and back-office technology

has to be pretty much aligned

with the local market practices,

whereas the fund managers

tend to use very sophisticated

front-end systems because

they are globally available,

and when you try to integrate

that with your back office, it

becomes a big challenge. We

have experience in countries like

Indonesia where the front office

is extremely sophisticated, multi-

currency, multiple asset class,

but the back end has limitations

where it cannot respond to the

sophistication you’re bringing in

the front end... One cannot easily

change the local set-up, so you

have to be in line with what the

market is doing.

Young: Legacy systems are far

more prevalent in cost centres.

People invest far more where

they can generate revenue and

they worry far less in areas which

are seen as cost centres. But I

think this approach is somewhat

naïve, because you’re only as

strong as your weakest point.

THE MIDDLE OFFICE IS WHERE EVERYTHING IS DUMPED, BECAUSE NOBODY KNOWS HOW TO GLUE THE OTHER TWO PARTS TOGETHER.

Ian Barringer, F&C Investments

-

22

of this rationalisation.

Young: The market is quite

fragmented. In the UK and

Europe, regulation’s still the

number-one concern. In the US,

they’re much more strategic and

the big and middle-sized houses

have got a much more modern

infrastructure that is built for the

future. That is the challenge for

Europe, because there have been

a lot of tactical, regulatory-led

projects but firms haven’t really

addressed the issues around

legacy systems and they are

slipping further behind other

parts of the world.

Barringer: The drivers for

technology have always been

in the front office but more so at

the moment, particularly in sales

and marketing. However, I think

there is an opportunity. With a

number of operating systems

and platforms facing retirement,

there is a focus on the back office.

People have realised we should

start doing something and big

replacement projects are being

initiated. Working out the total

cost is obviously still a challenge.

Funds Europe: Is there board-

level involvement in these

projects or are they confined

to IT?

Barringer: There is board-level

involvement. One of the tools

I’ve been using to provide some

transparency is roadmaps that

highlight pre-emptive milestones

– where support begins to fall

off, the stage where they are not

legacy yet but will be in two or

three years’ time. Funding of

these projects needs to occur at

that point, not once they have hit

the legacy threshold.

Doherty: The concept of cost

is changing. It used to be

solely about the cost of IT but

increasingly clients are talking

more inclined to invest in their

systems. There’s also a feeling

that this is a transformational time

in investment management. There

are new market opportunities and

people want to position their firm

as being more customer-friendly

and lower cost.

Vengayil: For the last few

years the focus has been on

rationalising the cost but now

there is a clear realisation that

what we are doing is sustainable

in savings and efficiency. We

handle a wide variety of front-

office tools in several asset

classes and that creates more

situations for legacy systems.

Sometimes you have a star

fund manager who is used to

a certain tool and has built in

some of his own algorithms.

From a technology perspective

it may have already become

obsolete, but from a functionality

and emotional attachment

perspective, you cannot take that

away. But in the last few years

we could drive those kinds of

changes because of the focus

on cost, people realised that

they could not afford the luxury

of running multiple platforms

and systems. In our case we by

and large have moved on to a

single, multi-asset class portfolio

management system and we

have eliminated a lot of tailor-

made stuff to bring them all into a

common platform.

Funds Europe: How do

you manage the economic

challenge of replacing legacy

systems with new technology?

Vengayil: In a lot of firms, the

new innovations and upgrades

are self-funded due to budget

limitations. That forces the

business to find efficiency

elsewhere in the chain and use

it in a place where one thinks it

is relevant. So that automatically

drives some

ROUNDTABLE

Spring 2015

They’re not looking at the total

cost of ownership, they’re looking

at the vendor spend, and the

vendor spend is incredibly low,

but the total cost of ownership

is usually vastly understated. To

create a business case you really

have to understand the total

cost of ownership, but not many

are willing to do that. Building a

business case is actually quite

easy, if you spend time and effort

putting it together, but you’ve got

to get out of denial first.

Barringer: This is very much

an issue I am tackling now. The

problem is primarily the bespoke

solutions; the glue that people put

between the back and the front,

the customisations that change

the system to fit the business

model. That is where there is

ingrained intellectual property.

Referring to a previous point, it

is the middle piece – the middle

office. That is where everything

is dumped, because nobody

knows how to glue the two parts

of business together.

Young: We are on the cusp of

more changes in the industry

than we’ve seen for a long, long

time. The ability to change and

acknowledge that you have

legacy systems is going to be

increasingly critical. It’s probably

been less of an issue over the

last decade, but it’s going to

be increasingly a sharper and

sharper issue for businesses to

address. The smart businesses

are looking at that. People in

denial are going to suffer badly,

Doherty: The regulatory

reporting thing has been very

interesting because it requires

you to bring data together from

all the way across the enterprise,

and that really brings home to

you how you’ve patched things

together. We’ve had some very

good market conditions for the

last few years, so people are

funds-europe.com 23

are seeing lengthier processes

between buyer and seller, and

sometimes people going back to

the drawing board and redrafting

their requirements. We have seen

it all over Europe. People are

afraid to take the wrong decision

because things are moving so fast

– this is totally understandable

and something we appreciate as

a vendor. But in the US, there has

been a move to cloud solutions.

Adoption is slower in Europe but,

if we were to do this roundtable

in five years’ time, there will be a

larger proportion using cloud-

based solutions where you pay

as you go, based on the number

of funds or portfolios you have on

this platform. We are also seeing

that the lines between us as a

vendor and our client are not

as sharp anymore, because we

sometimes find ourselves actually

‘competing’ with our clients when

it comes to combined technology

and outsourcing propositions.

Young: Firms have got a much

better, clearer idea of where they

compete with each other and in

the large parts of their operation

that are not competitive, they’re

much more prepared to take a

standard, off-the-shelf solution

or to outsource. Large parts of

about the cost of the product.

They are thinking in much more

holistic terms about, can we run

this product at 30 basis points

that we used to run at 80?

We have also started to build

models that look at the impact of

operations on fund performance.

You get drag effects like running

too much cash in the portfolio

but you also get the number of

fund managers building up –

people who are running little

spreadsheets on the side – and

the proportion of fund managers

to AuM is proving not to be

scalable. A lot of firms are now

thinking about the scalability of

the front office as well as the back

office and it all comes back to a

good platform where managers

can run portfolios side by side

and replicate them fluently and

spend their time having good

investment ideas – not trying to

run the platform from the front

office.

Vengayil: The two big costs for

asset managers are staff and

technology and a big percentage

of the latter is getting earmarked

towards regulatory developments

and keeping the lights on.

That leaves very little for new

innovations and development.

That’s where a lot more

pressure is coming back to

the IT or business to self-fund

the new projects and get some

sustainable technology which

you can redeploy into developing

some of these things. Earlier IT

projects were seen in isolation

but now they are seen as part of a

more holistic business process in

terms of keeping your technology

costs as variable as your revenue.

Young: As we see the rise in

passive management, people

are looking much more to

industrialise their process

but there are a lot of legacy

systems that are actually quite

good at processing. And if it is a

rudimentary investment process,

it can hide the problem.

The other issue around legacy

systems is RoI. The longer you’ve

had that system and the more

deeply embedded it is, the

longer and more expensive is the

programme to change it. So in

RoI terms it could take years, not

months. And your operating costs

will rise sharply until that system

is replaced. The longer they leave

it, the higher it costs, so they have

to find a way to generate that cost

in the short term. A lot of people

just keep putting it off.

Funds Europe: From a vendor

perspective, how do you get

over the notion that the bigger

the project is, the more it’s

going to cost and the longer it

will take to get that return?

Engdal: The RoI question seems

to be popping up all over the

place, which means that we

SOMETIMES YOU HAVE A STAR FUND MANAGER WHO IS USED TO A CERTAIN TOOL AND HAS BUILT IN HIS OWN ALGORITHMS. FROM A FUNCTIONALITY PERSPECTIVE, YOU CANNOT TAKE THAT AWAY.

Rakesh Vengayil, BNP Paribas Investment Partners

-

24

THE LONGER YOU’VE HAD THAT SYSTEM, THE LONGER AND MORE EXPENSIVE IS THE PROGRAMME TO CHANGE IT. IN RoI TERMS, IT COULD TAKE YEARS, NOT MONTHS.

Steve Young, Citisoft

design than cutting code and

building new systems. Now the

focus is on presentation and the

facilitation of ideas rather than

bespoke development.

Doherty: There needs to be a

director of information because

that is the company’s value,

and what a legacy system does,

actually, it separates the firm

from its information, and that’s its

crime.

Vengayil: We still do some

development in-house, but not

necessarily the core components.

That’s because we clearly

understand that’s not our core

competency; we outsource. But

given the complexity of front-to-

back models, when it comes to

interfacing and those kinds of

stuff, we try to do it ourselves.

Doherty: One of the key

developments is that IT lost

the battle for the company

website. Marketing just went

out and bought one from a

vendor. As the range of technical

competencies gets wider, there’s

this outsourcing of technical

competence. So there is still

bespoke code, but it’s not written

so unique, you have to build

your own. If you’re not unique,

you should avoid building your

own systems because of the

cost. I also think the industry’s

changing, the role and power

of IT is diminishing and the

number of people who are pure

IT heads and managers of IT

solely is diminishing. There are

some banks that don’t have IT

departments, but they have a

member of the board with IT

responsibility. That’s the way

the industry needs to go. We

are a long way from that in our

industry. Other industries are

already there... In the future,

vendors won’t just shift code

software in boxes, there will be a

service software hybrid model.

Barringer: It is about defining

technology because nowadays

the role of the IT department is

more about configuration and

ROUNDTABLE

Spring 2015

the middle and back office are

relatively commoditised, so why

have a bespoke legacy system

there, when you can share a

platform with the industry?

The problem is that there are

very few suppliers. The supplier

market’s as weak as I’ve known it

in terms of end products, so the

legacy issue is not easy for fund

managers. Ideally they want to

outsource, but there isn’t really a

shortlist of outsource providers

with a standard model. If you put

a shortlist together for let’s say a

back/middle office replacement

system, if you’ve got four or five

you’ve done very well. That’s not

a healthy situation, really.

Vengayil: The supply market

is weak because the demand

is not high enough. If you look

at our industry compared with

banking, where organisations

are addressing the second-

generation digital needs of their

clients and how they deliver it,

we are a bit more ‘old school’ and

conventional.

That could also be the reason

why this industry lives with a

whole lot of legacy systems,

because we have lived quite

comfortably doing things in a

conventional way. But one of

the reasons a lot of people are

speculating now is that there

could be a disruption where

some of these new technology

providers like Google can

capture the asset management

market by providing technology

and bringing us more

management expertise.

Funds Europe: Is there still

a place for the in-house,

bespoke, one-off design

system? Or will we not see

their like again? If so, does

that mean firms will be less

creative in their use of IT?

Young: The only reason to build

your own system is if you are

funds-europe.com 25

an easy thing to solve. The reason

people still have legacy systems

is because it is so hard to get off

them.

Engdal: My prediction would

be that you would see fewer

systems in production that are

categorised as legacy in the

future.

More firms will realise that

if they are running a legacy

platform, the chances are that

you can improve profitability and

business flexibility by moving to

a standard application. They will

likely be better off buying the

best off-the-shelf products they

can find and reap the benefits

of shared R&D investment on

maintaining their own systems.

We are seeing that to a larger

extent than we did just three, four

years ago. fe

in-house.

Engdal: I think IT is going to be

more about data. There are a

lot of firms getting a chief data

officer and I guess one of the

challenges is whether firms have

enough IT knowledge and data

knowledge at board level. You

can sometimes realise that as

you go higher in the company,

people don’t really have enough

competence and knowledge to

take decisions in some of these

more strategic investments.

Barringer: It has been the

role of IT to own the data for as

long as I have been working

in the industry. IT lay down the

pipes that data flows through,

together with the repository and

everything that processes. As the

role of IT evolves, people have

focused on particular areas of

functionality and have spun those

off into departments of their own,

maybe for survival reasons.

Doherty: Putting the ‘I’ back into

information technology.

Young: Yes, and taking the ‘T’

away.

Barringer: Very much so.

Vengayil: IT is no longer

perceived as purely back-end

function. They are very much

part of the strategic decision-

making process. There are

senior-level forums like the IT

Project Review Board where they

talk about active IT strategy in

conjunction with the business

strategy. IT is such a big part of

the firm’s investment that it has to

be combined with strategy.

Doherty: I think there has been

an important shift. IT used to

exist in isolation, and then we

all hopped up and down and

said: “We want to be involved in

decisions,” but basically what we

wanted to do was be able to say

“no” to things. The next phase

is that we want to contribute to

using IT to transform the firm.

Young: If you replace any piece

of IT, you have to consider a

number of options, including

offshoring and outsourcing, so

you’re not taking IT and replacing

it with IT. You’ve got to look much

broader. So you can’t have IT

people looking to replace IT.

There is a wider array of skills

involved and it is a much more

complex world now, which is why

the IT voice has got quieter.

The biggest problem with

legacy is actually replacing it –

working out your RoI, getting the

political support and embracing

change because you cannot swap

like for like. Everyone would

say legacy is a big issue in the

industry, but let’s not pretend it’s

26 Spring 2015

Friends Life Investments’ Luke Ransley talks about the legacy problems associated with in-house installations and discusses whether the trend towards outsourcing will prevent similar issues arising in the future.

BACK OFFICE TO THE FUTURE

ASSET MANAGER INTERVIEW

HISTORICALLY, LEGACY

issues have arisen in two main

areas – systems and applications.

For the former, the issues are

largely down to vendors. “The

operating systems on which the

applications are run, go through

various upgrades until the

point when they are no longer

supported by the vendor,” says

Luke Ransley, operations head at

Friends Life Investments.

“We have seen this recently

in mainstream computing with

Windows XP. So IT managers

have to work with vendors to

ensure that they are always on

upgraded versions, at least for

the core systems. If they are small

departments, you may resist the

urge to upgrade,” he says.

“This leaves you with a choice

of either upgrading to the latest

version or spending a lot of

money to move to a new system.”

The applications themselves

are also subject to new version

releases and, depending on how

embedded these applications

are, a radical change in a firm’s

business model may require new

applications and render existing

ones as legacy.

For example, the requirements

of new regulations such as EMIR

and MiFIR will require firms to

do their own reporting, rather

than relying on their brokers.

Consequently, this will force many

firms on to the latest versions of

their applications.

Similarly, there are implications

for the applications if the firm

enters a new business area (in

the sense of either asset class or

geography). “Where you have

legacy systems, the gap between

the functionality you have and the

functionality you need grows. That

puts pressure on the investment

managers,” says Ransley.

He adds that data management

is another area exposing the

legacy systems within firms.

“When you undergo significant

version upgrades, it can make it

very difficult to retrieve all of the

data that was on old systems prior

to the migration.

“One option is to do an Excel

download of the data you need

prior to the migration. But there

are also more sophisticated tools

that enable you to read the data

and act as a repository. You have

lost the application, so you need

an integration programme where

you can have pre-defined fields to

enable you to extract the data.”

A NEW STARTMaking the tough decision to

move from a legacy system to

a new platform can often be

dependent on the nature of the

system in question, says Ransley.

Core components such as the

order management, portfolio

management or investment

accounting systems are the ones

that cause most concern. However,

if it is a broker research tool, the

legacy issue is less significant,

increasing the likelihood that it

will be retained for as long as

possible.

That said, the traditional tale

of an asset manager with a

20-year-old system that has not

been updated for six years, or is

weighed down by a mismatched

array of homemade, Excel-based

add-ons, is most likely a thing of

the past, says Ransley.

“These days, IT departments

have much more of a say over

people developing their own

systems,” he notes.

In the past, fund managers

would ask to have a C++

programmer working in the

front office to do some minimal

coding. Before you knew it,

these proprietary programmes

had become critical parts of the

infrastructure, impenetrable to

all but the individuals who had

developed them.

“It is now less likely that firms

will have these systems that

cannot be supported once the

original developer has left,” says

Ransley. “IT departments have

policies about what systems

you can use and the way that

data is stored and managed –

and there is much more risk

assessment around IT governance

that make these legacy issues

much more visible.”

Issues such as these should not

arise at Ransley’s current role

at Friends Life Investment. The

internal investment management

arm of Friends Life (a firm created

WHERE YOU HAVE LEGACY SYSTEMS, THE GAP BETWEEN THE FUNCTIONALITY YOU HAVE AND THE FUNCTIONALITY YOU NEED GROWS. THAT PUTS PRESSURE ON THE INVESTMENT MANAGERS.

27 funds-europe.com

OLD SCHOOL:Sometimes small departments resist the urge to upgrade.

in 2011 from the amalgamation of

Friends Provident, the majority

of the Axa UK life insurance

business and Bupa Health

Assurance) has too short a history.

As Ransley puts it: “We are only

two years old and we outsource

everything.”

The firm employs two major

outsourcing providers. For order

management, it uses a front-office

vendor’s managed service. “They

run it all for us,” says Ransley. “We

get asked if we want to go on to

the next release, so that we are

either on the latest version or not

far off.” For investment operations,

Friends Life Investment uses the

outsourced offering of one of the

major asset-servicing providers.

SHIFTING THE BURDENOf course, opting for outsourcing

does not eradicate the legacy

problem, but transfers it instead

to the provider. The argument

goes that these providers will be

much more motivated to avoid

any such problems.

Ransley cites the issue of

downstream implications that

arise from system upgrades.

“A lot of firms will build

functionality on their current

applications. Then, when it

comes to upgrading, you have to

check that all the programmes

running off it will still work on

the new platform. If there are any

issues that arise with subsidiary

systems, then it can be enough

of an impediment to prevent

upgrading,” he says.

Most outsourcing providers will

be well aware of these potential

problems, he adds. “That is the

benefit of looking outside for

technology – the experience of

the vendors.”

Not only do the outsourcing

providers have to manage the

different demands and system

set-ups of each client, they

also have to aim for as much

standardisation as possible

and try to ensure that different

systems are able to communicate

with each other.

This is something that has

been highlighted by regulators

as well. For instance, the ‘Dear

CEO’ letters, sent by the UK’s

Financial Services Authority

in 2012, drew attention to the

operational risk that could result

from asset managers’ outsourcing

relationships if there was no

contingency plan in place to

enable them to switch from one

provider to another.

To allay these fears, it is

essential to ensure more standard

interfaces and compatibility

between the various third-party

systems employed by outsourcing

providers. Moreover, there has

to be full transparency for their

asset manager customers.

Fortunately, most vendors are

beginning to organise themselves

to be more transparent, says

Ransley. “With our providers, we

get told what version we are on

and whether we want to go on to

the next version. We get the same

level of transparency that we

would expect if we were running

these systems in-house.” fe

Are you counting the cost of your legacy system?

Is your current system holding you back? Are you ready for regulatory changes?

Read our seven sure signs that you have outgrown your portfolio management system.

To find out more visit www.capitaltrends.com