application guide for the afep-medef corporate …

TRANSCRIPT

1

HIGH COMMITTEE FOR CORPORATE GOVERNANCE

APPLICATION GUIDE FOR THE AFEP-MEDEF CORPORATE GOVERNANCE CODE OF LISTED CORPORATIONS

OF JUNE 2013

December 2014

2

This is a free translation of the 2nd edition of the Guide published by the High

Committee for Corporate Governance (HCGE). The purpose of the guide is to outline

the interpretation used by the HCGE for certain recommendations of the AFEP-

MEDEF Corporate Governance Code of Listed Corporations, and to provide tools to

facilitate the implementation thereof. It does not present any new general

recommendations subject to the “comply or explain” principle. The intention is for it

to evolve as the HCGE's work progresses.

Comments are presented in the order of the provisions of the code to which they refer.

Unless indicated otherwise, the remarks applicable to directors also apply to members of

Supervisory Boards.

The positions adopted by the HCGE in its first year, some of which are included in this

Guide, are explained in the first part of its Activity Report published in October 2014

(which can be consulted on the AFEP and MEDEF websites).

The HCGE would like to point out that Article 25.2 of the AFEP-MEDEF Code states that

the companies which refer to this code acknowledge the role of the HCGE, which is

notably responsible for making recommendations to the companies which consult it or

which are the subject of its self-referral interventions. This means that these HCGE

recommendations, which explain the recommendations of the code, are, like the latter,

subject to the “comply or explain” rule. As laid down in the AFEP-MEDEF Code,

companies are free not to comply with these recommendations, but in this case they

must, however, indicate in their annual report that they have received them and explain

why they are not following them. If they do not provide this explanation, and in this case

only, the HCGE reserves the right to name them in its next annual report. In some cases

where there is a time constraint, for example in the event of a significant breach of the

transparency rules relating to consulting the shareholders' meeting about executive

directors' compensation, this disclosure may take the form of a press release. Clearly, the

explanations provided must be “substantiated and adapted to the company's particular

situation and must convincingly indicate why this specific aspect justifies an exemption”.

3

Independent directors – § 9

According to the AFEP-MEDEF Code, it is up to the Board of Directors to “review individually the

position of each of its members on the basis of the criteria” for independence mentioned in § 9.4.

Furthermore, the code states that “the Board of Directors may consider that, although a particular

director meets all of the above criteria, he or she cannot be held to be independent owing to the

specific circumstances of the person or the company, due to its ownership structure or for any other

reason”. If the company does not comply with the proportions of independent directors

recommended by the code1, it should indicate how the sound operation of the Board is nevertheless

ensured.

Certain situations cannot be resolved immediately. In this case redress must be provided, for

example at the next renewal of the Board, and this intention must be clearly mentioned.

Directors on the Board for more than twelve years

Among the criteria to be reviewed by the committee or the Board in order for a director to

qualify as independent, the AFEP-MEDEF Code sets out the following criterion: “not to have

been a director of the corporation for more than twelve years”. If the Board considers that a

member who does not meet this criterion nevertheless qualifies as independent, particular

attention must be given to the explanations supporting this position, which must be based

on the specific situation of the company and the director concerned, and not on challenging

the appropriateness of the rule.

Application of the criterion governing the director's links with the company as a

“customer, supplier, investment banker or merchant banker”

Each company must assess how significant these links are, and present the criteria it deems

relevant according to its own specific features and those of the relationship in question. The

issue must be reviewed individually, and the criteria adopted must be mentioned. This

significance shall be assessed from the point of view of the company and from the point of

view of the director himself or herself. If none of the directors considered to be independent

has any direct or indirect business dealings with the corporation or its group, or if these

dealings are not significant, this must be explicitly stated in the reference document.

Independence of directors who hold executive or non-executive positions in a subsidiary

of the group

The duty of loyalty that the executive director of a subsidiary has with regard to this

subsidiary may create conflicts of interest during certain proceedings of the Board of the

parent company of which he or she is also a member. This must be taken into account in the

assessment of his or her independence. At the very least, if the Board nevertheless believes

that he or she still qualifies as independent, it might, for example, be specified that the

person concerned shall abstain from participating in decisions of the Board of the parent

company where there is a conflict of interests between the latter and the subsidiary.

1 Half of the Board in widely held corporations, at least one third in controlled companies within the meaning of

Art. L. 233-3 of the Commercial Code (§ 9.2 of the AFEP-MEDEF code), at least two thirds on the audit committee (§ 10.1) and a majority on committees in charge of appointments or nominations and compensation (§ 17.1 and 18.1).

4

Operating procedures of the nominations committee and the compensation

committee – § 17.1 and § 18.3

Paragraph 17.1 specifically states that “unlike the provisions governing the compensation committee,

the Chief Executive Officer shall be associated with the appointments or nominations committee’s

proceedings”.

This means that the Chief Executive Officer is consulted by the appointments or nominations

committee, despite not being a member thereof, especially where the committee is responsible for

both compensation and nominations. The same applies for the compensation committee, concerning

which § 18.3 specifies that it “must be informed of the compensation policy applicable to the

principal executive managers who are not executive directors of the company” and, for this purpose,

“the executive directors attend meetings of the compensation committee”.

Chief Executive Officer is given to mean the Chairman and CEO (Président directeur général) or the

CEO (directeur général) in one-tier companies, the Chairman of the Management Board or sole

managing director in companies with a Management Board and a Supervisory Board, and Statutory

Managers in limited stock partnerships (sociétés en commandite par actions).

Chairmanship of the compensation committee and participation of employee

directors in this committee – § 18.1

According to § 18.1 of the AFEP-MEDEF Code: “It [the compensation committee] should be chaired by an independent director. It is advised that an employee director be a member of this committee”.

These two sentences of the AFEP-MEDEF Code only refer to the compensation committee. They do not apply to the nominations committee if this is separate from the compensation committee.

Number of directorships – § 19

§ 19 of the code states that an executive director (of a listed corporation) should not hold more than

two other directorships in listed corporations, including foreign corporations, not affiliated with his

or her group. When a company has a separate Chairman, the Board of Directors of the corporation in

which he or she holds this position must assess the number of directorships he or she may hold

concurrently depending, in particular, on whether or not he or she is entrusted with specific tasks.

In the presentation of the directorships held by directors, the company must clearly indicate

whether or not the directorships in question are affiliated with his or her group and whether

or not the corporations in which these directorships are held are listed.

The code recommends that an executive director should hold no more than two other

directorships (the Board may deviate from this rule in the case of a non-executive

chairman), and a director no more than four other directorships in listed corporations,

including foreign corporations, not affiliated with his or her group. It specifies with regard to

directors that “this recommendation will apply at the time of appointment or the next

renewal of the term of office”.

5

This point also applies for limiting executive directors to two directorships. It should be

interpreted as meaning that “non-compliant” executive directors are not required to resign

during the term of office, but should refrain from accepting the renewal of a directorship not

affiliated with the group which would keep them over the limit.

Furthermore, the footnote under § 19 of the code states that the limit of two directorships does not

apply to the directorships held by an executive director of a company whose main activity is to

acquire and manage subsidiaries and holdings, in these same subsidiaries and holdings, held alone or

together with others.

This exemption shall be understood as follows:

If it is motivated by the specific situation of these executive directors as regards the time

they are capable of devoting to the performance of their directorships, this exemption shall

relate to them personally. It only refers to individuals who hold an executive directorship in

a listed corporation whose main activity is to acquire or manage holdings.

Consequently, this exemption is intended to be implemented and applied to and within each

of the listed corporations (i) in which these individuals hold a directorship and (ii) which are

direct or indirect subsidiaries or holdings, held alone or together with others, by the

company whose main activity is to acquire and manage such holdings and in which they hold

their executive directorship.

It does not therefore apply to the executive directors of companies which do not have this

activity as their main activity, even for the directorships they might hold in companies in

which a subsidiary of the company they run and which might itself have as its main activity

the acquisition and management of holdings, might have a holding.

Concurrent executive director and employee status – § 22

The AFEP-MEDEF Code recommends that “when an employee is appointed as executive director, it is

recommended to terminate his or her employment contract with the company or with a company

affiliated to the group, whether through contractual termination or resignation” (§ 22). This therefore

means the termination of the employment contract and not the simple suspension thereof that

French case law automatically applies. This recommendation of the code applies “to the Chairman,

Chief Executive Officer (directeur général), of companies having a Board of Directors, to the

Chairman of the Management Board or sole managing director of companies having a Management

Board and a Supervisory Board and to statutory managers of limited stock partnerships” (sociétés en

commandite par actions). It does not therefore affect deputy chief executive officers (directeurs

généraux délégués) and members of Management Boards.

If the company considers that the employment contract can nevertheless be maintained

(and suspended), the explanations provided must clearly show not only the justifications for

this decision, but also its consequences in terms of the payment that would arise from the

termination of the employment contract. Indeed, maintaining the employment contract

cannot result in exemption from the stipulations of the code concerning these points unless

the “comply or explain” principle is applied clearly and precisely.

6

The payment arising from the termination of an executive director’s employment contract

should not exceed an amount corresponding to two years’ fixed and variable compensation.

Moreover, payments are generally excluded in the event of serious or gross misconduct,

which is less strict than the terms laid down by the code for appointment as an executive

director (“imposed departure linked to a change in control or strategy”). If compliance with

the terms of the code is not possible legally due to firm commitments made to the executive

officer as part of his or her employment contract, the company must inform its shareholders

of this point.

In the event of the employment contract being maintained, the code does not prohibit the

concurrent drawing of the relevant payment with a termination payment in respect of the

directorship, subject to the terms of Article L. 225-42-1 of the Commercial Code (procedure

for related party transactions, performance conditions, etc.) if the dismissal under the

employment contract and the termination of the directorship (mandat social) occur at the

same time. However, it considers that this should only be possible if the total concurrent

indemnification does not exceed two years’ fixed and variable compensation as laid down

by § 23.2.5 of the AFEP-MEDEF Code.

Fixed part of executive directors' compensation – § 23.2.2

§ 23.2.2 of the AFEP-MEDEF Code governs the fixed part of executive directors' compensation.

The information presented in this regard must show either the date since which the fixed

compensation has remained unchanged, or the policy pursued by the Board in this area, particularly

if a significant variation occurred during the financial year.

Variable part of executive directors' compensation – § 23.2.3

§ 23.2.3 of the code sets fairly detailed rules concerning variable compensation designed, on the one

hand, to ensure that it is consistent with the company’s performance and the executive officer’s

contribution to it, and, on the other hand, to prohibit excesses. In the first instance, the criteria used

should be defined and communicated as precisely as possible. However, the code specifies that the

presentation of the criteria used must not “jeopardise the confidentiality that may be linked to

certain elements of determining the variable part of the compensation” (§ 24.2), so as not to give

indications about the company's strategy that might be exploited by competitors or, if applicable,

create confusion in the minds of investors with the forecasts communicated to them by the company

in the framework of any market “guidance”.

- These confidentiality requirements must only be invoked advisedly. Reluctance to

communicate the quantified or non-quantified objectives set for each criterion is

understandable, but it is generally possible to indicate the nature of the quantitative criteria

and the proportion of qualitative criteria in relation to quantitative criteria.

- It is pointed out that variable compensation must be expressed as a maximum percentage of

the fixed part (and not of the “target” amount). With regard to deferred and multi-annual

variable compensation in particular, where indicating such a maximum percentage of the

fixed compensation is not appropriate, companies shall present another method for

7

determining the maximum entitlements that might be awarded and/or acquired or paid at

maturity, in accordance with the “comply or explain” rule.

- The reference document must also indicate that the Board has assessed the level to which

the criteria have been met when it sets the amount of effective variable compensation.

With regard to deferred and multi-annual variable compensation, reference is also made to

the developments shown below in the corresponding paragraphs on the application of the

advisory resolution regarding executive directors' compensation (§ 24.3 of the code).

Stock options and performance shares – § 23.2.4

§ 23.2.4 of the code states that “it is necessary to determine periods preceding the disclosure of the

annual and interim financial statements, during which the exercise of the stock options is not

possible. The Board of Directors or Supervisory Board must determine these periods and, where

applicable, determine the procedure to be implemented by executive directors prior to any exercise of

the stock options, in order to ensure that they do not hold any information likely to prevent such

exercise".

Some companies choose only to apply this rule when options are exercised followed immediately by

the sale of the shares arising from this exercise, on the grounds that the capital gain is more likely to

be affected by rapid variations in the share price. As this provision is designed to protect companies

and their executive officers themselves from the risks related to insider misconduct and dealing, the

Boards must assess the degree of rigour they wish to apply to the supervision of option transactions.

In any event, they must clearly present the rules adopted.

The same paragraph of the code, amended in June 2013, states that “executive directors who are

beneficiaries of stock options and/or performance shares must make a formal commitment not to

engage in any hedging transactions in respect of their own risks, either on options or on shares

resulting from the exercise of options or on performance shares, until the end of the period

determined by the Board of Directors for holding shares” (§ 23.2.4).

This wording is more rigorous than in the previous version of the code, in that it requires executive

officers to make a “formal” commitment. In fact, prohibitions on engaging in hedging transactions

often feature in the stock option plans themselves. This is particularly necessary for options, as

hedging transactions are in direct contradiction with this method of compensation. If confirmation in

the form of a formal commitment is not given by the beneficiary executive officers, companies

should, at the very least, communicate the precise terms of the prohibition when it appears in stock

option plans.

8

Supplementary pension schemes – § 23.2.6

The following is clarified with regard to supplementary pension schemes for executive directors

subject to Article L. 137-11 of the Social Security Code:

Except for plans closed to new beneficiaries, which can no longer be altered, supplementary pension

schemes must be made compliant with the revised code.

Furthermore, § 23.2.6 of the Corporate Governance Code mentions figures the purpose of which

needs to be pointed out:

Consequently, in the fourth dash, it is specified that “each year, the increase in potential rights shall

be progressive in relation to the seniority in the scheme, and shall only account for a percentage

limited to 5% of the beneficiary’s compensation. This progression must be described”.

The aim of this point is to avoid an executive director with just a few years' seniority in the scheme

(e.g. one or two years) being able to liquidate his or her supplementary pension entitlements by

benefiting from the 45% maximum percentage of the reference income mentioned in the last

paragraph. It is therefore specified that beneficiaries must meet reasonable requirements of

seniority within the company, of at least two years, as determined by the Board of Directors, and

that the annual increase in rights must only account for a percentage limited to 5% of the

beneficiary's compensation. Consequently, the maximum percentage of the reference income should

only be reached after a minimum length of seniority in the scheme of nine years.

The last paragraph states that “information on individual potential rights, in particular the reference

income and the maximum percentage of this income which the supplementary pension scheme would

confer, must be made public. The percentage may not be more than 45% of the reference income

(fixed and variable compensation due in the reference period)”.

This means introducing a ceiling of 45% of the income which the supplementary pension scheme

would confer. When applying this text, the notion of reference income refers to the executive

director's actual income (fixed and variable) and not the reference income taken into account to

calculate pension entitlements as laid down in the rules governing the plan.

If the rules governing the plan should include an entitlements acquisition arrangement and a

supplementary pension ceiling linked to parameters other than the reference compensation (for

example, a multiple of the annual social security ceiling or a ceiling relating to all the pension

schemes), it is desirable to present an estimate showing compliance with the rules of the code.

Comprehensiveness of compensation information (service contracts) – § 24

§ 24 of the code stipulates that: “comprehensive information must be provided to shareholders so

that they can have a clear view, not only of the individual compensation paid to executive directors,

but also of the policy applied by the company in order to determine the compensation paid”.

9

If executive directors' compensation is paid through another company, whether or not this is the

parent company or a reference shareholder, and whether or not it is billed in full or in part to the

listed corporation, the information about this must nevertheless be comprehensive. In fact, even if

the compensation is not a direct charge for the company, shareholders must be in a position to

ensure that incentive-based mechanisms related to their company's performance are properly in

place, and that the overall compensation is not excessive. The information must therefore include

justification for the use of this extraordinary procedure and, for example, show that the executive

officer spends some of his or her time managing this third company, if its interests are sufficiently

aligned with those of the listed corporation for there to be no risk of conflict and if this management

does not significantly reduce the availability of the executive officer. All of the elements

demonstrating that the terms stipulated by the code are fully complied with must also be presented.

Consultation of shareholders on individual executive directors' compensation

– § 24.3

According to § 24.3 of the AFEP-MEDEF Code, “the Board must present the compensation of

executive directors at the Annual General Meeting. This presentation must cover the elements of the

compensation due or awarded at the end of the closed financial year to each executive director:

the fixed part;

the annual variable part and, where necessary, the multi-annual variable part with the

objectives that contribute to the determination of this variable part;

extraordinary compensation;

stock options, performance shares, and any other element of long-term compensation;

benefits linked to taking up or terminating office;

supplementary pension scheme;

any other benefits”.

The AFEP-MEDEF Code states that this presentation should be followed by an advisory vote by

shareholders. In this regard, the code recommends that at the shareholders' vote, one resolution be

presented for the Chief Executive Officer or the Chairman of the Management Board and one

resolution for the deputy chief executive officers or for the other members of the Management

Board2.

Finally, the AFEP-MEDEF Code states that: “when the ordinary shareholders' meeting issues a

negative opinion, the Board, acting on the advice of the compensation committee, must discuss this

matter at another meeting and immediately publish on the company's website a notice detailing how

it intends to deal with the opinion expressed by the shareholders at the General Meeting”.

2 See Question 3 below for the case of a non-executive Chairman in a company with a Board of Directors.

10

Question 1: What should the content of this presentation be?

A distinction should be made between informing shareholders about executive directors' compensation and the elements of compensation that are the subject of a vote.

Informing shareholders

In their annual report (which can, if applicable, be incorporated into the reference document), companies should present a comprehensive, specific chapter, prepared with the assistance of the compensation committee, dedicated to informing shareholders about executive directors' compensation, i.e. description of the compensation policy for these executive officers, detailed presentation of the annual and, if applicable, multi-annual fixed and variable parts (showing the amounts due and paid for the two previous financial years), information about options and performance shares, benefits in kind, commitments related to termination of office, pension schemes, etc.

This chapter shall generally contain the information that, in accordance with the Commercial Code, should appear in the management report drawn up by the Board and in the Chairman's report approved by the Board, this information being presented in the format recommended by the AFEP-MEDEF Code and the AMF.

Elements of compensation that are the subject of an advisory vote by shareholders

The AFEP-MEDEF Code recommends submitting for the opinion of shareholders the elements of compensation due or awarded to each executive director in respect of the closed financial year. This opinion shall be preceded by a presentation of these elements with the aim of informing their voting.

What is therefore being recommended is an ex post vote concerning the amount or valuation of the elements of compensation due or awarded during the last closed financial year, and not an ex ante vote concerning the compensation policy for the current financial year.

The shareholders' meeting shall give its opinion about the elements of compensation due or awarded during the closed financial year to each executive director by all companies affiliated to the group.

The elements of compensation “due” refer to the cash elements acquired by the executive officer that are certain, both in terms of their principle and amount, whether or not they have already been paid to the executive officer.

The elements of compensation “awarded” refer to the elements in securities and/or cash, the principle of which is established but the amount and/or number of which has not yet been acquired at the time when they are implemented (or “awarded”) and which, as a result, can only, if applicable, be given an accounting valuation.

These elements are specified below:

1. Fixed compensation

Element of the compensation submitted to a vote

amount of fixed compensation due in respect of the closed financial year

Presentation

any change in relation to the previous financial year

11

2. Annual variable compensation3

If the principle of annual variable compensation is established:

Element of the compensation submitted to a vote

amount of variable compensation due in respect of the closed financial year

if the amount is equal to 0, indication in this case that the performance criteria were not met or that the executive director waived his or her variable part

Presentation

indication of the different quantitative and/or qualitative criteria used to establish this variable compensation (subject, if applicable, to constraints related to the confidentiality of some of this information)

maximum percentage of the fixed compensation that the variable compensation can represent

if qualitative criteria are used, indication of the limit set for the qualitative part

If the principle of annual variable compensation is not established:

Element of the compensation submitted to a vote

indication that this element is not applicable

Presentation

indication that the principle of awarding variable compensation is not established

3. Deferred annual variable compensation

Deferred variable compensation is a form of annual variable compensation. The payment of variable compensation is, in fact, partly deferred over several financial years. For example, variable compensation due in respect of the closed financial year shall be paid partly in year N and partly in years N+1, N+2 and N+3, subject to meeting performance conditions. However, this is variable compensation due in respect of the closed financial year.

If the variable compensation due or awarded in respect of the closed financial year is deferred in full or in part:

Element of the compensation submitted to a vote

amount of deferred variable compensation due in respect of the closed financial year

if conditional deferred variable compensation is awarded, valuation of this deferred variable compensation at its book value

Presentation

description of the mechanism and, if applicable, the different quantitative and/or qualitative criteria on which the deferred payment of this variable compensation over one or more financial years is conditional

if qualitative criteria are used, indication of the limit set for the qualitative part

If the principle of deferred variable compensation is not established:

Element of the compensation submitted to a vote

indication that this element is not applicable

3 If the annual variable compensation is deferred in part, no. 3 applies.

12

Presentation

indication that the principle of awarding deferred variable compensation is not established

4. Multi-annual variable compensation

As multi-annual variable compensation is not linked to a single financial year, it is submitted to a vote by shareholders if an amount is due to the executive officer as a result of the implementation of the multi-annual variable compensation mechanism from which he or she benefits. This multi-annual variable compensation mechanism must, in any event, be described in the presentation even if an amount is not due in respect of the financial year, or be specifically referred to in the reference document.

If the principle of multi-annual variable compensation is established and an amount is due in respect of the closed financial year

Element of the compensation submitted to a vote

amount of the multi-annual variable compensation due in respect of the closed financial year, including when the amount is equal to 0, indicating, in this case, that the performance criteria were not met or that the executive officer waived his or her multi-annual variable compensation

Presentation

description of the mechanism(s) and the different quantitative and/or qualitative criteria used to establish this multi-annual variable compensation

If the principle of multi-annual variable compensation is established but no amount is due in respect of the closed financial year (except in the aforementioned case of not meeting performance criteria)

Element of the compensation submitted to a vote

indication that no amount is due

Presentation

description of the mechanism(s) and the different quantitative and/or qualitative criteria used to establish this multi-annual variable compensation or specific referral to the description given by the reference document

if qualitative criteria are used, indication of the limit set for the qualitative part

If the principle of multi-annual variable compensation is not established

Element of the compensation submitted to a vote

indication that this element is not applicable

Presentation

indication that no multi-annual variable compensation mechanism exists

However, if a maximum amount is determined when the mechanism is implemented by the Board

during the closed financial year, companies can select the presentation below:

Element of the compensation submitted to a vote

maximum amount of multi-annual variable compensation of which the mechanism was decided by the Board during the closed financial year

13

Presentation

description of the mechanism(s) and the different quantitative and/or qualitative criteria used to establish this multi-annual variable compensation

if qualitative criteria are used, indication of the limit set for the qualitative part

for subsequent financial years and as long as the mechanism lasts, description of the mechanism(s) and the different quantitative and/or qualitative criteria used to establish this multi-annual variable compensation or specific referral to the description given by the reference document

Companies subject to specific compensation regulations shall adapt the mechanism according to

their specific circumstances.

5. Extraordinary compensation

If the principle of extraordinary compensation is established:

Element of the compensation submitted to a vote

amount of the extraordinary compensation due in respect of the closed financial year

Presentation

justification for the extraordinary compensation

If the principle of extraordinary compensation is not established:

Element of the compensation submitted to a vote

indication that this element is not applicable

Presentation

indication that the principle of extraordinary compensation is not established

6. Stock options/performance shares and any other element of long-term compensation4

If an award is made during the closed financial year

Element of the compensation submitted to a vote

number and accounting valuation of the stock options and performance shares awarded during the closed financial year according to the method adopted for preparing the consolidated financial statements

Presentation

indication of the performance conditions on which the exercise of the options or the definitive acquisition of the shares are conditional

indication of the percentage of the capital represented by the award to the executive director

reminder of the date of authorisation by the shareholders' meeting, the resolution number and the date of the award decision by the Board

If no award is made during the closed financial year

Element of the compensation submitted to a vote

indication that this element is not applicable

4 Other elements of long-term compensation refer to awards of financial instruments, such as redeemable stock purchase warrants (BSAR) and stock purchase warrants (BSA).

14

Presentation

indication that no award was made during the closed financial year

7. Benefit for taking up a position (‘welcome bonus’)

Element of the compensation submitted to a vote

amount due in respect of a benefit for taking up a position in the event of the arrival of a new executive director during the closed financial year

Presentation

circumstances and grounds that gave rise to the payment of this benefit for taking up a position

8. Benefit for termination of office: termination payment/non-competition benefit

If a commitment exists and if the termination of office takes place during the closed financial year

Element of the compensation submitted to a vote

amount due in respect of a termination payment/non-competition benefit

Presentation

description of the terms and conditions of the commitment made by the company in respect of the termination of office of the executive director

reminder of the date of the decision by the Board, the date of submission to the shareholders' meeting and the resolution number in the framework of the procedure for related party transactions (conventions réglementées)

reminder of the decision by the Board stating whether (or not) the terms are met and, if applicable, settling the amount of the benefit

If a commitment exists and if the termination of office does not take place during the closed financial year

Element of the compensation submitted to a vote

indication that no amount is due in respect of the closed financial year

Presentation

description of the terms and conditions of the commitment made by the company in respect of the termination of office of the executive director

reminder of the date of the decision by the Board, the date of submission to the shareholders' meeting and the resolution number in the framework of the procedure for related party transactions

If no commitment exists

Element of the compensation submitted to a vote

indication that this element is not applicable

Presentation

indication that no commitment exists

15

9. Supplementary pension scheme

If the executive director is eligible for a supplementary pension scheme

Element of the compensation submitted to a vote

indication that no amount is due in respect of the closed financial year

Presentation

description of the supplementary pension scheme with defined benefits and/or defined contributions

- scheme with defined benefits: information about individual potential rights, particularly the reference income and the maximum percentage of this income which the supplementary pension scheme would confer

- scheme with defined contributions: if applicable, information about the contributions paid by the company and, if the company wants to improve its communication and has the corresponding information, estimate of the percentage of the executive officer's compensation that this scheme might confer

specify whether the scheme has been closed (on which date)

reminder of the date of the decision by the Board, the date of submission to the shareholders' meeting and the resolution number in the framework of the procedure for related party transactions

If the executive director is not eligible for a supplementary pension scheme

Element of the compensation submitted to a vote

indication that this element is not applicable

Presentation

indication that the executive officer is not eligible for a supplementary pension scheme

10. Directors' fees

If the executive officer receives directors' fees

Element of the compensation submitted to a vote

amount of directors' fees due in respect of the closed financial year

Presentation

rules governing the award of directors' fees: fixed part, variable part

If the executive officer does not receive directors' fees

Element of the compensation submitted to a vote

indication that this element is not applicable

Presentation

indication that the executive officer does not receive directors' fees

16

11. Any other benefits

If the executive officer receives any other benefit(s)

Element of the compensation submitted to a vote

valuation of the benefits

Presentation

description of any other benefits that the executive officer received during the closed financial year (car, accommodation, etc.)

If the director does not receive any other benefit(s)

Element of the compensation submitted to a vote

indication that this element is not applicable

Presentation

indication that the executive officer does not receive any other benefit(s)

Question 2 – What form should the presentation take?

The AFEP-MEDEF Code does not recommend any particular presentation format for the elements of compensation to which the advisory vote relates. Companies are therefore free to determine this presentation, provided it is comprehensive and easily understood. Several presentation formats may be contemplated (see content below), for example:

prepare a specific paragraph in the annual report/reference document about the elements of compensation submitted to a vote, which may also take the form of a summary table of the compensation due or awarded in respect of the last closed financial year, and make specific reference to it (option 1)

or

prepare a consolidated and clear presentation in the annual report/reference document of the notices published after the Board has set the elements of compensation of the executive directors, and make specific reference to it (option 2)

or

preferably, prepare a specific report (option 3)

The Board's report to the shareholders' meeting concerning the draft resolutions (often contained in the meeting brochure or the reference document) should contain this presentation or refer to it. These presentations may, if applicable, include cross-references to the annual report/reference document for more details.

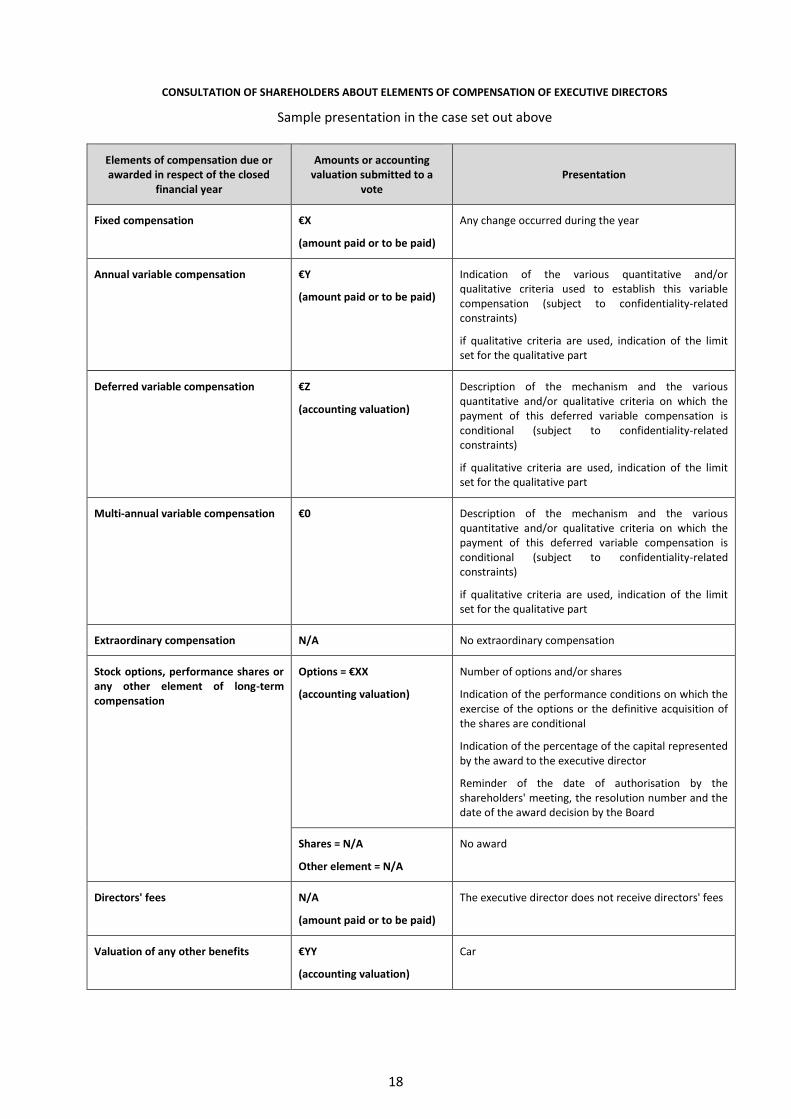

Sample presentation

If, for example, the factual situation is as follows concerning the closed financial year (financial year N):

fixed compensation of €X in respect of the closed financial year

annual variable compensation of €Y in respect of the closed financial year

implementation of conditional deferred variable compensation over the period N+1 to N+3 valued from an accounting point of view at €Z

17

implementation of multi-annual variable compensation (without a predetermined ceiling) in respect of the closed financial year

no extraordinary compensation

award of options during the closed financial year valued from an accounting point of view at €XX; no award of performance shares and no other element of long-term compensation

existence of a deferred commitment (termination payment), the executive officer's term of office not having ended during the closed financial year; no non-competition clause

the executive director is eligible for a supplementary pension scheme with defined benefits

the executive director does not receive directors' fees

the executive director receives any other benefits valued at €YY in respect of the closed financial year

18

CONSULTATION OF SHAREHOLDERS ABOUT ELEMENTS OF COMPENSATION OF EXECUTIVE DIRECTORS

Sample presentation in the case set out above

Elements of compensation due or awarded in respect of the closed

financial year

Amounts or accounting valuation submitted to a

vote Presentation

Fixed compensation €X

(amount paid or to be paid)

Any change occurred during the year

Annual variable compensation €Y

(amount paid or to be paid)

Indication of the various quantitative and/or qualitative criteria used to establish this variable compensation (subject to confidentiality-related constraints)

if qualitative criteria are used, indication of the limit set for the qualitative part

Deferred variable compensation €Z

(accounting valuation)

Description of the mechanism and the various quantitative and/or qualitative criteria on which the payment of this deferred variable compensation is conditional (subject to confidentiality-related constraints)

if qualitative criteria are used, indication of the limit set for the qualitative part

Multi-annual variable compensation €0

Description of the mechanism and the various quantitative and/or qualitative criteria on which the payment of this deferred variable compensation is conditional (subject to confidentiality-related constraints)

if qualitative criteria are used, indication of the limit set for the qualitative part

Extraordinary compensation N/A No extraordinary compensation

Stock options, performance shares or any other element of long-term compensation

Options = €XX

(accounting valuation)

Number of options and/or shares

Indication of the performance conditions on which the exercise of the options or the definitive acquisition of the shares are conditional

Indication of the percentage of the capital represented by the award to the executive director

Reminder of the date of authorisation by the shareholders' meeting, the resolution number and the date of the award decision by the Board

Shares = N/A

Other element = N/A

No award

Directors' fees N/A

(amount paid or to be paid)

The executive director does not receive directors' fees

Valuation of any other benefits €YY

(accounting valuation)

Car

19

Elements of compensation due or awarded in respect of the closed

financial year that are or have been submitted to a vote by the

shareholders' meeting in respect of the procedure for related party transactions and commitments

Amounts submitted to a vote Presentation

Termination payment €0 Indication of the terms and conditions of the commitment made by the company in respect of the termination of office of the executive director

Reminder of the date of the decision by the Board, the date of submission to the shareholders' meeting and the resolution number in the framework of the procedure for related party transactions

Non-competition benefit N/A There is no non-competition clause

Supplementary pension scheme

€0 Description of the supplementary pension scheme with defined benefits

Specification whether the scheme has been closed (date)

Reminder of the date of the decision by the Board, the date of submission to the shareholders' meeting and the resolution number in the framework of the procedure for related party transactions

Question 3: Should a specific resolution be specified in the case of a non-executive Chairman?

The AFEP-MEDEF Code recommends:

in a company with a Board of Directors: a separate resolution for the managing director or Chief Executive Officer and a resolution for the deputy chief executive officer(s).

in a company with a Management Board and Supervisory Board: one resolution for the Chairman of the Management Board and one resolution for the other members of the Management Board.

However, the title of § 24.3 refers to executive directors (dirigeants mandataires sociaux) for which the definition on p. 1 of the code includes the non-executive Chairman of the Board of Directors. In contrast, the Chairman of the Supervisory Board is not included in this definition.

It therefore appears advisable for the shareholders' meeting to give an opinion concerning the individual elements of compensation of the non-executive Chairman of the Board of Directors due or awarded in respect of the closed financial year and to present a specific resolution for this purpose. Given that the compensation of the separate Chairman is generally less complex, it is not necessary to include each of the headings (for example, extraordinary compensation, stock options, performance shares, termination payments, etc.) with the phrase “not applicable”. However, if he or she receives elements of compensation in addition to fixed compensation, these elements must be detailed.

20

Question 4: How should the draft resolution(s) be written?

It is proposed stating, either in the explanations of the resolutions or in the wording of the resolution, that the elements of compensation due or awarded in respect of the closed financial year to each executive director of the company are subject to the opinion of the shareholders in accordance with the recommendation of § 24.3 of the AFEP-MEDEF Corporate Governance Code revised in June 2013, to which the company refers pursuant to Article L. 225-37 of the Commercial Code.

The following sample resolution is proposed:

Title of the resolution

Opinion about the elements of compensation due or awarded in respect of the financial year closed on xx/xx/xxxx to [name], [position]

“The shareholders' meeting, [consulted pursuant to the recommendation of § 24.3 of the AFEP-MEDEF Corporate Governance Code of June 2013, which is the company's reference code pursuant to Article L. 225-37 of the Commercial Code], ruling according to the quorum and majority conditions required for ordinary shareholders' meetings, hereby gives a favourable opinion concerning the elements of compensation due or awarded in respect of the financial year closed on XX/XX/XXXX to [name] as presented in the annual report/reference document on page…".

In the case of a second resolution covering the deputy chief executive officer(s) or the members of the Management Board, the resolution should be adapted accordingly.

Question 5: What are the consequences of a negative opinion?

It is pointed out that the vote is negative when the majority of the votes of the shareholders present or represented has not been achieved (simple majority in AGMs).

In the event of a negative opinion, the AFEP-MEDEF Code recommends that the Board, acting on the advice of the compensation committee, should discuss this matter at another meeting and immediately publish on the company's website a notice detailing how it intends to address shareholders' expectations.

Periods and conditions for implementing the recommendations of the AFEP-

MEDEF Code

The revised corporate governance code was published on 16 June 2013. The new recommendations are applicable as from 17 June 2013, subject to the following specific features:

21

RECOMMENDATIONS OF THE CODE IMPLEMENTATION PERIODS AND CONDITIONS

Representation of men and women on Boards (§ 6)

- Achievement of a percentage of at least 20% women within a period of three years from the 2010 shareholders' meeting, i.e. no later than by the end of the 2013 AGM.

- Achievement of a percentage of at least 40% women within a period of six years from the 2010 shareholders' meeting, without prejudice to specific provisions applicable to Boards comprising eight members or less, i.e. no later than by the end of the 2016 AGM.

- For companies whose shares are newly admitted to trading on a regulated market, these three-year and six-year periods are counted from the year of admission.

Presence of an employee director on the compensation committee (§ 18.1)

Companies whose Board already includes one or more employee directors are subject to this recommendation immediately.

For companies whose Board did not previously include an employee director and which come within the scope of the Law on employment security of 2013, the employee director(s) should be elected or appointed six months after the shareholders' meeting making the statutory changes required for their election or appointment, with the AGM itself having to take place no later than in 2014.

The recommendation is applicable from the employee director(s) taking office, which must take place within the aforementioned periods.

Preponderant variable portion for directors' fees (§ 21.1)

This recommendation applies to directors' fees allocated in respect of 2014.

Limitation of the number of directorships in listed corporations, including foreign corporations, to five (§ 19)

In the event of the limit laid down being exceeded, this recommendation shall apply at the time of appointment or the next renewal of a director's term of office.

The same implementation period may be adopted concerning the recommendation relating to the number of executive directorships.

Non-competition benefits (§ 23.2.5) It is stated that, when the agreement is being concluded, the Board must incorporate a provision that authorises it to waive the implementation of the non-competition agreement when the executive director leaves. This recommendation applies to agreements concluded after 16 June 2013.

Supplementary pension schemes (§.23.2.6)

The conditions laid down (group of beneficiaries broader than the sole executive directors, reasonable requirements of seniority of at least two years, increase in potential rights progressive, limitation to 45% of the reference income, etc.) do not apply to plans closed to new beneficiaries, as these may not be altered.

Consultation of shareholders on individual executive directors' compensation (§ 24.3)

This consultation of shareholders shall apply from the 2014 AGMs.

High Committee in charge of monitoring implementation of the code (§ 25.2)

The High Committee was set up on 8 October 2013.

22

Summary of the information to be included in annual reports/reference

documents in order to meet the “comply or explain” requirement laid down

by Article L. 225-37 or L. 225-68 of the Commercial Code

In order to ensure the effective application of the “comply or explain” rule and take into account the changes to the code, AFEP and MEDEF have updated the summary of the information to be included in annual reports/reference documents (however, no order of presentation is required).

Reference to a corporate governance code

1. Companies' implementation of the “comply or explain” rule

Indication whether the company refers to the AFEP-MEDEF Code, specifying the provisions that have been deviated from and the reasons why

Indication in a heading or specific table of the recommendations that the company does not apply, with the relevant explanations5

If a company subject to a referral by the High Committee decides not to follow its recommendations, it must mention in its annual report/reference document the latter's opinion and the reasons why it has decided not to act on its recommendations

The governance structure

2. Mode of management

Mode of management chosen: company with a Board of Directors (separation or combination of the Chairman’s and CEO’s offices) or with a Management Board and Supervisory Board, followed by an explanation of the reasons and justifications for the choice, particularly in the event of a change in governance

In the event of the separation of the offices of Chairman and Chief Executive Officer, description of the tasks entrusted, if applicable, to the Chairman of the Board in addition to those conferred upon him or her by law

In the event of specific tasks entrusted to one director, particularly with the title of Lead Independent Director (administrateur référent) or Vice-Chairman, description of the tasks and the resources and prerogatives to which he or she has access

The Board of Directors

3. Independence of members of the Board of Directors

Number and names of the independent directors

Independence criteria adopted

Evaluation of how significant the relationship is with the company and explanation of the criteria that led to this evaluation

Conclusion of the review relating to independence

5 The explanation must be comprehensible, relevant and detailed. It must be substantiated and adapted to the company's particular situation and must convincingly indicate why this specific aspect justifies an exemption; it must state the alternative measures that have been taken if applicable, and must describe the actions that allow the company to comply with the aims of the relevant measure within the code. If a company intends to implement a recommendation in the future from which it has provisionally deviated, it must state when this temporary situation will come to an end.

23

4. Members of the Board of Directors

Beginning of the directorship (current directorship or first directorship) and expiry of the directorship

Term of the directorship and, if applicable, staggering rules

Age, gender and nationality of the director

Principal position

List of the directorships and positions held in other French or foreign corporations, clearly showing which are listed and which belong to the same group

Number of shares held in the company

Proportion of women on the Board

Legal basis of the election or appointment: art. L. 225-17, L. 225-23, L. 225-27, L. 225-27-1 of the Commercial code or other (privatised companies, etc.)

5. Information about meetings of the Board of Directors

Number of meetings

Rate of attendance of members

6. Evaluation of the Board of Directors

Performance of evaluations (point on the agenda or formal evaluation) and, if appropriate, any action taken

7. Internal rules of the Board of Directors

Existence

Stipulations concerning: the limitations that the Board of Directors places on the powers of the Chief

Executive Officer the principle whereby any material transaction outside the scope of the stated

strategy is subject to prior approval by the Board the rules whereby the Board is informed in particular of the corporation's financial

situation, cash position and commitments

The Board and the market

8. Financial rating

Company's ratings by financial rating agencies as well as any changes that have occurred during the financial year or no change

Board committees6

9. Audit committee

Existence

Stipulations concerning its duties and operating procedures

6 If there are other Board committees than as referred to herein, the same presentation should be used.

24

Membership names of the members and number of independent directors indication about the financial or accounting competence of the members

Activity report number of meetings rate of attendance report on the committee's activity during the previous financial year information about the existence of a presentation by the statutory auditors stressing

the essential points of the results of the statutory audit and the accounting methods chosen

information about the existence of a presentation by the Chief Financial Officer describing the corporation's risk exposures and its material off-balance sheet commitments

information about the selection procedure for the renewal of the statutory auditors

Working methods minimum period for reviewing the accounts prior to the review by the Board interview of the statutory auditors, and also the individuals responsible for finance,

accounting and treasury matters interview of the individuals responsible for internal audit and risk control existence of the option to call on outside experts

10. Committee in charge of appointments or nominations

Existence

Stipulations concerning its duties and operating procedures

Membership names of the members and number of independent directors involvement of the Chief Executive Officer in the proceedings of the committee

responsible for appointments or nominations

Activity report report on its activity during the previous financial year number of meetings rate of attendance

11. Committee in charge of compensation

Existence

Stipulations concerning its duties and operating procedures

Membership names of the members and number of independent directors information about the committee being chaired by an independent director information about the presence of an employee director on the committee

Activity report report on its activity during the previous financial year number of meetings rate of attendance

25

Concurrent executive director and employee status

12. Employment contract/directorship

Termination of the employment contract (table 10 appended to the code)

If the employment contract is maintained (suspended), indication of the justification for the Board's decision

Executive directors' compensation

13. Compensation of members of the Board of Directors

Overall and individual amount of directors' fees (table 3 appended to the code)

Rules for the allocation of these directors' fees

Mention that the variable part related to regular attendance or participation in a committee outweighs the fixed part

Information about directors' fees or extraordinary compensation allocated to a Lead Independent Director (administrateur référent) or Vice Chairman

14. Individual executive directors' compensation

Policy for determining executive directors' compensation

Rules governing changes to the fixed part

Rules for awarding the annual and/or multi-annual variable part indication of the criteria for determining this variable part: qualitative and

quantitative criteria (subject to the confidentiality of certain elements) limits placed on the qualitative part when there is one relationship between the variable part and the fixed part indication of the application of criteria regarding what had been specified during the

financial year and mention of the achievement of personal objectives detailed individual compensation of each executive director according to the

standardised presentation tables for executive officers appended to the code (tables 1 and 2)

rules laid down by the Board for holding a certain number of the company's shares as registered shares

15. Stock options

For all beneficiaries:

Award policy applicable to all beneficiaries, and separately, if applicable, the award policy applicable to executive directors

Nature of the options (purchase or subscription options)

No discount

Criteria used to define the categories of beneficiaries

Periodicity of the plans

Dilutive impact of each option award, except in the case of awards of stock purchase options

Summary table of the existing option plans according to table 8 appended to the code

Schemes involving employees in corporate performance (incentive scheme, profit-sharing scheme other than the mandatory scheme, granting of bonus shares, etc.)

26

In addition, for stock options awarded to executive directors:

Standardised presentation according to the tables appended to the code (tables 4 and 5) mentioning the valuation of the options awarded during the financial year according to the method used for the consolidated financial statements (table 4)

Fraction (of the capital) awarded to each executive director

Performance requirements decided by the Board for the exercise of the options (internal or external requirements with the option of combining these internal and external performance requirements where possible and relevant)

Mention of the formal commitment by the executive officer not to engage in any hedging transactions

Exercise prohibition period preceding the disclosure of the annual and interim financial statements

16. Performance shares

For all beneficiaries:

Award policy applicable to employees or to certain categories of employees and to executive directors

The conditions and, if applicable, the criteria, where determined by the Board

Dilutive impact of each share award (except in the case of existing share awards)

Summary table of the existing share awards according to table 9 appended to the code

Schemes involving employees in corporate performance (incentive scheme, profit-sharing scheme other than the mandatory scheme, granting of bonus shares, etc.)

In addition, for performance shares awarded to executive directors:

Standardised presentation according to the tables appended to the code (tables 6 and 7) mentioning the valuation of the shares awarded during the financial year (table 6)

Fraction (of the capital) awarded to each executive director

Performance requirements decided by the Board for the acquisition of shares (internal or external requirements with the option of combining these internal and external performance requirements where possible and relevant)

Information about the acquisition (at the end of the retaining period) of a specified quantity of shares determined by the Board

Mention of the formal commitment by the executive officer not to engage in any hedging transactions

17. Benefits for taking up a position (‘welcome bonus’)

- Mention of benefits for taking up a position granted to a new executive director

27

18. Termination payments

Indication of the performance conditions applicable

Mention that the performance conditions are assessed over at least two financial years

Indication that the indemnification of the executive officer is not allowed unless his or her departure is imposed and linked to a change of control or strategy

Two-year ceiling (fixed and variable compensation) and, if applicable, inclusion of the non-competition benefit in this ceiling

19. Non-competition benefit

Mention of the stipulation laid down, at the time of any new agreement, authorising the Board to waive the implementation of the agreement when the executive director leaves

Two-year ceiling (fixed and variable compensation) and, if applicable, inclusion of the termination payment in this ceiling

20. Supplementary pensions

Pension systems or commitments provided: existence or otherwise of a specific pension scheme for executive directors

Main features of the scheme

For schemes with defined benefits: broader group of beneficiaries than the sole executive directors, minimum seniority requirement of two years in order to benefit from it, progressive increase in rights depending on seniority limited to 5% of the beneficiary's compensation, benchmark period taken into account for the calculation of the benefits which must cover several years, existence of a ceiling of 45% of the income which the supplementary pension scheme would confer (see paragraph concerning § 23.2.6 of the code above).