annual results presentation for the 53 …€¢wholesale performance affected by deflation in ......

TRANSCRIPT

ANNUAL RESULTS PRESENTATION FOR THE 53 WEEKS ENDED 31 DECEMBER 2017

AGENDA

1. FINANCIAL REVIEW2. OPERATIONAL REVIEW3. STRATEGY & PROSPECTS

FINANCIAL REVIEW

Hans van Lierop

Financial summary (53 weeks)

SALES

R1.5bn 2 __

14.0%52 weeks: R1.3 billion

2016: R1.3 billion

GROSS PROFITMARGIN

TRADING PROFIT BEFORE INTEREST & TAX

HEADLINEEARNINGS

2016: 19.0%

R93.7bn2.7%

52 weeks: R92.1 billion

2016: R91.3 billion

18.8 % R2.7bn4.2%

52 weeks: R2.5 billion

2016: R2.6 billion

Financial highlights

SALES GROWTH EXPENSE MANAGEMENTTRADING PROFIT BEFORE INTEREST & TAX

HEADLINE EARNINGS

2.7 % 1.6% 4.2 % 14.0%

0.8% COMPARABLE 1.3% COMPARABLE

1.0% 1.2% 5.4 % 1.6%

DEC 2017

53 WEEKS

DEC 2017

52 WEEKS

COMP

SOUTH AFRICA SALES

FOOD & LIQUOR FOOD & LIQUOR

Good recovery in H2

8.3%

SA VS. EX-SA SALES SA SALES EX-SA SALES

Ex-SASales

91.7%

58% 50%

DURABLES

50%

4.8%

SASales 1.5%

Group Durables sales 0.9%

Group Food & Liquor sales 2.4%

EX-SA SALES

Ex-SA sales impacted by

currency weakness

DURABLES

42%

SA Liquor 8.4%

SA RetailFood 3.0%

Ex-SA Liquor 2.7%

Ex-SA Food 1.1%

SALES BY GEOGRAPHY

SALES BY CATEGORY

Constant currency 3.5%

TOTAL GROUP

Ex-SA Durables 10.4%

SA Durables 0.2%

Gross profit margin

Dec 2016

19.0%

PRODUCT MIX FOOD

DEFLATION

Lower Durable goods participation driving margin decline

GROSS PROFIT MARGIN

Dec 2017

18.8%

GROSS PROFIT MARGIN

0

10

20

30

40

50

60

70

80

90

100

Bill

ion

s

Sales Operating expenses

Exceptional expense management

Sustained cost discipline in difficult sales environment

• Maintained low cost

as % of sales

• Operational efficiency

• Capex efficiencies

DEC 2015 DEC 2016 DEC 2017

16.3% 16.3% 16.4%

Expense categories

EMPLOYMENT COSTS DEPRECIATION

OCCUPANCY COSTS

OTHER OPERATING EXPENSES

0.5 %

2.7% COMPARABLE

• Efficient scheduling

• Reduced shifts in DCs

• Selective replacement

• 48,000 FTEs (stable)

• 11 new store openings

• Capex spend heavily weighted

to second half

• Higher proportion of IT assets

in capex

• 2.8% increase in new trading

space

• Reduced rentals on lease

reviews

• Benefit of owned properties

• Focus on containing costs

• Administrative efficiency

• Reduction of non-essential

activities

• Leveraging group synergies

5.7 %

3.3% COMPARABLE

1.3%

0.5% COMPARABLE

1.4%

0.4% COMPARABLE

Divisional performance

R373.5m53 weeks: R454.3 million

2016: R390.7 million

R1,256.6m53 weeks: R1,313.1 million

2016: R1,254.2 million

R735.5m53 weeks: R797.5 million

2016: R715.3 million

R127.1m53 weeks: R179.0 million

2016: R276.9 million

Trading profit before interest and taxation 5.4% (53 weeks: 4.2%)

MASSDISCOUNTERS MASSWAREHOUSE MASSBUILD MASSCASH

• Soft sales in Durables

categories

• Good margin management

• Great expense management

• Good sales given the

environment

• Liquor performed

exceptionally well

• Some margin pressure from

product mix

• Expenses well managed

• Strong sales performance

• Higher Retail participation

• Great expense management

• Strong sales in Retail

• Weak sales in Wholesale

• Margin pressure from high

participation of commodities

• Good expense management

The 'trading profit before interest and tax' above is the amount per the Preliminary Condensed Consolidated Income Statement less the BEE transaction IFRS 2 charge.

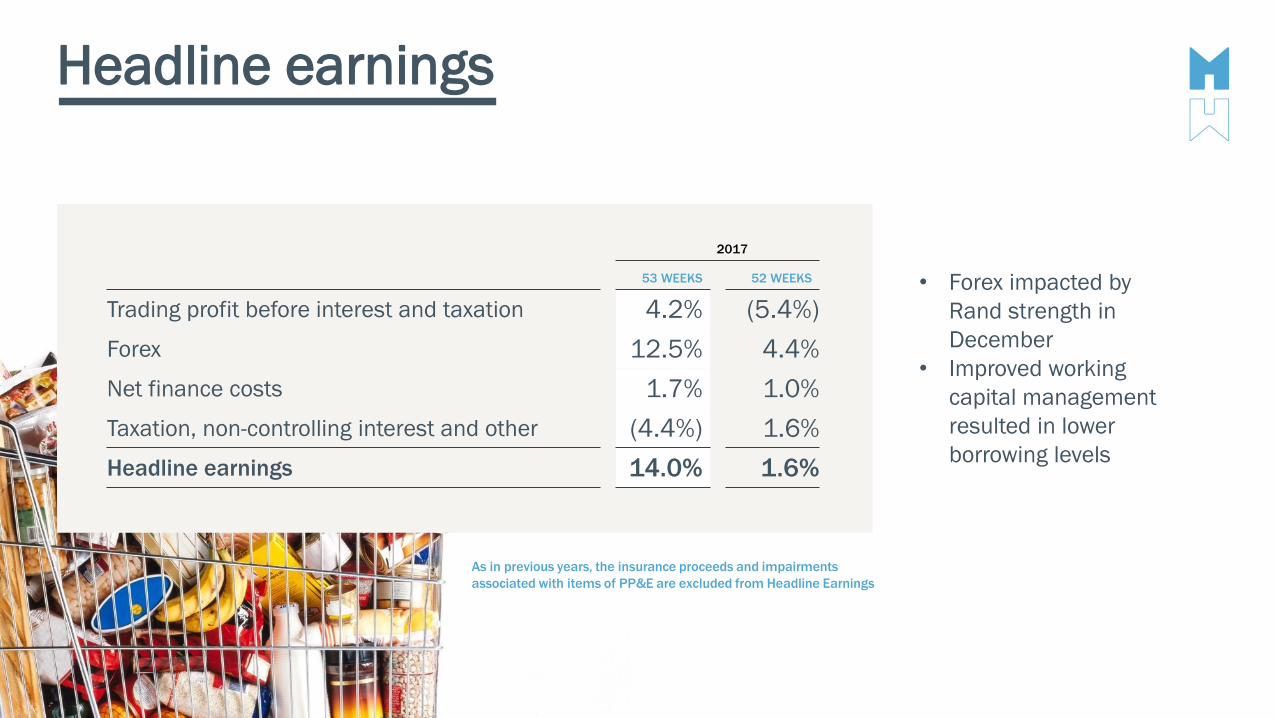

Headline earnings

As in previous years, the insurance proceeds and impairments

associated with items of PP&E are excluded from Headline Earnings

• Forex impacted by

Rand strength in

December

• Improved working

capital management

resulted in lower

borrowing levels

2017

53 WEEKS 52 WEEKS

Trading profit before interest and taxation 4.2% (5.4%)

Forex 12.5% 4.4%

Net finance costs 1.7% 1.0%

Taxation, non-controlling interest and other (4.4%) 1.6%

Headline earnings 14.0% 1.6%

Earnings

Earnings underpinned by strong cash generation

Rm DEC 2015 DEC 2016 DEC 2017

Operating cash before working

capital movements3,367 3,701 3,965

Working capital movements 370 (279) 706

Cash generated from operations 3,737 3,422 4,671

Interest and tax (1,068) (1,063) (1,389)

Replacement capex (984) (827) (679)

Free cash flow 1,685 1,532 2,603

CASH GENERATED FROM OPERATIONSEBITDA

Dec-15 Dec-16 Dec-17

R3

,12

2m

R3

,62

1m

R3

,60

0m

R3

,73

7m

R3

,42

2m

R4

,67

1m

Working capital

DEBTORS’ DAYSCREDITORS’ DAYSINVENTORY DAYS

• Intense focus on

stock management

•Debtors’ days stable

60

76

9

55

69

9

54

74

9

Dec-15 Dec-16 Dec-17

OPERATIONAL REVIEW

Guy Hayward

Key performances

total sales increase,

slowed in H2

comparable

decrease

sales growthMarket shares in

major appliances*

1.3%>35.0%3.0% 47%

* Source: GFK SA (Dec 2017)

RAPID GROWTHOF ONLINE SALES

SUPERB EXPENSE CONTROL

DURABLES SALES SOFT , GAINED MARKET SHARE

GOOD SA RETAIL FOOD GROWTH

Sales performance

MASSDISCOUNTERS

R20.0bn2016: R20.5bn

R27.3bn2016: R26.3bn

R13.0bn2016: R12.7bn

R31.9bn2016: R31.7bn

• Durables’ in deflation ( 2.5%)

“Real” comp sales improved in

H2 but still negative

• Game ex-SA sales decline 4.1%

but 10.5% in constant

currencies

• Strong Food & Liquor growth

( 5.9%)

• Marginally impacted by

deflation in commodities

• Soft Durables’ sales and

deflation

• Positive SA sales growth

( 3.2%)

• Strong Q4 sales performance.

Best in South African DIY / HI

• Negative ex-SA growth ( 7.1%),

but positive in constant

currencies ( 0.5%)

• Wholesale performance

affected by deflation in

commodities

• Negative ex-SA growth ( 5.0%)

• Good Retail sales growth of

5.8%

MASSWAREHOUSE MASSBUILD MASSCASH

4.2% comparable sales 2.4% comparable sales 1.6% comparable sales 2.3% comparable sales

Total sales 1.0%. Comparable sales 0.8%. New stores added 0.5%

SA Consumer Environment

-15

-10

-5

0

5

10

15

20

25

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22

% c

ha

ng

e

Actual Forecast

Growth in value of consumer spending on Durables (Source: BER)

• Consumer confidence was

negative & trended weaker

in 2015 to 2017

• Forecast average growth

in Durables’ spending

is 7.5%. This will benefit

Game, Makro & Builders

(in Durables’ sales)

• These forecasts do not

include any impact of

proposed 1% VAT hike

R109

R75

R34

R7

Commodities’ deflation

2016

EXPECTED INFLATIONARY GROWTH

DE

FLATIO

N

DEFLATIONARY IMPACT ON FOOD SALES

2017

An illustration

Commodities’ deflation – sales impact

COMMODITIES’ INFLATION /

DEFLATION IN 2016-17 MAKRO SALES IMPACTMASSCASH SALES IMPACT

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

No

v

De

c

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

No

v

De

c

2016 2017

Cost Inflation Sales Inflation

TOTAL MAKRO

MAKRO EXCL COMMODITIES

4.0%

4.9%

TOTAL MASSCASHWHOLESALE

MASSCASH WHOLESALE EXCL COMMODITIES

1.7%

1.5%

Builders

Game

Jumbo

BotswanaNamibia

Zambia

Mozambique

Uganda

Nigeria

Tanzania

Malawi

Ghana

Lesotho

Kenya

Africa

Ex-SA

R181mSA

R146m

SOUTH AFRICA

COMPETITORS

R39m

AFRICANSALES PER STORE

215,860M2 OF RETAIL SPACE

R7.6bnSALES

42STORES

STORE DETAILS

56 millionRSA POPULATION

429 millionAFRICA POPULATION

12COUNTRIES

28CITIES

SALES PER STORE FOUR TIMES HIGHER THAN COMPETITORS

Current portfolio

Swaziland

Builders

Game

Jumbo

BotswanaNamibia

Zambia

Mozambique

Uganda

Nigeria

Tanzania

Malawi

Ghana

Lesotho

Kenya

Swaziland

NEW

African growth

AFRICAN SPACE GROWTH (EX SA)>35.6%

2018KenyaKaren Waterfront

(Nairobi)

GhanaArchimoto (Accra)

Westhills (Accra)

MozambiqueMarginal (Maputo)

Zimpeto x 2 (Maputo)

ZambiaMakeni (Lusaka)

Twin Palms Mall (Lusaka)

2019NigeriaGateway (Abuja)

GhanaTakoradi

KenyaUhuru (Nairobi)

Village Market

(Nairobi)

Karen Waterfront

(Nairobi)

2020NigeriaIkeja (Lagos)

Maitama (Abuja)

Port Harcourt

ZambiaKitwe

Ndola

SwazilandMatsapha

GhanaTema (Accra)

ADDITIONAL SALES PER YEAR

R1.4bn

R0.8bn

R1.3bn

2018

2019

2020

Omnichannel

151 UNIQUE CUSTOMER

COLLECTION POINTS

SAP Hybris platforms:

• Builders (March 2017)

• Game (October 2017)

• Dion Wired (March 2018)

• Makro (September 2018)

FOUR ECOMMERCE

POINTS OF PRESENCE

MIGRATING TO A SINGLE SOFTWARE

SOLUTION

• 57 Builders Warehouse

stores

• 3 Dion Wired stores

• 21 Makro stores

• 70 Makro lockers

Wide & compelling Omnichannel offering

• Hi-tech

• Small appliances

• Major appliances

• Outdoor

• DIY

• Food

• Clothing

• Liquor

• Home Improvement

• Paint

• Garden

113 CATEGORIES

+327 millionPAGE VIEWS

61 millionVISITS

4%OF MAKRO’S TOTAL DURABLES SALES IN NOV & DEC ‘17

47% SALES GROWTH

• Builders Warehouse

launched in March

2017, and Q4 sales

were double those of

the year-to-date

• Game launched in

Nov 2017

OmnichannelQuarterly Online sales

Q1-2016 Q2-2016 Q3-2016 Q4-2016 Q1-2017 Q2-2017 Q3-2017 Q4-2017

Makro Dion Wired Builders Game

-0.2 -0.8

5.5

9.9

12.3

5.4

3.8

5.6

9.8

3.4

21

12.3

1514

8

21.2

8.7

15.4

Carbonated soft

drinks

Convenience

instant meals

Bath soaps Cheese Snacks Cereals Vitamins &

supplements

Long life fruit juice Oral care

Food / FMCG

Examples of categories growing ahead of the market

* Source: Information Resources Inc (IRi) (Dec 2017)

DEFINED GROCERY CATEGORIESANNUAL VALUE GROWTH %

Total market

Massmart

AUDIO-VISUAL

Television 2%

Navigation 4%

DVD-player/recorder 3%

MAJOR APPLIANCES

Vacuum cleaners 3%

Refrigeration 2%

Washing Machines 1%

GAMING/IT

Printing devices 1%

Media Tablets 1%

PC Software 3%

Durables

MASSMART MARKET SHARE GROWTHS

* Source: GFK SA (Dec 2017)

Private Label

Strong Private Label portfolio

Aro (Catering)

M Brand (Milk)

Campmaster, Logik,

Garden Master,

Aro, Trojan

Builders Pride,

Mastercraft,

Grip ,Stramm

15.2%

6.4%15FOOD

34GENERAL MERCHANDISE

9HOME IMPROVEMENT

58

RECOGNISED AS

NATIONAL CATEGORY LEADER

PRIVATE LABELSHARE VERSUSNATIONAL BRANDBRANDS IN PORTFOLIO

Black Friday: R1 billion sales

GROWTH

Makro 29%

Game 20%

Dion Wired 198%

Builders 100%

ONLINE SALES

increased to over

15% of Makro sales

SALES

31% in average Game

basket size

Update

Intense development and testing.

Implementation in Q1 2019. Legacy

system write-off of R11m in 2017

SAP ERP IN GAME MASSCASH CAPE TOWN WATER CRISISMerged Jumbo & Cambridge exec teams.

Lead by Kevin Vyvyan-Day. Combine

skills, reduce opex, leverage scale

Thorough contingency plans in place

for employees, customers, food safety,

store ops, health & safety

STRATEGY &PROSPECTS

Guy Hayward

Strategic priorities

Over the longer-term, our key areas of strategic focus remain unchanged:

To drive the growth and profitability

of the core South African business

over the medium-term

IMPROVE AND GROW OUR CORE BUSINESS

GROW AFRICA

GROW ONLINE/OMNICHANNEL

Sub-Saharan African expansion

through new stores in Builders

Warehouse, Game and Masscash

Expand, improve and refine our

online / ecommerce offerings in

DionWired, Game, Makro and

Builders Warehouse

Prospects

• The Group’s 2018 sales growth to date remains soft. Marked by higher sales growth to upper-income

customers and lower growth elsewhere

• Hopeful of an improved sales environment during 2018:

• New SA political leadership a very positive impact. Improving economic variables in the short-term,

the longer-term challenges are considerable but can be addressed

• Lower inflation, stronger Rand & potentially lower interest rates

• Commodities’ deflation to abate by mid-2018

• But uncertain about the impact of recent proposed VAT increase

Any reference to future financial

performance included in this

document has not been reviewed or

reported on by the Group’s external

auditors. The auditor’s report does

not necessarily report on all of the

information contained in this

announcement/financial results.

Shareholders are therefore advised

that in order to obtain a full

understanding of the nature of the

auditor’s engagement they should

obtain a copy of the auditor’s report

together with the accompanying

financial information from the

issuer’s registered office.

FOR FURTHER DETAILSWWW.MASSMART.CO.ZA/RESULTS2017

ADDITIONAL INFORMATIONCondensed Consolidated Income Statement

Tax Rate Reconciliation

Cash Flow Statement

Capital Expansion

Capex Per Category

Store Portfolio

Forecast Stores: Jan 2018 – Dec 2020

Restatement

New standards

Number of shares

Restated*

53 weeks 53rd week 52 weeks 52 weeks

December 2017 pro forma December 2017 December 2016 53 weeks 52 weeks

Rm (Reviewed) (note 5) (Pro forma) (Reviewed) % change % change

Revenue 94,029.1 1,586.8 92,442.3 91,564.9 2,7 1.0

Sales 93,735.2 1,586.6 92,148.6 91,250.0 2,7 1.0

Cost of sales (76,084.6) (1,284.5) (74,800.1) (73,924.7) (2.9) (1.2)

Gross profit 17,650.6 302.1 17,348.5 17,325.3 1.9 0,1

Other income 235.1 0.2 234.9 216.8 8.4 8.3

Depreciation and amortisation (1,095.4) - (1,095.4) (1,036.5) (5.7) (5.7)

Employment costs (7,402.9) (21.0) (7,381.9) (7,346.6) (0.8) (0.5)

Occupancy costs (3,187.0) (12.6) (3,174.4) (3,133.2) (1.7) (1.3)

Other operating costs (3,463.3) (17.5) (3,445.8) (3,397.8) (1.9) (1.4)

Trading profit before interest and taxation 2,737.1 251.2 2 485.9 2,628.0 4.2 (5.4)

Impairment of assets (18.9) - (18,9) (76.7) 75.4 75.4

Insurance proceeds on items in PP&E 58.8 - 58.8 98.1 (40.1) (40.1)

Operating profit before foreign exchange movements and interest 2,777.0 251.2 2,525.8 2,649.4 4.8 (4.7)

Foreign exchange loss (47.2) (7.3) (39.9) (141.8) 66.7 71.9

Operating profit before interest 2,729.8 243.9 2,485.9 2,507.6 8.9 (0.9)

- Finance costs (585.4) (10.8) (574.6) (601.0) 2.6 4.4

- Finance income 26.4 0.5 25.9 29.1 (9.3) (11.0)

Net finance costs (559.0) (10.3) (548.7) (571.9) 2.3 4.1

Profit before taxation 2,170.8 233.6 1,937.2 1,935.7 12.1 0.1

Taxation (649.1) (69.9) (579.2) (595.9) (8.9) 2.8

Profit for the year 1,521.7 163.7 1,358.0 1,339.8 13.6 1.4

Condensed Consolidated Income StatementExtract from Preliminary Reviewed Condensed Consolidated Results for the year ended 31 December 2017

* Certain comparative figures shown do no correspond with the 2016 financial statements and reflect statements made. Refer to note 6.

Tax rate reconciliation

%

Dec 2017

(Reviewed)

Dec 2016

(Reviewed))

Standard tax rate 28.0 28.0

Non-taxable income and disallowable expenses 0.8 0.2

Assessed loss not utilised 3.2 2.7

Other - including foreign tax adjustments (2.1) (0.1)

Group tax rate 29.9 30.8

Cash Flow Statement

Rm

Dec 2017

(Reviewed)

Restated*

Dec 2016

(Reviewed)

Operating cash before working capital

movements 3,964.7 3,700.9

Working capital movements 705.8 (279.0)

Cash generated from operations 4,670.5 3,421.9

Net interest and tax paid (1,388.6) (1,063.2)

Net investment to maintain operations (678.5) (826.7)

Free cash flow 2,603.4 1,532.0

Dividends paid (689.9) (453.2)

Dividends received 80.0 50.0

Investment to expand operations and other net

investing activities (1,128.2) (948.2)

Cash inflow before financing activities 865.3 180.6

* Certain comparative figures shown do no correspond with the 2016 financial statements and reflect statements made. Refer to note 6.

0.0

500.0

1 000.0

1 500.0

2 000.0

2 500.0

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Property expansion

Businesses acquired

Investment to expand

operations

Investment to maintain

operations

Total capex as a % of sales

Total capex as a % of sales

excluding business and

property acquisitions

Ca

pe

x a

s a

% o

f sa

les DEC

2012

DEC 2014

DEC 2013

DEC 2015

DEC 2016

DEC 2017

Capital expansion

Ca

pita

l exp

an

sio

n (R

m)

Capex per category

Rm

Dec 2017

(Reviewed)

Dec 2016

(Reviewed)

Land and buildings/leasehold improvements 533.8 393.3

Vehicles 5.2 31.0

Fixtures, fittings, plant and equipment 270.5 443.3

Computer hardware 28.8 56.8

Computer software 300.0 29.4

Investment to expand operations 1,138.3 953.7

Land and buildings/leasehold improvements 156.0 123.8

Vehicles 35.4 43.0

Fixtures, fittings, plant and equipment 328.9 300.7

Computer hardware 98.4 157.5

Computer software 59.8 201.7

Investment to maintain operations 678.5 826.7

46.9%

0.5%23.8%

2.5%

26.3%

Land & buildings/leasehold improvements

Vehicles

Fixtures, fittings, plant & equipment

Computer hardware

Computer software

EXPANSIONARY INVESTMENT

Total capex 1.9% of total sales (2016: 1.9%)

Store portfolio

Total Massdiscounters Masswarehouse Massbuild Masscash

423 166 21 108 128Up from 412

in Dec 2016

Up from 165

in Dec 2016

Up from 20 in Dec 2016 Up from 104

In Dec 2016

Up from 123

in Dec 2016

+11 Opened +1 Game

+1 in Ghana

+1 Makro

+1 in South Africa

+3 Builders Superstore

+3 in South Africa

+4 Retail

+4 in South Africa

+1 Builders Warehouse

+1 Zambia

+1 Wholesale

+1 in Zambia

Forecast stores: Jan 2018 – Dec 2020

This 12.4% increase includes an 35.6% increase in our ex-SA trading space

Total Massdiscounters Masswarehouse Massbuild Masscash

+54 +17 +1 +15 +21Up from 423 to 477 Up from 166 to 183 Up from 21 to 22 Up from 108 to 123 Up from 128 to 149

+34

+20

South Africa

Ex-SA

+16

+1

Game

+4 in South Africa

+4 in Ghana

+3 in Kenya

+4 in Nigeria

+1 in Zambia

DionWired

+1 in South Africa

+1 Makro

+1in South Africa

+6

+3

+6

Builders Warehouse

+1 in South Africa

+2 in Mozambique

+1 in Zambia

+1 in Swaziland

+1 in Kenya

Builders Express

+3 in South Africa

Builders Superstore

+6 in South Africa

+17

+4

Retail

+17 in South Africa

Wholesale

+1 in South Africa

+2 in Zambia

+1 in Mozambique

+12.4% +11.5% +8.0% +11.9% +17.0%Up from 1,612,916m2

to 1,812,296m2

Up from 548,544m2

to 611,627m2

Up from 231,021m2

to 249,521m2

Up from 456,313m2

to 510,614m2

Up from 377,038m2

to 441,134m2

Restatement

We have reconsidered our accounting with respect

to the valuation of inventory in line with IAS 2

‘Inventories’ relating to the valuation of inventory

including the capitalisation of costs and recognition

of rebates on inventory. Previously the value of

inventory incorrectly included certain elements of

preparing the product for sale while some rebates

were immediately recognised against cost of sales

rather than deferring these rebates in line with the

movement of inventory.

In addition, while preparing the 2017 Group cash

flow statement, we observed that elements of

unrealised foreign exchange movements had been

incorrectly included in the ‘Foreign exchange

movement on cash and cash equivalents’ line on

the 2016 Group cash flow statement.

We therefore concluded that both the error in the

application of the accounting policy of the Group’s

inventory valuation and the error of classification in

the disclosure of unrealised foreign exchange

differences on the face of the Group’s cash flow

statement should be corrected in accordance with

IAS 8: ‘Accounting policies, changes in accounting

estimates and errors’. The correction to the

accounting treatment is effective for the year ended

31 December 2017 and has been applied

retrospectively. This has therefore resulted in a

restatement of the comparative 2016 and 2015

periods. The aggregate effect of the restatement for

these periods is as follows:

New standards to come into effect

IFRS 16

‘Leases’

Key areas of impact

• On-balance sheet recognition of leased stores

• 362 of 423 stores are leased

• Operating lease commitments R15.1 billion

*Estimations based on the 2017 data

IMPLEMENTATION EFFECTIVE 1 JANUARY 2019 MODIFIED RETROSPECTIVE APPROACH

IMPLEMENTATION EFFECTIVE 1 JANUARY 2018 MODIFIED RETROSPECTIVE APPROACH

IFRS 9

‘Financial Instruments’

Key areas of impact

• Expected loss method on provision

for doubtful debts

• Impact of less than 2%* decrease

in net trade receivables

IFRS 15

‘Revenue from Contracts

with customers’

Key areas of impact

• Principal vs. Agent definition

• 5%* sales decrease

• Right of Return Asset and Return

obligation

• Impact of less than 1%* on current

assets and current liabilities

Number of shares

‘000

At Dec 2016 217,136.3

Shares issued 9.2

At Dec 2017 217,145.5

Weighted-average at Dec 2017 215,276.1

Diluted weighted-average at Dec 2017 219,352.1