annual report 2002 - grupo banco · pdf fileannual report 2002. 2 general information ......

TRANSCRIPT

Annual Report 2002

2

General Information

Banco Popular Español, S.A. was incorporated on July 14, 1926, and is registered in the Madrid MercantileRegister in volume 174, folio 44, page 5,458, 1st entry. The Bank is a member of the Deposit Guarantee Fundfor banking entities. 2002 was the Bank's 76th year of operations. The Bank's head office is located atVelázquez, 34. 28001 Madrid.

The Ordinary Shareholders' Meeting will take place on Thursday, June 26, 2003, at 1:00 p.m., at José Ortega yGasset, 29, Madrid.

The financial accounting and statistical data provided herein were prepared with the utmost objectivity, detail,reporting clarity and consistency over time, from the specifically prepared financial information periodically filedwith the Bank of Spain. The financial statements are presented in accordance with the standards applicable in2002, specifically those of Bank of Spain Circulars 4/1991, 2/1996, 5/1997 and 7/1998; the figures for periodsprior to the entry into force of the 1998 standards have been adjusted, as far as possible, to conform thereto.

Average balances were calculated on the basis of daily, monthly or quarterly data, depending on the informationavailable in each case. Figures in brackets are negative amounts, differences or variation rates.

In addition to the Annual Report and its accompanying documents, the Bank issues quarterly financial reports onits operations, including a detailed analysis of variations in assets, liabilities, earnings and profitability in eachquarter. All the information is available at the Banco Popular Shareholders Office (José Ortega y Gasset, 29.28006 Madrid; telephone: 34 91.520.72.65, fax: 34 91.577.92.09, e-mail: [email protected]). All theinformation is also available at: http://www.bancopopular.es

3

Contents Page

General information 2

List of tables, boxes and graphs in the Management Report 4

Banco Popular financial highlights 5

Board and management 6

Editorial 7-8

Management report 9-78

Banco Popular Group 11-54

Banco Popular 55-63

Banking subsidiaries 64-72

Nonbanking finance and service subsidiaries 73-78

Financial statements 79-138

Report of independent auditors 80

Financial reporting responsibility 81

Consolidated balance sheets and statements of income 82-84

Notes to the financial statements 85-138

Corporate Governance Report 139-149

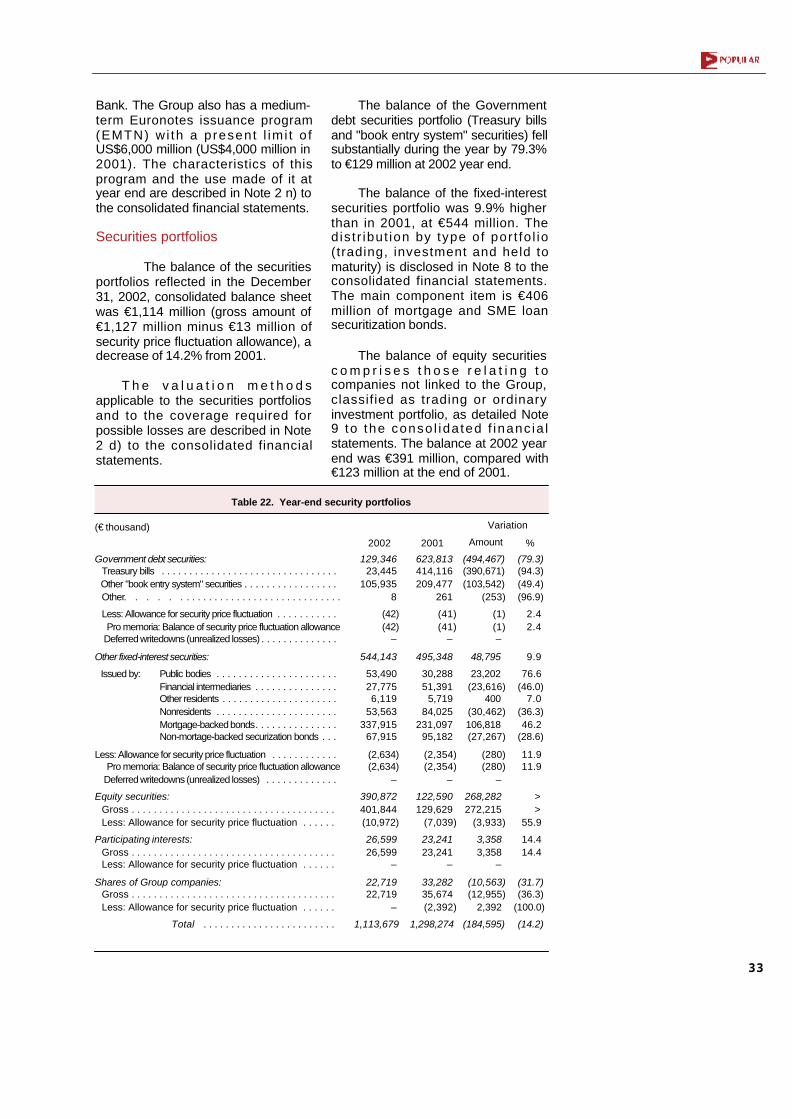

Assets and funds: Total assets. Shareholders' equity. Computable capital. Customer funds. Loans anddiscounts. Off-balance sheet risks. Risk management (Credit risk. Cross–border risk. Market risk. Liquidity risk).Securities portfolios. Goodwill in consolidation. Premises and equipment. Balance sheet in euros and foreigncurrency.

Income and profitability: Income statement. Yields and costs. Operating profitability. Final measures of return.Shareholders. Market performance of Banco Popular shares.

Assets and funds: Total assets. Shareholders' equity. Customer funds. Loans and discounts. Riskmanagement. Securities portfolio.

Income and profitability: Income statement. Yields and costs. Net interest revenue and ordinary revenue.Operating costs, depreciation and other operating income and expenses. Operating income. Net income andprofitability.

4

List of Tables, Boxes and Graphs in the Management Report

Tables Consolidated data

1. Summarized consolidated balance sheets2. Consolidated equity3. Customer funds4. Breakdown of euro customer deposits by size of balance5. Breakdown of customer deposits by region in Spain6. Customer deposits by original maturity7. Mutual funds, by type8. Loans and discounts9. Lending matrix

10. Breakdown of loans and discounts by region in Spain11. Loans and discounts by original maturity12. Off–balance sheet risks13. Risk concentration14. Risk distribution by industry15. Risk performance16. Allowance for nonperforming loans17. Country-risk and related allowances18. Country-risk by balance sheet caption19. Maturity and repricing gap in the balance sheet20. Value at Risk (VaR)21. Liquidity gap22. Security portfolios23. Goodwill in consolidation

24. Premises and equipment25. Summarized euro and foreign currency balance sheets26. Income statements27. Causal analysis of the variation in net interest revenue28. Service revenues29. Itemized breakdown of general expenses

and taxes other than income tax30. Operating efficiency31. Quarterly income and profitability32. Corporate income tax calculation33. Per share data34. Yields and costs35. Quarterly yields and costs36. Profitability37. Measures of return38. Breakdown of share ownership39. Common stock ownership distribution40. Shares controlled by the Board of Directors41. Evolution of price of Banco Popular common stock42. Market return on Banco Popular shares 1992-200243. Banco Popular share valuation measures44. Banco Popular share trading volume45. Treasury stock

46. Summarized balance sheets47. Customer funds48. Loans and discounts49. Risk performance50. Allowance for nonperforming loans

51. Security portfolios detail52. Comparative statements of income53. Yields and costs54. Profitability

Banco Popular

55. Customer funds and loans and discounts 56. Risk performance57. Profitability

58. Per share data59. Employees and branches60. Business volume and income returnAnnex: Summarized financial statements

Banking subsidiaries

1. Total assets managed2. Level of solvency3. Customer funds 4. Variation in total resident private-sector deposits5. Mutual funds6. Pension plans7. Loans and discounts8. Variation in total resident private-sector loans and discounts9. Customer funds and loans and discounts per employee

10. Customer funds and loans and discounts per branch11. Variation in the nonperforming loans ratio and coverage for

delinquent balances12. Service revenues

13. Operating efficiency14. Quarterly revenues15. Growth of income16. Income and dividend per share. Pay-out17. Customer spread18. Interest rates19. Net interest margin20. Quarterly ROA and ROE21. ROA and ROE22. Banco Popular vs. the market: 2002 stock market indices23. Market capitalization and book value 24. Share liquidity

Graphs

Boxes

Nonbanking finance and service subsidiariesSummarized financial statements

1. Summary of permanent management policies 2. Banco Popular ratings3. Commercial performance data for 2002

4. Commercial strategy5. Quality of earnings6. Banco Popular named “the best bank in Spain”

5

Banco Popular Financial Highlights (consolidated figures)

(€ million, unless otherwise indicated)

(a) After distribution of income for the year(b) Figures adjusted for the 2 x 1 split in February 2000(c) €0.78 per share were also paid to shareholders out of the paid-in surplus reserves

Business volumeTotal assets managed . . . . . . . . . . . . . . . . . . . . . . .On-balance sheet total assets . . . . . . . . . . . . . . . . .Total equity (a) . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Customer funds:

On-balance sheet funds . . . . . . . . . . . . . . . . . . . .Other intermediated funds . . . . . . . . . . . . . . . . . .

Loans and discounts . . . . . . . . . . . . . . . . . . . . . . . .Off-balance sheet risks . . . . . . . . . . . . . . . . . . . . . .

SolvencyBIS ratio (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Of which: Tier 1(%) . . . . . . . . . . . . . . . . . . . . . . . . .

Risk managementTotal risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Nonperforming loans . . . . . . . . . . . . . . . . . . . . . . . .Allowances for credit losses . . . . . . . . . . . . . . . . . . .Nonperforming ratio (%) . . . . . . . . . . . . . . . . . . . . . .Coverage (Credit loss allowance/Nonperforming loans) (%)

Income statementsNet interest revenue . . . . . . . . . . . . . . . . . . . . . . . . .Basic banking revenue . . . . . . . . . . . . . . . . . . . . . .Ordinary revenue . . . . . . . . . . . . . . . . . . . . . . . . . . .Operating income . . . . . . . . . . . . . . . . . . . . . . . . . . .Income before taxes . . . . . . . . . . . . . . . . . . . . . . . . .Net income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Net income attributable to Banco Popular Shareholders .

Net return and efficiencyAverage total assets . . . . . . . . . . . . . . . . . . . . . . . .Average total equity . . . . . . . . . . . . . . . . . . . . . . . .ROA (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .ROE (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Operating efficiency (%) . . . . . . . . . . . . . . . . . . . . . .

Per share data (b) Shares outstanding (thousands) . . . . . . . . . . . . . . .Share closing market price (€) . . . . . . . . . . . . . . . . .Share book value (€) . . . . . . . . . . . . . . . . . . . . . . . .Net income per share (€) . . . . . . . . . . . . . . . . . . . . .Dividend per share (€) . . . . . . . . . . . . . . . . . . . . . . .Price/Book value (P/BV) . . . . . . . . . . . . . . . . . . . . . .Price/Earnings (P/E) . . . . . . . . . . . . . . . . . . . . . . . . .

Other dataShareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Employees:

Spain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Abroad . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Branches:Spain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Abroad . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

ATMs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2001%

variation 2000 1999 19982002

47,08137,3952,296

35,55125,8659,686

27,8204,279

11.339.15

32,0982565060.80

197.68

1,4021,9692,0141,157

852614565

34,5702,0441.78

27.6537.20

217,15436.8810.572.6031.360

3.514.2

75,37912,30912,123

1862,1442,118

263,141

10.512.312.612.415.83.3

23.423.5

23.438.034.7

13.59.98.9

13.123.812.012.1

16.012.8

-5.7

12.612.110.3

(6.1)1.31.0

16.10.70.73.85.9

40,65131,3572,047

31,58622,2929,294

23,3083,182

11.489.55

26,4892093840.79

184.03

1,1271,6641,7841,011

810528491

28,6881,8061.84

27.1639.11

217,15437.109.43

2.2591.195

3.916.4

81,45511,94311,825

1182,0692,055

142,824

36,47326,3311,810

28,65818,51610,14218,9392,694

10.679.59

21,6321963280.91

167.44

1,0001,4671,513

777705466433

24,1411,7391.93

24.8841.90

217,15432.388.33

1.9651.075

3.916.5

87,27511,53911,419

1202,0041,989

152,377

34,16324,1561,831

26,38416,37710,00716,8962,413

12.0812.08

19,3122122941.10

138.79

9541,3661,413

687656439407

22,6471,7651.94

23.0544.25

221,55032.168.27

1.8370.977

3.917.5

84,13711,60011,515

851,9661,955

111,903

52,00642,0052,586

39,94629,94510,00134,3225,284

11.008.88

39,6043536820.89

192.98

1,5912,1642,1931,3081,055

688633

40,1072,3061.71

27.4735.69

217,15438.9711.912.9171.500

3.313.4

70,81612,46412,248

2162,1602,133

273,327

(c)

6

Francisco APARICIO, (Representing Sindicaturade Accionistas)Asociación de DirectivosIldefonso AYALADiethart BREIPOHLJosé María CATÁFrancisco DONATEEric GANCEDO *Luis HERRANDO *Manuel LAFFÓNLuis MIRALLES

José BRAVO, CastillaMiguel MOZO, VasconiaFrancisco PARDO, Andalucía

Antonio PUJOL, GaliciaEladio SEBASTIÁN, Crédito Balear

Casimiro MOLINSSantos MONTOROLuis MONTUENGA *Manuel MORILLOMiguel NIGORRAAlberto PARERAEnrique PÉREZ SALAJosé Ramón RODRÍGUEZ *Miguel Angel de SOLÍS Jorge STECHERRafael TERMES

Network Line ManagementBanco Popular

Senior Line Managers:Santiago BERROCAL, Madrid Antonio FÉREZ, Andalucía Francisco J. SAFONT, Cataluña

Regional Banking Subsidiaries

Other Banking and Financial Subsidiaries

Regional Managers:

Board and ManagementBoard of Directors Javier VALLS,* Chairman

Luis VALLS, * ChairmanGabriel GANCEDO, * Deputy Chairman

Angel RON, Chief Executive OfficerJesús PLATERO,* Secretary

Directors

Executive ManagementAngel RON, Chief Executive Officer

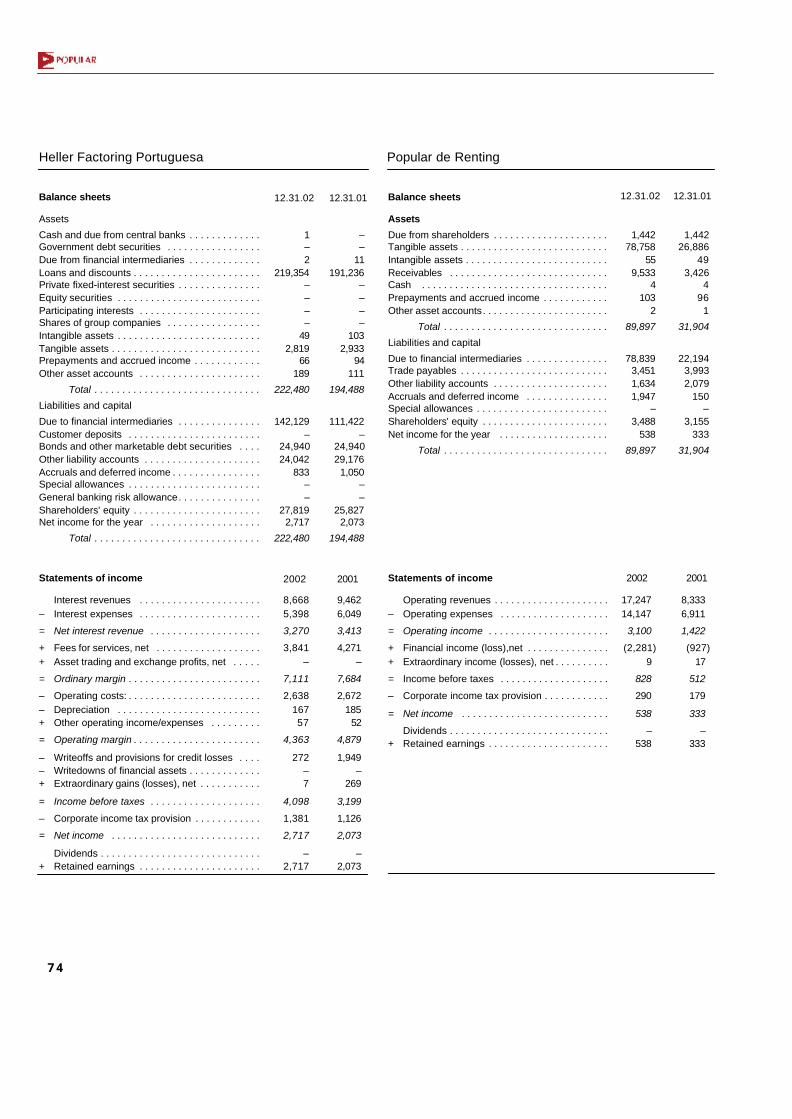

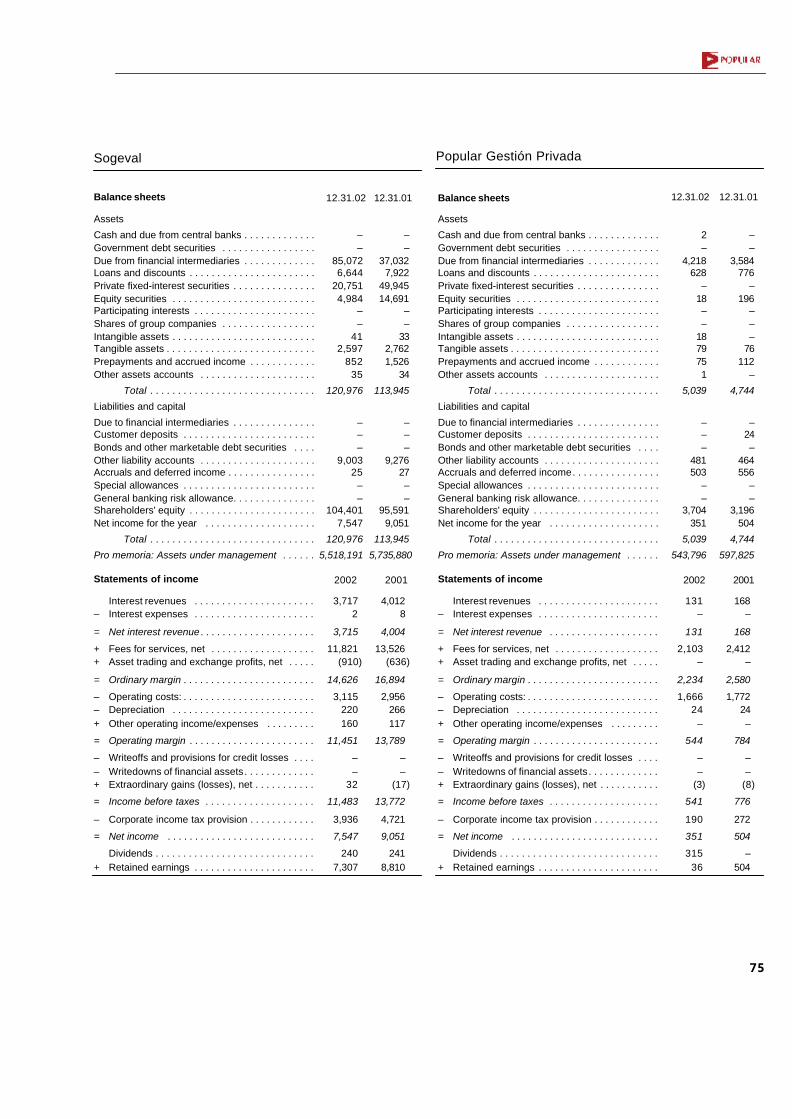

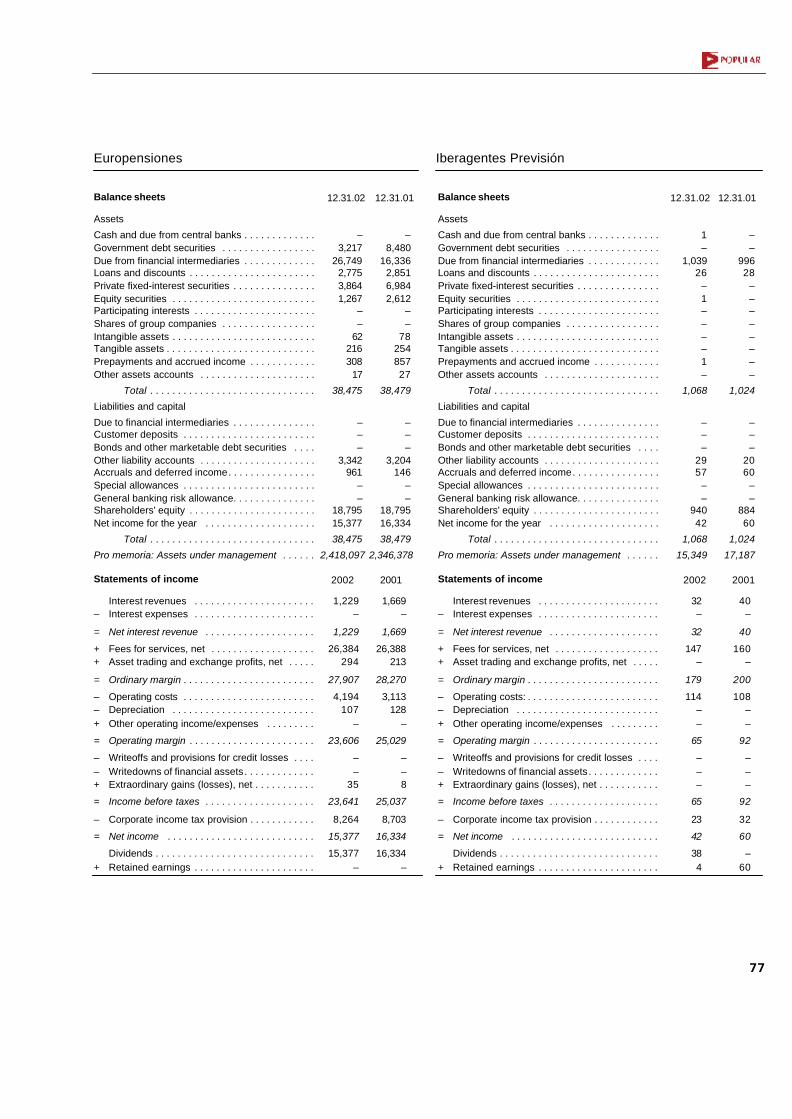

Pedro BERLINCHES, Europensiones and EurovidaJuan Manuel COBO, Heller Factoring EspañolaManuel FERRER, Gestora Europea de InversionesJavier GEFAELL, Popular Banca PrivadaGonzalo GÓMEZ, Banco Popular HipotecarioAlfonso JORDÁN, Sogeval

Aníbal MARQUES, Heller Factoring PortuguesaJuan MARTÍNEZ SAMPEDRO, Popular de RentingSusana de MEDRANO, Bancopopular-eJuan PÉREZ ENRÍQUEZ, Banco Popular FranceCarlos RAMOS, Popular BolsaJorge ROSELL, Popular de Participaciones Financieras

Eutimio MORALES, Technical resourcesAngel RIVERA, Human resources

Fernando de SOTO, Corporate Affairs

Rafael BERMEJO, Chief EconomistFrancisco FERNÁNDEZ DOPICO, Commercial networkRoberto HIGUERA, Chief Financial Officer

José SARTORIUS, International activities

Jesús ARELLANO, Control, internal audit, security and premisesIsaac BOTIJA, Remote bankingJuan ECHANOJAUREGUI, Investor relationsJosé María FERNÁNDEZ, Finance companiesFrancisco GÓMEZ, Commercial managementJulio HORTIGÜELA, Asset managementJosé María LUCÍA, LendingLuis Felipe MARCOS, Legal advisory services

Tomás PEREIRA, Risk prevention and impaired assetsAntonio RAMÍREZ, Information technologyErnesto REY, TreasuryRafael ROCA, ControllerJesús RODRÍGUEZ, Country manager PortugalFrancisco SANCHA, International commercial bankingJosé María SANZ, Compliance

José Ramón ALONSO, Castilla and LeónAlonso CUETOS, GaliciaAmadeu FONT, CanariasJesús M. GONZÁLEZ, Andalucía IJorge GOST, Madrid IIVicente LÓPEZ, Cataluña IJosé Luis MANSO, Asturias and CantabriaLuis MARÍN, ExtremaduraJosé Fernando MARTÍNEZ ISACH, Madrid IIIAntonio MÍNGUEZ, Murcia

Antonio PÉREZ, Andalucía IIJosé Manuel PIÑEIRO, AlicantePablo ROMERO, Aragón, Navarra and La RiojaAlfonso RUSPIRA, Cataluña IIJosé Luis SANGÜESA, País VascoAntonio SILVA, Castilla-La ManchaFrancisco SUBIRANA, Cataluña IIIJuan José TORREGLOSA, ValenciaCarlos VELÁZQUEZ, Madrid I

* Member of the Executive Committee

7

The year recently ended was characterized by the negative behavior of the world economy.Although 2001 had ended in a climate of pessimism following the grave events of September of thatyear and the lowering of expectations which those events caused, there was widespread agreementthat the recession would be very short - a "v-shaped recession" - and that activity would recoverwithin a few months. This was the context in which the rapid intervention of the central banksstarting in October 2001 to banish the risk of a global recession, with substantial interest rate cutsin Europe and the USA, must be viewed.

However, this forecast proved to be wrong and the expectations of recovery evaporated rapidly inthe early months of 2002, at the same time as new factors of pessimism emerged to darken theeconomic outlook. The leading European countries, considered to be the locomotives of growth,continued to show worrying signs of weakness in demand, with the fear of possible deflation.Moreover, the discovery of major accounting frauds at certain big US and European companies, inboth the old and the new economies, generated a climate of mistrust about the veracity of theinformation furnished to the markets, which did nothing to favor the relaunching of activity. Thesimultaneous failure by several European countries to comply with the financial stabilityagreements harmed the credibility of the EMU's economic policy. Lastly, recent months have seenthe increased possibility of a war in the Middle East which, among other consequences, wouldseriously affect oil prices and supplies. Faced by this somber panorama the central bankscontinued to relax monetary policy with further cuts in interest rates down to record low levels:2.75% in the euro area and 1.25% in the USA. The world's leading stock exchanges ended 2002with the sharpest falls for the last three years, despite brief and ephemeral moments of recovery,but without any glimpse of changes in the trend.

In short, the outlook at year end for the international economy - and for that of Spain, which isincreasingly integrated in a global world - was negative and, most worrying of all, was uncertain,with serious doubts about when and to what extent the repeatedly announced recovery would occur.

I shall be telling this with a sigh

Somewhere ages and ages hence:

Two roads diverged in a wood, and I

- I took the one less traveled by,

And that has made all the difference.

Robert Frost - The road not taken - Mountain Interval (1916)

8

Such was the scenario in which the performance of the Banco Popular Group summarized in thisAnnual Report should be placed. In a year marked by difficulty and scant visibility, the Grouppreserved its unwaivable signs of identity, expanded its customer base and market share and, at thesame time, maintained its high levels of solvency, profitability and efficiency, which are benchmarksof reference in the Spanish financial system. The stock market assessed these results without anyambiguity, and the price of Banco Popular stock rose by 5.7% in a year in which the Ibex-35 indexplummeted by 28.1%.

Going beyond the numbers, the year 2002 also saw the strengthening of two areas of priorityimportance for the Group: mortgage lending, and private banking and asset management.Additionally, in the early days of the current year, the Group has reached an agreement in principleto buy a bank in Portugal with a network of more than 100 branch offices, which will be thelaunching pad for development of the Popular model in that market.

A fter enduring years of incomprehension about the policies of the Group, aloof from the fads ofthe moment that trumpeted the advisability and desirability of big banking mergers, the entry intonew geographical markets - however distant and scantly known - and heavy investment in the neweconomy, Banco Popular pressed forward with its own criteria, not in order to be original butsimply to try and perform better the type of business of which it has proven experience, using itsown resources and applying its own way of doing things. We did not let ourselves be carried awayby what others were doing. We analyzed the new business opportunities and our means for enteringthem with a reasonable degree of success. In short, we followed the less traveled road, sometimesfeeling that we were "creatures from another planet" but guided by our confidence that it was thepath that best matched our culture and our capabilities.

T imes of difficulty lay bare the mistaken strategies, the organizational weaknesses forimplementing them successfully and, in short, the future expectations that are not firmly groundedin the unforgiving earth of realism. After a cycle of irrational exuberance, as the period of the lastfew years has so aptly been described, we now see banks going back to the basic concepts of ourbusiness, such as restrengthening commercial banking in the domestic market, particularly amongretail customers, giving priority to organic growth and purchases over mergers, and applying othercriteria which have been the signs of identity of our Group for many years. In some cases, the newstrategy has indeed been defined much more directly: take Banco Popular as the business andprofitability model of reference. These avowals reaffirm for us the validity of our corporate cultureand are a motive of pride for the Group's management and all its staff since, as the saying goes,imitation is the sincerest form of flattery.

January 2003

9

Management Report

This report reflects the opinion of the Management ofBanco Popular on the recent performance of andupcoming prospects for the Bank, and explains thepolicies on which daily management decisions havebeen based. The report also contains detailedsupplementary information on the financial statementsappearing later on in this document, drawn from the in-house accounting and statistical records underlyingmanagerial decisions.

Banco Popular Español, SA("Banco Popular" or "the Bank") is theparent banking company of a financegroup ("the Banco Popular Group" or"the Group") which at 2002 year-endalso included nine other banks whichwere either wholly- or majority-ownedand managed:

- Banco de Andalucía, Banco deCastilla, Banco de Crédito Balear,Banco de Galicia and Banco deVasconia, which operate in theregions indicated by their respectivenames.

- B a n c o P o p u l a r H i p o t e c a r i o ,specializing in property financing.

- Bancopopular-e, specializing inInternet banking.

- Popular Banca Privada, whichprovides private banking services inSpain.

- Banco Popular France, a commercialbank operating in France.

The Group also includes a total oft h i r t e e n c o m p a n i e s h a n d l i n gsubstantially all the range of financialservices: factor ing, mutual andpension fund management, securitiesintermediation, portfolio management,life insurance, insurance broking,venture capi ta l investment andequipment renting. Some of thesecompanies are joint ventures of BancoPopular and leading partner entities.The Group also includes other minorcompanies and several instrumentalcompanies to support its activities.

By virtue of Banco Popular'smajority in capital stock and voting

rights or the agreements with itspartners, the Group operates - to alleffects and purposes - as a singlewhole with unif ied direction andmanagement and common technicaland support services. The banking andother subsidiaries act as geographicalor functional units forming part of theBanco Popular Group organization, theonly special differentiating featuresbeing those arising from the differinglegal status of each.

Main variations in the compositionof the Group in 2002

The various changes in the scopeof consolidation of the Group during2002 included most notably:

Acquisition in May 2002 of the50% of the capital of Banco PopularHipotecario previously owned by thirdparties, converting this bank into awholly-owned subsidiary of the Group.

Acquisition in September 2002 of35% of the capital stock of FortiorHolding, the parent company ofIberagentes Activos (a securitiesc o m p a n y ) a n d o f t h r e e o t h e rc o m p a n i e s ( t w o m u t u a l f u n dmanagement companies and onepension plan management company),raising the Group's stake from 25% to60%. Iberagentes Act ivos wastransformed into a bank under thename of Popular Banca Privada.

Analysis of the Group's businessa n d e a r n i n g s i s b a s e d o n t h econsolidated financial statements,which include the financial statementsof the banks and aff i l iates afterelimination of the intragroup financialrelationships, consolidated by the

11

MANAGEMENT REPORT

2002 PERFORMANCE

12

global or proportional integration orequity methods, as appropriate,depending on their degree of linkagewith the parent company and line ofbusiness.

This Management Report startsby evaluating the performance of theconsolidated Group in the year, ascompared with the previous year,analyzing in detail its capital funds, thebusiness volume - assets and funds - ,r isk management, earnings andprofitability and the performance ofBanco Popular shares. Next, a similaranalysis is made of the Group's parente n t i t y a n d o f i t s n i n e b a n k i n gsubsidiaries, which are dealt with on amore summarized basis since they fileindividual financial statements. TheReport ends with the basic financialinformation (balance sheets andincome statements) of the mainfinancial service companies.

Assets and funds

Total assets

The consolidated balance sheetsas of December 31, 2002 and 2001,before the allocation of income for theyear, are summarized in Table 1. The"Financial Statements" section of theA n n u a l R e p o r t i n c l u d e s t h econsolidated balance sheets of thelast five years, in the public reportingformat demanded by the Bank ofSpain.

The to ta l on-ba lance sheetassets amounted to €42,005 million at2002 year end, €4,610 million (12.3%)more than at the end of 2001. Theaverage total assets during the yearwere €40,107 million, 16.0% higherthan in 2001.

The Group also managed othercustomer funds in off-balance sheetsavings instruments, amounting to€10,001 mil l ion at year end, anincrease of 3.3%. The composition ofthese assets is described in detail inthe subsection on customer funds.

Aggregating the on- and off-balance sheet assets, the tota lvolume of assets managed by theGroup at 2002 year end amounted to€52,006 million, up by 10.5% on2001.

Figure 1 plots the growth of year-end total assets managed in the lastfive years and a breakdown into thetwo groups considered.

Shareholders' equity

The Group's consolidated equitybefore the allocation of 2002 incomeamounted to €2 ,279 mi l l i on a tDecember 31, 2002, an increase of12.5% year-on-year.

The Bank's capital stock wasunchanged during the year at €108.6million.

Summary of permanent management policies Box 1

Signs of identity of the Group

- Preference for the domestic retail market- Commercial strategy orientated towards customer banking, based on

bonding through multiple products (cross-selling)- Personalized product offerings, tailored to the preferences of each

homogeneous customer segment- Multiple commercial distribution channels (branch office, card, ATM,

telephone, Internet banking)- Competition based on quality, flexibility and service personalization- Equal-footing agreements and alliances with other entities for the

performance of overall or specific activities

Management criteria

- Profitable growth of the business (increase of market share andmaximization of income)

- Maximum balance sheet soundness- High operating efficiency- Regularity in the conduct of the business, in earnings and in dividends- Flexible, flat and customer-orientated organization- Professionalism in decision-making processes- Active management of intellectual capital, staff training and motivation- Intensive use of information technology to strengthen commercial action- Internal and external reporting transparency

13

The main variations in reserveaccounts, including consolidationreserves, in 2002 were the allocationof €270.0 million for distribution ofyear 2001 earnings; the use of €33.0million from reserves (the amount netof capitalized taxes) to fund an earlyretirements plan described in detail inNote 2 i) to the consolidated financialstatements; a transfer of €12.8 millionof the remaining balance of a similartransaction in 2001; and €2.6 millionof other consolidation adjustments.

The proposed distribution ofearnings adopted by the directors ofBanco Popular on January 30, 2003i s d e s c r i b e d i n N o t e 4 t o t h econsolidated financial statements.Assuming that the ShareholdersMeeting of the Bank called for June26, 2003, approves this proposal,

consolidated equity will amount to€2,586.5 million, an increase of €290million (12.6%) over 2001.

The resulting book value pershare is €11.91, compared with€10.57 at December 31, 2001.

The amount and composition ofconsolidated equity at 2002 and 2001year ends are shown in the upper partof Table 2.

Computable capital

Law 13/1992 on consolidatedequity and supervision of creditentities required finance entities tohave at all times certain minimumcapital amounts, based on the volumeand composition of their assets andrisks.

Table 1. Summarized consolidated balance sheets

Variation

Amount %December 31

2001

Assets

Cash and due from central banks . . . . . . . . . .Government debt securities . . . . . . . . . . . . . . .Due from financial intermediaries . . . . . . . . . .Loans and discounts . . . . . . . . . . . . . . . . . . . .Private fixed-interest securities . . . . . . . . . . . .Equity securities . . . . . . . . . . . . . . . . . . . . . . .Participating interests . . . . . . . . . . . . . . . . . . .Shares of group companies . . . . . . . . . . . . . . .Intangible assets . . . . . . . . . . . . . . . . . . . . . . .Goodwill in consolidation . . . . . . . . . . . . . . . . .Tangible assets . . . . . . . . . . . . . . . . . . . . . . . .Prepayments and accrued income . . . . . . . . .Other asset accounts . . . . . . . . . . . . . . . . . . . .Losses at consolidated companies . . . . . . . . . .

Total . . . . . . . . . . . . . . . . . . . . . . . . . . .

Liabilities and capital

Due to financial intermediaries . . . . . . . . . . . .Customer deposits . . . . . . . . . . . . . . . . . . . . . .Bonds and other marketable debt securities . . . .Subordinated financing . . . . . . . . . . . . . . . . . . .Other liability accounts . . . . . . . . . . . . . . . . . .Accruals and deferred income . . . . . . . . . . . . .Special allowances . . . . . . . . . . . . . . . . . . . . .Negative difference in consolidation . . . . . . . .Shareholders' equity . . . . . . . . . . . . . . . . . . . .Minority interests. . . . . . . . . . . . . . . . . . . . . . . .Net income for the year . . . . . . . . . . . . . . . . . .

Total . . . . . . . . . . . . . . . . . . . . . . . . . . .

683,317129,346

4,706,69233,711,019

544,143390,87226,59922,71917,938

7,253568,280297,242890,345

9,355

42,005,120

6,965,94323,690,3296,009,968

245,356923,709301,041229,471

4182,288,076

663,074687,735

42,005,120

(1,203,788)(494,467)(262,233)

6,342,64848,795

268,2823,358

(10,563)(2,853)

(26,360)(12,314)

(2,728)(43,928)

5,712

4,609,561

40,8661,075,0933,023,502

(18,113)44,758

32(52,909)

(26)258,060164,727

73,571

4,609,561

(63.8)(79.3)

(5.3)23.2

9.9>

14.4(31.7)(13.7)(78.4)

(2.1)(0.9)(4.7)

>

12.3

0.64.8

>(6.9)5.1

–

(18.7)(5.9)

12.733.112.0

12.3

1,887,105623,813

4,968,92527,368,371

495,348122,59023,24133,28220,79133,613

580,594299,970934,273

3,643

37,395,559

6,925,07722,615,2362,986,466

263,469878,951301,009282,380

4442,030,016

498,347614,164

37,395,559

(€ thousand)Fig.1 Total assets managed

at year-end(€ million)

Off-balance sheet assets

Total on-balance sheet assets

0201009998

December 312002

5,000

17,500

55,000

42,500

30,000

47,081

52,006

34,163

40,651

42,00537,39531,35724,156

10,007

9,294

9,686

10,001

36,473

26,331

10,142

14

Capital for the purposes of thislegislation comprises, in addition tothe amounts shown as such in theconsolidated balance sheet, i.e.common stock and reserves, otheritems, namely minority interestsre la t i ng t o common sha res o fconsolidated aff i l iates, minorityinterests relating to preferred stock,and subordinated debt, albeit in thecase of these two latter items only upto a stated limit. On the contrary,i n tang ib le asse ts , goodw i l l i nconsolidation and other minor itemshave to be subtracted in calculatingcomputable capital.

In order to maintain solvency at aprudent level appropriate to the stronggrowth of i ts balance sheet , inDecember 2002 the Group issued€138 million of preferred stock, asd e t a i l e d i n N o t e 2 3 t o t h econsolidated financial statements.

At December 31, 2002, theGroup's computable capital, after thedistribution of income for the year,amounted to €3,490 million per theBank o f Spa in regu la t i ons , anincrease of €467 million (15.5%) over2001.

At that same date, the Group'scapital requirement under the Bank ofSpain regulations amounted to €2,913million and, accordingly, it had acushion of €577 million, 19.8% overthe minimum required amount. Theresulting solvency ratio was 9.59%,compared with the required minimumof 8%.

Under the capital requirementss t i p u l a t e d b y t h e B a n k f o rInternational Settlements (BIS) whichare those used internationally tomeasure the solvency of financeentities, the Group's computablecapital at 2002 year end of €4,020million was €1,097 million in excess ofthe required minimum of €2,924million, signifying a BIS solvency ratioof 11.0%, much above the minimumrequirement of 8%. Of the totalamount, the Tier 1 capital amountedto €3,245 million and the ratio for thistranche was 8.88%.

The ratings assigned to Banco Popular Group by the three leadinginternational credit rating agencies are the highest in the whole Spanishfinancial system. Banco Popular ranks 25th among world banks by solvency,and 7th if State-guaranteed government-owned entities are excluded fromthe list. The current ratings are as follows:

Standard & Poor's bases its latest (November 2002) assessment on "theBank's solid financial fundamentals, excellent earnings, sound asset qualityand good capitalization, as well as management's coherent and conservativestrategy".

The report goes on to say that Banco Popular will foreseeably maintain thehigh profitability achieved by it in the last six years despite the substantialchanges in the Spanish financial system, with a wave of bank mergers andlow interest rates. The report goes on: "the combination of a clearly definedstrategy focused on retail domestic banking, superior pricing policies,comparatively cheaper funding base and strong operating efficiency isindisputably one of the Bank's major strengths and a source of its greatfinancial flexibility". Also noted was the increased market share in lendingand deposits through organic growth, while at the same time safeguarding itsfinancial strengths. S & P considers that the Bank's prospects are "stable"despite the weakening of the economy, since it is considered that BancoPopular will maintain its record of strong profitability, which has been testedin very different economic growth and interest rate scenarios.

On January 10, 2003, Standard & Poor's confirmed the rating and the stableoutlook for Banco Popular, following the announcement by the Bank of anagreement in principle to purchase a bank in Portugal.

Moody's Investor Service confirmed in February 2002 the rating it hadassigned to Banco Popular in 1998, based on "the excellent financialfundamentals, high earning power and strong capitalization" and describedits rating outlook as "stable". It then highlighted the fact that the Bank'sactivity focuses on the domestic retail business which, combined with aprofitable branch network, enables it to obtain high recurring earnings and amuch higher level of profitability than the average for all Spanish banks,which is in turn one of the highest in Europe. The report further notes thatBanco Popular has been able to successfully adapt to an environment of lowinterest rates and to gain market share while simultaneously continuing toapply its customary prudent risk criteria.

Fitch Ratings also confirmed its rating and the "stable" rating outlook ofBanco Popular in a report of March 2002 which "reflects the excellent trackrecord of strong profitability and revenue generation, high asset quality andadequate capital". The rating agency added that Banco Popular "hasmaintained this position throughout various economic cycles, which is proofof its good management".

Banco Popular ratings Box 2

Agency Individual Short-term Long-term

Fitch IBCA A F1+ AAMoody´s A- P1 Aa1Standard & Poor´s A1+ AA

15

Table 2 shows the composition inthe last two years of the Group'scomputable capital per Bank of Spainand BIS regulations, together with themain solvency measures. Figure 2plots the same aggregates for the lastfive years.

Customer funds

At 2002 year end, on-balancesheet customer funds totaled €29,946million, up by 15.8% during the year.The average customer funds balanceamounted to €28,583 million, 19.6%more than a t the end o f 2001 .Customer funds were thereforefinancing 71% of the balance sheet atyear end and the same percentage ofthe average balances, compared with69% in 2001.

C u s t o m e r f u n d s c o m p r i s ecustomer deposits - ordinary deposits

and temporary sales of financialassets (repos)-, the funds raised bydebt securities, and subordinatedfinancing.

Customer deposits increased by4.8% in 2002 to €23,690 million atyear end, and the average balancesamounted to €23,445 mill ion, up10.2% in the year. Private sectorresidents' deposits - which represent86% of the total - increased by 5.0%to €20,432 million. By type, timedepos i ts were up by 9 .8% anddemand and savings accounts wereup by 4.7%; temporary sales ofassets declined by 22.1%.

In 2002 the Group's deposits ofprivate sector residents grew fasterthan those of Spanish banks as awhole, with an edge of 2.8 percentagepoints in average growth rates, grewslightly less (-1 percentage point) than

Fig.2 Level of solvency ( € million and %)

Computable capital

Minimum required

Bank of Spain solvency ratio.(Right-hand scale)

BIS ratio. (Right-hand scale)

Table 2. Consolidated equity (*)

Common stock . . . . . . . . . . . . . . . . . . . . . . . . . . . .Reserves . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Consolidation reserves . . . . . . . . . . . . . . . . . . . .Less:

Treasury stock . . . . . . . . . . . . . . . . . . . . . . . . .Losses at consolidated companies . . . . . . . . .

On-balance sheet equity . . . . . . . . . . . . . . . . . .Minority interests . . . . . . . . . . . . . . . . . . . . . . . . .

Preferred stock . . . . . . . . . . . . . . . . . . . . . . . . .Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Subordinated financing . . . . . . . . . . . . . . . . . . . .Less:

Intangible assets . . . . . . . . . . . . . . . . . . . . . . . .Goodwill . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Bank of Spain computable capital . . . . . . . . . . . . .Minimum requirement . . . . . . . . . . . . . . . . . . . . .Capital cushion . . . . . . . . . . . . . . . . . . . . . . . . . .Bank of Spain solvency ratio (%)BIS computable capital . . . . . . . . . . . . . . . . . . .Of which: Tier 1 capital . . . . . . . . . . . . . . . . . . . . .Minimum requirement . . . . . . . . . . . . . . . . . . . . .Capital cushion . . . . . . . . . . . . . . . . . . . . . . . . . . .BIS ratio (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Of which: Tier 1(%) . . . . . . . . . . . . . . . . . . . . . .

108,577

1,208,633

983,441

–

4,326

2,296,325

518,177

300,000

218,177

263,469

(20,791)

(33,613)

(742)

3,022,825

2,411,253

611,572

10.03

3,418,438

2,759,819

2,413,388

1,005,050

11.33

9.15

(€ thousand)

–

146,151

149,033

–

5,029

290,155

165,323

138,000

27,323

(18,113)

2,853

26,360

658

467,236

501,378

(34,142)

602,057

484,691

510,401

91,656

108,577

1,354,784

1,132,474

–

9,355

2,586,480

683,500

438,000

245,500

245,356

(17,938)

(7,253)

(84)

3,490,061

2,912,631

577,430

9.59

4,020,495

3,244,510

2,923,789

1,096,706

11.00

8.88

31.12.0131.12.02 Variation

(*) After distribution of 2002 income.

2,605

2,027

3,600

2,950

2,300

1,650

1,000 2

7

12

17

22

11.00

3,023

10.289.59

11.48

0201009998

10.80

12.08

2,411

2,913

1,477

10.03

3,490

1,994

10.67

9.50

1,965

1,655

11.33

16

those at savings banks, and more(+0.7 percentage points) than theaggregate for all Spanish banks andsavings banks. These figures showthat, as occurred in 2001, BancoPopular continued to gain marketshare for deposits in the domesticmarket, which is its priority field ofactivity.

F igu re 4 p lo t s t he ra tes o fvar iat ion in tota l pr ivate sectorresidents' deposits at all Spanishbanks and savings banks in theperiod November 2001 - November2002 (per the latest available Bank ofSpain data) as compared with thoseof the Group. It will be seen thatBanco Popular outperformed Spanishbanks as a whole throughout thisperiod, whereas its position withrespect to the growth at savingsbanks was fluctuating.

Debt and other marketab lesecurities, which amounted to €6,010million at year end, consist of twod i f fe ren t ca tegor ies wh ich a rediscussed below.

The first relates to medium-termnotes issued in the Euromarket by aGroup affiliate, guaranteed by BancoPopular, the proceeds of which areassigned in ful l to f inancing forresidents. These notes amounted to€4 ,240 mi l l i on a t year end , ascompared with €1,968 million a yearearlier. This strong growth of 116.7%was the outcome of the policy oflengthening the average term of fundsin order to permit prudent funding ofthe balance sheet in the face of thesharp growth in long-term credit,mainly for mortgages.

The second category includesthe issues of commercial papera m o u n t i n g t o € 1 , 7 4 5 m i l l i o n ,compared with €1,018 million at theend of 2001, a substantial increase of71.4% year-on-year. These short-term (up to 18 months) securities areplaced in the domestic market as analternative for deposits, and shouldtherefore be aggregated to thed e p o s i t s e v e n t h o u g h u n d e raccounting regulations they appearunder d i f ferent capt ions in thebalance sheet. Consequently, thetotal funds taken by the Group fromprivate sector residents amounted to€22,177 million, an increase of 8.3%in the year.

The subordinated debt relates tolong-term debt securities which rankafter common creditors for creditseniority purposes. The amount of€245 million was raised in four issuesdenominated in euros and othercurrencies by a Group subsidiary,guaranteed by Banco Popular. Allthese securities mature in ten years,although the issuer has the option toredeem them early after the end oft h e f i f t h y e a r . N o i s s u e s o fsubordinated debt were made in 2002and, therefore, the decrease of 6.9%with respect to 2001 year end wasdue exclusively to exchange ratevariations during the year.

The intermediated off-balancesheet funds, dealt with next, are the

12.31.0112.31.02

Variation

* Not comparable with 2001 because of a change in calculation methodology

Absolute %

Total number of customers (000)Individuals . . . . . . . . . . . . .Legal entities . . . . . . . . . . .

Internet customersBank-on-line Number of customers (000) . .

Individuals . . . . . . . . . . . . .Legal entities . . . . . . . . . . .

Bancopopular-eNumber of customers (000) . .

Productivity (Products sold per employee in the commercial network) . .

Cross-selling*(Products per customer) . . . . .

4,2523,925

327

614489125

39

277

40137724

27023733

38

8

4,6534,302

351

884726158

77

285

3.02

9.49.67.5

43.948.226.7

97.4

2.9

Commercial performance data for 2002 Box 3

17

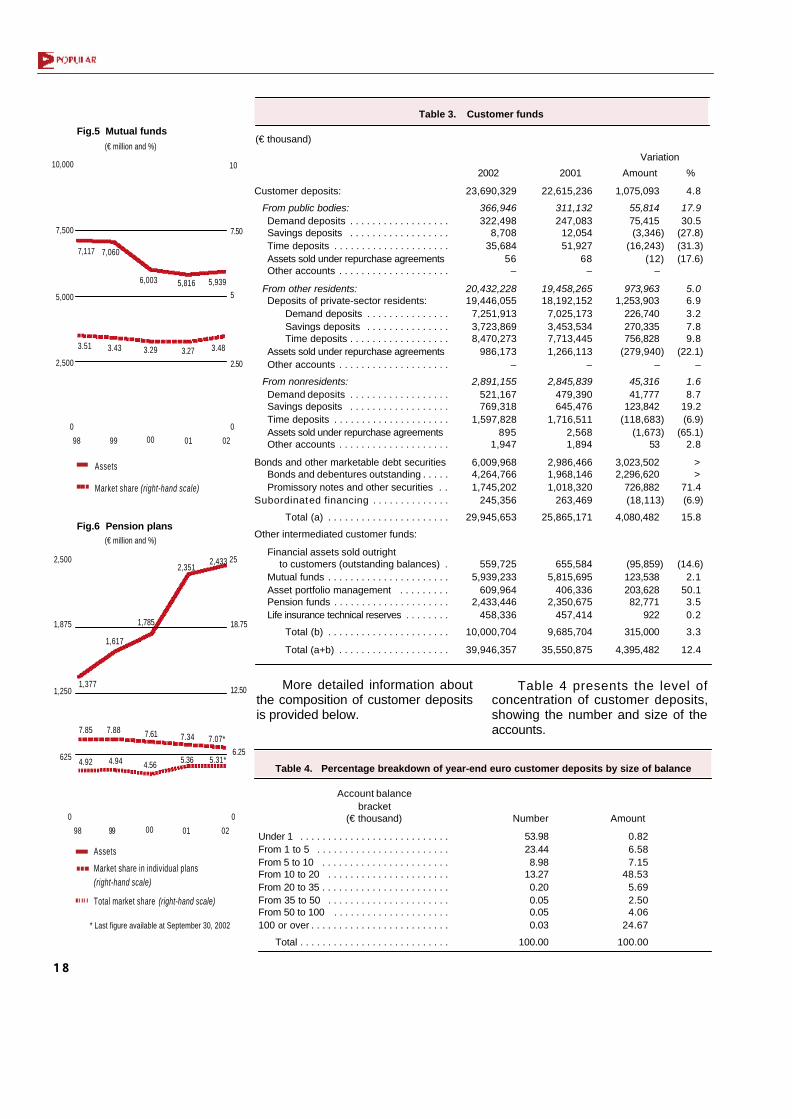

aggregate of the participations inmutual funds, managed portfolios,pension plans, funds raised viainsurance instruments, and financialassets sold to maturity. These fundstotaled €10,001 million at year end,an increase of 3.3% over the figure atthe same date in 2001.

The Group manages a total of 69m u t u a l f u n d s t h r o u g h s e v e r a lsubsidiaries and the assets managedamounted to €5,939 million, 2.1%more than a t the end o f 2001 .Following the acquisition of controllingstakes in two fund managementcompanies ( inc luded in For t iorHolding) in 2002, the variation incomparable terms with 2001 was adecline of 4.7%.

This decrease was due mainly tothe sharp depreciation of the assetsof equity funds (-17.2%) and mixedfunds (- 20.4%), but was lower thanthe decline in the stock marketsduring the year. The fixed-interest andmoneta ry asse t ( f i amm) fundsperformed well, with increases of30.0% and 9.9%, respect ive ly ,whereas the guaranteed fundsremained flat (+0.3%).

Causal analysis of the variationin fund assets dur ing the yeardiscloses that the volume of newcontributions was practically the sameas that of withdrawals, while the valueof the assets decreased by 4.7%.S i m u l t a n e o u s l y t h e r e w a s asubstantial transfer between fundstowards those of lower risk (monetaryassets and fixed-interest instruments).

The latest available advanceddata (to December) for this sector inSpain reveal that the total assets ofmutual funds fell in 2002 for the thirdyear running by 4.0%, and by 26.7%in the case of equity funds.

The Group's market share was3.48% compared with 3.27% in 2001.

The asse ts and secu r i t i esportfolios managed by the Group,including 37 open-end investmentcompanies (Simcav), amounted to€610 million, an increase of 50.1% inthe year. Adjusted for the effect of theinclusion in the Group of the FortiorHolding companies, the growth ratewas 1,3%.

The pension plans managed bythe Group amounted to €2,433million, up by 3.5% during the year.The scant growth was due to the poorp e r f o r m a n c e o f t h e m a r k e t smentioned earlier, since net inflows topension plans were 9.7% higher thanin 2001.

The Group's market share ini n d i v i d u a l p e n s i o n p l a n s ( a tSeptember 30, the latest date forwhich sector data are available) was7.07%, compared with 7.34% at theend of 2001. Considering all types ofpension plans, the market shares atthose same dates were 5.31% and5.36%, respectively.

Accordingly, the Group's total on-and off-balance sheet customer fundsa t 2002 yea r end amoun ted to€39,946 million, an increase of 12.4%over 2001.

Table 3 shows the composition oft o t a l c u s t o m e r f u n d s w i t h abreakdown by type of instrument andsector at 2002 year end, with thecomparative figures for 2001. Figure 3plots the variation in the last fiveyears.

Fig.3 Customer funds (€ million)

On-balance sheet funds

Other intermediated funds

0201009998

Fig.4 % annual variation in totalresident private-sector deposits

* Source: Bank of Spain

5,000

15,000

45,000

35,000

25,0009,294

22,292

39,946

26,384

31,586

35,551

10,001

10,007

25,865 29,94516,377

28,658

10,142

18,516

9,686

Popular

Banks*

0

4

16

12

8

20

Savings banks*

2001

N D J F M J A S NA M J O

2002

18

Table 4. Percentage breakdown of year-end euro customer deposits by size of balance

Under 1 . . . . . . . . . . . . . . . . . . . . . . . . . . .From 1 to 5 . . . . . . . . . . . . . . . . . . . . . . . .From 5 to 10 . . . . . . . . . . . . . . . . . . . . . . .From 10 to 20 . . . . . . . . . . . . . . . . . . . . . .From 20 to 35 . . . . . . . . . . . . . . . . . . . . . . .From 35 to 50 . . . . . . . . . . . . . . . . . . . . . .From 50 to 100 . . . . . . . . . . . . . . . . . . . . .100 or over . . . . . . . . . . . . . . . . . . . . . . . . .

Total . . . . . . . . . . . . . . . . . . . . . . . . . . .

Account balancebracket

(€ thousand) Number Amount

53.9823.448.98

13.270.200.050.050.03

100.00

0.826.587.15

48.535.692.504.06

24.67

100.00

More detailed information aboutthe composition of customer depositsis provided below.

Table 4 presents the level ofconcentration of customer deposits,showing the number and size of theaccounts.

Fig.5 Mutual funds (€ million and %)

Assets

Market share (right-hand scale)

Fig.6 Pension plans(€ million and %)

Assets

Market share in individual plans(right-hand scale)

* Last figure available at September 30, 2002

0

2,500

10,000

7,500

5,000

0201009998

0

10

2.50

7.50

5

0

625

2,500

1,875

1,250

0201009998

0

6.25

25

18.75

12.50

Total market share (right-hand scale)

Table 3. Customer funds

2002

Variation

Amount %

23,690,329

366,946322,498

8,70835,684

56–

20,432,22819,446,055

7,251,9133,723,8698,470,273

986,173–

2,891,155521,167769,318

1,597,828895

1,947

6,009,9684,264,7661,745,202

245,356

29,945,653

559,7255,939,233

609,9642,433,446

458,336

10,000,704

39,946,357

22,615,236

311,132247,083

12,05451,927

68–

19,458,26518,192,152

7,025,1733,453,5347,713,4451,266,113

–

2,845,839479,390645,476

1,716,5112,5681,894

2,986,4661,968,1461,018,320

263,469

25,865,171

655,5845,815,695

406,3362,350,675

457,414

9,685,704

35,550,875

1,075,093

55,81475,415(3,346)

(16,243)(12)

–

973,9631,253,903

226,740270,335756,828

(279,940)–

45,31641,777

123,842(118,683)

(1,673)53

3,023,5022,296,620

726,882(18,113)

4,080,482

(95,859) 123,538203,62882,771

922

315,000

4,395,482

4.8

17.930.5

(27.8)(31.3)(17.6)

5.06.93.27.89.8

(22.1)–

1.68.7

19.2(6.9)

(65.1)2.8

>>

71.4(6.9)

15.8

(14.6)2.1

50.13.50.2

3.3

12.4

(€ thousand)

Customer deposits:

From public bodies:Demand deposits . . . . . . . . . . . . . . . . . .Savings deposits . . . . . . . . . . . . . . . . . .Time deposits . . . . . . . . . . . . . . . . . . . . .Assets sold under repurchase agreements Other accounts . . . . . . . . . . . . . . . . . . . .

From other residents:Deposits of private-sector residents:

Demand deposits . . . . . . . . . . . . . . .Savings deposits . . . . . . . . . . . . . . .Time deposits . . . . . . . . . . . . . . . . . .

Assets sold under repurchase agreements Other accounts . . . . . . . . . . . . . . . . . . . .

From nonresidents:Demand deposits . . . . . . . . . . . . . . . . . .Savings deposits . . . . . . . . . . . . . . . . . .Time deposits . . . . . . . . . . . . . . . . . . . . .Assets sold under repurchase agreementsOther accounts . . . . . . . . . . . . . . . . . . . .

Bonds and other marketable debt securitiesBonds and debentures outstanding . . . . .Promissory notes and other securities . .

Subordinated financing . . . . . . . . . . . . . .

Total (a) . . . . . . . . . . . . . . . . . . . . . .

Other intermediated customer funds:

Financial assets sold outrightto customers (outstanding balances) .

Mutual funds . . . . . . . . . . . . . . . . . . . . . .Asset portfolio management . . . . . . . . .Pension funds . . . . . . . . . . . . . . . . . . . . .Life insurance technical reserves . . . . . . . .

Total (b) . . . . . . . . . . . . . . . . . . . . . .

Total (a+b) . . . . . . . . . . . . . . . . . . . .

2001

6,003

3.29 3.27 3.483.51

5,816 5,939

7,117 7,060

3.43

1,785

4.56 5.36

7.61 7.347.85

4.92

2,3512,433

1,377

1,617

7.88

4.94

7.07*

5.31*

19

T a b l e s 5 a n d 6 s h o w t h edistribution of customer deposits by

region in Spain and term in the lastfive years.

Table 7. Mutual funds, by type

VariationAmount En %2002 2001

FIAMM money market assets funds . . . . . . .FIM fixed-interest securities funds . . . . . . . .FIM equity securities funds . . . . . . . . . . . . .FIM mixed funds . . . . . . . . . . . . . . . . . . . . . .Guaranteed and other funds . . . . . . . . . . . .

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1,730,919884,949648,920

1,018,2921,532,615

5,815,695

1,903,1261,150,811

537,062810,768

1,537,466

5,939,233

172,207265,862

(111,858)(207,524)

4,851

123,538

9.930.0

(17.2)(20.4)

0.3

2.1

(€ thousand)

Table 5. Breakdown of customer deposits by region in Spain

Andalucía . . . . . . . . . . . . . . . . . . . . .Aragón . . . . . . . . . . . . . . . . . . . . . . .Asturias . . . . . . . . . . . . . . . . . . . . . .Balearic Islands . . . . . . . . . . . . . . . .Basque Country . . . . . . . . . . . . . . . .Canary Islands . . . . . . . . . . . . . . . . .Cantabria . . . . . . . . . . . . . . . . . . . . .Castilla-La Mancha . . . . . . . . . . . . . .Castilla-León . . . . . . . . . . . . . . . . . .Cataluña . . . . . . . . . . . . . . . . . . . . . .Extremadura . . . . . . . . . . . . . . . . . .Galicia . . . . . . . . . . . . . . . . . . . . . . .Madrid . . . . . . . . . . . . . . . . . . . . . . .Murcia . . . . . . . . . . . . . . . . . . . . . . .Navarra . . . . . . . . . . . . . . . . . . . . . . .Rioja . . . . . . . . . . . . . . . . . . . . . . .Valencia . . . . . . . . . . . . . . . . . . . . . .

Total . . . . . . . . . . . . . . . . . .

2001 2000 1999 19982002

18.181.172.163.223.382.180.502.17

10.1812.091.118.55

21.142.372.670.808.13

100.00

17.701.052.093.383.092.280.432.12

10.1311.87

1.148.58

22.452.392.670.797.84

100.00

18.161.072.163.822.932.430.412.10

10.5911.22

1.139.08

20.972.762.760.777.96

100.00

17.250.952.233.862.702.280.392.16

11.3811.16

1.159.41

20.712.482.87

.0.768.26

100.00

Region of Spain

18.181.201.982.893.17 1.950.402.20

10.4011.73

1.048.02

23.452.262.610.857.67

100.00

(Annual average %)

Demand1 to 3 months . . . . . . . . . . . . . .3 months to 1 year . . . . . . . . . .1 to 5 years . . . . . . . . . . . . . . . .Over 5 years . . . . . . . . . . . . . . . .Unclassified . . . . . . . . . . . . . . . .

Total . . . . . . . . . . . . . .

2001 2000 1999 19982002

Table 6. Year-end customer deposits by original maturity

45.8634.4310.81

6.272.63

–

100.00

47.9015.7719.6514.662.02

–

100.00

54.4712.2118.7111.103.370.14

100.00

59.4421.2013.185.74

– 0.44

100.00

Term

42.0716.7523.6414.78

2.76–

100.00

(Data in %)

Table 7 shows the variation inmutual fund assets by type, comparedwith 2001.

20

Loans and discounts

This capt ion compr ises thefinancing provided to customers in theform of loans, credits, discounts,overdrafts, financial leasing and otherlending instruments, recorded at thebalances receivable; the portion, if any,not used but drawable by the borroweris included in memorandum accountsunder the caption "Commitments -unused portion of credit lines".

At the end of 2002, the Group'sloans and discounts totaled €34,322million, an increase of 23.4% in theyear. In May 2002 the Group acquiredthe 50% of the capital stock of BancoPopular Hipotecario (BPH) hithertoowned by third parties, leading to theaddition at that date of €752 million ofassets, substantially all mortgageloans, to the consolidated balancesheet. Adjusted for this effect, the

growth of loans and discounts was20.5% over 2001 year end.

The average balance during theyear amounted to €30,959 million, anincrease of 20.0% over 2001.

T h e v o l u m e o f l e n d i n grepresented 82% of the balance sheettotal and 115% of the on-balancesheet customer funds at year end; thematching percentages for averagebalances during the year were 77%and 108%, respectively, with a slightincrease over 2001.

Net loans and discounts, i.e. afters u b t r a c t i o n o f t h e c r e d i t l o s sallowances to cover possible losses inthe event of non-recovery of theseassets, amounted to €33,711 million,an increase of 23.2%, and this is thefigure shown in the summarizedbalance sheet in Table 1.

Table 8. Loans and discounts

To public bodies:

Secured loans . . . . . . . . . . . . . . . .Other term loans . . . . . . . . . . . . . .Overdrafts and other . . . . . . . . . . .

To other residents:

Trade loans and discounts . . . . . .Secured loans:

Mortgage loans . . . . . . . . . . . . .Other . . . . . . . . . . . . . . . . . . . .

Other term loans:

Loans and credits . . . . . . . . . . . .Repos . . . . . . . . . . . . . . . . . . . .

Overdrafts and other . . . . . . . . . . .Financial leasing . . . . . . . . . . . . . .

To nonresidents:

Trade loans and discounts . . . . . .Secured loans . . . . . . . . . . . . . . . .

Mortgage loans . . . . . . . . . . . . .Other . . . . . . . . . . . . . . . . . . . .

Other term loans . . . . . . . . . . . . . .Overdrafts and other . . . . . . . . . . .

Nonperforming loans:

To public bodies . . . . . . . . . . . . . .To other residents . . . . . . . . . . . . .To nonresidents . . . . . . . . . . . . . .

Total . . . . . . . . . . . . . . . . . . . . .

(€ thousand)

Variation

Amounts In %2002 2001

30,429

–30,383

46

26,652,900

4,201,56311,262,796

11,223,59039,206

8,325,869

8,226,52999,340

1,009,1821,853,490

888,822

191,090302,389

296,0196,370

348,42246,921

247,859

698238,497

8,664

27,820,010

31,395

–31,180

215

32,740,751

4,474,63316,154,033

16,099,67654,357

8,869,530

8,715,726153,804

1,161,7682,080,787

1,204,258

239,053424,662

413,80910,853

499,81040,733

345,387

637334,544

10,206

34,321,791

966

–797169

6,087,851

273,0704,891,237

4,876,08615,151

543,661

489,19754,464

152,586227,297

315,436

47,963122,273

117,7904,483

151,388(6,188)

97,528

(61)96,0471,542

6,501,781

3.2

2.6>

22.8

6.543.4

43.438.6

6.5

5.954.8

15.112.3

35.5

25.140.4

39.870.4

43.4(13.2)

39.3

(8.7)40.317.8

23.4

Fig.7 Loans and discounts (€ million)

02009998 0110,000

16,500

36,000

29,500

23,000

23,308

27,820

34,322

16,896

18,939

Fig.8 % annual variation in totalresident private-sectorloans and discounts

* Source: Bank of Spain

Popular

Banks*

0

5

20

15

10

25

Savings banks*

2001

N D J F M J A S NA M J O

2002

21

Commercial strategy Box 4

The starting point of the Group's commercial management is a set of criteria that are systematically applied to all areasof the business and can be summarized by the following guidelines:

Focus on relationship banking: The aim is to construct a relationship of knowledge, of mutual confidence, so as tobind customers closely to the Group and to be able to offer them as wide a range of financial services as possible. Bycontrast with other banks, at Banco Popular looking after customers takes precedence over selling products to them.

Personalized services: The Group must have a range of products that is sufficiently varied and marketed with thenecessary flexibility to cater for the needs of a clientele of 350,000 small, medium and big companies and nearly fourand a half million private individuals, of very diverse sociological and financial profiles, with each customer calling for adifferent relationship that suits their different preferences as to products for savings and investment, financing, servicesand insurance. The notion of tailor-made service, which the Group adopted many years ago, continues to be one ofBanco Popular's signs of identity in the financial market.

Use of multiple marketing channels : The unwaivable objective of customer bonding can be achieved in many ways,depending on the characteristics of each segment. Branch offices are and will continue to be a key, but not the only,route for reaching customers in the commercial banking business. At the same time, other channels such as ATMs,telephone banking and above all Internet, are destined to play a growing role in the provision of services, enquiries aboutoperations and product information.

Optimization of the branch network

In recent years the Group has implemented a plan to expand the number of branch offices in the pursuit of greatermarket share and to insure the closest possible approximation to potential customers in areas with good growthprospects. In the three years 1999-2001 the retail commercial network in Spain (Banco Popular and the five regionalbanks) added 157 branch offices bringing the total to 2,110 branches at the end of 2001.

In 2002, the application of more selective criteria led to the opening of 40 new branch offices, mainly in majormetropolitan areas and certain tourist locations, and to the closure of 36 branches whose business volume or scantprofitability did not justify their continued existence. In short, the net increase in 2002 was four branch offices.

The Group also opened five new private banking branch offices in 2002, bringing the total outlets for the specializednetwork in this business segment to fifteen branches at the end of the year.

Internet banking: the Group's new corporate portal

Bank-on-line, the Group's Internet distribution channel, continued to grow at a strong rate during 2002, and by year endhad 884,000 customers, an increase of 270,000 (44%) in the year.

A new corporate portal was also launched that provides exhaustive information about the products of the Group banksand subsidiaries, most of which can be obtained through the site, together with a wizard for customers to facilitatebrowsing. The portal, the design of which has also been improved, also offers other added value services (a businesssearch engine, company information) and links to other Internet portals.

The commercial penetration of Bank-on-line, i.e. the number of customers who have signed up for this service, hasincreased appreciably and at year end had reached 45% of legal entity customers and nearly 17% of private individuals.These figures reflect the close interrelationship of Internet and conventional banking services.

New commercial management tools

In 2002 the Group equipped itself with new instruments to strengthen its commercial action, including most notably theimplementation of an analytical and operational CRM (Customer Relationship Management) system which makes itpossible, by means of greater knowledge of the customers and their product preferences, to design managementcampaigns and processes targeted on specific segments of the business.

22

Table 8 is a breakdown of theloans and discounts at December 31,2002, by type and sector, with thecomparative figures for 2001.

The credit extended to privatesector residents (other residents inthe table), which accounts for 95% ofthe total , amounted to €32,741million, a year-on-year increase of22.8%. Analysis by type disclosesthat mortgage loans, mostly forhomes, were the most dynamiccomponent, with year-on-year growthof 43.4% (35.3% adjusted for theinclusion of BPH), and accounted fornearly 47% of the Group's total loansand discounts. Trade discounts,which also include factoring and othertransact ions, were up by 6.5%,leasing transactions by 12.3% andoverdrafts by 15.1%, while unsecuredcredits and loans (other term loans)grew by 5.9%.

In 2002 the Group's loans andcredits to private sector residentsgrew much faster than in the Spanishfinancial system as a whole, with anedge of 9.2 percentage points over

Spanish all Spanish banks, of 2.5percentage points over savings banksand of 6.1 percentage points on theaggregate of banks and savingsbanks. As was the case in 2001,Banco Popular continued to win creditmarket share in 2002 in the domesticmarket, which is its area of priorityactivity.

Figure 8 plots the variation inlending to private sector residents byall Spanish banks and savings bankscompared with that of the Group inthe period from November 2001 toNovember 2002 (the latest for whichBank of Spain data are available). Asthis figure reveals, Banco Popularoutperformed both the banks and thesavings banks, and particularly theb a n k s , t h r o u g h o u t t h e p e r i o danalyzed.

Additional information about thestructure and features of loans anddiscounts is presented below.

Table 9 is a breakdown, for thelast two years, of year-end loans anddiscounts by amount and term. This

t a b l e s h o w s a h i g h d e g r e e o fdispersion of risks and a gradual shiftto longer terms and higher amounts,due to the expansion of mortgagelending in the small amounts and thegrowth of lending to companies, in themedium and high amounts.

The distribution of loans anddiscounts (business in Spain) byregion in Spain in the last five years isshown in Table 10, which also revealsthe high degree of dispersion of risksby location.

Table 9. Year-end lending matrix (%)

Up to 150 TotalOver 600150 to 600

Up to 3 months . . . . .3 months to 1 year . .1 to 3 years. . . . . . . .Over 3 years . . . . . . .

Total . . . . . .

6.184.342.316.71

19.54

13.6310.569.34

23.84

57.37

2002

26.1020.6014.7138.59

100.00

6.295.703.068.04

23.09

2001200220012002200120022001

Amounts (€ thousand)

Term

9.878.238.55

26.11

52.77

18.3617.5716.3447.73

100.00

4.475.905.27

13.36

29.01

4.013.442.528.26

18.23

Customer funds (on- and off- balancesheet)

Loans and discounts

Fig.9 Customer funds and loansand discounts per employee (€ thousand)

0201009998

3,500

2,875

2,250

1,625

1,000

3,205

2,645

2,260

1,457

2,754

1,952

2,313

2,888

2,484

1,641

Customer funds (on- and off- balancesheet)

Loans and discounts

Fig.10 Customer funds and loansand discounts per branch (€ thousand)

0201009998

20,000

16,500

13,000

9,500

6,000

11,265

15,266

16,582

18,494

13,649

12,976

15,890

8,596

14,301

9,451

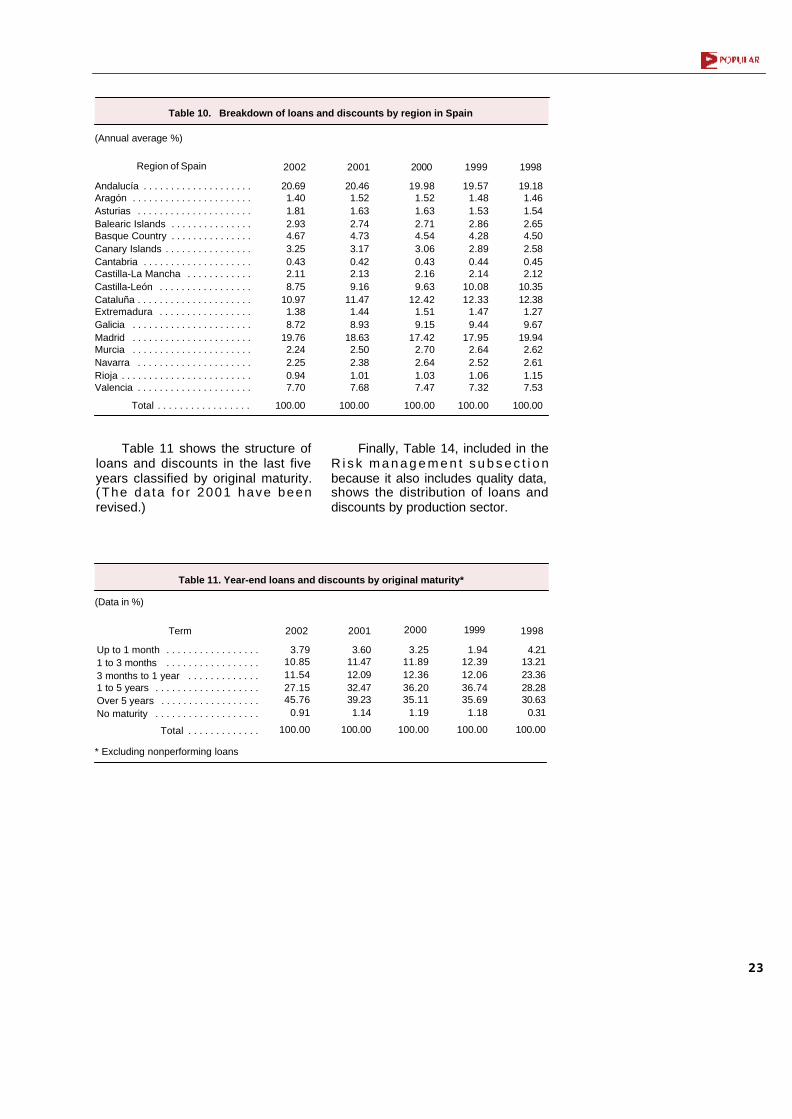

Table 11 shows the structure ofloans and discounts in the last fiveyears classified by original maturity.(The da ta fo r 2001 have beenrevised.)

Finally, Table 14, included in theR i s k m a n a g e m e n t s u b s e c t i o nbecause it also includes quality data,shows the distribution of loans anddiscounts by production sector.

23

Table 10. Breakdown of loans and discounts by region in Spain

Andalucía . . . . . . . . . . . . . . . . . . . .Aragón . . . . . . . . . . . . . . . . . . . . . .Asturias . . . . . . . . . . . . . . . . . . . . .Balearic Islands . . . . . . . . . . . . . . .Basque Country . . . . . . . . . . . . . . .Canary Islands . . . . . . . . . . . . . . . .Cantabria . . . . . . . . . . . . . . . . . . . .Castilla-La Mancha . . . . . . . . . . . .Castilla-León . . . . . . . . . . . . . . . . .Cataluña . . . . . . . . . . . . . . . . . . . . .Extremadura . . . . . . . . . . . . . . . . .Galicia . . . . . . . . . . . . . . . . . . . . . .Madrid . . . . . . . . . . . . . . . . . . . . . .Murcia . . . . . . . . . . . . . . . . . . . . . .Navarra . . . . . . . . . . . . . . . . . . . . .Rioja . . . . . . . . . . . . . . . . . . . . . . . .Valencia . . . . . . . . . . . . . . . . . . . . .

Total . . . . . . . . . . . . . . . . .

2001 2000 1999 19982002

20.691.401.812.934.673.250.432.118.75

10.971.388.72

19.762.242.250.947.70

100.00

20.461.521.632.744.733.170.422.139.16

11.471.448.93

18.632.502.381.017.68

100.00

19.981.521.632.714.543.060.432.169.63

12.421.519.15

17.422.702.641.037.47

100.00

19.571.481.532.864.282.890.442.14

10.0812.33

1.479.44

17.952.642.521.067.32

100.00

19.181.461.542.654.502.580.452.12

10.3512.381.279.67

19.942.622.611.157.53

100.00

Region of Spain

(Annual average %)

2001 2000 1999 19982002

Table 11. Year-end loans and discounts by original maturity*

* Excluding nonperforming loans

Term

Up to 1 month . . . . . . . . . . . . . . . . .1 to 3 months . . . . . . . . . . . . . . . . .3 months to 1 year . . . . . . . . . . . . .1 to 5 years . . . . . . . . . . . . . . . . . . .Over 5 years . . . . . . . . . . . . . . . . . .No maturity . . . . . . . . . . . . . . . . . . .

Total . . . . . . . . . . . . .

3.7910.8511.5427.1545.76

0.91

100.00

3.6011.4712.0932.4739.231.14

100.00

3.2511.8912.3636.2035.11

1.19

100.00

1.9412.3912.0636.7435.69

1.18

100.00

4.2113.2123.3628.2830.63

0.31

100.00

(Data in %)

24

Off-balance sheet risks

This category, included undermemorandum accounts, consists ofthe risks with customers not involvingthe disbursement of funds, alsoreferred to as off-balance sheet risks:avals, other sureties, documentarycredits and other guarantees.

These risks amounted to €5,284million at 2002 year end, up 23.5%year-on-year.

Table 12 contains comparative2002/2001 details of the compositionof these risks, classified by type ofoperation, and discloses the amounto f t he ba lances deemed to bedoubtfully recoverable and of the lossallowances booked for them.

Table 12. Year-end off-balance sheet risks

Guarantees and other sureties:

Credit and off-balance sheet risks of third parties .Foreign trade transactions . . . . . . . . . . . . . . . . . .Deferred payments on sales . . . . . . . . . . . . . . . .Housing construction . . . . . . . . . . . . . . . . . . . . .Construction, service or supply contracts . . . . . .Participation in tenders . . . . . . . . . . . . . . . . . . . .Liabilities to administrative agencies . . . . . . . . . . .Other liabilities . . . . . . . . . . . . . . . . . . . . . . . . . .

Documentary credits . . . . . . . . . . . . . . . . . . . . . . . .

Other contingent liabilities . . . . . . . . . . . . . . . . . . . .

Total . . . . . . . . . . . . . . . . . . . . . . . . . .

Pro memoria: Balances classified as doubtful . . . . .

Allowance for doubtful balances and country-risk . . .

Guarantees provided for. . .2002 2001% %

% variation

(€ thousand)

3,941,196

317,390103,875206,62044,474

498,56361,852

1,548,3121,160,110

310,717

27,111

4,279,024

8,917

(54,691)

4,897,752

319,043147,002404,08768,895

708,93286,419

1,654,1511,509,223

307,571

78,256

5,283,579

9,046

(70,207)

92.70

6.042.787.651.30

13.421.64

31.3128.56

5.82

1.48

100.00

0.17

(1.33)

92.11

7.422.434.831.04

11.651.45

36.1827.11

7.26

0.63

100.00

0.21

(1.28)

24.3

0.541.595.654.942.239.7

6.830.1

(1.0)

>

23.5

1.4

28.4

Risk management

Analysis of risk management inthe year must include a detailedexamination of the quality of the risksassumed by the Group on and off thebalance sheet and of the coveragebooked for possible losses that mayarise therefrom.

The substantial progression ofthe Group's lending activity in 2002was accompan ied by r i go rousanalysis of credi t requests andongoing monitoring of the risks, andeven more so in an environment likethat presently existing of economicslowdown and less visibility of thefuture. At the same time, in 2002 theGroup strengthened its criteria ofprudence by means of provisions tol o s s a l l o w a n c e s w h i c h , a s i s

customary, were higher than thoseset by the demanding Span ishbanking regulations.

The Group therefore starts theyear 2003 from a position of greats o u n d n e s s , i n a n t i c i p a t i o n o feconomic recovery being weaker ortardier than expected.

For the purposes of the followinganalysis, four categories of risk areaddressed: credit risk, cross-borderrisk, market risk and liquidity risk.

Credit risk

Cred i t r i sk a r i ses f rom thepossible loss triggered by the non-recovery of loans and discounts asregards their principal, interest andother contractual obligations of the

25

borrowers. In the case of off-balancesheet risks, it arises from the possiblefailure by customers to fulfill theircommitments, thus forcing the Bankto assume them because of theguarantee provided.

Since the Group's activities focusmainly on the domestic commercialbanking business, credit risk is themost important of the risks consideredhere.

Credit risk analysis requires theexistence of systematic proceduresfor classification of risks as past dueassets (in the event of breach of theloan repayment terms), doubtfullycollectible assets (due to the poorstate of the borrower's f inancialcondition), or disputed assets (wherethe existence of litigation makes asatisfactory outcome problematical).In the following paragraphs thesethree categories are denominated asa whole nonperforming loans ortroubled balances receivable.

R i sks t ha t i t has no t beenpossible to recover in the regulatorilystipulated terms are classified as baddebts and are written off and removedfrom the balance sheet using theprovisions recorded for this purposeor charged d i rec t l y to income,al though the Bank cont inues topursue repayment of them.

As coverage for its credit risk, theBank has booked a cred i t lossallowance, provisions to which arecharged to income and which is thesum of the three component itemsdescribed below.

F i r s t , t h e r e i s a s p e c i f i callowance for nonperforming loans inaccordance wi th a regu la tor i l yestablished calendar and, in the caseof the doubtful or disputed balances,based on a conservative estimate oftheir recoverability. Also, when aba lance c lass i f ied as t roub ledexceeds a stipulated percentage(25%), the regulations require aprov is ion to be booked fo r theremainder of the transaction or for thetotal risk of that particular borrower

( t h e s o - c a l l e d " c a r r y f o r w a r d "provisions).

Risk management thereforerequires all the assets to be correctlyc l a s s i f i e d , t r a n s f e r r i n g t o t h enonperforming loans caption thosethat meet any of the aforementionedconditions, and thereafter to recordprovisions for covering them. As anadditional measure of prudence,classi f icat ion as nonperformingtriggers the non-accrual of the intereston t hese asse ts , wh i ch i s no trecognized in income unless it iseffectively collected.

Secondly, there is a generalcredit loss allowance covering all thea s s e t s n o t c l a s s i f i e d a snonperforming, provision to which iscalculated as 1% of all outstandingrisks (loans and discounts, privatefixed-interest securit ies and off-balance sheet risks). The percentagei s 0 . 5 % i n t h e c a s e o f c e r t a i nmortgage assets deemed to be of lowrisk.

Thirdly, there is the statisticalcoverage allowance established bythe Bank of Spain and in force sinceJune 2000, which as in the previouscase is also applied for all outstandingrisks and is calculated in accordancewith coefficients based on the type ofrisk assumed (unsecured loans andcredits, secured balances, consumerfinancing, etc.).

Pursuant to these criteria, thecontrol of risk quality requires ameticulous process which starts withthe analysis of loan proposals,continues with the monitoring of therisks already assumed, and does notend until the borrowings are finallyrepa id i n acco rdance w i th theprojected contractual conditions.

For this purpose the Group hasin p lace formal procedures fore x t e n d i n g c r e d i t a n d f o r r i s kprevention, with which it permanentlyevaluates the borrowers on the basisof numerous variables, especially theeconomic and financial situation ofthe borrower and the data generated

26

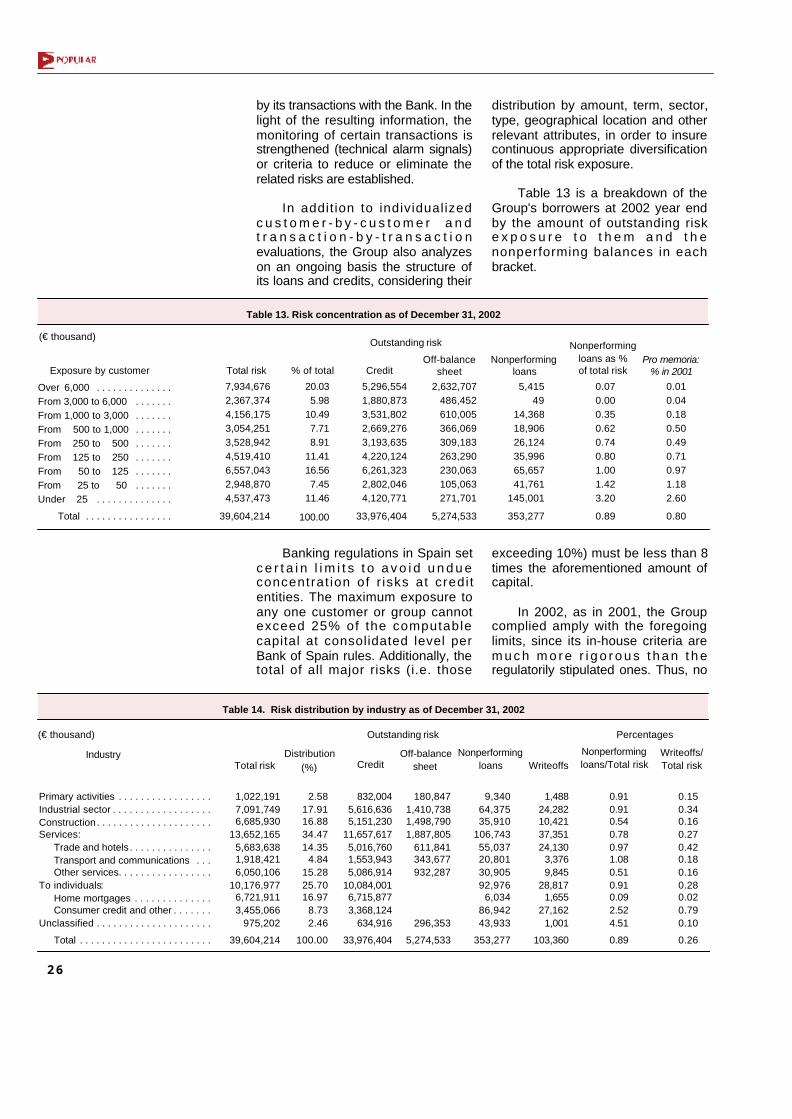

by its transactions with the Bank. In thelight of the resulting information, themonitoring of certain transactions isstrengthened (technical alarm signals)or criteria to reduce or eliminate therelated risks are established.

In addit ion to individualizedc u s t o m e r - b y - c u s t o m e r a n dt r a n s a c t i o n - b y - t r a n s a c t i o nevaluations, the Group also analyzeson an ongoing basis the structure ofits loans and credits, considering their

distribution by amount, term, sector,type, geographical location and otherrelevant attributes, in order to insurecontinuous appropriate diversificationof the total risk exposure.

Table 13 is a breakdown of theGroup's borrowers at 2002 year endby the amount of outstanding riske x p o s u r e t o t h e m a n d t h enonperforming balances in eachbracket.

Table 13. Risk concentration as of December 31, 2002

Over 6,000 . . . . . . . . . . . . . .From 3,000 to 6,000 . . . . . . .From 1,000 to 3,000 . . . . . . .From 500 to 1,000 . . . . . . .From 250 to 500 . . . . . . .From 125 to 250 . . . . . . .From 50 to 125 . . . . . . .From 25 to 50 . . . . . . .Under 25 . . . . . . . . . . . . . .

Total . . . . . . . . . . . . . . . .

CreditOff-balance

sheetNonperforming

loansTotal risk % of total

Nonperformingloans as % of total risk

Pro memoria:% in 2001Exposure by customer

Outstanding risk(€ thousand)

5,296,5541,880,8733,531,8022,669,2763,193,6354,220,1246,261,3232,802,0464,120,771

33,976,404

2,632,707486,452610,005366,069309,183263,290230,063105,063271,701

5,274,533

5,41549

14,36818,90626,12435,99665,65741,761

145,001

353,277

7,934,6762,367,3744,156,1753,054,2513,528,9424,519,4106,557,0432,948,8704,537,473

39,604,214

20.035.98

10.497.718.91

11.4116.567.45

11.46

100.00