an acuris company cmbs monthly update august 2017 … 2017 cmbs report 2.pdf · cmbs monthly report...

TRANSCRIPT

An Acuris Company

CMBS Monthly Update

AUGUST 2017

A Guide to United States CMBS Monthly Activity

Debtwire.com

CMBS Monthly Update

AUGUST 2017

A Monthly Guide to US CMBS Activity

Debtwire.com

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 2

Debtwire ABS

CONTENTS CMBS CREDIT UPDATE: 3

DISTRESSED LOANS UPDATE: 4

SECONDARY MARKET OVERVIEW: 5

SECONDARY MARKET DATA: 6

PRIMARY MARKET OVERVIEW: 7

PLACED ISSUANCE DATA: 8

JUNE ISSUANCE: 9-14

JUNE HEADLINES: 15-17

ABOUT US: 18

PRIMARY AUTHORS Ganesh Kalicharan

CRE Database Manager

+1 212 390 7845

Maura Webber Sadovi

Reporter, Assistant Editor

+1 773 540 8950

Sarika Gangar

Reporter

+1 408 891 2055

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 3

Hurricane Harvey’s path of destruction across Texas and Louisiana dominated investors’

attention as August closed out. Morningstar estimates that CMBS loan exposure is USD 19.4bn,

comprised of 1,529 commercial properties backing 1,277 CMBS loans. The volume of Fitch-rated

CMBS properties with exposure to Harvey is estimated at over USD 10bn, significantly larger

than the USD 2.4bn in Fitch-rated CMBS exposed to Hurricane Katrina.

Several CMBS with exposure to Hurricane Harvey traded during the last week of August, in some

cases as much as 10bps-12bps wider. Vacation season and a lack of specific property damage

details kept the late-August market reaction modest, said one investor.

Special servicers and borrowers continued to work out legacy loans in August. Special servicer C-

III Asset Management is planning to foreclose on 400 Atlantic Street, the Stamford, Connecticut,

office property that secures a USD 265m loan in GSMS 2007-GG10. The servicer is also analyzing

a suggested plan for a discounted payoff, which it has received from the borrower of the USD

55.5m Rosemont Commons loan in GSMS 2007-GG10.

CBL & Associates Properties reached a preliminary agreement to modify the USD 124.2m Mall of

Acadiana loan in BACM 2007-2, which is backed by a Lafayette, Louisiana, retail property. The REIT

also gave back the keys to Chesterfield Mall in Chesterfield, Missouri, which is held in LBUBS

2006-C6.

The USD 80m Bangor Mall loan in MSC 2007-1Q16 transferred to special servicer LNR Partners

due to imminent maturity default. The note on the Simon Property Group-owned shopping

center matures in October.

The largest tenant in the seven-property PPG Portfolio may not renew its lease next December

and exit two of the properties — or it might buy them. The medical offices back a USD 96.6m

loan comprising 64.3% of MSC 2006-HQ10.

A foreclosure sale on One AT&T Center, a 1.2m sq ft St. Louis, Missouri, office property, was

scheduled for 22 August. The building secures a USD 107.1m loan in BSCMS 2007-T26.

The USD 115.5m Koger Center loan has been modified to receive a three-year extension,

pushing its maturity to February 2020. The note makes up 21.9% of CSMC 2007-C1. The USD

51.7m Cherry Hill Corporate Center Pool loan, secured by a Massachusetts flex-industrial

building portfolio, was liquidated this month, causing a USD 674,210 realized loss to WBCMT

2007-C31.

The USD 25.5m Parkway Plaza loan, pulled from CD 2007-CD5, was bid at auction at USD 19.8m,

or 78 cents on the dollar. The final bid fell short of a July 2016 appraised value of USD 22m. The

sale is special servicer LNR Partners’ second attempt at unloading the note on the Norman,

Oklahoma, retail center.

Falling occupancy is creating long-term maturity default risk for the USD 38m Sarasota Square

loan in COMM 2013-CR9. Morningstar estimates the loan’s LTV has skyrocketed to 97.4% based

on current valuations. A Texas office property backing a USD 91m loan in WFRBS 2014-C24 is

facing occupancy issues as tenants BP and ConocoPhillips head for the exits. The 450,154 sq ft

property, Two Westlake Park, is located in Houston’s Energy Corridor.

A Los Angeles LLC that owns Crossroads Marketplace, a Chino Hills, California, retail center with

a USD 62m CMBS loan in special servicing, filed for Chapter 11 bankruptcy protection. The loan

makes up 10.3% of CGCMT 2007-C6. The University of Wisconsin-Oshkosh Foundation, the

university’s private fundraising group, has filed for Chapter 11 bankruptcy to protect itself from

ongoing litigation related to several real estate projects.

A New York state judge dismissed a complaint filed by Davidson Kempner Capital Management

against C-III Asset Management over the special servicer’s sale of loans from CSMC 2007-C5,

finding that DKCM doesn’t have standing to sue. An attorney for DKCM declined to say whether

the company will appeal, then described the decision as a “preliminary procedural hurdle.”

CWCapital is marketing six CMBS notes totaling USD 147m. The largest is a USD 64m loan on an

Orem, Utah, office complex. LNR Partners and C-III also have loans in the market. Exposed deals

include LBUBS 2006-C4, LBUBS 2007-C1, BSCMS 2006-PW11, WBCMT 2007-C32, BACM 2006-6

and BACM 2008-1.

CMBS Credit Update:

Harvey CMBS exposure estimates as high as USD 19.4bn; servicers make moves on 400 Atlantic and Mall of Acadiana workouts

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 4

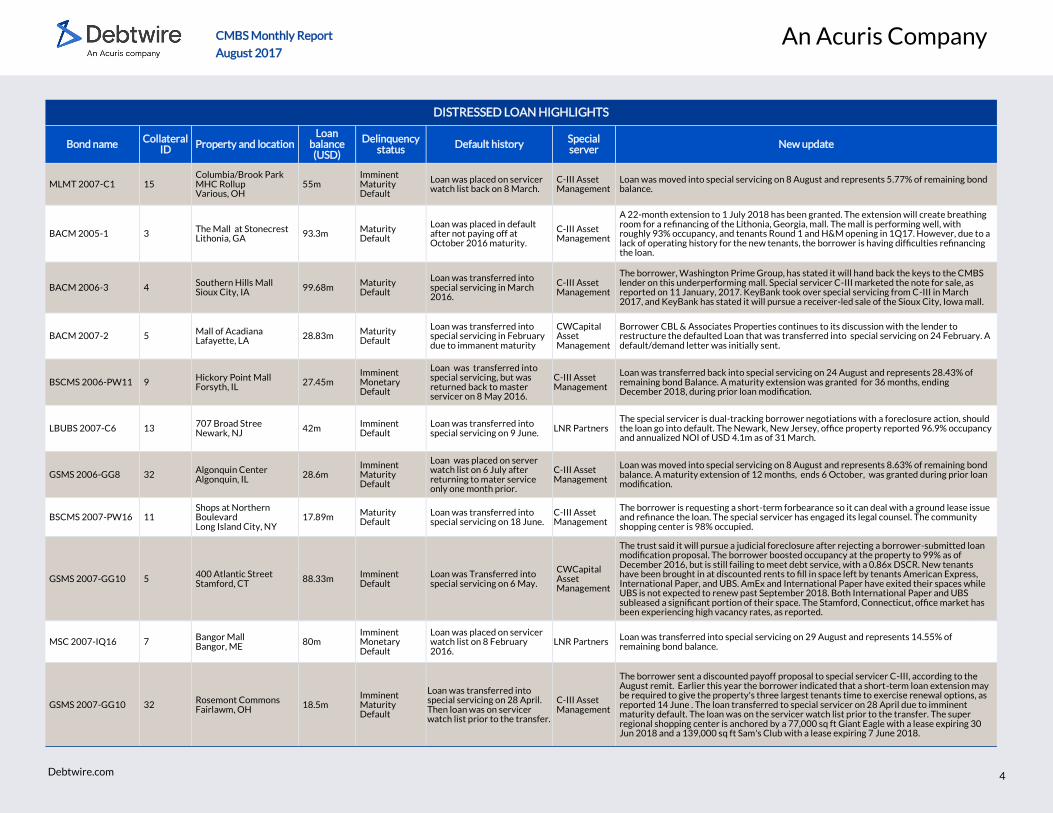

DISTRESSED LOAN HIGHLIGHTS

Bond name Collateral

ID Property and location

Loan balance (USD)

Delinquency status

Default history Special server

New update

MLMT 2007-C1 15 Columbia/Brook Park MHC Rollup Various, OH

55m Imminent Maturity Default

Loan was placed on servicer watch list back on 8 March.

C-III Asset Management

Loan was moved into special servicing on 8 August and represents 5.77% of remaining bond balance.

BACM 2005-1 3 The Mall at Stonecrest Lithonia, GA

93.3m Maturity Default

Loan was placed in default after not paying off at October 2016 maturity.

C-III Asset Management

A 22-month extension to 1 July 2018 has been granted. The extension will create breathing room for a refinancing of the Lithonia, Georgia, mall. The mall is performing well, with roughly 93% occupancy, and tenants Round 1 and H&M opening in 1Q17. However, due to a lack of operating history for the new tenants, the borrower is having difficulties refinancing the loan.

BACM 2006-3 4 Southern Hills Mall Sioux City, IA 99.68m

Maturity Default

Loan was transferred into special servicing in March 2016.

C-III Asset Management

The borrower, Washington Prime Group, has stated it will hand back the keys to the CMBS lender on this underperforming mall. Special servicer C-III marketed the note for sale, as reported on 11 January, 2017. KeyBank took over special servicing from C-III in March 2017, and KeyBank has stated it will pursue a receiver-led sale of the Sioux City, Iowa mall.

BACM 2007-2 5 Mall of Acadiana Lafayette, LA

28.83m Maturity Default

Loan was transferred into special servicing in February due to immanent maturity

CWCapital Asset Management

Borrower CBL & Associates Properties continues to its discussion with the lender to restructure the defaulted Loan that was transferred into special servicing on 24 February. A default/demand letter was initially sent.

BSCMS 2006-PW11 9 Hickory Point Mall Forsyth, IL

27.45m Imminent Monetary Default

Loan was transferred into special servicing, but was returned back to master servicer on 8 May 2016.

C-III Asset Management

Loan was transferred back into special servicing on 24 August and represents 28.43% of remaining bond Balance. A maturity extension was granted for 36 months, ending December 2018, during prior loan modification.

LBUBS 2007-C6 13 707 Broad Stree Newark, NJ

42m Imminent Default

Loan was transferred into special servicing on 9 June.

LNR Partners The special servicer is dual-tracking borrower negotiations with a foreclosure action, should the loan go into default. The Newark, New Jersey, office property reported 96.9% occupancy and annualized NOI of USD 4.1m as of 31 March.

GSMS 2006-GG8 32 Algonquin Center Algonquin, IL

28.6m Imminent Maturity Default

Loan was placed on server watch list on 6 July after returning to mater service only one month prior.

C-III Asset Management

Loan was moved into special servicing on 8 August and represents 8.63% of remaining bond balance. A maturity extension of 12 months, ends 6 October, was granted during prior loan modification.

BSCMS 2007-PW16 11 Shops at Northern Boulevard Long Island City, NY

17.89m Maturity Default

Loan was transferred into special servicing on 18 June.

C-III Asset Management

The borrower is requesting a short-term forbearance so it can deal with a ground lease issue and refinance the loan. The special servicer has engaged its legal counsel. The community shopping center is 98% occupied.

GSMS 2007-GG10 5 400 Atlantic Street Stamford, CT

88.33m Imminent Default

Loan was Transferred into special servicing on 6 May.

CWCapital Asset Management

The trust said it will pursue a judicial foreclosure after rejecting a borrower-submitted loan modification proposal. The borrower boosted occupancy at the property to 99% as of December 2016, but is still failing to meet debt service, with a 0.86x DSCR. New tenants have been brought in at discounted rents to fill in space left by tenants American Express, International Paper, and UBS. AmEx and International Paper have exited their spaces while UBS is not expected to renew past September 2018. Both International Paper and UBS subleased a significant portion of their space. The Stamford, Connecticut, office market has been experiencing high vacancy rates, as reported.

MSC 2007-IQ16 7 Bangor Mall Bangor, ME

80m Imminent Monetary Default

Loan was placed on servicer watch list on 8 February 2016.

LNR Partners Loan was transferred into special servicing on 29 August and represents 14.55% of remaining bond balance.

GSMS 2007-GG10 32 Rosemont Commons Fairlawm, OH

18.5m Imminent Maturity Default

Loan was transferred into special servicing on 28 April. Then loan was on servicer watch list prior to the transfer.

C-III Asset Management

The borrower sent a discounted payoff proposal to special servicer C-III, according to the August remit. Earlier this year the borrower indicated that a short-term loan extension may be required to give the property's three largest tenants time to exercise renewal options, as reported 14 June . The loan transferred to special servicer on 28 April due to imminent maturity default. The loan was on the servicer watch list prior to the transfer. The super regional shopping center is anchored by a 77,000 sq ft Giant Eagle with a lease expiring 30 Jun 2018 and a 139,000 sq ft Sam's Club with a lease expiring 7 June 2018.

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 5

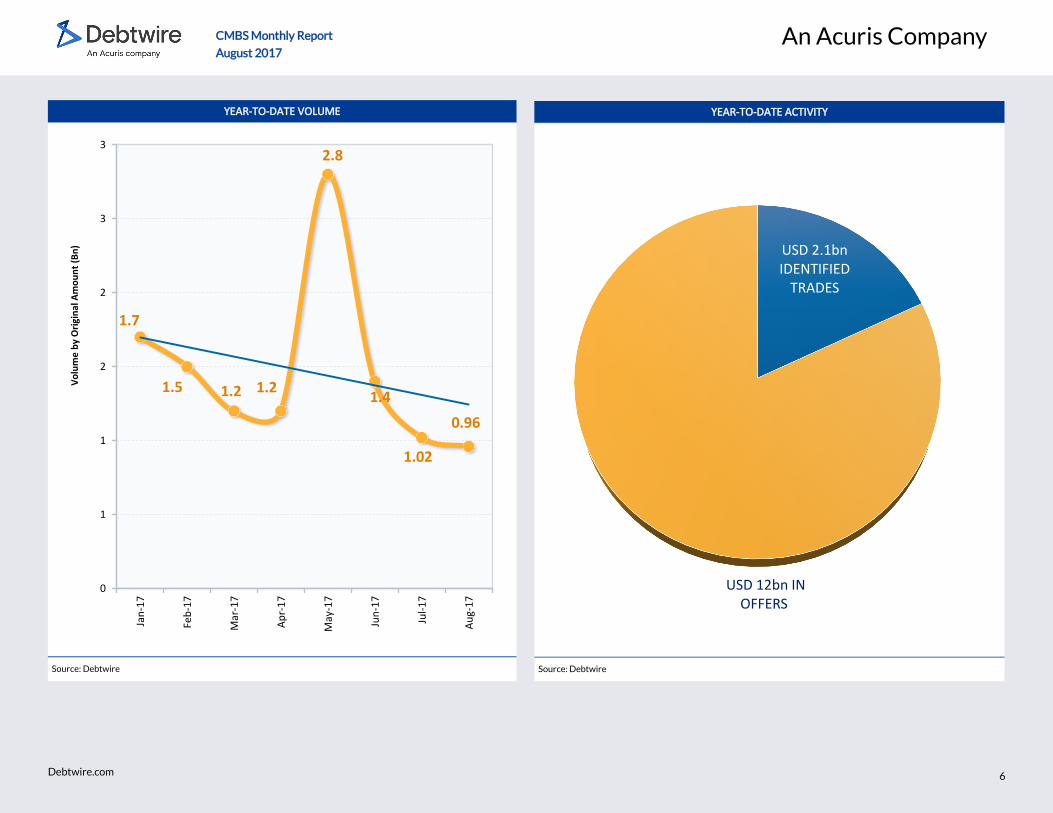

CMBS spreads held generally steady in August despite investor concerns about North Korea and the impact of Hurricane Harvey on CMBS backed by Houston-area commercial real estate.

For instance, post-crisis BBB- and A rated bonds ratcheted in to touch new lows for the year while AAAs and AAs held steady. BWIC volume fell to USD 958m (original) in the month from USD 1.02bn in July, reflecting the traditionally lighter trading volumes of late August.

Spreads on CMBS 2.0 BBB- and A bonds tightened by 7bps and 3bps, respectively, to 12-month-trailing period lows of S+ 388bps and S+ 172bps, according to investment bank analysts. Benchmark 10-year AAAs held steady at 89bps, and AA rated paper was steady at S+ 140bps after widening in July.

Legacy market spreads remained generally at July levels, with AJs, AMs, and benchmark AAAs at S+ 450bps, S+ 245bps and S+ 100bps, respectively. Liquidity lower in the stack is getting a boost from life insurers who bought more non-AAA rated CLO and CMBS paper in 1H17, according to Wells Fargo analysts.

Primary dealer holdings ticked down to USD 6.6bn for the week ending 16 August, compared with USD 6.9bn for the week ending 19 July, according to the Federal Reserve Bank of New York. From mid-June through mid-July, primary dealer CMBS holdings rose above USD 7bn for the first time in over a year.

The spread tightening was evident in the SASB sector early in the month. For instance, on 7 August a USD 3m AAA rated A bond from BAMLL 2012-PARK covered at S+ 56bps, after being talked at S+ 58bps. A USD 5m piece covered at S+ 64bps on 25 January, according to Debtwire ABS data. Also on 7 August, a USD 3m AAA rated A bond from VNDO 2012-6AVE covered at S+ 57bps, 2bps tight of talk. A USD 5m piece covered at S+ 63bps on 25 January.

Spreads remained tight later in the month as well. On 31 August a USD 16m WBCMT 2007-C33 AJ with exposure to the 666 Fifth Avenue New York City tower covered at 102-18, after being talked at prices in the 100-102 range, according to Empirasign. The property is partly owned by Jared Kushner’s family company.

But, as usual, some bonds traded wide due to specific collateral concerns. Collateral performance has improved in many seasoned deals, while others have had more successes refinancing than initially projected, according to one trader. Still, it’s “not 100% better for all deals. … Some are very leveraged to a couple trouble loans with adverse selection impacting the tail.”

For instance, a USD 2.2m BBB- rated WFCM 2015-C26 D covered wide at S+ 600bps after being talked in the S+ 565bps area on 14 August, according to Empirasign. The deal’s largest loans include the current USD 45.9m Chateau on the Lake full-service hotel in Branson, Missouri, owned by an affiliate of John Q Hammons Hotels and Resorts, which is in bankruptcy.

And after Hurricane Harvey a few trades of AAA bonds backed by debt on The Houston Galleria mall were 10bps-12bps wider than trades earlier in the month. But other bonds with Harvey exposure were talked at spreads tight or in line with recent history.

For example, a USD 1.1m JPMBB 2015-C28 A1 and a USD 1.4m JPMBB 2015-C28 A2 covered on 30 August at S+ 17bps and S+ 31bps, respectively, according to Empirasign. A USD 4m A2 piece of the deal was talked at S+ 35bps in March. The 1.2m sq ft super-regional Galleria mall in Houston backs the USD 1.05bn HGMT 2015-HGLR and USD 150m of debt in JPMBB 2015-C28.

A USD 16.158m DBUBS 2011-LC2A A1 and a USD 7.7m DBUBS 2011-LC2A A1FL traded 30 August after being talked at S+ 30bps and S+ 66.6bps, respectively, according to Empirasign. A USD 1.33m A1 piece was talked on 31 January at S+ 30bps. The transaction’s second-largest credit is the USD 214.525m Willowbrook Mall loan, backed by the 1.3m sq ft Houston retail property, Trepp data show.

A clearer view of the full impact of Harvey on commercial property and CMBS values will emerge later, investors say. “We’re still in a situation with life-saving operations going on down there,” said one investor on 31 August. “The reality is, when we make calls, there’s no one answering. We’re just hopeful that there is sufficient insurance in place to deal with this.”

CMBS Secondary Market:

Secondary tights hold steady as markets awaits Harvey’s full impact

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 6

YEAR-TO-DATE VOLUME

Source: Debtwire

1.7

1.5 1.2 1.2

2.8

1.4

1.02

0.96

0

1

1

2

2

3

3Ja

n-1

7

Feb

-17

Mar

-17

Ap

r-1

7

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Vo

lum

e b

y O

rigi

nal

Am

ou

nt

(Bn

)

YEAR-TO-DATE ACTIVITY

Source: Debtwire

USD 2.1bn IDENTIFIED

TRADES

USD 12bn IN OFFERS

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 7

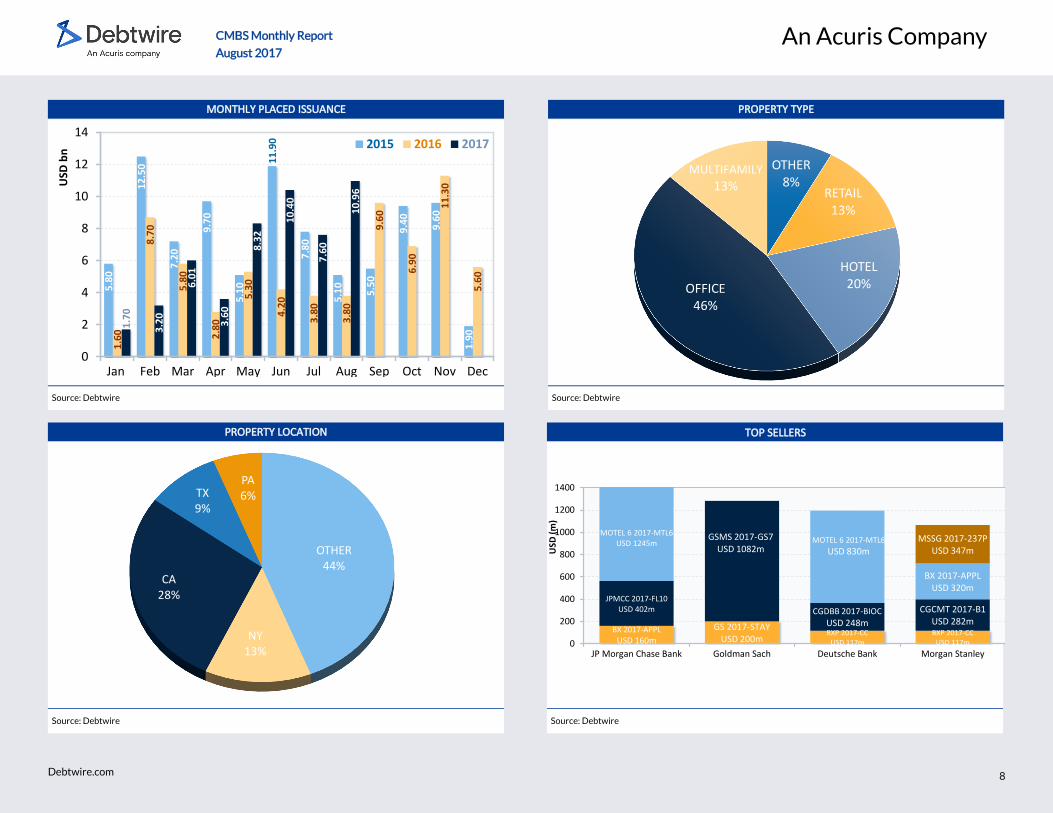

New CMBS issuance rose to USD 10.955bn in August, making it the most active month for new CMBS issuance this year. Issuers priced USD 7.6bn in July, USD 10.4bn in June and USD 8.3bn in CMBS in May. The supply pushed year-to-date CMBS volume to USD 52.34bn. At this point last year, primary CMBS issuance was just USD 36.1bn.

The single-asset/single-borrower market continued to be the main volume driver. Eight SASB deals priced with a total balance of USD 5.5bn, up from eight deals totaling USD 4bn in July. This month’s volumes were boosted by the late August pricing of the USD 2.1bn Motel 6 2017-MTL6, the largest SASB offering to come to market in almost four years.

JPMorgan and Deutsche Bank priced the Motel 6 deal’s USD 641.8m AAA rated A bonds at L+ 92bps, and its USD 49.7m B- rated G notes at L+ 575bps on 31 August. The deal is secured by interests in 460 Blackstone-owned Motel 6 hotels. In comparison, A bonds from the USD 508m BBCMS 2017-DELC, secured by the luxury Hotel del Coronado near San Diego, priced at L+ 85bps on 17 August.

Blackstone also tapped the market via the USD 825m CGDBB 2017-BIOC, secured by 15 office and lab properties, and the USD 800m BX 2017-APPL, backed by 51 hotel properties. The latter’s USD 251.6m AAA rated A piece printed at L+ 88bps, and USD 121.9m in B rated F bonds priced at L+ 425bps on 1 August.

In the conduit sector, four deals priced for a total of USD 3.9bn, up from USD 3.6bn across four deals in July.

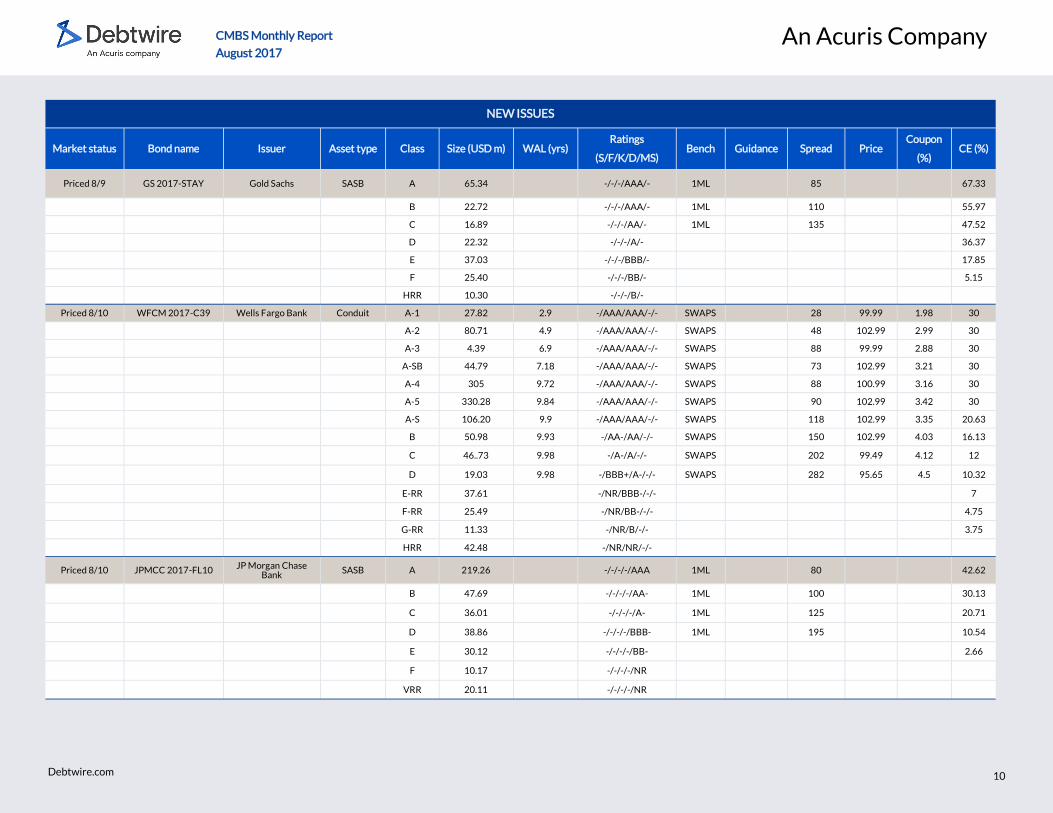

Wells Fargo and Barclays priced the USD 19.73m BBB+/A- rated (Fitch/KBRA) Ds of WFCM 2017-C39 at S+ 282bps on 10 August. The USD 1.1bn conduit’s USD 330.28m benchmark AAA rated A-5s priced at S+ 90bps. The deal is backed by 64 loans on 149 properties. The largest loan in the pool is a USD 70m credit on 225 & 233 Park Avenue South in Manhattan.

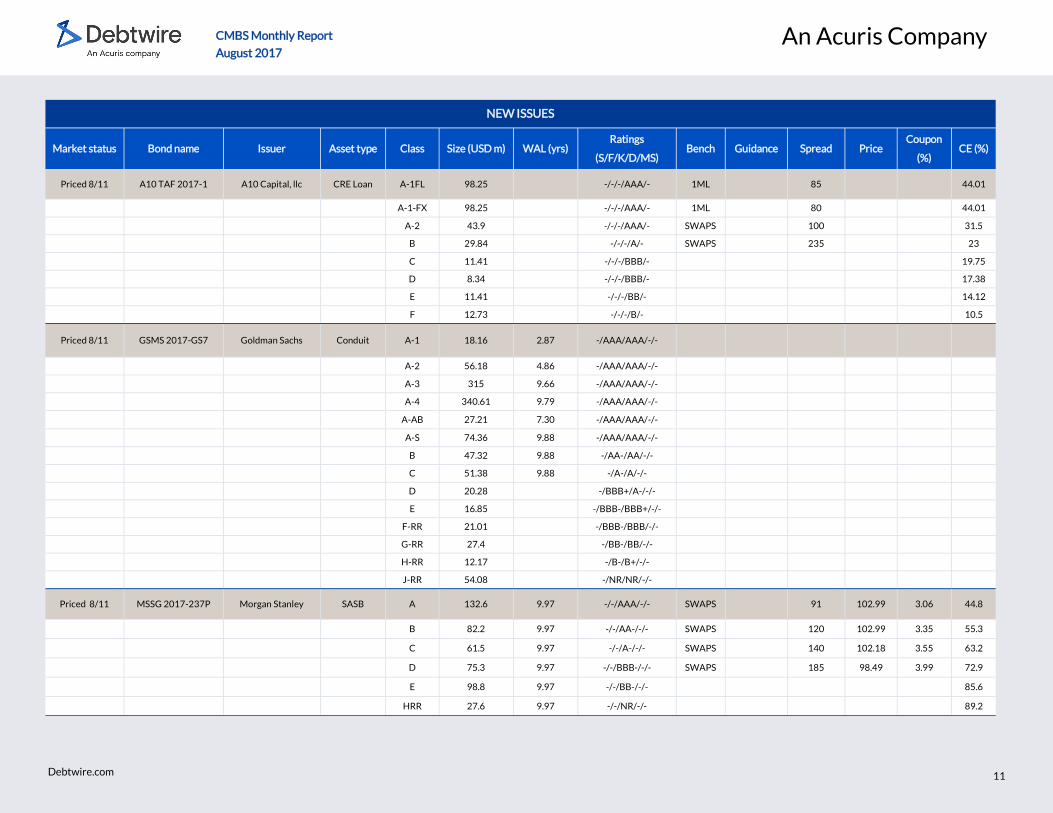

Goldman Sachs priced the USD 51.4m A-/A rated (Fitch/KBRA) Cs of GSMS 2017-GS7 at S+ 175bps on 11 August, 27bps tight of where comparable bonds from the previous conduit, WFCM 2017-C39, priced. The USD 1.1bn GSMS deal’s USD 340.6m benchmark senior AAA rated A-4s priced 5bps wide of where comparable bonds from WFCM priced. The Goldman conduit’s credit challenges include a high office asset class concentration, with 13 office properties comprising 50.4% of the pool balance, according to a Moody’s presale.

The USD 36.89m A-/A (Fitch/DBRS) rated Cs of CGCMT 2017-B1 priced 15 August at S+ 170bps. The USD 941.6m deal’s USD 268.1m AAA A-4s priced at S+ 90bps. Its top loans include a USD 92.7m credit backed by the General Motors Building in New York City and a USD 59m loan backed by the Lakeside Shopping Center in Metairie, Louisiana.

The USD 708.6m UBS 2017-C3 conduit’s USD 28.3m A-/A rated (Fitch/KBRA) Cs priced at S+ 200bps. The deal’s USD 181.922m benchmark A-4 AAAs priced at S+ 94bps.

Also in August, five CRE loan securitizations priced, reflecting a rising appetite for floating-rate paper.

The HUNT CRE 2017-FL1 CRE CLO’s USD 202.6m AAA rated As priced at L+ 100bps on 1 August. Wells Fargo priced the USD 301.78m Bancorp 2017-CRE2 on 11 August. The deal’s AA- rated USD 18.86m Bs priced at L+ 160bps, 5bps tight of where the USD 23.14m in AA rated Bs from the HUNT deal priced.

Early in the month three other smaller deals priced. JPMorgan priced the USD 402.2m JPMCC 2017-FL10’s USD 38.86m BBB- rated Ds and USD 219.26m AAA rated As at L+ 195bps and L+ 80bps, respectively. The RCMF 2017-FL1’s USD 24m BBB- rated Ds priced at L+ 385bps while its USD 141.4m AAA rated As priced at L+ 85bps. Finally, the USD 314.12m A10 TAF 2017-1’s USD 29.84m A rated Bs priced at S+ 235bps and its A1-FLs at L+ 85bps.

CMBS Primary Market:

August surprises with strong new issuance; YTD volume tops 2016

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 8

MONTHLY PLACED ISSUANCE

Source: Debtwire

PROPERTY TYPE

Source: Debtwire

PROPERTY LOCATION

Source: Debtwire

TOP SELLERS

Source: Debtwire

BX 2017-APPL

USD 160m

GS 2017-STAYUSD 200m

BXP 2017-CCUSD 117m

BXP 2017-CCUSD 117m

JPMCC 2017-FL10 USD 402m

GSMS 2017-GS7USD 1082m

CGDBB 2017-BIOC

USD 248m

CGCMT 2017-B1USD 282m

MOTEL 6 2017-MTL6 USD 1245m MOTEL 6 2017-MTL6

USD 830m

BX 2017-APPL USD 320m

MSSG 2017-237P USD 347m

0

200

400

600

800

1000

1200

1400

JP Morgan Chase Bank Goldman Sach Deutsche Bank Morgan Stanley

USD

(m

) OTHER

44%

NY13%

CA28%

TX9%

PA6%

5.8

0

12

.50

7.2

0

9.7

0

5.1

0

11

.90

7.8

0

5.1

0

5.5

0

9.4

0

9.6

0

1.9

0

1.6

0

8.7

0

5.8

0

2.8

0

5.3

0

4.2

0

3.8

0

3.8

0

9.6

0

6.9

0

11

.30

5.6

0

1.7

0

3.2

0

6.0

1

3.6

0

8.3

2

10

.40

7.6

0

10

.96

0

2

4

6

8

10

12

14

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

USD

bn

2015 2016 2017

OTHER8%

RETAIL13%

HOTEL 20%OFFICE

46%

MULTIFAMILY

13%

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 9

NEW ISSUES

Market status Bond name Issuer Asset type Class Size (USD m) WAL (yrs) Ratings

(S/F/K/D/MS) Bench Guidance Spread Price

Coupon

(%) CE (%)

Priced 8/1 BX 2017-APPL Morgan Stanley SASB A 251.56 1.9 -/-/-/AAA/- 1ML 88 100 66.9

B 88.83 1.9 -/-/-/AA/- 1ML 115 100 55.21

C 66.03 1.9 -/-/-/A/- 1ML 140 100 46.53

D 87.31 1.9 -/-/-/BBB/- 1ML 205 100 35.04

E 137.56 1.9 -/-/-/BB/- 1ML 315 100 16.94

F 121.89 1.9 -/-/-/NR/- 1ML 425 100 0.9

G 6.84 1.9 -/-/-/NR/- 1ML

RR 40 -/-/-/NR/-

Priced 8/2 RCMF 2017-FL1 Sutherland Asset

Management Corp. CRE Loan A 141.40 -/-/AAA/-/- 1ML 85 42

B 18.5 -/-/AA-/-/- 1ML 165 34.41

C 14.9 -/-/A-/-/- 1ML 225 28.3

D 24 -/-/BBB-/-/- 1ML 385 18.46

E 8.2 -/-/BB-/-/- 15.09

F 10.3 -/-/B-/-/- 10.87

G 26.5 -/-/NR/-/-

Priced 8/2 Hunt CRE 2017-FL1 Hunt Mortgage Company

CRE Loan A 202.55 3.22 -/-/-/AAA/- 1ML 100 100 42

A-2 17.46 3.98 -/-/-/AAA/- 1ML 130 100 37

B 23.14 4.33 -/-/-/AA/- 1ML 165 100 30.38

C 22.26 4.57 -/-/-/A/- 1ML 240 100 24

D 25.32 4.91 -/-/-/BBB/- 330 100 16.75

E 30.56 -/-/-/BB/- 8

Preferred 27.94 -/-/-/NR/-

Priced 8/3 CGDBB 2017-BIOC Citigroup SASB A 415.47 -/-/AAA/-/- 1ML L+ 75a 79 45.4

B 97.76 -/-/AA-/-/- 56

C 73.32 -/-/A-/-/- 64

D 98.94 -/-/BBB-/-/- 1ML L+ 160a 160 73.9

E 107.27 -/-/BB-/-/- 85.6

VRR 41.25 -/-/NR/-/-

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 10

NEW ISSUES

Market status Bond name Issuer Asset type Class Size (USD m) WAL (yrs) Ratings

(S/F/K/D/MS) Bench Guidance Spread Price

Coupon

(%) CE (%)

Priced 8/9 GS 2017-STAY Gold Sachs SASB A 65.34 -/-/-/AAA/- 1ML 85 67.33

B 22.72 -/-/-/AAA/- 1ML 110 55.97

C 16.89 -/-/-/AA/- 1ML 135 47.52

D 22.32 -/-/-/A/- 36.37

E 37.03 -/-/-/BBB/- 17.85

F 25.40 -/-/-/BB/- 5.15

HRR 10.30 -/-/-/B/-

Priced 8/10 WFCM 2017-C39 Wells Fargo Bank Conduit A-1 27.82 2.9 -/AAA/AAA/-/- SWAPS 28 99.99 1.98 30

A-2 80.71 4.9 -/AAA/AAA/-/- SWAPS 48 102.99 2.99 30

A-3 4.39 6.9 -/AAA/AAA/-/- SWAPS 88 99.99 2.88 30

A-SB 44.79 7.18 -/AAA/AAA/-/- SWAPS 73 102.99 3.21 30

A-4 305 9.72 -/AAA/AAA/-/- SWAPS 88 100.99 3.16 30

A-5 330.28 9.84 -/AAA/AAA/-/- SWAPS 90 102.99 3.42 30

A-S 106.20 9.9 -/AAA/AAA/-/- SWAPS 118 102.99 3.35 20.63

B 50.98 9.93 -/AA-/AA/-/- SWAPS 150 102.99 4.03 16.13

C 46..73 9.98 -/A-/A/-/- SWAPS 202 99.49 4.12 12

D 19.03 9.98 -/BBB+/A-/-/- SWAPS 282 95.65 4.5 10.32

E-RR 37.61 -/NR/BBB-/-/- 7

F-RR 25.49 -/NR/BB-/-/- 4.75

G-RR 11.33 -/NR/B/-/- 3.75

HRR 42.48 -/NR/NR/-/-

Priced 8/10 JPMCC 2017-FL10 JP Morgan Chase Bank

SASB A 219.26 -/-/-/-/AAA 1ML 80 42.62

B 47.69 -/-/-/-/AA- 1ML 100 30.13

C 36.01 -/-/-/-/A- 1ML 125 20.71

D 38.86 -/-/-/-/BBB- 1ML 195 10.54

E 30.12 -/-/-/-/BB- 2.66

F 10.17 -/-/-/-/NR

VRR 20.11 -/-/-/-/NR

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 11

NEW ISSUES

Market status Bond name Issuer Asset type Class Size (USD m) WAL (yrs) Ratings

(S/F/K/D/MS) Bench Guidance Spread Price

Coupon

(%) CE (%)

Priced 8/11 A10 TAF 2017-1 A10 Capital, llc CRE Loan A-1FL 98.25 -/-/-/AAA/- 1ML 85 44.01

A-1-FX 98.25 -/-/-/AAA/- 1ML 80 44.01

A-2 43.9 -/-/-/AAA/- SWAPS 100 31.5

B 29.84 -/-/-/A/- SWAPS 235 23

C 11.41 -/-/-/BBB/- 19.75

D 8.34 -/-/-/BBB/- 17.38

E 11.41 -/-/-/BB/- 14.12

F 12.73 -/-/-/B/- 10.5

Priced 8/11 GSMS 2017-GS7 Goldman Sachs Conduit A-1 18.16 2.87 -/AAA/AAA/-/-

A-2 56.18 4.86 -/AAA/AAA/-/-

A-3 315 9.66 -/AAA/AAA/-/-

A-4 340.61 9.79 -/AAA/AAA/-/-

A-AB 27.21 7.30 -/AAA/AAA/-/-

A-S 74.36 9.88 -/AAA/AAA/-/-

B 47.32 9.88 -/AA-/AA/-/-

C 51.38 9.88 -/A-/A/-/-

D 20.28 -/BBB+/A-/-/-

E 16.85 -/BBB-/BBB+/-/-

F-RR 21.01 -/BBB-/BBB/-/-

G-RR 27.4 -/BB-/BB/-/-

H-RR 12.17 -/B-/B+/-/-

J-RR 54.08 -/NR/NR/-/-

Priced 8/11 MSSG 2017-237P Morgan Stanley SASB A 132.6 9.97 -/-/AAA/-/- SWAPS 91 102.99 3.06 44.8

B 82.2 9.97 -/-/AA-/-/- SWAPS 120 102.99 3.35 55.3

C 61.5 9.97 -/-/A-/-/- SWAPS 140 102.18 3.55 63.2

D 75.3 9.97 -/-/BBB-/-/- SWAPS 185 98.49 3.99 72.9

E 98.8 9.97 -/-/BB-/-/- 85.6

HRR 27.6 9.97 -/-/NR/-/- 89.2

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 12

NEW ISSUES

Market status Bond name Issuer Asset type Class Size (USD m) WAL (yrs) Ratings

(S/F/K/D/MS) Bench Guidance Spread Price

Coupon

(%) CE (%)

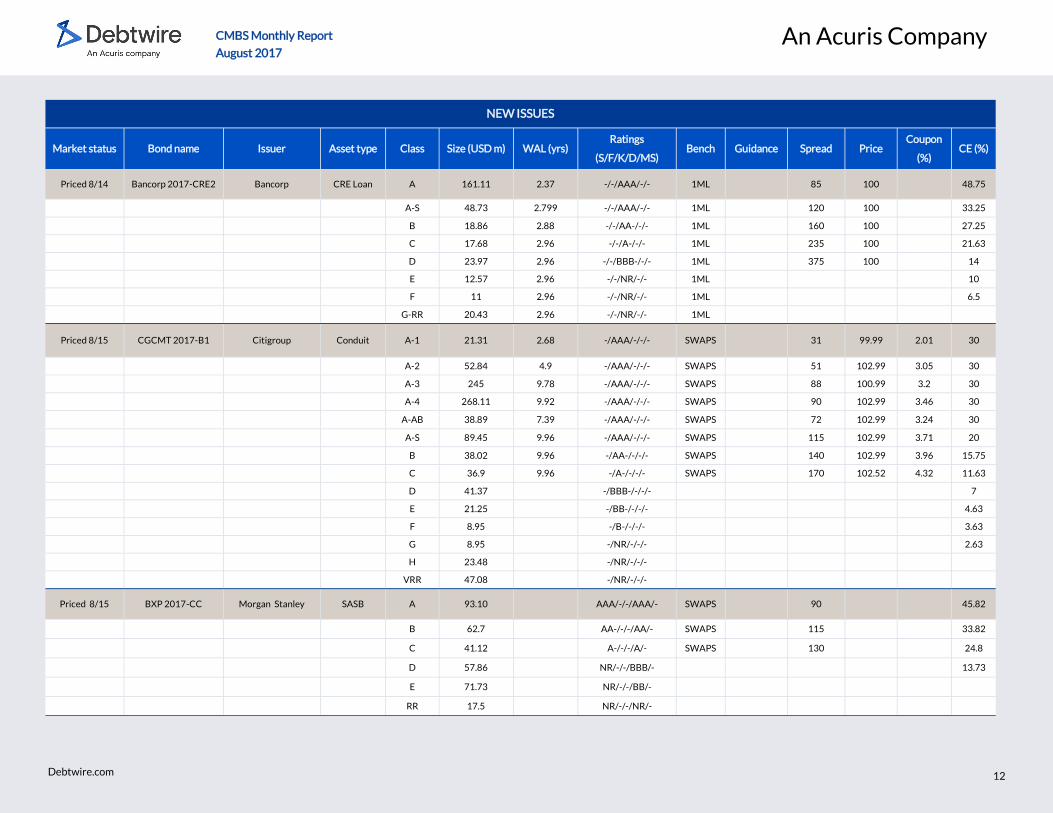

Priced 8/14 Bancorp 2017-CRE2 Bancorp CRE Loan A 161.11 2.37 -/-/AAA/-/- 1ML 85 100 48.75

A-S 48.73 2.799 -/-/AAA/-/- 1ML 120 100 33.25

B 18.86 2.88 -/-/AA-/-/- 1ML 160 100 27.25

C 17.68 2.96 -/-/A-/-/- 1ML 235 100 21.63

D 23.97 2.96 -/-/BBB-/-/- 1ML 375 100 14

E 12.57 2.96 -/-/NR/-/- 1ML 10

F 11 2.96 -/-/NR/-/- 1ML 6.5

G-RR 20.43 2.96 -/-/NR/-/- 1ML

Priced 8/15 CGCMT 2017-B1 Citigroup Conduit A-1 21.31 2.68 -/AAA/-/-/- SWAPS 31 99.99 2.01 30

A-2 52.84 4.9 -/AAA/-/-/- SWAPS 51 102.99 3.05 30

A-3 245 9.78 -/AAA/-/-/- SWAPS 88 100.99 3.2 30

A-4 268.11 9.92 -/AAA/-/-/- SWAPS 90 102.99 3.46 30

A-AB 38.89 7.39 -/AAA/-/-/- SWAPS 72 102.99 3.24 30

A-S 89.45 9.96 -/AAA/-/-/- SWAPS 115 102.99 3.71 20

B 38.02 9.96 -/AA-/-/-/- SWAPS 140 102.99 3.96 15.75

C 36.9 9.96 -/A-/-/-/- SWAPS 170 102.52 4.32 11.63

D 41.37 -/BBB-/-/-/- 7

E 21.25 -/BB-/-/-/- 4.63

F 8.95 -/B-/-/-/- 3.63

G 8.95 -/NR/-/-/- 2.63

H 23.48 -/NR/-/-/-

VRR 47.08 -/NR/-/-/-

Priced 8/15 BXP 2017-CC Morgan Stanley SASB A 93.10 AAA/-/-/AAA/- SWAPS 90 45.82

B 62.7 AA-/-/-/AA/- SWAPS 115 33.82

C 41.12 A-/-/-/A/- SWAPS 130 24.8

D 57.86 NR/-/-/BBB/- 13.73

E 71.73 NR/-/-/BB/-

RR 17.5 NR/-/-/NR/-

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 13

NEW ISSUES

Market status Bond name Issuer Asset type Class Size (USD m) WAL (yrs) Ratings

(S/F/K/D/MS) Bench Guidance Spread Price

Coupon

(%) CE (%)

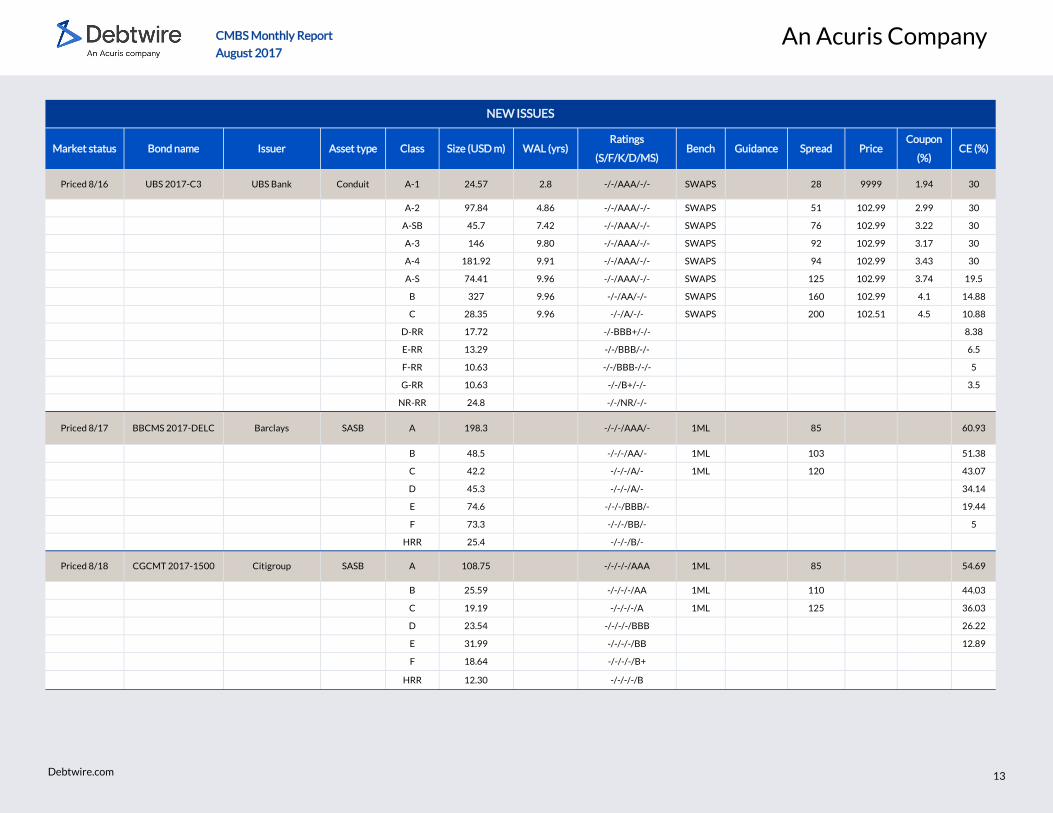

Priced 8/16 UBS 2017-C3 UBS Bank Conduit A-1 24.57 2.8 -/-/AAA/-/- SWAPS 28 9999 1.94 30

A-2 97.84 4.86 -/-/AAA/-/- SWAPS 51 102.99 2.99 30

A-SB 45.7 7.42 -/-/AAA/-/- SWAPS 76 102.99 3.22 30

A-3 146 9.80 -/-/AAA/-/- SWAPS 92 102.99 3.17 30

A-4 181.92 9.91 -/-/AAA/-/- SWAPS 94 102.99 3.43 30

A-S 74.41 9.96 -/-/AAA/-/- SWAPS 125 102.99 3.74 19.5

B 327 9.96 -/-/AA/-/- SWAPS 160 102.99 4.1 14.88

C 28.35 9.96 -/-/A/-/- SWAPS 200 102.51 4.5 10.88

D-RR 17.72 -/-BBB+/-/- 8.38

E-RR 13.29 -/-/BBB/-/- 6.5

F-RR 10.63 -/-/BBB-/-/- 5

G-RR 10.63 -/-/B+/-/- 3.5

NR-RR 24.8 -/-/NR/-/-

Priced 8/17 BBCMS 2017-DELC Barclays SASB A 198.3 -/-/-/AAA/- 1ML 85 60.93

B 48.5 -/-/-/AA/- 1ML 103 51.38

C 42.2 -/-/-/A/- 1ML 120 43.07

D 45.3 -/-/-/A/- 34.14

E 74.6 -/-/-/BBB/- 19.44

F 73.3 -/-/-/BB/- 5

HRR 25.4 -/-/-/B/-

Priced 8/18 CGCMT 2017-1500 Citigroup SASB A 108.75 -/-/-/-/AAA 1ML 85 54.69

B 25.59 -/-/-/-/AA 1ML 110 44.03

C 19.19 -/-/-/-/A 1ML 125 36.03

D 23.54 -/-/-/-/BBB 26.22

E 31.99 -/-/-/-/BB 12.89

F 18.64 -/-/-/-/B+

HRR 12.30 -/-/-/-/B

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 14

NEW ISSUES

Market status Bond name Issuer Asset type Class Size (USD m) WAL (yrs) Ratings

(S/F/K/D/MS) Bench Guidance Spread Price

Coupon

(%) CE (%)

Priced 8/31 Motel 6 2017-MTL6 JP Morgan Chase

Bank SASB A 641.82 -/-/AAA/-/- 1ML 92 32.4

B 226.67 -/-/AA-/-/- 1ML 119 43.8

C 167.2 -/-/A/-/- 1ML 140 52.3

D 220.97 -/-BBB-/-/- 1ML 215 63.4

E 348.46 -/-/BB-/-/- 1ML 325 81

F 316.45 -/-/B-/-/- 1ML 425 97

G 49.69 -/-/B-/-/- 1ML 575 99.5

RR 103.75 -/-/NR/-/-

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 15

RECENT DEBTWIRE COVERAGE

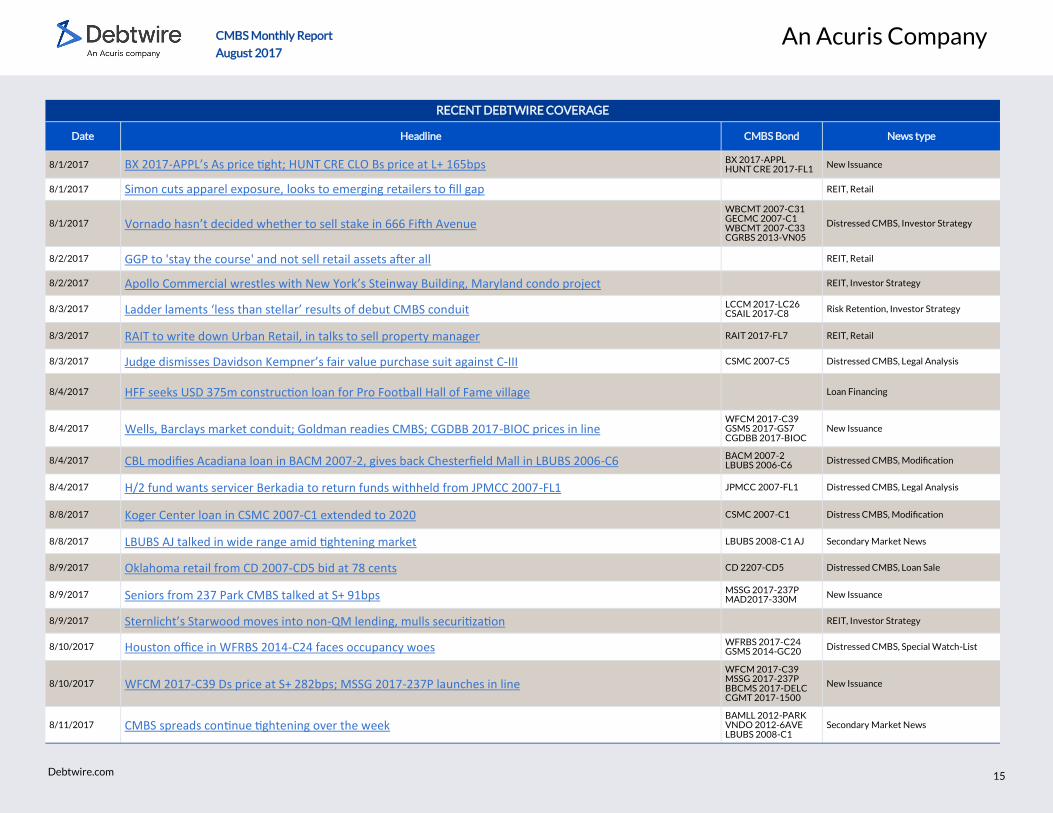

Date Headline CMBS Bond News type

8/1/2017 BX 2017-APPL’s As price tight; HUNT CRE CLO Bs price at L+ 165bps BX 2017-APPL HUNT CRE 2017-FL1

New Issuance

8/1/2017 Simon cuts apparel exposure, looks to emerging retailers to fill gap REIT, Retail

8/1/2017 Vornado hasn’t decided whether to sell stake in 666 Fifth Avenue

WBCMT 2007-C31 GECMC 2007-C1 WBCMT 2007-C33 CGRBS 2013-VN05

Distressed CMBS, Investor Strategy

8/2/2017 GGP to 'stay the course' and not sell retail assets after all REIT, Retail

8/2/2017 Apollo Commercial wrestles with New York’s Steinway Building, Maryland condo project REIT, Investor Strategy

8/3/2017 Ladder laments ‘less than stellar’ results of debut CMBS conduit LCCM 2017-LC26 CSAIL 2017-C8

Risk Retention, Investor Strategy

8/3/2017 RAIT to write down Urban Retail, in talks to sell property manager RAIT 2017-FL7 REIT, Retail

8/3/2017 Judge dismisses Davidson Kempner’s fair value purchase suit against C-III CSMC 2007-C5 Distressed CMBS, Legal Analysis

8/4/2017 HFF seeks USD 375m construction loan for Pro Football Hall of Fame village Loan Financing

8/4/2017 Wells, Barclays market conduit; Goldman readies CMBS; CGDBB 2017-BIOC prices in line WFCM 2017-C39 GSMS 2017-GS7 CGDBB 2017-BIOC

New Issuance

8/4/2017 CBL modifies Acadiana loan in BACM 2007-2, gives back Chesterfield Mall in LBUBS 2006-C6 BACM 2007-2 LBUBS 2006-C6

Distressed CMBS, Modification

8/4/2017 H/2 fund wants servicer Berkadia to return funds withheld from JPMCC 2007-FL1 JPMCC 2007-FL1 Distressed CMBS, Legal Analysis

8/8/2017 Koger Center loan in CSMC 2007-C1 extended to 2020 CSMC 2007-C1 Distress CMBS, Modification

8/8/2017 LBUBS AJ talked in wide range amid tightening market LBUBS 2008-C1 AJ Secondary Market News

8/9/2017 Oklahoma retail from CD 2007-CD5 bid at 78 cents CD 2207-CD5 Distressed CMBS, Loan Sale

8/9/2017 Seniors from 237 Park CMBS talked at S+ 91bps MSSG 2017-237P MAD2017-330M

New Issuance

8/9/2017 Sternlicht’s Starwood moves into non-QM lending, mulls securitization REIT, Investor Strategy

8/10/2017 Houston office in WFRBS 2014-C24 faces occupancy woes WFRBS 2017-C24 GSMS 2014-GC20

Distressed CMBS, Special Watch-List

8/10/2017 WFCM 2017-C39 Ds price at S+ 282bps; MSSG 2017-237P launches in line

WFCM 2017-C39 MSSG 2017-237P BBCMS 2017-DELC CGMT 2017-1500

New Issuance

8/11/2017 CMBS spreads continue tightening over the week BAMLL 2012-PARK VNDO 2012-6AVE LBUBS 2008-C1

Secondary Market News

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 16

RECENT DEBTWIRE COVERAGE

Date Headline CMBS Bond News type

8/14/2017 GSMS 2017-GS7, Bancorp CRE CLO price; BBCMS 2017-DELC hits market GSMS 2017-GS7 GCCFC 2007-GG9 Bancorp 2017-CRE2

New Issuance

8/14/2017 C-III gets DPO proposal on Rosemont retail loan in GSMS 2007-GG10 GSMS 2007-GG10 Distressed CMBS, Retail

8/14/2017 Stamford’s 400 Atlantic in GSMS 2007-GG10 headed for foreclosure GSMS 2007-GG10 Distressed CMBS, Foreclosure

8/15/2017 CMBS mezz with hotel exposure covers wide as market stabilizes WFCM 2015-C26 D WFRBS 2013-C1 D

Secondary Market News

8/15/2017 BXP C bonds price at S+ 130bps; CGCMT Cs price at S+ 170bps BXP 2017-CC CGCMT 2017-B1 CGCMT 2017-1500

New Issuance

8/16/2017 Foreclosure on One AT&T Center in BSCMS 2007-T26 set for next week BSCMS 2007-T2 Distressed CMBS, Foreclosure

8/16/2017 MSC 2006-HQ10 portfolio may lose another tenant, or it might sell that tenant some properties MSC 2006-HQ10 Distressed CMBS, Foreclosure

8/16/2017 Caesars opts for CMBS financing to fund bankruptcy exit Bankruptcy, New Issuance

8/17/2017 CWCapital markets USD 25.4m of loans from BACM deals BACM 2008-1 BACM 2006-6

Distressed CMBS, Loan Sale

8/18/2017 Koger Center loan mod details hit CSMC 2007-C1 CSMC 2007– C1 Distressed CMBS, Modification

8/18/2017 Secondary CMBS spreads hold steady amid politically charged week WFCM 2012-LC5 UBS 2017-C3 CGCMT 2017-B1

Secondary Market News

8/18/2017 Cherry Hill loan in WBCMT 2007-C31 liquidates with small loss WBCMT 2007-C31 Distressed CMBS, Liquidation

8/21/2017 Servicers marketing USD 122m in vintage CMBS loans LBUBS 2006-C4 LBUBS 2007-C1 BSCMS 2006-PW11

Distressed CMBS, Loan Sale

8/21/2017 UW-Oshkosh Foundation files for bankruptcy, cites CRE projects, litigation Bankruptcy, Legal Analysis

8/22/2017 Crossroads Marketplace in CGCMT 2007-C6 files for bankruptcy CGCMT 2007-C6 Distressed CMBS, Bankruptcy

8/23/2017 Sarasota Square in COMM 2013-CR9 may see maturity woes COMM 2013-CR9 Distressed CMBS

8/24/2017 JPMorgan preps Motel 6 CMBS deal Motel 6 2017-MTL6 New Issuance

8/25/2017 Tightening IOs help drive CMBS secondary volumes this week COMM 2017-CR19 COMM 2015-DC1 GSMS 2017-GC20

Secondary Market News

8/28/2017 SFIG files letter opposing Taberna CDO involuntary bankruptcy Taberna IV 2005-CDO Distresed CDO, Bankruptcy

8/29/2017 Simon’s Bangor Mall transfers to special servicing MSC 2007-1Q16 Distressed CMBS, Special Servicing

8/29/2017 CWCapital adds USD 57m in CMBS note offerings WBCMT 2007-C32 BACM 2006-6 LBUBS 2006-C4

Distressed CMBS, Loan Sale

An Acuris Company

Debtwire.com

CMBS Monthly Report

August 2017

Debtwire.com 17

RECENT DEBTWIRE COVERAGE

Date Headline CMBS Bond News type

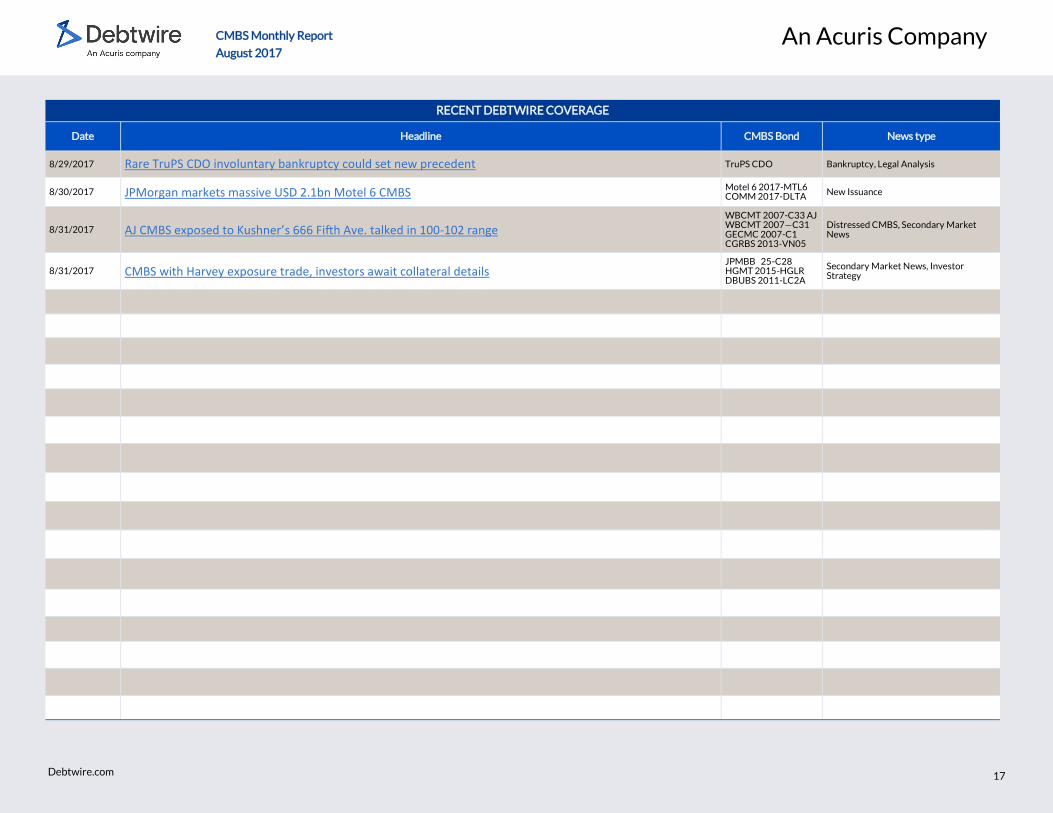

8/29/2017 Rare TruPS CDO involuntary bankruptcy could set new precedent TruPS CDO Bankruptcy, Legal Analysis

8/30/2017 JPMorgan markets massive USD 2.1bn Motel 6 CMBS Motel 6 2017-MTL6 COMM 2017-DLTA New Issuance

8/31/2017 AJ CMBS exposed to Kushner’s 666 Fifth Ave. talked in 100-102 range

WBCMT 2007-C33 AJ WBCMT 2007—C31 GECMC 2007-C1 CGRBS 2013-VN05

Distressed CMBS, Secondary Market News

8/31/2017 CMBS with Harvey exposure trade, investors await collateral details JPMBB 25-C28 HGMT 2015-HGLR DBUBS 2011-LC2A

Secondary Market News, Investor Strategy

CMBS Monthly Report

August 2017 An Acuris Company

Debtwire.com

Debtwire is an Acuris company

EMEA

10 Queen Street Place

London

EC4R 1BE

United Kingdom

+44 203 741 1000

Asia

Suite 1602-6

Grand Millennium Plaza

181 Queen’s Road, Central

Hong Kong

+ 612 9002 3131

Americas

330 Hudson St.

4th Floor

New York,

NY 10013 USA

+1 212 500 7537

Disclaimer

We have obtained the information provided in this report in good faith from sources that we consider to be reliable, but we do not independently verify the information. The information is not intended to provide tax, legal or investment advice. We shall not be liable for any mistakes, errors, inaccuracies or omissions in, or incompleteness of, any information contained in this report. All such liability is excluded to the fullest extent permitted by law. Data has been derived from company reports, press releases, presentations and Debtwire intelligence.

Debtwire reports on corporate debt situations before credit ratings are changed. Offering unique insights, credit analysis, debt data, and analytics for distressed debt and leveraged finance markets.

Subscribers choose Debtwire for speed and depth of coverage they can’t get anywhere else. Our reporters talk to an impressive range of contacts every day to bring you valuable early insight into fast evolving situations.

To complement your newsfeed, Debtwire’s credit analysis and research teams provide deep technical details and angles that help you understand situations more clearly.

Follow corporate debt situations as they

unfold

Find mandate opportunities in stressed/

distressed/restructuring situations, ahead of the market

Get real-time news on market-moving

events sent to your mobile or email

Get the full story on restructurings and

the players involved

Understand how regulatory

developments are affecting asset-backed securities

Capture early stage primary

opportunities and stay on top of the leveraged market

Debtwire.com

CMBS Monthly Report

August 2017 An Acuris Company

Debtwire.com

Debtwire is an Acuris company

EMEA

10 Queen Street Place

London

EC4R 1BE

United Kingdom

+44 203 741 1000

Asia

Suite 1602-6

Grand Millennium Plaza

181 Queen’s Road, Central

Hong Kong

Americas

330 Hudson St.

4th Floor

New York,

NY 10013 USA

Disclaimer

We have obtained the information provided in this report in good faith from sources that we consider to be reliable, but we do not independently verify the information. The information is not intended to provide tax, legal or investment advice. We shall not be liable for any mistakes, errors, inaccuracies or omissions in, or incompleteness of, any information contained in this report. All such liability is excluded to the fullest extent permitted by law. Data has been derived from company reports, press releases, presentations and Debtwire intelligence.

Debtwire ABS provides insight into opportunistic situations in the structured finance market. In addition to our unparalleled editorial coverage, subscribers have access to a bid list library alongside primary insurance and commercial real estate (CRE) databases.

With an ever-evolving market, Debtwire ABS tracks and reports on faulty legacy loans as well as emerging asset classes such as marketplace lending.

Subscribers choose Debtwire ABS for speed and depth of coverage they can’t get anywhere else. Our reporters talk to an impressive range of contacts every day to bring you valuable early insight into fast evolving situations.

Benefits and features:

Investigative coverage – Real-time news

and analysis of the securitization asset class, from origination to secondary

BWIC database – Extensive library of

bid lists that provides an instant historic backdrop alongside real-time updates

Primary Insurance database – Search for

new issues in the structured and securitized market from announcement and guidance to pricing

CRE and CMBS database – Easily filter

and search a growing list of specially serviced commercial real estate loans

Debtwire.com