amkor technology inc. - credit suisse

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

28 July 2015

Americas/United States

Equity Research

Semiconductor Equipment

Amkor Technology Inc.

(AMKR.OQ) DECREASE TARGET PRICE

Outlook consistent for another slow quarter

■ 2Q15 sales at the low end of guidance. Amkor's sales and profitability were below our lowered preview numbers of 15 July. Sales were US$737 mn, down 1% QoQ (vs -2% to +4% guidance) on Android weakness, excess fabless inventory, and lackluster PC/tablets. Lower sales impacted GM/OpM by -260 bp/-210 bp to 15.6%/5.2%, taking EPS to $0.04—below its $0.05-$0.15 guidance. Equipment capex was cut from US$450 mn to US$400 mn (-38%

YoY), plus US$150 mn was provided for K5, keeping FCF slightly negative.

■ Correction extends into 3Q15, but Apple boosts the 4Q outlook. 3Q15 sales were guided to be -5% to +2% QoQ, below our lowered +6% QoQ and the street's +11% QoQ estimates, keeping GMs at 13-16% vs our prior estimate of 19% and the street's 20%. Sales are falling the sharpest in mobile on Android weakness, although consumer (TV/STB) is lower and broad-based IDMs are staying more conservative. Off the lower base, we model 7% QoQ growth in 4Q15 due to double-digit exposure to Apple with

the AP, baseband, connectivity, sensors, and analog.

■ Targeting mild core growth in 2016 with a lift from J-Devices. We model +7% YoY Amkor base business plus US$1.02 bn consolidating J-Devices to drive 41% consolidated sales growth in 2016. Key targets will be WL CSP for mobile (15-20% of sales), China/Taiwan (5% of sales), automotive (>10% of sales), "SLIM and SWIFT" high-end packages, and continued growth from

memory (now 14% of sales). Inventory should also be more of a tailwind.

■ Reduce TP from US$7.40 to US$5.50—weakness getting priced in. On the softer outlook, we trim our 2015/16E EPS from US$0.62/0.70 to US$0.35/0.55. Our industry view remains muted due to higher fabless inventory, although a slowdown in consumer tech is increasingly getting priced in. We stay NEUTRAL with a lowered TP of US$5.50 (from US$7.40), based on 10x 2016E EPS and 1.0x forward P/B. Its valuation is at the low end of its trading

range—0.8x EV/sales (vs 0.5-1.2x) and 3.2x EV/EBITDA (vs 2.5-5.0x).

Share price performance

4

6

8

10

Jul-14 Oct-14 Jan-15 Apr-15

Daily Jul 28, 2014 - Jul 27, 2015, 7/28/14 = US$9.8

Price Indexed S&P 500 INDEX

On 07/27/15 the S&P 500 INDEX closed at 2067.64

Quarterly EPS 1Q 2Q 3Q 4Q 2013A 0.07 0.14 0.15 0.17 2014E 0.09 0.21 0.20 0.38 2015E 0.12 0.04 0.04 0.14

Financial and valuation metrics

Year 12/13A 12/14E 12/15E 12/16E EPS - (Excl. ESO) (US$) 0.53 0.87 0.35 0.55 EPS (CS adj.) (US$) 0.53 0.87 0.35 0.55 Prev. EPS (CS adj.) (US$) — — 0.62 0.70 P/E (CS adj., x) 9.3 5.6 14.0 8.9 P/E rel. (CS adj., %) 50.9 31.0 86.4 61.6 Revenue (US$ m) 2,956.4 3,129.4 2,981.7 4,202.7 EBITDA (US$ m) 652.5 761.2 687.8 886.9 Net debt (US$ m) 1,040 1,078 1,126 1,157 OCFPS (US$) 2.41 2.59 2.31 2.40 P/OCF (x) 2.5 1.9 2.1 2.1

Number of shares (m) 237.37 Price/sales(x) 0.37 BV/share (Next Qtr., US$) 4.5 P/BVPS (x) 0.98 Net debt (Next Qtr., US$ m) 1,021.3 Dividend (current, US$) 1.0 Dividend yield (%) 20.3

Source: Company data, Credit Suisse estimates

Rating NEUTRAL* Price (27 Jul 15, US$) 4.92 Target price (US$) (from 7.40) 5.50¹ 52-week price range 10.62 - 4.92 Market cap. (US$ mn) 1,167.88

*Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

[V] = Stock considered volatile (see Disclosure Appendix).

Research Analysts

Randy Abrams, CFA

886 2 2715 6366

Farhan Ahmad

415 249 7929

Nickie Yue

886 2 2715 6364

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 2

Focus tables and charts Exhibit 1: Amkor—June results and September guidance light; revising down 2015/16 estimates

AMKR

Actual CS Old Cons Guidance CS CS Old Cons Guidance CS CS Old Cons CS CS Old Cons

Total Revenue $736.7 $750.3 $750.0 $725 - 775mn $725.7 $796.8 $820.0 $700-750mn $2,981.7 $3,118.7 $4,042.0 $4,202.7 $4,439.4 $4,006.5

% Q/Q chng -0.8% 1.0% 1.0% -2% to +4% -1.5% 6.2% 11.3% -5% to +2%

% Y/Y chng -4.0% -2.2% -2.3% -10.7% -2.0% 0.9% -4.7% -0.3% 29.8% 40.9% 42.3% -0.9%

Total GM* 15.6% 18.2% 17.8% 16-19% 15.0% 19.4% 20.9% 13-16% 16.8% 19.0% 19.5% 16.7% 17.5% 21.3%

Operating Exp.* $76.5 $81.4 $78.5 $82.2 $315.2 $327.9 $413.5 $431.8

Operating Mgin* 5.2% 7.3% 7.0% 4.1% 9.0% 10.6% 6.3% 8.5% 8.8% 6.8% 7.8% 10.2%

Net Income* $9.6 $27.0 $23.7 $12-$35mn $10.7 $41.1 $50.2 $7mn-$14mn $83.2 $147.0 $189.0 $131.5 $167.0 $225.3

Net Margin* 0.0% 0.0% 3.2% 1.5% 5.2% 6.1% 2.8% 4.7% 4.7% 3.1% 3.8% 5.6%

EPS* $0.04 $0.11 $0.11 $0.05-$0.15 $0.04 $0.17 $0.17 -0.03-$0.06 $0.35 $0.62 $0.74 $0.55 $0.70 $0.98

Fully diluted shares 237.3 237.4 237.3 237.4 237.4 237.4 237.3 237.4

F2016ESep-15Jun-15 F2015E

Source: Company data, Credit Suisse estimates, Bloomberg consensus

Exhibit 2: Industry equipment orders declining in 2H15 Exhibit 3: GMs lower in 2Q/3Q on the weaker outlook

0

75

150

225

300

375

450

0

5

10

15

20

25

30

Jan

-01

Au

g-0

1

Ma

r-0

2

Oct-

02

Ma

y-0

3

De

c-0

3

Jul-

04

Fe

b-0

5

Se

p-0

5

Ap

r-06

No

v-0

6

Jun

-07

Jan

-08

Au

g-0

8

Ma

r-0

9

Oct-

09

Ma

y-1

0

De

c-1

0

Jul-

11

Fe

b-1

2

Se

p-1

2

Ap

r-13

No

v-1

3

Jun

-14

Jan

-15

Au

g-1

5

Equipment Bookings (US$ mn)

Stock Price

BE Bookings AMKR Stock

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

-$150,000

$0

$150,000

$300,000

$450,000

$600,000

$750,000

$900,000

Ma

r-09

Jun

-09

Se

p-0

9

Dec-0

9

Ma

r-10

Jun

-10

Se

p-1

0

Dec-1

0

Ma

r-11

Jun

-11

Se

p-1

1

Dec-1

1

Ma

r-12

Jun

-12

Se

p-1

2

Dec-1

2

Ma

r-13

Jun

-13

Se

p-1

3

Dec-1

3

Ma

r-14

Jun

-14

Se

p-1

4

Dec-1

4

Mar-

15

Jun

-15

Se

p-1

5

Dec-1

5

Revenue GM% OpM%

US$K GM (%)

Source: Company data, Credit Suisse estimates, SEMI Source: Company data, Credit Suisse estimates

Exhibit 4: FCF slightly negative due to K5's construction Exhibit 5: AMKR EV/EBITDA now at lower levels

-300

-200

-100

-

100

200

300

400

-$600

-$400

-$200

$0

$200

$400

$600

$800

F1

99

8

F1

99

9

F2

00

0

F2

00

1

F2

00

2

F2

00

3

F2

00

4

F2

005

F2

006

F2

007

F2

008

F2

00

9

F2

01

0

F2

01

1

F2

01

2

F2

01

3

F2

01

4

F2

01

5E

F2

01

6E

FCF (US$mn)Capex (US$ mn)

Operating CF Capex FCF

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

Sep

-05

Feb

-06

Ju

l-0

6

De

c-0

6

Ma

y-0

7

Oct-

07

Ma

r-08

Au

g-0

8

Ja

n-0

9

Ju

n-0

9

No

v-0

9

Ap

r-1

0

Sep

-10

Feb

-11

Ju

l-1

1

De

c-1

1

Ma

y-1

2

Oct-

12

Ma

r-13

Au

g-1

3

Ja

n-1

4

Ju

n-1

4

No

v-1

4

Ap

r-1

5

Sep

-15

EV/EBITDA

EV/EBITDA

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Exhibit 6: Amkor at a valuation discount but also has a lower ROE now Price Mkt Cap EV/Sales (x) EV/EBITDA (x) P/E Multiple (x) P/B Multiple (x) ROE Trough/Peak (EV/Sales)

Company Ticker 7/28/2015 (US$mn) 2014 2015 2016 2014 2015 2016 2014 2015 2016 2014 2015 2016 2014 2015 2016

Select backend peers

Amkor AMKR $4.25 $1,168 0.7 0.8 0.6 3.0 3.3 2.6 4.9 12.1 7.7 0.9 0.8 0.7 18.6 6.9 9.8

ASE 2311.TW $35.75 $8,857 1.2 1.1 1.0 5.6 5.4 5.1 12.1 12.9 11.3 1.9 1.9 1.8 15.7 14.5 15.6

SPIL 2325.TW $37.25 $3,676 1.4 1.4 1.2 4.4 4.0 3.7 10.0 9.5 8.6 1.6 1.5 1.5 16.3 16.1 17.2

Chipbond 6147.TWO $42.20 $867 1.8 1.8 1.5 5.4 5.5 4.5 10.7 11.8 8.0 1.2 1.2 1.1 11.0 9.8 13.4

ChipMOS 8150.TW $32.20 $934 1.0 1.1 0.9 3.5 3.3 2.9 8.3 10.2 8.9 1.5 1.5 1.4 18.2 14.4 15.4

Powertech 6239.TW $52.90 $1,280 1.0 0.9 0.8 3.1 2.8 2.6 12.5 10.6 9.8 1.3 1.2 1.1 10.3 11.3 11.6

Median 1.1 1.1 0.9 3.9 3.7 3.3 10.3 11.2 8.7 1.4 1.3 1.3 16.0 12.8 14.4

Mean 1.2 1.2 1.0 4.1 4.1 3.6 9.7 11.2 9.0 1.4 1.3 1.3 15.0 12.2 13.8 Source: Company data, Credit Suisse estimates

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 3

Outlook consistent for another slow quarter ahead of the Apple builds Amkor remains a technology leader in back-end packaging and test, with more

concentration on flip chip and wafer-level packaging (50% of revenue from advanced

packaging, versus 30% for ASE and SPIL), and most of its smartphones positioning is at

the higher end of the mobile market. In the near term, that high-end exposure is triggering

weakness as Samsung has shifted business from Amkor's top customer Qualcomm (17%

of sales in 2014) to its own internal silicon that is packaged mostly in-house in its back-end

facilities, and the other Android brands are seeing compression as mobile growth slows,

tablets decline and Apple takes more value share.

Beyond Android smartphones, Amkor is facing a more muted outlook from its broader

customer base, which we note (quarter-to-date) across fabless and IDMs' reporting—their

managements have guided 2Q15 sales on average to be down 2% QoQ, vs the normal 3-

5% QoQ growth, and inventory to be up a day to 94 days, up 16 days from last year, which

was more than the normal level. Amkor trimmed its 3Q15 revenue outlook to -5% to +2%

QoQ for 3Q15 vs the normal high-single-digit seasonality due to pullbacks from mobile and

consumer, and a bit of softness in the broad-based business, taking GMs down to 13-16%

and EPS to -US$0.03 to -US$0.06. The company should post mild growth in 4Q15 as it

ramps up Apple component orders for iPhone 6S. Equipment capex was also cut from

US$450 mn to US$400 mn, plus $150 mn was provided for facility investment in K5 in Korea.

The company should have relatively stable equipment investment next year but will still need

to spend US$200 mn to complete the construction of K5, pushing out positive FCF to 2017.

For 2016, we model a better year, with a +7% YoY Amkor base business plus a US$1.02

bn consolidating J-Devices driving 41% consolidated sales growth in 2016. Key targets will

be WL CSP for mobile (15-20% of sales), China/Taiwan (5% of sales), automotive (>10%

of sales), "SLIM and SWIFT" high-end packages, and continued growth from memory

(now 14% of sales). Inventory should also move from a headwind to a tailwind.

On the softer outlook, we trim our 2015/16E EPS from $0.62/0.70 to $0.35/0.55. Our

industry view remains muted due to higher fabless inventory and a slowdown in consumer

tech, although these are increasingly getting priced in. We maintain our NEUTRAL rating

with a lower TP of US$5.50 (from US$7.40), based on 10x 2016E EPS and 1.0x forward

P/B. The valuation is at the low end of its trading range—0.8x EV/sales (vs 0.5-1.2x) and

3.2x EV/EBITDA (vs 2.5-5.0x). This, in our view, is reasonable, although with growth

staying muted due to the mixed tech outlook the stock may remain range-bound, with a

possible trade into the iPhone ramp-up in 4Q15 and 1Q16 restocking as Amkor is

maintaining a pretty good share of the Apple processor business and peripheral

component orders.

Exhibit 7: Industry equipment orders declining in 2H15 Exhibit 8: FCF slightly negative due K5's construction

0

75

150

225

300

375

450

0

5

10

15

20

25

30

Jan

-01

Au

g-0

1

Ma

r-0

2

Oct-

02

Ma

y-0

3

De

c-0

3

Jul-

04

Fe

b-0

5

Se

p-0

5

Ap

r-06

No

v-0

6

Jun

-07

Jan

-08

Au

g-0

8

Ma

r-0

9

Oct-

09

Ma

y-1

0

De

c-1

0

Jul-

11

Fe

b-1

2

Se

p-1

2

Ap

r-13

No

v-1

3

Jun

-14

Jan

-15

Au

g-1

5

Equipment Bookings (US$ mn)

Stock Price

BE Bookings AMKR Stock

-300

-200

-100

-

100

200

300

400

-$600

-$400

-$200

$0

$200

$400

$600

$800

F1

99

8

F1

99

9

F2

00

0

F2

00

1

F2

00

2

F2

00

3

F2

00

4

F2

005

F2

006

F2

007

F2

008

F2

00

9

F2

01

0

F2

01

1

F2

01

2

F2

01

3

F2

01

4

F2

01

5E

F2

01

6E

FCF (US$mn)Capex (US$ mn)

Operating CF Capex FCF

Source: Company data, Credit Suisse estimates, SEMI Source: Company data, Credit Suisse estimates

Amkor has the leading

technology but is being

impacted by slowing mobile

and excess inventory

Amkor should return to mild

growth in 2016 and have

incremental earnings from

the consolidation of J-

Devices

Reducing estimates on the

lower sales outlook

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 4

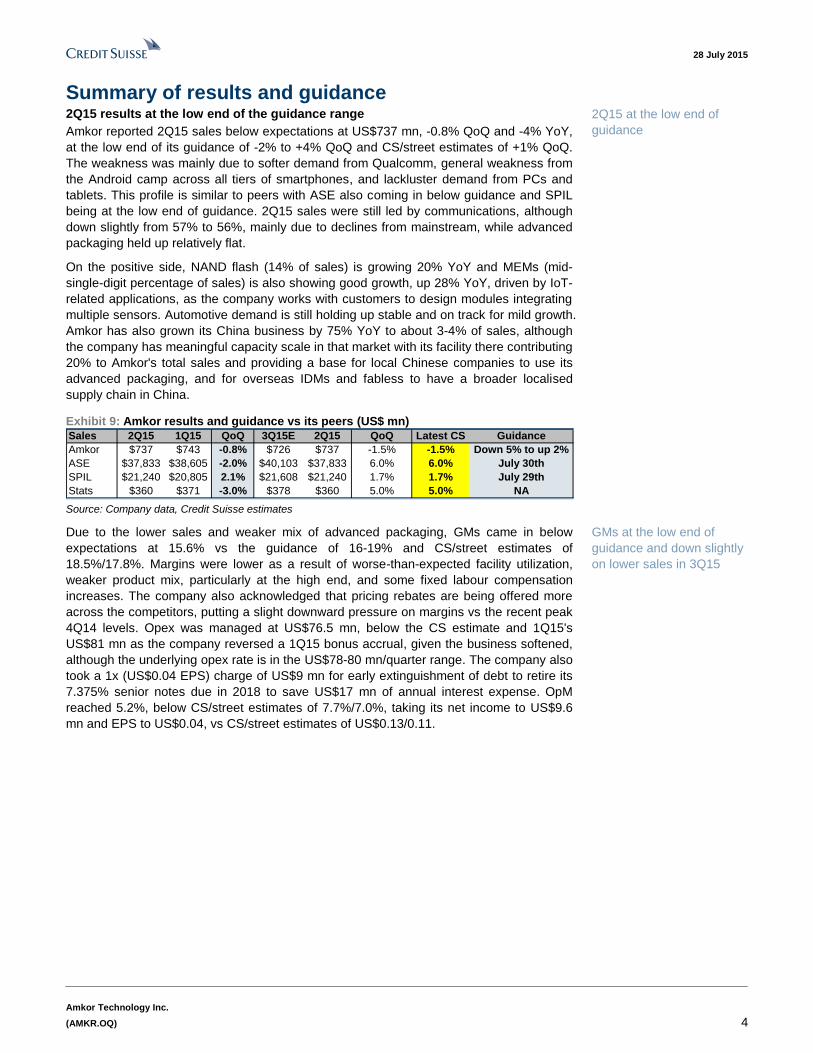

Summary of results and guidance 2Q15 results at the low end of the guidance range

Amkor reported 2Q15 sales below expectations at US$737 mn, -0.8% QoQ and -4% YoY,

at the low end of its guidance of -2% to +4% QoQ and CS/street estimates of +1% QoQ.

The weakness was mainly due to softer demand from Qualcomm, general weakness from

the Android camp across all tiers of smartphones, and lackluster demand from PCs and

tablets. This profile is similar to peers with ASE also coming in below guidance and SPIL

being at the low end of guidance. 2Q15 sales were still led by communications, although

down slightly from 57% to 56%, mainly due to declines from mainstream, while advanced

packaging held up relatively flat.

On the positive side, NAND flash (14% of sales) is growing 20% YoY and MEMs (mid-

single-digit percentage of sales) is also showing good growth, up 28% YoY, driven by IoT-

related applications, as the company works with customers to design modules integrating

multiple sensors. Automotive demand is still holding up stable and on track for mild growth.

Amkor has also grown its China business by 75% YoY to about 3-4% of sales, although

the company has meaningful capacity scale in that market with its facility there contributing

20% to Amkor's total sales and providing a base for local Chinese companies to use its

advanced packaging, and for overseas IDMs and fabless to have a broader localised

supply chain in China.

Exhibit 9: Amkor results and guidance vs its peers (US$ mn)

Sales 2Q15 1Q15 QoQ 3Q15E 2Q15 QoQ Latest CS Guidance

Amkor $737 $743 -0.8% $726 $737 -1.5% -1.5% Down 5% to up 2%

ASE $37,833 $38,605 -2.0% $40,103 $37,833 6.0% 6.0% July 30th

SPIL $21,240 $20,805 2.1% $21,608 $21,240 1.7% 1.7% July 29th

Stats $360 $371 -3.0% $378 $360 5.0% 5.0% NA Source: Company data, Credit Suisse estimates

Due to the lower sales and weaker mix of advanced packaging, GMs came in below

expectations at 15.6% vs the guidance of 16-19% and CS/street estimates of

18.5%/17.8%. Margins were lower as a result of worse-than-expected facility utilization,

weaker product mix, particularly at the high end, and some fixed labour compensation

increases. The company also acknowledged that pricing rebates are being offered more

across the competitors, putting a slight downward pressure on margins vs the recent peak

4Q14 levels. Opex was managed at US$76.5 mn, below the CS estimate and 1Q15's

US$81 mn as the company reversed a 1Q15 bonus accrual, given the business softened,

although the underlying opex rate is in the US$78-80 mn/quarter range. The company also

took a 1x (US$0.04 EPS) charge of US$9 mn for early extinguishment of debt to retire its

7.375% senior notes due in 2018 to save US$17 mn of annual interest expense. OpM

reached 5.2%, below CS/street estimates of 7.7%/7.0%, taking its net income to US$9.6

mn and EPS to US$0.04, vs CS/street estimates of US$0.13/0.11.

2Q15 at the low end of

guidance

GMs at the low end of

guidance and down slightly

on lower sales in 3Q15

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 5

Exhibit 10: June results at the low end, September guidance also light (US$ mn)

AMKR

Actual CS Old Cons Guidance CS CS Old Cons Guidance CS CS Old Cons

Total Revenue $736.7 $750.3 $750.0 $725 - 775mn $725.7 $796.8 $820.0 $700-750mn $776.5 $828.7 $831.0

% Q/Q chng -0.8% 1.0% 1.0% down 2% to up 4% -1.5% 6.2% 11.3% Down 5% to up 2% 7.0% 4.0% 1.3%

% Y/Y chng -4.0% -2.2% -2.3% -10.7% -2.0% 0.9% -9.0% -2.9% -2.6%

Total GM* 15.6% 18.2% 17.8% 16-19% 15.0% 19.4% 20.9% 13-16% 18.4% 20.3% 21.3%

R&D Expense* $20.0 $18.1 $20.6 $18.3 $20.8 $18.6

SG&A Expense* $56.4 $63.3 $58.0 $63.9 $58.5 $64.8

Operating Exp.* $76.5 $81.4 $78.5 $82.2 $79.3 $83.4

Operating Mgin* 5.2% 7.3% 7.0% 4.1% 9.0% 10.6% 8.2% 10.2% 11.0%

Net Income* $9.6 $27.0 $23.7 $12-$35mn $10.7 $41.1 $50.2 $7mn-$14mn $34.2 $50.3 $53.8

Net Margin* 0.0% 0.0% 3.2% 1.5% 5.2% 6.1% 4.4% 6.1% 6.5%

EPS* $0.04 $0.11 $0.11 $0.05-$0.15 $0.04 $0.17 $0.17 -0.03-$0.06 $0.14 $0.21 $0.19

Fully diluted shares 237.3 237.4 237.3 237.4 237.3 237.4

Sep-15Jun-15 Dec-15

Source: Company data, Credit Suisse estimates

3Q15 is guided to be weaker-than-expected due to mobile and consumer weakness

and sluggish order activity at the broad-based customers

Amkor guided 3Q15 sales of -5% to +2% QoQ to US$700-750 mn, below CS/street

estimates for +6%/+11% QoQ, mainly due to pullbacks from mobile and consumer, and a

bit of softness in the broad-based business. The company sees customers continuing to

deplete inventory and staying cautious to replenish orders with supply chain capacity not

as tight. While communications and consumer are expected to be sequentially down,

automotive, networking and computing should see small growth. We now estimate 3Q15

sales will be down 1.5% QoQ. On lower sales, weaker mix and weaker pricing

environment, margins were also guided lower to 13-16%, below CS/street estimates of

21%, taking the net income range to -US$7 mn to +US$14 mn in the quarter.

Exhibit 11: GMs lower in 2Q15/3Q15 on the weaker outlook

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

-$150,000

$0

$150,000

$300,000

$450,000

$600,000

$750,000

$900,000

Ma

r-09

Jun

-09

Se

p-0

9

Dec-0

9

Ma

r-10

Jun

-10

Se

p-1

0

Dec-1

0

Ma

r-11

Jun

-11

Se

p-1

1

Dec-1

1

Ma

r-12

Jun

-12

Se

p-1

2

Dec-1

2

Ma

r-13

Jun

-13

Se

p-1

3

Dec-1

3

Ma

r-14

Jun

-14

Se

p-1

4

Dec-1

4

Mar-

15

Jun

-15

Se

p-1

5

Dec-1

5

Revenue GM% OpM%

US$K GM (%)

Source: Company data, Credit Suisse research

4Q15 may see moderate growth on Apple's ramp-up

While 3Q15 is set for a pullback on weaker communications demand, the company still

expects a moderate rebound in 4Q15 on the back of Apple's refresh—we expect mid- to

high-single-digit QoQ growth for a peak quarter in 2015. Amkor expects 4Q15 recovery

from Apple's new platforms on 16/14nm along with good content packaging other chips

into that device (RF, sensors, connectivity, baseband) and also seasonally higher sales

from broader mainstream products. We trim our full-year sales growth estimate from flat to

down 4% YoY. Following lower sales growth and profitability, the company targets to

reduce opex by 5% YoY in 2015 to keep the cost structure in line with the lower sales.

3Q15 sales guidance: -5%

to +2% QoQ

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 6

Exhibit 12: Industry revenues falling off in 2015 Exhibit 13: Amkor market share still down slightly

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

YoY GrowthUS$ mn

SiP SPIL Amkor Stats YoY Growth

10%

15%

20%

25%

30%

35%

40%

45%

50%

$0$400$800

$1,200$1,600$2,000$2,400$2,800$3,200$3,600$4,000

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15E

ASE % of industryUS$ mn Sales

SiP SPIL Amkor Stats AMKR % of industry

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Amkor marketing technology capabilities to gain

share as customers migrate to advanced packages

As a strategy to differentiate its technology offerings, Amkor is now introducing a roadmap

of advanced packaging that combines more advanced substrate variations of its substrate

products (flip chip CSP and flip chip BGA), fan-out packaging and advanced wafer-level

packaging. At the advanced wafer-level packaging, the company has introduced a silicon

interposer solution (SLIM) that can work around using complicated through silicon vias and

an improved fan-out packaging architecture (SWIFT).

Exhibit 14: Amkor developing advanced packaging spanning fan-out, wafer-level and

advanced substrate packages

Source: Amkor

Amkor is now marketing its newly developed SWIFT (Silicon Wafer Integrated Fan Out

Tech) and SLIM (Silicon less integrated module) technologies. The company's fan-out and

2.5D solutions can combine multiple chips including processor, memory, base band and

other ICs, enabling customers to build very thin and very small products:

■ SLIM: Silicon interposer package. SLIM is a lower-cost solution that simplifies the

process and allows for supply-chain flexibility. The output will also deliver a reduction

in package thickness. It leverages Amkor's 2.5D wafer processing and assembly

equipment and expertise.

■ SWIFT: Advanced fan-out package. SWIFT is Amkor's advanced fan-out package

that targets mobile and networking applications. SWIFT combines baseband,

application processor, logic and memory to drive advanced die integration.

Amkor launching new fan-

out and wafer-level

packaging solutions for

2017 volumes

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 7

Exhibit 15: Amkor's advanced WLP positioning Exhibit 16: SLIM and SWIFT package definition

Source: Company data Source: Company data

Mobile under some pressure but diversifying into

new applications

To counteract the slowing smartphone and tablet growth rates, Amkor targets to keep its

high share at the flagship models while diversifying into new growth drivers, including (1)

expanding WL CSP in mobile (18% of sales), (2) growing China/Taiwan to 4-5% of sales,

(3) expanding automotive (>10% of sales), and (5) growing its MEMs/sensor business

(mid-single-digit contribution.

1. Another volume ramp-up for Apple, although some risk with TSMC InFO in

2016. We expect Amkor to maintain a good market share of the Apple processor

business out of TSMC this year, a project that should still reach 3-5% of 2H15

sales. In 2016, however, we believe TSMC will vertically integrate the business

using its internal InFO process as it is procuring equipment and has a large team

working with this customer on this strategic project. In the long term, Amkor has

presented a roadmap with SWIFT and SLIM to capture fan-out and 2.5D

businesses, but most of these volumes it notes would start from 2017.

2. US baseband high-end orders impacted by GS6; may recover when

Snapdragon 820 ramps up on Samsung 14nm. We believe Amkor was the

most exposed back-end supplier to Qualcomm's Snapdragon 810 licensing

technology supplied by Shinko, and consequently faces more impact in 2Q15

from that shift to Samsung. We see potential for some rebound in 2016 as

Qualcomm may recover some share into future high-end Samsung products with

the Snapdragon 820 moving back to Samsung on 14nm in late 2015. Qualcomm

still uses the external back-end suppliers, giving opportunity for Amkor to recover

share later in the year.

3. Low-cost Asian smartphone customer expansion. Amkor grew greater China

sales by about 75% in 1H15 to 3-4% of sales and targets to get to 4-5% of sales

exiting 2015. We believe Amkor has penetrated into a notable AP/baseband

smartphone IC supplier and in the longer term targets the largest China and

Taiwan IC design house.

Amkor's Apple business

ramping up again in 2015

but may be lost to TSMC

InFO in 2016

Qualcomm orders would

rebound if Snapdragon 820

is designed back into high-

end Samsung phones

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 8

Exhibit 17: End-market sales (US$ mn)—communications

the largest

Exhibit 18: Revenue % by end-market—communications

> 50%

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

De

c-1

2

Ma

r-1

3

Jun

-13

Se

p-1

3

De

c-1

3

Ma

r-1

4

Jun

-14

Se

p-1

4

De

c-1

4

Ma

r-1

5

Jun

-15

End Market Segments

Communications Computing Consumer Networking Industrial/Auto

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

De

c-1

2

Ma

r-1

3

Jun

-13

Sep-1

3

De

c-1

3

Ma

r-1

4

Jun-1

4

Se

p-1

4

De

c-1

4

Ma

r-1

5

Jun

-15

End Market Segments Mix

Communications Computing Consumer Networking Industrial/Auto

Source: Company data, Credit Suisse research Source: Company data, Credit Suisse research

4. Memory growth from Toshiba NAND and some Mobile DRAM. Memory is now

14% of sales and still growing at 20% YoY. The company targets to continue

outgrowing the NAND market and also continuing to supply mobile DRAM

packaging and test to a US customer.

5. Growth from automotive. Amkor's automotive business grew 25% YoY in 2014

to US$760 mn (US$410 mn J-Devices + US$350 mn Amkor), and the company

targets growing that to US$1 bn in the next few years (about 20% of expected

sales by 2017).

6. Fan-in WLP strength. Amkor has almost 100 customers using the fan-in wafer-

level packaging, a growing area now at 25-30% of advanced packaging sales (10-

15% of total), and providing a lift due to good returns as the business has low

material content and high level of service requirement for the turn-key assembly,

probe, and bumping businesses. Fan-in packaging is seeing growth from lower

pin count small form-factor mobile devices, including RF, connectivity and power

management.

7. Sensor and RF growing through SiP packaging. Amkor has also ramped up its

fingerprint IC packaging and MEMs sensors for automotive and IoT, with sensors

now about mid-single-digits contribution and is also now creating RF front-end

modules for mobile products. The company highlighted this as a growth area, and

we believe it presents an opportunity for the company to do more SiP advanced

packaging with good margins. Amkor's SiP combines one or more ICs of different

functionalities, which may include passive components and/or MEMS assembled

into a single package. SiP may contain one or more IC chips, either wirebonded,

flip chip, or both, plus other components that are traditionally found on the system

motherboard. Amkor's business model for SiP is a contrast to ASE, which is also

trying to do board-level SiP modules using its USI Shanghai contract

manufacturing footprint that is additive to the top line with high materials content

but at lower margins due to its high pass-through content.

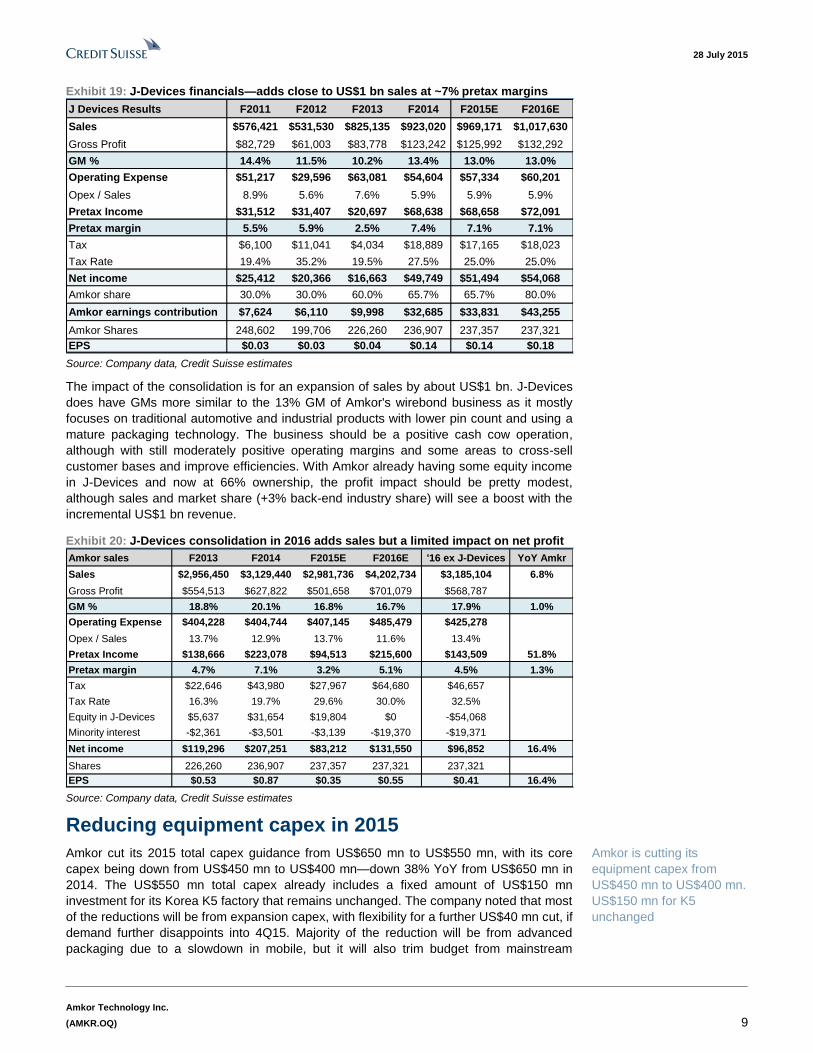

J-Devices acquisition provides incremental sales

once consolidated in 2016

Amkor currently owns 66% of J-Devices, a Japanese back-end supplier that has

consolidated several of the local back-end operations. Amkor disclosed in 2014 that J-

Devices had reached US$923 mn sales, US$123 mn gross profit and US$50 mn net

income. We believe that venture is now approaching US$1 bn run-rate for the fiscal year

ending March 2015. Amkor plans to raise its stake to 80% and consolidate operations in

2016, with a small minority interest deduction. We estimate by 2016 J-Devices could

contribute US$1 bn sales, 13% GMs, and 6% pretax margin and US$0.18 EPS.

Fan-in and sensor

packaging is growing

J-Devices consolidation

adds US$1 bn sales in 2016

once ownership reaches

80%

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 9

Exhibit 19: J-Devices financials—adds close to US$1 bn sales at ~7% pretax margins

J Devices Results F2011 F2012 F2013 F2014 F2015E F2016E

Sales $576,421 $531,530 $825,135 $923,020 $969,171 $1,017,630

Gross Profit $82,729 $61,003 $83,778 $123,242 $125,992 $132,292

GM % 14.4% 11.5% 10.2% 13.4% 13.0% 13.0%

Operating Expense $51,217 $29,596 $63,081 $54,604 $57,334 $60,201

Opex / Sales 8.9% 5.6% 7.6% 5.9% 5.9% 5.9%

Pretax Income $31,512 $31,407 $20,697 $68,638 $68,658 $72,091

Pretax margin 5.5% 5.9% 2.5% 7.4% 7.1% 7.1%

Tax $6,100 $11,041 $4,034 $18,889 $17,165 $18,023

Tax Rate 19.4% 35.2% 19.5% 27.5% 25.0% 25.0%

Net income $25,412 $20,366 $16,663 $49,749 $51,494 $54,068

Amkor share 30.0% 30.0% 60.0% 65.7% 65.7% 80.0%

Amkor earnings contribution $7,624 $6,110 $9,998 $32,685 $33,831 $43,255

Amkor Shares 248,602 199,706 226,260 236,907 237,357 237,321

EPS $0.03 $0.03 $0.04 $0.14 $0.14 $0.18 Source: Company data, Credit Suisse estimates

The impact of the consolidation is for an expansion of sales by about US$1 bn. J-Devices

does have GMs more similar to the 13% GM of Amkor's wirebond business as it mostly

focuses on traditional automotive and industrial products with lower pin count and using a

mature packaging technology. The business should be a positive cash cow operation,

although with still moderately positive operating margins and some areas to cross-sell

customer bases and improve efficiencies. With Amkor already having some equity income

in J-Devices and now at 66% ownership, the profit impact should be pretty modest,

although sales and market share (+3% back-end industry share) will see a boost with the

incremental US$1 bn revenue.

Exhibit 20: J-Devices consolidation in 2016 adds sales but a limited impact on net profit

Amkor sales F2013 F2014 F2015E F2016E '16 ex J-Devices YoY Amkr

Sales $2,956,450 $3,129,440 $2,981,736 $4,202,734 $3,185,104 6.8%

Gross Profit $554,513 $627,822 $501,658 $701,079 $568,787

GM % 18.8% 20.1% 16.8% 16.7% 17.9% 1.0%

Operating Expense $404,228 $404,744 $407,145 $485,479 $425,278

Opex / Sales 13.7% 12.9% 13.7% 11.6% 13.4%

Pretax Income $138,666 $223,078 $94,513 $215,600 $143,509 51.8%

Pretax margin 4.7% 7.1% 3.2% 5.1% 4.5% 1.3%

Tax $22,646 $43,980 $27,967 $64,680 $46,657

Tax Rate 16.3% 19.7% 29.6% 30.0% 32.5%

Equity in J-Devices $5,637 $31,654 $19,804 $0 -$54,068

Minority interest -$2,361 -$3,501 -$3,139 -$19,370 -$19,371

Net income $119,296 $207,251 $83,212 $131,550 $96,852 16.4%

Shares 226,260 236,907 237,357 237,321 237,321

EPS $0.53 $0.87 $0.35 $0.55 $0.41 16.4% Source: Company data, Credit Suisse estimates

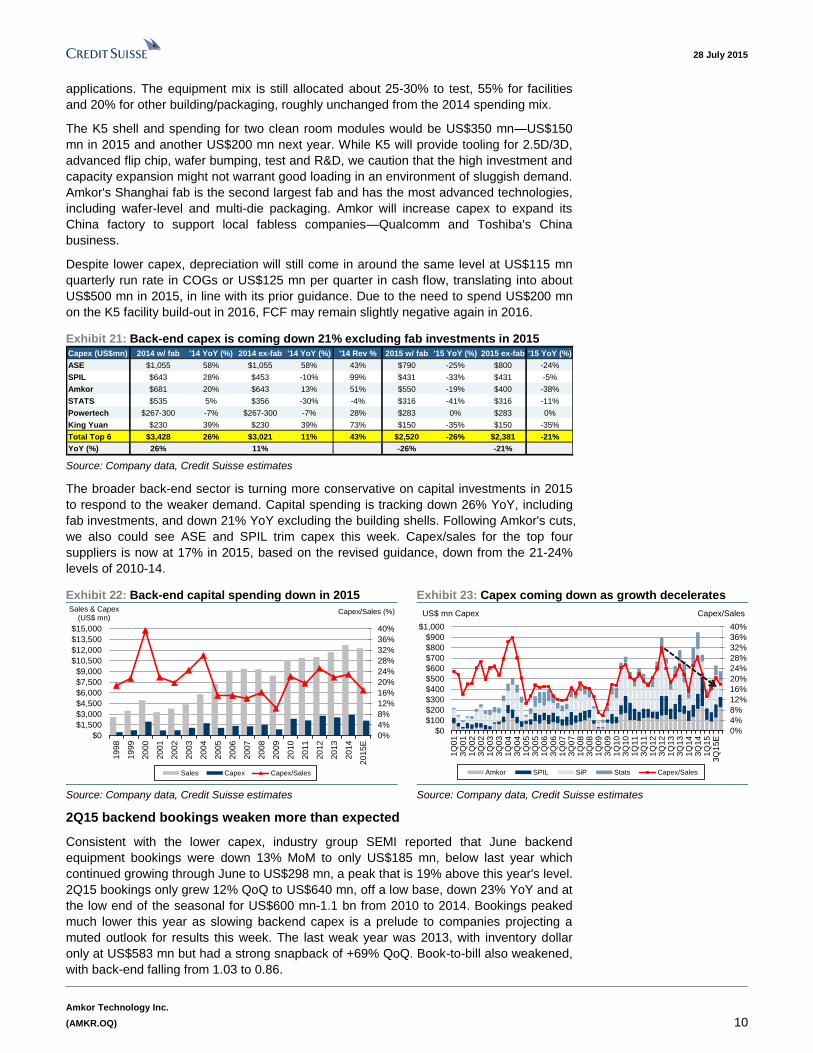

Reducing equipment capex in 2015

Amkor cut its 2015 total capex guidance from US$650 mn to US$550 mn, with its core

capex being down from US$450 mn to US$400 mn—down 38% YoY from US$650 mn in

2014. The US$550 mn total capex already includes a fixed amount of US$150 mn

investment for its Korea K5 factory that remains unchanged. The company noted that most

of the reductions will be from expansion capex, with flexibility for a further US$40 mn cut, if

demand further disappoints into 4Q15. Majority of the reduction will be from advanced

packaging due to a slowdown in mobile, but it will also trim budget from mainstream

Amkor is cutting its

equipment capex from

US$450 mn to US$400 mn.

US$150 mn for K5

unchanged

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 10

applications. The equipment mix is still allocated about 25-30% to test, 55% for facilities

and 20% for other building/packaging, roughly unchanged from the 2014 spending mix.

The K5 shell and spending for two clean room modules would be US$350 mn—US$150

mn in 2015 and another US$200 mn next year. While K5 will provide tooling for 2.5D/3D,

advanced flip chip, wafer bumping, test and R&D, we caution that the high investment and

capacity expansion might not warrant good loading in an environment of sluggish demand.

Amkor's Shanghai fab is the second largest fab and has the most advanced technologies,

including wafer-level and multi-die packaging. Amkor will increase capex to expand its

China factory to support local fabless companies—Qualcomm and Toshiba's China

business.

Despite lower capex, depreciation will still come in around the same level at US$115 mn

quarterly run rate in COGs or US$125 mn per quarter in cash flow, translating into about

US$500 mn in 2015, in line with its prior guidance. Due to the need to spend US$200 mn

on the K5 facility build-out in 2016, FCF may remain slightly negative again in 2016.

Exhibit 21: Back-end capex is coming down 21% excluding fab investments in 2015 Capex (US$mn) 2014 w/ fab '14 YoY (%) 2014 ex-fab '14 YoY (%) '14 Rev % 2015 w/ fab '15 YoY (%) 2015 ex-fab '15 YoY (%)

ASE $1,055 58% $1,055 58% 43% $790 -25% $800 -24%

SPIL $643 28% $453 -10% 99% $431 -33% $431 -5%

Amkor $681 20% $643 13% 51% $550 -19% $400 -38%

STATS $535 5% $356 -30% -4% $316 -41% $316 -11%

Powertech $267-300 -7% $267-300 -7% 28% $283 0% $283 0%

King Yuan $230 39% $230 39% 73% $150 -35% $150 -35%

Total Top 6 $3,428 26% $3,021 11% 43% $2,520 -26% $2,381 -21%

YoY (%) 26% 11% -26% -21% Source: Company data, Credit Suisse estimates

The broader back-end sector is turning more conservative on capital investments in 2015

to respond to the weaker demand. Capital spending is tracking down 26% YoY, including

fab investments, and down 21% YoY excluding the building shells. Following Amkor's cuts,

we also could see ASE and SPIL trim capex this week. Capex/sales for the top four

suppliers is now at 17% in 2015, based on the revised guidance, down from the 21-24%

levels of 2010-14.

Exhibit 22: Back-end capital spending down in 2015 Exhibit 23: Capex coming down as growth decelerates

0%

4%

8%

12%

16%

20%

24%

28%

32%

36%

40%

$0

$1,500

$3,000

$4,500

$6,000

$7,500

$9,000

$10,500

$12,000

$13,500

$15,000

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15E

Capex/Sales (%)Sales & Capex (US$ mn)

Sales Capex Capex/Sales

0%

4%

8%

12%

16%

20%

24%

28%

32%

36%

40%

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15E

Capex/SalesUS$ mn Capex

Amkor SPIL SiP Stats Capex/Sales

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

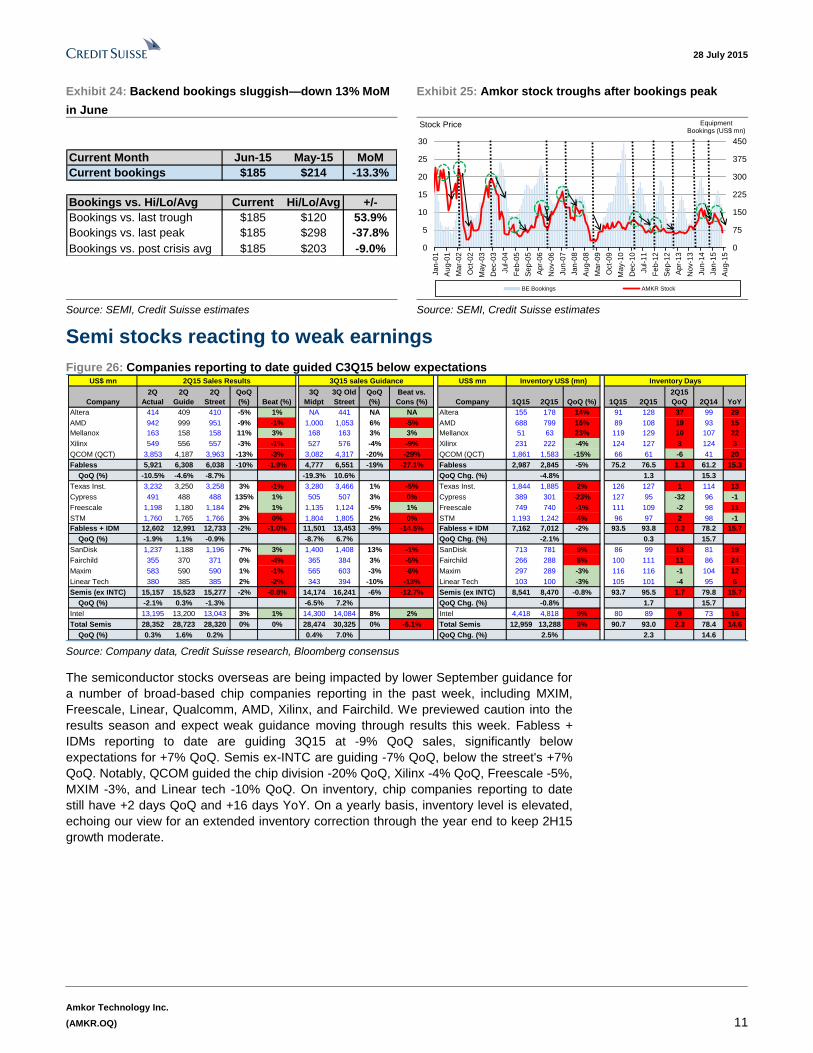

2Q15 backend bookings weaken more than expected

Consistent with the lower capex, industry group SEMI reported that June backend

equipment bookings were down 13% MoM to only US$185 mn, below last year which

continued growing through June to US$298 mn, a peak that is 19% above this year's level.

2Q15 bookings only grew 12% QoQ to US$640 mn, off a low base, down 23% YoY and at

the low end of the seasonal for US$600 mn-1.1 bn from 2010 to 2014. Bookings peaked

much lower this year as slowing backend capex is a prelude to companies projecting a

muted outlook for results this week. The last weak year was 2013, with inventory dollar

only at US$583 mn but had a strong snapback of +69% QoQ. Book-to-bill also weakened,

with back-end falling from 1.03 to 0.86.

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 11

Exhibit 24: Backend bookings sluggish—down 13% MoM

in June

Exhibit 25: Amkor stock troughs after bookings peak

Current Month Jun-15 May-15 MoM

Current bookings $185 $214 -13.3%

Bookings vs. Hi/Lo/Avg Current Hi/Lo/Avg +/-

Bookings vs. last trough $185 $120 53.9%

Bookings vs. last peak $185 $298 -37.8%

Bookings vs. post crisis avg $185 $203 -9.0%

0

75

150

225

300

375

450

0

5

10

15

20

25

30

Jan

-01

Au

g-0

1

Ma

r-0

2

Oct-

02

Ma

y-0

3

De

c-0

3

Jul-

04

Fe

b-0

5

Se

p-0

5

Ap

r-06

No

v-0

6

Jun

-07

Jan

-08

Au

g-0

8

Ma

r-0

9

Oct-

09

Ma

y-1

0

De

c-1

0

Jul-

11

Fe

b-1

2

Se

p-1

2

Ap

r-13

No

v-1

3

Jun

-14

Jan

-15

Au

g-1

5

Equipment Bookings (US$ mn)

Stock Price

BE Bookings AMKR Stock

Source: SEMI, Credit Suisse estimates Source: SEMI, Credit Suisse estimates

Semi stocks reacting to weak earnings

Figure 26: Companies reporting to date guided C3Q15 below expectations US$ mn 2Q15 Sales Results 3Q15 sales Guidance US$ mn Inventory US$ (mn) Inventory Days COGS

Company

2Q

Actual

2Q

Guide

2Q

Street

QoQ

(%) Beat (%)

3Q

Midpt

3Q Old

Street

QoQ

(%)

Beat vs.

Cons (%) Company 1Q15 2Q15 QoQ (%) 1Q15 2Q15

2Q15

QoQ 2Q14 YoY

Altera 414 409 410 -5% 1% NA 441 NA NA Altera 155 178 14% 91 128 37 99 29

AMD 942 999 951 -9% -1% 1,000 1,053 6% -5% AMD 688 799 16% 89 108 19 93 15

Mellanox 163 158 158 11% 3% 168 163 3% 3% Mellanox 51 63 23% 119 129 10 107 22

Xilinx 549 556 557 -3% -1% 527 576 -4% -9% Xilinx 231 222 -4% 124 127 3 124 3

QCOM (QCT) 3,853 4,187 3,963 -13% -3% 3,082 4,317 -20% -29% QCOM (QCT) 1,861 1,583 -15% 66 61 -6 41 20

Fabless 5,921 6,308 6,038 -10% -1.9% 4,777 6,551 -19% -27.1% Fabless 2,987 2,845 -5% 75.2 76.5 1.3 61.2 15.3

QoQ (%) -10.5% -4.6% -8.7% -19.3% 10.6% QoQ Chg. (%) -4.8% 1.3 15.3

Texas Inst. 3,232 3,250 3,258 3% -1% 3,280 3,466 1% -5% Texas Inst. 1,844 1,885 2% 126 127 1 114 13

Cypress 491 488 488 135% 1% 505 507 3% 0% Cypress 389 301 -23% 127 95 -32 96 -1

Freescale 1,198 1,180 1,184 2% 1% 1,135 1,124 -5% 1% Freescale 749 740 -1% 111 109 -2 98 11

STM 1,760 1,765 1,766 3% 0% 1,804 1,805 2% 0% STM 1,193 1,242 4% 96 97 2 98 -1

Fabless + IDM 12,602 12,991 12,733 -2% -1.0% 11,501 13,453 -9% -14.5% Fabless + IDM 7,162 7,012 -2% 93.5 93.8 0.3 78.2 15.7

QoQ (%) -1.9% 1.1% -0.9% -8.7% 6.7% QoQ Chg. (%) -2.1% 0.3 15.7

SanDisk 1,237 1,188 1,196 -7% 3% 1,400 1,408 13% -1% SanDisk 713 781 9% 86 99 13 81 19

Fairchild 355 370 371 0% -4% 365 384 3% -5% Fairchild 266 288 8% 100 111 11 86 24

Maxim 583 590 590 1% -1% 565 603 -3% -6% Maxim 297 289 -3% 116 116 -1 104 12

Linear Tech 380 385 385 2% -2% 343 394 -10% -13% Linear Tech 103 100 -3% 105 101 -4 95 6

Semis (ex INTC) 15,157 15,523 15,277 -2% -0.8% 14,174 16,241 -6% -12.7% Semis (ex INTC) 8,541 8,470 -0.8% 93.7 95.5 1.7 79.8 15.7

QoQ (%) -2.1% 0.3% -1.3% -6.5% 7.2% QoQ Chg. (%) -0.8% 1.7 15.7

Intel 13,195 13,200 13,043 3% 1% 14,300 14,084 8% 2% Intel 4,418 4,818 9% 80 89 9 73 16

Total Semis 28,352 28,723 28,320 0% 0% 28,474 30,325 0% -6.1% Total Semis 12,959 13,288 3% 90.7 93.0 2.3 78.4 14.6

QoQ (%) 0.3% 1.6% 0.2% 0.4% 7.0% QoQ Chg. (%) 2.5% 2.3 14.6 Source: Company data, Credit Suisse research, Bloomberg consensus

The semiconductor stocks overseas are being impacted by lower September guidance for

a number of broad-based chip companies reporting in the past week, including MXIM,

Freescale, Linear, Qualcomm, AMD, Xilinx, and Fairchild. We previewed caution into the

results season and expect weak guidance moving through results this week. Fabless +

IDMs reporting to date are guiding 3Q15 at -9% QoQ sales, significantly below

expectations for +7% QoQ. Semis ex-INTC are guiding -7% QoQ, below the street's +7%

QoQ. Notably, QCOM guided the chip division -20% QoQ, Xilinx -4% QoQ, Freescale -5%,

MXIM -3%, and Linear tech -10% QoQ. On inventory, chip companies reporting to date

still have +2 days QoQ and +16 days YoY. On a yearly basis, inventory level is elevated,

echoing our view for an extended inventory correction through the year end to keep 2H15

growth moderate.

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 12

Balance sheet leveraged—although debt refinancing

lessens the interest burden

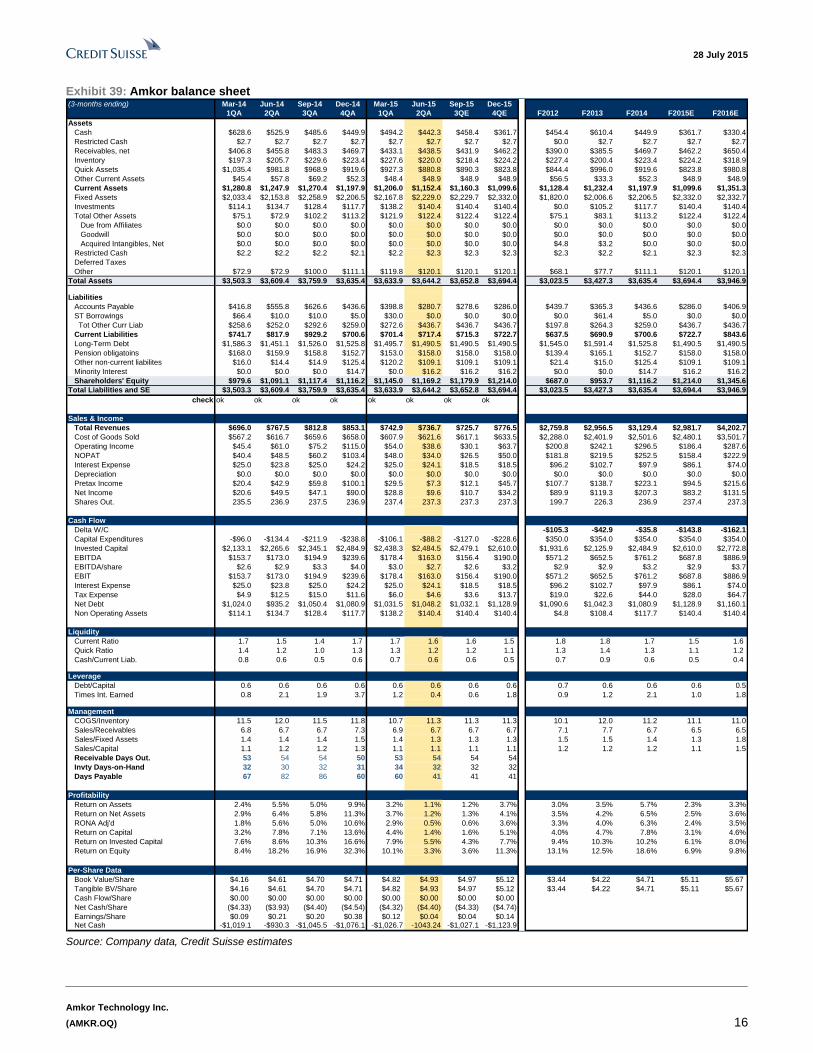

Exhibit 27: Amkor balance sheet relatively unchanged in June US$ mn, unless otherwise stated

Balance Sheet Mar-15 Jun-15 Q/Q %

Summary Actual Actual Change

Cash & Equivalents $494.2 $442.3 -10.5%

Total Debt $1,525.7 $1,490.5 -2.3%

Net Cash -$1,031.5 -$1,048.2 1.6%

Net Cash/Share -$4.32 -$4.40 1.7%

A/R $433.1 $438.5 1.2%

DSO 53 54 2.1%

Inventory $227.6 $220.0 -3.3%

Inventory Days 34 32 -5.5%

SH Equity (BV) $1,145.0 $1,169.2 2.1%

Book Value / Share $4.82 $4.93 2.2%

TBV / Share $4.82 $4.93 2.2% Source: Company data, Credit Suisse estimates

Amkor's balance sheet was slightly improved but still leveraged in 2Q15, with net debt

increasing from US$1,032 mn to US$1,048 mn and from -US$4.3 per share to -US$4.4

per share. Working capital increased for both receivables and inventory and had stable

book value at around US$4.93/share. The stock after hours was to 0.8x P/B, a discount to

its Taiwan peers at 1.3x P/B although ROE is also lower at 7% vs 13% for the Taiwan

back-end. The company still carries US$1.5 bn of debt on its balance sheet but is working

to reduce its interest burden by extinguishing the high-rate debt in 2Q15 at a discount to

par value—the company expects to save US$17 mn in annual interest expense and have

a US$18-19 mn quarterly run rate post the redemption.

Exhibit 28: Inventory days down QoQ in 2Q15 Exhibit 29: Receivable days up in 2Q15

20

22

24

26

28

30

32

34

36

38

40

$0

$50

$100

$150

$200

$250

Mar-

09

Jun

-09

Se

p-0

9

Dec-0

9

Mar-

10

Jun

-10

Se

p-1

0

Dec-1

0

Mar-

11

Jun

-11

Se

p-1

1

Dec-1

1

Mar-

12

Jun

-12

Se

p-1

2

Dec-1

2

Mar-

13

Jun

-13

Se

p-1

3

Dec-1

3

Mar-

14

Jun

-14

Se

p-1

4

Dec-1

4

Mar-

15

Jun

-15

Invento

ry D

ays

Invento

ry (

in $

mn)

Inventory Inventory Days

30

35

40

45

50

55

60

$0

$100

$200

$300

$400

$500

$600

Mar-

09

Jun

-09

Se

p-0

9

Dec-0

9

Mar-

10

Jun

-10

Se

p-1

0

Dec-1

0

Mar-

11

Jun

-11

Se

p-1

1

Dec-1

1

Mar-

12

Jun

-12

Se

p-1

2

Dec-1

2

Mar-

13

Jun

-13

Se

p-1

3

Dec-1

3

Mar-

14

Jun

-14

Se

p-1

4

Dec-1

4

Mar-

15

Jun

-15

Days

Sale

s O

uts

tandin

g

Receiv

able

( in $

mn)

Receivables Days Sales Outstanding

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Cutting estimates to reflect the weaker outlook

The Asian semi suppliers are seeing more muted growth in 2H15 due to the higher fabless

inventory and slowdown in smartphones and consumer tech (PCs/tablets/TVs), with each

end-market slightly below expectations YTD. On the softer 2H15 outlook, we trim

2015/16E EPS from US$0.62/0.70 to US$0.35/0.55.

Amkor's balance sheet

remains leveraged

Reducing 2016E sales to

-4.7% YoY from flat YoY

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 13

Exhibit 30: Revising down 2015 and 2016 estimates

AMKR

Actual CS CS Old Cons CS CS Old Cons

Total Revenue $3,129.4 $2,981.7 $3,118.7 $4,042.0 $4,202.7 $4,439.4 $4,006.5

% Q/Q chng

% Y/Y chng 5.9% -4.7% -0.3% 29.8% 40.9% 42.3% -0.9%

Total GM* 20.1% 16.8% 19.0% 19.5% 16.7% 17.5% 21.3%

R&D Expense* $76.9 $79.4 $73.0 $106.2 $97.2

SG&A Expense* $254.5 $235.9 $254.9 $307.3 $334.6

Operating Exp.* $331.4 $315.2 $327.9 $413.5 $431.8

Operating Mgin* 9.5% 6.3% 8.5% 8.8% 6.8% 7.8% 10.2%

Net Income* $207.3 $83.2 $147.0 $189.0 $131.5 $167.0 $225.3

Net Margin* 6.6% 2.8% 4.7% 4.7% 3.1% 3.8% 5.6%

EPS* $0.87 $0.35 $0.62 $0.74 $0.55 $0.70 $0.98

Fully diluted shares 236.9 237.4 237.4 237.3 237.4

F2016EF2014 F2015E

Source: Company data, Credit Suisse estimates, Bloomberg consensus

Valuation approaching support levels

After the recent correction on the weak consumer tech outlook and another 9% pullback

after hours, Amkor's valuation is reasonable with the stock trading at the low end of its

long-term range. Amkor is now trading at 3.3x/2.6x 2015/16E EV/EBITDA, vs the post-

crisis range of 2.5x-5.0x and EV/sales of 0.8x/0.6x for 2015/16 versus its post-crisis range

of 0.5x-1.2x. Amkor is also at a discount to peers averaging 4.1x EV/EBITDA and 1.2x

EV/sales.

Exhibit 31: AMKR EV/EBITDA now at lower levels Exhibit 32: AMKR EV/Sales at lower levels

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

Sep

-05

Feb

-06

Ju

l-0

6

De

c-0

6

Ma

y-0

7

Oct-

07

Ma

r-08

Au

g-0

8

Ja

n-0

9

Ju

n-0

9

No

v-0

9

Ap

r-1

0

Sep

-10

Feb

-11

Ju

l-1

1

De

c-1

1

Ma

y-1

2

Oct-

12

Ma

r-13

Au

g-1

3

Ja

n-1

4

Ju

n-1

4

No

v-1

4

Ap

r-1

5

Sep

-15

EV/EBITDA

EV/EBITDA

0.0

0.3

0.5

0.8

1.0

1.3

1.5

1.8

2.0

Ma

r-04

Sep

-04

Ma

r-05

Sep

-05

Ma

r-06

Sep

-06

Ma

r-07

Sep

-07

Ma

r-08

Sep

-08

Ma

r-09

Sep

-09

Ma

r-10

Sep

-10

Ma

r-11

Sep

-11

Ma

r-12

Sep

-12

Ma

r-13

Sep

-13

Ma

r-14

Sep

-14

Ma

r-15

Sep

-15

EV/Sales

EV/Sales multiple

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Amkor is also at a discount on P/B, trading at 0.8x/0.7x 2015/16E P/B, the bottom of its

post-crisis range and below the group average of 1.3x P/B. While Amkor's ROE used to be

at par with its competitors, it is now at 7%, below the average of 13%—although Amkor is

the first to report 2Q15 results and guide for 2H15, and we anticipate some weakness

across other backend companies as well taking down the group average ROE.

Exhibit 33: Amkor valuation reasonable vs peers Price Mkt Cap EV/Sales (x) EV/EBITDA (x) P/E Multiple (x) P/B Multiple (x) ROE Trough/Peak (EV/Sales)

Company Ticker 7/28/2015 (US$mn) 2014 2015 2016 2014 2015 2016 2014 2015 2016 2014 2015 2016 2014 2015 2016

Select backend peers

Amkor AMKR $4.25 $1,168 0.7 0.8 0.6 3.0 3.3 2.6 4.9 12.1 7.7 0.9 0.8 0.7 18.6 6.9 9.8

ASE 2311.TW $35.75 $8,857 1.2 1.1 1.0 5.6 5.4 5.1 12.1 12.9 11.3 1.9 1.9 1.8 15.7 14.5 15.6

SPIL 2325.TW $37.25 $3,676 1.4 1.4 1.2 4.4 4.0 3.7 10.0 9.5 8.6 1.6 1.5 1.5 16.3 16.1 17.2

Chipbond 6147.TWO $42.20 $867 1.8 1.8 1.5 5.4 5.5 4.5 10.7 11.8 8.0 1.2 1.2 1.1 11.0 9.8 13.4

ChipMOS 8150.TW $32.20 $934 1.0 1.1 0.9 3.5 3.3 2.9 8.3 10.2 8.9 1.5 1.5 1.4 18.2 14.4 15.4

Powertech 6239.TW $52.90 $1,280 1.0 0.9 0.8 3.1 2.8 2.6 12.5 10.6 9.8 1.3 1.2 1.1 10.3 11.3 11.6

Median 1.1 1.1 0.9 3.9 3.7 3.3 10.3 11.2 8.7 1.4 1.3 1.3 16.0 12.8 14.4

Mean 1.2 1.2 1.0 4.1 4.1 3.6 9.7 11.2 9.0 1.4 1.3 1.3 15.0 12.2 13.8 Source: Company data, Credit Suisse estimates

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 14

Exhibit 34: Amkor P/B now at a trough at only 0.8x Exhibit 35: Amkor P/B down slated for a rebound

0.8x

1.2x

2.0x

2.4x

0

5

10

15

Ap

r/09

Oct/0

9

Ap

r/10

Oct/1

0

Ap

r/11

Oct/1

1

Ap

r/12

Oct/1

2

Ap

r/13

Oct/1

3

Ap

r/14

Oct/1

4

Ap

r/15

US$ AMKR historical PB band

0%

7%

14%

21%

28%

35%

0

4

8

12

16

20

Jan

/11

Ap

r/11

Ju

l/11

Oct/1

1

Jan

/12

Ap

r/12

Ju

l/12

Oct/1

2

Jan

/13

Ap

r/13

Ju

l/13

Oct/1

3

Jan

/14

Ap

r/14

Ju

l/14

Oct/1

4

Jan

/15

Ap

r/15

Ju

l/15

Oct/1

5

Jan

/16

Ap

r/16

Ju

l/16

Oct/1

6US$ AMKR historical PB-ROE chart

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Amkor is still trading at a discount to its peers due to a more leveraged balance sheet and

lower operating margins. The company's current balance sheet has high debt/equity at

127% vs SPIL's only 39% and ASE 63%.

Exhibit 36: 2Q15 back-end balance sheet comparison Exhibit 37: Back-end valuation comparison Compares

(NT$mn/US$mn)ASE SPIL Amkor Stats

Cash and investments 57,399 37,790 442 195

Total debt 93,656 29,061 1,491 1,169

Net cash -36,257 8,729 -1,048 -974

Net cash/share (NT$) -4.61 2.82 -4.42 -0.44

Accounts receivable 43,009 17,367 281 221

Days sales outstanding 61 76 35 56

Inventory 47,605 4,509 220 75

Inventory days 83 27 35 20

Accounts payable days 55 43 41 99

Cash conversion days 88 60 29 -22

Debt / Equity 63% 39% 127% 124%

Shareholders' equity 148,329 75,035 1,169 945

Compares ASE SPIL Amkor Stats

2015E BVPS 19.0 24.2 5.1 0.4

P/B Ratio 1.9 1.5 1.0 0.8

2015E EPS 2.77 3.90 0.35 -0.01

P/E Ratio 12.9 9.5 14.0 n.m.

2015E EBITDA 1,751 956 688 353

EV/EBITDA 5.8 3.5 3.2 4.1

2015E Sales 5,325 2,860 2,760 1,487

EV/Sales 1.9 1.2 0.8 1.0

Enterprise Value 10,072 3,383 2,216 1,461

Market cap 8,857 3,676 1,168 740

Sharecount 7,868 3,098 237 2,202

Stock price: $35.75 $37.25 $4.92 $0.46

US$ conversion: $29.83 $29.83 $1.00 $1.35

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 15

Exhibit 38: Amkor income statement summary (3-months ending) Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

1QA 2QA 3QA 4QA 1QA 2QA 3QE 4QE F2012 F2013 F2014 F2015E F2016E

Total Sales $696,044 $767,459 $812,824 $853,113 $742,875 $736,722 $725,671 $776,468 $2,759,846 $2,956,450 $3,129,440 $2,981,736 $4,202,734

QoQ / YoY change -7.8% 10.3% 5.9% 5.0% -12.9% -0.8% -1.5% 7.0% -0.6% 7.1% 5.9% -4.7% 40.9%

Total COGS $567,224 $616,745 $659,607 $658,042 $607,928 $621,624 $617,062 $633,464 $2,287,975 $2,401,937 $2,501,618 $2,480,078 $3,501,655

Gross Profit $128,820 $150,714 $153,217 $195,071 $134,947 $115,098 $108,609 $143,004 $471,871 $554,513 $627,822 $501,658 $701,079

% GM 18.5% 19.6% 18.8% 22.9% 18.2% 15.6% 15.0% 18.4% 17.1% 18.8% 20.1% 16.8% 16.7%

incr GM 36.3% 30.7% 5.5% 103.9% 54.5% 322.6% 58.7% 67.7%

SG&A $62,424 $67,674 $61,600 $62,800 $62,942 $56,435 $57,959 $58,538 $217,000 $247,779 $254,498 $235,874 $307,256

% Sales 9.0% 8.8% 7.6% 7.4% 8.5% 7.7% 8.0% 7.5% 7.9% 8.4% 8.1% 7.9% 7.3%

R&D $21,045 $22,079 $16,437 $17,303 $18,026 $20,020 $20,561 $20,766 $54,118 $64,625 $76,864 $79,373 $106,222

% Sales 3.0% 2.9% 2.0% 2.0% 2.4% 2.7% 2.8% 2.7% 2.0% 2.2% 2.5% 2.7% 2.5%

Opex $83,469 $89,753 $78,037 $80,103 $80,968 $76,455 $78,519 $79,304 $271,118 $312,404 $331,362 $315,247 $413,479

Amort of GW $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 $0

Op Income $45,351 $60,961 $75,180 $114,968 $53,979 $38,643 $30,089 $63,700 $200,753 $242,109 $296,460 $186,411 $287,600

OpM % 6.5% 7.9% 9.2% 13.5% 7.3% 5.2% 4.1% 8.2% 7.3% 8.2% 9.5% 6.3% 6.8%

Interest Expense -$24,964 -$23,779 -$25,023 -$24,159 -$25,019 -$24,087 -$18,500 -$18,500 -$96,198 -$102,745 -$97,925 -$86,106 -$74,000

FX gain/loss $0 $0 $0 $0 $0 $0 $0 $0 -$2,670 $1,841 $0 $0 $0

Other Income -$36 $5,699 $9,626 $9,254 $498 -$7,290 $500 $500 $5,800 $9,080 $24,543 -$5,792 $2,000

Interest, Net -$25,000 -$18,080 -$15,397 -$14,905 -$24,521 -$31,377 -$18,000 -$18,000 -$93,068 -$91,824 -$73,382 -$91,898 -$72,000

One-Time Charge $0 $0 $0 $0 $0 $0 $0 $0 $0 -$11,619 $0 $0 $0

Pretax Income $20,351 $42,881 $59,783 $100,063 $29,458 $7,266 $12,089 $45,700 $107,685 $138,666 $223,078 $94,513 $215,600

% Sales 2.9% 5.6% 7.4% 11.7% 4.0% 1.0% 1.7% 5.9% 3.9% 4.7% 7.1% 3.2% 5.1%

Tax $4,929 $12,511 $14,985 $11,555 $5,999 $4,631 $3,627 $13,710 $19,001 $22,646 $43,980 $27,967 $64,680

% Tax Rate 24.2% 29.2% 25.1% 11.5% 20.4% 63.7% 30.0% 30.0% 17.6% 16.3% 19.7% 29.6% 30.0%

Equity in J-Devices JV $5,761 $20,036 $3,372 $2,485 $6,238 $7,566 $3,000 $3,000 $0 $5,637 $31,654 $19,804 $0

Minority Interest -$550 -$885 -$1,073 -$993 -$916 -$623 -$800 -$800 $1,169 -$2,361 -$3,501 -$3,139 -$19,370

Net Income $20,633 $49,521 $47,097 $90,000 $28,781 $9,578 $10,663 $34,190 $89,853 $119,296 $207,251 $83,212 $131,550

% Sales 3.0% 6.5% 5.8% 10.5% 3.9% 1.3% 1.5% 4.4% 3.3% 4.0% 6.6% 2.8% 3.1%

EPS $0.09 $0.21 $0.20 $0.38 $0.12 $0.04 $0.04 $0.14 $0.45 $0.53 $0.87 $0.35 $0.55

EPS (excl. option exp) $0.09 $0.21 $0.20 $0.38 $0.13 $0.05 $0.05 $0.15 $0.47 $0.55 $0.89 $0.37 $0.57

Primary Shares $0.09 $0.21 $0.20 $0.38 $0.12 $0.04 $0.04 $0.14 $0.42 $0.51 $0.87 $0.35 $0.55

EPS fully taxed (25%) -$0.08 -$0.06 -$0.05 -$0.05 -$0.08 -$0.10 -$0.06 -$0.06 -$0.22 -$0.35 -$0.25 -$0.30 -$0.31

Primary Shares 216,757 232,891 236,337 236,578 236,708 236,840 236,840 236,840 191,151 195,364 230,641 236,807 236,840

Fully Diluted Shares 235,497 236,872 237,509 236,937 237,424 237,321 237,321 237,321 199,706 226,260 236,907 237,357 237,321

EBIT $45,351 $60,961 $75,180 $114,968 $53,979 $38,643 $30,089 $63,700 $200,753 $242,109 $296,460 $186,411 $287,600

EBIT Margin % 3.0% 2.9% 2.0% 2.0% 2.4% 2.7% 2.8% 2.7% 7.3% 8.2% 9.5% 6.3% 6.8%

EBITDA $153,689 $173,012 $194,880 $239,585 $178,366 $162,972 $156,418 $190,029 $571,232 $652,455 $761,166 $687,785 $886,916

EBITDA Margin % 22.1% 22.5% 24.0% 28.1% 24.0% 22.1% 21.6% 24.5% 20.7% 22.1% 24.3% 23.1% 21.1%

Capex -$95,999 -$134,393 -$211,916 -$238,812 -$106,149 -$88,211 -$126,992 -$228,648 -$533,425 -$566,256 -$681,120 -$550,000 -$600,000

Depreciation $108,338 $112,051 $119,700 $124,617 $124,387 $124,329 $126,329 $126,329 $370,479 $410,346 $464,706 $501,374 $599,316

FCF (OCF-Capex) $36,407 -$14,491 -$72,549 -$29,936 $59,839 -$27,717 $16,131 -$96,762 -$130,971 -$82,958 -$80,569 -$48,508 -$193,441

FCF/Share $0.15 -$0.06 -$0.31 -$0.13 $0.25 -$0.12 $0.07 -$0.41 -$0.66 -$0.37 -$0.34 -$0.20 -$0.82 Source: Company data, Credit Suisse estimates

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 16

Exhibit 39: Amkor balance sheet (3-months ending) Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

1QA 2QA 3QA 4QA 1QA 2QA 3QE 4QE F2012 F2013 F2014 F2015E F2016E

Assets

Cash $628.6 $525.9 $485.6 $449.9 $494.2 $442.3 $458.4 $361.7 $454.4 $610.4 $449.9 $361.7 $330.4

Restricted Cash $2.7 $2.7 $2.7 $2.7 $2.7 $2.7 $2.7 $2.7 $0.0 $2.7 $2.7 $2.7 $2.7

Receivables, net $406.8 $455.8 $483.3 $469.7 $433.1 $438.5 $431.9 $462.2 $390.0 $385.5 $469.7 $462.2 $650.4

Inventory $197.3 $205.7 $229.6 $223.4 $227.6 $220.0 $218.4 $224.2 $227.4 $200.4 $223.4 $224.2 $318.9

Quick Assets $1,035.4 $981.8 $968.9 $919.6 $927.3 $880.8 $890.3 $823.8 $844.4 $996.0 $919.6 $823.8 $980.8

Other Current Assets $45.4 $57.8 $69.2 $52.3 $48.4 $48.9 $48.9 $48.9 $56.5 $33.3 $52.3 $48.9 $48.9

Current Assets $1,280.8 $1,247.9 $1,270.4 $1,197.9 $1,206.0 $1,152.4 $1,160.3 $1,099.6 $1,128.4 $1,232.4 $1,197.9 $1,099.6 $1,351.3

Fixed Assets $2,033.4 $2,153.8 $2,258.9 $2,206.5 $2,167.8 $2,229.0 $2,229.7 $2,332.0 $1,820.0 $2,006.6 $2,206.5 $2,332.0 $2,332.7

Investments $114.1 $134.7 $128.4 $117.7 $138.2 $140.4 $140.4 $140.4 $0.0 $105.2 $117.7 $140.4 $140.4

Total Other Assets $75.1 $72.9 $102.2 $113.2 $121.9 $122.4 $122.4 $122.4 $75.1 $83.1 $113.2 $122.4 $122.4

Due from Affiliates $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0

Goodwill $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0

Acquired Intangibles, Net $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $4.8 $3.2 $0.0 $0.0 $0.0

Restricted Cash $2.2 $2.2 $2.2 $2.1 $2.2 $2.3 $2.3 $2.3 $2.3 $2.2 $2.1 $2.3 $2.3

Deferred Taxes

Other $72.9 $72.9 $100.0 $111.1 $119.8 $120.1 $120.1 $120.1 $68.1 $77.7 $111.1 $120.1 $120.1

Total Assets $3,503.3 $3,609.4 $3,759.9 $3,635.4 $3,633.9 $3,644.2 $3,652.8 $3,694.4 $3,023.5 $3,427.3 $3,635.4 $3,694.4 $3,946.9

Liabilities

Accounts Payable $416.8 $555.8 $626.6 $436.6 $398.8 $280.7 $278.6 $286.0 $439.7 $365.3 $436.6 $286.0 $406.9

ST Borrowings $66.4 $10.0 $10.0 $5.0 $30.0 $0.0 $0.0 $0.0 $0.0 $61.4 $5.0 $0.0 $0.0

Tot Other Curr Liab $258.6 $252.0 $292.6 $259.0 $272.6 $436.7 $436.7 $436.7 $197.8 $264.3 $259.0 $436.7 $436.7

Current Liabilities $741.7 $817.9 $929.2 $700.6 $701.4 $717.4 $715.3 $722.7 $637.5 $690.9 $700.6 $722.7 $843.6

Long-Term Debt $1,586.3 $1,451.1 $1,526.0 $1,525.8 $1,495.7 $1,490.5 $1,490.5 $1,490.5 $1,545.0 $1,591.4 $1,525.8 $1,490.5 $1,490.5

Pension obligatoins $168.0 $159.9 $158.8 $152.7 $153.0 $158.0 $158.0 $158.0 $139.4 $165.1 $152.7 $158.0 $158.0

Other non-current liabilites $16.0 $14.4 $14.9 $125.4 $120.2 $109.1 $109.1 $109.1 $21.4 $15.0 $125.4 $109.1 $109.1

Minority Interest $0.0 $0.0 $0.0 $14.7 $0.0 $16.2 $16.2 $16.2 $0.0 $0.0 $14.7 $16.2 $16.2

Shareholders' Equity $979.6 $1,091.1 $1,117.4 $1,116.2 $1,145.0 $1,169.2 $1,179.9 $1,214.0 $687.0 $953.7 $1,116.2 $1,214.0 $1,345.6

Total Liabilities and SE $3,503.3 $3,609.4 $3,759.9 $3,635.4 $3,633.9 $3,644.2 $3,652.8 $3,694.4 $3,023.5 $3,427.3 $3,635.4 $3,694.4 $3,946.9

check ok ok ok ok ok ok ok ok

Sales & Income

Total Revenues $696.0 $767.5 $812.8 $853.1 $742.9 $736.7 $725.7 $776.5 $2,759.8 $2,956.5 $3,129.4 $2,981.7 $4,202.7

Cost of Goods Sold $567.2 $616.7 $659.6 $658.0 $607.9 $621.6 $617.1 $633.5 $2,288.0 $2,401.9 $2,501.6 $2,480.1 $3,501.7

Operating Income $45.4 $61.0 $75.2 $115.0 $54.0 $38.6 $30.1 $63.7 $200.8 $242.1 $296.5 $186.4 $287.6

NOPAT $40.4 $48.5 $60.2 $103.4 $48.0 $34.0 $26.5 $50.0 $181.8 $219.5 $252.5 $158.4 $222.9

Interest Expense $25.0 $23.8 $25.0 $24.2 $25.0 $24.1 $18.5 $18.5 $96.2 $102.7 $97.9 $86.1 $74.0

Depreciation $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0

Pretax Income $20.4 $42.9 $59.8 $100.1 $29.5 $7.3 $12.1 $45.7 $107.7 $138.7 $223.1 $94.5 $215.6

Net Income $20.6 $49.5 $47.1 $90.0 $28.8 $9.6 $10.7 $34.2 $89.9 $119.3 $207.3 $83.2 $131.5

Shares Out. 235.5 236.9 237.5 236.9 237.4 237.3 237.3 237.3 199.7 226.3 236.9 237.4 237.3

Cash Flow

Delta W/C -$105.3 -$42.9 -$35.8 -$143.8 -$162.1

Capital Expenditures -$96.0 -$134.4 -$211.9 -$238.8 -$106.1 -$88.2 -$127.0 -$228.6 $350.0 $354.0 $354.0 $354.0 $354.0

Invested Capital $2,133.1 $2,265.6 $2,345.1 $2,484.9 $2,438.3 $2,484.5 $2,479.1 $2,610.0 $1,931.6 $2,125.9 $2,484.9 $2,610.0 $2,772.8

EBITDA $153.7 $173.0 $194.9 $239.6 $178.4 $163.0 $156.4 $190.0 $571.2 $652.5 $761.2 $687.8 $886.9

EBITDA/share $2.6 $2.9 $3.3 $4.0 $3.0 $2.7 $2.6 $3.2 $2.9 $2.9 $3.2 $2.9 $3.7

EBIT $153.7 $173.0 $194.9 $239.6 $178.4 $163.0 $156.4 $190.0 $571.2 $652.5 $761.2 $687.8 $886.9

Interest Expense $25.0 $23.8 $25.0 $24.2 $25.0 $24.1 $18.5 $18.5 $96.2 $102.7 $97.9 $86.1 $74.0

Tax Expense $4.9 $12.5 $15.0 $11.6 $6.0 $4.6 $3.6 $13.7 $19.0 $22.6 $44.0 $28.0 $64.7

Net Debt $1,024.0 $935.2 $1,050.4 $1,080.9 $1,031.5 $1,048.2 $1,032.1 $1,128.9 $1,090.6 $1,042.3 $1,080.9 $1,128.9 $1,160.1

Non Operating Assets $114.1 $134.7 $128.4 $117.7 $138.2 $140.4 $140.4 $140.4 $4.8 $108.4 $117.7 $140.4 $140.4

Liquidity

Current Ratio 1.7 1.5 1.4 1.7 1.7 1.6 1.6 1.5 1.8 1.8 1.7 1.5 1.6

Quick Ratio 1.4 1.2 1.0 1.3 1.3 1.2 1.2 1.1 1.3 1.4 1.3 1.1 1.2

Cash/Current Liab. 0.8 0.6 0.5 0.6 0.7 0.6 0.6 0.5 0.7 0.9 0.6 0.5 0.4

Leverage

Debt/Capital 0.6 0.6 0.6 0.6 0.6 0.6 0.6 0.6 0.7 0.6 0.6 0.6 0.5

Times Int. Earned 0.8 2.1 1.9 3.7 1.2 0.4 0.6 1.8 0.9 1.2 2.1 1.0 1.8

Management

COGS/Inventory 11.5 12.0 11.5 11.8 10.7 11.3 11.3 11.3 10.1 12.0 11.2 11.1 11.0

Sales/Receivables 6.8 6.7 6.7 7.3 6.9 6.7 6.7 6.7 7.1 7.7 6.7 6.5 6.5

Sales/Fixed Assets 1.4 1.4 1.4 1.5 1.4 1.3 1.3 1.3 1.5 1.5 1.4 1.3 1.8

Sales/Capital 1.1 1.2 1.2 1.3 1.1 1.1 1.1 1.1 1.2 1.2 1.2 1.1 1.5

Receivable Days Out. 53 54 54 50 53 54 54 54

Invty Days-on-Hand 32 30 32 31 34 32 32 32

Days Payable 67 82 86 60 60 41 41 41

Profitability

Return on Assets 2.4% 5.5% 5.0% 9.9% 3.2% 1.1% 1.2% 3.7% 3.0% 3.5% 5.7% 2.3% 3.3%

Return on Net Assets 2.9% 6.4% 5.8% 11.3% 3.7% 1.2% 1.3% 4.1% 3.5% 4.2% 6.5% 2.5% 3.6%

RONA Adj'd 1.8% 5.6% 5.0% 10.6% 2.9% 0.5% 0.6% 3.6% 3.3% 4.0% 6.3% 2.4% 3.5%

Return on Capital 3.2% 7.8% 7.1% 13.6% 4.4% 1.4% 1.6% 5.1% 4.0% 4.7% 7.8% 3.1% 4.6%

Return on Invested Capital 7.6% 8.6% 10.3% 16.6% 7.9% 5.5% 4.3% 7.7% 9.4% 10.3% 10.2% 6.1% 8.0%

Return on Equity 8.4% 18.2% 16.9% 32.3% 10.1% 3.3% 3.6% 11.3% 13.1% 12.5% 18.6% 6.9% 9.8%

Per-Share Data

Book Value/Share $4.16 $4.61 $4.70 $4.71 $4.82 $4.93 $4.97 $5.12 $3.44 $4.22 $4.71 $5.11 $5.67

Tangible BV/Share $4.16 $4.61 $4.70 $4.71 $4.82 $4.93 $4.97 $5.12 $3.44 $4.22 $4.71 $5.11 $5.67

Cash Flow/Share $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00

Net Cash/Share ($4.33) ($3.93) ($4.40) ($4.54) ($4.32) ($4.40) ($4.33) ($4.74)

Earnings/Share $0.09 $0.21 $0.20 $0.38 $0.12 $0.04 $0.04 $0.14Net Cash -$1,019.1 -$930.3 -$1,045.5 -$1,076.1 -$1,026.7 -1043.24 -$1,027.1 -$1,123.9

Source: Company data, Credit Suisse estimates

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 17

Exhibit 40: Amkor cash flow statement (3-months ending) Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

1QA 2QA 3QA 4QA 1QA 2QA 3QE 4QE F2012 F2013 F2014 F2015E F2016E

Operating

Net Income before Extraordinaries $21.2 $50.4 $48.2 $14.1 $29.7 $10.2 $10.7 $34.2 $62.9 $111.7 $133.9 $84.8 $131.5

Depreciation and Amortization $108.3 $112.1 $119.7 $124.6 $124.4 $124.3 $126.3 $126.3 $370.5 $410.3 $464.7 $501.4 $599.3

Deferred Taxes and Investment Tax Credit $0.0 $0.0 $0.0 $0.0 $0.0

Loss on impairment of investment $0.0

Other Operating Activities -$4.3 -$28.9 -$3.8 $27.8 $0.0 $5.2 -$16.0 -$9.2 $0.0 $0.0

Equity in loss of investees

Minority Interest

Gross Cash Flow - Operating $125.2 $133.6 $164.1 $166.6 $154.1 $134.5 $137.0 $160.5 $439.4 $517.6 $589.4 $586.1 $730.9

Extraordinary Items $0.0 $0.0 $0.0 $0.0 $0.0 $2.5 $0.0 $0.0

Loss(Gain) - Sale Prop, Plant and Equip $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0

Net Chg in Operating Assets and Liabs $6.7 -$30.3 $6.4 $41.7 $10.9 -$25.1 $6.1 -$28.6 -$56.4 $39.9 $24.5 -$36.7 -$162.1

A/R -49.041 -27.492 $13.6 $35.5 -$35.5 $6.6 -$30.2 $0.0 $0.0 -$62.9 -$23.7 -$188.3

Other Rec's

Inventories -8.371 -23.889 $6.2 -$4.2 $4.2 $1.6 -$5.8 $0.0 $0.0 -$26.1 -$4.2 -$94.7

Due from Affiliates

Other Curr Assets -12.404 -11.422 $17.0 $3.9 -$3.9 $0.0 $0.0

Other non-current assets

A/P 139.016 70.801 -$190.0 -$37.8 $37.8 -$2.1 $7.4 $0.0 $0.0 $19.8 $5.3 $120.9

Accrued Expenses -6.51 40.571 -$33.6 $13.6 -$62.3 $0.0 $0.0

Other LT Liabilities

Net Cash Flow - Operating $131.9 $103.3 $170.4 $208.2 $176.0 $52.3 $143.1 $131.9 $383.0 $557.5 $613.9 $503.3 $568.7

Investing

Capital Expenditures ("accrual basis") -$96.0 -$134.4 -$211.9 -$238.8 -$106.1 -$88.2 -$127.0 -$228.6 -$533.5 -$556.3 -$681.1 -$550.0 -$600.0

Capital Expenditures ("cash basis") -$96.0 -$134.4 -$211.9 -$238.8 -$106.1 -$88.2 -$127.0 -$228.6 -$533.4 -$566.3 -$681.1 -$550.0 -$600.0

Sale of Property and Investments $0.7 $16.7 -$15.2 $0.6 $3.3 $0.8 $0.0 $0.0 $2.7 $27.2 $2.8 $4.1 $0.0

Acquisitions and Investments $0.0 $0.0 -$15.8 $0.0 -$12.9 $8.4 $0.0 $0.0 $0.0 -$41.9 -$15.8 -$4.6 $0.0

Other Investing Activities -$0.3 -$0.1 $0.0 $0.0 -$0.3 -$1.0 $0.0 $0.0 $16.8 -$59.6 -$0.4 -$1.3 $0.0

Net Cash Flow - Investing -$95.5 -$117.8 -$243.0 -$238.2 -$116.1 -$80.0 -$127.0 -$228.6 -$513.9 -$640.5 -$694.5 -$551.8 -$600.0

Financing

Cash Dividends $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0

Borrowings under revolving credit facilities $0.0 $30.0 $150.0

Payment under revolving credit facilities $0.0 -$30.0

Proceeds from issuance of short-term working capital facility$0.0 $0.0

Payments of short-term working capital facility $0.0 $0.0

Change in Current Debt $0.0 $0.0 $0.0 $340.0 $0.0 $0.0 $0.0 $0.0 $0.0 $340.0 $0.0

Change in Long-Term Debt $0.0 -$60.0 $0.0 -$5.9 -$35.0 -$495.0 $0.0 $0.0 $217.4 $283.4 -$65.9 -$530.0 $0.0

Payment of Debt Issuane Costs $0.0 $0.0

Change in Capital Stock $0.0 $0.0 $0.0 $6.3 $0.6 -$0.6 $0.0 $0.0 -$80.8 $0.0 $6.3 $0.0 $0.0

Other Financing Activity -$18.4 $3.5 $0.7 -$6.1 -$0.2 $0.5 $0.0 $0.0 -$0.6 $0.0 -$20.3 $0.2 $0.0

Net Cash Flow - Financing -$18.4 -$56.5 $0.7 -$5.7 -$4.7 -$35.1 $0.0 $0.0 $110.0 $280.1 -$80.0 -$39.8 $0.0

Currency Effect $0.2 -$0.1 $0.1 -$0.1 $0.0 $0.0 $0.0 $0.0 -$0.6 $0.2 $0.1 $0.0 $0.0

Increase (Dec) Cash & ST Investments $18.1 -$71.1 -$71.8 -$35.7 $55.2 -$62.8 $16.1 -$96.8 -$21.5 $197.4 -$160.5 -$88.3 -$31.3

Cash and Cash Equivalents at the beginning of the period$610.4 $628.6 $525.9 $485.6 $449.9 $494.2 $442.3 $458.4 $474.0 $454.4 $610.4 $449.9 $361.7

Cash and Cash Equivalents at the end of the period $628.6 $525.9 $485.6 $449.9 $494.2 $442.3 $458.4 $361.7 $454.4 $610.4 $449.9 $361.7 $330.4

Free Cash Flow $36.4 -$14.5 -$72.5 -$29.9 $59.8 -$27.7 $16.1 -$96.8 -$131.0 -$83.0 -$80.6 -$48.5 -$193.4

FCF/ Share $0.15 -$0.06 -$0.31 -$0.13 $0.25 -$0.12 $0.07 -$0.41 -$0.66 -$0.37 -$0.34 -$0.20 -$0.82

Capex/Rev -14% -18% -26% -28% -14% -12% -18% -29% -19% -19% -22% -18% -19%

Dep / Rev 16% 15% 15% 15% 17% 17% 17% 16%

Revenue $696.0 $767.5 $812.8 $853.1 $742.9 $736.7 $725.7 $776.5 $2,759.8 $2,956.5 $3,129.4 $2,981.7 $3,216.0 Source: Company data, Credit Suisse estimates

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 18

Companies Mentioned (Price as of 27-Jul-2015)

Advanced Micro Devices, Inc. (AMD.OQ, $1.62) Advanced Semicon. Engr. (2311.TW, NT$35.75) Altera Corp. (ALTR.OQ, $48.92) Amkor Technology Inc. (AMKR.OQ, $4.92, NEUTRAL[V], TP $5.5) Apple Inc (AAPL.OQ, $122.77) Audience, Inc. (ADNC.OQ, $4.89) Broadcom Corp. (BRCM.OQ, $50.79) Cypress Semiconductor Corp. (CY.OQ, $11.57) Fairchild Semiconductor International Inc. (FCS.OQ, $14.565) Freescale Semiconductor Inc. (FSL.N, $36.62) Google, Inc. (GOOGL.OQ, $658.27) Infineon Technologies AG (IFXGn.DE, €10.18) Integrated Dvc (IDTI.OQ, $19.17) Intel Corp. (INTC.OQ, $28.35) Intersil Corp. (ISIL.OQ, $11.4) JCET (600584.SS, Rmb19.53) KYEC (2449.TW, NT$19.75) Linear Technology Corp. (LLTC.OQ, $40.27) Maxim Integrated Products (MXIM.OQ, $33.85) MediaTek Inc. (2454.TW, NT$317.5) Mellanox Technologies Ltd. (MLNX.OQ, $44.51) Microchip Technology Inc. (MCHP.OQ, $41.78) NXP Semiconductors N.V. (NXPI.OQ, $88.22) Novatek Microelectronics Corp Ltd (3034.TW, NT$114.5) ON Semiconductor Corp. (ONNN.OQ, $10.14) QUALCOMM Inc. (QCOM.OQ, $61.98) STATS (STTS.SI, S$0.46) STMicroelectronics NV (STM.PA, €6.958) Samsung Electronics (005930.KS, W1,230,000) SanDisk Corp. (SNDK.OQ, $61.16) Silicon Laboratories Inc. (SLAB.OQ, $50.15) Silicon Mtn Tec (SIMO.OQ, $27.65) Siliconware Precision (2325.TW, NT$37.25) Taiwan Semiconductor Manufacturing (2330.TW, NT$134.0) Tessera Tech (TSRA.OQ, $34.4) Texas Instruments Inc. (TXN.OQ, $49.03) Toshiba (6502.T, ¥386) Xilinx (XLNX.OQ, $40.06)

Disclosure Appendix

Important Global Disclosures

Randy Abrams, CFA, Farhan Ahmad and Nickie Yue each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

3-Year Price and Rating History for Amkor Technology Inc. (AMKR.OQ)

AMKR.OQ Closing Price Target Price

Date (US$) (US$) Rating

26-Oct-12 4.05 6.00 O

25-Apr-13 3.86 5.50

26-Jul-13 4.34 *

30-Jul-13 4.28 5.50 O

29-Apr-14 7.80 8.40

29-Jul-14 9.43 10.20 N *

28-Oct-14 6.33 8.00

11-Feb-15 8.69 9.00

15-Jul-15 5.65 7.40

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark*over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

28 July 2015

Amkor Technology Inc.

(AMKR.OQ) 19

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.