alternative investment funds - bathiya.com research-labs/aif.pdf · alternate investment funds 5 6....

TRANSCRIPT

Alternative

Investment Funds -A regulatory perspective

Financial Advisory Lab at:

Mumbai | Thane | Baroda

www.shbathiya.com

Alternate Investment Funds 1

This research paper on Alternate Investment Funds (AIF) is prepared and compiled by the members of Financial

Advisory Lab at S. H. Bathiya & Associates for knowledge dissemination and learning to the Firm members and

its clients. This research paper provides general information and guidance on AIF which aims in creating a

structure where regulatory framework is available for all shades of private pool of capital or investment vehicle

so that such funds are channelized in the desired space in a regulated manner without posing systematic risk.

The research paper should be read in conjunction with the Disclaimer as forming a part of this research paper.

For any further details and clarification on the research paper:

Write us at [email protected] or

Call us at 022 – 4355 8000 / 4275 8000

Date of research paper: 21st

September, 2012

Research Team:

1. Mr. Jatin A. Thakkar

2. Mr. Ankit Davda

3. Mr. Kunal Jhaveri

4. Mr. Jatin N. Thakkar

5. Mr. Hitesh Sharma

6. Ms. Shraddha Mehta

Mentor Partners:

1. Mr. Umesh Lakhani

2. Mr. Anand Bathiya

AAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAAA

Alternate Investment Funds 2

Contents

INTRODUCTION .................................................................................................................................. 3

SALIENT FEATURES ............................................................................................................................. 3

REGISTRATION PROCESS .................................................................................................................... 7

SPONSOR & MANAGER ...................................................................................................................... 8

INVESTMENT CONDITIONS AND RESTRICTIONS ................................................................................ 9

GENERAL OBLIGATIONS ................................................................................................................... 12

CONFLICT OF INTEREST .................................................................................................................... 12

TRANSPARENCY................................................................................................................................ 12

VALUATION ...................................................................................................................................... 13

MAINTENANCE OF RECORDS ........................................................................................................... 13

WINDING UP .................................................................................................................................... 14

TAX “PASS THROUGH” FOR AIFS ...................................................................................................... 15

CONCLUSION .................................................................................................................................... 15

ABBREVIATIONS & DISCLAIMER: ...................................................................................................... 15

Alternate Investment Funds 3

INTRODUCTION

An investment fund is an organisation, entity or firm that pools funds from a large number of small

investors. By aggregating the funds of retail investors into a specific investment, in line with the

objectives of the investors, an investment company gives individual investors access to a wider

range of securities and also achieving economies of scale by bringing down the trading cost. Private

bankers, trust managers or other advisers often direct some or all of the assets of their clients

towards fund investments.

With a view to extending the perimeter of regulation to unregulated funds and ensuring systemic

stability, increasing market efficiency, encouraging formation of new capital and protecting the

interest of investors, the Securities & Exchange Board of India (‘SEBI’ or ‘Board’) approved proposal

to frame SEBI (Alternative Investment Funds) Regulations, 2012 and on May 21, 2012, notified the

SEBI (Alternative Investment Funds) Regulations, 2012 (‘AIF Regulations’). The AIF Regulations

would be a replacement to the SEBI (Venture Capital Funds) Regulations, 1996 (‘VCF Regulations’)

SEBI issued the AIF Regulations in order to create a structure where regulatory framework is

available for all shades of private pool of capital or investment vehicles so as to channelize and

better regulate the funds where institutions or HNIs invest. The need for the framework arises in

order to detect fraud, unfair trade practices and minimize conflicts of interest through disclosures,

incentive structures, reporting requirements and legal agreements.

SALIENT FEATURES

A. Scope of the Regulations and applicability to existing funds

All funds whether operating as Private Equity Funds, Real Estate Funds, Hedge Funds, Venture

Capital Funds, Pooled vehicles, etc. must register with SEBI under the AIF Regulations.

The VCF Regulations shall be repealed. However, existing VCFs shall continue to be regulated by the

VCF Regulations till the existing fund or scheme managed by the fund is wound up. Existing VCFs,

however, shall not raise any fresh funds. Such VCFs may also seek re-registration under AIF

regulations subject to approval of 66.67% of their investors by value.

Existing funds not registered under the VCF Regulations will not be allowed to float any new

scheme without registration under AIF Regulations.

Existing funds not registered under the VCF Regulations which seek registration but are not able to

comply with all provisions of AIF Regulations may seek exemption from the SEBI from strict

compliance with the AIF Regulations.

There is no minimum exemption based on the number of investors which means even if money is

held on behalf of two or more persons, to be invested, that will amount to AIF.

Alternate Investment Funds 4

Similarly, there is no exemption with respect to the size of investment, which means that

irrespective of how small a fund is, it will still require to follow the AIF Regulations.

B. Categories of funds

The AIF Regulations seek to cover all types of funds broadly under 3 categories. An application can

be made to SEBI for registration as an AIF under one of the following 3 categories:-

1. Category I AIF: AIFs with positive spill-over effects on the economy, for which certain

incentives or concessions might be considered by SEBI or GOI or other regulators in India;

and which shall include VCFs, SME Funds, Social Venture Funds and Infrastructure Funds. It

includes those AIFs that invest in sectors which are considered socially and economically

relevant for the country.

2. Category II AIF: This forms the residual category, funds which cannot be classified either as

Category I or III will be classified as Category II.

3. Category III AIF: It covers AIFs including hedge funds that are considered to have negative

externalities such as worsening systemic risk through leverage or complex trading

strategies. The regulatory restrictions and conditions are more stringent for this category of

AIF.

C. Other salient features

1. AIF Regulations will be applicable to all pooled investment vehicles other than Mutual

Funds, Collective Investment Schemes, Family Trusts, ESOP Trusts, Employee Welfare

Trusts, and holding companies, funds managed by Asset Reconstruction Companies,

Securitisation Trust or any such pool of funds which are directly regulated by any other

regulator in India. In that sense, the AIF Regulations are the residuary regulations which can

possibly apply to large number of funding vehicles.

2. Category I and II AIFs shall be close-ended and shall have a minimum tenure of 3 years.

However, Category III AIF may either be close-ended or open-ended.

3. Schemes may be launched under an AIF subject to filing of Information Memorandum

(‘IM’) with the SEBI along with applicable fees.

4. Units of close ended schemes of AIF may be listed on stock exchange subject to a minimum

tradable lot of Rs. One Crore. However, AIF shall not raise funds through stock exchange

mechanism.

5. AIFs shall not be permitted to invest more than 25% of the investible funds in one Investee

Company. Further, AIFs shall not invest in associate companies except if it obtains requisite

approval from the investors.

Alternate Investment Funds 5

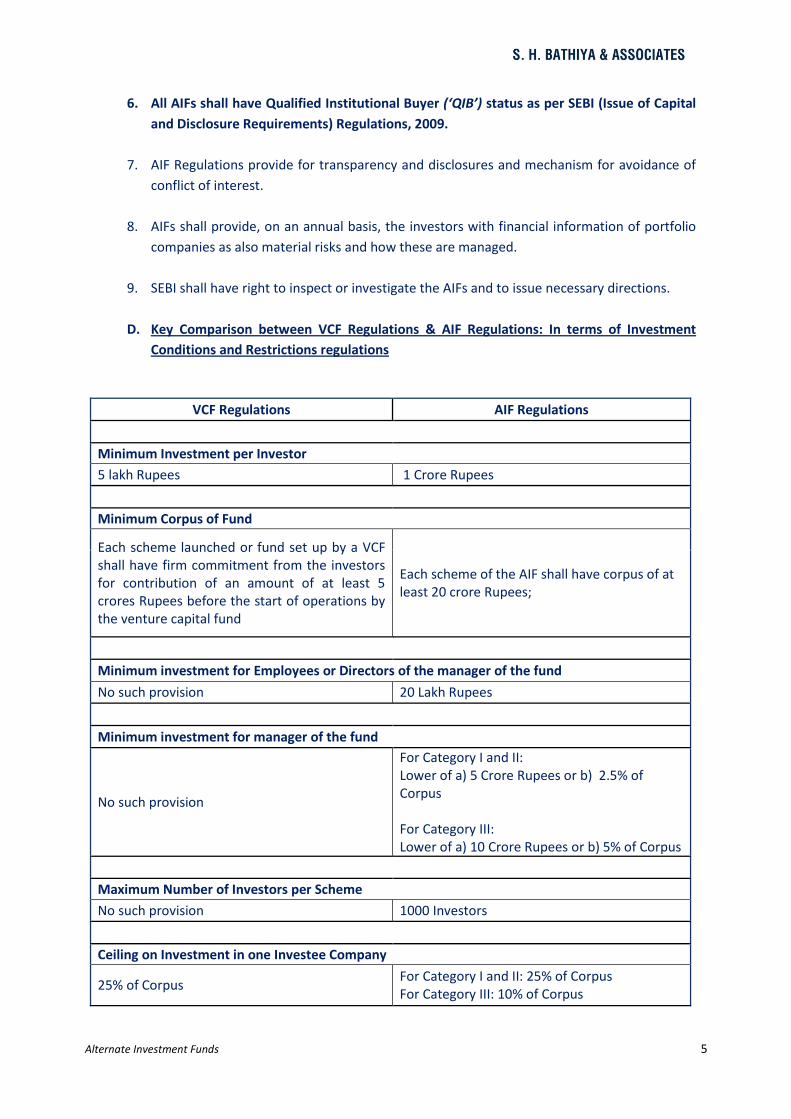

6. All AIFs shall have Qualified Institutional Buyer (‘QIB’) status as per SEBI (Issue of Capital

and Disclosure Requirements) Regulations, 2009.

7. AIF Regulations provide for transparency and disclosures and mechanism for avoidance of

conflict of interest.

8. AIFs shall provide, on an annual basis, the investors with financial information of portfolio

companies as also material risks and how these are managed.

9. SEBI shall have right to inspect or investigate the AIFs and to issue necessary directions.

D. Key Comparison between VCF Regulations & AIF Regulations: In terms of Investment

Conditions and Restrictions regulations

VCF Regulations AIF Regulations

Minimum Investment per Investor

5 lakh Rupees 1 Crore Rupees

Minimum Corpus of Fund

Each scheme launched or fund set up by a VCF shall have firm commitment from the investors for contribution of an amount of at least 5 crores Rupees before the start of operations by the venture capital fund

Each scheme of the AIF shall have corpus of at least 20 crore Rupees;

Minimum investment for Employees or Directors of the manager of the fund

No such provision 20 Lakh Rupees

Minimum investment for manager of the fund

No such provision

For Category I and II: Lower of a) 5 Crore Rupees or b) 2.5% of Corpus For Category III: Lower of a) 10 Crore Rupees or b) 5% of Corpus

Maximum Number of Investors per Scheme

No such provision 1000 Investors

Ceiling on Investment in one Investee Company

25% of Corpus For Category I and II: 25% of Corpus For Category III: 10% of Corpus

Alternate Investment Funds 6

Investment in Associate

A VCF is not allowed to invest in its Associate An AIF can invest in associates subject to approval of 75% of investors by value of their investment.

Additional Conditions for AIF

No such provision

a) Co-investment in an investee company by a Manager or Sponsor shall not be on terms more favourable than those offered to the AIF; b) Un-invested portion of the corpus may be invested in liquid mutual funds or bank deposits or other liquid assets of higher quality such as Treasury bills, CBLOs, etc. till deployment of funds as per objective.

1. Key Definitions:

Change in definition of Venture Capital Fund:

As defined in VCF Regulations:

“Venture Capital Fund” means a fund established in the form of a trust or a company

including a body corporate and registered under these regulation which—

a) has a dedicated pool of capital;

b) raised in a manner specified in the regulations; and

c) invests in accordance with the regulations;

As defined in AIF Regulations:

“Venture Capital Fund” means an AIF which invests primarily in unlisted securities of start-

ups, emerging or early-stage venture capital undertakings mainly involved in new products,

new services, technology or intellectual property right based activities or a new business

model;

Additional definitions in AIF regulations:

“Alternative Investment Fund” means any fund established or incorporated in

India in the form of a trust or a company or a limited liability partnership or a body

corporate which-

i. is a privately pooled investment vehicle which collects funds from investors,

whether Indian or foreign, for investing it in accordance with a defined

investment policy for the benefit of its investors; and

Alternate Investment Funds 7

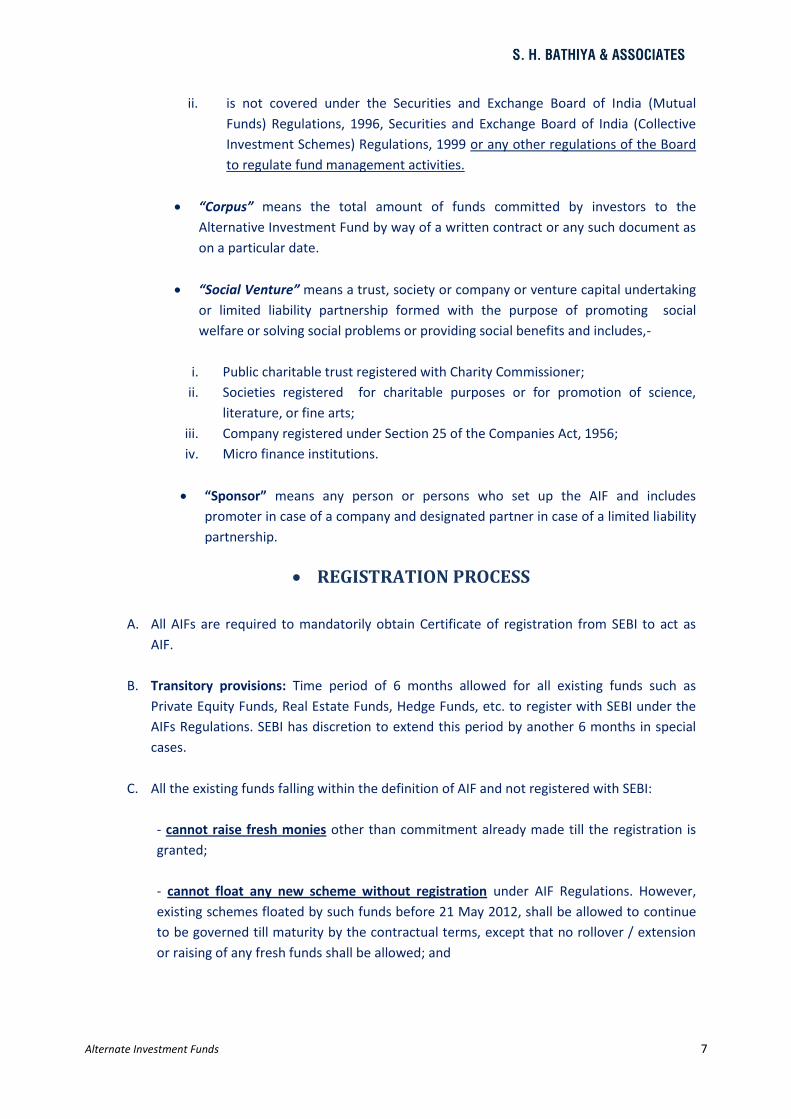

ii. is not covered under the Securities and Exchange Board of India (Mutual

Funds) Regulations, 1996, Securities and Exchange Board of India (Collective

Investment Schemes) Regulations, 1999 or any other regulations of the Board

to regulate fund management activities.

“Corpus” means the total amount of funds committed by investors to the

Alternative Investment Fund by way of a written contract or any such document as

on a particular date.

“Social Venture” means a trust, society or company or venture capital undertaking

or limited liability partnership formed with the purpose of promoting social

welfare or solving social problems or providing social benefits and includes,-

i. Public charitable trust registered with Charity Commissioner;

ii. Societies registered for charitable purposes or for promotion of science,

literature, or fine arts;

iii. Company registered under Section 25 of the Companies Act, 1956;

iv. Micro finance institutions.

“Sponsor” means any person or persons who set up the AIF and includes

promoter in case of a company and designated partner in case of a limited liability

partnership.

REGISTRATION PROCESS

A. All AIFs are required to mandatorily obtain Certificate of registration from SEBI to act as

AIF.

B. Transitory provisions: Time period of 6 months allowed for all existing funds such as

Private Equity Funds, Real Estate Funds, Hedge Funds, etc. to register with SEBI under the

AIFs Regulations. SEBI has discretion to extend this period by another 6 months in special

cases.

C. All the existing funds falling within the definition of AIF and not registered with SEBI:

- cannot raise fresh monies other than commitment already made till the registration is

granted;

- cannot float any new scheme without registration under AIF Regulations. However,

existing schemes floated by such funds before 21 May 2012, shall be allowed to continue

to be governed till maturity by the contractual terms, except that no rollover / extension

or raising of any fresh funds shall be allowed; and

Alternate Investment Funds 8

- seeking registration with SEBI but are not able to comply with all provisions of AIF

Regulations may seek exemption from SEBI from strict compliance with the AIFs

Regulations.

D. Existing SEBI registered VCFs:

- continue to be regulated by the VCF Regulations till the existing fund or scheme managed

by the fund is wound up;

- cannot increase the targeted corpus of the fund or scheme as it stands on 21 May 2012;

- cannot launch any new scheme after 21 May 2012; and

- may seek re-registration under AIF Regulations subject to approval of 2/3 of their

investors by value. The SEBI VCF Regulations are repealed w.e.f. 21 May 2012.

E. The certificate of registration, once granted, shall be valid till the concerned AIF is wound

up.

SPONSOR & MANAGER

A. “Manager” as defined in the AIF Regulations means any person or entity who is appointed by

the Alternative Investment Fund to manage its investments by whatever name called and

may also be same as the sponsor of the Fund.

B. Following are some of the key aspects with respect to role / function of Sponsor & Manager

under the AIFs Regulations:

1. Sponsor or Manager shall have the continuing interest in AIF at least of the following

amount in the form of investment in AIF and such interest shall not be through waiver of

management fees:

For Category I and II AIF For Category III AIF

Lower of: 2.5% of the corpus or INR 50 million

Lower of: 5% of the corpus or INR 100 million

2. Sponsor or Manager shall disclose their investment in the AIF to the investors of AIF.

3. Sponsor or Manager shall appoint a custodian registered with SEBI for safekeeping of

securities if the corpus of AIF is more than INR 5 billion. However, for Category III AIF,

irrespective of the size of the corpus, appointment of custodian is mandatory.

4. Sponsor and Manager of AIF shall act in a fiduciary capacity towards its investors and shall

disclose to the investors, all conflicts of interests as and when they arise or seem likely to

arise.

Alternate Investment Funds 9

5. Any fees ascribed to the Sponsor or Manager and any fees charged to AIF or any investee

company by an associate of the Sponsor or Manager shall be disclosed periodically to the

investor.

INVESTMENT CONDITIONS AND RESTRICTIONS

A. Fund Raising Mechanism:

1. General Conditions:

AIF may raise funds subject to following conditions:

i. Funds may be raised from Indian as well as foreign investors including NRI’s through issue

of units

ii. AIF may form various schemes to raise funds and such schemes shall have minimum

corpus of Rupees 20 crores

iii. Minimum amount of investment from an investor should be at least Rs. 1 crore

Exception: Minimum amount to be Rs. 25 lakhs instead of Rs. 1 crore in case of investment

by employees or directors of AIF or of Manager of the AIF

iv. Manager or Sponsor to have continuing interest in the AIF of at least 2.5% of the corpus or

Rs. 5 crore whichever is less and such interest should be in the form of direct investment

by subscribing to units of the AIF and should not be through waiver of management fees

Exception: In case of Category III AIF, continuing interest should be at least 5% of the

corpus of Rs. 10 Crore viz. doubles the normal requirements.

v. Maximum investors for each scheme is restricted to 1000; alternatively an AIF may have

more than 1000 investors if it has more than one scheme

vi. Funds can be raised only through private placement basis from domestic as well as

international investors however no public issues allowed. This draws a borderline

between AIF CIS and MF which can invite public subscriptions.

2. Fund Raising Procedure:

i. As mentioned earlier, AIF may raise funds by launching various schemes

ii. For each scheme, AIF needs to file placement memorandum or information memorandum

(IM) with SEBI at least 30 days prior to launching the scheme along with requisite fees

Exception: No fees to be paid for launching first scheme.

Alternate Investment Funds 10

iii. IM should contain all material information about the AIF and the Manager and should

contain minimum disclosures as provided in Regulation 11(2) to help investors to take

informed investment decision.

iv. SEBI may give comments on IM within 30 days of filing and AIF shall be duty bound to

incorporate such comments in IM prior to launch of scheme.

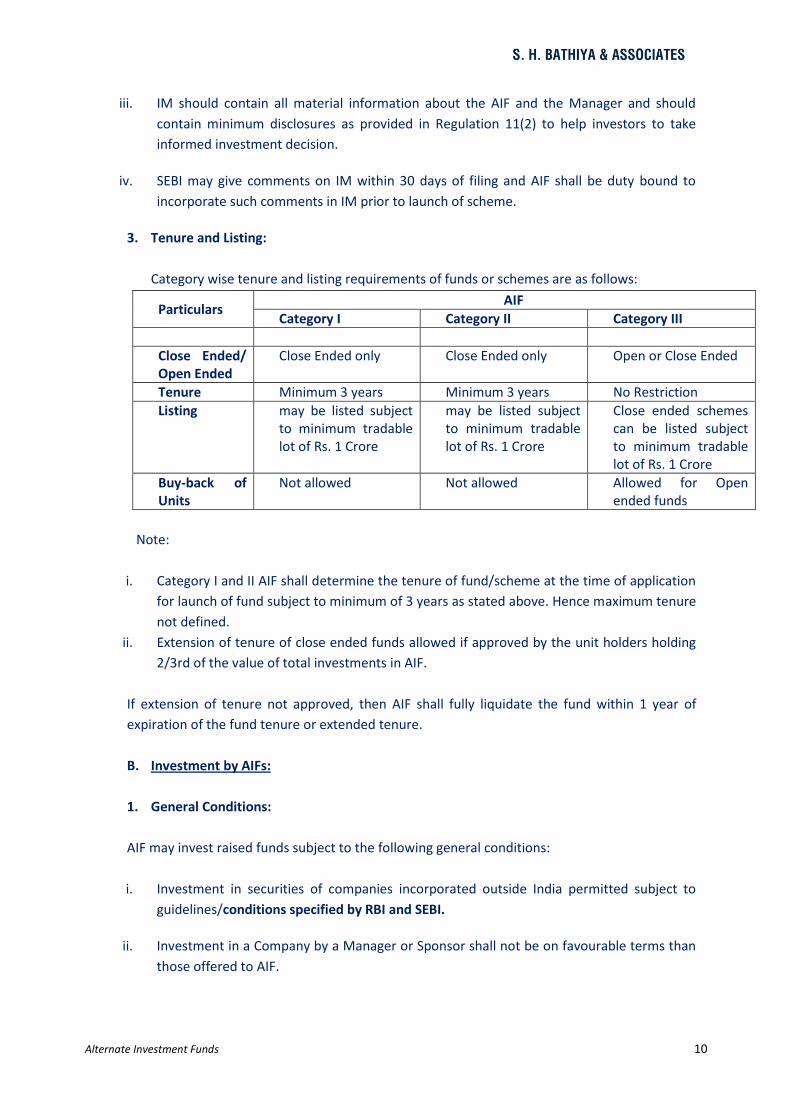

3. Tenure and Listing:

Category wise tenure and listing requirements of funds or schemes are as follows:

Particulars AIF

Category I Category II Category III

Close Ended/ Open Ended

Close Ended only Close Ended only Open or Close Ended

Tenure Minimum 3 years Minimum 3 years No Restriction

Listing may be listed subject to minimum tradable lot of Rs. 1 Crore

may be listed subject to minimum tradable lot of Rs. 1 Crore

Close ended schemes can be listed subject to minimum tradable lot of Rs. 1 Crore

Buy-back of Units

Not allowed Not allowed Allowed for Open ended funds

Note:

i. Category I and II AIF shall determine the tenure of fund/scheme at the time of application

for launch of fund subject to minimum of 3 years as stated above. Hence maximum tenure

not defined.

ii. Extension of tenure of close ended funds allowed if approved by the unit holders holding

2/3rd of the value of total investments in AIF.

If extension of tenure not approved, then AIF shall fully liquidate the fund within 1 year of

expiration of the fund tenure or extended tenure.

B. Investment by AIFs:

1. General Conditions:

AIF may invest raised funds subject to the following general conditions:

i. Investment in securities of companies incorporated outside India permitted subject to

guidelines/conditions specified by RBI and SEBI.

ii. Investment in a Company by a Manager or Sponsor shall not be on favourable terms than

those offered to AIF.

Alternate Investment Funds 11

iii. Maximum investment in an investee company shall be restricted to 25% of the corpus in

case of Category I and II AIF AND in case of Category III AIF it is 10% of the corpus.

iv. Investment in associates not allowed.

Exception: Possible if such investment decision is approved by 75% of the unit holders in

terms of value of their investment in AIF.

v. Till deployment as per investment objective, the un-invested portion of the corpus may be

invested in liquid mutual funds or bank deposits or other liquid assets of higher quality.

vi. AIF may act as Nominated Investor in case of SME companies public offerings whereby it

can enter into an agreement with merchant bankers to subscribe to the issue in case of

under-subscription.

vii. Such other conditions as the SEBI may prescribe from time to time.

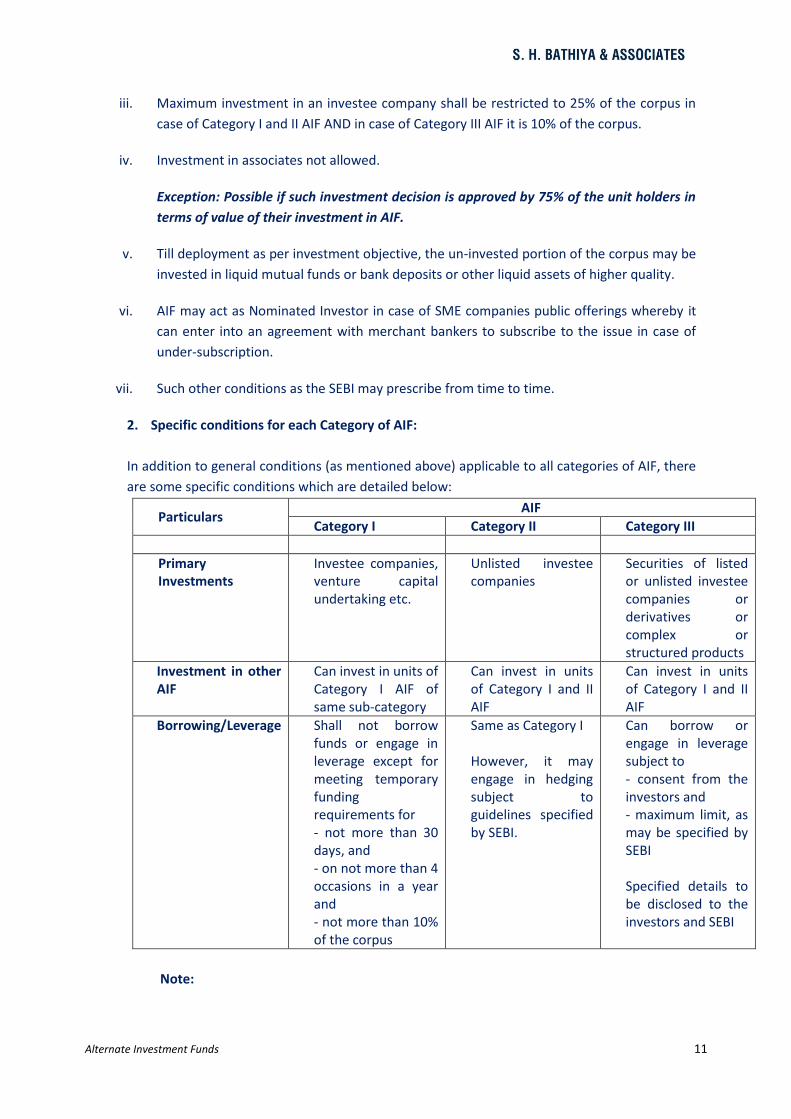

2. Specific conditions for each Category of AIF:

In addition to general conditions (as mentioned above) applicable to all categories of AIF, there

are some specific conditions which are detailed below:

Particulars AIF

Category I Category II Category III

Primary Investments

Investee companies, venture capital undertaking etc.

Unlisted investee companies

Securities of listed or unlisted investee companies or derivatives or complex or structured products

Investment in other AIF

Can invest in units of Category I AIF of same sub-category

Can invest in units of Category I and II AIF

Can invest in units of Category I and II AIF

Borrowing/Leverage Shall not borrow funds or engage in leverage except for meeting temporary funding requirements for - not more than 30 days, and - on not more than 4 occasions in a year and - not more than 10% of the corpus

Same as Category I However, it may engage in hedging subject to guidelines specified by SEBI.

Can borrow or engage in leverage subject to - consent from the investors and - maximum limit, as may be specified by SEBI Specified details to be disclosed to the investors and SEBI

Note:

Alternate Investment Funds 12

i. “Investee Company” means any company, special purpose vehicle or limited liability

partnership or body corporate in which an AIF makes an investment.

ii. Under Category I AIF, there are 4 sub-category funds viz. 1) Venture Capital Funds 2) SME

Fund 3) Social Venture Fund and 4) Infrastructure Fund and for each category there are

certain investment conditions and restrictions intended to serve the objective which each

fund’s nomenclature denotes.

GENERAL OBLIGATIONS

A. AIFs to regularly review policies and procedures and their implementation to ensure

continued appropriateness.

B. The Sponsor or Manager of AIF shall appoint a custodian registered with the Board for

safekeeping of securities if the corpus of the AIF is more than Rs 500 crore (Category III AIF

shall appoint such custodian irrespective of the size of corpus)

C. All AIF shall inform the Board in case of any change in the Sponsor, Manager or

designated partners or any other material change.

D. Prior approval of the Board to be obtained in case of change in control of the AIF,

Sponsor or Manager.

E. Books of accounts of AIF shall be audited annually by a qualified auditor.

CONFLICT OF INTEREST

A. The Sponsor and Manager shall act in a fiduciary capacity and shall disclose all conflicts of

interests to the investors.

B. Manager shall establish and implement written policies and procedures to identify, monitor

and appropriately mitigate conflicts of interest.

C. Managers and Sponsors shall abide by high level principles on avoidance of conflicts of

interest with associated persons, as may be specified by the Board from time to time.

TRANSPARENCY

A. AIFs shall ensure transparency and disclosure of information to investors on the following:

B. Periodical disclosure of financial, risk management, operational, portfolio, and

transactional information regarding fund investments.

C. Any fees ascribed to the Manager or Sponsor; and any fees charged to the AIF or any

investee company by an associate of the Manager or Sponsor.

D. Any inquiries / legal actions by legal or regulatory bodies in any jurisdiction

Alternate Investment Funds 13

E. Any material liability arising during the AIF’s tenure.

F. Any breach of a provision of the placement memorandum or agreement made with the

investor or any other fund documents.

G. Change in control of the Sponsor or Manager or Investee Company

H. Reports to investors at least on an annual basis, within 180 days from the year end,

including the following information, as may be applicable:

1. Financial information of investee companies

2. Material risks and how they are managed which may include concentration risk at fund

level; foreign exchange risk at fund level; leverage risk at fund and investee company

levels; realization risk (i.e. change in exit environment) at fund and investee company

levels; strategy risk (i.e. change in or divergence from business strategy) at investee

company level; reputation risk at investee company level; extra-financial risks, including

environmental, social and corporate governance risks, at fund and investee company

level.

3. Category III AIF shall provide quarterly reports to investors in respect of the above

information within 60 days of end of the quarter:

4. Any significant change in the key investment team

5. Information for systemic risk purposes (including the identification, analysis and mitigation

of systemic risks) to be provided when required by the Board.

VALUATION

A. AIF shall provide to investors a description of its valuation procedure and of the

methodology for valuing assets.

B. Category I and Category II AIFs shall undertake valuation of their investments, at least once

in every six months; by an independent valuer (such period may be enhanced to one year

on approval of at least 75% of the investors by value of their investment in AIF.)

C. Category III AIFs shall ensure that calculation of the net asset value (NAV) is independent

from the fund management function and such NAV shall be disclosed to the investors on

quarterly basis for close ended Funds and on monthly basis for open ended funds.

MAINTENANCE OF RECORDS

A. the assets under the scheme/fund;

B. valuation policies and practices;

C. investment strategies;

D. particulars of investors and their contribution;

Alternate Investment Funds 14

E. Rationale for investments made.

These records shall be maintained for a period of 5 years after the winding up of the fund.

WINDING UP

A. An AIF set up as a trust shall be wound up:

B.

1. when the tenure of the AIF or all schemes launched by AIF, is over; or

2. if it is the opinion of the trustees or the trustee company, as the case may be, that the

AIF be wound up in the interests of investors in the units; or

3. if 75% of the investors by value of their investment in AIF pass a resolution at a meeting

of unit holders that the AIF be wound up; or

4. if the Board so directs in the interests of investors.

5. An AIF set up as a LLP shall be wound up in accordance with the provisions of The

Limited Liability Partnership Act, 2008 on occurrence of events mentioned above in (1)

(a) or (c) or (d)

6. AIF set up as a company shall be wound up in accordance with the provisions of the

Companies Act, 1956 (1 of 1956).

7. AIF set up as a body corporate shall be wound up in accordance with the provisions

of the statute under which it is constituted.

8. The trustees or trustee company or the Board of Directors or designated partners of

AIF, as the case maybe, shall intimate the Board and investors of the circumstances

leading to the winding up.

9. On and from the date of such intimation no further investments shall be made on

behalf of AIF.

10. Within 1 year from the date of intimation the assets shall be liquidated, and the

proceeds accruing to investors shall be distributed to them after satisfying all liabilities.

11. Subject to the conditions, if any, contained in the placement memorandum or

contribution agreement or subscription agreement, as the case may be, in specie

distribution of assets of AIF, shall be made at any time, including on winding up as per

the preference of investors, after obtaining approval of at least 75% of the investors by

value of their investment in AIF.

12. Upon winding up of AIF, the certificate of registration shall be surrendered to the

Board.

Alternate Investment Funds 15

TAX “PASS THROUGH” FOR AIFS

The SEBI press release states that SEBI will work with the central government to obtain “pass

through” treatment for AIFs for tax purposes. This is an interesting proposal because under the

existing income tax laws, only “VCFs registered with SEBI” are eligible for this tax treatment.

However, as per explanation under Regulation 3 (4) (a), only Category I funds shall be treated as

venture capital funds for the purpose of Section 10 (23FB) of the Income-tax Act, 1961. Therefore,

if the central government agrees to provide tax “pass through” treatment to all AIFs, which will

be a very encouraging move and would further facilitate fund investments in general.

The AIF Regulations now seemingly curtail that benefit and limit it only to Category I AIFs. If there

is significant delay in passing the necessary amendments to the Income Tax Act to effect “pass

through” status for all AIFs (and similar kind of thing has happened before – with LLPs, for

example, when it took more than a year to get clarity on the tax status of LLPs), that could

adversely affect investment strategies and structuring of AIFs in the interim.

CONCLUSION

India as a nation has been a witness to plenty of varied investment schemes in different shades of

grey. The AIF Regulations are a step in the right direction as they bring transparency around the

issue of regulation of private pools of capital that are raised locally for deployment by various types

of investment funds. It will help in monitoring the unregulated funds; encourage formation of new

capital and investor protection. It will enable several variety of funds that were not possible in the

past like social capital funds, real estate funds, hedge funds etc. AIF Regulations possess several

features like investment strategy, disclosure of periodic information to investors, valuation

procedure, audit of fund, dispute resolution, winding up of funds etc. These comprehensive

Regulations would surely bring greater clarity to the market and the investors and its

comprehensive nature will bring several investment entities under the watchdog that were hitherto

unregulated by SEBI. Also, the investments in AIF can be used as a tool to reduce investment risk

through diversification thereby helping the investors in the market. The classification between the

three categories is also a socially-desirable change.

ABBREVIATIONS & DISCLAIMER:

Sr. No. Abbreviations

1 AIF Alternative Investment Funds

2 AIFs Regulations SEBI (Alternative Investment Funds) Regulations, 2012

3 INR Indian Rupees

4 LLP Limited Liability Partnership

5 CIS Scheme SEBI (Collective Investment Scheme), Regulations 1999

Alternate Investment Funds 16

6 ESOP Employee Stock Option Plan

7 SME Small, Micro and Medium Enterprise

8 QIB Qualified Institutional Buyers

9 CBLO Collaterized Borrowing and Lending Obligation

10 NAV Net Asset Value

11 NRI Non Resident Indian

12 VCF Venture Capital Fund

13 VCF Regulations SEBI (Venture Capital Funds) Regulations, 1996

14 SEBI Securities & Exchange Board of India

15 HNIs High Net-worth Individuals/Investors

16 GoI Government of India

17 MF Mutual Fund

Alternate Investment Funds 17

DISCLAIMER

The document provides general information and guidance as on date of preparation and does not express views or expert

opinions of S. H. Bathiya & Associates as a Firm. The research paper is meant for general guidance and no responsibility for

loss arising to any person acting or refraining from acting as a result of any material contained in this paper will be accepted

by S. H. Bathiya & Associates. It is recommended that professional advice be sought based on the specific facts and

circumstances. This research paper does not substitute the need to refer to the original pronouncements. Further, this

document may contain material that is confidential, privileged and product for the sole use of the intended recipient. Any

review, reliance or distribution by others or forwarding without express permission is strictly prohibited. If you are not the

intended recipient, please contact the sender and delete all copies. If you have received this communication in error, or if you

or your employers do not consent to email messages of this kind, please notify us immediately by responding to our email

and then delete it from your system. No liability is accepted for any harm that may be caused to your systems or data by this

message. This paper is for the in-house firm members, Clients and request-recipients of S. H. Bathiya & Associates only. In

case this mail doesn't concern you, please unsubscribe from mailing list. Errors and omissions expected. The views and

compilations does not necessarily translate into views of the Firm.

The source of this research is inclusive of various publicly available information, data and statistics from various sources

including the internet. Reliability of these sources of information and their copyright protections has not been independently

verified by us.

Mumbai Offices:

2, Tardeo AC Market, 4th Floor, Tardeo Road, Mumbai - 400 034. Tel. 022-4355 8000

A-2\D, Haridwar, Mathuradas Road, Kandivli (W), Mumbai - 400 067. Tel. 022-4275 8000

202-A, Harmony, Court Naka, Station Road, Thane (W) - 400 601. Tel. 022-65620111

Gujarat Office:

304, 3rd Floor, Manubhai Tower, ‘C’ Block, Sayajiganj, Vadodara – 390005. Tel. 0265-3074503

www.shbathiya.com