alternative capital solutions for reinsurance · alternative capital solutions for reinsurance...

TRANSCRIPT

Alternative Capital Solutions for Reinsurance

Kevin Gomes, Thomas Cherian & Sharanjit Paddam

© Taylor Fry and Thomas Cherian

This presentation has been prepared for the Actuaries Institute 2014 General Insurance Seminar. The Institute Council wishes it to be understood that opinions put forward herein are not necessarily those of the Institute and the Council is not

responsible for those opinions.

Outline • Introduction • What is alternative capital?

– Types of Alternative Capital

– Recent Transactions – Case Study – Triggers

• The alternative RI capital market – Amounts issued

– By Trigger type – By Perils and cedants

• Implications for Australia? • Drivers of supply • Drivers of demand • Obstacles to growth in

Australia • Future?

3

Introduction • Our presentation

– Draws on existing literature • Our qualifications

– Not experts, just interested • Rationale for topic

– Recent massive growth – Implications for Australia?

4

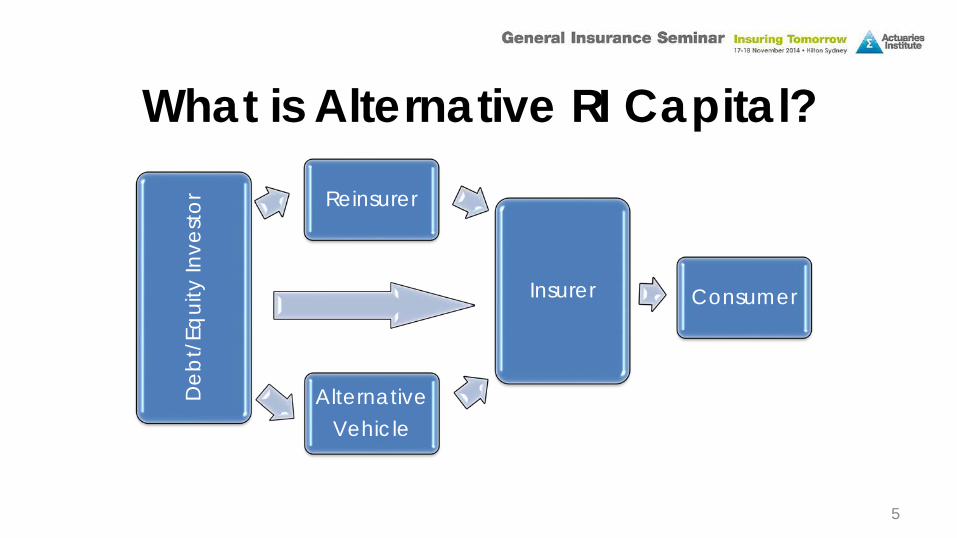

What is Alternative RI Capital? D

ebt/

Equi

ty In

vest

or Reinsurer

Insurer Consumer

Alternative Vehicle

5

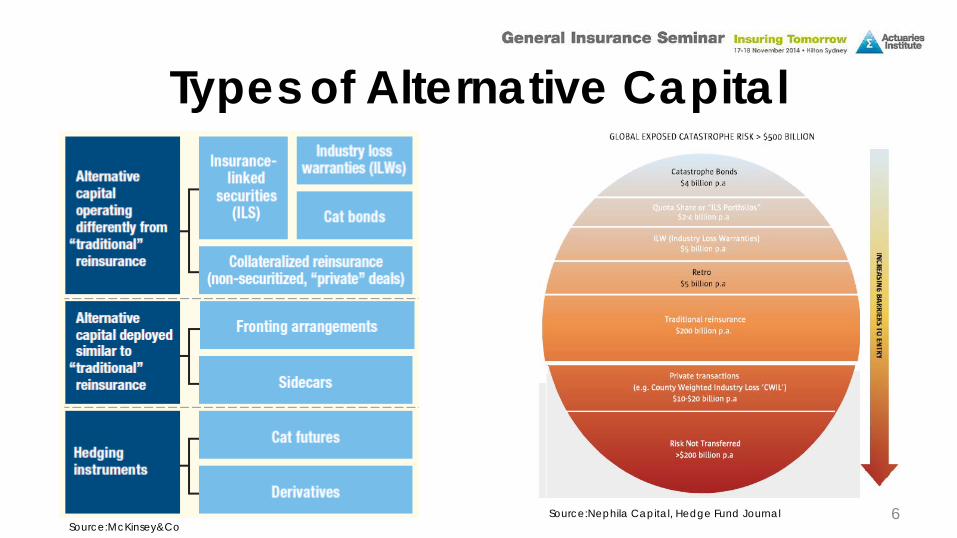

Types of Alternative Capital

Source:McKinsey&Co Source:Nephila Capital, Hedge Fund Journal 6

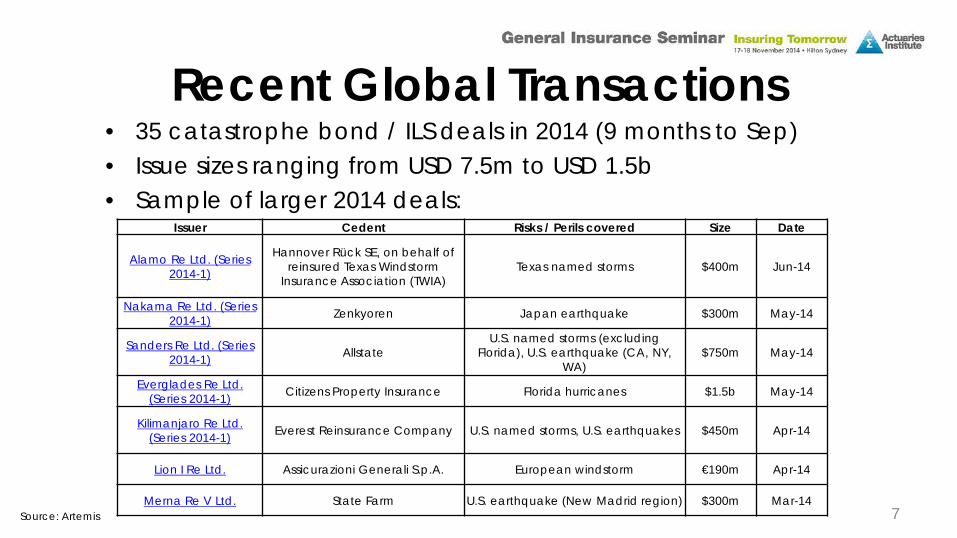

Recent Global Transactions • 35 catastrophe bond / ILS deals in 2014 (9 months to Sep) • Issue sizes ranging from USD 7.5m to USD 1.5b • Sample of larger 2014 deals:

Issuer Cedent Risks / Perils covered Size Date

Alamo Re Ltd. (Series 2014-1)

Hannover Rück SE, on behalf of reinsured Texas Windstorm

Insurance Association (TWIA) Texas named storms $400m Jun-14

Nakama Re Ltd. (Series 2014-1) Zenkyoren Japan earthquake $300m May-14

Sanders Re Ltd. (Series 2014-1) Allstate

U.S. named storms (excluding Florida), U.S. earthquake (CA, NY,

WA) $750m May-14

Everglades Re Ltd. (Series 2014-1) Citizens Property Insurance Florida hurricanes $1.5b May-14

Kilimanjaro Re Ltd. (Series 2014-1) Everest Reinsurance Company U.S. named storms, U.S. earthquakes $450m Apr-14

Lion I Re Ltd. Assicurazioni Generali S.p.A. European windstorm €190m Apr-14

Merna Re V Ltd. State Farm U.S. earthquake (New Madrid region) $300m Mar-14 Source: Artemis 7

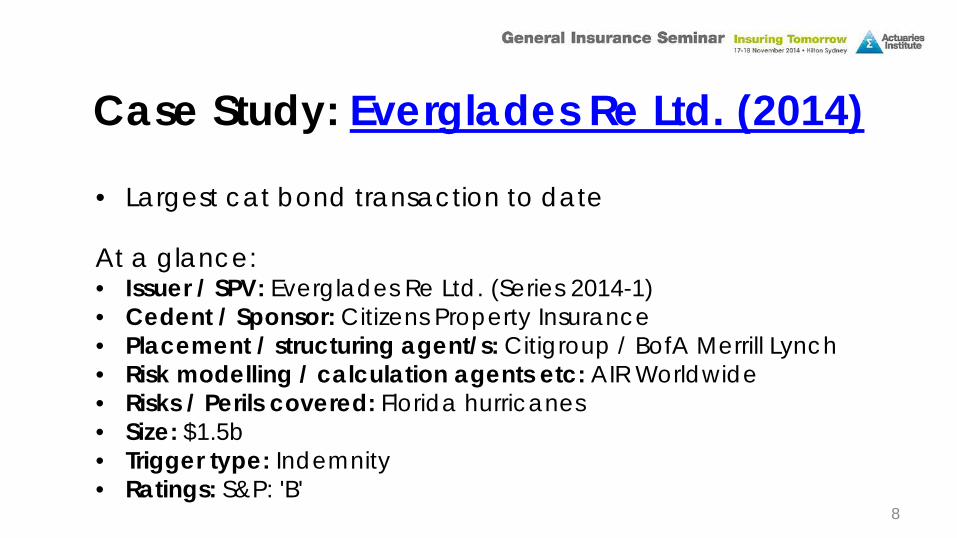

Case Study: Everglades Re Ltd. (2014)

• Largest cat bond transaction to date At a glance: • Issuer / SPV: Everglades Re Ltd. (Series 2014-1) • Cedent / Sponsor: Citizens Property Insurance • Placement / structuring agent/s: Citigroup / BofA Merrill Lynch • Risk modelling / calculation agents etc: AIR Worldwide • Risks / Perils covered: Florida hurricanes • Size: $1.5b • Trigger type: Indemnity • Ratings: S&P: 'B'

8

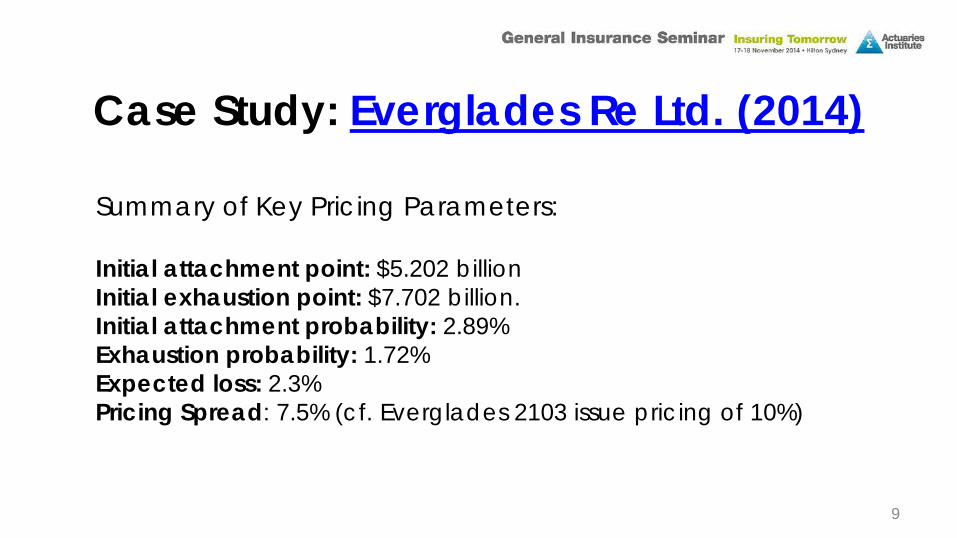

Case Study: Everglades Re Ltd. (2014)

Summary of Key Pricing Parameters: Initial attachment point: $5.202 billion Initial exhaustion point: $7.702 billion. Initial attachment probability: 2.89% Exhaustion probability: 1.72% Expected loss: 2.3% Pricing Spread: 7.5% (cf. Everglades 2103 issue pricing of 10%)

9

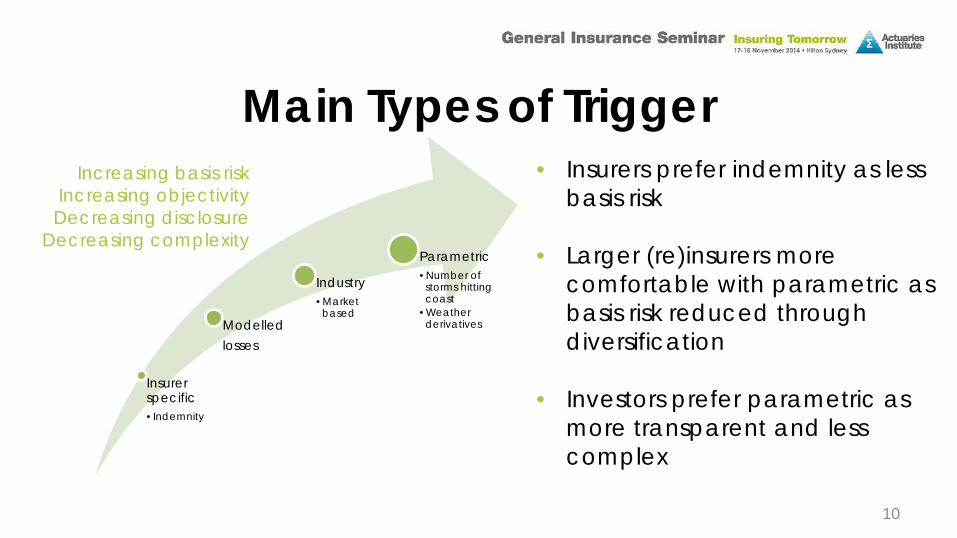

Main Types of Trigger

Insurer specific •Indemnity

Modelled losses

Industry •Market

based

Parametric •Number of

storms hitting coast

•Weather derivatives

• Insurers prefer indemnity as less basis risk

• Larger (re)insurers more comfortable with parametric as basis risk reduced through diversification

• Investors prefer parametric as more transparent and less complex

Increasing basis risk Increasing objectivity Decreasing disclosure

Decreasing complexity

10

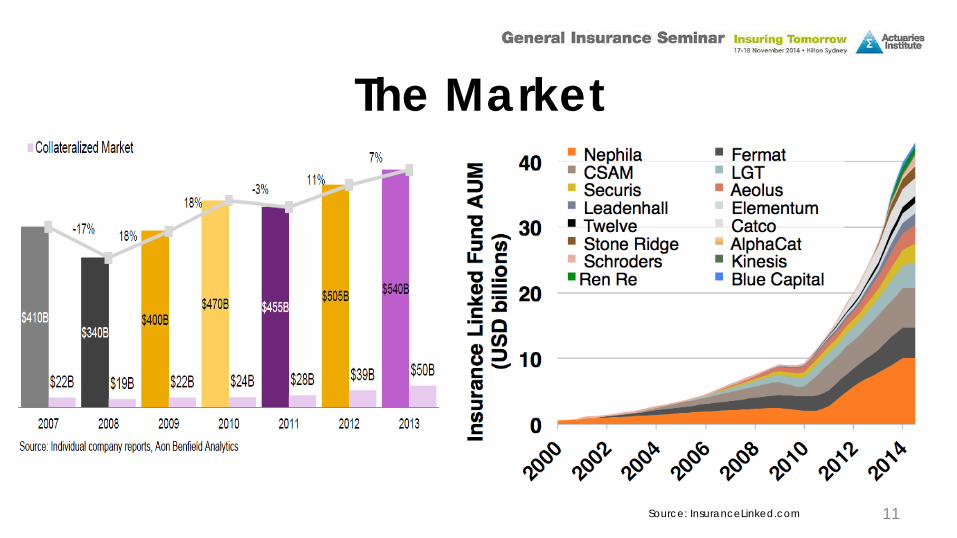

The Market

Source: InsuranceLinked.com 11

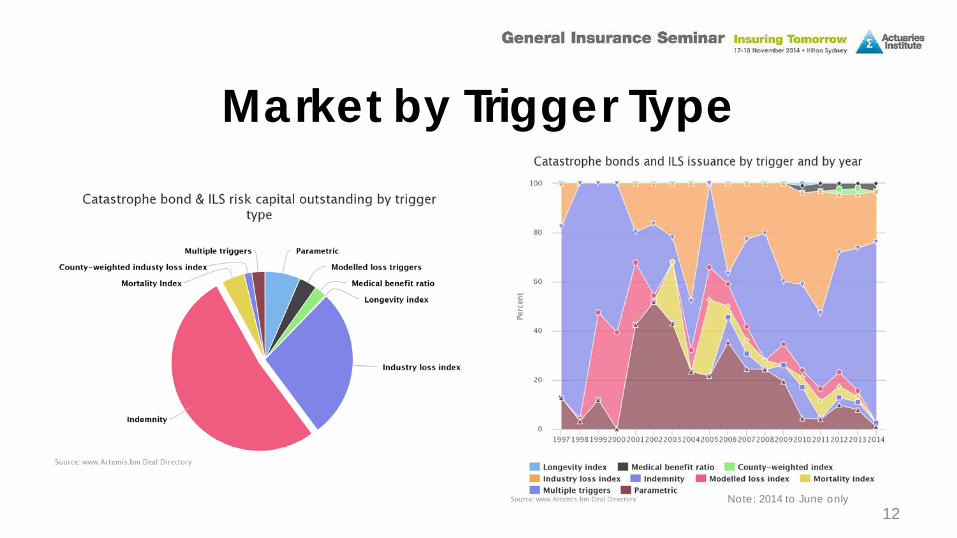

Market by Trigger Type

Note: 2014 to June only 12

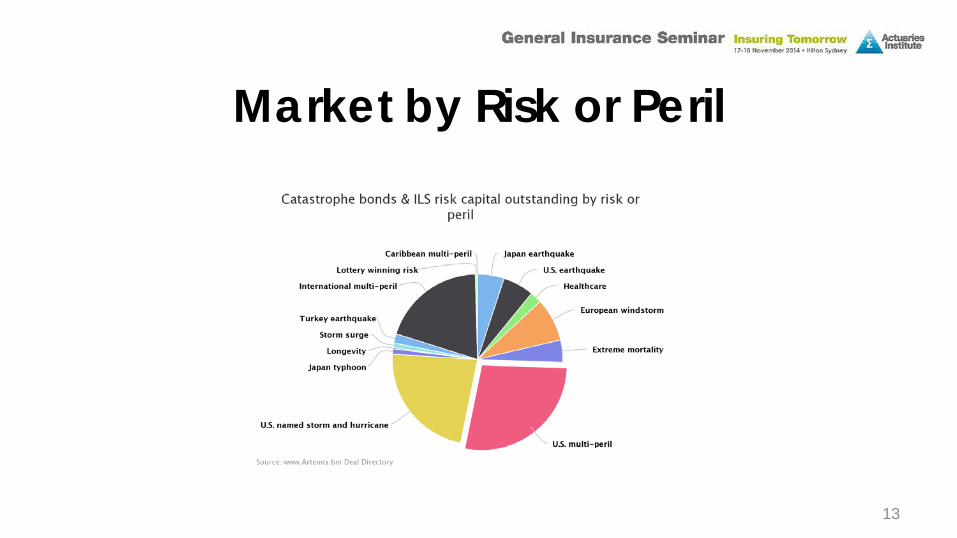

Market by Risk or Peril

13

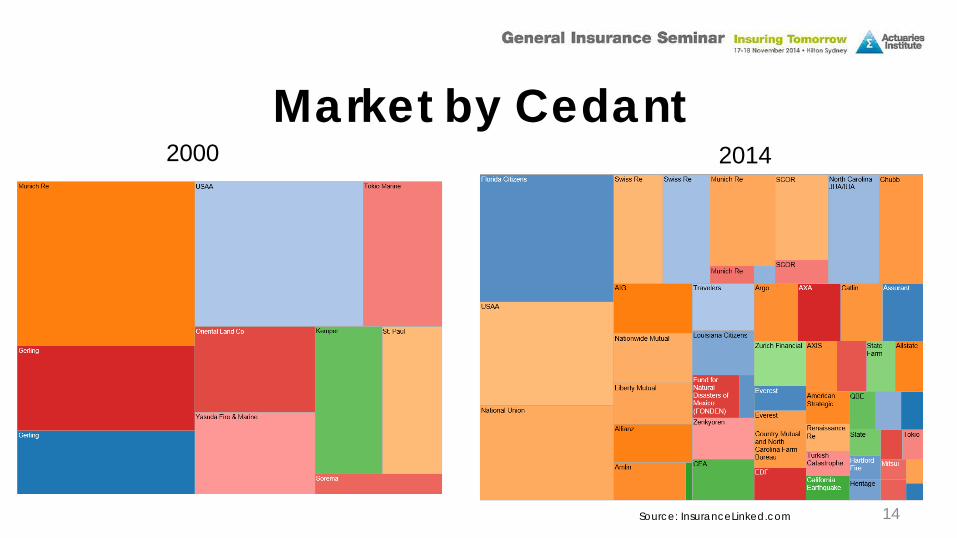

Market by Cedant 2000

Source: InsuranceLinked.com

2014

14

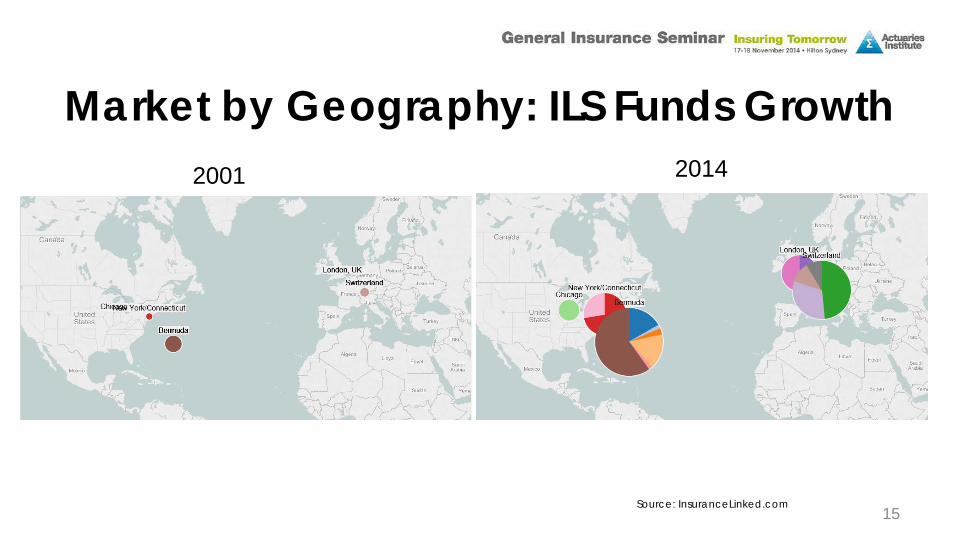

Market by Geography: ILS Funds Growth 2001 2014

Source: InsuranceLinked.com 15

Implications for Australia? • Mostly secondary effects • Increase in alternative reinsurance capital, giving

increased overall RI capacity, giving cheaper traditional reinsurance rates

• Spill-over into casualty as well as property • Longer term could lead to softening of direct

premium rates as capacity chases risk • Potential opportunities for Australian investors • (Lesser impact from lack of diversification benefits for

traditional reinsurers) 16

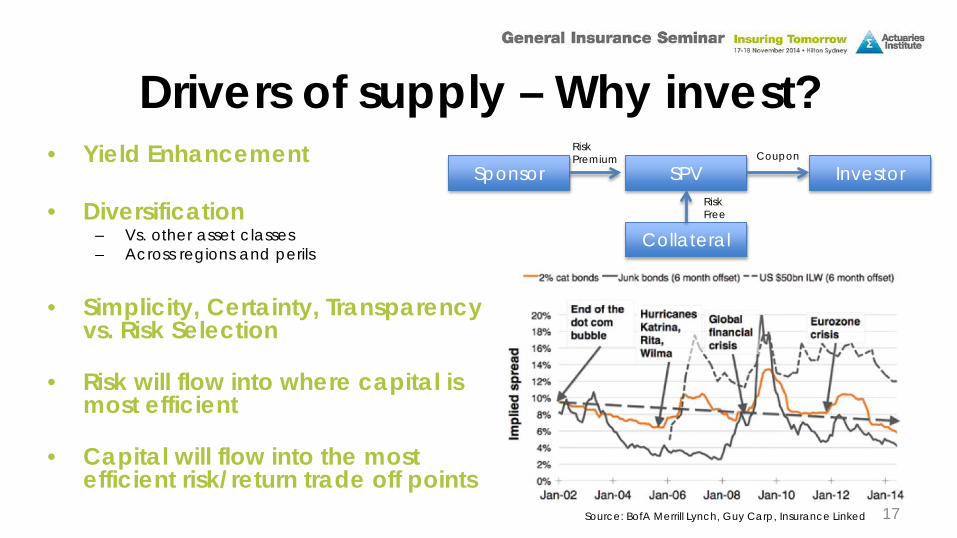

Drivers of supply – Why invest? • Yield Enhancement

• Diversification

– Vs. other asset classes – Across regions and perils

• Simplicity, Certainty, Transparency vs. Risk Selection

• Risk will flow into where capital is most efficient

• Capital will flow into the most efficient risk/return trade off points Source: BofA Merrill Lynch, Guy Carp, Insurance Linked 17

Sponsor SPV Investor

Collateral

Risk Free

Coupon Risk Premium

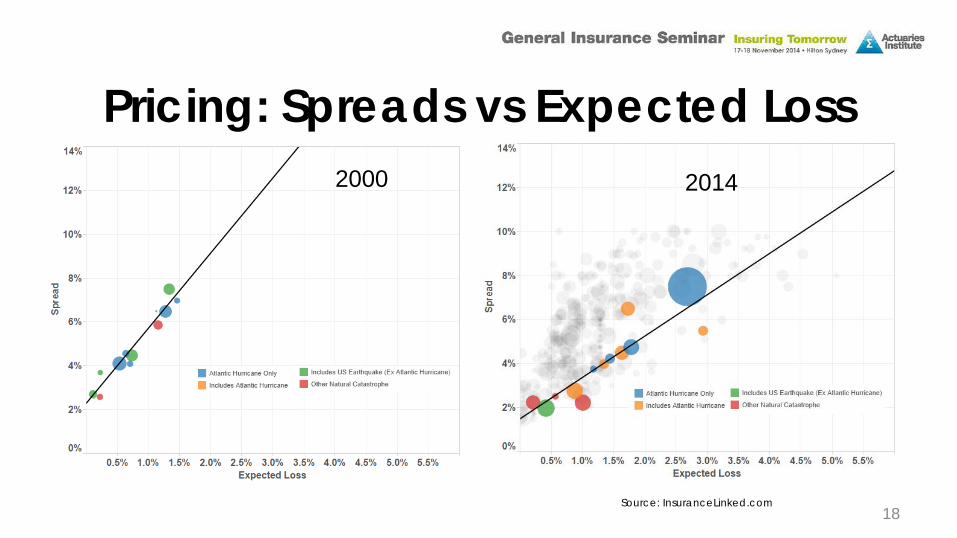

Pricing: Spreads vs Expected Loss

Source: InsuranceLinked.com

2014 2000

18

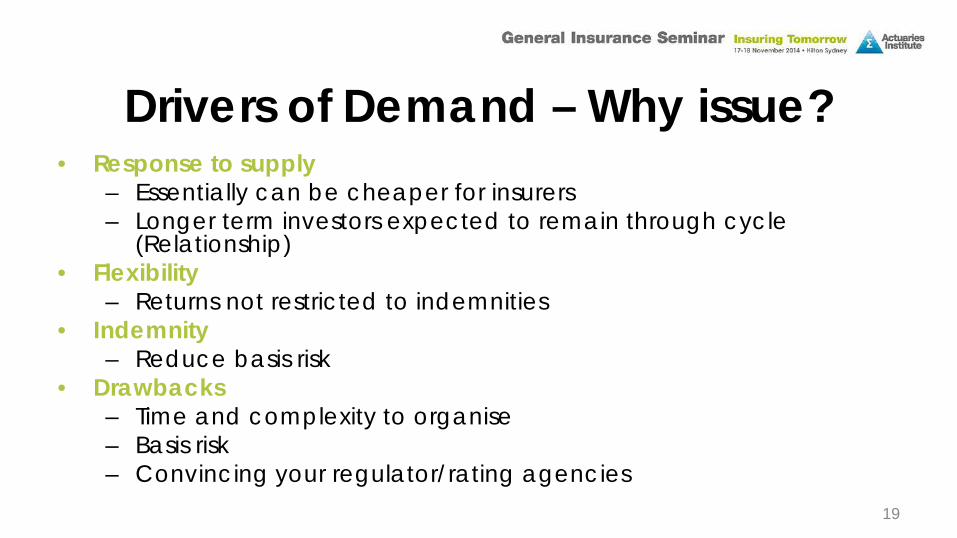

Drivers of Demand – Why issue? • Response to supply

– Essentially can be cheaper for insurers – Longer term investors expected to remain through cycle

(Relationship) • Flexibility

– Returns not restricted to indemnities • Indemnity

– Reduce basis risk • Drawbacks

– Time and complexity to organise – Basis risk – Convincing your regulator/rating agencies

19

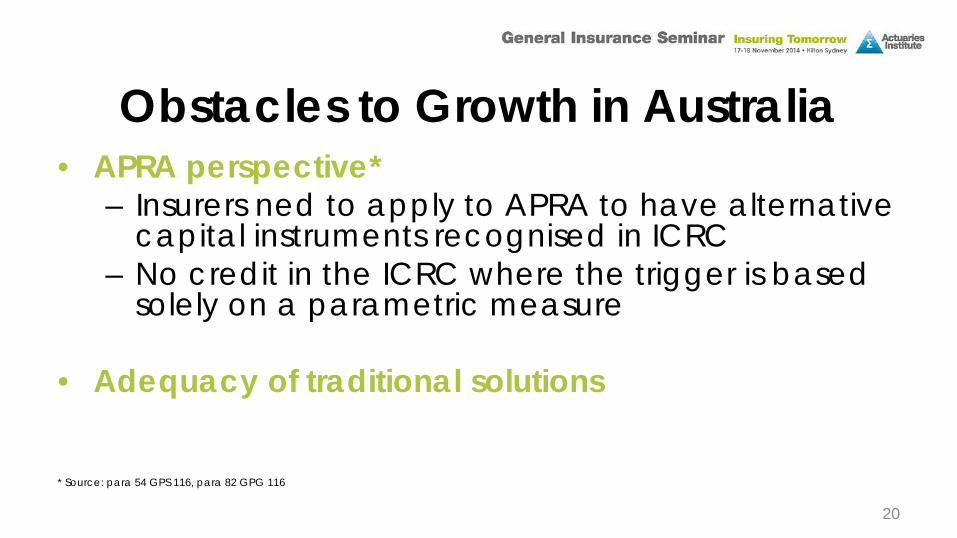

Obstacles to Growth in Australia • APRA perspective*

– Insurers ned to apply to APRA to have alternative capital instruments recognised in ICRC

– No credit in the ICRC where the trigger is based solely on a parametric measure

• Adequacy of traditional solutions

* Source: para 54 GPS 116, para 82 GPG 116

20

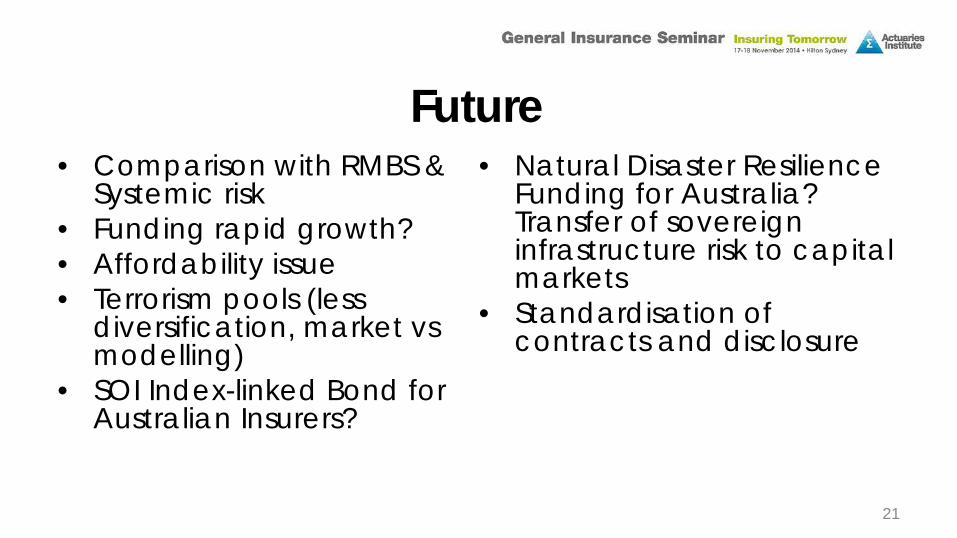

Future • Comparison with RMBS &

Systemic risk • Funding rapid growth? • Affordability issue • Terrorism pools (less

diversification, market vs modelling)

• SOI Index-linked Bond for Australian Insurers?

• Natural Disaster Resilience Funding for Australia? Transfer of sovereign infrastructure risk to capital markets

• Standardisation of contracts and disclosure

21