al-ijarah thumma al-bay (aitab)

DESCRIPTION

TRANSCRIPT

AL IJARAH AND AL IJARAH THUMMA AL

BAI’ (AITAB)(MOTOR VEHICLE

FINANCING)SITI MUNIRAH ABD WAHAB

NUR WIRDA AHMED

AL IJARAH Ijarah is an Arabic term with origin in

Islamic,meaning to give something on a rental basis or wages.It is Islamic alternative to conventional leasing. Generally, Ijarah concept means selling benefit or use or service for a fixed price or wage.

Under this concept, the Bank makes available to the customer the use of service of assets / equipments such as plant, office automation,motor vehicle for a fixed period and price.Ijarah gives the Lessee the right to access the equipment on payment of the first installment. This is important as it is the access and use (and not ownership) of equipment that generates income.

Ijarah is used for two different situation:

1)Ijarah ‘Amal

It means contract between Employer(Mustajir) and Employee(Ajir) and wages((Ujrah). This type of ijarah include every transaction where the service of a person are hired by someone else and the wages is for effort o skill used.

For example : ABC Islamic Bank hires Encik Mansur as a product manager on a monthly salary of RM7000.So that ABC Islamic Bank is mustajir, Encik Mansur is ajir and RM7000 is ujrah.

Potongan ayat Al-Quran berkaitan Al-Ijarah

Al-Kahfi: 77

Artinya : ”Maka keduanya berjalan; hingga tatkala keduanya sampai kepada penduduk

suatu negeri, mereka minta dijamu kepada penduduk negeri itu, tetapi penduduk negeri itu tidak mau menjamu mereka, kemudian keduanya mendapatkan dalam negeri itu dinding rumah yang hampir roboh, maka Khidhr menegakkan dinding itu. Musa berkata: Jikalau kamu mau, niscaya kamu mengambil upah untuk itu.” (QS. 18:77)

Tafsir Surat Al kahfi menceritakan tentang Musa dan sahabatnya Khidir, keduanya

berkelana setelah sebelumnya mencapai kesepakatan untuk bersahabat. Khidir mensyaratkan agar Musa yang memulai menanyakan sesuatu yang ganjil baginya, sebelum Khidir menerangkan dan menjelaskannya., setelah dua kali perjalanan mereka sampai pada negeri Elia atau Li’ama atau Bakhla, namun penduduk negeri itu menolak untuk menjamu mereka. Di negeri itu pula mereka mendapati ada sebuah rumah yang hampir roboh. Lalu Khidir menegakkannya kembali. Musa kemudian mengatakan kepada Khidir untuk meminta upah kepada penduduk negeri atas perbuataanya telah menegakkan rumah tersebut, apalagi setelah penduduk negeri itu sama sekali tidak menjamu mereka.

Ayat ini dapat dijadikan rujukkan bahawa manusia dapat meminta upah atas pekerjaan yang telah dilakukan.

Hadist Rasulullah SAW

Hadis riwayat Ibnu Majah dari Ibnu Umar, bahawa Nabi Muhammad saw. Bersabda :

Artinya : Berikanlah upah pekerja sebelum keringatnya kering.

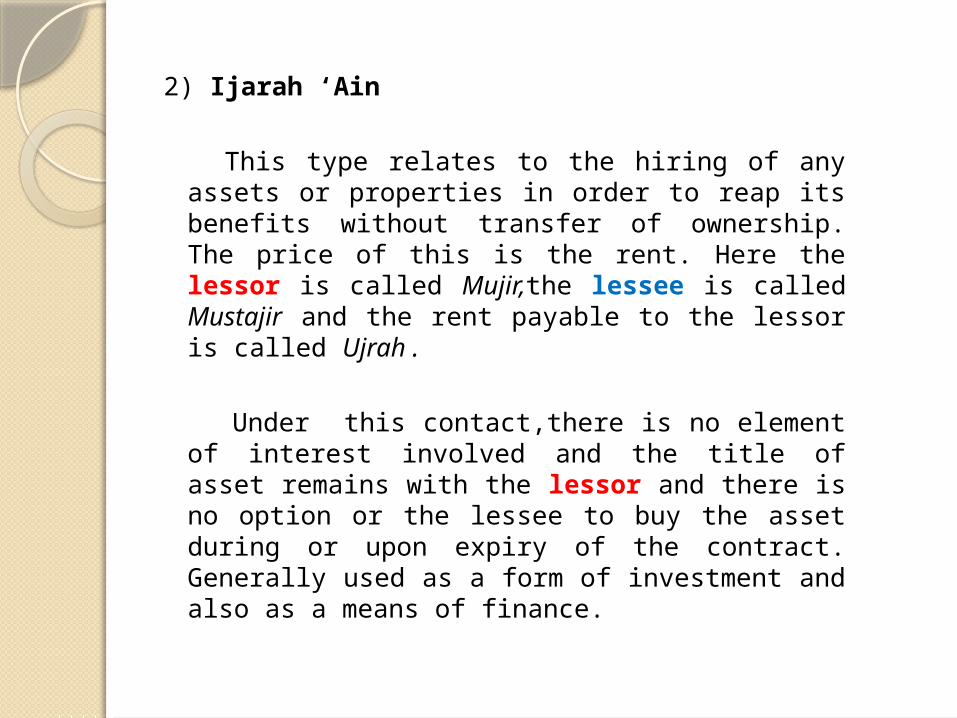

2) Ijarah ‘Ain

This type relates to the hiring of any assets or properties in order to reap its benefits without transfer of ownership. The price of this is the rent. Here the lessor is called Mujir,the lessee is called Mustajir and the rent payable to the lessor is called Ujrah .

Under this contact,there is no element of interest involved and the title of asset remains with the lessor and there is no option or the lessee to buy the asset during or upon expiry of the contract. Generally used as a form of investment and also as a means of finance.

Hadis riwayat Abu Daud dari Saad bin Abi Waqqash, bahawa Nabi Muhammad saw. Bersabda:

Artinya : Kami pernah menyewakan tanah dengan (bayaran) hasil pertaniannya, maka Rasulullah melarang kami melakukan hal tersebut dan memerintahkan agar kami menyewakannya dengan emas atau perak.

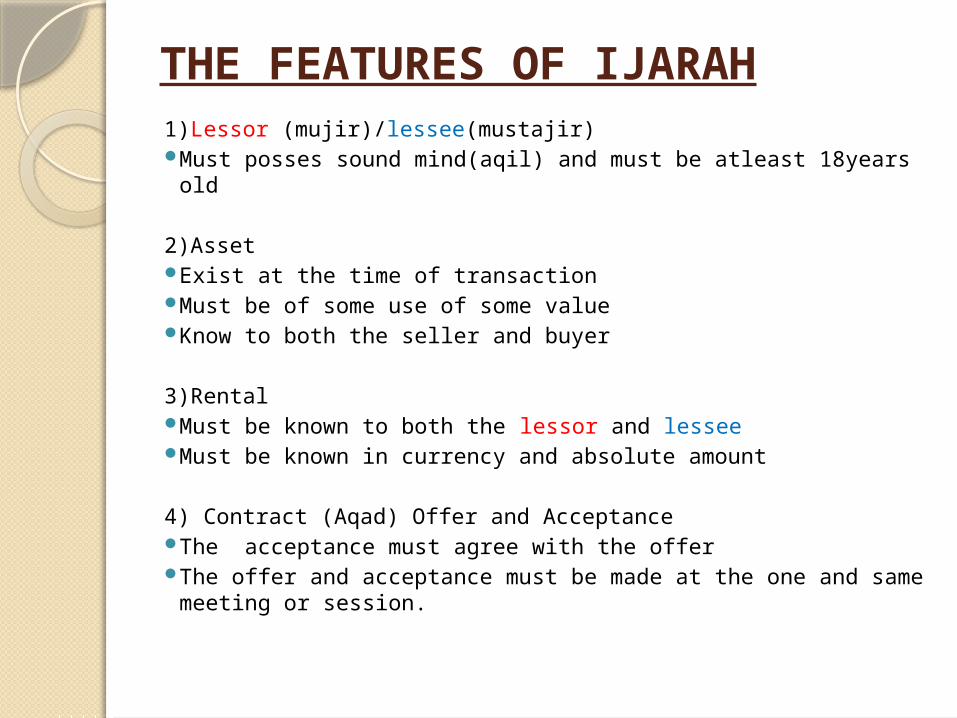

THE FEATURES OF IJARAH1)Lessor (mujir)/lessee(mustajir) Must posses sound mind(aqil) and must be atleast 18years old

2)Asset Exist at the time of transaction Must be of some use of some value Know to both the seller and buyer

3)Rental Must be known to both the lessor and lessee Must be known in currency and absolute amount

4) Contract (Aqad) Offer and Acceptance The acceptance must agree with the offer The offer and acceptance must be made at the one and same

meeting or session.

AL-IJARAH THUMMA AL BAI’(AITAB).

The Islamic Concept of البيع ثم refers to Lease إجارةor Hire or Rent ending with the Purchase. AITAB comparies two contracts, Ijarah (leasing) contract to be followed by a bai’ (sale) contract. Parties enter into contracts that come into effect serially, to form a complete lease/ buyback transaction. The first contract is an Ijarah that outlines the terms for leasing or renting over a fixed period, and the second contract is a Bai that triggers a sale or purchase once the term of the Ijarah is complete.

Consequency, two major contracts of Islamic hire

purchase were formed as new modes financing namely Al Ijarah Thumma Al Bai (a contract of leasing ending with sale) or Al Ijarah Muntahiya Bittamlik (a contract of leasing ending with ownership). Widely adopted as an instrument to be in motor vechicle financing and Bank Islam was the first bank launch AITAB in Malaysia.

For example, in a car financing facility, Pak Samad (lessee) enters into the first contract and leases the car from the owner (lessor) at an agreed amount over a specific period. When the lease period expires, the second contract comes into effect, which enables the lessee to purchase the car at an agreed to price.

Akad ini terdapat dua keadaan iaitu Harus dan Haram

1. Haram

Apabila berlaku dua akad berbeza untuk satu barang pada masa yang sama / secara serentak

2. Harus

Apabila berlaku dua akad secara berasingan, pada masa berlainan contohnya pemeteraian akad jual beli dilakukan selepas selesai akad sewa, atau perjanjian pertukaran hak milik dilakukan di akhir penyewaan

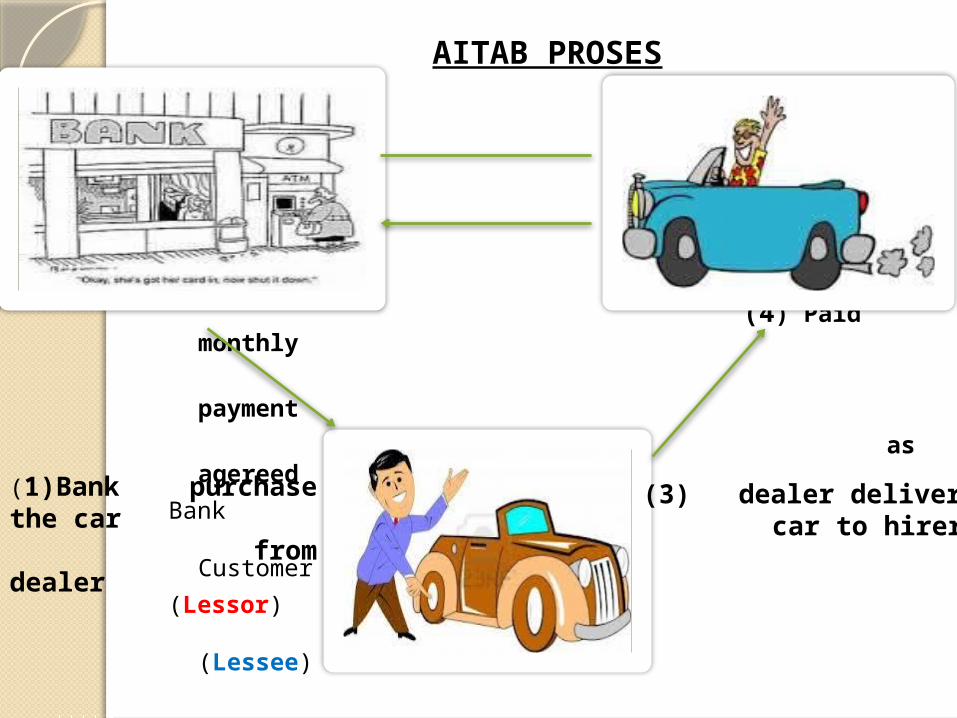

AITAB PROSES

(2) bank hirer car

to customer

(4) Paid monthly

payment

as agereed

Bank Customer

(Lessor) (Lessee)

Dealer

(1)Bank purchase the car from dealer

(3) dealer deliver car to hirer

Under AITAB bank has an authority over the leased asset, if the customer defaulted,bank can take an action against him and repossess the asset. If customer constantly pays and them satisfies all required payment,the bank will sell the asset to him at the end of the agreement

THE ELEMENTS OF AITAB1)Lessor (mujir)/lessee(mustajir) Must posses sound mind(aqil) and must be atleast 18years

old

2)Asset Exist at the time of transaction Must be of some use of some value Know to both the seller and buyer

3)Rental Must be known to both the lessor and lessee Must be known in currency and absolute amount

4) Contract (Aqad) Offer and Acceptance The acceptance must agree with the offer The offer and acceptance must be made at the one and

same meeting or session.

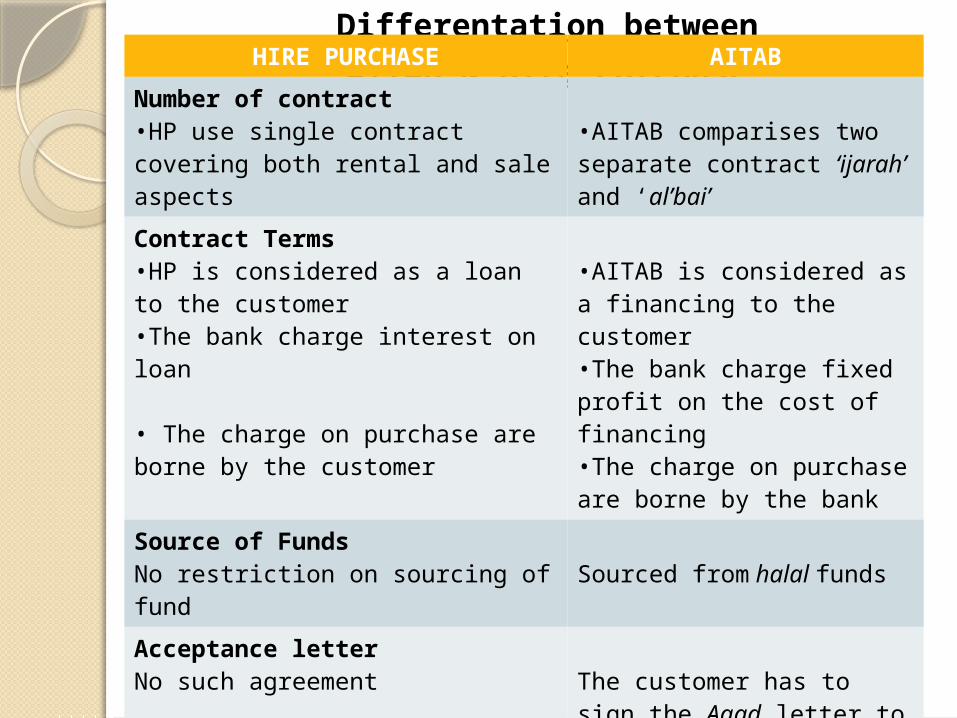

Differentation between AITAB & Hire Purchase

HIRE PURCHASE AITAB

Number of contract•HP use single contract covering both rental and sale aspects

•AITAB comparises two separate contract ‘ijarah’ and ‘al’bai’

Contract Terms•HP is considered as a loan to the customer•The bank charge interest on loan

• The charge on purchase are borne by the customer

•AITAB is considered as a financing to the customer•The bank charge fixed profit on the cost of financing•The charge on purchase are borne by the bank

Source of FundsNo restriction on sourcing of fund Sourced from halal funds

Acceptance letterNo such agreement The customer has to sign

the Aqad letter to denote the offer and acceptance of transaction.

InsuranceUsing conventional Using takaful

APPLICATION ON SEVERAL BANKS IN MALAYSIA

Dari perspektif produk perbankan Islam. Ia boleh dilihat dalam dua bentuk seperti berikut :-

i. Ijarah secara operasi (Operating lease)

ii. Pembiayaan secara Ijarah (Financial lease)

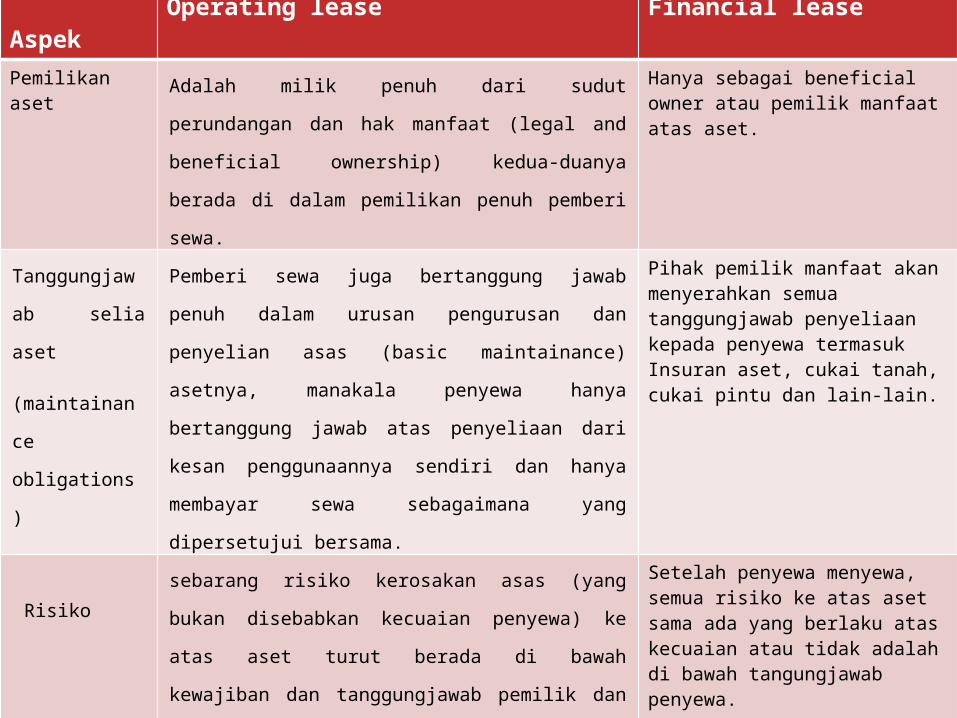

Aspek Operating lease Financial leasePemilikan aset Adalah milik penuh dari sudut perundangan

dan hak manfaat (legal and beneficial

ownership) kedua-duanya berada di dalam

pemilikan penuh pemberi sewa.

Hanya sebagai beneficial owner atau pemilik manfaat atas aset.

Tanggungjaw

ab selia aset

(maintainanc

e obligations)

Pemberi sewa juga bertanggung jawab penuh

dalam urusan pengurusan dan penyelian asas

(basic maintainance) asetnya, manakala

penyewa hanya bertanggung jawab atas

penyeliaan dari kesan penggunaannya sendiri

dan hanya membayar sewa sebagaimana yang

dipersetujui bersama.

Pihak pemilik manfaat akan menyerahkan semua tanggungjawab penyeliaan kepada penyewa termasuk Insuran aset, cukai tanah, cukai pintu dan lain-lain.

Risikosebarang risiko kerosakan asas (yang bukan

disebabkan kecuaian penyewa) ke atas aset

turut berada di bawah kewajiban dan

tanggungjawab pemilik dan bukannya penyewa,

atas sebab itu, pemilik akan mengambil Takaful

ke atas aset.

Setelah penyewa menyewa, semua risiko ke atas aset sama ada yang berlaku atas kecuaian atau tidak adalah di bawah tangungjawab penyewa.

Penamatan • Boleh ditamatkan pada bila-bila masa

dengan redha kedua belah pihak, tanpa

sebarang pampasan atau jumlah sewa

tertunggak (bergantung kepada terma

sewaan),

• Selepas penamatan kontrak, aset akan kekal

di bawah milik pemberi sewa seperti biasa.

· Boleh ditamatkan tetapi

pihak penyewa mestilah

membayar semua sewaan

tertunggak secara sekaligus

· Aset sesudah itu akan

menjadi milik penyewa

secara sepenuhnya.

This facility is based on the concept of Al-Ijarah Thumma Al-Bai or hire purchase contract.

Under the Shariah principles of Ijarah (Lease) and Bai' (Sale), firstly the Bank will purchase a vehicle required by a customer from a dealer / third party and subsequently lease it out to the customer for a certain period agreed by both the bank and the customer subject to terms and conditions.

Upon completion of the lease period, the Bank will sell the vehicle to the customer at an agreed price. MHP is governed by Hire Purchase Act 1967.

FEATURES

Financing based on the contract of Al-Ijarah Thumma Al-Bai (hire purchase);

The Bank purchases the vehicle identified by the customer from a dealer / third party;

The vehicle to be financed by the Bank can either be new or used and of any make and models including national or non-national brands;

Margin of finance is up to 85%;

Payment period is up to 7 years.

BENEFITS

Fixed rental rate;

Rebate will be given for early settlement cases;

No security deposit required;

Comprehensive Takaful coverage with profit-sharing features (Mudharabah concept);

Convenient on-line payment facility at all our branches on real time basis.

HIRE PURCHASE-I•To purchase commercial and industrial vehicles.

Eligibility•Private Limited Companies•Public Limited Companies•Cooperatives

Financing Amount•Financing of up to 70% from the purchase price

Financing Period•Maximum 10 years

THE END!

THANK YOU!

ANY QUESTION?