agricultural insurance feasibility study - world bank agricultural insurance feasibility study june...

TRANSCRIPT

KAZAKHSTAN

Agricultural �Insurance �Feasibility �Study

June 2012

AgriculTure ANd rurAl developmeNT uNiT

SuSTAiNAble developmeNT depArTmeNT

europe ANd ceNTrAl ASiA regioN

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

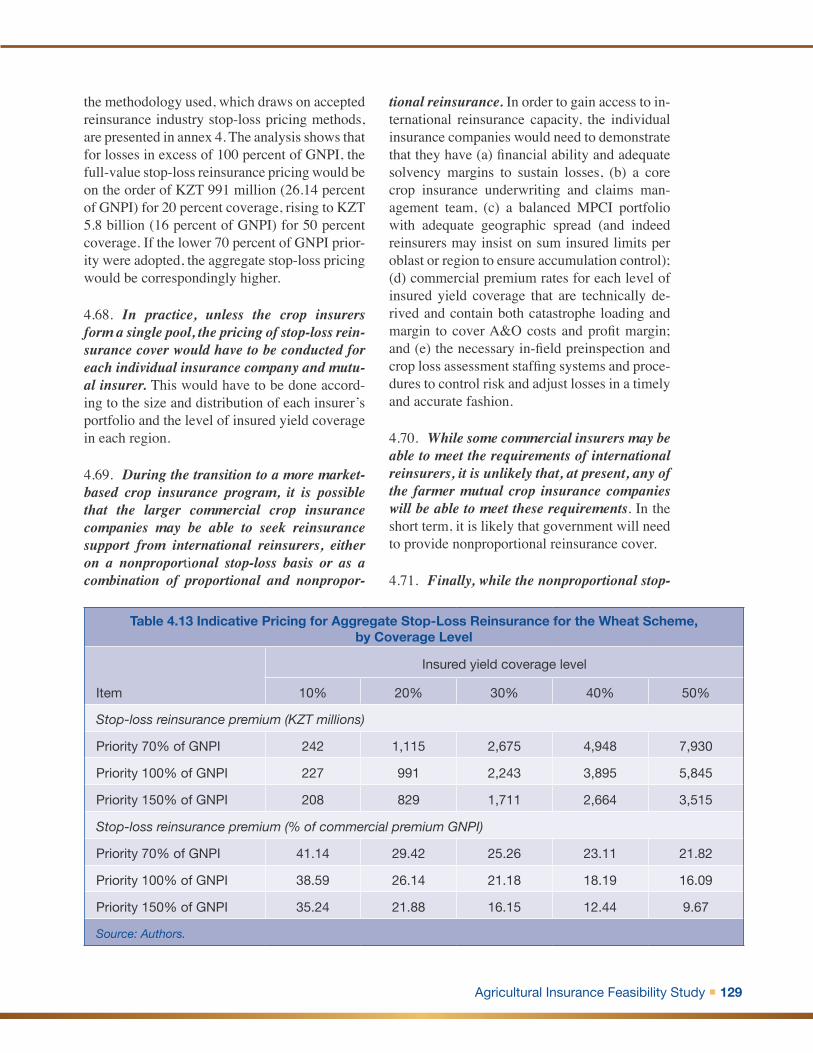

lic D

iscl

osur

e A

utho

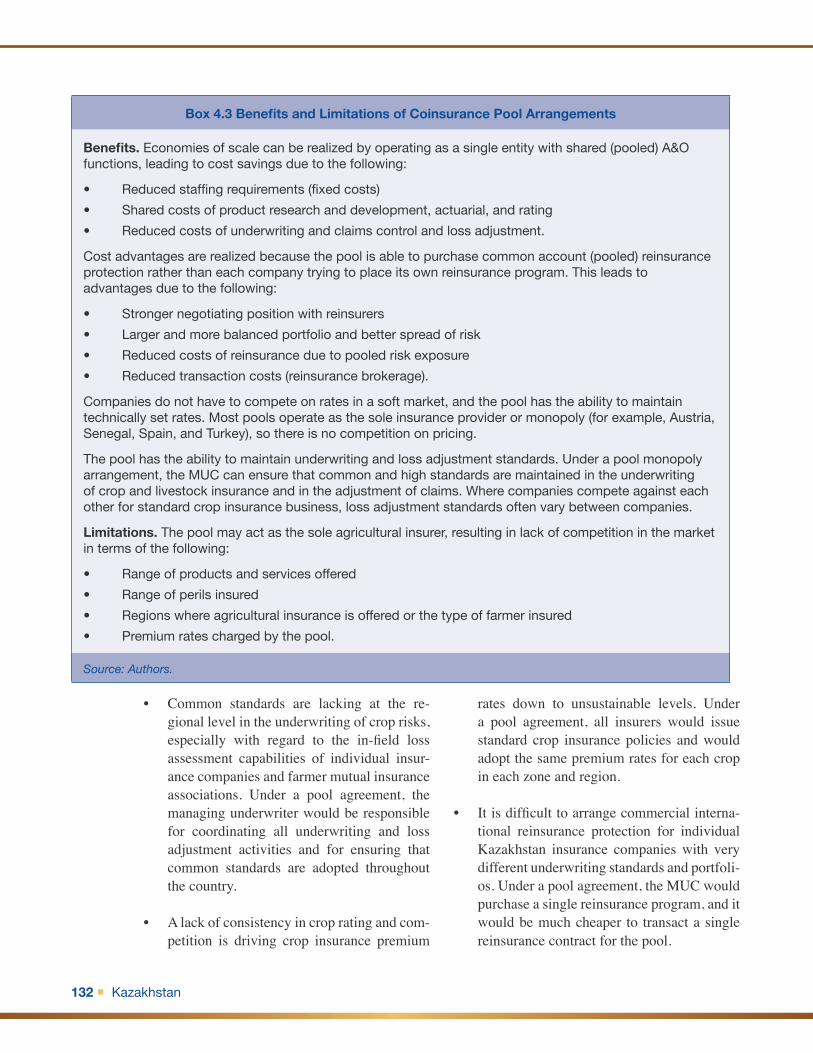

rized

Pub

lic D

iscl

osur

e A

utho

rized

Disclaimer:

This �volume �is �a �product �of �the �staff �of �the �International �Bank �for �Reconstruction �and �Development �/ �The �World �Bank. �The �findings, �interpretations, �and �conclusions �expressed �in �this �paper �do �not �neces-sarily �reflect �the �views �of �the �Executive �Directors �of �The �World �Bank �or �the �governments �they �repre-sent.

The �World �Bank �does �not �guarantee �the �accuracy �of � the �crop �production �and �yield �data �and �crop �insurance �financial �data �included �in �this �work �and �on �which �basis �some �analyses �have �been �made �and �from �which �some �conclusions �have �been �drawn �and �recommendations �made. �The �World �Bank �cannot �be �held �responsible �for �any �insurance �result �or �other �financial �outcome �which �might �arise �from �any �decisions �or �actions �taken �by �insurers �or �any �other �party �as �a �consequence �of �the �contents �of �this �report. �The �boundaries, �colors, �denominations, �and �other �information �shown �on �any �map �in �this �work �do �not �imply �any �judgment �on �the �part �of �The �World �Bank �concerning �the �legal �status �of �any �territory �or �the �endorsement �or �acceptance �of �such �boundaries.

Cover �photos: �The �World �Bank �Photo �Library. �Cover �and �Layout �design: �Duina �Reyes

2012 �The �International �Bank �for �Reconstruction �and �Development �/ �The �World �Bank1818 �H �Street, �NWWashington, �DC �20433www.worldbank.org

KazaKhstan

Agricultural Insurance Feasibility Study

June 2012

agriculture and rural development unit

sustainable development department

europe and central asia region

Agricultural Insurance Feasibility Study 3

Table of Contents

acknowledgments ........................................................................................................... 5

abbreviations ................................................................................................................... 6

executive summary ......................................................................................................... 8Context and Scope of the Study ............................................................................................ 8

Crop Risk Assessment ......................................................................................................... 10

Review of Compulsory Crop Insurance Program ................................................................. 11

Strategy and Options for Strengthening the Current Crop Insurance Scheme ................... 15

Opportunities for New Crop Insurance Products ................................................................. 28

Tailoring Crop Insurance to the Needs of Small Farmers in South Kazakhstan .................. 33

agricultural insurance Feasibility study: summary of recommendations for improvement of the obligatory crop insurance scheme in Kazakhstan ................. 36

chapter 1: introduction and objectives of the study ................................................. 41Importance of Agriculture in Kazakhstan ............................................................................. 42

Agricultural Crop Production in Kazakhstan ........................................................................ 42

Government Policy for Agriculture ....................................................................................... 44

Exposure of Agriculture to Natural and Climatic Disasters .................................................. 44

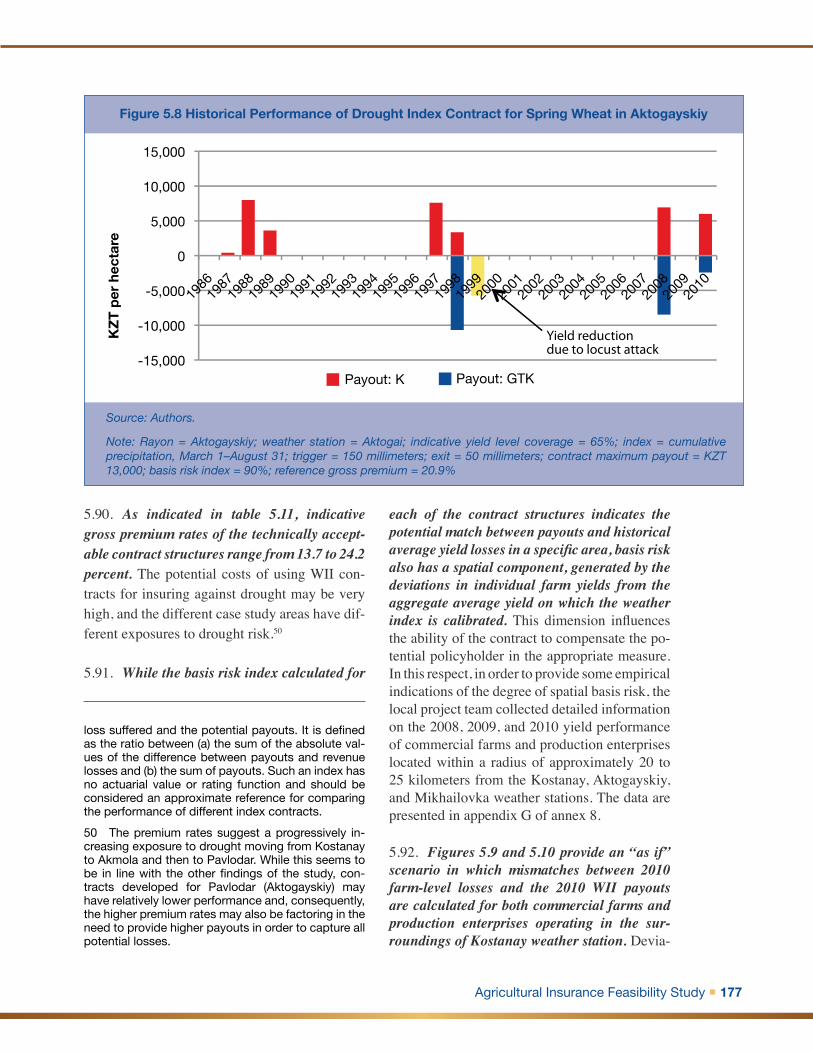

Government Objectives for Crop Insurance ........................................................................ 45

Objectives and Scope of the Study ..................................................................................... 46

Outline of the Report ........................................................................................................... 48

chapter 2: crop and Weather risk assessment ........................................................ 49Objectives and Scope of Agricultural Crop and Weather Risk Assessment ........................ 49

Data Availability for Crop and Weather Risk Assessment .................................................... 49

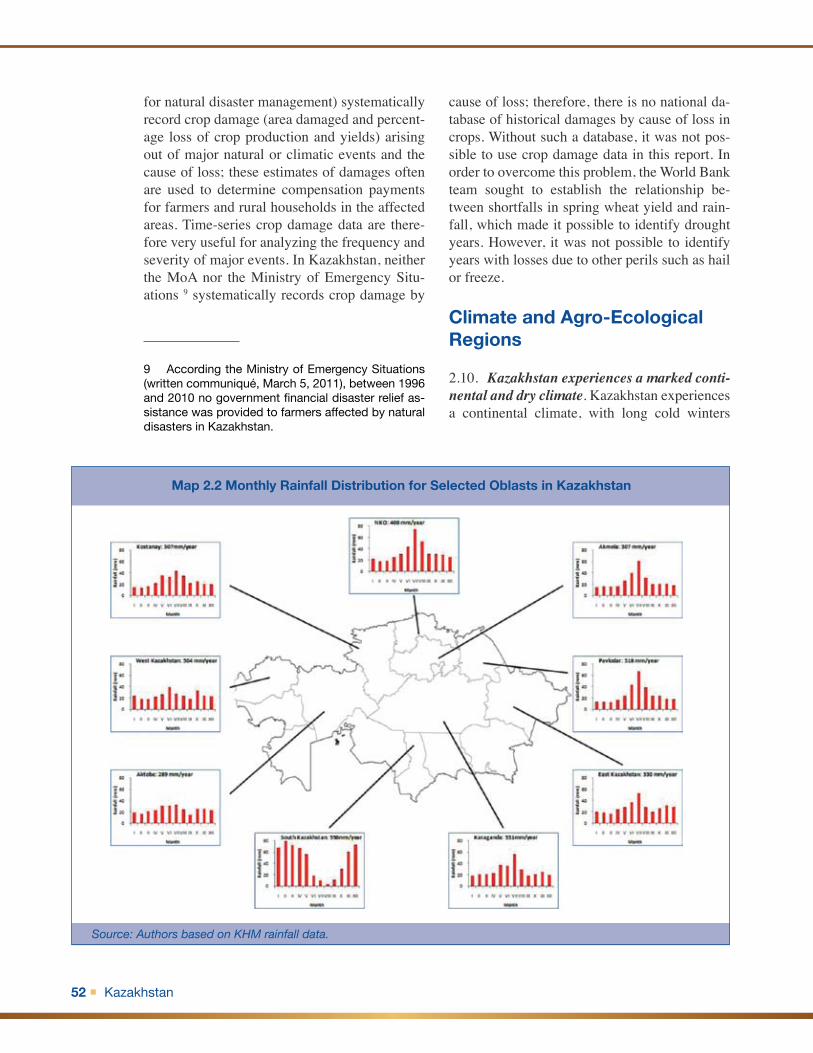

Climate and Agro-Ecological Regions ................................................................................ 52

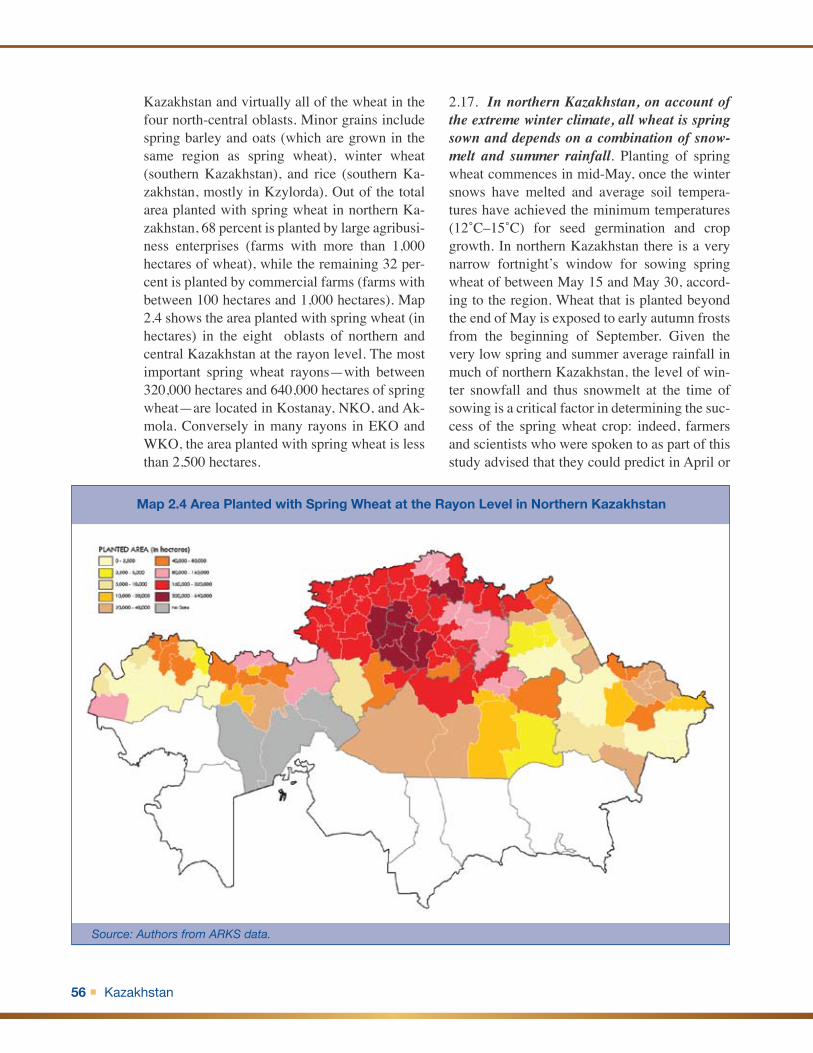

Overview of Spring Wheat Crop Production in Kazakhstan ................................................ 54

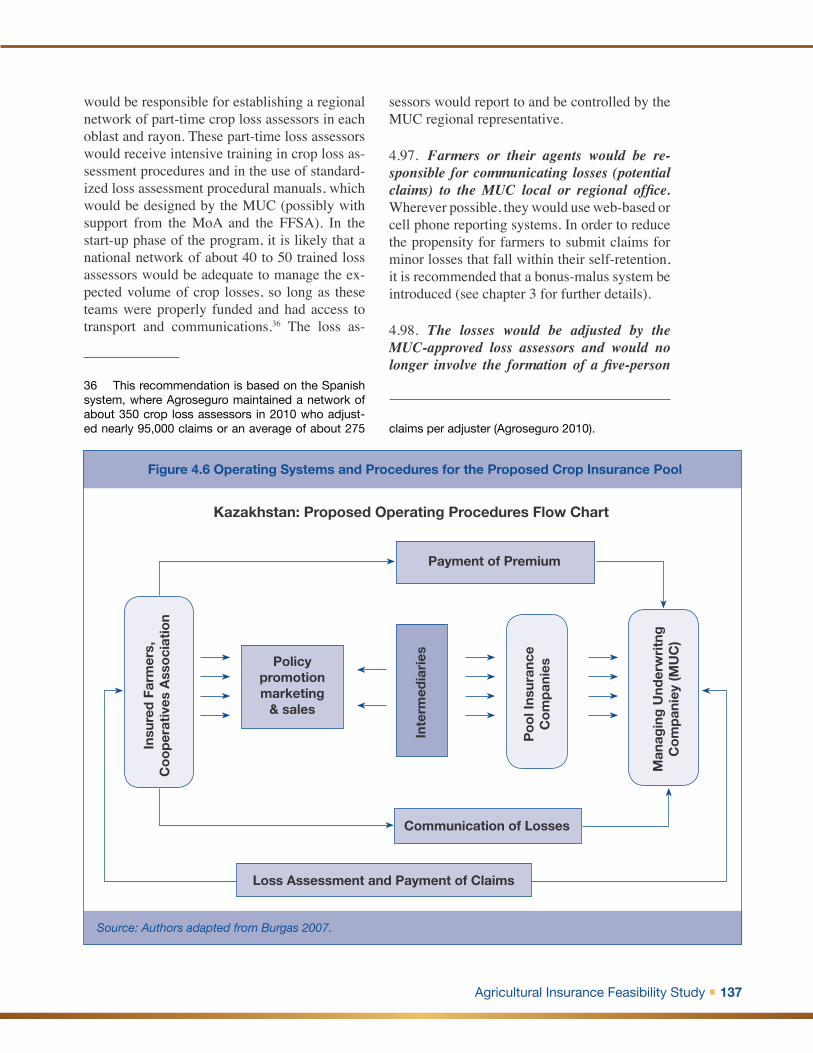

Key Climatic Perils and Impact on Crop Production and Yields .......................................... 61

Assessment of Crop Production Risk Exposures ................................................................ 65

chapter 3: review of Kazakhstan crop insurance program .................................... 70Policy and Regulatory Framework for Crop Insurance ........................................................ 70

Compulsory Crop Insurance Policy Terms and Conditions ................................................. 71

Government Financial Support to Crop Insurance in Kazakhstan ....................................... 78

Performance Assessment: Technical Results, Liabilities, Reinsurance .............................. 80

Assessment of the Technical, Operational, and Institutional Features of the Compulsory Crop Insurance Program ................................................................................. 92

Evaluation of Crop Insurance Effectiveness for Key Stakeholders ...................................... 98

4 Kazakhstan

chapter 4: strategy and options for strengthening the current crop insurance program ...................................................................................................... 101

Phase 1: Returning the Obligatory Crop Insurance Scheme to Profitability and Financial Stability ............................................................................................................... 102

Phase 2: Transition toward a Market-Based Crop Insurance System ............................... 120

Phase 3: Transformation into a Fully Commercial Crop Insurance Scheme ..................... 130

chapter 5: opportunities for new crop insurance products .................................. 145Named-Peril Crop Insurance .............................................................................................. 145

Area-Yield Index Crop Insurance ....................................................................................... 151

Crop Weather Index Insurance .......................................................................................... 167

chapter 6: tailoring crop insurance to the needs of lower-income smaller Farmers .......................................................................................................... 184

Identification of Appropriate Crop Insurance Products ..................................................... 184

Farmer Segmentation and Crop Insurance ........................................................................ 186

Tailoring Crop Insurance for Different Client Levels ........................................................... 187

Organizational and Operational Systems for Small Farmer Crop Insurance ..................... 192

Identification of Operational Linkages to Bundle Programs .............................................. 199

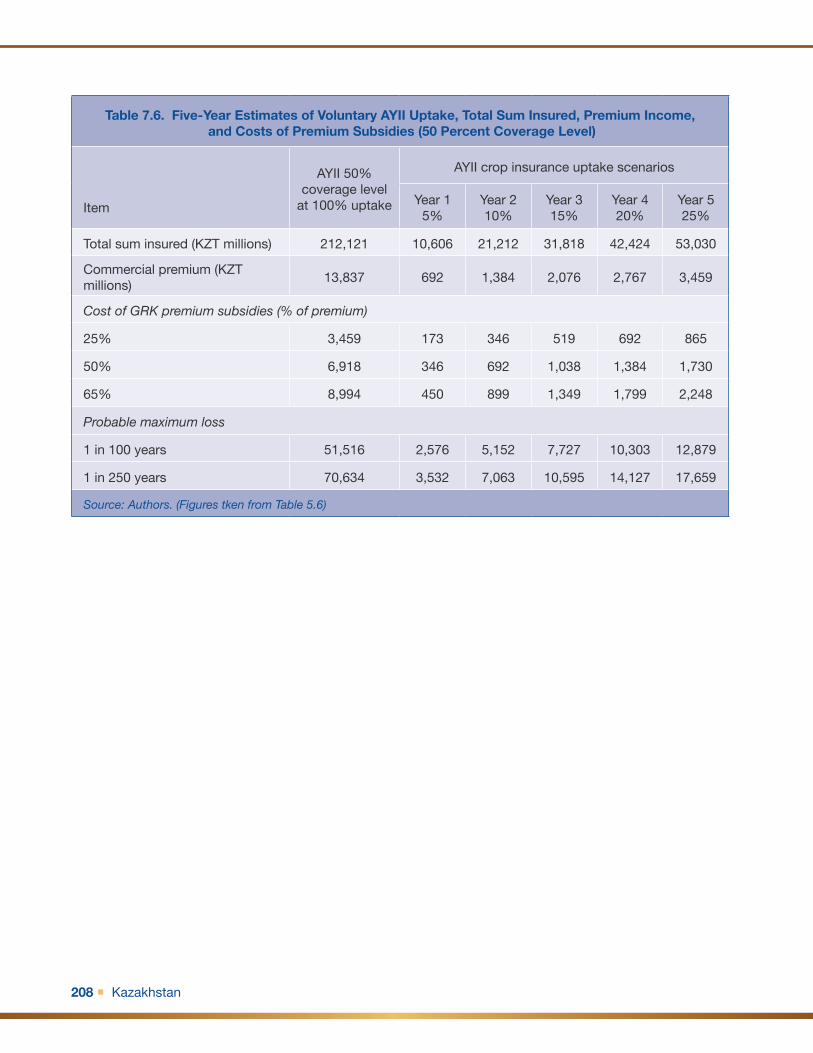

chapter 7: Fiscal implication of various insurance products on the gKr budget ................................................................................................................. 201

bibliography ................................................................................................................. 209

Agricultural Insurance Feasibility Study 5

Acknowledgments

The report was prepared by the World Bank in partnership with the Second Agricultural Post Privatization Assis-

tance Project (APPAP II) and was authored by a team led by Sandra Broka (Senior Rural Finance Specialist, ECSS1, World Bank) and Meiram Akchukakov (Program Coordinator, APPAP II). The team was composed of Ramiro Iturrioz (Se-nior Agricultural Insurance Specialist, Insurance for the Poor Program, GCMNB, World Bank—Technical Leader); Talimjan Urazov (Operations Officer, ECSS1, World Bank); Charles Stutley (Consultant, ARMT, ARD, World Bank); An-drea Stoppa (Consultant, ARMT, ARD, World Bank); Bakhyt Sattybaeva (Consultant, APPAP II); Lunara Umralinova (Consultant, APPAP II); Marina Gabdulinova (Consultant, APPAP II); Aigerim Malik (Consultant, APPAP II); and Arka Consulting, the local consultant firm se-lected by APPAP II for this project.

The team acknowledges the contributions of all stakeholders, including the Ministry of Ag-riculture (MoA) and, in particular, the Depart-ment of Investment Policy and External Rela-tions and the Department of Strategic Planning in Agribusiness and Innovation Policy; the JSC Fund for Financial Support for Agriculture,

Hydro Meteorological Service of Kazakhstan (Kazhydromet, KHM); the National Agency of Statistics; the Agency for Financial Market and Financial Institutions Regulation and Control; the National Space Agency; JSC; the Union of Farmers of Kazakhstan; the Scientific Research Institute of Economy of Agro-Industrial Com-plex and Development of Rural Territories; the A. Barayev Kazakh Scientific and Research Institute of Grain Farming; Akimat of Enbek-shilder rayon; Akimat of Bulandinskky rayon; Akimat of Altynsarin rayon; Kazakh Instrakh Halyk Group Insurance Company; Pana Insur-ance Company; Grain Insurance Company; “Agro-Insurance” Mutual Insurance Society; “SFK-Insurance” Mutual Insurance Society; and “Dostyk 05” Company Ltd.

The authors are grateful to the peer reviewers John Nash (Lead Economist, LCSSD, World Bank), Olivier Mahul (Program Coordinator, FCMNB, World Bank), and Gary Reusche (Op-erations Officer, IFC).

The team gratefully acknowledges funding sup-port from the Commodity Risk Management Multi-donor Trust Fund.

6 Kazakhstan

Abbreviations

A&O Administrative and Operating

Agroseguro Agrupación Española de Entidades Aseguradoras de los Seguros Agrarios Combinados (Spanish Group of Insurance Entities of the Combined Agrarian Insurance)

AIC Agricultural Insurance Company of India

APPAP II Second Agricultural Post Privatization Assistance Project

ARD Agriculture and Rural Development Department, World Bank

ARKS National Agency of Statistics

ARMT Agriculture Risk Management Team

AYII Area-Yield Index Insurance

Centner Grain production unit equivalent to 100 kilograms

CJSC Kazakh Actuarial Center

CoV Coefficient of Variation

CRAM Crop Risk Assessment Model

EEL Each and Every Loss

EKO East Kazakhstan Oblast

FAPRAC Fund for the Care of Rural Population Affected by Weather Contingencies (Mexico)

FFSA Fund for Financial Support for Agriculture

GDP gross domestic product

GMFP Grameen Fisheries and Livestock Foundation (Bangladesh)

GNPI Gross Net Premium Income

GRK Government of the Republic of Kazakhstan

GRP Group Risk Plan (United States)

HTR Hydrothermal Ratio

Agricultural Insurance Feasibility Study 7

IU Insured Unit

K Humidity factor

KHM Hydro Meteorological Service of Kazakhstan (alternatively known as Kazhydromet)

KZT Kazakhstan tenge (monetary currency of Kazakhstan)

LIC Loss of Investment Costs (crop insurance policy)

LIF Livestock Insurance Fund (Bangladesh)

MFI Microfinance Institution

MoA Ministry of Agriculture

MPCI Multiple-Peril Crop Insurance

MT Metric tonne, equivalent to 1,000 kilograms

MU Managing Underwriter

MUC Managing Underwriting Company

NAIS National Agricultural Insurance Scheme (India)

NCSRT National Center of Space Research and Technologies

NDVI Normalized Difference Vegetation Index

NGO Nongovernmental Organization

NKO North Kazakhstan Oblast

NSA National Space Agency

Oblast Administrative Region of Kazakhstan

PML Probable Maximum Loss

PPP Private-Public Partnership

Rayon Administrative area within an oblast

SIF Self-Insured Fund (Mexico)

SKO South Kazakhstan Oblast

TSI Total Sum Insured

VaR Value at Risk

WII Weather Index Insurance

WKO West Kazakhstan Oblast

WTO World Trade Organization

8 Kazakhstan

Executive Summary

context and scope of the study

1. Agriculture is a very important socioeco-nomic sector in Kazakhstan. Approximately 7.3 million people (47.2 percent of the total popula-tion) currently live in rural areas, and agricul-ture employs more than 22 percent of the labor force in the country. Agriculture contributes 5.92 percent of Kazakhstan’s gross domestic product (GDP). The country is one of the major global producers and exporters of grains (main-ly wheat). Other principal agricultural products include meat, wool, cotton, and milk. Farming areas occupy more than 220 million hectares (about 74 percent of the country’s total area), of which cereal-growing areas occupy about 13 million to 14 million hectares. The major grain crop is spring wheat, which is grown predomi-nantly under extensive low-cost production sys-tems in northern and central Kazakhstan.

2. In northern and central Kazakhstan, spring wheat production and yields are highly influenced by climatic and biological factors. On account of the very uncertain climatic condi-tions, Kazakhstan has the highest year-on-year variation in national average wheat production and yields of any major wheat-producing and -exporting country. Drought is the most perva-sive peril, affecting rain-fed crop production in northern Kazakhstan, and severe droughts are ex-perienced every two to five years. Spring wheat crops can also be damaged by hailstorms, early autumn frost, pests, and diseases. This study es-timates that, on average, about 14.71 percent of the total value of the national spring wheat crop

is lost due to drought and other perils every year, valued at KZT 66.5 billion (US$443 million).1 In 1998, an extreme drought year, physical loss-es were on the order of 7 million metric tons, equivalent to as high as 42 percent of the total expected value of wheat production. Very severe drought losses were experienced in spring wheat most recently in 2008 and again in 2010.

3. The Government of the Republic of Ka-zakhstan (GRK) introduced a national compul-sory crop insurance scheme in 2005 in order to provide grain producers and other farmers with a minimum level of protection against catastrophic climatic events. The scheme was enacted through the Law on Compulsory Crop Insurance, which is dated March 10, 2004 and became operational in 2005. The law established the terms and conditions for implementation of a compulsory loss of investment costs (LIC) insur-ance policy providing comprehensive protection against the loss of production costs invested in growing a range of strategic grain, oilseed, and other field crops. The Kazakhstan crop insurance scheme is based on a public-private partnership (PPP) implemented by the private commercial and mutual insurance companies and supported by government financial subsidies on claims. The implementing agencies are the Ministry of Ag-riculture (MoA), through the Direction of Stra-tegic Planning, the Fund for Financial Support for Agriculture (FFSA), the private commercial

1 Kazakhstan’s currency is the tenge. This report uses a current 2011 exchange rate of KZT 150 = US$1.00, unless otherwise stated.

Agricultural Insurance Feasibility Study 9

insurance companies, the farmer mutual crop in-surance associations, and the local authorities in each oblast and rayon. Under the PPP, the GRK provides financial contributions to the crop in-surance scheme through an indemnity fund—the FFSA—and indemnifies 50 percent of the costs of all crop insurance claims.

4. The GRK’s decision to introduce a na-tional compulsory crop insurance scheme for the most important crops grown in the country should be viewed in the context of government’s policy toward agriculture. The GRK recognizes the importance of the agriculture sector in diver-sifying economic growth, reducing rural pov-erty, and improving food security, with a strong emphasis on maintaining rural welfare for the country’s predominantly small farmers, as set out in the strategic Three-Year Plan for Agri-culture, 2009–11. Government’s introduction of compulsory insurance was designed mainly to guarantee that small farmers and agricultural wage laborers would have a minimum level of financial protection in the event of catastrophic crop production losses. Since the late 1990s, the government has significantly increased its finan-cial support to the crop sector, providing direct input subsidies, subsidized credit, and output price support. Under its goal of meeting World Trade Organization (WTO) accession terms, Ka-zakhstan will need to reduce its direct subsidies to agriculture; however, WTO legislation does not prohibit government from increasing its fi-nancial subsidies to agricultural crop and live-stock insurance.

5. Overall, the crop insurance scheme has not performed well. Over the past six years, the scheme achieved very high levels of uptake, but also encountered major operational and financial problems. Crop insurance penetration is very high in Kazakhstan, averaging 74 percent of the eligible cropped area for the period 2005–10. The high uptake is a function of the compulsory nature of the scheme. Notwithstanding the high level of penetration, insurance results were very poor over the past three years, with the result that

many commercial insurers have ceased to sup-port the scheme. From an operational viewpoint, the scheme is very costly to administer, and it is underrated in several regions. As the terms and conditions of cover are determined by govern-ment and fixed by law, the insurance companies have little say in risk acceptance and underwrit-ing decisions, and today only three companies continue to support the scheme. Finally, private commercial insurers and farmer mutual insurers are very exposed to catastrophic losses, as the scheme is not currently reinsured against excess losses.

6. During 2011, the World Bank, under the risk management component of the Agri-cultural Post Privatization Assistance Project (APPAP II), performed a comprehensive study to review, refine, and improve the compulsory crop insurance scheme in Kazakhstan. The study reviewed the Kazakhstan compulsory crop insurance scheme and made recommendations for its strengthening and transition over time to a more market-based agricultural insurance system. The study also assessed the potential to introduce new crop insurance products and pro-grams to complement the existing LIC policy. The study included the following specific com-ponents:

Review of the compulsory crop insur-a. ance scheme in Kazakhstan. A detailed diagnostic review was carried out of the technical basis of the LIC policy as well as the institutional and organizational features, of the public private partner-ship scheme, and its operating systems, procedures, and financial performance of the PPP scheme. This review identified a series of key issues and challenges for scheme management to address.

Identification of a phased strategy to b. transform this scheme into a finan-cially sustainable market-oriented sys-tem. Drawing on local expertise and in-ternational experience and best practice,

10 Kazakhstan

a phased strategy was identified for the next three to five years to strengthen the scheme, return it to profitability, and transform it into a sustainable market-based system that is supported both by the public sector and by international re-insurers.

Assessment of agricultural riskc. . A for-mal crop risk assessment was performed for spring wheat, the country’s most im-portant export crop. This risk assessment was intended to assist policy makers, planners, and crop insurers in the plan-ning, design, and rating of new crop in-surance products. Owing to the size of the country, it was agreed that the scope of the risk assessment would be limited to spring wheat grown in the eight most im-portant oblasts of Kazakhstan: Kostanay, Akmola, North Kazakhstan (NKO), East Kazakhstan (EKO), West Kazakhstan (WKO), Pavlodar, Karaganda, and Ak-tobe.

Analysis of crop insurance products.d. Four new types of crop insurance prod-ucts were analyzed that, in the future, could either complement or replace the current LIC policy: (1) individual grower multiple-peril crop insurance (MPCI), (2) crop hail cover, (3) area-yield index insurance (AYII), and (4) weather index insurance (WII). For the purpose of the feasibility studies, the research on area-yield index insurance was performed for spring wheat grown in the eight selected oblasts of Kazakhstan. For crop hail and weather index insurance products, the re-search focused on spring wheat grown in Altynsarinski and Auliyekolski rayons in Kostanay; Aktogayskiy and Zhelezinski rayons in Pavlodar; and Bulandinski and Enbekshilderski rayons in Akmola.

Identification of challenges for develop-e. ing crop insurance for small farmers in Kazakhstan. The final objective of this

study was to identify ways to tailor the provision of crop insurance to the needs of resource-poor farmers located in south-ern Kazakhstan. Tole-bi rayon in South Kazakhstan (SKO) was selected for more in-depth study.

Brief Assessment of the Fiscal Implica-f. tion of the various crop insurance prod-ucts on the GKR budget.

crop risk assessment

7. A detailed risk assessment was conduct-ed of weather risks and their impact on spring wheat crop production and yields in northern Kazakhstan. The risk assessment comprised the following components: (a) a review of the availability and quality of time-series crop pro-duction data and the availability of weather data in Kazakhstan for spring wheat risk assessment and insurance design and rating purposes; (b) a review of climatic and agro-ecological regions and spring wheat crop production systems in the selected oblasts of Kazakhstan; (c) a detailed statistical analysis of spring wheat production and yields and the climatic constraints to pro-duction, including an analysis of rainfall data and the relationship to national and rayon-level spring wheat crop production and yields; and fi-nally (d) application of a crop risk assessment model (CRAM) that uses time-series rayon-lev-el production and yield data to estimate values at risk, expected losses, and expected claims costs for spring wheat in the eight selected oblasts in Kazakhstan. This latter analysis is very relevant to crop insurers’ understanding of risk accumu-lation and maximum expected losses in spring wheat. Full results of the risk assessment are presented in chapter 2.

8. The crop risk assessment of rayon-level crop production and yields for spring wheat in the northern and central regions of Kazakh-stan found that this crop is heavily exposed to losses caused by droughts. This is evidenced by the average loss cost estimated by the CRAM for the 17-year period from 1994 up to 2010 of

Agricultural Insurance Feasibility Study 11

KZT 66.5 billion (14.71 percent of the total val-ue at risk of spring wheat production) and a cal-culated 1-in-100-year probable maximum loss (PML) of KZT 246.8 billion (54 percent of the gross value of production for spring wheat). The highest average annual expected losses in spring wheat apply to Aktobe (22 percent of the spring wheat crop value) and to WKO (40 percent of the spring wheat crop value) located in western Kazakhstan. Except in a few rayons situated in the north of Aktobe and in the southwest of WKO, spring wheat average yields are both low and highly variable in most of the rayons located in these two western oblasts, which re-ceive much lower and erratic rainfall. Converse-ly, spring wheat production is much less risky in the northern oblasts of NKO, Kostanay, and Akmola, which receive higher and more stable precipitation.

9. The need for accurate and independent measurement and recording of crop produc-tion, crop yield, and weather data at local up to national levels is critical to the design, rat-ing, and implementation of any crop insurance scheme. On the basis of this study, it is apparent that the GRK has very efficient meteorological, agricultural, and statistical services. The avail-ability of production and weather data is, in gen-eral, very good. Kazakhstan has a modern and efficient national meteorological service, Hydro Meteorological Service (alternatively known as Kazhydromet or KHM), which provided time-series rainfall data for a sample of weather sta-tions in the selected rayons. These data enabled a detailed assessment of rainfall and yield rela-tionships and provided the basis for the design and rating of prototype WII products. There is, however, a key constraint at present: the density of weather stations in such a vast territory as Ka-zakhstan is inadequate to implement a national commercial micro-level crop WII scheme in the near future. Kazakhstan also has good statistical records of spring wheat crop area, production, and yield at the rayon, oblast, and national lev-els, which are collected by the National Agency of Statistics (ARKS). These data enabled the de-sign and rating of prototype individual grower

MPCI and area-yield index crop insurance prod-ucts for Kazakhstan (as detailed in chapters 4 and 5).

review of compulsory crop insurance program

10. Chapter 3 of this report provides a de-tailed review of the technical, operational, in-stitutional, and financial features of and chal-lenges faced by the compulsory crop insurance scheme.

technical challenges

11. The Kazakhstan compulsory crop insur-ance policy is a loss of yield policy that indemni-fies the insured when the value of the harvested production falls short of the costs invested in growing the crop due to the action of insured perils. The LIC policy has several advantages: (a) it provides comprehensive MPCI protection to the farmer against the loss of production costs invested in growing the crop, and (b) it can be used in situations where there is inadequate or no information on the historical crop yields of individual farmers. However, it also has several potential drawbacks, including the need for in-field yield-based loss assessment where partial losses are involved and the difficulty of estab-lishing objectively the salvageable amount of the crop, its sale value, and whether this salvage value exceeds the insured investment costs lead-ing to a claim.

12. The coverage levels provided by the LIC crop insurance scheme in Kazakhstan are ex-tremely low and do not provide adequate lev-els of financial protection to the farmer in the event of loss. Although the compulsory scheme offers a series of optional sum insured levels for farmers to choose from, based on different crop technology levels and costs of production vary-ing from low to high production costs, in prac-tice practically all farmers in Kazakhstan elect the cheapest or lowest option for sum insured coverage—about KZT 3,500 (slightly less than US$25) per hectare nationally for spring wheat

12 Kazakhstan

in 2010—because this option has the lowest pre-mium. On average, farmers only insure between 20 and 30 percent of their total production costs. The very low levels of crop insurance cover are, therefore, often inadequate to put farmers back into production in the event of a major crop loss.

13. The methodology for rating LIC insur-ance premiums in Kazakhstan should be re-vised. Currently, crop insurance premiums are calculated for each crop at the oblast level, when they should to be calculated at the rayon level or even higher levels of disaggregation in order to take into account differences in risk either at the rayon level or at the individual farmer level. Crop insurance premium rates are fixed by law. They were last adjusted in 2008 and now need to be adjusted on an actuarial basis. Crop insur-ance premium rates are set for each type of crop and group of oblasts according to minimum and maximum rates, and insurers are not permitted to charge higher rates even when they are actu-arially required.

14. The basis of indemnity on the LIC policy requires strengthening. Crop output valuation prices are determined at the time of harvest, as opposed to being preagreed and specified in the policy wording. This means that neither the insurers nor the government can calculate their liability in the event of claims: when out-put prices are low, the policy is much more ex-posed to losses than when prices are high. This issue should be addressed by introducing fixed, preagreed harvest valuation prices at the time of signing the policy agreement.

operational challenges

15. The obligatory nature of the scheme pre-vents underwriters from exercising proper risk selection and control over the underwriting of their crop insurance portfolios. Insurance com-panies are obliged to accept all crop insurance risks (that is, individual farmers) even when the farmers are poor risks (that is, they do not use the correct crop production or husbandry practices for growing the insured crop) or the farms are

located in such high-risk areas that they would normally be considered uninsurable by commer-cial crop insurers.

16. Policy sales are currently permitted to continue up to the time of sowing, when farm-ers are in a good position to predict whether the growing season will be poor, and this exposes the program to moral hazard. Where preexist-ing drought conditions are developing, farmers may modify their behavior by (a) electing to buy the maximum level of “normative costs” sum insured in the expectation of receiving a claims payment or (b) incurring less than their normal level of expenditure on crop husbandry and in-puts because they know they are likely to lose their crops, in which case, they can expect to claim on their insurance policies (this is termed moral hazard).

17. Private insurance companies do not have their own network of locally based quali-fied agronomists to inspect the insured farms at the time of sowing. Such inspections are needed to confirm whether the farmer has complied with the correct sowing practices, seed rates, and so forth. As such, cover is open to moral hazard. The costs of establishing such a network and inspecting each and every farm would be pro-hibitively high for the insurers, which, under the current rating system, are not able to increase rates to cover their administrative and operating (A&O) expenses.

18. Loss adjustment requires the participa-tion of several parties, is expensive, and some-times lacks transparency. In Kazakhstan, up to five persons are involved in adjusting crop losses at the local level, and this is a very time-consuming and costly exercise. There is a need to rationalize the loss assessment procedure and to reduce its costs.

institutional challenges

19. The Kazakhstan compulsory crop insur-ance scheme is a public-private partnership. It is highly regulated by government and is under-

Agricultural Insurance Feasibility Study 13

written by the private commercial (and mutual) insurance sector, with financial claims subsidy support provided by government through the FFSA. As such, the insurance companies are unable to accept or reject individual crop risks (farmers), which is a fundamental principle of crop underwriting. In most countries where ag-ricultural insurance PPPs exist, the main role of government is to provide legal and regulatory support and financial subsidies.

20. Crop insurance in Kazakhstan is writ-ten by commercial insurers and farmer mutual insurance associations. The level of participa-tion of the private insurance companies is very low (only three commercial insurers participate in the scheme), and there is a danger that, un-less the scheme can be returned to profitability, the private insurance companies may cease to provide their support altogether. Conversely, the participation of farmer mutual crop insurance associations is gaining importance. As of 2011, more than 38 farmer mutual associations were offering crop insurance in Kazakhstan.

21. Private insurance companies and farmer mutual associations providing crop insurance are not equally regulated. While private insur-ance companies are regulated by the Agency for Financial Market and Financial Regulation and Control, the farmer mutual crop insurance as-sociations are regulated separately by the Law on Mutual Insurance. Nonlife private insurance companies are required to have minimum capi-tal of KZT 1.2 billion (US$8.0 million) in order to operate and are frequently monitored on their solvency, net retentions, and implementation of risk management procedures. Conversely, the farmer mutual associations offering crop insur-ance are not subject to minimum capital require-ments, controls over net retentions, or solvency requirements. In 2010 several mutuals report-edly did not collect enough crop insurance pre-miums to pay the full amount of claims incurred during the 2010 crop season. There is a need to ensure that the private companies and mutuals are regulated equally under the crop insurance scheme.

government support

22. The GRK provides major financial sup-port to the compulsory crop insurance scheme. This support is provided in two ways: (a) by compensating the insurers for 50 percent of all the claims incurred and (b) by funding the A&O expenses of the FFSA. The 50 percent claims compensation fund is administered by the FFSA, which is responsible for monitoring and manag-ing the financial transactions of this insurance scheme on behalf of the government and for ap-proving the claims reimbursements to individual insurance companies. Over the past six years, the GRK provided KZT 4.7 billion to the FFSA, of which 93 percent was allocated to settling the 50 percent of claims and 9 percent to paying the A&O expenses of the FFSA. During this period, the FFSA reimbursed the insurance companies a total of KZT 3.84 billion, equivalent to 46.7 per-cent of total claims paid or an average of KZT 641 million (US$4.3 million) per year.

Financial challenges

23. The compulsory crop insurance pro-gram in Kazakhstan experienced poor overall underwriting results over the period 2005 to 2010. The long-term average loss ratio for the six-year period was 140 percent, and in four of the six years, the scheme operated at a financial loss, with a loss ratio (gross claims to premium) exceeding 100 percent. The average net loss ratio for the insurance companies after receiv-ing the 50 percent government claims subsidies was 75 percent. Over the past three years (2008 to 2010), the results deteriorated badly, with an average loss ratio of 182 percent (99 percent af-ter government claims subsidies); the worst loss was experienced in 2010, with a loss ratio of 261 percent.

24. Scheme performance varies widely across different regions, and the very poor underwrit-ing results in Aktobe and WKO are making the scheme financially unviable. The pattern of claims varies widely by geographic region. The best-performing oblast is NKO, which over

14 Kazakhstan

the past six years contributed 22 percent of total scheme liability but only 3 percent of claims and had a long-term loss ratio of only 24 percent. At the other extreme, Aktobe and WKO in western Kazakhstan, which collectively accounted for only 4.8 percent of total scheme liability, in-curred 41 percent of all claims and had six-year long-term loss ratios of 381 and 507 percent, re-spectively. These two oblasts are severely preju-dicing the financial viability of the national crop insurance program, and measures for controlling the claims costs in these two oblasts must be in-troduced.

25. The private insurance companies and mutuals do not have access to reinsurance

on their 50 percent retained claims, and they are extremely exposed to catastrophic drought losses. This is a major issue that will need to be addressed under any future reform of the Ka-zakhstan crop insurance scheme.

evaluation of crop insurance effectiveness for Key stakeholders

26. The Kazakhstan compulsory crop in-surance scheme was launched with very well-intentioned social and economic objectives, but it is failing to meet the requirements of its key stakeholders, including farmers, crop insurers, and government. The program was

FarmersDissatisfaction with compulsory nature of crop insurance.•

Reluctance to purchase insurance in spite of being compulsory.•

Extremely low levels of coverage.•

Difficulties in understanding the insurance agreement especially the • basis of indemnity and loss assessment procedures.

governmentVery good social intentions, but compulsory nature of the • program is very unpopular with most farmers.

Intention of obligatory insurance in early years to develop crop • insurance market has not been achieved.

Uncertainties about financial exposure.•

Uncertainties about budgeting claims participation in • catastrophic events.

insurers:Limitations to perform risks selection/underwriting.•

No incentives to invest in underwriting/claims • management infraestructure.

Uncertainties about financial exposure.•

Difficulties to gain access to reinsurance.•

Concern by private commercial insurers that they do not face a level • playing field with the Farmers’ Mutual Crop Insurance Associations.

Crop Insurance has been unprofitable to date.•

Figure 1 Key issues Facing main stakeholders involved in the compulsory crop insurance scheme

Source: Authors.

Agricultural Insurance Feasibility Study 15

originally conceived as a mechanism to ensure that all farm workers and small peasant farm-ers would receive a minimum indemnity in the event of crop failure due to drought or other nat-ural and climatic perils. The obligatory nature of the scheme was intended to be a short-term measure that would enable the development of a sound and stable crop insurance market based on a partnership between the private and public sectors, while at the same time providing time to educate farmers in the benefits of crop insurance so that they would continue to purchase cover once the scheme was made voluntary. After six years, the scheme has failed to develop a strong crop insurance market and to educate farmers. The fact that the program is very unpopular with many farmers also suggests that it is failing to meet its social objectives. Finally, government faces major uncertainties over its financial expo-sure to claims (figure 1).

strategy and options for strengthening the current crop insurance scheme

27. A phased approach is recommended for strengthening and improving the obligatory crop insurance scheme in Kazakhstan and for gradually converting it into a fully market-based commercial crop insurance system.The proposed approach involves three distinct phases: (a) strengthening the current obligatory scheme and achieving financial stability (short term, one to three years); (b) moving toward a market-based crop insurance system (short term, one to three years); and (c) becoming a fully market-based pool crop insurance system backed up by international reinsurance under a PPP suitable for Kazakhstan (medium term, three to five years).

phase 1: short-term measures to strengthen the existing compulsory scheme

Measures to Strengthen the Legal and Regulatory Framework

28. In the short term, it is recommended

that the Law on Compulsory Crop Insurance be amended to permit insurance companies greater flexibility in determining the premium rates and other terms and conditions of cover they provide under the LIC policy. While it is assumed that crop insurance will continue to be obligatory for farmers in the short term, the law should be amended to permit insurers to set their own terms, conditions of cover, and, especially, premium rates (see chapter 4).

Measures to Strengthen the Design and Rating of the LIC Policy

29. Practical measures were identified for strengthening the design of the LIC policy. These measures are listed in box 1; full details are provided in chapter 4, and key recommenda-tions for strengthening are highlighted in box 1.

30. There is a need to consider increasing the sums insured. Currently, the LIC policy does not provide adequate levels of protection for the majority of farmers. If the levels of sum insured coverage were to increase under this program, farmers would receive higher levels of protection, but this would have to be accompa-nied by increases in the premium rates that in-surers would have to charge and in the amount of premium farmers would have to pay. With in-creased sums insured, the insurance companies would face a much higher financial liability in the event of severe drought losses, and it would be essential for them to have comprehensive re-insurance protection. For government, the higher coverage levels would mean a correspondingly higher budgetary allocation to cover the 50 per-cent claims reimbursements. The sums insured in each rayon should be set according to (a) the actual production costs of different types of farmers in each rayon and (b) the risk exposure in each rayon.

31. There is a need to revise the crop pre-mium rating methodology in order to (a) intro-duce a system of rayon-level premium rates and (b) update the premium rates on an actuarial basis. The six-year long-term gross loss ratio at end-2010 was 140 percent (equal to a 70 percent loss ratio net of the government’s 50 percent

16 Kazakhstan

claims reimbursement), suggesting that, on av-erage, the scheme has operated on a breakeven basis. The premium rates were last revised in 2008; however, the performance of the scheme deteriorated very badly over the past three years, with an average loss ratio of 182 percent (loss ratio of 91 percent net of the government’s 50 percent claims subsidy). In some oblasts, includ-ing NKO and Kostanay, the scheme performed very well, but in others, including Aktobe, WKO, and Zhambyl, it performed very poorly. There are also major differences in the pattern of losses among rayons in individual oblasts and a need to revise the oblast rating methodology by introducing a system of rayon-level actuarially determined premium rates for each crop. Final-

box 1 measures to strengthen the design of the loss of investment costs policy

criteria for acceptance of risk and compulsion of cover. Even if the government decides in the short term to maintain compulsory crop insurance for all producers, special consideration will need to be given to farmers located in Aktobe and WKO.

insured perils. Current coverage should be maintained to include loss or damage to crop production due to “adverse weather events,” as defined.

sales cutoff date. A policy sales cutoff date of April 1 should be introduced.

cover period. The cover period should be from the time of crop emergence and full stand establishment (for example, 10 centimeters for wheat) through to completion of the harvest.

insured unit (iu). The IU is currently defined as the “individual field.” For farms of less than 250 hectares, the IU should perhaps be redefined as “the total area of all fields of the same crop grown in the same location or farm.”

sum insured. Government should amend the law to permit insurance companies to have the option of establishing an agreed sum insured with each farmer according to its own circumstances and insurance requirements.

premium rates. Government should amend the obligatory law to permit each insurance company to set its own premium rates for each crop and zone. Actuarial rating should be introduced to reflect differences in risk exposures between rayons in each oblast and possibly differences in levels of technology use and risk exposures between farmers.

bonus-malus system. It is recommended that underwriters introduce a bonus-malus system on the compulsory crop insurance scheme. The objectives of the bonus-malus are (a) to introduce rating of individual farmers and (b) to reduce the submission of speculative claims notices by farmers.

basis of indemnity and claims settlement. The crop sales price, which is used to value actual production in the event of a partial loss, should be preagreed and based on an average historical farm-gate sales price for each crop in each rayon and stated in the policy wording.

Source: Authors.

ly, it is recommended that a bonus-malus system be introduced into the crop rating methodology (see chapter 4).2

Measures to Improve Scheme Profitability

32. The financial viability of the crop insur-ance scheme is being adversely affected by the inclusion of Aktobe and WKO. Over the past six

2 Under a bonus-malus system, a farmer who does not submit a claim is rewarded at the renewal date of his policy by receiving a reduction in his premium rate (termed the “bonus”), while a farmer who submits a claim sees an increase in his rate at the time of re-newal (termed the “malus”).

Agricultural Insurance Feasibility Study 17

years Aktobe and WKO collectively accounted for only 4.8 percent of total scheme liability, but contributed 41 percent of total claims and had actual loss ratios of 381 and 507 percent, respec-tively. Over this period, if Aktobe and WKO had not been included in the scheme, this would have led to a reduction in total premium earn-ings of only 13 percent, but would have led to a huge savings in claims costs for insurers of 40 percent of actual claims (or a reduction in claims of KZT 3.3 billion—US$22.0 million) and a re-duction in the six-year long-term gross loss ratio from 140 to 96 percent. Following application of the government 50 percent reimbursement of claims, the “as if” loss ratio for the scheme would have been reduced to about 48 percent (table 1). These two oblasts (in common with much of the northern and central regions of Ka-zakhstan) were traditionally livestock grazing regions that were converted to cereal (mainly spring wheat) production during Soviet times. The underlying problem in most of Aktobe and WKO is that soils are mostly poor and average annual rainfall is very low: in a normal year, rainfall is barely adequate for growing spring wheat in most rayons in these two oblasts. As such, these oblasts are very marginal for spring wheat crop production. No matter how a crop

insurance policy is structured, production will always be very heavily exposed to loss and the technical and commercial premium rates that would have to be charged will be so high (an average commercial rate prior to application of government claims subsidies of between 37 per-cent in Aktobe and 66 percent in WKO) as to make the scheme commercially unviable. There are, however, a few areas where spring wheat production is more stable and where crop insur-ance might be considered in the future, albeit at very high rates, including the rayons of Taskal-isky and Kaztalisky located in the southwest of WKO and the rayons of Karagaly and Martuk located in northern Aktobe.

Options for WKO and Aktobe

33. The first option for insurance compa-nies to consider would be to continue operat-ing the LIC scheme in Aktobe and WKO on the understanding that government will reimburse them for a higher percentage of claims in these two oblasts. Currently, government reimburses insurers for 50 percent of the value of all paid claims. Under this option, the GRK would agree to indemnify a higher percentage of claims in-

table 1 actual results of the crop insurance scheme with and without aktobe and WKo

Item Actual portfolio

(with Aktobe and WKO)Modified portfolio|(without

Aktobe and WKO)% reduction

Number of policies 140,961 134,193 −5

Total insured area (number of hectares)

73,770,915 69,453,803 −6

Sum insured (thousands of KZT) 242,631,438 231,048,598 −5

Premiums (thousands of) 5,861,958 5,102,670 −13

Average premium rate (%) 2 2 −9

Claim payments (thousands of KZT)

8,222,776 4,910,314 −40

Loss ratio (%) 140 96 −31

Loss cost (%) 3.39 2.13 −37

Source: Authors based on FFSA crop insurance data for 2005–10.

18 Kazakhstan

curred in Aktobe and WKO only. The insurance industry has asked government to consider rais-ing its share to 70 or 75 percent of total claims in these two oblasts in 2012. Over the past six years, government’s 50 percent contribution to claims costs amounted to about KZT 4.1 billion or an annual average of KZT 0.685 billion per year. If government agreed to increase its share of claims in Aktobe and WKO, the “as if” an-nual total cost to government would increase as follows under the two options: (a) under option A, 75 percent claims share in Aktobe and WKO, the cost would increase to KZT 0.823 billion per year, an increase of 20 percent, and (b) un-der option B, 100 percent claims share in Ak-tobe and WKO, the cost would increase to KZT 0.961 billion per year, an increase of 40 percent. Option B shows the maximum expected costs to government if it wishes to continue includ-ing Aktobe and WKO in the LIC scheme and assumes that insurance companies act purely as administrators in these two oblasts, but do not accept any claims liability: the “as if” 100 percent claims cost to government in these two oblasts would average about KZT 550 million or US$3.7 million per year. While this option may provide government a short-term solution to re-taining the support and underwriting capacity of the insurance industry and increasing the prof-itability of the program, it does not tackle the fundamental issue in the medium to long term, which is that commercial spring wheat crop in-surance is not financially viable in most of the rayons located in Aktobe and WKO.

34. The second option for government to consider would be to take Aktobe and WKO out of the crop insurance scheme altogether and to establish a separate disaster relief scheme for producers of annual crops in these two oblasts. The argument for removing Aktobe and WKO from the scheme centers on the following: (a) these areas receive very marginal rainfall and therefore are not suitable for growing annual grain crops and (b) from a crop insurance view-point, these oblasts (with the possible exception of a few rayons listed above) are effectively un-insurable, with six-year long-term loss costs of 22 and 40 percent, respectively, and catastrophic

losses every other year, with loss ratios (claims to premium ratios) as high as 1,000 percent in major drought years. It is therefore necessary for government to consider whether to continue promoting annual crops in these oblasts, but to use a separate disaster relief fund to compensate farmers in severe drought years. The cost of this disaster relief compensation program for farm-ers in Aktobe and WKO, assuming the same 100 percent original claims costs and compensa-tion levels as under the current LIC insurance scheme, would be exactly the same as the 100 percent claims compensation option outlined previously: the average cost to government for these two oblasts would be about KZT 550 mil-lion (US$3.7 million) per year, with a peak of about KZT 1.6 billion (US$10.7 million) in a very severe drought year, such as 2010. Op-tions for some form of macro-level catastrophe drought weather index insurance (WII) cover are also examined in this report.

Measures to Strengthen the Scheme’s Operating Systems and Procedures

35. In conjunction with the changes in de-sign identified to strengthen the LIC policy, administrators of the scheme should consider a series of potential measures to improve un-derwriting and claims operating systems and procedures and to reduce the costs of these operations. Box 2 summarizes some of the key operational areas that require strengthening. In the specific case of loss assessment, the current procedures, whereby a committee of up to five individuals from five different organizations is involved in the in-field loss assessment, must be rationalized and made more cost-effective, and the insurance companies should be given a more central role in loss assessment. At the same time, impartiality and fairness must be maintained for both the insured and the insurer. In the short term, Kazakhstan does not have independent firms of certified and approved loss adjusters who specialize in crop loss assessment, but in the medium term, options should be explored for creating such specialists.

Agricultural Insurance Feasibility Study 19

Measures to Strengthen the Institutional Framework

36. In the short term, a major challenge is to find ways to encourage more private commer-cial insurance companies to support the crop insurance scheme. Several measures identified under this study should be attractive to local in-surers, including (a) the introduction of actuari-ally determined premium rates, (b) the measures to reduce insurers’ liability in Aktobe and WKO, and (c) recommendations for strengthening loss assessment procedures and for giving insurers more direct control over this important function. However, in the medium term, it is also probable that insurers will insist on being given greater control over risk selection and underwriting if they are to join the scheme.

37. There is also a need to create a level playing field for commercial insurers and the farmer mutual insurance associations. Mutual

insurance associations should in the future be regulated by the Agency for Financial Market and Financial Institutions Regulation and Con-trol and be required to follow the same guide-lines with regard to capital requirements and insurance reserves as commercial insurance companies. Failing to do so creates biased com-petition and increases the chances that mutual associations will fail to meet their financial ob-ligations.

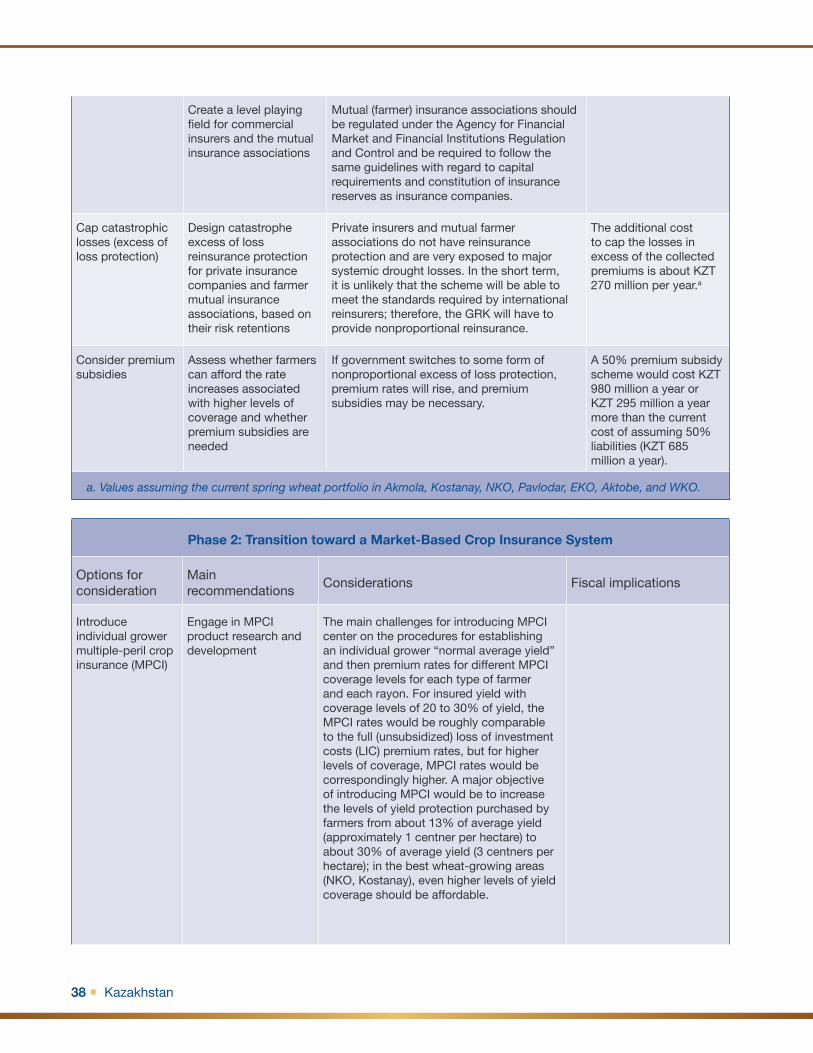

Measures to Cap Catastrophic Losses (Excess of Loss Protection)

38. Both the crop insurance companies and the farmer mutual crop insurance associations in Kazakhstan are very exposed to catastrophic losses that exceed their reserves, and options for enhanced reinsurance protection need to be considered. The GRK currently provides free proportional reinsurance protection equal to 50

box 2. options for streamlining and reducing the costs of policy marketing, preinspections, and loss assessment

introduce preinspections. A system of sample preinspections should be considered for large farms in northern Kazakhstan. Preinspections are needed in order to minimize moral hazard.

streamline loss notification and loss assessment procedures and make them more cost-effective. The law should be modified to simplify the loss notification obligations of the insured, to enable loss assessment functions to be managed by the insurance companies, and to streamline procedures and reduce the costs of loss assessment. A bonus-malus system should be introduced to dissuade farmers from submitting claims except where a major loss has occurred and is likely to lead to an indemnity.

use remote sensing to support in-field loss assessment. The National Space Agency (NSA) already applies remote sensing to estimate crop sown area, production, and yield for the MoA and to monitor crop status during the growing season. The crop insurance scheme managers should review potential supporting roles by the NSA in loss assessment.

review policy marketing and distribution channels with a view to reducing costs. Currently most policies are sold through local agents located in each oblast and subregion. The agents are currently paid 10 percent brokerage by law. Alternative crop insurance marketing and distribution channels should be promoted in order to reduce costs, including sales though cooperatives and farmer associations, input dealers, rural banks, and grain merchants.

offer farmer awareness programs on crop insurance. In conjunction with the proposed improvements in operating systems and procedures, greater emphasis needs to be placed on farmer awareness programs about the basis of insurance and indemnity in the current LIC program.

Source: Authors.

20 Kazakhstan

percent of the claims to the private insurance companies and mutuals in Kazakhstan. However, neither the private insurers nor the mutuals have any reinsurance protection on their 50 percent retentions, and they are therefore very exposed to major systemic drought losses. In the case of the private insurance companies, their abil-ity to absorb catastrophic losses is much higher than that of the mutuals because of their much larger size, their capital and claims reserves, and their diversified nonlife insurance portfolios, under which crop insurance only represents a fraction of their overall premium earnings and overall liability. In 2010 there is evidence that some mutuals could not meet their claims obli-gations in full because the claims exceeded their premium earnings: they therefore had to prorate down claims. There is an urgent need to design catastrophe excess of loss reinsurance protection for both the private insurance companies and the mutual associations on their 50 percent reten-tions through some form of nonproportional or stop-loss reinsurance protection.

39. In the short term, it is unlikely that the Kazakhstan obligatory crop insurance scheme will be able to meet the standards required to attract international reinsurers; therefore, any nonproportional reinsurance solutions will probably have to be provided by the GRK. Some indicative rating analyses were carried out for a GRK aggregate (that is, over the whole crop insurance scheme) stop-loss reinsurance protec-tion3 for spring wheat under the assumptions of the existing LIC scheme sum insured and actu-arially determined rates for priority levels of 70

3 Stop-loss reinsurance is a type of nonproportional reinsurance protection that is designed to cap an in-surer’s claims liability at a preagreed amount (value), which is referred to as the priority. Any claims above the priority are then transferred (ceded) to the rein-surer to settle, up to the limit of the reinsurer’s liability, which is defined in the reinsurance agreement. The priority is often expressed as a percentage of the pre-mium income that is underwritten by the insurance scheme, net of any policy cancellations and returns of premium; hence the term gross net premium in-come.

and 100 percent of gross net premium income (GNPI). This analysis was conducted separately, first assuming that Aktobe and WKO are includ-ed in the scheme and then assuming that they are excluded. Although this is a preliminary analy-sis, it is considered robust and suggests that the indicative costs of providing full value (that is, up to 100 percent of the total sum insured) ag-gregate stop-loss protection in excess of 100 percent and 70 percent priorities would be on the order of KZT 0.27 billion (US$1.8 million) to KZT 0.31 billion (US$ 2.1) per year (see chapter 4).

Premium Subsidies

40. If government were to switch its support from a share of 50 percent of claims to some form of nonproportional excess of loss protec-tion, the insurers would need to increase their premium rates and the GRK would need to consider whether such rates are affordable or whether premium subsidies are needed. Over the past six years, government’s 50 percent of claims liability was an average of KZT 685 mil-lion per year (US$4.6 million), but in severe drought years such as 2010, it was much higher, at KZT 1.4 billion (US$9.3 million), and the total cost was KZT 4.1 billion (US$27.3 mil-lion) in claims compensation. If instead, over the past six years, government had provided 50 percent premium subsidies, the total cost would have been somewhat higher, at KZT 5.86 billion (US$39.1 million) total, or an average of KZT 0.98 billion (US$6.5 million) per year.

41. The GRK should study very carefully the issues surrounding premium subsidies before deciding whether to switch from subsidizing claims to subsidizing premiums. In the current system, government compensates 50 percent of the claims costs and then caps premium rates at approximately 50 percent of the technically required rates. In some regions of the country, current premium rates are above the actuarially required rates and in others actual rates are far too low. On the one hand, this results in distorted crop insurance price signals in the market, and,

Agricultural Insurance Feasibility Study 21

on the other hand, the 50 percent claims compen-sation does not provide local insurers with the ca-tastrophe protection they need on their retained claims. Finally, international reinsurers are not willing to support an underpriced scheme. While the authors are very cautious about recommend-ing premium subsidies, it would be preferable in Kazakhstan to have an actuarially rated and commercially priced program and then for gov-ernment to decide whether to provide financial support in the form of premium subsidies, to provide nonproportional stop-loss reinsurance protection in the short term, and to promote the participation of international reinsurers in the medium term.

phase 2: transition toward a market-based crop insurance system

42. The proposed transition over the next few years to a market-based crop insurance system in Kazakhstan is centered on (1) the in-troduction of individual grower MPCI, either as a complement to or as a substitute for the current LIC policy and (2) the introduction of formal excess of loss reinsurance protection for the crop insurance industry. It is assumed that crop insurance would continue to be obligatory for farmers during this interim phase and that Aktobe and WKO would no longer be included in the scheme because spring wheat cannot be commercially insured in these two oblasts. It is intended that farmers in these two oblasts would be protected by a separate disaster relief mecha-nism.

Individual Grower MPCI Cover for Spring Wheat

43. The transition from the existing LIC cover to a more standardized individual grower MPCI policy would be relatively simple. The crop insurers of the LIC policy have gained con-siderable experience in underwriting loss of yield multiple-peril crop insurance and in conducting in-field loss assessment to establish actual yields and the amount of loss. This experience would enable them relatively easily to design, rate, and implement individual grower MPCI.

44. MPCI and LIC insurance products are slightly different. The main differences be-tween an individual grower MPCI product and the LIC policy include (a) the establishment of a preagreed insured yield at the time of policy subscription (the insured yield is usually calcu-lated as a percentage of the individual farmer’s historical average or normal crop yield or the local area average yield), (b) a preagreed unit valuation price, which is applied to the insured yield to calculate the sum insured, and (c) loss assessment, which involves measuring the ac-tual yield, comparing it to the insured yield, and indemnifying the amount of shortfall at the preagreed valuation price. Insurance and indem-nity procedures that are based on loss of yield are potentially much more transparent and un-derstandable for farmers than the existing LIC policy, and loss assessment is also much more objective, as yield loss is measured rather than expected shortfall in production costs and then compared to the estimated value of the remain-ing crop (salvage revenue).

45. The international experience is that MPCI is very popular with farmers, but be-cause the premiums associated with this prod-uct are high, most schemes depend on govern-ment support in the form of premium subsidies. The international literature on MPCI often high-lights the drawbacks encountered under volun-tary schemes of antiselection and moral hazard, the difficulties of establishing average farmer yields and corresponding premium rates, the high costs of premiums requiring government support in the form of premium subsidies, and the often very high costs of individual grower in-field loss inspection and loss assessment. While these arguments are indeed valid, they apply as equally to the existing LIC policy in Kazakh-stan. Currently, issues of antiselection are less of a problem because the scheme is obligatory for all farmers, but because it is a loss of yield multiple-peril scheme, it shares the drawbacks of other MPCI schemes.

46. In Kazakhstan, the main challenge for introducing individual grower MPCI centers

22 Kazakhstan

on the procedures for establishing an individ-ual grower “normal average yield” and then establishing premium rates for different MPCI coverage levels in each rayon. On the basis of international experience, it is believed that the quality of the rayon-level crop production and yield data in Kazakhstan is good enough to en-able the 17 years of data on spring wheat yield to be used to design and rate an individual grower MPCI program. As the historical rayon-level data on spring wheat crop production and yield are available for both production enterprises and commercial farmers, separate coverage levels and premium rates can be offered for each type of farmer, if required.

47. A detailed rating analysis was conducted for MPCI cover for spring wheat grown in the six main oblasts (excluding WKO and Aktobe) located in northern Kazakhstan. The statistical rating methodology used in this study to estab-lish individual grower MPCI rates conforms to the MPCI rating procedures used by the in-ternational crop insurance industry. The spring wheat MPCI rates presented in this report are indicative of commercial premium rates for a 60 percent target loss ratio, but final decisions over rates will be taken by insurers and their reinsurers. For insured yield coverage of 20 to 30 percent of yield, the MPCI rates would be roughly comparable to the full (unsubsidized) LIC premium rates, but for higher levels of cov-erage, rates would be correspondingly higher. See chapter 4.

48. It is likely that, if individual grower MPCI is introduced into Kazakhstan, the GRK will need to consider subsidies for the higher premiums. Chapter 4 makes some preliminary estimates of the costs to government under dif-ferent uptake scenarios.

Risk Financing and Reinsurance

49. If individual grower MPCI is introduced for spring wheat and other crops, and higher coverage levels and sums insured are offered to farmers, this would have important impli-

cations for insurers’ and government’s liabil-ity in the event of severe drought losses. For these reasons, a detailed analysis is conducted in chapter 4 of the PML associated with increased coverage levels for the spring wheat program. The analysis suggests that, for a maximum 50 percent coverage level, the expected losses that might occur every 10 years could be on the order of KZT 36.3 billion (US$242 million, or 17.13 percent of the value of the total sum insured, TSI), and for a 1-in-100-year PML, the expected loss could be on the order of KZT 99.7 billion (US$665 million, or 47 percent of TSI).

50. Given the exposure of spring wheat pro-duction to catastrophic drought risks in Ka-zakhstan, it is extremely unlikely that the in-surance sector would be willing to assume the increased liabilities implied under the proposed MPCI program unless the government is will-ing to provide reinsurance support for this ini-tiative. Currently, government is providing 50:50 quota-share reinsurance protection to the private commercial crop insurers and mutual crop insur-ers, but, as previously noted, this protection does not cap their exposure to catastrophic losses. Therefore, for the purposes of this study, some preliminary analyses were conducted for non-proportional stop-loss reinsurance protection for the spring wheat MPCI program.

51. Some preliminary modeling was con-ducted to establish the indicative pricing for aggregate stop-loss reinsurance protection for the spring wheat MPCI program. The modeling was conducted assuming full-value protection and priority levels of 70, 100, and 150 percent of Gross Net Premium Income, GNPI, for the four levels of MPCI insured yield coverage. The analysis found that, for a full-value aggregate stop-loss reinsurance protection for losses in ex-cess of 100 percent of GNPI, the stop-loss rein-surance pricing would be on the order of KZT 991 million (US$6.6 million) for 20 percent coverage, rising to KZT 5.8 billion (US$38.7 million) for 50 percent coverage. If the lower 70 percent of GNPI priority were adopted, the ag-

Agricultural Insurance Feasibility Study 23

gregate stop-loss pricing would be correspond-ingly higher.

52. In phase 2, it is possible that some of the larger private commercial crop insurers would be able to arrange their own reinsurance pro-grams with international reinsurers. If these insurance companies can demonstrate that, even under an obligatory crop insurance scheme, they are underwriting a balanced portfolio by risk and region, are adopting technically based MPCI rating, and have strengthened their MPCI loss assessment systems and procedures, then they should be able to arrange both proportional and nonproportional reinsurance through leading in-ternational reinsurers of this class of business.

phase 3: transformation into a commercial crop insurance pool scheme supported by international reinsurance

53. In the final phase, it is assumed that the scheme will be transformed into a fully mar-ket-based PPP agricultural insurance scheme. Central features of such a scheme would include (a) voluntary crop insurance, (b) formation of an agricultural pool coinsurance system to crowd in private commercial insurers (and possibly mutu-al crop insurers if they can conform to insurance market regulations), (c) a formal program of in-ternational reinsurance protection for the pool, and (d) suitable backing by the government, which might include financial support for pre-mium subsidies or catastrophe risk financing.

Transition from Obligatory to Voluntary Crop Insurance

54. As part of the transition to a market-based crop insurance system, policy makers in Kazakhstan will need to consider making crop insurance voluntary. Kazakhstan is one of a small minority of countries to adopt obligatory crop insurance and is almost unique in trying to implement obligatory crop insurance through the private commercial insurance sector. Inter-national experience suggests that agricultural in-

surance should be a voluntary class of insurance. In many countries (including India, the Philip-pines, and Mexico), the links between public sector provision of crop credit and crop insur-ance are very close, and banks make their lend-ing conditional on the farmer having crop insur-ance in place at the time of receiving the loan. In other words, crop insurance is mandatory for borrowers, but voluntary for nonborrowers.

55. If crop insurance is made voluntary in Kazakhstan, it is likely that there will be a ma-jor reduction in the demand for crop insurance in the short term, while the farming sectors ad-just to the realities of a demand-driven volun-tary crop insurance system. At this stage, it is not possible to predict how great the contraction in demand for voluntary crop insurance may be, but it is likely to be significant. Under a volun-tary system, crop insurers would be free to select which types of farmers, which crops, and which regions they are willing to underwrite.

Rationale for and Features of an Agricultural Insurance Pool in Kazakhstan

56. Coinsurance pools for agricultural in-surance have proved to be very popular with private and mutual insurers in many countries. Most notable are the Agroseguro pool in Spain,4 the TARSIM pool in Turkey, the livestock insur-ance pool in the Philippines, the hail insurance pool in Austria, and various other pool arrange-ments in Argentina, China, Malawi, Mongolia, and Ukraine.

57. The rationale for recommending the for-mation of a coinsurance pool in Kazakhstan centers on several key factors. These include the following:

The very small number of private com-a. mercial companies that are currently

4 Agroseguro stands for Agrupación Española de Entidades Aseguradoras de los Seguros Agrarios Combinados (Spanish Group of Insurance Entities of the Combined Agrarian Insurance).

24 Kazakhstan

supporting this scheme and the need to crowd in commercial insurers if crop in-surance is to remain a viable proposition in Kazakhstan. LIC/MPCI crop insurance is a catastrophe class of business, and many insurance companies are reluctant to risk their capital on it; however, under a pool agreement, individual companies can participate with very small shares of the overall risk if they wish.

The prohibitively high start-up invest-b. ment costs for individual insurance companies in creating their own internal crop underwriting and claims depart-ments and then in developing regional networks of marketing and sales agents to sell the product and trained crop in-spectors and loss assessors to implement the scheme. Pools offer the opportunity to create a single centralized insurance underwriting and claims management and loss assessment capability (often termed a managing underwriter company, MUC); individual members of the pool contrib-ute to the costs of running the MUC, while benefiting from the advantages of economies of scale.

The lack of common standards at the re-c. gional level in the underwriting of crop risks, especially with regard to the in-field loss assessment capabilities of indi-vidual insurance companies and farmer mutual insurance associations. Under a pool agreement, the MUC would be re-sponsible for coordinating all underwrit-ing and loss adjustment activities and for ensuring that common standards are ad-opted throughout the country.

A lack of consistency in crop rating and d. competition, which is driving down the crop insurance premium rates to unsus-tainable levels. Under a pool agreement, all insurers would issue standard crop insurance policies and would adopt the same premium rates for each crop in each zone and region.

The difficulties of arranging commercial e. international reinsurance protection for individual Kazakhstan insurance com-panies with very different underwriting standards and portfolios. Under a pool agreement, the MUC would purchase a single reinsurance program, which would lower the transaction costs and thus the cost of reinsurance.

58. There are also potential drawbacks to introducing pools to underwrite agricultural insurance. Classical economic theory would ar-gue that forming a pool (with monopolistic or oligopolistic tendencies) reduces competition, particularly over the pricing of insurance prod-ucts. These arguments do not apply directly to Kazakhstan, where there is currently no com-petitive market for agricultural insurance, a single product is available, and premium rates are fixed by law. While initially each member of the pool would offer standard crop insurance policies and uniform technical premium rates, the aim over several years would be to expand the range of crop insurance products available in the Kazakhstan market, to achieve economies of scale in key areas such as loss assessment, to lower commercial premium rates overall, and to improve the insurance services provided to farmers.

59. The proposed Kazakhstan agricultural insurance pool would involve the active par-ticipation of the public and private sectors. The central feature of the new system would be the creation of an agricultural coinsurance pool, which would be designed to underwrite all classes of agricultural insurance business. It is recommended that the pool coinsurers also cre-ate a separate managing underwriting company (MUC), which would be responsible for un-derwriting the scheme, handling premiums and loss assessment, settling claims, and negotiating reinsurance on behalf of members of the pool. Members would be responsible for marketing crop insurance through their sales distribution networks. The public sector, including the insur-ance regulator, the MoA, and the FFSA, would play very important roles in the proposed sys-

Agricultural Insurance Feasibility Study 25

tem. The FFSA would continue to act as the main public sector implementing agency for the scheme, but would no longer participate in field-level loss assessment; instead, it would (a) coor-dinate with the crop insurance pool’s MUC in the development of the technical studies required to design new crop, livestock, forestry, and aqua-culture insurance policies and programs, (b) manage the FFSA and disburse funds (including, as appropriate, premium subsidies and catastro-phe reinsured claims payments) to the MUC on behalf of the pool coinsurers, (c) maintain crop insurance underwriting and claims databases,

and (d) provide information and advice to farm-ers. An outline institutional framework for the agricultural insurance pool is shown in figure 2, which draws on the organizational structures of the Spanish and Turkish agricultural insurance pools.

60. Details of the proposed operating sys-tems and procedures for the Kazakhstan agri-cultural insurance pool are set out in chapter 4. The MUC would be responsible for the func-tions of product design and rating, underwriting and risk acceptance, claims administration, and

Source: Authors.

Figure 2 organizational Framework of the proposed agricultural insurance pool scheme

Find for Financial Support to Agriculture (FFSA)

Ministry of Agriculture Agency for Financial Market

and Financial Institutions Regulation and Control

Farmers Associations, Cooperatives, Rural Banks and other Aggregators Large Farmer production Enterprises

Small and Medium Farmers

Managing Underwriting Company