agenda - s23.q4cdn.com

TRANSCRIPT

Agenda

Wednesday, March 7, 2012

8:00-8:05am Welcome Coleen Tabor

8:05-8:35am Strategy Review and Business Update Jeff Turner

8:35-9:05am Financial Performance and Outlook Phil Anderson

9:05-9:25am Fuselage Segment: Operational Efficiency David Coleal

9:25-9:40am BREAK

9:40-10:00am Propulsion Segment: Value Engineering John Pilla

10:00-10:20 am Wing Segment: New Program Execution Alex Kummant

10:20-10:40 am 787 Program Update Terry George

10:40-11:00 am Aligning the Team for Success Sam Marnick

11:00-11:05 am Closing Remarks Jeff Turner

Forward-Looking Information

Cautionary Statement Regarding Forward-Looking Statements:

This presentation contains “forward-looking statements” that may involve many risks and uncertainties. Forward-looking statements reflect our current expectations or forecasts of future events. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “intend,” “estimate,” “believe,” “project,” “continue,” “plan,” “forecast,” or other similar words, or the negative thereof, unless the context requires otherwise. These statements reflect management’s current views with respect to future events and are subject to risks and uncertainties, both known and unknown. Our actual results may vary materially from those anticipated in forward-looking statements. We caution investors not to place undue reliance on any forward-looking statements. Important factors that could cause actual results to differ materially from those reflected in such forward-looking statements and that should be considered in evaluating our outlook include, but are not limited to, the following: our ability to continue to grow our business and execute our growth strategy, including the timing, execution and profitability of new programs; our ability to perform our obligations and manage costs related to our new commercial and business aircraft development programs and the related recurring production; margin pressures and the potential for additional forward-losses on aircraft development programs; our ability to accommodate, and the cost of accommodating, announced increases in the build rates of certain aircraft, including, but not limited to, the Boeing B737, B747, B767 and B777 programs, and the Airbus A320 and A380 programs; the effect on business and commercial aircraft demand and build rates of the following factors: continuing weakness in the global economy and economic challenges facing commercial airlines, a lack of business and consumer confidence, and the impact of continuing instability in global financial and credit markets, including, but not limited to, any failure to avert a sovereign debt crisis in Europe; customer cancellations or deferrals as a result of global economic uncertainty; the success and timely execution of key milestones such as deliveries of Boeing’s new B787 and first flight, certification and first delivery of Airbus’ new A350 XWB aircraft programs, receipt of necessary regulatory approvals, and customer adherence to their announced schedules; our ability to enter into profitable supply arrangements with additional customers; the ability of all parties to satisfy their performance requirements under existing supply contracts with Boeing and Airbus, our two major customers, and other customers and the risk of nonpayment by such customers; any adverse impact on Boeing’s and Airbus’ production of aircraft resulting from cancellations, deferrals or reduced orders by their customers or from labor disputes or acts of terrorism; any adverse impact on the demand for air travel or our operations from the outbreak of diseases or epidemic or pandemic outbreaks; returns on pension plan assets and impact of future discount rate changes on pension obligations; our ability to borrow additional funds or refinance debt; competition from original equipment manufacturers and other aerostructures suppliers; the effect of governmental laws, such as U.S. export control laws and U.S. and foreign anti-bribery laws such as the Foreign Corrupt Practices Act and United Kingdom Bribery Act, environmental laws and agency regulations, both in the U.S. and abroad; the cost and availability of raw materials and purchased components; our ability to successfully extend or renegotiate our primary collective bargaining contracts with our labor unions; our ability to recruit and retain highly skilled employees and our relationships with the unions representing many of our employees; spending by the U.S. and other governments on defense; the possibility that our cash flows and borrowing facilities may not be adequate for our additional capital needs or for payment of interest on and principal of our indebtedness; our exposure under our existing senior secured revolving credit facility to higher interest payments should interest rates increase substantially; the effectiveness of our interest rate and foreign currency hedging programs; the outcome or impact of ongoing or future litigation, claims and regulatory actions; and our exposure to potential product liability and warranty claims. These factors are not exhaustive and it is not possible for us to predict all factors that could cause actual results to differ materially from those reflected in our forward-looking statements. These factors speak only as of the date hereof, and new factors may emerge or changes to the foregoing factors may occur that could impact our business. As with any projection or forecast, these statements are inherently susceptible to uncertainty and changes in circumstances. Except to the extent required by law, we undertake no obligation to, and expressly disclaim any obligation to, publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. You should review carefully the sections captioned “Risk Factors” in our 2011 Form 10-K filed February 23, 2012 for a more complete discussion of these and other factors that may affect our business.

Jeff Turner

President and Chief Executive Officer

March 7, 2012

Strategy Review and Business Update

Strong, Experienced Team

Spirit AeroSystems Executive Leadership

= Presenting Today

2

Division of $67B company

Controlling some of the costs

100% Boeing supplier

Part of a duopoly

Cost center

Cost manager

Independent ~$5.2B Company

Controlling all of the costs

Global industry partner

Multiple customers

Multiple competitors

Profit maker

Low-cost leader

From To

June 2005 2012

Focused on Execution, Growth and Diversification

Transformation and Growth

3

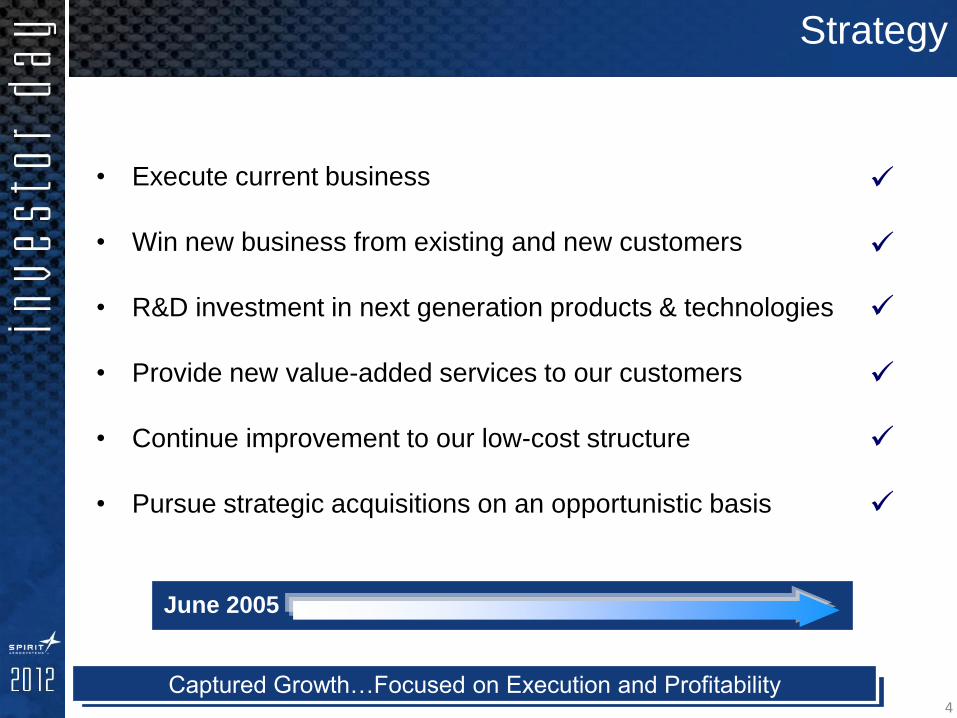

• Execute current business

• Win new business from existing and new customers

• R&D investment in next generation products & technologies

• Provide new value-added services to our customers

• Continue improvement to our low-cost structure

• Pursue strategic acquisitions on an opportunistic basis

June 2005

Captured Growth…Focused on Execution and Profitability

Strategy

4

8 Comprehensive AeroStructures Partner… Design and Build

Executing the Core Business

5

~ 1,300 HARDWARE PRODUCTION & DESIGN SUPPLIERS

Spirit Worldwide Operations / Aftermarket

Worldwide Supply Base

Competing Globally with Global Resources

Successful Management of Global Supply Chain

~ 1,400 Hardware Production & Design Suppliers

6

Global Resources

Air Traffic Growth

Strong Long-Term Growth

0

2

4

6

8

10

12

14

1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

RP

Ks

(tr

illio

n)

20-year global

traffic growth

CAGR 4.9%

Forecast: 2x

air traffic in 15

years

Source: Airline Monitor, Spirit analysis

7

Strong Demand for Replacements & Growth Airplanes

Source : Boeing 2011 Commercial Market Outlook 8

Spirit’s Core Business

Well Positioned on Best Selling Commercial Airplanes

B737 B747

B777

B767

A320 A380

= Spiri t Responsibility

Shipset Value: $5.6–7.5MM Shipset Value: $8.4–14.6MM Shipset Value: $4.0–6.9MM

Shipset Value: $10-11.3MM Shipset Value: $0.9–1.4MM Shipset Value: $1.2MM

9

Delivered forward fuselage unit #60 to Charleston, SC

Excellent overall product quality

The 787-9 activities are progressing

Continuing to work with supply base in preparation for production ramp-up

Focused on cost reduction initiatives

787

787 Forward Fuselage Cockpit = Spirit Responsibility

787 Forward Fuselage

Growth with Boeing

Successfully Expanding Our Capabilities 10

Shipset Value: $8.0-12.0MM

A350 XWB

Design and build A350 XWB Section 15 and wing front spar in new state-of-the-art composites facility

Initial fabrication of production units underway

Shipped first production center fuselage panels from our North Carolina facility to our Saint-Nazaire, France facility for assembly in 2011, delivered to the customer in the first quarter

Shared investment between Spirit, Airbus, suppliers and local governments

Foundation for future composites expansion

Saint-Nazaire, France

Kinston, North Carolina

Growth with Airbus

= Spirit Responsibility

Leveraging Our Design and Build Capability to New Customers 11

Shipset Value: $4.0-5.0MM

Diversification Platforms

Partnering With Market Leaders

Gulfstream G280

Gulfstream G650 Mitsubishi Regional Jet (MRJ)

Bombardier CSeries

Sikorsky CH-53K

Boeing P-8A Poseidon

Business / Regional Jets Military

= Spiri t Responsibility

Shipset Value: $1-2MM

Shipset Value: 5.5-6.5MM

12

Sikorsky CH-53K Heavy Lift Helicopter Boeing P-8A Poseidon

Design-Build Composite

Cockpit and Cabin Design-Build

Fuselage

First Unit Delivered To Customer

Expanding Into New Markets

Military Aircraft Development

13

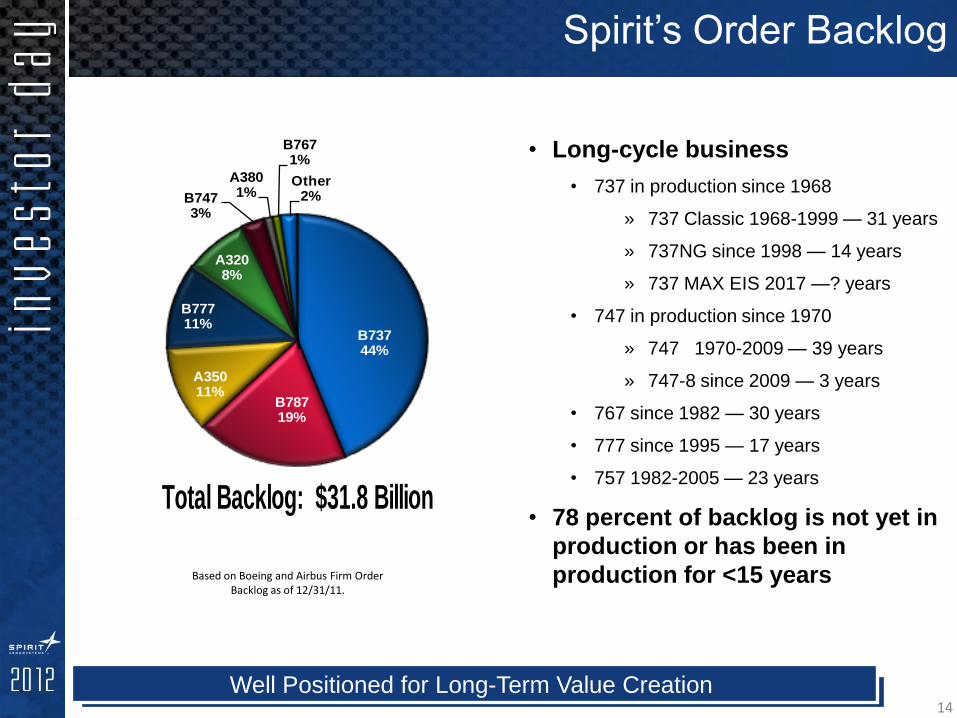

17 Well Positioned for Long-Term Value Creation

• Long-cycle business

• 737 in production since 1968

» 737 Classic 1968-1999 — 31 years

» 737NG since 1998 — 14 years

» 737 MAX EIS 2017 —? years

• 747 in production since 1970

» 747 1970-2009 — 39 years

» 747-8 since 2009 — 3 years

• 767 since 1982 — 30 years

• 777 since 1995 — 17 years

• 757 1982-2005 — 23 years

• 78 percent of backlog is not yet in

production or has been in

production for <15 years

B73744%

B78719%

A35011%

B77711%

A3208%

B7473%

A3801%

B7671%

Other2%

2244

Total Backlog: $31.8 Billion

Based on Boeing and Airbus Firm Order Backlog as of 12/31/11.

Spirit’s Order Backlog

14

18 Extending the Life of Successful Platforms

737 MAX

Entry into Service 2017

Substantially the same content as 737 NG

68-inch fan diameter — improved operating efficiencies

Feb 2012 - To date, the 737 MAX has orders and commitments for more than 1,000 airplanes from 15 customers

= Spirit Responsibility

737 MAX 9

737 MAX 8

Spirit’s Order Backlog…Extending

15

Growing Core Market

High Growth Platforms, Backlog Growth

Executing New Business

Leading the Outsourcing Trend

787 Content

Growth Through Core Business Expansion and Diversification

Long-Term Value Creation

16

17

Phil Anderson

Senior Vice President &

Chief Financial Officer

March 7, 2012

Financial Performance and Outlook

Agenda

• Executing the strategy

• Financial Performance

• Growth, Profitability, and New Programs

• 2012 Financial Guidance

2

Executing The Strategy

3

Development 5-7 years

1-2 Years

20-30 Year Product Lifecycles

Full Production 12 – 21 Years Initial

Production

A350 XWB

CSeries Pylon

MRJ Pylon

CH-53K

787

G280

G650

BR725

P-8

747-8

Core Business

737

777

767

A320

A330/A340

A380

High Reducing Financial

Risk

Generated

over $2B in Cash since

2005

Aggressively invested In growth and diversification…

More selective going forward

Business Risk

Mitigation

Contracting

Program Mgmt

Execution

Change Control

Capital Structure and

Liquidity Mgmt

Mitigation

Backlog Management

Production Rate Management

Reduce capital intensive nature of the business

Move to more variable costs

Proactive capital structure and liquidity management

Re-invested in new

programs

Economically sensitive, cyclical

Quality Products, Capable and Reliable Supplier — Financially Strong

Investing in Core Business Growth

Investing in diversification and

managing to risk

Str

ate

gy E

xe

cu

tio

n

Ris

k M

an

age

me

nt

1

2

3

4

5

6

7 8

9 10

Total Ship Set Deliveries by Year Ship Set Deliveries by Customer

Rate Increases Driving Higher Deliveries

5 Year Delivery Trend

4

520

520

49 -

200

400

600

800

1,000

1,200

2007 2008 2009 2010 2011S

hip

Se

t D

eli

ve

rie

s

Boeing Airbus Other

963 978 1,029

969

1,089

-

200

400

600

800

1,000

1,200

2007 2008 2009 2010 2011

To

tal

Sh

ip S

et

De

liv

eri

es

by

Ye

ar

Financial Results

One time Impacts

Annual Revenues

(1.8)%

10.9% 10.8%

7.4%

8.6%

7.3%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

2006 2007 2008 2009 2010 2011

Operating Margin

$0.14

$2.13 $1.91

$1.37 $1.55

$1.35

$2.00-$2.15

$-

$0.50

$1.00

$1.50

$2.00

$2.50

2006 2007 2008 2009 2010 2011 2012F

EPS (Fully Diluted)

5

One time impacts

Core Business and 787 Growth

Guidance

Guidance

Volume Driven Growth — Development Efforts Impacting Earnings

$3,208

$3,861 $3,772 $4,079 $4,172

$4,864

$5,200-$5,400

$-

$1,000

$2,000

$3,000

$4,000

$5,000

2006 2007 2008 2009 2010 2011 2012F

In M

illio

ns

Financial Results

* Partial Year Results… Spirit began operations on June 17, 2005

$224

$274

$180

$211

($14)

$125

($47)

>$300

($50)

$0

$50

$100

$150

$200

$250

$300

$350

2005* 2006 2007 2008 2009 2010 2011 2012F

In M

illio

ns

Cash Flow from Operations Capital Expenditures

$145

$343

$288

$236 $228

$288

$250 ~$250

$0

$50

$100

$150

$200

$250

$300

$350

2005* 2006 2007 2008 2009 2010 2011 2012F

In M

illio

ns

6

Guidance

Guidance

Strong Cash Flow From Core Business — Reinvesting for Growth

Strong core business cash flow

Customer Advances Advance Repayments

New Program Investments

Volume Increase Dri

vers

New Program Investments

Capacity

Expansion

Maintenance Capital

Dri

vers

Financial Results

Solid Balance Sheet to Support Diversification, Growth and Cyclicality

* Partial Year Results… Spirit began operations on June 17, 2005

$722 $618 $595 $588

$894

$1,197 $1,201

$241 $184

$133 $217

$369

$482

$178

$-

$200

$400

$600

$800

$1,000

$1,200

2005* 2006 2007 2008 2009 2010 2011

In M

illio

ns

Debt Cash

Cash/Debt Balances Net Debt to Capital

7

Customer Advances Advance Repayments

Bond Issuancse

Credit-line

$650M

IPO and Customer Advances Stand Alone Financing

Dri

vers

60%

34%

27%

22%25%

28%

34%

0%

10%

20%

30%

40%

50%

60%

70%

2005* 2006 2007 2008 2009 2010 2011

Growth and Profitability

8

5 Year Growth Trend

9

Program 2007

Deliveries

2011

Deliveries

%

Delivery

Growth

737 331 377 14%

777 83 78 (6%)

767 13 23 77%

747 18 17 (6%)

787 1 25 2,400%

A320 359 403 12%

Revenue 5 Year Growth Drivers

Core Business Growth

Market Demand Accelerating Growth Trend

10

Program 2011

Deliveries

Customer Announced

Rates

% Delivery Growth

737 377 42 / Month 34%

777 78 8.3 / Month 28%

767 23 2 / Month Hold

747 17 1.5 / Month Hold

787 25 10 / Month 380%

A320 403 42 / Month 25%

New Programs

Business Jets

Initial Production

Increasing Growth

A350 XWB Initial Production

Increasing Growth

Other New Programs

Initial Production

Revenue Growth Outlook

Growth Accelerating to Fill Strong Market Demand

2012

Guidance

Projected

9.7% 9.9%9.3%

10.5%9.6%

8.3%

11.2%

10.0%

0%

2%

4%

6%

8%

10%

12%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

Adjusted Operating Margins

Solid Core Operating Margins On Growing Volume

11

$M 1Q 2Q 3Q 4Q 1Q 2Q* 3Q 4Q

Revenue 1,043 1,056 1,002 1,071 1,050 1,466 1,130 1,219

GAAP

Operating

Income

93 86 82 96 70 64 121 102

New Program

Charges 3 28 53 10 41

Other 8 19 11 13 3 4 (4) (21)

Adjusted Op.

Income 101 105 93 112 101 121 127 122

Adjusted Op.

Margin 1.

9.7% 9.9% 9.3% 10.5% 9.6% 8.3% 11.2% 10.0%

* Includes the impact of 787 MOA

2010 2011

2010 2010 2011 2011

Revenue Operating Margins

1. Non-GAAP measure. Definitions, reconciliations, and further disclosures regarding this non-GAAP measure are appended to this document.

New Program Investments and Inventory

12

Spirit Programs

New Program Diversification Strategy 13

• Revenues and costs projected for

contract block (fixed # of units)

• As contract matures, includes

actual and projected costs

• SPR revenue reconciliation on

units shipped

• Book profit margins reflect average

gross profit

• Difference between actual and

average cost reflected in inventory

• SPR updates profit estimates

every quarter

Revenue

Average

Gross Profit

Actual Cost

exceeds Average

so Inventory

builds

Average Cost

Actual Cost

below

Average so

Inventory declines

Units Delivered/Time

Revenue &

Cost/Unit

New Progams Contract Block Units

787 500

G650 350

G280 250

BR725 350

747-8 56

14

Contract Accounting New Program Perspective

Most Important SPR Accounting Policy

146 280

418 441 485 495 475

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2006 2007 2008 2009 2010 2011 2012F 2013F

$ M

illi

on

Capitalized Pre-production

694 1,006

1,302 1,309 1,263 1,323 1,225

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2006 2007 2008 2009 2010 2011 2012F 2013F

$ M

illi

on

Physical InventoryIncludes Non-recuring Production Costs

42 57 162

457

760 813

1,150

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2006 2007 2008 2009 2010 2011 2012F 2013F

$ M

illi

on

Deferred Inventory

882

1,343

1,882

2,207

2,508 2,631

2,850

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2006 2007 2008 2009 2010 2011 2012F 2013F

$ M

illi

on

Total Inventory

Inventory Trend and Outlook

15

New Program Investment Peaking

Total Inventory Deferred Inventory

Physical Inventory Includes Non-recurring Production Costs

Capitalized Pre-Production

~

~

~

~

Reinvesting For Growth and Diversification

Cash Flow from Operations

16

Excludes 787 MOA settlement cash received in 4th quarter 2010

As reported

Financial Guidance

Guidance

Improving Cash Flow

Strong core business cash flow increasing

Advance repayments moderating

New program investments peaking

Dri

vers

1. Non-GAAP measure. Definitions, reconciliations, and further disclosures regarding this non-GAAP measure are appended to this document.

1.

Financial Guidance

17

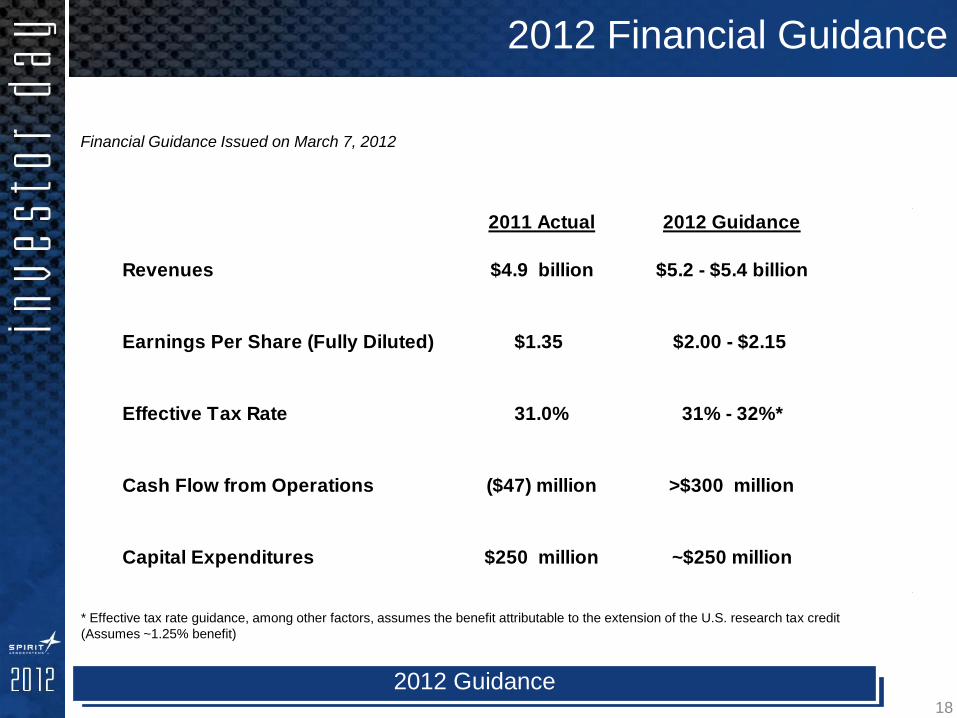

2012 Financial Guidance

2012 Guidance

Financial Guidance Issued on March 7, 2012

* Effective tax rate guidance, among other factors, assumes the benefit attributable to the extension of the U.S. research tax credit

(Assumes ~1.25% benefit)

18

2011 Actual 2012 Guidance

Revenues $4.9 billion $5.2 - $5.4 billion

Earnings Per Share (Fully Diluted) $1.35 $2.00 - $2.15

Effective Tax Rate 31.0% 31% - 32%*

Cash Flow from Operations ($47) million >$300 million

Capital Expenditures $250 million ~$250 million

Revenue

Gross Profit Margins

• Significant growth from 787 and new programs moving to production

• Growth from core program rate increases

• Incremental margin improvement in new accounting blocks

• Moving work to lower-cost locations (Malaysia, North Carolina)

• Modest labor cost increases expected in current environment

• Dilutive new program margins

SG&A/R&D • Combined SG&A and R&D 4% - 4.25%

Free Cash Flow

• Liquidated first tranche of 787 advances and spread second tranche over

1,000 units

• New programs move to revenue generating production units

• New program investment peaking

• 737 MAX investment

• Opportunities to improve inventory turns for legacy programs

• No pension funding anticipated for U.S. defined benefit plan

Post 2012 Financial Trends

Top Line Growth & Cash Generation 19

Financial Summary

• Captured Growth

• New program investment peaking

• Moving to positive cash flow

• Looking Forward…

– Focused on productivity and efficiency

– More modest investment environment… Product refresh

– Be more selective on “clean sheet” design opportunities

– Continue to proactively manage capital structure and liquidity

20

40 Executing Our Strategy

Business Summary

• Strong long-term market demand

• Strategically positioned on best programs in commercial

aerospace

• Revenue growth projected as market demand increases

• Core business driving earnings growth and strong cash flows

• Continuing to manage development program risk

• Financially strong

21

41 Delivering Value

22

23

Non-GAAP Measure Disclosure

Management believes that the non-GAAP (Generally Accepted Accounting Principles) measures (indicated by 1) used in this

report provide investors with important perspectives into the company’s ongoing business performance. The company does

not intend for the information to be considered in isolation or as a substitute for the related GAAP measure. Other companies

may define the measure differently.

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Revenue (GAAP) 1,043.3$ 1,056.0$ 1,002.0$ 1,071.1$ 1,049.6$ 1,465.6$ 1,129.7$ 1,218.9$

Operating Income (GAAP) 93.0$ 85.7$ 82.4$ 95.9$ 69.6$ 63.6$ 120.5$ 102.4$

New Program Charges

Gulfstream G280 2.8$ 53.3$ 28.5$

Sikorsky CH-53K 28.2$ 10.0$ (9.2)$

B747-8 18.3$

B787

A350 XWB 3.0$

Total New Proram Charges -$ -$ -$ 2.8$ 28.2$ 53.3$ 10.0$ 40.6$

Other

Cumulative Catch 8.2$ 4.2$ 10.1$ 3.1$ (6.3)$ (3.7)$ (21.2)$

Warranty and Extranordinary Rework 9.0$

IAM Stock Compensations 18.9$

IAM Early Retirement Incentive 6.5$

UAW Stock Compensation 3.3$

UAW Early Retirement 1.8$

Total Other 8.2$ 18.9$ 10.7$ 13.4$ 3.1$ 4.5$ (3.7)$ (21.2)$

Total 8.2$ 18.9$ 10.7$ 16.2$ 31.3$ 57.8$ 6.3$ 19.4$

Adjusted Operating Income 101.2$ 104.6$ 93.1$ 112.1$ 100.9$ 121.4$ 126.8$ 121.8$

Adjusted Operating Margin 9.7% 9.9% 9.3% 10.5% 9.6% 8.3% 11.2% 10.0%

12/31/2010

Cash Flow From Operations (GAAP) 125.1$

Boeing Memorandum of Agreement ("MOA") (236.2)$

Cash Flow From Operations Excluding MOA (111.10)$

2010 2011

David Coleal

Senior VP / General Manager

Fuselage Business Segment

March 7, 2012

Fuselage Segment: Operational Efficiency

2

Fuselage Segment

Boeing 747

Boeing 777

Boeing 787

Boeing 737

Boeing 767 Sikorsky

Airbus A350 XWB

Fuselage Segment Perspective

$2,425.0

$1,221.5

$1,207.8

Fuselage Propulsion Wing

2011 Revenues

$1,570.0

$1,790.7 $1,758.4

$2,003.6 $2,035.1

$2,425.0

$-

$500.0

$1,000.0

$1,500.0

$2,000.0

$2,500.0

$3,000.0

2006 2007 2008 2009 2010 2011$

Mill

ion

Fuselage Revenues

3

$ Million

Strong Core Business Growth

Excludes All other segment income of $9.5M

• Reduce Operating Costs and Improve Product Quality to Increase

Margins and Enhance Customer Satisfaction

• Engage/Optimize Supply Base to Meet Initiatives

• Lead New Programs for Manufacturable / On Schedule / Cost

Efficient Product to Ensure Profitability

• Engage and Develop our Employees / Leaders to Maximize

Performance

• Document, Share and Deploy Best Practices to Achieve

Functional Excellence (SQCDT)

Fuselage Segment Focus

4

Value Engineering

Operational

Discipline Lean Maturity

• Design For Manufacturing

• Knowledge Based

Engineering

• Functional Excellence

• Spirit EXACT

• Daily Communication

• Rapid Problem Solving

• Focused Execution

• Employee Engagement

• Leadership Visibility

• Growth Platform for

Lean

• Continuous Improvement

• Waste Reduction

• Flow Reduction

• Improved Quality

• Cost Reduction

• Customer Satisfaction

Engaged Workforce

Operational Efficiency Model

Keys to Continued Success

5

Daily Operational Discipline

Rapid Communication & Problem Solving at All Levels 6

Lean Maturity Approach

Focus on an Engaged Team….All the Time! 7

Oklahoma Slat Moving Line • Labor efficiency

• Optimized flow

Prestwick

Automated Drilling • Improved quality

• Reduced testing

• Structural optimization

Propulsion Streamlined Parts Cleaning

• Reduced flow

• Reduction of hazardous waste

Fuselage Pull Production System •Reduced inventory

•Increased throughput

•Lower overtime

Lean Maturity Across Spirit

Improving Efficiency Across the Company

Malaysia 787 Fixed Leading Edge

• Inventory reduction

• Improved cycle time

• Labor/shipping cost reduction

8

9

John Pilla

Senior VP / General Manager

Propulsion Business Segment

March 7, 2012

Propulsion Segment: Value Engineering

Propulsion Segment

Boeing 787 Boeing 767

Boeing 777 Boeing 737

Boeing 747

Gulfstream 650

Bombardier C-Series

Mitsubishi MRJ

2

Propulsion Segment Perspective

2011 Revenues Propulsion Revenues

$887.7

$1,063.6 $1,031.7 $1,030.0 $1,061.8

$1,221.5

$-

$200.0

$400.0

$600.0

$800.0

$1,000.0

$1,200.0

$1,400.0

2006 2007 2008 2009 2010 2011

$ M

illi

on$2,425.0

$1,221.5

$1,207.8

Fuselage Propulsion Wing

3

$ Million

Strong Core Business Growth

Excludes All other segment income of $9.5M

• Reduce Operating Costs and Improve Product Quality to Increase

Margins and Enhance Customer Satisfaction

• Engage/Optimize Supply Base to Meet Initiatives

• Lead New Programs for Manufacturable / On Schedule / Cost

Efficient Product to Ensure Profitability

• Engage and Develop our Employees / Leaders to Maximize

Performance

• Document, Share and Deploy Best Practices to Achieve

Functional Excellence (SQCDT)

Propulsion Segment Focus

4

Value Engineering

Keys to Continued Success 5

Value Engineering

Operational

Discipline Lean Maturity

• Design For Manufacturing

• Knowledge Based

Engineering

• Functional Excellence

• Spirit EXACT

• Daily Communication

• Rapid Problem Solving

• Focused Execution

• Employee Engagement

• Leadership Visibility

• Growth Platform for

Lean

• Continuous Improvement

• Waste Reduction

• Flow Reduction

• Improved Quality

• Cost Reduction

• Customer Satisfaction

Engaged Workforce

Design Develop Produce

$

Greatest Impact

Program Phases

Design For Manufacturing

Investing Up Front for Long Term Production Benefits 6

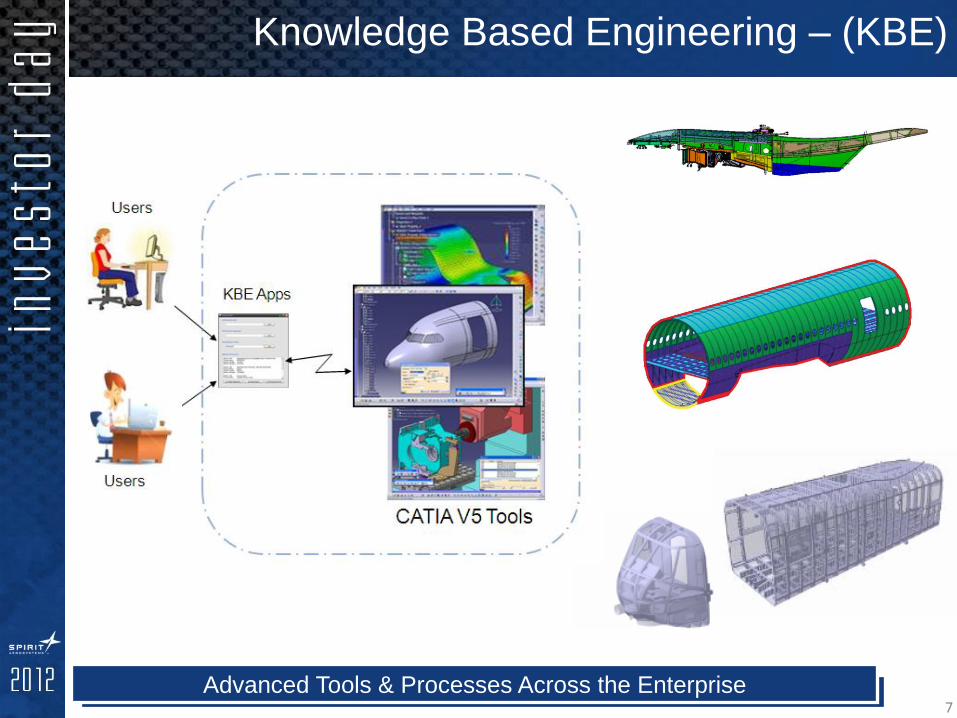

Knowledge Based Engineering – (KBE)

Advanced Tools & Processes Across the Enterprise 7

Spirit Exact

Spirit Exact Reduces Cost , Variation, and Lead Time 8

Detail Tooling • Part location & measurement

• Framework for drill plate support

Automated Tooling • Self-locating parts

• Flexible robotic drilling

™

Value Engineering

9

Spirit developed this patent pending

Inflexion™ reconfigurable tooling process

to enable high levels of part integration with

lower manufacturing costs than traditional

tooling approaches.

™

Enabling Fully Integrated Structures

10

Alex Kummant

Senior VP/ General Manager

Oklahoma Operations

March 7, 2012

Wing Segment: New Program Execution

Wing Segment

2

Boeing 777

Gulfstream 650

Boeing 747

Boeing 787

Gulfstream 280

Airbus A320

Airbus A380

Boeing 737

Wing Segment Perspective

2011 Revenues Wing Revenues

$2,425.0

$1,221.5

$1,207.8

Fuselage Propulsion Wing

$720.3

$985.5 $955.6 $1,024.4

$1,067.4

$1,207.8

$-

$200.0

$400.0

$600.0

$800.0

$1,000.0

$1,200.0

$1,400.0

2006 2007 2008 2009 2010 2011

$ M

illio

n

3

$ Million

Strong Core Business Growth

Excludes All other segment income of $9.5M

• Reduce Operating Costs and Improve Product Quality to Increase

Margins and Enhance Customer Satisfaction

• Engage/Optimize Supply Base to Meet Initiatives

• Lead New Programs for Manufacturable / On Schedule / Cost

Efficient Product to Ensure Profitability

• Engage and Develop our Employees / Leaders to Maximize

Performance

• Document, Share and Deploy Best Practices to Achieve

Functional Excellence (SQCDT)

Wing Segment Focus

4

Spirit Strategy

•Boeing Products – Seattle, WA

– 737

– 777

– 747

– 787

•Gulfstream – Savannah, GA

– G650

•IAI - Tel Aviv, Israel (Gulfstream)

– G280

•Airbus - Europe

– A320

– A350

– A380

North Carolina

Prestwick, Scotland

Malaysia

McAlester

Tulsa

IAI Legacy Airbus GAC Bus Ops Strategy

Aero Strategy

Boeing

Global Market

Team Aligned to Focus on Customer and Cost 5

Executing the Business Strategic Placement Lean Investment Plant Floor Evolution

A320 787

200+ Lean Events for 2012 737 Slat Moving Line

A380 737 777 747

Executing Core Business

6 Focused on Continuous Improvement

• 737 stationary tools

• Limited floor space

• Interrupted product flow

• Limited lighting

• Optimized moving product flow

• Improved lighting/quality

• Operational effectiveness

Talladega Assembly Line

737 Flaps and Slats Program

7

• Fixed Leading Edge line transition to Malaysia

• Incorporating improvements

• Work-in-Process reduction

• Improved cycle time and delivery flow

• Labor and shipping cost reductions

Fixed Leading Edge

Detailed Assembly

787 Wing Leading Edge Program

8

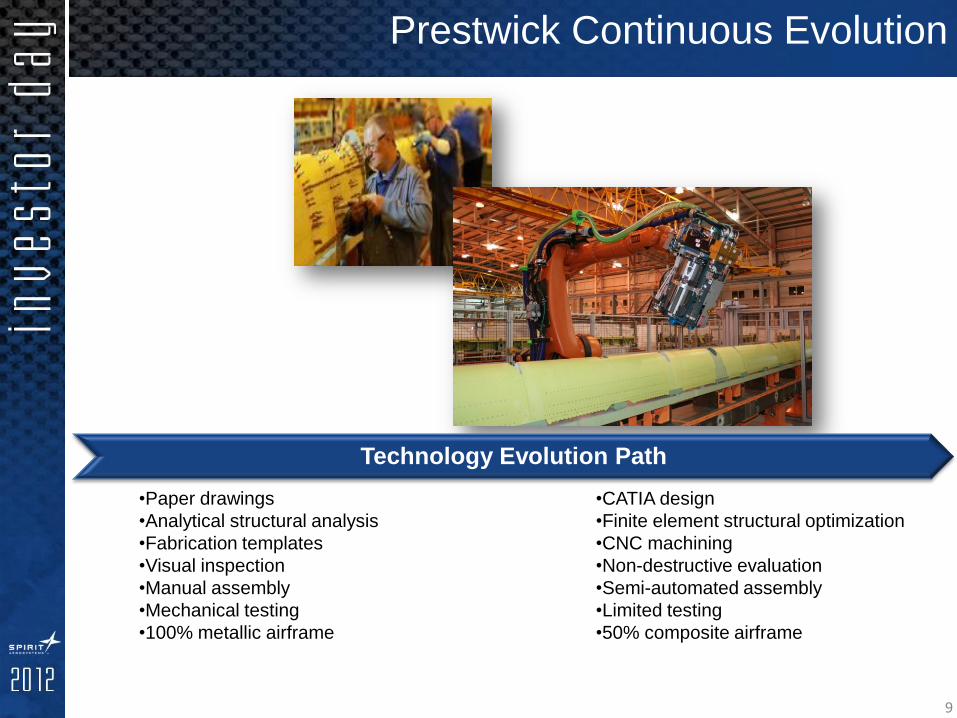

•Paper drawings

•Analytical structural analysis

•Fabrication templates

•Visual inspection

•Manual assembly

•Mechanical testing

•100% metallic airframe

•CATIA design

•Finite element structural optimization

•CNC machining

•Non-destructive evaluation

•Semi-automated assembly

•Limited testing

•50% composite airframe

Prestwick Continuous Evolution

Technology Evolution Path

9

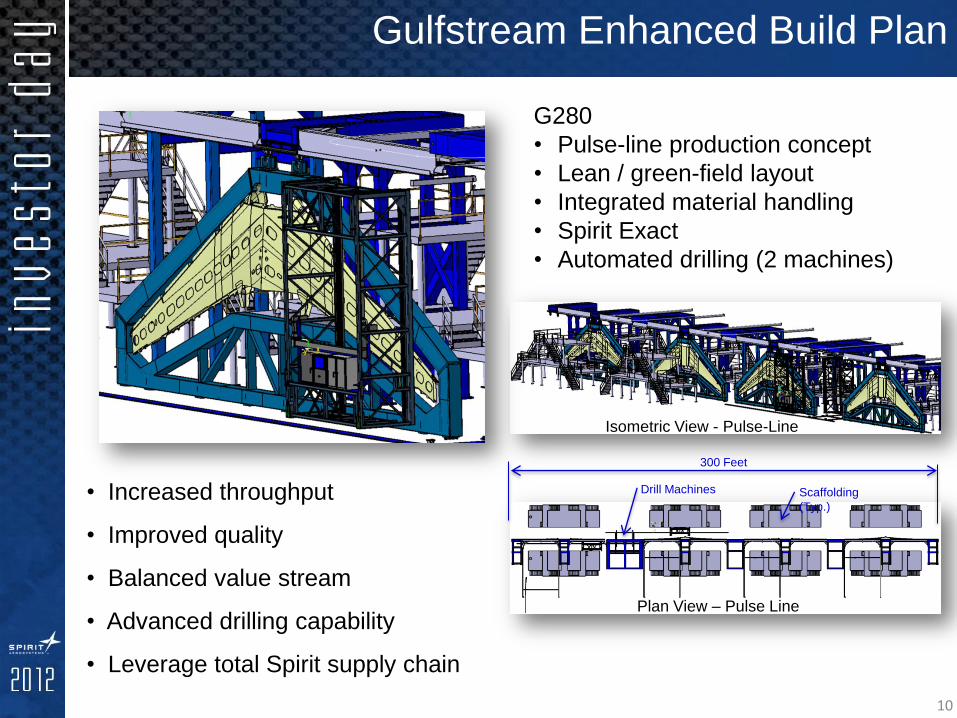

G280

• Pulse-line production concept

• Lean / green-field layout

• Integrated material handling

• Spirit Exact

• Automated drilling (2 machines)

• Increased throughput

• Improved quality

• Balanced value stream

• Advanced drilling capability

• Leverage total Spirit supply chain

Isometric View - Pulse-Line

Plan View – Pulse Line

Scaffolding

(Typ.)

Drill Machines

300 Feet

Gulfstream Enhanced Build Plan

10

• Supply chain improvements

• Technology development

• Early start to -1000

• Full implementation of Spirit Exact

• Flawless fit-up of parts

• Ease of integration with Center Wing Box

A350 XWB Leading Edge Spar

• Technology validated

• Achieved mass targets

• In series production

• Strong schedule position

• Few defects

• Rate capable

• Spirit Exact-integration with Fixed Leading Edge

• Common wing & -1000 next up

A350 XWB Section 15

Customer Response to Product

11

Spirit France

Up-front Program Planning

Capture and Manage Program

Requirements

Program Execution

Change Management

Training and Coaching

On Time, Profitable New Program Execution

•Program

management plan

•Gated review

process

•Value stream

mapping

•IPT/Org Identified

•Manage OEM’s

requirements

•System

Engineering

•Team center SE

tool

•Contracting

•Integrated

program schedules

•Earned value

management

•Life cycle

management

•Risk , Issue &

Opportunity

•Accountability

•Electronic

document

management

•Change boards

•Robust Change

Management

•Knowledge

sharing

•Customer

Relationship

Management

•Critical Chain

Scheduling

•PMBP Training

Program Management Best Practices

12

New Program Execution

13

Terry George

Vice President 787 Program

March 7, 2012

787 Program Update

787 Program Summary

2

Boeing 787

• 787-8 certified and in-service

• 787-9 in development

• Strong customer base and order backlog

• 870 orders with 56 identified customers

Strong Customer Demand Strong Customer Demand

555, 64%

315, 36%

787-9

787-8

787 Orders

As of: February 2012

Source: Boeing website

Spirit 787 Statement of Work

3 Strong Customer Demand Design, Build and Deliver Flight Ready Structures

• Forward Fuselage

• Delivered ship set #59 to Everett, WA

• Delivered ship set #60 to Charleston, SC

• Excellent condition of assembly

• Planning to deliver approx. 40 Fuselage ship sets in 2012

• Engine Pylons

• Delivered ship set #62

• Wing Components

• Fixed leading edge ship set #75 and moveable leading edge

#61 delivered

• Engineering

• Beginning to Release Engineering for the 787-9 Derivative

Spirit 787 Program Update

4

Forward Fuselage double load — February 2012

Spirit’s Industry Leading Capability

5 Strong Customer Demand Demonstrated Quality, Capability, Reliability and Partnership

In-Service Support

Integrated Supply

Chain Management

Product

Design

Carbon Fiber

Fight Deck

Forward

Fuselage

Delivery

Fully integrated supply chain

World class production

Large-Scale

Automation and

Manufacturing

From design using

base materials…

To fully installed,

operational flight

deck…

To reliable delivery

and support

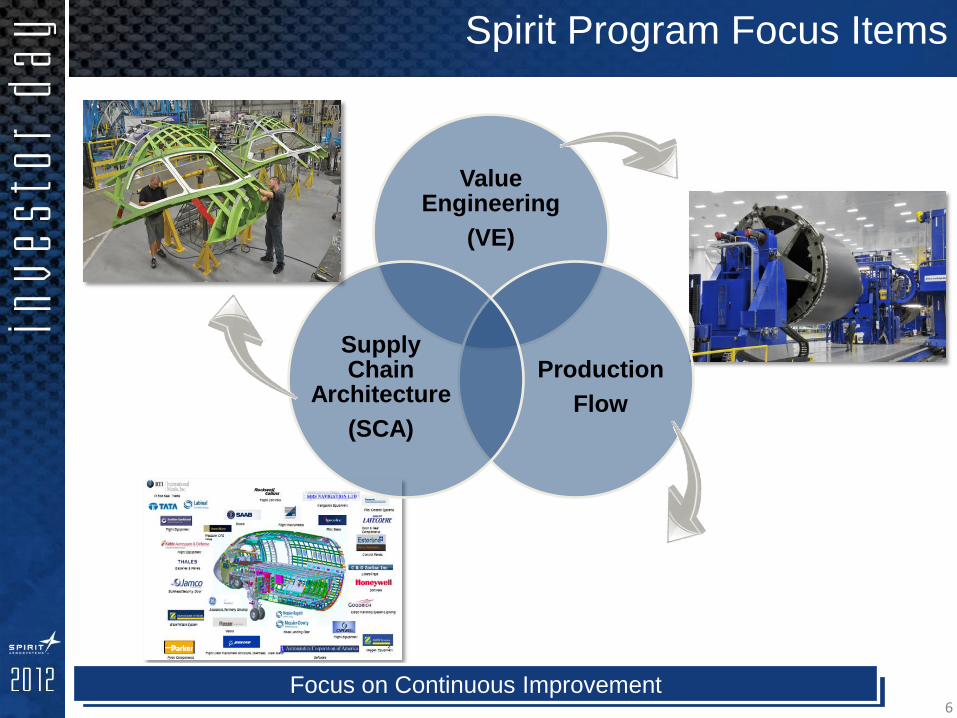

Value Engineering

(VE)

Production

Flow

Supply Chain

Architecture

(SCA)

Spirit Program Focus Items

6

NWW FWD Bulkhead Bolt to Rivet Monolithic Cab Focus on Continuous Improvement

3.5apm 7.0apm 10apm 5.0apm

Rate Readiness Overview

7 Robust Rate Readiness Planning

People Ready

Supply Chain Ready

Factory Ready

Summary

• Strong orders and backlog

• Spirit content demonstrates capabilities

• Focused on quality and cost improvements

8

9

Sam Marnick

Senior VP / Corporate

Administration & Human Resources

March 7, 2012

Aligning the Team

The Spirit Team

A Growing Global Team

2

People Strategy

• Deploy performance management

• Align individual, team & enterprise performance

• Embed daily management & operating disciplines

Drive performance excellence to protect

and grow spirit

• Identify, acquire & develop global talent

• Focus training on-the-job & on knowledge transfer

Build the team for the future to deliver spirit’s strategic

advantage

• Focus labor relationships on driving value

• Realize productivity & efficiency gains

Build strategic internal and external partnerships

Opportunity to Focus on Labor

3

New Model

Variable

Fixed

Previous Model

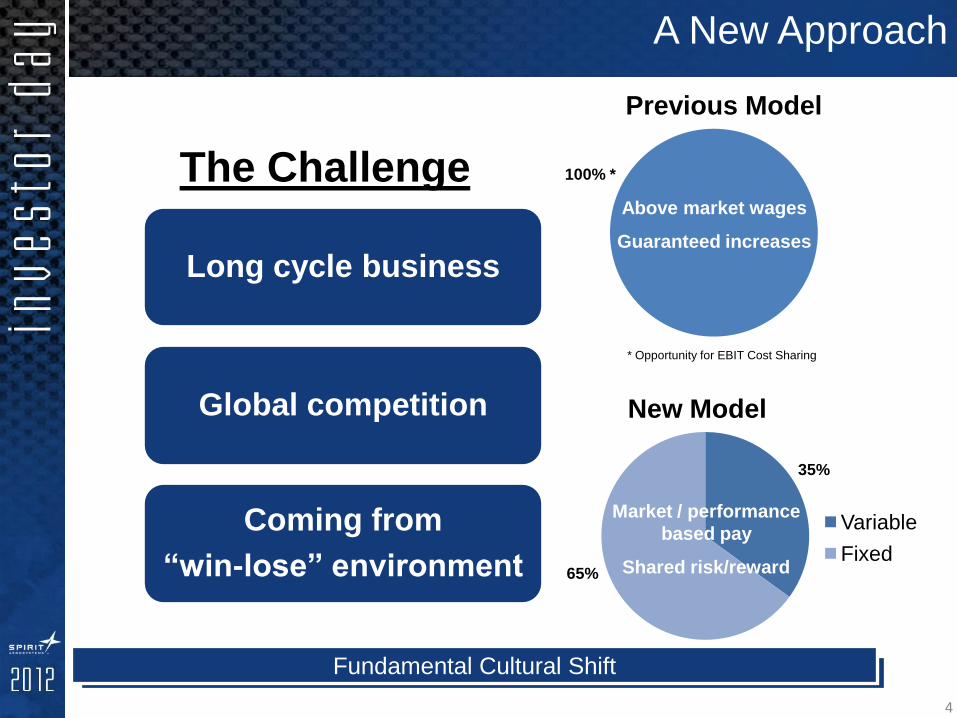

The Challenge

Long cycle business

Global competition

Coming from

“win-lose” environment

* Opportunity for EBIT Cost Sharing

A New Approach

Fundamental Cultural Shift

4

Market / performance

based pay

Shared risk/reward

Above market wages

Guaranteed increases

100% *

35%

65%

Laying the Foundation for Success

Better

Understand

the Unions

Cooperative

Partnership

Reinforce

Expectations

Proactively Managing the Dialogue

5

Capacity,

Productivity, and

Performance

&

Functional

Excellence

Ensure Stability for our customers and competitiveness of the unit,

through an enhanced partnership with a long-term agreement

Build the Flexibility required to maintain a healthy business that aligns with the production cycles

and productivity challenges

Provide Health Care options that Align with the Needs of the

Employees, as well as supporting the realities of the economic

market conditions through the life of the contract

Align Compensation with market and business performance, while

providing baseline protection

Keep The Company Healthy & The Team for The Future Intact

Contract Objectives

6

―Win-Win‖ Outcomes

Key Success Factors

Visible Leadership

Educate About Spirit

Shared Responsibility

Targeted Interaction

Where We Are Today

Creating a Drumbeat on the Floor 7

• Long Term Agreements in Place

-IAM, IBEW, UAW, & SPEEA-WTPU

• Collaborative Relationships

- Living agreements that can flow with the business

• Performance Compensation

- Company & bargaining unit specific performance targets

• Health Care Cost Escalation

- Incentives to migrate to lower costs & encourage wellness

Summary

Building on a Solid Foundation

8

9

Jeff Turner

President and Chief Executive Officer

March 7, 2012

Closing Comments

• Positioned on best selling platforms in the business

• Core business execution is strong — extending life of programs

• Successfully delivering higher production volumes — increasing through 2014

• New programs transitioning to production

• Focused on execution

• Financially strong

Long Term Value Creation

Summary

2

3