agenda: 2015 analyst and investor...

TRANSCRIPT

0

1

Agenda: 2015 Analyst and Investor Meeting

Overview Mike Lamach

Business Operating System Todd Wyman & Paul CamutiJohn EvansGary MichelDave Regnery

Q&A

Break: 15 Minutes

Sustainability & Energy Efficiency Manlio ValdésRandy NewtonRay PittardJeff Watson

Q&A

Climate Didier Teirlinck

Industrial Robert Zafari

Financial Sue Carter

Q&A

2

Safe Harbor

This presentation includes “forward-looking statements,” which are statements that are nothistorical facts, including statements that relate to the mix of and demand for our products,performance of the markets in which we operate, our share repurchase program includingthe amount of shares to be repurchased and timing of such repurchases, our projectedfinancial performance for 2015 second-quarter, full-year and beyond and assumptionsregarding our effective tax rate. These forward-looking statements are based on our currentexpectations and are subject to risks and uncertainties, which may cause actual results todiffer materially from our current expectations. Such factors include, but are not limited to,global economic conditions, demand for our products and services, the impact of currencyand tax law changes. Additional factors that could cause such differences can be found inour Form 10-K for the year ended December 31, 2014, and other SEC filings. We assumeno obligation to update these forward-looking statements.

This presentation also includes adjusted non-GAAP financial information which should beconsidered supplemental to, not a substitute for, or superior to, the financial measurecalculated in accordance with GAAP. Further information about the adjusted non-GAAPfinancial information is included in financial tables attached to the earnings news releasethat can be found at www.ingersollrand.com.

All data for beyond the first quarter of 2015 are estimates.

Overview

Mike Lamach

Chairman and CEO

2015 Investor and Analyst Conference

4

Strong, recognized brandsWell positioned in both

geographic and end marketsLeading market shares

OperationalExcellence

BalancedCapital Allocation

AcceleratingRevenue Growth

Sustainable, Profitable Growth and Shareholder Value

Our Model to Deliver Shareholder Value

5

• Top-quartile performance for peer groupand overall manufacturing companies

• High participation rate at 95%

• Improved on every survey dimension

• 95% retention of key talent Overall

Engagement

Satisfaction

Pride

Intent to Stay

Employee Commitment, Engagementand Development Critical to Change Culture

2010 2012 2013 2014

Employee Engagement Score

Satisfaction

Pride

Advocacy

Intent to Stay

#1 in Category

#9 in Innovativeness AmongAll Most Admired Companies

6

Total Recordable Incident Rate Lost Time Incident Rate

Year-Over-YearQ1 2015 Performance

65%33%

Year-Over-YearQ1 2015 Performance

Distinguished Safety Performance Due toRigor, Engagement of Employees

Focus and Positive Outcomes are Continuing

0.00

0.50

1.00

1.50

2.00

World Class Performance

0.00

0.10

0.20

0.30

0.40

World Class Performance

7

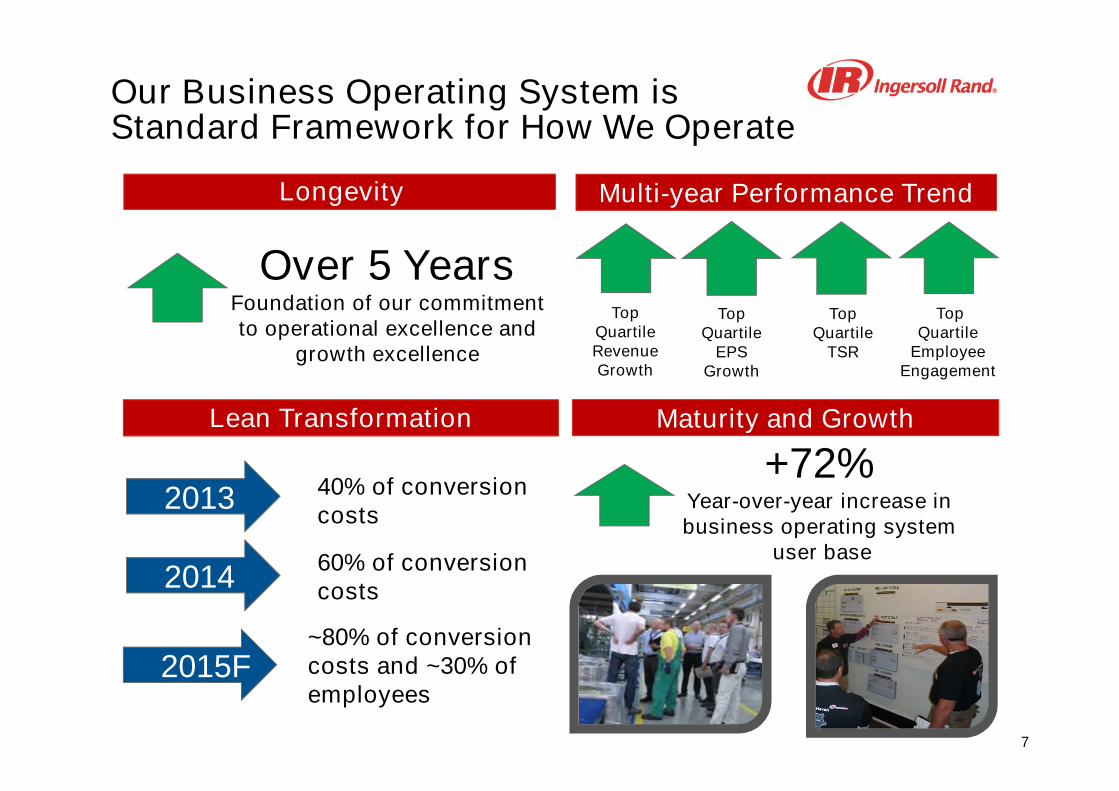

Our Business Operating System isStandard Framework for How We Operate

TopQuartileRevenueGrowth

TopQuartile

EPSGrowth

TopQuartile

EmployeeEngagement

TopQuartile

TSR

Maturity and Growth

Multi-year Performance Trend

Over 5 YearsFoundation of our commitmentto operational excellence and

growth excellence

2013

2014

40% of conversioncosts

60% of conversioncosts

2015F~80% of conversioncosts and ~30% ofemployees

+72%Year-over-year increase inbusiness operating system

user base

Lean Transformation

Longevity

8

ProductManagement

SupplyChain

Engineering &Technology

• Rigorous analytics, market segmentation and customer insights• Generating, developing and launching offerings• Reduce cycle times and increase speed to market

Idea Launch

Value Stream Expansion Offers SignificantOpportunity to Grow and Expand Margins

Product Growth Team-Led Value Streams

Sales ForceCapability &

Channel

Strategy&

Analytics

CustomerValue

Value Stream Discipline

9

Urbanization

Ingersoll Rand Possesses Expertise toAddress Pressing World Challenges

Energy Consumption

Food & Water Scarcity

Climate Change

Industrial Productivity& Efficiency

10

Much Progress…More Opportunity Ahead

• Strong momentum and further upside

‒ Attractive end markets

‒ Leading brands and growth through innovation

‒ Substantial position in developing markets with significant potential

• Excellent management team executingconsistently on strategy

• Value creation model deliverssustainable results and returns toshareholders

‒ Growth

‒ Operational Excellence

‒ Balanced capital allocation

Business Operating System (BOS)A systematic way to grow and improve execution

Paul CamutiSVP, Innovation and Chief Technology Officer

Todd WymanSVP, Global Operations & Integrated Supply Chain

2015 Investor and Analyst Conference

12

Premier Performance

Engaged Employees Delighted Customers Confident Shareholders

13

Operational Excellence

Ingersoll Rand Business Operating System (BOS)

Goal DeploymentProcess

FunctionalExcellence

CommonSystems

Value StreamTransformation

14

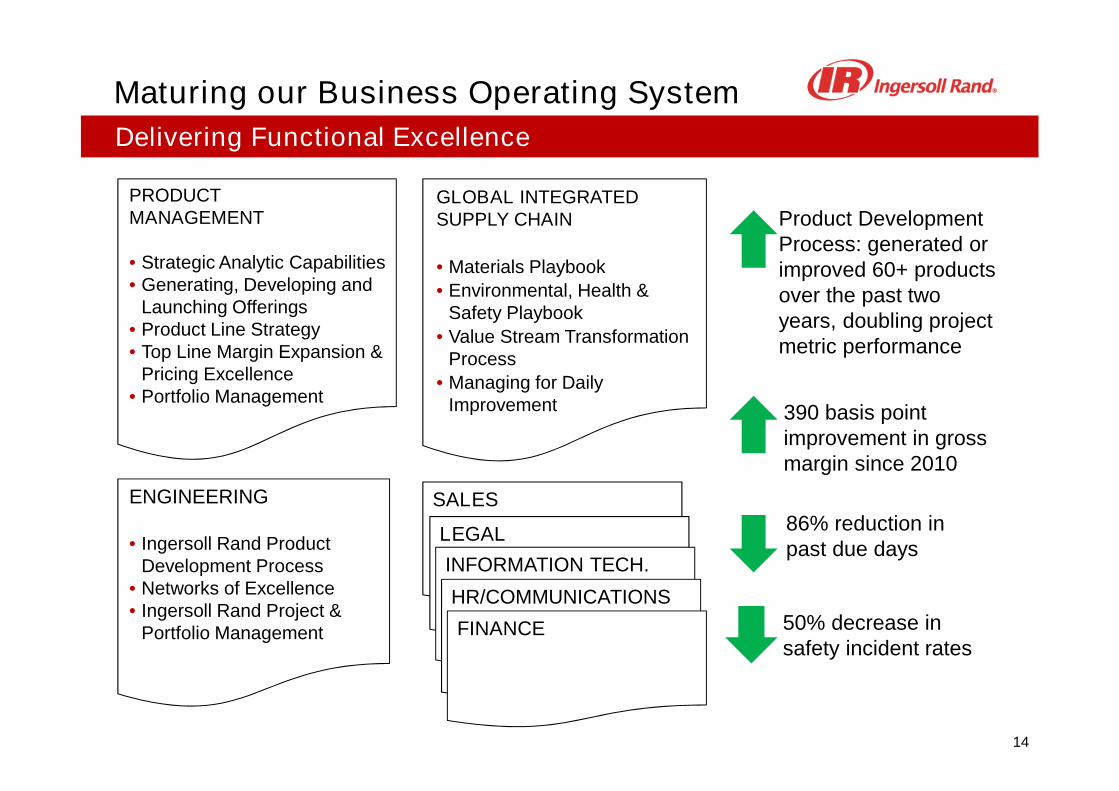

Delivering Functional Excellence

Maturing our Business Operating System

SALES

LEGAL

INFORMATION TECH.

HR/COMMUNICATIONS

FINANCE

ENGINEERING

• Ingersoll Rand ProductDevelopment Process

• Networks of Excellence• Ingersoll Rand Project &

Portfolio Management

PRODUCTMANAGEMENT

• Strategic Analytic Capabilities• Generating, Developing and

Launching Offerings• Product Line Strategy• Top Line Margin Expansion &

Pricing Excellence• Portfolio Management

GLOBAL INTEGRATEDSUPPLY CHAIN

• Materials Playbook

• Environmental, Health &Safety Playbook

• Value Stream TransformationProcess

• Managing for DailyImprovement

50% decrease insafety incident rates

390 basis pointimprovement in grossmargin since 2010

Product DevelopmentProcess: generated orimproved 60+ productsover the past twoyears, doubling projectmetric performance

86% reduction inpast due days

15

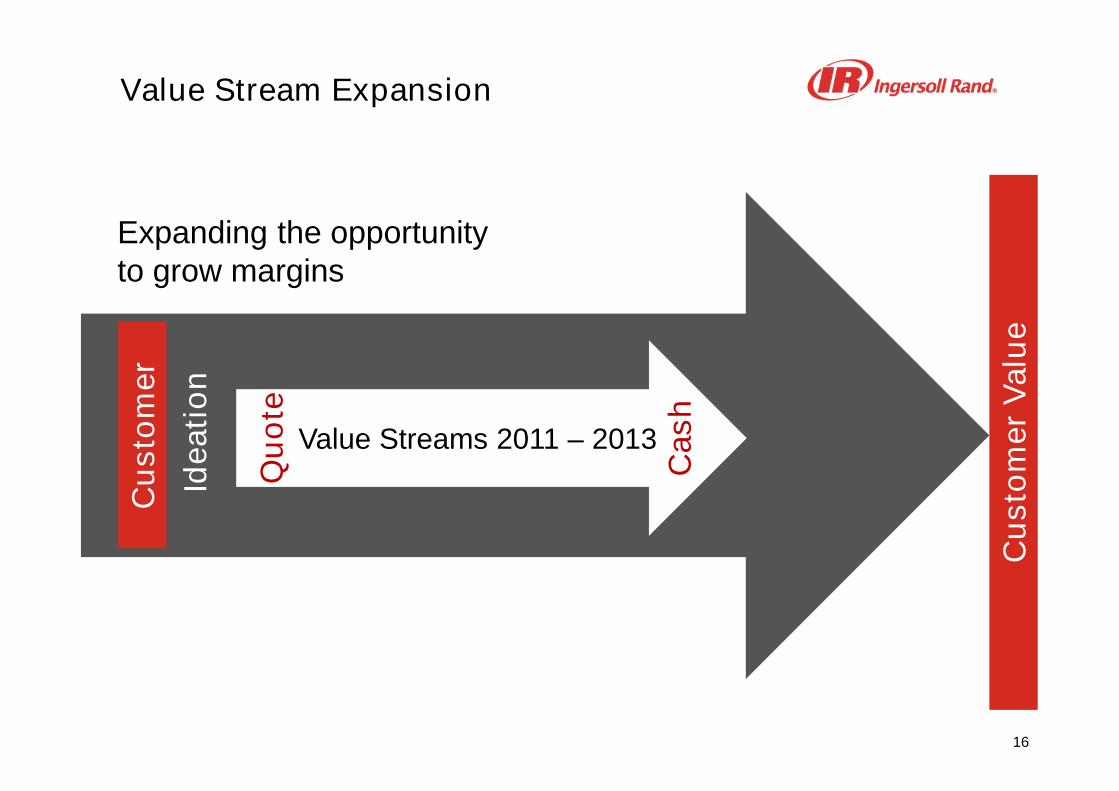

Value Stream Evolution

Cash

Qu

ote

Value Streams 2011 – 2013

Cost ofPoor Quality

Delivery InventoryTurns

Safety IncidentRates

Leverage EmployeeEngagement

Separation of Results

Cu

sto

mer

Valu

e

Cu

sto

mer

16

Expanding the opportunityto grow margins

Cash

Qu

ote

Value Stream Expansion

Value Streams 2011 – 2013

Ideati

on

Cu

sto

mer

Valu

e

Cu

sto

mer

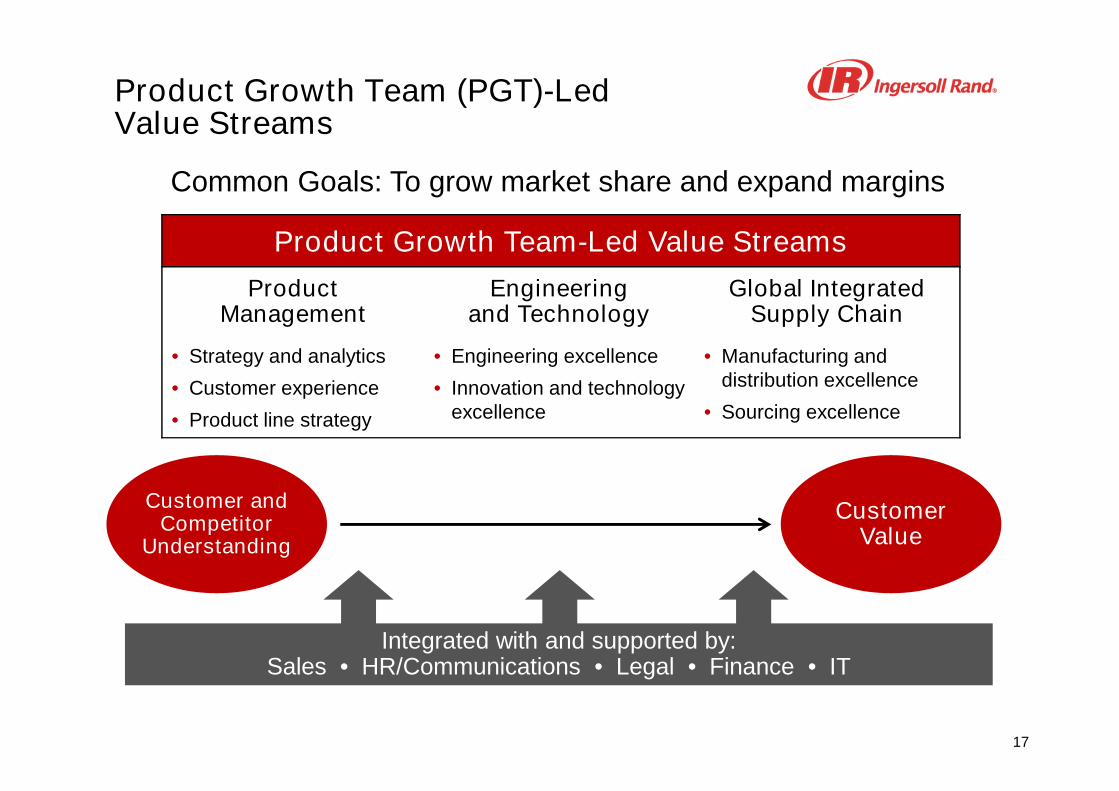

17

Common Goals: To grow market share and expand margins

Product Growth Team (PGT)-LedValue Streams

Product Growth Team-Led Value Streams

ProductManagement

Engineeringand Technology

Global IntegratedSupply Chain

• Strategy and analytics

• Customer experience

• Product line strategy

• Engineering excellence

• Innovation and technologyexcellence

• Manufacturing anddistribution excellence

• Sourcing excellence

Integrated with and supported by:Sales • HR/Communications • Legal • Finance • IT

Customer andCompetitor

Understanding

CustomerValue

18

Transformation Opportunities

2014 Accomplishments

• Average PGT revenuegrowth 4x the rest ofIngersoll Rand

• All PGT-led valuestreams met 2014margin expansion goalsand exceeded companyaverage

• Strong double-digit laborproductivity in modelvalue stream Conversion

Costs underTransformation

EmployeesParticipating inTransformation

~20%

60%

100%

Opportunity

100%

80%

~30%

?

2015

Opportunity

2015

2016

19

Product Management• Market segmentation

Global Integrated SupplyChain• Managing for daily

improvement• Production preparation

process• Expansion of value

stream

Reaping Encouraging Results

Business Operating System (BOS) in Action

Product Management• Portfolio management

Engineering• Ingersoll Rand Product

Development Process• Ingersoll Rand Project &

Portfolio Management

Product Management• Strategic analytic

capabilities• Generating, developing

and launching offerings

Global Integrated SupplyChain• Materials management

playbook• Sales, inventory, and

operations planning

Power Tools Residential HVACCommercial HVAC

NA/EMEA

Power Tools

John Evans

President, Power Tools

2015 Investor and Analyst Conference

Application of BOS Tools

21

• Provider of premium power tools and products to global customers

• Broad vertical market coverage

• Outstanding brand equity and reputation for quality and reliability

• Strong performance since formation in late 2013

Ingersoll Rand Power Tools

EMEIA is Europe, Middle East, India, and Africa. Services includes aftermarket parts, accessories, and service.

A Leading Industrial Power Tools Business

• 8 core product lines

• 43,000+ SKUs

• 5 manufacturing sites

• 1,500+ global customers

• 75% book & turn

North AmericaEMEIAAsia PacificLatin America

66%19%11%4%

EquipmentServices

83%17%

Vehicle Service AssemblyIndustrialApplied PowerProducts

22

• Analytics revealed a portfolio of product groups with varying levels of competitiveness

• We identified the most attractive markets in which to compete - and made strategicchoices on how to provide differentiated value to customers

Analysis and Data-Driven Decision Making

Strategic Choice Cascade

We Applied the BOS to our Strategy

What is ourwinning

aspiration?

Where will weplay?

How will wewin?

What capabilitiesmust we have?

What managementsystems do we

need?

Accelerated by theseelements of the BOS

toolkit:

SBU Strategy Process

Customer Buying Process

Market Attractiveness

Relative Competitive Position(RCP)

Strategic Analytics Playbook

Strategy Communication

23

• Analytics revealed a portfolio of product groups with varying levels of competitiveness

• We identified the most attractive markets in which to compete - and made strategicchoices on how to provide differentiated value to customers

Analysis and Data-Driven Decision Making

Strategic Choice Cascade

We Applied the BOS to our Strategy

What is ourwinning

aspiration?

Where will weplay?

How will wewin?

What capabilitiesmust we have?

What managementsystems do we

need?

#1 Choice of mechanics

Precision fastening

Electrification

Strategic Choices

24

• We identified an opportunity to profitably grow revenue by improving delivery leadtimes

• We systematically applied the BOS playbook to deliver significant improvement

Sales, Inventory and OperationsPlanning (SIOP)

Value Stream AnalysisMaterials ManagementPlaybook

We reduced cycle time for 75% of our COGS footprint…

3

Order

1

Schedule

2

Manufacture Ship

4

94% reduction 60% reduction

…improving customerexperience

Results indicated were achieved over five quarters.

25 point gain in CustomerSatisfaction Index

12 point gain in on-timedelivery

40% reduction in pastdue backlog

~10 point improvementin revenue growth rate

Accelerated by these elements of the BOS toolkit:

Transforming our Key Value Stream

Residential HVACApplication of BOS Tools

Gary S. Michel

SVP and President, Residential HVAC

2015 Investor and Analyst Conference

26

Single FamilyReplacement

(Owner, Non-OwnerOccupied)

Multi-FamilyReplacement

Residential NewConstruction

(Single/Multi-Family)

Dealer SalesOffices

IndependentDistributors

Dealer Network

Builder

Retail /E-Commerce

Residential HVAC

Multiple brands, channels, plants and customer buying behaviors

Manufacturing Portfolio Channels to Market Customers

Heating/Cooling(Ducted/Ductless)

Controls

Home Automation

Energy Management

Remote Diagnostics

Air Quality

Geothermal

Tyler, Texas

Trenton, New Jersey

Fort Smith, Arkansas

Vidalia, Georgia

Lynn Haven, Florida

Monterrey, Mexico

Bridgeton, Missouri(National Distribution Center)

27

• Operational excellence

• Total market focus

• New product designswith rapid and effectivecommercialization

• Nexia diagnostics andcontrols

• Energy efficiency leadership

‒ Variable Speed

‒ Ultra high efficiency systems

• Continued reliability andquality leadership

• Channel improvements

• Segmented offerings

• Enhanced customerexperience

• Employee engagement

Strategic Priorities

A Product for every home75% of portfolio new since 2011

Compelling BrandExperience

DifferentiatedSolutions

Total MarketSolutions

27

28

Project Management

(Competency)

Ingersoll Rand ProductDevelopment Process

(Processes)

Ingersoll Rand ProjectPortfolio Management

(Resource Management)

Portfolio ManagementProcess

Ingersoll Rand Project BOS

Common system of capabilities for successful project execution

New ProductDevelopment

New TechnologyProcess

QualityProductivity Sustaining

Project Management

29

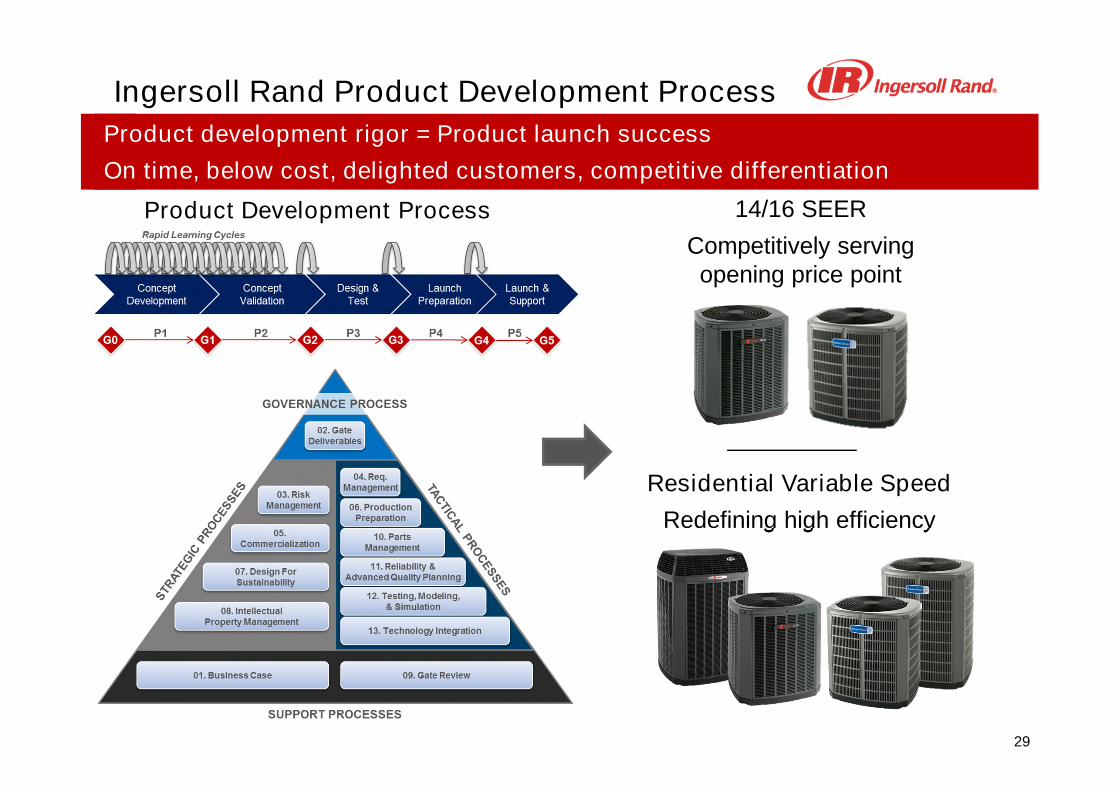

Ingersoll Rand Product Development Process

Product development rigor = Product launch success

On time, below cost, delighted customers, competitive differentiation

Residential Variable Speed

Redefining high efficiency

Product Development Process 14/16 SEER

Competitively servingopening price point

30

Variable Speed Product Development RigorData-driven choices, executed precisely for competitive differentiationand delighted customers

• 80 field trial unitsacross country

• 50k run hours

• 200k simulations

• 7 billion datapoints collected

• Real-time costanalysis

• Software reusability

TechnologyIntegration

• Early field trialinvestigations

• Jump-starton testing

• Utilized remoteconnectivity andtelematics

• 20 patents pending

• Streamlinedproduct design

• Product trainingand certificationfor quality installs

• Mobile-friendlydealer tools

Testing &Simulation

Commercialization

• Modeling forProduction

• Pre-pilot build

• Processimprovements sixmonths prior topilot

ProductionPreparation

Process

31

A home run for homeowners, contractors and Ingersoll Rand

Results

Ingersoll Rand

• Reinventing high efficiency segment; more than 50% share invariable speed

• Successful technology platform upon which to build

Dealers/Contractors

• Fast, easy to install and service

• Dealer diagnostics for superior homeowner support, moreefficient maintenance or repairs

Homeowners

• Home energy efficiency savings

• Precision comfort maintained within one-half of one degree

• Quietest, most reliable variable speed offering in industry

32

Competitor A Competitor BTrane TruComfort

American StandardAccuComfort

Streamlined Design of Variable Speed Product

Which system would you rather build and service?

33

Summary

Leveraging Business Operating System to create value for homeowners,channel partners and business Profitable growth and margin expansion

Residential Variable Speed

Redefining high efficiency

14/16 SEER

Competitively servingopening price point

would recommend Variable Speedto family and friends

• “This is a kick ass machine”

• “Crisp and cool!”

• “Power consumption dropped ~30%vs last year”

• “The gas bill dropped over $100from last year!”

• “Can’t even hear it running”

Trane Light Commercial UnitaryFocus on Product Growth Team Led Value Streams

Dave Regnery

President, HVAC CommercialNorth America, Europe and Middle East (EMEA)

2015 Investor and Analyst Conference

35

Teaming product management, supplychain and engineering to work towardsthe same goals

• Grow market share

• Increase margin

Value of Product Growth Teams

Use customers’ buying processes andsegmentation to define our strategy

• Achieve organic revenue growth targets

• Grow market share

• Expand contribution margin

• Manage product or portfolio pricing

• Develop a robust innovation portfolio

• Engage all functions to deliver on thesegoals

Applying Product Growth Teams

ProductManagement

Engineering

IntegratedSupplyChain

HR / Finance / Legal

General / Strategic Management

36

Foundation™

Introduction to Light Commercial Unitary

North America Light Commercial Rooftop market is ~$1.7B with longterm historical growth rate of 4%

Tra

ne

LC

UP

ort

foli

o

Value Stream Overview

3 to 12.5 Tons

12.5 to 25 Tons70%

30%

Market Size by Tonnage

Small Retail &Restaurants

Office & BigBox Stores

Precedent™

Voyager™

Impack™

37

Business Operating System (BOS) in action

Light Commercial UnitaryProduct Growth Team Standard Work

• Helps ensure constantflow and consistencyacross the value streamprocess

POWER TOOLS

• Conduct detailedquantitative andqualitative customeranalysis

.

• Develop hypothesisand test methodology

.

• Define buying behaviorprocesses

.

• Create strategyand execute

• Guide for the goaldeployment andalignment process

.

• Aligns and displayscritical metrics

.

• Effective way to identifysolutions and drawconclusions

Visual ManagementProduction Preparation

Process (3P)Market Segmentation

38

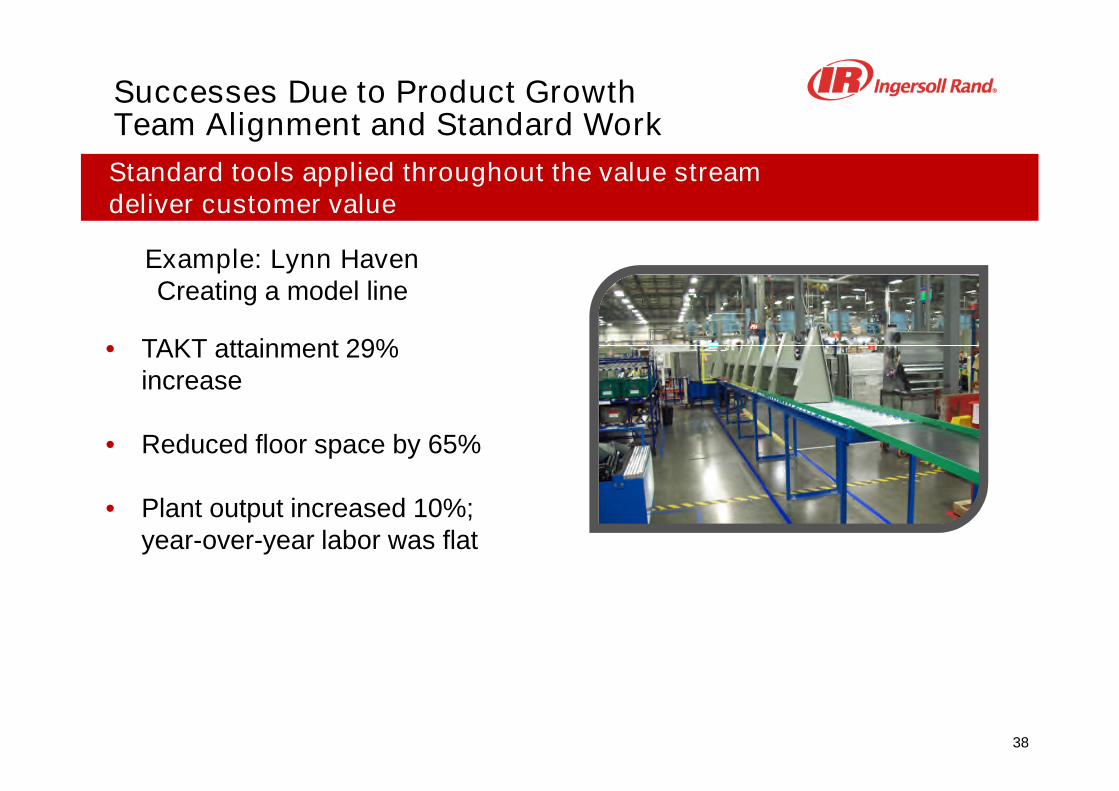

Successes Due to Product GrowthTeam Alignment and Standard Work

Standard tools applied throughout the value streamdeliver customer value

Example: Lynn HavenCreating a model line

• TAKT attainment 29%increase

• Reduced floor space by 65%

• Plant output increased 10%;year-over-year labor was flat

39

Successes Due to Product GrowthTeam Alignment and Standard Work

Standard tools applied throughout the value streamdeliver customer value

Example: Managing for Daily ImprovementStandard work and visual management

• Actions are aligned andsynchronized across functions

• Allows for rapid problem solving

• Increase in employeeengagement scores across theboard – model line, sales andproduct management

40

Successes Due to Product GrowthTeam Alignment and Standard Work

Standard tools applied throughout the value streamdeliver customer value

Example: Large Metro AreaImproving speed of time to fill

• Applying operationalexcellence to sales processwas a critical milestone

• +2 points Light CommercialUnitary (LCU) market sharegrowth in this metro area

• Double digit revenue growthin Q1 2015 for LCU products

QUOTE LEAD TIME <= 15 MIN

41

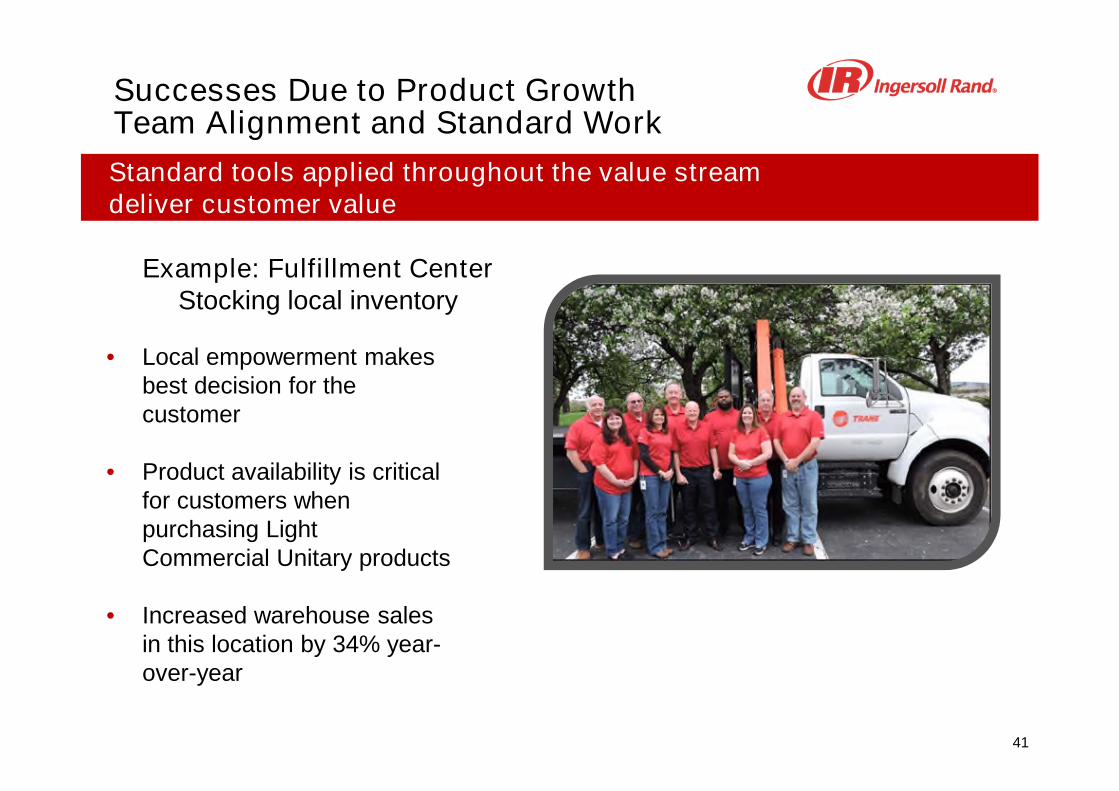

Successes Due to Product GrowthTeam Alignment and Standard Work

Standard tools applied throughout the value streamdeliver customer value

Example: Fulfillment CenterStocking local inventory

• Local empowerment makesbest decision for thecustomer

• Product availability is criticalfor customers whenpurchasing LightCommercial Unitary products

• Increased warehouse salesin this location by 34% year-over-year

42

Steady Light Commercial Unitary market share and

revenue growth from 2012-2014

Product Growth Team-Led Value Streamsis All About Profitable Share Growth

Margin Enhancement +200 basis points

Revenue Growth Double Digit

Market Share Steady Growth

43

Product Growth Teams are the NextGeneration of Operational Excellence

• Product Growth Teams are fueling growth and margin enhancements

• This concept is easy to understand, but requires disciplined executionand is difficult to competitively replicate

• The concept drives a differentiated customer experience to alignmentwith all functions at every level

2015 Investor and Analyst Conference

Sustainability and Energy EfficiencyEnvironmental Regulations

Manlio ValdésPresident, Compressed Air Systems and Services

45

Today’s Regulatory Environment

Active and engaged beyond compliance

Energy EfficiencyGreenhouse Gas

EmissionsRefrigerants

• Company subject matter experts participate in internationalcodes and standards committees and regulatory bodies inChina, Middle East, Europe and North America tounderstand and shape direction

• Strong alignment between regulatory landscape and ourexpertise in energy efficiency and environmentalsustainability

• Regulation is driving innovation and moving the bar higherfor the entire industry

Macro-economic trends driving increase in regulations

46

Innovation PortfolioCustomer InsightsModeling &Simulation

Applying BOS to Address Regulations

Tools to translate and make data-driven decisions around regulations

• Understanding developing regulatory framework and areas where we create value

• Confirming product performance – industry leading efficiency and sustainability

• Reducing product development cycle time

• Leveraging strengths across businesses – technology, modeling, machining and testing

Design forSustainability

Networks ofExcellence

Precision Machining

And deliver innovation which offers unique value to customers

• Up to 15% more efficient• Leading class

performance• Design for improved

reliability

RS-SeriesCompressor

• Option of alternativerefrigerant before phase out

• Industry-leading efficiency• Strong product performance

and reliability

Trane AirCooled Screw

Chiller

47

Applying BOS for Greater Leverage

• Network Of Excellence- Compression- Refrigeration- Heat exchange

• Precision Manufacturing- Tolerances- Design- Common tools, processes

and sites

• Centrifugal expertise in gascompression applicable toengineered centrifugal andapplied HVAC businesses

• Critical tolerance control to driveenergy efficiencies incompressors and HVACequipment

Portfolio Commonality Examples

SBUs Represented

48

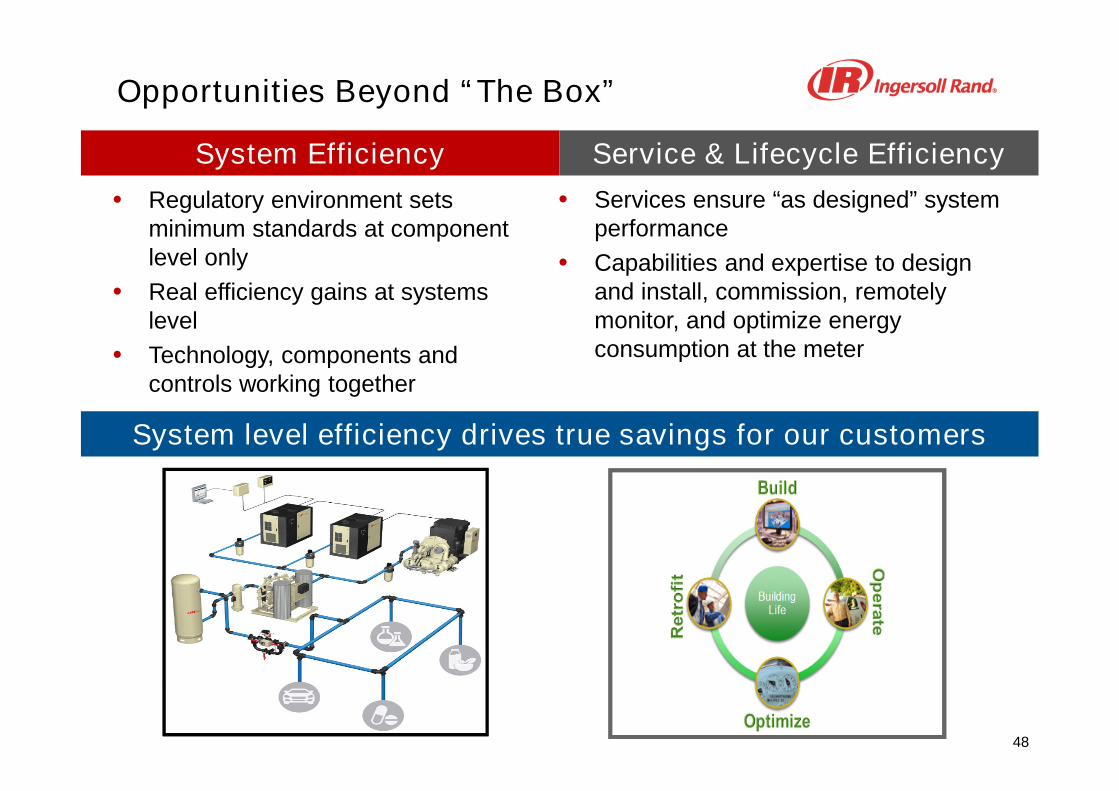

Opportunities Beyond “The Box”

System Efficiency

• Regulatory environment setsminimum standards at componentlevel only

• Real efficiency gains at systemslevel

• Technology, components andcontrols working together

Service & Lifecycle Efficiency

• Services ensure “as designed” systemperformance

• Capabilities and expertise to designand install, commission, remotelymonitor, and optimize energyconsumption at the meter

System level efficiency drives true savings for our customers

Regulation Inspired Innovation

Randy Newton

Vice President Enterprise Engineering

2015 Investor and Analyst Conference

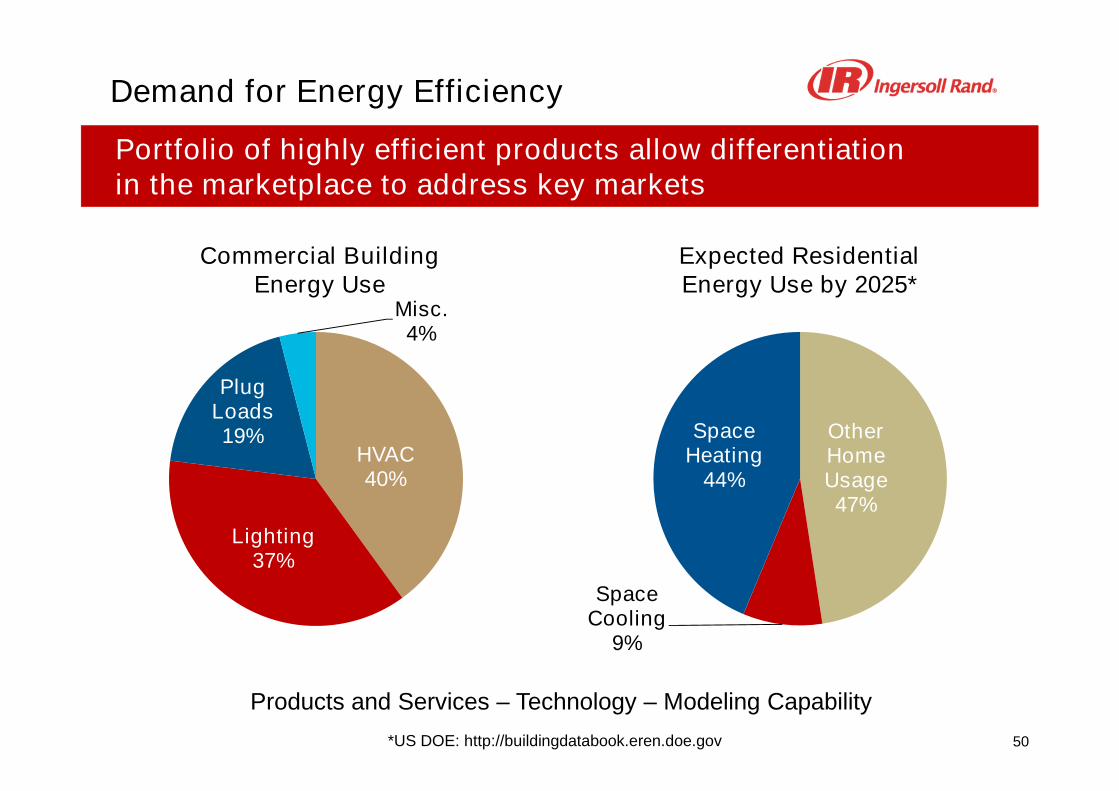

50

OtherHomeUsage47%

SpaceCooling

9%

SpaceHeating

44%HVAC40%

Lighting37%

PlugLoads19%

Misc.4%

Portfolio of highly efficient products allow differentiationin the marketplace to address key markets

Expected ResidentialEnergy Use by 2025*

Demand for Energy Efficiency

Products and Services – Technology – Modeling Capability

*US DOE: http://buildingdatabook.eren.doe.gov

Commercial BuildingEnergy Use

51

Global Opportunities

75% of infrastructure globally that will exist in 2050 hasyet to be built

We will see a 70-85% increase in our urban population inthe next 35 years

In India, 85% of buildings that will exist in 2050 have yetto be built

The growing and urbanizing population will requirehousing and food

Demand for sustainable growth

52

Our Path Forward

Leveraging our strengths

Refrigerants

• 36 inventiondisclosures inpast 2 years

• 13 expected patents

Energy Management & Services

TechnologyNew Products & Services

53

Comfortable, Sustainable, EfficientEnvironments

GrowingUrbanization

GrowingPopulation

Drive forCompetitiveness

Innovation

A world of sustainable progress and enduring results

Sustainability and Energy EfficiencyTransport Refrigeration

Ray Pittard

President, Transport Solutions

2015 Investor and Analyst Conference

55

External factors that impact Transport Refrigeration

Macro Global Trends

UrbanizationChina cold chain infrastructure

Environmentally-driven LegislationEPA & Euro engine laws; PIEK noise levels and non-dieselusage in European cities

Food Waste due to SpoilageEmerging countries excess of 50% food spoilage

Traceability within the Cold ChainFood Safety & Security

SustainabilityGlobal Warming; reducing greenhouse gas emissions

56

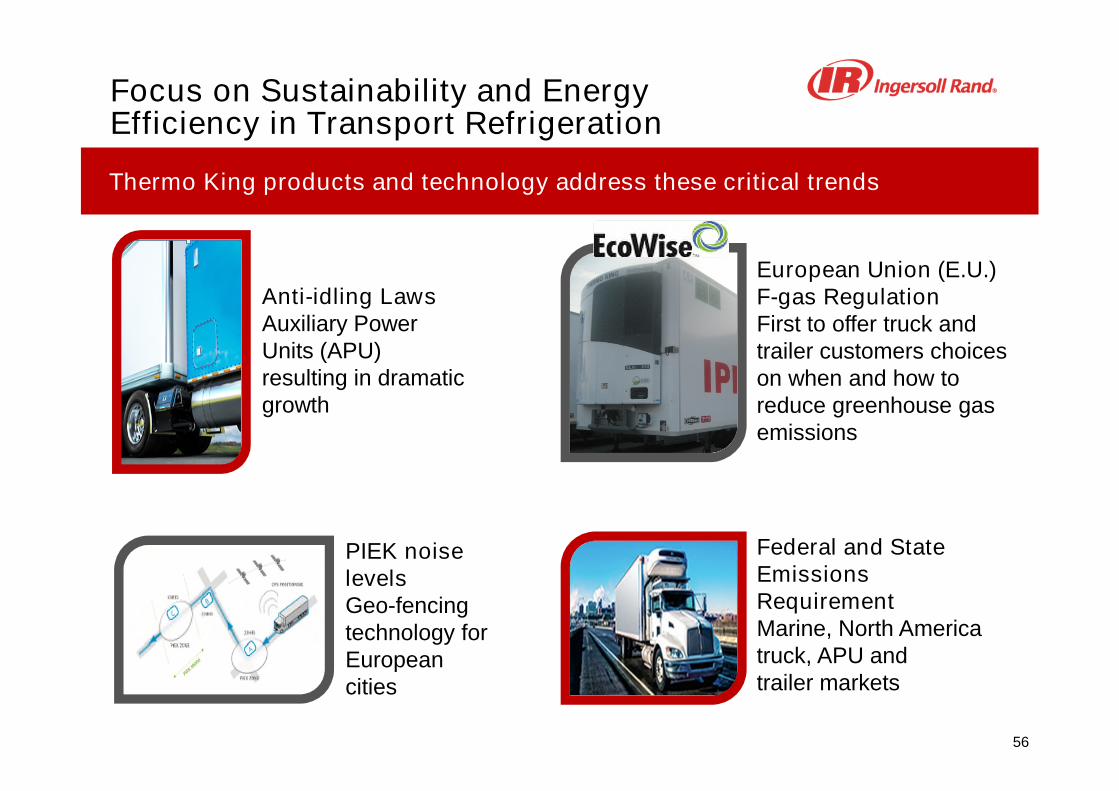

Thermo King products and technology address these critical trends

Focus on Sustainability and EnergyEfficiency in Transport Refrigeration

Anti-idling LawsAuxiliary PowerUnits (APU)resulting in dramaticgrowth

Federal and StateEmissionsRequirementMarine, North Americatruck, APU andtrailer markets

PIEK noiselevelsGeo-fencingtechnology forEuropeancities

European Union (E.U.)F-gas RegulationFirst to offer truck andtrailer customers choiceson when and how toreduce greenhouse gasemissions

57

Complex environment in North America

In-Depth Review: NA Trailer Market

• North America Trailer business

- Large, profitable and growing

• Regulatory challenges intransportation

- EPA Mandated Tier IV FinalEmissions

- Not voluntary for OEMs

• Customers were frustrated with Class8 tractor emission changes

• Fuel costs, reliability andsustainability are critical to ourcustomers’ success

• In this complex environment, wedeveloped the Precedent portfolio

REGULATION

CU

ST

OM

ER

VA

LU

E

CO

MP

ET

ITO

RS

CLASS 8 TRACTOR OEMS

58

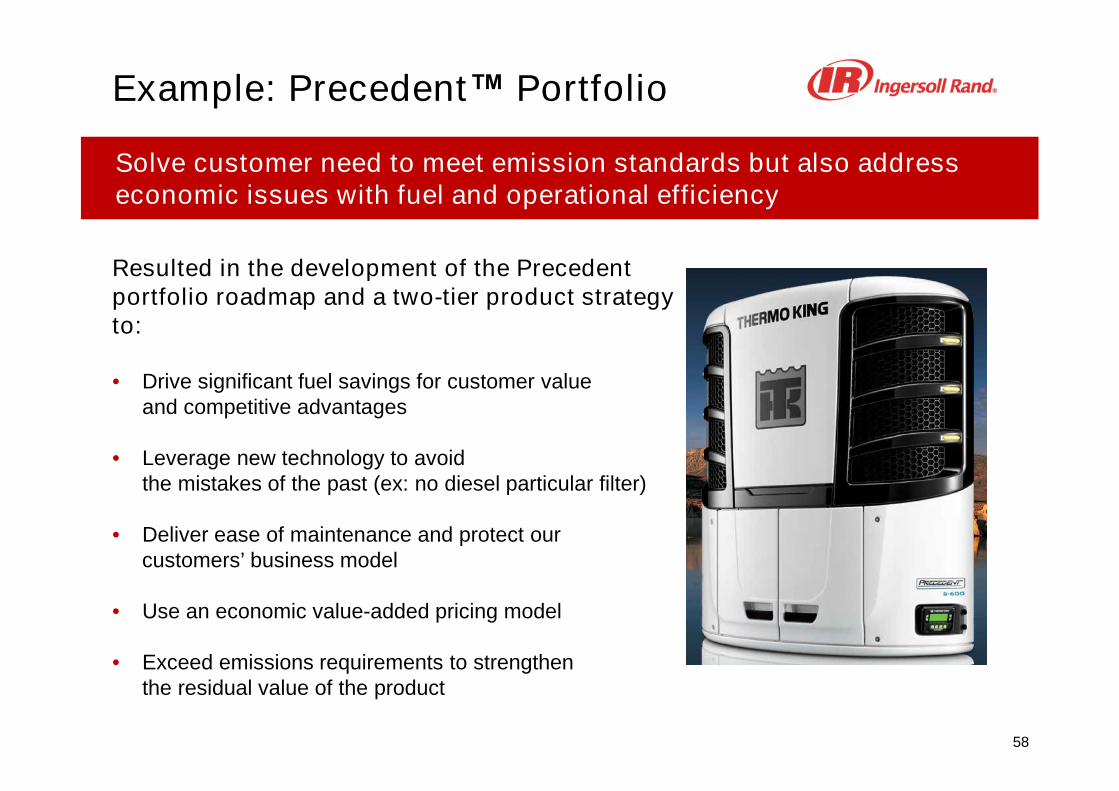

Solve customer need to meet emission standards but also addresseconomic issues with fuel and operational efficiency

Resulted in the development of the Precedentportfolio roadmap and a two-tier product strategyto:

• Drive significant fuel savings for customer valueand competitive advantages

• Leverage new technology to avoidthe mistakes of the past (ex: no diesel particular filter)

• Deliver ease of maintenance and protect ourcustomers’ business model

• Use an economic value-added pricing model

• Exceed emissions requirements to strengthenthe residual value of the product

Example: Precedent™ Portfolio

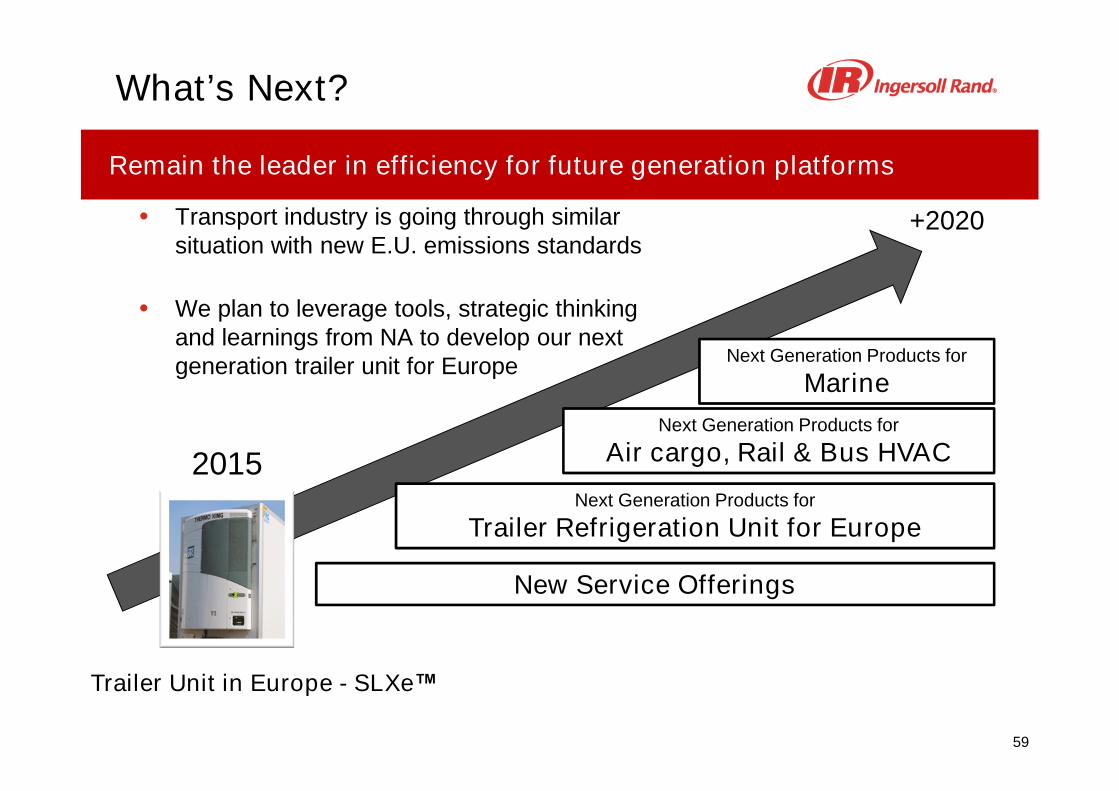

59

Remain the leader in efficiency for future generation platforms

• Transport industry is going through similarsituation with new E.U. emissions standards

• We plan to leverage tools, strategic thinkingand learnings from NA to develop our nextgeneration trailer unit for Europe

2015

Trailer Unit in Europe - SLXe™

New Service Offerings

Next Generation Products for

Air cargo, Rail & Bus HVAC

+2020

Next Generation Products for

Trailer Refrigeration Unit for Europe

Next Generation Products for

Marine

What’s Next?

VRF Markets and Opportunity for Trane

Variable Refrigeration Flow Systems

Jeff WatsonVice President, Product Management and MarketingHVAC Commercial, North America

2015 Investor and Analyst Conference

61

Applied - Chilled-Water, Air-Handling Variable Air Volume (VAV) System

Overview of HVAC Systems and Serviceswithin Commercial Applications

62

Unitary - Rooftop Variable Air Volume (VAV) System

Overview of HVAC Systems and Serviceswithin Commercial Applications

63

Variable Refrigerant Flow (VRF) System

Overview of HVAC Systems and Serviceswithin Commercial Applications

64

64%

27%

5%4%

VRF Growth Rate2014 vs 2013

Asia Pacific +11%

EMEA +9%

N. America +23%

L. America +27%

VRF is one of the fastest growing product lines in North America

Overview of VRF Global Market Growth

Applied

Unitary

VRF

Total HVAC EquipmentMarket (North America

2014) +$4.8B

VRF represents less than10% of the total market

$1.6B

$2.8B

$400M

• Trane was one of, if not the first, to sell VRF inNorth America; ~25% of the overall market issold through our channels

• Trane has doubled its VRF business overthree years

• Trane VRF portfolio strategy is to have a mixof manufactured and sourced products

VRF Sales by Geography

64

65

Recommended HVAC system applications by vertical

Commercial Applications

Lrg.OfficeHotels

SmallRetail

DataCenters Medical

VRF

Unitary

Applied

K-12 Warehouse

Sm.Office Retail

66

Life Cycle Cost

Efficiency

SimultaneousHeating/Cooling

Retrofit (No A/C)

First Cost

Safety

Humidity Control

Ventilation

Selecting the right system to efficiently meet application requirements

System Comparisons Good Poor

AppliedSystem

Strength

AppliedSystem

Strength

VRFSystem

Strength

UnitarySystem

Strength

?

VRF UnitaryAppliedFeature

67

• We believe Trane is the trusted systems partner because we advisecustomers on how to pick the right system to meet their facility goals

• In addition to product, our strength is local and regional design,controls and service capabilities to help owners, designers andcontractors with all their VRF system needs

• Trane will continue to invest and grow our VRF business andcapabilities globally

Trane is Well Positioned for Successwith VRF

Climate Segment Update

Didier TeirlinckExecutive Vice President, Climate Segment

2015 Investor and Analyst Conference

69

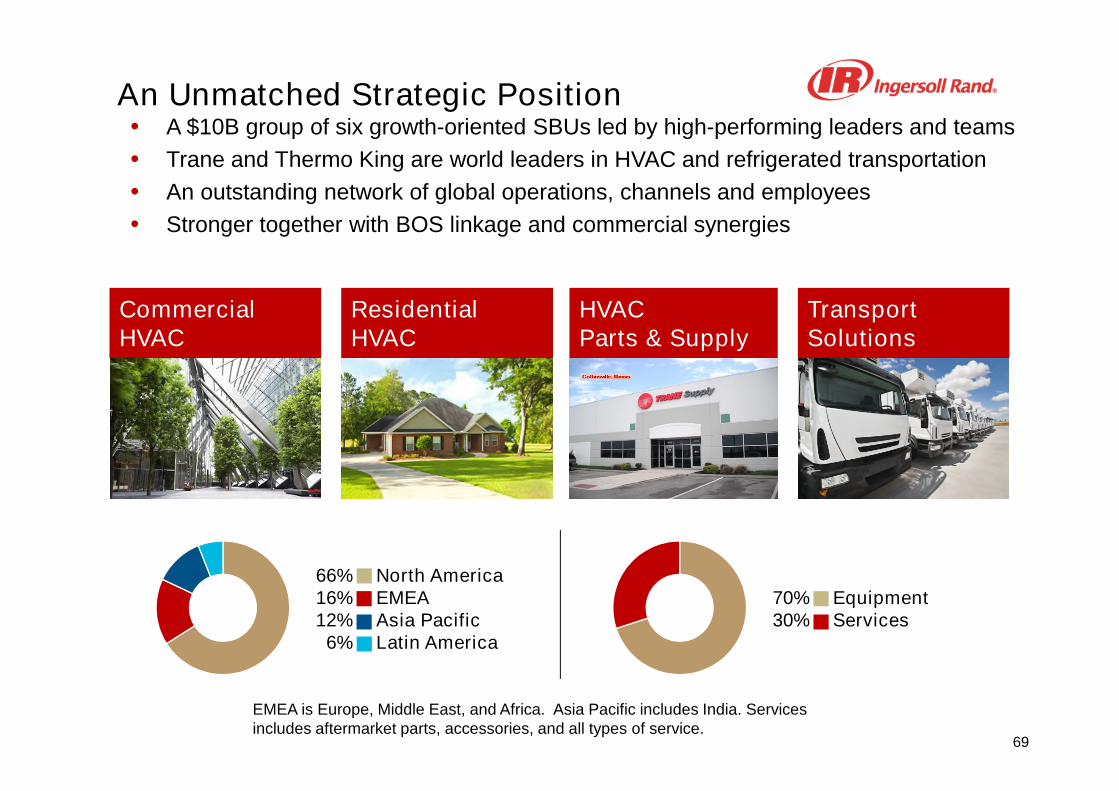

An Unmatched Strategic Position• A $10B group of six growth-oriented SBUs led by high-performing leaders and teams

• Trane and Thermo King are world leaders in HVAC and refrigerated transportation

• An outstanding network of global operations, channels and employees

• Stronger together with BOS linkage and commercial synergies

EMEA is Europe, Middle East, and Africa. Asia Pacific includes India. Servicesincludes aftermarket parts, accessories, and all types of service.

CommercialHVAC

ResidentialHVAC

HVACParts & Supply

TransportSolutions

66%16%12%6%

North AmericaEMEAAsia PacificLatin America

70%30%

EquipmentServices

70

We are in Structurally Attractive Markets

• Our base markets are growing on the strength of secular global drivers: energy efficiency,urbanization, food and pharmaceutical safety, regulation and others

• Short-term cyclicality reverts to long-term growth in HVAC and transport markets

Sources: AHRI (2013-2014) and management estimates (2015-17); IHS Medium and Heavy Commercial Vehicle IndustryForecast, February 2015. EMEA is Europe, Middle East and Africa.

-0.8%0.5%

1.9%

7.5% 6.4%

'13 '14 '15 '16 '17

North America and EMEA Medium and Heavy Commercial Vehicle Market (>6t)YOY % Change in Units; 2015 = 939k units

North America HVAC Market, Unitary and Applied SystemsYOY % Change in Size; 2015 = $4.67B

1.3%

3.9% 4.0%

5.9% 6.3%

'13 '14 '15 '16 '17

+ 4.3%CAGR

+ 3.1%CAGR

71

• North America has turned the corner; solid growth in high growth marketsincluding China and Southeast Asia

• Strength in non-residential and residential HVAC markets; transport positive

Regional HVAC+R Outlook Trends

• United States Non-Residentialconstruction is recovering

• United States Residential newconstruction and multi-family aregrowing fast

• Strong growth in Middle East andAfrica

• Latin America shows a mixed picture

• China growing at slower rates

• India slowly recovering

North America

Latin America

Europe

Middle East and Africa

China

Southeast Asia

India

The Market Outlook is Favorable

72

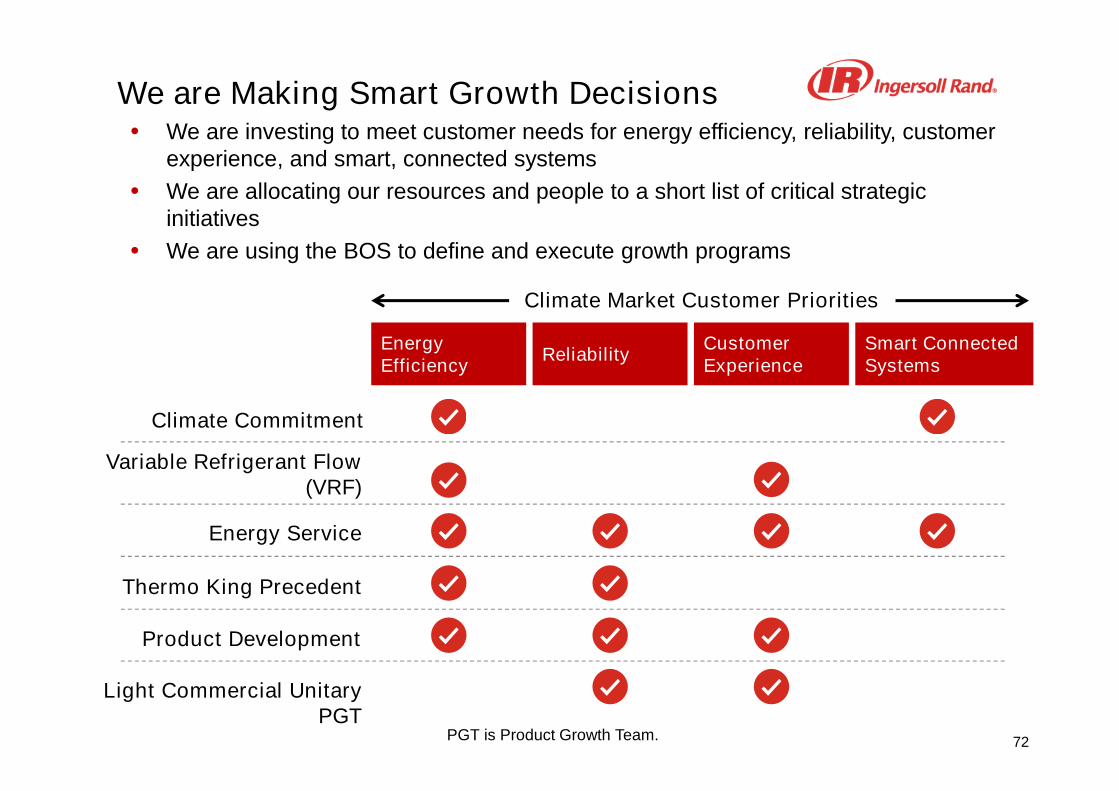

We are Making Smart Growth Decisions• We are investing to meet customer needs for energy efficiency, reliability, customer

experience, and smart, connected systems

• We are allocating our resources and people to a short list of critical strategicinitiatives

• We are using the BOS to define and execute growth programs

EnergyEfficiency

ReliabilityCustomerExperience

Climate Market Customer Priorities

Smart ConnectedSystems

PGT is Product Growth Team.

Variable Refrigerant Flow(VRF)

Energy Service

Thermo King Precedent

Product Development

Light Commercial UnitaryPGT

Climate Commitment

73

The FRIGOBLOCK Acquisition is on Track

• Closed the acquisition on March 4, 2015

• Integration is proceeding to plan; deep engagement from all functions and work streams

• Company values and culture are a strong fit with Ingersoll Rand

Integration

Growth

• Technology and engineering leverage remains promising• Synergies are materializing across several functions

• Order book and backlog are strong; will offset headwindsfrom weak Euro

• Beginning to execute comprehensive growth plan

74

We Will Deliver Strong Financial Results

• We have been executing to our plan

• We have aggressive but achievable targets for revenue and operating margin

2014 2016F

Revenue Drivers

• Global market growth

• Share growth

• VRF and HVAC Parts expansion

• Energy service

• Service and contracting

Operating Margin Drivers

• Product development

• Productivity

• Services and Parts expansion

• Strategic price actions

12.2%13-14%

Adjusted Operating Margin

Industrial Segment Update

Robert Zafari

Executive Vice President, Industrial Segment

2015 Investor and Analyst Conference

76

Our Businesses are in Leading Positions• A $3.3B group of five growth-oriented Strategic Business Units

• Ingersoll Rand, ARO and Club Car are #1 or #2 brands in their core markets

• World-class engineered and mission-critical products, systems and services

• Balanced across industries, geographic regions, equipment and aftermarket

• SBUs are stronger together with BOS linkage and channel synergies

2014 pro-forma results including Cameron Centrifugal. EMEIA is Europe, Middle East, Indiaand Africa. Services includes aftermarket parts, accessories and service.

AIR Power ToolsFluidManagement

MaterialHandling

Club Car

51%23%21%5%

North AmericaEMEIAAsia PacificLatin America

65%35%

EquipmentServices

77

We are in Structurally Attractive Markets• Leveraging a large array of growing industrial segments worldwide

• Demanding industrial customers understand and pay for value

Chart reflects management estimates for 2014 Industrial Segment pro-forma results and includes CameronCentrifugal. Growth estimates reflect 2015-16 MAPI Industrial Outlook data and management estimates.

Industrial Segment Revenue Distribution by Vertical Market2014 FY

11%

2%

3%

3%

4%

4%

4%

5%

5%

5%

6%

6%

6%

7%

11%

18%

Others

Natural Gas

Electronics

Mining

Consumer

Utility

Metals

Garage

Food & Beverage

Motor Vehicle

Chemical & Pharma

Power Generation

Industrial Gas

Oil

Golf & Turf

Manufacturing

Growth > Industrial Average

Growth < Industrial Average

Growth = Industrial Average

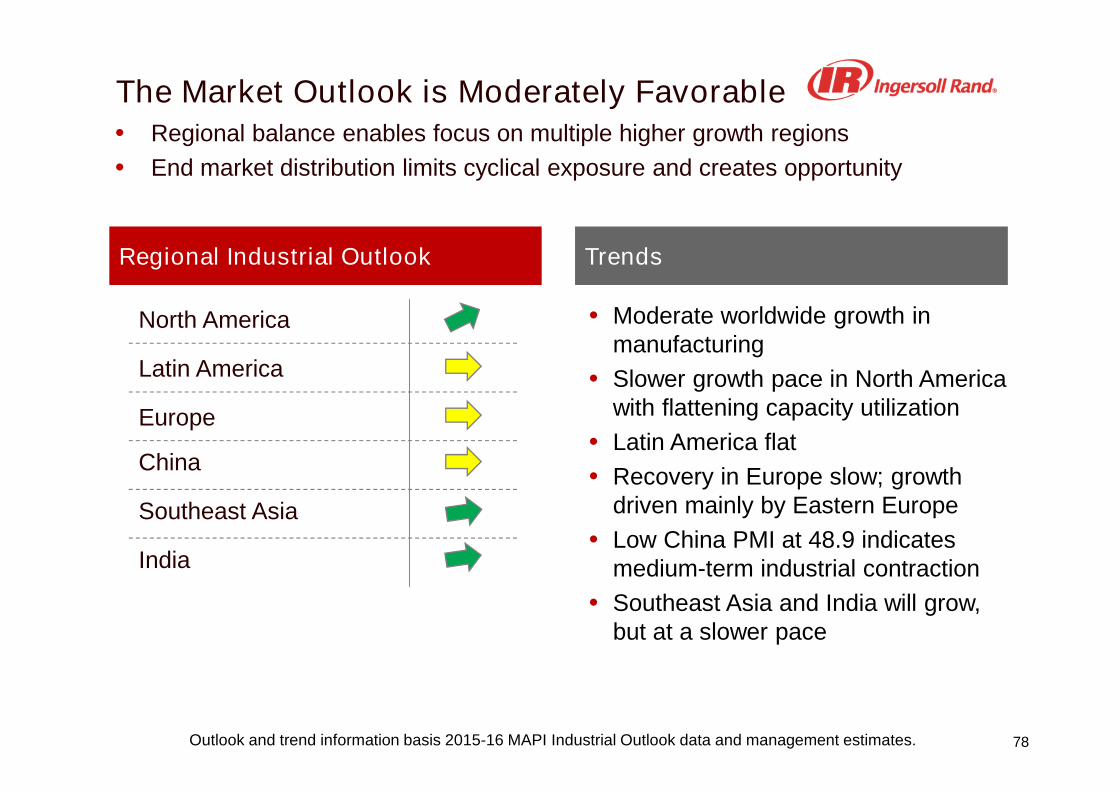

78

The Market Outlook is Moderately Favorable• Regional balance enables focus on multiple higher growth regions

• End market distribution limits cyclical exposure and creates opportunity

Outlook and trend information basis 2015-16 MAPI Industrial Outlook data and management estimates.

Regional Industrial Outlook Trends

• Moderate worldwide growth inmanufacturing

• Slower growth pace in North Americawith flattening capacity utilization

• Latin America flat

• Recovery in Europe slow; growthdriven mainly by Eastern Europe

• Low China PMI at 48.9 indicatesmedium-term industrial contraction

• Southeast Asia and India will grow,but at a slower pace

North America

Latin America

Europe

China

Southeast Asia

India

79

Growth Driven by Industrial Megatrends

• Key initiatives address five durable industrial megatrends

• Investments advance the Industrial segment’s four fundamental strategies

• BOS defines the execution of segment growth programs

CustomerExperience

Technology ServicesChannelExpansion

Reliability EfficiencySmart ConnectedSystems

ExpertAssistance

Safety

How• Customer for Life• Electrification• Precision Fastening• Fluid Intelligence• Connected Car• Compressor Efficiency

Strategic Pillars

Industrial Megatrends

Where• Manufacturing• Food & Beverage• Pharmaceutical• Oil & Gas• Motor Vehicle• Electronics• Garage

With• Talent and Engagement• Operational Excellence• Growth Excellence• Product Growth Teams• Networks of Excellence• ERP System

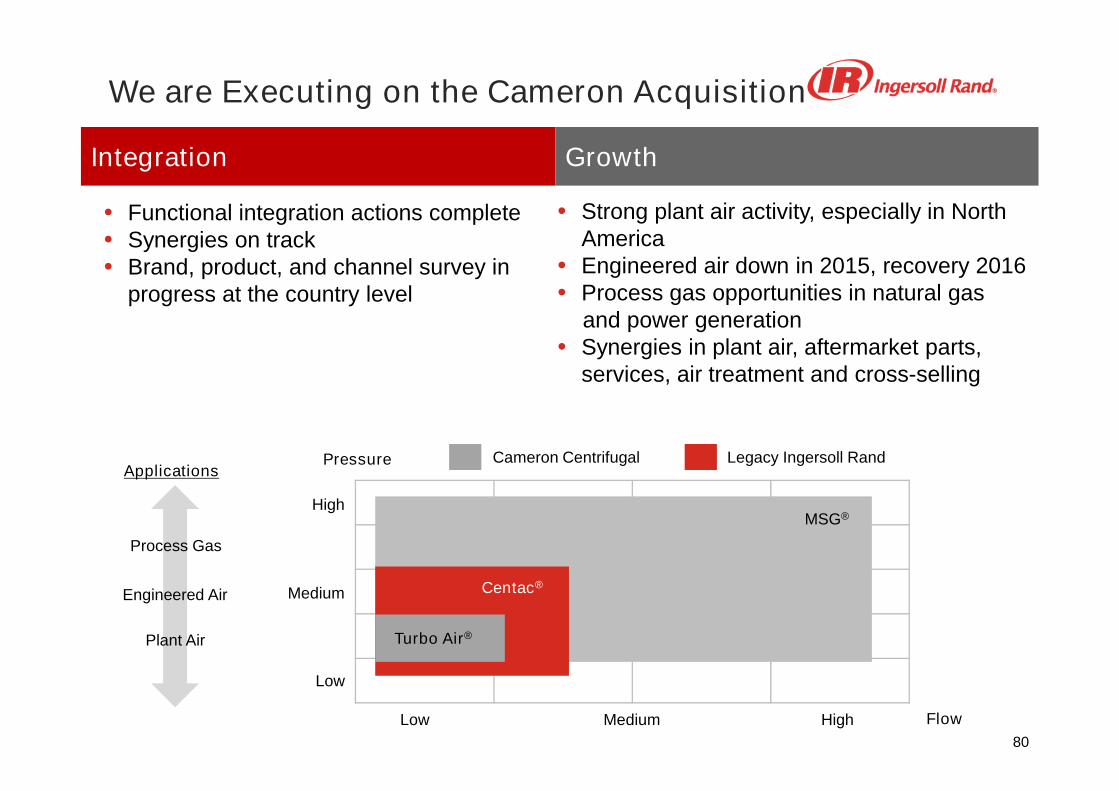

80

• Strong plant air activity, especially in NorthAmerica

• Engineered air down in 2015, recovery 2016• Process gas opportunities in natural gas

and power generation• Synergies in plant air, aftermarket parts,

services, air treatment and cross-selling

We are Executing on the Cameron Acquisition

Integration Growth

• Functional integration actions complete• Synergies on track• Brand, product, and channel survey in

progress at the country level

Process Gas

Engineered Air

Plant Air

Applications

High

Medium

Low

Low Medium High

Pressure

Flow

MSG®

Turbo Air®

Centac®

Cameron Centrifugal Legacy Ingersoll Rand

81

• Industrial continues journey for revenue and operating margin growth

• Clear levers to drive revenue and operating margin gains

We Will Deliver Profitable Growth

2014 2016F

Revenue Drivers

• Global market growth

• Share growth

• State-of-the-art products andtechnologies

• New services across all SBUs

• Channel expansion

• Comprehensive focus on reliability

Operating Margin Drivers

• State of the art products andtechnologies

• Operational excellence for productivity inmanufacturing and services

• Extensive use of Networks of Excellence

14.8%

15-16%

Adjusted Operating Margin

Financial Summary

Sue CarterSenior Vice President and CFO

2015 Investor and Analyst Conference

83

Adjusted Operating and EBITDA MarginsShow Steady Improvements in Operating Performance

2011 2012 2013 2014

Operating Margin EBITDA

8.7% 9.2%

12.0%11.6%

12.3%

9.6% 11.0%

13.6%

$11.9 $12.0 $12.3$12.9

2011 2012 2013 2014

Revenue $, Bil.

84

Balancing Capital Allocation AlternativesCreates Shareholder Value

Balance Sheet

• BBB Rating• No debt maturities until 2018

M&A

• Focused on core businesses• Value accretive on a risk

adjusted basis

Share Repurchase

• Repurchased 98M sharesfor $4.6B from 2011-14

• At a minimum will offsetshare dilution

Organic Investment

• New Product Dev.• BOS expansion• CAPEX=Depreciation

CompetitiveDividend

• Peer group payout• 28% dividend

CAGR, 2011-15Shareholder

Value

84

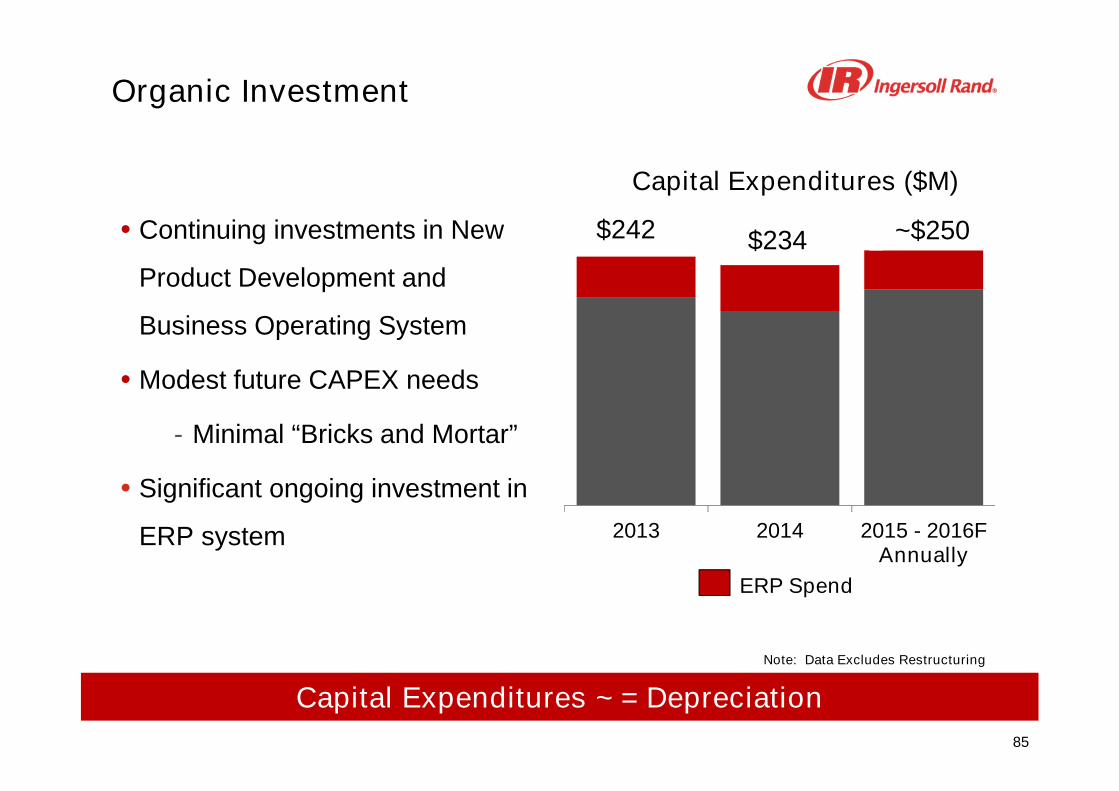

85

$242 $234

2013 2014 2015 - 2016FAnnually

Organic Investment

• Continuing investments in New

Product Development and

Business Operating System

• Modest future CAPEX needs

- Minimal “Bricks and Mortar”

• Significant ongoing investment in

ERP system

Capital Expenditures ($M)

Capital Expenditures ~ = Depreciation

ERP Spend

~$250

Note: Data Excludes Restructuring

86

Debt Maturity ProfileNo near term maturities

8 8 8 8 8 8 8 8 8 8 8

750

350

700

500

306

37

125150

300

500

300

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2043 2044

PutableAnnually

$, Mil

87

Strong Dividend Growth

Annual Dividend Per Share

$2.08$2.57

$2.67

$3.33

2011 2012 2013 2014

• $1.16 per share dividend for 2015

• 2015 dividend increased by 16% from 2014

• 28% dividend CAGR 2011 to 2015

$0.43

$0.64

$0.84

$1.00

$1.16

2011 2012 2013 2014 2015F

Adjusted EPS

88

2011 2012 2013 2014

840

1,2001,375

250

2015F

Share Repurchase

Avg. Shares outstanding, Mil Share Repurchase, $M

• New authorization in 2014 of $1.5B ; ~$900 Million remaining• ~98M shares for $4.6B for 2011 to 2014• Average share price of repurchase = $46.50 per share

339311 298

274 270

2011 2012 2013 2014 2015F

1,162Allegion

Distribution

36.3

#Shares Purchased, Mil.

21.8 23.018.4

89

M&A Framework

• Maintaining disciplined process; pipeline built from strategic plan

• Leverage existing businesses products, technologies and geographies

• Accretive to EBITDA, EPS and ROIC first full year of ownership

• Best talent on integration teams

• Will not overpay

Cameron Centrifugal Compressor FRIGOBLOCK

Key Product Lines

90

Balanced Future Cash Deployment

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 2015 Future

Share Repurchases

M&A or Share Rep.

Acquisitions

Dividends

Debt Paydown

91

Free Cash Flow

Long term goal 1X net income

2013 2014 2015 Target

~950 to 1,000

810860

$ Millions

Excludes restructuring, one-time spin costs and refinancing premium

92

Full-Year 2015 Forecast

Y-O-YRevenueChange

AdjustedOperating

Margin

Climate‒ Reported‒ Organic--ExFX

2% to 3%4% to 5%

12.5% to13.5%

Industrial‒ Reported‒ Organic

FX[-3%]andCameron[+12%]

13% to 14%4% to 5%

14.5% to15.5%*

Total ReportedOrganic

4% to 5%4% to 5%

11% to 12%*

*Includes Cameron operating results plus acquisition-related amortization costs of ~$6 million per quarter andexcludes inventory step-up costs of ~$12 million for both Q1 and Q2

93

Changes From Prior 2014 to 2016 forecast

• GDP Growth

- Slower than expected Asia and South America

• 17% drop in Euro vs $

- Revenue drag offset by acquisitions

- ($0.25) impact on EPS

• Lower than expected inflation

• End markets

- US Institutional recovery just beginning

- Stronger Thermo King North America

• Ongoing investments to drive future growth

94

Revenue Growth 4% to 5% 4% to 5%

Operating Income Growth 13% to 15% 13% to 15%

Operating Margin Change 85 bps to 100 bps 85 to 100 bps

Adjusted EPS 15% to 20% CAGR 15% to 20% CAGRBased on 24-26% tax rate Based 24-26% tax rate

Business Unit Operating Margins

- Climate 12% to 13% 13% to 14% in 2016

- Industrial 17% to 19% 15% to 16% in 2016

Cash Generation(X Net Income) 1.0 times 1.0 times

- Working capital/revenues 2% to 3% 3% to 4%

- 2016 ROIC ~10% ~10%

Ingersoll Rand Targets 2013 to 2016

Nov 2013 Forecast May 2015 Forecast

95

Ingersoll Rand

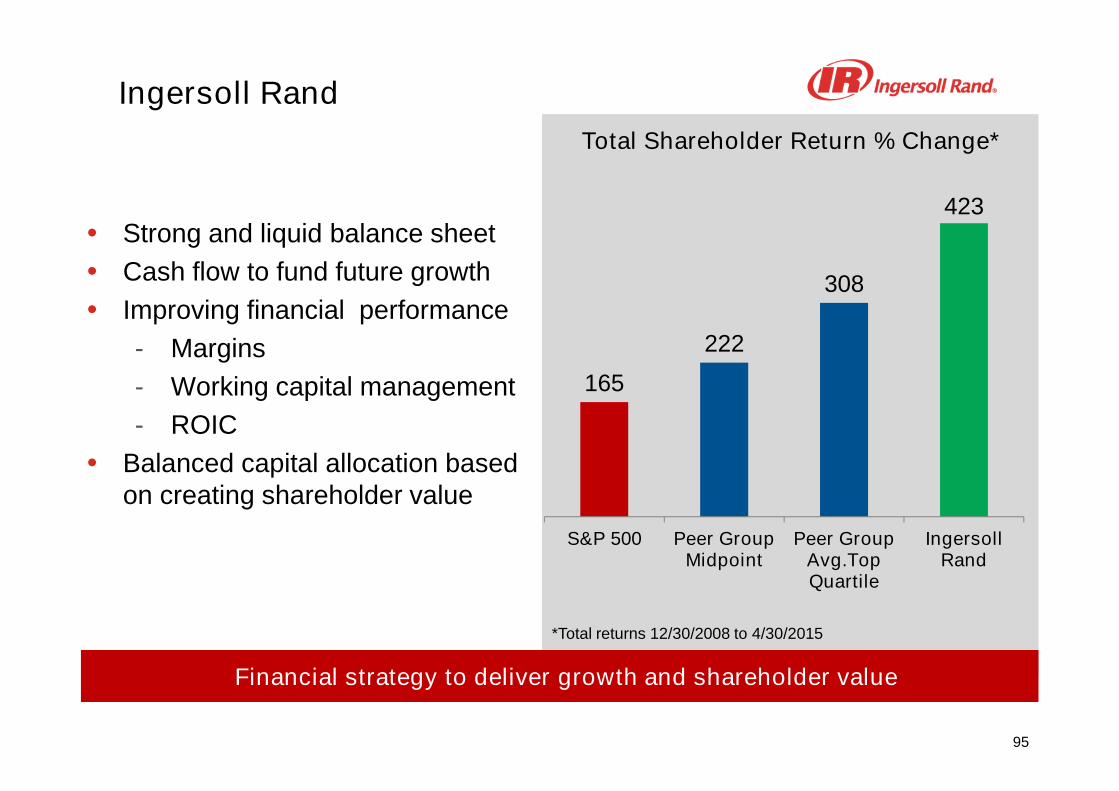

• Strong and liquid balance sheet

• Cash flow to fund future growth

• Improving financial performance

- Margins

- Working capital management

- ROIC

• Balanced capital allocation basedon creating shareholder value

Financial strategy to deliver growth and shareholder value

165

222

308

423

S&P 500 Peer GroupMidpoint

Peer GroupAvg.TopQuartile

IngersollRand

Total Shareholder Return % Change*

*Total returns 12/30/2008 to 4/30/2015

96