africa singapore business forum 2016 west africa: …/media/ie singapore/files/asbf2016... · forum...

TRANSCRIPT

Deals Advisory

Africa Singapore Business Forum 2016West Africa: Region Overview

Strictly Private and ConfidentialAugust 2016

Disclaimer "This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it."

"(c) 2016 PwC. All rights reserved. PwC refers to the Nigeria member firms, and may sometimes refer to the PwC network. Each member firm is a separate legal entity.

Please see www.pwc.com/structure for further details"

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

1 Overview of Africa 4

2 Key Economies in West Africa 7

3 Nigeria 8

4 Ghana 15

5 Cote d'Ivoire 18

6 Gabon and Equatorial Guinea 21

7 PwC point of view 25

8 PwC Experience in West Africa 27

Agenda

3Africa Singapore Business Forum 2016

Agenda

PwCAugust 2016

Confidential Information for the sole benefit and use of PwC’s Client.

Overview of Africa

Africa Singapore Business Forum 2016 • West Africa: Region Overview

4

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

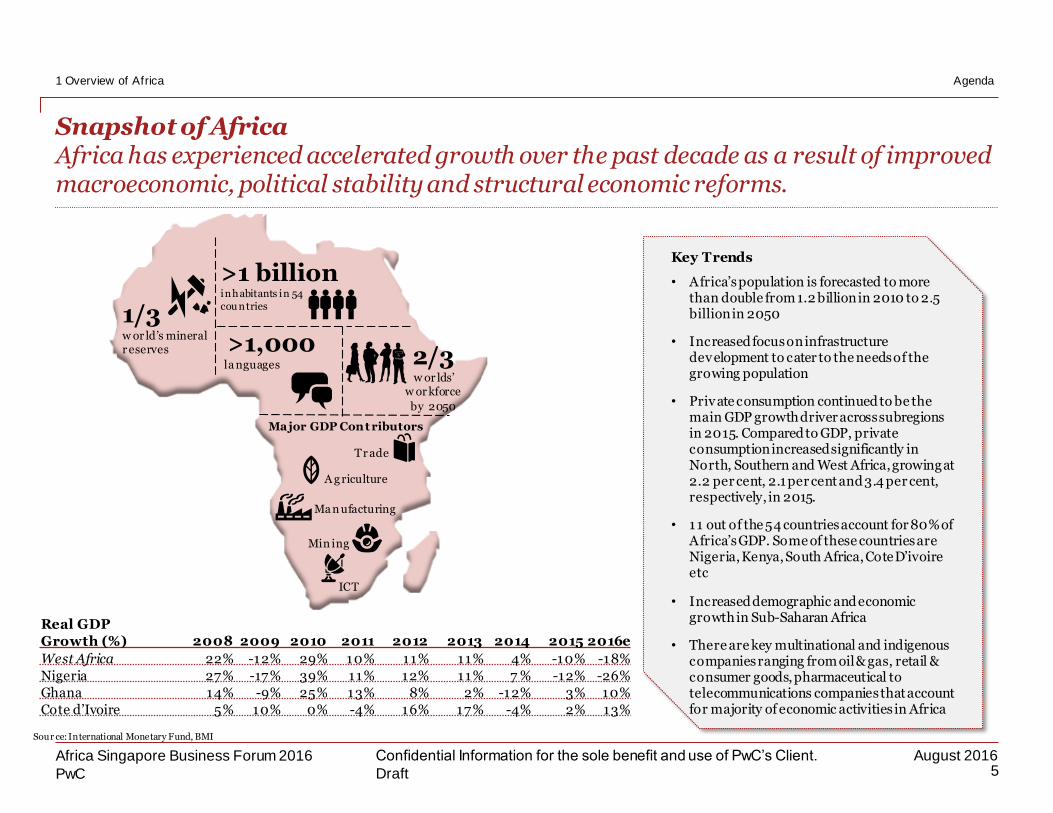

Snapshot of AfricaAfrica has experienced accelerated growth over the past decade as a result of improved macroeconomic, political stability and structural economic reforms.

5Africa Singapore Business Forum 2016

1 Overview of Africa

Key Trends

• Africa’s population is forecasted to more than double from 1.2 billion in 2010 to 2.5 billion in 2050

• Increased focus on infrastructure development to cater to the needs of the growing population

• Private consumption continued to be the main GDP growth driver across subregionsin 2015. Compared to GDP, private consumption increased significantly in North, Southern and West Africa, growing at 2.2 per cent, 2.1 per cent and 3.4 per cent, respectively, in 2015.

• 11 out of the 54 countries account for 80% of Africa’s GDP. Some of these countries are Nigeria, Kenya, South Africa, Cote D’ivoireetc

• Increased demographic and economic growth in Sub-Saharan Africa

• There are key multinational and indigenous companies ranging from oil & gas, retail & consumer goods, pharmaceutical to telecommunications companies that account for majority of economic activities in Africa

Real GDP

Growth (%) 2008 2009 2010 2011 2012 2013 2014 2015 2016e

West Africa 22% -12% 29% 10% 11% 11% 4% -10% -18%

Nigeria 27% -17% 39% 11% 12% 11% 7 % -12% -26%

Ghana 14% -9% 25% 13% 8% 2% -12% 3% 10%

Cote d’Ivoire 5% 10% 0% -4% 16% 17% -4% 2% 13%

>1 billion inhabitants in 54 cou ntries

>1,000la nguages 2/3

w or lds’ w or kforce

by 2050

1/3w or ld’s mineral r eserves

Sour ce: International Monetary Fund, BMI

Ma jor GDP Cont ributors

A g riculture

Tr ade

ICT

Min ing

Ma n ufacturing

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

West Africa is increasingly identified as an attractive destination for investors across all economic sectors

6Africa Singapore Business Forum 2016

1 Overview of Africa

Libreville

Kananga

Ndola

Nacala

Dar es Salaam

Zanzibar

Mombasa

Beira

Kalemie

Antananarivo

Maputo

Lusaka

Bulawayo

Harare

Gaborone

Johannesburg

Durban

Port Elizabeth

MaseruMbabane

Cape Town

Luderitz

Walvis Bay

Windhoek

Namibe

Menongue

Lobito

Malanje

Lilongwe

Mbeya

Lake Tanganyika

Luanda

Kinshasa

Brazzaville

Pointe-Noire

Toliara

Pretoria

Agadez

Zinder

Faya-Largeau

N' DjamenaMaiduguri

Kano

Abuja

Khartoum

Al Fashir

Juba

Waw

Asmara

Addis

Ababa

Port Sudan

Malabo

Yaounde

Bangui

Djibouti

Berbera

Mogadishu

Kisangani

Bujumbura

Nairobi

Kampala

Kigali

Bechar

Tripoli

Al Jawf

Oran

Algiers Tunis

Cairo

Aswan

ConstantineRabat

Marrakech

Casablanca

Laâyoune

TombouctouNema

Nouakchott

Tamanrasset

NiameyBamako

AlexandriaBanghazi

Abidjan

Accra

Loma

Porto-Novo

Ouagadougou

Lagos

Dakar

Monrovia

Freetown

Banjul

Conakry

Bissau

TANZANIA

BURUNDI

EQUATORIAL GUINEA

ANGOLA

REPUBLIC

OF THE

CONGO

MALAWI

ZAMBIAMOZAMBIQUE

MADAGASCAR

ZIMBABWE

BOTSWANA

SWAZILAND

LESOTHO

SOUTHAFRICA

NAMIBIA

ANGOLA

NIGER

CHAD

SUDAN

ETHIOPIA

DJIBOUTI

ERITREA

UGANDA

SOMALIA

KENYA

DEMOCRATIC

REPUBLIC

OF THE CONGO

(ZAIRE)

CENTRAL

AFRICAN

REPUBLIC

RWANDAGABON

NIGERIA

CAMEROON

TUNISIA

MOROCCO

WESTERN SAHARA

ALGERIA

MALI

LIBYAEGYPT

BENIN

TOGOCÔTE

D’IVOIRE

BURKINA FASOGUINEA

SENEGAL

GHANA

LIBERIA

MAURITANIA

SIERRA LEONE

THE GAMBIA

GUINEA BISSAU

Lake

Nyasa

Lake

Victoria

MediterraneanSea

RedSea

IndianOcean

IndianOcean

AtlanticOcean

AFRICA

WEST AFRICA

Region West A frica

GDP (nominal) USD 691 bn (2014)

Land Area 5,112,903km2

Population (T otal)

344mn (2014)

Population (15-64yrs)

183mn (2014)

Density 49.2/km2

Climate Tropical

Currency Naira (NGN), Cedi (GHS), W. African CFA franc (XOF), Dalasi (GMD), Franc (GNF), Dollar (LRD), Leone (SLL), Escudo (CVE),

Religion Christianity, Islam, African Traditional

Major Economies

Nigeria, Ghana, Cote d’Ivoire

Major Cities Lagos, Abuja, Accra, Abidjan, Port Harcourt

ECOWAS

• The Economic Community of West African States (ECOWAS) consists of 15 West African Countries

• ECOWAS was founded 28 May 1975 with the signing of the Treaty of Lagos

• The mission of ECOWAS is to promote economic integration across the region

• The Chairman is Ellen Johnson SirleafSou rce: BMI

Agenda

PwCAugust 2016

Confidential Information for the sole benefit and use of PwC’s Client.

Key Economies in West Africa

Africa Singapore Business Forum 2016 • West Africa: Region Overview

7

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Nigeria

8Africa Singapore Business Forum 2016

3 Nigeria Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Compelling investment opportunity - NigeriaNigeria is Africa’s largest economy and most populous nation

9Africa Singapore Business Forum 2016

3 Nigeria

Sou rce: CIA , National Bureau of Statistics, World Bank, Central Bank Of Nigeria

POPULATIONNo 1Economy in Africa

OFFICIAL LANGUAGE

CURRENCY

22nd largest

economy in the

world

DEMOGRAPHICS

CLIMATE

43%0-14 years

3% 65 years +

54%15-64 years

English

OIL PRODUCTION

No 1 producer

of crude oil in

Africa and 6th

largest in the world

Naira (NGN)

N

TIME ZONE

GMT +1

Tropical

36states and a

Federal Capital Territory,

Abuja

181.5mn

Over 250ethnic groups

Cou ntry Nigeria

Capital Abuja

President Muhammadu Buhari

GDP USD 484.4 bn (2015)USD 340 bn (post Naira float in June 2016)

Land Area 923,768km2

Exchange rate NGN 325 / USD (19th August, 2016)

Natural Resources

Petroleum, Iron ore, Coal and others

Religion Christianity, Islam

DiallingCode 234

Commercial Centres

Lagos, Port Harcourt, Abuja, Kano, Ibadan

ECONOMY

Key Highlights

• Urban population of 47.8%

• 13.6 mn active social media accounts

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Why invest in Nigeria?Significant growth trajectory driven by abundant natural resources and an enabling investment framework

10Africa Singapore Business Forum 2016

3 Nigeria

Stable political atmosphere

Low minimum wage

Fair tax policies

Large population workforce

Favourable government policies

22ndlargest economy in the

world and Africa’s largest economy.

A population of over 181 mn and growing, Nigeria represents the largest consumer demand in Africa.

In 2014, Nigeria received over

USD 8.3 bn in foreign

direct investments.

Easy access to market

Large road network

Sou rce: World Bank, PwC A nalysis

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Diversified investment opportunities across various sectors

11Africa Singapore Business Forum 2016

3 Nigeria

Entertainment and Hospitality

Manufacturing MiningAgriculture

Energy & Power Transportation

Key sectors identified by the government with medium to long term investment / development opportunities

Nigeria has 84 mn hectares of arable

land which is more than twice the size of Japan.

Nigeria accounts for 23.1% of

manufacturing activity in Africa

Over 40 mineral resources in over 500locations as at 2015

2ndlargest gas reserve in Africa (5.1 tcm)

and the 9thin the world in 2015

Estimated power demand of over 15 GW,but generation of ~2.5GW in June 2016

Extensive national rail network at

3,557 km, second only to South

Africa in length.

Sou rce: BMI, PwC Analysis

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Key enablers in the Nigeria investment equation

12Africa Singapore Business Forum 2016

3 Nigeria

Solving the Power ChallengeExperiencing growing pains but private sector leadership of the sector bodes well for the future

Increased focus on Public-Private Partnerships

Building Stronger Technical PartnershipsLimited locally developed technology platforms and technical expertise

Political stability and improved regulatory environment Stable democracy and successful civilian-to-civilian transition since 1999

Population and urbanization dynamic guarantees an offtake

market and a robust labour force

Infrastructure across all sector prioritized for

Investment

Sou rce: FMA RD, World Atlas, FAO, IITA , UNDP, IUF

Solving the Transport ChallengeIncreased involvement of the private sector in transport infrastructure is a huge focus

Better PlanningImproving culture of master planning and project planning, management and reviews

Local funding de-risking international fundingIncreased capabilities to deliver an investment base of locally generated equity and debt financing

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Success stories: illustrative transactions in Nigeria

13Africa Singapore Business Forum 2016

3 Nigeria

Investor/Target Industry Year Deal Size Description

Consumer Goods

2016 US$700 million

• Coco-Cola acquired 40% stake in Chi Ltd, a leading juice producer in Nigeria, with an option to increase its stake to 100%

ConsumerGoods

2015 US$ 450 million

• Kellogg Company, American cereal giant, paid US$450 million for a 50% stake in Nigeria-based Multipro, a food sales and distribution company owned by Tolaram, with an option to buy a stake in Tolaram's African unit

Oil and Gas 2013 US$ 3 billion

• Helios formed a US$3billion joint venture with BTG Pactual and Petrobras to explore for oil and gas in Angola, Benin, Gabon, Namibia, Nigeria and Tanzania

Retail 2015 US$ 54 million

• Actis, an emerging market focused private equity fund, invested US$54 million in Food Lover’s Market, an independent African food retailer

Telecommunications

2014 US$ 2.6billion

• ECP (Emerging Capital Partners), a private equity fund, invested US$2.6 billion in form of equity and debt in IHS for the acquisition of 2,100 towers, construction of new towers, and upgrade of existing towers in Nigeria

• The transaction won the Deal of the year at the PEA GP & Advisor Awards 2015

Success Story: Building an Industrial Conglomerate

• West Africa’s largest manufacturing conglomerate and one of the largest in Africa.

• Dangote group has operations in cement production, sugar & salt refining, flour milling, transportation & logistics, food & beverage and real estate

• Listed on the Nigerian Stock exchange and has subsidiaries in 5 other African countries. These are Ghana, Benin, South Africa, Cameroon and Zambia

• 26,000 employees with about US$ 3 billion in revenue in 2014. Market capitalisation of its cement subsidiary is US$ 14 billion

• Developing a US$ 9 billion oil refinery and petrochemical complex in Nigeria

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Simplifying and enabling your business / project investment decisionThe Nigerian Investment Promotion Commission (NIPC) was created to serve as the nation’s investment gateway

14Africa Singapore Business Forum 2016

3 Nigeria

Identification and invitation of potential investors to specific projects

Assistance in company incorporation processes

Coordination and streamlining of the activities of relevant agencies

3

4

5

Assistance in processing of regulatory approvals and permits from agencies

6

Promoting networking among investors7

Way s In Which NIPC

Helps To Foster Investments

Matchmaking local entrepreneurs with foreign partners

2

1Provision of investment information

The NIPC offers a one-stop-shop solution to ensure efficiency, transparency, and convenience for investors towards business entry processes as well as the guaranteed protection of investments.

Sou rce: corporate-nigeria.com, .nipc.gov.ng

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Ghana

15Africa Singapore Business Forum 2016

4 Ghana Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Ghana is one of Africa’s most active economies and stable democracies, having enjoyed above average economic growth due to the development of new sectors in addition to recent oil discoveries

16Africa Singapore Business Forum 2016

4 Ghana

Sources: CIA Factbook, Global-rates, World Bank, Oanda, IBGE, Trade Economics, IMF, Pw C Reports & Analysis

Cou ntry Gh a na

Area 238,533 sq km

Population 26.33mn (2015 est)

Climate Tropical

Natural Resources

Gold, Timber, Industrial diamonds, rubber, petroleum, silver, salt, limestone

GDP US$36.04bn (2015)

GDP Real Growth Rate 3.5% (2015)

LabourForce 11 .54mn (2015)

Unemployment rate 5.2% (2013)

MajorCities Accra, Kumasi

Currency Cedi

Tax and Regulation

2014

1. Corporate Income Tax (CIT) 25%

2. Personal Income Tax 0-25%

3. Ease of pay ing taxes ranking 68/189

* Average world tax rate is 43.1%

CÔTED’IVOIRE

TOGO BENIN

BURKINA FASO

Badou

Bohicon

Baf iloBouna

Cape Coast

Sekondi

Awaso

Kumasi

Kof oridua

Ho

Suny ani

Tamale

Wa

Bolgatanga

Lomé

Accra

Ghana

LakeVolta

Gulf of Guinea0 25 50 75 Kilometers

75 Miles50250

Ghana

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Ghana is one of Africa’s most active economies and stable democracies, having enjoyed above average economic growth due to the development of new sectors in addition to recent oil discoveries

17Africa Singapore Business Forum 2016

4 Ghana

Sources: CIA Factbook, Global-rates, World Bank, Oanda, IBGE, Trade Economics, IMF, Pw C Reports & Analysis

2015 GDP Contribution by Sector

2 1%

2 8 %5 1%

Agriculture Industry Services

Key facts • The Ghanaian economy is driven by exports of its valuable natural resources such as gold and oil, as well as manufacturing

Telecommunications

• Ghana has been successful in expanding access to mobile services with 30.36millionn mobile subscriptions at the end of December 2014

• Major players in the industry are MTN, Vodafone, Tigo and Airtel. Other players include Globacom and Expresso

Oil and Gas • Ghana is an energy economy in transition. Having been largely import-dependent for decades, the start-up of the Jubilee oil field in 2010 has transformed the country into a net exporter

• Ghana faces the same internal capacity challenges as many other African countries

Retail • Department store chain in the countryinclude Woolworths, pick n pay

• Global makeup brand Maybelline officially launched in Ghana during May 2015

• The country's urban and wealthy areas have experienced a number of modern retail projects

Consumer Goods

• Presence of major fast moving consumer goods companies in the country. Some of these companies include Unilever, PZ cussons

• Consumer goods purchase account for 41%of total monthly household expenditure

32

37 39 40

35 36

40

0%

13%

8%

2%

-12%

3%

10%

(15%)

(10%)

(5%)

0%

5%

10%

15%

0

5

10

15

20

25

30

35

40

45

2010 2011 2012 2013 2014 2015 2016e

US

Db

n

Ghana Nominal GDP

GDP GDP Growth

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Cote d'Ivoire

18Africa Singapore Business Forum 2016

5 Cote d'Ivoire Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Cote d’Ivoire has shown steady recovery from major political crisis and shows prospects for growth

19Africa Singapore Business Forum 2016

5 Cote d'Ivoire

Sou rce: African Development Bank Group, Business Monitor International, CIA Factbook

Cou ntry Cot e d’Iv oire

Area 322,463 sq km

GDP $31.17bn (2015)

GDP – real growth rate

8.6% (2015 est.)

Population 23.3mn (2015)

Urban population 54.2% of total population (2015)

Inflation rate (consumer prices)

1 .2% (2015 est.)

Natural resources Petroleum, Natural gas, Diamonds, Iron ore, Gold, Copper, Cocoa beans, Coffee etc.

Climate Tropical

Official language French

Currency CFA

Primary airport Abidjan

Odienné

Korhogo

Séguéla Bondoukou

Man Bouaké

Daloa

Adzopé

Dabou

Abidjan

Aboisso

San-Pédro

GHANA

BURKINAFASO

MALI

GUINEA

LIBERIA

YAMOUSSOUKRO

Gulf of Guinea

CÔTE D’IVOIRE

Tax and Regulation

2014

1. Corporate Income Tax (CIT) 25%

2. Personal Income Tax 60%

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Cote d’Ivoire has shown steady recovery from major political crisis and shows prospects for growth

20Africa Singapore Business Forum 2016

5 Cote d'Ivoire

1 8 %

2 0%

6 2 %

Agriculture Industry Services

Sources: CIA Factbook, Global-rates, World Bank, Oanda, IBGE, Trade Economics, IMF, Pw C Reports & Analysis

2015 GDP Contribution by Sector

• 54.2% of Cote d’Ivoire’s total population is the urbanpopulation, leaving the rural population at 45.8%. It isexpected to reach 57.5% by year 2020

• Cote d’Ivoire has a literacy rate of 43.1%

• Cote d’Ivoire’s working Population (15-64 years) of thetotal population is 55.4%

Consumer Goods

• Rising income and an underdeveloped consumer goods sector have made Cote d’Ivoire a destination for consumer goods companies looking to expand

Oil and Gas • Cote d’Ivoire has significant offshore petroleum and natural gas reserves which has caused a major boom for the country’s revenue

• Oil refining and processing has also been another major source of revenue

Retail • Cote d'Ivoire's retail sector should experience rapid growth as a result of underdevelopment, rising income level. The entrance of Jumia in 2013 has

opened up e-commerce sector in the country

T elecommunications

• Major players in this sector are MTN, Orange, Moov, GreenN and Koz• In 2014, Cote d’Ivoire had 23.9million mobile subscribers accounting for 109%

penetration rate. Value added Service is the major source of value for customers

Key sectors driving growth

25 24

28

33 31 32

36

0%

-4%

16%17%

-4%

2%

13%

(10%)

(5%)

0%

5%

10%

15%

20%

0

5

10

15

20

25

30

35

40

2010 2011 2012 2013 2014 2015 2016e

US

Db

n

Cote d'Ivoire Nominal GDP

GDP GDP Growth

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Gabon and Equatorial Guinea

21Africa Singapore Business Forum 2016

6 Gabon and Equatorial Guinea Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Gabon – Macro-economic Overview

22Africa Singapore Business Forum 2016

6 Gabon and Equatorial Guinea

Cou ntry Ga bon

Area 267,667 sq km

GDP $14.35 bn(2015)

GDP – real growth rate 4% (2015)

GDP – per capita (PPP) $18,600(2015)

Population 1 .71mn

Labour force 653,700 (2015)

Literacy rate 83.2%

Inflation rate 0.1% (2015)

Climate Tropical

Urban population 87 .2% of total population (2015)

Official language French

4 %

3 9 %

5 7 %

Agriculture

Industry

Services

2015 GDP Contribution by Sector

Oyem

Makokou

Kango

Booué

LastoursvilleLambarénéPort-Gentil

MouilaFranceville

Tchibanga

Mayumba

Owendo

CAMEROON

EQUATORIAL

GUINEA

REP. OF

THE CONGO

REP. OF

THE CONGO

Bight

of

Biafra

Corisco

Bay

South

Atlantic

Ocean

GABON

LIBREVILLE

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Why invest in Gabon?

23Africa Singapore Business Forum 2016

6 Gabon and Equatorial Guinea

Quality investor services

Development of transport infrastructure

Construction of a Tax Free Trade

Zone

Commitment to economic growth

Politically stable Strong foreign trade relations

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

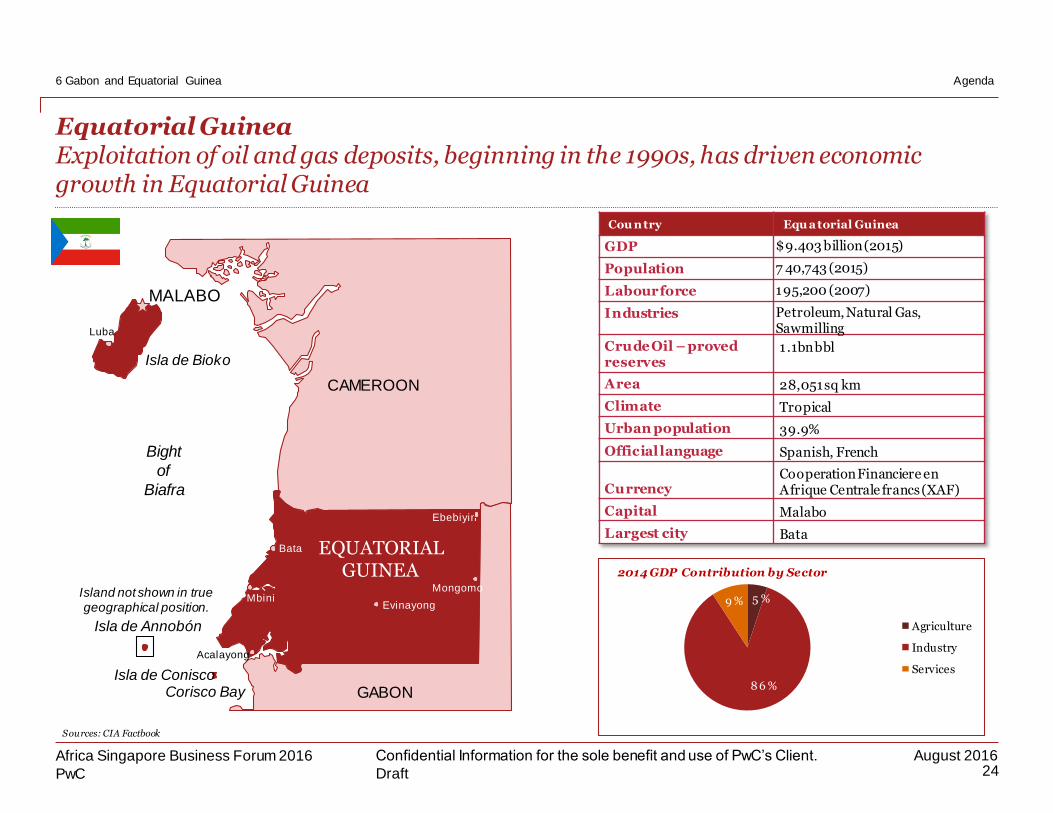

Equatorial GuineaExploitation of oil and gas deposits, beginning in the 1990s, has driven economic growth in Equatorial Guinea

24Africa Singapore Business Forum 2016

6 Gabon and Equatorial Guinea

Luba

Bata

Ebebiyin

Mongomo

EvinayongMbini

Acalayong

Isla de Bioko

Isla de Conisco

Isla de Annobón

Island not shown in truegeographical position.

Bight

of

Biafra

Corisco Bay

MALABO

EQUATORIALGUINEA

CAMEROON

GABON

Cou ntry Equ a torial Guinea

GDP $9.403 billion (2015)

Population 7 40,743 (2015)

Labourforce 195,200 (2007)

Industries Petroleum, Natural Gas, Sawmilling

CrudeOil – proved reserves

1 .1bn bbl

Area 28,051 sq km

Climate Tropical

Urban population 39.9%

Official language Spanish, French

CurrencyCooperationFinanciere en Afrique Centrale francs (XAF)

Capital Malabo

Largest city Bata

Sources: CIA Factbook

5 %

8 6 %

9 %

Agriculture

Industry

Services

2014 GDP Contribution by Sector

Agenda

PwCAugust 2016

Confidential Information for the sole benefit and use of PwC’s Client.

PwC point of view

Africa Singapore Business Forum 2016 • West Africa: Region Overview

25

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Africa will continue to experience significant investment interest

26Africa Singapore Business Forum 2016

7 Pw C point of view

Africa’s real GDP growth is expected to increaseby about 4.3 per cent in 2016 and 4.4 per cent in2017, led by strong domestic demandand by investment, particularly in infrastructure

By 2025, Urbanization will be above 50% of Africa. A quarter of global population will be African by 2050 – large retail and consumer, communication, and telecommunications opportunities

Infrastructure spend in Africa to reach US$ 180 billion per annum by 2025- caused by increased demand for energy, transportation, ICT, consumer goods, water supply and urbanisation

Consumer spending will nearly double to $1 trillion by 2020. Africa would have the largest labour force by 2050

Africa is dominating global growth with its growth in population, capital inflows and infrastructure development

Emergence of more African multinationals similar to Dangote Group, MTN group, KenolKobil and Shoprite

West Africa’s growth is projected to increase to about 5.2 per cent in 2016 and 5.3 per cent in 2017, boosted mainly by an improving economic performance in Nigeria, with its emphasis on diversifying investments into non-oil sectors

Private equity investment in Africa has increased by 20% yearly for the last decade, making it the fastest growing private equity market globally

Agenda

PwCAugust 2016

Confidential Information for the sole benefit and use of PwC’s Client.

PwC Experience in West Africa

Africa Singapore Business Forum 2016 • West Africa: Region Overview

27

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

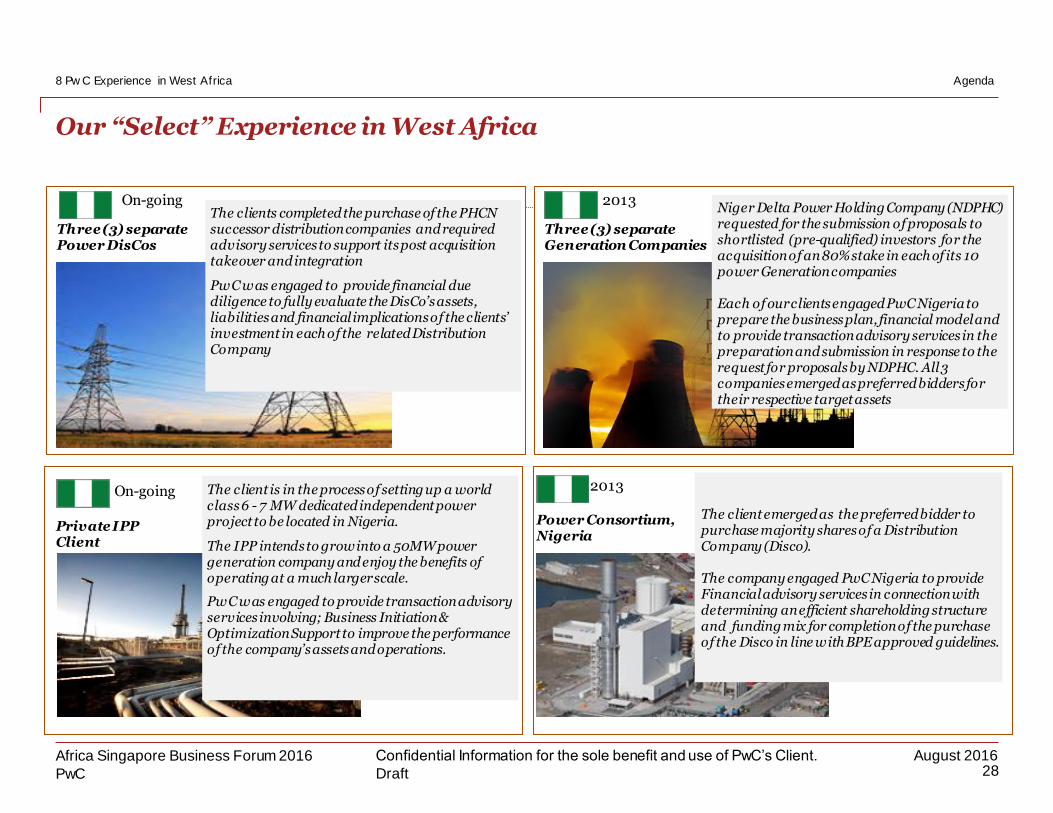

Our “Select” Experience in West Africa

28Africa Singapore Business Forum 2016

8 Pw C Experience in West Africa

The clients completed the purchase of the PHCN successor distribution companies and required advisory services to support its post acquisition takeover and integration

PwC was engaged to provide financial due diligence to fully evaluate the DisCo’s assets, liabilities and financial implications of the clients’ investment in each of the related Distribution Company

Three (3) separate Power DisCos

On-going 2013

Three (3) separate Generation Companies

Niger Delta Power Holding Company (NDPHC) requested for the submission of proposals to shortlisted (pre-qualified) investors for the acquisition of an 80% stake in each of its 10 power Generation companies

Each of our clients engaged PwC Nigeria to prepare the business plan, financial model and to provide transaction advisory services in the preparation and submission in response to the request for proposals by NDPHC. All 3 companies emerged as preferred bidders for their respective target assets

Private IPP Client

On-going The client is in the process of setting up a world class 6 - 7 MW dedicated independent power project to be located in Nigeria.

The IPP intends to grow into a 50MW power generation company and enjoy the benefits of operating at a much larger scale.

PwC was engaged to provide transaction advisory services involving; Business Initiation & Optimization Support to improve the performance of the company’s assets and operations.

2013

Power Consortium, Nigeria

The client emerged as the preferred bidder to purchase majority shares of a Distribution Company (Disco).

The company engaged PwC Nigeria to provide Financial advisory services in connection with determining an efficient shareholding structure and funding mix for completion of the purchase of the Disco in line with BPE approved guidelines.

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

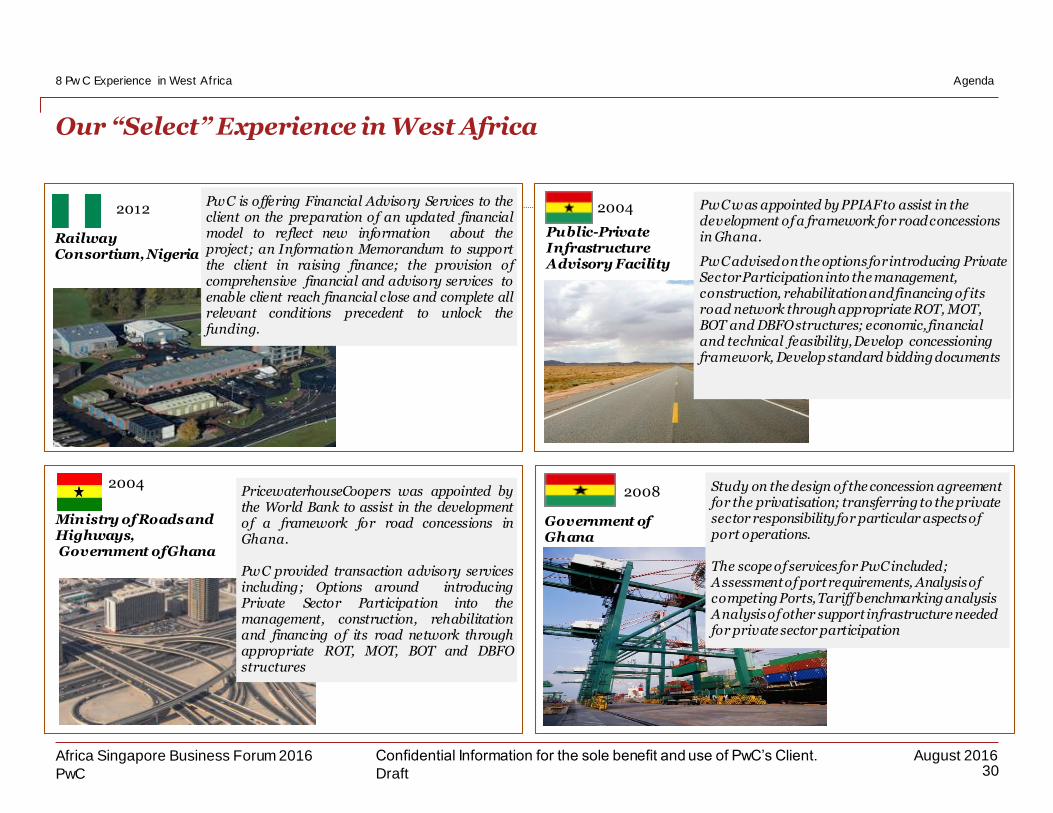

Our “Select” Experience in West Africa

29Africa Singapore Business Forum 2016

8 Pw C Experience in West Africa

The client, a state owned electricity generator, appointed PwC to advise on the divestment of a proportion of the equity in Ghana’s main thermal power plant to an American utility, CMS.

PwC services included: Reviewing the previous valuation of the power project; financial modeling of the project, Preparing an information memorandum, setting the proposed terms of the divestiture, and a fair value report; Negotiating the terms with CMS.

State owned electricity generator

PwC was appointed by PPIAF to assist in the development of a framework for road concessions in Ghana.

The study focused on: Advising the Government of Ghana on options for introducing Private Sector Participation into the management, construction, rehabilitation and financing of its road network through appropriate ROT, MOT, BOT and DBFO structures; economic, financial and technical feasibility, Develop concessioning framework, Develop standard bidding documents

Public-Private Infrastructure Advisory Facility

2004

111111111111111111111111111111111111111``

Ministry of Finance and Economic Planning

The Ministry of Finance and Economic Planning of Ghana required the assistance of suitable professionals to advise on the dualisationof the 237km Accra-Kumasi Toll highway, through a PPP arrangement.

PwC advised on key aspects of the transaction including: Overall project management; feasibility studies; Construction and operational managements; Advising on the appropriate procurement of the project.

2008

2000

Ministry of Finance and Economic Planning

The Ministry of Finance and Economic Planningof Ghana required the assistance of suitableprofessionals to advise on the dualisation of the237km Accra-Kumasi Toll highway, through aPPP arrangement.

PwC advised on key aspects of the transactionincluding: Overall project management;feasibility studies; Construction and operationalmanagements; Advising on the appropriateprocurement of the project.

2008

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Our “Select” Experience in West Africa

30Africa Singapore Business Forum 2016

8 Pw C Experience in West Africa

Railway Consortium, Nigeria

PwC is offering Financial Advisory Services to theclient on the preparation of an updated financialmodel to reflect new information about theproject; an Information Memorandum to supportthe client in raising finance; the provision ofcomprehensive financial and advisory services toenable client reach financial close and complete allrelevant conditions precedent to unlock thefunding.

2012

Ministry of Roads and Highways,Government of Ghana

2004PricewaterhouseCoopers was appointed bythe World Bank to assist in the developmentof a framework for road concessions inGhana.

PwC provided transaction advisory servicesincluding; Options around introducingPrivate Sector Participation into themanagement, construction, rehabilitationand financing of its road network throughappropriate ROT, MOT, BOT and DBFOstructures

PwC was appointed by PPIAF to assist in the development of a framework for road concessions in Ghana.

PwC advised on the options for introducing Private Sector Participation into the management, construction, rehabilitation and financing of its road network through appropriate ROT, MOT, BOT and DBFO structures; economic, financial and technical feasibility, Develop concessioning framework, Develop standard bidding documents

Public-Private Infrastructure Advisory Facility

2004

Study on the design of the concession agreement for the privatisation; transferring to the private sector responsibility for particular aspects of port operations.

The scope of services for PwC included;Assessment of port requirements, Analysis of competing Ports, Tariff benchmarking analysisAnalysis of other support infrastructure needed for private sector participation

Government of Ghana

2008

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Our “Select” Experience in West Africa

31Africa Singapore Business Forum 2016

8 Pw C Experience in West Africa

Property Investor

2012 The client required market and financialfeasibility study for the residential component ofa mixed-use development in Abuja, Nigeria.

PwC provided services which include marketresearch and analysis for residential sector,review of master plan and recommendations,supply and demand assessments, and financialanalysis for the project.

A hotel in Accra

2012

Group Company in Ghana

2012 The project involved the assessment of theproperty market in Accra for office andresidential accommodation which was expectedto feed into the client’s business plan to beincluded in a proposal to be submitted topotential lenders.

PwC advised on the project documentationincluding a review of the client’s plan for theproposed project. The scope of services include:

The client required a market and financialfeasibility study for a proposed mixed usedevelopment to be anchored by a 250-room hotelin the Central Business Districtof Accra, Ghana.

PwC conducted high-level market research andprovided an assessment of the alternativepossible components for the project whichinvolved analysis of the residential, lodging,retail, serviced apartments, and office marketsin Accra

2010

Government-Affiliated Holding Company

2012

Real Estate Developer, Nigeria

The project involved the provision ofconsultancy services for the development of ashoppingmall in Nigeria.

PwC was engaged by the Project Financecompany to design and develop the businessprocess model, organisational structures, jobdescriptions for key roles and the policies &procedures manuals.

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Our “Select” Experience in West Africa

32Africa Singapore Business Forum 2016

8 Pw C Experience in West Africa

2010

Government-Affiliated Holding CompanyUpstream Oil and Gas Company, Nigeria

PwC was engaged by a Nigeria UpstreamPetroleum Company interested developing 2parcels of lands into both commercial andresidentialproperty.

PwC was mandated to carry out a feasibilitystudy into the Nigerian real estate andconstruction industry highlighting the marketand demand risks as they affect the proposedproject.

Mixed Use Devt., Benin

PwC was engaged to provide a review of a market and financial feasibility followed by capital sourcing for a mixed-use development in Porto-Novo, Benin. The project components comprised hotel, residential apartments, commercial offices, industrial park, and warehousing and storage.

The scope of services include: Market Analysis; Review of Feasibility Study; Financial Modeling; Project Finance

2012 2009

2010

Government-Affiliated Holding CompanyUpstream Oil and Gas Company

PwC was engaged by a Nigeria UpstreamPetroleum Company interested developing 2parcels of lands into both commercial andresidentialproperty.

PwC was mandated to carry out a feasibilitystudy into the Nigerian real estate andconstruction industry highlighting the marketand demand risks as they affect the proposedproject.

PwC was engaged to provide a review of a market and financial feasibility of setting up a crude oil refining facility in nigeria

PwC scope of services include: Market analysis; commercial analysis of feedstock yield, location analysis, feedstock contracting options, high level returns analysis

Indigenous Investment Company

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Our “Select” Experience in West Africa

33Africa Singapore Business Forum 2016

8 Pw C Experience in West Africa

2010

Government-Affiliated Holding Company

Indigenous Hospital Indigenous Hospital

Health Regulatory Organization

Indigenous Hospital

The client sought to develop a 5-year growth strategy. PwC’s services included: Assessment of the healthcare industry in Nigeria to assess market size, growth trends and drivers, consumer behaviour and competitive landscape; Internal analysis of the hospital covering several areas including people, processes, systems and policies; Identification and assessment of various models for future operations; Support in identification of viable strategies to support the client’s growth aspirations

PwC was engaged to perform a reaccreditation of HMOs to determine their level of compliance with prescribed conditions and standards as well as proferrelevant recommendations that would strengthen the operation of the HMOs.

Services included: Review and update of the accreditation checklist; Assessment of HMO’s level of compliance in four major areas; Identification of gaps and areas for strengthening

PwC was engaged by a leading health care institution in Nigeria to provide advisory services towards articulating and financing its growth and expansion strategy.

PwC carried out an options analysis of one of the client’s assets and conducted a review of the client’s baseline business model, valuation and returns analysis. Other phases of the project would include examining and refining the client’s growth and expansion strategy and assisting the client to secure appropriate financing for the expansion program.

PwC was engaged to provide financial advisory services to a multi-specialist hospital in the pre-construction stage of developing a health facility.

PwC conducted a review of the client’s existing financial model and then went on to develop a clean build financial model and confidential information memorandum which was issued to potential investors and financiers.

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Our “Select” Experience in West Africa

34Africa Singapore Business Forum 2016

8 Pw C Experience in West Africa

Telco Investment company, Nigeria

2014 A Telecommunications Investment companyintends to acquire the business units and assets of anational carrier in the Nigeriantelecommunications industry. PwC was engaged toassist with the entire acquisition process of theTelecommunication assets.

PwC provided Bid acquisition and advisoryservices to guide the acquisition of the nationalcarrier company

State Water Corporation, Nigeria

PwC in partnership with an engineering firmwas engaged by the corporation to provideTransaction Advisory Services for publicsector Water supply Scheme.Services included: Need, technical, socio•-economic, legal and commercial viabilityassessments, Initial environmentalexamination assessment, Preliminary riskand stakeholder assessment, Affordabilityand value for money assessment, PPP optionand financial analysis

To help meet the Millenium Development Goals(MDGs) in the water sector in 8 countries inAfrica, the EIB launched the Water ProjectPreparation Facility (WPPF) to fund technicalassistance for projectpreparationactivities.PwC provided the following services: Projectidentification and selection, Critical review ofsuccessful and failed past projects, Inventory ofon-going and proposed projects in each country.Design of potential projects, with emphasis onPPPs & identification of co-financiers. Pre-selection of projectsasper WPPFcriteria.

European Investment Bank (EIB)

2008Project Green, Nigeria

2014 The client, a Nigerian company that had equitystake in a Gabonese refinery wanted to conduct avaluationof their equity stake.

PwC was engaged to provide financial advisoryservice. The services provided include buildingfinancial projections, the valuation of the refineryand the stake of the Nigeriancompany.

2012

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

Recent Financial Advisory Mandates in West Africa (1/2)

35Africa Singapore Business Forum 2016

8 Pw C Experience in West Africa

PROJECT FIDDLE

Nig erian mortgage bank

seeking to restructure its bu siness

Serv ices Provided: Fin ancial modelling and

v aluation

PROJECT T RIBECA

Nig erian m ortgage bank

r a ising capital

Serv ices Provided: Bu sin ess plan, financial

m odel and capital raising

PROJECT CONCORD

Nig erian commercial

ba n king raising Tier 1 Ca pital

Serv ices Provided: Fin ancial model and

Ca pital raising

PROJECT GLOW

Nig erian commercial

ba n k requesting support for the valuation of a

su bsidiary for goodwill im pairment

Serv ices Provided:

Fin ancial model and Ca pital raising

PROJECT WINDSA IL

A Nig erian pension fund

a dministrator requiring fin ancial projections for

str ategic planning pu rposes

Serv ices Provided:

Fin ancial modelling

PROJECT LILA C

Nig erian property

dev elopment company r a ising capital

Serv ices Provided:

Fin ancial m odel and Ca pital raising

PROJECT CRYST AL

Nig erian microfinance

ba n k seeking to raise ca pital

Serv ices Provided: Fin ancial projections and

v aluation

PROJECT KA CHI

Nig erian health care

pr ov ider a ssessing the v iability of an intended

pr oject

Serv ices Provided: Fin ancial modelling and

commercial due diligence

PROJECT A ST ON

Nig erian a sset

m anagement company seeking an appraisal of

a n intended m erchant ba n king business

Serv ices Provided:

Fin ancial modelling

PROJECT ST YLE

PE firm seeking to invest

in a key player in the r etail industry

Serv ices Provided: Fin ancial model review

a n d commercial due diligence

Agenda

PwC

August 2016Confidential Information for the sole benefit and use of PwC’s Client.

Draft

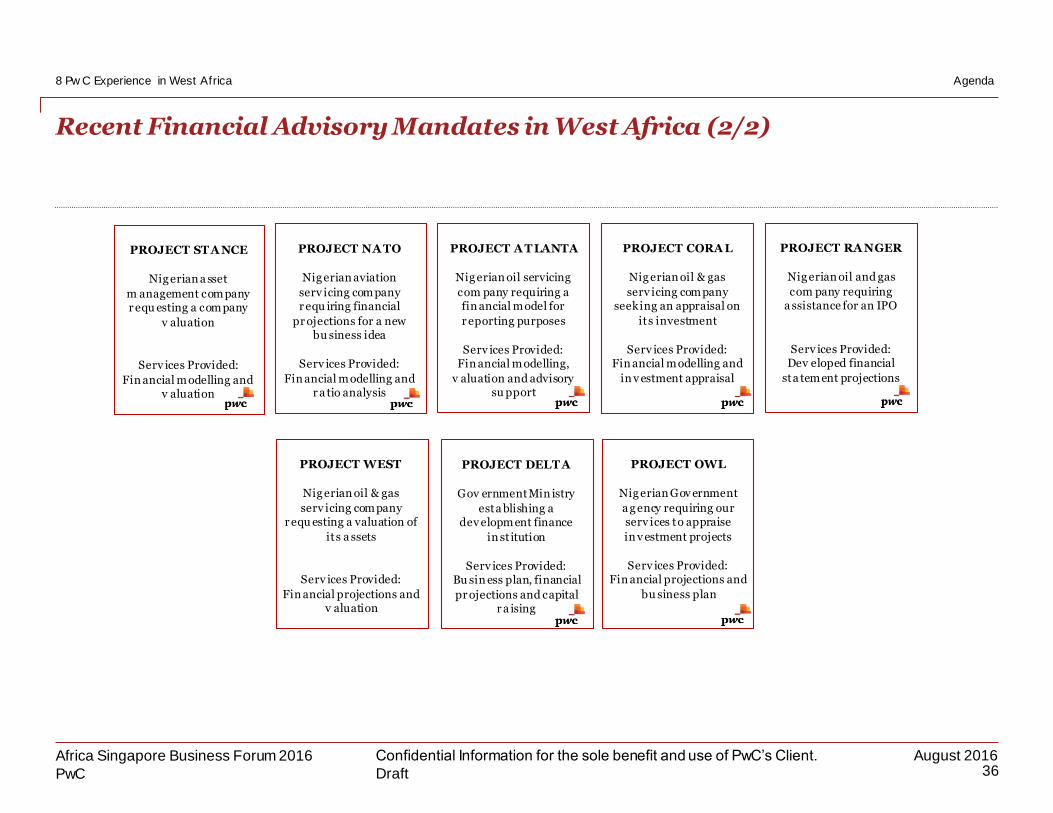

Recent Financial Advisory Mandates in West Africa (2/2)

36Africa Singapore Business Forum 2016

8 Pw C Experience in West Africa

PROJECT WEST

Nig erian oil & gas

serv icing company r equ esting a valuation of

its a ssets

Serv ices Provided:

Fin ancial projections and v aluation

PROJECT RA NGER

Nig erian oil and gas

com pany requiring a ssistance for an IPO

Serv ices Provided: Dev eloped financial

sta tement projections

PROJECT CORA L

Nig erian oil & gas

serv icing company seeking an appraisal on

its investment

Serv ices Provided: Fin ancial modelling and

in v estment appraisal

PROJECT A T LANTA

Nig erian oil servicing

com pany requiring a fin ancial model for

r eporting purposes

Serv ices Provided: Fin ancial modelling,

v aluation and advisory su pport

PROJECT OWL

Nig erian Gov ernment

a g ency requiring our serv ices to appraise

in v estment projects

Serv ices Provided: Fin ancial projections and

bu siness plan

PROJECT DELT A

Gov ernment Min istry

esta blishing a dev elopment finance

in st itution

Serv ices Provided: Bu sin ess plan, financial

pr ojections and capital r a ising

PROJECT NA TO

Nig erian aviation

serv icing company r equ iring financial

pr ojections for a new bu siness idea

Serv ices Provided:

Fin ancial modelling and r a tio analysis

PROJECT ST A NCE

Nig erian a sset

m anagement com pany r equ esting a com pany

v aluation

Serv ices Provided:

Fin ancial m odelling and v aluation

Agenda

PwC

Contact Details:

Ian Aruofor

PartnerPwC | Deals AdvisoryDirect: +234 1 271 1700 Ext 47001Cell : +234 805 609 9667

Thank you

PwC provides industry-focused assurance, tax, human resource and advisory services to build public trust and enhance value for our clients and their stakeholders. The PricewaterhouseCoopers network in Africa has member firms in 33 countries with over 6,000 professional staff. Together with more than 208,000 people in 157 countries around the world, we share our thinking, experience and solutions to develop fresh perspectives and practical advice.

‘PricewaterhouseCoopers’ refers to the network of member firms of PricewaterhouseCoopers International Limited. Each member firm is a separate and independent legal entity.

Thank you

© 2016 PricewaterhouseCoopers Limited. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Limited, which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.