advanced financial management as per syllabus

TRANSCRIPT

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 1/68

PAPER III -5.ADVANCED FINANCIAL MANAGEMENT

Unit – 1

An overview of Corporate Financing Patterns of Corporate Financing in

India.

Overview of Pattern of Corporate Financing in India

The pattern of corporate financing in India has been different throughout its economic history.The outline of corporate financing in India has been determined by the economic rules andregulations that operate at different points of time.

Pattern of Corporate Financing in India from 1960 to 1990

During the 30-year period in Indian economy ranging from 1960 to 1990 the stress of Indianeconomy was on public finance. There were a lot of rules and regulations regarding variouseconomic issues like rates of interest and many more.

During the middle part of the decade of 80s there was some change in the Indian economicscenario.The performance of the capital markets in India improved.

Pattern of Corporate Financing in India from 1990 onwards

After 1992 a lot of reforms have been made in the capital markets of India. The performance of the stock markets of India was remarkable in the 1990s. This was keeping with the healthy state

of the Indian economy in and around that time.

All this altered the trend of corporate financing in India. The dependency on banks for loans or other financial assistance reduced to a significant extent. The equity capital that was gained fromthe capital markets came up as a suitable alternative for them.

The Gross Domestic Product of India rose steadily in this period. The Gross Domestic Productwent up by about 4.3% in 1992-93. The Gross Domestic Product of India again increased byalmost 2% in the year 1995-96. The growth rate of the Gross Domestic Product of India has beenimpressive in the recent years.

Role of Banking Sector in Pattern of Corporate Financing in India

The banking sector of India has played an important role in the context of the development of Indian economy. The banks of India have been doing well with the distribution of funds andmonetary resources for the purpose of the development of India's economy.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 2/68

Equity versus Debt –

Debt vs. equity financing is one of the most important decisions facing managers who needcapital to fund their business operations. Debt and equity are the two main sources of capitalavailable to businesses, and each offers both advantages and disadvantages. "Absolutely nothing

is more important to a new business than raising capital," Steve Jefferson wrote in Pacific Business News (Jefferson, 2001). "But the way that money is raised can have an enormousimpact on the success of a business."

DEBT FINANCING

Debt financing takes the form of loans that must be repaid over time, usually with interest.Businesses can borrow money over the short term (less than one year) or long term (more thanone year). The main sources of debt financing are banks and government agencies, such as theSmall Business Administration (SBA). Debt financing offers businesses a tax advantage, becausethe interest paid on loans is generally deductible. Borrowing also limits the business's future

obligation of repayment of the loan, because the lender does not receive an ownership share inthe business.

However, debt financing also has its disadvantages. New businesses sometimes find it difficult tomake regular loan payments when they have irregular cash flow. In this way, debt financing canleave businesses vulnerable to economic downturns or interest rate hikes. Carrying too muchdebt is a problem because it increases the perceived risk associated with businesses, makingthem unattractive to investors and thus reducing their ability to raise additional capital in thefuture.

EQUITY FINANCING

Equity financing takes the form of money obtained from investors in exchange for an ownershipshare in the business. Such funds may come from friends and family members of the businessowner, wealthy "angel" investors, or venture capital firms. The main advantage to equityfinancing is that the business is not obligated to repay the money. Instead, the investors hope toreclaim their investment out of future profits. The involvement of high-profile investors may alsohelp increase the credibility of a new business.

The main disadvantage to equity financing is that the investors become part-owners of the business, and thus gain a say in business decisions. "Equity investors are looking for a partner aswell as an investment, or else they would be lenders," venture capitalist Bill Richardsonexplained in Pacific Business News (Jefferson, 2001). As ownership interests become diluted,managers face a possible loss of autonomy or control. In addition, an excessive reliance onequity financing may indicate that a business is not using its capital in the most productivemanner.

Both debt and equity financing are important ways for businesses to obtain capital to fund their operations. Deciding which to use or emphasize, depends on the long-term goals of the business

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 3/68

and the amount of control managers wish to maintain. Ideally, experts suggest that businessesuse both debt and equity financing in a commercially acceptable ratio. This ratio, known as thedebt-to-equity ratio, is a key factor analysts use to determine whether managers are running a business in a sensible manner. Although debt-to-equity ratios vary greatly by industry andcompany, a general rule of thumb holds that a reasonable ratio should fall between 1:1 and 1:2.

Some experts recommend that companies rely more heavily on equity financing during the earlystages of their existence, because such businesses may find it difficult to service debt until theyachieve reliable cash flow. But start-up companies may have trouble attracting venture capitaluntil they demonstrate strong profit potential. In any case, all businesses require sufficient capitalin order to succeed. The most prudent course of action is to obtain capital from a variety of sources, using both debt and equity, and hire professional accountants and attorneys to assistwith financial decisions.

Factors influencing Capital Structure –

Meaning of Capital Structure

Capital Structure is referred to as the ratio of different kinds of securities raised by a firm aslong-term finance. The capital structure involves two decisions-

a. Type of securities to be issued are equity shares, preference shares and longterm borrowings( Debentures).

b. Relative ratio of securities can be determined by process of capital gearing.On this basis, the companies are divided into two-

i. Highly geared companies- Those companies whose proportion of

equity capitalization is small.

ii. Low geared companies- Those companies whose equity capitaldominates total capitalization.

For instance - There are two companies A and B. Total capitalization amounts to be Rs.20 lakh in each case. The ratio of equity capital to total capitalization in company A isRs. 5 lakh, while in company B, ratio of equity capital is Rs. 15 lakh to totalcapitalization, i.e, in Company A, proportion is 25% and in company B, proportion is75%. In such cases, company A is considered to be a highly geared company andcompany B is low geared company.

Factors Determining Capital Structure

1. Trading on Equity- The word “equity” denotes the ownership of thecompany. Trading on equity means taking advantage of equity share capitalto borrowed funds on reasonable basis. It refers to additional profits thatequity shareholders earn because of issuance of debentures and preferenceshares. It is based on the thought that if the rate of dividend on preferencecapital and the rate of interest on borrowed capital is lower than the general

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 4/68

rate of company’s earnings, equity shareholders are at advantage whichmeans a company should go for a judicious blend of preference shares,equity shares as well as debentures. Trading on equity becomes moreimportant when expectations of shareholders are high.

2. Degree of control- In a company, it is the directors who are so calledelected representatives of equity shareholders. These members have got

maximum voting rights in a concern as compared to the preferenceshareholders and debenture holders. Preference shareholders havereasonably less voting rights while debenture holders have no voting rights. If the company’s management policies are such that they want to retain theirvoting rights in their hands, the capital structure consists of debentureholders and loans rather than equity shares.

3. Flexibility of financial plan- In an enterprise, the capital structure shouldbe such that there is both contractions as well as relaxation in plans.Debentures and loans can be refunded back as the time requires. Whileequity capital cannot be refunded at any point which provides rigidity toplans. Therefore, in order to make the capital structure possible, the

company should go for issue of debentures and other loans.

4. Choice of investors- The company’s policy generally is to have differentcategories of investors for securities. Therefore, a capital structure shouldgive enough choice to all kind of investors to invest. Bold and adventurousinvestors generally go for equity shares and loans and debentures aregenerally raised keeping into mind conscious investors.

5. Capital market condition- In the lifetime of the company, the market priceof the shares has got an important influence. During the depression period,the company’s capital structure generally consists of debentures and loans.While in period of boons and inflation, the company’s capital should consist of

share capital generally equity shares.

6. Period of financing- When company wants to raise finance for short period,it goes for loans from banks and other institutions; while for long period itgoes for issue of shares and debentures.

7. Cost of financing- In a capital structure, the company has to look to thefactor of cost when securities are raised. It is seen that debentures at thetime of profit earning of company prove to be a cheaper source of finance ascompared to equity shares where equity shareholders demand an extra sharein profits.

8. Stability of sales- An established business which has a growing market and

high sales turnover, the company is in position to meet fixed commitments.Interest on debentures has to be paid regardless of profit. Therefore, whensales are high, thereby the profits are high and company is in better positionto meet such fixed commitments like interest on debentures and dividendson preference shares. If company is having unstable sales, then the companyis not in position to meet fixed obligations. So, equity capital proves to besafe in such cases.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 5/68

9. Sizes of a company- Small size business firms capital structure generallyconsists of loans from banks and retained profits. While on the other hand,big companies having goodwill, stability and an established profit can easilygo for issuance of shares and debentures as well as loans and borrowingsfrom financial institutions. The bigger the size, the wider is totalcapitalization.

Importance of Capital Structure – Capital Structure Planning :

Capital structure planning is very important to survive the business in long run. After simple

watching the balance sheet of company, you see two sides of balance sheet. One side is liability

side and other side is asset side. Liability side is the mixture of finance of company which

company has collected from internal and external sources and it has been used or will be used for development of company.

Liability side of balance sheet is made under perfect capital structure planning. Finance

manager and other promoters decides which source of fund or funds should be selected after

monitoring the factors affecting capital structures. So, capital structure planning makes

strong balance sheet. The right capital structure planning also increases the power of company to

face the losses and changes in financial markets. Following points shows the importance of

capital structure and its planning.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 6/68

1. To reduce the overall risk of company

When we make capital structure before actual getting money from money supplier, we can do

many adjustments for reducing our overall risk. Suppose, we have made capital structure inwhich we add three sources of fund, one is equity share, and other is debenture and last is pref.shares. Because we know that we have to pay debt at its maturity at any cost and its interest atfixed rate. So, we try to get minimum debt in new business because in new business our rate of return will be less than rate of interest and for getting more loan means taking high risk of returnmore amount of interest even there is no profit.

But, if our business will be succeeded, at that time, we can increase estimated amount of debt by just changing the value of debt in capital structure (written just for planning) in excel sheet. Wecan easily pay the interest because our ROI is very high. At that, time company can enjoy thetrading on equity. But finance manager should also careful watch whether shareholders are

more expected regarding dividend or not. Because high expectation will also against thedevelopment of our company.

2. To do adjustment according to Business Environment

Company also adjusts different sources expected amount according to business environment.Suppose in future, if government of India cuts off his relation with China, from where our company is getting fund, it will definitely tough for us to get more money from China. But proper planning of capital structure of future sources will be helpful for us to enlarge our area for getting money. In finance, it is called maneuverability. It means to create mobility of sources of fund by including maximum alternatives in planned capital structure. Suppose, if RBI increasesthe interest rate, it means your cost for getting debt will be high, at that time, you can choose anyother cheap source of fund.

3. Idea generation of new source of fund

Good planning of capital structure will make versatile to finance manager for getting moneyfrom new sources. If you have studied Wikipedia’s page of venture capital or private equity sources, you would precisely understand that how finance managers of company are generatingnew and new idea for getting money from public at low risk . Promoters or managers do 10minutes meeting with investors and motivate them by showing the special event which they havemade in PPT

Theories of Capital Structure – 1st Theory of Capital Structure

Name of Theory = Net Income Theory of Capital Structure

This theory gives the idea for increasing market value of firm and decreasing overallcost of capital. A firm can choose a degree of capital structure in which debt is morethan equity share capital. It will be helpful to increase the market value of firm and

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 7/68

decrease the value of overall cost of capital. Debt is cheap source of financebecause its interest is deductible from net profit before taxes. After deduction of interest company has to pay less tax and thus, it will decrease the weightedaverage cost of capital.

For example if you have equity debt mix is 50:50 but if you increase it as 20: 80, it

will increase the market value of firm and its positive effect on the value of pershare.

High debt content mixture of equity debt mix ratio is also called financial leverage.Increasing of financial leverage will be helpful to for maximize the firm's value.

2nd Theory of Capital Structure

Name of Theory = Net Operating income Theory of Capital Structure

Net operating income theory or approach does not accept the idea of increasing the

financial leverage under NI approach. It means to change the capital structure doesnot affect overall cost of capital and market value of firm. At each and every level of capital structure, market value of firm will be same.

3rd Theory of Capital Structure

Name of Theory = Traditional Theory of Capital Structure

This theory or approach of capital structure is mix of net income approach and netoperating income approach of capital structure. It has three stages which youshould understand:

Ist Stage

In the first stage which is also initial stage, company should increase debt contentsin its equity debt mix for increasing the market value of firm.

2nd Stage

In second stage, after increasing debt in equity debt mix, company gets the positionof optimum capital structure, where weighted cost of capital is minimum andmarket value of firm is maximum. So, no need to further increase in debt in capitalstructure.

3rd Stage

Company can gets loss in its market value because increasing the amount of debt incapital structure after its optimum level will definitely increase the cost of debt andoverall cost of capital.

4th Theory of Capital Structure

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 8/68

Name of theory = Modigliani and Miller

MM theory or approach is fully opposite of traditional approach. This approach saysthat there is not any relationship between capital structure and cost of capital.

There will not effect of increasing debt on cost of capital.

Value of firm and cost of capital is fully affected from investor's expectations.Investors' expectations may be further affected by large numbers of other factorswhich have been ignored by traditional theorem of capital structure.

Role of EBIT-

Definition of 'Earnings Before Interest & Tax - EBIT'

An indicator of a company's profitability, calculated as revenue minus expenses,

excluding tax and interest. EBIT is also referred to as "operating earnings","operating profit" and "operating income", as you can re-arrange the formula to be

calculated as follows:

EBIT

=

Revenue - Operating

Expenses

Also known as Profit Before Interest & Taxes (PBIT), and equals Net Income with

interest and taxes added back to it.

Investopedia explains 'Earnings Before Interest & Tax -EBIT'

In other words, EBIT is all profits before taking into account interest payments andincome taxes. An important factor contributing to the widespread use of EBIT is theway in which it nulls the effects of the different capital structures and tax rates usedby different companies. By excluding both taxes and interest expenses, the figurehones in on the company's ability to profit and thus makes for easier cross-companycomparisons.

EBIT was the precursor to the EBITDA calculation, which takes the process furtherby removing two non-cash items from the equation (depreciation and amortization).

EPS Analysis –

Definition of 'Earnings Per Share - EPS'

The portion of a company's profit allocated to each outstanding share of common stock. Earnings per share serves as an indicator of a company's profitability.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 9/68

Calculated as:

When calculating, it is more accurate to use a weighted average number of shares

outstanding over the reporting term, because the number of shares outstanding can

change over time. However, data sources sometimes simplify the calculation by

using the number of shares outstanding at the end of the period.

Diluted EPS expands on basic EPS by including the shares of convertibles or

warrants outstanding in the outstanding shares number.

Investopedia explains 'Earnings Per Share - EPS'Earnings per share is generally considered to be the single most important variable

in determining a share's price. It is also a major component used to calculate the

price-to-earnings valuation ratio.

For example, assume that a company has a net income of $25 million. If the

company pays out $1 million in preferred dividends and has 10 million shares

for half of the year and 15 million shares for the other half, the EPS would be $1.92

(24/12.5). First, the $1 million is deducted from the net income to get $24 million,

then a weighted average is taken to find the number of shares outstanding (0.5 x

10M+ 0.5 x 15M = 12.5M).

An important aspect of EPS that's often ignored is the capital that is required to

generate the earnings (net income) in the calculation. Two companies could

generate the same EPS number, but one could do so with less equity (investment) -

that company would be more efficient at using its capital to generate income and,

all other things being equal, would be a "better" company. Investors also need to be

aware of earnings manipulation that will affect the quality of the earnings number.

It is important not to rely on any one financial measure, but to use it in conjunction

with statement analysis and other measures.

Cost of Capital –

Capital is the term used by firms for funds needed for investment

purposes, i.e., capital equipment

(not for day to day operating needs)

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 10/68

This capital carries a cost because each source of capital funding costs

money to raise (i.e., issuing stock costs a lot of money)

Definition of 'Cost Of Capital'

The required return necessary to make a capital budgeting project, such as buildinga new factory, worthwhile. Cost of capital includes the cost of debt and the cost of

equity.

The cost of capital determines how a company can raise money (through a stock

issue, borrowing, or a mix of the two). This is the rate of return that a firm would

receive if it invested in a different vehicle with similar risk.

Sources of Capital

Borrowing: issue Bonds, bank loans,

Issuing Preferred stock

Issuing Common stock

Net Income (earnings)

Each of these sources carries a different cost based on the required rate of

return of each provider (source) of these funds

Computation of Cost of Capital for each source of Finance -

Learning Goals

Determining the value of K, the required rate of return for an investor

Sources of capital funding (Debt, Equity)

Cost of each type of funding

Calculation of the weighted average cost of capital funding (WACC) = K

Construction and use of the marginal cost of capital schedule (MCC) fordecision making

Weighted Average cost of capital.

Definition of 'Weighted Average Cost Of Capital - WACC'

A calculation of a firm's cost of capital in which each category of capital is

proportionately weighted. All capital sources - common stock, preferred stock,

bonds and any other long-term debt - are included in a WACC calculation. All else

equal, the WACC of a firm increases as the beta and rate of return on equity

increases, as an increase in WACC notes a decrease in valuation and a higher risk.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 11/68

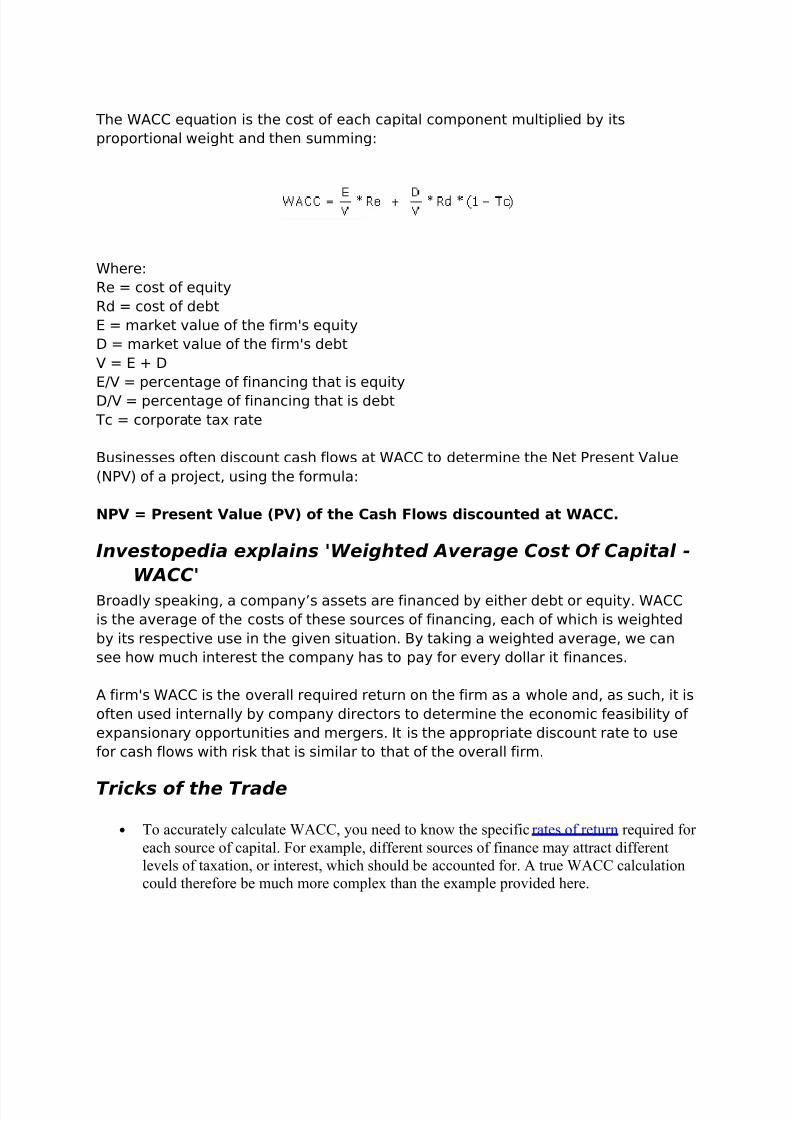

The WACC equation is the cost of each capital component multiplied by its

proportional weight and then summing:

Where:

Re = cost of equity

Rd = cost of debt

E = market value of the firm's equity

D = market value of the firm's debt

V = E + D

E/V = percentage of financing that is equity

D/V = percentage of financing that is debt

Tc = corporate tax rate

Businesses often discount cash flows at WACC to determine the Net Present Value

(NPV) of a project, using the formula:

NPV = Present Value (PV) of the Cash Flows discounted at WACC.

Investopedia explains 'Weighted Average Cost Of Capital -

WACC'

Broadly speaking, a company’s assets are financed by either debt or equity. WACC

is the average of the costs of these sources of financing, each of which is weighted

by its respective use in the given situation. By taking a weighted average, we can

see how much interest the company has to pay for every dollar it finances.

A firm's WACC is the overall required return on the firm as a whole and, as such, it is

often used internally by company directors to determine the economic feasibility of

expansionary opportunities and mergers. It is the appropriate discount rate to use

for cash flows with risk that is similar to that of the overall firm.

Tricks of the Trade

• To accurately calculate WACC, you need to know the specific rates of return required for

each source of capital. For example, different sources of finance may attract differentlevels of taxation, or interest, which should be accounted for. A true WACC calculationcould therefore be much more complex than the example provided here.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 12/68

• Critics of WACC argue that financial analysts rely on it too heavily, and that the

algorithm should not be used to assess risky projects, where the cost of capital willnecessarily be higher to reflect the higher risk.

• Investors use WACC to help decide whether a company represents a good investment

opportunity. To some extent, WACC represents the rate at which a company producesvalue for investors—if a company produces a return of 20% and has a WACC of 11%,then the company creates 9% additional value for investors. If the return is lower than theWACC, the business is unlikely to secure investment.

• Although the WACC formula seems simple, different analysts will often come up with

different WACC calculations for the same company depending on how they interpret thecompany’s debt, market value, and interest rates.

Unit - 2

Valuation of Bonds and Shares :

Basic Valuation Model –

Valuation of Bonds -

Valuation of Equity Shares: Parameters in the Dividend Discount Model -

Dividend

Growth Model and the NPVGO Model - P/E Ratio Approach – Book Value

Approach.

Unit - 3

Components of Working Capital Working Capital –

What is working capital?

Working capital is the money needed to fund the normal, day to day operations of your business. It ensures you have enough cash to pay your debts and expenses asthey fall due, particularly during your start-up period.Very few new businesses are profitable as soon as they open their doors. It takes

time to reach your breakeven point and start making a profit. The working capital cycle

The working capital cycle measures the time between paying for goods supplied toyou and the final receipt of cash to you from their sale. It is desirable to keep thecycle as short as possible as it increases the effectiveness of working capital.The working capital cycle is made up of four core components:

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 13/68

Cash (funds available)Creditors (accounts payable)Inventory (stock on hand)Debtors (accounts payable)

Diagram of the working capital cycle The key to successful cash management is to be in control of each step in thecycle. If you can quickly convert your trading operations into available cash, youwill be increasing the liquidity in your business and will be less reliant on cashfrom customers, extended terms from suppliers, overdrafts, and loans. What's the right level of working capital?

The right level of working capital depends on the industry and the particular circumstances of the business.For example: Businesses that only sell services, and do not need to pay cash for inventory need a lower level of working capital. Businesses that take asubstantial amount of time to make of sell a product will need a higher level of working capital.It is important you work out the right level of working capital you will need. If theworking capital is too:

high - your business has surplus funds which are not earning a return; andlow - may indicate that your business is facing financial difficulties.

The formula used to calculate working capital for your business is:(NOTE: You will need figures from your most recent balance sheet)

working capital ($ value) = current assets - current liabilities

This calculation will not give you a sense of whether your working capital safety

margin is wide enough. The working capital ratio (current ratio/liquidity ratio) willgive you a better measure of liquidity. Working capital as a percentage of salesMost business owners have a clear idea of their weekly, monthly, or quarterlysales levels, so you may prefer to calculate how much working capital you need asa percentage of sales.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 14/68

The formula used to calculate an estimate of working capital as a percentage of sales for your business is: (NOTE: You will need figures from your most recent

balance sheet and profit and loss statement)

Working capital = (Inventory + accounts receivable - accounts payable)as a % of sales Sales x 100

and:

Working capital ($ value) = sales x (working capital as a % of sales)

For example: Working capital as a percentage of sales of 35% means that you need$35 for every $100 of sales to fund the sale to allow for the time delay in theworking capital cycle.

This method is useful for businesses going through a period of growth andexpansion to work out how much extra working capital you need if turnover increased by a certain amount.

Policies Liquidity –

Profitability

Linkages –

Factors determining Working Capital –

FACTORS DETERMINING WORKING CAPITAL

REQUIREMENT

The working capital needs of a firm are determined and influenced by variousfactors. A wide variety of considerations may affect the quantum of working capitalrequired and these considerations may vary from time to time. The working capitalneeded at one point of time may not be good enough for some other situation. Thedetermination of working capital requirement is a continuous process and must beundertaken on a regular basis in the light of the changing situations. Following aresome of the factors which are relevant in determining the working capital needs of

the firm:

1. Basic Nature of Business: The working capital requirement is closely relatedto the nature of the business of the firm. In case of a retail shop or a trading firm,the amount of working capital required is small enough. Most of the transactionsare undertaken in cash and the length of the operating cycle is generally small. Thetrading concerns usually have smaller needs of working capital, however, in certaincases, large inventories of goods may be required and consequently the working

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 15/68

capital may be large. In case of financial concerns (engaged in financial business)there may not be stock of goods but these firms do have to maintain sufficientliquidity all the times.

In case of manufacturing concerns, different types of production processes areperformed. One unit of raw material introduced in the production schedule may

take a long period before it is available as finished goods for sale. Funds areblocked not only in raw materials but also in labor expenses and overheads at everystage of production. The operating cycle is usually a longer one and sales are madegenerally on credit terms. So, in case of manufacturing concerns, there is arequirement of substantial working capital.

2. Business Cycle Fluctuations: Different phases of business cycle i.e., boom,recession, recovery etc. also affect the working capital requirement. In case of boom conditions, inflationary pressure appears and business activities expand. As aresult, the overall need for cash, inventories etc. increases resulting in more andmore funds blocked in these current assets. In case of recession period however,there is usually a dullness in business activities and there will be an opposite effect

on the level of working capital requirement. There will be a fall in inventories andcash requirement etc.

3. Seasonal Operations: If a firm is operating in goods and services havingseasonal fluctuations in demand, then the working capital requirement will alsofluctuate with every change. In a cold drink factory, the demand will certainly behigher during summer season and therefore, more working capital is required tomaintain higher production, in the form of larger inventories and biggerreceivables. On the other hand, if the operations are smooth and even through outthe year then the working capital requirement will be constant and will not beaffected by the seasonal factors.

4. Market Competitiveness: The market competitiveness has an importantbearing on the working capital needs of a firm. In view of the competitiveconditions prevailing in the market, the firm may have to offer liberal credit termsto the customers resulting in higher debtors. Even larger inventories may bemaintained to serve an order as and when received; otherwise the customer may goto some other supplier. Thus, the working capital tends to be high as a result of greater investment in inventories and receivable. On the other hand, amonopolistic firm may not require larger working capital. It may ask the customersto pay in advance or to wait for some time after placing the order.

5. Credit Policy: The credit policy means the totality of terms and conditions onwhich goods are sold and purchased. A firm has to interact with two types of creditpolicies at a time. One, the credit policy of the supplier of raw materials, goods etc.,and two, the credit policy relating to credit which it extends to its customers. Inboth the cases, however, the firm while deciding its credit policy, has to take care of the credit policy of the market. For example, a firm might be purchasing goods andservices on credit terms but selling goods only for cash. The working capitalrequirement of this firm will be lower than that of a firm which is purchasing cashbut has to sell on credit basis.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 16/68

6. Supply Conditions: The time taken by a supplier of raw materials, goods etc.after placing an order, also determines the working capital requirement. If goodsare received as soon as or in a short period after placing an order, then thepurchaser will not like to maintain a high level of inventory of that good. Otherwise,larger inventories should be kept e.g., in case of imported goods. It is often seenthat the shopkeepers may not be keeping stock of all items, but whenever there is a

demand, they procure from the wholesaler/producer and supply it to theircustomers.

Thus, the working capital requirement of a firm is determined by a host of factors.Every consideration is to be weighted relatively to determine the working capitalrequirement. Further, the determination of working capital requirement is not oncea while exercise, rather a continuous review must be made in order to assess theworking capital requirement in the changing situation. There are various reasonswhich may require the review of the working capital requirement e.g., change incredit policy, change in sales volume etc.

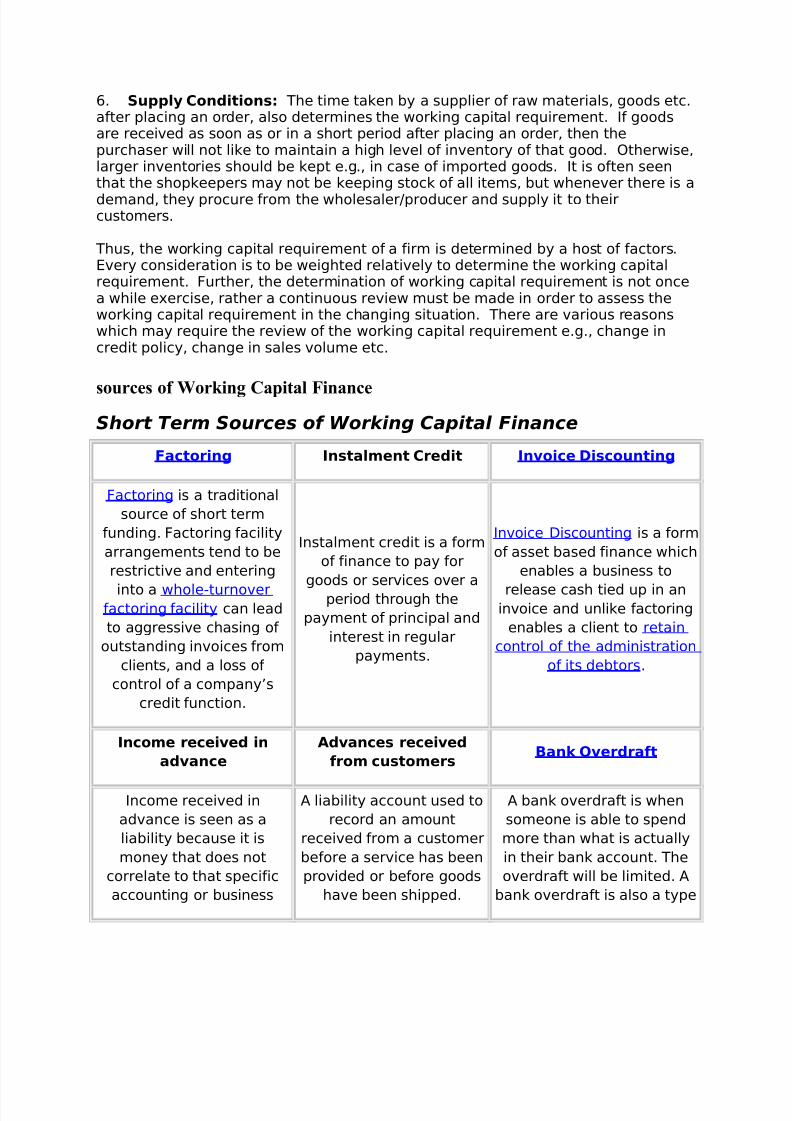

sources of Working Capital Finance

Short Term Sources of Working Capital Finance

Factoring Instalment Credit Invoice Discounting

Factoring is a traditional

source of short term

funding. Factoring facility

arrangements tend to be

restrictive and entering

into a whole-turnoverfactoring facility can lead

to aggressive chasing of

outstanding invoices from

clients, and a loss of

control of a company’s

credit function.

Instalment credit is a form

of finance to pay for

goods or services over a

period through the

payment of principal and

interest in regular

payments.

Invoice Discounting is a form

of asset based finance which

enables a business to

release cash tied up in aninvoice and unlike factoring

enables a client to retain

control of the administration

of its debtors.

Income received in

advance

Advances received

from customersBank Overdraft

Income received in

advance is seen as a

liability because it is

money that does not

correlate to that specific

accounting or business

A liability account used to

record an amount

received from a customer

before a service has been

provided or before goods

have been shipped.

A bank overdraft is when

someone is able to spend

more than what is actually

in their bank account. The

overdraft will be limited. A

bank overdraft is also a type

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 17/68

year but rather for one that

is still to come. The income

account will then be

credited to the income

received in advance

account and the income

received in advance will be

debited to the income

account such as rent.

of loan as the money is

technically borrowed.

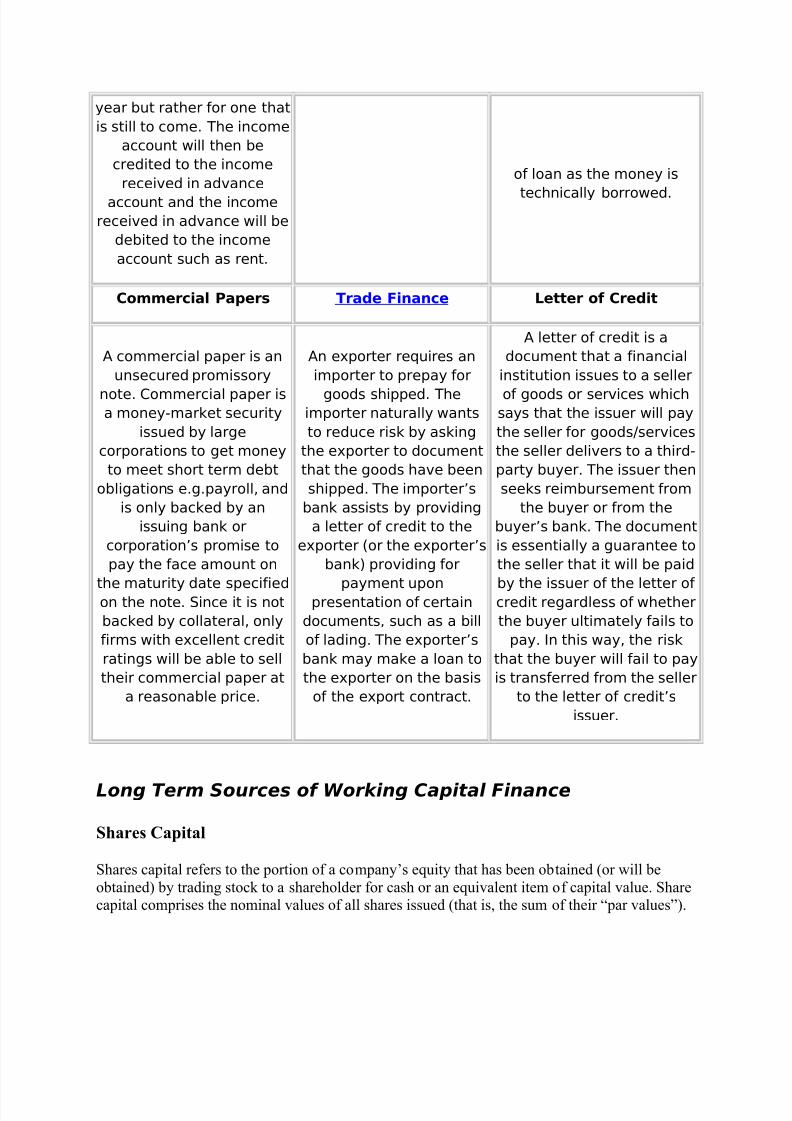

Commercial Papers Trade Finance Letter of Credit

A commercial paper is an

unsecured promissory

note. Commercial paper isa money-market security

issued by large

corporations to get money

to meet short term debt

obligations e.g.payroll, and

is only backed by an

issuing bank or

corporation’s promise to

pay the face amount on

the maturity date specifiedon the note. Since it is not

backed by collateral, only

firms with excellent credit

ratings will be able to sell

their commercial paper at

a reasonable price.

An exporter requires an

importer to prepay for

goods shipped. Theimporter naturally wants

to reduce risk by asking

the exporter to document

that the goods have been

shipped. The importer’s

bank assists by providing

a letter of credit to the

exporter (or the exporter’s

bank) providing for

payment uponpresentation of certain

documents, such as a bill

of lading. The exporter’s

bank may make a loan to

the exporter on the basis

of the export contract.

A letter of credit is a

document that a financial

institution issues to a seller

of goods or services whichsays that the issuer will pay

the seller for goods/services

the seller delivers to a third-

party buyer. The issuer then

seeks reimbursement from

the buyer or from the

buyer’s bank. The document

is essentially a guarantee to

the seller that it will be paid

by the issuer of the letter of credit regardless of whether

the buyer ultimately fails to

pay. In this way, the risk

that the buyer will fail to pay

is transferred from the seller

to the letter of credit’s

issuer.

Long Term Sources of Working Capital Finance

Shares Capital

Shares capital refers to the portion of a company’s equity that has been obtained (or will beobtained) by trading stock to a shareholder for cash or an equivalent item of capital value. Sharecapital comprises the nominal values of all shares issued (that is, the sum of their “par values”).

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 18/68

Share capital can simply be defined as the sum of capital (cash or other assets) the company hasreceived from investors for its shares.

Debenture

A debenture is a document that either creates a debt or acknowledges it, and it is a debt withoutcollateral. In corporate finance, the term is used for a medium- to long-term debt instrument used by large companies to borrow money. A debenture is like a certificate of loan evidencing the factthat the company is liable to pay a specified amount with interest and although the money raised by the debentures becomes a part of the company’s capital structure, it does not become sharecapital. Debentures are generally freely transferable by the debenture holder.

Loan from financial institution

A loan is a type of debt which it entails the redistribution of financial assets over time, betweenthe lender and the borrower. In a loan, the borrower initially receives or borrows an amount of

money from the lender, and is obligated to pay back or repay an equal amount of money to thelender at a later time. Typically, the money is paid back in regular installments, or partialrepayments; in an annuity, each installment is the same amount. Acting as a provider of loans isone of the principal tasks for financial institutions like banks. A secured loan is a loan in whichthe borrower pledges some asset (e.g. a car or property) as collateral. Unsecured loans aremonetary loans that are not secured against the borrower’s assets.

-Inventory Management –

Defining Inventory

Inventory is an idle stock of physical goods that contain economic value, and are held in variousforms by an organization in its custody awaiting packing, processing, transformation, use or salein a future point of time.

Any organization which is into production, trading, sale and service of a product will necessarilyhold stock of various physical resources to aid in future consumption and sale. While inventoryis a necessary evil of any such business, it may be noted that the organizations hold inventoriesfor various reasons, which include speculative purposes, functional purposes, physicalnecessities etc.

From the above definition the following points stand out with reference to inventory:

All organizations engaged in production or sale of products hold inventory inone form or other.

Inventory can be in complete state or incomplete state.

Inventory is held to facilitate future consumption, sale or furtherprocessing/value addition.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 19/68

All inventoried resources have economic value and can be considered asassets of the organization.

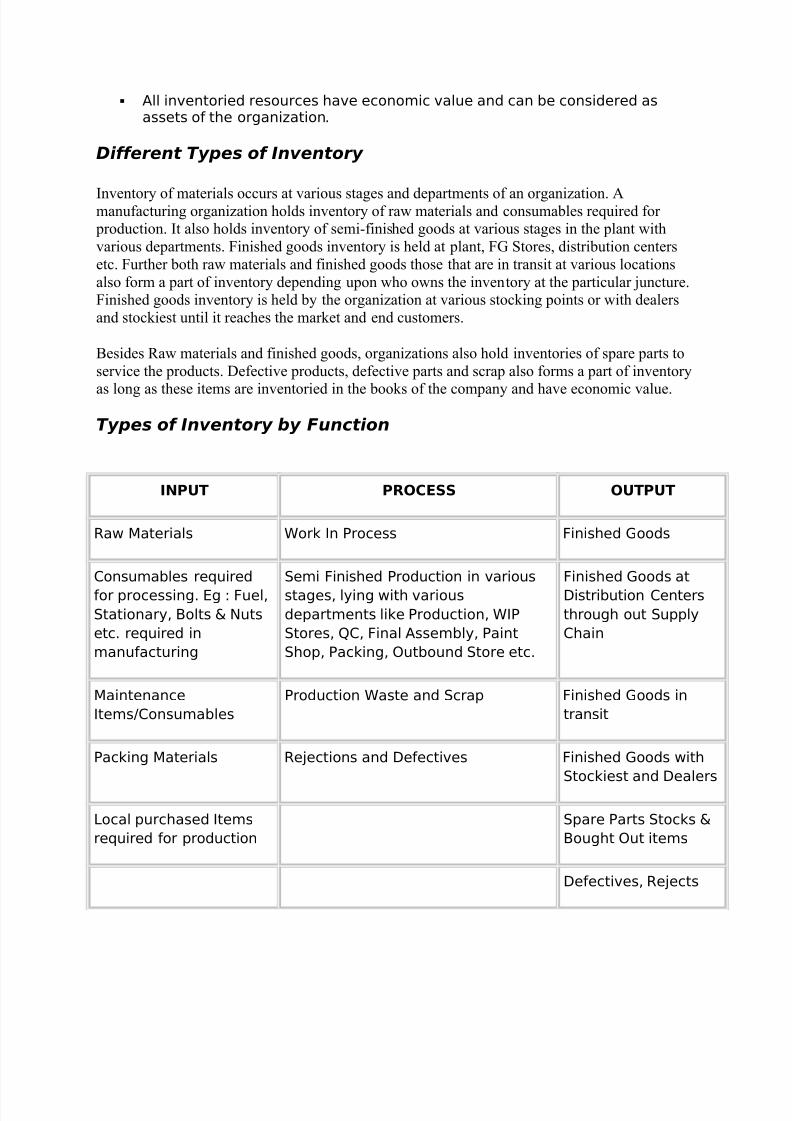

Different Types of Inventory

Inventory of materials occurs at various stages and departments of an organization. Amanufacturing organization holds inventory of raw materials and consumables required for production. It also holds inventory of semi-finished goods at various stages in the plant withvarious departments. Finished goods inventory is held at plant, FG Stores, distribution centersetc. Further both raw materials and finished goods those that are in transit at various locationsalso form a part of inventory depending upon who owns the inventory at the particular juncture.Finished goods inventory is held by the organization at various stocking points or with dealersand stockiest until it reaches the market and end customers.

Besides Raw materials and finished goods, organizations also hold inventories of spare parts toservice the products. Defective products, defective parts and scrap also forms a part of inventory

as long as these items are inventoried in the books of the company and have economic value.

Types of Inventory by Function

INPUT PROCESS OUTPUT

Raw Materials Work In Process Finished Goods

Consumables required

for processing. Eg : Fuel,

Stationary, Bolts & Nuts

etc. required in

manufacturing

Semi Finished Production in various

stages, lying with various

departments like Production, WIP

Stores, QC, Final Assembly, Paint

Shop, Packing, Outbound Store etc.

Finished Goods at

Distribution Centers

through out Supply

Chain

Maintenance

Items/Consumables

Production Waste and Scrap Finished Goods in

transit

Packing Materials Rejections and Defectives Finished Goods with

Stockiest and Dealers

Local purchased Items

required for production

Spare Parts Stocks &

Bought Out items

Defectives, Rejects

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 20/68

and Sales Returns

Repaired Stock and

Parts

Sales Promotion &

Sample Stocks

Receivables Management –

Receivables Management

Managing and collecting commercial receivables (unpaid receivables between companies or organisations) is linked to the credit insurance business and the information business.

Coface has succeeded in considerably reducing its claims expenses by setting up efficientreceivables management processes, developing excellent knowledge of local payment andcollection regulations and practices, accurately predicting the commercial and financial behaviour of buyers throughout the world and closely monitoring changes in their behaviour.

Coface RBI (Recovery Business Intelligence) provides a tailor-made service for the recovery of large trade debts in all countries. In the field of debt collection, Coface RBI responds to theneeds of credit managers and financial groups with regard to atypical or complex transactions.

Collecting debts is a full time job that requires experienced, fully trained and efficient resources.Coface allows you to take advantage of its negotiating skills and legal expertise to collect cashon your behalf, either in our name or yours, on a confidential basis.

You can benefit from our experience and recognition in this field:

- Better manage your amount of outstandings,- Maintain your trading relationship with a valued customer either on domestic or internationallevel- Be fully informed of progress,- Get liquidity and cash flow- Increase own company financial attractiveness- Save personal resources

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 21/68

Money Market Instruments.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 22/68

Money Market Instruments provide the tools by which one can

operate in the money market.

Types Of Money Market Instruments

Treasury Bills: The Treasury bills are short-term money market

instrument that mature in a year or less than that. The

purchase price is less than the face value. At maturity the

government pays the Treasury Bill holder the full face

value.The Treasury Bills are marketable, affordable and risk

free. The security attached to the treasury bills comes at the

cost of very low returns.

Certificate of Deposit: The certificates of deposit are basically

time deposits that are issued by the commercial banks with

maturity periods ranging from 3 months to five years. The

return on the certificate of deposit is higher than the Treasury

Bills because it assumes a higher level of risk.

Advantages of Certificate of Deposit as a money market

instrument 1. Since one can know the returns from before, the

certificates of deposits are considered much safe.

2. One can earn more as compared to depositing money in

savings account.

3. The Federal Insurance Corporation guarantees the

investments in the certificate of deposit.

Disadvantages of Certificate of deposit as a money market

instrument:

1. As compared to other investments the returns is less.

2. The money is tied along with the long maturity period of

the Certificate of Deposit. Huge penalties are paid if one gets

out of it before maturity.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 23/68

Commercial Paper: Commercial Paper is short-term loan that

is issued by a corporation use for financing accounts

receivable and inventories. Commercial Papers have higher

denominations as compared to the Treasury Bills and the

Certificate of Deposit. The maturity period of CommercialPapers are a maximum of 9 months. They are very safe since

the financial situation of the corporation can be anticipated

over a few months.

Banker's Acceptance: It is a short-term credit investment. It is

guaranteed by a bank to make payments. The Banker's

Acceptance is traded in the Secondary market. The banker's

acceptance is mostly used to finance exports, imports andother transactions in goods. The banker's acceptance need

not be held till the maturity date but the holder has the

option to sell it off in the secondary market whenever he finds

it suitable.

Euro Dollars: The Eurodollars are basically dollar- denominated

deposits that are held in banks outside the United States.

Since the Eurodollar market is free from any stringent regulations, the banks can operate at narrower margins as

compared to the banks in U.S. The Eurodollars are traded at

very high denominations and mature before six months. The

Eurodollar market is within the reach of large institutions only

and individual investors can access it only through money

market funds.

Repos: The Repo or the repurchase agreement is used by the

government security holder when he sells the security to a

lender and promises to repurchase from him overnight.

Hence the Repos have terms raging from 1 night to 30 days.

They are very safe due government backing.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 24/68

Unit - 4

Mergers and Acquisitions :

An entrepreneur may grow its business either by internal expansion or by external expansion. In

the case of internal expansion, a firm grows gradually over time in the normal course of the business, through acquisition of new assets, replacement of the technologically obsoleteequipments and the establishment of new lines of products. But in external expansion, a firmacquires a running business and grows overnight through corporate combinations. Thesecombinations are in the form of mergers, acquisitions, amalgamations and takeovers and havenow become important features of corporate restructuring. They have been playing an importantrole in the external growth of a number of leading companies the world over. They have become popular because of the enhanced competition, breaking of trade barriers, free flow of capitalacross countries and globalisation of businesses. In the wake of economic reforms, Indianindustries have also started restructuring their operations around their core business activitiesthrough acquisition and takeovers because of their increasing exposure to competition both

domestically and internationally.

Mergers and acquisitions are strategic decisions taken for maximisation of a company's growth by enhancing its production and marketing operations. They are being used in a wide array of fields such as information technology, telecommunications, and business process outsourcing aswell as in traditional businesses in order to gain strength, expand the customer base, cutcompetition or enter into a new market or product segment.

Mergers or Amalgamations

A merger is a combination of two or more businesses into one business. Laws in India use the

term 'amalgamation' for merger. The Income Tax Act,1961 [Section 2(1A)] definesamalgamation as the merger of one or more companies with another or the merger of two or more companies to form a new company, in such a way that all assets and liabilities of theamalgamating companies become assets and liabilities of the amalgamated company andshareholders not less than nine-tenths in value of the shares in the amalgamating company or companies become shareholders of the amalgamated company.

Thus, mergers or amalgamations may take two forms:-

Merger through Absorption:- An absorption is a combination of two or morecompanies into an 'existing company'. All companies except one lose their identity in

such a merger. For example, absorption of Tata Fertilisers Ltd (TFL) by Tata ChemicalsLtd. (TCL). TCL, an acquiring company (a buyer), survived after merger while TFL, anacquired company (a seller), ceased to exist. TFL transferred its assets, liabilities andshares to TCL.

Merger through Consolidation:- A consolidation is a combination of two or morecompanies into a 'new company'. In this form of merger, all companies are legallydissolved and a new entity is created. Here, the acquired company transfers its assets,liabilities and shares to the acquiring company for cash or exchange of shares. For

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 25/68

example, merger of Hindustan Computers Ltd, Hindustan Instruments Ltd, IndianSoftware Company Ltd and Indian Reprographics Ltd into an entirely new companycalled HCL Ltd.

A fundamental characteristic of merger (either through absorption or consolidation) is that the

acquiring company (existing or new) takes over the ownership of other companies and combinestheir operations with its own operations.

Besides, there are three major types of mergers:-

Horizontal merger:- is a combination of two or more firms in the same area of business.For example, combining of two book publishers or two luggage manufacturingcompanies to gain dominant market share.

Vertical merger:- is a combination of two or more firms involved in different stages of production or distribution of the same product. For example, joining of a TVmanufacturing(assembling) company and a TV marketing company or joining of a

spinning company and a weaving company. Vertical merger may take the form of forward or backward merger. When a company combines with the supplier of material, itis called backward merger and when it combines with the customer, it is known asforward merger.

Conglomerate merger:- is a combination of firms engaged in unrelated lines of businessactivity. For example, merging of different businesses like manufacturing of cement products, fertilizer products, electronic products, insurance investment and advertisingagencies. L&T and Voltas Ltd are examples of such mergers.

Acquisitions and Takeovers

An acquisition may be defined as an act of acquiring effective control by one company over assets or management of another company without any combination of companies. Thus, in anacquisition two or more companies may remain independent, separate legal entities, but theremay be a change in control of the companies. When an acquisition is 'forced' or 'unwilling', it iscalled a takeover. In an unwilling acquisition, the management of 'target' company would opposea move of being taken over. But, when managements of acquiring and target companies mutuallyand willingly agree for the takeover, it is called acquisition or friendly takeover.

Under the Monopolies and Restrictive Practices Act, takeover meant acquisition of not less than25 percent of the voting power in a company. While in the Companies Act (Section 372), acompany's investment in the shares of another company in excess of 10 percent of the subscribed

capital can result in takeovers. An acquisition or takeover does not necessarily entail full legalcontrol. A company can also have effective control over another company by holding a minorityownership.

Advantages of Mergers & Acquisitions

The most common motives and advantages of mergers and acquisitions are:-

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 26/68

Accelerating a company's growth, particularly when its internal growth is constrained dueto paucity of resources. Internal growth requires that a company should develop itsoperating facilities- manufacturing, research, marketing, etc. But, lack or inadequacy of resources and time needed for internal development may constrain a company's pace of growth. Hence, a company can acquire production facilities as well as other resources

from outside through mergers and acquisitions. Specially, for entering in new products/markets, the company may lack technical skills and may require specialmarketing skills and a wide distribution network to access different segments of markets.The company can acquire existing company or companies with requisite infrastructureand skills and grow quickly.

Enhancing profitability because a combination of two or more companies may result inmore than average profitability due to cost reduction and efficient utilization of resources.This may happen because of:-

• Economies of scale:- arise when increase in the volume of production leads to a

reduction in the cost of production per unit. This is because, with merger, fixedcosts are distributed over a large volume of production causing the unit cost of production to decline. Economies of scale may also arise from other indivisibilities such as production facilities, management functions andmanagement resources and systems. This is because a given function, facility or resource is utilized for a large scale of operations by the combined firm.

• Operating economies:- arise because, a combination of two or more firms may

result in cost reduction due to operating economies. In other words, a combinedfirm may avoid or reduce over-lapping functions and consolidate its managementfunctions such as manufacturing, marketing, R&D and thus reduce operatingcosts. For example, a combined firm may eliminate duplicate channels of distribution, or crate a centralized training center, or introduce an integrated planning and control system.

• Synergy:- implies a situation where the combined firm is more valuable than the

sum of the individual combining firms. It refers to benefits other than thoserelated to economies of scale. Operating economies are one form of synergy benefits. But apart from operating economies, synergy may also arise fromenhanced managerial capabilities, creativity, innovativeness, R&D and marketcoverage capacity due to the complementarity of resources and skills and awidened horizon of opportunities.

Diversifying the risks of the company, particularly when it acquires those businesseswhose income streams are not correlated. Diversification implies growth through thecombination of firms in unrelated businesses. It results in reduction of total risks throughsubstantial reduction of cyclicality of operations. The combination of management andother systems strengthen the capacity of the combined firm to withstand the severity of the unforeseen economic factors which could otherwise endanger the survival of theindividual companies.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 27/68

A merger may result in financial synergy and benefits for the firm in many ways:-

• By eliminating financial constraints

•

By enhancing debt capacity. This is because a merger of two companies can bringstability of cash flows which in turn reduces the risk of insolvency and enhancesthe capacity of the new entity to service a larger amount of debt

• By lowering the financial costs. This is because due to financial stability, the

merged firm is able to borrow at a lower rate of interest.

Limiting the severity of competition by increasing the company's market power. Amerger can increase the market share of the merged firm. This improves the profitabilityof the firm due to economies of scale. The bargaining power of the firm vis-à-vis labour,suppliers and buyers is also enhanced. The merged firm can exploit technological

breakthroughs against obsolescence and price wars.

Procedure for evaluating the decision for mergers and acquisitions

The three important steps involved in the analysis of mergers and acquisitions are:-

Planning:- of acquisition will require the analysis of industry-specific and firm-specificinformation. The acquiring firm should review its objective of acquisition in the contextof its strengths and weaknesses and corporate goals. It will need industry data on marketgrowth, nature of competition, ease of entry, capital and labour intensity, degree of regulation, etc. This will help in indicating the product-market strategies that are

appropriate for the company. It will also help the firm in identifying the business unitsthat should be dropped or added. On the other hand, the target firm will need informationabout quality of management, market share and size, capital structure, profitability, production and marketing capabilities, etc.

Search and Screening:- Search focuses on how and where to look for suitablecandidates for acquisition. Screening process short-lists a few candidates from manyavailable and obtains detailed information about each of them.

Financial Evaluation:- of a merger is needed to determine the earnings and cash flows,areas of risk, the maximum price payable to the target company and the best way tofinance the merger. In a competitive market situation, the current market value is the

correct and fair value of the share of the target firm. The target firm will not accept anyoffer below the current market value of its share. The target firm may, in fact, expect theoffer price to be more than the current market value of its share since it may expect thatmerger benefits will accrue to the acquiring firm.

A merger is said to be at a premium when the offer price is higher than the target firm's pre-merger market value. The acquiring firm may have to pay premium as an incentive to

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 28/68

target firm's shareholders to induce them to sell their shares so that it (acquiring firm) isable to obtain the control of the target firm.

Regulations for Mergers & Acquisitions

Mergers and acquisitions are regulated under various laws in India. The objective of the laws isto make these deals transparent and protect the interest of all shareholders. They are regulatedthrough the provisions of :-

The Companies Act, 1956

The Act lays down the legal procedures for mergers or acquisitions :-

• Permission for merger:- Two or more companies can amalgamate only when the

amalgamation is permitted under their memorandum of association. Also, theacquiring company should have the permission in its object clause to carry on the

business of the acquired company. In the absence of these provisions in thememorandum of association, it is necessary to seek the permission of theshareholders, board of directors and the Company Law Board before affecting themerger.

• Information to the stock exchange:- The acquiring and the acquired companies

should inform the stock exchanges (where they are listed) about the merger.

• Approval of board of directors:- The board of directors of the individual

companies should approve the draft proposal for amalgamation and authorise themanagements of the companies to further pursue the proposal.

• Application in the High Court:- An application for approving the draft

amalgamation proposal duly approved by the board of directors of the individualcompanies should be made to the High Court.

• Shareholders' and creators' meetings:- The individual companies should hold

separate meetings of their shareholders and creditors for approving theamalgamation scheme. At least, 75 percent of shareholders and creditors inseparate meeting, voting in person or by proxy, must accord their approval to thescheme.

• Sanction by the High Court:- After the approval of the shareholders andcreditors, on the petitions of the companies, the High Court will pass an order,

sanctioning the amalgamation scheme after it is satisfied that the scheme is fair and reasonable. The date of the court's hearing will be published in twonewspapers, and also, the regional director of the Company Law Board will beintimated.

• Filing of the Court order:- After the Court order, its certified true copies will be

filed with the Registrar of Companies.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 29/68

• Transfer of assets and liabilities:- The assets and liabilities of the acquired

company will be transferred to the acquiring company in accordance with theapproved scheme, with effect from the specified date.

• Payment by cash or securities:- As per the proposal, the acquiring company will

exchange shares and debentures and/or cash for the shares and debentures of theacquired company. These securities will be listed on the stock exchange.

NPV of a Merger –

osts and Benefits of Merger

When a company ‘A’ acquires another company say ‘B’, then it is a capital investment decisionfor company ‘A’ and it is a capital disinvestment decision for company ‘B”. Thus, both the

companies need to calculate the Net Present Value (NPV) of their decisions.

To calculate the NPV to company ‘A’ there is a need to calculate the benefit and cost of themerger. The benefit of the merger is equal to the difference between the value of the combinedidentity (PV AB) and the sum of the value of both firms as a separate entity. It can be expressed asBenefit = (PV AB) – (PV A+ PVB)

Assuming that compensation to firm B is paid in cash, the cost of the merger from the point of view of firm A can be calculated as

Cost= Cash - PVB

Thus NPV for A = Benefit –Cost= (PV AB – (PV A + PVB)) – (Cash – PVB)

the net present value of the merger from the point of view of firm B is the same as the cost of themerger for ‘A’. Hence, NPV to B = (Cash - PVB)

NPV of A and B in case the compensation is in stock

In the above scenario we assumed that compensation is paid in cash, however in real life

compensation is paid in terms of stock. In that case, cost of the merger needs to be calculatedcaarefully. It is explained with the help of an illustration – Firm A plans to acquire firm B. Following are the statistics of firms before the merger –

A B

Market price per share Rs.50 Rs.20

Number of Shares 500,000 250,000

Market value of the firm Rs.25 Rs.5

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 30/68

million million

The merger is expected to bring gains, which have a PV of Rs.5 million. Firm A offers 125,000shares in exchange for 250,000 shares to the shareholders of firm B.

The cost in this case is defined as –

Cost = αPV AB - PVB

Where a represents the fraction of the combined entity received by shareholders of B.In the above example, the share of B in the combined entity is – α = 125,000 / (500,000 + 125,000) = 0.2

assuming that the market value of the combined entity will be equal to the sum of present valueof the separate entities and the benefit of merger. Then,

PV AB = PV A+ PVB+ Benefit = 25 + 5 + 5 = Rs.35 million

Cost = αPV AB - PVB = 0.2 x 35 – 5= Rs.2 million

thus

NPV to A =Benefit – Cost= 5 –2 = Rs.3 million NPV to B = Cost to A = Rs 2 million

Defensive Strategies to prevent take over attempts –

Other Takeover DefensesPoison pill

is someti mes used more broadly to descr ibe othe r types of ta keove r defenses that involve thetarget taking some action. Although the broad category of ta k e o v e r de fe n s e s (mo re c o mmo n l ykno wn as "s ha rk re pel len ts" ) i nc lud es the t radit ional shareholder r ights plan poisonpill. Other anti-takeover protectionsinclude:•Classified boards with staggered terms.

•Limitations on the ability to call special meetings or ta ke action by written consent.•Supermajority vote requirements to approve mergers.•Supermajority vote requirements to remove directors.•T h e t a r g e t a d d s t o i t s c h a r t e r a p r o v i s i o n w h i c h g i v e s t h ec u r r e n t shareholders the right to sell their shares to the acquirer at an increased price(usuall y100% above rece nt average share price ), if the acquire r's share of the company reaches a

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 31/68

critical limit (usually one third). This kind of poison p i l l ca n no t s t o p a d e te r m i n e d a c qu i r e r ,but ensu res a h igh pr i c e for the company.•The target takes on largedebtsin an effort to make the debt load too high to be attractive—the acquirer would eventually have to pay the debts.•T h e c o m p a n y b u y s a n u m b e r o f s m a l l e r c o m p a n i e s u s i n g a stock swap,diluting thevalue of the target's stock.•The target grants its employeesstock optionsthat immediately vest if thecompany is takenover. This is intended to give emp loyees an incent ive to continue working for the target companyat least until a merger is completedins te ad of lo ok in g fo r a ne w jo b as so on as ta ke ov er d i s c u s s i o n s b e g i nH o w e v e r , w i t h t h e r e l e a s e o f t h e " golden handcuffs", many discontentedemployees mayquit immediately after they've cashed in their stock options.This poison pill may create an exodus of talented employees. In many high-tech businesses, attrition of talentedhuman resourcesoften means anemptyshell is left behind for the new owner.•Peoplesoftguaranteed its customers in June 2003 that if it were acquiredwithin two years,presumably by its rivalOracle Corporation, and productsuppo r t we re r edu ced w i th in f our

y e ar s , i t s c u st o me r s w o ul d r e ce i ve a r e f u n d o f b e t w e e n t w o a n d f i v e t i m e st h e f e e s t h e y h a d p a i d f o r t h e i r Peoplesoft software licenses. The hypothetical cost toOracle was valued atas mu ch as US$1.5 billion. Peoplesoft a llowed the guarantee to expirei nApr i l 2004 . I f Peo p l eSo f t had no t p repared i t se l f by a dop t i ng e f f ec t i ve takeover defenses, it is unclear if Oracle would have significantly raised itsoriginal bid of $16 per share. Theincreased bid provided an additional $4.1 billion for PeopleSoft's shareholders.•The practice of having staggered elections for the board of directors. Fo r example, if acompany had nine directors, then three directors would be upfo r r e -e l e c t i o n ea c h ye a r , w i t h ath ree -ye ar ter m. Thi s wou ld pre se nt a potent ia l acqui rer with the posi tion of having ahostile board for at least ayear a fter the first election. In some companies, ce rtainpercentages of the board (33%) may be enough to block key decisions (such as a fullmerger agreement or major asset sale), so an acquirer may not be able to close

an acquisition for years after having purchased a majority of the target's stock.As of December 31, 2008,47.05% of the companies in the S&P Super 1500had a classified boardRecent DevelopmentsShareholder Input on Poison PillsMor e co mp a ni es ar e gi vi ng sh ar e ho ld er s a sa y onp oi so n p i l ls . A cc or di ng t o F a c t S e t S h a r k R e p e l l e n t d a t a , s o f a r t h i s y e a r 2 1 c o m p a n i e s t h a t a d o p t e d o r extended a poison pill have publicly disclosed they plan toput the poison pill to ashareholder vote within a year. That's already more than 2008's full year total of 18and in fact is the most in any year since the first poison pill was adopted in the early1980s.

Leveraged Buy outs Spin-offs and Restructurings –

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 32/68

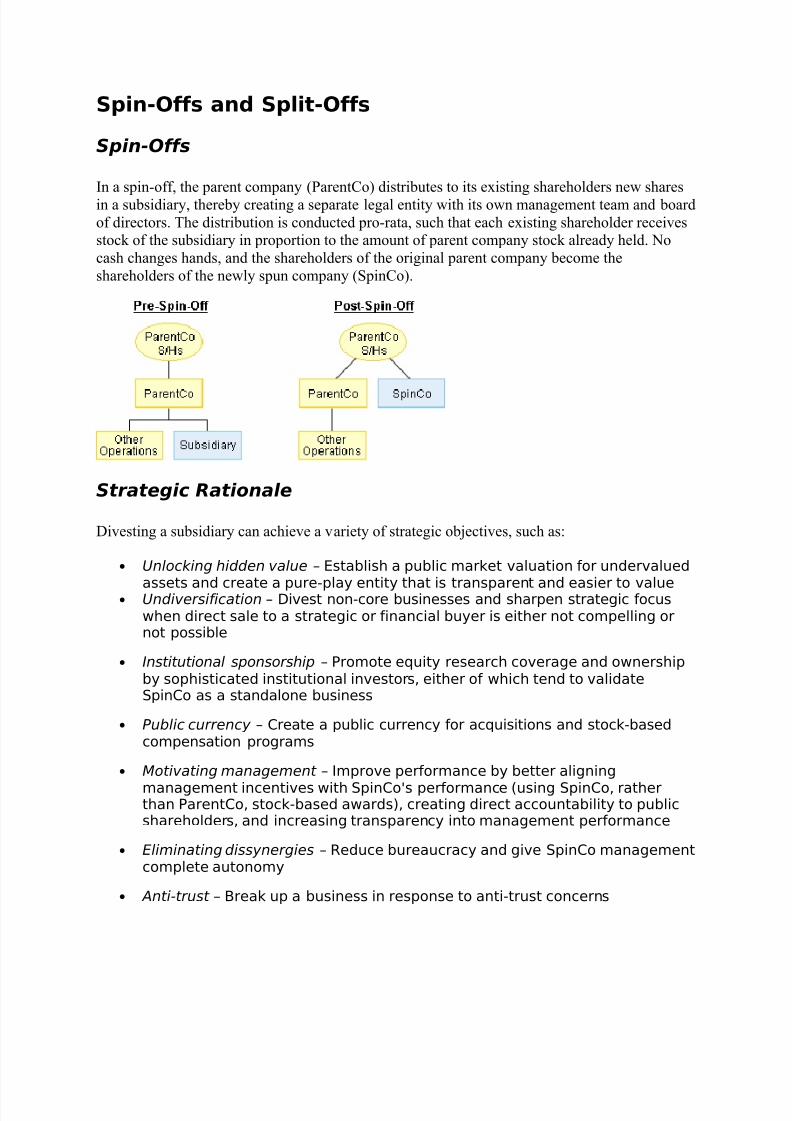

Spin-Offs and Split-Offs

Spin-Offs

In a spin-off, the parent company (ParentCo) distributes to its existing shareholders new sharesin a subsidiary, thereby creating a separate legal entity with its own management team and boardof directors. The distribution is conducted pro-rata, such that each existing shareholder receivesstock of the subsidiary in proportion to the amount of parent company stock already held. Nocash changes hands, and the shareholders of the original parent company become theshareholders of the newly spun company (SpinCo).

Strategic Rationale

Divesting a subsidiary can achieve a variety of strategic objectives, such as:

• Unlocking hidden value – Establish a public market valuation for undervalued

assets and create a pure-play entity that is transparent and easier to value• Undiversification – Divest non-core businesses and sharpen strategic focus

when direct sale to a strategic or financial buyer is either not compelling ornot possible

• Institutional sponsorship – Promote equity research coverage and ownershipby sophisticated institutional investors, either of which tend to validateSpinCo as a standalone business

• Public currency – Create a public currency for acquisitions and stock-basedcompensation programs

• Motivating management – Improve performance by better aligning

management incentives with SpinCo's performance (using SpinCo, ratherthan ParentCo, stock-based awards), creating direct accountability to publicshareholders, and increasing transparency into management performance

• Eliminating dissynergies – Reduce bureaucracy and give SpinCo managementcomplete autonomy

• Anti-trust – Break up a business in response to anti-trust concerns

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 33/68

• Corporate defense – Divest "crown jewel" assets to make a hostile takeoverof ParentCo less attractive

Transaction Structure

In general, there are four ways to execute a spin-off:

• Regular spin-off – Completed all at once in a 100% distribution toshareholders

• Majority spin-off – Parent retains a minority interest (< 20%) in SpinCo anddistributes the majority of the SpinCo stock to shareholders

• Equity carve out (IPO) / spin-off – Implemented as a second step following anearlier equity carve-out of less than 20% of the voting control of thesubsidiary

• Reverse Morris Trust – Implemented as a first step immediately preceding a

Reverse Morris Trust transaction

ParentCo's existing credit agreements may impose restrictions on divestitures that are material innature. It is important to determine if any credit terms will be violated if ParentCo spins off asubsidiary that materially contributes to its business.

Tax Implications

A spin-off is usually tax-free under Internal Revenue Code (IRC) Section 355, meaning that notaxable gain is recognized by either the parent entity or the parent's existing shareholders. Toqualify for favorable tax treatment, the spin-off must meet the requirements of Section 355:

• The parent and subsidiary must both have been engaged in an "active tradeor business" the entire 5 years preceding the spin-off, and neither entity mayhave been acquired during that period in a taxable transaction.

• ParentCo and SpinCo must continue in an active trade or business followingseparation.

• ParentCo must have tax control before the spin-off, defined as ownership of at least 80% of the vote and value of all classes of subsidiary stock.

• ParentCo must relinquish tax control as a result of the spin-off (< 80% voteand value).

• The spin-off must have a valid business purpose, and cannot be used as a"device" to distribute earnings (dividends).

• The parent's shareholders, collectively, must retain continuity of interest inboth parent and subsidiary for a 4-year period beginning 2 years before thespin-off by maintaining 50% equity ownership interest in both companies (achange in control of either ParentCo or SpinCo during this period could triggera tax liability for the ParentCo). This is the anti-Morris Trust rule.

7/27/2019 Advanced Financial Management as Per Syllabus

http://slidepdf.com/reader/full/advanced-financial-management-as-per-syllabus 34/68

If the unusual event that a spin-off does not qualify for tax-free treatment, there are two levels of tax:

• Ordinary income at the shareholder level equal to the FMV of subsidiary stockreceived (similar to a dividend) and

• Capital gain on the sale of stock at the parent entity level equal to the FMV of subsidiary stock distributed less the parent's inside basis in that stock.