adrian hart, bis shrapnel

TRANSCRIPT

INFRASTRUCTURE & MINING

ECONOMIC & CONSTRUCTION OUTLOOK – OCTOBER 2014

Adrian Hart, Senior Manager Infrastructure & Mining

INFRASTRUCTURE & MINING

About BIS Shrapnel: 50 Years

Established in 1964 as Philip Shrapnel & Co: Australia’s leading provider of

industry research, analysis and forecasting services

Our goal is to provide businesses with the information required to make the

best possible decisions

We offer a unique combination of disciplines: market research, analysis and

forecasting

We are a completely independent firm with no vested interests in the industry

sectors and markets which we research and forecast.

100% Australian owned

INFRASTRUCTURE & MINING

About BIS Shrapnel

Highly regarded economic forecaster, industry & construction expert

Focus on analysing and forecasting investment

Highly volatile, swing variable with different drivers

Driver of economic growth now, and productive capacity in the future

Econometric modeling of investment does not work

Need ‘bottom up’ and ‘top down’ approaches

Key ‘real economy’ impact of investment is construction

Construction itself has high multiplier effects.

INFRASTRUCTURE & MINING

ROADS RAIL PORTS

TELECOMSMINING & HEAVY INDUSTRY

MAINTENANCECOST ESCALATIONPOWER

WATER & WASTE WATER

About BIS Infrastructure & Mining

INFRASTRUCTURE & MINING

Presentation Outline

Economic State of Play & Outlook

Global

National

Construction State of Play & Outlook

National

State Differences

Segment Differences

Implications and Risks

What should we be doing now?

What should we be looking out for in future?

What are the key risks to be aware of?

INFRASTRUCTURE & MINING

Key Messages

National economy will be weaker than expected in 2014/15 . . .Large declines to come through in mining (oil and gas) investment

Waiting for non-mining investment to come through (will be 1-2 years away)

Affected by overvalued dollar

NSW economy will outperform most states (except for NT)Residential investment coming through now, infrastructure later – supporting businesses

Focus on Western Sydney in Federal Budget

But coal industry still under pressure from weak prices / overvalued dollar

Harder road ahead for WA and QLDFalling commodity prices stymieing mining investment

Tight government finances delaying upswing in public investment

Risk of synchronised construction downturn in WA, as residential joins the rest

Global economy re-accelerating in 2014 . . .China, though slowing, making up a greater share of global growth

US economy on the verge of a sustainable recovery

Europe still a mess

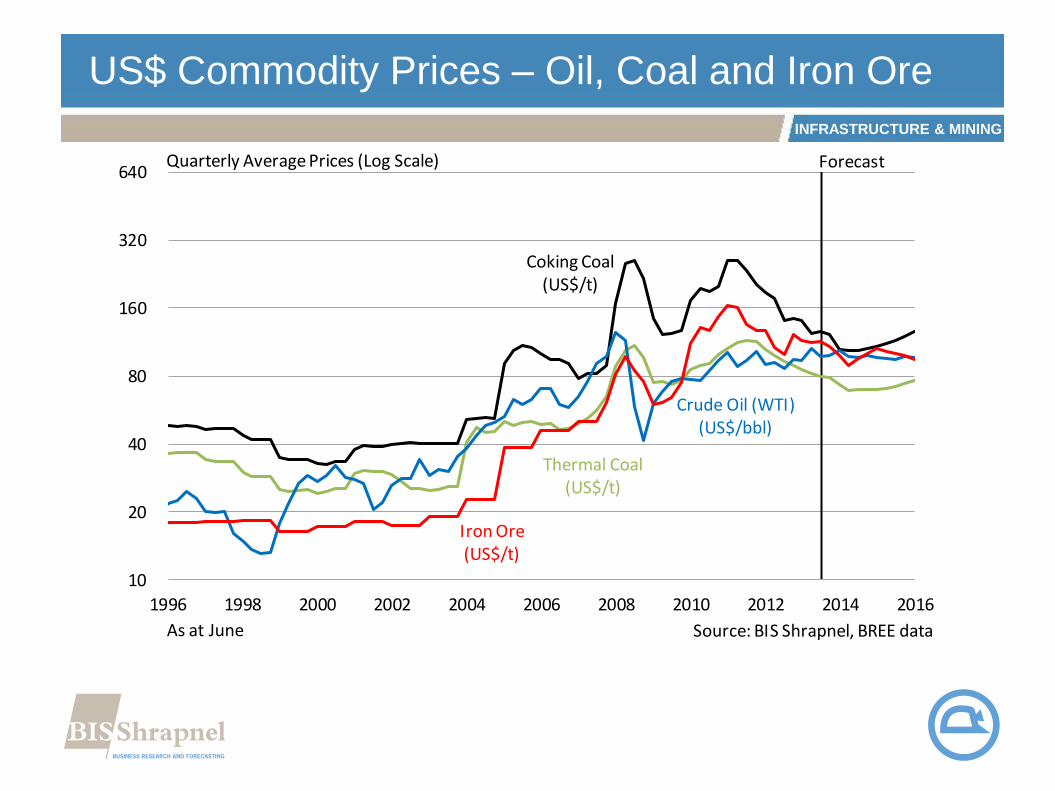

. . . but commodity prices will remain in a weaker rangeMarginal costs of production falling through efficiency drive / rising production

Supply outpacing demand – next step is higher cost production to exit the market

Lower exchange rate required to improve competitiveness

INFRASTRUCTURE & MINING

Implications

Weak growth ahead, but economy and drivers will be very different later

Plan for growth and profitability on 3-5 year horizon

Investment will drive momentum of growthSequence of investment cycles from here

Investment cycles out of syncNeed to be tactical about markets to target

Interest rates have come down

Think about the best time to lock in

Leases & construction costs

Industry & regional differences

INFRASTRUCTURE & MINING

Risks

Structural readjustment of economy takes longer than expected:A$ stays too high for too long

Delays recovery and investment in trade-ables sectors – including mining

Global economy sees further crises or weaker growthChina / Russia / US / Europe

Impact on prices and investment

Domestic politics stymie fiscal policyDelays to the next round of infrastructure projects

Federal and State issues

Low growth economy (2014/15) stymies consumer spending

Regulatory environment inhibits new investmentUncertainty over energy, mining and industrial policies

Federal Senate a mess

INFRASTRUCTURE & MINING

ECONOMIC OUTLOOK

INFRASTRUCTURE & MINING

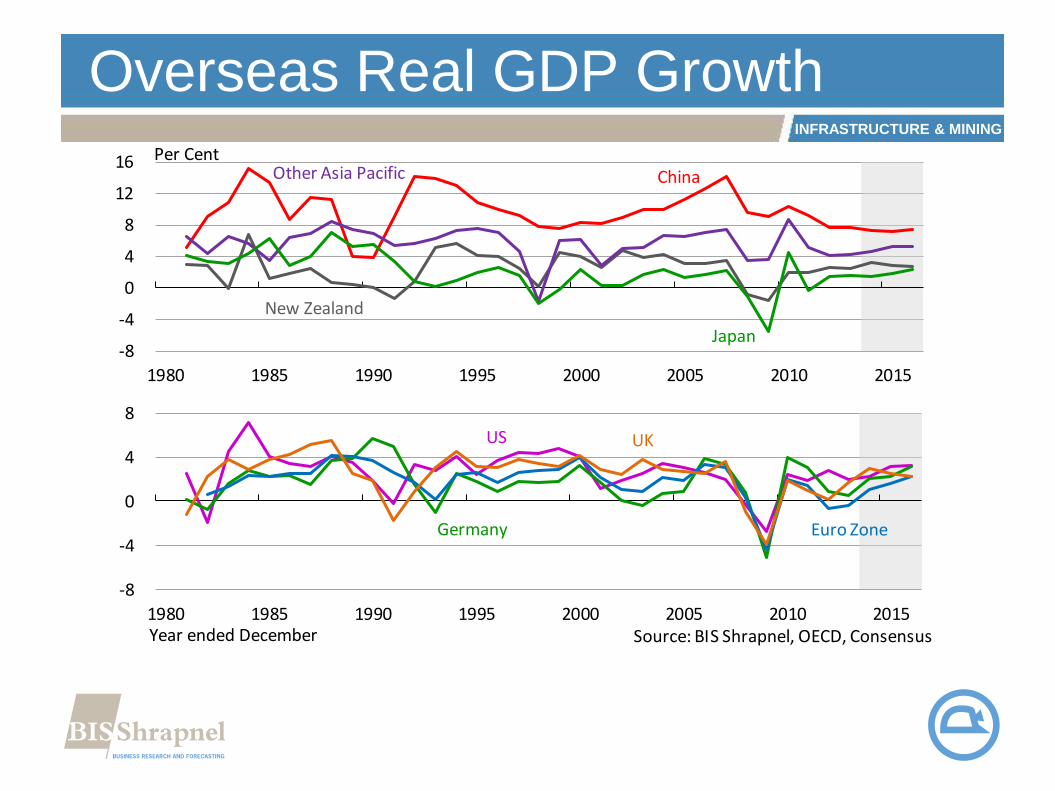

Economic Outlook: Global

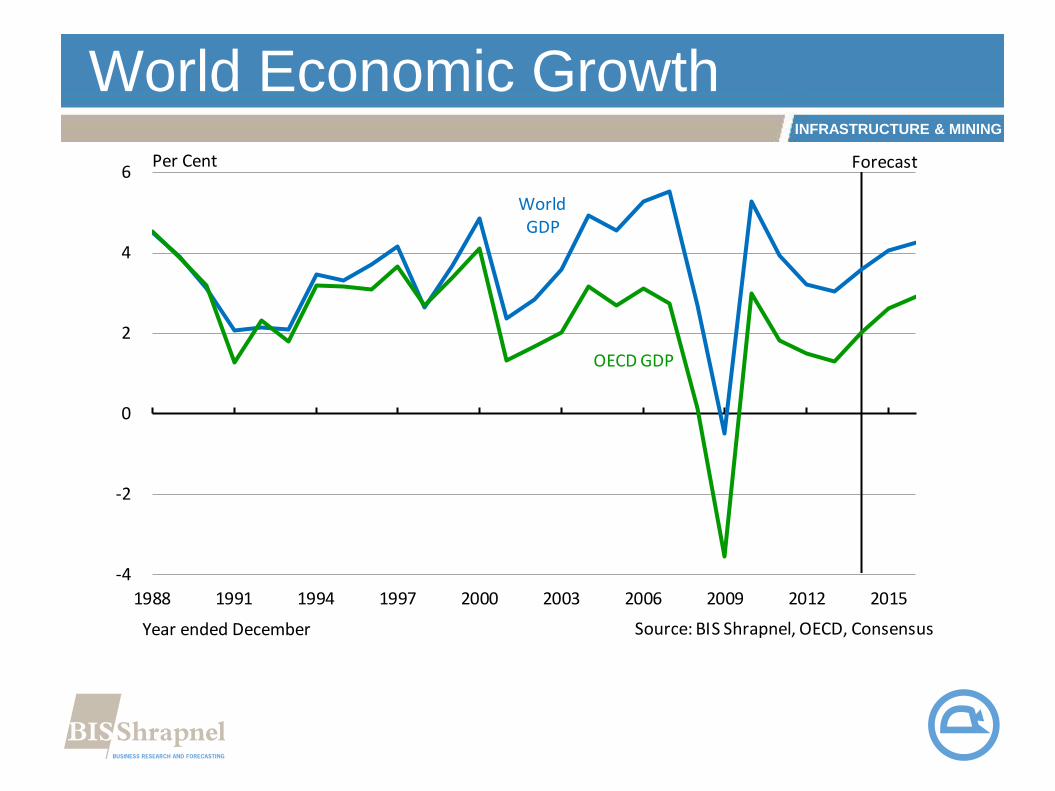

Global economic growth slumped to 3.2% in calendar 2012

o Fading of stimulus following stronger growth in 2011

o Chinese growth slowed from 9.3% to 7.7% - affecting regional economy

o Euro economy in recession – Germany & France join the slowdown

o US economy showed signs of life

2013 was more of the same . . .

o Global growth troughed at 3.0% for 2013; 1.3% for OECD

o Chinese growth slowed along with investment boom

o US fundamentals improved but growth still sluggish

o US will need to pick up as Chinese growth rate slows over next 5 years

INFRASTRUCTURE & MINING

Economic Outlook: Global

Calendar 2014 expected to be stronger . . .

o Global GDP growth forecast to accelerate to 3.5% as . . .

o Euro economy emerges weakly from recession

o Chinese growth to be sustained between 7-7.5% . . . but easing

o US economy still looking for a sustainable recovery but is improving

. . . but there are also risks

o Stability of China’s economy and financial system

o Impact of stronger US economy on capital flows to developing economies

o Impacts of rolling back monetary stimulus in US

o Structural problems in Euro economy remain

o Emerging geo-political risks in Middle East and Eastern Europe

INFRASTRUCTURE & MINING

Overseas Real GDP Growth

-8

-4

0

4

8

12

16

1980 1985 1990 1995 2000 2005 2010 2015

Per Cent

New Zealand

Other Asia Pacific China

Japan

-8

-4

0

4

8

1980 1985 1990 1995 2000 2005 2010 2015Year ended December Source: BIS Shrapnel, OECD, Consensus

Euro ZoneGermany

US UK

INFRASTRUCTURE & MINING

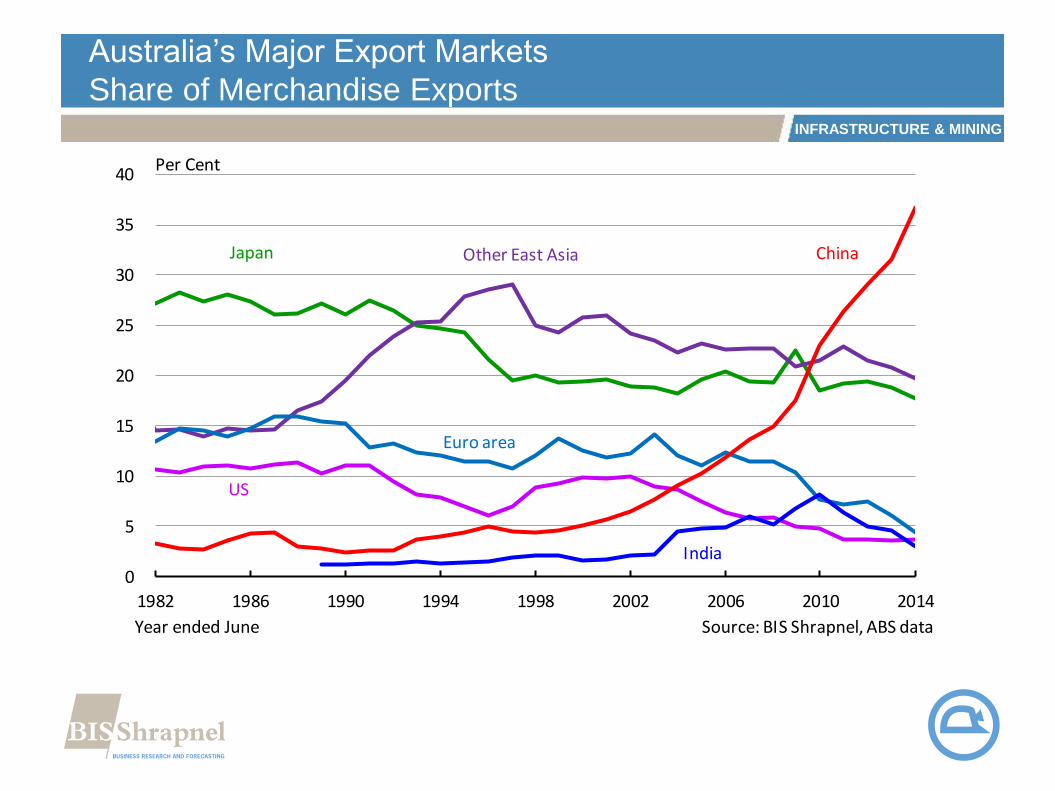

Australia’s Major Export Markets

Share of Merchandise Exports

0

5

10

15

20

25

30

35

40

1982 1986 1990 1994 1998 2002 2006 2010 2014

Year ended June Source: BIS Shrapnel, ABS data

Japan

Euro area

China

US

Other East Asia

India

Per Cent

INFRASTRUCTURE & MINING

World Economic Growth

-4

-2

0

2

4

6

1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

Per Cent Forecast

OECD GDP

World GDP

Year ended December Source: BIS Shrapnel, OECD, Consensus

INFRASTRUCTURE & MINING

US$ Commodity Prices – Oil, Coal and Iron Ore

10

20

40

80

160

320

640

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Forecast

As at June Source: BIS Shrapnel, BREE data

Quarterly Average Prices (Log Scale)

Crude Oil (WTI)(US$/bbl)

Coking Coal(US$/t)

Thermal Coal(US$/t)

Iron Ore(US$/t)

INFRASTRUCTURE & MINING

A$ Commodity Prices – Oil, Coal and Iron Ore

10

20

40

80

160

320

640

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Forecast

As at June Source: BIS Shrapnel, BREE data

Quarterly Average Prices (Log Scale)

Crude Oil (WTI)(A$/bbl)

Coking Coal(A$/t)

Thermal Coal(A$/t)

Iron Ore(A$/t)

INFRASTRUCTURE & MINING

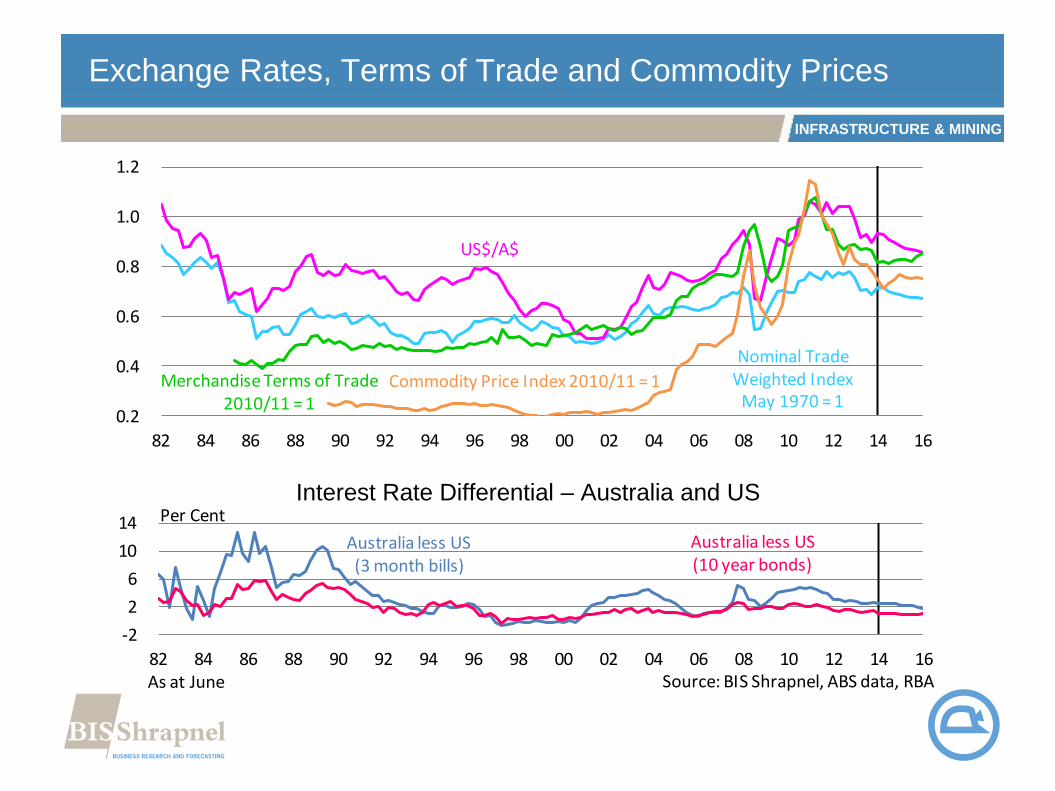

Exchange Rates, Terms of Trade and Commodity Prices

Interest Rate Differential – Australia and US

0.2

0.4

0.6

0.8

1.0

1.2

82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16

Forecast

Nominal Trade Weighted Index

May 1970 = 1Commodity Price Index 2010/11 = 1Merchandise Terms of Trade

2010/11 = 1

US$/A$

-2

2

6

10

14

82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16As at June Source: BIS Shrapnel, ABS data, RBA

Per Cent

Australia less US(3 month bills)

Australia less US(10 year bonds)

INFRASTRUCTURE & MINING

CPI Inflation Measures

Headline, Underlying, Tradeables and Non-tradeables

-3

0

3

6

9

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Source: BIS Shrapnel, ABS dataAs at June

Non-tradeables CPI Headline

Tradeables

-2

0

2

4

6

8

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

ForecastAnnual Per Cent

RBA Underlying MeasureCPI Headline

RBA Inflation Target

INFRASTRUCTURE & MINING

Interest Rates and Margins – Australia

0

2

4

6

8

10

12

96 98 00 02 04 06 08 10 12 14 16

Forecast

Cash Rate

Prime Overdraft Rate

RBA Underlying Measure Real Housing Rate

Housing Variable Rate

Per Cent

RBA Inflation Target

0

2

4

6

8

96 98 00 02 04 06 08 10 12 14 16As at June Source: BIS Shrapnel, ABS data, RBA

Prime Overdraft Rate - Cash Rate

Housing Variable Rate - Cash Rate

INFRASTRUCTURE & MINING

Economic Trends: Australia

2013/14: Mild pickup as Investment Boom became Export Boom

o GDP growth through 2013/14 accelerated to 2.9% - still weak!

o Again, growth is highly uneven and driven mostly by exports

Domestic demand (GNE) growth of just 1.2% (weakest since 2001)

Investment fell another 1.4%; consumption growth around 2.5%

Public investment flat (18% below Sept 2010 peak)

Private investment fell 2.6% (1st since GFC): Mining vs Dwellings

External contribution +2% (Exports UP 6.8%; Imports down 2.3%)

Construction work done grew only 0.2% - unsynchronised

INFRASTRUCTURE & MINING

Economic Outlook: Australia

OUTLOOK: Weaker growth ahead before recovery

o 2014/15: GDP growth to slip back towards 2.5%

Falls in non-dwelling investment the biggest problem

Further falls in public investment before recovery

Dwelling pickup to continue but struggles to offset mining downturn

Growth in consumer spending remains subdued

Narrowing in net export contribution

Still waiting for recovery in other parts of the economy

o 2015/16: GDP growth returning near trend – but risks ahead

Total investment returns to positive growth (lower dollar helps)

Pickup in employment – but RBA returns to tightening bias

INFRASTRUCTURE & MINING

Basic Economic Indicators

Moving Annual Totals

-4

-2

0

2

4

6

8

88 90 92 94 96 98 00 02 04 06 08 10 12 14 16

Per Cent Forecast

External Contribution

Real GNE

Real GDP

-2

-1

0

1

2

3

4

88 90 92 94 96 98 00 02 04 06 08 10 12 14 16

Year ended June Source: BIS Shrapnel, ABS data

Contribution to Domestic Demand - Per Cent Forecast

New Business Investment

Government Expenditure

Dwelling Investment

Private Consumption

INFRASTRUCTURE & MINING

CONSTRUCTIONAUSTRALIA

INFRASTRUCTURE & MINING

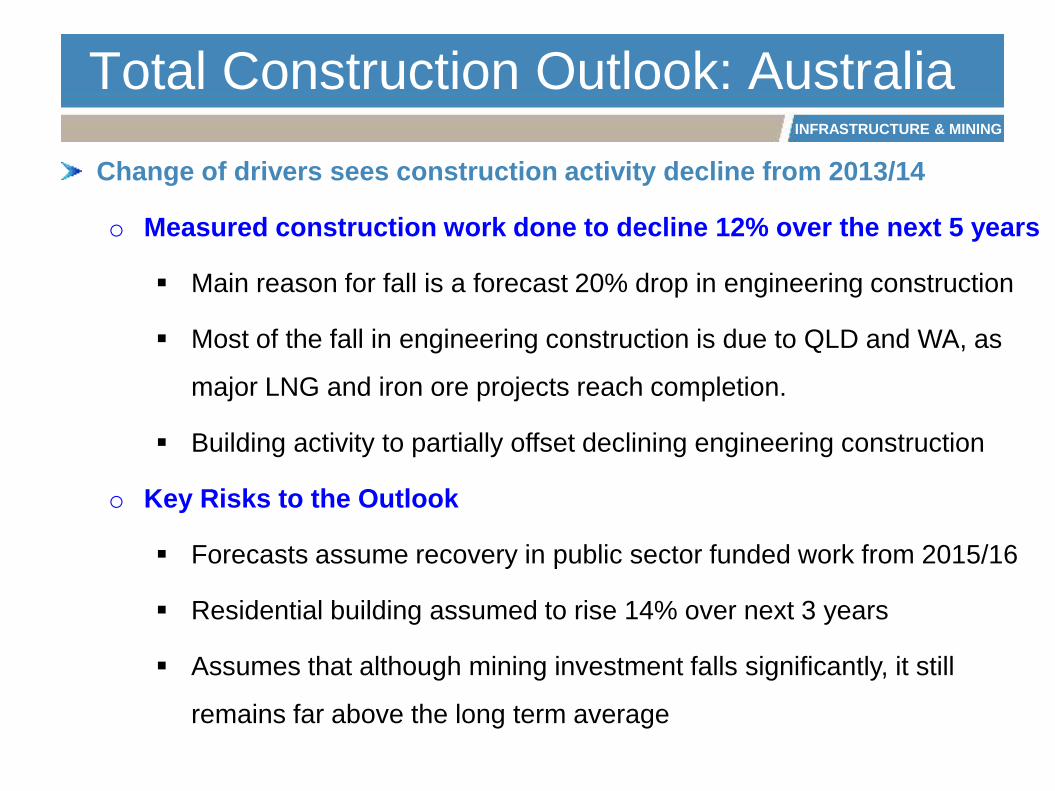

Total Construction Outlook: Australia

Change of drivers sees construction activity decline from 2013/14

o Measured construction work done to decline 12% over the next 5 years

Main reason for fall is a forecast 20% drop in engineering construction

Most of the fall in engineering construction is due to QLD and WA, as

major LNG and iron ore projects reach completion.

Building activity to partially offset declining engineering construction

o Key Risks to the Outlook

Forecasts assume recovery in public sector funded work from 2015/16

Residential building assumed to rise 14% over next 3 years

Assumes that although mining investment falls significantly, it still

remains far above the long term average

INFRASTRUCTURE & MINING

Australian Construction Activity

0

50

100

150

200

250

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

$ Billion

Year Ended June

Non-Residential Building Work Done

Dwelling Building Work Done

Engineering Construction Work Done

Source: BIS Shrapnel, ABS Data

‘91 recession

‘01 slump

‘08 financial crisis

One NationProjects

Y2K Projects

Housing boom/bust

GST

Private funding boom

Public funding boom

Resources boom

INFRASTRUCTURE & MINING

Private New Capital Expenditure

Constant 2011/12 prices

2

4

8

16

32

64

128

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Mining

Forecast$ Billion (Log Scale)

Rental, Hiring & Real Estate

Manufacturing

Transport & Storage

Year ended June Source: BIS Shrapnel, ABS data

INFRASTRUCTURE & MINING

Coal Outlook

0

100

200

300

400

500

600

700

0

2

4

6

8

10

12

14

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

Black coal production (Mtpa)

Coal construction work done ($b)

Year ended June Source: BIS Shrapnel, ABS, BREE

$ Billion Mtpa

INFRASTRUCTURE & MINING

Iron Ore Outlook

0

200

400

600

800

1,000

0

5

10

15

20

25

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

Iron ore production (Mtpa)

Iron ore construction work done ($b)

Year ended June Source: BIS Shrapnel, ABS, BREE

$ Billion Mtpa

INFRASTRUCTURE & MINING

Oil and Gas Outlook

0

40

80

120

160

200

0

10

20

30

40

50

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

Natural Gas Production (Gm3)

Oil & gas construction work done ($b)

Year ended June Source: BIS Shrapnel, ABS, BREE

$ Billion Gm3

INFRASTRUCTURE & MINING

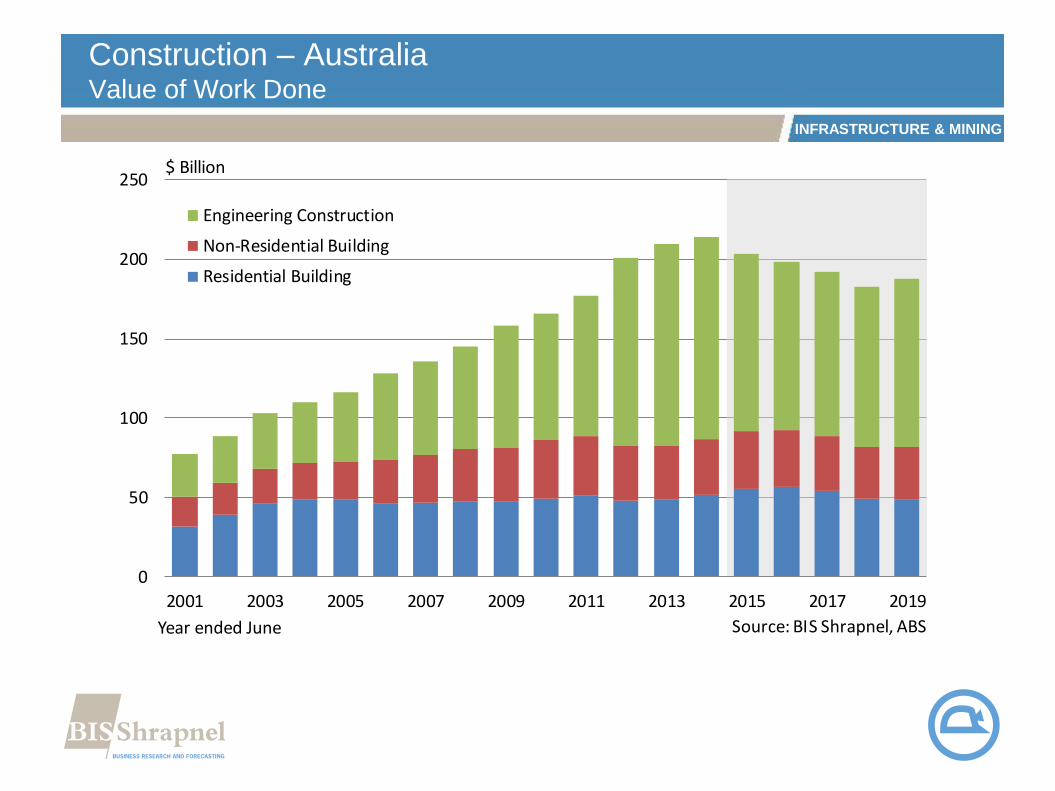

Construction – AustraliaValue of Work Done

0

50

100

150

200

250

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Year ended June

Engineering Construction

Non-Residential Building

Residential Building

Source: BIS Shrapnel, ABS

$ Billion

INFRASTRUCTURE & MINING

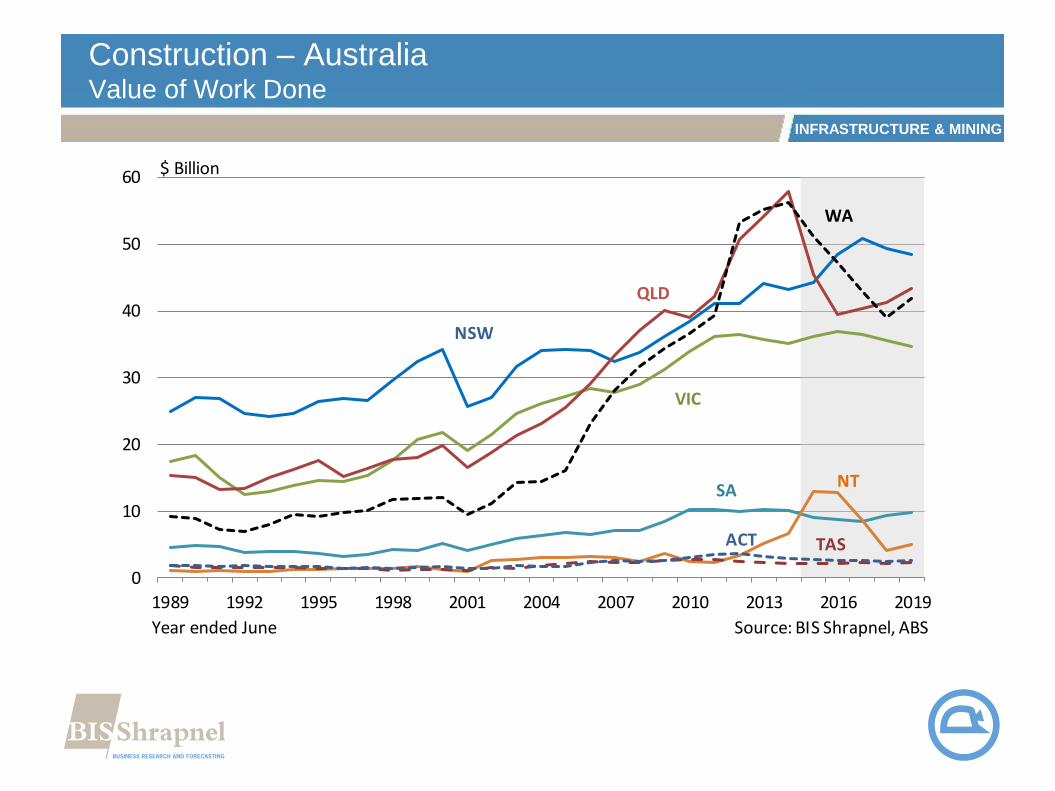

Construction – AustraliaValue of Work Done

0

10

20

30

40

50

60

1989 1992 1995 1998 2001 2004 2007 2010 2013 2016 2019

Source: BIS Shrapnel, ABS

$ Billion

Year ended June

NSW

QLD

VIC

WA

SA NT

ACT TAS

INFRASTRUCTURE & MINING

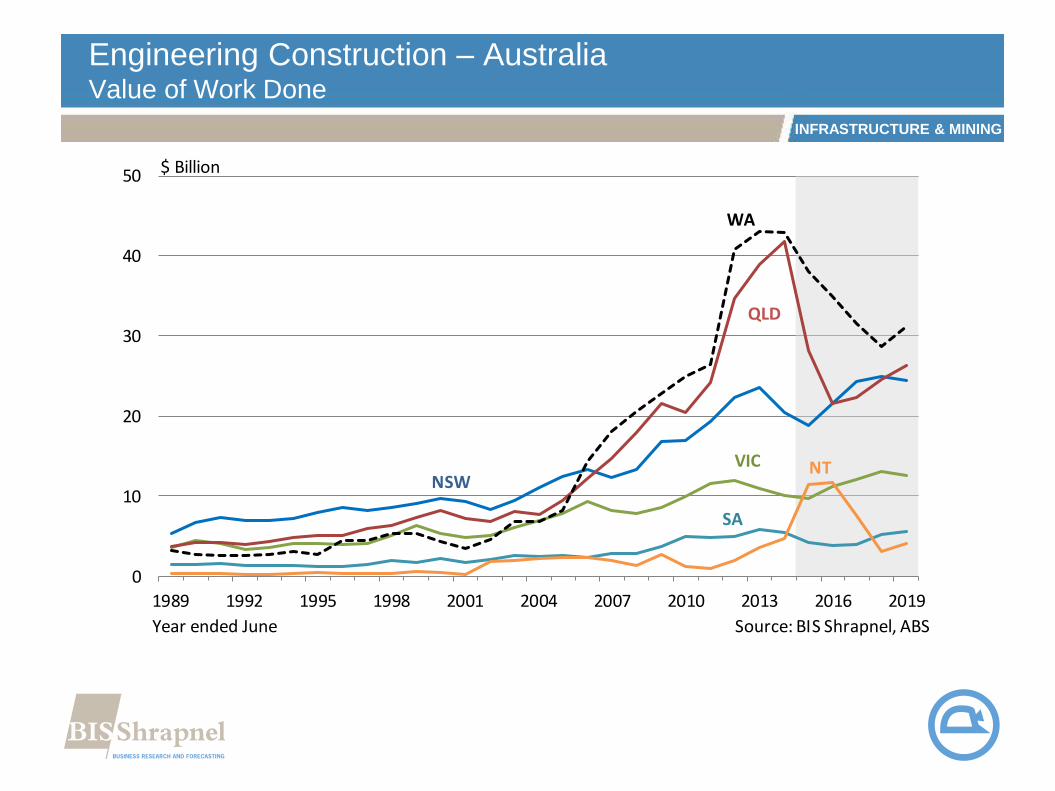

Engineering Construction – AustraliaValue of Work Done

0

10

20

30

40

50

1989 1992 1995 1998 2001 2004 2007 2010 2013 2016 2019

Source: BIS Shrapnel, ABS

$ Billion

Year ended June

NSW

QLD

VIC

WA

SA

NT

INFRASTRUCTURE & MINING

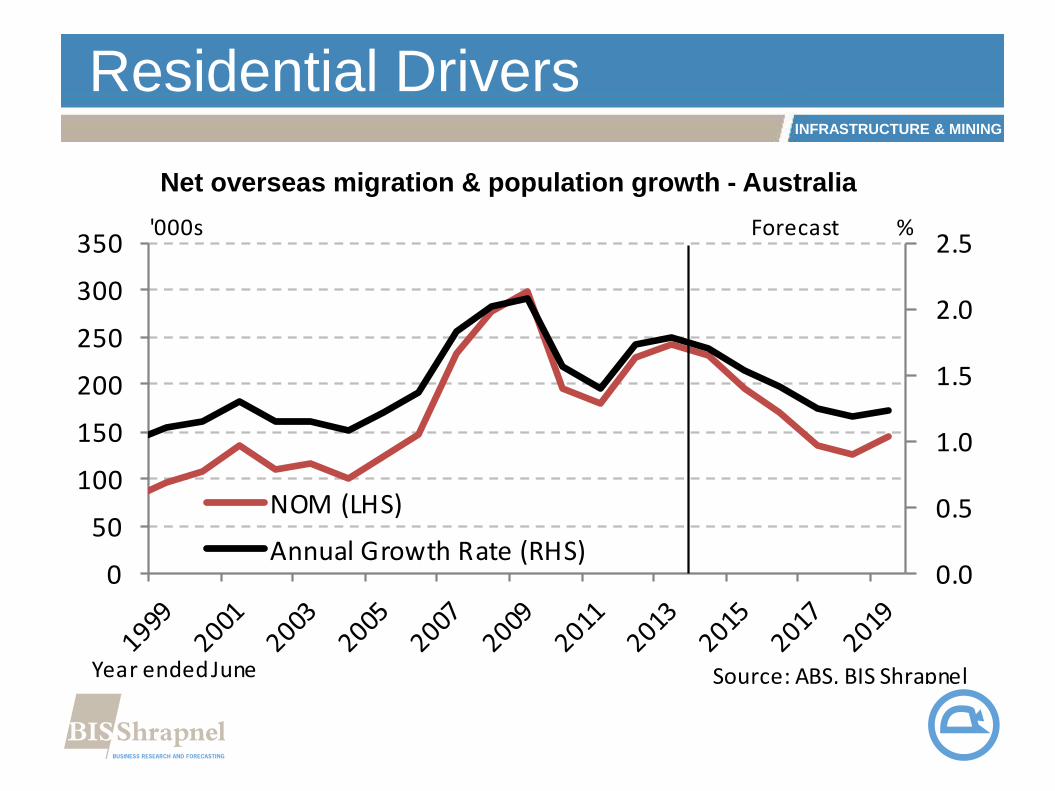

Residential Drivers

Net overseas migration & population growth - Australia

0.0

0.5

1.0

1.5

2.0

2.5

0

50

100

150

200

250

300

350

NOM (LHS)

Annual Growth Rate (RHS)

Year ended June Source: ABS, BIS Shrapnel

Forecast'000s %

INFRASTRUCTURE & MINING

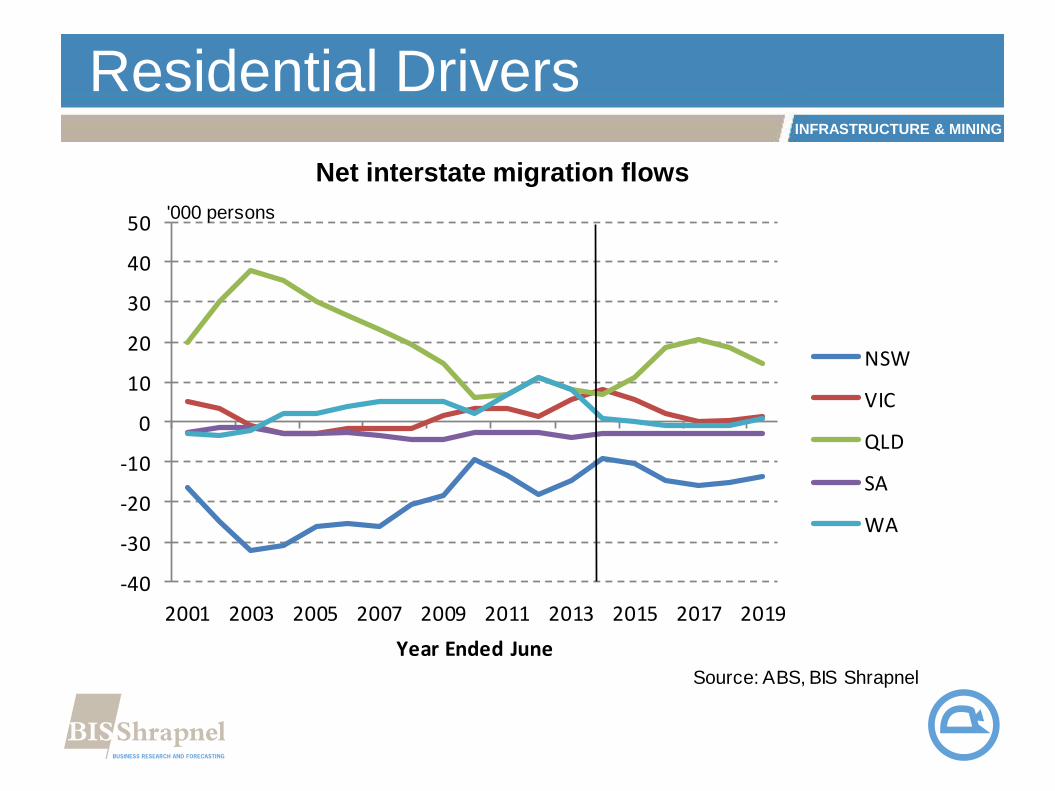

Residential Drivers

Net interstate migration flows

-40

-30

-20

-10

0

10

20

30

40

50

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Year Ended June

NSW

VIC

QLD

SA

WA

'000 persons

Source: ABS, BIS Shrapnel

INFRASTRUCTURE & MINING

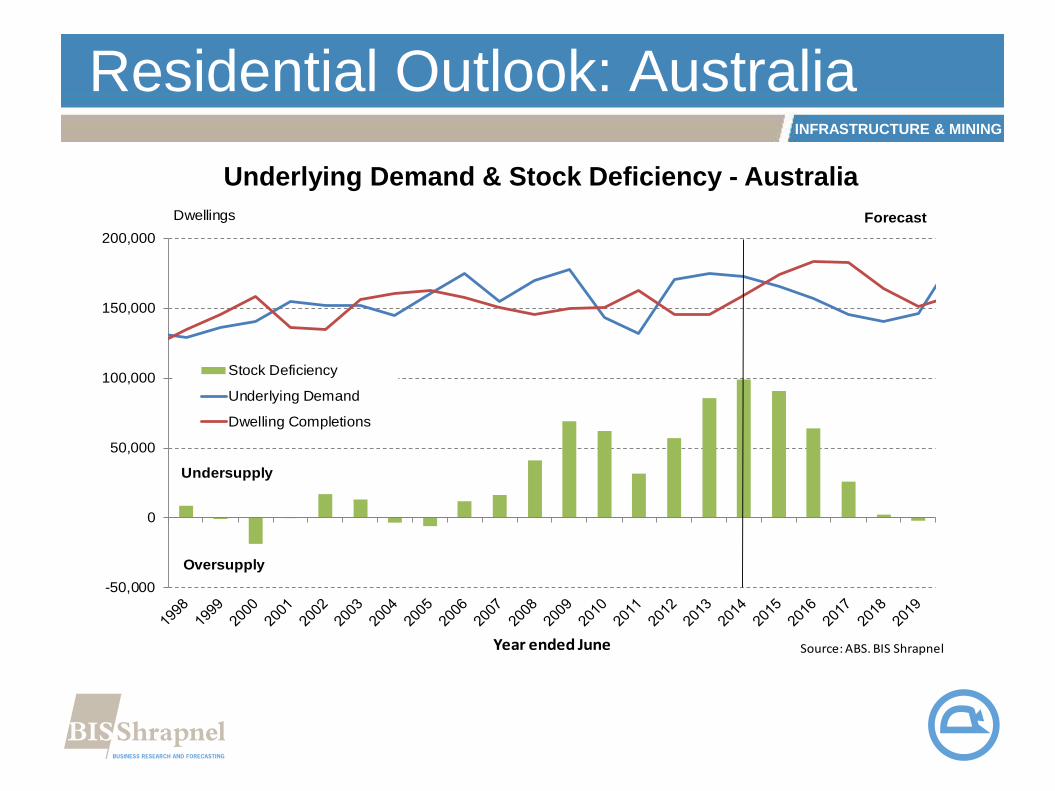

Residential Outlook: Australia

Underlying Demand & Stock Deficiency - Australia

-50,000

0

50,000

100,000

150,000

200,000

Dwellings

Year ended June

Stock Deficiency

Underlying Demand

Dwelling Completions

Undersupply

Oversupply

Forecast

Source: ABS. BIS Shrapnel

INFRASTRUCTURE & MINING

Dwelling commencements by state

0

10

20

30

40

50

60

1989 1992 1995 1998 2001 2004 2007 2010 2013 2016 2019

Source: BIS Shrapnel, ABS

Number of dwelling commencements ('000)

Year ended June

NSW

QLD

VIC

WASA

INFRASTRUCTURE & MINING

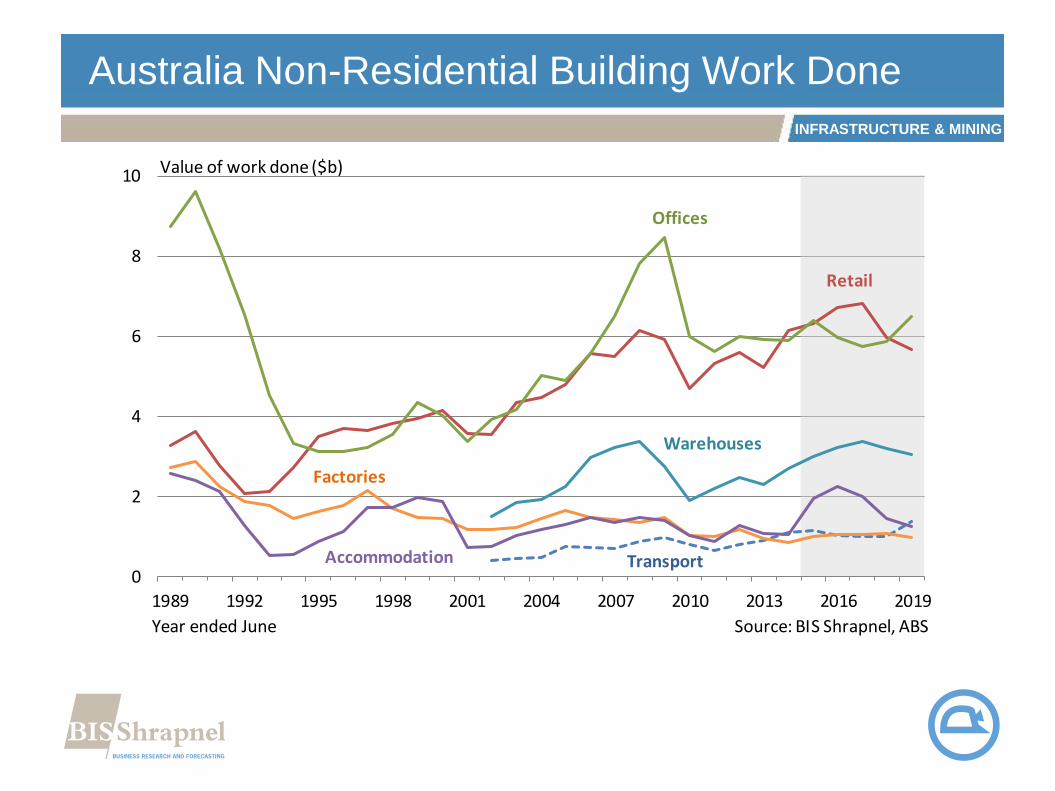

Australia Non-Residential Building Work Done

0

2

4

6

8

10

1989 1992 1995 1998 2001 2004 2007 2010 2013 2016 2019

Source: BIS Shrapnel, ABS

Value of work done ($b)

Year ended June

Transport

Retail

Offices

Factories

Warehouses

Accommodation

INFRASTRUCTURE & MINING

Australia Non-Residential Building Work Done

0

2

4

6

8

10

12

1989 1992 1995 1998 2001 2004 2007 2010 2013 2016 2019

Source: BIS Shrapnel, ABS

Value of work done ($b)

Year ended June

Aged Care

Education

Health

Entertainment

INFRASTRUCTURE & MINING

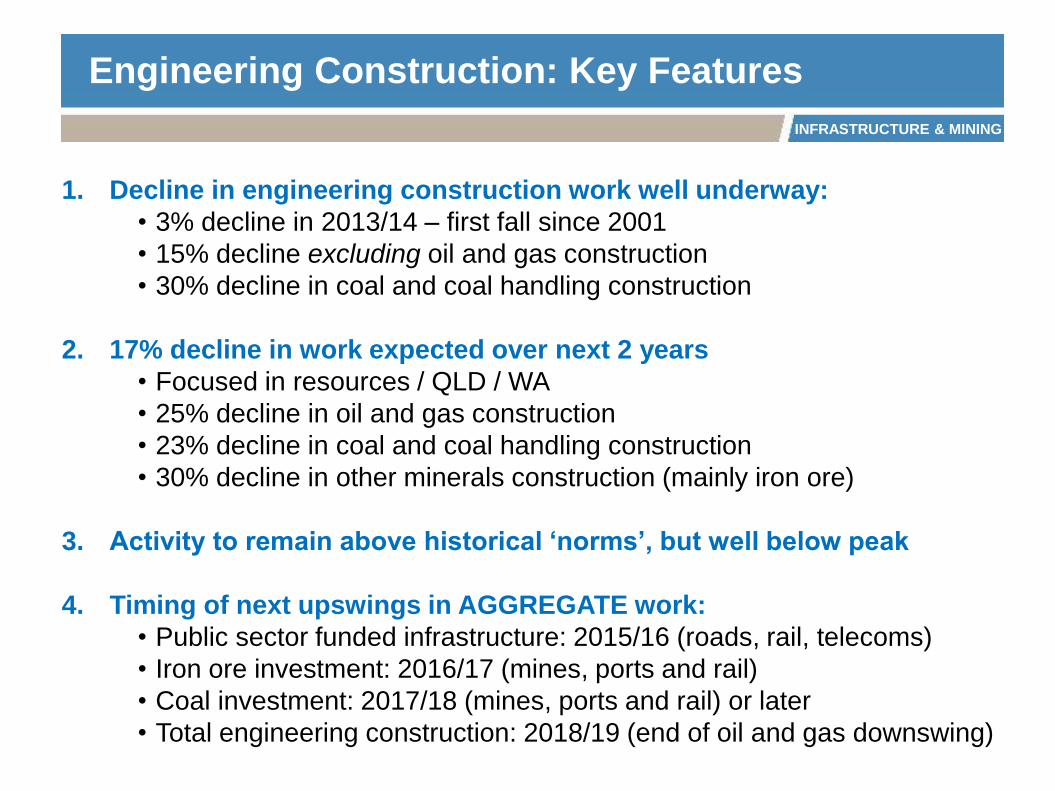

Engineering Construction: Key Features

1. Decline in engineering construction work well underway:

• 3% decline in 2013/14 – first fall since 2001

• 15% decline excluding oil and gas construction

• 30% decline in coal and coal handling construction

2. 17% decline in work expected over next 2 years

• Focused in resources / QLD / WA

• 25% decline in oil and gas construction

• 23% decline in coal and coal handling construction

• 30% decline in other minerals construction (mainly iron ore)

3. Activity to remain above historical ‘norms’, but well below peak

4. Timing of next upswings in AGGREGATE work:

• Public sector funded infrastructure: 2015/16 (roads, rail, telecoms)

• Iron ore investment: 2016/17 (mines, ports and rail)

• Coal investment: 2017/18 (mines, ports and rail) or later

• Total engineering construction: 2018/19 (end of oil and gas downswing)

INFRASTRUCTURE & MINING

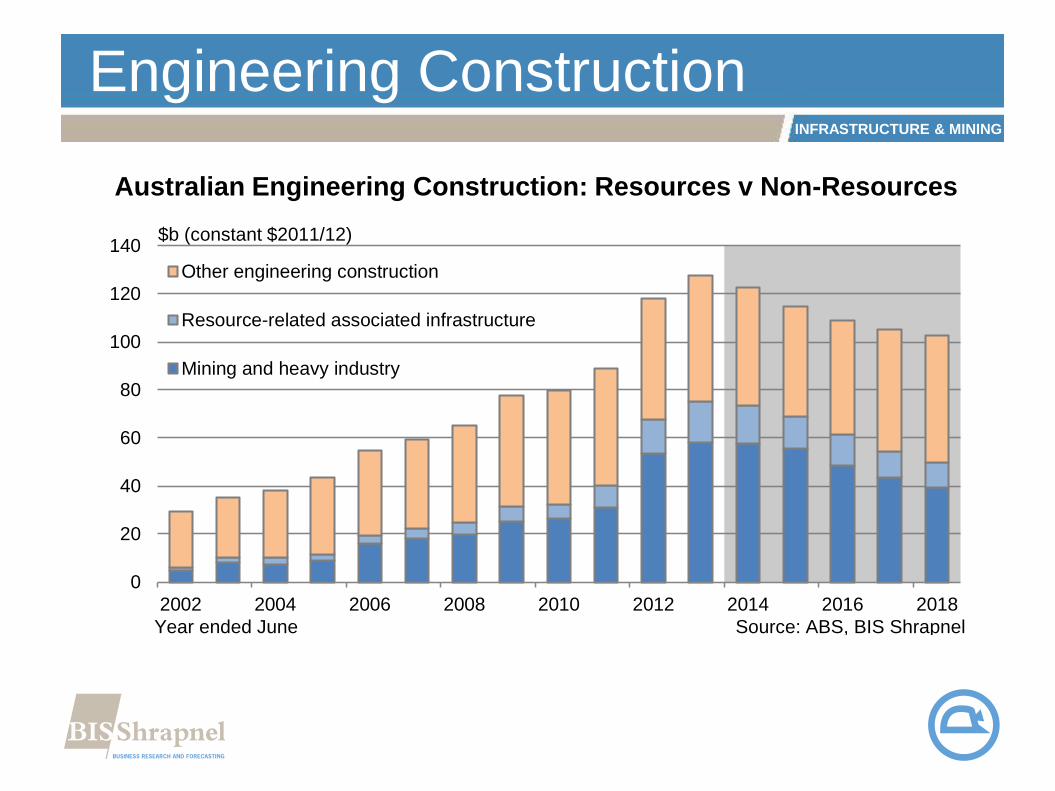

Engineering Construction

Australian Engineering Construction: Resources v Non-Resources

0

20

40

60

80

100

120

140

2002 2004 2006 2008 2010 2012 2014 2016 2018

Other engineering construction

Resource-related associated infrastructure

Mining and heavy industry

$b (constant $2011/12)

Year ended June Source: ABS, BIS Shrapnel

INFRASTRUCTURE & MINING

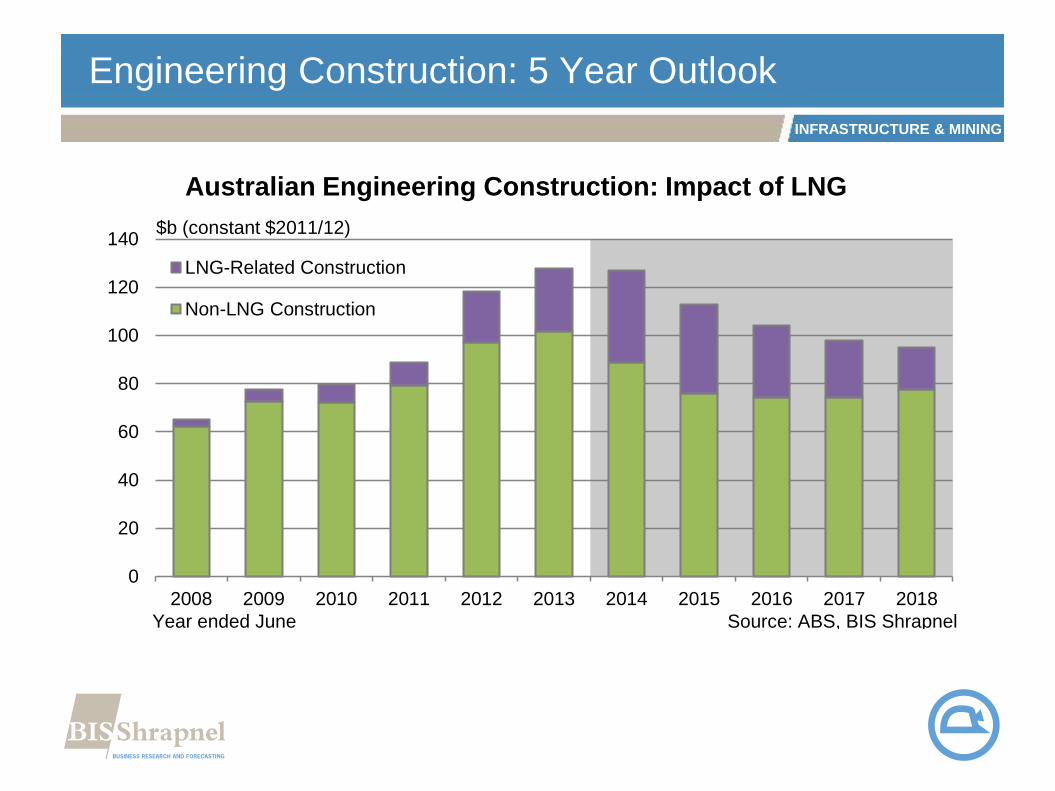

Engineering Construction: 5 Year Outlook

Australian Engineering Construction: Impact of LNG

0

20

40

60

80

100

120

140

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

LNG-Related Construction

Non-LNG Construction

$b (constant $2011/12)

Year ended June Source: ABS, BIS Shrapnel

INFRASTRUCTURE & MINING

Engineering Construction: 5 Year Outlook

Australian Non-Resources Engineering Construction

0

10

20

30

40

50

60

2002 2004 2006 2008 2010 2012 2014 2016 2018

Other engineering construction

$b (constant $2011/12)

Year ended June Source: ABS, BIS Shrapnel

INFRASTRUCTURE & MINING

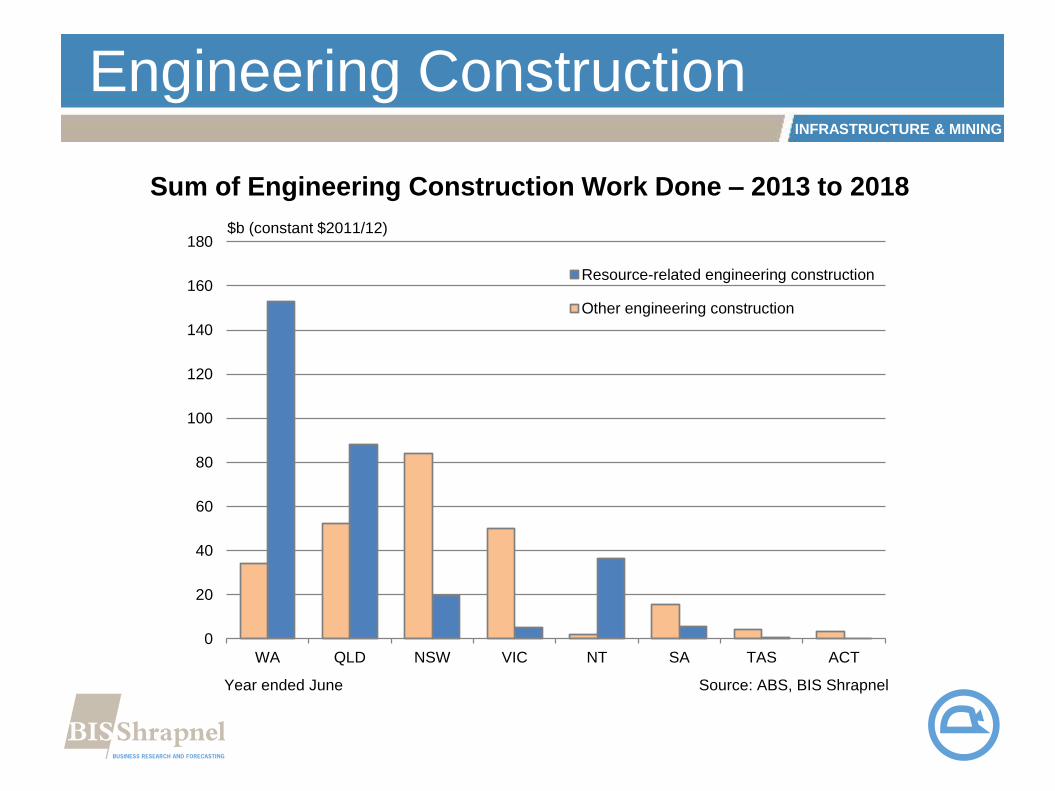

Engineering Construction

Sum of Engineering Construction Work Done – 2013 to 2018

ACTTASSANTVICNSWQLDWA

0

20

40

60

80

100

120

140

160

180

Resource-related engineering construction

Other engineering construction

$b (constant $2011/12)

Year ended June Source: ABS, BIS Shrapnel

INFRASTRUCTURE & MINING

Engineering Construction – AustraliaValue of Work Done

0

5

10

15

20

25

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Roads (Current) Roads (May-14)

Railways (Current) Railways (May-14)

Harbours (Current) Harbours (May-14)

Year ended June Source: BIS Shrapnel, ABS

$ Billion

INFRASTRUCTURE & MINING

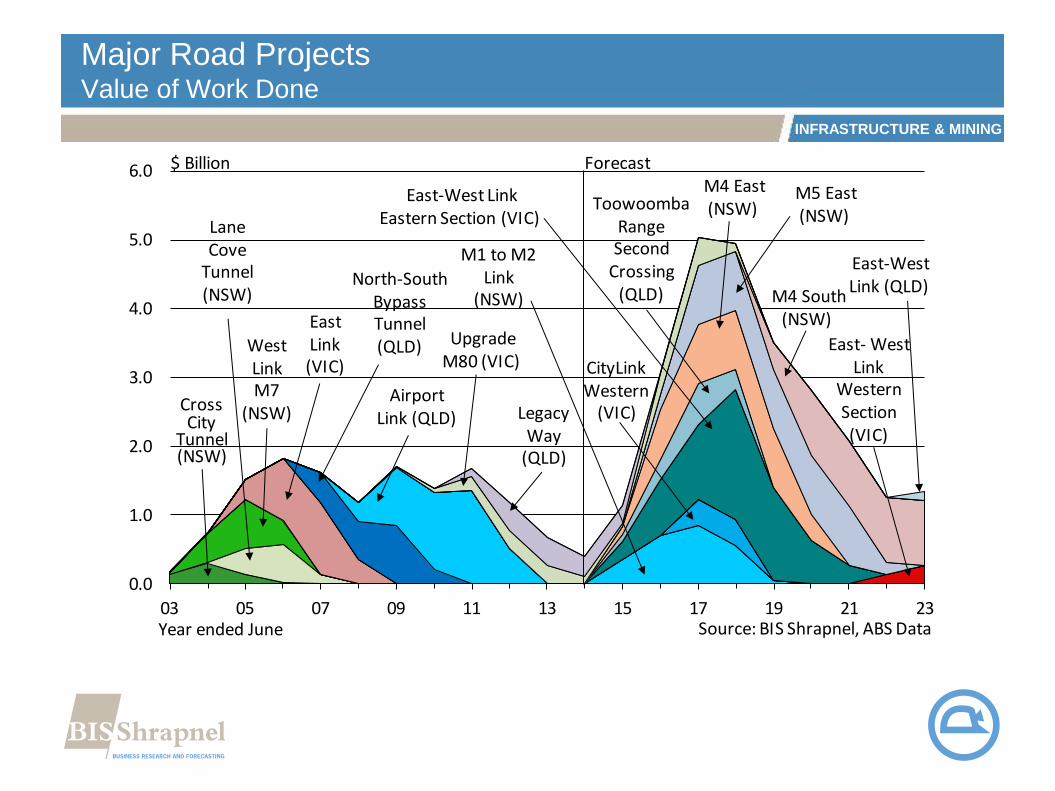

Major Road ProjectsValue of Work Done

0.0

1.0

2.0

3.0

4.0

5.0

6.0

03 05 07 09 11 13 15 17 19 21 23

North-South Bypass Tunnel (QLD)

CrossCity

Tunnel (NSW)

West LinkM7

(NSW)Airport

Link (QLD)

M1 to M2 Link

(NSW)

Lane Cove

Tunnel(NSW)

Source: BIS Shrapnel, ABS DataYear ended June

Forecast$ Billion

East-West Link Eastern Section (VIC)

M4 East(NSW)

East- West Link

Western Section(VIC)

East Link (VIC)

Upgrade M80 (VIC)

Legacy Way

(QLD)

CityLink Western

(VIC)

Toowoomba Range Second

Crossing (QLD)

East-West Link (QLD)

M5 East(NSW)

M4 South(NSW)

INFRASTRUCTURE & MINING

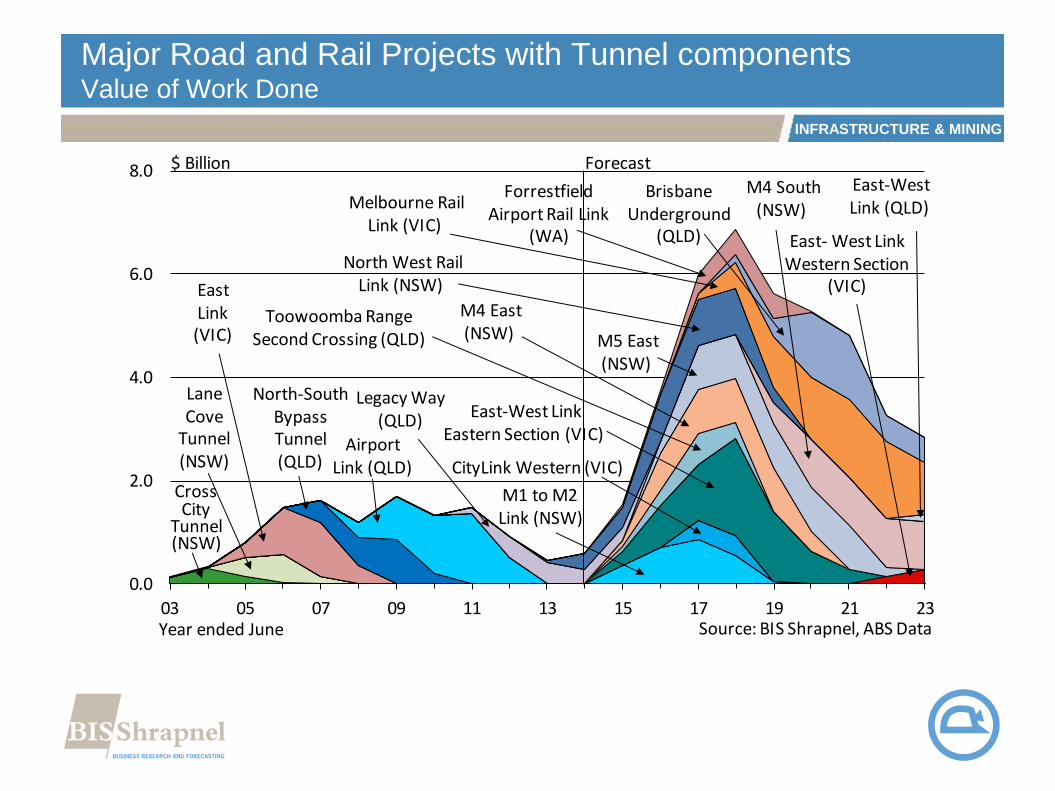

Major Road and Rail Projects with Tunnel componentsValue of Work Done

0.0

2.0

4.0

6.0

8.0

03 05 07 09 11 13 15 17 19 21 23

North-South Bypass Tunnel (QLD)

CrossCity

Tunnel (NSW)

Airport Link (QLD)

M1 to M2 Link (NSW)

Lane Cove

Tunnel(NSW)

Source: BIS Shrapnel, ABS DataYear ended June

Forecast$ Billion

M4 East(NSW)

East Link (VIC)

Legacy Way(QLD)

CityLink Western (VIC)

Toowoomba RangeSecond Crossing (QLD)

East-West Link (QLD)

M5 East(NSW)

M4 South(NSW)

East-West Link Eastern Section (VIC)

East- West Link Western Section

(VIC)

North West Rail Link (NSW)

Melbourne Rail Link (VIC)

Brisbane Underground

(QLD)

Forrestfield Airport Rail Link

(WA)

INFRASTRUCTURE & MINING

Engineering Construction – AustraliaValue of Work Done

0

3

6

9

12

15

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Water (Current) Water (May-14)

Sewerage (Current) Sewerage (May-14)

Electricity (Current) Electricity (May-14)

Year ended June Source: BIS Shrapnel, ABS

$ Billion

INFRASTRUCTURE & MINING

Engineering Construction – AustraliaValue of Work Done

0

2

4

6

8

10

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Pipelines (Current) Pipelines (May-14)

Recreation (Current) Recreation (May-14)

Telecommunications (Current) Telecommunications (May-14)

Year ended June Source: BIS Shrapnel, ABS

$ Billion

INFRASTRUCTURE & MINING

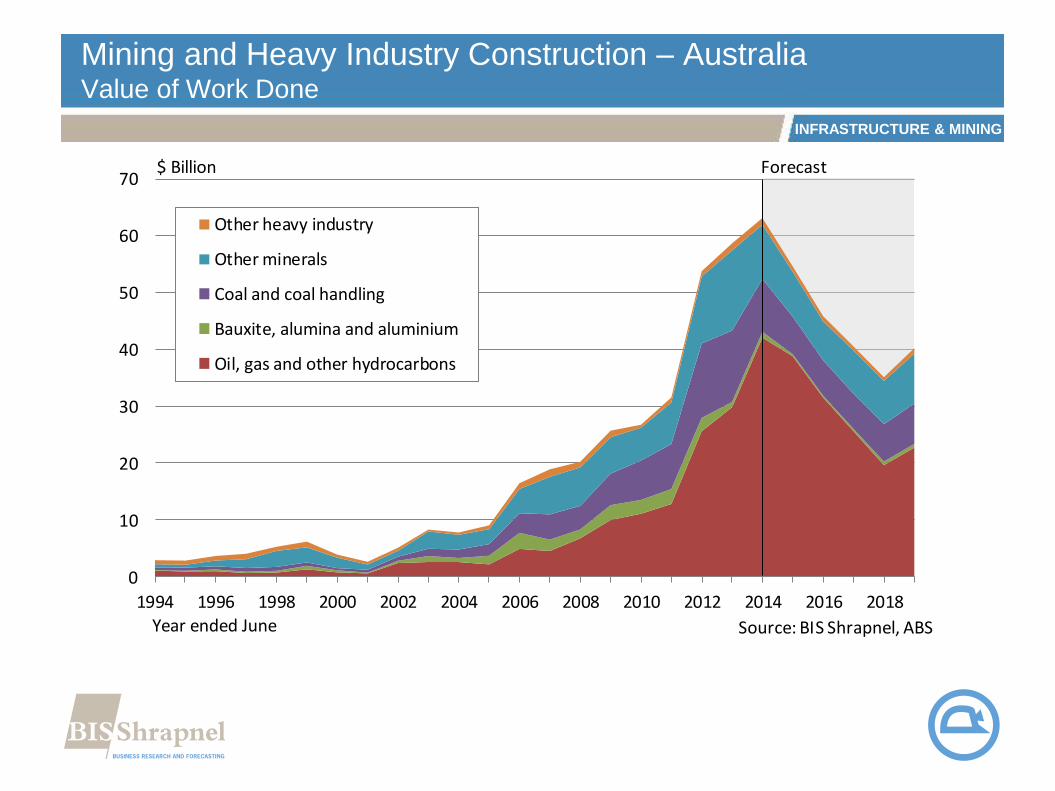

Mining and Heavy Industry Construction – AustraliaValue of Work Done

0

10

20

30

40

50

60

70

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Other heavy industry

Other minerals

Coal and coal handling

Bauxite, alumina and aluminium

Oil, gas and other hydrocarbons

Year ended June Source: BIS Shrapnel, ABS

$ Billion Forecast

INFRASTRUCTURE & MINING

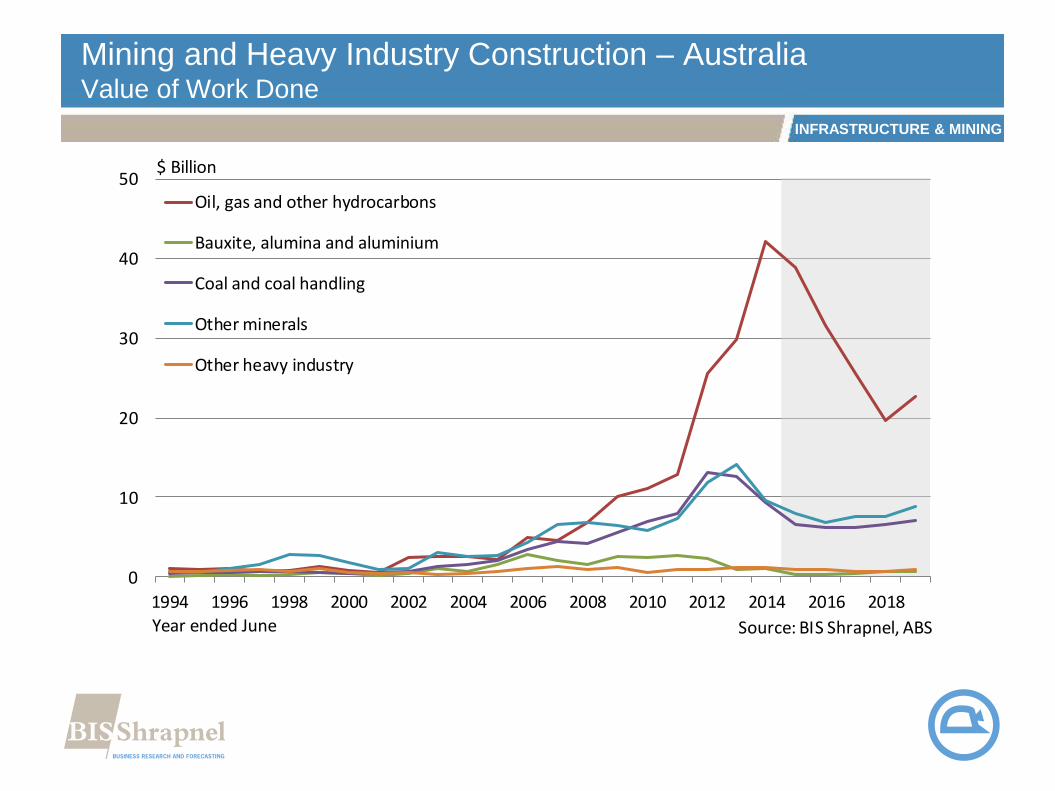

Mining and Heavy Industry Construction – AustraliaValue of Work Done

0

10

20

30

40

50

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Oil, gas and other hydrocarbons

Bauxite, alumina and aluminium

Coal and coal handling

Other minerals

Other heavy industry

Year ended June Source: BIS Shrapnel, ABS

$ Billion

INFRASTRUCTURE & MINING

Summary & Implications

Industry structure and investment cycles driving different outcomesDifferences in global and national outlooks

Differences by state, region, and construction segment

Weak domestic economic conditions persist before a recoveryStrong GDP figures masking weak growth in domestic demand

Unemployment will move higher / inflation not a problem / low interest rates

Private and public investment drivers in reverse …

… but this will change as broader re-investment comes through

Opportunities vary by sector and stateNSW will be the strongest performing state through next few years

Opportunities in housing, roads, tunnels, telecoms and parts of non-residential

Sustaining capital opportunities in CSG and mining – long term value

Similarly operations and maintenance growth prospects are strong

Further, smaller investment cycles ahead as economy rebalances

Businesses need effective plans to target the next wavesEconomy will muddle through next 12-18 months

Watch key risk factors – global demand and A$ trigger new investment

Look for opportunities by sector and region

Understand the differences to previous investment cycles