a.d.banker&company - amazon s3 · self-study study and test at ... recommended that jack leave...

TRANSCRIPT

Homeowners InsuranceA.D.Banker&Company

Since 1979, A.D.Banker&Company has provided high quality training to insurance and securities producers across the country. With options in all 50 states we are your one source for prelicensing and continuing education.

At A.D.Banker the Choice is Yours...

• Daily Reporting• Knowledgeable Customer Service• Relevant and Informative Topics• Experienced Instructors• State Required Training • Online or Printed Exams

www.adbanker.com 1.800.866.2468

AdjusterAnnuity SuitabilityCrop RiskEthicsFloodGeneral/BridgeHomeowners ValuationLife & HealthLTC PartnershipMedicareProperty & Casualty

Self-Study

Study and test at your own pace with a book or PDF

Classroom

Learn from the experience of other professionals

Webinar

Participate live from anywhere with internet access

Online Course

Engage interactively through interesting online courses

Once licensed, producers can meet their Continuing Education requirements in all states while meeting product-specific requirements.

Go to www.adbanker.com to see what is available in your area!

A.D.Banker&Company exam preparation and continuing education

Homeowners Insurance

Chapter 1 Introduction to the Homeowners Policy ............................................................ 1Fire Policy; Standard Fire Policy; Package Policies; Pricing; Deductibles; Agent’s Responsibility; Errors and Omissions Coverage; Summary; Review Questions

Chapter 2 Overview of the Homeowners Policy ............................................................... 10Definitions; Eligibility; Insuring Agreement; Perils, Hazards, and Causes of Loss; Basic, Broad, and Open Perils; Review Questions

Chapter 3 Sections I and II Coverages of the Homeowners Policy ................................. 20Section I – Property Coverages; Section II – Liability; Review Questions

Chapter 4 Homeowners Policy Forms ............................................................................... 31HO-1 - Basic Form; HO-2 – Broad Form; HO-3 – Special Form; HO-3 Loss Settlement; HO-5 – Comprehensive Form; HO-8 – Modified Coverage Form; HO-4 – Contents Broad Form; HO-6 – Unit-Owners Form; Homeowners Form Comparison of Typical Perils; Review Questions

Chapter 5 Homeowners Policy Property Coverages ........................................................ 41Additional Coverages; Section I – Property Exclusions; Section I – Conditions; Section I – Property Endorsements; Review Questions

Chapter 6 Liability Coverages E and F .............................................................................. 52Additional Coverages; Section II – Exclusions; Coverage E – Personal Liability Exclusions; Coverage F – Medical Payments to Others Exclusions; Section II – Conditions; Section I and II – Conditions; Business Endorsements; Umbrella Liability Coverage; Review Questions

Chapter 7 Underwriting and Claims ................................................................................... 61Underwriting; Claims; Claims Settlement – Property; Appraisal; Claim Settlement – Liability; Course Summary; Review Questions

Review Questions Answer Key ............................................................................................. 69

Table of Contents

i

Copyright 2013© A.D. Banker & Company®, L.L.C.

This course, seminar, or publication provides general information regarding the subject matter covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional service. If legal advice or other expert assistance is required, the services of a competent professional person should be sought. The publisher hereby expressly excludes all warranties.

0313

Florida Unauthorized Entities

An entity that is required to be licensed or registered with the Florida Office of Insurance Regulation but is operating without the proper authorization is identified as an unauthorized insurer. All persons have the responsibility of conducting reasonable research to ensure they are not writing policies or placing business with an unauthorized insurer. Any person who, directly or indirectly, aid or represent an unauthorized insurer can lose their licenses or face other disciplinary sanctions.

Please see section 626.901, Florida Statutes, to read the laws. Lack of careful screening can result in significant financial loss to Florida consumers due to unpaid claims and/or theft of premiums. Under Florida law, a person can be charged with a third-degree felony and also held liable for any unpaid claims and refund of premiums when representing an unauthorized insurer. It is the person’s responsibility to give fair and accurate information regarding the companies they represent.

ii

Chapter 1

Introduction to the Homeowners PolicyIt was 2:00 am when the Johnson family woke up to a loud lightning crack and then a crash. Jack and Marie Johnson raced to check on their two children, 17 year-old Mike and 12 year-old Mary. Everyone was fine but was shocked to find the roof had caved into the fourth unoccupied bedroom and the rain was drizzling into the room. After a quick check on the damage, Jack guessed it was caused by lightning that struck a tree in their backyard which then fell over onto the roof and crashed into the bedroom. He couldn’t tell if the lightning caused a roof fire so he called 911 for assistance from the fire department. The fire department arrived a few minutes later and found that yes, there were live embers in the roofing shingles and after putting out all remaining fire sparks, recommended that Jack leave the house and call his insurance company. Jack’s insurance agent, Tom Goodsense, told Jack to immediately call the 24-hour claims service line.

Homeowners insurance is a very important product for a large market. The homeowners policy is designed to protect the insured’s investment in the home and personal possessions.

Example: Jack and Marie found out that not only would the insurance company pay for their hotel room that night, but also for a damage restoration company to come out immediately to stop further damage by installing a temporary roof and removing the damaged materials. They also set up fans to dry out the water-soaked interior.

About two-thirds of housing units countrywide are owner-occupied and 25% of all property/casualty premiums are homeowners policy premiums. Net written premiums for homeowners exceed $60 billion. While over 90% of homeowners have insurance in place, only about two-thirds of those households have some sort of disaster-preparedness kit or plan. That doesn’t mean, however, that homeowners are adequately insured or prepared for a loss. In fact, almost 70% of homes in the U.S. are underinsured for insurance purposes, yet, for most policyholders, their home is their single most valuable property possession and their largest investment.

The chance that some of Agent Tom Goodsense’s homeowners insurance clients will have a claim is great, and all too often claimants have issues with the claim settlement and how the adjuster determines the coverage. Almost 6% of insureds have a claim each year. Like Jack and Marie, Tom’s clients will look to him for help, both before and after a claim, so it is important for Tom to understand what he is selling the insured and how to minimize potential for present and future conflicts and misunderstandings.

Fire PolicyHomeowners insurance has come a long way! In 1666 the Great Fire of London caused devastation to the city. In response to that devastation, the first insurance offices selling fire insurance were established in London. Fast forwarding to the 1800s in the United States, Jack’s ancestors were able to buy a fire insurance policy that combined the fire policy, the policy conditions, and proposals (later called endorsements). The policy was based on hazard classes which identified the likelihood of fire loss ranging from ‘not hazardous’, such as a building made of brick to ‘extra hazardous’, such as a building made of wood. The hazard classes also identified the type of property or the business conducted in the building ranging from ‘not hazardous’, such as coffee or household furniture to ‘extra hazardous’ such as commercial basket makers or a blacksmith. The cost of insurance was determined by these hazard classes. The difference in cost to the property owner could vary from $0.25 per $100 of insurance for the non-hazardous risk to $.90 per $100 of insurance for the most hazardous risk.

1

2 HOmeOwneRS InSURAnce

Standard Fire PolicyBy the early 1900s, however, insurance companies continued the practice of insuring both personal and commercial risks with their own individual fire policies. Lack of uniformity was a concern. Jack’s great-great-grandfather bought his first home in 1919 for his bride and insured it with the first 165 line Standard Fire Policy created in 1918 by a group of insurance experts and the New York legislature mandated it as the only fire policy to be sold. Other states followed New York’s lead, and uniformity was achieved. Over the next several decades, changes were made to update and clarify the standard fire policy.

The Standard Fire Policy included four parts:Part 1 was the Declarations which described the location of the property, the insured amount covered, and the name of the insured.

Part 2 was the Agreements which included the premium and the covered perils of fire, lightning, and removal.

Part 3 was the Conditions which described the circumstances for coverage and the duties of the insured and insurer.

Part 4 was the Exclusions which specified the loss perils that were not covered.

Package PoliciesUp until the mid-20th century, perils needed by the insured were provided by either an endorsement to the policy or through the issuance of a separate policy. But when Jack’s grandfather bought a home in 1957 for his growing family, he was able to insure his new home with a package insurance policy. In this new and innovative policy, developed around the mid-1950s, insurance companies combined coverages into one policy which included the Standard Fire Policy perils plus additional extended perils covering personal property and personal liability. Package or multi-line policies offer fewer coverage gaps and savings in premiums, thus eliminating multiple policies and making things easier for both the agent and the insured.

The parts of the packaged homeowners policy are:Insuring Agreement (AAIS: Agreement)DefinitionsSection I – Property Coverages (AAIS: Perils Insured Against – Coverages A,B,C,and D)

Coverage A – Dwelling Coverage B – Other Structures Coverage C – Personal PropertyCoverage D – Loss of Use

Section I – Perils Insured AgainstSection I – ExclusionsSection I – ConditionsSection II – Liability Coverages

Coverage E – Personal LiabilityCoverage F – Medical Payments to Others

Section II – ExclusionsSection II – Additional CoveragesSection II – ConditionsSections I and II - ConditionsEndorsements

A.D. Banker&company©

3ChAPTEr 1: INTrODUCTION TO ThE hOMEOwNErS POLICY

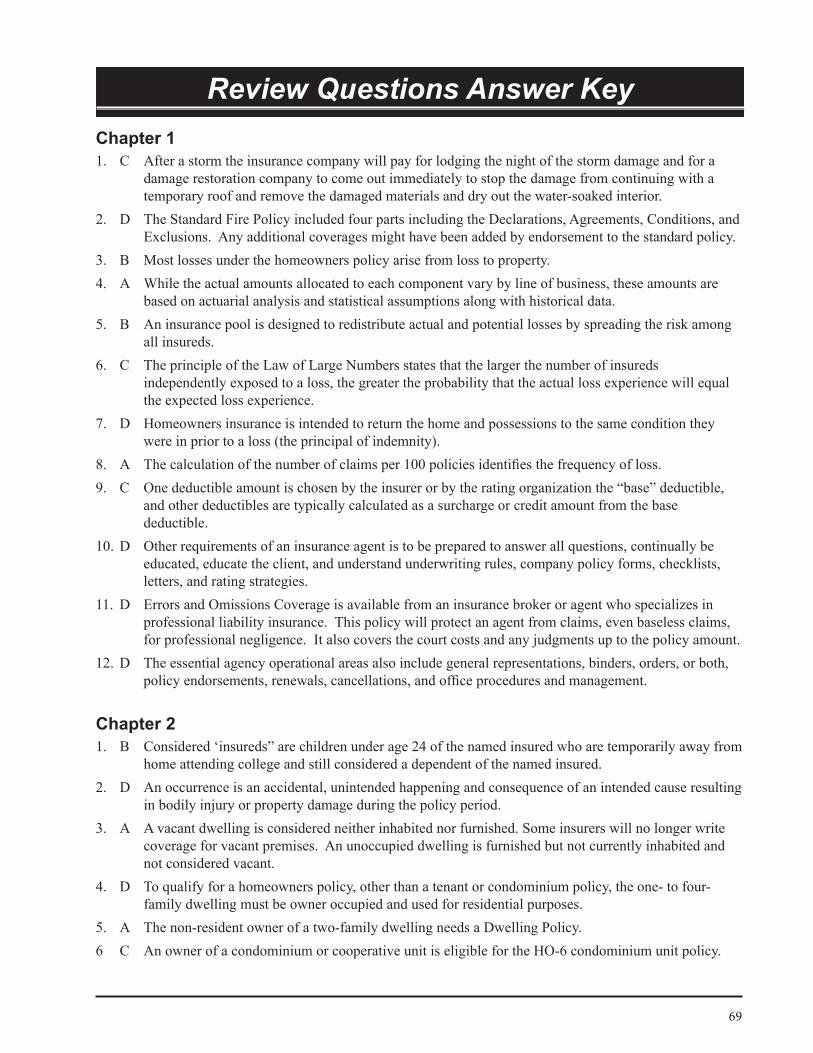

Most losses under the homeowners policy arise from loss to property. Approximately 95% of all incurred homeowners losses are property losses. While liability coverage is provided under the homeowners policy, homeowners coverage is a Property line. Like personal auto insurance, homeowners insurance is a personal lines product.

PricingLike those insurance experts in the 1600s, today’s insurance companies also have pricing strategies. Today, insurance companies calculate premiums using similar components for all property and casualty lines. They do not just “pull the premiums out of the air.” While the actual amounts allocated to each component vary by line of business, these amounts are based on actuarial analysis and assumptions along with historical data. Agents need to understand the basics of insurance pricing in order to be able to explain premium changes to their insureds.

The homeowners policy is a contractual financial agreement designed to redistribute actual and potential losses by spreading the risk among all insureds called an “insurance pool.” The pool maintains economic balance through actuarial analysis and ratemaking and assigns premiums based on the expected losses of the insureds in the pool. The larger the number of insureds independently exposed to a loss, the greater the probability that the actual loss experience will equal the expected loss experience. This principle is called the “ Law of Large Numbers.” This principle of actuarial science has seen numerous challenges, especially when natural disasters cause enormous losses in all lines of insurance. But, with sound statistical analysis, appropriate use of reinsurance opportunities, and sound fiscal management, the industry has been able to maintain a sound insurance infrastructure.

Homeowners insurance is based on the principal of “indemnity,” intending to return the home and possessions to the same condition they were in prior to a loss. There is to be no gain from a loss. In order to stay in business the insurance company must be successful in estimating the expected loss on a large scale and pricing the risks accordingly.

Following is a hypothetical chart representative of what the industry may target on an average basis. It demonstrates the allocation process using average amounts:

A.D. Banker&company©

4 HOmeOwneRS InSURAnce

how does the insurance company determine its profitability? In this example, a company looks at the prior year and determines the net earned premium:

Net premiums earned ($000) = $59,721,095

The company considers the components of underwriting as a percent of the earned premium. The dollars spent last year on the actual loss and the expenses for adjusting those claims determines the loss and loss adjustment expenses:

Incurred loss and loss adjustment expenses 62.0%

Total Loss and loss adjustment expenses 62.0%

Other expenses must be included. For example, commissions paid to agents and brokerage expenses must be considered. Other underwriting expenses, such as the cost of evaluating a new business application, are also included when determining the total expense of underwriting:

Commissions and brokerage expenses incurred 13.0%

Other underwriting expenses incurred 15.0%

Taxes 5.0%

Total underwriting expenses incurred 33.0%

Finally the dividends paid to policyholders and investment gains on income are included with the grand total of 104%:

Dividends to policyholders 9.0%

The percent of all the expenses adds up to 107% of the earned premium. In dollars, the net earned premium for last year was $59,721,095, but the expenses cost 104% of that, or $62,109,939.

Combined ratio after dividends 104.0%

Note that there was an underwriting loss of $2,388,844 as the combined ratio after dividends exceeds 100%. For every $1.00 received in earned premium, $1.04 was paid in losses and expenses. This company is not recognizing a profit and may need to consider raising premiums.

The “frequency,” or number of property damage claims per 100 policies, is 96% of all of the homeowners losses. The “severity,” or amount of property damage costs of incurred claims per accident year excluding loss adjustment expenses, is less than 65%. While there are more property damage claims, the liability claims excluding loss adjustment expenses are more expensive.

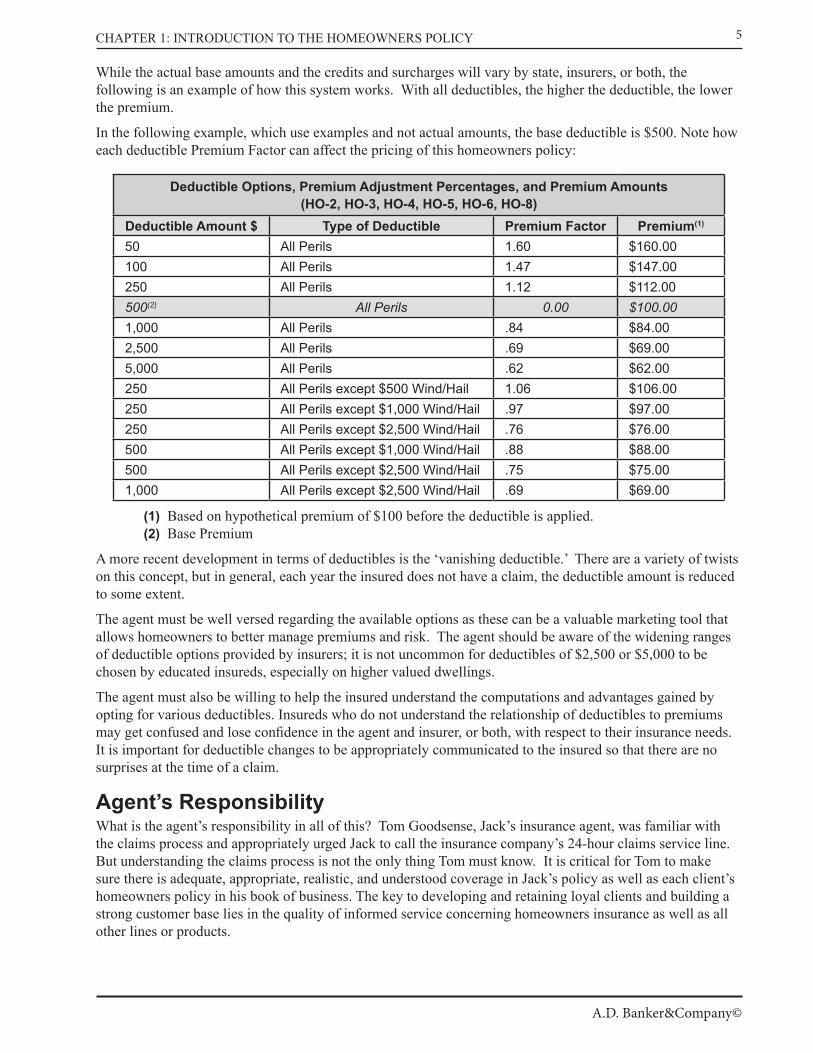

DeductiblesTo help meet a company’s actuarial goals and reduce the premium, insurers use deductibles as a tool to reduce the severity of losses. A deductible means that portion of the insured loss paid by the insured or reduced by the insurer in the final claims settlement. Deductibles only apply to the property section of the homeowners policy. These deductibles will vary by company and also depend on underwriting criteria. One deductible amount is chosen by the insurer or by the rating organization (e.g., ISO or AAIS) as the “base” deductible, and other deductibles are typically calculated as a surcharge or credit amount applied to the base deductible. Over the years, the base deductibles used by the various companies have risen as overall costs and inflation have risen.

A.D. Banker&company©

5ChAPTEr 1: INTrODUCTION TO ThE hOMEOwNErS POLICY

While the actual base amounts and the credits and surcharges will vary by state, insurers, or both, the following is an example of how this system works. With all deductibles, the higher the deductible, the lower the premium.

In the following example, which use examples and not actual amounts, the base deductible is $500. Note how each deductible Premium Factor can affect the pricing of this homeowners policy:

Deductible Options, Premium Adjustment Percentages, and Premium Amounts (HO-2, HO-3, HO-4, HO-5, HO-6, HO-8)

Deductible Amount $ Type of Deductible Premium Factor Premium(1)

50 All Perils 1.60 $160.00100 All Perils 1.47 $147.00250 All Perils 1.12 $112.00500(2) All Perils 0.00 $100.001,000 All Perils .84 $84.002,500 All Perils .69 $69.005,000 All Perils .62 $62.00250 All Perils except $500 Wind/Hail 1.06 $106.00250 All Perils except $1,000 Wind/Hail .97 $97.00250 All Perils except $2,500 Wind/Hail .76 $76.00500 All Perils except $1,000 Wind/Hail .88 $88.00500 All Perils except $2,500 Wind/Hail .75 $75.001,000 All Perils except $2,500 Wind/Hail .69 $69.00

(1) Based on hypothetical premium of $100 before the deductible is applied. (2) Base Premium

A more recent development in terms of deductibles is the ‘vanishing deductible.’ There are a variety of twists on this concept, but in general, each year the insured does not have a claim, the deductible amount is reduced to some extent.

The agent must be well versed regarding the available options as these can be a valuable marketing tool that allows homeowners to better manage premiums and risk. The agent should be aware of the widening ranges of deductible options provided by insurers; it is not uncommon for deductibles of $2,500 or $5,000 to be chosen by educated insureds, especially on higher valued dwellings.

The agent must also be willing to help the insured understand the computations and advantages gained by opting for various deductibles. Insureds who do not understand the relationship of deductibles to premiums may get confused and lose confidence in the agent and insurer, or both, with respect to their insurance needs. It is important for deductible changes to be appropriately communicated to the insured so that there are no surprises at the time of a claim.

Agent’s Responsibilitywhat is the agent’s responsibility in all of this? Tom Goodsense, Jack’s insurance agent, was familiar with the claims process and appropriately urged Jack to call the insurance company’s 24-hour claims service line. But understanding the claims process is not the only thing Tom must know. It is critical for Tom to make sure there is adequate, appropriate, realistic, and understood coverage in Jack’s policy as well as each client’s homeowners policy in his book of business. The key to developing and retaining loyal clients and building a strong customer base lies in the quality of informed service concerning homeowners insurance as well as all other lines or products.

A.D. Banker&company©

6 HOmeOwneRS InSURAnce

With homeowners insurance there is a wide array of high-dollar risks involved with property ownership. Tom’s approach must be to knowledgeably present to each “new client” a risk and coverage analysis and policy quote as well as to each of his renewal clients. Tailoring a policy to meet each client’s risk needs is a vital part of providing good service and building a lasting relationship, since shopping the Internet for insurance is a reality.

The professional agent must be familiar with insurance information from the State, the insurer, and the insured. State variances, regulations, and territory differences must be familiar to the agent. The agent must be educated about the insurer’s policies, procedures, underwriting rules, and options. Finally, the agent must be tuned into the individual needs and risks of the insured client. how can Tom meet all these expectations? He must:

• Be willing to “dig” to access necessary underwriting information

• Know how to ask the right questions

• Be prepared to answer all questions, and do so correctly

• Continually educate himself and the client or insured

• Have a strong working knowledge of:

◦ Underwriting rules ◦ State regulations (including what is required to renew an insurance license) ◦ Company policy forms ◦ rating strategies (including use of deductibles) ◦ Customer checklists ◦ Sample form letters ◦ Presentation aids ◦ Numerous other tools ◦ The competition

Errors and Omissions CoverageTom and his fellow agents understand how important it is to meet these expectations. But what happens if something goes wrong? what happens if an agent makes an error when submitting a homeowners application? Just like Jack’s need for coverage to protect his home, Tom needs coverage to protect his business and work product. Tom needs Errors and Omissions (E&O) Coverage and should contact an insurance broker or agent who specializes in professional liability insurance. This policy will protect him from claims, even baseless claims, for professional negligence. E&O coverage also covers the court costs and any judgments up to the policy amount.

Because agents need to give special attention to risk management that will help prevent errors and omissions allegations, Tom is adding to his list of “must do’s.” He must also be aware of proper procedures for essential agency operational areas such as:

• General and ethical representations

• Binders, orders, or both

• Expirations

• Policy endorsements, renewals, cancellations, and exclusions

• Office procedures and management

A.D. Banker&company©

7ChAPTEr 1: INTrODUCTION TO ThE hOMEOwNErS POLICY

SummaryThe homeowners policy provides financial protection for the named insured against various perils and disasters as described in the policy. Most policies contain features that allow the insured and agent to custom design acceptable coverage for each need or risk. The hO-3 form, or some version of it, is generally the most popular policy form in use today. It is estimated that over 84% of the hO policies in the United States are written on the hO-3 form. This course material is based on the hO 00 03 (05 11) policy form created by the Insurance Services Office, or ISO (1), and the hO 0003 (09 08) created by the American Association of Insurance Services, or AAIS (2)

(1) http://www.iso.com – ISO is a leading source of information about personal and commercial lines property and casualty insurance risk.

(2) http://www.aaisonline.com – AAIS is a national advisory organization that develops policy forms and rating information used by property/casualty insurers.

Please note the following:

• This course is intended to be a summary of important concepts and parts of the homeowners programs.

• where possible, the important AAIS deviations from the standard ISO will be noted in italics.

• Individual insurance companies often use their own forms, or ISO or AAIS forms with individualized company enhancements.

• The insurance agent must be educated about the individual policies, forms, and endorsements of the insurance companies that are represented and with those of the carriers with which he or she competes.

A.D. Banker&company©

Chapter 1 Review Questions

1. Immediately following a covered loss, an insurance company will pay for all of the following, EXCEPT:a. A hotel room for the nightb. Temporary roof repairsc. 5% of the total damaged. Company to dry out water damage

2. The 165 line Standard Fire Policy had each of the following parts, EXCEPT:a. Declarationsb. Exclusionsc. Conditionsd. Endorsements

3. which of the following losses is the most common loss claimed under a homeowners policy?a. Liabilityb. Propertyc. Lost wagesd. Personal property

4. The actual premium of an insurance policy can vary by line of business and is not based on which of the following?a. Stock market trendsb. Actuarial analysisc. Statistical assumptionsd. Historical data

5. which of the following is designed to redistribute actual and potential losses by spreading the risk?a. Actuarial distributionb. Insurance poolc. Underwriting loss ratiod. Insurance contract

6. The more insureds there are in a group, the greater the likelihood is that the insurance company can predict the loss experience. This principle is called the:a. Law of Actuarial Integrityb. Insurance Relativityc. Law of Large Numbersd. Principle of Indemnity

7. Homeowners insurance is intended to put a person back in the same position he was prior to a loss. which of the following does this describe?a. Law of Actuarial Integrityb. Insurance Relativityc. Law of Large Numbersd. Principle of Indemnity

8

9

8. which of the following calculations calculate frequency?a. Claims per 100 policiesb. Claims times the severityc. Claims per 1,000 policiesd. Severity divided by the number of claims

9. which of the following is the premium factor of the base deductible?a. $100b. $1,000c. $0d. $50

10. A homeowners insurance agent must be able to do all of the following, EXCEPT:a. Know how to ask the right questionsb. Be aware of the state insurance regulationsc. Know the competitiond. Assist the claims representative

11. which of the following does an agent need for protection from a lawsuit filed by an angry client for negligence in selling an insurance policy?a. Professional Liability endorsement to the homeowners policyb. Homeowner Agent Protectionc. Agent Liability Coveraged. Errors and Omissions Coverage

12. The essential agency operational areas include all of the following, EXCEPT:a. Ethical representationsb. Expirationsc. Exclusionsc. Eligibility

ChAPTEr 1 rEvIEw QUESTIONS

A.D. Banker&company©

Chapter 2

Overview of the Homeowners PolicyDefinitionsThere are important terms that must be defined in order to understand their meaning and importance to homeowners insurance. The following words are found in the Definitions section of the policy. As is the case with most insurance policies, there are numerous words defined in the policy in order to clarify coverage.

Named InsuredThe homeowners policy defines the “named insured” as that person shown on the Declarations page. The spouse of the named insured, if a resident in the same household, is also a “named insured.”

Example: John and Marie are married and live together in a home they purchased ten years ago and insure the home with A+ Insurance. While John is listed as the only Named Insured on the policy, Marie is also a named insured, with all the named insured policy rights, because she is a resident spouse. Bill lives next door to John and also insures his home with A+ on which he is the Named Insured. Bill and Julie, his wife, co-own the home. Bill and Julie are separated and Julie moved out a month ago. Is Julie a named insured on the policy?

Answer: Although Julie is still married to John and on the title to the home, she is no longer a named insured since she no longer resides in the insured home.

InsuredThe homeowners policy specifically defines the meaning of “insured” to include the following:

• The named insured.

• Relatives residing in the same household as the named insured are also covered, such as children or caretakers.

• Considered ‘insureds” are children under age 24 of the named insured who are temporarily away from home attending college and still considered a dependent of the named insured. This also includes children under the age of 21 in the care of the named insured or household resident relative temporarily at school.

• Other persons under the age of 21 and in the care of the named insured or resident relative are also covered under the policy. Examples could be foster children, foreign exchange students, or wards of the court.

• Persons responsible for the named insured’s animals or watercraft would be covered unless they are in the business of doing so or are doing so without the named insured’s consent.

• Anyone hired by the named insured to operate a covered vehicle for the maintenance of the premises and who does so with the named insured’s consent would be an insured under the policy.

Example: Harry and Mary own an insured home in Ohio. Their 21-year-old son, Barry, is a freshman at college in New York. For the two years prior to attending college in New York, Barry supported himself working in New York where he shared an apartment with several others. He still works part-

10

11ChAPTEr 2: OvErvIEw OF ThE hOMEOwNErS POLICY

time to support himself. Last night, Barry found that a number of items including his laptop and TV were missing from his apartment, and he reported the theft to the police. The next day Harry calls his agent, to report the loss. Will Barry’s stolen items be covered under Harry’s policy?

Answer: Barry is not an insured under the policy as he is no longer a dependent of Harry and Mary. He is supporting himself and moved out of his parent’s home prior to attending college.

Insured Location Insured location is defined in the homeowners policy as the residence premises shown in the Declarations. This includes other premises used in connection with a covered premise, other structures and grounds used by the named insured as a residence shown on the Declaration or acquired during the policy period by the named insured to be used as a residence.

Also included as insured locations are non-owned premises where the insured is temporarily residing, vacant land owned by the insured and not used for farming, land owned by or rented to an insured where a one- to four-family dwelling is being built as a residence, and any part of a premise occasionally rented to an insured for other-than-business use.

Cemetery plots, markers, and vaults are included in most insurers’ provisions up to limits stated in the policy.

Occurrence An occurrence is an accidental, unintended happening. It is also an unintended consequence of an intended cause, including continuous and repeated exposure to substantially the same harmful conditions that result in bodily injury or property damage during the policy period.

Residence Employees Employees of an insured or employees leased to an insured by an agreement with a labor leasing firm, whose duties are related to the maintenance or use of the residence premises or other insured locations, are considered residence employees. These household or domestic employees of the insureds are covered on the residence premises or elsewhere while acting within the scope of their duties as long as those duties do not relate to an off-premises business of the insured.

Example: The insured has a woman clean her house on a weekly basis. The woman uses the insured’s tools and cleaning supplies and cleans under the supervision of the insured. The woman cleans houses for others as well. On her way home from her weekly cleaning for the insured, she stops at the grocery store and on her way out of the store; her phone and her purse containing $150 are stolen. Are the stolen goods covered under the insured’s policy?

Answer: She is on her way home and no longer performing duties for the insured and therefore not considered a residence employee.

Residence PremisesThe residence premise is shown on the Declarations page and is the one-family dwelling in which the named insured resides, or the two-, three-, or four-family dwelling in which the named insured resides in one unit. It includes other structures and grounds at the location of the residence premises, e.g., a free-standing garage or shed on the property where the residence is located. The residence premise is also that part of any other building where the named insured resides.

An unoccupied dwelling is furnished, but not currently inhabited, and not considered vacant. A vacant dwelling doesn’t contain enough personal property to support occupancy as a residence. Some insurers will no longer write coverage for vacant premises.

Example: Jack and Marie owned a vacation home on a lake not far from their home. They spent many weekends enjoying the lake. During that time the vacation home was fully furnished with the

A.D. Banker&company©

12 HOmeOwneRS InSURAnce

Johnson’s furnishings and some of their clothes. Is this dwelling, while the Johnson’s were back in their primary residence, considered vacant?

Answer: No, it was uninhabited when the family was back in the city, but because it was still furnished, it was not vacant and subject to the vacancy restrictions in the homeowners policy.

Example: Jack and Marie decided to sell the vacation home. They moved everything back to a storage facility in the city. Is the home vacant?

Answer: Yes, since it is now uninhabited and not furnished, it is considered vacant.

There are many other definitions in the policy, both in the Definitions section and throughout other sections as well. remember that a definition in an insurance policy not only defines the meaning of the word, but it also helps explain what is and is not covered.

EligibilityTo qualify for a homeowners policy, other than a tenant or condominium policy, the one- to four-family dwelling must be owner occupied and used for residential purposes. Owner-occupied means that the property or residential premises must be occupied by the named insured who is an owner of the dwelling. A one-family dwelling may not be occupied by more than one additional family or two roomers or boarders. A two-, three-, or four-family dwelling may not be occupied by more than two families, or one family with two roomers or boarders. (The AAIS program allows one- to four-family dwellings used principally for private residential purposes, and each family may be occupied by a maximum of one family with no more than two boarders or roomers, or two families with no boarders or roomers.)

Both programs insure two-, three-, or four-family dwellings in which each co-owner occupies a separate living quarter with a separate entrance. Both interests are covered by insuring co-owner #1 as the named insured with dwelling and dwelling liability coverage on a homeowners policy and coverage on #1’s personal property and personal liability. Co-owner #2 will be listed as an Additional Insured on #1’s homeowners policy giving #2 dwelling and dwelling liability coverage. #2 will be covered for personal property and liability on a tenant homeowners policy.

while obtaining a mortgage is a common method of financing a home, there are other options that will impact the homeowners policy differently. The mortgagee is covered by a mortgage clause. However, it is also possible to purchase a home on a long-term installment or lease basis, or land contract, in which the seller maintains title to the home until the terms are met. The seller’s interest is covered by the Additional Insured endorsement providing dwelling and premises liability coverage. (AAIS rules the approval of this situation is at the option of the company.)

A dwelling under construction that is intended for private residential used by the owner-occupants is eligible for the homeowners policy.

Two situations involving legal ownership are also eligible for coverage under the homeowners policy. The first is the life estate arrangement in which an individual’s interest in the dwelling is limited to the individual’s life.

Example: Under a life estate arrangement Jack left his home to his sister, Jan, for her lifetime. Upon her passing the home will revert to Jack’s children. As soon as she occupies the home, Jan becomes the named insured on the homeowners policy and the owner’s interest is covered by the Additional Insured endorsement.

The second is a property held in trust. ISO lists the trust as the named insured with a trust endorsement and the intended occupant is the trustee who is covered for the “business use” of administering the trust and the bodily injury and property damage arising out of the ownership, maintenance, or use of the residence premises. (AAIS has two additional insured endorsements and limits the liability coverage to incidents arising out of the insured premises.)

A.D. Banker&company©

13ChAPTEr 2: OvErvIEw OF ThE hOMEOwNErS POLICY

Often seasonal or secondary residences may be issued on separate policies dependent on the insurer’s underwriting criteria or due to agent licensing issues. Generally, a seasonal residence located in or out of the same state as the primary residence can be covered by a separate homeowners policy. If within the same state as the primary, and covered by the same insurer, the seasonal home can be covered by just Section I coverage, and extend the Section II liability coverage from the primary. (AAIS covers both the primary and seasonal, if both are within the same state, by endorsing the seasonal onto the primary policy. Otherwise, a separate policy must be issued.)

Incidental farming on the premises is acceptable when insuring a dwelling with a homeowners policy as long as the primary use of the property is residential. Endorsements are available for a farm property away from the residence premises if farming is not the insured’s primary occupation.

An owner of a condominium or cooperative unit is eligible for the hO 00 06 policy (AAIS HO 0006). This policy is primarily used to cover a residence in which no more than one additional family or two boarders or roomers reside. Because the interior of the unit is real property, the policy provides coverage for building property and other structures under Coverage A - Dwelling; no Coverage B is provided. Units held in trust are eligible for coverage.

If the dwelling is rented to a tenant, the insured owner would have to add an endorsement, i.e., ISO’s hO 17 33 (05 11), or purchase a Dwelling Property Policy instead of a homeowners policy, such as:

• Basic Form (DP-1)

• Broad Form (DP-2)

• Special Form (DP-3)

The tenant, however, may obtain a Contents Broad Form policy, hO-4. Like the other homeowners policies, one additional family or two boarders or roomers are allowed. The tenant or renter can occupy an apartment, single family dwelling, or mobile home. Owner-occupants of structures that do not qualify for other homeowner policies can obtain personal property and liability coverage under this policy; however, no building coverage is provided.

The use of the residence premises under any form of coverage must be residential, not commercial or business. Any commercial or business activities on the premises must be incidental and conducted only by the homeowner. The premises must be occupied primarily as a residence. Examples of eligible home-based businesses include professional or business offices and private schools in music, dance, or photography. Home day care operations are not eligible unless endorsed.

The policy must be endorsed to extend liability and property coverage to the incidental occupancy; when endorsed, only premises liability coverage is provided. Any limitation on business personal property under Coverage C is removed. Since a permitted incidental occupancy may be located in the dwelling or a detached structure, endorsements are available to extend coverage accordingly.

Insuring AgreementThe ISO homeowners policy insuring agreement is very simple. The insurance company provides the insurance described in the policy in return for the premium and compliance with all policy provisions.

This agreement is a classic example of a contract of adhesion. The contract is developed by the insurer in its entirety, and the insured must accept it as is.

Perils, Hazards, and Causes of lossA “peril” is the cause of a loss. The homeowners policy may cover “named perils,” which means the specific perils covered by the policy are listed in the policy. Other policies do not specifically define the covered perils and are known as open perils policies, which cover losses caused by any peril except those specifically excluded in the policy. The open perils policy usually generates a higher premium than a named perils policy does and provides correspondingly broader and more extensive coverage.

A.D. Banker&company©

14 HOmeOwneRS InSURAnce

The open perils policy is the most popular policy. In the ISO homeowners program, the hO-3 provides building coverage on an open perils basis and personal property coverage on a named perils basis.

The policies that define coverage by listing the named perils will sometimes include definitions of the peril. For example, the “aircraft” peril includes coverage for self-propelled missiles and spacecraft.

Other perils are not defined, such as “fire,” “lightning,” or “riot or civil commotion.” So how does an insured determine whether the loss is covered? Common law has long described, and continues to describe, the terms not specifically defined in the policy, such as fire. “Common law” means unwritten law developed primarily from judicial decisions which are based on customs or previous case decisions (i.e. precedent).

Fire is a good example of how common law defines a peril. There are two types of fire: hostile and friendly. “Friendly fire” means a fire that is contained in its intended location. “Hostile fire” means fire that burns somewhere it wasn’t intended to burn.

Example: An example of a friendly fire is a fire within a fireplace. A burning log that accidently rolls out of the fireplace and burns the family room rug is now a hostile fire because it is burning outside its intended boundaries.

A “cause of loss” is also referred to as a peril insured against. While the smoke from agricultural smudging is a peril, it is not a “cause of loss” because it is not a peril insured against. The policy will not cover damage caused by agricultural smudging.

A “hazard” is an increase in the probability that a loss will occur. having an open fireplace without a fireplace screen is a hazard. The lack of a screen increases the probability that a fire loss will occur.

Example: Consider a cracked sidewalk, a pile of oily rags, or a broken hand rail on a stairway. Are these hazards?

Answer: Yes, these types of hazards are called “physical” hazards.

There are three types of hazards:

1. A “physical” hazard is the use, condition, or occupancy of property, such as the fireplace or handrail used in the previous examples.

2. A “moral” hazard is the characteristics and behaviors of people, such as the tendency of a dishonest person to steal; such characteristics and traits increase the chance of a loss.

3. A “morale” hazard is the state of mind or attitude of a person that increases the chance of loss. The person doesn’t worry about a potential loss and may take fewer precautions.

Example: Jack’s neighbor, Jim, left his keys under the welcome mat and paid someone to steal his old TV—is this a moral hazard?

Answer: This moral hazard increased the likelihood of a theft claim.

Example: Jack doesn’t lock his front door when he leaves for work in the morning—is this a morale hazard?

Answer: This morale hazard increases the chance of a theft or vandalism claim.

In a named perils policy, it is incumbent upon the insured to prove the peril that caused the loss or damage. In an open perils policy, the insurer must prove that an exclusion applies. The following perils are considered “named perils” and insure property included in the hO-2, hO-4, hO-6, and the personal property section of the hO-3 policies:

Fire Direct physical damage caused by fire includes flame, smoke, soot, excessive heat, and scorching. It also includes direct damage caused by firefighters while putting out a fire. Indirect losses, such as a hole in the roof or water damage that are caused by the firefighters are also covered. Only damage caused by a hostile fire is covered.

A.D. Banker&company©

15ChAPTEr 2: OvErvIEw OF ThE hOMEOwNErS POLICY

LightningAs a phenomenon of weather, lightning is naturally generated electricity from the atmosphere. The policy covers damage caused directly by lightning and from the fire caused by lightning.

Windstorm or HailWindstorm is the natural movement of air and can range from a strong gust of wind that causes a tree to fall and damage Jack’s roof to a tornado or Category 5 hurricane that can destroy a home. Some policies include wind exclusions that limit coverage for damage caused by wind. Hail is frozen precipitation and can range from very small pea-sized pellets to large, grapefruit-sized chunks of ice.

ExplosionExplosion is not defined in the policy, so the interpretation can be broad. One definition that has evolved from common law is that explosion is a sudden, accidental, and violent bursting usually accompanied by a large noise.

Riot or Civil CommotionA riot is a violent public disorder or disturbance of the peace by 3 or more persons with a common intent to execute a violent and turbulent political act or to terrorize people. An act by one person throwing bricks is not a riot; it is an act of vandalism. A civil commotion involves more people and is more serious, such as a prolonged disturbance or one that is highly violent in nature.

AircraftAircraft are self-propelled vehicles capable of flight, such as helicopters and airplanes. The policy specifically includes self-propelled missiles and spacecraft. There is no requirement of direct physical contact between the aircraft and the damaged property. A sonic boom can cause direct physical damage by shattering windows. The policy also covers property damage from a motorized model or hobby aircraft.

VehiclesDefined by common law in some jurisdictions to be damage caused by a self-propelled conveyance with wheels, this peril is defined by others as the peril of vehicle collision. Some forms include restricted definitions and exclusions.

SmokeThis peril is defined as the “sudden and accidental damage from smoke, including the emission or puffback of smoke, soot, fumes, or vapors from a boiler, furnace, or related equipment.” The definition continues to describe perils that are not considered “smoke,” such as that caused by smoke from agricultural smudging or industrial operations. Essentially, smoke is particles in the air that are emitted from a burning substance.

Vandalism and Malicious MischiefVandalism is the intentional destruction or ruination of another person’s property. Malicious mischief adds the hateful component to the intentional, negligent, and unprovoked damage to, or destruction of, another person’s property.

A.D. Banker&company©

16 HOmeOwneRS InSURAnce

TheftTheft is the unlawful taking of personal property with intent to deprive the rightful owner of it. Theft includes damage caused by attempted theft and loss of property from a known place when it is likely that the property has been stolen. The peril of theft does not insure theft committed by an insured or from that part of the residence premises that is rented to others. Property such as trailers, campers, and watercraft, when away from the residence premises, is not covered. Also not covered is theft of property at another residence owned by, rented to, or occupied by the insured when the insured is not living there. The property of an insured who is away at school is not covered for theft unless the student was on the premises where the theft occurred during the 90 days immediately before the loss.

Falling ObjectsThe falling object is not covered, but the damage it causes is covered, except when the property is contained within the dwelling and the roof or outside wall has not been damaged. If an insured drops something within the dwelling and causes damage, there is no coverage. If something falls from outside and damages the roof or outside wall before damaging property inside the dwelling, there is coverage.

Weight of Ice, Snow, or Sleet This peril is covered when the weight causes damage to a building or property contained in a building.

Accidental Discharge or Overflow of Water or SteamThe discharge or overflow must occur within a plumbing, heating, air conditioning, or automatic fire protective sprinkler system, or from within a household appliance. The system or appliance itself is not covered. Loss caused by freezing is not covered under this peril. Damage occurring on the residence premises that was caused by discharge or overflow originating off the premises is excluded. Any loss caused by mold, fungus, or wet rot is excluded unless it is hidden within the walls or ceilings, beneath the floors, or above the ceilings. A sump pump or related equipment, roof drain, gutter, downspout or similar equipment are not considered covered systems or appliances.

Sudden & Accidental Tearing Apart, Cracking, Burning, or BulgingExcept for freezing, this plumbing and heating peril covers steam or hot water heating systems, air conditioning or automatic fire protective sprinkler systems, and appliances used for heating that suddenly and accidently tear apart, crack, burs, or bulge.

Freezing Freezing of a plumbing, heating, air conditioning, automatic fire protective sprinkler system, or household appliance is covered under this peril. There is no coverage if the insured fails to maintain heat in the building or shut off and drain systems and appliances of water.

Sudden and Accidental Damage from Artificially Generated Electrical CurrentArtificially generated damage means any electrical current other than naturally generated electrical charges. Examples of naturally occurring current include lightning or static electricity and an example of artificially generated electrical current is a power surge. Not covered under this peril is loss to tubes, transistors, electronic components or circuitry that are part of appliances, fixtures, computers, home entertainment units or other types of electronic apparatus.

A.D. Banker&company©

17ChAPTEr 2: OvErvIEw OF ThE hOMEOwNErS POLICY

Volcanic EruptionThis peril eliminates any confusion as to whether the damage caused by an erupting volcano is covered under the explosion peril. Damage from the violent discharge of steam and volcanic material—including airborne shock waves, volcanic ash, and lava flow—are covered. If structural damage occurs as a result of this covered peril, the debris removal is also covered. Aftershocks that occur within 72-hours after the initial eruption are covered as part of the same volcanic eruption, thus allowing for the submission of a single claim and application of one deductible. Damage from earth movement, earthquake, land shock waves, or tremors is not covered.

Sinkhole CollapseAAIS includes sinkhole collapse as a named peril. Sinkhole collapse results from subterranean voids created by the action of water on a limestone or similar rock formation. The dwelling and other structures only are covered. Not covered is the cost of filling the sinkhole or the value of the land.)

Basic, Broad, and Open Perils

A.D. Banker&company©

Chapter 2 Review Questions

1. which of the following is NOT considered an insured under the homeowners policy?a. Person responsible for the named insured’s animalsb. A son, age 26, who is a student away at college, but still living with his parents during the summer.c. 16 year old foster child under the care of the insured’s aunt who lives with the insured. d. A gardener who uses the insured’s pick-up truck to pick up landscaping supplies.

2. An accidental, unintended happening is called a(n) __________________a. Bodily injuryb. Accidentc. Incidentd. Occurrence

3. If a dwelling is neither inhabited nor furnished, it is considered:a. Vacant b. Unoccupiedc. Rentald. Seasonal

4. what is the maximum number of family units in one dwelling that qualifies for a homeowners policy?a. 1b. 2c. 3d. 4

5. Which of the following would not qualify for the Additional Insured endorsement to the homeowners policy?a. The interest of the non-resident owner of a two-family building b. One of two co-owners, where each resides in respective units in a two-family dwellingc. A person selling a home under a land contractd. Home owner creates a life estate arrangement

6. An owner of a condominium or cooperative unit is eligible for which homeowners policy?a. hO-1b. hO-4c. hO-6d. hO-8

7. The peril of fire is not defined in the policy. what determines the definition of “fire” during the claim investigation?a. Fire departmentb. Common Lawc. Claim Adjusterd. Civil Law

18

19

8. A(n) ___________ fire is one that burns where it is not supposed to burn.a. Friendlyb. Fireplacec. Hostiled. Unfriendly

9. which of the following is a morale hazard?a. A dishonest actb. Cracked sidewalkc. An irresponsible persond. A person that takes few precautions

10. which of the following losses is an indirect loss?a. hole in the roof caused by a fireman’s hoseb. Soot created within a chimneyc. Excessive heat causing a flamed. Fire inside a fireplace

11. A loss is covered in which of the following theft situations?a. A theft loss to property in a rented room.b. Damage caused during an attempted theft loss.c. Theft of property from the insured’s summer home while the insured is fishing on the lake.d. Theft of a camper at a campground.

12. The peril of weight of snow, ice, and sleet covers which of the following?a. Fence surrounding the insured’s premisesb. Swimming poolc. House foundationd. Property contained in a building

ChAPTEr 2 rEvIEw QUESTIONS

A.D. Banker&company©

Chapter 3

Sections I and II Coverages of the Homeowners Policy

In this chapter, we will look at the sections of the homeowners policy and its coverages as well as its exclusions. Once we understand how each coverage works, we will put them together in the policy forms.

The coverages in the homeowners policy are:

• Section I – Property Coverages

◦ Coverage A – Dwelling (AAIS: Residence) ◦ Coverage B – Other Structures (AAIS: Related Private Structures) ◦ Coverage C – Personal Property ◦ Coverage D – Loss of Use (AAIS: Additional Living Costs and Loss of Rents)

• Section II – Liability Coverages

◦ Coverage A – Dwelling (AAIS: Residence) ◦ Coverage B – Other Structures (AAIS: Related Private Structures) ◦ Coverage C – Personal Property ◦ Coverage D – Loss of Use (AAIS: Additional Living Costs and Loss of Rents)

Section I – Property CoveragesCoverage A – Dwelling Professional agents perform their jobs best when working with informed clients who have been provided with enough coverage to protect them adequately when disaster strikes. The agent must advise the client to purchase enough insurance to pay for the costs of rebuilding or replacing insured dwellings and attached structures. If the client fails to purchase adequate insurance, he or she will be underinsured at the time of a loss. Coverage A insures the dwelling, attached structures and fixtures, and materials and supplies located either on or next to the residence premises that are intended for use in the construction, alteration, or repair of the dwelling or other structure on the premises. The Section I deductible applies to Coverage A.

It is important to note the word “attached.” Examples of attached building items that are insured under Coverage A include built-in cabinets, appliances, plumbing, heating, and permanently installed air-conditioning systems, electrical wiring, wall-to-wall carpeting, and fences if they are attached directly to the dwelling. If a building is attached to the main dwelling, whether by wall or by roof, that building is considered part of the dwelling. For example, garages and car ports are covered if they share a wall or the roof line with the dwelling.

If the structure is not attached, and there is a clear separation between the dwelling and the structure, the structure is insured under coverage, Coverage B - Other Structures.

20

21ChAPTEr 3: SECTIONS I AND II COvErAGES OF ThE hOMEOwNErS POLICY

Example: Jack’s brother-in-law tells you he has a guest house. After further questioning, you learn there is a walkway between the guest house and the main house. However, the walkway is really a breezeway and it connects to the main house by a common roof. Is the guest house considered part of the dwelling and covered under Coverage A?

Answer: Yes, since the guest house is connected by the roof to the main house, it is part of the dwelling and covered under Coverage A – Dwelling.

Coverage A is intended to indemnify the insured for the costs to repair or replace damaged property if the home is damaged by fire, hail, lightning, or other covered perils.

Coverage A provides no coverage for the following:

LandLand is not covered because, even if damaged, does not depreciate or lose value. However, liability claims arising from the premises, lot, or land are covered.

Flood Flood coverage can be obtained by the purchase of a separate policy from the National Flood Insurance Program or a private insurer. Agents should advise all applicants and clients that all homeowners policies specifically exclude loss or damage caused by flood.

EarthquakeEarthquake coverage can sometimes be added by an endorsement to the policy; however, in most states subject to significant earthquake exposure, the earthquake risk must be covered under a separate policy.

Routine wear and tear, maintenance and neglectMaintenance-related problems, normal wear and tear, and the insured’s failure to care for property are the homeowner’s responsibility. Claims that arise out of these situations may be difficult to handle as the insured might be considered a morale hazard.

Coverage B – Other StructuresCoverage B provides coverage for detached structures on the residence premises that are separated from the dwelling by clear space. Examples include garages, sheds, gazebos, and swimming pools. Other structures also include fixtures only attached to land, such as fences, driveways, patios, sidewalks, ornamental rock gardens, and retaining walls. While clear space is an indicator of Coverage B, other structures connected by a fence, utility line, or similar connection are also covered.

The amount of insurance automatically provided for Coverage B is 10% of the Coverage A limit; it applies to all of the insured’s other structures. Use of Coverage B does not reduce the limit applying to Coverage A. Coverage B can be increased if the value of all the other structures on the residence premises exceed 10% of the Coverage A limit. The policy deductible applies to losses under this coverage.

Coverage B will indemnify the insured for the costs to repair or replace the other structures if damaged by fire, hail, lightning, or other covered perils.

Coverage B provides no coverage for the following:

LandLike Coverage A, land is not covered.

A.D. Banker&company©

22 HOmeOwneRS InSURAnce

BusinessDetached structures used primarily for business purposes are not covered and need to be covered by a separate, commercial or business owner’s type of policy. Detached structures from which business is conducted on an incidental and an approved basis are not covered unless an endorsement is added to the policy.

RentalOther structures rented or held for rental to any person other than a tenant of the dwelling are not covered. The exception is rental of a private garage for garaging purposes. An endorsement is available to remove this exclusion if another structure is rented for residential dwelling purposes.

Business StorageOther structures used to store “business” property are not covered. The exception is “business” property including gas or liquids other than a vehicle fuel tank, that is solely owned by the insured or a tenant of the dwelling.

Clearly, underinsuring or improperly insuring other structures will cause problems. The agent and the insured must take steps in advance to avoid such situations.

Example: Jack’s dwelling is insured for $400,000 under Coverage A. He also has a variety of other structures on the residence premises. Recently, a large brush fire occurred in the area, and it destroyed a small barn and damaged an attached garage on the property. Jack’s pool also sustained significant damage from the fire and the pool’s pump, heater, and a solar heating system were also damaged.

The replacement and repair costs were as follows:

Barn – $30,000

Garage – $25,000

Pool repair and cleanup – $5,000

Pool pump, heater, and solar system – $15,000

Ignoring the deductible, how much could Jack collect from his insurance company for this loss? (Assume no other unusual circumstances or losses.)

Answer: The garage was attached, so the $25,000 cost to replace the damaged portion was fully covered under Coverage A. If the insured had the standard 10% of Coverage A applicable to Coverage B, then there was a total of $40,000 available to pay claims. However, the total of all losses to other structures was $50,000 ($30,000 for the barn, $5,000 for the pool repair, and $15,000 for the pool and related equipment). The insured could only collect $40,000, thus there was a $10,000 shortage.

Coverage C – Personal Property Coverage C, often referred to as Contents Coverage, applies to personal property owned or used by the insured while it is anywhere in the world. Personal property of guests and residence employees, while on the residence premises, is also covered if the named insured elects it to be covered after a loss. Examples of covered personal property include furniture, clothing, linens, televisions, audio equipment, dishes, and other personal items owned by the insured, the insured’s family members who live in the residence premises, and others who are defined as an “insured” under the policy.

The standard amount of insurance under Coverage C is 50% of Coverage A. However, many insurers have increased those limits to 70% or 80% of Coverage A. The policy deductible applies to losses under this coverage.

A.D. Banker&company©

23ChAPTEr 3: SECTIONS I AND II COvErAGES OF ThE hOMEOwNErS POLICY

The policy limits coverage for certain types of property and excludes coverage for other types of property:

Other ResidencesThe limit for personal property usually located at an insured’s residence other than the residence premises is 10% of Coverage C, or $1,000, whichever is greater. If the insured has moved out of the residence due to repairs, renovations, or rebuilding, this 10% limit does NOT apply. Also, in a newly acquired principal residence, the limit does not apply for 30 days from the time the property began to be moved.

Self-storage FacilitiesThe limit for personal property owned or used by an insured and located in a self-storage facility is 10% of Coverage C, or $1,000, whichever is greater. If the insured has moved out of the residence due to repairs, renovations, or rebuilding, this limit doesn’t apply. The limit also does not apply if the property is usually located in an insured’s residence other than the residence premises.

Special Limits for Certain Classes of Personal PropertyMany insurers establish special limits of liability for certain types of personal property. These limits do not increase the total limit of liability for Coverage C; instead, they set maximum limits for certain higher risk items insured by the homeowners policy.

If the insured believes the standard policy form does not adequately insure the value of these items, the agent should advise the insured to consider separate coverage. Such separate coverage can be purchased in the form of a separate policy, often referred to as inland marine coverage or personal property floaters, or coverage may be added by adding the Scheduled Personal Property endorsement to the homeowners policy. Using any of the methods, separate coverage will provide much broader protection than the unendorsed homeowners policy does. Most inland marine and personal property floaters do not contain a deductible.

Special limits of liability usually apply to the following classes of personal property:

• Money

• Coin and stamp collections

• Jewelry

• Guns

• Furs and fur garments

• Silverware

• Portable electronic equipment

• Camera equipment

• Musical instruments

• Golfer’s equipment

• Antiques

• Collectible items

The special limits vary depending upon the type of property, where it’s located at the time of loss, and the insurer’s guidelines. The limit per class of personal property is usually the total limit per occurrence for all property in the specific class (e.g., jewelry). Some classes of property require a deductible; others don’t. Some policys may not provide theft coverage away from the insured’s premises or no wind and hail coverage unless items are located inside a fully enclosed structure.

A.D. Banker&company©

24 HOmeOwneRS InSURAnce

The following special limits apply to the ISO hO 00 03 form (2011 edition), and they vary on other policy forms (i.e., AAIS or insurers’ manuscripted forms). The dollar values listed represent the total limit applicable to any one loss. This listing contains a general description of the more common special limits and coverage under any policy is always subject to conditions, limitations, and exclusions contained in the contract:

• $200 (AAIS: $250) on money, notes, gold, silver other than silverware, coins, and metals, stored value cards, smart cards, and scrip

• $1,500 on securities, letters of credit, passports, tickets, stamps

• $1,500 on watercraft including its trailers, equipment, and outboard motors

• $1,500 on trailers not used with watercraft

• $1,500 (AAIS: $2,500) for loss by theft of jewelry, watches, precious and semi-precious stones, and furs

• $2,500 for loss by theft of firearms and related equipment

• $2,500 for loss by theft of silverware, silver-plated ware, goldware, platinumware, pewterware, including silver, gold, or pewter flatware, hollowware, tea sets, trays and trophies

• $2,500 on property on the residence premises that is used primarily for business purposes

• $1,500 on property away from the residence premises and used primarily for business purposes

• $1,500 on portable electronic equipment that reproduces, receives or transmits audio, visual, or data signals, is designed to be operated by more than one power source, and is in or upon a motor vehicle

• $250 for antennas, tapes, wires, records, disks or other media

The insured should be encouraged to maintain adequate documentation of all personal property, including

• Serial and model numbers

• Purchase dates

• Prices and values

• Still or video pictures

• Records, receipts, and pictures should be stored away from the premises, such as in a safe deposit box or remotely in an electronic format

Coverage C Property Not Covered: Property separately described and specifically insuredArticles separately described and specifically insured, regardless of the limit for which they are insured in any insurance policy, are not covered by the homeowners policy.

Animals, birds, or fish Motor vehiclesNo coverage is provided for motorized vehicles unless they are not required to be licensed for use on public roads AND are used to service a residence or assist the handicapped.

Example: An ATV the insured takes to various off-road locations, such as the sand dunes, is not covered on the homeowners policy. A garden tractor the insured uses to mow his lawn and to haul materials around the residence property is covered.

A.D. Banker&company©

25ChAPTEr 3: SECTIONS I AND II COvErAGES OF ThE hOMEOwNErS POLICY

AircraftThe aircraft exclusion applies to any conveyance used or designed for flight. Model and hobby aircraft not used to carry people or cargo are covered.

HovercraftHovercraft is excluded and means a self-propelled motorized ground effect vehicle and includes flarecraft and air cushion vehicles.

Roomers, boarders, and other tenantsUnless the property is owned by someone who is related to an insured, personal property of roomers, boarders, and other tenants is not covered.

Property in an apartment rented to othersProperty owned by the insured and in an apartment regularly rented or held for rental to others is not covered; however, an Additional Coverage does provide $2,500 of coverage, per rented unit, for Landlord’s Furnishings.

Rented property off-premisesProperty rented or held for rental to others off the residence premises is not covered.

Business dataBusiness records, regardless of where and how stored, is not covered. The cost of blank recording or storage media and prerecorded computer programs available on the retail market are covered.

Credit cardsCredit cards and electronic fund transfer cards or access devices used solely for deposit or withdrawal or transfer of funds are not covered. An Additional Coverage does provide limited coverage of $500 for such cards and devices.

Water or steamWater and steam are not considered covered property.

Additional items not provided coverage while away from the insured premises include:

• Unattached camper bodies

• Trailers not used with watercraft

• Building materials and supplies

Often, the homeowners policy provides no coverage for electronic devices or accessories that can be operated from the electrical system of a motor vehicle or watercraft while they are in or on the vehicle or watercraft and would need coverage from the insured’s personal auto policy, for instance, a portable GPS in a car.

The agent should encourage clients to report major purchases of personal property to be sure adequate coverage is provided by the homeowners policy. Many insurers have stock brochures to assist clients keep an organized inventory of their belongings; some insurers of higher value homes will even include inventory help as part of their homeowners program.

A.D. Banker&company©

26 HOmeOwneRS InSURAnce

Coverage D – Loss of Use (AAIS: Additional Living Costs and Loss of Rent)Coverage D provides coverage for three types of indirect loss: Additional Living Expense, Fair Rental value, and Civil Authority Prohibits Use. Coverage is triggered when the residence premises is not fit to live in because of direct damage caused by a covered peril.

Additional Living Expense coverage makes payment for non-continuing living expenses (those over and above the insured’s normal living expenses) that arise from a covered loss. These are additional or increased living expenses necessitated by the insured’s inability to live in the dwelling or use a structure while repairs or reconstruction take place.

Example: A fire in the kitchen of Jack’s home caused smoke damage. Jack and his family can’t live in the home and are now staying in an apartment until the damage is repaired. Their monthly expenses are $2,000 for the mortgage, $200 for property taxes, $250 for homeowners insurance, and $300 for utilities. The monthly rent for the apartment is $1,800 plus another $200 for utilities.

How much should Jack expect to receive from his insurer under Additional Living Expense coverage?

Answer: The only expenses that are in excess of Jack’s normal, continuing expenses are the apartment’s rent and utilities. Thus, Jack will receive $1,800 plus $200 for a total of $2,000 if he is unable to live in his home for a month.

It should be noted that the Additional Living Expense portion of Coverage D is intended to reimburse insureds for only the increase in living expenses necessary to maintain their normal standards of living. The insured will not be reimbursed for regular and ongoing expenses, such as mortgage payments, groceries, and utilities.

Example: If Jack decided to stay at a hotel and dine out every night instead of renting an apartment and eating in, would the policy pay for those expenses?

Answer: It all depends on Jack’s lifestyle. If he lives in a small three bedroom home in a modest neighborhood, the insurer will only reimburse an amount that represents a hotel typical of his lifestyle. However, if Jack lives in a 10,000 square foot home in the most expensive part of town, it is possible the insurer will reimburse the costs of a hotel and meals. Remember, the reimbursement is for additional expenses necessary to maintain a normal standard of living.

Fair Rental Value coverage makes payment for the fair rental value of that part of the residence premises rented by the insured, or held for rental to others, that is unfit to live in after a covered loss. Essentially, because the tenant can no longer occupy the damaged portion of the residence, he or she won’t be paying rent and the insured won’t receive that expected income. Coverage D covers the fair rental value less any expenses that aren’t ongoing.

Payment for additional living expense and fair rental value is made for the shortest time needed to repair or replace the damaged property or for the insured to settle elsewhere.

Civil Authority Prohibits Use coverage makes payment for additional living expense and fair rental value in certain circumstances when the residence premises doesn’t suffer direct damage. This coverage applies after circumstances that require government agencies to deny access to damaged areas, sometimes for long periods of time. Evacuation or prohibited use after wildfires, explosions, and other natural disasters trigger coverage, but the loss must arise from a covered peril.

Example: On Sunday, a brush fire broke out near the Jack’s parent’s family home. On Monday everyone in the neighborhood was forced to evacuate. Jack decided to drive to the desert, stay at a hotel, and enjoy a small family vacation while they were evacuated. He and his family returned home on Friday night and learned they were allowed back home on Thursday morning. What expenses might he be entitled to under Civil Authority Prevents Use coverage?

Answer: If the evacuation was required by the civil authorities, Jack would be reimbursed for his additional living expenses while evacuated. However, because they could have returned home on Thursday, Friday’s expenses will not be reimbursed.

A.D. Banker&company©

27ChAPTEr 3: SECTIONS I AND II COvErAGES OF ThE hOMEOwNErS POLICY

Losses or expenses not covered under Coverage D include the cancellation of a lease or agreement.

The period of time for which additional living expense and fair rental value are paid is limited to the shortest time required to repair or replace the premises or, if the insured moves to a new, permanent residence, the shortest time for relocation to be completed. Additional living expenses, loss of rent, and civil authority prohibited use expenses are not limited by the expiration of the policy.

Many policies limit Coverage D to 20% of the Coverage A limit of liability. Some policies may provide coverage for an unlimited amount in terms of dollars, but they will limit the amount of time. As is the case with many of the coverages under the policy, higher limits are available by endorsement. The deductible does apply to this coverage.

Section II – LiabilityCoverage E – Personal Liability (AAIS: Coverage L)Coverage E provides coverage for claims and lawsuits brought against an insured because of bodily injury or property damage that are caused by an occurrence that takes place during the policy period—to which this coverage applies. Also covered are certain supplementary payments, such as claims expenses, premiums for bonds, lost wages to assist the insurer in the investigation or defense of claims and lawsuits, and interest incurred on settlements or judgments. No deductible applies to this coverage.

Payments are made for damages only if an insured is legally liable, up to the limit of liability appearing on the Declarations.

Bodily Injury means bodily harm, sickness, or disease and includes the required care, loss of services, and death that results. Emotional injury and embarrassment are not included in this definition.

Property Damage means physical injury to, destruction of, or loss of use of tangible property or premises.

The standard limit of liability is $100,000 and is included at no additional premium. Higher limits are available at a modest premium increase. Agents should be diligent when working with clients and advising them about purchasing adequate financial protection for their individual needs, assets, and responsibilities. Because the costs of defense are often higher than settlements and judgments, defense coverage is extremely valuable. The policy requires the insurer to continue providing a defense, in addition to the limit of liability appearing on the Declarations, until the policy exhausts its limit of liability by payment of a judgment or settlement.

Having too little liability protection is common because people don’t expect to be responsible for causing injury or damage—or to be sued.

Example: Marie’s sister, Joan, has a mixed breed dog, Buttons, who only weighs 35 pounds but is quite exuberant. Emily, a 4-year-old neighbor, was visiting and Buttons nipped her ankle during her visit. Emily’s parents sued Joan, whose homeowners insurer settled the lawsuit for $25,000.

Even friendly dogs can injure someone. Almost 5 million dog bites occur each year and, of those, approximately 800,000 require medical care. Nearly a third of all homeowners liability claim payments are due to dog bites and insurers pay almost $500 million in dog bite claims annually.

Owning a dog isn’t the only liability hazard that a homeowner might have. A few examples of unexpected liability claims include:

• Neighbor’s child falls out of a tree in the insured’s back yard and breaks her leg

• Insured hits a golf ball and breaks the picture window of a home on the 8th hole

• A guest trips on broken porch steps, falls, and sprains an ankle

• A guest is injured when diving into the insured’s swimming pool

A.D. Banker&company©

28 HOmeOwneRS InSURAnce