accounting traps to avoid - wilwinn.com · services industry and has been with the firm since 2005....

TRANSCRIPT

1

Accounting Traps to Avoid

Presented by Wilary Winn

Douglas Winn, President Brenda Lidke, Director

September 27, 2016

2

Today’s Presenters Douglas Winn – President Mr. Winn co-founded Wilary Winn in the summer of 2003 and his primary responsibility is to set the firm's strategic direction. Mr. Winn is a nationally recognized expert in financial institution accounting and regulatory reporting and has led seminars on the subject for many of the country's largest public accounting firms, the AICPA, the FDIC, and the NCUA. Mr. Winn began his career as a practicing CPA for Arthur Young & Company - now Ernst & Young.

3

Today’s Presenters Brenda Lidke - Director Ms. Lidke has over 15 years of experience in the financial services industry and has been with the firm since 2005. Her areas of expertise include modeling of complex cash flows and financial analysis. Brenda manages and leads Wilary Winn’s fair value business line and is one of the country's foremost experts regarding purchase accounting.

Topics Covered

• True Sale • Merger Related Topics

– Day One Accounting – PCI Loans under ASC 310-30 – Goodwill

• Mortgage Banking Activities – Mortgage Banking Derivatives – Loans Held for Sale – Mortgage Servicing Rights

4

• Why – Off balance sheet exposures came back onto the balance sheet during the financial crisis

• What – Sales accounting is a very complex topic discussed in ASC 860-10-40

• Issue – A transfer of a loan or portion of a loan that does not meet true sale is a secured borrowing

5

Criteria for a Sale*

1) The transferred financial assets have been isolated from the transferor – put presumptively beyond the reach of the transferor and its creditors, even in bankruptcy or other receivership.

2) No condition both constrains the transferee (or third party holder of its beneficial interests) from taking advantage of its right to pledge or exchange and provides more than a trivial benefit to the transferor – “continuing involvement.”

3) The transferor, its consolidated affiliates included in the financial statements being presented, or its agents do not maintain effective control over the transferred financial assets or third-party beneficial interests related to those transferred assets.

*ASC 860-10-40-5 6

Cannot Divide a Financial Asset Unless You Create a

Participating Interest Which Must Meet 3 Criteria – ASC 860-10-40-6A

1. Proportionate ownership rights with equal priority to each participating

interest holder.

2. Involves no recourse (other than standard representations and warranties) to, or subordination by, any participating interest holder.

3. Does not entitle any participating interest holder to receive cash before any other participating interest holder – exception for market rate servicing.

7

Examples

• Auto loan participation

• Transfer of seasoned loans to FNMA

8

Example

Sell a 90% interest in a pool of auto loans to yield 2.5% to purchaser Weighted average yield of pool is 4.0% Spread retained is 1.5%

The Trap: The interest spread

The Solution: Divide the spread into a market rate servicing fee of 1% which can be disproportionate and make the remaining .50% pari passu

9

Example

Transfer pool of loans to FNMA – yield 4% - MBS 3% Receive MBS backed by same loans in return along with an interest only strip of .50% and the right to service the loans for .25% (guarantee fee .25%)

Why – transfer credit risk and more favorable risk based capital treatment

The Trap: The interest only strip

10

The Solution

Two safe harbors:

1. The servicing contract – safe harbor for market rate servicing – ASC 860-10-40-6A.

2. Agreements to purchase or redeem transferred financial assets – involves normal representations and warranties – ASC 860-10-40-6A.

The interest only strip remains the issue: The solution is the unit of account – the credit union sold 100% of the loan and in exchange received the MBS, the interest only strip and the right to service the loan as sales proceeds ASC 860-10-55-17G.

11

• Fair Value Purchase Accounting is required on business combinations – The assets and liabilities of the merging-in business

need to brought over at fair value – The difference between the overall value of the

business and the fair value of the net assets is the goodwill or bargain purchase in the deal

12

13

Fair Value of Merging-in Credit Union Book Fair Fair

Value Value % Value $ DifferenceASSETSCash and Cash Equivalents 8,500,000 100.0% 8,500,000 - Certificate of Deposit 600,000 100.5% 603,000 3,000 Other Investments 10,000,000 100.0% 10,000,000 - Total Loans and Leases 70,000,000 97.0% 67,900,000 (2,100,000) Total Loans and Leases - Loss Allowance (700,000) 0.0% - 700,000 Foreclosed and Repossessed 100,000 100.0% 100,000 - Land and Building 8,000,000 75.0% 6,000,000 (2,000,000) Other Fixed Assets 1,500,000 100.0% 1,500,000 - Other Assets 2,000,000 100.0% 2,000,000 - Core Deposit Intangible - 1.0% 630,000 630,000 Total Assets 100,000,000 97.2% 97,233,000 (2,767,000)

LIABILITIESNon-maturity Deposits 63,000,000 100.0% 63,000,000 - Share Certificates of Deposit 28,000,000 100.5% 28,148,400 148,400 Other Liabilities 350,000 100.0% 350,000 - Total Liabilities 91,350,000 100.2% 91,498,400 148,400

EQUITY 8,650,000 90.0% 7,785,000 (865,000)

Total Liabilities and Equity 100,000,000 99.3% 99,283,400 (716,600)

Entity Valuation 90.0% 7,785,000 FV of Assets and Liabilities + CDI 5,734,600 Assistance Received - Goodwill (Bargain Purchase) 2,050,400

$97,233,000 minus $91,283,400 equals

$5,734,600 of Net Fair Value

Goodwill is the “plug” that makes the balance sheet

balance. The goodwill of $2,050,400 + the $97,233,000 FV if

assets equals the FV of the liabilities of

$99,283,400

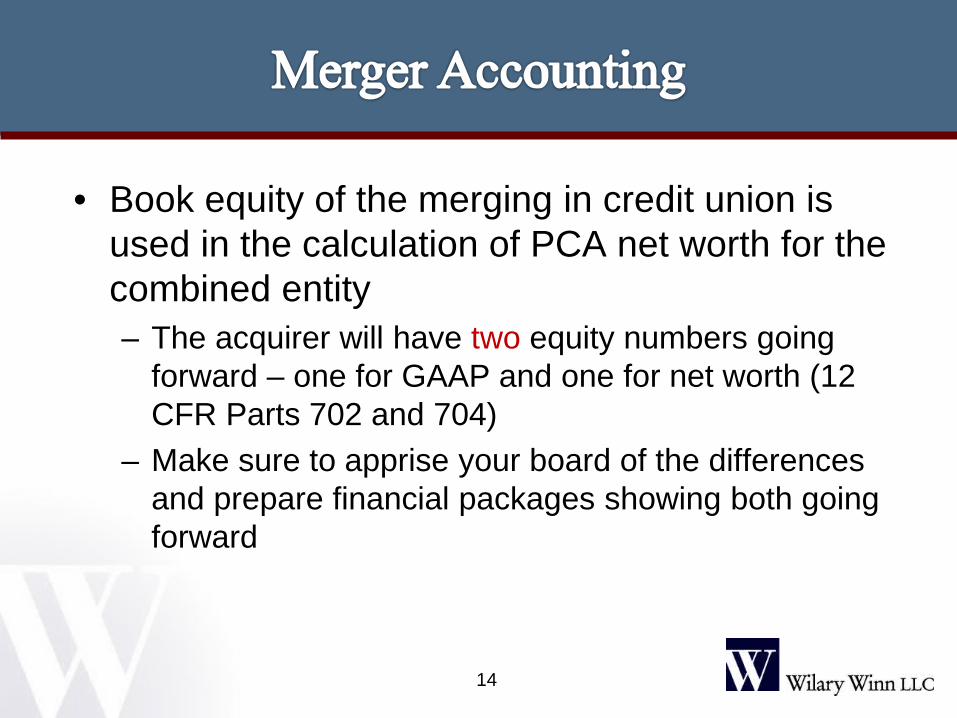

• Book equity of the merging in credit union is used in the calculation of PCA net worth for the combined entity – The acquirer will have two equity numbers going

forward – one for GAAP and one for net worth (12 CFR Parts 702 and 704)

– Make sure to apprise your board of the differences and prepare financial packages showing both going forward

14

15

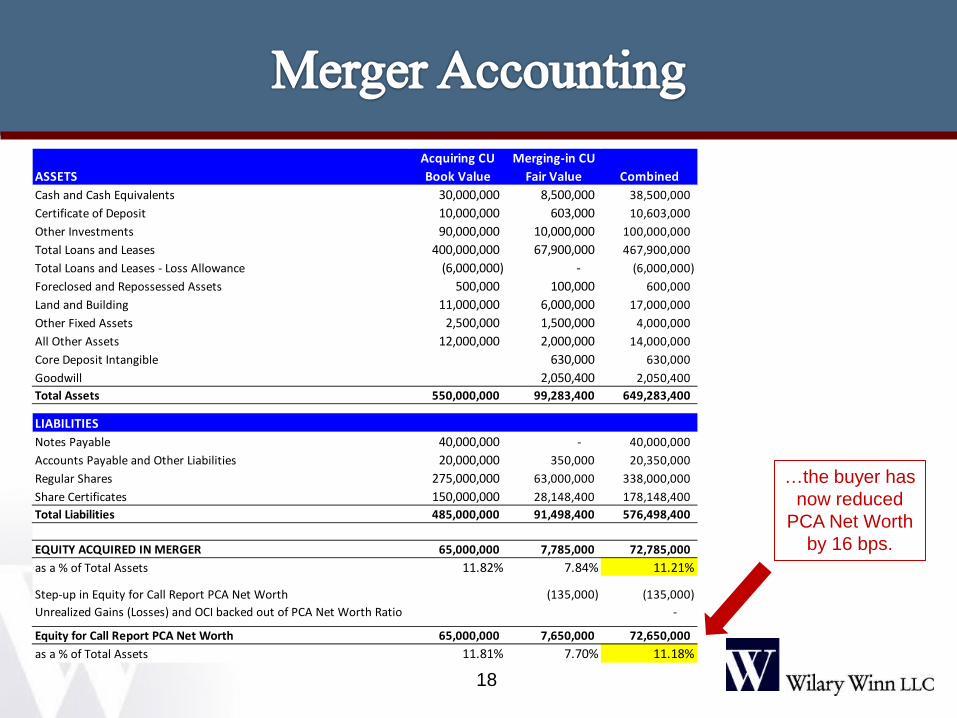

Acquiring CU Merging-in CUASSETS Book Value Fair Value CombinedCash and Cash Equivalents 30,000,000 8,500,000 38,500,000 Certificate of Deposit 10,000,000 603,000 10,603,000 Other Investments 90,000,000 10,000,000 100,000,000 Total Loans and Leases 400,000,000 67,900,000 467,900,000 Total Loans and Leases - Loss Allowance (6,000,000) - (6,000,000) Foreclosed and Repossessed Assets 500,000 100,000 600,000 Land and Building 11,000,000 6,000,000 17,000,000 Other Fixed Assets 2,500,000 1,500,000 4,000,000 All Other Assets 12,000,000 2,000,000 14,000,000 Core Deposit Intangible 630,000 630,000 Goodwill 2,050,400 2,050,400 Total Assets 550,000,000 99,283,400 649,283,400

LIABILITIESNotes Payable 40,000,000 - 40,000,000 Accounts Payable and Other Liabilities 20,000,000 350,000 20,350,000 Regular Shares 275,000,000 63,000,000 338,000,000 Share Certificates 150,000,000 28,148,400 178,148,400 Total Liabilities 485,000,000 91,498,400 576,498,400

EQUITY ACQUIRED IN MERGER 65,000,000 7,785,000 72,785,000 as a % of Total Assets 11.82% 7.84% 11.21%

Step-up in Equity for Call Report PCA Net Worth 865,000 865,000 Unrealized Gains (Losses) and OCI backed out of PCA Net Worth Ratio -

Equity for Call Report PCA Net Worth 65,000,000 8,650,000 73,650,000 as a % of Total Assets 11.81% 8.71% 11.34%

Two different equity numbers to keep track of going forward

• The Trap: Writing off items on the merging-in institution's books so you do not have to take an income hit on the combined books.

• The solution: Do not make any adjustments to the merging-in credit union’s books prior to merger. This is not allowed under GAAP and it will reduce the amount of equity obtained in the merger.

16

17

Fair Value of Merging-in Credit Union Book Pre-Merger Book Fair Fair

Value Adjustment Value Value % Value $ DifferenceASSETSCash and Cash Equivalents 8,500,000 8,500,000 100.0% 8,500,000 - Certificate of Deposit 600,000 600,000 100.5% 603,000 3,000 Other Investments 10,000,000 10,000,000 100.0% 10,000,000 - Total Loans and Leases 70,000,000 70,000,000 97.0% 67,900,000 (2,100,000) Total Loans and Leases - Loss Allowance (700,000) (1,000,000) (1,700,000) 0.0% - 1,700,000 Foreclosed and Repossessed 100,000 100,000 100.0% 100,000 - Land and Building 8,000,000 8,000,000 75.0% 6,000,000 (2,000,000) Other Fixed Assets 1,500,000 1,500,000 100.0% 1,500,000 - Other Assets 2,000,000 2,000,000 100.0% 2,000,000 - Core Deposit Intangible - - 1.0% 630,000 630,000 Total Assets 100,000,000 (1,000,000) 99,000,000 98.2% 97,233,000 (1,767,000)

LIABILITIESNon-maturity Deposits 63,000,000 63,000,000 100.0% 63,000,000 - Share Certificates of Deposit 28,000,000 28,000,000 100.5% 28,148,400 148,400 Other Liabilities 350,000 350,000 100.0% 350,000 - Total Liabilities 91,350,000 91,350,000 100.2% 91,498,400 148,400

EQUITY 8,650,000 7,650,000 101.8% 7,785,000 135,000

Total Liabilities and Equity 100,000,000 99,000,000 100.3% 99,283,400 283,400

Entity Valuation 101.8% 7,785,000 FV of Assets and Liabilities + CDI 5,734,600 Assistance Received - Goodwill (Bargain Purchase) 2,050,400

Entity valuation remains the same

and goodwill remains the same.

However….

18

Acquiring CU Merging-in CUASSETS Book Value Fair Value CombinedCash and Cash Equivalents 30,000,000 8,500,000 38,500,000 Certificate of Deposit 10,000,000 603,000 10,603,000 Other Investments 90,000,000 10,000,000 100,000,000 Total Loans and Leases 400,000,000 67,900,000 467,900,000 Total Loans and Leases - Loss Allowance (6,000,000) - (6,000,000) Foreclosed and Repossessed Assets 500,000 100,000 600,000 Land and Building 11,000,000 6,000,000 17,000,000 Other Fixed Assets 2,500,000 1,500,000 4,000,000 All Other Assets 12,000,000 2,000,000 14,000,000 Core Deposit Intangible 630,000 630,000 Goodwill 2,050,400 2,050,400 Total Assets 550,000,000 99,283,400 649,283,400

LIABILITIESNotes Payable 40,000,000 - 40,000,000 Accounts Payable and Other Liabilities 20,000,000 350,000 20,350,000 Regular Shares 275,000,000 63,000,000 338,000,000 Share Certificates 150,000,000 28,148,400 178,148,400 Total Liabilities 485,000,000 91,498,400 576,498,400

EQUITY ACQUIRED IN MERGER 65,000,000 7,785,000 72,785,000 as a % of Total Assets 11.82% 7.84% 11.21%

Step-up in Equity for Call Report PCA Net Worth (135,000) (135,000) Unrealized Gains (Losses) and OCI backed out of PCA Net Worth Ratio -

Equity for Call Report PCA Net Worth 65,000,000 7,650,000 72,650,000 as a % of Total Assets 11.81% 7.70% 11.18%

…the buyer has now reduced

PCA Net Worth by 16 bps.

• The Trap: Calculating a Bargain Purchase in a

credit union merger transaction.

• The solution: Bargain Purchases are very rare and the GAAP requires you to recheck your numbers if you calculate a Bargain Purchase (ASC 805-30-30-5). Usually, we would only see a Bargain Purchase on a credit union merger when there was NCUA assistance in the deal.

19

20

Fair Value of Merging-in Credit Union Book Fair Fair

Value Value % Value $ DifferenceASSETSCash and Cash Equivalents 8,500,000 100.0% 8,500,000 - Certificate of Deposit 600,000 100.5% 603,000 3,000 Other Investments 10,000,000 25.0% 2,500,000 (7,500,000) Total Loans and Leases 70,000,000 97.0% 67,900,000 (2,100,000) Total Loans and Leases - Loss Allowance (700,000) 0.0% - 700,000 Foreclosed and Repossessed 100,000 100.0% 100,000 - Land and Building 8,000,000 75.0% 6,000,000 (2,000,000) Other Fixed Assets 1,500,000 100.0% 1,500,000 - Other Assets 2,000,000 100.0% 2,000,000 - Core Deposit Intangible - 1.0% 630,000 630,000 Total Assets 100,000,000 89.7% 89,733,000 (10,267,000)

LIABILITIESNon-maturity Deposits 63,000,000 100.0% 63,000,000 - Share Certificates of Deposit 28,000,000 100.5% 28,148,400 148,400 Other Liabilities 350,000 100.0% 350,000 - Total Liabilities 91,350,000 100.2% 91,498,400 148,400

EQUITY 8,650,000 0.0% - (8,650,000)

Total Liabilities and Equity 100,000,000 91.5% 91,498,400 (8,501,600)

Entity Valuation 0.0% - FV of Assets and Liabilities + CDI (1,765,400) Equity Acquired in Merger (floor of FV of Assets & Liabilities) -

FV of Assets and Liabilities + CDI (1,765,400) Assistance Received 3,000,000 Goodwill (Bargain Purchase) (1,234,600)

The NCUA knows that the investments need to be written down and that the

value of the building is less than book.

Both these adjustments would

eat up all the equity, so they are willing to

give $3M in assistance to an

acquirer in order to take on this credit

union.

There entity value is zero as the CU would

not have enough capital to continue if

the investments were recorded properly.

The acquirer believes

the fair value of all the assets and liabilities is a

negative $1.765M. However, with the

$3M in cash from the NCUA, the acquirer receives a $1.235M

gain.

21

In a Bargain Purchase transaction, the acquirer does not get to count the book

equity toward net worth.

Acquiring CU Merging-in CU NCUAASSETS Book Value Fair Value Assistance CombinedCash and Cash Equivalents 30,000,000 8,500,000 3,000,000 41,500,000 Certificate of Deposit 10,000,000 603,000 10,603,000 Other Investments 90,000,000 2,500,000 92,500,000 Total Loans and Leases 400,000,000 67,900,000 467,900,000 Total Loans and Leases - Loss Allowance (6,000,000) - (6,000,000) Foreclosed and Repossessed Assets 500,000 100,000 600,000 Land and Building 11,000,000 6,000,000 17,000,000 Other Fixed Assets 2,500,000 1,500,000 4,000,000 All Other Assets 12,000,000 2,000,000 14,000,000 Core Deposit Intangible 630,000 630,000 Goodwill - Total Assets 550,000,000 89,733,000 3,000,000 642,733,000

LIABILITIESNotes Payable 40,000,000 - 40,000,000 Accounts Payable and Other Liabil ities 20,000,000 350,000 20,350,000 Regular Shares 275,000,000 63,000,000 338,000,000 Share Certificates 150,000,000 28,148,400 178,148,400 Total Liabilities 485,000,000 91,498,400 - 576,498,400

EQUITY ACQUIRED IN MERGER 65,000,000 (1,765,400) 3,000,000 66,234,600 as a % of Total Assets 11.82% -1.97% 10.31%

Step-up in Equity for Call Report PCA Net Worth - Unrealized Gains (Losses) and OCI backed out of PCA Net Worth Ratio -

Equity for Call Report PCA Net Worth 65,000,000 (1,765,400) 3,000,000 66,234,600 as a % of Total Assets 11.81% -1.96% 10.30%

• What is a PCI loan? • Removal from ASC 310-30 Status • Accounting for PCI loans • Change under CECL standard

22

FAS ASC 310-30 - Loans and Debt Securities

Acquired with Deteriorated Credit Quality

• The determination of whether acquired loans are to be accounted for under FAS ASC 310-30 must be made at acquisition and loans cannot transition out of this status afterwards.

• The loan must meet two requirements (ASC 310-30-05-1 and 05-2): – The deterioration in credit quality occurred subsequent to origination. – It is probable that the acquirer will be unable to collect all

contractually required payments from the borrower.

• Revolving loans are excluded from FAS ASC 310-30 23

Removal from PCI status

• The Trap: Once the loan is elected as PCI under FAS ASC 310-30, it cannot be re-designated (ASC 310-30-40). The loan cannot be refinanced out of PCI even if it performing.

• The solution: Review each of the probable loans at time of acquisition to determine which ones in in scope. Most institutions have a materiality threshold when classifying PCI loans such as loan size or credit deterioration. Do not designate PCI loans that you do not have to.

24

Timing of Cash Flows

• The Trap: Pushing out the timing of expected cash flows will result in a required loan loss reserve.

• The solution: Make sure the lending team reviews the PCI loans and estimates a realistic timeframe in which the payments will be collected. This includes extensions!

25

Accounting for PCI Loans

• Loan is initially recorded at fair value as of the acquisition • In order to record the fair value, we recommend

recording the loan at its principal balance and then create a contra account to bring the loan down to fair value

$150,000 Principal Balance ($ 50,000) Contra Account $100,000 Fair Value (or Net Carrying Value)

26

Accounting for PCI Loans - Continued

• Based on these metrics: – Coupon rate is 4% – Loan amortization term is 180 month, monthly P&I is $1,110 – Discount rate is 10% – Loan is expected to default and have loss in month 12 of $45,543

• The total gross cash flows collected are: $1,110 x 11= $12,205 + remaining loan balance at start of month 12 of $143,182 less loss of $45,543 = total of $109,844. Present valued at 10%, this amount is $100,000, thus the $50,000 contra account.

27

Accounting for PCI Loans – Continued

Initial Valuation

28

SchedEnding Prin Interest Total Discount PV PV

Period Balance Payment Defaults Losses Recoveries Payment Cash Flows Rate Factor CFs0 150,000 1 149,390 610 - - - 500 1,110 10.00% 99.17% 1,100 2 148,779 612 - - - 498 1,110 10.00% 98.35% 1,091 3 148,165 614 - - - 496 1,110 10.00% 97.54% 1,082 4 147,550 616 - - - 494 1,110 10.00% 96.73% 1,073 5 146,932 618 - - - 492 1,110 10.00% 95.94% 1,064 6 146,312 620 - - - 490 1,110 10.00% 95.14% 1,056 7 145,690 622 - - - 488 1,110 10.00% 94.36% 1,047 8 145,066 624 - - - 486 1,110 10.00% 93.58% 1,038 9 144,440 626 - - - 484 1,110 10.00% 92.80% 1,030

10 143,812 628 - - - 481 1,110 10.00% 92.04% 1,021 11 143,182 630 - - - 479 1,110 10.00% 91.28% 1,013 12 - - 143,182 45,543 97,639 - 97,639 10.00% 90.52% 88,384

Total 6,818 143,182 45,543 97,639 5,387 109,844 100,000

Accounting for PCI Loans – Continued

• The “accretable yield” is the difference between the gross expected cash flows of $109,844 and the $100,000 of fair value.

• This $9,844 is accreted into income over the expected remaining life at the 10% discount rate.

• As the amount is accreted, the carrying value is increased by this amount. However, the carrying amount is also decreased by the principal received.

• The principal received will lower the loan balance. The excess of the accretion over the interested received lowers the contra account. 29

Accounting for PCI Loans – Continued

Initial Valuation

30

Loan Loan AccretionLoan Contra Carrying Principal Interest Accretion Accretion less

Period Balance Account Value Received Received Rate Income Loan Int0 150,000 (50,000) 100,000 1 149,390 (49,667) 99,724 610 500 10.0% 833 333 2 148,779 (49,334) 99,445 612 498 10.0% 831 333 3 148,165 (49,001) 99,164 614 496 10.0% 829 333 4 147,550 (48,668) 98,881 616 494 10.0% 826 332 5 146,932 (48,336) 98,596 618 492 10.0% 824 332 6 146,312 (48,004) 98,308 620 490 10.0% 822 332 7 145,690 (47,673) 98,018 622 488 10.0% 819 332 8 145,066 (47,342) 97,725 624 486 10.0% 817 331 9 144,440 (47,011) 97,430 626 484 10.0% 814 331

10 143,812 (46,680) 97,132 628 481 10.0% 812 330 11 143,182 (46,350) 96,832 630 479 10.0% 809 330 12 45,543 (45,543) - 97,639 - 10.0% 807 807

Total 104,457 5,387 9,844 4,457

Accounting for PCI Loans – Continued

• Our example continues and 3 months have gone by and all cash flows were collected as expected

• However, we now believe we will not receive the recovery on the loan for an additional 6 months – We need to establish an additional loss reserve – The recovery amount of $97,639 is still the same amount, but

because the timing is different, we need to book an additional reserve of $4,401

– This reserve is the difference between the recalculated fair value and the existing carrying value

31

Accounting for PCI Loans – Continued

Quarter 1

32

Ending Sched TotalLoan Prin Interest Cash Discount PV PV

Period Balance Payment Defaults Losses Recoveries Payment Flows Rate Factor CFs3 148,165 4 147,550 616 - - - 494 1,110 10.0% 99.2% 1,100 5 146,932 618 - - - 492 1,110 10.0% 98.4% 1,091 6 146,312 620 - - - 490 1,110 10.0% 97.5% 1,082 7 145,690 622 - - - 488 1,110 10.0% 96.7% 1,073 8 145,066 624 - - - 486 1,110 10.0% 95.9% 1,064 9 144,440 626 - - - 484 1,110 10.0% 95.1% 1,056

10 143,812 628 - - - 481 1,110 10.0% 94.4% 1,047 11 143,182 630 - - - 479 1,110 10.0% 93.6% 1,038 12 - - 143,182 - - - - 10.0% 92.8% - 13 - - - - - - - 10.0% 92.0% - 14 - - - - - - - 10.0% 91.3% - 15 - - - - - - - 10.0% 90.5% - 16 - - - - - - - 10.0% 89.8% - 17 - - - - - - - 10.0% 89.0% - 18 - - - 45,543 97,639 - 97,639 10.0% 88.3% 86,211

Total 4,983 143,182 45,543 97,639 3,893 106,515 94,763

Accounting for PCI Loans - Continued

Quarter 1

33

Recorded Recalc'd Loan New Loan Loan AccretionLoan Contra Carrying Fair Loss Carrying Principal Interest Accretion Accretion less

Period Balance Account Value Value Reserve Value Received Received Rate Income Loan Int3 148,165 (49,001) 99,164 94,763 (4,401) 94,763 4 147,550 (48,729) (4,377) 94,443 616 494 10.0% 790 296 5 146,932 (48,459) (4,353) 94,121 618 492 10.0% 787 295 6 146,312 (48,188) (4,328) 93,796 620 490 10.0% 784 295 7 145,690 (47,919) (4,304) 93,468 622 488 10.0% 782 294 8 145,066 (47,649) (4,280) 93,137 624 486 10.0% 779 293 9 144,440 (47,381) (4,256) 92,804 626 484 10.0% 776 293

10 143,812 (47,113) (4,232) 92,468 628 481 10.0% 773 292 11 143,182 (46,846) (4,208) 92,129 630 479 10.0% 771 291 12 143,182 (46,141) (4,145) 92,896 - - 10.0% 768 768 13 143,182 (45,431) (4,081) 93,670 - - 10.0% 774 774 14 143,182 (44,715) (4,016) 94,451 - - 10.0% 781 781 15 143,182 (43,993) (3,952) 95,238 - - 10.0% 787 787 16 143,182 (43,264) (3,886) 96,032 - - 10.0% 794 794 17 143,182 (42,530) (3,820) 96,832 - - 10.0% 800 800 18 45,543 (41,790) (3,754) 0 97,639 - 10.0% 807 807

Total 102,622 3,893 11,752 7,859

Timing of Cash Flows

• We have just booked a reserve not based on credit but because of the expected timing of collected cash flows.

• The solution: Make sure the lending team reviews the

PCI loans and estimates a realistic timeframe in which the payments will be collected, including possible extensions.

34

Improved Loan

• The Trap: If the loan performs better than initially expected, the credit component from the initial valuation cannot be released. Instead the accretion rate is increased to bring the adjustment into income over time.

• The solution: Make sure loans that are valued individually are reviewed by the lending team individually and they estimate a realistic expected loss for each loan. Don’t just apply a general % of reserve to all loans of a certain quality.

35

Improved Loan

Quarter 1 – Expect lower future losses

36

Ending Sched TotalLoan Prin Interest Cash Discount PV PV

Period Balance Payment Defaults Losses Recoveries Payment Flows Rate Factor CFs3 148,165 4 147,550 616 - - - 494 1,110 10.0% 99.2% 1,100 5 146,932 618 - - - 492 1,110 10.0% 98.4% 1,091 6 146,312 620 - - - 490 1,110 10.0% 97.5% 1,082 7 145,690 622 - - - 488 1,110 10.0% 96.7% 1,073 8 145,066 624 - - - 486 1,110 10.0% 95.9% 1,064 9 144,440 626 - - - 484 1,110 10.0% 95.1% 1,056

10 143,812 628 - - - 481 1,110 10.0% 94.4% 1,047 11 143,182 630 - - - 479 1,110 10.0% 93.6% 1,038 12 - - 143,182 25,543 117,639 - 117,639 10.0% 92.8% 109,173

Total 4,983 143,182 25,543 117,639 3,893 126,515 117,725

Improved Loan

Quarter 1 – Expect lower future losses

37

Recorded Recalc'd Loan New Loan Loan AccretionLoan Contra Carrying Fair Loss Carrying Principal Interest Accretion Accretion less

Period Balance Account Value Value Reserve Value Received Received Rate Income Loan Int3 148,165 (49,001) 99,164 117,725 - 99,164 4 147,550 (46,666) 100,884 616 494 34.2% 2,829 2,335 5 146,932 (44,279) 102,653 618 492 34.2% 2,878 2,386 6 146,312 (41,840) 104,472 620 490 34.2% 2,929 2,439 7 145,690 (39,348) 106,343 622 488 34.2% 2,981 2,493 8 145,066 (36,799) 108,267 624 486 34.2% 3,034 2,548 9 144,440 (34,194) 110,246 626 484 34.2% 3,089 2,605

10 143,812 (31,530) 112,282 628 481 34.2% 3,145 2,664 11 143,182 (28,806) 114,376 630 479 34.2% 3,203 2,724 12 25,543 (25,543) 0 117,639 - 34.2% 3,263 3,263

Total 122,622 3,893 27,351 23,457

CECL is good news for PCI loans!

• Under the CECL standard a separate credit loss allowance is established at time of purchase and is part of the ALLL (ASC 326-10-65).

• Unfavorable and favorable changes related to credit run through this allowance immediately. There is no more increase to accretable yield for favorable changes.

• Loans will be defined as purchased with credit deterioration (“PCD”). PCD assets are those which have experienced a more than insignificant deterioration in credit quality since inception.

38

• Goodwill Basics • Current testing requirements • PCC Election

– One time election; impacts all future deals – Testing still required

• New FASB proposal for testing

39

Goodwill Basics

• Goodwill arises from a merger transaction • It is not amortized; remains on books as an asset

(ASC 350-20-35-1) • Required to be tested at least annually for

impairment • Does not count toward the new Risk Based Net

Worth calculation

40

Current Goodwill Testing Requirements

• Current testing requirements require a two-step process to test for impairment.

• Step 1 is to determine if the fair value of the entity exceeds its book value. If yes, goodwill is not impaired. If not, move to Step 2.

• Step 2 determines how much of the goodwill is impaired by comparing the overall fair value of assets and liabilities against the value of the entity to recalculate goodwill.

• A qualitative test can be performed in following years once a Step 1 has been passed.

41

• The Trap: Electing the PCC Alternative to write-off

current goodwill in order to not have to do annual testing.

• The solution: Only elect this accounting alternative if you are fairly certain what your future goodwill situation will be.

42

PCC Accounting Alternative

• On January 16, 2014, the FASB issued Accounting Standards Update (ASU) No. 2014-02, Accounting for Goodwill.

• An organization has to elect the accounting alternative to amortize goodwill. Once elected, the accounting applies to all current and all future goodwill.

• Goodwill is amortized over 10 years or less. • Impairment test is still required for a triggering event.

43

FASB’s Newest Proposal

• On May 12, 2016, FASB proposed eliminating Step 2 of the current goodwill impairment test. – Impairment of goodwill would be tested by completing the

current Step 1 and any amount that fair value is under book value is written off, up to the goodwill amount.

• Companies can still perform a qualitative test prior to moving to a Step 1 test.

• FASB is currently in re-deliberations after receiving comment letters in July.

44

• Mortgage Banking Derivatives

• Loans Held for Sale

• MSR Accounting

• MSR Hedging

45

Interest Rate Lock Commitments (IRLCs)

• Interest rate lock in commitments on mortgage loans that will be held for resale are derivatives (FAS ASC 815-10-15-71)

• Commitments to originate mortgage loans to be held for investment and other types of loans are generally not derivatives

Mortgage Banking Derivatives

46

IRLC Value

• IRLCs should be initially recorded at fair value

• Subsequent changes in fair value are to be measured and reported on the balance sheet and income statement

Mortgage Banking Derivatives

47

Types of Forward Sales Commitments

• Mandatory delivery

• Best efforts delivery

• Master agreements

Mortgage Banking Derivatives

48

Mandatory Delivery Commitment

• An institution commits to deliver a certain amount of loans to an investor at a specified price on or before a specified date

• Requires a pair-off fee based on then current market prices to compensate investor for any shortfall

Mortgage Banking Derivatives

49

Mandatory Delivery Commitment

Mortgage Banking Derivatives

50

Underlying

Notional Amount

Mandatory Delivery Commitment

• Has a “specified underlying” - the specified price

• Requires little or no initial net investment

• Has a “notional amount” - the principal amount of the loan

• Requires or permits net settlement by paying a pair-off fee based on then current market prices

• Is a derivative – ASC 815-10-15-83

Mortgage Banking Derivatives

51

Best Efforts Delivery Commitment

• An institution commits to deliver an individual loan of a specified principal amount and quality to an investor if the loan to the underlying borrower closes

• Generally not considered a derivative until the loan closes because it does not meet the net settlement criteria

Mortgage Banking Derivatives

52

Netting of Derivatives for Reporting Purposes

• May net gains and losses of individual derivative commitments only under certain conditions, generally only under the legal right of offset – ASC 815-10-45-2 and 5

• The value of sales commitments covering the pipeline may not be netted against the value of the IRLCs, they must be reported separately

• The value of sales commitments covering the warehouse may not be netted against the value of the warehouse loans, they must be reported separately

Mortgage Banking Derivatives

53

Mortgage Pipeline

Mortgage Banking Derivatives

Base Rates down Rates upInterest Rate Lock Commitments Case 100 bps 100 bpsIRLC 100.00 +4.00 -4.00

BE Commitment 102.00 0.00 0.00

Mandatory Commitment 102.00 -4.00 +4.00

54

Accounting Traps

• Trap One: Marking the IRLCs to the forward commitment price

• Solution: Mark to the market

• Trap Two: Debits and credits do not align when using best efforts forwards because the IRLC is a derivative and is accounted for at FV while the best effort is not

• Solution: Elect fair value for best effort forwards – ASC 815-10-15-4b

Mortgage Banking Derivatives

55

Possible Ways to Account for Loans Held for Sale

• Lower of cost or fair value • Fair value • Cash flow hedge

56

Closed Loans Held for Sale

Mortgage Banking Derivatives

Base Rates down Rates upClosed Loans Held for Sale (LOCOM) Case 100 bps 100 bpsClosed Loan 100.00 0.00 -4.00

BE Commitment* 102.00 -4.00 +4.00

Mandatory Commitment 102.00 -4.00 +4.00

* Wilary Winn believes best efforts commiments morph into mandatory commitments once the loan closes.

57

• The Trap: Debits and credits do not align when using lower of cost or fair value when interest rates drop because the forward sale commitment is a derivative which has incurred a loss in value and the loan cannot be written up above cost

• The solution: Elect fair value for loans held for sale

58

Accounting for Servicing of Financial Assets

• Must initially recognize servicing rights at their fair value – ASC 860-50-25-1

• Credit Union an elect either the amortization method or the fair value method for future reporting of its MSRs

59

MSR Asset or Liability - FAS ASC 860-50-30

The benefits of the servicing, including the servicing fees, ancillary income, float, etc. must exceed “adequate compensation” in order to have a servicing asset. If not, the servicer has a liability. Adequate compensation includes a profit and is determined by the marketplace. It is based on marketplace costs, not the servicer’s internal costs.

Mortgage Servicing Rights

60

Initial Recording of MSR

• Servicing assets and liabilities must be reported separately

• A servicing asset can become a servicing liability over its life and vice versa

Mortgage Servicing Rights

61

• The Trap: Assuming that if the servicing fee is “normal” there is no asset or liability

• The Solution: Value mortgage servicing rights

62

How to Account for the MSR after Initial Recording?

FAS ASC paragraph 860-50-35-1 allows the asset to be measured and reported in one of two ways:

1) Amortization Method 2) Fair Value Method

A servicer can select either method, but cannot switch methodologies unless it moves to the Fair Value method at the beginning of the fiscal year before interim financial statements have been released. A servicer cannot go back to the amortization method after it has elected Fair Value.

Mortgage Servicing Rights

63

Amortization Method

Amortize the MSR in proportion and over the period of estimated net servicing income (level yield method) and assess servicing assets for impairment based on fair value at each reporting date.

Mortgage Servicing Rights

64

• The Trap: Write off the asset at the loan level when it pays off

• The Solution: Remember that the level yield amortization includes prepayments. Assess for impairment at the stratification level

65

Impairment

• Impairment is best measured at the loan level and is reported at the predominant risk characteristic stratum

• There is a difference between temporary impairment, which is accounted for through an allowance and permanent impairment, which requires a direct write-off

Mortgage Servicing Rights

66

67

100

200

300

400

500

600

700

800

0.400%

0.550%

0.700%

0.850%

1.000%

1.150%

1.300%

1.450%M

ar. 2

008

Sept

. 200

8

Mar

. 200

9

Sept

. 200

9

Mar

. 201

0

Sept

. 201

0

Mar

. 201

1

Sept

. 201

1

Mar

. 201

2

Sept

. 201

2

Mar

. 201

3

Sept

. 201

3

Mar

. 201

4

Sept

. 201

4

Mar

. 201

5

Sept

. 201

5

Mar

. 201

6

Value of MSR Asset

MSR Value % Prepayment Speed

Fair Value Method

• The fair value is determined at each reporting period • The asset is adjusted to equal its fair value • The difference is taken into income or expense for that

reporting period • The Trap: Forgetting how volatile the value can be

• The Solution: Use amortization method or hedge

Mortgage Servicing Rights

68

Mortgage Servicing Rights

69

Negative Convexity

Hedging MSRs

• MSRs can be hedged using derivatives that increase in value when interest rates decrease – floors, POs, etc.

• The Trap: MSRs have a yield curve with negative convexity and obtaining hedge accounting is very difficult

• The Solution: Elect fair value for the MSR portfolio

Mortgage Servicing Rights

70

Resources

Mortgage Servicing Rights

71

http://www.wilwinn.com/insights-and-resources.html

Asset Liability Management, Capital Stress Testing, Concentration Risk Analyses, and CECL

Matt Erickson [email protected] Mergers and Acquisitions, ASC 310-30, Goodwill Impairment Testing,

and TDRs: Brenda Lidke [email protected] Servicing Rights and Mortgage Banking Derivatives: Eric Nokken [email protected] Non-agency MBS: Amin Mohomed [email protected]

72

Contact Information

Wilary Winn LLC First National Bank Building

332 Minnesota Street, Suite 1750W Saint Paul, MN 55101

651-224-1200

www.wilwinn.com

73