accounting and financial management day 1

TRANSCRIPT

Information

• Management accounts explain and communicate complex processes and procedures

• Figures are used to communicate information• Secret is to keep it simple and understandable• Complexity and/or jargon leads to bad

decisions and a loss of control• Complexity creates fear of numbers

Financial information

• Financial information is a language that is universally used and accepted

• Formats may vary• Terminology may vary e.g. Profits v

surplus, stock v inventory

Management tool

• Financial information should be a valuable management tool

• The tool assists with:– Planning and control– Creating and supporting strategy– Improving efficiency and effectiveness– Comparing, monitoring & reporting– Measuring performance (project/

organisation, internal & external)

Communication tool

Very important aspect Structure this so it is Understandable Two way process Constructive Partners not assassins!

Format

• No prescribed format• There will be many different types of information• Depends on audience• What they need to know

Relevant & Timely

Information must be relevant What does the reader need? What is relevant to that position?

Information must be presented within an appropriate time frame Too early – accuracy? Too late - relevancy/ action?

Preparation

•Who?•Do they understand what is required?•Do they understand operations?•Can they make recommendations?•Will they be listened to?

Ownership

•Does someone take responsibility for preparing them?•Does someone take responsibility of acting on the information?•Who are they reporting to?

Action

•Is something done with the information?

Fixed Assets

•Confusion over certain items as to what they are•Definition depends on 3 factors

•Purpose of purchase•Expected life of item•The cost

Fixed Assets - 2

•If purchased for resale then it is stock•If used to passively generate an income then an investment•If to be used in furtherance of normal activities, it could be a fixed asset

Fixed Assets - 3

•Expected life important •Fixed asset if expected life is longer than a year•If less than 1 year – “expense” it•If more than 1 year – “Capitalise” it

Fixed Assets - 4

•Materiality•If high cost than capitalise•If low cost expense it•Use Common Sense

Depreciation

•Represents a transfer of value from the capital value to the profit and loss account•Trying to represent the true value of using the asset for that year•Can be very complex – e.g. land – this tends to increase in value

Depreciation - 2

•Estimate life expectancy of asset•Charge annual account on estimated life expectancy

•Wear and tear•Obsolescence•Uneconomical/ unreliable•Inadequacy – change in type/size of goods dealt with•Depletion•Expiry

Closing value

•There may be a residual value•Estimate life expectancy of asset•Difficult to estimate•Can use “Reducing Balance” method, rather than•“Straight Line” method

Depreciation meaning

•A decrease in value over a period of time•Replacement shortfall – difference between residual value of old item and amount needed to replace it •Allocation of cost – charge to P&L for the “cost” of use in that period

Disposal

•A profit or loss brought about on disposal has to be reflected in the accounts•e.g. car w/off over 4 years to zero values –now sell it at £1,000 – caused a profit to be generated•e.g. A laptop written down to half price over two years, on sale only realise a quarter of purchase price – loss caused

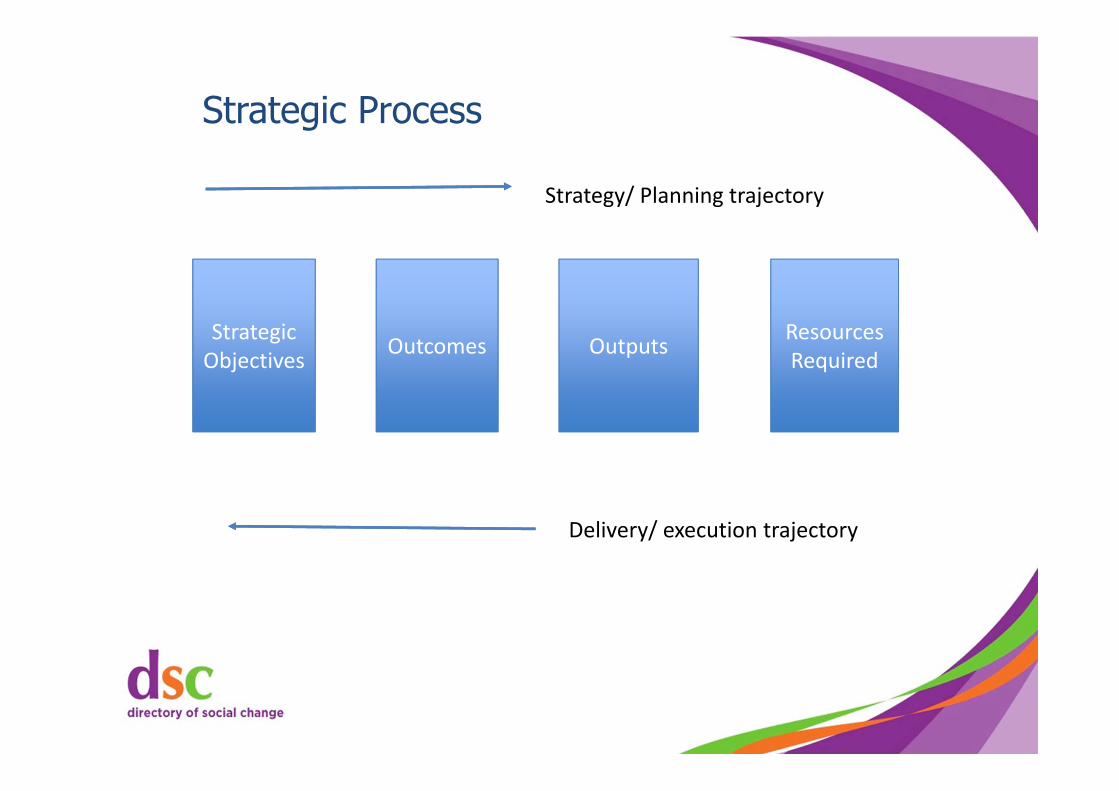

Strategic Process

Strategic Objectives Outcomes Outputs Resources

Required

Delivery/ execution trajectory

Strategy/ Planning trajectory

© Red Ochre 2016

Planning

•The resources required to deliver the strategy need to be costed•Need to be sure you really understand your project and/or your organisation•Working out the “money” requirement leads to an adjustment of the amount and timing of the resource input (more grounded in reality)•Now have a better handle on the funding requirement to deliver strategy•This is known as Financial Forecasting

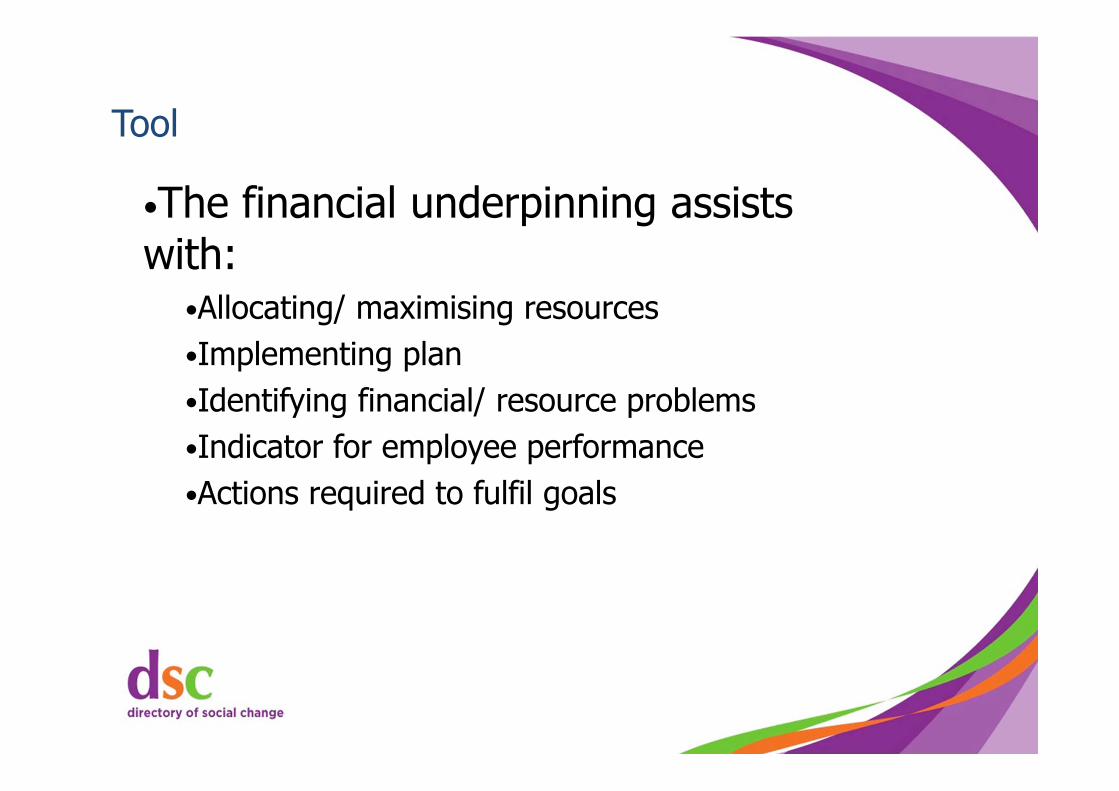

Tool

•The financial underpinning assists with:

•Allocating/ maximising resources •Implementing plan•Identifying financial/ resource problems•Indicator for employee performance•Actions required to fulfil goals

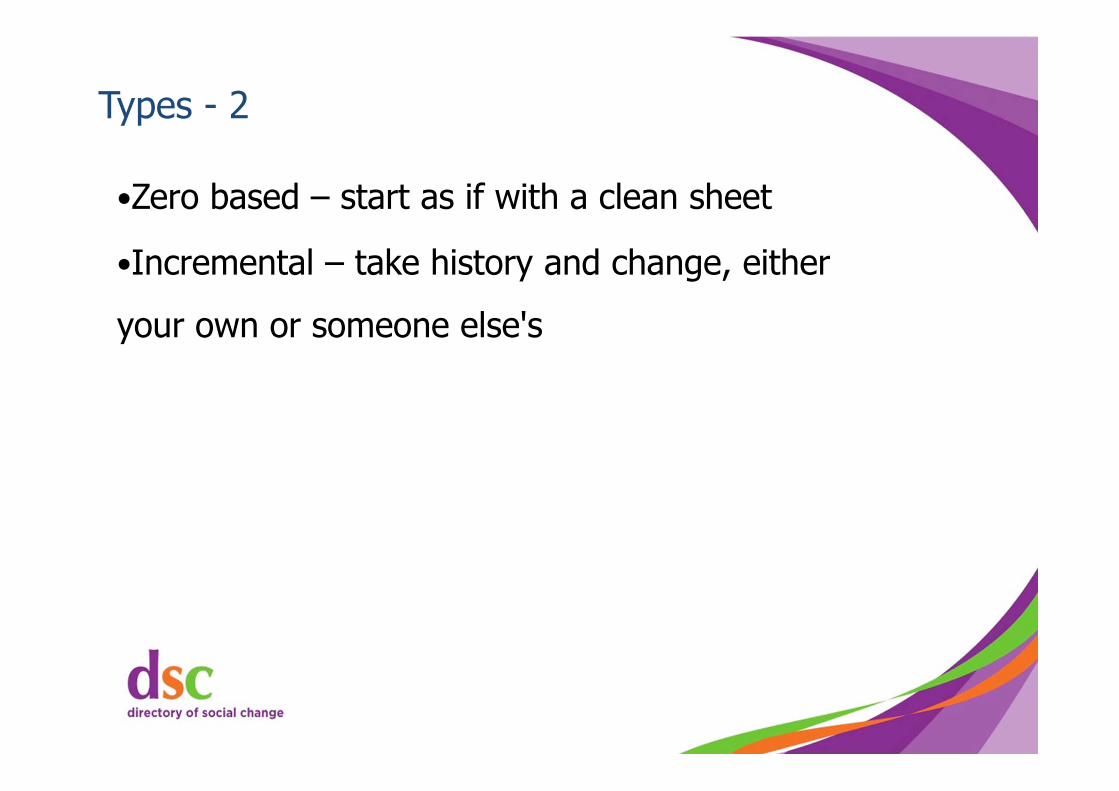

Types

•Revenue•Cash•Project•Capital

Types - 2

•Zero based – start as if with a clean sheet

•Incremental – take history and change, either your own or someone else's

Assumptions

•With experience (historical evidence or personal experience) the accuracy of assumptions increases•The closer to the present the more accurate the assumption•Need to be reasonable and need to be robust when questioned

Revenue

•Hard to predict•Incremental if history•Look at what others are doing•Research and back up what you believe

Income expectation

Absolutely need Require

Have in hand Need to get

Nice to have

Funder What for

Have capability/ resources

AHow much

BLikelihood %

C = A x BExpectation

A

B

C

Total Value

© Red Ochre 2016

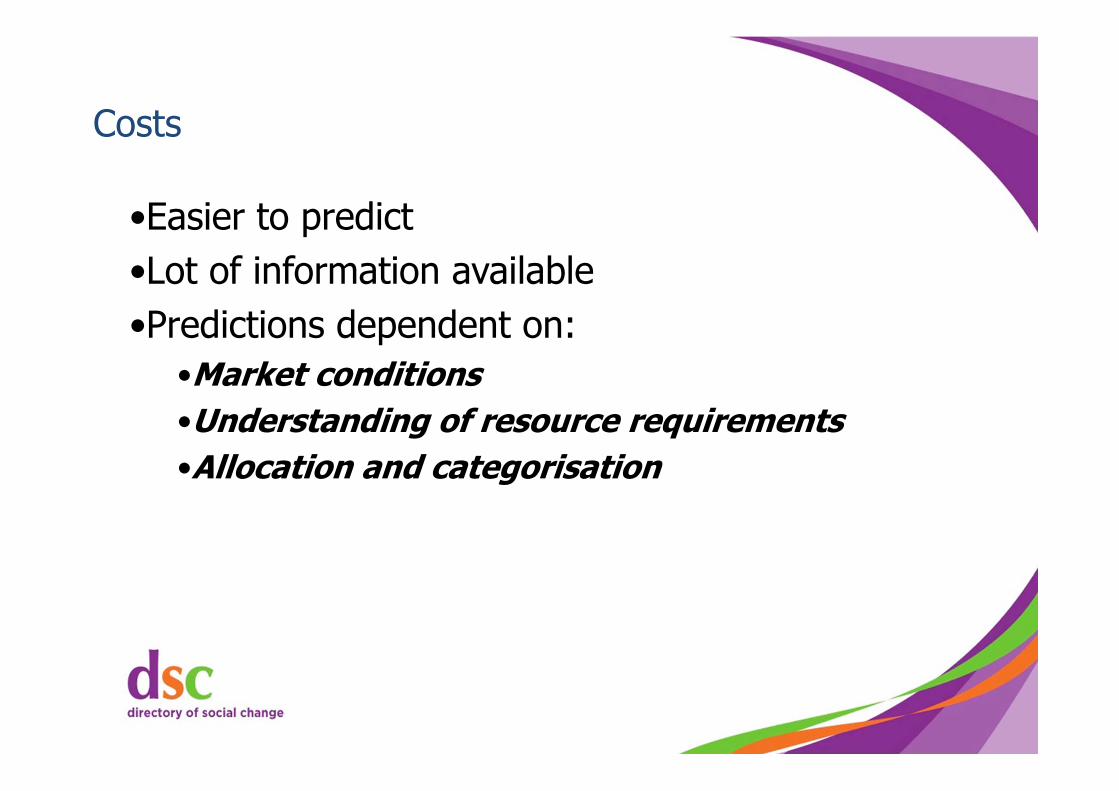

Costs

•Easier to predict•Lot of information available•Predictions dependent on:

•Market conditions•Understanding of resource requirements•Allocation and categorisation

Other considerations

•What is controllable•What is uncontrollable•Phasing of costs e.g. utilities•Spikes in resources•Understanding how to cut back if predictions slow, late or wrong

Types of Cost

•Variable costs•These are costs that change with activity, so that each time something is done there is a cost associated with it

•Fixed costs•These are costs that are incurred even where there is no activity

Types of Cost

•Project costs•Can these be regarded as being variable? They are activity related but also include an element of fixed costs

•Core costs•These could be seen to be fixed, yet also include some variable element

Types of Cost

•Understanding costs ensures that you can:• Control the business• Get the pricing right• Measure your performance•Explain why you charge more or less if challenged to do so

Financial planning

FundingCash in

ExpenditureCash out

How?When?

DependenciesWho By?

Resources RequiredInitial plan

Hypothetical

Reality check

Resources RequiredWorking plan

Plan “B”

© Red Ochre 2016

Budgets

•Budgets are tactical tools•What have you planned to deliver in the next 12 months•What resources do you have, what more do you need to get in•How are you going to deliver the plan•How are you going to monitor progress•What actions will come about as a result of the monitoring & reporting

Budgetary processStrategic Plan

Set GoalsOutcomes/ Outputs Identify

Portfolio of

Initiatives

Design Delivery

ProgrammeBusiness Plan

Quantify Resource

Requirement(Budget)

Monitor Progress

Reports

Compare actual to budget

Decide on action

Change strategy?

© Red Ochre 2016

Variance

•The difference between budgets and historical information for the same period is called a variance•Variances are useful management tools as they highlight areas where assumptions are incorrect and areas where there is potential for improvement

Reasons for inaccuracies

•Inadequate information•Circumstances beyond your control

•Staff departures•Grant cut backs•Funder default•Natural disasters