financial accounting - test bank...

TRANSCRIPT

INSTRUCTOR’S MANUAL

Richard Michalski

FINANCIAL ACCOUNTING Canadian Edition

Jeffrey Waybright Spokane Community College

Liang-Hsuan Chen University of Toronto Scarborough

Rhonda Pyper University of Ottawa

Toronto

ISBN: 978-0-13-261030-8

Copyright © 2013 Pearson Canada Inc. All rights reserved. This work is protected by Canadian copyright laws and is provided solely for the use of instructors in teaching their courses and assessing student learning. Dissemination or sale of any part of this work

(including on the Internet) will destroy the integrity of the work and is not permitted. The copyright holder grants permission to instructors who have adopted Financial Accounting, Canadian Edition, by Jeffrey

Waybright, Liang-Hsuan Chen, and Rhonda Pyper, to post this material online only if the use of the website is restricted by access codes to students in the instructor’s class that is using the textbook and provided the

reproduced material bears this copyright notice.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Copyright © 2013 Pearson Canada Inc.

Table of Contents

Introduction to the Instructor’s Manual ............................................................................. iii

Sample 10-Week Syllabus ................................................................................................. iv

Sample 16-Week Syllabus ............................................................................................... viii

Tips for Taking Your Course from Traditional to Hybrid, Blended, or Online .............. xiii

Student Handout (Tips on How to Get an A in This Class)............................................. xvi

Chapter 1: Business, Accounting, and You .........................................................................1

Chapter 2: Analyzing and Recording Business Transactions ............................................25

Chapter 3: Adjusting and Closing Entries .........................................................................44

Chapter 4: Ethics, Internal Control, and Cash ...................................................................63

Chapter 5: Accounting for a Merchandising Business ......................................................83

Chapter 6: Inventory ........................................................................................................103

Chapter 7: Sales and Receivables ....................................................................................122

Chapter 8: Long-Term Assets..........................................................................................143

Chapter 9: Current Liabilities and Long-Term Debt .......................................................170

Chapter 10: Corporations: Share Capital and Retained Earnings....................................193 Chapter 11: The Cash Flow Statement ............................................................................214

Chapter 12: Financial Statement Analysis.......................................................................230

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Copyright © 2013 Pearson Canada Inc. iii

Introduction to the Instructor’s Manual

Welcome to the Instructor’s Manual for Waybright, Chen, Pyper, Financial Accounting, Canadian Edition. This brief guide will help you use these resources to utilize your time most effectively. This product contains, for each chapter:

1) A Chapter Overview, which includes:

Chapter Outline

Learning Objectives

Key Terms

2) A Lecture Outline, which includes, for each major chapter topic:

Canadian Financial Accounting Learning Outcomes

Related Learning Objectives

Related PowerPoint slides (including comments pertaining to each slide)

Teaching Tips (examples, analogies, discussion questions, suggested topic emphasis, etc.)

3) A Student Summary Handout (reflecting all major chapter topics and sub-topics) 4) An Assignment Grid for each chapter’s Short Exercises, Exercises, Problems,

Continuing Exercise, Continuing Problem, and Comprehensive Problem (as applicable), indicating the:

subject matter

related Learning Objective(s)

suggested completion time

level of difficulty

5) A Chapter Quiz (including solutions) NOTE: The Instructor’s Manual is designed to be used in conjunction with the related PowerPoint slides for each chapter.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Copyright © 2013 Pearson Canada Inc. iv

TITLE OF SCHOOL

DEPARTMENT OF BUSINESS & MANAGEMENT

PRINCIPLES OF ACCOUNTING

Winter Quarter 2013 Instructor: Office: Office Hours: Office Phone: E-Mail: Required Materials: Text – Financial Accounting by Waybright, Chen, Pyper Other - MyAccountingLab online access (this is packaged with the text at the bookstore or may also

be purchased directly from the publisher at www.myaccountinglab.com). Your course ID number for the class is:

Course Description and Student Outcomes:

Students will learn basic principles of accounting theory and practice currently used in accounting information systems. Topics covered include accounting for service and merchandising business enterprises. The processes of analyzing, journalizing, and posting are covered in depth, as well as adjusting accounts, preparing financial statements, and completing the accounting cycle. Deferrals, accruals, accounting for merchandise inventory, ethics and internal controls, cash, and receivables are also covered.

Students will be able to:

1. Communicate in the basic language of business (accounting); understand and apply International Financial Reporting Standards (IFRS) and the important ethical issues surrounding financial reporting.

2. Explain the purpose and importance of accounting information.

3. Construct a chart of accounts. Evaluate, analyze, and enter business transactions in the accounting equation.

4. Journalize and post transactions and prepare a trial balance.

5. Make adjusting and closing entries and prepare financial statements in good form.

6. Record transactions for merchandising activities using the perpetual inventory system, and prepare multi-step income statements and classified balance sheets.

7. Evaluate, cost, and differentiate between the FIFO, Average Cost, and Specific Identification inventory methods and articulate the financial statement effects of the different methods under different economic conditions.

8. Understand an internal control system and discuss business ethics.

9. Prepare bank reconciliations and accurately record petty cash transactions.

10. Record transactions for accounts and notes receivable. Compare and contrast the two methods of estimating uncollectible accounts and prepare aging schedules.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Sample 10-Week Syllabus

Copyright © 2013 Pearson Canada Inc. v

ASSESSMENTS

All graded homework, quizzes and exams must be taken by the date and time scheduled. Make-ups will not be allowed without making prior arrangements. Documented medical emergencies or school-related business will be handled on a case-by-case basis.

You are not allowed to utilize your textbook or notes during the chapter quizzes, the mid-term, or the final exam. (If you need them, then you have not prepared well enough.) You should also not have assistance from any other person while taking quizzes or tests.

This course is designed to achieve the learning outcomes listed above. Performance in this class depends upon the accomplishment of these outcomes. Students are graded on demonstration of knowledge or competence rather than for effort alone. Students may use calculators on exams provided the calculator does not have the capability of storing text in memory. Use of calculators capable of storing text will be considered an act of academic dishonesty.

GRADING POLICY

Item Possible Graded Homework 20% Case Studies, etc. 10% Chapter Quizzes 25% Mid-Term Exam (Chapters 1, 2, 3, 5, 6) 20% Final Exam (Chapters 1–8) 25%

Total 100%

Note Note Note You will not receive a grade higher than a 1.9 unless you score a 70% or higher on the comprehensive final exam regardless of your total points earned.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Sample 10-Week Syllabus

Copyright © 2013 Pearson Canada Inc. vi

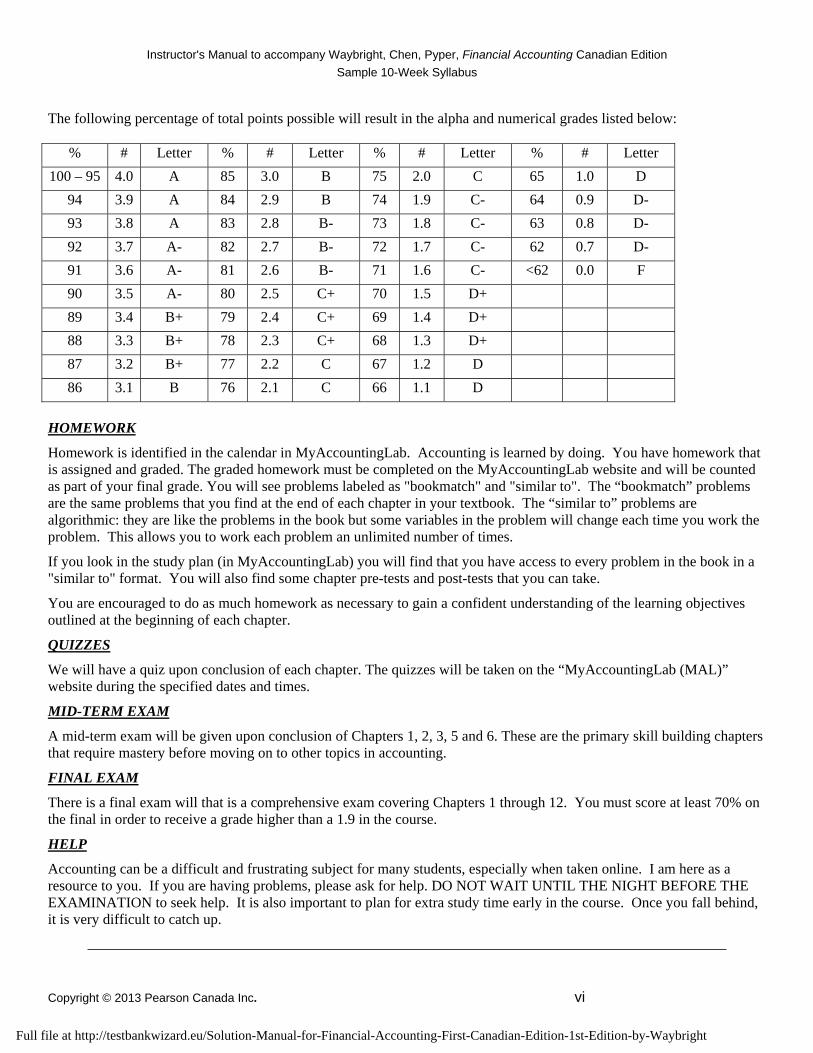

The following percentage of total points possible will result in the alpha and numerical grades listed below:

% # Letter % # Letter % # Letter % # Letter

100 – 95 4.0 A 85 3.0 B 75 2.0 C 65 1.0 D

94 3.9 A 84 2.9 B 74 1.9 C- 64 0.9 D-

93 3.8 A 83 2.8 B- 73 1.8 C- 63 0.8 D-

92 3.7 A- 82 2.7 B- 72 1.7 C- 62 0.7 D-

91 3.6 A- 81 2.6 B- 71 1.6 C- <62 0.0 F

90 3.5 A- 80 2.5 C+ 70 1.5 D+

89 3.4 B+ 79 2.4 C+ 69 1.4 D+

88 3.3 B+ 78 2.3 C+ 68 1.3 D+

87 3.2 B+ 77 2.2 C 67 1.2 D

86 3.1 B 76 2.1 C 66 1.1 D

HOMEWORK

Homework is identified in the calendar in MyAccountingLab. Accounting is learned by doing. You have homework that is assigned and graded. The graded homework must be completed on the MyAccountingLab website and will be counted as part of your final grade. You will see problems labeled as "bookmatch" and "similar to". The “bookmatch” problems are the same problems that you find at the end of each chapter in your textbook. The “similar to” problems are algorithmic: they are like the problems in the book but some variables in the problem will change each time you work the problem. This allows you to work each problem an unlimited number of times.

If you look in the study plan (in MyAccountingLab) you will find that you have access to every problem in the book in a "similar to" format. You will also find some chapter pre-tests and post-tests that you can take.

You are encouraged to do as much homework as necessary to gain a confident understanding of the learning objectives outlined at the beginning of each chapter.

QUIZZES

We will have a quiz upon conclusion of each chapter. The quizzes will be taken on the “MyAccountingLab (MAL)” website during the specified dates and times.

MID-TERM EXAM

A mid-term exam will be given upon conclusion of Chapters 1, 2, 3, 5 and 6. These are the primary skill building chapters that require mastery before moving on to other topics in accounting.

FINAL EXAM

There is a final exam will that is a comprehensive exam covering Chapters 1 through 12. You must score at least 70% on the final in order to receive a grade higher than a 1.9 in the course.

HELP

Accounting can be a difficult and frustrating subject for many students, especially when taken online. I am here as a resource to you. If you are having problems, please ask for help. DO NOT WAIT UNTIL THE NIGHT BEFORE THE EXAMINATION to seek help. It is also important to plan for extra study time early in the course. Once you fall behind, it is very difficult to catch up.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Sample 10-Week Syllabus

Copyright © 2013 Pearson Canada Inc. vii

CLASS GUIDELINES

No calculators capable of storing text are allowed during the final exam. You may not use your cell phone as a calculator. I suggest purchasing a four-function calculator at the

bookstore. No head phones or ear buds (mp3 players) allowed during the final exam. Cheating will not be tolerated. Any student caught will receive a 0.0 grade for the quarter. Students who stop attending class, but do not officially withdraw, will receive a 0.0 grade.

SUBJECT TO CHANGE

Course Schedule

Session Date Topic Reading Assignment and Class Preparation

After Class Homework

Assignment* 1 Business, Accounting and

You Chapter 1; S1-3, S1-11, S1-14, E1-5A, E1-9A

S1-1, E1-6A, E1-8A, P1-1A

2 Analyzing and Recording Business Transactions

Chapter 2; S2-12, S2-13, E2-2A, E2-6A

S2-5, E2-3A, P2-1A, P2-2A

3 Adjusting and Closing Entries Chapter 3; S3-2, S3-8, S3-10, E3-1A, E3-4A

S3-12, E3-5B, E3-7B, P3-6A

4 Accounting for a Merchandising Business

Chapter 5; – S5-2, S5-9, S5-10, E5-3A, E5-9A

S5-1, E5-4A, P5-7A, P5-2A

5 Inventory Chapter 6; – S6-7, S6-8, S6-9, E6-3A, E6-5A

E6-1A, S6-11, P6-3, P6-6A

Mid-Term

6 Ethics, Internal Control, and Cash Sales and Receivables

Chapter 4; S4-1, S4-2, S4-5, S4-6, S4-7 Chapter 7; S7-2, S7-8, S7-11, E7-3A

S4-2, S4-10, S4-11, S4-12 S7-5, E7-4B, P7-1A, E7-6A

7 Long-Term Assets Chapter 8; S8-4, S8-15, E8-1A, E8-7A

S8-16, E8-5A, P8-2A, P8-5A

8 Current Liabilities and Long-Term Debt Corporations: Share Capital and Retained Earnings

Chapter 9; S9-9, S9-14, E9-1A, E9-3A, E9-7A Chapter 10; S10-6, E10-1A, E10-5A, E10-12A

S9-3, S9-4, P9-1A, E9-4B S10-1, E10-4B, E10-6A, P10-7A

9 The Cash Flow Statement

Chapter 11; S11-4, S11-12, E11-2A, E11-4A

S11-2, S11-3, S11-6, P11-11B, P11-3B

10 Financial Statement Analysis Chapter 12; S12-2, S12-3, S12-6, E12-1A

S12-1, P12-2A, P12-4A

Final Exam

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Copyright © 2013 Pearson Canada Inc. viii

TITLE OF SCHOOL

DEPARTMENT OF BUSINESS & MANAGEMENT

PRINCIPLES OF ACCOUNTING

Spring Semester 2013 Instructor: Office: Office Hours: Office Phone: E-Mail: Required Materials: Text – Financial Accounting by Waybright, Chen, Pyper Other - MyAccountingLab online access (this is packaged with the text at the bookstore or may also

be purchased directly from the publisher at www.myaccountinglab.com). Your course ID number for the class is:

Course Description and Student Outcomes:

Students will learn the basic principles of accounting theory and practice currently used in accounting information systems. Topics covered include accounting for service and merchandising business enterprises. In the first part of the course the processes of analyzing, journalizing, and posting are covered in depth. Next, accounting for deferrals, accruals, adjusting accounts, preparing financial statements, and completing the accounting cycle is covered. Accounting for merchandising businesses, inventory, ethics, and internal controls are also covered. The second half of the course is designed to provide the student with a more in-depth study of specific topics including cash and receivables, property, plant and equipment (fixed assets), natural resources, intangible assets, current and long-term liabilities, and accounting for corporations. The capstone piece to this course is the addition of the statement of cash flows and financial statement analysis. Upon successful completion of this course you will have the necessary competence and skills to move on to more intermediate and advanced topics in financial accounting.

Students will be able to:

1. Communicate in the basic language of business (accounting); understand and apply International Financial Reporting Standards (IFRS) and the important ethical issues surrounding financial reporting.

2. Explain the purpose and importance of accounting information.

3. Construct a chart of accounts. Evaluate, analyze, and enter business transactions in the accounting equation.

4. Journalize and post transactions and prepare a trial balance.

5. Make adjusting and closing entries and prepare financial statements in good form.

6. Record transactions for merchandising activities using the perpetual inventory system, and prepare multi-step income statements and classified balance sheets.

7. Evaluate, cost, and differentiate between the FIFO, Average Cost, and Specific Identification inventory methods and articulate the financial statement effects of the different methods under different economic conditions.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Sample 16-Week Syllabus

Copyright © 2013 Pearson Canada Inc. ix

8. Understand an internal control system and discuss business ethics.

9. Prepare bank reconciliations and accurately record petty cash transactions.

10. Record transactions for accounts and notes receivable. Compare and contrast the two methods of estimating uncollectible accounts and prepare aging schedules.

11. Record depreciation for plant assets, depletion of natural resources, and amortization of intangible assets. You will analyze and select between Straight Line, Declining Balance, and Units of Production methods of depreciation and understand the tax and financial reporting ramifications of each method.

12. Establish the initial cost of assets, analyze and journalize additional expenditures related to fixed assets, and dispose of fixed assets.

13. Characterize and account for current liabilities, such as accounts payable, short-term notes payable, sales tax payable, and contingent liabilities.

14. Analyze and account for long-term liabilities to include issuing bonds at both premiums and discounts, and make adjusting entries for interest expense using the straight-line method of amortization.

15. Identify the characteristics of a corporation and be able to analyze and account for corporate transactions, including shares (common and preferred), payment of dividends, and purchase of treasury shares.

16. Analyze and account for the formation of a corporation; prepare a classified balance sheet for a corporation and journalize transactions associated with corporations to include sale of shres, declaration and payments or distribution of dividends, and treasury share transactions.

17. Prepare cash flow statements using the indirect and direct method. Distinguish among operating, investing, and financing cash flows.

18. Evaluate the performance of a company. This will be accomplished by using standard analysis tools such as vertical and horizontal analysis, common-size financial statements, and standard financial ratios.

ASSESSMENTS

All graded homework, quizzes and exams must be taken by the date and time scheduled. Make-ups will not be allowed without making prior arrangements. Documented medical emergencies or school-related business will be handled on a case-by-case basis.

You are not allowed to utilize your textbook or notes during the chapter quizzes, the mid-term, or the final exam. (If you need them, then you have not prepared well enough.) You should also not have assistance from any other person while taking quizzes or tests.

This course is designed to achieve the learning outcomes listed above. Performance in this class depends upon the accomplishment of these outcomes. Students are graded on demonstration of knowledge or competence rather than for effort alone. Students may use calculators on exams provided the calculator does not have the capability of storing text in memory. Use of calculators capable of storing text will be considered an act of academic dishonesty.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Sample 16-Week Syllabus

Copyright © 2013 Pearson Canada Inc. x

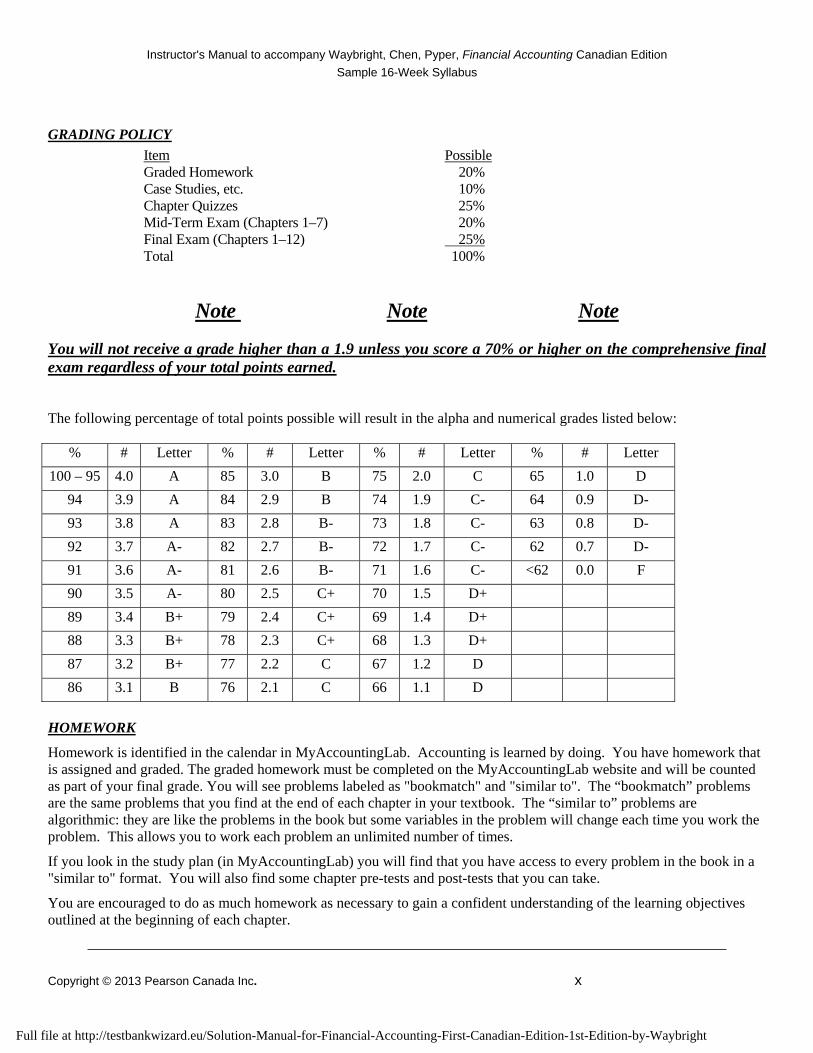

GRADING POLICY

Item Possible Graded Homework 20% Case Studies, etc. 10% Chapter Quizzes 25% Mid-Term Exam (Chapters 1–7) 20% Final Exam (Chapters 1–12) 25%

Total 100%

Note Note Note You will not receive a grade higher than a 1.9 unless you score a 70% or higher on the comprehensive final exam regardless of your total points earned. The following percentage of total points possible will result in the alpha and numerical grades listed below:

% # Letter % # Letter % # Letter % # Letter

100 – 95 4.0 A 85 3.0 B 75 2.0 C 65 1.0 D

94 3.9 A 84 2.9 B 74 1.9 C- 64 0.9 D-

93 3.8 A 83 2.8 B- 73 1.8 C- 63 0.8 D-

92 3.7 A- 82 2.7 B- 72 1.7 C- 62 0.7 D-

91 3.6 A- 81 2.6 B- 71 1.6 C- <62 0.0 F

90 3.5 A- 80 2.5 C+ 70 1.5 D+

89 3.4 B+ 79 2.4 C+ 69 1.4 D+

88 3.3 B+ 78 2.3 C+ 68 1.3 D+

87 3.2 B+ 77 2.2 C 67 1.2 D

86 3.1 B 76 2.1 C 66 1.1 D

HOMEWORK

Homework is identified in the calendar in MyAccountingLab. Accounting is learned by doing. You have homework that is assigned and graded. The graded homework must be completed on the MyAccountingLab website and will be counted as part of your final grade. You will see problems labeled as "bookmatch" and "similar to". The “bookmatch” problems are the same problems that you find at the end of each chapter in your textbook. The “similar to” problems are algorithmic: they are like the problems in the book but some variables in the problem will change each time you work the problem. This allows you to work each problem an unlimited number of times.

If you look in the study plan (in MyAccountingLab) you will find that you have access to every problem in the book in a "similar to" format. You will also find some chapter pre-tests and post-tests that you can take.

You are encouraged to do as much homework as necessary to gain a confident understanding of the learning objectives outlined at the beginning of each chapter.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Sample 16-Week Syllabus

Copyright © 2013 Pearson Canada Inc. xi

QUIZZES

We will have a quiz upon conclusion of each chapter. The quizzes will be taken on the “MyAccountingLab (MAL)” website during the specified dates and times.

MID-TERM EXAM

A mid-term exam will be given upon conclusion of Chapters 1 through 7. These are the primary skill-building chapters that require mastery before moving on to other topics in accounting.

FINAL EXAM

There is a final exam will that is a comprehensive exam covering Chapters 1 through 12. You must score at least 70% on the final in order to receive a grade higher than a 1.9 in the course.

HELP

Accounting can be a difficult and frustrating subject for many students especially when taken online. I am here as a resource to you. If you are having problems, please ask for help. DO NOT WAIT UNTIL THE NIGHT BEFORE THE EXAMINATION to seek help. It is also important to plan for extra study time early in the course. Once you fall behind, it is very difficult to catch up.

CLASS GUIDELINES

No calculators capable of storing text are allowed during the final exam. You may not use your cell phone as a calculator. I suggest purchasing a four-function calculator at the

bookstore. No head phones or ear buds (mp3 players) allowed during the final exam. Cheating will not be tolerated. Any student caught will receive a 0.0 grade for the quarter. Students who stop attending class, but do not officially withdraw, will receive a 0.0 grade.

SUBJECT TO CHANGE

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Sample 16-Week Syllabus

Copyright © 2013 Pearson Canada Inc. xii

Session Date Topic Reading Assignment

and Class PreparationAfter Class Homework

Assignment* 1 Business, Accounting and

You Chapter 1; S1-3, S1-11, S1-14, E1-5A, E1-9A

S1-1, E1-6A, E1-8A, P1-1A

2 Analyzing and Recording Business Transactions

Chapter 2; S2-12, S2-13, E2-2A, E2-6A

S2-5, E2-3A, P2-1A, P2-2A

3 Adjusting and Closing Entries Chapter 3; S3-2, S3-8, S3-10, E3-1A, E3-4A

S3-12, E3-5B, E3-7B, P3-6A

4 Accounting for a Merchandising Business

Chapter 5; – S5-2, S5-9, S5-10, E5-3A, E5-9A

S5-1, E5-4A, P5-7A, P5-2A

5 Inventory Chapter 6; – S6-7, S6-8, S6-9, E6-3A, E6-5A

E6-1A, S6-11, P6-3, P6-6A

6 Ethics, Internal Control, and Cash

Chapter 4; S4-1, S4-2, S4-5, S4-6, S4-7

S4-2, S4-10, S4-11, S4-12

7 Sales and Receivables

Chapter 7; S7-2, S7-8, S7-11, E7-3A

S7-5, E7-4B, P7-1A, E7-6A

8 Mid-Term Examination 9 Long-Term Assets Chapter 8; S8-4, S8-15,

E8-1A, E8-7A

S8-16, E8-5A, P8-2A, P8-5A

9 Current Liabilities and Long-Term Debt

Chapter 9; S9-9, S9-14, E9-1A, E9-3A, E9-7A

S9-3, S9-4, P9-1A, E9-4B

10 Current Liabilities and Long-Term Debt

Chapter 9: S9-1, S9-2, E9-2A, E9-6A

E9-1B, P9-1B, P9-2B

11 Corporations: Paid-In Capital and Retained Earnings

Chapter 10; S10-6, E10-1A, E10-5A, E10-12A

S10-1, E10-4B, E10-

6A, P10-7A

12 Corporations: Share Capital and Retained Earnings

Chapter 10: E10-1B, E10-2B

P10-5B, P10-6B, P10-7B

13 The Cash Flow Statement

Chapter 11; S11-4, S11-12, E11-2A, E11-4A

S11-2, S11-3, S11-6, P11-11B, P11-3B

14 Financial Statement Analysis Chapter 12; S12-2, S12-3, S12-6, E12-1A

S12-1, P12-2A, P12-4A

15 Financial Statement Analysis Chapter 12: E12-2B, E12-4B, E12-5B

E12-6B, P12-3A, P12-4B, P12-5B

16 Final Examination

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Copyright © 2013 Pearson Canada Inc. xiii

Tips for Taking Your Course from Traditional to Hybrid, Blended, or Online

1. Don’t try to take the “entire” course online in one semester. Decide on a two-semester strategy for implementation, implementing graded online homework FIRST. By only implementing the homework portion of the online solution, you don’t overwhelm yourself with having to learn every piece of the online component in one semester, regardless of whether it is MyAccountingLab or some other solution. Additionally, this allows you the flexibility to add other graded assignments later that first semester, if you choose.

2. Define homework by chapter in your syllabi, rather than identifying specific exercises or problems. During the first semester, as you and your students get accustomed to the online resources, you may need to be more flexible. Further, this gets your students used to looking “online” for their assignments.

3. Schedule one day in class in a computer lab (or some class time, if you can’t get into a computer lab), to demonstrate. This allows you to gain a “captive audience” so that you can show the class some of the resources you want them to use. It also allows you to highlight some of the resources that they may find useful in their learning.

I use this time in conjunction with the VARK analysis (I require students to complete this)—http://www.vark-learn.com/english/page.asp?p=questionnaire.

Then I can also point out which online tools will help specific learning styles for the students. Also, it gives those visual and kinesthetic learners a chance to “see” the tools.

4. Use MyAccountingLab’s static/book match problems to demonstrate in class problems or exercises. This is a good way to not only save you time in setting up in class assignments, but it also demonstrates to the student the completion ease of the MyAccountingLab homework solution. I set up a “static” course that has all the book match problems in it and use that course for demonstrating this in class. Remember, you have 5 book match/static questions (A, B, C, D, and E) with versions A and B being in your student’s text in the end-of-chapter material.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Sample 16-Week Syllabus

Copyright © 2013 Pearson Canada Inc. xiv

5. Same as Item 4, except using only the Excel spreadsheets. Have the students print out the Excel or PDF worksheets for book match/static questions before covering the material in class. Again, this establishes the online centre as the “go to” place for students to glean information.

6. The first assignments I give after demonstrating the online login/registration are submitted via their online e-mail account. For this, I use the e-mail students option from the gradebook. I submit their first assignment via e-mail to try in myaccountinglab.com. This is a “bonus” points only assignment; the students are eager to try online tools (no penalty—only bonus point reward) and it gets them registered more quickly in myaccountinglab.com. I suggest using something like the built-in pre-test chapter questions.

7. Have students give each other feedback. One of the problems with teaching online is that giving feedback to all of your students all the time can quickly get out of control. The way to deal with this is to have students give the initial drafts of their papers to other students for feedback. You give a grade to the feedback based on how helpful the original author finds it. Then you only have to review papers one time, and many of the problems should be worked out before you see them. (Contributed by Jas Bhangal, Chabot College.)

8. Set up discussion forums. You might, for example, ask a critical thinking question on one of the key chapter topics. Your students will have a certain amount of time to (1) post an answer to your question, and (2) post a response or comment on the answer of another student. You can offer extra credit for the “best” response.

Alternatively, you might ask students to answer one of the end-of-chapter or additional online questions/case problems within a set period of time. The first one to respond can get an extra credit point. The first student who “adds value” to the answer can also get an extra point.

(Contributed by Jas Bhangal, Chabot College.)

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Sample 16-Week Syllabus

Copyright © 2013 Pearson Canada Inc. xv

9. Set up online group competitions. Divide your online class into teams. Assign a problem or a current event situation (something regarding current economic problems, an ethical dilemma, etc…) for which students will need to conduct research, answer your questions, and post an analytical response. Assign extra credit points for the first complete response, a few less for the second response, etc.

You might also ask each team to develop a scenario, a list of questions, and responses for an additional class project. Reward those teams who submit activities that you deem suitable for use in the course.

NOTE: This suggestion could be used in class as well.

(Contributed by Lydia R. Botsford, DeAnza College.)

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Copyright © 2013 Pearson Canada Inc. xvi

STUDENT HANDOUT

Tips on how to use the resources and online tools to get an A in this class:

READ the chapter. Yes, I know it’s hard, but it’s an important 30 minutes to an hour spent in learning this material.

WATCH the Demo Docs. Right after reading, view the interactive multi-media demo docs for the chapter.

PRACTISE homework online. Sure it makes sense when your professor goes over the assignment—they’ve been doing this for a long time. There is no substitute for doing problems/exercises. That’s how you learn accounting. And the online homework assignments are algorithmic, so they are already set up for you to practise problems until you “get it.”

STUDY in groups. Creating study groups is a great way to expand your learning. These groups will not only increase your number of resources to go to for help, but they also create a sort of accountability that will help keep you on track for success.

Learn WHY as well as HOW. Sure the “how” to do it is a big part of accounting, but if you can learn why you are doing a particular accounting task, it will be much easier to perform the task.

RELATE topics to your personal life or job. The best way to ensure you understand a topic is to apply it to your life or job.

ASK questions. When online, use the “Ask my instructor” button to ask specific homework questions at the point you have them. Also, ask questions while in class. Don’t assume you are the only one who doesn’t understand. Your questions help you and other students learn.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Copyright © 2013 Pearson Canada Inc. 1

Chapter 1 Business, Accounting, and You

I. Chapter Overview

The chapter begins with a description of the accounting process and an explanation of the essential role of accounting in business. Accounting is credited with teaching “the language of business.” The text discusses how accounting information is used to monitor operations and how the financial information is needed by various users—businesses, investors, creditors, suppliers, customers, regulatory agencies, and taxing authorities. How to interpret and use the financial statements is illustrated. Ethics is defined, and the importance of ethical business behavior is discussed.

In the next section of the chapter, three types of businesses are introduced:

service, merchandising, and manufacturing. The choices for the form of business organizations are explained. The advantages and disadvantages of three forms of business organization, namely sole proprietorship, partnership, and corporation. The text discusses the accounting principles and concepts that govern financial accounting.

The accounting equation—Assets = Liabilities + Shareholders’ Equity—is

introduced, and each element of the equation is defined. A variety of transactions are analyzed, and the affect of the transactions on the accounting equation is demonstrated. The financial statements—income statement, statement of changes in equity, statement of financial position, and cash flow statement—are introduced.

A Demo Doc problem allows students to record the effect of transactions on the

accounting equation and prepare financial statements. Decision Guidelines are presented to assist the student in understanding the factors that should be considered when opening a business.

A. Chapter Outline

Why Study Accounting?

What Is Accounting?

How Are Businesses Organized?

What Are the Career Opportunities in Accounting-Related Fields?

What Accounting Principles and Concepts Govern the Field of Accounting?

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 2

How Is the Accounting Equation Used to Record Business Transactions?

What Do Financial Statements Report, and How Are They Prepared?

Focus on Users

B. Learning Objectives (p. 22)

After studying Chapter 1, your students should be able to:

1. Describe the major types of business organizations

2. Identify career opportunities in accounting and related fields

3. Explain the key accounting principles and conceptual framework

4. Analyze transactions using the basic accounting equation

5. Understand and be able to prepare basic financial statements

C. Key Terms

Accounts payable

Accounts receivable

Accounting

Accounting Standards for Private Enterprises (ASPE)

Accrual basis accounting

Assets

Balance sheet

Businesses

Canadian Accounting Standards for Private Enterprises

Common shares

Comparability

Conceptual framework

Corporation

Cost–benefit

Current cost

Dividends

Entity

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 3

Ethics

Expenses

Financial accounting

Financial statements

Fundamental accounting equation

Going-concern principle

Historical cost

Income statement

International Financial Reporting Standards (IFRS)

Liabilities

Managerial accounting

Manufacturing business

Materiality

Merchandising business

Net income

Net loss

Note payable

On account

Owner(s)’s capital

Partnership

Prepaid expenses

Present value

Profit

Realizable value

Relevance

Reliability

Retail business

Retained earnings

Revenue

Service business

Share capital

Shareholder

Shareholders’ equity

Sole proprietorship

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 4

Cash flow statement

Statement of changes in equity

Statement of comprehensive income

Statement of financial position

Third party

Timeliness

Transaction

Understandability

Wholesale business

Withdrawals

II. Lecture Outline 1. Why Study Accounting? (pp. 4-6) 1.1 Canadian Financial Accounting Learning Outcome:

A-1 Identify and apply accounting concepts and principles found in the Conceptual Framework

1.2 Learning Objective:

Explain the key accounting principles and conceptual framework.

1.3 Related PowerPoint slides: 1-3

Slide 1-3

Comments:

This tells us why we study accounting in the first place.

1.4 Teaching Tips:

To promote discussion, ask students if they have heard of the various accounting scandals that have taken place in the past decade

Emphasize how accounting focuses the importance of ethical behaviour,

using high profile cases such and Enron and Nortel as examples

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 5

2. What Is Accounting? (pp. 6-7) 1.1 Canadian Financial Accounting Learning Outcome:

A-1 Identify and apply accounting concepts and principles found in the Conceptual Framework

1.2 Learning Objective:

Explain the key accounting principles and conceptual framework.

1.3 Related PowerPoint slides: 1-4

Slide 1-4

Comments:

A general slide outlining what financial accounting is all about.

1.4 Teaching Tips:

Emphasize that financial statements are primarily directed at external users who need to make decisions about whether to invest in the company, lend it money, etc.

You may want to ask students if they have ever applied for a loan, and if

so, what the lender wanted to know about them; among the items will likely be: 1) How much did you make? 2) What do you own? 3) What do you owe? Indicate that financial statements like the income statement and the balance sheet answer these very questions about a company as opposed to an individual.

3. How Are Businesses Organized? (pp. 7-9) 1.1 Canadian Financial Accounting Learning Outcome:

A-1 Identify and apply accounting concepts and principles found in the Conceptual Framework

1.2 Learning Objective:

Describe the major types of business organizations.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 6

1.3 Related PowerPoint slides: 1-5 to 1-8

Slide 1-5

Comments:

The three types of businesses include a service business, a merchandising business, and a manufacturing business.

• A service business provides services to its customers. In other words, what it sells is time. Common types of service businesses are law firms, accounting firms, physical therapy offices, painting companies, automotive repair shops, etc. • A merchandise business sells physical goods or products to its customers. Common types of merchandise businesses are grocery stores, automobile dealerships, sporting goods stores, etc. A merchandise business may be either a wholesale business or a retail business. • Manufacturing businesses produce the physical goods that they sell to their customers. Common types of manufacturing businesses are automobile manufacturers, the makers of clothing, soft drink manufacturers, etc.

Slide 1-6 Comments:

A business can be organized as a sole proprietorship, partnership, or as a

corporation. A sole proprietorship is a business entity that has one owner. For legal purposes and for tax purposes, the business and the owner are

considered the same.

A partnership is very similar to a sole proprietorship except that it has two or more owners. For legal purposes, the owners (partners) and the business are considered the same.

A corporation differs from a sole proprietorship or a partnership in that it is

a separate legal entity from the owners. This legal separation is very attractive to the business owners because it limits their personal liability to what they have invested in the corporation.

Slide 1-7 Comments:

This exhibit summarizes the key attributes of the three types of business structures.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 7

Slide 1-8 Comments:

If the owners decide to put personal assets into the business, those assets are now considered to be the assets of the business.

1.4 Teaching Tips:

Emphasize that we spend a lot of time talking about accounting for manufacturing companies because they typically have products to sell, which allows us to talk about concepts like inventory and cost of goods sold which do not apply to service businesses

Emphasize that the biggest difference between corporations and sole

proprietorships/partnerships is the equity section of the balance sheet

Emphasize that we spend much of our time talking about public companies i.e. those that issue shares because that enables us to consider issues relating to contributed capital

Emphasize that the personal financial affairs of the owners of the

company i.e. shareholders need to be kept separate from those of the business that they have invested in

4. What Are the Career Opportunities in Accounting-Related Fields? (pp. 10-11) 1.1 Canadian Financial Accounting Learning Outcome:

A-1 Identify and apply accounting concepts and principles found in the Conceptual Framework

1.2 Learning Objective:

Identify career opportunities in accounting and related fields.

1.3 Related PowerPoint slides: 1-9

Slide 1-9

Comments:

This exhibit summarizes the career opportunities. Emphasize that there are two distinct types of accounting (financial, management) that could lead to very different career paths.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 8

1.4 Teaching Tips:

Emphasize that there are two distinct types of accounting (financial,

management) that could lead to very different career paths 6. What Accounting Principles and Concepts Govern the Field of

Accounting? (pp. 11-14) 1.1 Canadian Financial Accounting Learning Outcome(s):

A-1 Identify and apply accounting concepts and principles found in the Conceptual Framework A-18 Compare and contrast IFRS and ASPE

1.2 Learning Objective:

Explain the key accounting principles and conceptual framework.

1.3 Related PowerPoint slides: 1-10 to 1-16

Slide 1-10 Comments:

Accounting standards help to facilitate comparison across different

companies yet they try to accommodate the specific accounting needs of very different types of businesses. IFRS has not been adopted by the United States as yet, which poses challenges to the quest for harmonized accounting standards around the world.

Slide 1-11 Comments:

Financial statements involve elements (the set of them), recognition (the act of including a given item somewhere in the financial statements), measurement (converting economic events into numbers), and reporting (communicating to users through financial statements)

Slide 1-12

Comments:

Accounting information should be useful for evaluating the past and predicting the future. Usefulness is the most important characteristic of

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 9

accounting information. To be useful, information must be relevant, reliable, comparable, and understandable.

Relevant

Must be significant enough to influence business decisions. Should help confirm or correct users’ expectations. Must be timely to be relevant. Can be used to evaluate the past and predict the future.

Reliable

Can depend on it and can verify its accuracy. Information must be completely independent of the person reporting it. Must be a faithful representation of what it intends to convey Truthfulness of the information can be verified.

Comparability

Investors can compare financial information between two similar companies.

Understandable

A person with a reasonable knowledge of business should be able to understand them.

Slide 1-13

Comments:

Under IFRS, business may choose one of these four methods that best reflects their economic activities and reality. Revenue should be recognized when it is earned, which could be at time of production, invoicing, delivery, or cash collection. The full-disclosure principle means that the firm must disclose any circumstances and events that would make a difference to the users of the financial statements.

Slide 1-14

Comments:

Materiality refers to a given item’s impact on a firm’s overall financial operations. Cost benefit analysis involves weighing the cost of acquiring information against the benefit of its use for decision making. Information must be timely in a sense that it should be available to decision makers before it loses its ability to influence decisions.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 10

Slide 1-15

Comments:

The monetary unit assumption means that the items on the financial statements are measured in monetary units.

The economic entity assumption means that the firm’s financial records

and financial statements are completely separate from those of the firm’s owners.

The time period assumption means that the life of a business can be

divided into meaningful time periods for financial reporting.

The going concern assumption relates to the expectation that a company will stay in business for the foreseeable future.

Slide 1-16

Comments:

This exhibit brings together the various aspect of the conceptual framework in a diagram.

1.4 Teaching Tips:

Indicate that IFRS has not been adopted by the United States as yet, which poses challenges to the quest for harmonized accounting standards around the world

Emphasize that accounting standards help to facilitate comparison across

different companies yet they try to accommodate the specific accounting needs of very different types of businesses

Emphasize how the various aspects of the Conceptual Framework fit

together

Emphasize that the cost principle implies a tradeoff between objectivity and relevance; you may want to use the example of a business purchasing some land in Year 1 at $500,000, whose market value then rises to $1,000,000 by the end of Year 3, and then discuss what the students think the land amount should appear as on the Year 3 balance sheet, $500,000 or $1,000,000

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 11

7. How Is the Accounting Equation Used to Record Business

Transactions? (pp. 14-22) 1.1 Canadian Financial Accounting Learning Outcome:

A-3 Analyze and record transactions and their effects on the financial statements

1.2 Learning Objective:

Analyze transactions using the basic accounting equation.

1.3 Related PowerPoint slides: 1-17 to 1-20

Slide 1-17

Comments:

The accountant needs to keep track of information, so he or she can tell people how the company is performing. The accountant must keep track of two main things at the same time.

First, the accountant must track what the company owns that has value. In accounting, the things of value that the company owns are called assets.

In addition, the accountant must track the ownership rights to the assets.

In other words, if the business was to close its doors at any given time, who would have a right to the company assets?

Slide 1-18 Comments:

Accountants will record the effects of transactions in the accounting

equation. A transaction is any event that has a financial impact on the business. If

something changes either what the company has or who owns it, it must be recorded in the accounting equation.

Slide 1-19 Comments:

Before we start looking at how transactions affect the accounting

equation, let us take a closer look at the shareholders’ equity section of the equation. In order to provide more useful information to various

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 12

people, the shareholders’ equity section can be broken down into smaller subcategories:

1. Common shares is used to reflect shareholders’ equity, which is the

result of the owners of the business investing assets into the business.

2. Retained earnings is used to reflect shareholders’ equity, which is the

result of the business having earnings that have been retained in the business.

Slide 1-20

Comments:

The retained earnings subcategory can now be further broken down into smaller subcategories to help the accountant provide even better information. These subcategories and what they reflect are as follows:

• Revenues are used to reflect an increase in retained earnings, which is the result of the business providing goods and services.

• Expenses are used to reflect a decrease in retained earnings, which is the result of the business incurring costs related to providing goods and services.

• Dividends are used to reflect a decrease in retained earnings, which is the result of the owners receiving assets (usually cash) from the business.

1.4 Teaching Tips:

You may want to use some analogies to assist students in remembering the difference between an income Statement and a Balance Sheet e.g. whereas an Income Statement is like a video, a Balance Sheet is like a photograph; or, an Income Statement is like a tripometer in a car in two ways: they both keep track of something (kilometres, revenues, expenses) for a period of time and the balances of both are reset to zero at the end of the period; conversely, a Balance Sheet is like an odometer in a car because they both give you the unique balances of something (kilometres, assets, liabilities, equity) at one point in time and they do not reset to zero

Emphasize that the Accounting Equation serves two purposes: 1) the

framework for the Balance Sheet and 2) in its expanded version, it facilitates keeping track of everything that takes place in a business, whether it affects the Balance Sheet or the Income Statement

Emphasize that financial statements are, in effect, a summary of all of the

transactions that take place

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 13

8. What Do Financial Statements Report, and How Are They Prepared? (pp. 22-27)

1.1 Canadian Financial Accounting Learning Outcome: A-2 Describe the components of and prepare the four basic financial statements

1.2 Learning Objective:

Understand and be able to prepare basic financial statements.

1.3 Related PowerPoint slides: 1-21, 1-22

Slide 1-21

Comments:

To present the results of a business’s transactions for a period, financial statements need to be prepared. These reports show the entity’s financial information to interested stakeholders both inside and outside the organization. The following basic financial statements are prepared by most organizations:

Statement of Comprehensive Income Income Statement Statement of Changes in Equity Statement of Financial Position or the Balance Sheet Cash Flow Statement

Slide 1-22

Comments:

The financial statements are prepared in the following order:

Income statement/statement of comprehensive income Statement of changes in equity Statement of financial position Cash flow statement

The reason for this order is that the net income figure from the income

statement is needed in order to prepare the statement of changes in equity. Likewise, the ending retained earnings balance from the statement of changes in equity is needed to prepare the statement of financial position.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 14

1.4 Teaching Tips:

Emphasize that the Income Statement and Balance Sheet are linked through the Retained Earnings account, since you need Net Profit to get the RE balance; that is why the Income Statement needs to be done first

9. Focus on Users (pp. 28-29) 1.1 Canadian Financial Accounting Learning Outcome:

A-1 Identify and apply accounting concepts and principles found in the Conceptual Framework

1.2 Learning Objective:

Understand and be able to prepare basic financial statements.

1.3 Related PowerPoint slides: 1-23

Slide 1-23

Comments: There are a broad range of users of financial statements, each having their

own reason for being interested in the financial statements of a company. 1.4 Teaching Tips:

Emphasize that there are a broad range of users of financial statements,

each having their own reason for being interested in the financial statements of a company

You may want to ask students what the interest is of each of the users listed

on PP slide 1-23

You may want to mention that another user (stakeholder) of financial statements is the community that the business is located in, since it is often a key employer in the community

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 15

III. Student Summary Handout 1) Why Study Accounting?

a) Accounting teaches “the language of business”

b) Accounting emphasizes the importance of ethical business behaviour

c) An understanding of accounting helps individuals ensure that the business is

healthy and profitable

2) What is Accounting?

a) Financial Accounting

b) Financial Statements

3) How Are Businesses Organized?

Types

a) Service Business

b) Merchandising Business

c) Manufacturing Business

Choice

a) Sole proprietorship

b) Partnership

c) Corporation

Public

Private

The Business Entity Concept

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 16

4. What Are the Career Opportunities in Accounting-Related Fields?

a) Financial Accounting

b) Management Accounting

c) Taxation

d) Banking and Financial Services

5) What Accounting Principles and Concepts Govern the Field of Accounting?

International Financial Reporting Standards

The Conceptual Framework

a) Financial statements

Elements

Recognition

Measurement

Reporting

b) Qualitative Characteristics of Accounting Information

Relevance

Reliability

Comparability

Understandability

c) Accounting Principles

Cost

Revenue recognition

Full disclosure

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 17

d) Constraints

Materiality

Cost benefit

Timeliness

e) Assumptions

Monetary unit

Economic entity

Time period

Going concern

6) How Is the Accounting Equation Used to Record Business Transactions?

a) Assets, Liabilities, and Shareholders’ Equity

b) The Accounting Equation

c) Transaction analysis

d) Components of Shareholders’ Equity

i) Share capital

ii) Retained Earnings

e) Components of Retained Earnings

i) Revenues

ii) Expenses

iii) Dividends

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 18

7) What Do Financial Statements Report, and How Are They Prepared?

Financial Statements

a) Statement of Comprehensive Income

b) Income Statement

c) Statement of Changes in Equity

d) Statement of Financial Position or the Balance Sheet

e) Cash Flow Statement

Relationships Among the Financial Statements

8) Focus on Users

a) Bookkeepers

b) Managers

c) Shareholders and Potential Investors

d) Creditors

e) Competitors

f) Government and Regulatory Bodies

g) Unions

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 19

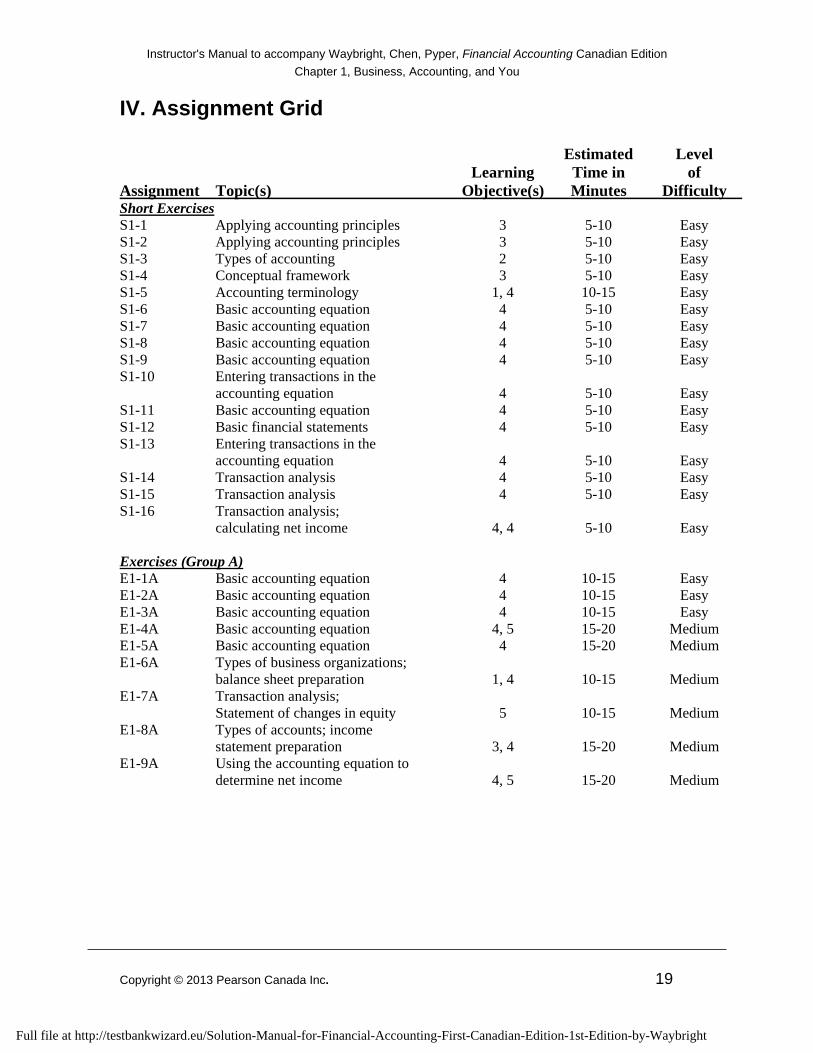

IV. Assignment Grid Estimated Level Learning Time in of Assignment Topic(s) Objective(s) Minutes Difficulty Short Exercises S1-1 Applying accounting principles 3 5-10 Easy S1-2 Applying accounting principles 3 5-10 Easy S1-3 Types of accounting 2 5-10 Easy S1-4 Conceptual framework 3 5-10 Easy S1-5 Accounting terminology 1, 4 10-15 Easy S1-6 Basic accounting equation 4 5-10 Easy S1-7 Basic accounting equation 4 5-10 Easy S1-8 Basic accounting equation 4 5-10 Easy S1-9 Basic accounting equation 4 5-10 Easy S1-10 Entering transactions in the

accounting equation 4 5-10 Easy S1-11 Basic accounting equation 4 5-10 Easy S1-12 Basic financial statements 4 5-10 Easy S1-13 Entering transactions in the

accounting equation 4 5-10 Easy S1-14 Transaction analysis 4 5-10 Easy S1-15 Transaction analysis 4 5-10 Easy S1-16 Transaction analysis;

calculating net income 4, 4 5-10 Easy Exercises (Group A) E1-1A Basic accounting equation 4 10-15 Easy E1-2A Basic accounting equation 4 10-15 Easy E1-3A Basic accounting equation 4 10-15 Easy E1-4A Basic accounting equation 4, 5 15-20 Medium E1-5A Basic accounting equation 4 15-20 Medium E1-6A Types of business organizations;

balance sheet preparation 1, 4 10-15 Medium E1-7A Transaction analysis;

Statement of changes in equity 5 10-15 Medium E1-8A Types of accounts; income statement preparation 3, 4 15-20 Medium E1-9A Using the accounting equation to determine net income 4, 5 15-20 Medium

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 20

Estimated Level Learning Time in of Assignment Topic(s) Objective(s) Minutes Difficulty Exercises (Group B) E1-1B Basic accounting equation 4 10-15 Easy E1-2B Basic accounting equation 4 10-15 Easy E1-3B Basic accounting equation 4 10-15 Easy E1-4B Using the accounting equation to determine net income 4, 5 15-20 Medium E1-5B Transaction analysis 4 15-20 Medium E1-6B Types of business organizations; balance sheet preparation 1, 4 10-15 Medium E1-7B Transaction analysis; statement of

changes in equity 5 10-15 Medium E1-8B Types of accounts; income sheet preparation 3, 4 15-20 Medium E1-9B Using the accounting equation to determine net income 4, 5 15-20 Medium

Problems (Group A) P1-1A Transaction analysis and preparation of net income 4, 5 20-25 Medium P1-2A Income statement and balance sheet transactions and preparation 4, 5 25-30 Difficult P1-3A Preparing income statement; statement of retained earnings, and balance sheet 5 20-25 Medium P1-4A Preparing income statement and balance sheet; identify financial information 5 25-30 Medium P1-5A Error analysis and preparation of balance sheet 5 20-25 Difficult

Problems (Group B) P1-1B Transaction analysis and preparation of net income 4, 5 20-25 Medium P1-2B Income statement and balance sheet transactions and preparation 4, 5 25-30 Difficult P1-3B Preparing income statement, statement of retained earnings, and balance sheet 5 20-25 Medium P1-4B Preparing income statement and balance sheet; identify financial information 5 25-30 Medium P1-5B Error analysis and preparation of balance sheet 5 20-25 Difficult

Continuing Exercise First in sequence that begins an accounting 4, 5 25 Medium cycle

Continuing Problem First in sequence that begins an accounting 4, 5 60-75 Medium cycle

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 21

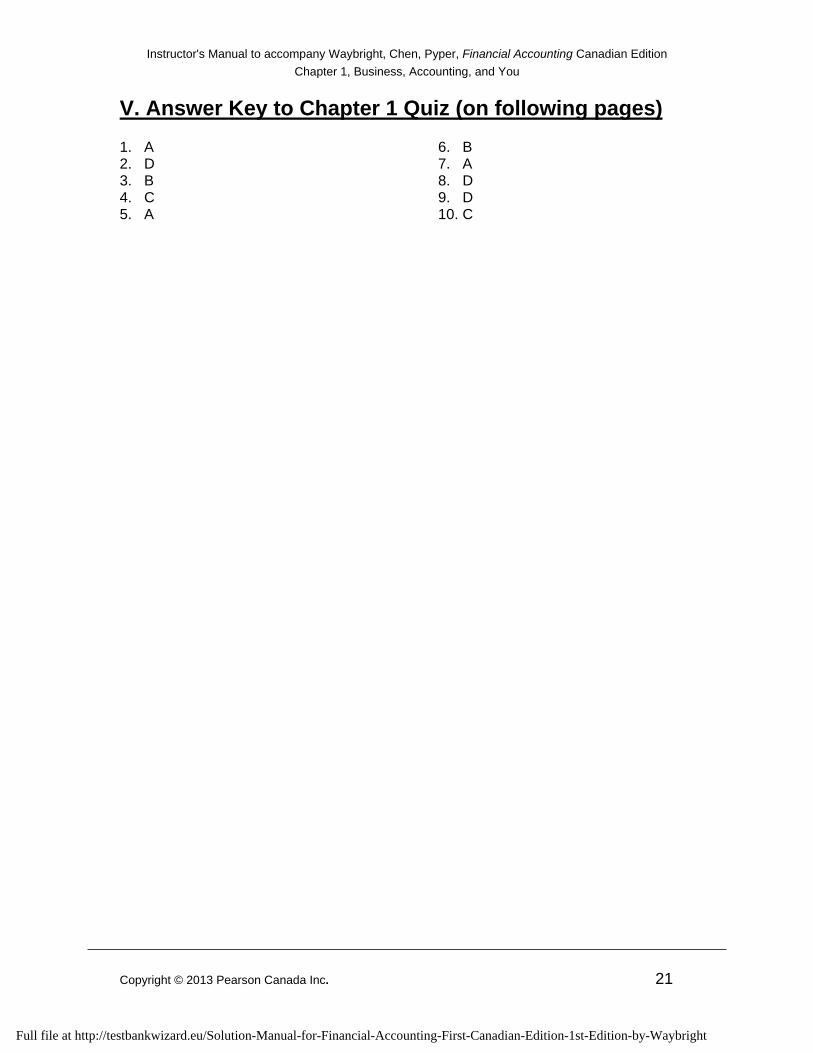

V. Answer Key to Chapter 1 Quiz (on following pages) 1. A 2. D 3. B 4. C 5. A

6. B 7. A 8. D 9. D 10. C

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 22

Chapter Quiz Name Date Section

CHAPTER 1 TEN-MINUTE QUIZ

Circle the letter of the best response. 1. Which of the following statements is FALSE?

A. The proprietorship form of business organization protects the personal assets of the owners from creditors of the business.

B. A proprietorship has a single owner. C. Accounting is the information system that measures business activities,

processes that information into reports, and communicates the results to decision makers.

D. The FASB determines how accounting is practiced in the United States.

2. The primary objective of financial reporting is to:

A. present information in an ethical manner. B. provide information useful to managers in making daily decisions. C. provide information to the federal government. D. provide information useful for investment and lending decisions.

3. Wilbur Corp. operates a fishing tackle shop. The company needs to borrow

money to expand; therefore, it prepared financial statements to present to the banker. Wilbur Corp. obtained appraisals of all the assets of the business to ensure that the balance sheet would reflect the most current value of the assets. Wilbur Corp. has violated which of the following principles or concepts?

A. Reliability principle B. Cost principle C. Going-concern principle D. Stable-monetary-unit concept

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 23

4. Which of the following statements is FALSE?

A. Assets are economic resources that are expected to benefit future periods. B. Expenses are decreases in shareholders’ equity that result from

delivering goods and services to customers. C. Revenues are assets that represent economic benefits. D. Liabilities are economic obligations to outsiders.

5. A payment on account:

A. decreases assets. B. increases liabilities. C. increases shareholders’ equity. D. increases assets.

6. Which of the following transactions increases shareholders’ equity?

A. Collection of an account receivable B. Issuance of common shares for cash C. Payment of salaries D. Cash purchase of land

7. A balance sheet reports the:

A. assets, liabilities, and shareholders’ equity on a particular date. B. difference between revenues and expenses during the period. C. change in the retained earnings during the period. D. cash receipts and cash payments during the period.

8. If assets increase $40,000 during the period and liabilities decrease $8,000

during the period, shareholders’ equity must have:

A. increased $32,000. B. decreased $48,000. C. decreased $32,000. D. increased $48,000.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright

Instructor's Manual to accompany Waybright, Chen, Pyper, Financial Accounting Canadian Edition

Chapter 1, Business, Accounting, and You

Copyright © 2013 Pearson Canada Inc. 24

9. The following information about the assets and liabilities at the end of 2011 and 2012 is given below:

2011 2012

Assets $75,000 $90,000 Liabilities 36,000 45,000

If net income was $1,500 and there were no dividends, how much did equity increase from new share issuances? A. $40,500 B. $45,000 C. $ 6,000 D. $ 4,500

10. The amount of net income shown on the income statement also appears on the:

A. statement of financial position. B. balance sheet. C. statement of retained earnings D. statement of cash flows.

Full file at http://testbankwizard.eu/Solution-Manual-for-Financial-Accounting-First-Canadian-Edition-1st-Edition-by-Waybright