about doing business in the gothenburg region … · about doing business in the gothenburg region...

TRANSCRIPT

SCANDINAVIA'S MOST EXPANSIVE REGION

100%FACTS & FIGURES

ABOUT DOING BUSINESS IN THE GOTHENBURG

REGION 2017

2 3

In Summer 2016, the American company Uber announced that it would be putting 100 self-driving Volvo XC90 cars into traffic in Pittsburgh. This collaboration is an example of how new, digitally-driven services are changing the shape of the business environment in Gothenburg.

Three reasons why interest in Gothenburg is rocketing Gothenburg-based companies have, in recent years, invested millions in developing new products and services. The names behind these large sums include global brands like Ericsson, AB Volvo, AstraZeneca, Saab, Volvo Cars and multiple other companies of various sizes. A quarter of the country's private R&D investments are made in the Gothenburg region. This has made the region a world leader in areas such as autonomous, connected and electrically-powered vehicles.

Construction plans worth a total of 100 billion euros are attracting investors at a scope never previously seen in Gothenburg. Gothenburg is expanding in the ideal city location and offers unique testing possibilities for new services.

The rapid pace of digitalisation opens up opportunities for companies and people with the ability to think creatively, such as the Gothenburg-based company Fingerprint Cards, which creates smart ID solutions for billions of people.

Gothenburg or Silicon ValleyThe three points are interconnected. San Francisco-based Uber's development collaboration with Volvo Cars is a prime example. New solutions can come from high-technology industry in Gothenburg just as easily as from new technology and services companies in the Silicon Valley.

A valuable domestic marketIn Gothenburg, large construction projects are located right in the middle of the city, where the ethos is that this represents a fantastic opportunity to test something new. A domestic market with this attitude is of immense value for companies putting significant investments into R&D. The full chain is in place in Gothenburg – from the analysis of people's needs and society's challenges to in-demand products and international trade. What begins as concept development continues with the design of products and services, testing in an urban environment and large-scale production. In addition, the city boasts global marketing and established trade routes direct to the large export markets.

Challenges that call for new partnershipsBut the city is also facing some substantial challenges. Certain competence is scarce in trade and industry here – not least in the construction sector. The consequences of segregation and a housing shortage are serious. These are putting Gothenburg's capacity for cooperation to the test. The business sector, the city/region and the universities need to work together to take on these challenges.

The approach to collaboration has made Lindholmen one of Sweden's most knowledge-rich areas. Another example is AstraZeneca, which has opened up its research facilities to small, promising companies working in its networks. These collaboration models are new even from an international perspective. They contribute both to finding answers to major societal issues and to making Gothenburg an interesting option for investments and establishments.

billion100 euros are expected to be invested by 2035

Pho

to: H

ans

Wre

tlin

g / Ä

lvst

rand

en U

tvec

klin

g

BUSINESS REGION GÖTEBORG is responsible for business development in the City of Gothenburg and represents thirteen municipalities in the region.

Why interest in Gothenburg is record high

4 5

Contents:

A REGION MOVING FORWARD Page 7 – 13Gothenburg's labour market. International and national competitiveness.1.HIGH LEVEL OF GLOBAL INTERACTION Page 14–18Import and export. Foreign-owned companies. International visitors. 2.GROWTH & LABOUR MARKET Page 19 –23Emerging industries. Largest employment growth. Employment rate. 3.BUSINESS Page 24– 27Largest employers. Prominent clusters. Corporate climate and entrepreneurship. 4.POPULATION, LIFESTYLE & EDUCATION Page 28 – 30Demographics. Level of education. Seats of learning.5.COSTS & TAXES Page 31– 34Salary and rent levels. Tax regulations. Tax reductions.6.CLIMATE, ENVIRONMENT & SUSTAINABLE DEVELOPMENT Page 35–38Waste management. Air quality. Green Gothenburg. 7.

Pho

to: H

ans

Wre

tlin

g / Ä

lvst

rand

en U

tvec

klin

g

6 77

A REGION MOVING FORWARDThe Gothenburg region is an attractive part of the country which is experiencing growth through a number of exciting developments. This transformation is illustrated in both national and international comparisons.

1.P

hoto

: Mos

tpho

tos

/ BR

G

Pho

to: P

er P

ixel

Pet

erso

n / G

öteb

org

& C

o

8 9

A REGION MOVING FORWARD A REGION MOVING FORWARD

Growth strategy – to expand in terms of both population and area

Growth in the Gothenburg regional labour market since the year 2000

Labour market region by 2030

Current labour market region

The Gothenburg region is growing more rapidly than anyone could have predicted. In addition, major investments are being made in infrastructure and urban development, which in turn attracts more commuters and new inhabitants. By around 2030, it is likely that Uddevalla, Trollhättan and Borås will be a part of Gothenburg's labour market. For example, commuting from Trolllhättan to Gothenburg has increased by just over 30 per cent in the last three years alone. This increase suggests that, in the near future, we will also be able to include Trollhättan and its surrounding municipalities in Gothenburg's labour market. For this reason, local politicians in the Gothenburg region have adopted a new, offensive growth strategy. 44,000

more workplaces

new inhabitants

more jobs

63%increase in total wage sum

60%increase in GRP (Gross regional product)

40%A local labour market is a division of Sweden based on commuting patterns. When commuting between municipalities reaches the extent that these municipalities can be seen to be dependent on one another, a labour market region is formed.

THE FOLLOWING 18 MUNICIPALITIES ARE INCLUDED IN GOTHENBURG'S LABOUR MARKET: Ale, Alingsås, Bollebygd, Falkenberg, Gothenburg, Härryda, Kungsbacka, Kungälv, Lerum, Lilla Edet, Mölndal, Orust, Partille, Stenungsund, Tjörn, Varberg, Vårgårda and Öckerö.

increase in productivity

SOME OF THE KEY GOALS ARE:

10,000 new inhabitants per year.

By the year 2030, the entire Gothenburg region will be strengthened with a further 180,000 residences and 110,000 work places.

Particular focus is being placed on the core of the region, central Gothenburg, where 45,000 residences and 60,000 work places will be added by 2030.

Gothenburg's labour market in 2030 will encompass 1.75 million inhabitants, compared with 1.17 million inhabitants today.

GOTHENBURG

170,000

117,000

Borås

Varberg

UddevallaTrollhättan

ww

10 11

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

Sweden

The Gothenburg region – a leading research region which is highly competitive on the international stage

1, 2… 5 … 195, 196

Competence**GLOBAL CITIES TALENT

COMPETITIVENESS INDEX 2017

5TH OF 46 CITIES

The index ranks cities on their capacity to attract, develop and retain competence. Gothenburg's

high ranking is motivated by:

• High quality of life• Well-educated population

Source: INSEAD and Adecco

OF SWEDEN'S TOTAL R&D INVESTMENTS, OUR LEADING INDUSTRIES ACCOUNT FOR:

• Automotive – 61%• Chemicals, food and pharmaceuticals – 42% • Professional services – 27%

R&D SHARE OF GDP

of Sweden's total R&D investments within the private sector are made in the Gothenburg region*

* Indicators refer to West Sweden. ** Indicators refer to City of Gothenburg.

REAL R&D EXPENDITURE IN SEK PER EMPLOYEE IN THE PRIVATE SECTOR

Gothenburg region Stockholm region Malmö region Sweden

Competitiveness*EUROPE 2020

REGIONAL INDEX

5TH OF 268 REGIONS

Assesses how close EU regions are to their target strategies for achieving improved competitiveness. The

Gothenburg region has achieved all of its established EU targets and is praised for, among other things:

• Employment• Higher education level

• R&D

Source: European Commission

Growth potential*PERFORMANCE INDEX 2014

10TH OF 117 REGIONS

Assesses large European city regions with the best future growth potential.

The Gothenburg region scores highly in:

• Economic growth• Employment

Source: BAK Basel

Innovations**REGIONAL INNOVATION

SCOREBOARD 2016 INNOVATION LEADER AMONG

214 REGIONS Assesses the innovation performance of European regions.

West Sweden is named in the report as a European innovation leader. Among other things, the region achieves distinctions for:

• Increased employment within knowledge- based professions

• Process and product innovations within SME

• Highly educated population

• Export of high-technology goods

Source: European Commission

Connectivity**EUROPEAN CITIES AND REGIONS

OF THE FUTURE 2016/2017

9TH OF 468 CITIES/REGIONS

Ranks cities and regions in Europe with the best IT and logistics infrastructure.

Among large European cities, Gothenburg is ranked ninth when it comes to the best

IT and logistics infrastructure. Source: fDi

Source: Statistics Sweden

* Refers to companies' R&D investments in Västra Götaland County. Source: Statistics Sweden

25%

2001 2003 2005 2007 2009 2011 2013 2015

A REGION MOVING FORWARD A REGION MOVING FORWARD

12 13

3

2

1

% 0

-1

Stoc

khol

m re

gion

Oslo

regi

on

Lyon

regi

on

Stut

tgar

t reg

ion

Goth

enbu

rg re

gion

*

Wes

tern

Euro

pe

Vien

na re

gion

Helsi

nki r

egio

n

Öres

und r

egio

n

Ham

burg

regi

on

Lille

regi

on

Fran

kfur

t reg

ion

Mila

n reg

ion

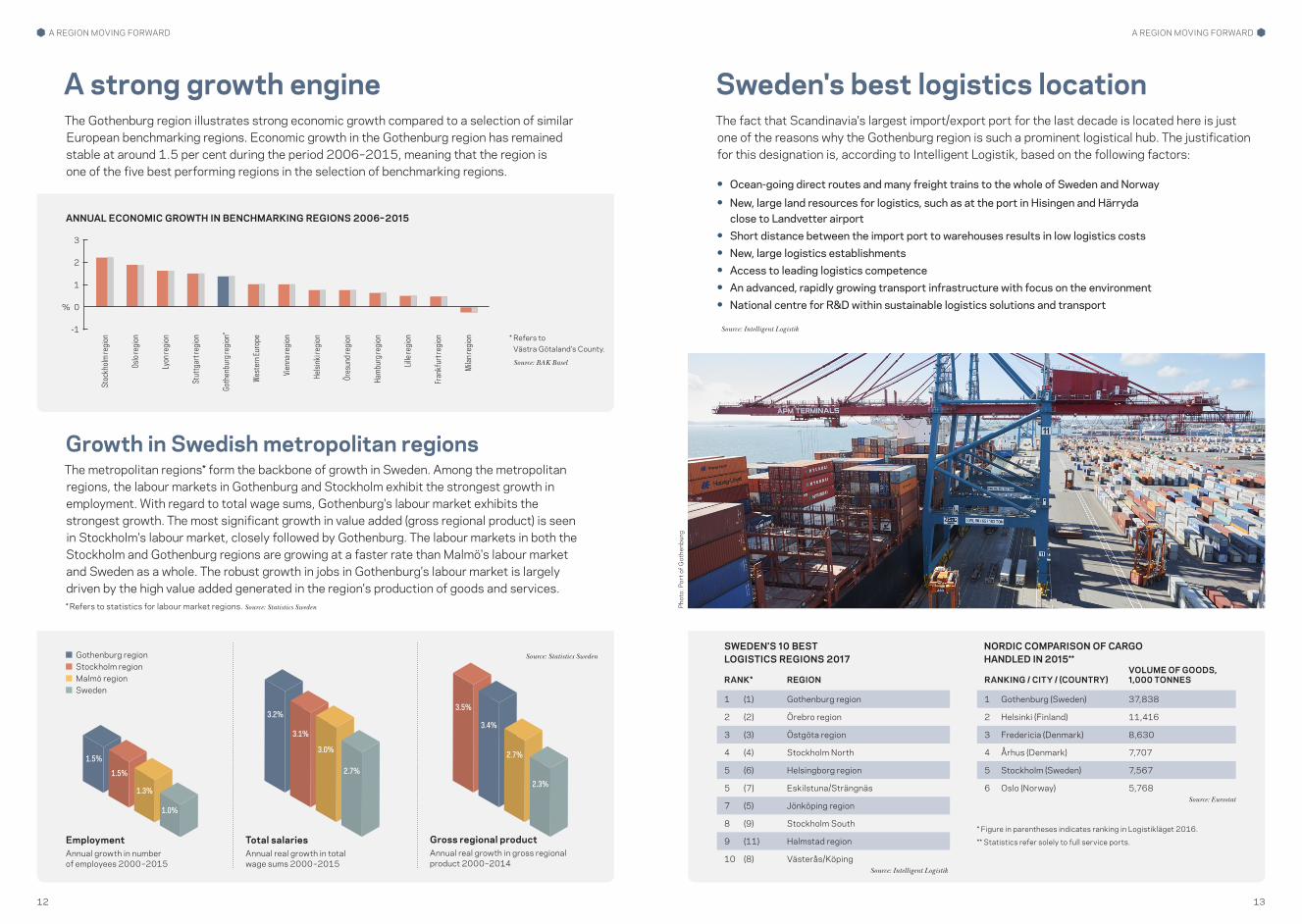

The Gothenburg region illustrates strong economic growth compared to a selection of similar European benchmarking regions. Economic growth in the Gothenburg region has remained stable at around 1.5 per cent during the period 2006–2015, meaning that the region is one of the five best performing regions in the selection of benchmarking regions.

A strong growth engine

Growth in Swedish metropolitan regionsThe metropolitan regions* form the backbone of growth in Sweden. Among the metropolitan regions, the labour markets in Gothenburg and Stockholm exhibit the strongest growth in employment. With regard to total wage sums, Gothenburg's labour market exhibits the strongest growth. The most significant growth in value added (gross regional product) is seen in Stockholm's labour market, closely followed by Gothenburg. The labour markets in both the Stockholm and Gothenburg regions are growing at a faster rate than Malmö's labour market and Sweden as a whole. The robust growth in jobs in Gothenburg's labour market is largely driven by the high value added generated in the region's production of goods and services.

Sweden's best logistics location

RANKING / CITY / (COUNTRY)VOLUME OF GOODS, 1,000 TONNES

1 Gothenburg (Sweden) 37,838

2 Helsinki (Finland) 11,416

3 Fredericia (Denmark) 8,630

4 Århus (Denmark) 7,707

5 Stockholm (Sweden) 7,567

6 Oslo (Norway) 5,768

NORDIC COMPARISON OF CARGO HANDLED IN 2015**

RANK* REGION

1 (1) Gothenburg region

2 (2) Örebro region

3 (3) Östgöta region

4 (4) Stockholm North

5 (6) Helsingborg region

5 (7) Eskilstuna/Strängnäs

7 (5) Jönköping region

8 (9) Stockholm South

9 (11) Halmstad region

10 (8) Västerås/Köping

SWEDEN'S 10 BEST LOGISTICS REGIONS 2017Source: Statistics Sweden

* Refers to statistics for labour market regions. Source: Statistics Sweden

Employment Annual growth in number of employees 2000–2015

Total salaries Annual real growth in total wage sums 2000–2015

Gross regional product Annual real growth in gross regional product 2000–2014

1.5%

1.5%

1.3%

1.0%

3.2%

3.1%

3.0%

2.7%

3.5%

3.4%

2.7%

2.3%

ANNUAL ECONOMIC GROWTH IN BENCHMARKING REGIONS 2006–2015

The fact that Scandinavia's largest import/export port for the last decade is located here is just one of the reasons why the Gothenburg region is such a prominent logistical hub. The justification for this designation is, according to Intelligent Logistik, based on the following factors:

• Ocean-going direct routes and many freight trains to the whole of Sweden and Norway

• New, large land resources for logistics, such as at the port in Hisingen and Härryda close to Landvetter airport

• Short distance between the import port to warehouses results in low logistics costs• New, large logistics establishments• Access to leading logistics competence• An advanced, rapidly growing transport infrastructure with focus on the environment• National centre for R&D within sustainable logistics solutions and transport

Source: Intelligent Logistik

Gothenburg region Stockholm region Malmö region Sweden

* Figure in parentheses indicates ranking in Logistikläget 2016.

** Statistics refer solely to full service ports.

Source: Eurostat

Source: Intelligent Logistik

* Refers to Västra Götaland's County.

Source: BAK Basel

Pho

to: P

ort o

f Got

henb

urg

A REGION MOVING FORWARD A REGION MOVING FORWARD

15

Exports to the region’s largest trading partnersThe real value of the Gothenburg region's goods exports increased by 6 per cent between 2015 and 2016. During the same period, real growth in Sweden's goods exports remained essentially unchanged. The positive development of exports in the region can largely be explained by its competitive products which generate high added value for the innovative business environment. The USA retains its position as the Gothenburg region’s most important export market, followed by Norway. Germany and Denmark are two further key destinations for the Gothenburg region's goods exports.

Source: Statistics Sweden

Imports from the region’s largest trading partnersIn contrast to the Gothenburg region's goods exports, the import of goods into the region developed in line with Sweden as a whole between 2015 and 2016. Real growth landed at 2 per cent for both the Gothenburg region and Sweden. All import origins on the top 10 list are also included on the list of the Gothenburg region's 10 most important export destinations. The Gothenburg region's comprehensive bilateral trade figures are an important indicator that the region's companies benefit from the opposing country's technologies.

Source: Statistics Sweden

RANK COUNTRYVALUE OF EXPORTED

GOODS 2016, MSEK

1 USA 26,734

2 Norway 26,438

3 Germany 19,541

4 Denmark 15,236

5 UK 13,040

6 Finland 12,895

7 China 12,691

8 Netherlands 9,980

9 France 9,049

10 Japan 3,864

Västra Götaland County total 238,882

Gothenburg region total 192,191

Gothenburg region's share of Swedish exports 16%

TOP 10 EXPORT DESTINATIONS 2016

RANK COUNTRYVALUE OF IMPORTED

GOODS 2016, MSEK

1 Germany 39,052

2 Netherlands 19,171

3 Norway 14,660

4 UK 14,538

5 Denmark 13,811

6 China 13,387

7 France 8,180

8 USA 5,470

9 Finland 4,437

10 Japan 2,957

Västra Götaland County total 217,608

Gothenburg region total 173,928

Gothenburg region's share of Swedish imports 15%

TOP 10 IMPORT COUNTRIES OF ORIGIN 2016

The region's imports and exportsThe majority of the Gothenburg region's exported goods comprise vehicles and other means of transport – an industry which is also largest in terms of import value. The product groups other machinery and manufactured goods, as well as computers, electronics and optics account for a substantial portion of goods exchange with trading partners. The automotive industry demonstrated the highest increase in goods exports between 2015 and 2016. Measured in real SEK, goods exports in the automotive industry increased by a full SEK 13 billion. The product group computers, electronics and optics accountedfor a considerable upswing in goods exports, with a real increase of approximately 4 billion.

Source: Statistics Sweden

IMPORTS AND EXPORTS OF GOODS BY PRODUCT GROUP 2016

0 30,000 60,000 120,00090,000

HIGH LEVEL OF GLOBAL INTERACTION

HIGH LEVEL OF GLOBAL INTERACTIONShipping and international trade have been integral to the Gothenburg region for almost 400 years. Of course, the cargo has changed somewhat over the years, but the flow of goods continues to play a critical role for the development and growth of the region's companies. Every fifth employee in the Gothenburg region works in a foreign-owned company. At the same time, new records are being set for travelling to and from the region.

Unless otherwise specified, the statistics in this and the chapters to come refer to the 13 member municipalities in the Gothenburg region’s municipal association: Ale, Alingsås, Göteborg, Härryda, Kungsbacka, Kungälv, Lerum, Lilla Edet, Mölndal, Partille, Stenungsund, Tjörn and Öckerö!

export companies constitute approximately two thirds of Västra Götaland County's total export companies and

just over 9 per cent of all Sweden's export companies.

The region's4,300

* Import value is confidential.

Value of exported goods 2016, MSEK

Value of imported goods 2016, MSEK

2.P

hoto

: upp

er P

ort o

f Got

henb

urg,

low

er M

atto

n / B

RG

14

Motor vehicles and other transport equipment

Other machines and manufactured goods

Computers, electronic and optical productsChemicals, pharmaceuticals,

rubber and plasticsWood, paper and printing services

Basic metals and fabricated metal products

Textiles and clothes

Coke and petroleum

Products connected to services *

Food products, beverages and tobacco

Products of agriculture, forestry and fishing

Mining and quarrying *

16 17

0100002000030000400005000060000700008000090000

05

10152025303540

-20-15-10-505

101520

Norway tops the list, with the UK experiencing most growthThe list of countries which own companies in the Gothenburg region is dominated by Northwestern Europe. Norway tops the list as the country with most foreign-owned companies, followed by Germany and the USA. An additional 18 companies with UK ownership have been established, while 19 companies from Luxembourg have been discontinued, meaning that the Netherlands overtakes Luxembourg to take sixth position on the list.

Source: Statistics Sweden

The number of employees in foreign-owned companies is increasingThe number of employees in foreign-owned companies has almost quadrupled during the period 1990–2015. In 2015, just over 84,000 people were employed by foreign-owned companies in the Gothenburg region. In spite of the decrease in foreign-owned companies in the Gothenburg region during the period 2014–2015, the number of employees in these companies rose by 4 per cent (equivalent to around 3,000 employees). The most substantial increases in employee numbers among foreign-owned companies were seen in companies from China, Denmark and the Netherlands. In Sweden as a whole, the number of employees in foreign-owned companies decreased by around 0.5 per cent.

Source: Statistics Sweden

Many foreign-owned companies in the regionSince 1990, the number of foreign-owned companies in the Gothenburg region has grown steadily. In 2015 there were approximately 2,300 foreign-owned companies in the Gothen-burg region. These foreign-owned companies accounted for approximately 3,000 work places in the Gothenburg region. From 2014 to 2015, the number of foreign-owned companies in the Gothenburg region decreased by about 20. The most foreign-owned companies in the region originate from Norway, followed by Germany, the USA and Denmark.

Source: Statistics Sweden

RANK* COUNTRY

NUMBER OF COMPANIES

2014

NUMBER OF COMPANIES

2015CHANGE

2014–2015

1 (1) Norway 461 463 2

2 (2) Germany 280 275 -5

3 (3) USA 227 221 -6

4 (4) Denmark 214 215 1

5 (5) UK 173 191 18

6 (7) Netherlands 142 141 -1

7 (6) Luxembourg 143 124 -19

8 (8) Finland 111 115 4

9 (9) France 86 81 -5

10 (10) Switzerland 66 64 -2

Gothenburg region total 2,297 2,274 -23

THE 10 MOST COMMON COUNTRIES OF ORIGIN AMONG FOREIGN-OWNED COMPANIES

NUMBER OF EMPLOYEES IN FOREIGN-OWNED COMPANIES 1990–2015

10,000

0

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

1990199119921993199419951996199719981999

200120022003200420052006

2007200820092010

20132014

20122011

NUMBER OF FOREIGN-OWNED COMPANIES AND WORK PLACES 1990–2015

HIGH LEVEL OF GLOBAL INTERACTION

* Figure in parentheses refers to rank in 2014

2015

500

1000

1500

2000

2500

3000

0

1,000

1,500

2,000

2,500

3,000

19901991199219931994199519961997199819992000200120022003200420052006

2007200820092010

20132014

20122011

2015

Work places Companies

Strong growth in exported goods from the Gothenburg region Since 2010, the Gothenburg region has experienced strong growth in goods exports, and with the exception of 2012, goods exports from the region have been at a much stronger level than for Sweden as a whole. In 2016, the Gothenburg region noted a real increase in goods exports of 6 per cent, while the corresponding figure for Sweden as a whole was marginal.

Source: Statistics Sweden

2012 2013 2014 2015 2016

% 0

20

10

ANNUAL REAL GROWTH IN GOODS EXPORTS IN THE GOTHENBURG REGION AND SWEDEN 2010–2016

Sweden Gothenburg region

15

5

-5

-10

-15

20112010

Highest value of goods exports per employee in Gothenburg region The fact that the Gothenburg region's companies are export intensive can be ascertained from studying goods exports in SEK per employee. In 2016, the Gothenburg region's companies exported goods at a value of approximately SEK 400,000 per employee. The Gothenburg region's generated export value per employee is substantially higher than that of the other two metropolitan regions and Sweden as a whole.

Source: Statistics Sweden

GOODS EXPORTS IN SEK PER EMPLOYEE IN METROPOLITAN REGIONS AND SWEDEN 2016

0

100,000

5,000

150,000

250,000

350,000

200,000

400,000

300,000

Sweden Gothenburg region

Stockholm region

Malmö region

Pho

to: P

ort o

f Got

henb

urg

2000

HIGH LEVEL OF GLOBAL INTERACTION

18

20000

30000

40000

50000

60000

70000

19

Record numbers for trips to and from the region and for overnight staysGothenburg Landvetter Airport set a new record in 2016 with approximately 6.4 million air passengers. Never before have so many air travellers made the journey to and from the Gothenburg region's largest airport. The region's hotels, cabin villages and hostels also experienced a good 2016, with overnight stays reaching a record of 4.7 million. The top five countries of origin of foreign visitors for 2016 is unchanged compared with the previous year. Norwegians are the most numerous visitors, followed by Germans, Brits, Danes and Americans.

Source: Swedish Transport Agency and Statistics Sweden

The international population is increasingIn 2016, around 190,000 inhabitants of the Gothenburg region were born abroad (19 per cent of the region's population). Compared with the previous year, this is an increase of around 9,000 foreign-born inhabitants, equivalent to a 5 per cent increase. Iraq, Iran and Finland head the list of country of birth. Somalia has advanced from its position in 2015 to overtake the former Yugoslavia for sixth place. Those born in Syria have seen the largest increase, in terms of number and percentage, while Finnish-born inhabitants have decreased the most.

Source: Statistics Sweden

FOREIGN-BORN INHABITANTS 2016

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2014

2015

2013

2

3

4

5

7

6

NUMBER OF AIR PASSENGERS AND OVERNIGHT STAYS IN THE GOTHENBURG REGION

2016

COUNTRYNUMBER

2015NUMBER

2016 IN NUMBER IN PER CENT

Iraq 15,292 15,558 266 1.7%

Iran 14,826 15,128 302 2.0%

Finland 11,187 10,922 -265 -2.4%

Poland 8,842 9,065 223 2.5%

Bosnia and Herzegovina 8,700 8,849 149 1.7%

Somalia 7,932 8,531 599 7.6%

Former Yugoslavia 8,388 8,320 -68 -0.8%

Syria 5,476 8,085 2,609 47.6%

Turkey 4,993 5,177 184 3.7%

Norway 4,937 4,923 -14 -0.3%

Gothenburg region total 180,408 189,329 8,921 4.9%

CHANGE 2015–2016

Millions of air passengers Millions of overnight stays

Pho

to: G

öran

Ass

ner

GROWTH & LABOUR MARKETThe Gothenburg region's business environment is characterised by global and knowledge-intensive manufacturing companies, such as Volvo, SKF and AstraZeneca, among others. The total wage sum in the Gothenburg region is growing at a faster rate than the country as a whole and other metropolitan regions. Above all, this growth is most prominent within the construction industry and the services sector. Overall, the region experiences growth at a higher rate than the national average. A rapidly expanding knowledge-intensive services sector supports the manufacturing companies. The region's business environment is gaining further nuance through growing businesses in the hotels and restaurants, construction and real estate industries.

Pho

to: u

pper

Jen

nie

Sm

ith

/ Göt

ebor

g &

Co,

low

er G

öran

Ass

ner /

BR

G

3. HIGH LEVEL OF GLOBAL INTERACTION

20 21

-4-3-2-101234

0,00,51,01,52,02,53,03,54,04,55,05,56,0

GROWTH & LABOUR MARKET

The Gothenburg region – an engine for growth in Sweden In 2016, real total wage sum levels in the Gothenburg region grew by 4.6 per cent. The Gothenburg region experienced a higher rate of growth in the real total wage sum than Sweden as a whole, which grew by just under 4 per cent in 2016.

Source: Statistics Sweden

ANNUAL REAL GROWTH IN TOTAL WAGE SUM 2001–2016

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2013

2014

2012

2011

0

1

2

3

4

6

%

2015

2016

5

Gothenburg region Sweden

ANNUAL REAL GROWTH IN TOTAL WAGE SUM BY SECTOR IN THE GOTHENBURG REGION 2000–2016

CONSTRUCTION COMPANIES SERVICE COMPANIES

PUBLIC SECTOR INDUSTRIAL COMPANIES

The construction and services sectors have experienced the highest real growth in total wage sumThe average annual growth in real wage sum levels in the Gothenburg region during the period 2000–2016 has been around 3.5 per cent. In terms of individual industries, the largest growth has occurred within the construction sector, followed by the services sector. The economic situation in the construction sector is predicted to be strong during the coming year. The companies' highly developed services and a booming public sector are contributing ever more to the region's economy.

Source: Statistics Sweden

A good measure of regional growth is to assess the development of the

total wage sum. This figure can go up as a result of increased

productivity or by more people being employed.

GROWTH & LABOUR MARKET

Healthcare and care sector has the most employeesHealthcare and care is the sector with the most employees in the Gothenburg region, followed by business services. Compared with Sweden as a whole, the Gothenburg region has a larger proportion of its population employed within business services, retail, manufacturing and transport.

Source: Statistics Sweden

SECTORGOTHENBURG

REGION

% SWEDEN

%

Health care and care 76,002 15.1 786,549 16.6

Commerce 69,921 13.9 553,322 11.7

Business services 65,416 13.0 572,862 12.1

Manufacturing and mining 64,333 12.8 560,475 11.9

Education 51,692 10.3 498,757 10.6

Construction 32,699 6.5 333,079 7.0

Transportation 27,878 5.5 224,663 4.8

Public administration 24,718 4.9 271,747 5.8

Personal and cultural services 21,931 4.4 209,780 4.4

Information and communication 21,765 4.3 178,994 3.8

Hotels and restaurants 18,570 3.7 164,006 3.5

Property 8,651 1.7 76,821 1.6

Financial services and insurance 7,222 1.4 92,600 2.0

Energy and the environment 4,831 1.0 53,067 1.1

Unknown 4,371 0.9 49,311 1.0

Agriculture, forestry and fishing 2,614 0.5 99,312 2.1

Total 502,614 4,725,345

EMPLOYMENT (+16 YEARS OF AGE) BY SECTOR 2015

Employment in the Gothenburg region is growing faster than the nationIn 2015, there were approximately 503,000 individuals employed in the Gothenburg region. This represents an increase of 26 per cent since the year 2000, or 104,000 employed persons.

Source: Statistics Sweden

employed in healthcare and care in the Gothenburg region in 2015

The number of employed in the Gothenburg region in 2015

EMPLOYMENT GROWTH IN THE GOTHENBURG REGION AND SWEDEN 2001– 2015

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2014

2013

2012

2011

-4

-3

-2

-1

0

1

2

3

4

%

2015

Gothenburg region Sweden

76,002

502,614

3.9%

3.5% 1.6%

4.9%

22 23

0

10

20

30

40

4

6

8

10

-10 0 10 20 30

Greatest job growth in business services All sectors in the Gothenburg region have demonstrated an increase in the number of employees following the financial crisis in 2008. The Swedish manufacturing and extraction sector has experienced negative growth, while the Gothenburg region is heading in the other direction. Business services is the sector experiencing the highest growth in the Gothen-burg region, followed by hotels and restaurants. Compared with Sweden, the Gothenburg region has a much larger employment growth rate within manufacturing, information and communication, education and professional services, while Sweden overall demonstrates more robust growth within energy and environment, retail and hotels and restaurants.

Source: Statistics Sweden

PERCENTAGE CHANGE IN EMPLOYMENT BY SECTOR 2009–2015

Business servicesHotels and restaurants

EducationConstruction

PropertyInformation and communication

Public administrationPersonal and cultural services

Healthcare and careEnergy and the environment

CommerceManufacturing and mining

TransportationFinancial services and insurance

-10 0 10 20 30 %

Gothenburg region Sweden

Office-based employees in the Gothen-

burg region will increase by

100,000 from today's 150,000 employees to around

250,000 employees in 2035.

Source: Evidens

Pho

to: B

engt

Kje

llin

/ BR

G

Small companies experiencing the most rapid growth in employeesSince 2006, companies with 1–4 employees have experienced the strongest percentage growth in employment in the Gothenburg region. During the period 2006–2016, employees in companies with 1–4 employees rose by 30 per cent. Companies with 5–19 employees and the region's largest companies also demonstrate high percentage growth in employees. However, in terms of absolute number, companies with 20–199 employees are clearly growing the most, with more than 27,000 new employees during the period 2006–2016.

Source: Statistics Sweden

Small establishments account for the majority of the region's total establishments The Gothenburg region's numerous small establishments provide the majority of the region's establishments (approximately 90 per cent of the establishments have fewer than five employees). Between 2006 and 2016, the number of establishments increased by just over 26,000. By far and away the largest increase in establish-ments was found among the region's self- employed (i.e. establishments without employees), followed by establishments with 1–4 employees.

Source: Statistics Sweden

CHANGE IN NUMBER OF EMPLOYEES BY SIZE CATEGORY 2006–2016

0%

10

20

40

30

1–4 employees

5–19 employees

20–199 employees

200> employees

Unemployment in the Gothenburg region lowest among metropolitan regionsIn 2007, both Gothenburg and Sweden as a whole reported largely similar unemployment rates. The positive development of employment in the Gothenburg region from the year 2010 onwards has resulted in a continued decrease in unemployment. Unemployment in the Gothen-burg region is lowest among the country's metropolitan regions, and around 2 percentage points lower than in Sweden.

Source: Swedish Public Employment Service and Statistics Sweden

% 4

6

8

10

2000

2002

2004

2006

2008

2010

2016

2014

2012

UNEMPLOYMENT AMONG 16–64 YEAR OLDS, ANNUAL AVERAGE FROM 2000 ONWARDS

SIZE CATEGORY

NUMBER OF ESTABLISHMENTS

2006

NUMBER OF ESTABLISHMENTS

2016CHANGE

2006–2016

Establishments without employees 58,256 74,921 16,665

1–4 employees 17,811 24,703 6,892

5–19 employees 8,218 10,139 1,921

20–199 employees 3,350 3,943 593

200> employees 202 264 62

Total 87,837 113,970 26,133

ESTABLISHMENTS IN THE GOTHENBURG REGION 2006 AND 2016, BY SIZE CATEGORY

Gothenburg region Sweden

2001

2003

2005

2007

2009

2011

2013

2015

establishments in total in the Gothenburg region 2016113,970

GROWTH & LABOUR MARKET GROWTH & LABOUR MARKET

30%25%

17%21%

2524

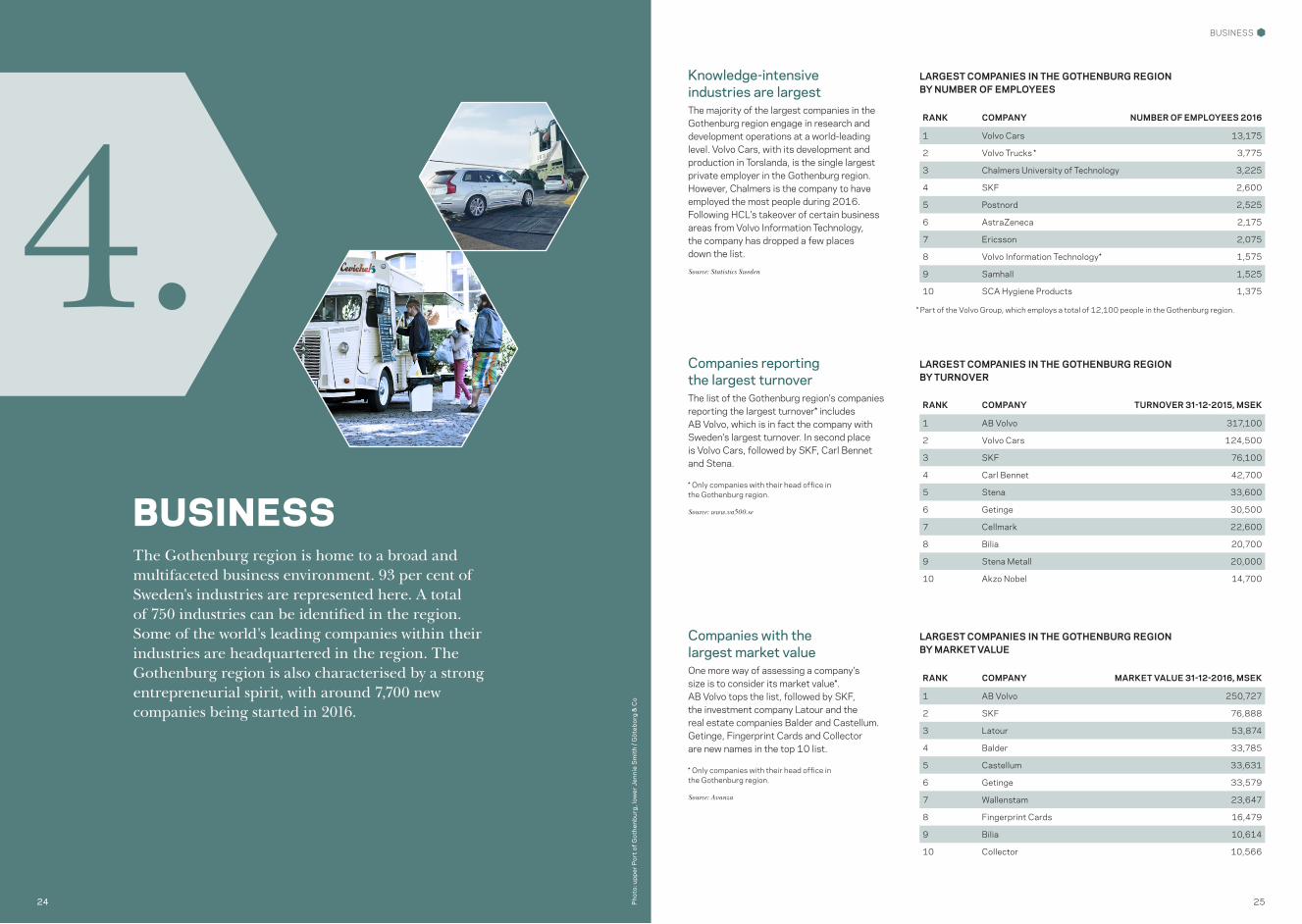

BUSINESSThe Gothenburg region is home to a broad and multifaceted business environment. 93 per cent of Sweden's industries are represented here. A total of 750 industries can be identified in the region. Some of the world's leading companies within their industries are headquartered in the region. The Gothenburg region is also characterised by a strong entrepreneurial spirit, with around 7,700 new companies being started in 2016.

4.P

hoto

: upp

er P

ort o

f Got

henb

urg,

low

er J

enni

e S

mit

h / G

öteb

org

& C

o

BUSINESS

Knowledge-intensive industries are largestThe majority of the largest companies in the Gothenburg region engage in research and development operations at a world-leading level. Volvo Cars, with its development and production in Torslanda, is the single largest private employer in the Gothenburg region. However, Chalmers is the company to have employed the most people during 2016. Following HCL's takeover of certain business areas from Volvo Information Technology, the company has dropped a few places down the list.

Source: Statistics Sweden

RANK COMPANY NUMBER OF EMPLOYEES 2016

1 Volvo Cars 13,175

2 Volvo Trucks * 3,775

3 Chalmers University of Technology 3,225

4 SKF 2,600

5 Postnord 2,525

6 AstraZeneca 2,175

7 Ericsson 2,075

8 Volvo Information Technology* 1,575

9 Samhall 1,525

10 SCA Hygiene Products 1,375

LARGEST COMPANIES IN THE GOTHENBURG REGION BY NUMBER OF EMPLOYEES

LARGEST COMPANIES IN THE GOTHENBURG REGION BY TURNOVER

LARGEST COMPANIES IN THE GOTHENBURG REGION BY MARKET VALUE

Companies reporting the largest turnoverThe list of the Gothenburg region's companies reporting the largest turnover* includes AB Volvo, which is in fact the company with Sweden's largest turnover. In second place is Volvo Cars, followed by SKF, Carl Bennet and Stena.

* Only companies with their head office in the Gothenburg region.

Source: www.va500.se

Companies with the largest market valueOne more way of assessing a company's size is to consider its market value*. AB Volvo tops the list, followed by SKF, the investment company Latour and the real estate companies Balder and Castellum. Getinge, Fingerprint Cards and Collector are new names in the top 10 list.

* Only companies with their head office in the Gothenburg region.

Source: Avanza

RANK COMPANY TURNOVER 31-12-2015, MSEK

1 AB Volvo 317,100

2 Volvo Cars 124,500

3 SKF 76,100

4 Carl Bennet 42,700

5 Stena 33,600

6 Getinge 30,500

7 Cellmark 22,600

8 Bilia 20,700

9 Stena Metall 20,000

10 Akzo Nobel 14,700

RANK COMPANY MARKET VALUE 31-12-2016, MSEK

1 AB Volvo 250,727

2 SKF 76,888

3 Latour 53,874

4 Balder 33,785

5 Castellum 33,631

6 Getinge 33,579

7 Wallenstam 23,647

8 Fingerprint Cards 16,479

9 Bilia 10,614

10 Collector 10,566

* Part of the Volvo Group, which employs a total of 12,100 people in the Gothenburg region.

26 27

0

10

20

30

40

50

60

70

2000

4000

6000

8000

10000

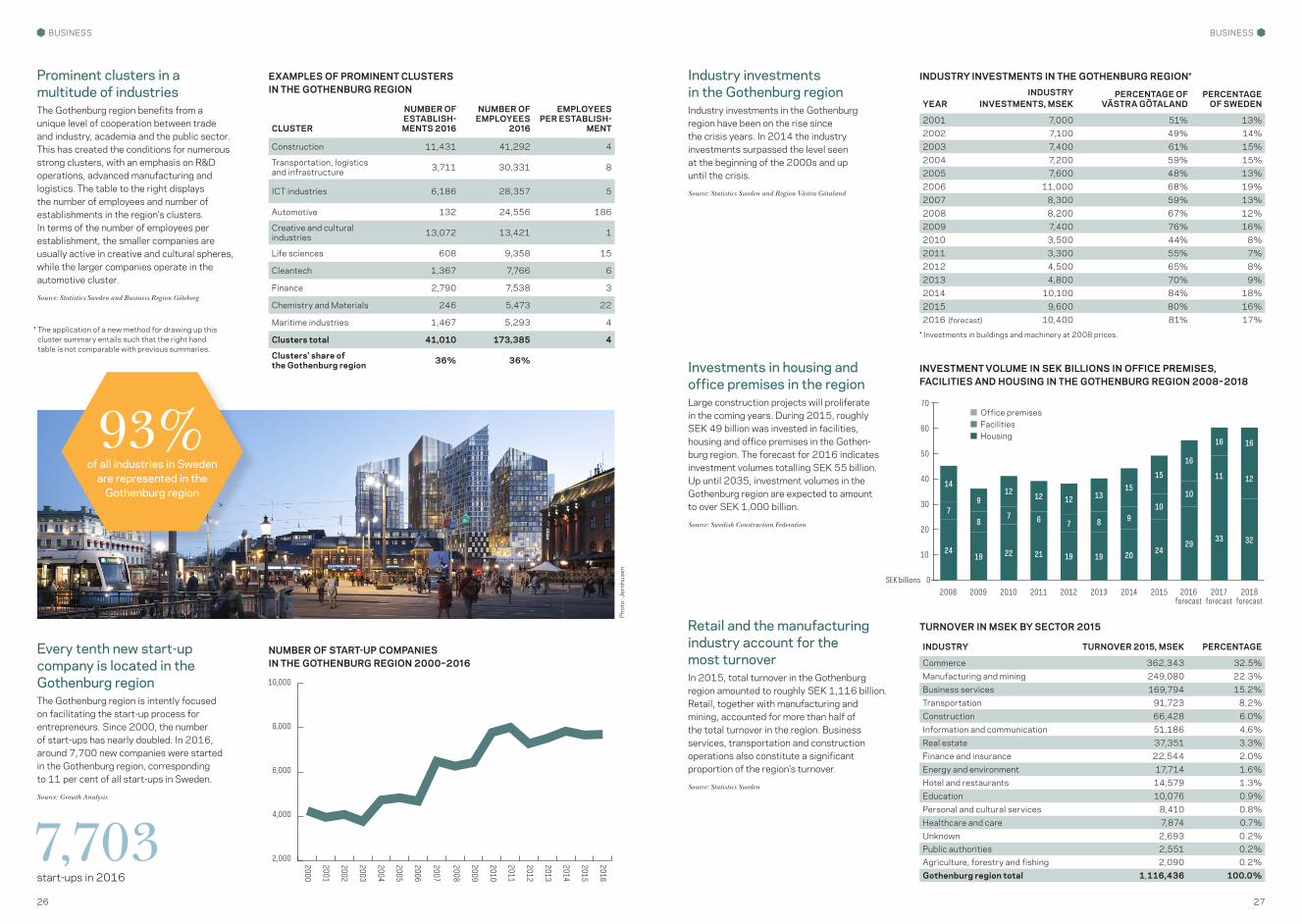

Prominent clusters in a multitude of industries The Gothenburg region benefits from a unique level of cooperation between trade and industry, academia and the public sector. This has created the conditions for numerous strong clusters, with an emphasis on R&D operations, advanced manufacturing and logistics. The table to the right displays the number of employees and number of establishments in the region's clusters. In terms of the number of employees per establishment, the smaller companies are usually active in creative and cultural spheres, while the larger companies operate in the automotive cluster.

Source: Statistics Sweden and Business Region Göteborg

EXAMPLES OF PROMINENT CLUSTERS IN THE GOTHENBURG REGION

CLUSTER

NUMBER OF ESTABLISH-MENTS 2016

NUMBER OF EMPLOYEES

2016

EMPLOYEES PER ESTABLISH-

MENT

Construction 11,431 41,292 4

Transportation, logistics and infrastructure 3,711 30,331 8

ICT industries 6,186 28,357 5

Automotive 132 24,556 186

Creative and cultural industries 13,072 13,421 1

Life sciences 608 9,358 15

Cleantech 1,367 7,766 6

Finance 2,790 7,538 3

Chemistry and Materials 246 5,473 22

Maritime industries 1,467 5,293 4

Clusters total 41,010 173,385 4

Clusters' share of the Gothenburg region 36% 36%

BUSINESS

Every tenth new start-up company is located in the Gothenburg regionThe Gothenburg region is intently focused on facilitating the start-up process for entrepreneurs. Since 2000, the number of start-ups has nearly doubled. In 2016, around 7,700 new companies were started in the Gothenburg region, corresponding to 11 per cent of all start-ups in Sweden.

Source: Growth Analysis

NUMBER OF START-UP COMPANIES IN THE GOTHENBURG REGION 2000–2016

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2013

2016

2012

2014

2,000

4,000

6,000

8,000

10,000

start-ups in 2016

7,703

* The application of a new method for drawing up this cluster summary entails such that the right hand table is not comparable with previous summaries.

2015

of all industries in Sweden are represented in the

Gothenburg region

93%

Pho

to: J

ernh

usen

Industry investments in the Gothenburg regionIndustry investments in the Gothenburg region have been on the rise since the crisis years. In 2014 the industry investments surpassed the level seen at the beginning of the 2000s and up until the crisis.

Source: Statistics Sweden and Region Västra Götaland

Retail and the manufacturing industry account for the most turnoverIn 2015, total turnover in the Gothenburg region amounted to roughly SEK 1,116 billion. Retail, together with manufacturing and mining, accounted for more than half of the total turnover in the region. Business services, transportation and construction operations also constitute a significant proportion of the region's turnover.

Source: Statistics Sweden

INDUSTRY INVESTMENTS IN THE GOTHENBURG REGION*

INDUSTRY TURNOVER 2015, MSEK PERCENTAGE

Commerce 362,343 32.5%Manufacturing and mining 249,080 22.3%Business services 169,794 15.2%Transportation 91,723 8.2%Construction 66,428 6.0%Information and communication 51,186 4.6%Real estate 37,351 3.3%Finance and insurance 22,544 2.0%Energy and environment 17,714 1.6%Hotel and restaurants 14,579 1.3%Education 10,076 0.9%Personal and cultural services 8,410 0.8%Healthcare and care 7,874 0.7%Unknown 2,693 0.2%Public authorities 2,551 0.2%Agriculture, forestry and fishing 2,090 0.2%Gothenburg region total 1,116,436 100.0%

Investments in housing and office premises in the regionLarge construction projects will proliferate in the coming years. During 2015, roughly SEK 49 billion was invested in facilities, housing and office premises in the Gothen-burg region. The forecast for 2016 indicates investment volumes totalling SEK 55 billion. Up until 2035, investment volumes in the Gothenburg region are expected to amount to over SEK 1,000 billion.

Source: Swedish Construction Federation

INVESTMENT VOLUME IN SEK BILLIONS IN OFFICE PREMISES, FACILITIES AND HOUSING IN THE GOTHENBURG REGION 2008–2018

2008 2009 2010 2011 2012 2013 2014 2015 2016forecast

SEK billions 0

10

20

30

40

70

50

60

2017forecast

2018forecast

TURNOVER IN MSEK BY SECTOR 2015

Office premises Facilities Housing

24

7

14

19

8

9

22

7

12

21

6

12

19

7

12

19

8

13

20

9

15

24

10

15

29

10

16

33

11

16

32

12

16

BUSINESS

YEARINDUSTRY

INVESTMENTS, MSEKPERCENTAGE OF

VÄSTRA GÖTALANDPERCENTAGE

OF SWEDEN

2001 7,000 51% 13%2002 7,100 49% 14%2003 7,400 61% 15%2004 7,200 59% 15%2005 7,600 48% 13%2006 11,000 68% 19%2007 8,300 59% 13%2008 8,200 67% 12%2009 7,400 76% 16%2010 3,500 44% 8%2011 3,300 55% 7%2012 4,500 65% 8%2013 4,800 70% 9%2014 10,100 84% 18%2015 9,600 80% 16%2016 10,400 81% 17%

* Investments in buildings and machinery at 2008 prices.

(forecast)

28 29

800000850000900000950000

10000001050000110000011500001200000

0,0

0,5

1,0

1,5

2,0

POPULATION, LIFESTYLE & EDUCATIONMore and more people are choosing to live and work in the Gothenburg region. In 2017 there will be more than one million inhabitants in the region. In 2016, the population of the region increased by approximately 15,000 inhabitants. The population is relatively young and more highly educated than the national average. Access to academic education and world-class companies makes the region more attractive. The Gothenburg region's two major higher learning institutes collectively have around 50,000 students. In terms of human capital and lifestyle, Gothenburg ranks highly among large European cities.

5.P

hoto

: upp

er K

jell

Hol

mne

r / G

öteb

org

& C

o, lo

wer

Jon

atha

n Fe

rnst

röm

/ B

RG

To live and work in a growing regionEvery year since 2000, the Gothenburg region's population has increased by around one per cent, with the region seeing a greater growth than Sweden throughout the entirety of the 2000s. In 2016, the absolute increase was largest in the age group 25–34, which increased by around 5,200 new inhabitants. A large increase was also seen in the age group 5–14, with approximately 3,000 new inhabitants.

Source: Statistics Sweden

Population growth continuingFor many years, the Gothenburg region has had a positive birth rate and net positive migration. In 2016, the population of the region increased by approximately 15,000 inhabitants. If the annual growth rate of around 11,000 inhabitants were to continue, the region would be home to approximately 1.2 million people in 2030.

Source: Statistics Sweden and Region Västra Götaland

Younger than the national averageBy comparing different age groups in Gothenburg region to those of Sweden it becomes clear that the region's population is relatively young. The age group 0–44 is larger than the national composition, while the age group 45–65 is smaller.

Source: Statistics Sweden

inhabitants in the Gothenburg region during 2016

997,446

Population Population forecast

800,000

900,000

850,000

950,000

1,050,000

1,000,000

1,150,000

1,200,000

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2030

2028

1,100,000

POPULATION OF THE GOTHENBURG REGION

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2010

2012

2015

2016

2014

2013

% 0

0.5

1.0

1.5

2.0

Gothenburg region Sweden

ANNUAL POPULATION GROWTH

35

30

25

20

15

10

5

% 0

Gothenburg region Sweden

0–24 25–44 45–64 65+

POPULATION 2016 BY AGE GROUP

POPULATION, LIFESTYLE & EDUCATION

30 31

POPULATION, LIFESTYLE & EDUCATION

Higher-learning institutes in the Gothenburg regionThe region's two major higher learning institutions are Chalmers University of Technology, with 13,000 students, and the University of Gothenburg, with 37,000. Both universities are among the world's elite in numerous areas of research, with around 50 departments providing education.

Source: University of Gothenburg and Chalmers University of Technology

Higher level of education than the national average Compared with Sweden as a whole, a larger proportion of the age group 25–64 in the Gothenburg region has a post-secondary education, up to the level of research- based education.

Source: Statistics Sweden

NUMBER OF STUDENTS AT CHALMERS UNIVERSITY OF TECHNOLOGY AND UNIVERSITY OF GOTHENBURG 2016

approx.50,000

SEK was the Gothenburg region's net cost for culture. Per inhabitant, the

Gothenburg region's cost for culture is just over SEK 1,000 per year.

Source: Swedish Agency for Cultural Policy Analysis

Gothenburg is seen as the most social of the three metropolitan regions and its inhabitants are the most

liberal in relation to others' lifestyles.

Source: hostelworld.com

1st place1 billion

7,000highly-educated technical

professionals change employers in the Gothenburg region – which

promotes productivity.

Source: Statistics Sweden and CIRCLE

Gothenburg region Sweden

Secondary education

Tertiary education and research education

Primary education

0 10 20 30 40 50 %

HIGHEST LEVEL OF EDUCATION COMPLETED AMONG THOSE AGED 25–64, 2015

Pho

to: u

pper

Sup

erst

udio

/ G

öteb

org

& C

o, lo

wer

Bea

tric

e Tö

rnrö

s / G

öteb

org

& C

o

COSTS & TAXESIt is relatively beneficial to establish a company in Gothenburg. The corporate tax rate is low and the rental market is among the hottest in Europe. In addition, foreign key workers in Sweden are granted a certain degree of tax relief.

6.

Pho

to: u

pper

Ben

gt K

jelli

n / B

RG

, low

er E

lisab

eth

Dun

ker /

Göt

ebor

g &

Co

32 33

COSTS & TAXES

Salary levels in the Gothenburg RegionReporting the salary spread with the help of percentile gives a fair view of the most common salaries. In the adjacent table, the value in the column for, for example, the 10th percentile corresponds to the top earning 10 per cent of the respective category. E.g., 10 per cent of the region's shop assistants within retail earn SEK 22,100 or less, while 60 per cent of the same group earn SEK 28,500 or less.

* Figures rounded to the nearest hundred.

Source: Almega, September 2016

PROFESSIONMONTHLY SALARY (SEK)

10TH PER-CENTILE

40TH PER-CENTILE

60TH PER-CENTILE

90TH PER-CENTILE

Management: economy and finance 35,400 54,200 65,000 105,300

Middle management: economy and finance 37,200 48,600 59,000 84,300

Management: personnel and HR 35,000 52,900 64,100 103,300

Middle management: personnel and HR 34,900 48,000 58,300 82,800

Management: administration and planning 43,000 59,300 73,000 138,300

Middle management: administration and planning 31,300 44,100 50,200 76,500

Management: sales and marketing 41,500 57,100 66,300 99,400

Middle management: sales and marketing 39,900 53,600 60,600 83,200

Management: IT 42,800 57,600 67,100 95,000

Middle management: IT 43,200 54,400 60,700 75,300

Management: information, communication and PR 41,900 62,100 74,600 122,200

Middle management: information, communication and PR 35,000 53,000 57,300 74,800

Management: purchasing, logistics and transport 34,000 50,900 60,800 103,100

Middle management: purchasing, logistics and transport 34,700 47,300 55,200 72,600

Accountants and economists 27,500 35,300 42,200 58,400

Management and business developers 32,600 42,300 49,100 69,300

Market analysts and marketers 32,000 40,600 46,900 64,000

Systems analysts and IT architects 36,700 44,900 48,900 59,500

Software and systems developers 30,500 39,000 43,600 53,500

Engineers and technicians: construction 27,600 32,900 37,300 50,200

Engineers and technicians: electrotechnology 27,400 35,000 39,900 51,900

Engineers and technicians: chemicals and chemical technology 27,900 34,300 37,800 48,000

Computer technicians 26,100 34,100 37,900 47,800

Salespeople 27,000 36,200 42,400 56,200

Purchasers and procurers 30,200 37,200 42,000 55,200

Office assistants and secretaries 22,400 27,600 30,100 38,000

Shop assistants: retail 22,100 26,200 28,500 38,300

MARKET SALARY STATISTICS 2016*

Fees for employersAll employers pay social security contributions for their employees. These comprise funding for pensions, health care and other social benefits. The charge amounts to a total of 31.42 per cent.

Source: The Tax Agency

EMPLOYER'S CONTRIBUTIONS FOR SOCIAL INSURANCE

% OF SALARY 2017

Retirement pension charge 10.21

Survivors' pension charge 0.70

Health insurance charge 4.35

Parental insurance 2.60

Work injury charge 0.20

Labour market charge 2.64

General payroll charge 10.72

Total statutory employer's contributions for social insurance 31.42Tax relief for foreign key personnel

Source: Taxation of Research Workers Board

25%

COSTS & TAXES

Office rentalRental prices vary considerably between different districts in Gothenburg. The map below provides an overview of the various areas of Gothenburg, with a summary of rental prices for these areas listed to the right. The highest rent is paid in the CBD*, while the lowest rent is observed in West and East Gothenburg.

Source: JLL

OFFICE RENTAL PRICES PER AREA Q4 2016

SEK/m2 per year

Competitive corporate taxThe Swedish corporate tax rate is competitive in a European context. The corporate tax rate in Sweden was reduced to 22 per cent from 1 January 2013, and remains at the same level in 2017.

Source: KPMG, 2017

Comparison of taxesSince 2013, Sweden has become one of the most attractive places in the world for holding companies. Sweden offers more than 80 tax agreements in addition to the low corporate tax rate. Sweden's tax climate also holds up well in comparison to other countries, as companies are not taxed on interest income, share dividends and royalties.

Source: Deloitte, 2017

CORPORATE TAX RATES – A EUROPEAN COMPARISON

COMPARISON OF TAXES*

UK

Finland

Sweden

Denmark

Netherlands

Spain*

Germany**

Italy

France*

0 5 10 15 2520 30 35 %

*Tax rates refer to payments to individuals not resident in the country.

TYPE OF TAX

Interest 0% 0% 0% 0% 0% 20% 0%

Dividend 0% 0% 20% 25% 0% 0% 30%

Royalties 0% 22% 20% 15% 0% 20% 30%

SWEDEN

DENMARK

FINLAND

GERMANY

NETHERLANDS

UK USA

* Small and new companies can benefit from lower corporate tax.** The corporate tax rate in Germany varies between 29.72 and 33 per cent depending on geographical location.

E20HISINGEN

EAST GOTHENBURG

NORRA ÄLVSTRANDEN

CBD*

OTHER INNER CITY

MÖLNDALWEST GOTHENBURG

E6

* Central Business District.

0

500

1,000

1,500

2,000

2,500

3,000

CBD* Other inner city

Norra Älvstranden

Other Hisingen

West Gothenburg

East Gothenburg

Mölndal

0 5 10 15 20 25 30 35Frankrike*

ItalienTyskland**

Spain*Nederländerna

DenmarkSwedenFinland

Storbritannien

34 35

COSTS & TAXES

STOCKHOLM

HELSINKI

OSLO

GOTHENBURG

COPENHAGEN

GOTHENBURG

SEK 100

SEK 840

SEK 3,000

SEK 55,900

COPENHAGEN

SEK 153

SEK 2,300

SEK 47,700

HELSINKI

SEK 114

SEK 1,180

SEK 3,200

SEK 59,500

OSLO

SEK 182

SEK 3,150

SEK 4,500

SEK 74,900

STOCKHOLM

SEK 105

SEK 1,300

SEK 6,200

SEK 89,200

Sources: Numbeo, JLL and Global Property Guide. Exchange rates from NOK to SEK, DKK to SEK and Euro to SEK obtained 12 February 2017.

NORDIC COST COMPARISONS

SEK 5,030

A cheaper meal

Office rent per m2 CBD / year

Average price per m2 city apartment

Monthly cost for a nursery place

CLIMATE, ENVIRONMENT & SUSTAINABLE DEVELOPMENTThe Gothenburg region boasts world-leading competence in sustainable development and environmental technology solutions. The region has numerous partnerships involving energy, urban development, transport, travel and waste management, aiming to reduce impact on the environment. An area which has met with considerable success is district heating. Another sign that the region is heading in the right direction in its work with the environment, climate and sustainable development is that the interest in green bonds has been huge, and new issues of green bonds have been proliferating at record pace.

7.

Pho

to: S

uper

stud

io /

Göt

ebor

g &

Co

36 37

050

100150200250300350400450500

0

100

200

300

400

500

600

0

10

20

30

40

50

60

708090

100110120130140150160170

Better air quality in GothenburgFor decades, Gothenburg has worked actively to continuously improve the city's air quality. Sulphur emissions have decreased by almost 100 per cent and are close to zero. Over a long period, the region has reduced its nitrogen dioxide emissions to a very low level. In the last 10 years, the region has also succeeded in reversing the downward trend for particle matter levels (PM10).

* Annual average unavailable for certain years due to insufficient statistical documentation.

Source: Environment Administration, City of Gothenburg

CO2 emissions are decreasing in spite of increased economic activity The region's emissions of carbon dioxide have been at a constant level for the most part of the 2000s, but in recent years these emissions have been substantially reduced. At the same time, the economic growth of the region stands at around 53 per cent, and the population has increased by 16 per cent, meaning that the emissions per growth unit have decreased (we can only measure emissions produced in the region). Since 2000, carbon dioxide emissions in the region have decreased by 12 per cent, in spite of the three large refineries in Gothenburg and the chemical industry's facilities in Stenungsund.

Source: Statistics Sweden and National Emissions Database

AIR QUALITY IN GOTHENBURG 1981–2015*

DEVELOPMENT OF REAL GROSS REGIONAL PRODUCT (GRP) AND CO2 IN THE GOTHENBURG REGION, 2000–2014 (INDEX 2000 = 100)

2001

2005

20011983

2002

2000

2005

2003

1981

1987

1985

1993

1991

19892003

2007

2006

1999

1997

1995

2004

2011

2013

2007

2008

2009

2010

2013

2012

2011

0

10

70

80

90

100

110

120

130

140

170

160

150

40

20

50

30

60

µg/m3

CLIMATE, ENVIRONMENT & SUSTAINABLE DEVELOPMENT

2015

2009

2014

Nitrogen dioxide Particulate matter (PM10) Sulphur dioxide

Real GRP CO2

Pho

to: E

lect

riC

ity

ElectriCity is a collaboration project to create a more sustainable public transport system.

Index

CLIMATE, ENVIRONMENT & SUSTAINABLE DEVELOPMENT

WASTE MANAGEMENT IN GOTHENBURG 1992–2015 Emissions and incinerationGothenburg is talented at waste management. Even though the city incinerates more waste than before, emissions are steadily decreasing. The heat from waste incineration covers a third of the district heating in the region and approximately 5 per cent of the electricity demand in Gothenburg. In addition, 60 per cent of generated electricity comes from biogas.

*Statistics refer to Sävenäs waste treatment facility.

Source: Renova

2001

2003

2004

1993

1997

1992

1999

2005

2006

2000

2002

2007

2008

2009

2001

2010

2012

2014

2013

0

100

200

300

400

500

Incinerated waste (ktonnes)600

2001

2003

2004

1993

1997

1992

1999

2005

2006

2000

2002

2007

2008

2009

2001

2010

2012

2014

2013

0

50

100

150

200

250

300

350

450

400

500Emissions (tonnes)

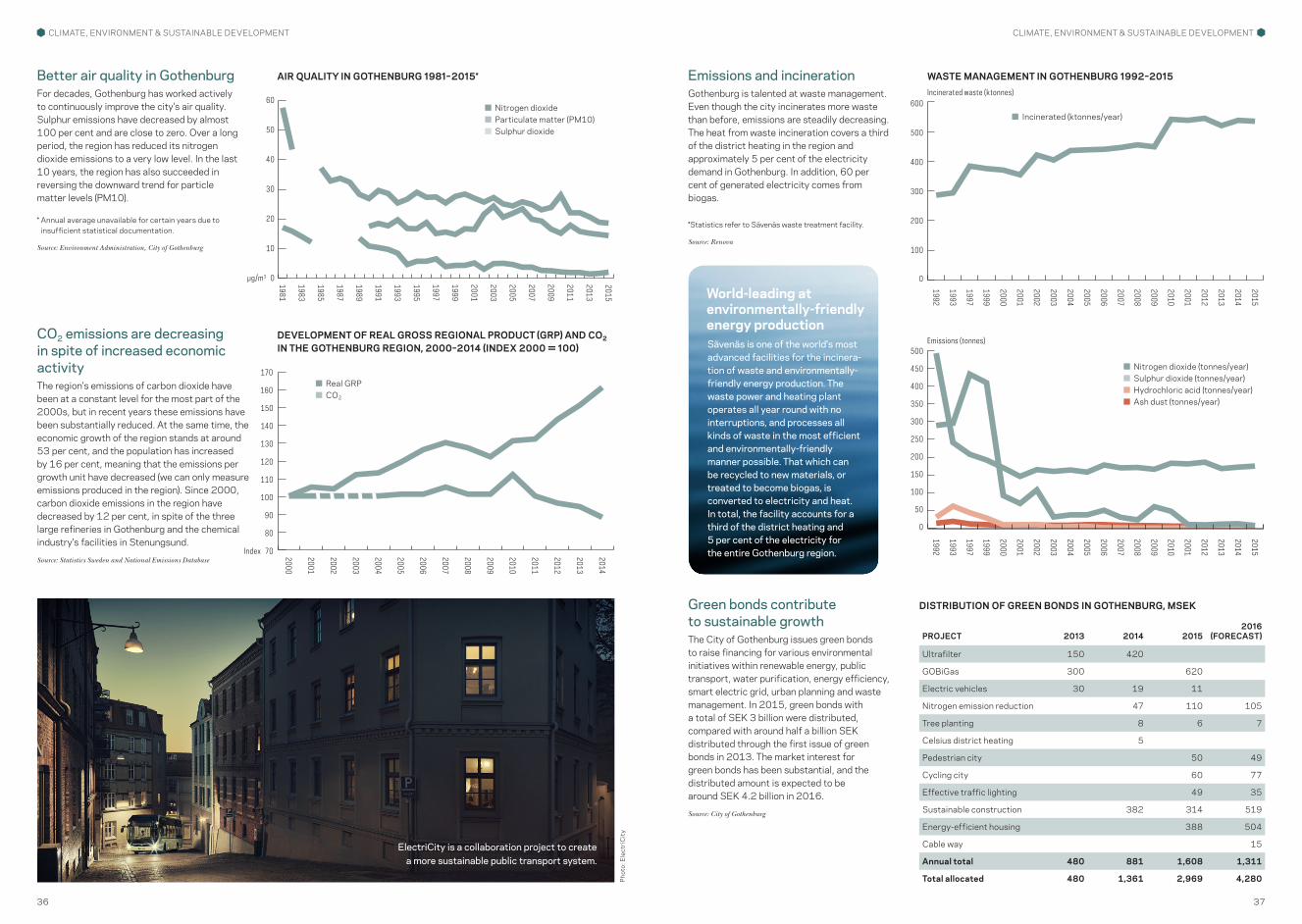

Green bonds contribute to sustainable growthThe City of Gothenburg issues green bonds to raise financing for various environmental initiatives within renewable energy, public transport, water purification, energy efficiency, smart electric grid, urban planning and waste management. In 2015, green bonds with a total of SEK 3 billion were distributed, compared with around half a billion SEK distributed through the first issue of green bonds in 2013. The market interest for green bonds has been substantial, and the distributed amount is expected to be around SEK 4.2 billion in 2016.

Source: City of Gothenburg

DISTRIBUTION OF GREEN BONDS IN GOTHENBURG, MSEK

PROJECT 2013 2014 20152016

(FORECAST)

Ultrafilter 150 420

GOBiGas 300 620

Electric vehicles 30 19 11

Nitrogen emission reduction 47 110 105

Tree planting 8 6 7

Celsius district heating 5

Pedestrian city 50 49

Cycling city 60 77

Effective traffic lighting 49 35

Sustainable construction 382 314 519

Energy-efficient housing 388 504

Cable way 15

Annual total 480 881 1,608 1,311

Total allocated 480 1,361 2,969 4,280

20152015

Sävenäs is one of the world's most advanced facilities for the incinera-tion of waste and environmentally-friendly energy production. The waste power and heating plant operates all year round with no interruptions, and processes all kinds of waste in the most efficient and environmentally-friendly manner possible. That which can be recycled to new materials, or treated to become biogas, is converted to electricity and heat. In total, the facility accounts for a third of the district heating and 5 per cent of the electricity for the entire Gothenburg region.

World-leading at environmentally-friendly energy production

Incinerated (ktonnes/year)

Nitrogen dioxide (tonnes/year) Sulphur dioxide (tonnes/year) Hydrochloric acid (tonnes/year) Ash dust (tonnes/year)

-

0

20

40

60

80

100

38

Renewable energy in public transportThe proportion of vehicle miles driven with renewable fuel is steadily on the increase in the Gothenburg region. In 2010, around 36 per cent of the Gothenburg region's public transport was fuelled by renewable sources. By 2016, this figure had gone up to around 93 per cent. Biodiesel and biogas have contributed the most to phasing out the non-renewable fuels in the region's public transport. In more recent years, tall oil and animal waste (HVO) have strongly contributed to phasing out the non-renewable fuels in the region's public transport.

Source: Västtrafik

2010 2011 2012 2013 2014 20150

20

40

60

80

100

PERCENTAGE OF VEHICLE KILOMETRES WITH RENEWABLE FUEL IN PUBLIC TRANSPORT IN THE GOTHENBURG REGION

%2016

36%

49%58%

73%80% 85%

93%

Did you know…Waste = heatThere are a number of collection systems

for waste in the Gothenburg region. A certain amount of waste is recycled to become

new material, while other waste is used to produce electricity, heat or fuel.

Source: Green Gothenburg

90%of all apartment

buildings in Gothenburg have district heating

Gothenburg is a world leader in district heating. District heating contributes to better air while making it possible to use heat that

would otherwise be lost.

Source: Göteborg Energi

The world's bestThe Port of Gothenburg works proactively

and with a long-term approach to minimise the environmental impact of shipping operations and to contribute to sustainable transport. The port is

internationally renowned for its environmental work and is classed as one of the world's

leading ports in this area.

Source: Port of Gothenburg 2020will see Landvetter Airport's carbon

dioxide emissions reach zero. The airport is already taking strict measures to reduce its

environmental impact and carbon dioxide emissions have sunk drastically. The airport is certified

to the highest level according to an international standard for its work to

reduce emissions.

Source: Swedavia

1%of heating in Gothenburg is powered by oil.

Source: Business Region Göteborg

HVO Electricity Biogas Biodiesel

Pho

to: P

ort o

f Got

henb

urg

Photo cover: upper Göran Assner / BRG, illustration: Varpunen, lower Per Pixel Peterson / Göteborg & Co

Find out more from Business Region Göteborg's other reports and publications on the business environment in the Gothenburg region at www.businessregiongoteborg.com

Economic OutlookEconomic Outlook provides a summarised view of the economic situation in Gothenburg in comparison to other regions. The report presents many up-to-date performance indicators for trade and industry, including those linked to the labour market. Published quarterly.

Investment MappingThe Gothenburg region is on the verge of - and has already begun implementing – substantial investments in both infrastructure and urban development. This report maps out the planned investments, which total an estimated 100 billion euros by 2035.

Looking for business opportunitiesThis publication presents some of the key business and investment opportunities in the Gothenburg region.

Retail GuideRetail Guide is an annual publication that presents retail opportunities in the Gothenburg region, and provides facts and information about the market, demand and supply.

MORE FROM US!

CLIMATE, ENVIRONMENT & SUSTAINABLE DEVELOPMENT

Business Region Göteborg AB. P.O, Box 111 19, SE-404 23 Gothenburg Visiting address: Norra Hamngatan 14, 1st Floor. Telephone: +46 31 367 61 00

www.businessregiongoteborg.com [email protected]

Val

enti

n&B

yhr.