abertura – fabio: 10 min - klabin – relações com …ri.klabin.com.br/ptb/3245/klabin...

TRANSCRIPT

DEZEMBRO DE 2015

KLBN11 / KLBAY

INSTITUTIONAL PRESENTATION

3Q16

KLBN11

DISCLAIMER

The statements contained in this presentation related to the business outlook, operating and financial projections, and growth

prospects of Klabin S.A. are merely projections, and as such are based exclusively on the expectations of the Company’s

management concerning the future of the business.

These forward-looking statements depend substantially on the market conditions, the performance of the Brazilian economy,

the industry and international markets, and therefore are subject to change without prior notice.

This presentation on Klabin’s performance includes non-accounting and accounting data, such as operating and financial

information, as well as projections based on Management’s expectations. Note that the non-accounting data has not been

reviewed by the Company’s independent auditors.

The Company’s management believes EBITDA may provide useful information on the Company’s operating performance and

allow for comparisons with other companies in the same industry. Note however that EBITDA is not a measure established in

accordance with generally accepted accounting principles of the International Financial Reporting Standards – IFRS, and may be

defined and calculated differently by other companies.

2

170k tpy

RECYCLED FIBERS

265 THOUSAND TPY

INTEGRATED BUSINESS MODEL

DIVERSIFIED AND FLEXIBLE

* Installed capacity

TOTAL LAND

489k hectares

140k hectares

90k hectares

PINE EUCALYPTUS

PUMA PULP

FIBERS

3.5 million tpy

1.1mi tpy short fiber

0.4mi tpy long fiber &

fluff pulp

INTEGRATED

PULP

1.8mi tpy

PAPER

2.0 million tpy

COATED

BOARDS

750k

tpy

CONTAINERBOARDS

1.25mi tpy

CONVERSION

920 thousand tpy

CORRUGATED

BOXES

INDUSTRIAL

BAGS

750k tpy

PLANTED FORESTS

230k hectares

46 38

22 22

10 7 4 4

a b c d e f g

STRUCTURAL COMPETIVENESS HIGH PRODUCTIVITY ON FIBERS

24

31

35

3942 42

4446 47

20

30

40

50

<69 70-89 90-04 05 06-09 10-11 12-15 16-20 21-25

58 44

25 20 12 10 6 4

a b c d e f g

Eucalyptus m³/ha/year

Forestry

LOW AVERAGE

HAULING DISTANCE

PR with PUMA 66 Km

SC 74 Km

Mean Annual Increment (MAI) - KLABIN

PLANTED AREA

230 TSD HECTARES

OF HIGH YIELD FOREST

26

3541

50 5258 61

65

20

30

40

50

60

70

<73 74-85 85-95 95-05 05-11 12-15 16-20 21-25

m3/ha/year

Pine

Pine Eucalyptus

E E

* Source: Ibá and Klabin

Source: Hawkins Wright – april 2016

288

447

174

409

462

272

335

5 million

tonnes

ANNUAL

CAPACITY

10 million

tonnes

15 million

tonnes

20 million

tonnes

25 million

tonnes

30 million

tonnes

FOB

US$/TONNES

Softwood

Hardwood

STRUCTURAL COMPETITIVENESS GLOBAL SOFTWOOD AND HARDWOOD CASH COST

240

2Q16 3Q16

256

PULP CASH COST

USD per tonne

RAMP UP

85% OF THE MILL CAPACITY

TOTAL PRODUCTION IN THE 3Q16

294 THOUSAND TONNES

CASH COST REDUCTION

COST DILUTION ON TRACK

STRUCTURAL COMPETITIVENESS PUMA MILL EVOLUTION

production

capacity

production

cash cost

US$/tonnes

STRUCTURAL COMPETIVENESS LOW CASH COST POSITION

Source: Poyry 4Q15, 1US$ = R$ 3,50 Paper Machine (PM)

LPB PRODUCTION SITES

PM7

PM9

BEST CASH COST ON LPB PRODUCTION

35% LOWER THAN OTHER PLAYERS

KRAFTLINER

Market Share*

40%

INDUSTRIAL

BAGS

Market Share

50%

CORRUGATED

Market Share

18%

COATED

BOARDS

Market Share

50%

PAPER AND PACKAGING LEADERSHIP IN RESILIENT MARKETS

* Of Brazilian installed capacity

13% Other

consumer goods Building

8%

Others Food 67%

MARKETS DESTINATION

EUCALYPTUS PULP

BEKP IN BALES

PINE PULP

BSKP IN BALES

LONG FIBER FLUFF IN

REELS

PULP MARKETS DIFFERENT FIBERS, DIFFERENT MARKETS

KLABIN, THE PULP SOLUTION

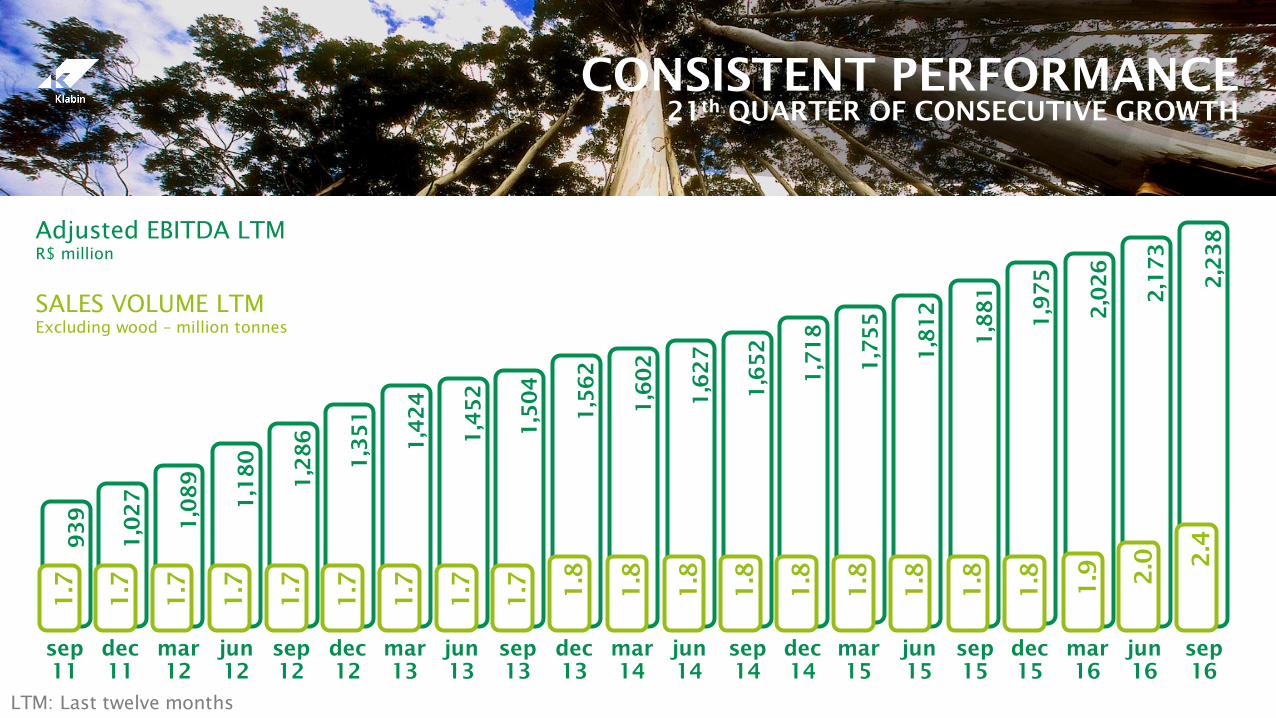

CONSISTENT PERFORMANCE 21

th QUARTER OF CONSECUTIVE GROWTH

SALES VOLUME LTM

Excluding wood – million tonnes

Adjusted EBITDA LTM

R$ million

1,0

27

dec

11

1,0

89

mar

12

93

9

sep

11

1,1

80

jun

12

1,2

86

sep

12

1,3

51

dec

12

1,4

24

mar

13

1,4

52

jun

13

1,5

04

sep

13

1,5

62

dec

13

1,6

02

mar

14

1,6

27

1.7

1.7

1.7

1.7

1.7

1.7

1.7

1.7

1.7

1.8

1.8

1.8

jun

14

1,6

52

sep

14

1,7

18

dec

14

1,7

55

mar

15

1,8

12

jun

15

1,8

81

1.8

1.8

1.8

1.8

1.8

sep

15

LTM: Last twelve months

1,9

75

1

.8

dec

15

2,0

26

1

.9

mar

16

2,1

73

2

.0

jun

16

2,2

38

2

.4

sep

16

INCREASING FLEXIBILITY AND

INTEGRATION

HEVI

Location: Manaus (AM)

EMBALPLAN

Location : Rio Negro (PR)

INCREASE OF

KLABIN PRESENCE IN DIFFERENT REGIONS

NO CLIENTS OVERLAP NEW MARKETS

70 THOUSAND TONNES

CAPACITY INCREASE

NEW CORRUGATED BOXES UNITS

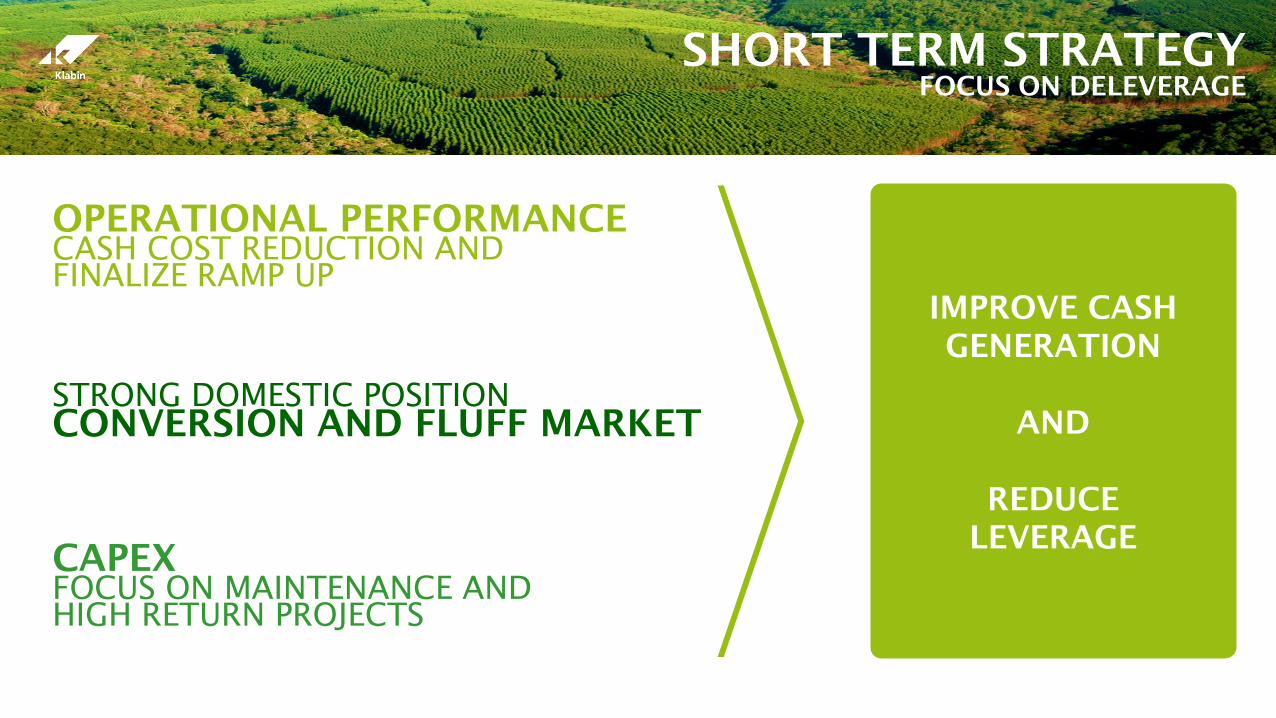

SHORT TERM STRATEGY FOCUS ON DELEVERAGE

STRONG DOMESTIC POSITION

CONVERSION AND FLUFF MARKET

CAPEX

FOCUS ON MAINTENANCE AND

HIGH RETURN PROJECTS

OPERATIONAL PERFORMANCE

CASH COST REDUCTION AND

FINALIZE RAMP UP

IMPROVE CASH

GENERATION

AND

REDUCE

LEVERAGE

FUTURE GROWTH

EXPANDING THE INTEGRATED BUSINESS MODEL

* Installed capacity

TOTAL LAND

489k hectares

140k hectares

90k hectares

PINE EUCALYPTUS

PUMA PULP

FIBERS

3.5 million tpy

1.1mi tpy short fiber

0.4mi tpy long fiber &

fluff pulp

INTEGRATED

PULP

1.8mi tpy

PAPER AND CONVERSION

FUTURE GROWTH

COATED

BOARDS

750k

tpy

170k tpy

RECYCLED FIBERS

265 THOUSAND TPY

CONTAINERBOARDS

1.25mi tpy

CORRUGATED

BOXES

INDUSTRIAL

BAGS

750k tpy

PLANTED FORESTS

230k hectares

FOCUS IN PAPER AND

PACKAGING

3Q16 RESULTS

67%

33%

463

44%

56%

787

67%

33%

1.446

57%

43%

1.965

585

520

SALES VOLUME

Excluding wood- tsd tonnes

NET REVENUE

R$ million

SALES VOLUME, NET REVENUE

AND EBITDA

ADJUSTED EBITDA

R$ million

3Q15 3Q16 3Q15 3Q16 3Q15 3Q16

EXPORTS

DOMESTIC

MARKET

26%

74%

106

23%

77%

94

174

226

61%

39%

172

58%

42%

181

551 528

KRAFTLINER COATED BOARDS

3Q15 3Q16 3Q15 3Q16 3Q15 3Q16 3Q15 3Q16

EXPORTS

DOMESTIC

MARKET

PAPER BUSINESS UNIT

SALES VOLUME NET REVENUE SALES VOLUME NET REVENUE

tsd tonnes tsd tonnes R$ million R$ million

183

174

621

577

CONVERSION BUSINESS UNIT

3Q15 3Q16 3Q15 3Q16

SALES VOLUME NET REVENUE

tsd tonnes R$ million

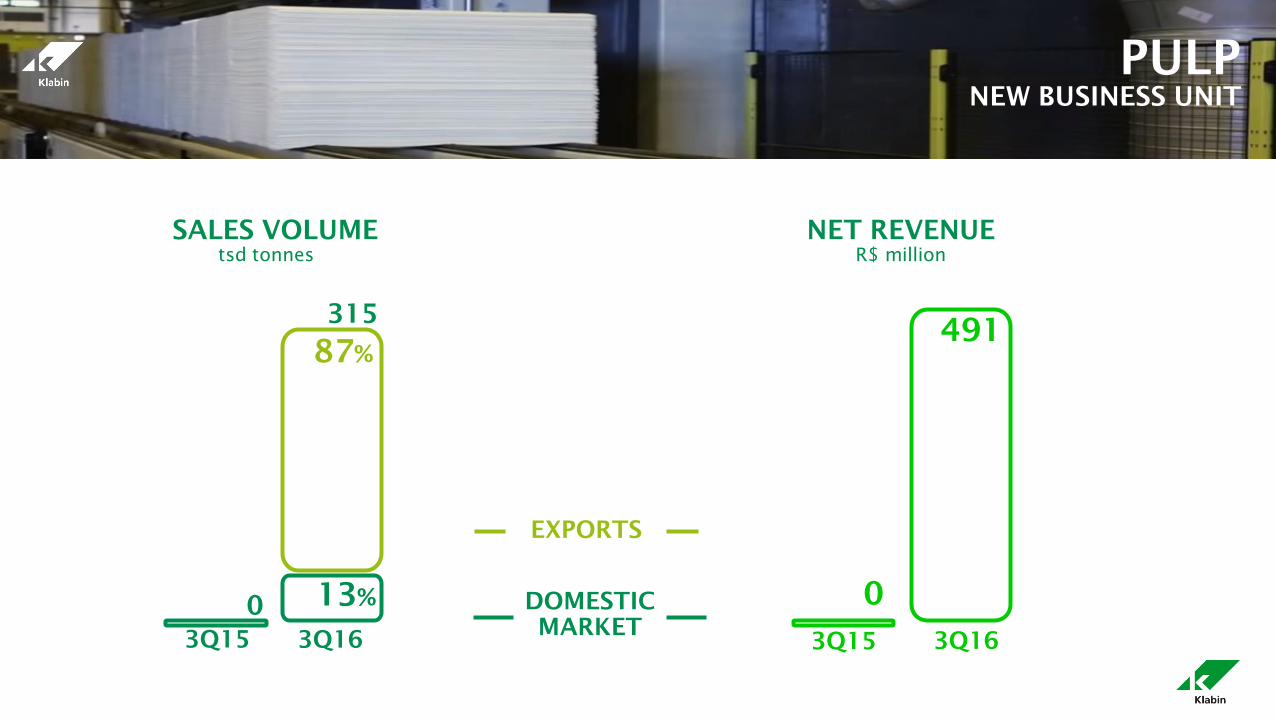

0

3Q15

13%

87%

315

3Q16 3Q15 3Q16

491

0

PULP NEW BUSINESS UNIT

EXPORTS

DOMESTIC

MARKET

SALES VOLUME NET REVENUE

tsd tonnes R$ million

CASH COST

3Q15 3Q16

UNIT

CASH COST

3Q16

R$/tonne

Labor /

third parties

33%

Wood /

Fibers

16%

Chemicals

13%

Freight

12%

Maintenance

/ stoppage

9%

Electricity

7%

Fuel Oil

4%

Others

6%

CASH COST

BREAKDOWN

3Q16

1,773

2,024

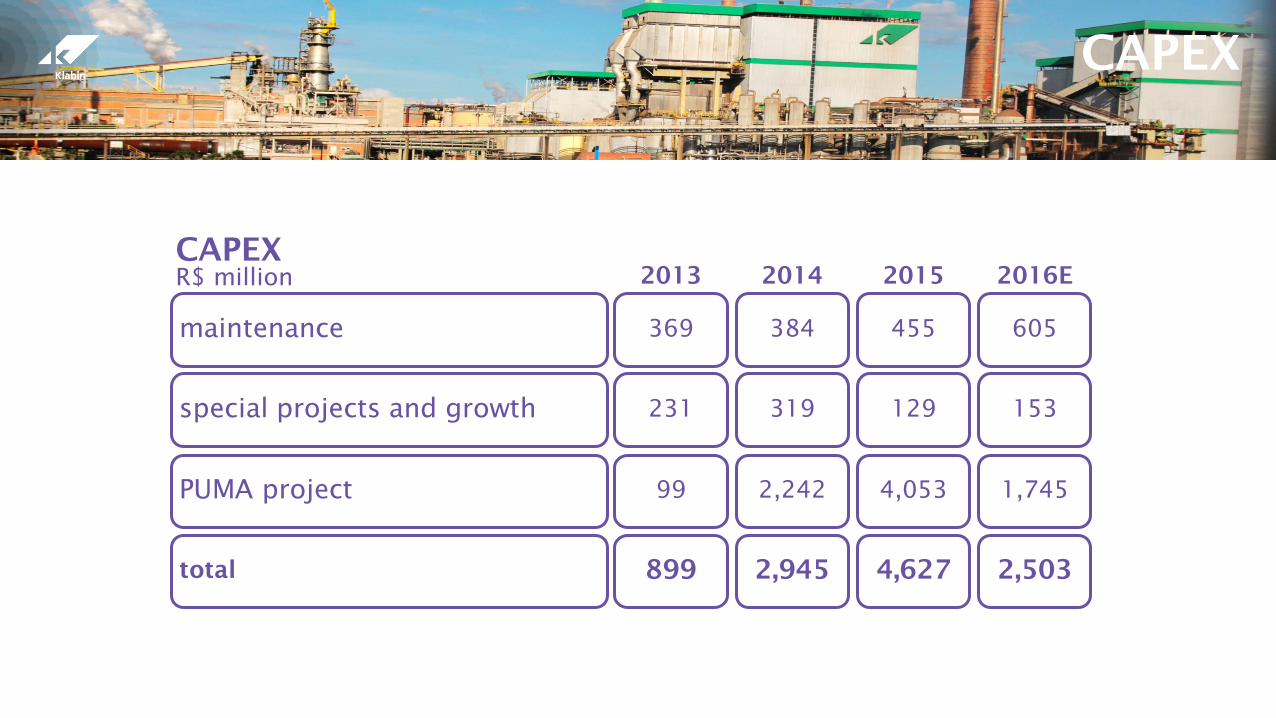

CAPEX

maintenance

CAPEX

R$ million

special projects and growth

PUMA project

total

2013

369

231

99

899

2014

384

319

2,242

2,945

2015

455

129

4,053

4,627

2016E

605

153

1,745

2,503

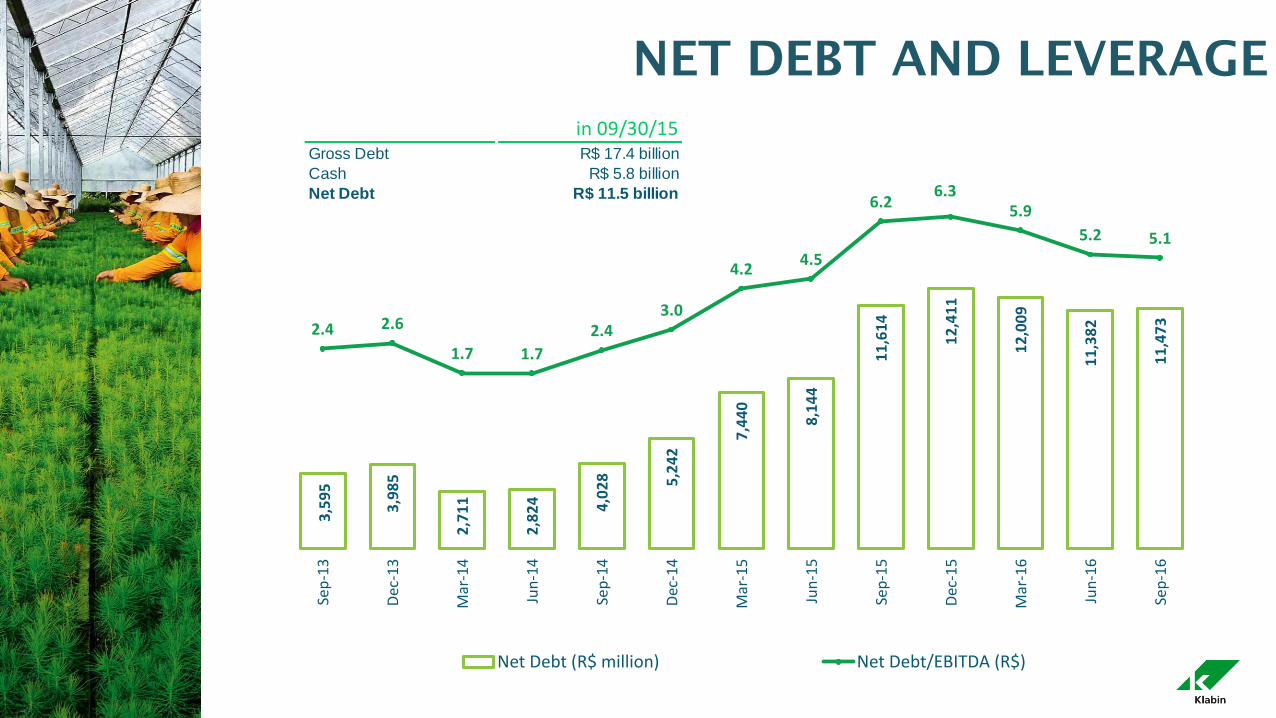

NET DEBT AND LEVERAGE

3,5

95

3,9

85

2,7

11

2,8

24

4,0

28

5,2

42

7,4

40

8,1

44

11

,61

4

12

,41

1

12

,00

9

11

,38

2

11

,47

3 2.4 2.6

1.7 1.7

2.43.0

4.24.5

6.26.3

5.9

5.2 5.1

-4.0-3.5-3.0-2.5-2.0-1.5-1.0-0.50.00.51.01.52.02.53.03.54.04.55.05.56.06.57.0

(1,000)

1,000

3,000

5,000

7,000

9,000

11,000

13,000

15,000

17,000

Sep

-13

Dec

-13

Mar

-14

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

Sep

-15

Dec

-15

Mar

-16

Jun

-16

Sep

-16

NET DEBT AND LEVERAGE

Net Debt (R$ million) Net Debt/EBITDA (R$)

in 09/30/15Gross Debt R$ 17.4 billion

Cash R$ 5.8 billion

Net Debt R$ 11.5 billion

DEBT MATURITY

Cash position

5,810 SOLID CASH POSITION

Local currency : R$ 5.6 billionAverage tenor: 40 months

Foreign currency: R$ 12 billionAverage tenor : 50 months

Foreign Currency12,024

LocalCurrency 5,168

Gross Debt17,192

R$ million

121 146 266

896

678 619

1,189

526 404 343

244

1

237

429

666

1,391 1,571 1,647

1,554

1,569

1,106

426

1,895

198

358

575

932

2,287 2,249 2,266

2,744

2,096

1,510

770

2,139

200

3Q16 4Q16 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025/26

Foreign Currency 12,508

Local Currency 5,381

Gross Debt 17,889

R$ million

405

84 163

651

858 773

596

1.070

502 380

323 227

1

573

129 115

816

1.545 1.722

1.687

1.678

1.300

1.059

390

2.094

216

977

212 278

1.468

2.402 2.495

2.283

2.748

1.803

1.439

713

2.321

218

2Q16 3Q16 4Q16 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025/26

APPENDIX

GLOBAL PULP INCREASING DEMAND IN BOTH FIBERS

2015

24.7

2016

25.4

2017

25.0 26.2

2019 2018

24.3

2014

23.7

CAGR +2%

2020

26.2

LONG FIBER

31.0

2016

32.3

2017

33.2

2018

34.1

2019

35.0

2020

CAGR +3%

28.9

2014 2015

30.0

Asia/ Africa

China

Latin America

Europe

North America

SHORT FIBER

Source: Hawkins Wright Million tonnes per year

CHINA LEADS THE GROWTH

FLUFF BRAZIL IS THE 3RD LARGEST MARKETOF DISPOSABLE DIAPERS IN THE WORLD

Source : Euromonitor

610 788

1,005 1,183

1,363

1,605

1,861

2,133

2,430

2,733

3,042

2016 2014 2013 2012 2015 2011 2009 2010 2020 2019 2018 2017

SALES OF DIAPERS FOR ADULTS

R$ million

3,398

4,000 4,645

4,827 5,279

5,768 6,272

6,790 7,297

7,864

8,468

2016 2014 2013 2012 2015 2011 2009 2010 2020 2019 2018 2017

SALES OF DIAPERS FOR INFANT

R$ million 9,139

3,377

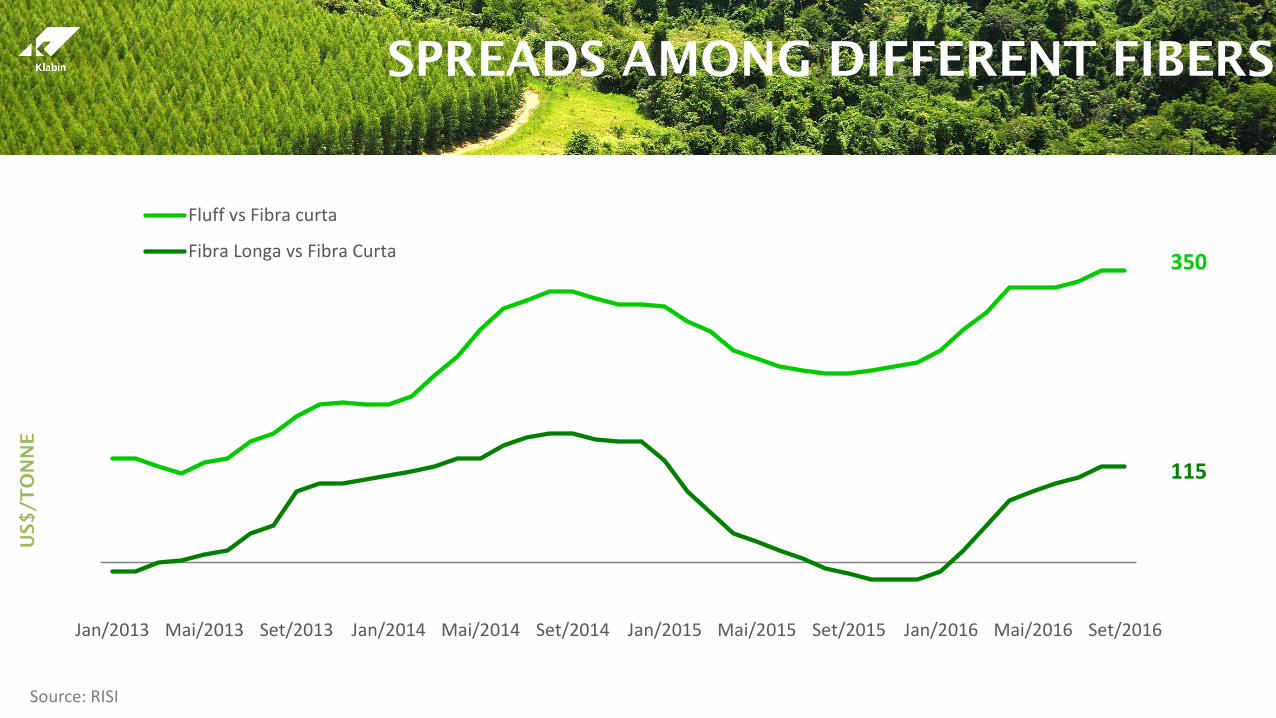

SPREADS AMONG DIFFERENT FIBERS

115

350

Source: RISI

US$

/T

ON

NE

Jan/2013 Mai/2013 Set/2013 Jan/2014 Mai/2014 Set/2014 Jan/2015 Mai/2015 Set/2015 Jan/2016 Mai/2016 Set/2016

Fluff vs Fibra curta

Fibra Longa vs Fibra Curta

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

0% 20% 40% 60% 80%

PACKAGING MARKETS

FOCUS IN LARGE AND GROWING MARKETS

PAPER MARKETS DEMAND (2014-2030)

Source: POYRY

100%

Share of consumption in 2014

Tissue KLABIN Pulp

Containerboards KLABIN kraftliner and recycled paper Cartonboards

KLABIN coated boards

Sackpaper KLABIN sack kraft and

industrial bags

Market A

Market B

Market C

Market E Market D

Demand growth per year

KLABIN MARKETS

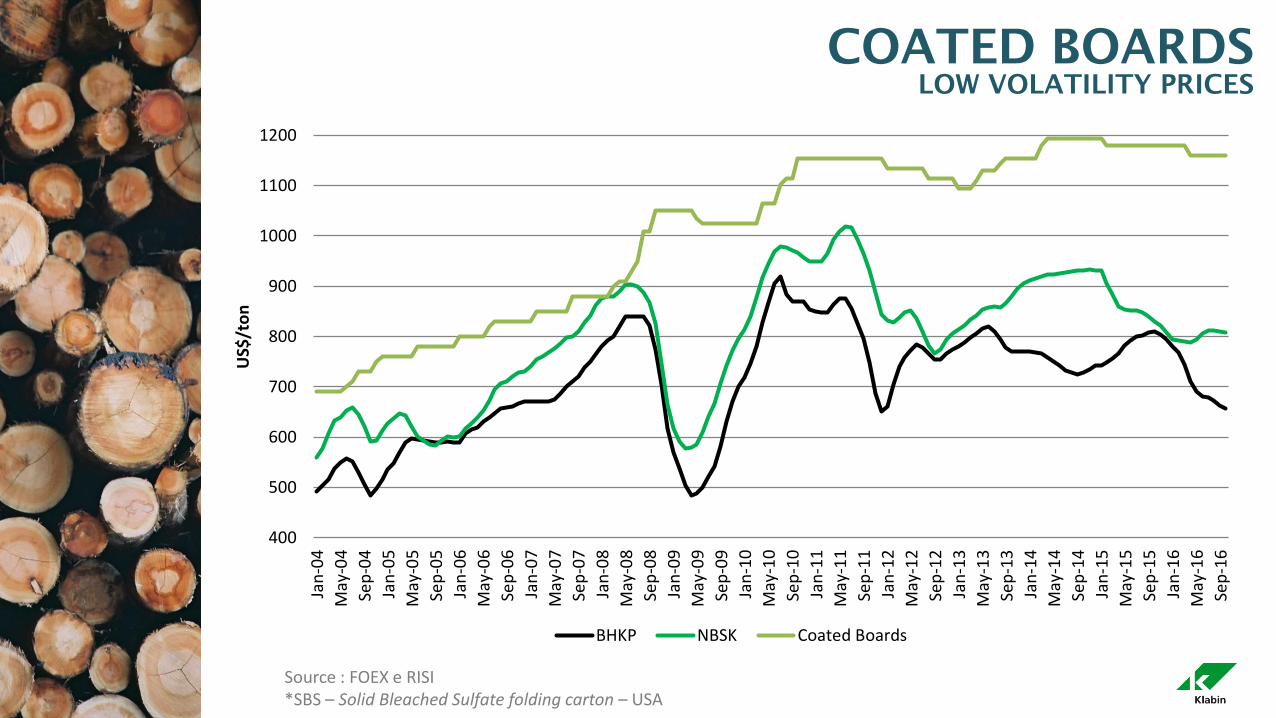

COATED BOARDS LOW VOLATILITY PRICES

Source : FOEX e RISI *SBS – Solid Bleached Sulfate folding carton – USA

*

400

500

600

700

800

900

1000

1100

1200

Jan

-04

May

-04

Sep

-04

Jan

-05

May

-05

Sep

-05

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Sep

-15

Jan

-16

May

-16

Sep

-16

US$

/to

n

BHKP NBSK Coated Boards

SUSTAINABILITY PERFORMANCE

39

55 59

81

95 Not

disclosed

2011 2012 2013 2014 2015 2016

Climate Change Score

Disclosing environmental footprint since 2006

2015 BEST PRACTICE OF NATURAL CAPITAL

MANAGEMENT

The company that advanced most in fighting

deforestation in supply chain 2014

3rd CONSECUTIVE YEAR

One of the most sustainable

companies of Brazil

2013 2014 2015

Klabin

ISE 74,5%

2013

82%

2015

WWF Environmental

Paper Company Index

“WWF EPECI recognizes transparency

and continual improvement”