a sustainable business model based on innovation ... - roche · 1 roche a sustainable business...

TRANSCRIPT

11

RocheA sustainable business model based on innovation and productivity gains

Karl Mahler, Head of Investor Relations

2

(1) pricing and product initiatives of competitors; (2) legislative and regulatory developments and economic conditions;(3) delay or inability in obtaining regulatory approvals or bringing products to market;(4) developments in financial market conditions, including the market for acquisition financing and other capital markets and fluctuations in

currency exchange rates;(5) uncertainties in the discovery, development or marketing of new products or new uses of existing products, including without limitation

negative results of clinical trials or research projects and unexpected side-effects of pipeline or marketed products; (6) increased government pricing pressures or changes in third party reimbursement rates; (7) interruptions in production;(8) loss of or inability to obtain adequate protection for intellectual property rights;(9) Litigation;(10) the inherent uncertainties involved in negotiations with the special committee of Genentech and that there can be no assurances that a

negotiated transaction will ultimately be agreed to or consummated;(11) potential difficulties in integrating the businesses of Genentech and Roche, and that some or all of the anticipated benefits of the

proposed transaction may not be realized on the schedule contemplated or at all;(12) that future dividends are subject to the discretion of the board of directors of Roche and a number of other factors, some of which are

beyond the control of Roche;(13) the ability of Roche to generate cash flow to, among other things, repay acquisition-related debt as currently contemplated; (14) loss of key executives or other employees; and(15) adverse publicity and news coverage.

The directors of Genentech who are also employees of Roche will not take part in the consideration of the proposed transaction by the Genentech board and accordingly are not permitted to comment or respond to questions regarding the transaction as representatives of Genentech.

For marketed products discussed in this presentation, please see full prescribing information on our website – www.roche.com

All mentioned trademarks are legally protected.

This presentation contains certain forward-looking statements. These forward-looking statements may be identified by words such as “believes”, “expects”, “anticipates”, “projects”, “intends”, “should”, “seeks”, “estimates”, “future” or similar expressions or by discussion of, among other things,strategy, goals, plans or intentions. Various factors may cause actual results to differ materially in the future from those reflected in forward-looking statements contained in this document, including among others:

3

Performance up-date

Strategy

Main trends influencing long term value propositions

Summary

4

2008 Sales: ~CHF 4 bn underlying organic sales

Strong impact by currencies and Tamiflu pandemic

2'018

2'713

4'306

-1,593

-516

978

1'185

125

-3,229

+9 % +11 % +4 % +10 % +10 % +6 %-86 % -1 %

Roche Pharma

Genentech Chugai Diagnostics Division

Group

Tamiflupandemic

Group incl. Tamiflu pandemic

FX Group CHF~CHF 4 bn organic

sales growth

CHF m

5

Sales 46.1 45.6 -0.5 -1 +6

Operating profit 14.5 13.9 -0.5 -4 +4

as % of sales 31.4 30.5

Net income 11.4 10.8 -0.6 -5

as % of sales 24.8 23.8

Core EPS 11.85 11.04 -7 +2

ChangeCHF billion 2007 2008 CHF billion % loc %

2008: Core EPS target achieved

While increasing investments in R&D and despite difficult financial environment

6

Performance up-date

Our Strategy and the changing environment

Main trends influencing long term value propositions

Summary

7

Roche’s unique window of opportunity

The industry

Low replacement power of current earnings levels

Poor pipelines

Cost cutting

2007 2013-14

Growth

Bridging the cliffs, Cost-cutting, Diversification

Peers

Roche

Roche’s unique position

Stability of

business model

Roche

Extended stability

Low generic exposure

Investment into the future

8

Focus on our core businesses

Generics

Low

High

Premium for Innovation

Roche Focus Dia

MedTech

OTC

Pharma

High

Medical

Differentiation

9

Roche’s strategy focuses along either dimension

Source: SDI Analysis

Proximityto Core

(regardingproducts)

Proximity to Core(regarding business model)

Gen

erics

Gen

erics

Vacc

ines

Vacc

ines

Corixa

Zentiva

Lek

Hexal

Chiron

Domantis

Sirtris

Sabex

Bubble size depicts value of acquisition

*

BioVeris

NimbleGen

GlycArt

Phar

ma

Phar

ma

10

Major arguments for and against diversification

For Diversification Against Diversification

• Risk mitigation • If not a top tier performer- potential value

destruction

• Potentially lower acquisition

costs vs. pharma acquisitions

• Different business models increase

integration complexity

• Lower overall R&D investment

spend / risk for generic drugs• Lower margins (e.g. for generic drugs)

• Broader R&D pipeline (e.g.

vaccines)

• Oversight of good pharma deals due to

lack of focus

Risk mitigation vs. lack of focus

11SDI Analysis; Source: Annual Reports of corresponding companies, datastream, currency rates (average 365 days)

200720052004 20062003

150

100

200

50

0

Operative Cash Flow per employee250

CHF 000’s

Novartis

Roche

Sanofi-Aventis

GSK

Profitability measures

Operating cash flow per employee

12

Years

NDA Review

Not to invest in the future means being out of business in ten years

1 2 3 4 5 6 7 8 9 10

Drug development timeline*

Pre-clinical R&D

Clinical R&D

*Source: www.fda.gov/fdac/graphics/newdrugspecial/drugchart.pdf

Refill of top line

Maturing portfolio

13

A well risk balanced approach to investment

Most projects in late stage de-risked

2007 2008

New Molecular

Entities

Line

Extensions

����

����

����

����

����

����

*PPARαγαγαγαγ

1 LE in Phase I

11 LEs in Phase II

36 LEs in Phase III

NMEsin

Phase III

16 NMEs in Phase II

40 NMEs in Phase I

pertuzumab

ocrelizumab

TDM-1

taspoglutide (GLP-1)

dalcetrapib (CETPi)

% of Pharma Development spend

Proof of Concept

* Formal decision to move into phase III pending

42% 40%

14

Roche: Late stage projects with high success rate

Roche R&D pipeline, phase III projects

0

15

30

45

2005 2006 2007 2008

Other

Oncology

Metabolic

Autoimmune

41

33

3842

Terminations 0 1 1 2

Attrition rates % 0 2.6 2.4 4.9

0

20

40

60

80

100

'95-'99

'96-'00

'97-'01

'98-'02

'99-'03

'00-'04

'01-'05

'02-'06

Success Rate (%)

Industry Median

Roche

60

70

80

90

100

'95-'99

'96-'00

'97-'01

'98-'02

'99-'03

'00-'04

'01-'05

'02-'06

Attrition Rate (%)

Industry Median

Roche

Responsible management of R&D spend Higher attrition in early stage - higher success in late stage

Preclinical, Phase I and II Phase III and Registration

Source: R&D General Metrics Study, KMR GROUP, INC

16

Performance up-date

Strategy

Main trends influencing long term value propositions

Personalized Healthcare- Roche best positioned

Summary

17

Main trends influencing the long-term value propositions

Maximizing assets on hand

Personalised Healthcare

1818

Personalised Healthcare

Increasing demand by stakeholders

Better cost / benefit

Payers

More competitive

Industry

Better efficacy & safety profile

Regulators

Best treatment

Patients &

Physicians

19

Scenarios for PHC Added Value Distribution

Value captured by different stakeholders depending on IP and timing of diagnostic

Diagnostic afterDrug Launch

Diagnostic withDrug Launch

IP for Diagnostic

No IP for Diagnostic

Breast CancerAssay

Rx

Payor

Dx

Low

High

High

K-Ras Test

Rx

Payor

Dx

Low

High

Medium

Herceptin andHer2 test

Rx

Dx

Payor

High

Medium

Neutral

B-Raf inhibitor B-Raf mutant test

Rx

Dx

Payor

High

High

Neutral

20

Main trends influencing the long-term value propositions

Maximizing assets on hand

Personalised Healthcare

21

Major growth opportunities outside the US for key products

4451 51

59 65 71 76

5649 49

41 35 29 24

0

20

40

60

80

100

AVASTIN MABTHERA CELLCEPT TARCEVA XELODA HERCEPTIN PEGASYS

% of sales

Nth AmericaEU / ROW (incl. Japan)

Time on

market

22

Key drivers for long term development in place

Develop the short term drivers while not neglecting the long term opportunities

existing Earlier Phases

ILLUSTRATIVE

Inherent development risk

Maturity of portfolio

Low

High

Oncology

Inflammation

Metabolic

CNSVirology

23

Each cancer type is different

And needs a specific treatment approach

0%

20%

40%

60%

80%

100%

CRC BC NSCLC

3rd line

2nd line

1st line

adjuvant

Adjuvant DFS at 3 years*

Metastatic median OS * 25 months 36 months

* Assuming best current care, Incidence: GLOBOCAN 2002 and Roche market research

11 months

81 %72 % 50 %

Incidence

Survival

24

First in class mechanisms establishing new standards of care

Rank Drug Sales ($m) MAT 3Q08

1 MabThera 4,189

2 Herceptin 4,129

3 Avastin 4,052

4 Glivec 3,491

5 Taxotere 2745

6 Eloxatine 2,236

7 Arimidex 1,944

8 Gemzar 1,601

9 Erbitux 1,412

10 Casodex 1,343

First in class

Successful products need to be first class entrants –the race begins early in R&D

25

Top 10 Oncology Products Sales and market shares in seven major markets in 2007

Roche/Genetech’s MabThera, Herceptin and Avastin

dominate the current cancer brands market

Rituxan$3,216m

Herceptin$2,653m

Avastin$2,651m

Gleevec$1,990m

Eloxatin$1,964m

Taxotere$1,837m

Lupron$1,411m

Arimidex$1,364m

Gemzar$1,156m

Erbitux$1,040m

-10%

0%

10%

20%

30%

40%

50%

0% 2% 4% 6% 8% 10% 12%

Market share, 2007

CA

GR

, 200

6-07

Bubble size represents 2007 sales

Source: Datamonitor, MIDAS Sales Data, IMS Health, April 2008, Copyright ©, reprinted with permission

Rituxan$3,216m

Herceptin$2,653m

Avastin$2,651m

Gleevec$1,990m

Eloxatin$1,964m

Taxotere$1,837m

Lupron$1,411m

Arimidex$1,364m

Gemzar$1,156m

Erbitux$1,040m

-10%

0%

10%

20%

30%

40%

50%

0% 2% 4% 6% 8% 10% 12%

Market share, 2007

CA

GR

, 200

6-07

Bubble size represents 2007 sales

Source: Datamonitor, MIDAS Sales Data, IMS Health, April 2008, Copyright ©, reprinted with permission

DMHC2416: Commercial Insight: Top 20 Therapy Cancer Brands (08/2008)

26

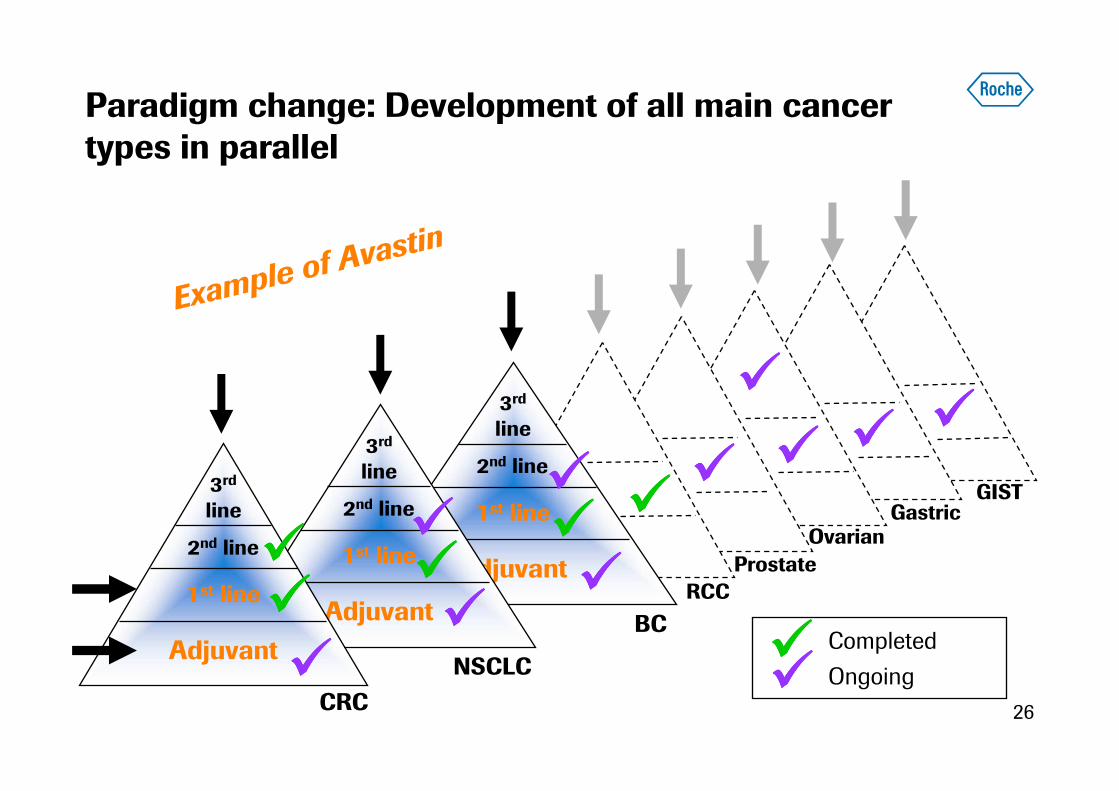

GIST

3rd

line

2nd line

1st line

Adjuvant

BC

3rd

line

2nd line

1st line

Adjuvant

NSCLC

Paradigm change: Development of all main cancer types in parallel

3rd

line

2nd line

1st line

Adjuvant

CRC

Completed

Ongoing

RCC

Prostate

OvarianGastric

��������

����

�������� ����

�������� ����

��������

����

��������

����

Example o

f Avastin

��������

27

Double-digit growth continues

Europe/RoW

• Continued strong increase in Avastin sales,

driven by strong uptake in mCRC and mBC

• Emerging markets contributing to

continued growth of MabThera, Herceptin

and Tarceva

Japan

• Strong launches of Avastin, Tarceva, and

adjuvant Herceptin

Oncology franchise approaches CHF 20 billion in sales

0.0

4.0

8.0

12.0

16.0

20.0

2004 2005 2006 2007 2008

Europe/RoW US Japan

local growth

+27 %

+9 %

+20 %

+15 %

Oncology sales(CHF billion)

53%

40%

7%

28

Exciting mid / early-stage opportunities in oncology

3rd generation anti-CD20- potential for improvement over MabThera based on Glycart technology

ADCC= (antibody dependent cell-mediated cytotoxicity); CDC= (complement dependent cytotoxicity)

Improved product features

Increased direct cell death

Increased ADCC

Lower CDC

Phase I in NHL

GA101: Phase II ongoingPhase I data presented at ASH 2009

Extended patent life for many other monocloncal antibodies?

MabThera

Herceptin

Pertuzumab.

29

Key drivers for long term development in place

Develop the short term drivers while not neglecting the long term opportunities

existing Earlier Phases

ILLUSTRATIVE

Inherent development risk

Maturity of portfolio

Low

High

Oncology

Inflammation

Metabolic

CNSVirology

30

Rheumatoid Arthritis: Not all patients respond to current therapy

Gold standard therapy anti-TNF + MTX

MTX alone

anti-TNF + MTX

anti-TNF alone

Only 1 of 3 patients receives significant benefit

% A

CR

70 R

espo

nder

s Unmet Medical Need

ACR 70====70%%%% Improvement in:

Disease activity – patientDisease activity – physicianPatient assessment of PainPhysical disabilityAcute phase reactants – CRP,ESR

31

Comprehensive development program in RA

Covers all treatment stages

ActemraTOWARD*(DMARDs IR)

RADIATE*(Anti-TNF IR)

MabTheraMIRROR*

(MTX IR, dose escalation)

SCORE**(DMARDs IR)

LITHE**(MTX IR, X-ray study)

current Tx paradigm

IMAGE**(MTX naive, X-ray study)

OPTION*(MTX IR)

REFLEX(Anti-TNF IR)

SERENE*(MTX IR)

AMBITION*(6 mnth MTX free/ MTX naive,

monotherapy)

NSAIDs or Cox-2 TNF inhibitors 2nd biologic(+/-MTX) (+/-MTX)

DMARDs

* Indication not yet approved, awaiting regulatory approval

** Phase III trial in progress

32

Key drivers for long term development in place

Develop the short term drivers while not neglecting the long term opportunities

existing Earlier Phases

ILLUSTRATIVE

Inherent development risk

Maturity of portfolio

Low

High

Oncology

Inflammation

Metabolic

CNSVirology

33

CD20 targeting: new treatment strategy for MS

Very promising signals from Phase II with rituximab

• Total cumulative mean number of

gadolinium lesions was reduced by 91

%, p<0.0001)

• Patients with relapses over 24 weeks in

the treated arm was 14.5 % compared

to 34.3 % in the placebo (58 percent

relative reduction, p = 0.0238)

Ocrelizumab: Phase II placebo-controlled program in RRMS

34

Performance up-date

Strategy

Main trends influencing long term value propositions

Summary

35

Roche Pharma pipeline overview

Focused on five Disease Biology Areas

MabThera

AvastinHerceptin

TarcevaPertuzumab

Oncology

Xeloda

ApomabApo2L/TRAIL

On HandPromising Late

StageEmerging Mid-Term

Early Stage

RA/Inflammation

Virology

R7128 HCV pol. Inh.

TamifluR3484 HPV16

Pegasys

R7227 HCV prot. inh.

R1594 ocrelizumab

9 ph. I compounds

ActemraMabThera

R667 RARγγγγ

16 ph. I compounds

R1507 (IGF-1R mAb)

R1583 GLP-1

Metabolic/CV

9 ph. I compoundsR1439 dual PPAR

R1658 CETP Inh.

CNS

4 ph. I compoundsR3487 Alzheimer’s

ocrelizumab RRMSR1678 Schizophrenia

R7159 3rd gen anti-CD20

Anti-CD40 mAbHedgehog inhibitor

T-DM1

36

Roche: M&D and G&A % to sales

Freeing up resources for innovation

20%

25%

30%

35%

40%

2002 2003 2004 2005 2006 2007

Roche (Prescription)

GSK

Sanofi-Aventis

Eli Lilly

AstraZeneca

Merck & Co.

Novartis

37

Investing into the future

R&D % to sales

10%

15%

20%

25%

2002 2003 2004 2005 2006 2007

Roche (Prescription)

GSK

Sanofi-Aventis

Eli Lilly

AstraZeneca

Merck & Co.

Novartis

38

Patent expiry 2008-2012

Roche short-/medium-term has the strongest patent protected portfolio… and highest share of biotech products

42

6962

54 51 48 4841

36

24

14

0

20

40

60

80

100

Total

Market

GSK

Pfizer

AZ

S-A J&J

MSD

Lilly

Novartis

Abbott

Roche

2008-2012 2013 & beyond

Source: IMS Health MIDAS Market Segmentation MAT June 2008, Ethical protected brand sales only.

SHARE OF PROTECTED SALES EXPIRING % US$

Top 10 Corporations Protected Sales Expiring to 2012 & Beyond (US$ Const)

39

Roche: A unique “investment case”

Clear and focused strategy

– Medically differentiated products

– Poised to become leader in Personalised Healthcare

Attractive risk profile

– Low generic risk; lowest among European large-cap players

Assets in place for sustained success

– World market leader in Oncology

– Emerging Rheumatology & Autoimmune, and Metabolic franchises

Industry-leading organic growth

Unique high-tech healthcare investment

40

We Innovate Healthcare

41

Personalised Healthcare

Benefit for industry

Today Future

Reduced Patient pool

Price increase /stability

Faster penetration

Better patient

compliance

Increased market share

Time to market, line extensions

Benefit from patient stratification

42

0%

5%

10%

15%

20%

25%

30%

35%

Q405

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

0%

5%

10%

15%

20%

25%

30%

35%

Q405

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

First line Second line

Source: Synovate Patient Monitor and Top-Up, Top-5 EU

Avastin

Patient share Patient share

Avastin

Avastin in mCRC: Strong uptake continues