a study on financial performance of selected indian...

TRANSCRIPT

International Journal of Research in Management, Science & Technology (E-ISSN: 2321-3264)

Vol. 2, No. 3, December 2014 Available at www.ijrmst.org

2321-3264/Copyright©2014, IJRMST, December 2014

81

A Study on Financial Performance of Selected Indian

Banks Dr.Manvinder Tandon

#1, Dr. Bimal Anjum

*2, Julee

#3

Abstract-The Indian banking sector plays an important role in the

economic development of the country and is the most dominant

segment of the financial sector. The banking sector has shown a

remarkable responsiveness to the needs of the planned economy. It

has brought about a considerable progress in its efforts at deposit

mobilization and has taken a number of measures in the recent

past for accelerating the rate of growth of deposits. Banks play a

positive role in economic development of a country as repositories

of community’s savings and as purveyors of credit. It also helps

channel savings to investments and encourage. This study analyses

that PNB has the highest return on Net Worth (mean) which is a

sign that management of Punjab national bank is at using leverage

to increase profits and profit margins. It is also indicating a sign of

good management.SBI and PNB has the highest return on capital

employed (mean) which indicates that SBI and PNB are realizing

highest return from its capital employed. State bank of India has

highest Dividend Payout Ratio (Mean) which is a sign that the SBI

has highest percentage of profit distribute as dividend to equity

shareholders. Bank of Baroda has the Return on Assets (mean)

which is a sign that management of Bank is using Assets fund more

efficiently to increase earning capacity. It is also suggested that

Bank of India has lowest Divided per share & Earning per share so

bank has improved its profit accordingly increase in its DPS EPS.

Keywords: deposit mobilization, Shareholders Fund, Capital

Employed, EPS etc.

I. INTRODUCTION

In today‟s scenario banking plays a vital role in the growth and

development of developing countries like India.Banks lubricate

the entire monetary and financial system and ensure smooth

operations. With the imitation of the process of liberalization

and globalization of the economy.The financial sector,

particularly the commercial banks, not only in urban areas, but

also in rural areas where the first to experience the winds of

change. However, these changes were experienced more in

urban areas than in rural areas. The economic reforms in India

started in early nineties, but their outcomes visible now major

changes took place in the functioning of banks in India only

after liberalization, globalization and privatization.

The banking sector has shown a remarkable responsiveness to

the needs of the planned economy. It has brought about a

considerable progress in its efforts at deposit mobilization and

has taken a number of measures in the recent past for

accelerating the rate of growth of deposits.The activities of

commercial banking have growth in multi-directional ways as

well as multi-dimensional manner.. In a way, commercial banks

have emerged as key financial agencies for rapid economic

development. By pooling the savings together, banks can make

available funds to specialized institutions which finance

different sectors of the economy, needing capital for various

purposes, risks and durations. By contributing to government

securities, bonds and debentures of term-lending institutions in

the fields of agriculture, industries and now housing, banks are

also providing these institutions with an access to the common

pool of savings mobilized by them, to that extent relieving them

of the responsibility of directly approaching the saver. This

intermediation role of banks is particularly important in the

early stages of economic development and financial

specification. A country like India, with different regions at

different stages of development, presents an interesting

spectrum of the evolving role of banks, in theMatter of inter-

International Journal of Research in Management, Science & Technology (E-ISSN: 2321-3264)

Vol. 2, No. 3, December 2014 Available at www.ijrmst.org

2321-3264/Copyright©2014, IJRMST, December 2014

82

mediation and beyond. The present paper throws the light on the

financial performance the top five banks of India chosen on the

basis of market capitalization.

II. REVIEW OF LITERATURE

Mohan (2005) focused on the efficiency and productivity

changes in the Indian banking concluded that the patterns of

efficiency and technological changes witnessed in Indian

banking can be viewed as consistent with in response to the

forces of deregulationMaji and dey, (2006) analyzed how

strongly the process of globalization and liberalization has

influenced the Indian banking sector. The ongoing reforms in

the banking sector, with their thrust on transparency, efficiency

and profitability, have forced the Indian banking sector to adopt

suitable strategies with focus on productivity, profitability,

competitiveness and sustainability. SubashC.Ray (2000),

India‟s public sector banks (PSBs) are compared unfavorably

with their private sector counterparts, domestic and foreign of

PSBs. Ved Pal and Malik (2007) examined that the difference

in financial characteristics of public, private and foreign sector

banks based on factors such as profitability, liquidity, risk and

efficiency. Aggarwal, A.K., Singh, D. and Chaturvedi, N.

(2007-08) analyzed the performance of the banking sector and

considered as a proxy for the economy as a whole, due to banks

wide spectrum of exposures.

III. OBJECTIVES OF THE STUDY

The main objectives of study are as follow:

1 .To knows about selected Indian banks and their profitability

position.

2. To examine the financial position of selected banks.

IV. RESEARCH METHODOLOGY

A. Research design

The present study adopts an analytical and descriptive

research design. The data of the sample banks (for a period

of Five years from 2009-2013) has been collected by using

a software Prowess software. The sample size of selected

Indian banks has been selected for the purpose of the study

on the basis of market capitalization. They are:

1. State Bank of India (SBI)

2. Bank of Baroda

3. Punjab National Bank

4. Bank of India

5. Canara Bank

B. Sample design

1) Sampling Technique: The study is done with special

reference to top 5 Indian banks.

2) Sample Size: Top five Indian Banks are chosen as

sample size for the study on the Basis of market

capitalization.

C. Sources of data

The relevant secondary data has been collected from“Prowess

Software”&Bank‟s financial reports & Websites.

D. Time period of study

The study has been conducted during March 2009 to

March.2014.

E. Tools used for analysis

1) Ratio analysis:Profitability Ratios have been calculated

for the past five years for the purpose of analysis.

Ratios being designed are named as:

Return on Total Shareholder‟s Fund(RONW)

Return on Capital Employed

Return on Assets

Earnings Per Share (EPS)

Dividend Per Share (DPS)

Capital adequacy Ratio

International Journal of Research in Management, Science & Technology (E-ISSN: 2321-3264)

Vol. 2, No. 3, December 2014 Available at www.ijrmst.org

2321-3264/Copyright©2014, IJRMST, December 2014

83

Dividend Payout Ratio

2) Mean

3) Standard deviation

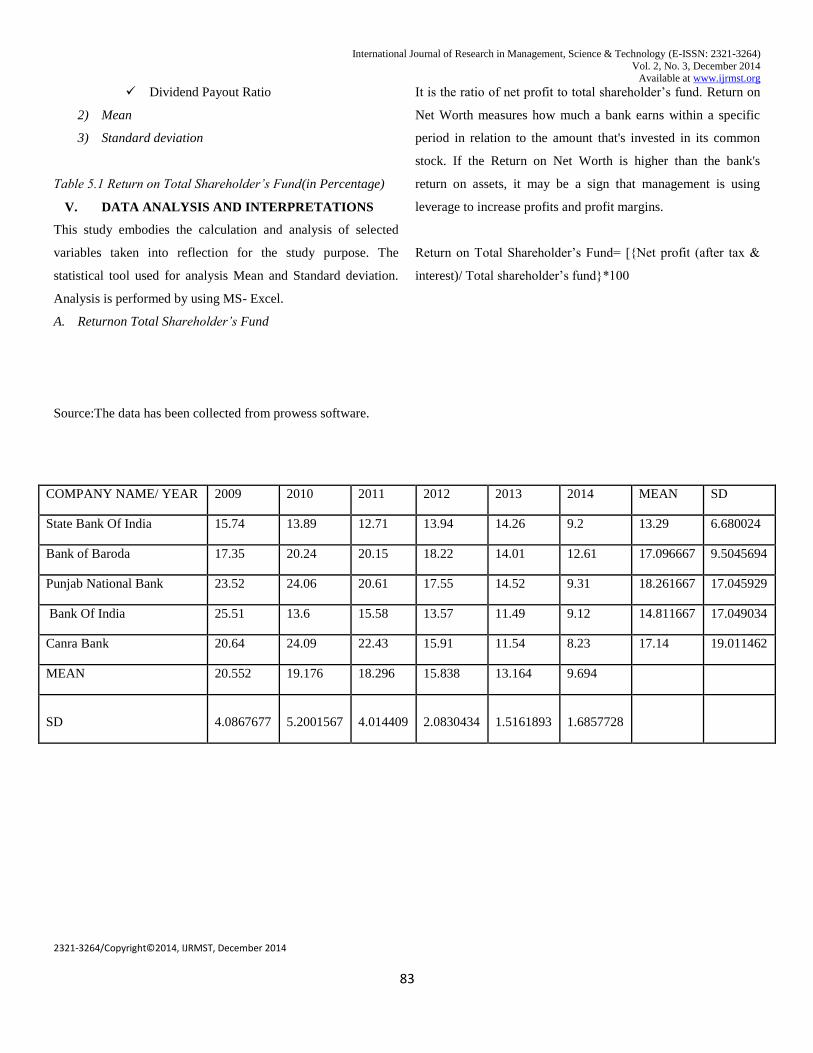

Table 5.1 Return on Total Shareholder’s Fund(in Percentage)

V. DATA ANALYSIS AND INTERPRETATIONS

This study embodies the calculation and analysis of selected

variables taken into reflection for the study purpose. The

statistical tool used for analysis Mean and Standard deviation.

Analysis is performed by using MS- Excel.

A. Returnon Total Shareholder’s Fund

It is the ratio of net profit to total shareholder‟s fund. Return on

Net Worth measures how much a bank earns within a specific

period in relation to the amount that's invested in its common

stock. If the Return on Net Worth is higher than the bank's

return on assets, it may be a sign that management is using

leverage to increase profits and profit margins.

Return on Total Shareholder‟s Fund= [{Net profit (after tax &

interest)/ Total shareholder‟s fund}*100

Source:The data has been collected from prowess software.

COMPANY NAME/ YEAR 2009 2010 2011 2012 2013 2014 MEAN SD

State Bank Of India 15.74 13.89 12.71 13.94 14.26 9.2 13.29 6.680024

Bank of Baroda 17.35 20.24 20.15 18.22 14.01 12.61 17.096667 9.5045694

Punjab National Bank 23.52 24.06 20.61 17.55 14.52 9.31 18.261667 17.045929

Bank Of India 25.51 13.6 15.58 13.57 11.49 9.12 14.811667 17.049034

Canra Bank 20.64 24.09 22.43 15.91 11.54 8.23 17.14 19.011462

MEAN 20.552 19.176 18.296 15.838 13.164 9.694

SD 4.0867677 5.2001567 4.014409 2.0830434 1.5161893 1.6857728

International Journal of Research in Management, Science & Technology (E-ISSN: 2321-3264)

Vol. 2, No. 3, December 2014 Available at www.ijrmst.org

2321-3264/Copyright©2014, IJRMST, December 2014

84

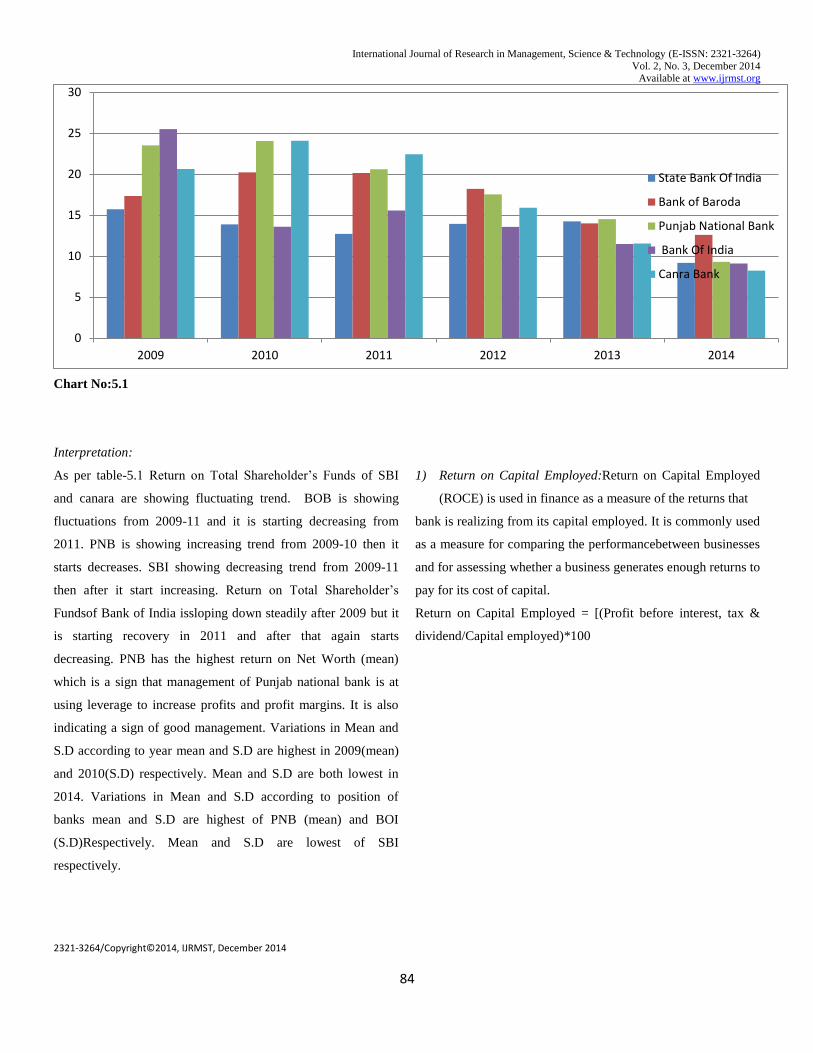

Chart No:5.1

Interpretation:

As per table-5.1 Return on Total Shareholder‟s Funds of SBI

and canara are showing fluctuating trend. BOB is showing

fluctuations from 2009-11 and it is starting decreasing from

2011. PNB is showing increasing trend from 2009-10 then it

starts decreases. SBI showing decreasing trend from 2009-11

then after it start increasing. Return on Total Shareholder‟s

Fundsof Bank of India issloping down steadily after 2009 but it

is starting recovery in 2011 and after that again starts

decreasing. PNB has the highest return on Net Worth (mean)

which is a sign that management of Punjab national bank is at

using leverage to increase profits and profit margins. It is also

indicating a sign of good management. Variations in Mean and

S.D according to year mean and S.D are highest in 2009(mean)

and 2010(S.D) respectively. Mean and S.D are both lowest in

2014. Variations in Mean and S.D according to position of

banks mean and S.D are highest of PNB (mean) and BOI

(S.D)Respectively. Mean and S.D are lowest of SBI

respectively.

1) Return on Capital Employed:Return on Capital Employed

(ROCE) is used in finance as a measure of the returns that

bank is realizing from its capital employed. It is commonly used

as a measure for comparing the performancebetween businesses

and for assessing whether a business generates enough returns to

pay for its cost of capital.

Return on Capital Employed = [(Profit before interest, tax &

dividend/Capital employed)*100

0

5

10

15

20

25

30

2009 2010 2011 2012 2013 2014

State Bank Of India

Bank of Baroda

Punjab National Bank

Bank Of India

Canra Bank

International Journal of Research in Management, Science & Technology (E-ISSN: 2321-3264)

Vol. 2, No. 3, December 2014 Available at www.ijrmst.org

2321-3264/Copyright©2014, IJRMST, December 2014

85

Table 5.2 Return on Capital Employed(In Percentage)

COMPANY NAME/ YEAR 2009 2010 2011 2012 2013 2014 MEAN SD

State Bank Of India 8.99 8.62 8.54 9.45 9.35 9.22 9.028333 0.380705

Bank of Baroda 8.51 7.86 7.76 8.22 7.81 7.19 7.891667 0.448884

Punjab National Bank 10.14 9.24 9.09 9.71 9.86 9.29 9.555 0.411084

Bank Of India 9.44 8.14 7.78 8.56 8.54 8.23 8.448333 0.564568

Canara Bank 9.61 9.14 8.62 9.52 9.49 9.62 9.333333 0.390982

MEAN 9.338 8.6 8.358 9.092 9.01 8.71

SD 0.619330283 0.604318 0.576472 0.658916 0.826045 0.99567

Source:The data has been collected from prowess software.

Interpretation:As per table-2 Return on Capital Employed of

PNB and canara bank are showing decreasing trend from 2009-

11 and after that it increases, BOI is showing decreasing trend

from 2009-2011 and then remains constant from 2012-13 .SBI

and BOB both are showing fluctuating trend .PNB has the

highest return on capital employed (mean) which indicates that

PNB is realizing highest returns from its capital employed in

comparison to other banks taken under study. Variations in

Mean and S.D according to year mean and S.D are highest in

2009& 2012. Mean and S.D are both lowest in 2011. Variations

0

2

4

6

8

10

12

2009 2010 2011 2012 2013 2014

State Bank Of India

Bank of Baroda

Punjab National Bank

Bank Of India

Canra Bank

International Journal of Research in Management, Science & Technology (E-ISSN: 2321-3264)

Vol. 2, No. 3, December 2014 Available at www.ijrmst.org

2321-3264/Copyright©2014, IJRMST, December 2014

86

in Mean and S.D according to position of banks mean and S.D

are highest of PNB (mean) & BOI (S.D) respectively. Mean and

S.D are both lowest of BOB.

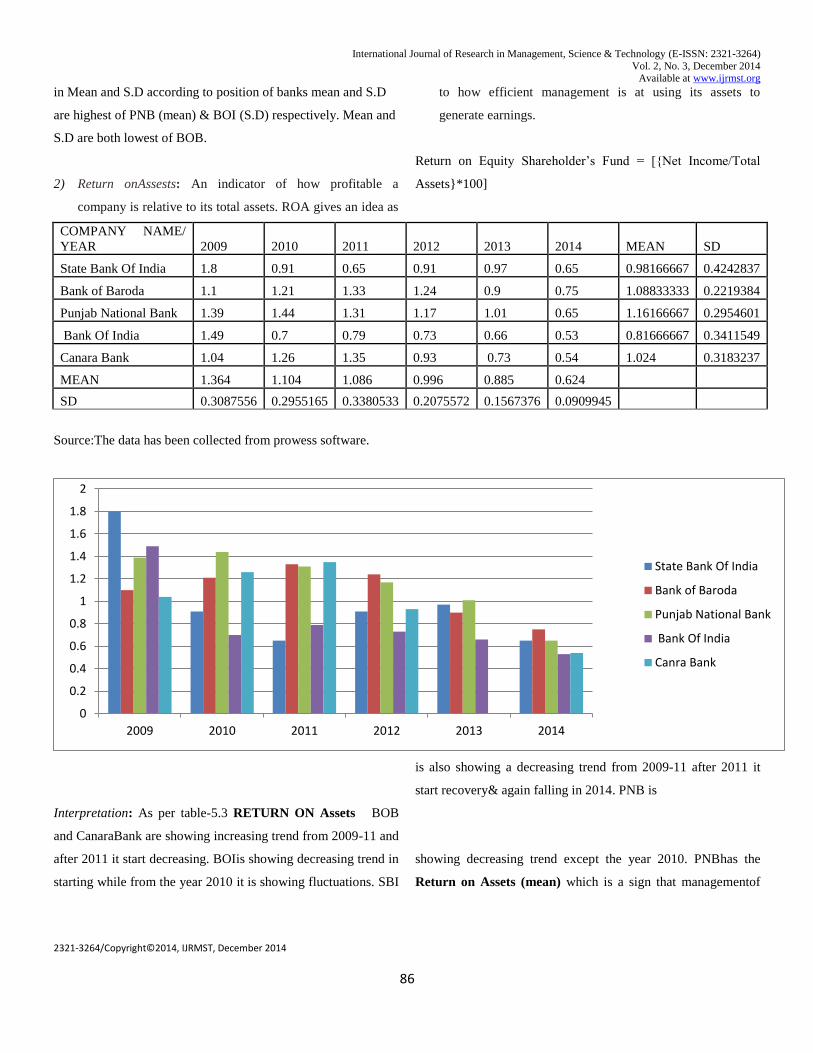

2) Return onAssests: An indicator of how profitable a

company is relative to its total assets. ROA gives an idea as

to how efficient management is at using its assets to

generate earnings.

Return on Equity Shareholder‟s Fund = [{Net Income/Total

Assets}*100]

COMPANY NAME/

YEAR 2009 2010 2011 2012 2013 2014 MEAN SD

State Bank Of India 1.8 0.91 0.65 0.91 0.97 0.65 0.98166667 0.4242837

Bank of Baroda 1.1 1.21 1.33 1.24 0.9 0.75 1.08833333 0.2219384

Punjab National Bank 1.39 1.44 1.31 1.17 1.01 0.65 1.16166667 0.2954601

Bank Of India 1.49 0.7 0.79 0.73 0.66 0.53 0.81666667 0.3411549

Canara Bank 1.04 1.26 1.35 0.93 0.73 0.54 1.024 0.3183237

MEAN 1.364 1.104 1.086 0.996 0.885 0.624

SD 0.3087556 0.2955165 0.3380533 0.2075572 0.1567376 0.0909945

Source:The data has been collected from prowess software.

Interpretation: As per table-5.3 RETURN ON Assets BOB

and CanaraBank are showing increasing trend from 2009-11 and

after 2011 it start decreasing. BOIis showing decreasing trend in

starting while from the year 2010 it is showing fluctuations. SBI

is also showing a decreasing trend from 2009-11 after 2011 it

start recovery& again falling in 2014. PNB is

showing decreasing trend except the year 2010. PNBhas the

Return on Assets (mean) which is a sign that managementof

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

2009 2010 2011 2012 2013 2014

State Bank Of India

Bank of Baroda

Punjab National Bank

Bank Of India

Canra Bank

International Journal of Research in Management, Science & Technology (E-ISSN: 2321-3264)

Vol. 2, No. 3, December 2014 Available at www.ijrmst.org

2321-3264/Copyright©2014, IJRMST, December 2014

87

PNB is using Assets fund more efficiently to increase earning

capacity in comparison to other banks. Variations in Mean and

S.D according to year mean and S.D are highest in 2009 and

2011 respectively. Mean and S.D are lowest in 2014

respectively. Variations in Mean and S.D according to position

ofbanks mean and S.D are highest of PNBand SBI respectively.

Mean and S.D are lowest of Bank of India and BOB

respectively.

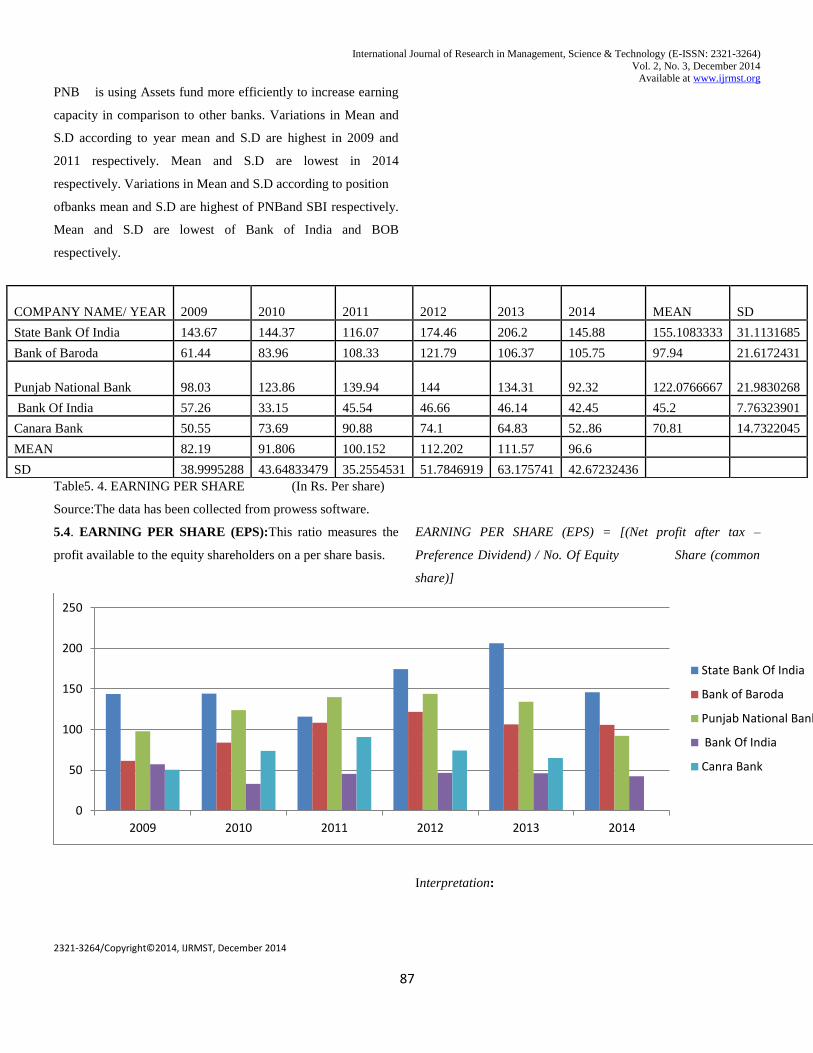

Table5. 4. EARNING PER SHARE (In Rs. Per share)

Source:The data has been collected from prowess software.

5.4. EARNING PER SHARE (EPS):This ratio measures the

profit available to the equity shareholders on a per share basis.

EARNING PER SHARE (EPS) = [(Net profit after tax –

Preference Dividend) / No. Of Equity Share (common

share)]

Interpretation:

0

50

100

150

200

250

2009 2010 2011 2012 2013 2014

State Bank Of India

Bank of Baroda

Punjab National Bank

Bank Of India

Canra Bank

COMPANY NAME/ YEAR 2009 2010 2011 2012 2013 2014 MEAN SD

State Bank Of India 143.67 144.37 116.07 174.46 206.2 145.88 155.1083333 31.1131685

Bank of Baroda 61.44 83.96 108.33 121.79 106.37 105.75 97.94 21.6172431

Punjab National Bank 98.03 123.86 139.94 144 134.31 92.32 122.0766667 21.9830268

Bank Of India 57.26 33.15 45.54 46.66 46.14 42.45 45.2 7.76323901

Canara Bank 50.55 73.69 90.88 74.1 64.83 52..86 70.81 14.7322045

MEAN 82.19 91.806 100.152 112.202 111.57 96.6

SD 38.9995288 43.64833479 35.2554531 51.7846919 63.175741 42.67232436

International Journal of Research in Management, Science & Technology (E-ISSN: 2321-3264)

Vol. 2, No. 3, December 2014 Available at www.ijrmst.org

2321-3264/Copyright©2014, IJRMST, December 2014

88

As per table-5.4 Earning Per Shareof BOB and PNB is showing

increasing trend from 2009 but suddenly decrease in 2013. SBI

is showing increasing trend of Earning per share in all years

expect the financial year 2011& 2014. BOI is showing

decreasing trend of Earning per share in the year 2010 after that

it is showing the flat trend or almost same the year 2010 to

2014. SBI has the highest Earning per share (mean) which

means that SBI has the highest EPS which means that it has

highest profits available to equity shareholders on per share

basis in comparison to other banks. Variations in Mean and S.D

according to year mean and S.D are highest in 2012 and

2014respectively. Mean and S.D are lowest in 2009 and 2011

respectively. Variations in Mean and S.D according to position

of banks mean and S.D are highest of SBI and PNB respectively

but BOB has the highest S.D after that state bank of India.

Mean and S.D are lowest of Bank of India respectively.

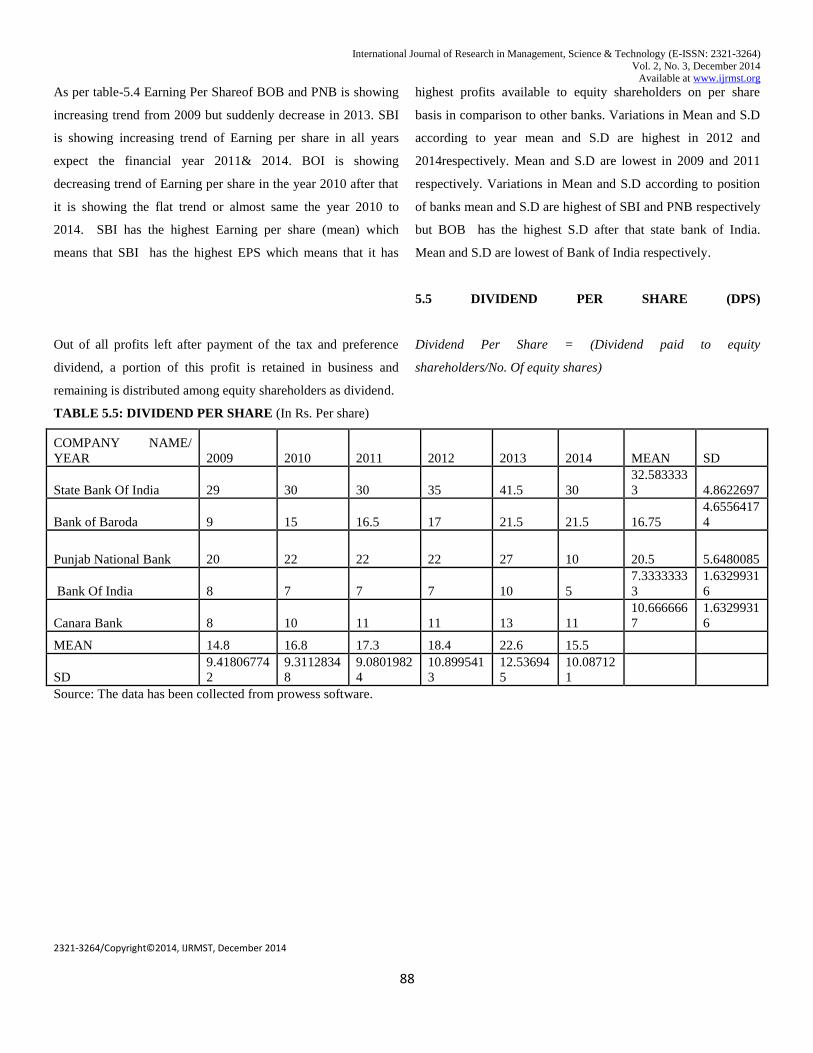

5.5 DIVIDEND PER SHARE (DPS)

Out of all profits left after payment of the tax and preference

dividend, a portion of this profit is retained in business and

remaining is distributed among equity shareholders as dividend.

Dividend Per Share = (Dividend paid to equity

shareholders/No. Of equity shares)

TABLE 5.5: DIVIDEND PER SHARE (In Rs. Per share)

COMPANY NAME/

YEAR 2009 2010 2011 2012 2013 2014 MEAN SD

State Bank Of India 29 30 30 35 41.5 30

32.583333

3 4.8622697

Bank of Baroda 9 15 16.5 17 21.5 21.5 16.75

4.6556417

4

Punjab National Bank 20 22 22 22 27 10 20.5 5.6480085

Bank Of India 8 7 7 7 10 5

7.3333333

3

1.6329931

6

Canara Bank 8 10 11 11 13 11

10.666666

7

1.6329931

6

MEAN 14.8 16.8 17.3 18.4 22.6 15.5

SD

9.41806774

2

9.3112834

8

9.0801982

4

10.899541

3

12.53694

5

10.08712

1

Source: The data has been collected from prowess software.

International Journal of Research in Management, Science & Technology (E-ISSN: 2321-3264)

Vol. 2, No. 3, December 2014 Available at www.ijrmst.org

2321-3264/Copyright©2014, IJRMST, December 2014

89

Interpretation:

As per table-5.5DIVIDEND PER SHARE Bank of Baroda and

Canara bank are showing increasing trend except 2014. State

Bank of India is also showing a decrease in Dividend per Share

from 2009-2010 but after it increases and then is remains

constant (flat trend) from 2010-2012. after that it shows

increasing DPS in the financial year 2013 .PNB and BOI are

showing fluctuating trend from 2009 to2014. Dividend per

Share of Bank ofBaroda is showing increasing trend.State Bank

of India has thehighest Dividend per Share (mean) which means

that it has highest dividend available to equity shareholders on

per share basis in comparison to other 4 banks. Variations in

Mean and S.D according to year mean and S.D are both highest

in 2013. Mean and S.D are both lowest in 2009 and 2011.

Variations in Mean and S.D according to position of banks

mean and S.D are both highest of State bank of India. Mean and

S.D are lowest of Bank of India.

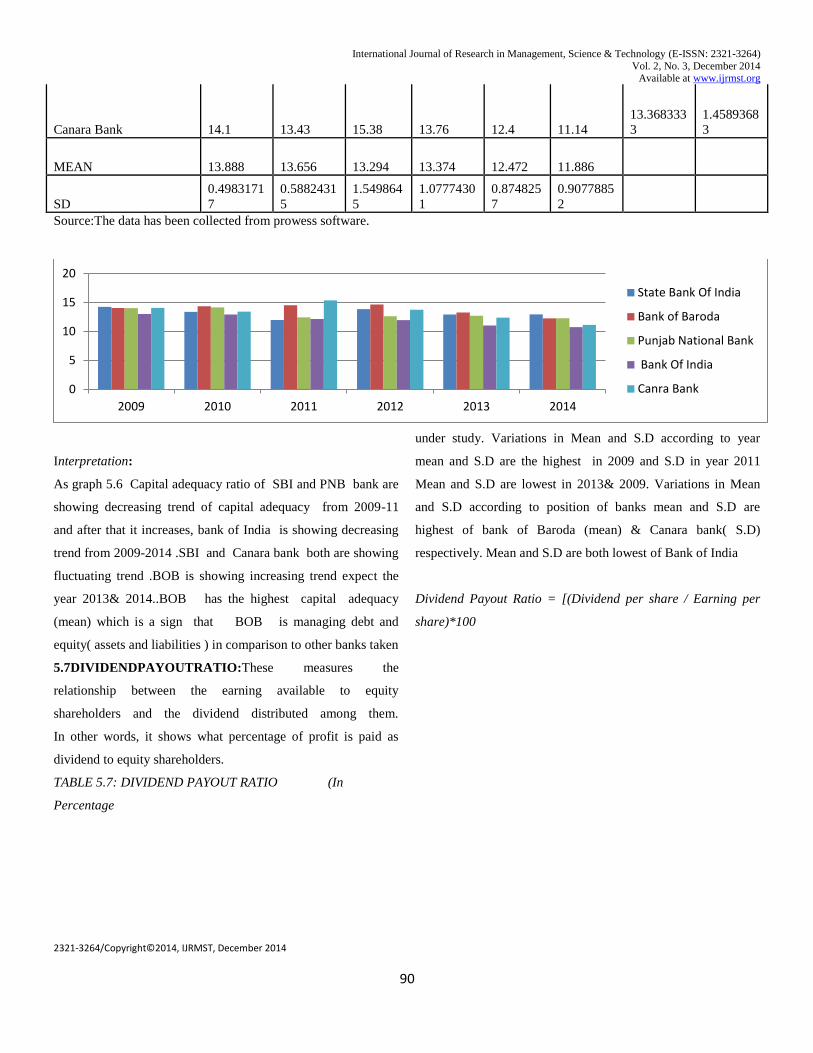

5.6. CAPITAL ADEQUACY RATIO: capital adequacy ratio

is the ratio which determines the banks capability to meet the

time liabilities and other risk as credit risk. It is calculated by

using this formula;

Capital Adequacy Ratio = [(Equity /Assets)*100]

COMPANY NAME/

YEAR 2009 2010 2011 2012 2013 2014 MEAN SD

State Bank Of India 14.25 13.39 11.98 13.86 12.92 12.96

13.226666

7

0.7992913

5

Bank of Baroda 14.05 14.36 14.52 14.67 13.3 12.28

13.863333

3

0.9151757

6

Punjab National Bank 14.03 14.16 12.42 12.63 12.72 12.29

13.041666

7

0.8308890

8

Bank Of India 13.01 12.94 12.17 11.95 11.02 10.76 11.975

0.9412066

7

0

5

10

15

20

25

30

35

40

45

2009 2010 2011 2012 2013 2014

State Bank Of India

Bank of Baroda

Punjab National Bank

Bank Of India

Canara Bank

International Journal of Research in Management, Science & Technology (E-ISSN: 2321-3264)

Vol. 2, No. 3, December 2014 Available at www.ijrmst.org

2321-3264/Copyright©2014, IJRMST, December 2014

90

Canara Bank 14.1 13.43 15.38 13.76 12.4 11.14

13.368333

3

1.4589368

3

MEAN 13.888 13.656 13.294 13.374 12.472 11.886

SD

0.4983171

7

0.5882431

5

1.549864

5

1.0777430

1

0.874825

7

0.9077885

2

Source:The data has been collected from prowess software.

Interpretation:

As graph 5.6 Capital adequacy ratio of SBI and PNB bank are

showing decreasing trend of capital adequacy from 2009-11

and after that it increases, bank of India is showing decreasing

trend from 2009-2014 .SBI and Canara bank both are showing

fluctuating trend .BOB is showing increasing trend expect the

year 2013& 2014..BOB has the highest capital adequacy

(mean) which is a sign that BOB is managing debt and

equity( assets and liabilities ) in comparison to other banks taken

under study. Variations in Mean and S.D according to year

mean and S.D are the highest in 2009 and S.D in year 2011

Mean and S.D are lowest in 2013& 2009. Variations in Mean

and S.D according to position of banks mean and S.D are

highest of bank of Baroda (mean) & Canara bank( S.D)

respectively. Mean and S.D are both lowest of Bank of India

Dividend Payout Ratio = [(Dividend per share / Earning per

share)*100

5.7DIVIDENDPAYOUTRATIO:These measures the

relationship between the earning available to equity

shareholders and the dividend distributed among them.

In other words, it shows what percentage of profit is paid as

dividend to equity shareholders.

TABLE 5.7: DIVIDEND PAYOUT RATIO (In

Percentage

0

5

10

15

20

2009 2010 2011 2012 2013 2014

State Bank Of India

Bank of Baroda

Punjab National Bank

Bank Of India

Canra Bank

International Journal of Research in Management, Science & Technology (E-ISSN: 2321-3264)

Vol. 2, No. 3, December 2014 Available at www.ijrmst.org

2321-3264/Copyright©2014, IJRMST, December 2014

91

Source: The data has been collected from prowess software.

Interpretation:

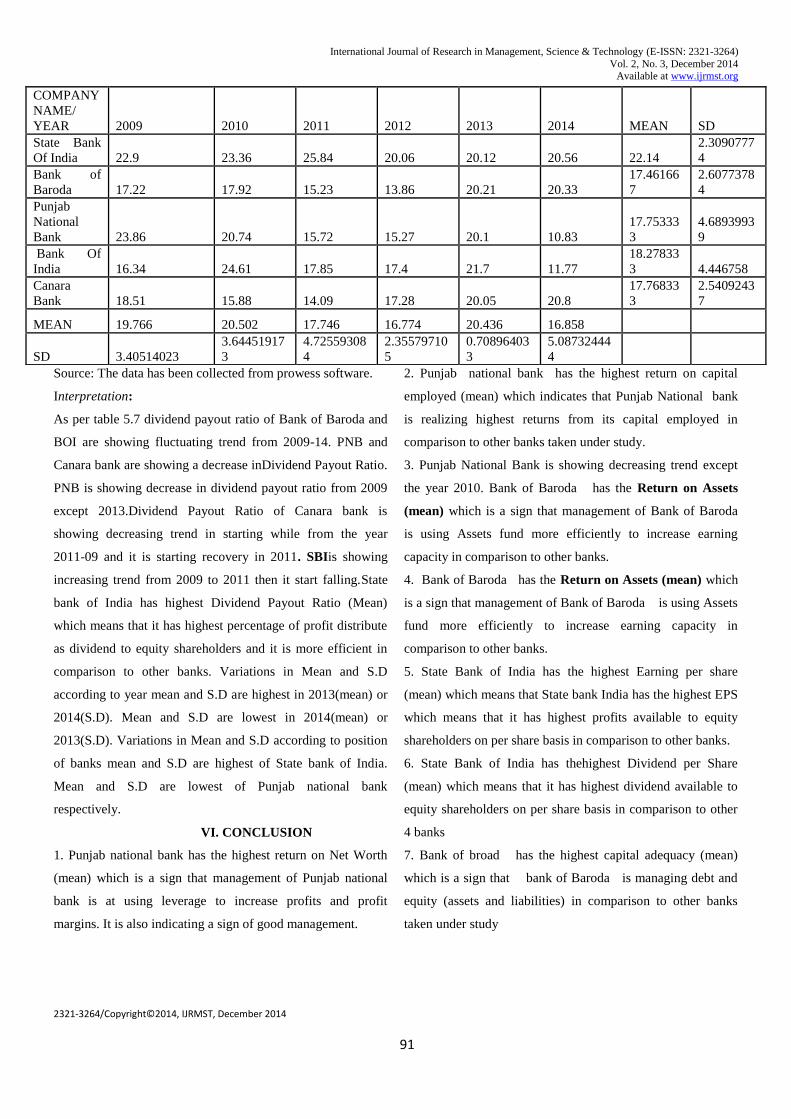

As per table 5.7 dividend payout ratio of Bank of Baroda and

BOI are showing fluctuating trend from 2009-14. PNB and

Canara bank are showing a decrease inDividend Payout Ratio.

PNB is showing decrease in dividend payout ratio from 2009

except 2013.Dividend Payout Ratio of Canara bank is

showing decreasing trend in starting while from the year

2011-09 and it is starting recovery in 2011. SBIis showing

increasing trend from 2009 to 2011 then it start falling.State

bank of India has highest Dividend Payout Ratio (Mean)

which means that it has highest percentage of profit distribute

as dividend to equity shareholders and it is more efficient in

comparison to other banks. Variations in Mean and S.D

according to year mean and S.D are highest in 2013(mean) or

2014(S.D). Mean and S.D are lowest in 2014(mean) or

2013(S.D). Variations in Mean and S.D according to position

of banks mean and S.D are highest of State bank of India.

Mean and S.D are lowest of Punjab national bank

respectively.

VI. CONCLUSION

1. Punjab national bank has the highest return on Net Worth

(mean) which is a sign that management of Punjab national

bank is at using leverage to increase profits and profit

margins. It is also indicating a sign of good management.

2. Punjab national bank has the highest return on capital

employed (mean) which indicates that Punjab National bank

is realizing highest returns from its capital employed in

comparison to other banks taken under study.

3. Punjab National Bank is showing decreasing trend except

the year 2010. Bank of Baroda has the Return on Assets

(mean) which is a sign that management of Bank of Baroda

is using Assets fund more efficiently to increase earning

capacity in comparison to other banks.

4. Bank of Baroda has the Return on Assets (mean) which

is a sign that management of Bank of Baroda is using Assets

fund more efficiently to increase earning capacity in

comparison to other banks.

5. State Bank of India has the highest Earning per share

(mean) which means that State bank India has the highest EPS

which means that it has highest profits available to equity

shareholders on per share basis in comparison to other banks.

6. State Bank of India has thehighest Dividend per Share

(mean) which means that it has highest dividend available to

equity shareholders on per share basis in comparison to other

4 banks

7. Bank of broad has the highest capital adequacy (mean)

which is a sign that bank of Baroda is managing debt and

equity (assets and liabilities) in comparison to other banks

taken under study

COMPANY

NAME/

YEAR 2009 2010 2011 2012 2013 2014 MEAN SD

State Bank

Of India 22.9 23.36 25.84 20.06 20.12 20.56 22.14

2.3090777

4

Bank of

Baroda 17.22 17.92 15.23 13.86 20.21 20.33

17.46166

7

2.6077378

4

Punjab

National

Bank 23.86 20.74 15.72 15.27 20.1 10.83

17.75333

3

4.6893993

9

Bank Of

India 16.34 24.61 17.85 17.4 21.7 11.77

18.27833

3 4.446758

Canara

Bank 18.51 15.88 14.09 17.28 20.05 20.8

17.76833

3

2.5409243

7

MEAN 19.766 20.502 17.746 16.774 20.436 16.858

SD 3.40514023

3.64451917

3

4.72559308

4

2.35579710

5

0.70896403

3

5.08732444

4

International Journal of Research in Management, Science & Technology (E-ISSN: 2321-3264)

Vol. 2, No. 3, December 2014 Available at www.ijrmst.org

2321-3264/Copyright©2014, IJRMST, December 2014

92

8. State bank of India has highest Dividend Payout Ratio

(Mean) which means that it has highest percentage of profit

distribute as dividend to equity shareholders and it is more

efficient in comparison to other banks.

REFERENCES

1. A.K. Aggarwal, Singh, D. and N. Chaturvedi, “India‟s

Banking Sector –Consolidation and Convergence: Balancing

on the Brink?‟ Punjab Journal of Business Studies, 3(2), Oct.-

March, 39-46, 2007-2008

2. T.K Chakrabarthy, „Profitability of Banks: An empirical

attempt for identification of variable of income and

expenditure of scheduled commercial banks for Profit

Planning,' Proceedings of the Bank Economists Conference

3.17-3.61, 1986.

3. Amandeep. 1991, Profit and Profitability of Indian

Nationalized Banks, Ph.D. Thesis, Punjab University,

Chandigarh.

3. John A. Goddard and John O.S Wilson, “The Profitability

of European Banks: A Cross-Sectional and Dynamic Panel

Analysis” 32(3) 363-381, 2004

4. Kumar and Sreeramulu, Employees productivity and cost-

A Comparative Study of Banks in India During 1997 to 2008.

5. Pal Ved& N.S. Malik .A Multivariate Analysis of the

financial characteristics of Commercial Banks in India. The

Icfai Journal of Bank Management .VI (3).2007

6. Ram PratapSinha, "Business Efficiency of Public Sector

Commercial Banks: A Data Envelopment Approach," The

IUP Journal of Applied Economics, 0(1), 7-27, 2008

7. S.J. Sampath, “Monitoring the Variables Determining the

Profitability of Banks,” Bankingfor better Profitability, 3(2)

691-699, 1990

8. R.K. Uppal, “Indian Banking – Prime Determinants of

Profitability, Emerging Issues and Future Outlook,” GITAM

Journal of Management, 7(2) 78-106, 2000.